Embed Size (px)

DESCRIPTION

Vattenfall Full Year Results 2007. Presentations by Lars Josefsson, CEO and Jan Erik Back, CFO 7 February 2008. Highlights 2007 - Group. Net sales increased 5.8% to SEK 143,639 million (135,802) EBIT increased 2.7% to SEK 28,583 million (27,821) Profit after tax increased - PowerPoint PPT Presentation

Citation preview

© Vattenfall AB

VattenfallFull Year Results 2007

Presentations by

Lars Josefsson, CEO and

Jan Erik Back, CFO

7 February 2008

7 Feb 2008© Vattenfall AB

2Highlights 2007 - Group

Net sales increased5.8% to SEK 143,639 million (135,802)

EBIT increased2.7% to SEK 28,583 million (27,821)

Profit after tax increased4.2% to SEK 20,686 million (19,858)

Net debt decreasedby SEK 5,667 million to SEK 43,740 millioncompared with 31 December 2006

7 Feb 2008© Vattenfall AB

3

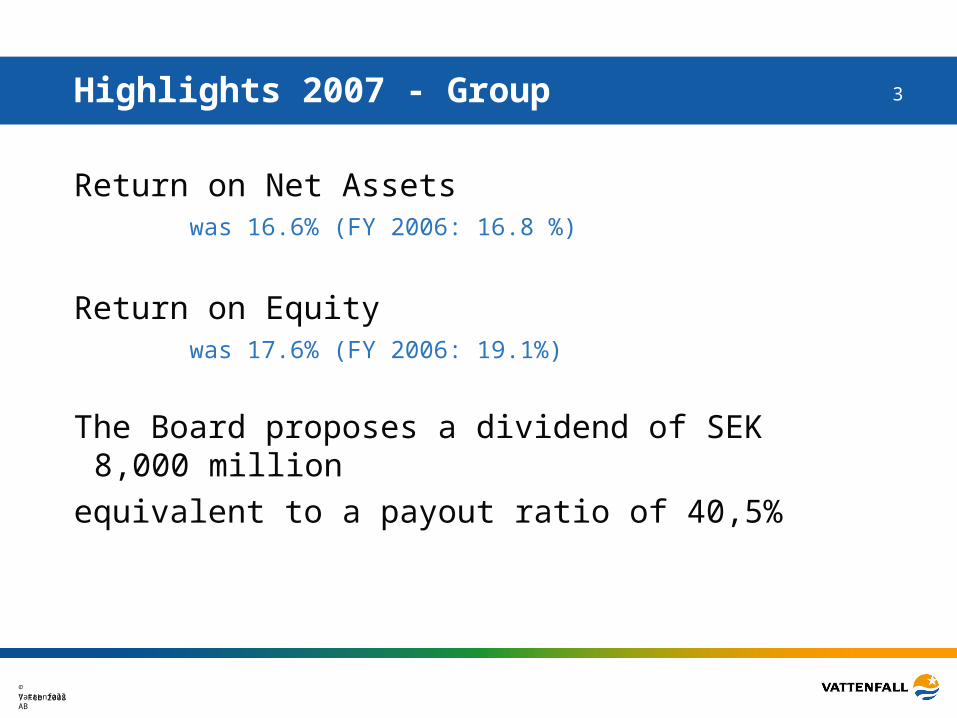

Return on Net Assetswas 16.6% (FY 2006: 16.8 %)

Return on Equitywas 17.6% (FY 2006: 19.1%)

The Board proposes a dividend of SEK 8,000 million

equivalent to a payout ratio of 40,5%

Highlights 2007 - Group

7 Feb 2008© Vattenfall AB

4Highlights Q4 2007 - Group

Net sales decreased2.8% to SEK 38,329 million (39,428)

EBIT increased24.7% to SEK 6,752 million (5,413)

Profit after tax decreased44.4% to SEK 3,676 million (6,609)

Net debt decreasedby SEK 784 million to SEK 43,740 millionvs 30 September 2007

7 Feb 2008© Vattenfall AB

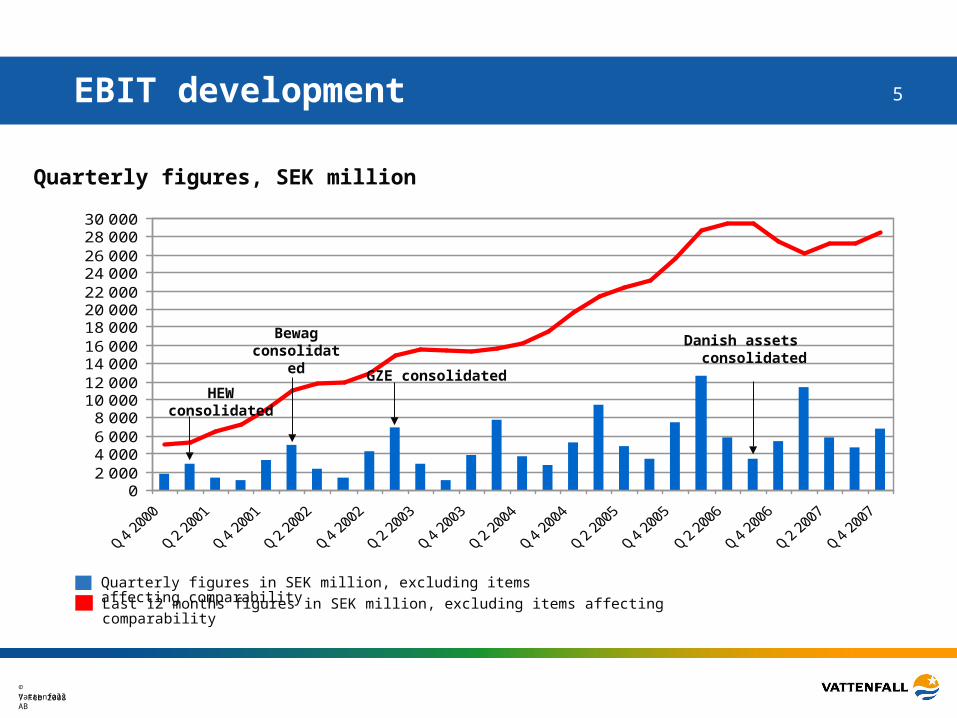

5EBIT development

Quarterly figures, SEK million

Quarterly figures in SEK million, excluding items affecting comparability

Last 12 months figures in SEK million, excluding items affecting comparability

02 0004 0006 0008 000

10 00012 00014 00016 00018 00020 00022 00024 00026 00028 00030 000

HEW consolidated

Bewag consolidated

GZE consolidated

Danish assets consolidated

7 Feb 2008© Vattenfall AB

6

55.2

73.8

35.21.2

77.7

51.3

36.6

1.9

14.0

21.8

8.20.6

Lower nuclear but higher fossil generation

21 %

41 %

20.6

14.8

9.00.4

HydroNuclearFossilOther

FY 2007 total: 167.6 TWh FY 2006 total: 165.4 TWh

Q4 2006 total: 44.8 TWhQ4 2007 total: 44.7 TWh

Other=wind, biofuel, waste

7 Feb 2008© Vattenfall AB

7

15.5

8.5

11.2

14.8

10.710.7

5.6

3.2

4.1

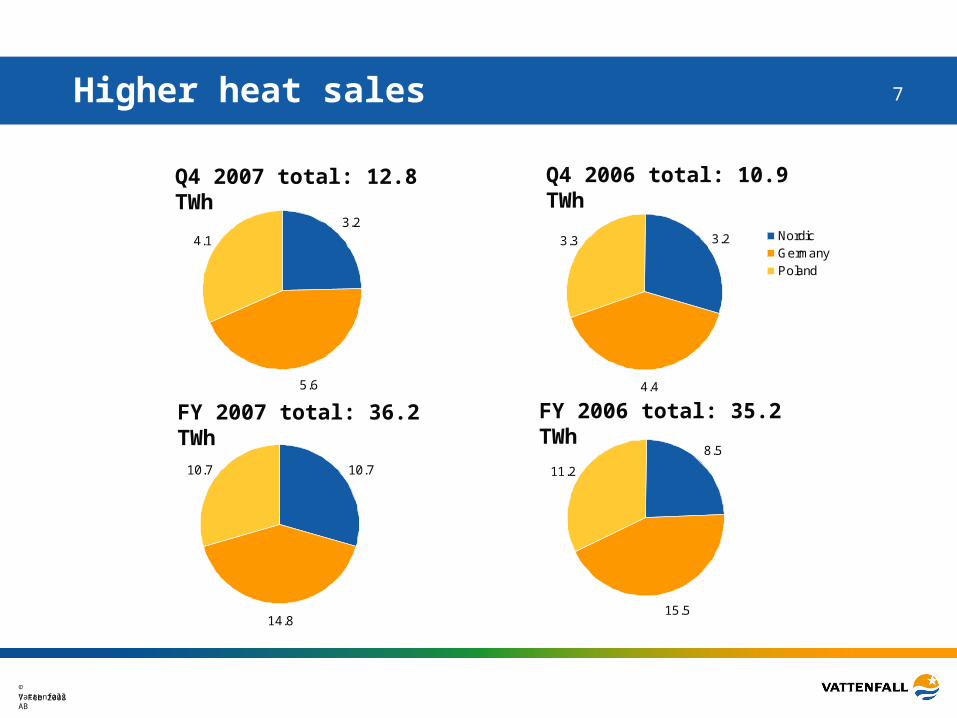

Higher heat sales

21 %

41 %

4.4

3.23.3 NordicGermanyPoland

FY 2007 total: 36.2 TWh FY 2006 total: 35.2 TWh

Q4 2006 total: 10.9 TWhQ4 2007 total: 12.8 TWh

7 Feb 2008© Vattenfall AB

8Important events

• Unplanned outages at German nuclear plants

• Loss of retail customers in Germany but increasing market shares in the Nordic countries

• Several changes in senior Management

• Continued harsh network regulation in Germany

• Major climate initiatives including launching of an ambitous CO2

reduction target – to cut emissions by 50% until 2030

• Quantitative targets set for each ”strategic ambition”

7 Feb 2008© Vattenfall AB

9Nuclear update – post outages on 28 June

• Damage at German nuclear plant Krümmel has been repaired, some work is still under way

• Following the events, the work at the nuclear power plants Brunsbüttel and Krümmel, a testing and renovations programme as well as the instituting of the September 2007 recommendations, is continued.

• The plants will remain shut-down until these activities are fully completed.

• FY 2007 financial impact totals approximately EUR 201 million(SEK 1,900 million)

Krümmel (1,346 MW) Brunsbüttel (771 MW)

7 Feb 2008© Vattenfall AB

10Important events

• Unplanned outages at German nuclear plants

• Loss of retail customers in Germany but increasing market shares in the Nordic countries

• Several changes in senior Management

• Continued harsh network regulation in Germany

• Major climate initiatives including launching of an ambitous CO2

reduction target

• Quantitative targets set for each ”strategic ambition”

7 Feb 2008© Vattenfall AB

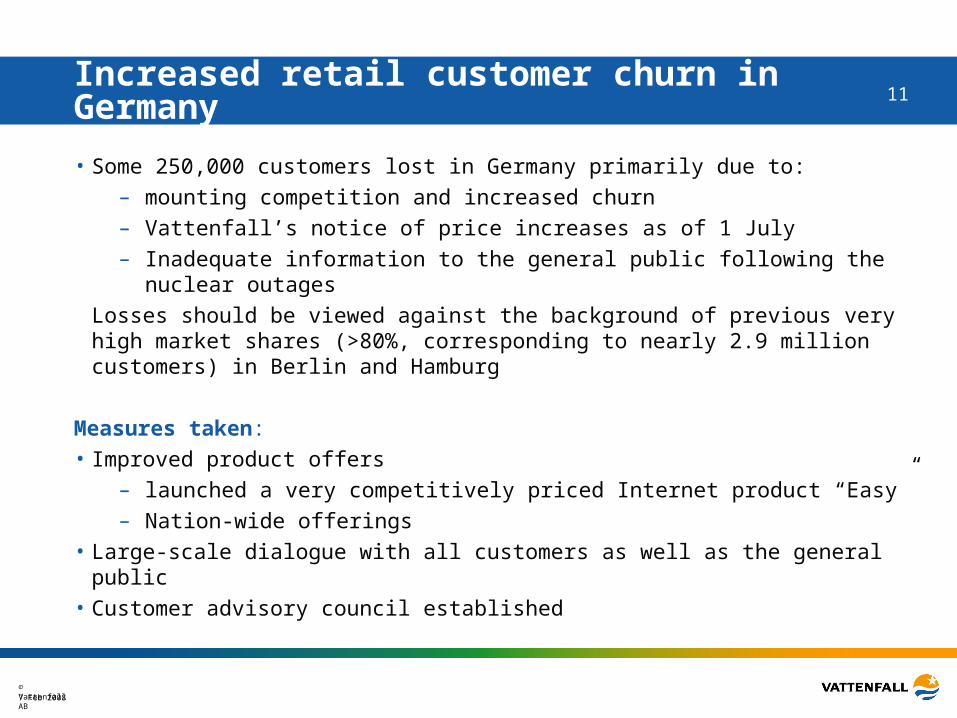

11Increased retail customer churn in Germany

• Some 250,000 customers lost in Germany primarily due to:

– mounting competition and increased churn

– Vattenfall’s notice of price increases as of 1 July

– Inadequate information to the general public following the nuclear outages

Losses should be viewed against the background of previous very high market shares (>80%, corresponding to nearly 2.9 million customers) in Berlin and Hamburg

Measures taken:

• Improved product offers

– launched a very competitively priced Internet product “Easy”

– Nation-wide offerings

• Large-scale dialogue with all customers as well as the general public

• Customer advisory council established

7 Feb 2008© Vattenfall AB

12We are growing our market shares in Sweden

• Vattenfall has exceeded one (1) million customers in the Nordic countries

• Vattenfall’s Swedish retail customer market share has grown from 13% to 15%.

• Customer satisfaction index has improved

• Vattenfall’s products are considered best in the market

7 Feb 2008© Vattenfall AB

13Important events

• Unplanned outages at German nuclear plants

• Loss of retail customers in Germany but increasing market shares in the Nordic countries

• Several changes in senior Management

• Continued harsh network regulation in Germany

• Major climate initiatives including launching of an ambitous CO2

reduction target – to cut emissions by 50% until 2030

• Quantitative targets set for each ”strategic ambition”

7 Feb 2008© Vattenfall AB

14Management and organisational changes

July 2007 Klaus Rauscher resigned asHead of Vattenfall Europe AG and BG Germany.Hans-Jürgen Cramer appointed actingHead of Business Group Germany

August 2007 Helmar Rendez appointednew Head of Group Strategies

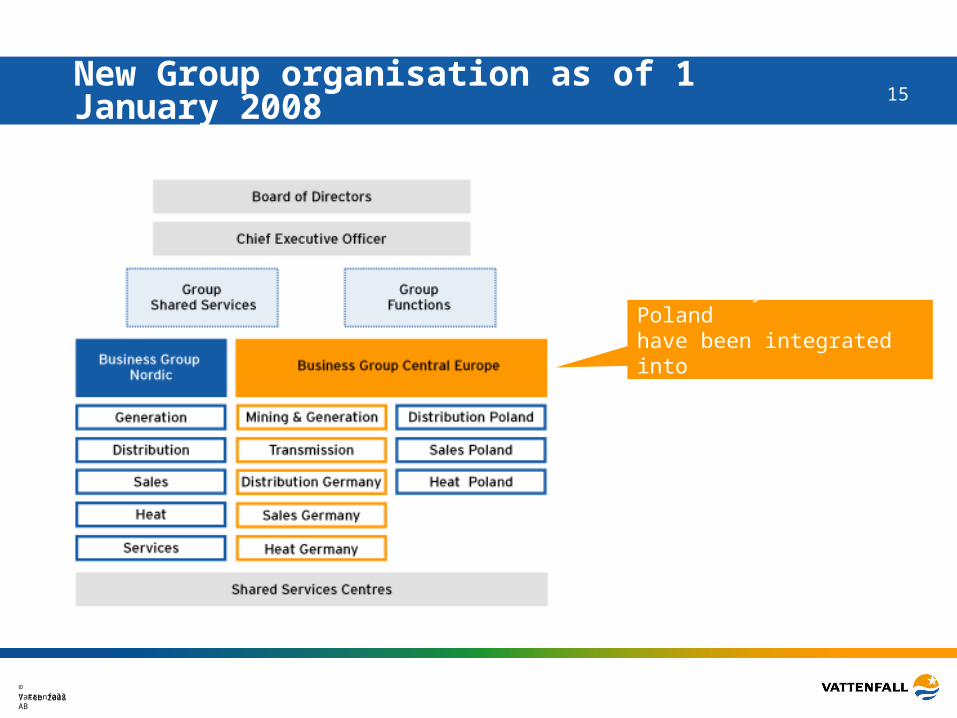

January 2008 BG Germany and BG Poland integrated intoBG Central Europe.Tuomo Hatakka appointedHead of BG Central Europe

February 2008 Carolina Wallenius appointed new Head of Group Communications

February 2008 New composition of Executive Group Management (EGM)

7 Feb 2008© Vattenfall AB

15New Group organisation as of 1 January 2008

BG Germany and BG Poland have been integrated intoBG Central Europe

7 Feb 2008© Vattenfall AB

16Important events

• Unplanned outages at German nuclear plants

• Loss of retail customers in Germany but increasing market shares in the Nordic countries

• Several changes in senior Management

• Continued harsh network regulation in Germany

• Major climate initiatives including launching of an ambitous CO2

reduction target – to cut emissions by 50% until 2030

• Quantitative targets set for each ”strategic ambition”

7 Feb 2008© Vattenfall AB

17Rulings from German network regulator

May 2007 The higher Regional Court in Düsseldorf overruled the Regulator’s demand for retroactive tariff reduction

Jan 2008 Bundesnetzagentur ruling on the Distribution business for DSO

Berlin and Hamburg (tariffs valid until end of 2008):• 16% cut on applied tariff in Berlin meaning 10% lower tariff

level compared with 2007• 18% cut on applied tariff in Hamburg meaning virtually

unchanged tariff level compared with 2007

Jan 2008 Ruling on the Transmission business (tariff valid until end of 2008)• 15% cut on applied tariff meaning about 4% higher tariff level compared with 2007. However, costs for e.g. balancing power have increased.

7 Feb 2008© Vattenfall AB

18Important events

• Unplanned outages at German nuclear plants

• Loss of retail customers in Germany but increasing market shares in the Nordic countries

• Several changes in senior Management

• Continued harsh network regulation in Germany

• Major climate initiatives including launching of an ambitous CO2

reduction target – to cut emissions by 50% until 2030

• Quantitative targets set for each ”strategic ambition”

7 Feb 2008© Vattenfall AB

19Vattenfall has published a global Climate Map

For more information see www.vattenfall.com

7 Feb 2008© Vattenfall AB

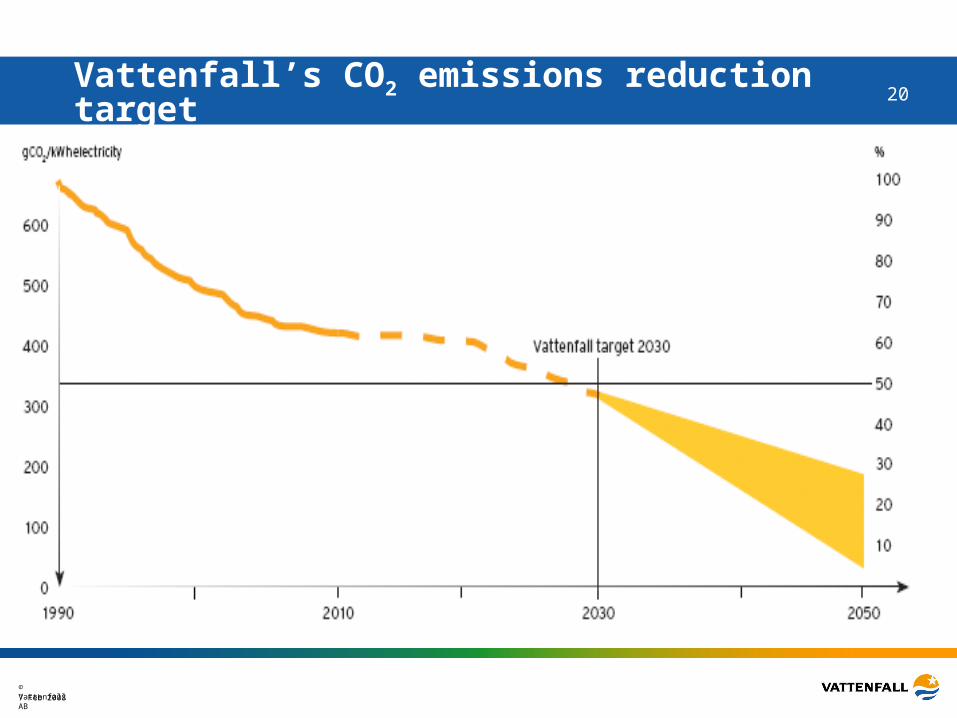

20Vattenfall’s CO2 emissions reduction target

7 Feb 2008© Vattenfall AB

21Important events

• Unplanned outages at German nuclear plants

• Loss of retail customers in Germany but increasing market shares in the Nordic countries

• Several changes in senior Management

• Continued harsh network regulation in Germany

• Major climate initiatives including launching of an ambitous CO2

reduction target – to cut emissions by 50% until 2030

• Quantitative targets set for each ”strategic ambition”

7 Feb 2008© Vattenfall AB

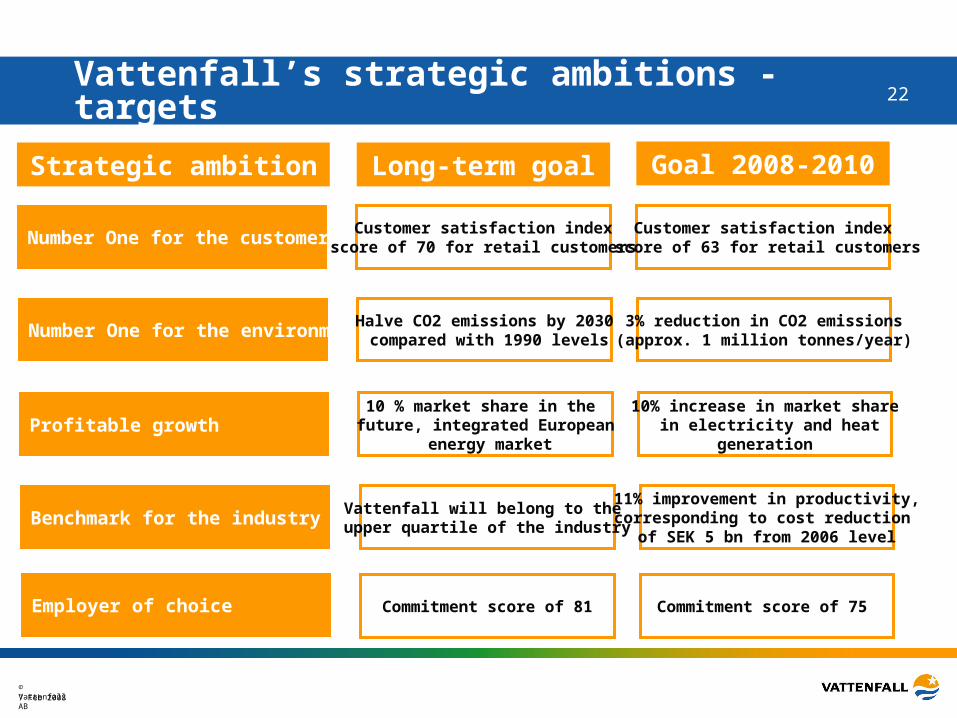

22Vattenfall’s strategic ambitions - targets

Number One for the customer

Number One for the environment

Profitable growth

Benchmark for the industry

Employer of choice

Strategic ambition

Customer satisfaction index score of 70 for retail customers

Halve CO2 emissions by 2030 compared with 1990 levels

10 % market share in the future, integrated European

energy market

Vattenfall will belong to the upper quartile of the industry

Commitment score of 81

Long-term goal

Customer satisfaction index score of 63 for retail customers

3% reduction in CO2 emissions(approx. 1 million tonnes/year)

10% increase in market share in electricity and heat

generation

11% improvement in productivity,corresponding to cost reduction

of SEK 5 bn from 2006 level

Commitment score of 75

Goal 2008-2010

© Vattenfall AB

Financials

Jan Erik Back, CFO

7 Feb 2008© Vattenfall AB

24

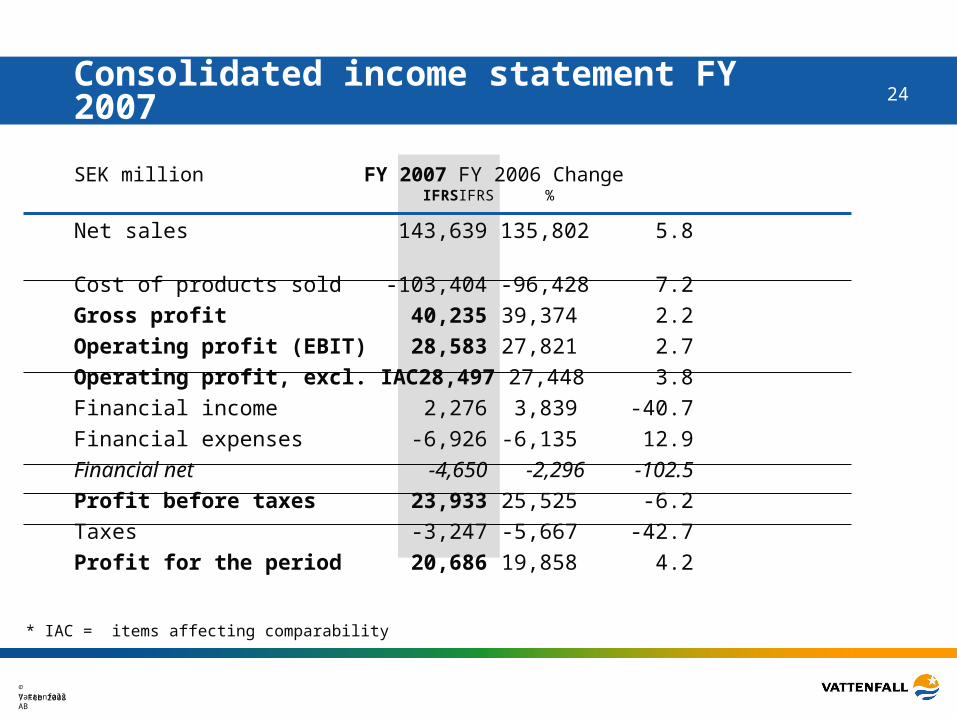

SEK million FY 2007 FY 2006 Change IFRS IFRS %

Consolidated income statement FY 2007

* IAC = items affecting comparability

Net sales 143,639 135,802 5.8

Cost of products sold -103,404 -96,428 7.2

Gross profit 40,235 39,374 2.2

Operating profit (EBIT) 28,583 27,821 2.7

Operating profit, excl. IAC 28,497 27,448 3.8

Financial income 2,276 3,839 -40.7

Financial expenses -6,926 -6,135 12.9

Financial net -4,650 -2,296 -102.5

Profit before taxes 23,933 25,525 -6.2

Taxes -3,247 -5,667 -42.7

Profit for the period 20,686 19,858 4.2

7 Feb 2008© Vattenfall AB

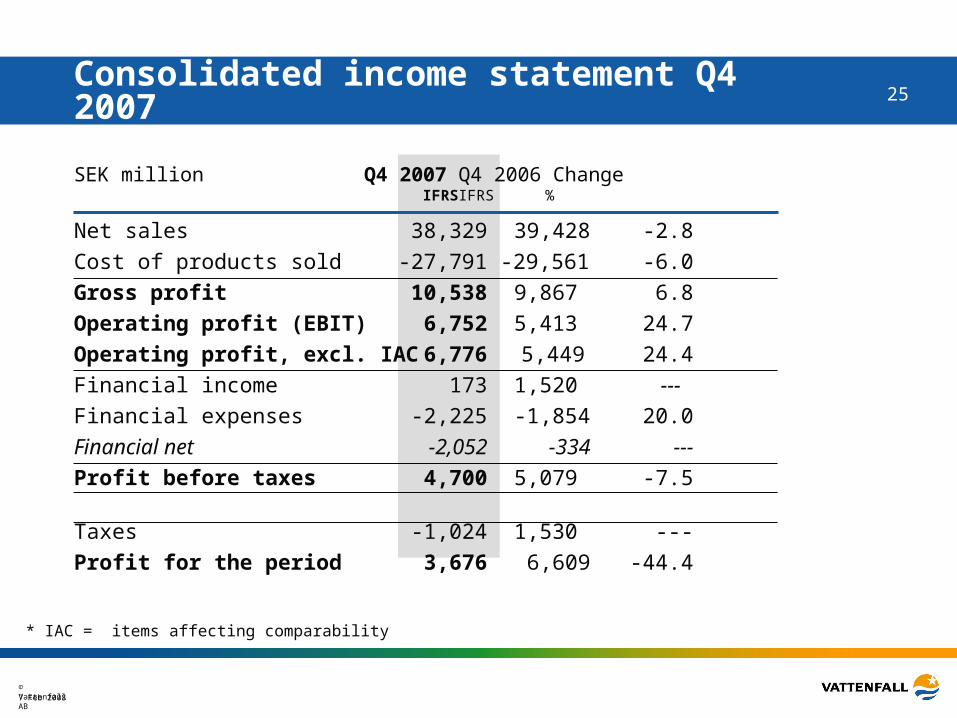

25

SEK million Q4 2007 Q4 2006 Change IFRS IFRS %

Consolidated income statement Q4 2007

* IAC = items affecting comparability

Net sales 38,329 39,428 -2.8

Cost of products sold -27,791 -29,561 -6.0

Gross profit 10,538 9,867 6.8

Operating profit (EBIT) 6,752 5,413 24.7

Operating profit, excl. IAC 6,776 5,449 24.4

Financial income 173 1,520 ---

Financial expenses -2,225 -1,854 20.0

Financial net -2,052 -334 ---

Profit before taxes 4,700 5,079 -7.5

Taxes -1,024 1,530 ---

Profit for the period 3,676 6,609 -44.4

7 Feb 2008© Vattenfall AB

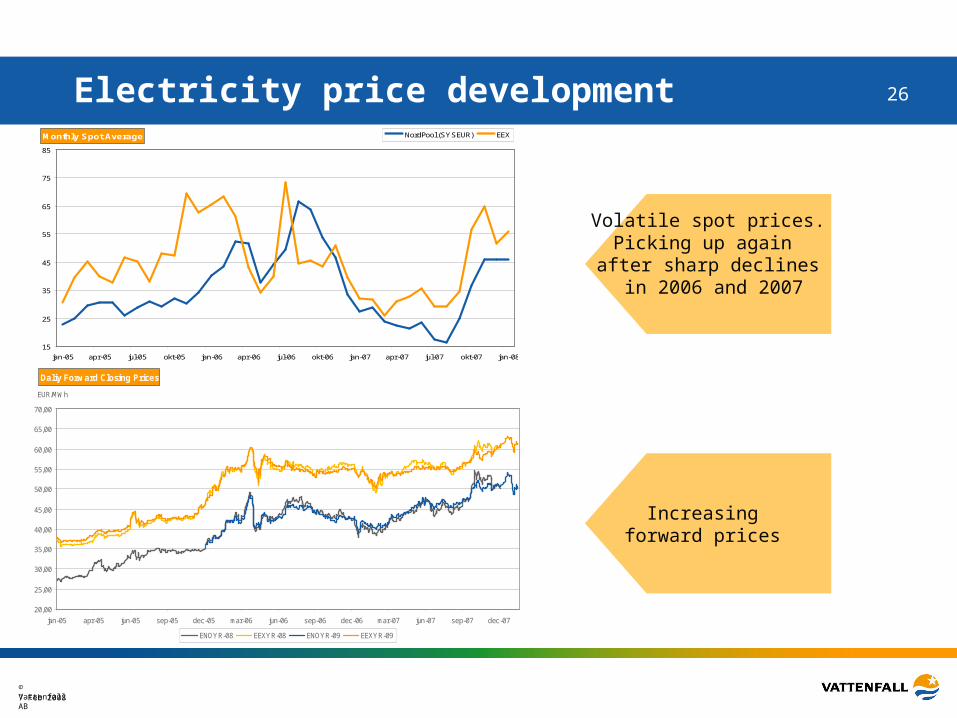

26Electricity price development

Volatile spot prices.Picking up again

after sharp declines in 2006 and 2007

Increasing forward prices

Monthly Spot Average

15

25

35

45

55

65

75

85

jan-05 apr-05 jul-05 okt-05 jan-06 apr-06 jul-06 okt-06 jan-07 apr-07 jul-07 okt-07 jan-08

NordPool (SYSEUR) EEX

Daliy Forward Closing Prices

20,00

25,00

30,00

35,00

40,00

45,00

50,00

55,00

60,00

65,00

70,00

jan-05 apr-05 jun-05 sep-05 dec-05 mar-06 jun-06 sep-06 dec-06 mar-07 jun-07 sep-07 dec-07

ENOYR-08 EEXYR-08 ENOYR-09 EEXYR-09

EUR/MWh

7 Feb 2008© Vattenfall AB

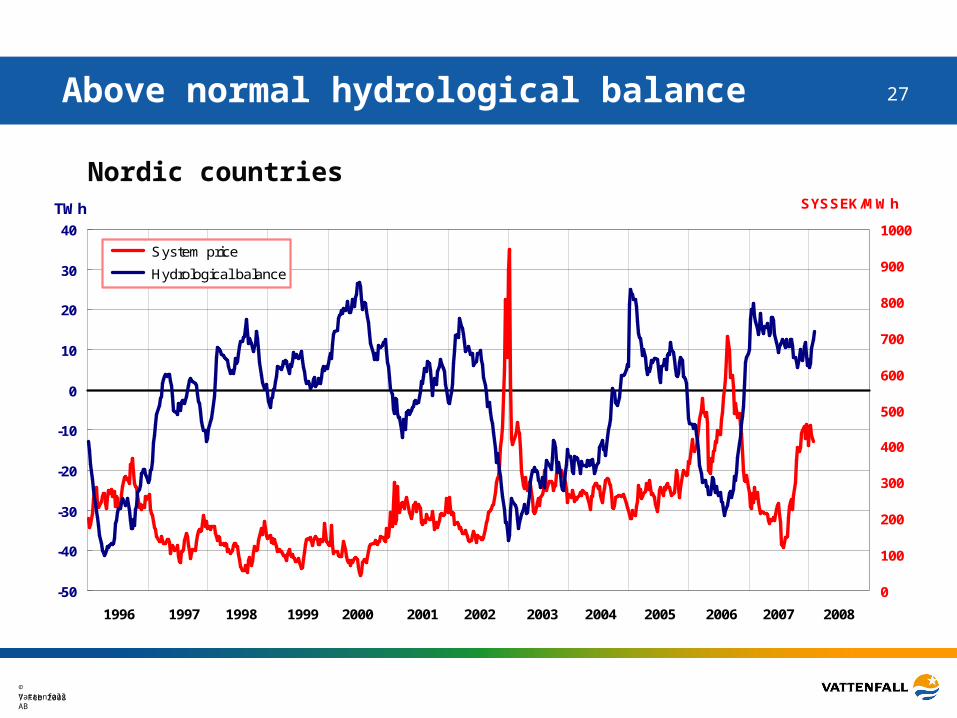

27Above normal hydrological balance

-50

-40

-30

-20

-10

0

10

20

30

40

0

100

200

300

400

500

600

700

800

900

1000

System price

Hydrological balance

SYSSEK/MWhTWh

1996 199919981997 2003200220012000 2004 2005 2006 2007 2008

Nordic countries

7 Feb 2008© Vattenfall AB

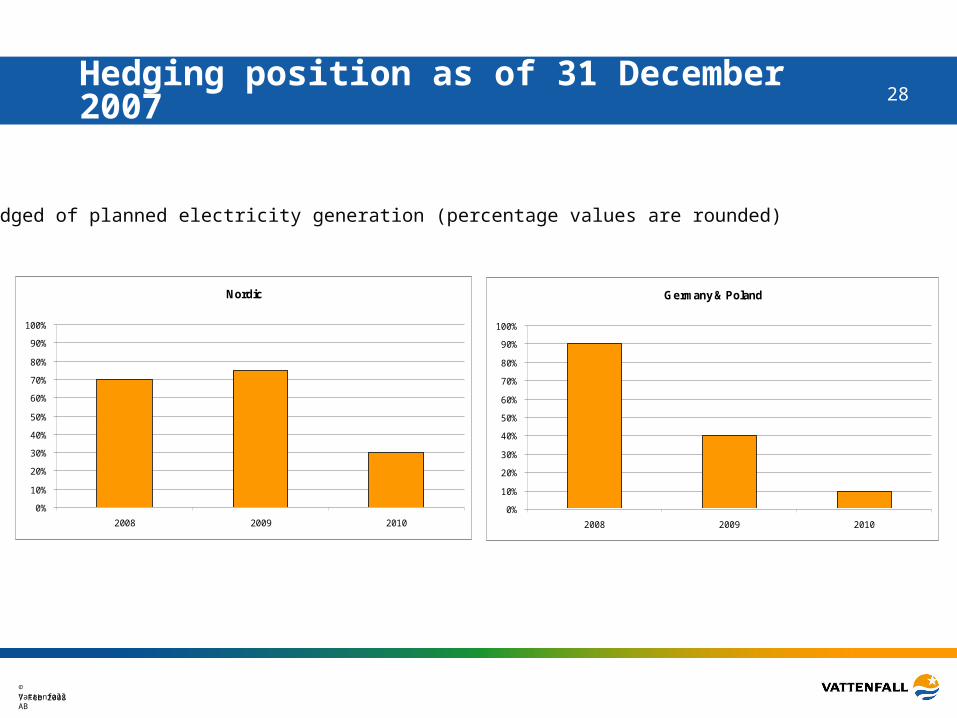

28Hedging position as of 31 December 2007

% hedged of planned electricity generation (percentage values are rounded)

Nordic

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2008 2009 2010

Germany & Poland

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2008 2009 2010

7 Feb 2008© Vattenfall AB

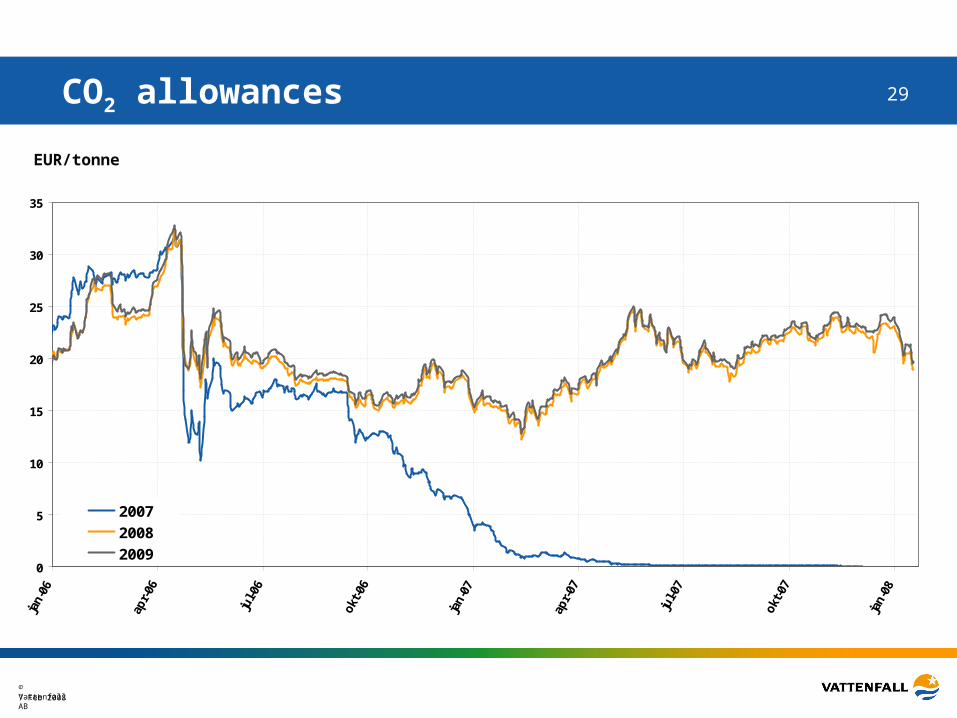

29

EUR/tonne

CO2 allowances

0

5

10

15

20

25

30

35

2007

2008

2009

7 Feb 2008© Vattenfall AB

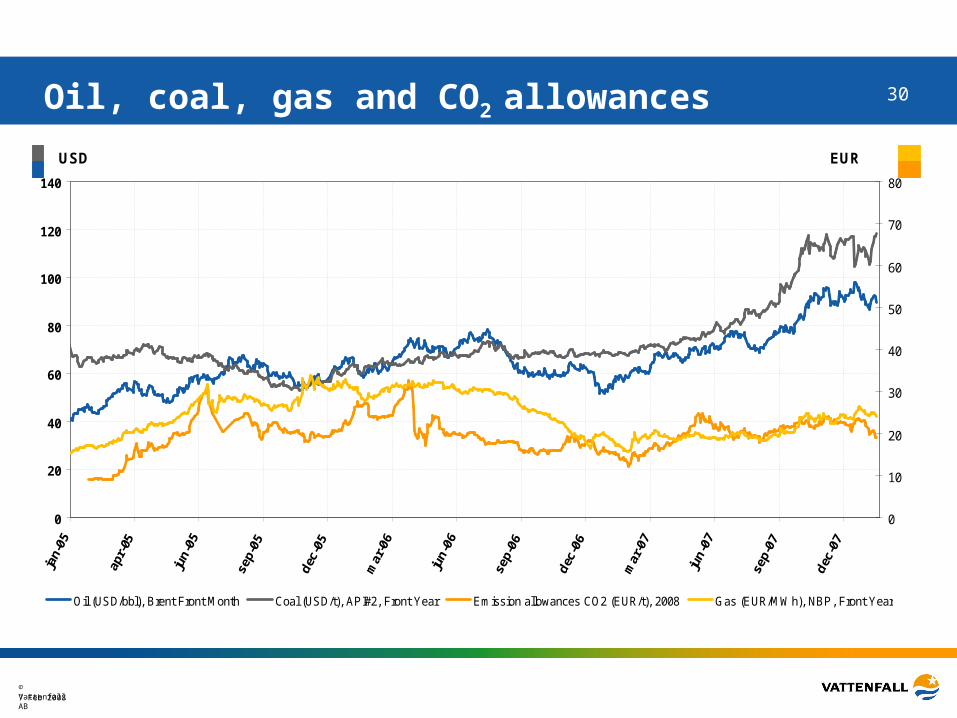

30Oil, coal, gas and CO2 allowances

0

20

40

60

80

100

120

140

0

10

20

30

40

50

60

70

80

Oil (USD/bbl), Brent Front Month Coal (USD/t), API#2, Front Year Emission allowances CO2 (EUR/t), 2008 Gas (EUR/MWh), NBP, Front Year

USD EUR

7 Feb 2008© Vattenfall AB

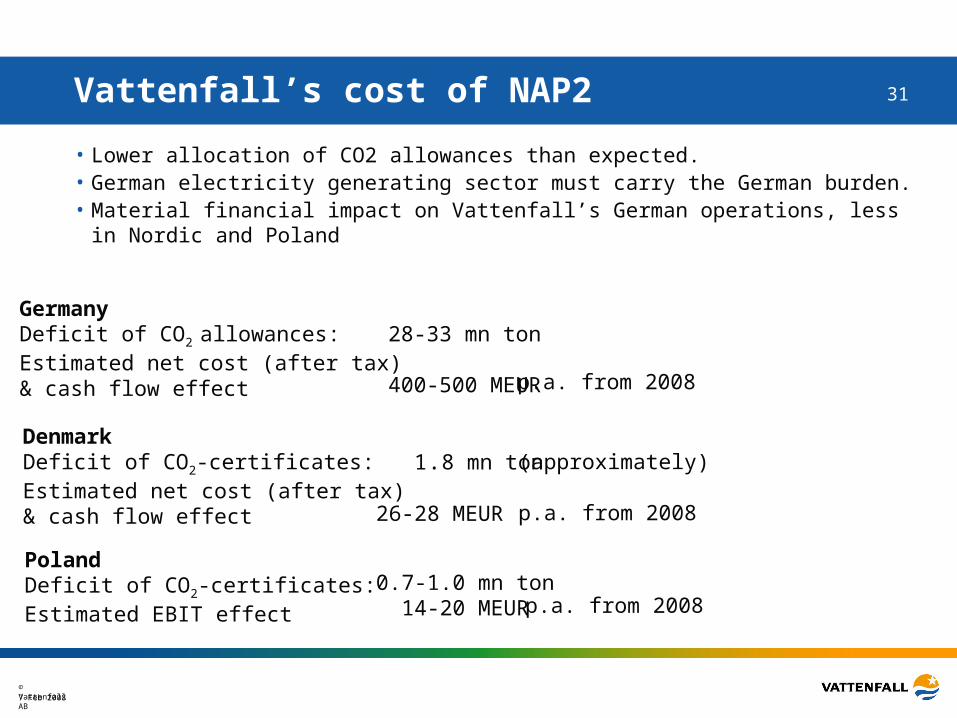

31Vattenfall’s cost of NAP2

• Lower allocation of CO2 allowances than expected.• German electricity generating sector must carry the German burden. • Material financial impact on Vattenfall’s German operations, less in Nordic

and Poland

Germany Deficit of CO2 allowances:Estimated net cost (after tax) & cash flow effect

28-33 mn ton

400-500 MEUR p.a. from 2008

DenmarkDeficit of CO2-certificates:Estimated net cost (after tax)& cash flow effect

1.8 mn ton

26-28 MEUR

(approximately)

p.a. from 2008

PolandDeficit of CO2-certificates:Estimated EBIT effect

0.7-1.0 mn ton 14-20 MEUR p.a. from 2008

7 Feb 2008© Vattenfall AB

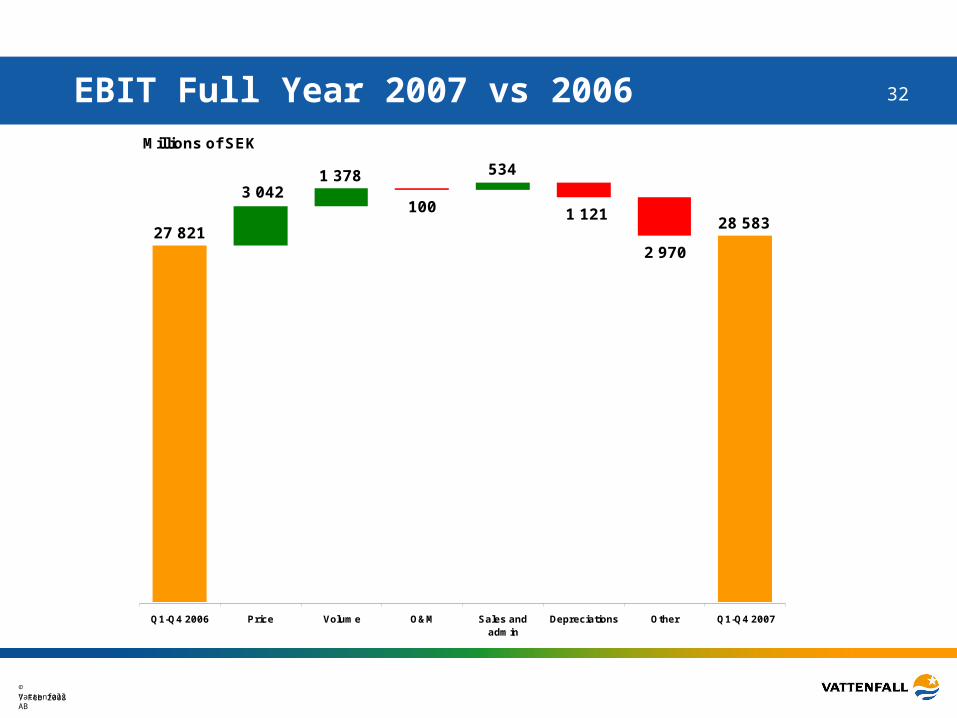

32EBIT Full Year 2007 vs 2006

27 82128 583

3 0421 378

100

534

1 121

2 970

Q1-Q4 2006 Price Volume O&M Sales andadmin

Depreciations Other Q1-Q4 2007

Millions of SEK

7 Feb 2008© Vattenfall AB

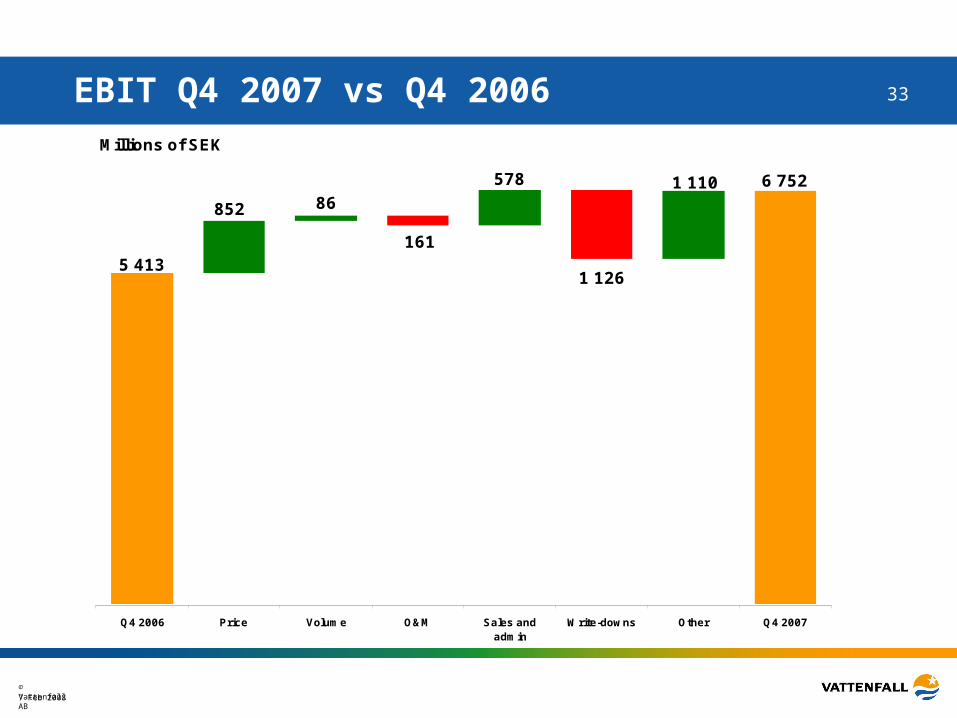

33EBIT Q4 2007 vs Q4 2006

5 413

6 752

852 86

161

578

1 126

1 110

Q4 2006 Price Volume O&M Sales andadmin

Write-downs Other Q4 2007

Millions of SEK

7 Feb 2008© Vattenfall AB

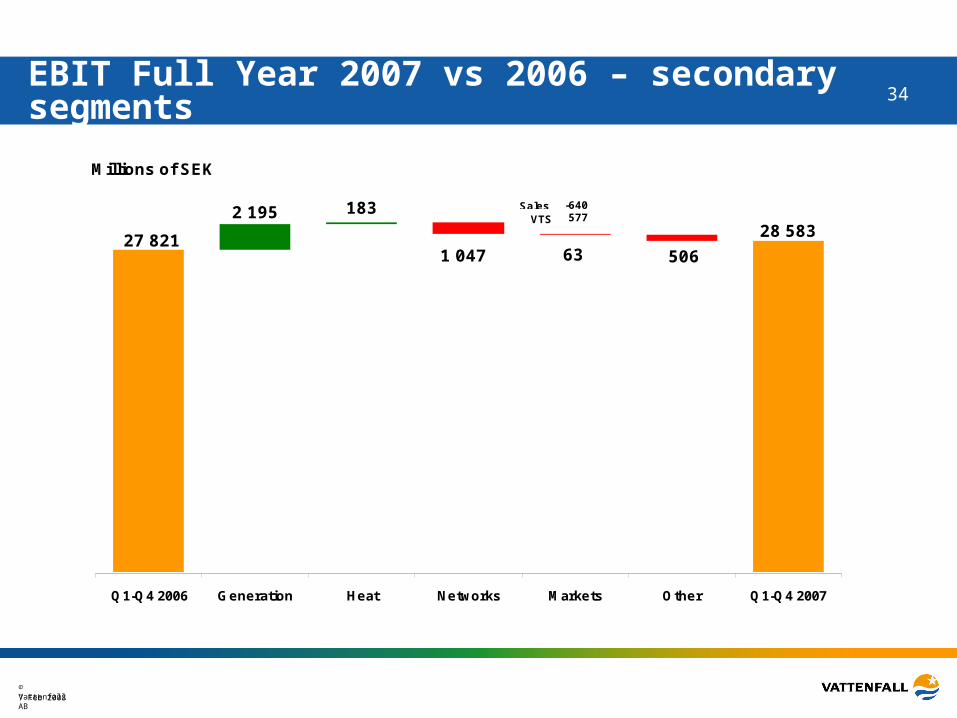

34EBIT Full Year 2007 vs 2006 – secondary segments

27 82128 583

2 195 183

1 047 63 506

-640577

Q1-Q4 2006 Generation Heat Networks Markets Other Q1-Q4 2007

Millions of SEK

SalesVTS

7 Feb 2008© Vattenfall AB

35EBIT Q4 2007 vs Q4 2006 – secondary segments

6 752

5 413

74401

2161 096

448

580

-179

Q4 2006 Generation Heat Networks Markets Other Q4 2007

Millions of SEK

VTSSales

7 Feb 2008© Vattenfall AB

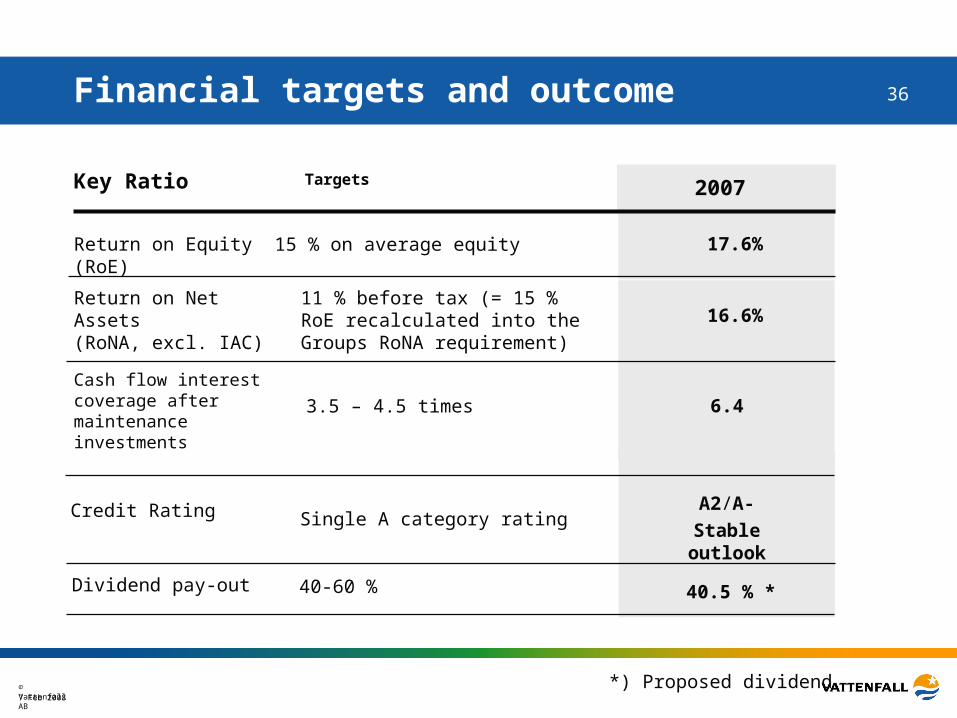

36Financial targets and outcome

2007

Single A category ratingCredit Rating

3.5 – 4.5 times

Cash flow interest coverage after maintenance investments

11 % before tax (= 15 % RoE recalculated into the Groups RoNA requirement)

Return on Net Assets(RoNA, excl. IAC)

Return on Equity (RoE)

TargetsKey Ratio

15 % on average equity 17.6%

16.6%

6.4

A2/A-

Stable outlook

40-60 %Dividend pay-out 40.5 % *

*) Proposed dividend

7 Feb 2008© Vattenfall AB

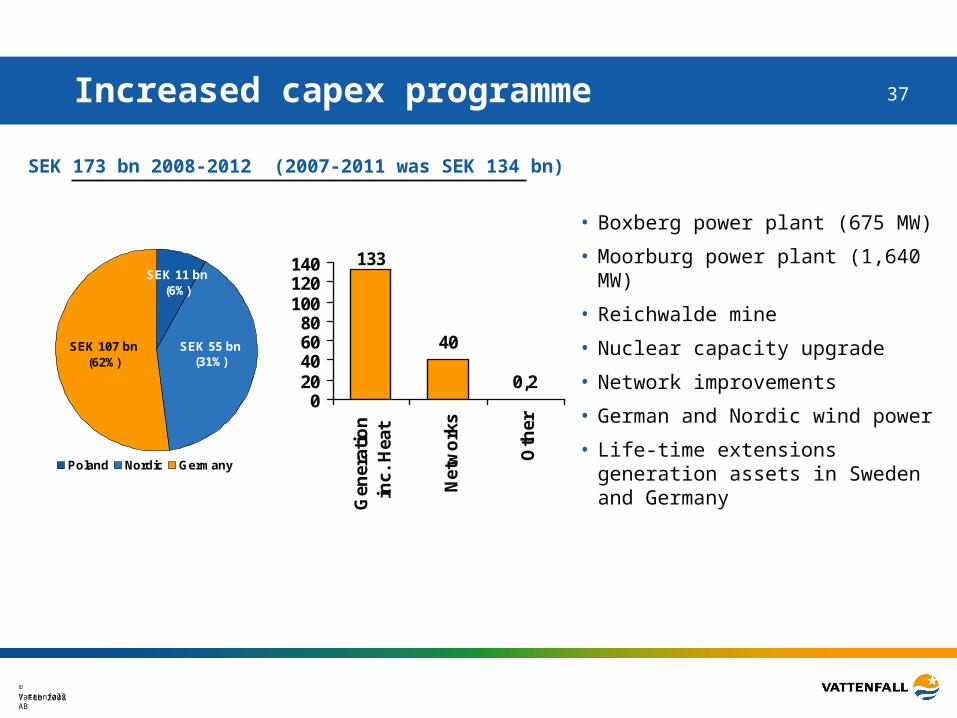

37Increased capex programme

SEK 173 bn 2008-2012 (2007-2011 was SEK 134 bn)

133

40

0,20

20406080

100120140

Gen

erat

ion

inc.

Hea

t

Net

wo

rks

Oth

er

• Boxberg power plant (675 MW)

• Moorburg power plant (1,640 MW)

• Reichwalde mine

• Nuclear capacity upgrade

• Network improvements

• German and Nordic wind power

• Life-time extensions generation assets in Sweden and Germany

SEK 55 bn(31%)

SEK 107 bn(62%)

SEK 11 bn(6%)

Poland Nordic Germany

7 Feb 2008© Vattenfall AB

38

SEK million 31/12/07 31/12/06 Change IFRS IFRS % I

Consolidated balance sheet

Non-current assets 264,864 251,893 5.1

Current assets 73,372 71,273 2.9

Total assets 338,236 323,166 4.7

Equity 124,132 107,674 15.3

Capital Securities 9,341 8,911 4.8

Interest-bearing liabilitites 57,848 62,664 -7.7

Interest-bearing provisions 56,250 49,217 14.3

Pension provisions 17,735 16,877 5.1

Tax liabilities 26,632 33,460 -20.4

Other non-interest-bearing liabilitites 46,298 44,363 4.4

Total equity and liabilities 338,236 323,166 4.7

7 Feb 2008© Vattenfall AB

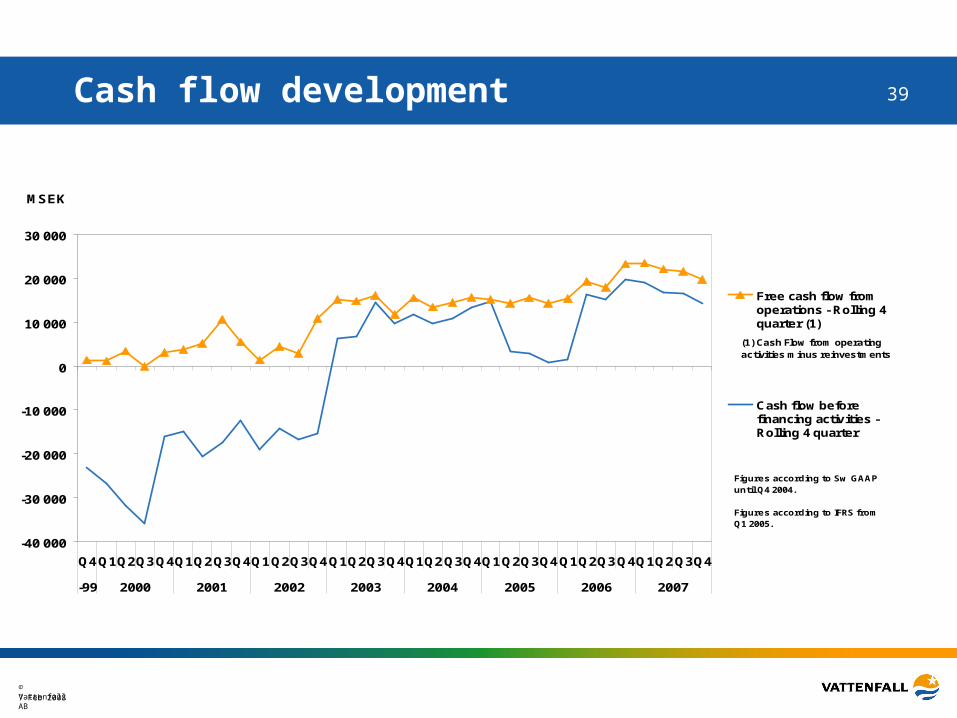

39Cash flow development

-40 000

-30 000

-20 000

-10 000

0

10 000

20 000

30 000

Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4

-99 2000 2001 2002 2003 2004 2005 2006 2007

Free cash flow fromoperations - Rolling 4quarter (1)

Cash flow beforefinancing activities -Rolling 4 quarter

MSEK

(1) Cash Flow from operating activities minus reinvestments

Figures according to Sw GAAP until Q4 2004.

Figures according to IFRS from Q1 2005.

7 Feb 2008© Vattenfall AB

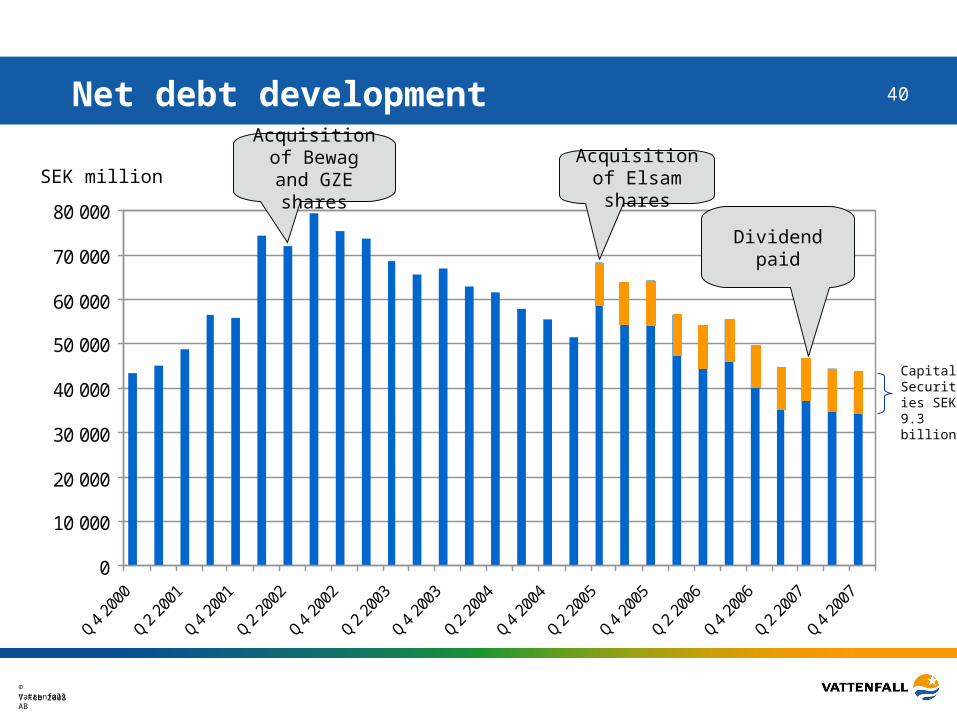

40Net debt development

SEK million

0

10 000

20 000

30 000

40 000

50 000

60 000

70 000

80 000

Capital Securities SEK 9.3 billion

Acquisition of Elsam shares

Acquisition of Bewag and GZE shares

Dividend paid

7 Feb 2008© Vattenfall AB

41

Thank you for your attention

© Vattenfall AB

Back-up slides

7 Feb 2008© Vattenfall AB

43Highlights 2007 - Nordic

• EBIT decreased by 696 SEK million to SEK 12 591 million (-5,2%)

• Higher Fuel and O&M costs – mainly due to Danish operations.

• Lower results in Distribution due to the storm ”Per” (290 MSEK) and provsions for restructuring measures (160 MSEK).

• Higher electricity generation due to increased hydro-, fossil- and wind power.

• All windmills at the Lillgrund windpower farm are now generating electricity.

7 Feb 2008© Vattenfall AB

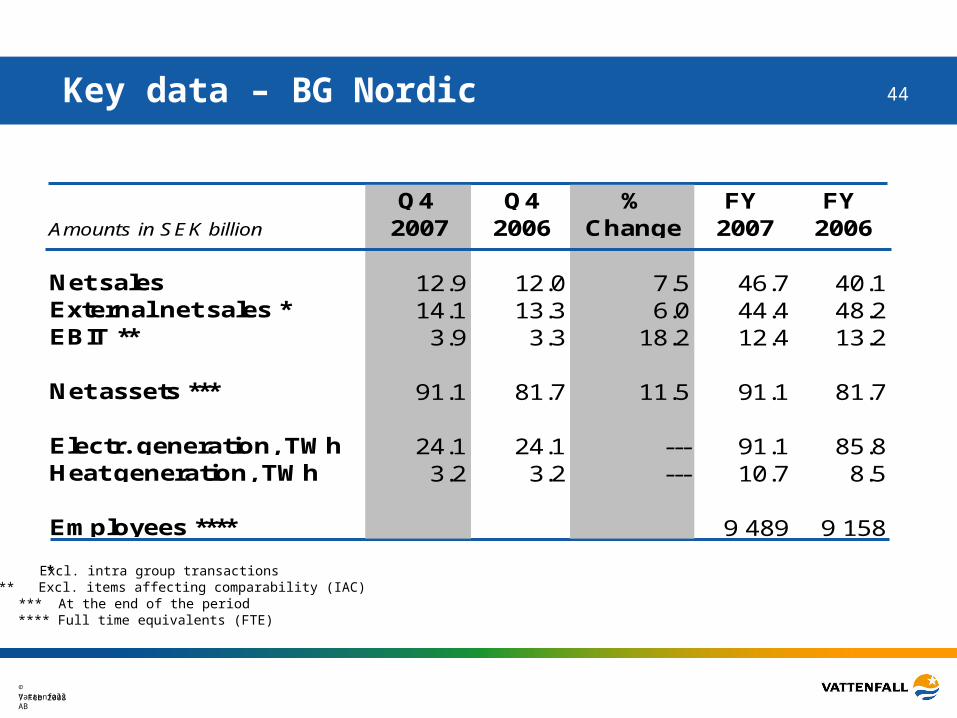

44Key data – BG Nordic

* Excl. intra group transactions** Excl. items affecting comparability (IAC)*** At the end of the period**** Full time equivalents (FTE)

Q4 Q4 % FY FY Amounts in SEK billion 2007 2006 Change 2007 2006

Net sales 12.9 12.0 7.5 46.7 40.1External net sales * 14.1 13.3 6.0 44.4 48.2EBIT ** 3.9 3.3 18.2 12.4 13.2

Net assets *** 91.1 81.7 11.5 91.1 81.7

Electr. generation, TWh 24.1 24.1 --- 91.1 85.8Heat generation, TWh 3.2 3.2 --- 10.7 8.5

Employees **** 9 489 9 158

7 Feb 2008© Vattenfall AB

45Highlights 2007 - Germany

• EBIT increased by SEK 1,454 million to SEK 15 338 million (+10,5%).

• BU Mining & Generation increased its result, despite nuclear outages and impairment losses for pumped storage plants of 1 110 MSEK, thanks to higher prices as well as hedging.

• BU Heat improved its result from the electricity business, mainly due to higher electricity prices.

• Warm weather and storms in the beginning of the year had a negative effect on the BU Heat and BU Distribution businesses.

• Higher feed-in from windpower caused higher EEG costs.

• NAP2 - Total national emissions cut to 453 million tonnes per year. (NAP1 was 499 million tonnes). Vattenfall estimates an annual deficit of 28-33 million tonnes. Estimated cost (after tax) totals EUR 400-500 million.

7 Feb 2008© Vattenfall AB

46Key data – BG Germany

* Excl. intra group transactions** Excl. items affecting comparability (IAC)*** At the end of the period**** Full time equivalents (FTE)

Q4 Q4 % FY FY Amounts in SEK billion 2007 2006 Change 2007 2006

Net sales 29.8 28.5 4.6 112.5 101.5External net sales * 20.6 20.0 3.0 77.5 70.0

EBIT ** 2.8 1.9 47.4 15.4 13.7

Net assets *** 67.8 61.8 9.7 67.8 61.8

Electr. generation, TWh 19.2 19.6 -2.0 72.8 76.2Heat generation, TWh 5.6 4.4 27.3 14.8 15.5

Employees **** 19 656 19 821

7 Feb 2008© Vattenfall AB

47Highlights 2007 - Poland

• EBIT almost flat compared with FY 2006.

• BU Distribution’s results decreased due to tariff reductions which could only partly be compensated by higher volumes.

• Lower heat volumes and prices were compensated by higher prices on electricity.

• Significant positive effect in BU Heat, due to sold excess CO2 allowances.

7 Feb 2008© Vattenfall AB

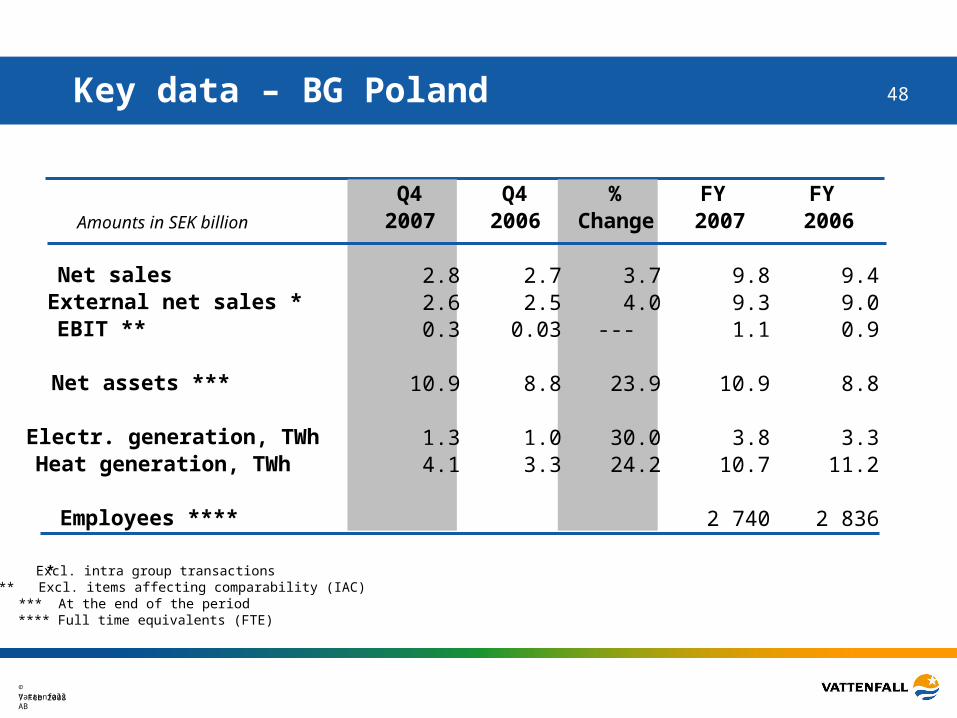

48Key data – BG Poland

* Excl. intra group transactions** Excl. items affecting comparability (IAC)*** At the end of the period**** Full time equivalents (FTE)

Q4 Q4 % FY FY Amounts in SEK billion 2007 2006 Change 2007 2006

Net sales 2.8 2.7 3.7 9.8 9.4External net sales * 2.6 2.5 4.0 9.3 9.0

EBIT ** 0.3 0.03 --- 1.1 0.9

Net assets *** 10.9 8.8 23.9 10.9 8.8

Electr. generation, TWh 1.3 1.0 30.0 3.8 3.3Heat generation, TWh 4.1 3.3 24.2 10.7 11.2

Employees **** 2 740 2 836

7 Feb 2008© Vattenfall AB

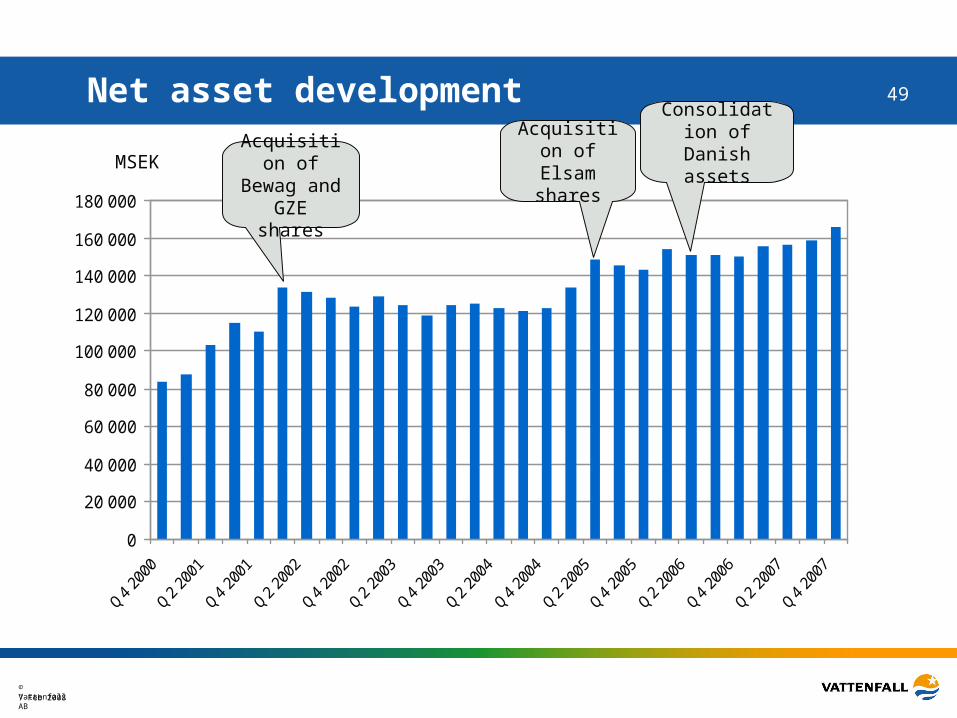

49Net asset development

0

20 000

40 000

60 000

80 000

100 000

120 000

140 000

160 000

180 000

MSEKAcquisition of Elsam shares

Acquisition of Bewag and GZE shares

Consolidation of Danish

assets

7 Feb 2008© Vattenfall AB

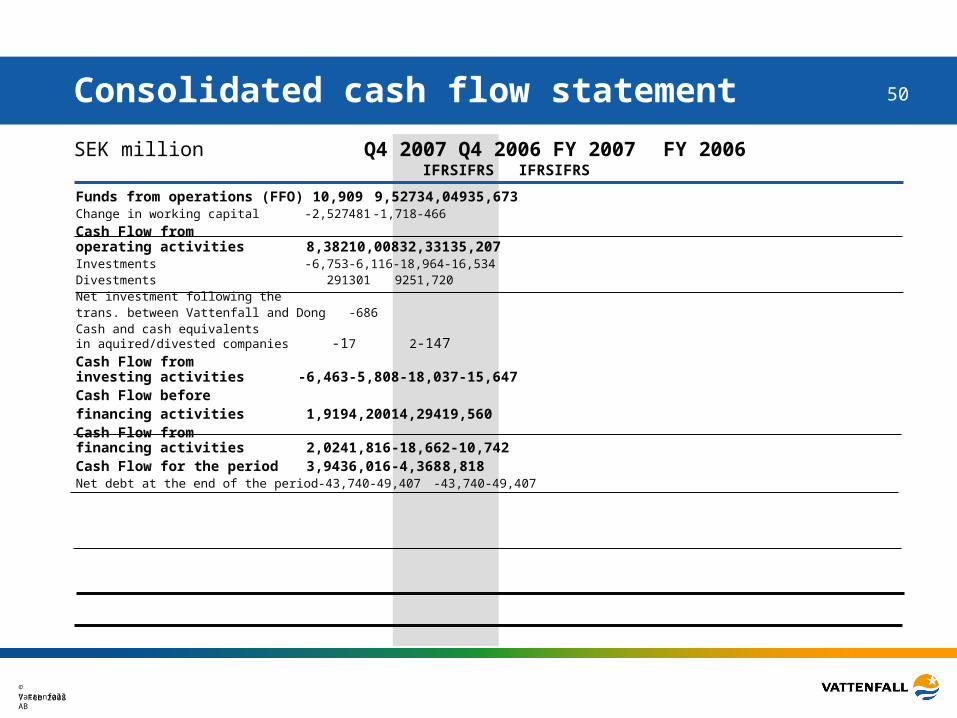

50

SEK million Q4 2007 Q4 2006 FY 2007 FY 2006IFRS IFRS IFRS IFRS

Funds from operations (FFO) 10,909 9,527 34,04935,673Change in working capital -2,527 481 -1,718-466

Cash Flow from operating activities 8,382 10,008 32,33135,207Investments -6,753 -6,116 -18,964-16,534Divestments 291 301 9251,720Net investment following thetrans. between Vattenfall and Dong -686Cash and cash equivalents in aquired/divested companies -1 7 2-147Cash Flow from investing activities -6,463 -5,808 -18,037-15,647Cash Flow before financing activities 1,919 4,200 14,29419,560Cash Flow from financing activities 2,024 1,816 -18,662-10,742Cash Flow for the period 3,943 6,016 -4,3688,818Net debt at the end of the period -43,740 -49,407 -43,740-49,407

Consolidated cash flow statement

7 Feb 2008© Vattenfall AB

51

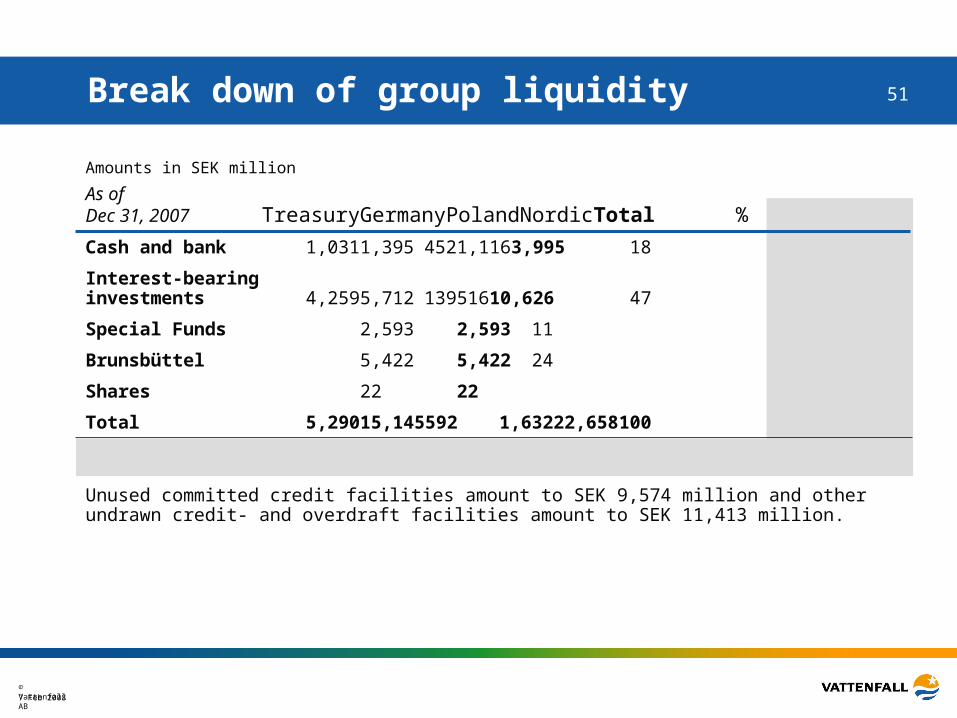

Amounts in SEK million

As ofDec 31, 2007 Treasury Germany Poland NordicTotal %

Cash and bank 1,031 1,395 452 1,1163,995 18

Interest-bearing investments 4,259 5,712 139 51610,626 47

Special Funds 2,593 2,593 11

Brunsbüttel 5,422 5,422 24

Shares 22 22

Total 5,290 15,145 592 1,63222,658 100

Unused committed credit facilities amount to SEK 9,574 million and other undrawn credit- and overdraft facilities amount to SEK 11,413 million.

Break down of group liquidity

7 Feb 2008© Vattenfall AB

52

Amounts in SEK million

As of Dec 31, 2007 Treasury Germany Poland Nordic Total %

Subordinated perpetual Capital Securities 9,341 9,341 14

MTN 652 652 1

EMTN 30,946 30,946 46

Liabilities to assoc. companies 7,106 4,000 11,106 17

Liabilities to minority shareholders 51 5,740 5,791 9

Bank loans and others 1,072 6,273 130 1,878 9,354 14

Total 49,117 10,324 130 7,619 67,190 100

Break down of group debt

7 Feb 2008© Vattenfall AB

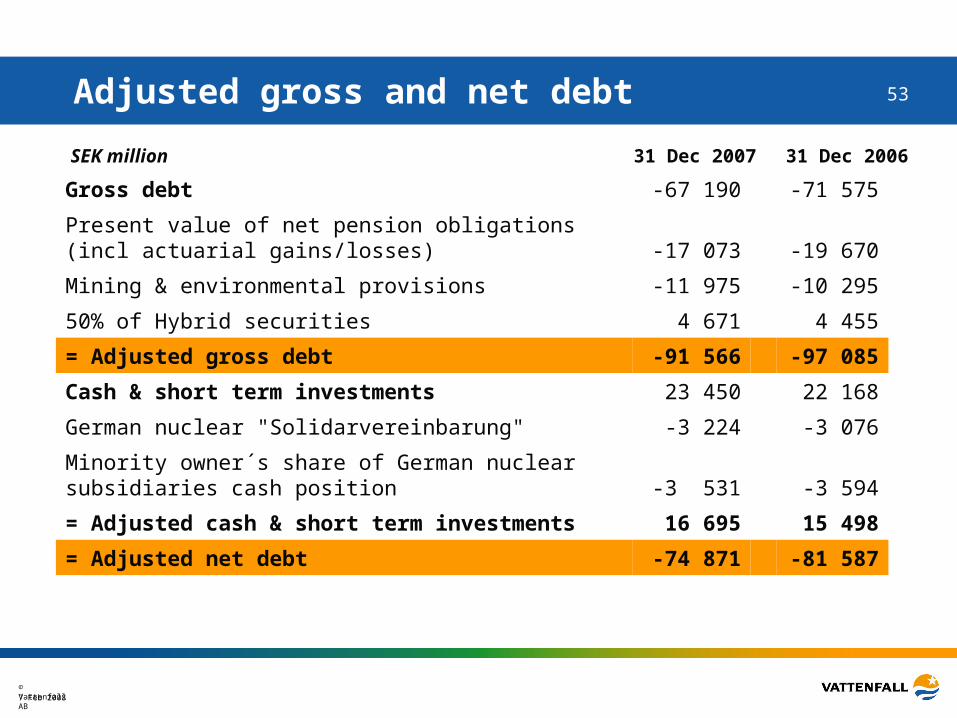

53Adjusted gross and net debt

31 Dec 2007 31 Dec 2006SEK million

Gross debt -67 190 -71 575

Present value of net pension obligations (incl actuarial gains/losses) -17 073 -19 670

Mining & environmental provisions -11 975 -10 295

50% of Hybrid securities 4 671 4 455

= Adjusted gross debt -91 566 -97 085

Cash & short term investments 23 450 22 168

German nuclear "Solidarvereinbarung" -3 224 -3 076

Minority owner´s share of German nuclear subsidiaries cash position -3 531 -3 594

= Adjusted cash & short term investments 16 695 15 498

= Adjusted net debt -74 871 -81 587

7 Feb 2008© Vattenfall AB

54Vattenfall debt maturity profile

Dec 31, 2007 Dec 31, 2006

Duration (years) 3,3 1) 3,3

Average time to maturity (years) 6,7 1) 6,6

Net debt (SEK bn) 43,7 49,4

SEK million

Excluding loans from associated companies and minority owners

1) Based on external debt. Excluding Capital Securities the duration is 2,6 years and average time to maturity 6,5 years.

0

2000

4000

6000

8000

10000

12000

2007 2009 2011 2013 2015 2017 2019 2021 2023 2025 2027 2029 2031 2033 2035 2037

2006 12 31

2007 12 31

7 Feb 2008© Vattenfall AB

55

16,877

26,358

10,295

29,845

1,375

4,6876,502

17,735

29,813

11,975

23,704

2,109

4,8047,549

Pensions

Nuclear

Mining

Taxes

Other

Personnel

Legal

Group provisions (IFRS) up by 1.8%

31 Dec 2007

SEK 97,689 million

31 Dec 2006

SEK 95,969 million

7 Feb 2008© Vattenfall AB

56Return on equity

0%

5%

10%

15%

20%

25%

30%

Rolling 4-quarterIFRS excl IAC

Rolling 4-quarter SwGAAP excl IAC

Average 4-years (16quarter) Sw. GAAP.IFRS from Q42004. Excl. IACRequirement 15%

7 Feb 2008© Vattenfall AB

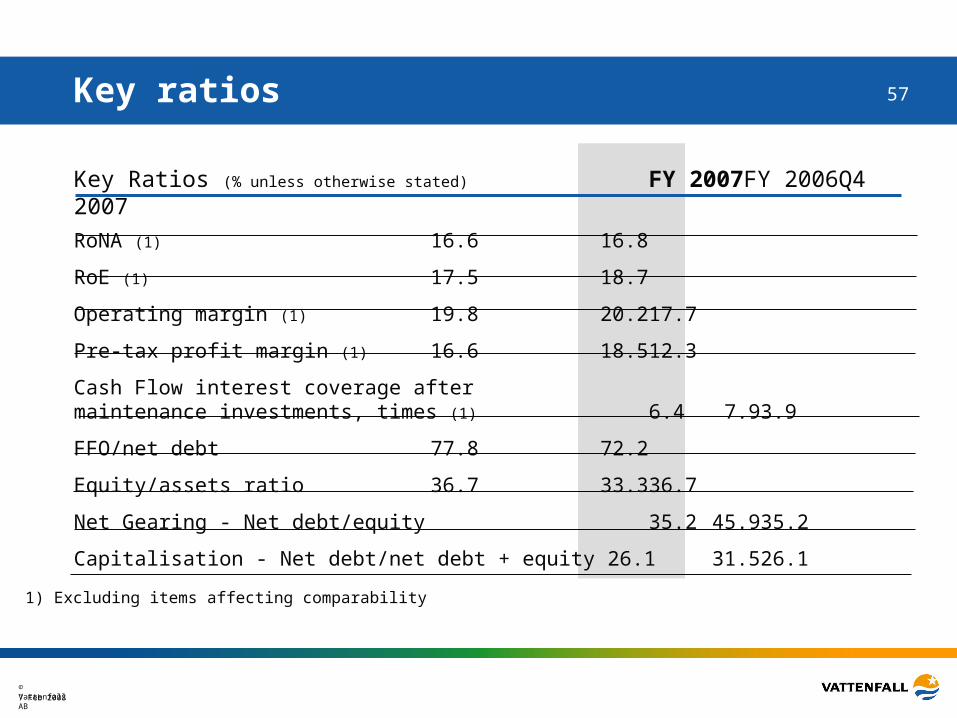

57Key ratios

Key Ratios (% unless otherwise stated) FY 2007 FY 2006 Q4 2007

RoNA (1) 16.6 16.8

RoE (1) 17.5 18.7

Operating margin (1) 19.8 20.2 17.7

Pre-tax profit margin (1) 16.6 18.5 12.3

Cash Flow interest coverage aftermaintenance investments, times (1) 6.4 7.9 3.9

FFO/net debt 77.8 72.2

Equity/assets ratio 36.7 33.3 36.7

Net Gearing - Net debt/equity 35.2 45.9 35.2

Capitalisation - Net debt/net debt + equity 26.1 31.5 26.1

1) Excluding items affecting comparability