Embed Size (px)

Citation preview

VALUE-ADDED TAX

INFORMATION LEAFLET NO. 2/06

Concert and Theatre Tickets,Admission to live events,Concert Promoters,Non-Established Performers.& General Live Entertainment

January, 2006 www.revenue.ie

Revenue Legislation Services

This information leaflet which sets out the current practice at the date of its issue is intended for guidance only and does not purport to be a definitive legal interpretation of the provision of the Value Added Tax Act 1972 (as amended).

Contents

1. Definitions

2. Legislation – Relevant sections of the VAT Act

3. Summary

3.1 Background

3.2 Ticket prices, promoter’s fees and ticket agent’s commissions

3.3 Performers fees

3.4 Security, catering and similar services

3.5 Traders selling goods or services within a venue

4. Events which come within the scope of the exemption from VAT

5. Events which are liable to VAT at 13.5%

6. Events which are liable to VAT at 21%

7. Traders operating within a venue

8. VAT rates for ticket sales and other supplies associated with an event

9. Treatment of non-established performers and traders

9.1 Relevant sections of the VAT Act

9.2 What VAT obligations have non-established traders?

9.3 Non-established traders – what liability has the provider of premises?

9.4 Non-established performers – who accounts for Vat on performances?

9.5 What VAT obligations have non-established promoters?

9.6 Non-established promoters – what liability has the provider of the premises?

10. The withdrawal of the ‘50% (50/50) rule’ for non-established performers

11. Treatment of performers who promote their own performances

12. Sales of tickets by ticket agents and distributors

13. The VAT treatment of advance ticket sales

14. Royalties, licence fees etc. paid by promoters or performers

15. Date from which this leaflet takes effect

16. Enquiries

Appendix I New concession regarding the supply of certain kinds of food

and drink

Appendix II The ‘Theatres’ concession’ – food or drink served in a separate

room

Value Added Tax

Information Leaflet No. 2/06

Live theatrical and musical events

1 Definitions

In this Information Leaflet, certain terms have specific meanings assigned to them, as

follows:

“Admission”: The allowing of an audience into an event. Admission includes the

selling of tickets and the taking of money at the entrance, so that the person who sells a

ticket for an event is deemed to be providing admission, and is treated for VAT

accordingly.

“Food and drink”: This includes all types of food, hot or cold, and all drinks,

including water, and soft drinks. By concession, Revenue is prepared to extend the

exemption from VAT to include events where certain types of food and drink are

available (see Appendix 1).

“Live theatrical or musical event (event)”: A play, musical, concert, recital,

dramatic presentation, dance presentation, cabaret, comedy act or similar event

performed before a live audience.

“Performance”: The time when the performers are actually on stage or otherwise

providing the entertainment for the audience.

“Performer(s)”: The actors, musicians, dancers and comedians etc. who entertain the

audience. Also includes a group, such as a theatre company, which has the actual

performers as employees.

“Premises-provider”: A person who owns, occupies or controls the venue (including

land in the case of an open-air outdoor event) in which an event is to take place.

“Promotion”: The financing or organizing of an event, including publicizing and

other ventures to increase sales or public awareness.

“Self-promoting performer”: A performer who finances, organizes and publicizes

the performance and/or event.

“Ticket agent/ticket seller”: A person engaged by the promoter to distribute and sell

tickets for an event, normally reimbursed by way of a charge to the customer included

in the ticket price and/or by commission charged to the promoter.

2 Legislation - relevant sections of the VAT Act

The law provides for an exemption from VAT for the following:

“ promotion of and admissions to live theatrical or musical performances,

including circuses, but not including

(a) dances, or

(b) performances in conjunction with which facilities are available for the

consumption of food or drink during all or part of the performance by

persons attending the performance”. [Paragraph (viii) of the First Schedule to the VAT Act 1972 (as amended)]

The law further provides that the following are liable to VAT at 13.5 per cent:

“ promotion of and admissions to live theatrical or musical performances,

excluding

(a) dances, and

(b) performances specified in paragraph (viii) of the First Schedule;”[Paragraph (vi) of the Sixth Schedule to the VAT Act 1972 (as amended)].

The promotion of and admissions to dances are liable at the standard rate of 21 per

cent. Where a dance is held on licensed premises, the law also specifies who is

responsible for accounting for VAT:

“The licensee of any premises (being premises in respect of which a licence for

the sale of intoxicating liquor either on or off those premises was granted)

shall be deemed to be the promoter of any dance held, during the subsistence of

that licence, on those premises and shall be deemed to have received the total

money, excluding tax, paid by those admitted to the dance together with any

other consideration received or receivable in connection with the dance” [Section 8 (3C)(a) of the VAT Act 1972 (as amended)]

3 Summary

3.1 Background

The exemption from VAT for live theatrical and musical events was introduced in

1985. In the intervening two decades a certain amount of confusion has arisen

concerning the type of events to which it applies. Following a number of requests for

clarification it was decided to issue this leaflet to restate the law and provide guidance

regarding its application.

This Information Leaflet sets out the VAT treatment of the different services involved

in the staging of live theatrical and musical events. These services include promoting

the event, distributing and selling tickets, providing security and catering, the sale of

concessions within the venue, the sale of goods within the venue, the performing of the

artists, and the granting of admission. Each of these subjects is dealt with in detail in

the main body of the leaflet and a brief synopsis of their treatment for VAT is set out

below.

3.2 Ticket prices, promoter’s fees and ticket agent’s commission

The law provides that promoter’s fees and admission charges for a live event are liable

to 13.5 per cent VAT if food or drink is available at the event (See Paragraph 5). If no

food or drink is available, then promoter’s fees and admission charges are exempt from

VAT (See Paragraph 4). Non-resident promoters are obliged to register for and charge

VAT in Ireland (See Paragraph 9). Commission fees, credit card handling charges and

any other charges made by ticket selling agents form part of the price of the ticket, and

are liable to VAT at the same rate (See Paragraph 12).

In conjunction with the law, a concession currently operates (See Appendix II – The

Theatres’ Concession) in respect of venues where food or drink is provided, and must

be consumed, in a part of the venue completely separate from the performance. In

addition, as a result of the consultation process undertaken for this leaflet, a new

concessionary treatment is being offered by Revenue in respect of the supply of certain

types of food and drink at events (See Appendix I for full details). In effect, the supply

of crisps, sweets, soft drinks and water will not make an otherwise exempt event liable

to VAT. Only the supply of substantial snacks, hot food or alcoholic drink will be

considered when deciding if an event is exempt or liable to VAT.

3.3 Performer’s fees

Any fee charged by a performer is liable to VAT at 21 per cent. A performer who is

registered for VAT will issue a VAT invoice for the amount of his/her fee and charge

VAT at 21 per cent on the full amount of that fee. A non-resident performer will

normally not be required to register for VAT in Ireland. In the case of performances

by non-resident performers, the person who hired the performer, normally the

promoter, will account for the VAT (See Paragraph 9). If the actual performers are

employees of a production company, then the amount received by that company is

regarded as the performance fee, rather than the salary paid to the performers. Where a

performer promotes his/her own performance, then the fee paid may be split as

between the promotion activities and the performance (See Paragraph 10).

3.4 Security, catering and similar services

These services are all liable to VAT at the appropriate rates (See Paragraph 7). If a

company supplying these services is not established in Ireland it must register and

account for VAT.

3.5 Traders selling goods or services within a venue

Goods and services sold in the course of an event are liable to VAT in the usual way.

Non-resident traders are obliged to register for VAT prior to trading. Concessions

that permit traders to sell goods or services within a venue are liable to VAT at 21 per

cent on the full amount received in respect of the granting of the concession (See

Paragraph 8).

4 Events which come within the scope of the exemption from VAT

The exemption from VAT covers promotion charges and admission fees for all live

events in venues where there are no facilities available for consumption of substantial

snacks, hot food or alcoholic drink (see Appendix 1) during all or part of the

performance by persons attending. Promotion of and admission to any indoor live

theatrical or musical event will be exempt where:

No substantial snacks, hot food or alcoholic drink are supplied to persons

attending the event during any part of the performance.

No substantial snacks, hot food or alcoholic drink are available for purchase

during any part of the event in the room in which the performance is taking place.

No substantial snacks, hot food or alcoholic drink are available for purchase at

any part of the venue which can subsequently be taken by persons attending the

event or on their behalf into the room in which the performance is taking place.

Indoor events to which the exemption applies generally include plays, concerts and

similar events in theatres and concert halls, and any other halls or similar

establishments where substantial snacks, hot food or alcoholic drink are not permitted

to be consumed during all or part of the performance.

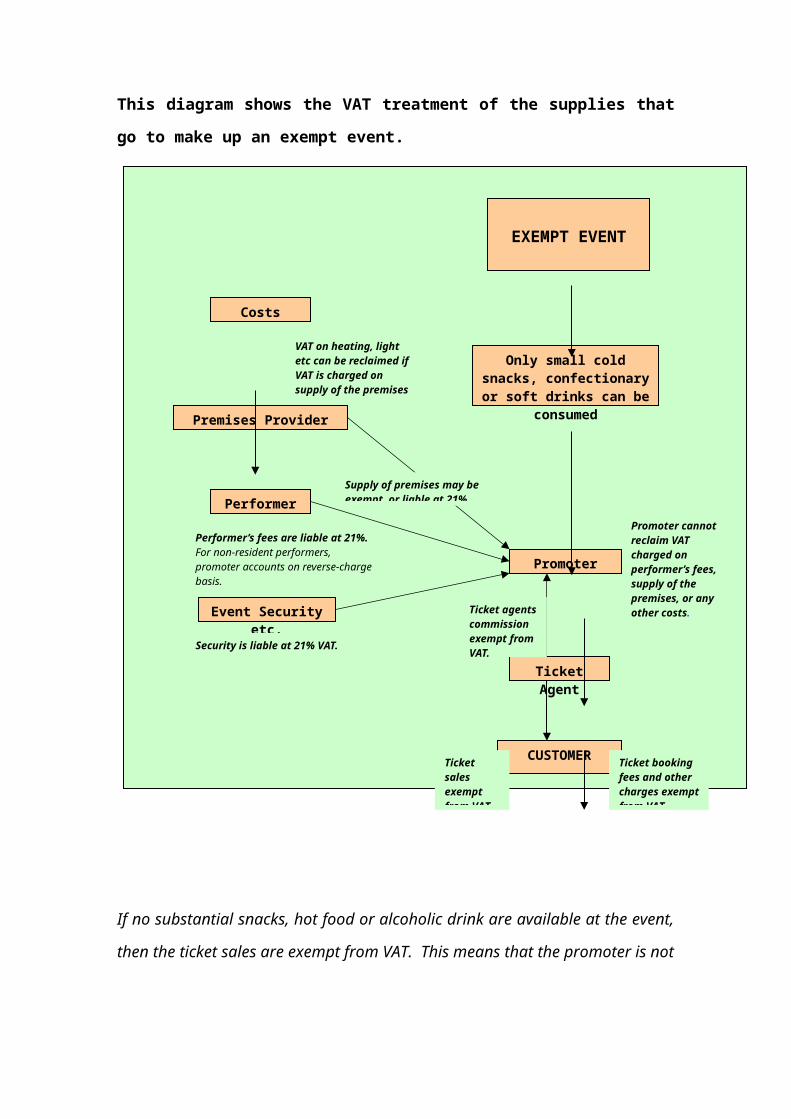

This diagram shows the VAT treatment of the supplies that go to make up an

exempt event.

If no substantial snacks, hot food or alcoholic drink are available at the event, then the

ticket sales are exempt from VAT. This means that the promoter is not able to recover

VAT charged by performers, security etc. in connection with the event.

EXEMPT EVENT

Only small cold snacks, confectionary or soft drinks

can be consumed

CUSTOMER

Costs

Premises Provider

Event Security etc.

Ticket Agent

Performer

VAT on heating, light etc can be reclaimed if VAT is charged on supply of the premises

Promoter cannot reclaim VAT charged on performer’s fees, supply of the premises, or any other costs.

Performer’s fees are liable at 21%. For non-resident performers, promoter accounts on reverse-charge basis. Promoter

Security is liable at 21% VAT.

Ticket agents commission exempt from VAT.

Ticket booking fees and other charges exempt from VAT.

Supply of premises may be exempt, or liable at 21% VAT

Ticket sales exempt from VAT.

5 Events which are liable to VAT at 13.5%?

The exemption does not cover promotion of or admission to events where facilities are

available for the consumption of substantial snacks, hot food or alcoholic drink during

all or part of the performance by persons attending the performance. This exclusion

from exemption also applies where a separate charge is made for the food and drink.

The 13.5% rate of VAT applies to events where there are facilities for the

consumption * of substantial snacks, hot food or alcoholic drink during the

performance by persons attending the performance. VAT at this rate must be

accounted for on money received for tickets, and any fee charged by the promoter in

relation to these events. However, this VAT may be offset by the right of the promoter

and the ticket agent to recover any VAT charged to them in connection with the

staging of the event, such as VAT on the performer’s fee, security, hire of equipment

etc.

* The expression ‘facilities for the consumption of food or drink’ does not imply a

formal sit-down venue. If people attending an event can obtain food or drink and

consume it, then it must be accepted that facilities are available to do so.

Accordingly, VAT is chargeable at 13.5% on promotion and admission charges in

respect of any live theatrical or musical event under Paragraph (vi) of the Sixth

Schedule to the VAT Act 1972 (as amended) where:

Substantial snacks, hot food or alcoholic drink are provided to persons attending

the event in the room/venue in which the performance takes place as part of the

admission fee.

Substantial snacks, hot food or alcoholic drink are available for purchase by

persons attending the event in the room/venue in which the performance is taking

place.

Substantial snacks, hot food or alcoholic drink are available for purchase at any

part of the venue which can subsequently be taken by persons attending the event

or on their behalf into the room/venue where the performance is taking place.

Events to which the reduced (13.5%) rate applies generally include:

Cabaret and other performances where the consumption of substantial snacks, hot

food or alcoholic drink are associated with the performance.

Musical or comedy performances in theatres, public houses and other venues

where substantial snacks, hot food or alcoholic drink are served during the course

of the performance.

Performances in hotels, restaurants or other establishments where substantial

snacks, hot food or alcoholic drink are supplied in conjunction with the

performance.

Outdoor concerts where substantial snacks, hot food or alcoholic drink are

available within the confines of the venue.

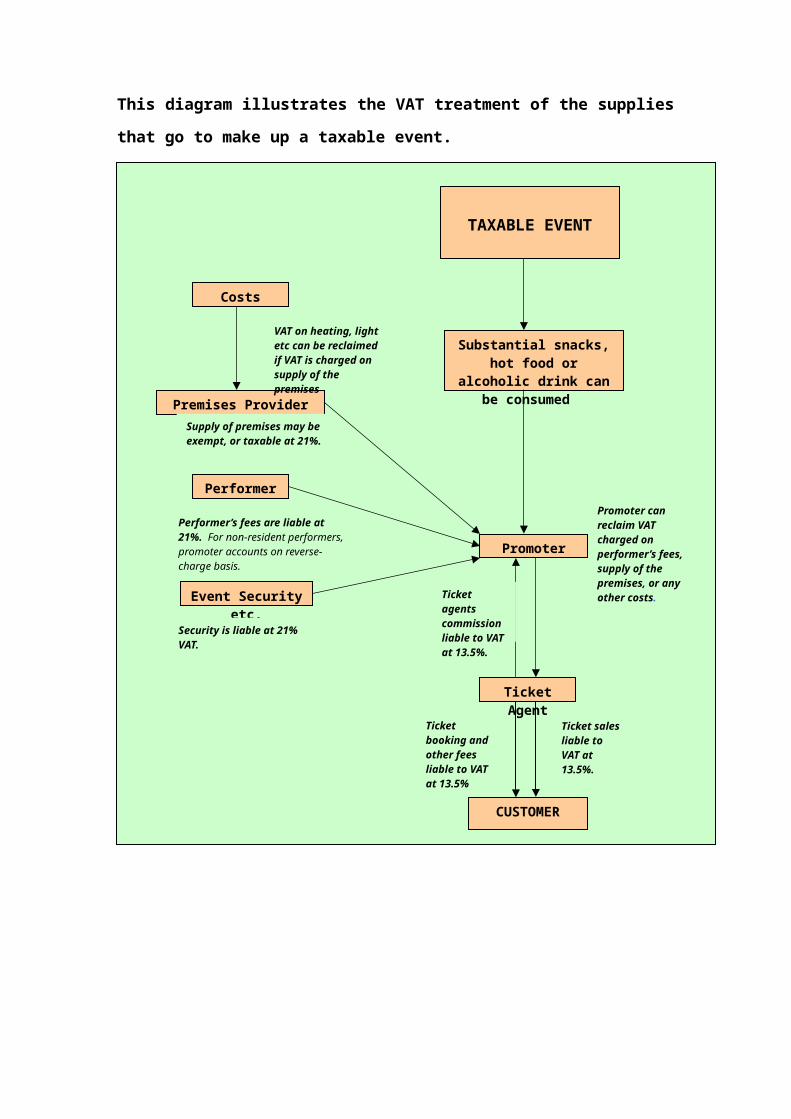

This diagram illustrates the VAT treatment of the supplies that go to make up a

taxable event.

If substantial snacks, hot food or alcoholic drink are available at the event, then the

ticket sales are liable to VAT at 13.5%. This allows the promoter to recover VAT

charged by performers, security etc. in connection with the event. Since much of the

VAT charged to the promoter is at the 21% rate, the promoter may actually be in a net

VAT repayment position - i.e. the VAT charged to the promoter in respect of costs may

exceed the VAT due on ticket sales.

TAXABLE EVENT

Substantial snacks, hot food or alcoholic drink can be

consumed

CUSTOMER

Costs

Premises Provider

Event Security etc.

Ticket Agent

Performer

VAT on heating, light etc can be reclaimed if VAT is charged on supply of the premises

Promoter can reclaim VAT charged on performer’s fees, supply of the premises, or any other costs.

Performer’s fees are liable at 21%. For non-resident performers, promoter accounts on reverse-charge basis. Promoter

Security is liable at 21% VAT.

Ticket agents commission liable to VAT at 13.5%.

Ticket sales liable to VAT at 13.5%.

Supply of premises may be exempt, or taxable at 21%.

Ticket booking and other fees liable to VAT at 13.5%

6 Events which are liable to VAT at 21%?

Neither the exemption nor the reduced rate applies to the promotion of or admission to

venues where the entertainment, if any, is not a live theatrical or musical performance.

The standard rate of VAT applies to charges made in respect of the promotion of or

admission to these venues.

Venues and events to which the standard (21%) rate applies generally include:

o Dances,

o Discotheques,

o Night-clubs and similar clubs,

o Public houses and any other such premises where there is no live musical or

theatrical performance.

N.B. The 21% rate of VAT applies to dances, whether or not there is a live band. In

these cases, it will be clear that people are attending the dance, rather than the

performance by the band.

7 Traders operating within a venue

Where a concession, licence or right is granted to any person to sell food, drink or any

merchandise, or to supply any services, in a venue, any consideration paid in respect of

such a concession, licence or right is liable to VAT at the standard (21%) rate. Any

traders operating such a concession, licence or right must register and account for VAT

in the usual way in respect of sales made by them. However, the sale of programmes

containing only details of the performance is regarded as ancillary to the performance,

and liable to VAT at the same rate as the admission fee.

All traders are also responsible for ensuring that they possess all relevant permits and

licences required by law or regulations. In particular, any trader selling alcoholic

drinks at an event must possess a licence in his/her own name issued under the

Intoxicating Liquor Licensing Acts which allows the sale of alcoholic drinks at the

venue and for that event. It is illegal for a trader at an event to sell intoxicating liquor

under a licence granted to any other person, including the promoter of the event.

8 VAT rates for ticket sales and other supplies associated with an

event

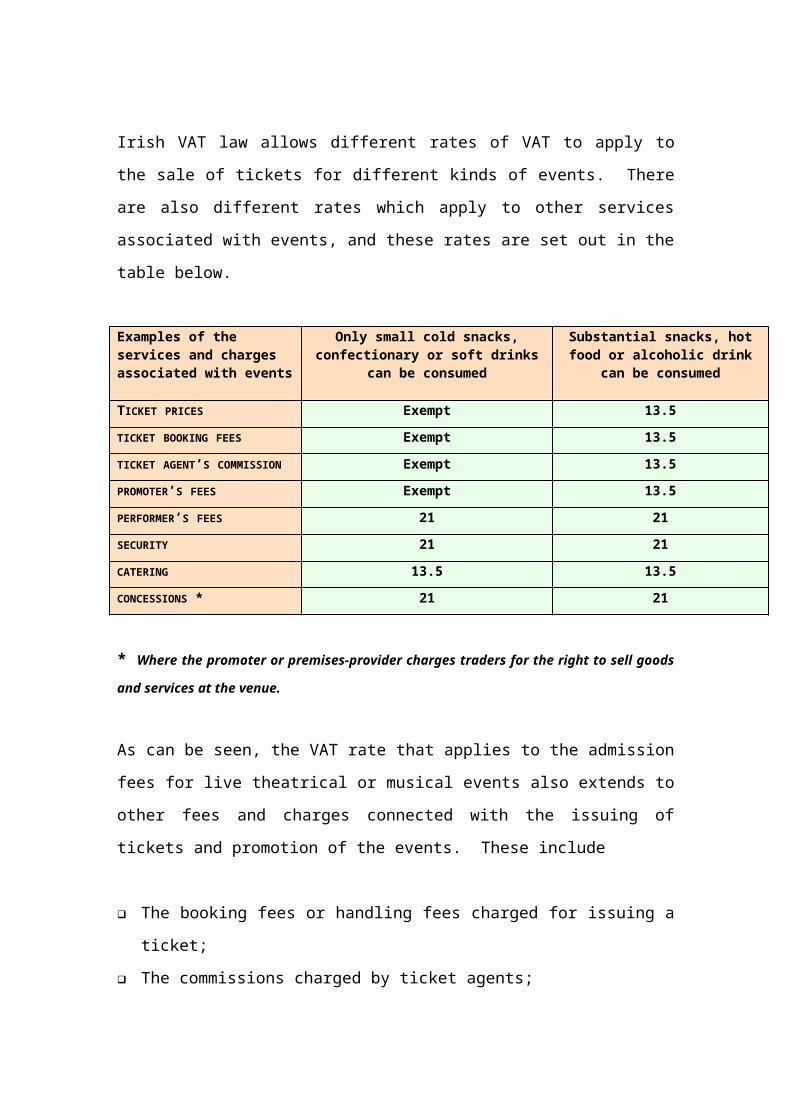

Irish VAT law allows different rates of VAT to apply to the sale of tickets for different

kinds of events. There are also different rates which apply to other services associated

with events, and these rates are set out in the table below.

Examples of the services and charges associated with events

Only small cold snacks, confectionary or soft drinks can be consumed

Substantial snacks, hot food or alcoholic drink can be consumed

TICKET PRICES Exempt 13.5

TICKET BOOKING FEES Exempt 13.5

TICKET AGENT’S COMMISSION Exempt 13.5

PROMOTER’S FEES Exempt 13.5

PERFORMER’S FEES 21 21

SECURITY 21 21

CATERING 13.5 13.5

CONCESSIONS * 21 21

* Where the promoter or premises-provider charges traders for the right to sell goods and services at

the venue.

As can be seen, the VAT rate that applies to the admission fees for live theatrical or

musical events also extends to other fees and charges connected with the issuing of

tickets and promotion of the events. These include

The booking fees or handling fees charged for issuing a ticket;

The commissions charged by ticket agents;

The fees charged by promoters to performers who have hired them to organise

events;

The fees charged by promoters to venue owners for sourcing performers;

9 Treatment of non-established performers and traders

A separate information leaflet deals with the VAT treatment of cultural, artistic and

entertainment services supplied by non-established persons. The provisions contained

in that leaflet which refer to the supply of services by non-established performers are

included below.

9.1 Relevant sections of the VAT Act

The law provides that

“where a person not established in the State supplies a cultural, artistic, entertainment

or similar service in the State, then any person, other than a person acting in a private

capacity, who receives that service shall

(i) in relation to it, be a taxable person or be deemed to be a taxable person,

and

(ii) be liable to pay the tax chargeable as if that taxable person had in fact

supplied the service for consideration in the course or furtherance of

business;

but where that service is commissioned or procured by a promoter, agent or other

person not being a person acting in a private capacity, then that promoter, agent or

person shall be deemed to be the person who receives the service;”[Section 8(2)(aa) of the VAT Act 1972 (as amended)]

In addition Section 8(2)(d) of the VAT Act 1972 (as amended) provides that a

‘premises provider’ (being a person who owns, occupies or controls land) who allows

non-established traders or promoters to operate on the land, has certain obligations

with regard to the VAT liability of these non-established traders or promoters.

In the case of non-established traders supplying goods for a period of less than 7

consecutive days on the land, the premises provider must, not later than 14 days before

the day on which the non-established trader is allowed to trade on the land, notify the

local Revenue District of the name and address of the trader, the dates on which the

trader intends to supply goods, and the address of the land.

In the case of non-established promoters supplying a cultural, artistic, entertainment, or

similar service, the premises provider must, not later than 14 days before the day on

which the service is scheduled to begin, notify the local Revenue District of the name

and address of the promoter, and the dates, duration and venue of the event or

performance.

Where a premises provider fails to provide true and correct information as required,

then he/she may be made jointly and severally liable with the non-established trader or

promoter for the VAT due in respect of the supplies made by them.

9.2 What VAT obligations have non-established traders?

Where non-established performers or any other non-established traders make sales of

merchandise such as CDs, posters, t-shirts etc at a venue in the State, they are obliged

to register and account for VAT on all such sales and all other supplies made by them.

9.3 Non-established traders – What liability has the provider of the premises?

Where a person who owns, occupies or controls premises (whether the owner or a third

party) allows a non-established trader to supply goods for a period of less than seven

consecutive days on the premises in which a performance is to be held, the provider of

the premises must give the following information to Revenue:

The name and address of the non-established trader.

The dates on which the non-established trader intends to trade on the premises

The address of the premises

The provider of the premises must give this information to the District Officer of the

appropriate local Revenue District not later than 14 days before the performance is

scheduled to begin.

Where this information is not given to Revenue as set out above, the provider of the

premises may be made jointly and severally liable with the non-established trader for

the VAT liability in respect of the supplies of goods in the premises concerned. In

practice, this means that if the non-established trader fails to register and account for

any VAT due in respect of sales made in the State, the provider of the premises,

whether the owner or a third party or both jointly, will become liable for the entire

amount of VAT due.

9.4 Non-established performers – who accounts for VAT on performances?

A non-established performer is an individual who is not normally resident in the State

or who does not have a business establishment here. It also may be a performance

company which does not have a business establishment here. Section 8(2)(aa) of the

VAT Act as set out in paragraph 9.1 above provides that a non-established performer

is not obliged to register and account for VAT in respect of live theatrical or musical

performances in the State. Instead, the promoter, agent or other person (including non-

established promoters etc – see Paragraph 9.5) who commissions the performance or

event is automatically obliged to account for the VAT due. This applies even where

the turnover from the performance does not exceed registration thresholds.

9.5 What VAT obligations have non-established promoters?

Non-established promoters supplying services in Ireland must register and account for

VAT on taxable supplies made by them, and also in respect of any payments made by

them to non-established performers*. In practice this means that registration is

required in all circumstances, except only where the non-established promoter is

promoting only a performance by a performer registered for VAT in Ireland, and this

performance features in an event which comes under the exemption from VAT. *This

applies even where the payments are the subject of a separate contract covering a

number of performances in different countries, or where the performer issues an

invoice from an establishment outside the State in respect of the performance. If the

place of supply of the performance is Ireland, then the VAT liability for payments to

the performer arises in Ireland.

9.6 Non-established promoters – what liability has the provider of premises?

Where a non-established promoter arranges for the supply of live musical or theatrical

entertainment, the person who owns, occupies or controls the premises in which the

performance is to take place has certain obligations to Revenue.

The provider of the premises must give the following information to Revenue:

The name and address of the non-established promoter.

Details such as the dates, duration and venue of the performance.

The provider of the premises must give this information to the District Officer of the

appropriate local Revenue District not later than 14 days before the performance is

scheduled to begin.

Where this information is not given to Revenue as set out above, the provider of the

premises may be made jointly and severally liable with the non-established promoter

for the VAT liability in respect of the performance. In practice, this means that if the

non-established promoter fails to register and account for any VAT due, the provider

of the premises, whether the owner or a third party or both jointly, will become liable

for the entire amount of VAT due.

10 The withdrawal of the ‘50% (50/50) rule’ for non-established

performers

The ‘50% rule’ was an administrative procedure whereby Revenue, on a concessional

basis, allowed promoters/performers/venue owners (as appropriate) to account for

VAT on performances by non-established performers as follows:

“50% of the gross income @ 21% was treated as being the amount of tax payable by

the performer on his/her performance at the event. There were no input credits

available against this amount. There were no further reductions available.”

This was intended to simplify the application of VAT for non-established performers.

However, the law was changed to remove the requirement for non-established

performers to register and account for VAT, with effect from March 2002 (see

Paragraph 9.4 above). This change removed the necessity for the ‘50% rule’.

However this ‘rule’ continued to be applied in certain circumstances.

In order to ensure a consistent approach to the taxation of performances by non-

established performers, the provisions of the legislation referred to in Paragraph 9.4

above must now apply in all circumstances. The ‘50% rule’ therefore can no longer

apply to such performances, and this concession is now withdrawn (but see Paragraph

15 for effective date).

11 Treatment of performers who promote their own performances

Where a performer promotes, either by him/herself or with others, an event in which

he/she is performing, any payment received must be apportioned as between the

performance and the promotion. Any such apportionment will depend on the

individual circumstances, and the performer must demonstrate to the satisfaction of

Revenue that the apportionment is a correct one. Where the actual performers are

employees of the promoter or another company, the promoter or other company is

liable for VAT on the performance.

If a performer can show evidence of real work carried out in the promotion of the

event, Revenue is prepared to accept that a portion of the payment received by a self-

promoting performer may be treated as being in respect of the promotion, up to a

maximum of 40 per cent of the total, which is either exempt or liable to VAT

according to the nature of the event. The remainder, at least 60 per cent, is treated as

being in respect of the performance, and liable to VAT at the standard (21%) rate.

12 Sales of tickets by ticket agents and distributors

A promoter of an event may use a ticket agent to sell tickets for events. Promoters and

ticket agents may also use a network of distributors, such as local music stores, to

ensure a broad distribution of tickets. The actual sale of a ticket by a promoter, a ticket

agent or distributor is the supply to the customer of the right to admission to an event.

Accordingly, for an event that does not come within the scope of the exemption, the

agent or distributor who sells a ticket is liable to account for VAT on the full sale price

(the face value of the ticket and all booking charges and fees whatsoever, including

any commission charged to the promoter) at the rate appropriate to the event.

The agent or distributor should issue a VAT invoice for the commission on the sale.

The person to whom the agent or distributor forwards the balance of the ticket price

(e.g. another agent or the promoter) must issue a VAT invoice on receipt of the money,

and account for VAT on the amount received.

The diagram below illustrates the VAT treatment of the sale of tickets for a

taxable event by ticket agents and distributors.

Promoter

Customer

Ticket Agent

Distributor

Distributor sells ticket to customer, granting right of admission to an event

Distributor accounts for VAT on full amount paid by customer at the time of payment

Ticket agent issues VAT invoice to distributor on receipt of ticket money

Distributor issues VAT invoice for commission on ticket sale

Promoter issues VAT invoice to ticket agent on receipt of ticket money

Ticket agent issues VAT invoice for commission on ticket sale

Payment for ticket Ticket to customer

Where a ticket agent or promoter sells a ticket directly to a customer, the agent or promoter accounts for VAT on the full amount paid by customer at the time of payment

13 The treatment of advance ticket sales

Payments received in advance of the supply of goods or services are always liable to

VAT at the time the payment is made. This also applies to sales of tickets for live

theatrical and musical events, where these are sold prior to the date on which the event

takes place (but see Paragraph 15 for effective date).

Ticket sales in advance are liable to VAT by reference to the date on which the ticket

is sold and VAT must be accounted for in the taxable period in which the sale is made,

and not when the event takes place. The rate of VAT that applies is always the rate

current at the time of sale of the ticket.

If an event is cancelled, and the promoter, ticket-agent or distributor refunds the full

amount of the ticket, including VAT, to the purchaser, a claim may be made in the

next VAT return for a repayment of any VAT previously submitted.

It should be noted that advance payments by promoters to performers are also liable to

VAT at the time of payment.

14 Royalties, licence fees etc. paid by promoters or performers

Certain performances consist of or contain material which is subject to copyright or

similar intellectual property protection. Any fee charged by a person registered for

VAT in Ireland in respect of the right to use this material is liable to VAT at 21 per

cent.

Where the person who holds the copyright etc. is not established in the State, then

payments made come within the scope of the Fourth Schedule to the VAT Act 1972

(as amended). This means that the promoter or performer who pays the fee must also

account for the VAT on the fee as though he/she had supplied the right to use the

material. If the event comes within the scope of the exemption, then this VAT may not

be recovered.

15 Date from which this leaflet takes effect

This Information Leaflet is issued in order to clarify the application of VAT to live

theatrical and musical events. In some cases, the treatment of certain issues as set out

in the leaflet may entail changes from current practice. In recognition of difficulties

that traders might encounter with a sudden implementation of these changes, Revenue

is prepared to defer implementation of these to a later date.

Accordingly, the 50% or 50/50 rule (see Paragraph 10) may continue to operate until 1

January 2007. The VAT due on any events taking place on or after 1 January 2007

must be accounted for as set out in Paragraph 9 above.

Tickets sold in advance (see Paragraph 13) for events taking place before 1 January

2007 may continue to be treated in accordance with current practices. However, VAT

must be accounted for on tickets sold in advance for events taking place on or after 1

January 2007 by reference to the date on which the ticket is sold.

Otherwise, the provisions contained in the leaflet should be regarded as effective from

the date of the appropriate governing legislation.

16 Enquiries

For further information on any VAT matter, whether a general enquiry or an enquiry

relating to a specific transaction, you should contact your local Revenue District.

Details for all Revenue Districts can be found by clicking here.

VAT Interpretation Branch,

Indirect Taxes Division,

Dublin Castle.

Appendix I: New concession regarding the supply of certain kinds of

food and drink

Previously, where food and/or drink were available at any event, the promotion and

admission fees were in all cases liable to VAT. However, in recognition of certain

practical difficulties, and to ensure consistency of treatment, Revenue is prepared to

concessionally disregard the supply of certain items of food and drink when

considering the VAT treatment of events.

Revenue will allow the exemption to continue to apply to events where certain cold

snack foods, confectionary and soft drinks can be consumed during the performance.

This means that promotion charges and the sales of tickets for these events will not

now be subject to VAT, whereas previously the availability of any food and drink

would have denoted a VAT liability. The items of food and drink to which this

concession refers are as follows:

Food DrinkConfectionary:

Savoury snacks:

Fruit

Packets of sweets Bars (e.g.

chocolate) Chewing gum Lollipops etc.

Crisps and similar snacks

Peanuts Popcorn (incl.

heated)

Soft drinks:

Water:

Hot drinks:

Carbonated (fizzy) drinks

Fruit juices Milk ‘Smoothies’ and

other milk or yoghurt based drinks

‘Slushies’ and similar ice drinks.

Still bottled water Sparkling bottled

water

Tea Coffee Hot chocolate

Sales of any other kind of food and drink including sandwiches, wraps, hot snacks,

meals and alcoholic drink are not included in this concession. The sale of such items

would have the effect of bringing the event within the scope of VAT.

Appendix II: The ‘Theatres’ Concession’ - food or drink supplied in a

separate room

Many theatres allow the supply of food and drink during an interval or intermission in

a performance. Revenue concessionally allowed the exemption from VAT to continue

to apply to these events on the following conditions:

The food and drink was only available in a room separate from the auditorium in

which the performance was taking place,

The performance was not visible from the room where the food or drink is

available,

Patrons were not permitted to take the food or drink into the auditorium where the

performance was taking place before, during or after the interval.

While this concession was originally only granted in respect of theatres, Revenue has

extended it to include other types of performances in other venues. Accordingly, in the

case of any event, where substantial snacks, hot food or alcoholic drink (See Appendix

I above) are available to the audience at any stage during the performance, then the

event remains within the exemption if it is the stated and enforced policy of the

management that the following conditions are adhered to:

Substantial snacks, hot food or alcoholic drink are only available in a separate part

of the venue from that in which the performance takes place,

The performance is not visible from the area where the substantial snacks, hot food

or alcoholic drink are available,

Patrons are not permitted to take substantial snacks, hot food or alcoholic drink

into the part of the venue where the performance takes place at any time during the

performance.

The availability of substantial snacks, hot food or alcoholic drink under any other

circumstances would have the effect of bringing the event within the scope of VAT.