Embed Size (px)

Citation preview

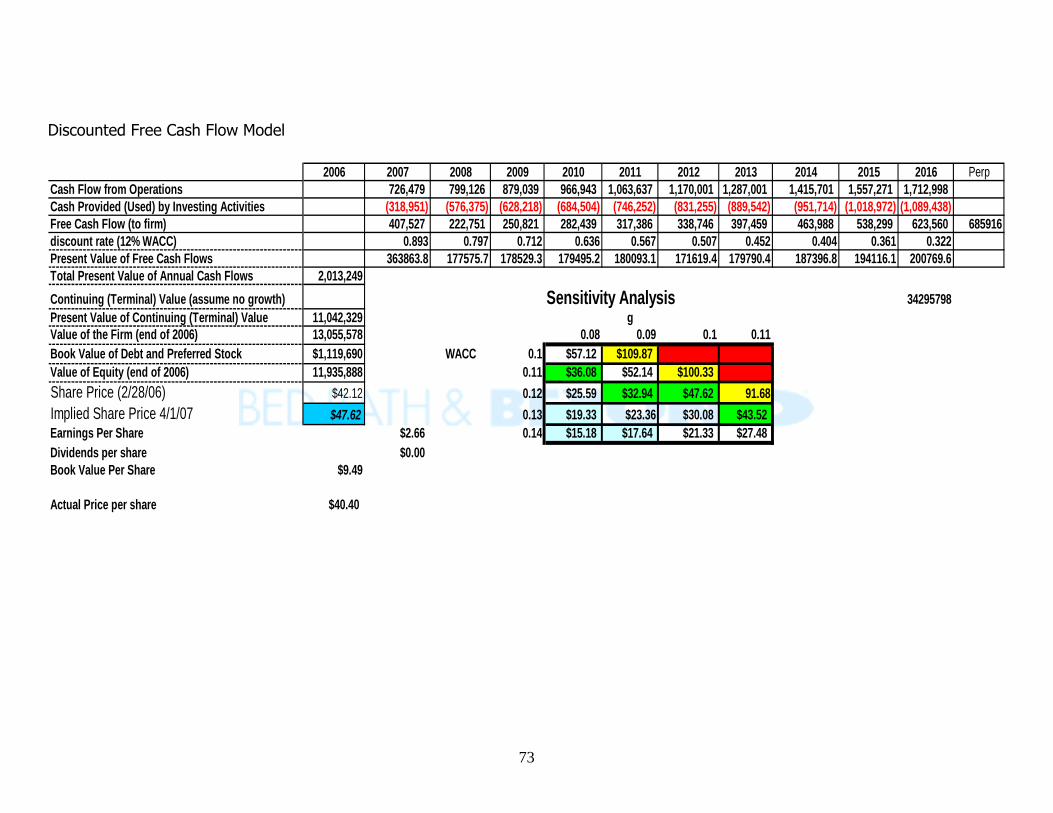

Valued at 1 April, 2007

Matthew Lewis: [email protected] Tyler Page: [email protected]

Alex Segreti: [email protected] Andrea Spencer: [email protected]

Stephen Wiggins: [email protected]

1

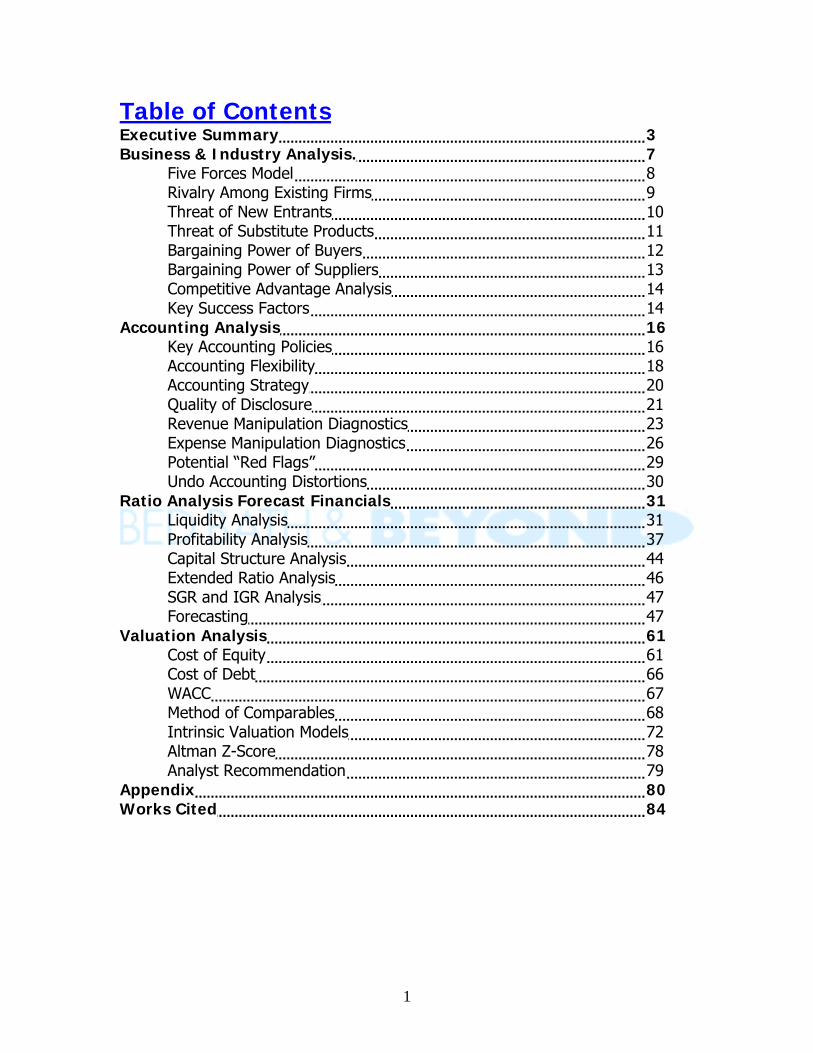

Table of Contents Executive Summary 3 Business & Industry Analysis. 7

Five Forces Model 8 Rivalry Among Existing Firms 9 Threat of New Entrants 10 Threat of Substitute Products 11 Bargaining Power of Buyers 12 Bargaining Power of Suppliers 13 Competitive Advantage Analysis 14 Key Success Factors 14

Accounting Analysis 16 Key Accounting Policies 16 Accounting Flexibility 18 Accounting Strategy 20 Quality of Disclosure 21 Revenue Manipulation Diagnostics 23 Expense Manipulation Diagnostics 26 Potential “Red Flags” 29 Undo Accounting Distortions 30

Ratio Analysis Forecast Financials 31 Liquidity Analysis 31 Profitability Analysis 37 Capital Structure Analysis 44 Extended Ratio Analysis 46 SGR and IGR Analysis 47 Forecasting 47

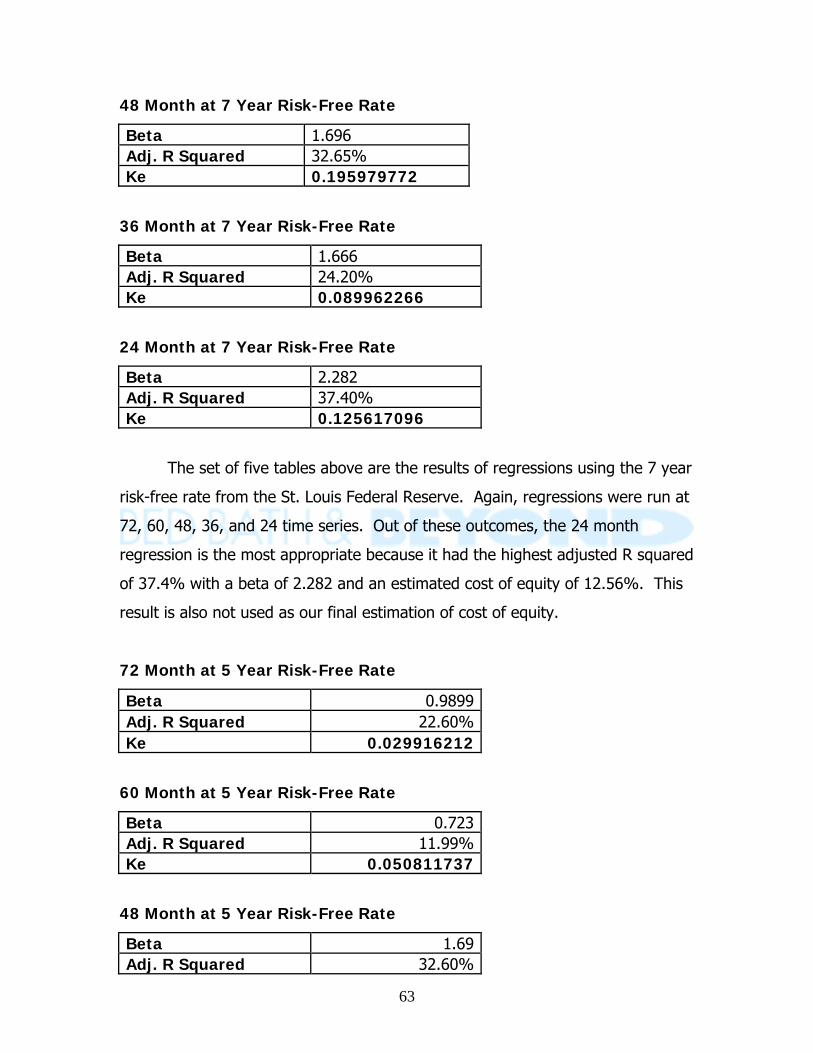

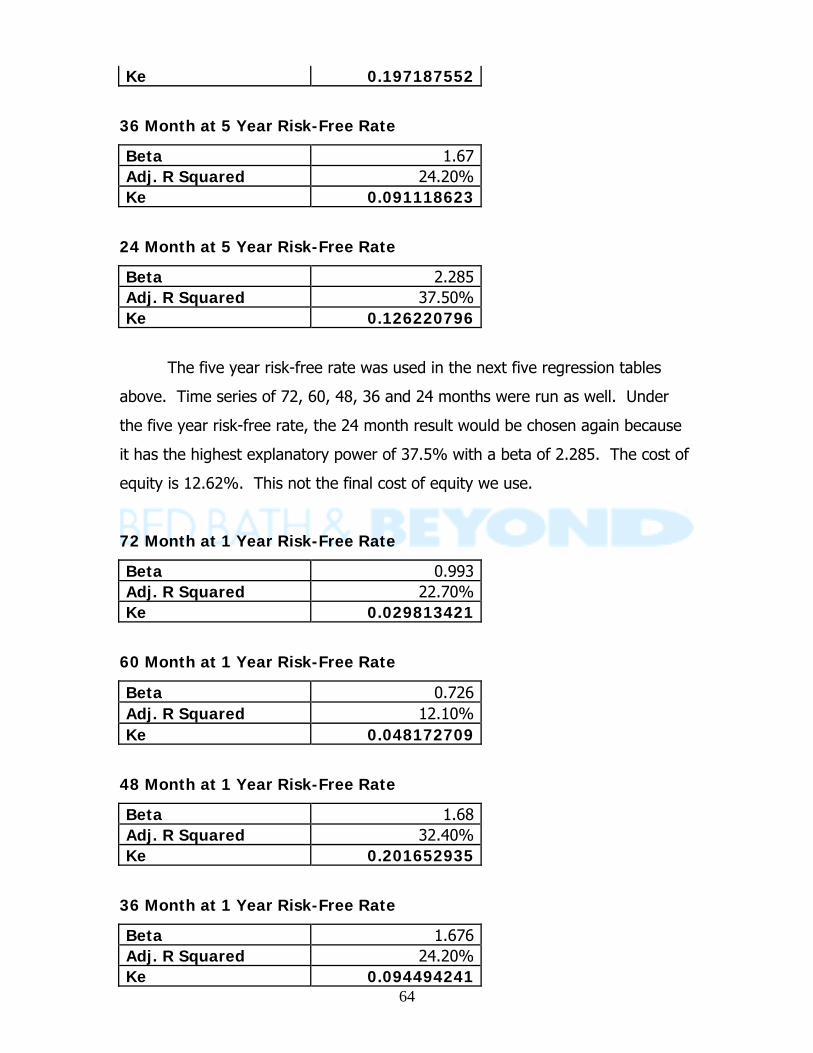

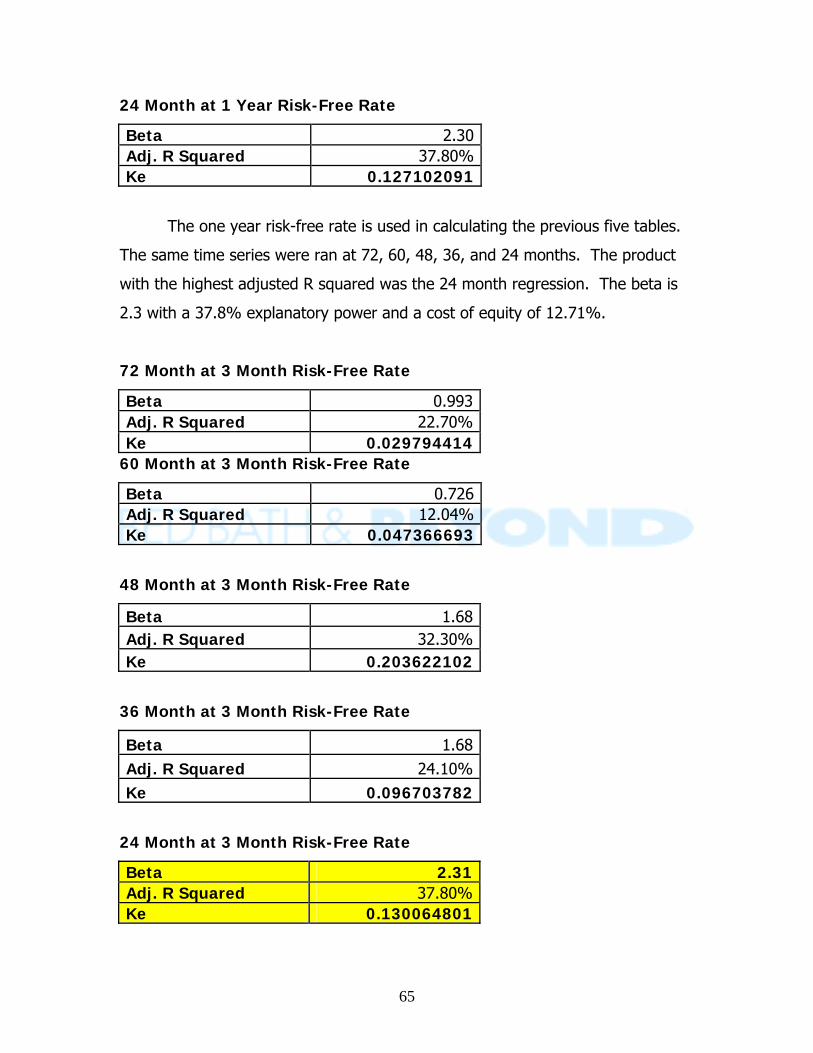

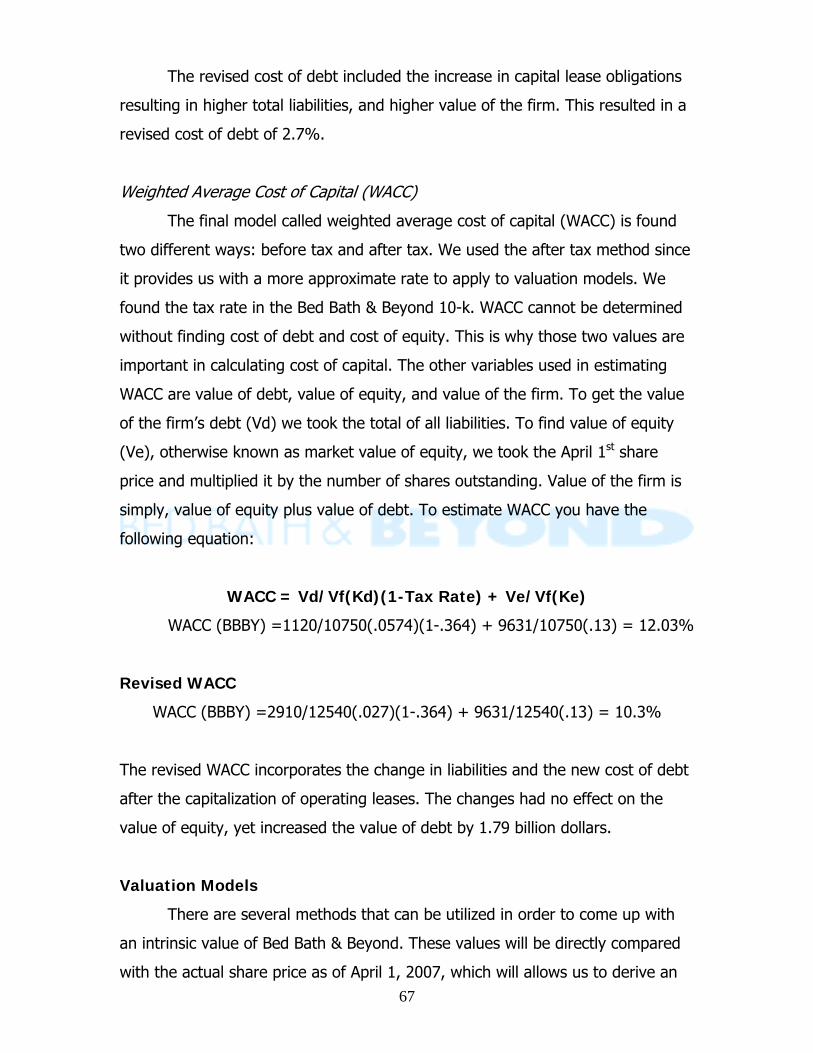

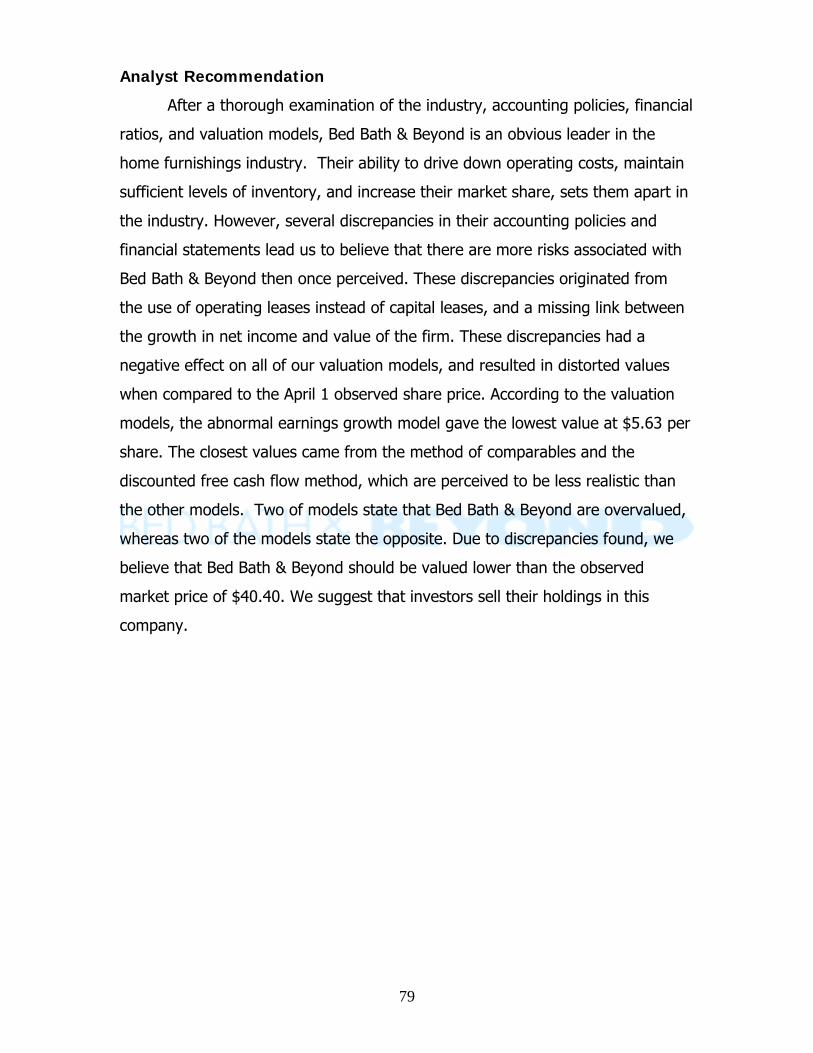

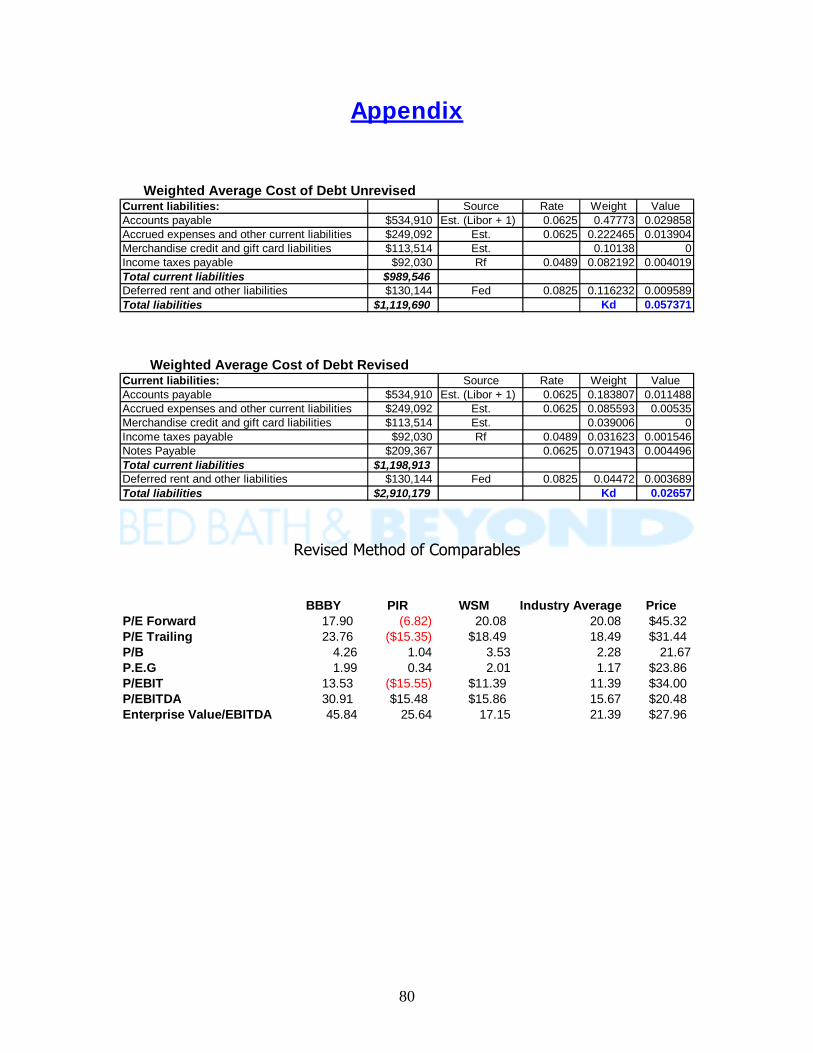

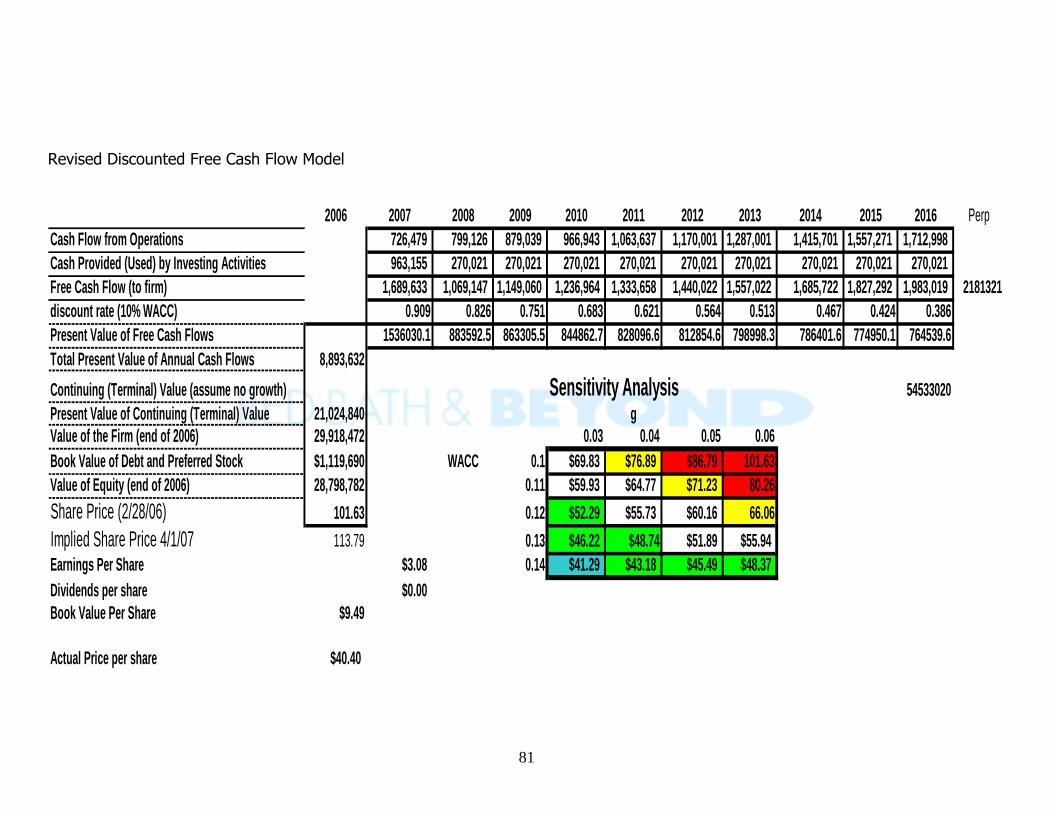

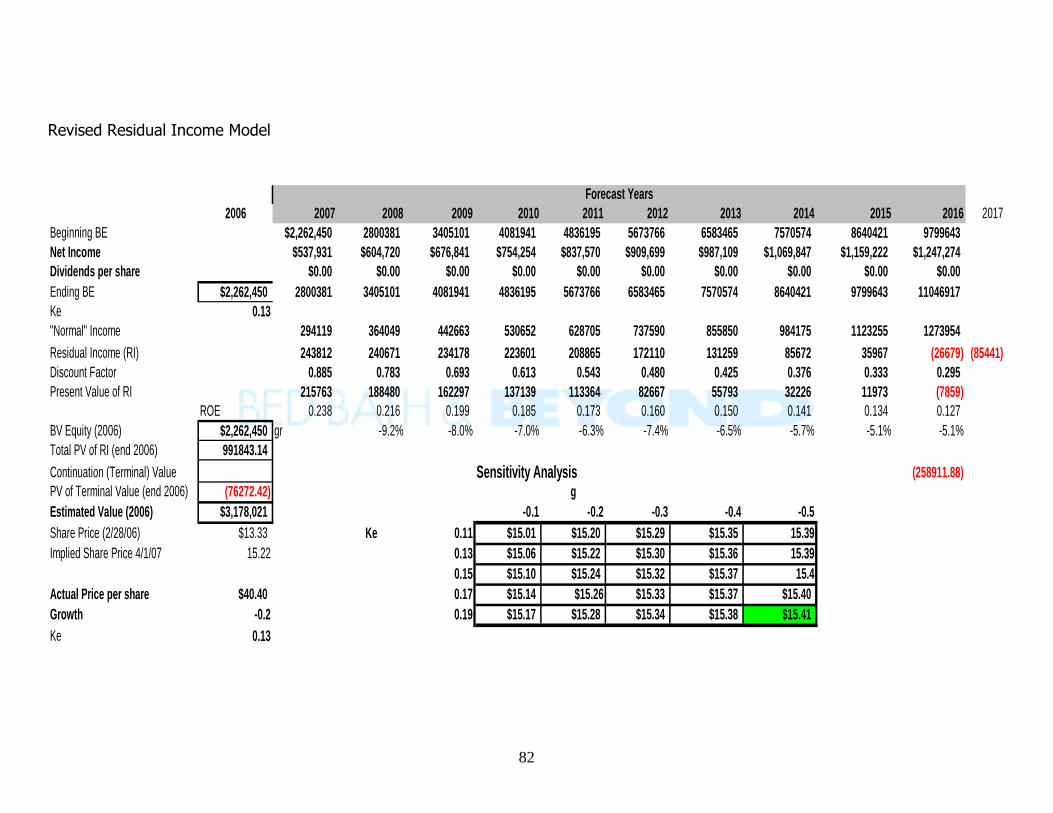

Valuation Analysis 61 Cost of Equity 61 Cost of Debt 66 WACC 67 Method of Comparables 68 Intrinsic Valuation Models 72 Altman Z-Score 78 Analyst Recommendation 79

Appendix 80 Works Cited 84

2

3

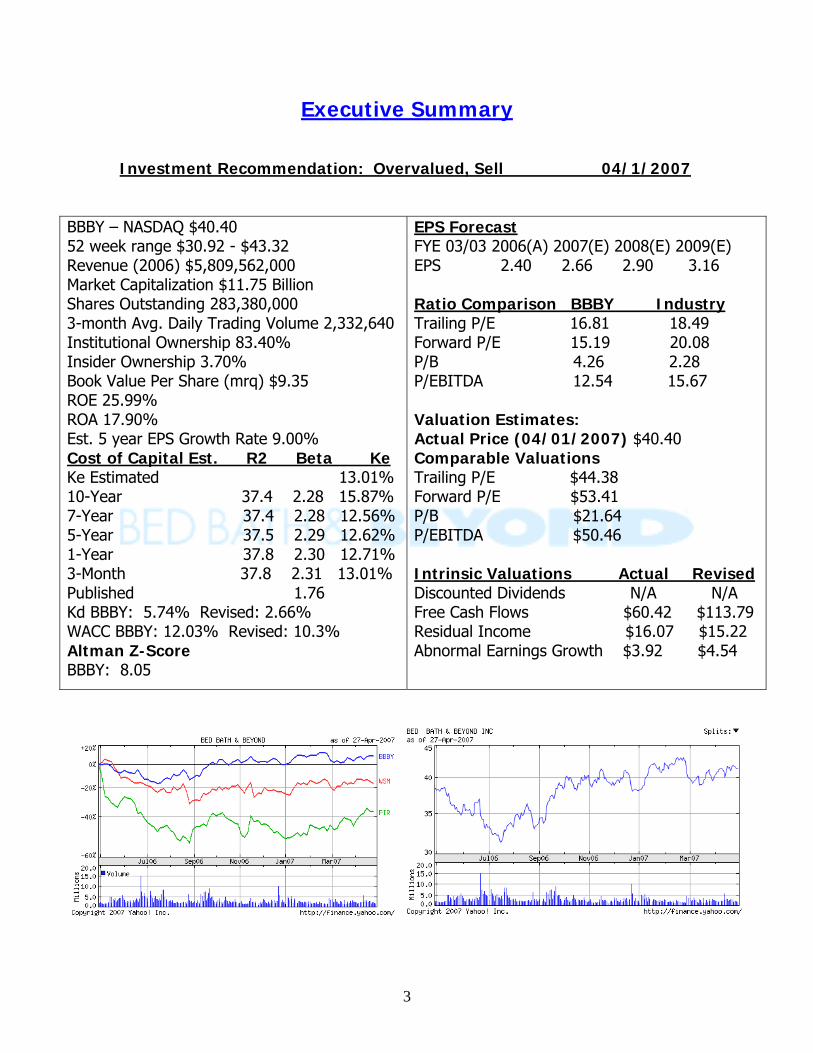

Executive Summary Investment Recommendation: Overvalued, Sell 04/1/2007

BBBY – NASDAQ $40.40 52 week range $30.92 - $43.32 Revenue (2006) $5,809,562,000 Market Capitalization $11.75 Billion Shares Outstanding 283,380,000 3-month Avg. Daily Trading Volume 2,332,640 Institutional Ownership 83.40% Insider Ownership 3.70% Book Value Per Share (mrq) $9.35 ROE 25.99% ROA 17.90% Est. 5 year EPS Growth Rate 9.00% Cost of Capital Est. R2 Beta Ke Ke Estimated 13.01% 10-Year 37.4 2.28 15.87% 7-Year 37.4 2.28 12.56% 5-Year 37.5 2.29 12.62% 1-Year 37.8 2.30 12.71% 3-Month 37.8 2.31 13.01% Published 1.76 Kd BBBY: 5.74% Revised: 2.66% WACC BBBY: 12.03% Revised: 10.3% Altman Z-Score BBBY: 8.05

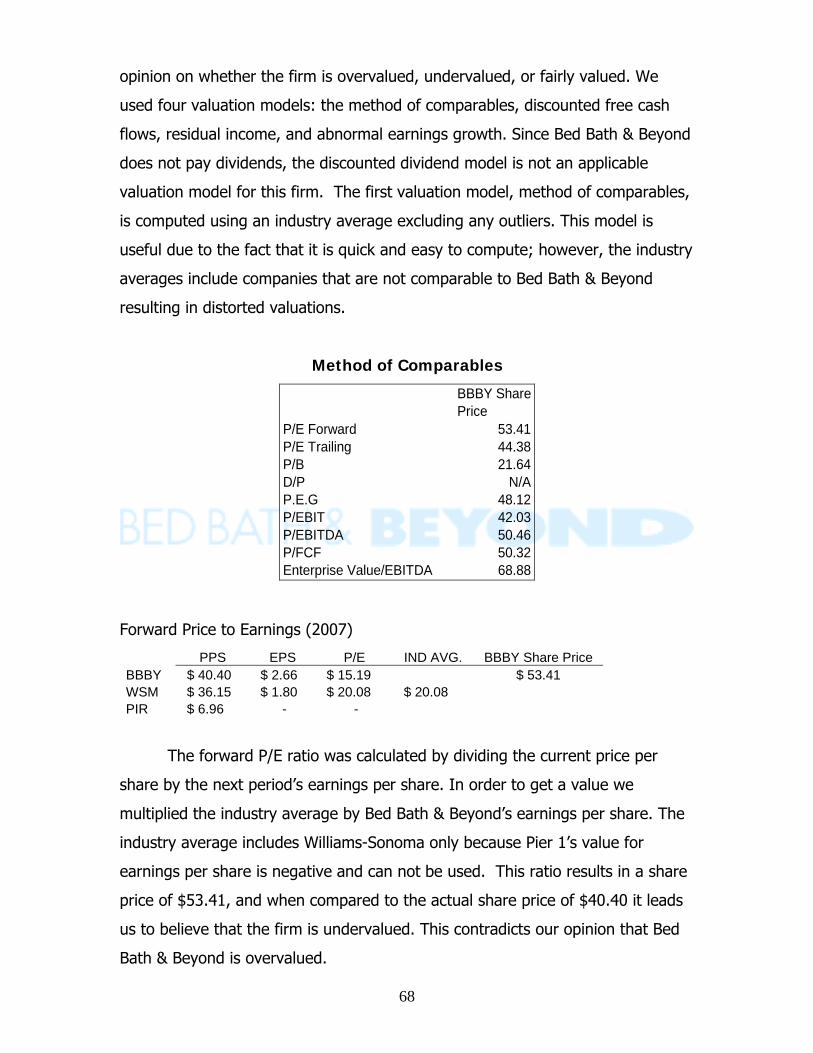

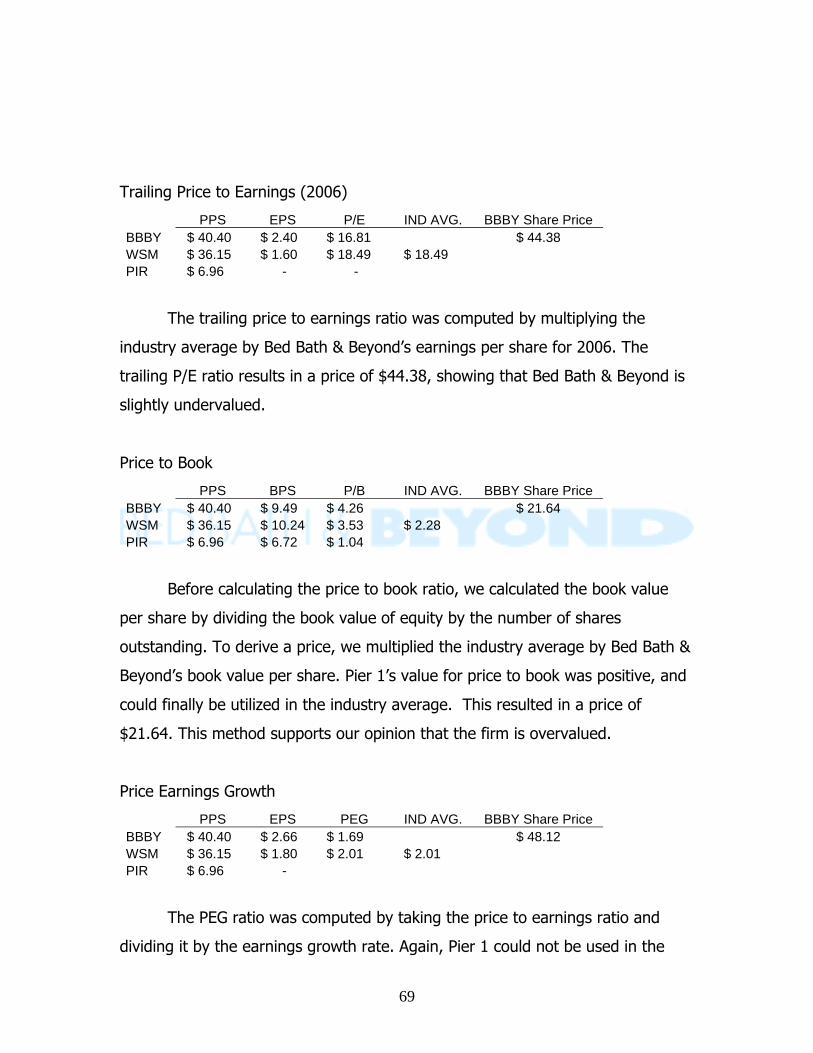

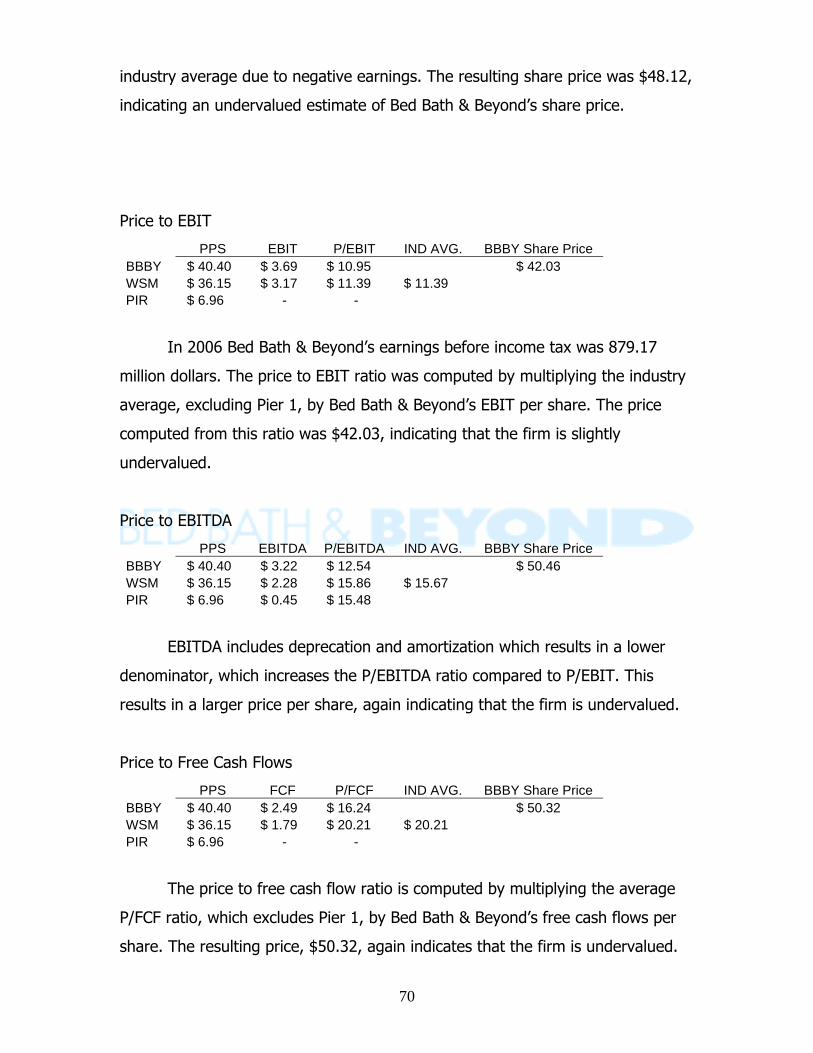

EPS Forecast FYE 03/03 2006(A) 2007(E) 2008(E) 2009(E) EPS 2.40 2.66 2.90 3.16 Ratio Comparison BBBY Industry Trailing P/E 16.81 18.49 Forward P/E 15.19 20.08 P/B 4.26 2.28 P/EBITDA 12.54 15.67 Valuation Estimates: Actual Price (04/01/2007) $40.40 Comparable Valuations Trailing P/E $44.38 Forward P/E $53.41 P/B $21.64 P/EBITDA $50.46 Intrinsic Valuations Actual Revised Discounted Dividends N/A N/A Free Cash Flows $60.42 $113.79 Residual Income $16.07 $15.22 Abnormal Earnings Growth $3.92 $4.54

4

Recommendation – Overvalued Firm – Sell Business, Industry Overview and Analysis Bed Bath & Beyond is one of the largest home furnishings and domestic

merchandise retailers in the country. They have expanded from two stores in

1971 to over 800 stores located in 46 states and Puerto Rico. This industry is

classified as highly competitive. The key players are Bed Bath & Beyond, Linens-

N-Things, Williams Sonoma, and Pier 1. The home furnishings industry is also

comprised of discount merchandise firms such as, Wal-Mart and Target. These

firms have the ability to steal some of the market share since a consumer can

find a variety of items in one store, and often at a lower price. However, the key

firms prosper since they have a greater variety of home furnishing products and

usually more knowledgeable associates. Overall, it is difficult to enter this

industry with a history of established firms. A firm must obtain a large amount of

capital and resources to be able to enter and compete with this developed

industry. Substitute products in this industry are a relatively moderate threat.

Firms in this industry usually carry similar products at similar prices, making it

easy for a consumer to switch back and forth between firms. Customers have a

lot of bargaining power in the industry. This means that firms in the industry

have to compete on price, resulting in smaller profit margins. Finally, suppliers

for the industry have a relatively low bargaining power over firms. Firms and

consumers both benefit from lower inventory costs, the result of an

overabundance of suppliers.

Accounting Analysis

An accounting analysis is performed to evaluate a firm’s accounting

practices in comparison to the realities of their current and prospective financial

position. The 10-k released each year by Bed Bath & Beyond contains vital

information identifying the firm’s key accounting policies. Bed Bath & Beyond

5

must be efficient managing operating costs, maintaining sufficient inventory

levels, and must possess strong expansion initiatives.

In keeping with generally accepted accounting principles (GAAP), Bed

Bath & Beyond follows aggressive accounting policies. The quality of disclosure

that a 10-k provides is of high importance to potential investors. Bed Bath &

Beyond inadequately discloses line item information within financial statements,

and fails to go beyond what is already there. This lack of disclosure appears to

be the industry standard, and requires a more meticulous evaluation of the

numbers presented in the financial statements.

Screening ratios are utilized to express any possible manipulations to

revenues or expenses. “Red flags” could be raised from negative trends in these

ratios that could possibly indicate inflated revenues or expenses being booked as

assets. Bed Bath & Beyond does not show any alarming trends in revenue

manipulation because they have the net income to support increases in sales.

However, Bed Bath & Beyond does have a declining CFFO/OI ratio. This is a

concern because operating expenses should increase with revenues. The

greatest concern about Bed Bath & Beyond’s accounting policies is their use of

operating leases. Operating Leases are a form of off-balance sheet transactions,

and expressed as only an operating expense. If these leases were capitalized,

Bed Bath & Beyond would be forced to include approximately 2.13 billion in long-

term liabilities and leased assets on the balance sheet.

Financial Analysis and Forecast

In valuing a firm, financial ratios can show how successful the firm

operates. Financial ratios can be broken down into three categories: liquidity,

profitability, and capital structure ratios. Liquidity ratios consist of seven ratios

that each explain Bed Bath & Beyond’s ability to pay back current liabilities and

debt. After compiling results, Bed Bath & Beyond’s overall liquidity appears to

have a declining trend. This could directly affect their financial position and

competitive advantages in the industry. Profitability ratios provide an idea about

6

the historical profitably, as well as, the ability to continue to efficiently generate

profits for the firm. The six ratios used in evaluating profitability, have steadily

increased over the past five years for Bed Bath & Beyond. Increases in net

income and efficient management practices have contributed to this steady

increase in profitability. Finally, the capital structure analysis examines the

percentage of the firm’s value that is comprised of debt and equity. We were

only able to utilize the debt to equity ratio because Bed Bath & Beyond does not

posses any notes payable or interest expense.

Forecasting Bed Bath & Beyond’s financial statements for ten years

allowed us to get an idea of where the company will be in the future. On the

income statement, sales and net earnings forecasts doubled which caused equity

to outgrow total assets. In order to account for this growth in the firm, total

assets had to be increased in proportion to equity. The firm was then forecasted

after the operating leases were capitalized and adjusted on the balance sheets.

Analysis Evaluations

In order to come up with an opinion on the value of the firm, we utilized

four intrinsic valuation models. The inconsistency of numbers in the financial

statements distorted the results from the valuation models. The residual income

ad AEG model resulted in the lowest intrinsic values, whereas the method of

comparables and free cash flow models were more accurate. The outcomes of

these ratios lead us to believe that Bed Bath & Beyond is an overvalued firm.

7

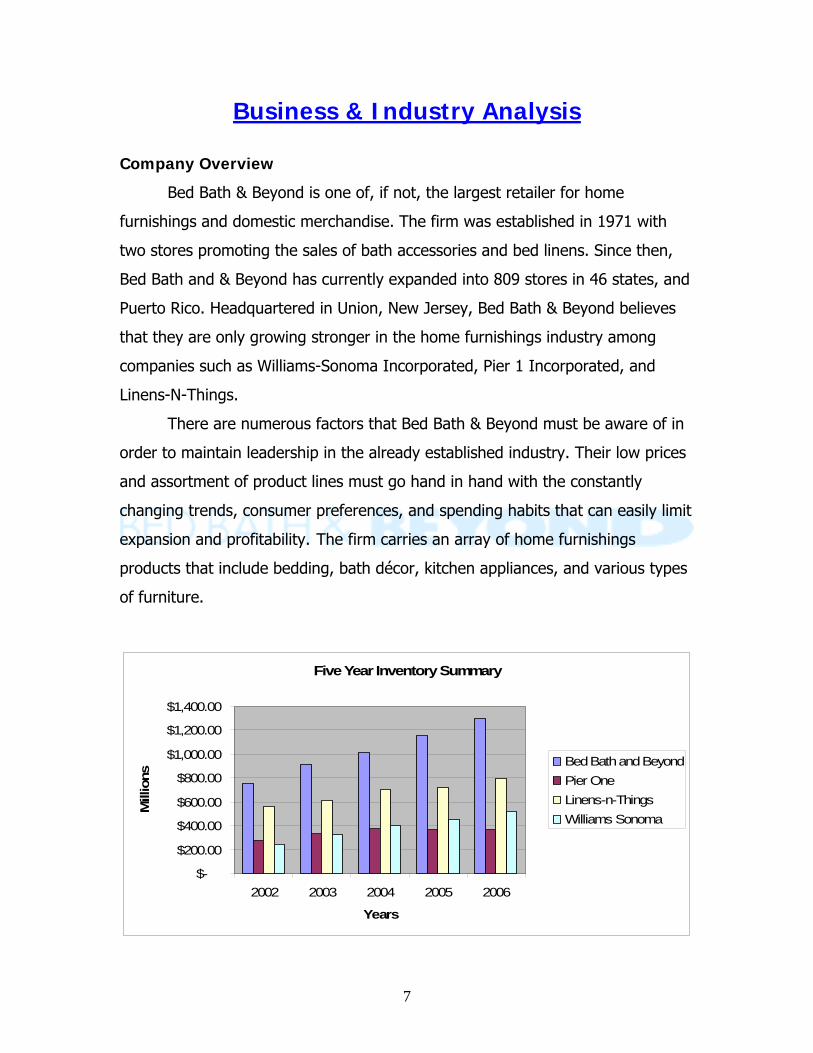

Five Year Inventory Summary

$-

$200.00

$400.00

$600.00

$800.00

$1,000.00

$1,200.00

$1,400.00

2002 2003 2004 2005 2006

Years

Mill

ions

Bed Bath and BeyondPier OneLinens-n-ThingsWilliams Sonoma

Business & Industry Analysis

Company Overview

Bed Bath & Beyond is one of, if not, the largest retailer for home

furnishings and domestic merchandise. The firm was established in 1971 with

two stores promoting the sales of bath accessories and bed linens. Since then,

Bed Bath and & Beyond has currently expanded into 809 stores in 46 states, and

Puerto Rico. Headquartered in Union, New Jersey, Bed Bath & Beyond believes

that they are only growing stronger in the home furnishings industry among

companies such as Williams-Sonoma Incorporated, Pier 1 Incorporated, and

Linens-N-Things.

There are numerous factors that Bed Bath & Beyond must be aware of in

order to maintain leadership in the already established industry. Their low prices

and assortment of product lines must go hand in hand with the constantly

changing trends, consumer preferences, and spending habits that can easily limit

expansion and profitability. The firm carries an array of home furnishings

products that include bedding, bath décor, kitchen appliances, and various types

of furniture.

8

Bed Bath & Beyond has steadily increased its inventory over the past five

years, and attained an 11.63 billion dollar market capitalization. This is credited

primarily to new store expansion and efficiency of operations. Competitors in the

industry such as Williams-Sonoma Inc., and Pier 1 Inc., trail with the following

market caps: 3.84 billion, and 596 million. Comparable figures for Linens-N-

Things are unavailable since it is a privately held company. Over the past five

years, the total inventory of Bed Bath & Beyond has increased from 754 million

in 2002, to 1.3 billion dollars in 2006. These numbers support the company’s

goals to expand operations and store space. During fiscal 2006, the company is

planning on opening 80 new Bed Bath & Beyond stores. As a leader in the

industry, the company’s shares of stock have increased just over eight dollars

since March 2002, from 34 dollars in March 2002, to 40.40 dollars on April 1,

2007.

Five Forces Model

In order to analyze the profit potential of Bed Bath & Beyond, it is

important to understand the industry in which the firm competes. There are five

areas that need to be examined in order to understand where Bed Bath &

Beyond stands in the Home Furnishings Industry. The following table

summarizes the results from the analysis of the five forces as they pertain to Bed

Bath & Beyond.

Home Furnishings Industry

Rivalry Among Firms Highly Competitive

Threat of New Entrants Low Threat

Threat of Substitute Products Moderate Threat

Bargaining Power of Buyers Very High (High Customer Power)

Bargaining Power of Suppliers Very Low (Low Supplier Power)

9

Rivalry Among Existing Firms

Industry growth

A company’s profitability is directly related to the competition between

existing firms in the industry. The retail industry has always been known to be

extremely competitive. The home furnishings industry, which Bed Bath & Beyond

is classified under, is currently growing. Although the industry is expanding, firms

must still compete for market share among each other. The growth is steady in

this industry due to the constant demand for household products. This demand

gradually increases as consumer’s needs increase. This creates high competition

in price, customer service, and the market share of the company definitely plays

a role in its ability to compete.

Concentration

There are many different firms in the home furnishings industry. The big

competitors include Linens-N-Things, Pier 1, Williams Sonoma, and Bed Bath &

Beyond. Many other firms compete in this industry in an indirect manner;

examples include discount stores such as Target and Wal-Mart. The high level of

competition results in a largely fragmented industry, and severe price

competition.

Differentiation

“The extent to which firms in an industry can avoid head on competition

depends on the extent to which they can differentiate their products and

services” (Palepu 2-3). This is a challenge in this industry because many of the

products are undifferentiated. Market share and store image are extremely

important because consumers are going to shop at a place they recognize.

Fixed/Variable Costs

It is common in the industry to have high fixed costs. Many companies

rely on the use of operating leases for retail locations, merchandising, and

10

inventory. These are fixed rents for certain periods of time. The yearly operating

leases are discussed in detail in a later section, but the average rent was 340

million dollars per year. Variable costs in the industry generally come from

inventory. Many companies try to maintain large quantities of inventory, and are

vulnerable to the risk of excess volume if current consumer preferences were to

change.

Threat of New Entrants

Scale Economies

Growing industries tend to attract new entrants because they are seen as

having profit potential. In the home furnishings industry, the threat of new

entrants is classified as being very low because of economies of scale. The

industry growth is driving down the average price of products. New entrants

would have to be extremely large in order to gain market share due to the highly

concentrated industry. Bed Bath & Beyond is just one of many firms operating in

this industry. There are several other firms that can compete on the same level

of Bed Bath & Beyond like Linen-N-Things, and Williams-Sonoma. In addition,

they all must compete with all other major discount and department stores such

as Wal-Mart and Target. Economies of scale are clearly a deterrent for new firms

that attempt to enter the industry. If new firms were to enter, they would

probably suffer from the cost disadvantage, or face the choice of investing in a

large capacity.

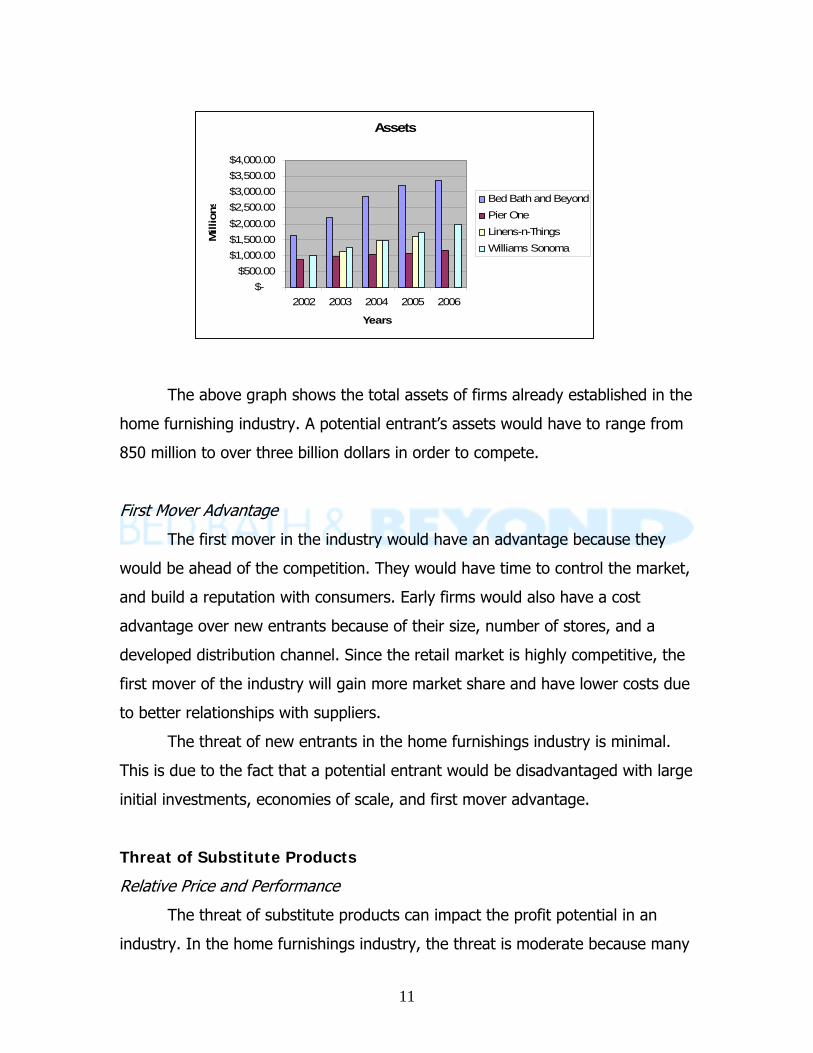

11

The above graph shows the total assets of firms already established in the

home furnishing industry. A potential entrant’s assets would have to range from

850 million to over three billion dollars in order to compete.

First Mover Advantage

The first mover in the industry would have an advantage because they

would be ahead of the competition. They would have time to control the market,

and build a reputation with consumers. Early firms would also have a cost

advantage over new entrants because of their size, number of stores, and a

developed distribution channel. Since the retail market is highly competitive, the

first mover of the industry will gain more market share and have lower costs due

to better relationships with suppliers.

The threat of new entrants in the home furnishings industry is minimal.

This is due to the fact that a potential entrant would be disadvantaged with large

initial investments, economies of scale, and first mover advantage.

Threat of Substitute Products

Relative Price and Performance

The threat of substitute products can impact the profit potential in an

industry. In the home furnishings industry, the threat is moderate because many

Assets

$-$500.00

$1,000.00$1,500.00$2,000.00$2,500.00$3,000.00$3,500.00$4,000.00

2002 2003 2004 2005 2006

Years

Mill

ions

Bed Bath and BeyondPier OneLinens-n-ThingsWilliams Sonoma

12

items perform the same functions and are priced similarly. There are many

discount stores which sell these items, but many consumers choose the specialty

stores. Access to distribution channels is easy to obtain. A new entrant would not

have difficulty establishing a relationship with a supplier, but a new entrant may

not be able to get favorable terms with a supplier. Therefore, their cost would be

too high, prices of their goods would be higher, and they would not be able to

compete in the industry.

Buyer’s Willingness to Switch

The consumers within this industry are focused on purchasing products at

the lowest possible price. For this reason, their willingness to switch between

firms in the industry is very high. The buyers have flexibility to choose between

firms in the industry, resulting in further depletion of prices.

Bargaining Power of Buyers

When considering customer power, two main factors come into play. One

of which is the bargaining power of the purchaser. In this industry, customers

have high bargaining power because of the intense concentration of similar

competitors. Bargaining power is developed when companies in the industry are

attempting to attract customers to purchase from them and not revert to other

retailers. The other factor would be price sensitivity. Bargaining power and price

sensitivity go hand in hand. The retailers in this industry must have some level of

price sensitivity in order to get those customers. This tends to be difficult

because home furnishing products are undifferentiated.

Differentiation

Retail firms in this industry all carry similar inventories, causing the

products and firms to be undistinguishable. This permits the customers to pit the

firms against each other in price competition. The firm that competes at the

lowest cost is going to gain the customer for the same product that they could

13

find elsewhere. In the home furnishings industry, it is hard to differentiate

products. This causes an industry-wide problem and many companies find it

difficult to prevent their consumer sales from going to their competitors.

Bargaining Power of Suppliers

Suppliers are considered to have power when there are few firms and

substitutes in the industry. Therefore, the supplier power is extremely low within

the home furnishings industry. The four major firms that exist in this

environment are able to intimidate the suppliers in order to achieve the lowest

cost on a product. Suppliers rely on the major companies in this industry to help

them generate profits. Therefore, suppliers prefer a retailer with a substantial

amount of customer traffic. The firms in this industry attempt to leverage

themselves against suppliers to get the lowest cost, which in turn will lower costs

to the consumer.

Switching costs

Since the industry contains many suppliers, the cost of switching suppliers

is affordable. Suppliers are constantly competing to have their products on the

shelves at these retailers. Therefore, suppliers do not have much bargaining

power. Since limited power exists on the suppliers’ behalf, switching costs for

firms in this industry are relatively non-existent.

Number of Suppliers

Suppliers are plentiful in the home furnishings industry. One firm

recorded having approximately 4,300 suppliers. The largest supplier accounted

for only 4% of total merchandise purchases. According to Bed Bath & Beyond’s

10-k, the top ten leading suppliers account for a minimal total of 18% for

merchandise purchases. If suppliers were to increase their costs, buyers have

the power and freedom to turn to other suppliers at lower costs.

14

Competitive Advantage Analysis

Industry Classification

The home furnishings and domestic merchandise retail industry is very

competitive. A person can go to almost any store and get items they need for

their home. Bed Bath & Beyond, Linens-N-Things, and Pier 1 tend to offer more

specialty items that are less likely found in discount stores like Target and Wal-

Mart. These home furnishing stores also provide many advantages beyond

specialty items, such as, limited crowds, and a timely shopping experience. As of

now, Bed Bath & Beyond leads the industry in sales followed by Linens-N-Things,

Williams-Sonoma, and Pier 1. Firms in this industry present their merchandise in

a distinct manner that maximizes the customers shopping experience; whereas,

stores such as Target and Wal-Mart, have domestic merchandise in select isles

throughout their stores.

Key success factors for the industry

Cost leadership

The main success factor in this industry is cost leadership. Since there are

many different competitors, the company that can supply name brand or similar

products for the lowest price will attract more customers. Most cities will contain

several home furnishing companies, expressing the ease of going to another

company to purchase the product.

Differentiation

Today the industry’s top goal is to maintain quality goods and everyday

low pricing. They do this by observing competitor’s prices often to ensure their

prices are matched, if not lower. Superior customer service also drives the

success of the industry. The firm with employees most knowledgeable about the

goods the store carries, and where they are located throughout the store, have

an advantage over the other competitors. Another goal is to have their isles set

15

up where customers can easily see the many goods that appeal to them and the

wide-selection the firms in the industry offers.

Merchandise assortment sets firms in the home furnishings industry apart

from department stores. Many home furnishing companies carry the same type

of goods as the department stores, but a wider variety of brands, gadgets, and

prices. Today the competitors of this industry carry linens, kitchen goods, beauty

care, furnishings, and other house wares. Having more of these goods drive

more customers to these stores for unique or hard to find products that you may

not find at a department store. Store personnel are encouraged to tailor each

store to the city in which it is located. This means that items will vary based on

demographics, climate, and constantly changing trends.

16

Accounting Analysis

Key Accounting Policies

An accounting analysis is performed to evaluate a firm’s accounting

practices in comparison to the realities of their current and prospective financial

position. In other words, do the firm’s accounting actions define or explain the

numbers represented in the financial statements? Before an analysis can begin,

one must first identify the firm’s key success factors and risks. Bed Bath &

Beyond operates in a highly competitive home furnishings industry and must

focus on managing operating costs, maintaining sufficient inventory levels in an

industry with changing customer preferences, and strong expansion initiatives.

“Judgment is used in areas such as the inventory valuation, impairment of long

lived assets, goodwill, stock-based compensation, and future operating lease

obligations” (BBBY 10-k). This freedom can lead management to more

aggressive accounting practices in order to meet the firm’s key success factors.

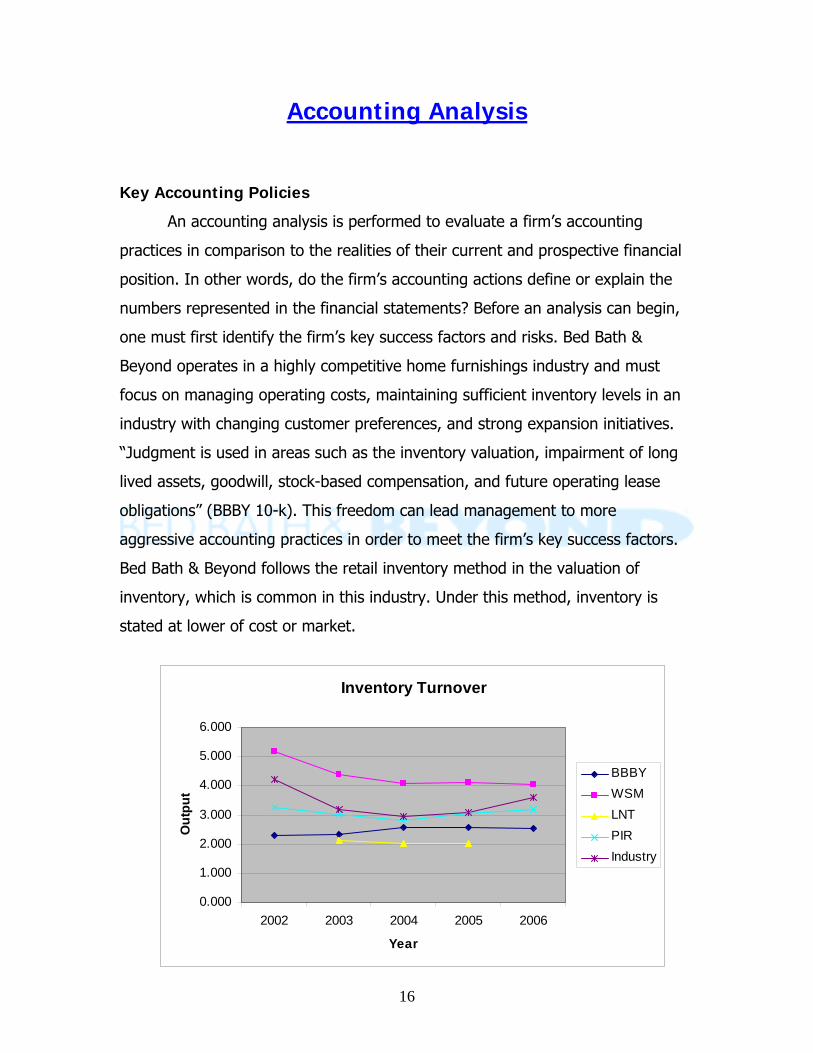

Bed Bath & Beyond follows the retail inventory method in the valuation of

inventory, which is common in this industry. Under this method, inventory is

stated at lower of cost or market.

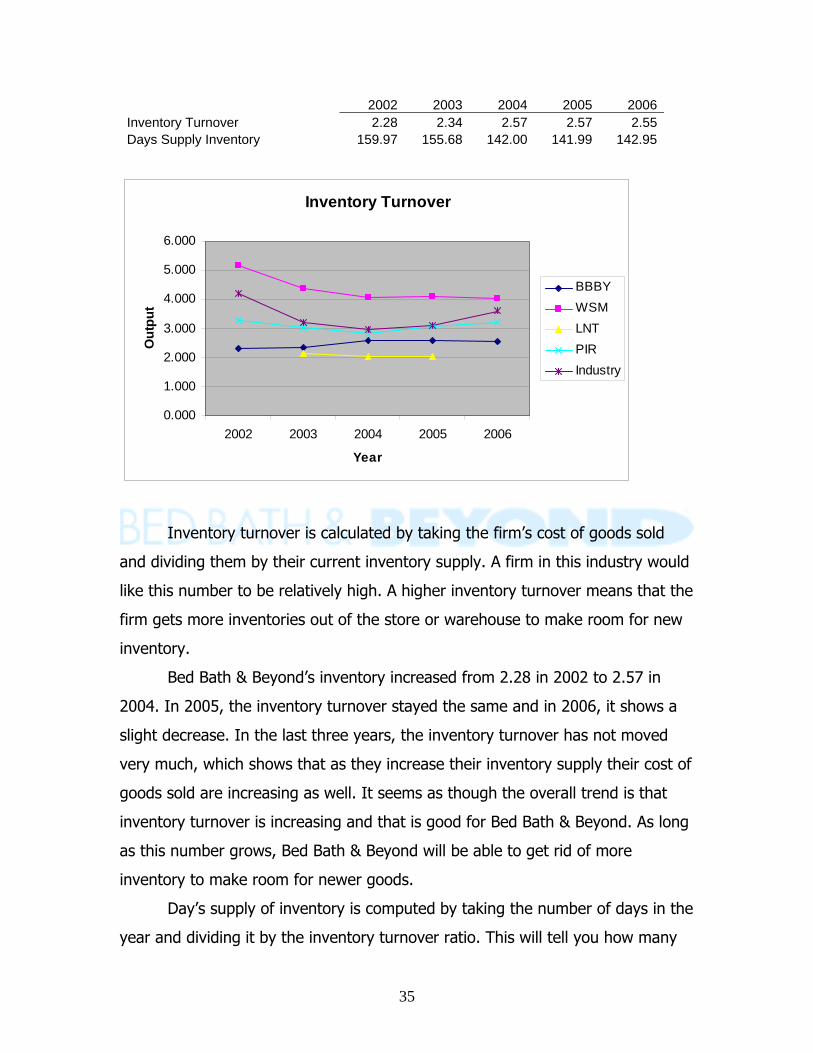

Inventory Turnover

0.000

1.000

2.000

3.000

4.000

5.000

6.000

2002 2003 2004 2005 2006

Year

Out

put

BBBYWSMLNTPIRIndustry

17

Over the past five years, Bed Bath & Beyond’s inventory levels have

steadily increased from 750 million to 1.3 billion dollars in 2006. The rapid

growths in these values are the result of large number of new store openings.

Their efficiency in moving inventory is calculated by the inventory turnover ratio.

The industry as a whole has seen a decline in this efficiency from 2002 to 2004.

However, it has recovered from the decline in 2005 and 2006.

Bed Bath & Beyond bases a large portion of profitability upon expansion of

new stores. Since it would be extremely costly to own each of these buildings,

the firm conducts business through operating leases on their retail stores,

warehouses, and office facilities. Operating leases are lease agreements with

scheduled rent over a period of time. A benefit of an operating lease is that there

is not a liability on the balance sheet. Instead, the lease is shown as an expense

on the income statement ( Stern.nyu.edu). The terms of Bed Bath & Beyond

leases range from 5-20 years, usually with renewal options at increased rates.

They are also responsible for paying insurance, taxes, and various maintenance

charges (BBBY 10-k). Operating Leases can lead to grossly underestimated

liabilities on the financial statements. Managers can use this aggressive form of

accounting to mislead investors on the true elements of the balance sheet.

Bed Bath & Beyond chooses to store majority of its merchandise in the

retail store themselves. This directly correlates with their key success factor of

maintaining adequate inventory to meet customers’ needs. The firm also has two

distribution centers and twelve warehouses to store excess inventory, and fulfill a

portion of its internet orders. This means that inventory is usually shipped

directly from manufacturers to Bed Bath & Beyond stores. In addition, the firm

manages two E-Fulfillment centers that serve as distribution centers specifically

for internet orders.

18

Accounting Flexibility

All publicly-traded firms are required to submit a variety of reports to the

SEC each year. Ideally, the numbers represented in the reports are in agreement

with GAAP (generally accepted accounting principles). However, some managers

have a certain degree of flexibility, or leniency in the disclosure of their financial

reports. For example, in the event of inventory valuation, the manager can use

methods such as LIFO, FIFO, or a weighted-average cost. As previously stated,

majority of the home furnishings industry uses lower of cost or market to value

their inventory. When Bed Bath & Beyond acquired Christmas Tree Stores in

2003, they chose to value CTS’s inventory using the FIFO method. This gives the

firm the opportunity to control inventory valuation of particular acquisitions

within the company. If the firm chooses to increase cost of goods sold, to lessen

income taxes, a LIFO valuation would be implemented. The FIFO method could

be implemented if the firm is focused on decreasing expenses. Alterations in

valuation must be monitored over the years because an inconsistency in policy

could raise concerns.

Managers within the industry also have the flexibility to report balance

sheet values in two separate books: one for financial reporting purposes, and

one for income tax purposes. There could easily be a difference between the

income reported to shareholders, and the income reported to the IRS. In 2006,

Bed Bath & Beyond claimed “a net current deferred income tax asset of 70.1

million dollars and a net non current deferred income tax liability of 16.3 million

dollars (BBBY 10-k). This aggressive accounting policy allows managers to stray

from the industry standard of straight-line-depreciation and use an accelerated

depreciation process to receive tax benefits.

The choice of using operating leases over capital leases is another area

which firms have flexibility. Firms often choose to lease long term assets rather

than purchase them as is the case with Bed Bath & Beyond; they choose to

operate using only operating leases. Operating leases are common among the

industry. This can lead to a deceptive view of the company’s financial position

19

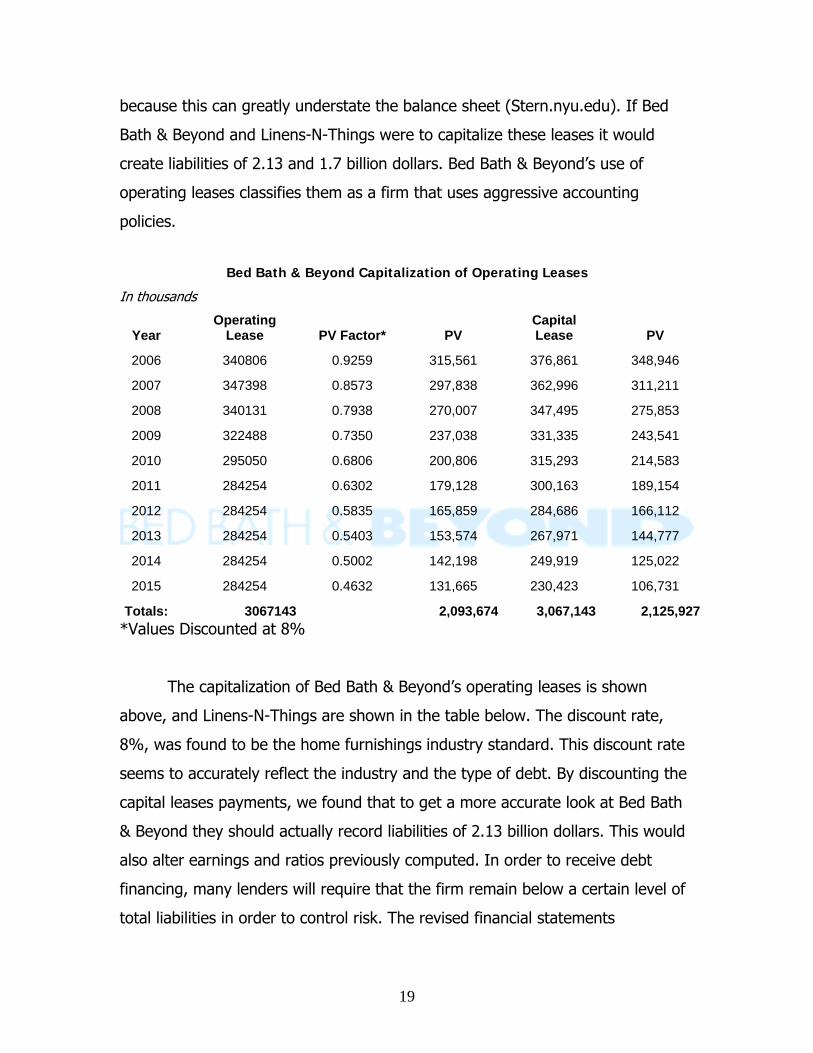

because this can greatly understate the balance sheet (Stern.nyu.edu). If Bed

Bath & Beyond and Linens-N-Things were to capitalize these leases it would

create liabilities of 2.13 and 1.7 billion dollars. Bed Bath & Beyond’s use of

operating leases classifies them as a firm that uses aggressive accounting

policies.

Bed Bath & Beyond Capitalization of Operating Leases

In thousands

Year Operating

Lease PV Factor* PV Capital Lease PV

2006 340806 0.9259 315,561 376,861 348,946

2007 347398 0.8573 297,838 362,996 311,211

2008 340131 0.7938 270,007 347,495 275,853

2009 322488 0.7350 237,038 331,335 243,541

2010 295050 0.6806 200,806 315,293 214,583

2011 284254 0.6302 179,128 300,163 189,154

2012 284254 0.5835 165,859 284,686 166,112

2013 284254 0.5403 153,574 267,971 144,777

2014 284254 0.5002 142,198 249,919 125,022

2015 284254 0.4632 131,665 230,423 106,731

Totals: 3067143 2,093,674 3,067,143 2,125,927*Values Discounted at 8%

The capitalization of Bed Bath & Beyond’s operating leases is shown

above, and Linens-N-Things are shown in the table below. The discount rate,

8%, was found to be the home furnishings industry standard. This discount rate

seems to accurately reflect the industry and the type of debt. By discounting the

capital leases payments, we found that to get a more accurate look at Bed Bath

& Beyond they should actually record liabilities of 2.13 billion dollars. This would

also alter earnings and ratios previously computed. In order to receive debt

financing, many lenders will require that the firm remain below a certain level of

total liabilities in order to control risk. The revised financial statements

20

incorporating this change in liabilities are presented in the undo accounting

distortions section.

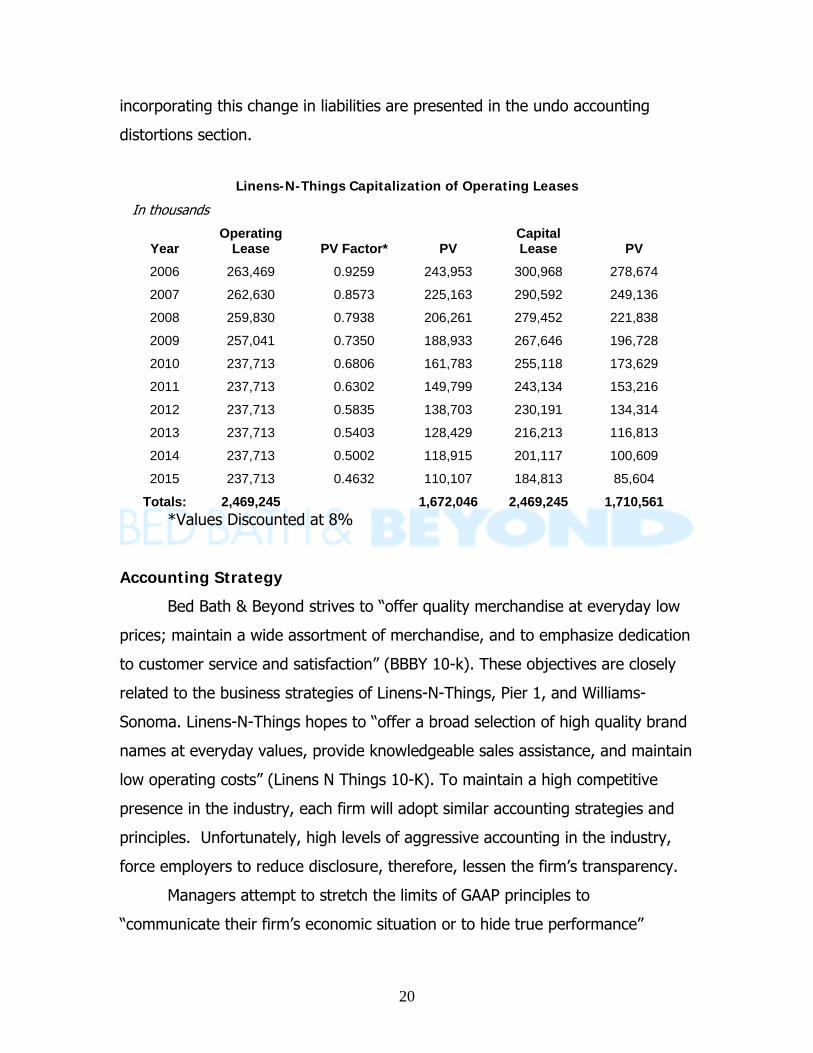

Linens-N-Things Capitalization of Operating Leases

In thousands

Year Operating

Lease PV Factor* PV Capital Lease PV

2006 263,469 0.9259 243,953 300,968 278,674

2007 262,630 0.8573 225,163 290,592 249,136

2008 259,830 0.7938 206,261 279,452 221,838

2009 257,041 0.7350 188,933 267,646 196,728

2010 237,713 0.6806 161,783 255,118 173,629

2011 237,713 0.6302 149,799 243,134 153,216

2012 237,713 0.5835 138,703 230,191 134,314

2013 237,713 0.5403 128,429 216,213 116,813

2014 237,713 0.5002 118,915 201,117 100,609

2015 237,713 0.4632 110,107 184,813 85,604

Totals: 2,469,245 1,672,046 2,469,245 1,710,561 *Values Discounted at 8%

Accounting Strategy

Bed Bath & Beyond strives to “offer quality merchandise at everyday low

prices; maintain a wide assortment of merchandise, and to emphasize dedication

to customer service and satisfaction” (BBBY 10-k). These objectives are closely

related to the business strategies of Linens-N-Things, Pier 1, and Williams-

Sonoma. Linens-N-Things hopes to “offer a broad selection of high quality brand

names at everyday values, provide knowledgeable sales assistance, and maintain

low operating costs” (Linens N Things 10-K). To maintain a high competitive

presence in the industry, each firm will adopt similar accounting strategies and

principles. Unfortunately, high levels of aggressive accounting in the industry,

force employers to reduce disclosure, therefore, lessen the firm’s transparency.

Managers attempt to stretch the limits of GAAP principles to

“communicate their firm’s economic situation or to hide true performance”

21

(Palepu 3-6). The use of operating leases in the industry provides off balance

sheet transactions that could easily go unnoticed by the average shareholder.

The home furnishings industry does not exhibit a great amount of

seasonality. However, there is a substantial increase in sales in the months of

August, November, and December (BBBY 10-k). This is why Bed Bath & Beyond

chooses their fiscal year to end on the last Saturday nearest February 28th. This

is a strategy they use in order to begin and end the accounting year in virtually

the same position, a month with a consistent level of sales from year to year.

Quality of Disclosure

Shareholders rely on the company’s 10-k to research information about

the firm, and to decide whether or not to invest in the company. The quality of

disclosure that a 10-k provides is of high importance. It can show the firm’s true

operations and value through financial statements, footnotes, and supplemental

disclosure. The quality of disclosure and transparency of the firm lie in the

managers’ hands of that company. This is because the managers have control

over what to disclose in their 10-k while following the guidelines of FASB, SEC

and GAAP.

In order to get a good idea of one company’s disclosure, one should

research the industry first. The home furnishings industry as a whole is very

aggressive when it comes to reporting the accounting. Aggressive accounting is

not always a good thing. Sometimes it can lead to inadequate disclosures to

make the company appear better financially. Also, overall the industry has an

extremely limited disclosure. The industry’s 10-ks are inadequate on the amount

of information disclosed, compared to companies in the technology and

manufacturing fields.

After having a general idea of the home furnishings industry, Bed Bath &

Beyond’s level of disclosure can be better understood when reviewing the 10-k.

Bed Bath & Beyond practices aggressive accounting along with their competitors;

and because of their large market share, they are often seen as being more

22

aggressive relative to other firms in the industry. When first looking at their 10-k,

one might think that the disclosure and information provided is efficient and

useful, but in reality it is not. The numbers represented in Bed Bath & Beyond’s

income statement, balance sheet, and statement of cash flows, are all extremely

vague. For example, there is no concise explanation of what makes up “other

assets” in the condensed balance sheet. It gives the basic points, but does not

go much deeper than surface level. There are many components on these

financial statements that are missing. An effective valuation of a firm is difficult

when the amount of information disclosed is limited.

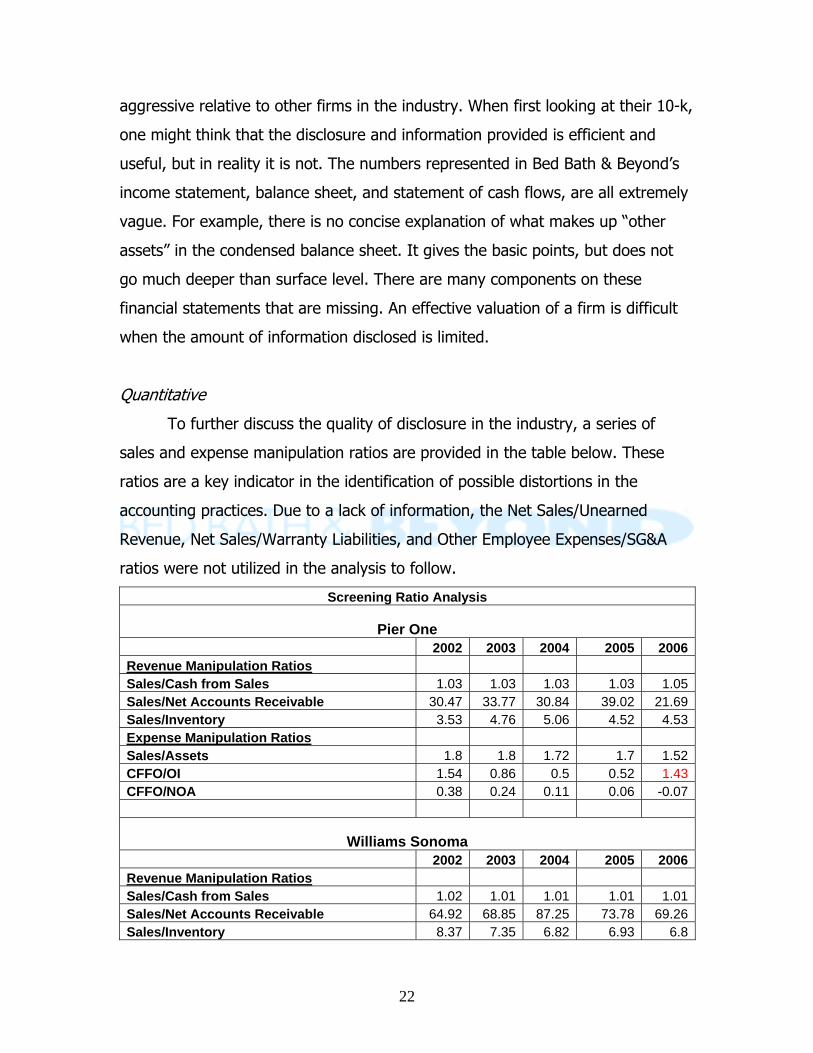

Quantitative

To further discuss the quality of disclosure in the industry, a series of

sales and expense manipulation ratios are provided in the table below. These

ratios are a key indicator in the identification of possible distortions in the

accounting practices. Due to a lack of information, the Net Sales/Unearned

Revenue, Net Sales/Warranty Liabilities, and Other Employee Expenses/SG&A

ratios were not utilized in the analysis to follow.

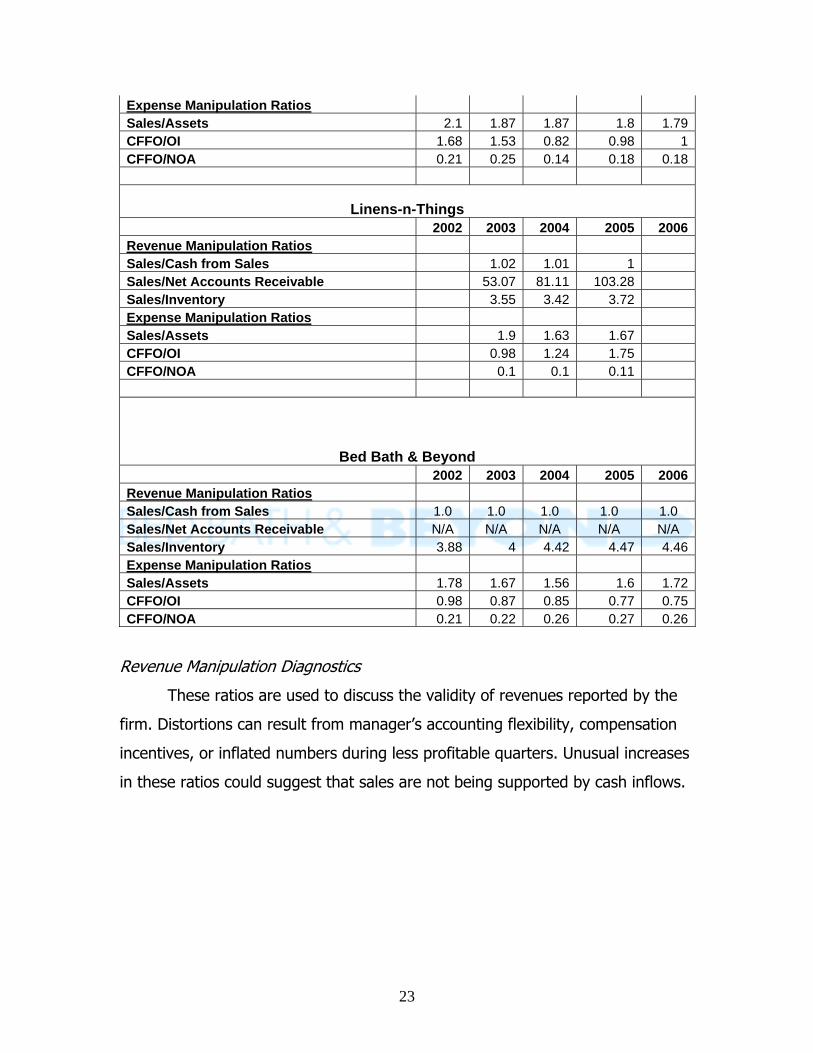

Screening Ratio Analysis

Pier One 2002 2003 2004 2005 2006Revenue Manipulation Ratios Sales/Cash from Sales 1.03 1.03 1.03 1.03 1.05Sales/Net Accounts Receivable 30.47 33.77 30.84 39.02 21.69Sales/Inventory 3.53 4.76 5.06 4.52 4.53Expense Manipulation Ratios Sales/Assets 1.8 1.8 1.72 1.7 1.52CFFO/OI 1.54 0.86 0.5 0.52 1.43CFFO/NOA 0.38 0.24 0.11 0.06 -0.07

Williams Sonoma 2002 2003 2004 2005 2006Revenue Manipulation Ratios Sales/Cash from Sales 1.02 1.01 1.01 1.01 1.01Sales/Net Accounts Receivable 64.92 68.85 87.25 73.78 69.26Sales/Inventory 8.37 7.35 6.82 6.93 6.8

23

Expense Manipulation Ratios Sales/Assets 2.1 1.87 1.87 1.8 1.79CFFO/OI 1.68 1.53 0.82 0.98 1CFFO/NOA 0.21 0.25 0.14 0.18 0.18

Linens-n-Things 2002 2003 2004 2005 2006Revenue Manipulation Ratios Sales/Cash from Sales 1.02 1.01 1 Sales/Net Accounts Receivable 53.07 81.11 103.28 Sales/Inventory 3.55 3.42 3.72 Expense Manipulation Ratios Sales/Assets 1.9 1.63 1.67 CFFO/OI 0.98 1.24 1.75 CFFO/NOA 0.1 0.1 0.11

Bed Bath & Beyond 2002 2003 2004 2005 2006Revenue Manipulation Ratios Sales/Cash from Sales 1.0 1.0 1.0 1.0 1.0 Sales/Net Accounts Receivable N/A N/A N/A N/A N/A Sales/Inventory 3.88 4 4.42 4.47 4.46Expense Manipulation Ratios Sales/Assets 1.78 1.67 1.56 1.6 1.72CFFO/OI 0.98 0.87 0.85 0.77 0.75CFFO/NOA 0.21 0.22 0.26 0.27 0.26

Revenue Manipulation Diagnostics

These ratios are used to discuss the validity of revenues reported by the

firm. Distortions can result from manager’s accounting flexibility, compensation

incentives, or inflated numbers during less profitable quarters. Unusual increases

in these ratios could suggest that sales are not being supported by cash inflows.

24

Sales/Cash From Sales

0.970.980.99

11.011.021.031.041.051.06

2002 2003 2004 2005 2006

Year

Out

put

Pier OneWilliams SonomaLinens-n-ThingsBed Bath & Beyond

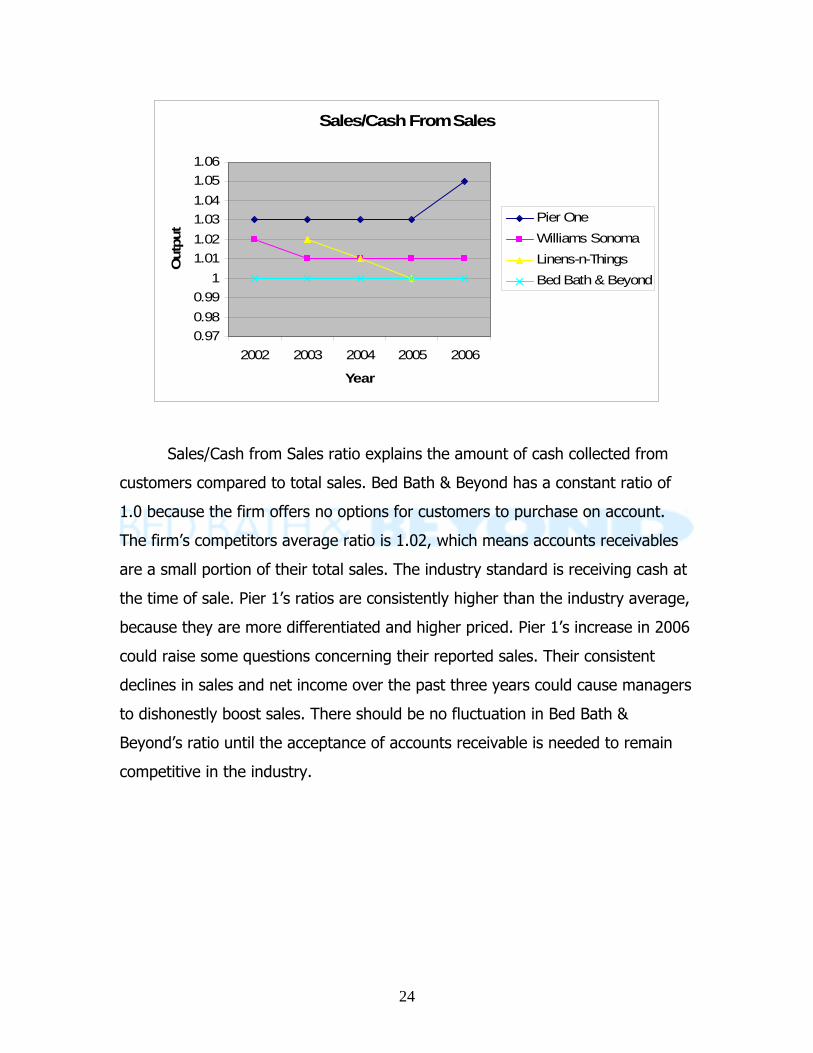

Sales/Cash from Sales ratio explains the amount of cash collected from

customers compared to total sales. Bed Bath & Beyond has a constant ratio of

1.0 because the firm offers no options for customers to purchase on account.

The firm’s competitors average ratio is 1.02, which means accounts receivables

are a small portion of their total sales. The industry standard is receiving cash at

the time of sale. Pier 1’s ratios are consistently higher than the industry average,

because they are more differentiated and higher priced. Pier 1’s increase in 2006

could raise some questions concerning their reported sales. Their consistent

declines in sales and net income over the past three years could cause managers

to dishonestly boost sales. There should be no fluctuation in Bed Bath &

Beyond’s ratio until the acceptance of accounts receivable is needed to remain

competitive in the industry.

25

Sales/Net Accounts Receivables

0

20

40

60

80

100

120

2002 2003 2004 2005 2006Year

Out

put

Pier OneWilliams SonomaLinens-n-ThingsBed Bath & Beyond

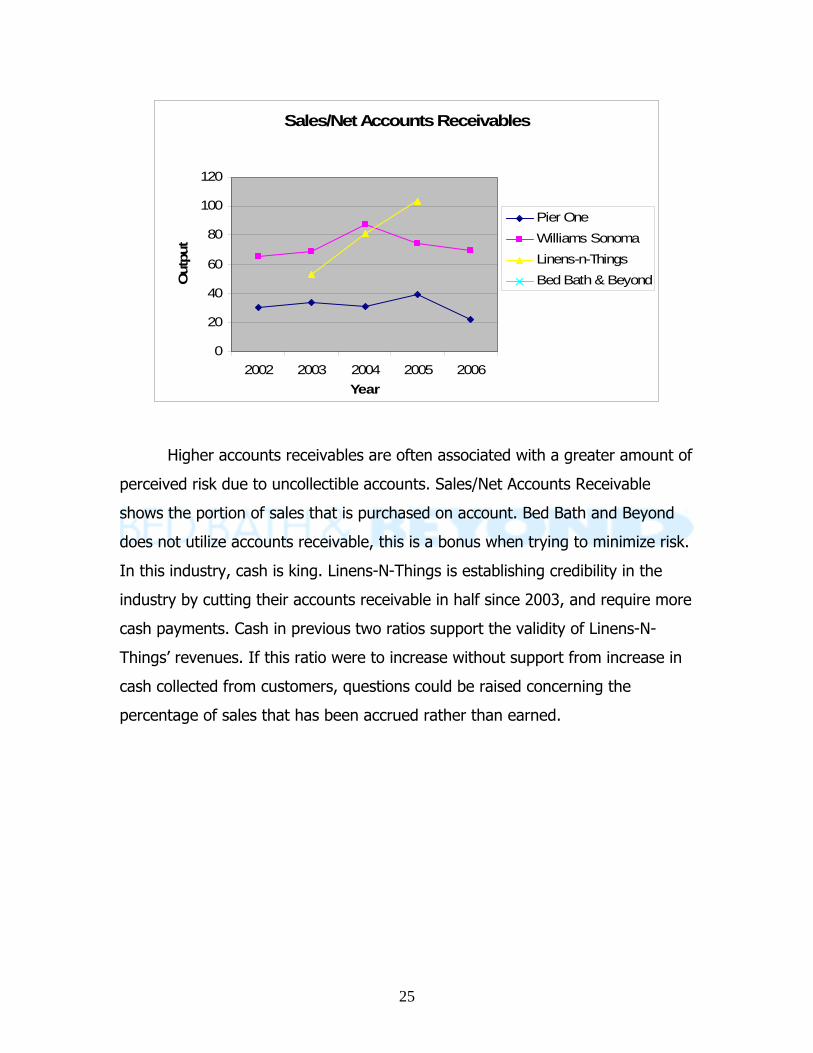

Higher accounts receivables are often associated with a greater amount of

perceived risk due to uncollectible accounts. Sales/Net Accounts Receivable

shows the portion of sales that is purchased on account. Bed Bath and Beyond

does not utilize accounts receivable, this is a bonus when trying to minimize risk.

In this industry, cash is king. Linens-N-Things is establishing credibility in the

industry by cutting their accounts receivable in half since 2003, and require more

cash payments. Cash in previous two ratios support the validity of Linens-N-

Things’ revenues. If this ratio were to increase without support from increase in

cash collected from customers, questions could be raised concerning the

percentage of sales that has been accrued rather than earned.

26

Sales/Inventory

0123456789

2002 2003 2004 2005 2006

Year

Out

put

Pier OneWilliams SonomaLinens-n-ThingsBed Bath & Beyond

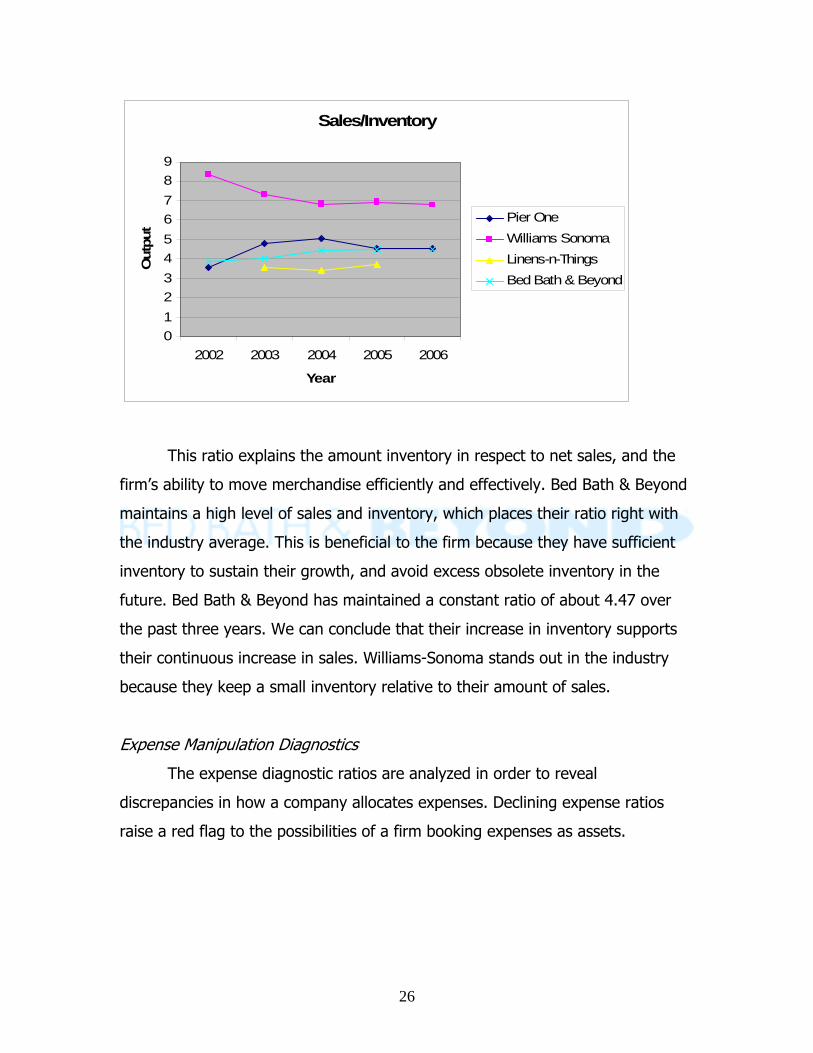

This ratio explains the amount inventory in respect to net sales, and the

firm’s ability to move merchandise efficiently and effectively. Bed Bath & Beyond

maintains a high level of sales and inventory, which places their ratio right with

the industry average. This is beneficial to the firm because they have sufficient

inventory to sustain their growth, and avoid excess obsolete inventory in the

future. Bed Bath & Beyond has maintained a constant ratio of about 4.47 over

the past three years. We can conclude that their increase in inventory supports

their continuous increase in sales. Williams-Sonoma stands out in the industry

because they keep a small inventory relative to their amount of sales.

Expense Manipulation Diagnostics

The expense diagnostic ratios are analyzed in order to reveal

discrepancies in how a company allocates expenses. Declining expense ratios

raise a red flag to the possibilities of a firm booking expenses as assets.

27

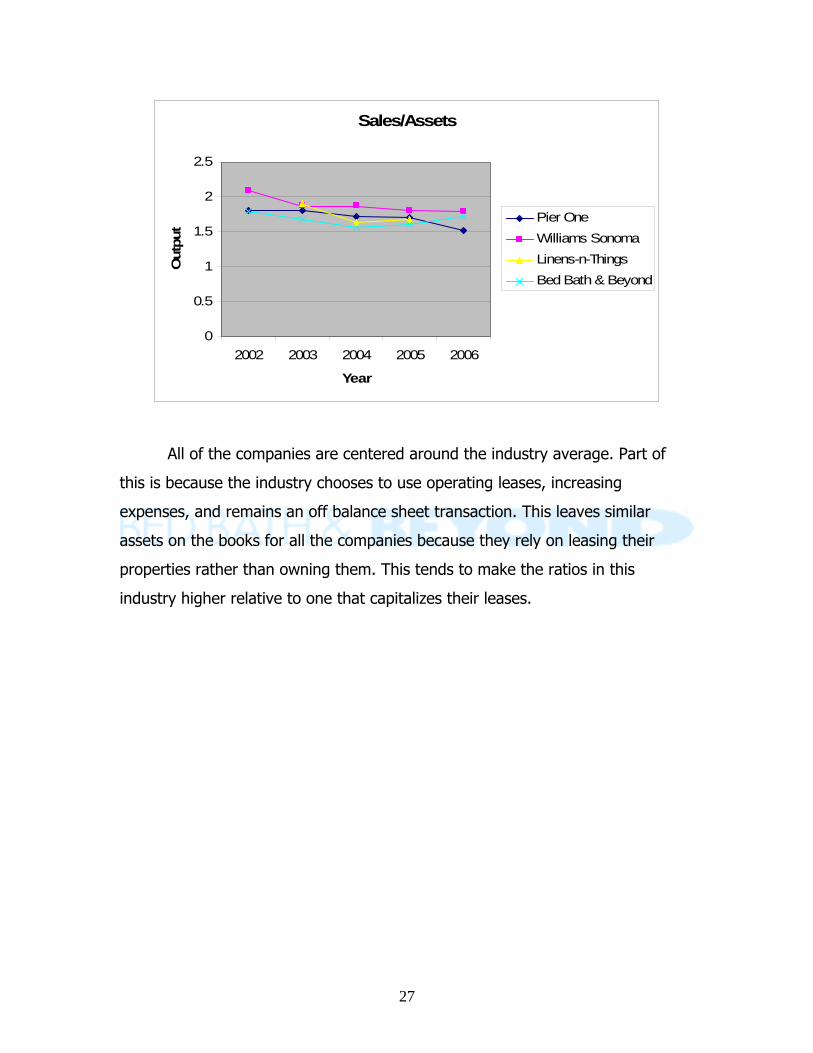

Sales/Assets

0

0.5

1

1.5

2

2.5

2002 2003 2004 2005 2006

Year

Out

put

Pier OneWilliams SonomaLinens-n-ThingsBed Bath & Beyond

All of the companies are centered around the industry average. Part of

this is because the industry chooses to use operating leases, increasing

expenses, and remains an off balance sheet transaction. This leaves similar

assets on the books for all the companies because they rely on leasing their

properties rather than owning them. This tends to make the ratios in this

industry higher relative to one that capitalizes their leases.

28

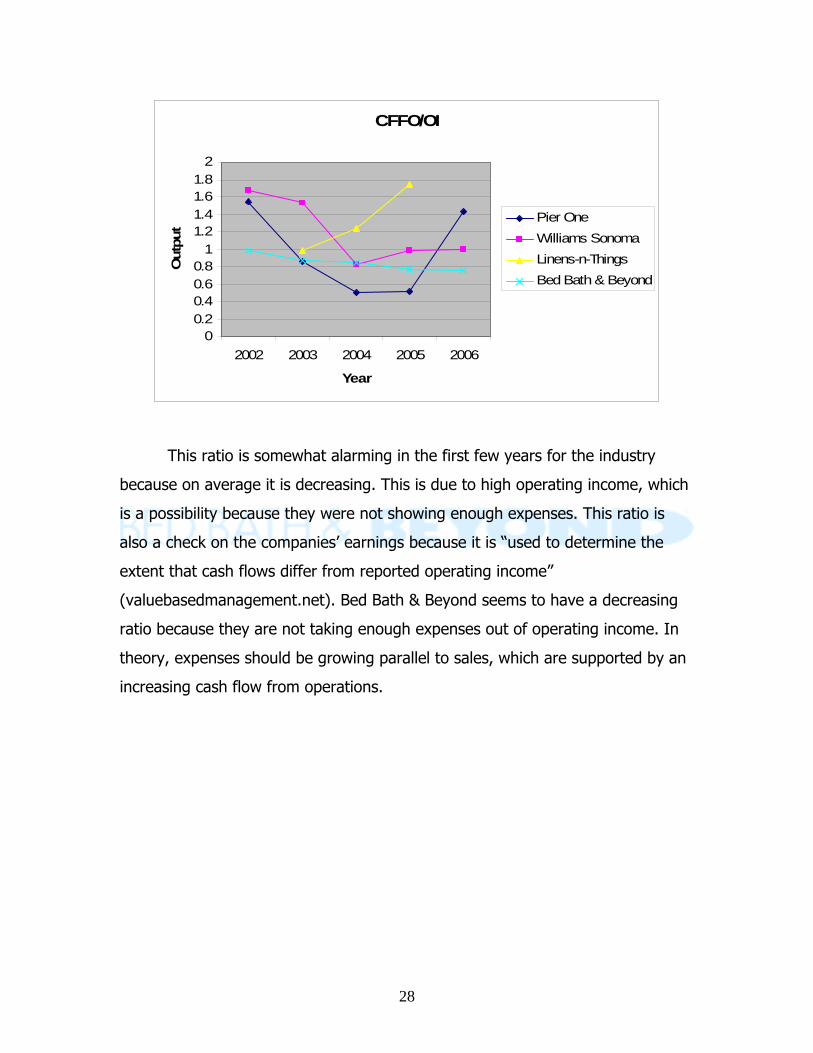

CFFO/OI

00.20.40.60.8

11.21.41.61.8

2

2002 2003 2004 2005 2006

Year

Out

put

Pier OneWilliams SonomaLinens-n-ThingsBed Bath & Beyond

This ratio is somewhat alarming in the first few years for the industry

because on average it is decreasing. This is due to high operating income, which

is a possibility because they were not showing enough expenses. This ratio is

also a check on the companies’ earnings because it is “used to determine the

extent that cash flows differ from reported operating income”

(valuebasedmanagement.net). Bed Bath & Beyond seems to have a decreasing

ratio because they are not taking enough expenses out of operating income. In

theory, expenses should be growing parallel to sales, which are supported by an

increasing cash flow from operations.

29

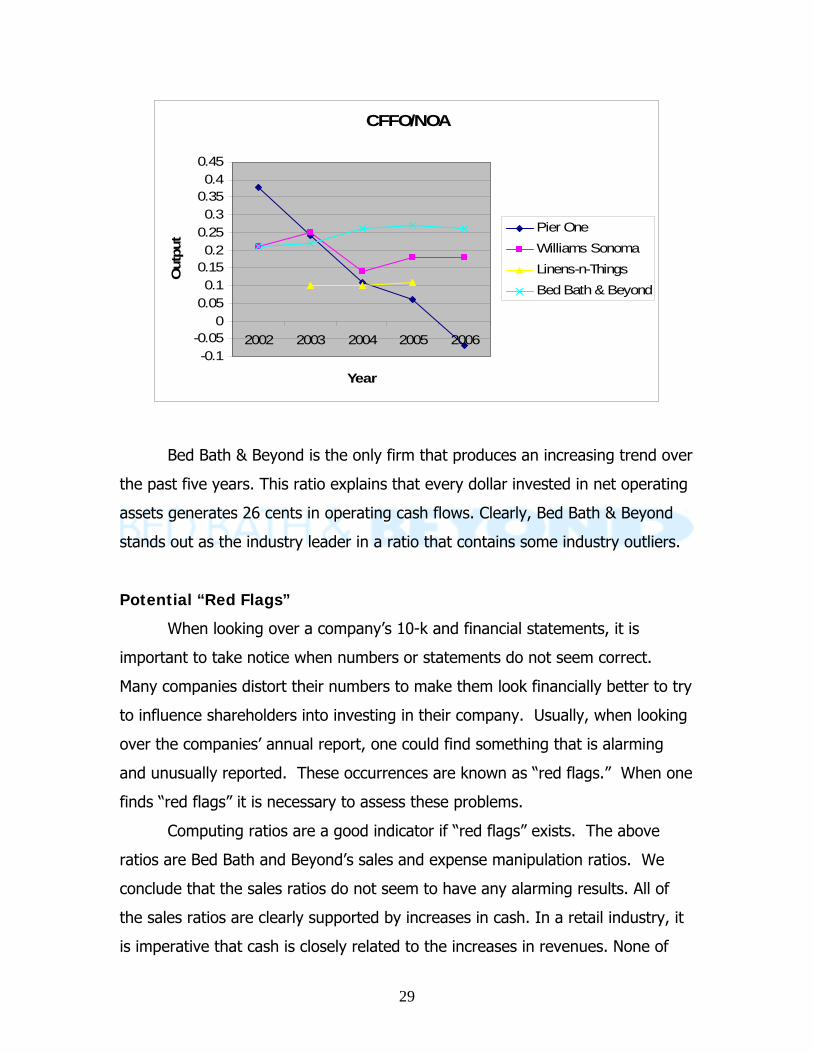

CFFO/NOA

-0.1-0.05

00.050.1

0.150.2

0.250.3

0.350.4

0.45

2002 2003 2004 2005 2006

Year

Out

put

Pier OneWilliams SonomaLinens-n-ThingsBed Bath & Beyond

Bed Bath & Beyond is the only firm that produces an increasing trend over

the past five years. This ratio explains that every dollar invested in net operating

assets generates 26 cents in operating cash flows. Clearly, Bed Bath & Beyond

stands out as the industry leader in a ratio that contains some industry outliers.

Potential “Red Flags”

When looking over a company’s 10-k and financial statements, it is

important to take notice when numbers or statements do not seem correct.

Many companies distort their numbers to make them look financially better to try

to influence shareholders into investing in their company. Usually, when looking

over the companies’ annual report, one could find something that is alarming

and unusually reported. These occurrences are known as “red flags.” When one

finds “red flags” it is necessary to assess these problems.

Computing ratios are a good indicator if “red flags” exists. The above

ratios are Bed Bath and Beyond’s sales and expense manipulation ratios. We

conclude that the sales ratios do not seem to have any alarming results. All of

the sales ratios are clearly supported by increases in cash. In a retail industry, it

is imperative that cash is closely related to the increases in revenues. None of

30

the expense ratios seem to be decreasing in value with the exception of

CFFO/OI. This could raise concerns that expenses are not being recorded

accurately or correctly allocated with the growing revenues.

Another area for concern with the corporation’s accounting strategy is

their strict use of operating leases. At the end of 2005 Bed Bath & Beyond had a

total of around $3.1 billion dollars in current and future obligations, all of which

registered under operating lease agreements. According to their 10-k, offices,

warehouses, manufacturing facilities, and equipment are all capital items that are

being expensed as a part of an operating lease rather than being capitalized and

recorded in the corporation’s financial statements.

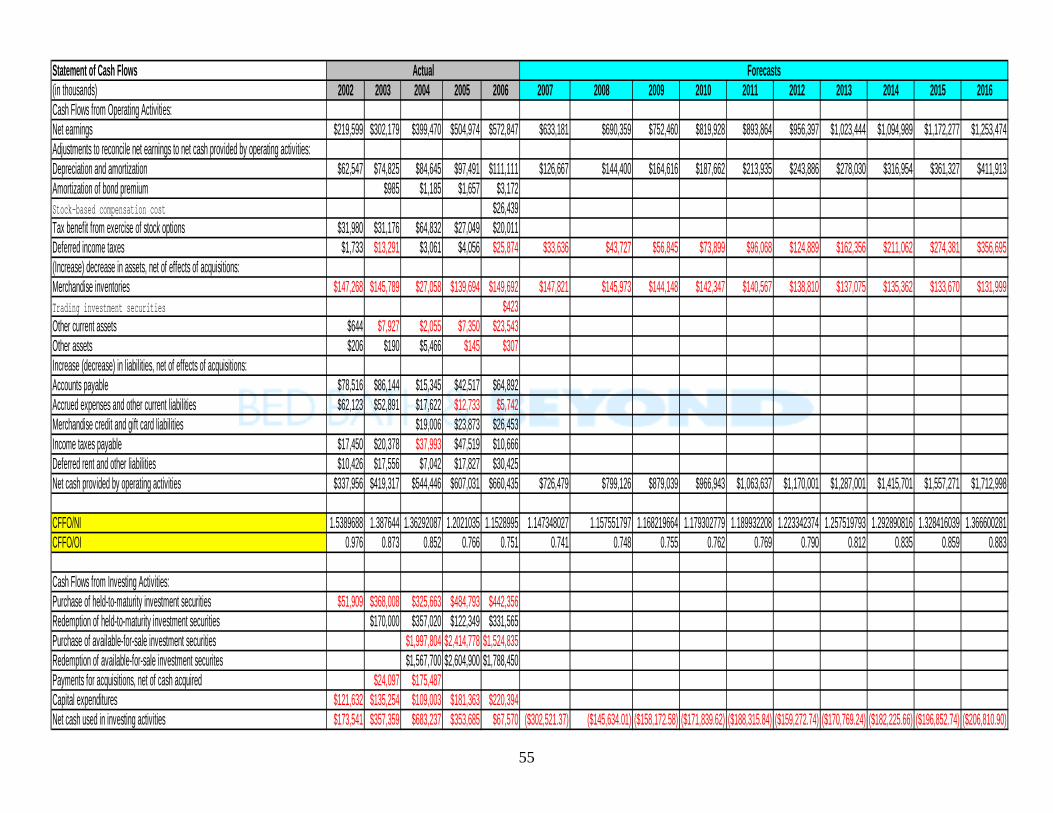

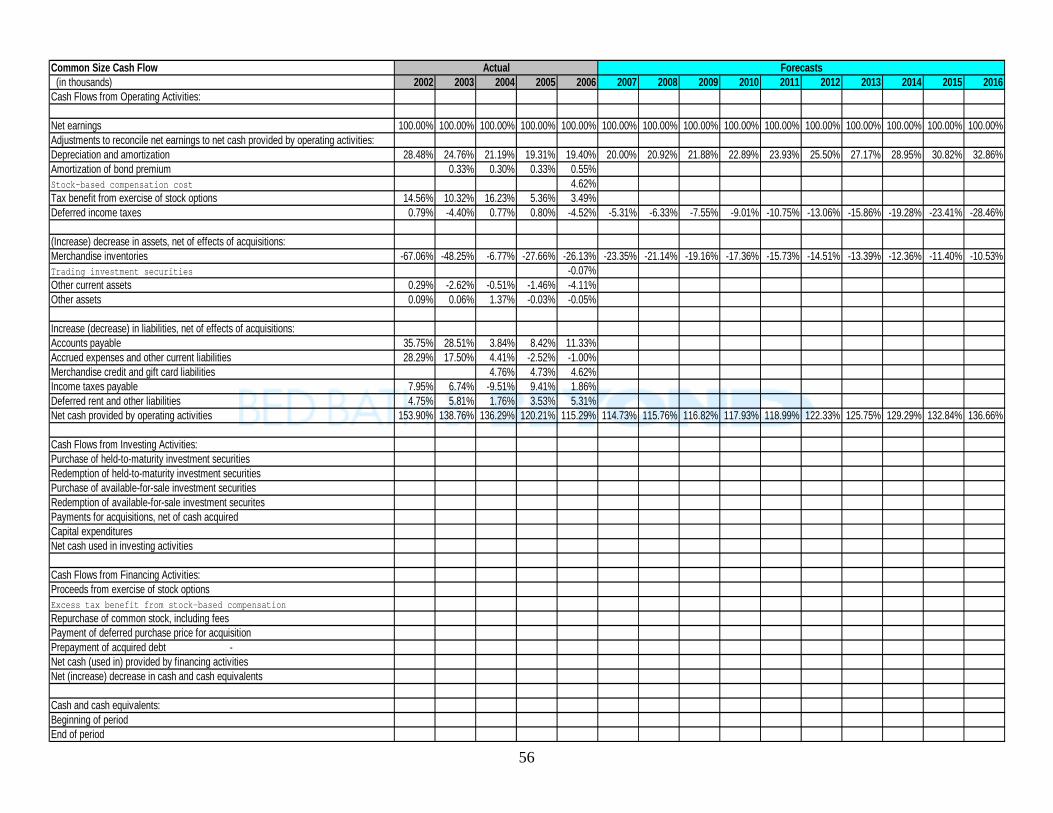

Undo Accounting Distortions

As mentioned in the accounting flexibility section as well as the red flags

section, Bed Bath & Beyond chose not use any capital leases. For comparison

purposes, we converted their operating leases over to capital leases, and

discounted the payments by 8% to find the present value. After discounting the

payments, we concluded that Bed Bath & Beyond should add about $2.13 billion

dollars to their value of long term liabilities, increasing the value from $1.12

billion to approximately $3 billion. Therefore, the current values of long term

liabilities are extremely understated. The financial statements reflecting this

increase in liabilities are included in the forecasting section that follows.

31

Ratio Analysis & Forecast Financials

Ratio Analysis

Profitability and growth are two key components in the valuation of a firm.

Ratio analysis offers a measure of financial performance and efficiency

management for a firm. After the ratios are reviewed, they can be utilized in

forecasting the financial statements. The critical analysis of these two measures

can help us better understand historically where the firm has been, and where

speculated trends will lead the firm in the future. Financial ratio analysis can be

categorized into liquidity, profitability, and capital structure analysis. The

relationships explained in the analysis of the financial statements will compare

Bed Bath & Beyond’s position to competitors in the home furnishing industry, as

well as, the firm’s past performance.

Trend and Cross Sectional Analysis

Once the ratios have been computed for the past five years, their results

are analyzed for any emerging trends. The trends are then used to logically

forecast various aspects of the firm’s financial statements. Since trends are

speculated, the firm’s future performance will be subject to the one that defines

the trends. A cross-sectional analysis is one that “facilitates examining the

relative performance of a firm within its industry, holding industry-level factors

constant” (Palepu 5-1). Bed Bath & Beyond’s performance will be compared to

other competitors in the industry to observe how established the firm is in the

industry.

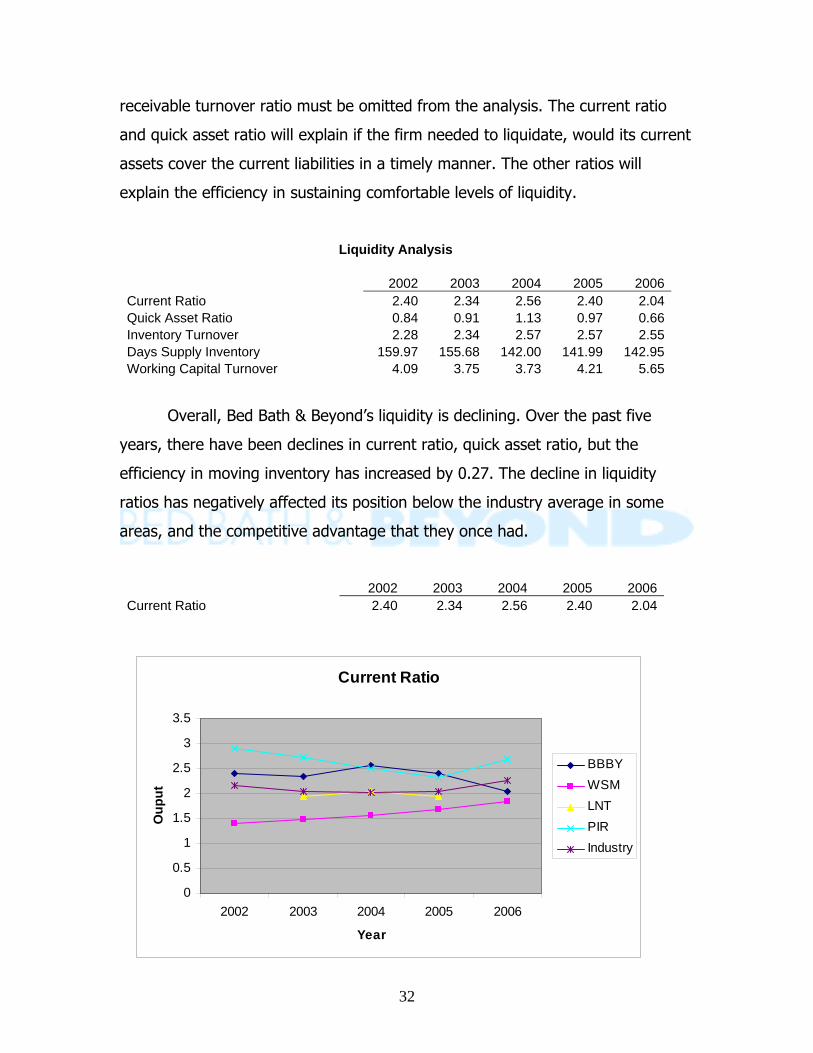

Liquidity Ratios

Liquidity Ratios provide valuable insight on Bed Bath & Beyond’s ability to

meet its short-term liabilities. The ratios used in this analysis are the current

ratio, quick asset ratio, inventory turnover, and working capital turnover. Bed

Bath & Beyond does not have any accounts receivables, so the accounts

32

Current Ratio

0

0.5

1

1.5

2

2.5

3

3.5

2002 2003 2004 2005 2006

Year

Oup

ut

BBBYWSMLNTPIRIndustry

receivable turnover ratio must be omitted from the analysis. The current ratio

and quick asset ratio will explain if the firm needed to liquidate, would its current

assets cover the current liabilities in a timely manner. The other ratios will

explain the efficiency in sustaining comfortable levels of liquidity.

Liquidity Analysis

2002 2003 2004 2005 2006Current Ratio 2.40 2.34 2.56 2.40 2.04Quick Asset Ratio 0.84 0.91 1.13 0.97 0.66Inventory Turnover 2.28 2.34 2.57 2.57 2.55Days Supply Inventory 159.97 155.68 142.00 141.99 142.95Working Capital Turnover 4.09 3.75 3.73 4.21 5.65

Overall, Bed Bath & Beyond’s liquidity is declining. Over the past five

years, there have been declines in current ratio, quick asset ratio, but the

efficiency in moving inventory has increased by 0.27. The decline in liquidity

ratios has negatively affected its position below the industry average in some

areas, and the competitive advantage that they once had.

2002 2003 2004 2005 2006Current Ratio 2.40 2.34 2.56 2.40 2.04

33

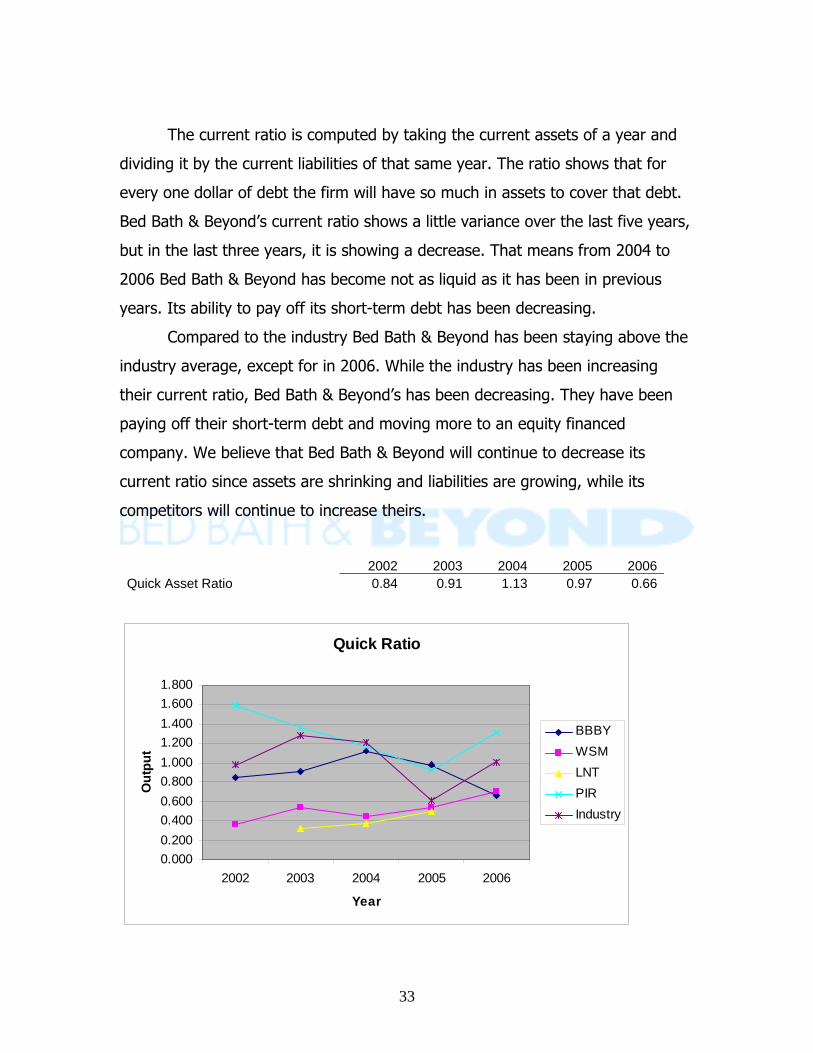

The current ratio is computed by taking the current assets of a year and

dividing it by the current liabilities of that same year. The ratio shows that for

every one dollar of debt the firm will have so much in assets to cover that debt.

Bed Bath & Beyond’s current ratio shows a little variance over the last five years,

but in the last three years, it is showing a decrease. That means from 2004 to

2006 Bed Bath & Beyond has become not as liquid as it has been in previous

years. Its ability to pay off its short-term debt has been decreasing.

Compared to the industry Bed Bath & Beyond has been staying above the

industry average, except for in 2006. While the industry has been increasing

their current ratio, Bed Bath & Beyond’s has been decreasing. They have been

paying off their short-term debt and moving more to an equity financed

company. We believe that Bed Bath & Beyond will continue to decrease its

current ratio since assets are shrinking and liabilities are growing, while its

competitors will continue to increase theirs.

2002 2003 2004 2005 2006Quick Asset Ratio 0.84 0.91 1.13 0.97 0.66

Quick Ratio

0.0000.2000.4000.6000.8001.0001.2001.4001.6001.800

2002 2003 2004 2005 2006

Year

Out

put

BBBYWSMLNTPIRIndustry

34

To compute the quick asset ratio an analyst takes the companies quick

assets and dividing them by current liabilities. A company’s quick assets are

those that are turned into cash when needed. These include cash, securities, and

accounts receivables. The quick asset ratio shows how fast a company can

convert its immediate cash to pay off short-term debt. This ratio will tell us that

for every dollar of current liabilities there is $0.66 of quick assets to cover that

debt.

From 2002 to 2004 Bed Bath & Beyond increased its quick asset ratio

considerably from $0.84 to $1.13. That tells us in those years they were more

quick assets supplied for every dollar of current liabilities. From 2004 to 2006

Bed Bath & Beyond’s quick asset ratio began to decrease because current

liabilities were increasing while quick assets stayed relatively steady. This shows

that company has been losing its liquidity over the last 3 years.

Bed Bath & Beyond was keeping its quick asset ratio close to most of its

competitors, but since 2004 they have been increasing their quick assets while

Bed Bath & Beyond has been decreasing theirs. They are now well below the

industry average for quick assets and the decrease over the last few years leads

us to believe that they will continue to decrease quick assets and increase

current liabilities.

35

2002 2003 2004 2005 2006Inventory Turnover 2.28 2.34 2.57 2.57 2.55Days Supply Inventory 159.97 155.68 142.00 141.99 142.95

Inventory Turnover

0.000

1.000

2.000

3.000

4.000

5.000

6.000

2002 2003 2004 2005 2006

Year

Out

put

BBBYWSMLNTPIRIndustry

Inventory turnover is calculated by taking the firm’s cost of goods sold

and dividing them by their current inventory supply. A firm in this industry would

like this number to be relatively high. A higher inventory turnover means that the

firm gets more inventories out of the store or warehouse to make room for new

inventory.

Bed Bath & Beyond’s inventory increased from 2.28 in 2002 to 2.57 in

2004. In 2005, the inventory turnover stayed the same and in 2006, it shows a

slight decrease. In the last three years, the inventory turnover has not moved

very much, which shows that as they increase their inventory supply their cost of

goods sold are increasing as well. It seems as though the overall trend is that

inventory turnover is increasing and that is good for Bed Bath & Beyond. As long

as this number grows, Bed Bath & Beyond will be able to get rid of more

inventory to make room for newer goods.

Day’s supply of inventory is computed by taking the number of days in the

year and dividing it by the inventory turnover ratio. This will tell you how many

36

days it takes a firm to sell its inventory. Bed Bath & Beyond has been decreasing

their days supply of inventory which is favorable to them. They are keeping

products on the shelves fewer days each year. From 2002 to 2006, they have

dropped their supply of inventory by more than Two weeks. That tells us

consumers are buying more of their products every year, which makes space for

newer inventory to be kept on hand.

Compared to the industry average Bed Bath & Beyond has been keeping a

slow pace with the rest of their competitors. That shows that they are moving

with the industry. While many of its competitors are increasing their days supply

of inventory Bed Bath & Beyond is not. Many of its competitors are keeping

products on hand a few days longer each year compared to their last year, while

Bed Bath & Beyond has been decreasing theirs at a slow pace. We believe that

this shows Bed Bath & Beyond has favorable improvements over its competitors

when it comes to inventory supply.

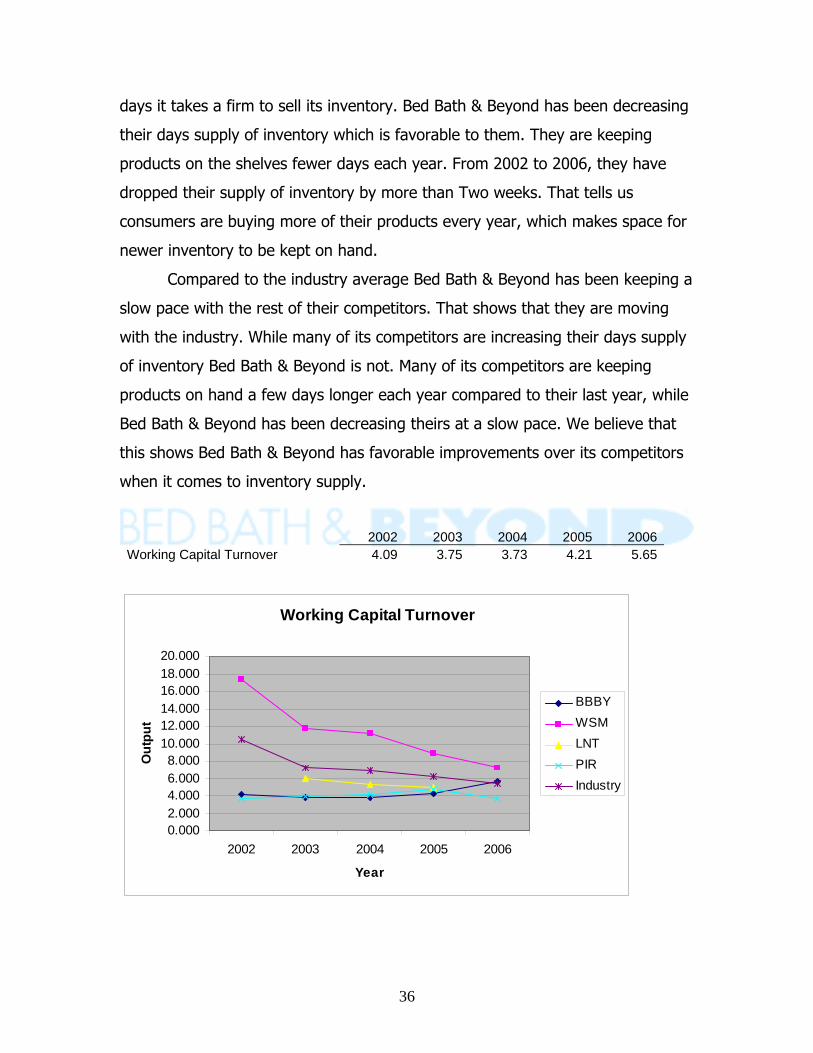

2002 2003 2004 2005 2006Working Capital Turnover 4.09 3.75 3.73 4.21 5.65

Working Capital Turnover

0.0002.0004.0006.0008.000

10.00012.00014.00016.00018.00020.000

2002 2003 2004 2005 2006

Year

Out

put

BBBYWSMLNTPIRIndustry

37

Computing working capital turnover is done by taking the company’s sales

and dividing it by its working capital. Working capital is current assets minus

current liabilities. This ratio shows how a firm uses its working capital to

generate sales. Companies want high working capital turnover because that

means their sales are increasing.

From 2002 to 2005, Bed Bath & Beyond’s working capital turnover stayed

relatively constant with not much movement, but in 2006, it jumped almost 1.5

points. That tells us that sales in 2006 increased while working capital decreased.

The industry has been showing a decline in working capital while Bed Bath

& Beyond has started to show an increase. Even though Bed Bath & Beyond has

been increasing they are only at the industry average and not above all of their

competitors.

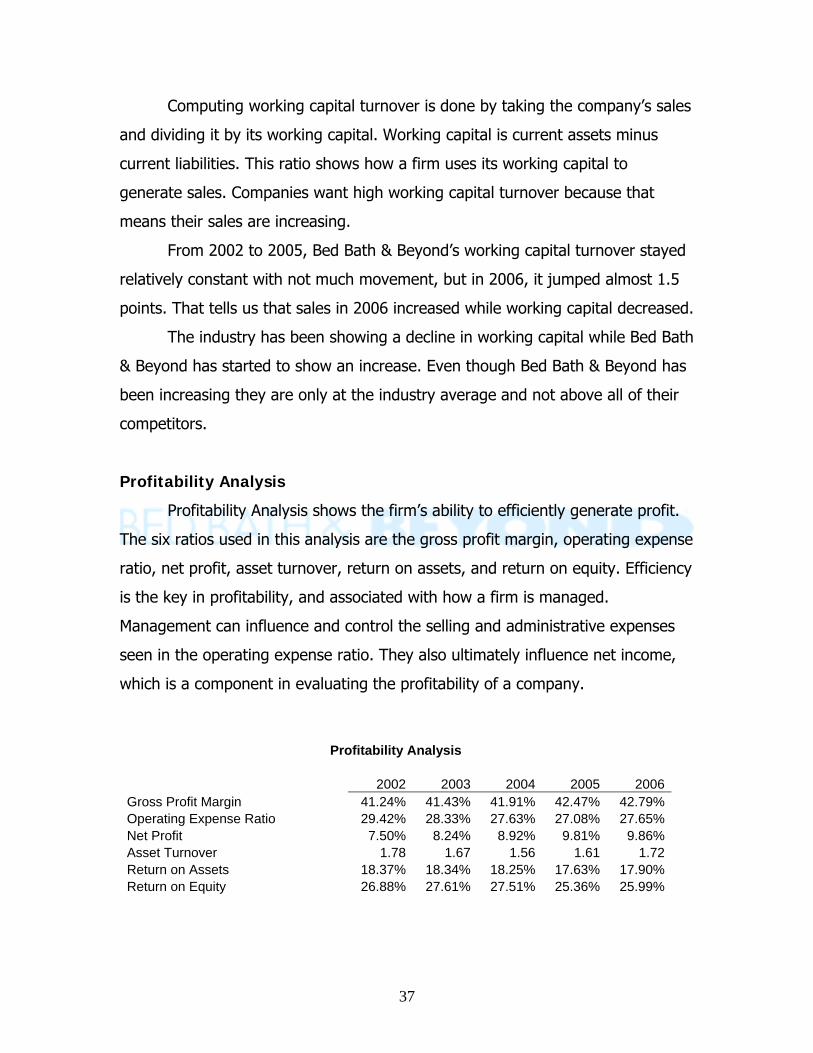

Profitability Analysis

Profitability Analysis shows the firm’s ability to efficiently generate profit.

The six ratios used in this analysis are the gross profit margin, operating expense

ratio, net profit, asset turnover, return on assets, and return on equity. Efficiency

is the key in profitability, and associated with how a firm is managed.

Management can influence and control the selling and administrative expenses

seen in the operating expense ratio. They also ultimately influence net income,

which is a component in evaluating the profitability of a company.

Profitability Analysis 2002 2003 2004 2005 2006

Gross Profit Margin 41.24% 41.43% 41.91% 42.47% 42.79%Operating Expense Ratio 29.42% 28.33% 27.63% 27.08% 27.65%Net Profit 7.50% 8.24% 8.92% 9.81% 9.86%Asset Turnover 1.78 1.67 1.56 1.61 1.72Return on Assets 18.37% 18.34% 18.25% 17.63% 17.90%Return on Equity 26.88% 27.61% 27.51% 25.36% 25.99%

38

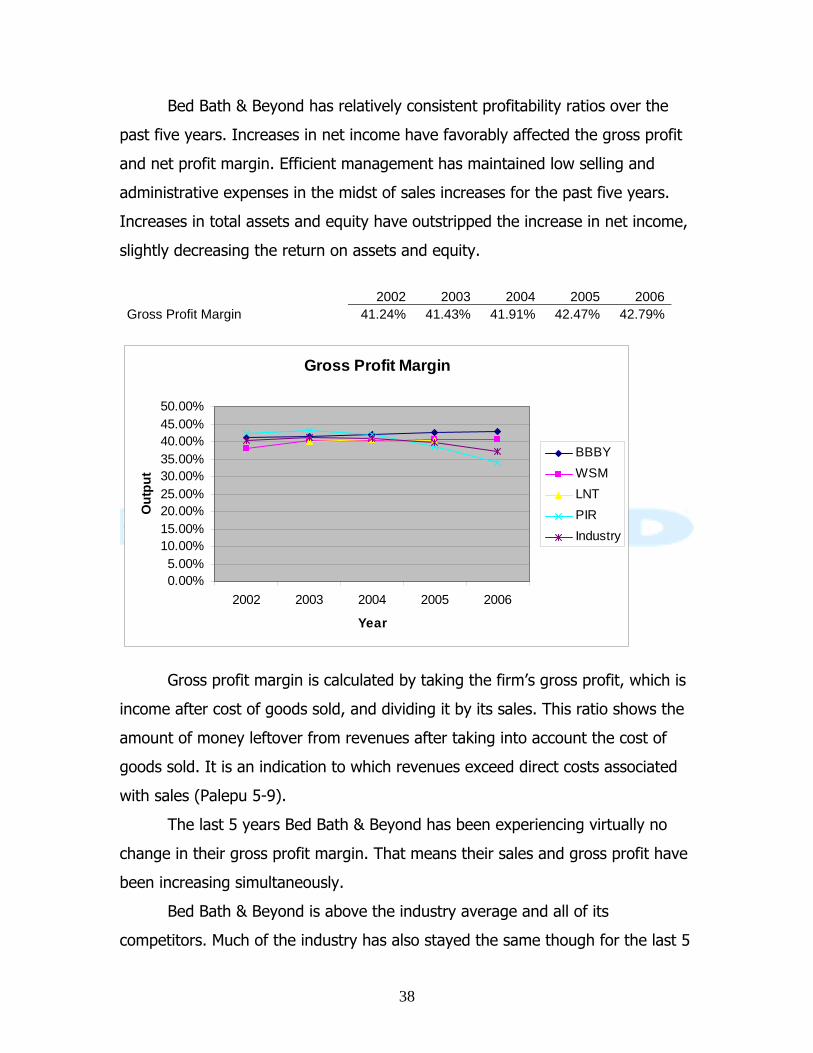

Bed Bath & Beyond has relatively consistent profitability ratios over the

past five years. Increases in net income have favorably affected the gross profit

and net profit margin. Efficient management has maintained low selling and

administrative expenses in the midst of sales increases for the past five years.

Increases in total assets and equity have outstripped the increase in net income,

slightly decreasing the return on assets and equity.

2002 2003 2004 2005 2006

Gross Profit Margin 41.24% 41.43% 41.91% 42.47% 42.79%

Gross Profit Margin

0.00%5.00%

10.00%15.00%20.00%25.00%30.00%35.00%40.00%45.00%50.00%

2002 2003 2004 2005 2006

Year

Out

put

BBBYWSMLNTPIRIndustry

Gross profit margin is calculated by taking the firm’s gross profit, which is

income after cost of goods sold, and dividing it by its sales. This ratio shows the

amount of money leftover from revenues after taking into account the cost of

goods sold. It is an indication to which revenues exceed direct costs associated

with sales (Palepu 5-9).

The last 5 years Bed Bath & Beyond has been experiencing virtually no

change in their gross profit margin. That means their sales and gross profit have

been increasing simultaneously.

Bed Bath & Beyond is above the industry average and all of its

competitors. Much of the industry has also stayed the same though for the last 5

39

years as well. Many of the competitors are experiencing the same growth in

sales and gross profit as Bed Bath & Beyond.

2002 2003 2004 2005 2006

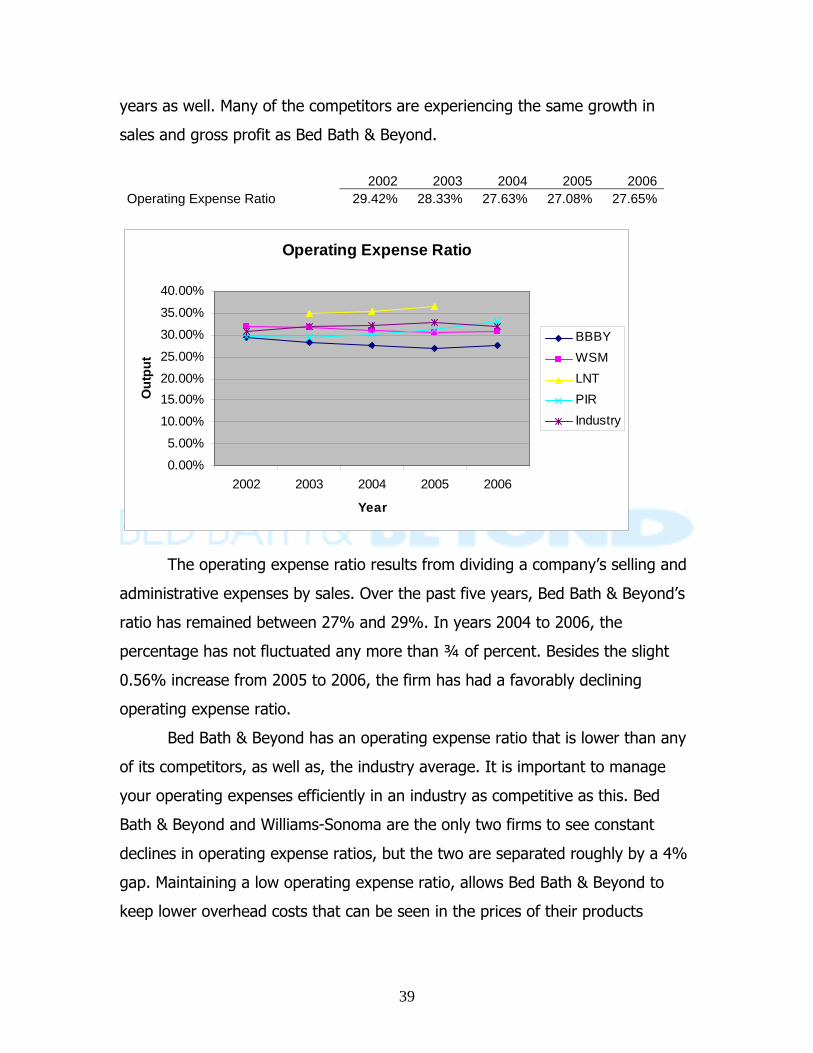

Operating Expense Ratio 29.42% 28.33% 27.63% 27.08% 27.65%

Operating Expense Ratio

0.00%

5.00%

10.00%

15.00%20.00%

25.00%

30.00%

35.00%

40.00%

2002 2003 2004 2005 2006

Year

Out

put

BBBYWSMLNTPIRIndustry

The operating expense ratio results from dividing a company’s selling and

administrative expenses by sales. Over the past five years, Bed Bath & Beyond’s

ratio has remained between 27% and 29%. In years 2004 to 2006, the

percentage has not fluctuated any more than ¾ of percent. Besides the slight

0.56% increase from 2005 to 2006, the firm has had a favorably declining

operating expense ratio.

Bed Bath & Beyond has an operating expense ratio that is lower than any

of its competitors, as well as, the industry average. It is important to manage

your operating expenses efficiently in an industry as competitive as this. Bed

Bath & Beyond and Williams-Sonoma are the only two firms to see constant

declines in operating expense ratios, but the two are separated roughly by a 4%

gap. Maintaining a low operating expense ratio, allows Bed Bath & Beyond to

keep lower overhead costs that can be seen in the prices of their products

40

relative to the industry. The firm possesses the ability to increase sales without

seeing a drastic change in selling and administrative expenses.

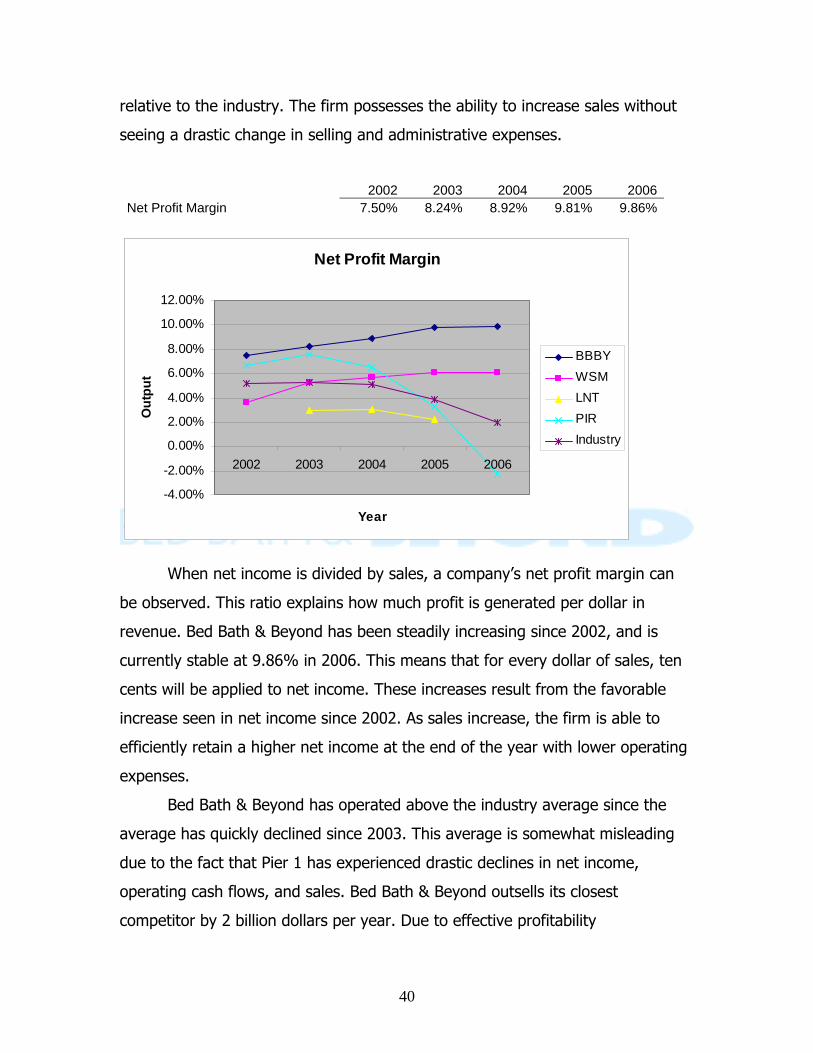

2002 2003 2004 2005 2006Net Profit Margin 7.50% 8.24% 8.92% 9.81% 9.86%

Net Profit Margin

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

2002 2003 2004 2005 2006

Year

Out

put

BBBYWSMLNTPIRIndustry

When net income is divided by sales, a company’s net profit margin can

be observed. This ratio explains how much profit is generated per dollar in

revenue. Bed Bath & Beyond has been steadily increasing since 2002, and is

currently stable at 9.86% in 2006. This means that for every dollar of sales, ten

cents will be applied to net income. These increases result from the favorable

increase seen in net income since 2002. As sales increase, the firm is able to

efficiently retain a higher net income at the end of the year with lower operating

expenses.

Bed Bath & Beyond has operated above the industry average since the

average has quickly declined since 2003. This average is somewhat misleading

due to the fact that Pier 1 has experienced drastic declines in net income,

operating cash flows, and sales. Bed Bath & Beyond outsells its closest

competitor by 2 billion dollars per year. Due to effective profitability

41

management, the firm’s sheer sales volume will bring a greater net profit margin

than the industry.

2002 2003 2004 2005 2006

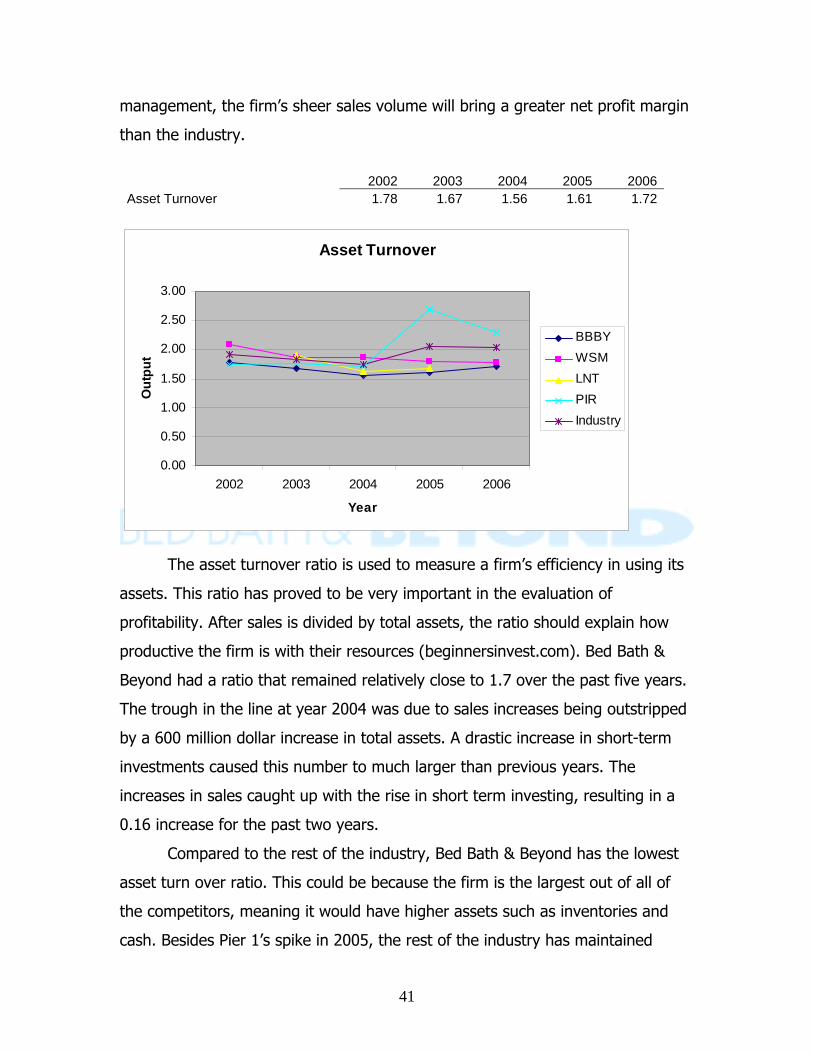

Asset Turnover 1.78 1.67 1.56 1.61 1.72

Asset Turnover

0.00

0.50

1.00

1.50

2.00

2.50

3.00

2002 2003 2004 2005 2006

Year

Out

put

BBBYWSMLNTPIRIndustry

The asset turnover ratio is used to measure a firm’s efficiency in using its

assets. This ratio has proved to be very important in the evaluation of

profitability. After sales is divided by total assets, the ratio should explain how

productive the firm is with their resources (beginnersinvest.com). Bed Bath &

Beyond had a ratio that remained relatively close to 1.7 over the past five years.

The trough in the line at year 2004 was due to sales increases being outstripped

by a 600 million dollar increase in total assets. A drastic increase in short-term

investments caused this number to much larger than previous years. The

increases in sales caught up with the rise in short term investing, resulting in a

0.16 increase for the past two years.

Compared to the rest of the industry, Bed Bath & Beyond has the lowest

asset turn over ratio. This could be because the firm is the largest out of all of

the competitors, meaning it would have higher assets such as inventories and

cash. Besides Pier 1’s spike in 2005, the rest of the industry has maintained

42

relatively consistent asset turnover ratios. Williams-Sonoma surpasses Bed Bath

& Beyond, as well as, the rest of the industry because its sales are primarily mail

order. This allows Williams-Sonoma to keep lower inventories on hand,

maintaining high levels of efficiency.

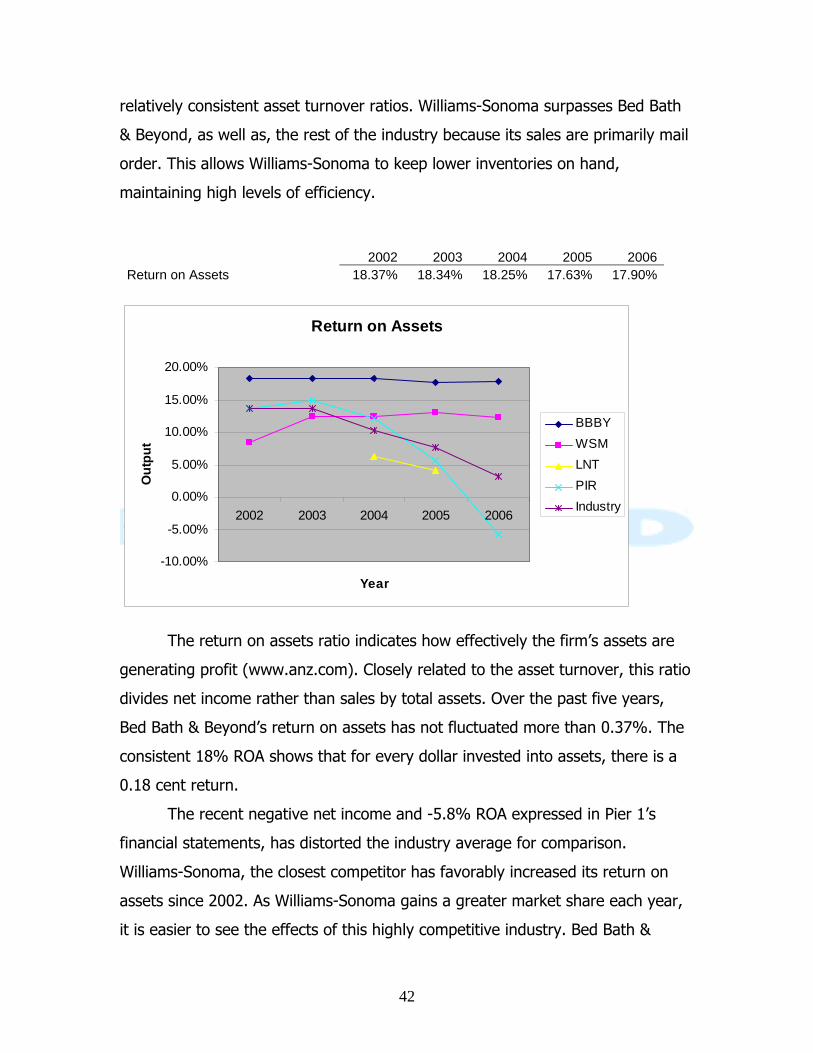

2002 2003 2004 2005 2006Return on Assets 18.37% 18.34% 18.25% 17.63% 17.90%

Return on Assets

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

2002 2003 2004 2005 2006

Year

Out

put

BBBYWSMLNTPIRIndustry

The return on assets ratio indicates how effectively the firm’s assets are

generating profit (www.anz.com). Closely related to the asset turnover, this ratio

divides net income rather than sales by total assets. Over the past five years,

Bed Bath & Beyond’s return on assets has not fluctuated more than 0.37%. The

consistent 18% ROA shows that for every dollar invested into assets, there is a

0.18 cent return.

The recent negative net income and -5.8% ROA expressed in Pier 1’s

financial statements, has distorted the industry average for comparison.

Williams-Sonoma, the closest competitor has favorably increased its return on

assets since 2002. As Williams-Sonoma gains a greater market share each year,

it is easier to see the effects of this highly competitive industry. Bed Bath &

43

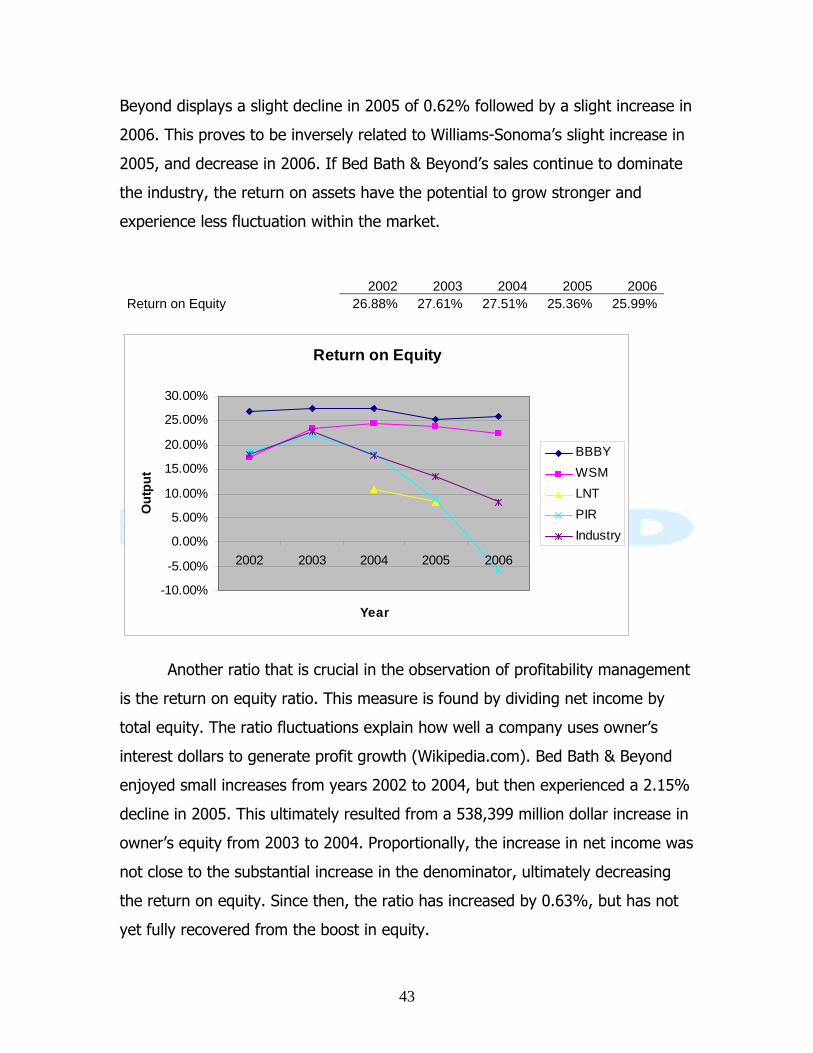

Beyond displays a slight decline in 2005 of 0.62% followed by a slight increase in

2006. This proves to be inversely related to Williams-Sonoma’s slight increase in

2005, and decrease in 2006. If Bed Bath & Beyond’s sales continue to dominate

the industry, the return on assets have the potential to grow stronger and

experience less fluctuation within the market.

2002 2003 2004 2005 2006Return on Equity 26.88% 27.61% 27.51% 25.36% 25.99%

Return on Equity

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

2002 2003 2004 2005 2006

Year

Out

put

BBBYWSMLNTPIRIndustry

Another ratio that is crucial in the observation of profitability management

is the return on equity ratio. This measure is found by dividing net income by

total equity. The ratio fluctuations explain how well a company uses owner’s

interest dollars to generate profit growth (Wikipedia.com). Bed Bath & Beyond

enjoyed small increases from years 2002 to 2004, but then experienced a 2.15%

decline in 2005. This ultimately resulted from a 538,399 million dollar increase in

owner’s equity from 2003 to 2004. Proportionally, the increase in net income was

not close to the substantial increase in the denominator, ultimately decreasing

the return on equity. Since then, the ratio has increased by 0.63%, but has not

yet fully recovered from the boost in equity.

44

Bed Bath & Beyond has maintained a high return on equity compared to

the industry, yet is closely followed by Williams-Sonoma. Williams-Sonoma had a

49.3 million dollar increase in net income from 2002 to 2003 with no increase in

equity, causing a 6% increase in ROE. Since 2004 their ratios have stabilized and

slightly declined. The industry average includes an extremely volatile Pier 1, and

exaggerates the declines shown by Bed Bath & Beyond and Williams-Sonoma

from 2004-2006.

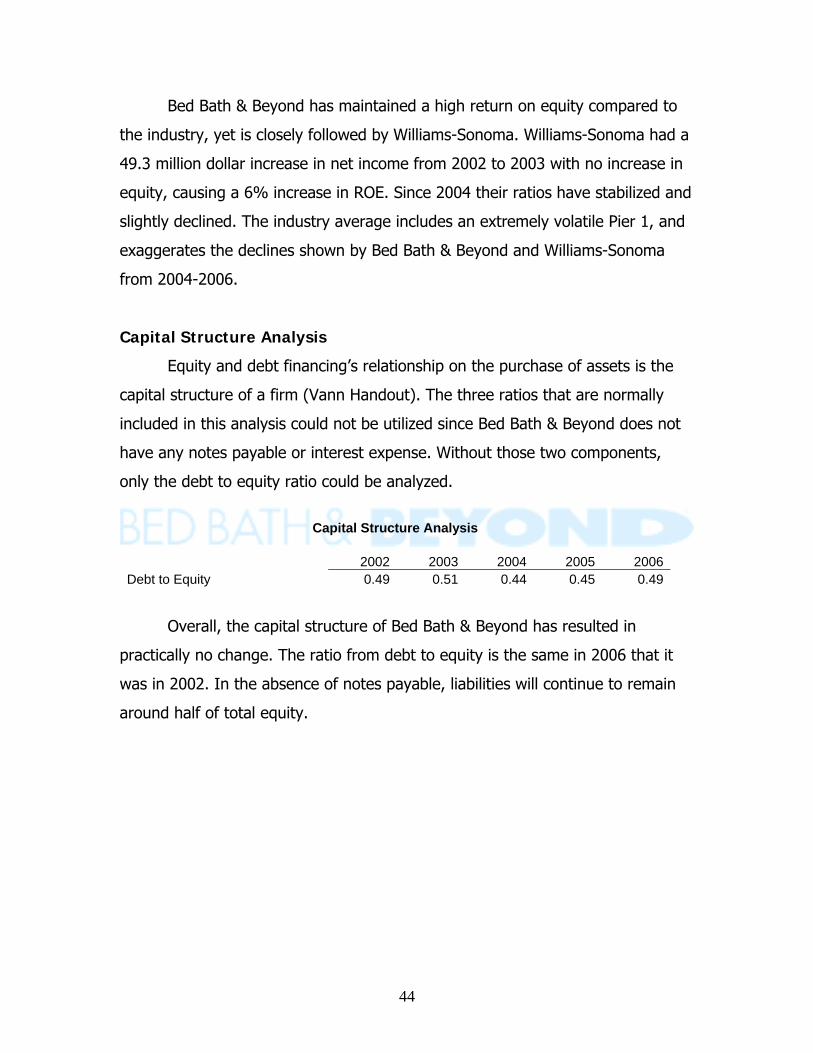

Capital Structure Analysis

Equity and debt financing’s relationship on the purchase of assets is the

capital structure of a firm (Vann Handout). The three ratios that are normally

included in this analysis could not be utilized since Bed Bath & Beyond does not

have any notes payable or interest expense. Without those two components,

only the debt to equity ratio could be analyzed.

Capital Structure Analysis

2002 2003 2004 2005 2006Debt to Equity 0.49 0.51 0.44 0.45 0.49

Overall, the capital structure of Bed Bath & Beyond has resulted in

practically no change. The ratio from debt to equity is the same in 2006 that it

was in 2002. In the absence of notes payable, liabilities will continue to remain

around half of total equity.

45

Debt-Equity Ratio

0.000

0.200

0.400

0.600

0.800

1.000

1.200

2002 2003 2004 2005 2006

Year

Out

put

BBBYWSMLNTPIRIndustry

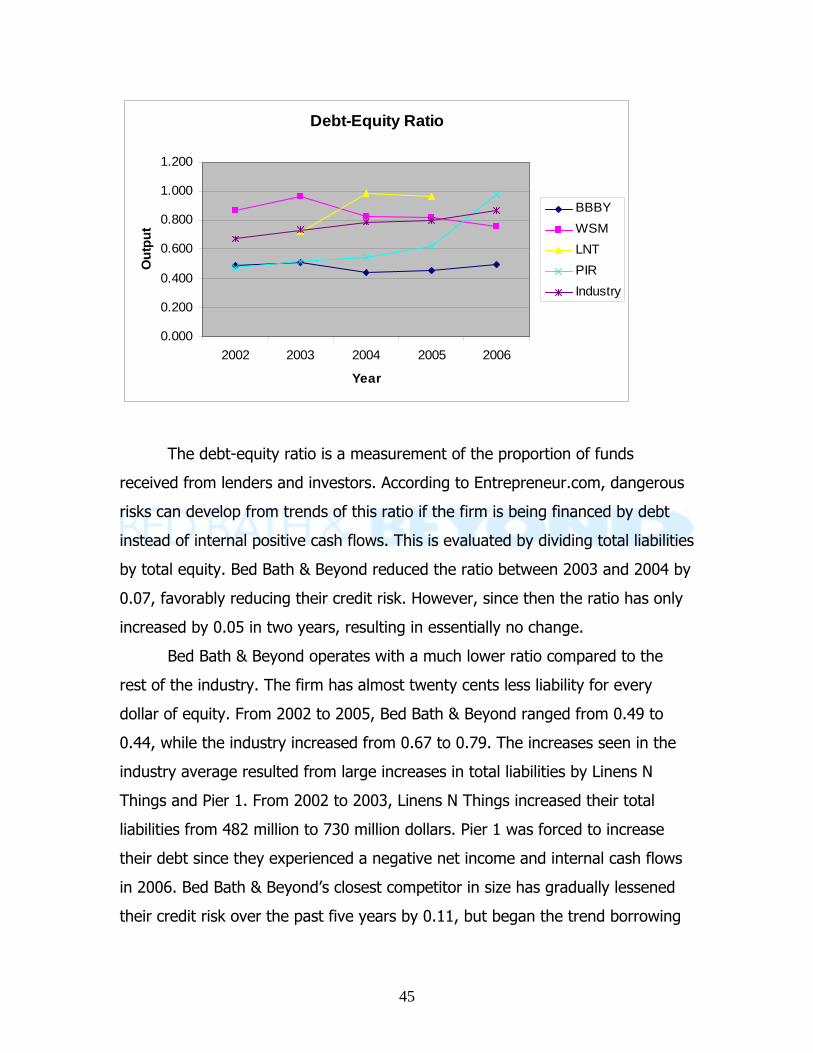

The debt-equity ratio is a measurement of the proportion of funds

received from lenders and investors. According to Entrepreneur.com, dangerous

risks can develop from trends of this ratio if the firm is being financed by debt

instead of internal positive cash flows. This is evaluated by dividing total liabilities

by total equity. Bed Bath & Beyond reduced the ratio between 2003 and 2004 by

0.07, favorably reducing their credit risk. However, since then the ratio has only

increased by 0.05 in two years, resulting in essentially no change.

Bed Bath & Beyond operates with a much lower ratio compared to the

rest of the industry. The firm has almost twenty cents less liability for every

dollar of equity. From 2002 to 2005, Bed Bath & Beyond ranged from 0.49 to

0.44, while the industry increased from 0.67 to 0.79. The increases seen in the

industry average resulted from large increases in total liabilities by Linens N

Things and Pier 1. From 2002 to 2003, Linens N Things increased their total

liabilities from 482 million to 730 million dollars. Pier 1 was forced to increase

their debt since they experienced a negative net income and internal cash flows

in 2006. Bed Bath & Beyond’s closest competitor in size has gradually lessened

their credit risk over the past five years by 0.11, but began the trend borrowing

46

almost 87 cents for every dollar received by investors. Bed Bath & Beyond proves

to have the best financial leverage and credit risk in its industry. Also, the firm’s

consistency over the past five years has proved to look appealing to potential

investors since Bed Bath & Beyond has the greatest amount of equity.

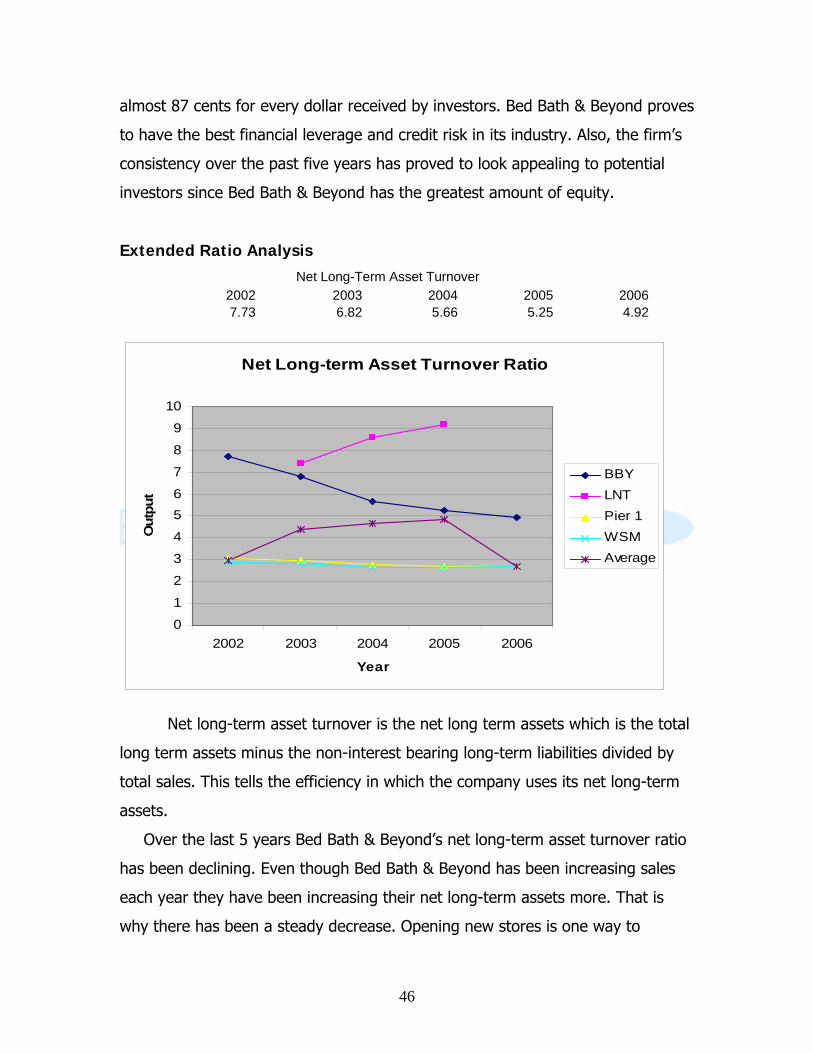

Extended Ratio Analysis Net Long-Term Asset Turnover

2002 2003 2004 2005 2006 7.73 6.82 5.66 5.25 4.92

Net Long-term Asset Turnover Ratio

0

1

2

3

4

56

7

8

9

10

2002 2003 2004 2005 2006

Year

Out

put

BBYLNTPier 1WSMAverage

Net long-term asset turnover is the net long term assets which is the total

long term assets minus the non-interest bearing long-term liabilities divided by

total sales. This tells the efficiency in which the company uses its net long-term

assets.

Over the last 5 years Bed Bath & Beyond’s net long-term asset turnover ratio

has been declining. Even though Bed Bath & Beyond has been increasing sales

each year they have been increasing their net long-term assets more. That is

why there has been a steady decrease. Opening new stores is one way to

47

decrease this ratio. Even though the new store is contributing to sales, it is not

doing enough to increase the net long-term asset ratio.

Compared to the industry Bed Bath & Beyond is doing the opposite. Their

main competitors have been constant or had an increasing net long-term asset

turnover ratio. This is an unfavorable condition for Bed Bath & Beyond since the

higher the ratio the more productive they are at using their net long term assets.

SGR & IGR Analysis

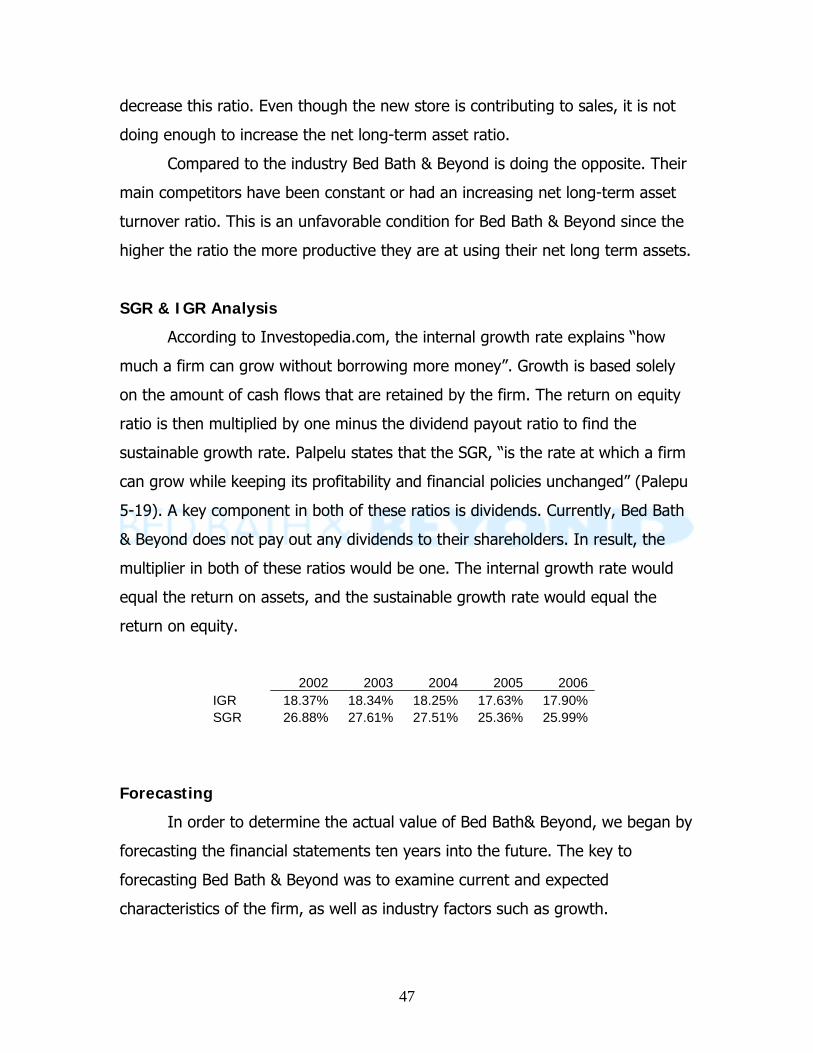

According to Investopedia.com, the internal growth rate explains “how

much a firm can grow without borrowing more money”. Growth is based solely

on the amount of cash flows that are retained by the firm. The return on equity

ratio is then multiplied by one minus the dividend payout ratio to find the

sustainable growth rate. Palpelu states that the SGR, “is the rate at which a firm

can grow while keeping its profitability and financial policies unchanged” (Palepu

5-19). A key component in both of these ratios is dividends. Currently, Bed Bath

& Beyond does not pay out any dividends to their shareholders. In result, the

multiplier in both of these ratios would be one. The internal growth rate would

equal the return on assets, and the sustainable growth rate would equal the

return on equity.

2002 2003 2004 2005 2006 IGR 18.37% 18.34% 18.25% 17.63% 17.90% SGR 26.88% 27.61% 27.51% 25.36% 25.99%

Forecasting

In order to determine the actual value of Bed Bath& Beyond, we began by

forecasting the financial statements ten years into the future. The key to

forecasting Bed Bath & Beyond was to examine current and expected

characteristics of the firm, as well as industry factors such as growth.

48

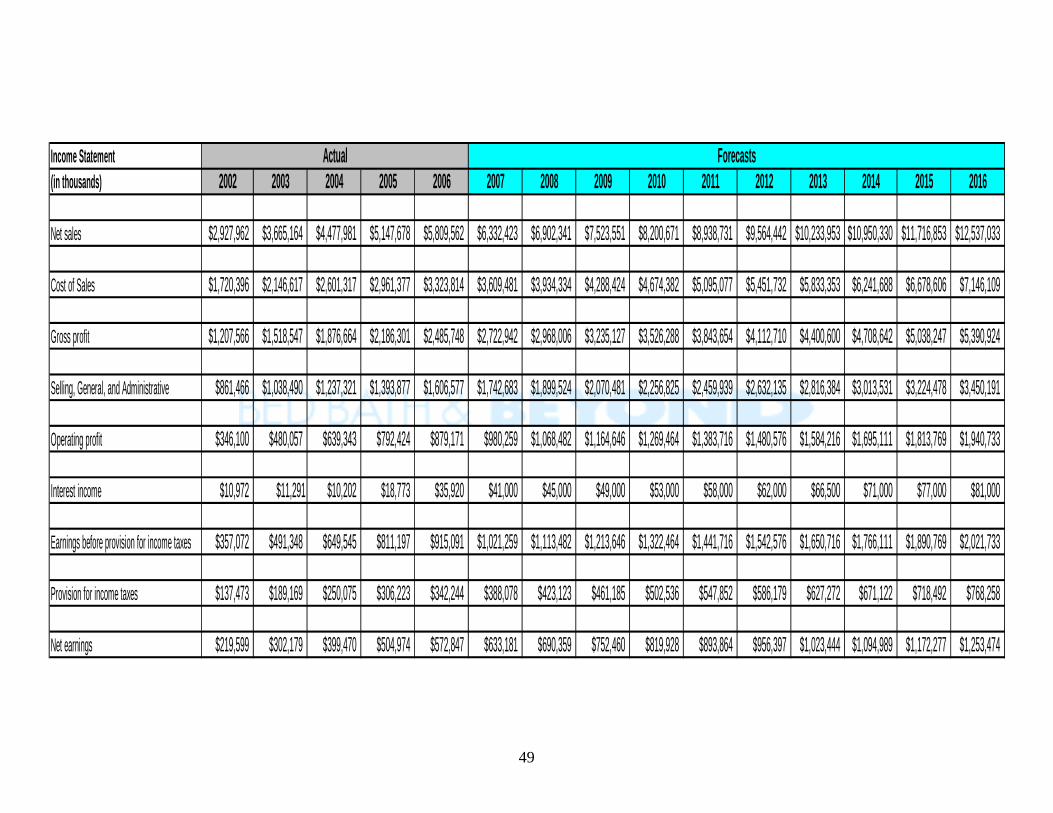

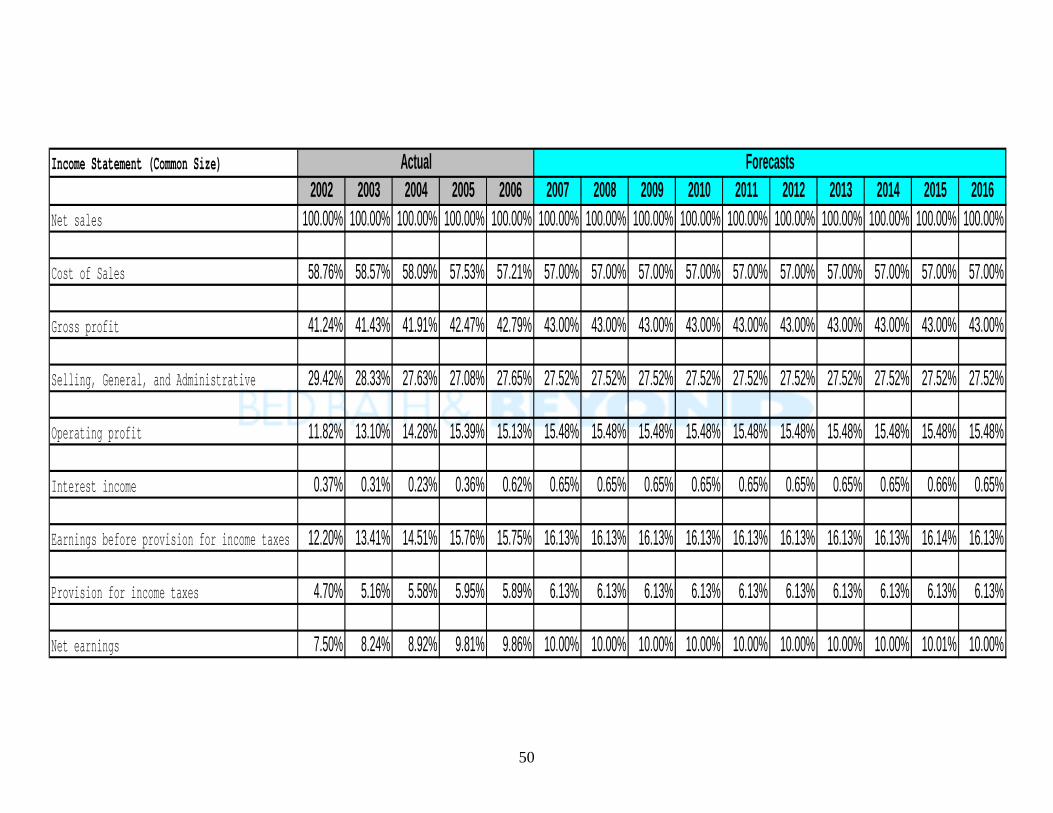

Income Statement

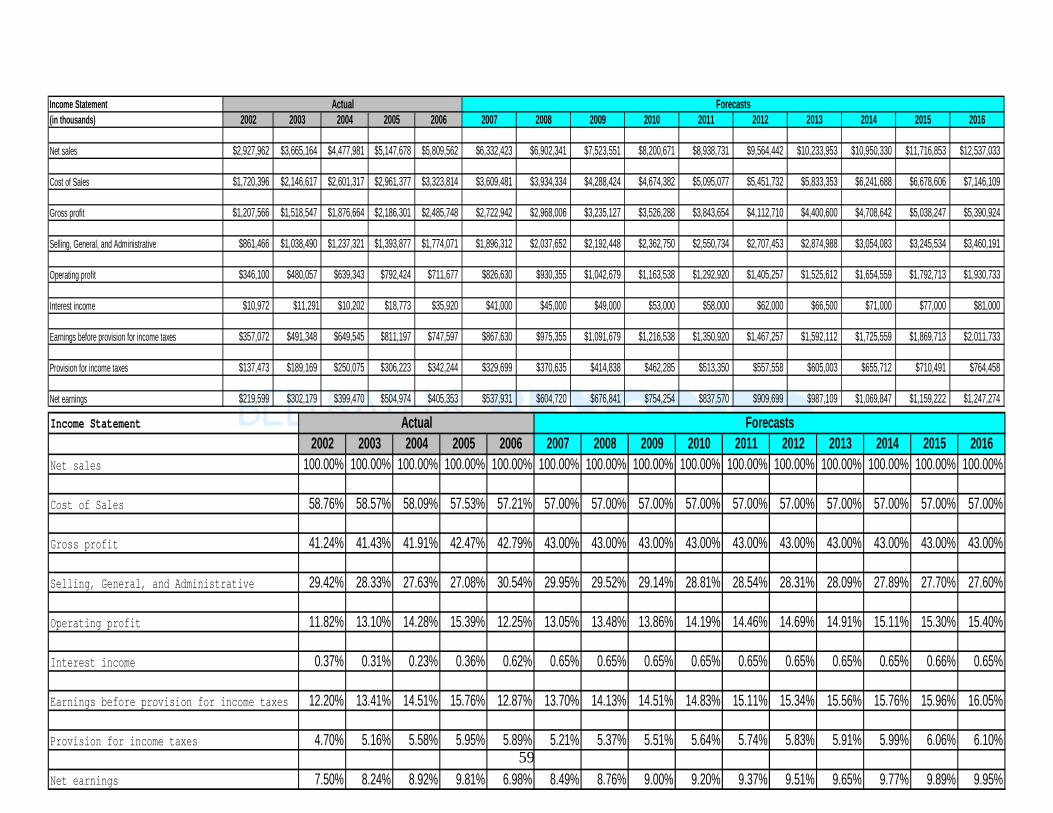

In order to forecast the income statement we had to look for trends in the

financial statements from the last five years. We determined that sales growth

was mean reverting which led us to believe that the yearly growth was going to

keep decreasing until it was back to the industry average. The growth rate for

2002 was 25% and gradually decreased yearly until 2006 when it was 12%. We

followed this trend and projected the growth from 2007 to 2011 to grow at 9%,

and 7% growth thereafter. The rest of the income statement was forecast from

trends found in the last five years. Cost of sales was forecasted as 57% of net

sales, selling, general, and administrative were forecasted as 64% of gross

profit, interest income was 4% of total earnings, and provision for income taxes

was 38% of total earnings.

49

Income Statement(in thousands) 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Net sales $2,927,962 $3,665,164 $4,477,981 $5,147,678 $5,809,562 $6,332,423 $6,902,341 $7,523,551 $8,200,671 $8,938,731 $9,564,442 $10,233,953 $10,950,330 $11,716,853 $12,537,033

Cost of Sales $1,720,396 $2,146,617 $2,601,317 $2,961,377 $3,323,814 $3,609,481 $3,934,334 $4,288,424 $4,674,382 $5,095,077 $5,451,732 $5,833,353 $6,241,688 $6,678,606 $7,146,109

Gross profit $1,207,566 $1,518,547 $1,876,664 $2,186,301 $2,485,748 $2,722,942 $2,968,006 $3,235,127 $3,526,288 $3,843,654 $4,112,710 $4,400,600 $4,708,642 $5,038,247 $5,390,924

Selling, General, and Administrative $861,466 $1,038,490 $1,237,321 $1,393,877 $1,606,577 $1,742,683 $1,899,524 $2,070,481 $2,256,825 $2,459,939 $2,632,135 $2,816,384 $3,013,531 $3,224,478 $3,450,191

Operating profit $346,100 $480,057 $639,343 $792,424 $879,171 $980,259 $1,068,482 $1,164,646 $1,269,464 $1,383,716 $1,480,576 $1,584,216 $1,695,111 $1,813,769 $1,940,733

Interest income $10,972 $11,291 $10,202 $18,773 $35,920 $41,000 $45,000 $49,000 $53,000 $58,000 $62,000 $66,500 $71,000 $77,000 $81,000

Earnings before provision for income taxes $357,072 $491,348 $649,545 $811,197 $915,091 $1,021,259 $1,113,482 $1,213,646 $1,322,464 $1,441,716 $1,542,576 $1,650,716 $1,766,111 $1,890,769 $2,021,733

Provision for income taxes $137,473 $189,169 $250,075 $306,223 $342,244 $388,078 $423,123 $461,185 $502,536 $547,852 $586,179 $627,272 $671,122 $718,492 $768,258

Net earnings $219,599 $302,179 $399,470 $504,974 $572,847 $633,181 $690,359 $752,460 $819,928 $893,864 $956,397 $1,023,444 $1,094,989 $1,172,277 $1,253,474

Actual Forecasts

50

Income Statement (Common Size)2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Net sales 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00%

Cost of Sales 58.76% 58.57% 58.09% 57.53% 57.21% 57.00% 57.00% 57.00% 57.00% 57.00% 57.00% 57.00% 57.00% 57.00% 57.00%

Gross profit 41.24% 41.43% 41.91% 42.47% 42.79% 43.00% 43.00% 43.00% 43.00% 43.00% 43.00% 43.00% 43.00% 43.00% 43.00%

Selling, General, and Administrative 29.42% 28.33% 27.63% 27.08% 27.65% 27.52% 27.52% 27.52% 27.52% 27.52% 27.52% 27.52% 27.52% 27.52% 27.52%

Operating profit 11.82% 13.10% 14.28% 15.39% 15.13% 15.48% 15.48% 15.48% 15.48% 15.48% 15.48% 15.48% 15.48% 15.48% 15.48%

Interest income 0.37% 0.31% 0.23% 0.36% 0.62% 0.65% 0.65% 0.65% 0.65% 0.65% 0.65% 0.65% 0.65% 0.66% 0.65%

Earnings before provision for income taxes 12.20% 13.41% 14.51% 15.76% 15.75% 16.13% 16.13% 16.13% 16.13% 16.13% 16.13% 16.13% 16.13% 16.14% 16.13%

Provision for income taxes 4.70% 5.16% 5.58% 5.95% 5.89% 6.13% 6.13% 6.13% 6.13% 6.13% 6.13% 6.13% 6.13% 6.13% 6.13%

Net earnings 7.50% 8.24% 8.92% 9.81% 9.86% 10.00% 10.00% 10.00% 10.00% 10.00% 10.00% 10.00% 10.00% 10.01% 10.00%

Actual Forecasts

51

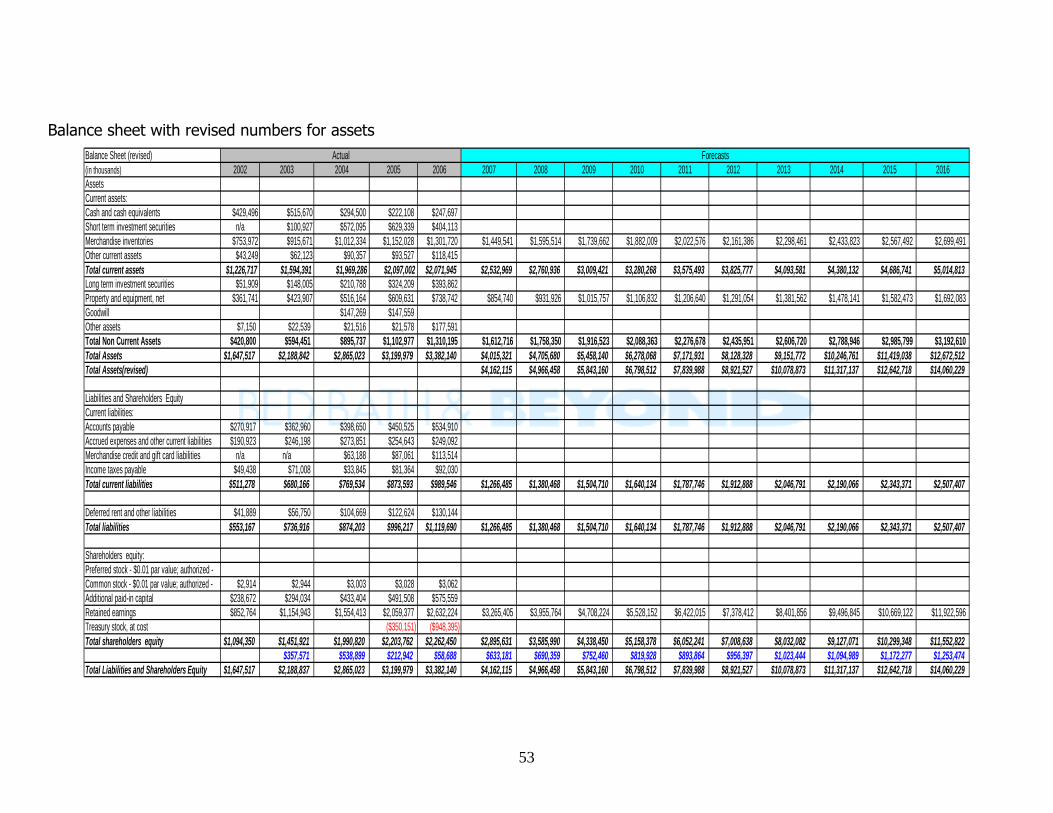

Balance Sheet

The balance sheet was forecasted using a combination of trends, ratios,

and averages. We computed total assets using the assets turnover ratio that was

held constant at 1.7. Total equity was computed by adding the current year’s net

income to the ending book value of equity. We then computed total liabilities.

Long term liabilities were equal to current liabilities, which were computed by

taking the difference between total equity and total assets. Current assets were

calculated using the current ratio held at 2.0. We chose the current ratio of 2.0

because there was a decreasing trend over the last five years of ratios, and we

believe Bed Bath & Beyond will sustain a current ratio no lower than 2.0.

Property, plant, and equipment were forecasted at 56% of non current assets,

and merchandise inventory was forecasted by adding the cash outflow on

inventory from the statement of cash flows to the ending balance of inventory on

the balance sheet.

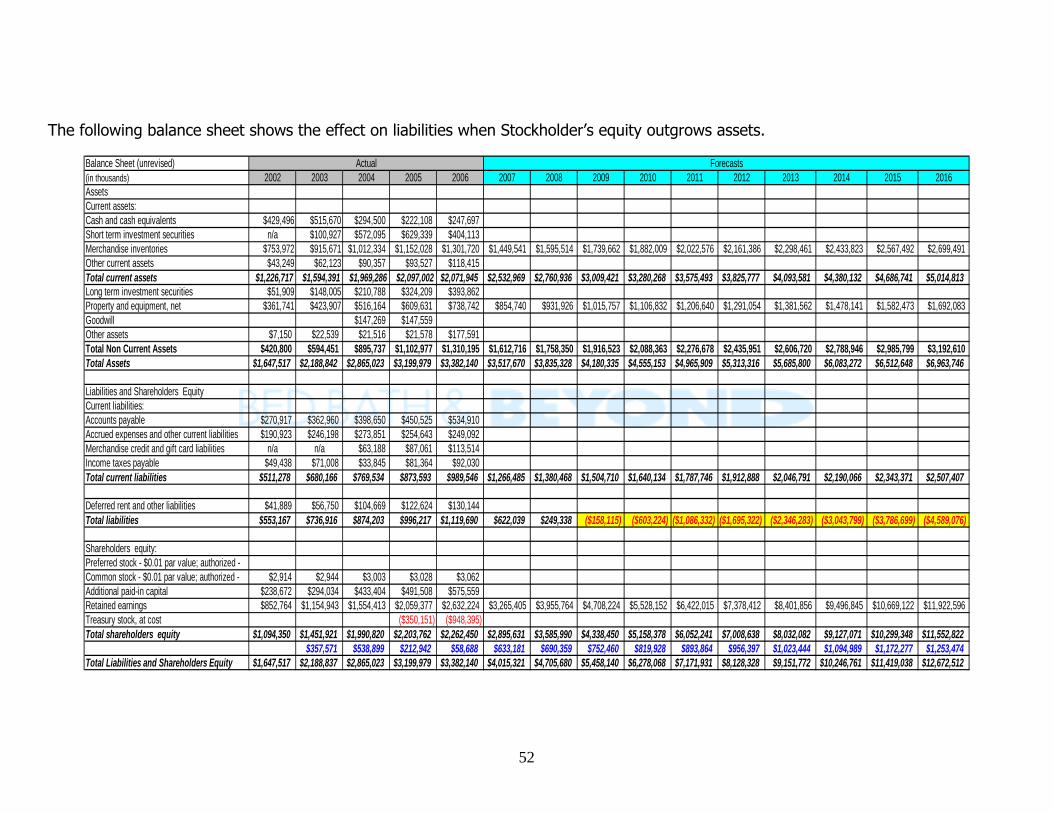

After forecasting the balance sheet elements, we found that stockholder’s

equity was growing at a much faster rate than assets. We did not want to

drastically change assets because we were confident in the method we used to

forecast them. In order to balance, we attempted to decrease liabilities, but the

values were negative by the year 2009. We were then forced to increase assets.

We computed assets by taking the ending balance of total assets and adding net

income for that year. There was a slight difference between total assets and total

liabilities and stockholder’s equity. This amount was added to assets setting both

sides of the equation, A = L + OE, equal to each other.

The inconsistency in Bed Bath & Beyond’s balance sheet raises concerns

because the constant increase in net earnings is not accounted for in any asset

account. This is a problem because a company that is as profitable as Bed Bath

& Beyond should be reinvesting in assets or paying dividends to stockholders. In

2005 and 2006 the company repurchased stock valuing 350 million and 948

million. The reason behind this is unknown, but we speculate this could be an

attempt to deceivingly inflate their share price with fewer shares outstanding. An

investor may falsely believe that more shares are being traded than there

actually are.

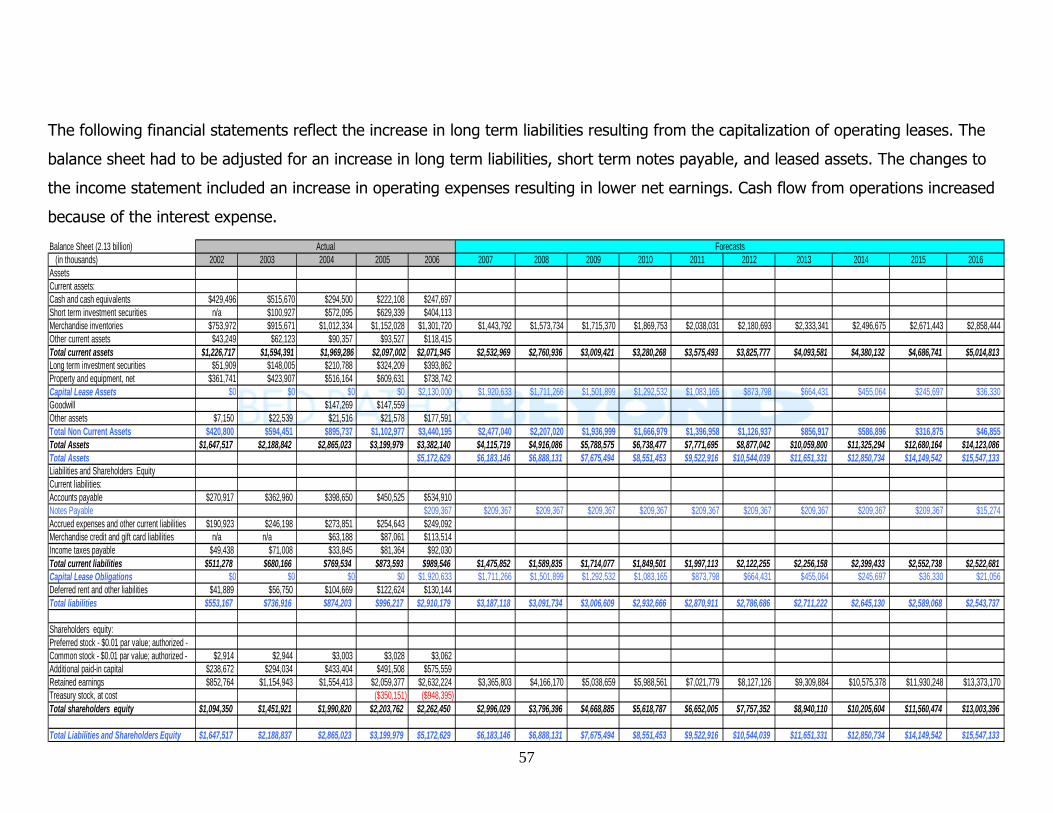

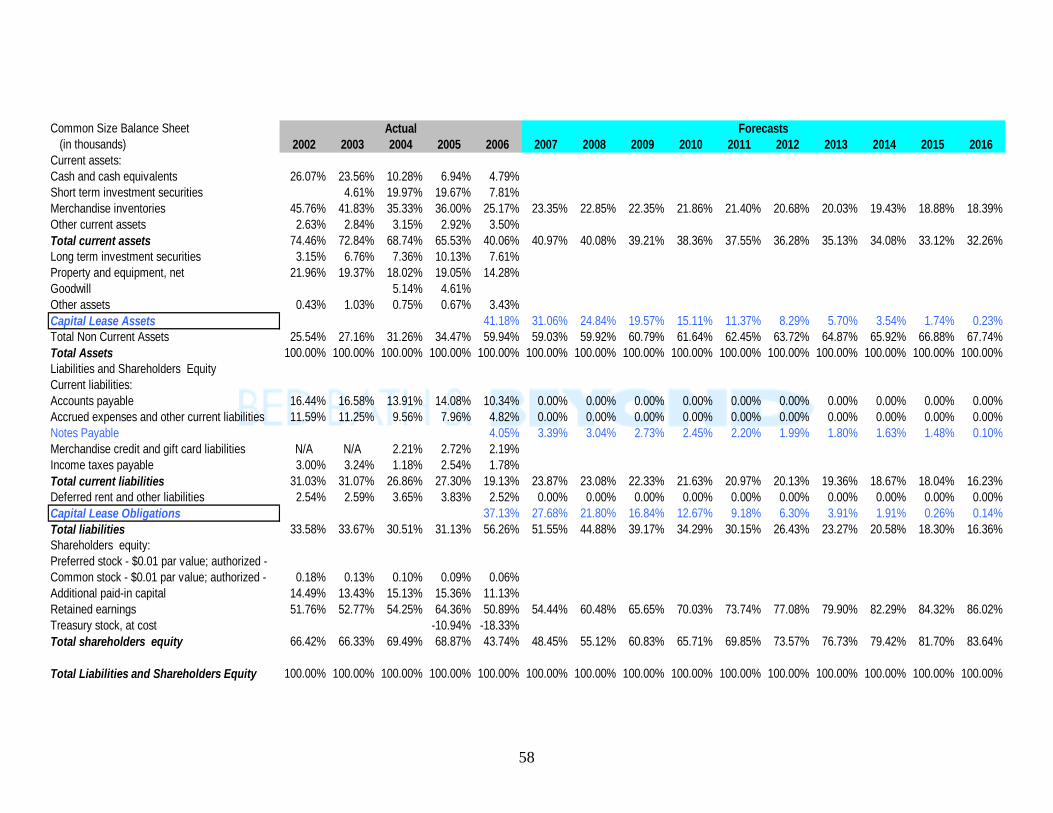

52

The following balance sheet shows the effect on liabilities when Stockholder’s equity outgrows assets.