Embed Size (px)

Citation preview

VAT in the GCCLatest Developments and Business Impact

Latest Developments

2

01

PwC

VAT recent developments

3

A common VAT frameworkThe GCC Member states are in the process of agreeing a common framework for the introduction of a VAT system in the GCC. A formal announcement of the Treaty is expected shortly afterwards. Upon ratification of the GCC Treaty, each Member State is expected to issue its own national VAT legislation based on the agreed common principles.

Go live The introduction of VAT across the GCC is expected to take effect from 1 January 2018.

VAT regulationsThese regulations will provide guidance to tax payers in each GCC Member State on the interpretation of the VAT legislation in that Member State. We anticipate that the regulations will be issued shortly after the VAT legislation is issued.

VAT legislationEach Member State will issue its own VAT legislation in accordance with the common principles outlined in the GCC Treaty. It is expected that some countries will issue VAT legislation shortly after announcement of the treaty by the GCC.

PwC

VAT in the GCC

Our understanding of the

GCC VAT system

4PwC

VAT in the GCC

• Expected transition period between 12 to 15 months

• Envisaged system is a standard fully-fledged VAT system applying on most supplies of goods and services with possible exemptions/exceptions

Standard rate 5%

VAT at Import

Minimum annual turnover

VAT on goods & services

Possible VAT exemptions

Exports subject to 0%

Deduction of input VAT

Periodical filing and reporting

Designing the VAT law to deliver a

‘win-win’ taxation model

• An ideal tax system should help governments raise essential revenue, and should do so without discouraging economic activity and without deviating too much from tax systems in other countries

5

Criterion Key results for both the business community and the tax authorities

Simplicity Easy to implement and to apply

Efficiency Low compliance costs

High collections and self-policing

Certainty Limited need for litigation

High voluntary compliance

Broad-based Limited special systems and exceptions

Proportionality Taxable amount not to exceed consideration actually paid

Competitiveness Appropriate exemptions

Non-distortionary Neutrality in competition between the States and Industries

PwC

VAT in the GCC

VAT/GST design benchmark

• The design of the VAT/GST system has a direct impact on cost of compliance and cost of collection

6

Low

Single VAT rate

Few exemptions

Simple and clear regulation

E-filing

Proportional penalties

High

Multiple VAT rates

Multiple exemptions

Complex and inefficient obligations

Lack of facilitating instruments

Burdensome fines

SingaporeAustraliaChileNorwayBrazil

Low

Mexico

New ZealandEU

High

PwC

VAT in the GCC

VAT Key Features

7

02

PwC

What is VAT?

8PwC

• Value Added Tax (“VAT”) is a tax on consumption

• Transaction based tax – VAT is levied at each stage in the chain of production/distribution

• VAT charged on supplies/VAT deducted on purchases

• Collected by businesses on behalf of the VAT Administration

• Self-assessment system - Businesses submit a periodic VAT return to the Tax Authority in which they calculate the Net VAT amount and either pay or get a refund for this amount

VAT in the GCC

How VAT works

10PwC

VAT in the GCC

Business charges VAT on sales(output VAT)

Business pays VAT on purchases (input VAT)

Net VAT (output VAT– input VAT)

Payable to the VATAdministration

Refundable by the VAT Administration

NegativePositive

Equals

Less

Taxable supplies

A taxable supply at the standard rate is a supply on which tax is charged at 5% and

for which the related input tax is deductible

Retail purchases

Car sales and rentals

Hotels and Restaurants

Repairs and maintenance

services

Common Standard rate Supplies

A taxable supply at the zero rate – a zero-rated supply - is a taxable supply on which tax is charged at zero percent and for which the

related input tax is deductible

Common Zero-Rated Supplies

Basic FoodMedicines and

Medical Equipment

ExportsCertain means of Transport

11PwC

VAT in the GCC

Exempt Supplies

An exempt supply is a supply on which tax is not charged and for which the related input tax is not deductible

Healthcare EducationResidential Dwellings

Domestic Passenger Transport

Common Exempt Supplies

12PwC

VAT in the GCC

Reverse Charge (Or self

assessed VAT)

13PwC

VAT in the GCC

ServiceCo

UAE

Company X

Service flow

• Reverse charge rules typically apply to services received from suppliers established outside the country

• The recipient accounts for the VAT due on the supply on his VAT return (instead of the supplier) • The VAT accounted for by the recipient is deductible as input VAT on the same VAT return

VAT Groups

Corporate entity

Legally independent but closely bound to

the other members by financial,

economic and organisational links

Established and registered for VAT

in the relevant countries

Not a member of another VAT group

in the country

General conditions to be met by each member of a VAT group in a country

14PwC

VAT in the GCC

• Under VAT groups, independent legal persons are allowed to be treated as a single taxable person under certain conditions

• A VAT group scheme allows for two or more companies to be considered for VAT purposes as a single taxable person

• Intra group supplies are disregarded for VAT purposes

Example 1 – Fully Taxable

Business

Sales

$100,000,000 Taxable Supplies

Costs

$50,000,000 Local purchases/imports

$20,000,000 Salaries

$10,000,000 Services from abroad

VAT Return

VAT due on sales $ 1,500,000

VAT due on reverse charge $ 500,000

Total due $2,000,000

VAT deductible on purchases $ 2,500,000

VAT deductible reverse charge $ 500,000

Total Deductible $3,000,000

Net amount Refundable ($1,000,000)

• 70% of exports sales subject to 0% VAT

• 30% sales subject to 5% VAT

• Purchases and imports subject to 5% VAT

• Entitlement to claim input VAT = 100% of input VAT

15PwC

VAT in the GCC

Example 2 – Exempt Business

Sales

$100,000,000 Supplies

Costs

$50,000,000 Local purchases/imports

$20,000,000 Salaries

$10,000,000 Services from abroad

VAT Return

VAT due on sales $ 0

VAT due on reverse charge $ 500,000

Total due $ 500,000

VAT deductible on purchases $ 0

VAT deductible reverse charge $ 0

Total Deductible $ 0

Net amount Payable $ 500,000

Non-deductible VAT$3,000,000

• Sales exempt from VAT

• Purchases and imports subject to 5% VAT

• No Entitlement to claim input VAT

16PwC

VAT in the GCC

Example 3 – Mixed Business

Sales

$100,000,000 Supplies

Costs

$50,000,000 Local purchases/imports

$20,000,000 Salaries

$10,000,000 Services from abroad

VAT Return

VAT due on sales $ 2,500,000

VAT due on reverse charge $ 500,000

Total due $3,000,000

VAT deductible on purchases $ 2,000,000

VAT deductible reverse charge $ 400,000

Total Deductible $2,400,000

Net amount Payable $ 600,000

• 50% of sales subject to 5% VAT

• 30% of sales subject to 0% VAT

• 20% of sales exempt from VAT

• Purchases and imports subject to 5% VAT

• Entitlement to claim (taxable supplies / total supplies) = 80% of input VAT

17PwC

VAT in the GCC

Compliance Requirements

17

03

PwC

VAT Records – Normal

requirements

VAT records must be kept for a specific period of time. Records may be kept on paper or electronically. Records must be accurate, complete and readable.

1. Copies of all issued invoices

2. Originals of all received invoices

3. Debit or Credit notes

4. Import and Export records

5. Records of any goods given for free or allocated for private use

6. Records of all zero-rated or VAT exempt supplies and purchases

7. A VAT General Ledger Account

Examples of records that need to be kept

19PwC

VAT in the GCC

VAT Invoices – Normal

requirements

Ref Number Description Quantity Unit Price exclusive of VAT

Unit Priceinclusive of VAT

Total exclusive of VAT Total inclusive of VAT

DateInvoice Serial Number

Name of Taxable PersonVAT Registration NumberAddress and Contact Details

Name of CustomerVAT Registration NumberAddress and Contact Details

Total

Applicable VAT rate

VAT amount

Subtotal

VAT INVOICE

• Only VAT-registered businesses can issue VAT invoices.• Valid invoices should be kept.• VAT invoices are a requirement for deducting input VAT - Invalid

invoice, pro-forma invoice, statement or delivery note are not accepted.

20PwC

VAT in the GCC

VAT Return example

• Self-assessment system • Businesses submit a

regular VAT return to the Tax Authority

• Must report all VAT on sales and purchases made in the period, including intra-GCC transactions

• Calculate the Net VAT amount and either pay or get a refund for this amount

VAT Return For the period 31-Jan-18

VAT on Sales 1 x

VAT due on acquisitions from other Members States 2 x

TOTAL VAT Due (sum of Boxes 1 and 2) 3 x

VAT reclaimed on purchases and other inputs(including acquisitions from the GCC)

4 x

NET VAT to be paid to Tax Authority 5 x

Total value of sales and all other outputs excluding any VAT 6 X

Total value of purchases and all other inputs excluding any VAT 7 x

Total value of supplies of goods and related costs, excluding any VAT, to other GCC Member States

8 x

Total value of acquisitions of goods and related costs, excluding any VAT, from other GCC Member States

9 x

21PwC

VAT in the GCC

Industry Focus

21

04

PwC

Construction

23PwC

VAT in the GCC

Construction services likely to be subject to VAT at 5%

Need to consider time of supply / when VAT is due

Invoicing (progress payments, valuations, etc)

Long term contracts / transitional arrangements

Refunds

Suppliers / sub contractors

Documentation to reclaim VAT on costs (self billing / other arrangements)

Unregistered suppliers

Real Estate

Complex / different types of supplies

- Commercial / Residential

- Land, buildings, or both

- Sales / Leases

Commercial Sales should be taxable at 5%

Residential sales may be exempt

Leases may be exempt (possibly with an option to tax for commercial)

Long term v short term – definitions – different treatment

Time of supply

VAT recovery on costs

Can be complex / apportionment of VAT

24PwC

VAT in the GCC

Education

25PwC

VAT in the GCC

The institution must not systematically aim to make a profit;

Any profits made, may not be distributed, but must be reinvested to improve education or to maintain.

Education most likely to be exempt

This applies to primary education to higher education, even if carried out by an independent contractor

No output VAT, VAT non recoverable

VAT would be a cost on organization

Providing taxable and non taxable supplies: Pro- rata deductibility

Only exempt supply: no VAT return

Food Services

26PwC

VAT in the GCC

Basic food (list): zero-rated

Food: standard VAT rate (5%)

Food services: standard VAT rate (5%)

Invoices (B2B and B2C) / till receipts

Reporting

Records, returns

Manufacturing

• Goods manufactured and sold within the country is subject to 5% VAT

• Imports:

• Goods imported from outside the country into a (fenced) Free Zone are considered to be outside the customs / VAT territory of the relevant country

• Goods stored in (fenced) Free Zone are not subject to customs duties nor VAT

• VAT is charged at a rate of 5% on the value of the sale upon removal from free zone into the country

27PwC

VAT in the GCC

Retail

28PwC

VAT in the GCC

Rates

5%, 0%, exempt / importance of correct coding

Pricing / Retail price inclusive of VAT

Business promotions – Vouchers – Gift cards – Free products –Free supplies

3 for the price of 2 / buy one get one free / mixed rate goods

Loyalty schemes

Delivery charges

Online sales

VAT Implementation Considerations

28

04

PwC

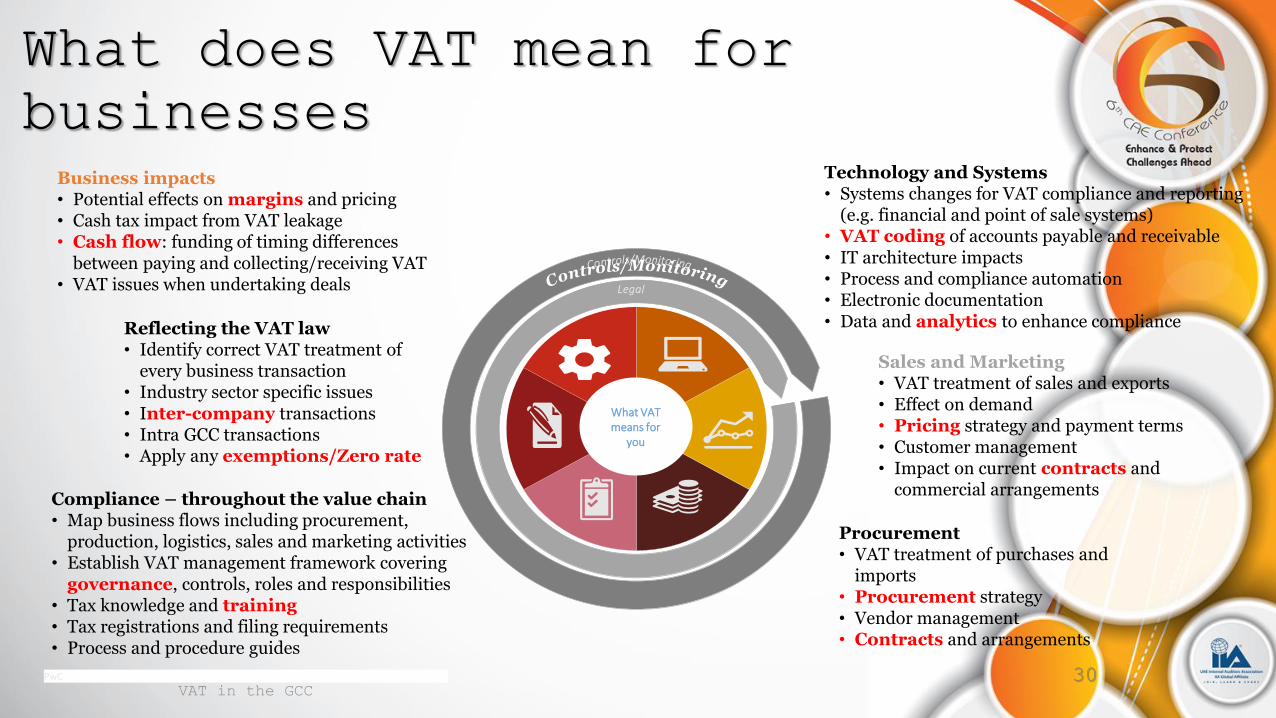

Business impacts• Potential effects on margins and pricing• Cash tax impact from VAT leakage• Cash flow: funding of timing differences

between paying and collecting/receiving VAT• VAT issues when undertaking deals

Technology and Systems• Systems changes for VAT compliance and reporting

(e.g. financial and point of sale systems) • VAT coding of accounts payable and receivable • IT architecture impacts• Process and compliance automation• Electronic documentation• Data and analytics to enhance compliance

Sales and Marketing• VAT treatment of sales and exports • Effect on demand• Pricing strategy and payment terms• Customer management• Impact on current contracts and

commercial arrangements

Procurement • VAT treatment of purchases and

imports • Procurement strategy• Vendor management• Contracts and arrangements

Compliance – throughout the value chain• Map business flows including procurement,

production, logistics, sales and marketing activities • Establish VAT management framework covering

governance, controls, roles and responsibilities• Tax knowledge and training• Tax registrations and filing requirements• Process and procedure guides

Reflecting the VAT law• Identify correct VAT treatment of

every business transaction• Industry sector specific issues• Inter-company transactions• Intra GCC transactions • Apply any exemptions/Zero rate

What does VAT mean for

businesses

30

What VAT means for

you

PwC

VAT in the GCC

Claims & Documentation

Calculations and adjustments

Incorrect rates applied to sales/sales omitted

Delays with VAT payment/invoices

Invalid or missing documentation

Invalid/insufficient documentation to support VAT claim

Invalid VAT claims e.g.:

Claiming VAT in relation to Exempt/non business transactions

Claiming foreign tax on returns (i.e. VAT incurred in other countries)

Errors in calculation of VAT due/reclaimable

Clerical/manual/system errors

Omitting inter-company transactions

Journals adjustments

Manual corrections

Transactions outside system/one off/irregular

30PwC

VAT in the GCC

Challenges

33PwC

VAT in the GCC

VAT implementation

• Have you the appropriate resources to be compliant• Who will be responsible • Do you understand the new law/regulations• How do you keep up to date with changes

Interaction with tax authority

• Refunds/enquiries/audits • Records/supporting documents to deal with

audits/enquiries• Unclear matters/process to deal• Education/resources/training• Potential delays with refunds/time incurred by business

Manage change

• Transitional VAT tax issues – existing and future contracts• Understand tax planning and fraudulent VAT practices• Test drive overall VAT commercial chain before going live• Manage increased administrative costs• Manage cash flow, understand possible P&L impact

Communication

• Educate stakeholders internal and external – “top down” approach / contractual obligations / financial and accounting prerequisites / system and accounting requirements / training and workshops at all levels

• Interview sessions with all key stakeholders• Compile information through standard VAT templates – line

by line characterization and location analysis of revenues/expenses

VAT Implementation Project

32

05

PwC

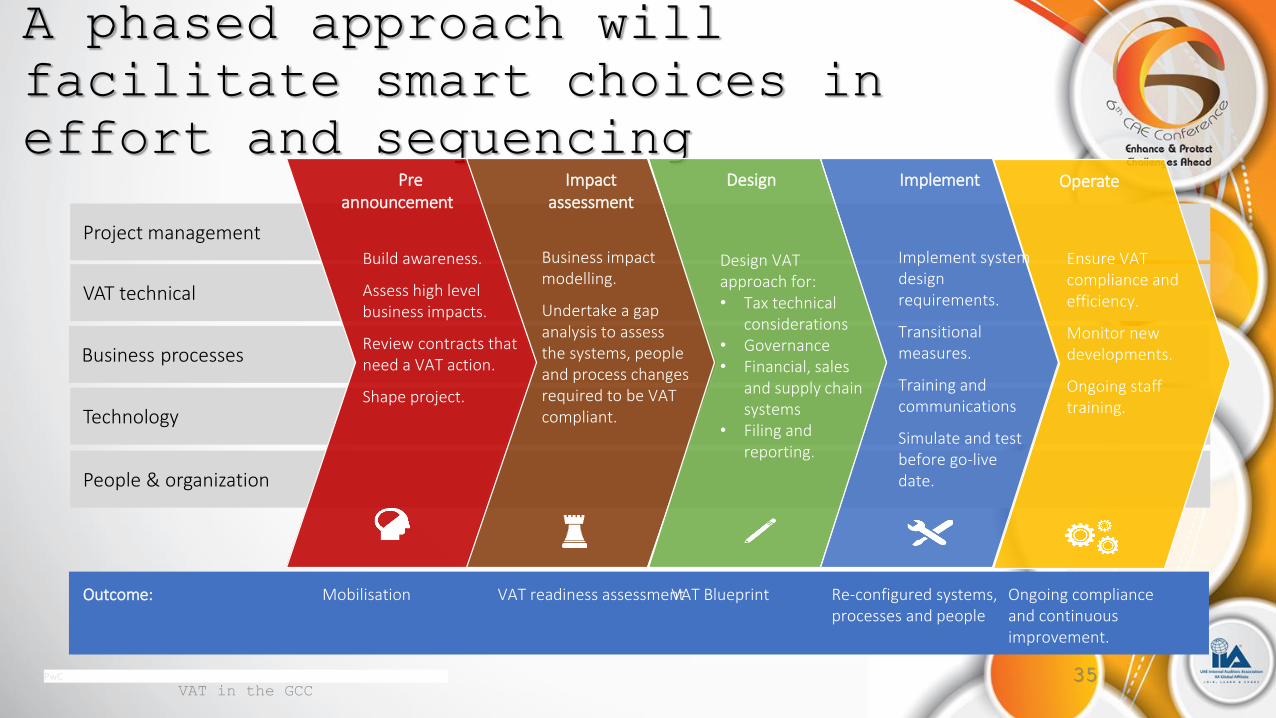

A phased approach will

facilitate smart choices in

effort and sequencing

VAT technical

Project management

Business processes

Technology

People & organization

Impact assessment

Design Implement OperatePre announcement

Business impact modelling.

Undertake a gap analysis to assess the systems, people and process changes required to be VAT compliant.

Build awareness.

Assess high level business impacts.

Review contracts that need a VAT action.

Shape project.

Design VAT approach for: • Tax technical

considerations • Governance• Financial, sales

and supply chain systems

• Filing and reporting.

Implement system design requirements.

Transitional measures.

Training and communications

Simulate and test before go-live date.

Ensure VAT compliance and efficiency.

Monitor new developments.

Ongoing staff training.

Mobilisation VAT readiness assessmentVAT Blueprint Re-configured systems, processes and people

Ongoing compliance and continuous improvement.

Outcome:

35PwC

VAT in the GCC

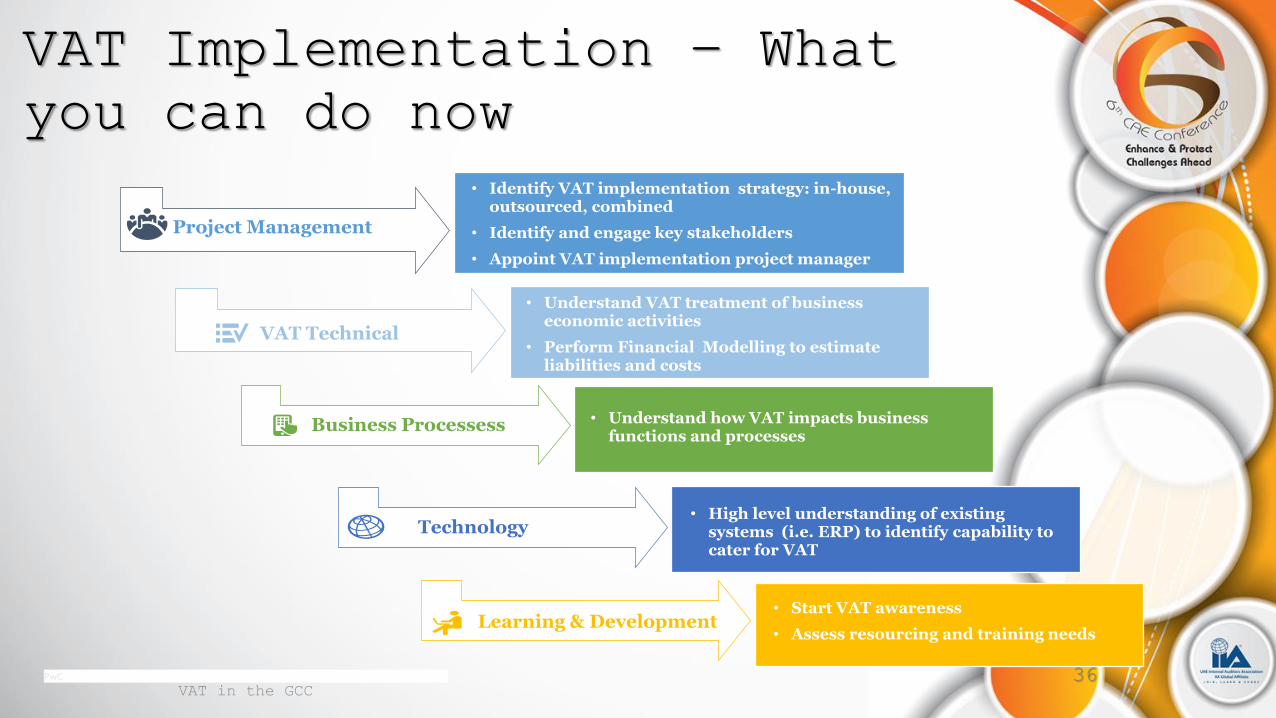

VAT Implementation – What

you can do now

• Understand VAT treatment of business economic activities

• Perform Financial Modelling to estimate liabilities and costs

• High level understanding of existing systems (i.e. ERP) to identify capability to cater for VAT

• Start VAT awareness

• Assess resourcing and training needs

VAT Technical

Business Processess

Technology

Learning & Development

• Understand how VAT impacts business functions and processes

Project Management

• Identify VAT implementation strategy: in-house, outsourced, combined

• Identify and engage key stakeholders

• Appoint VAT implementation project manager

36PwC

VAT in the GCC

© 2016 PwC. All rights reserved. Not for further distribution without the permission of PwC. “PwC” refers to the network of member firms of PricewaterhouseCoopers International Limited (PwCIL), or, as the context requires, individual member firms of the PwC network. Each member firm is a separate legal entity and does not act as agent of PwCIL or any other member firm. PwCIL does not provide any services to clients. PwCIL is not responsible or liable for the acts or omissions of any of its member firms nor can it control the exercise of their professional judgment or bind them in any way. No member firm is responsible or liable for the acts or omissions of any other member firm nor can it control the exercise of another member firm’s professional judgment or bind another member firm or PwCIL in any way.

• Jeanine Daou

• Middle East Indirect Tax Leader

• T: +971 (0) 4 304 3744

• Nadine Bassil

• Middle East Indirect Tax Director

• T: +971 (0)4 304 3688