Embed Size (px)

Citation preview

Value-Creation in Strategic Alliance Portfolios and

the Moderating Role of Environmental Munificence

Kimin Kim

Strategy and Organization Area

Desautels Faculty of Management

McGill University, Montreal

August 2010

A thesis submitted to McGill University in partial fulfillment of the requirements of the degree

of Doctor of Philosophy

© Kimin Kim 2010

ii

This page left intentionally blank.

iii

Abstract

Prior research on alliance portfolios has concentrated primarily on the

focal firm as the recipient of benefits or bearer of risks derived from its alliance

portfolio. However, since partners co-create benefits and share the risks together

with the focal firm, positive or negative values may be created and shared

between the focal firm and its partners. In this thesis, we posit that value-creation

occurs between the focal firm and the partners in an alliance portfolio, and

examine how the portfolio configuration (i.e., the size, diversity, and density)

influences the stock market’s valuation of the partners following the

announcements of a major event involving the focal firm. Furthermore, we

examine how environmental munificence moderates the relationship between the

portfolio configuration and the stock market’s valuation of the partners.

To test the hypotheses we map two sets of alliance portfolios of 120 focal

firms in the U.S. Internet sector: during 1995-1999 for a high munificence

environment and during 1999-2003 for a low munificence environment. Using

event study methods, we find that firms that allied to a focal firm that maintains

higher portfolio diversity and/or higher portfolio density are likely to enjoy

greater abnormal returns when the focal firm announces corporate events. We also

find that portfolio density is likely to be associated with higher abnormal returns

in low munificence environments than in high munificence environments.

This doctoral thesis advances alliance portfolio research and event study

research by investigating performance implications of the portfolio configuration

iv

from the perspective of the impact on partners rather than the focal firm.

Moreover, our findings provide practitioners with prescriptive guidance and

assistance with respect to alliance-related decision-makings.

v

Résumé

Les recherches précédentes sur les portefeuilles d'alliances sont

principalement concentrées sur les firmes focales en tant que récipiendaires de

bénéfices ou porteuses des risques dérivés de leurs portefeuilles d'alliances.

Cependant, comme les partenaires co-produisent les bénéfices et partagent les

risques ensemble, et avec la firme focale, des valeurs positives ou négatives

peuvent être créées et partagées entre la firme focale et ses partenaires. Dans cette

thèse, nous postulons que, dans un portefeuille d'alliances, il y a production de

valeur-création entre la firme focale et ses partenaires. Nous examinons comment

la configuration du portefeuille (i.e., sa grandeur, sa diversité et sa densité)

influence l'évaluation boursière des partenaires après l'annonce d'un évènement

majeur impliquant la firme focale. En outre, nous examinons comment la

munificence de l'environnement modère la relation entre la configuration du

portefeuille et l'évaluation en bourse des partenaires.

Afin de tester nos hypothèses, nous considérons deux groupes de

portefeuilles d'alliances de 120 firmes focales oeuvrant dans le secteur de

l'Internet aux États-Unis durant la période 1995-1999 pour un environnement de

haute munificence et la période 1999-2003 pour un environnement de faible

munificence.

À l'aide de la méthode d'étude d'évènements, nous constatons que les

firmes qui se sont associées à une firme focale qui maintient un plus grand degré

de diversité et/ou de densité dans son portefeuille sont susceptibles de jouir d'une

plus grande rentabilité anormale lors de l'annonce d'évènements corporatifs par la

vi

firme focale. Nous constatons aussi que la densité du portefeuille est

probablement associée à une plus grande rentabilité anormale dans un

environnement de faible munificence que dans un environnement de haute

munificence.

En examinant les implications de la performance de la configuration du

portefeuille du point de vue de son impact sur les partenaires plutôt que sur la

firme focale, cette thèse contribue à la recherche sur les portefeuilles d'alliances

ainsi que la recherche sur les études d'évènements. De plus, nos résultats profitent

aux praticiens en leur fournissant une meilleure compréhension des portefeuilles

d'alliances et de la performance qui facilitera la prise de décision au regard des

alliances.

vii

Acknowledgements

It has been a long journey; it started in 2001 when my then-employer KT

(Korea Telecom) agreed to support me in my pursuit of a PhD (thanks KT!). This

initial phase of my doctorate, during which I wholeheartedly explored the

intellectual frontiers of the field, was interrupted in 2005 when KT requested that

I come back to work in Korea. I resumed my studies in 2009, and am now

approaching the finish line as I submit this thesis. In this long journey, I have met

many extraordinary individuals to whom I would like to express my appreciation.

First and foremost, the completion of this thesis would not have been

possible without the insightful guidance and instruction of my supervisors,

Professors Jan Jörgensen and Wonseok Oh, who have always been ready to give

thoughtful advice and warm encouragement. They have helped me to more clearly

consider other standpoints, think deeper, and pursue better solutions, not just in

research but also in life. Working with them was an invaluable learning

experience. I am very fortunate to have them and remain deeply indebted to them.

It has been a great honor as well to learn from all my committee members:

Professors Michael Carney, Jorge Niosi, and Hamid Etemad. Their valuable

comments and feedback, in different stages of my doctoral studies, have allowed

me to advance, improve, and enrich this work. The diverse perspectives that I

have learned from them will allow me to go beyond this thesis and develop new

directions for my future research.

I would also like to express my appreciation to Professors Jin Nam Choi,

Robert David, Margaret Graham, Mary Dean Lee, Henry Mintzberg, Paola Perez-

viii

Aleman, and George Alex Whitmore. In the classes, seminars, and workshops that

they led, these extraordinary scholars have given me both the inspiration and the

aspiration to become an academic of similar standing. My fellow PhD students

have never made me feel alone in the journey. Being in the “same boat,” they

have never been reluctant to help me, either intellectually or emotionally. Some of

them have left the program to pursue other interests, many have graduated, and

others remain; but all of them will be with me in my memory. Thanks are due to

Ms. Stella Scalia, Mr. Pierre Cambron, Mr. Hector Cantor, and Mr. Antero

Branco, whose excellent administrative and technical services have allowed me to

more easily pursue my research.

I express my gratitude to my parents and parents-in-law. They survived

through the war when still very young and worked very hard throughout their

entire lives. They have encouraged me to meet any challenge and have always

given me their unconditional support. They will remain my models for continued

progress in the school of life. I extend thanks to Gibo Shim, Kyungim Min,

Kyungjoon Min, and Joonkeun Kim, all dear friends in Korea who have taken

care of my parents as they do their own. I am deeply indebted to them.

Finally, I must thank my wife, Jeong Hwa Seo. Marrying her has been my

greatest achievement. I cannot express in words my appreciation for all she has

done to support me during this long journey. My children, Hyunteh and Gyoorie,

have likewise always supported me in their own unique ways. I know that they

have long (and patiently) waited for this moment, and I am so glad that we can

finally share the joy of completion of my PhD together.

ix

TABLE OF CONTENTS

Chapter 1. Introduction 1

Chapter 2. Literature Review 7

2.1. Motivations for alliance formation 7

2.2. Strategic alliances and firm performance 10

2.2.1. Dyadic alliances and firm performance 12

2.2.2. Alliance networks and firm performance 19

2.2.3. Alliance Portfolios and firm performance 22

2.3. Environmental munificence 26

Chapter 3. Theory and Hypotheses 33

3.1. Value-creation in alliance portfolios 33

3.2. The configuration of alliance portfolios 35

3.2.1. Portfolio size 36

3.2.2. Portfolio size and environmental munificence 38

3.2.3. Portfolio diversity 39

3.2.4. Portfolio diversity and environmental munificence 43

3.2.5. Portfolio density 44

3.2.6. Portfolio density and environmental munificence 47

Chapter 4. Data and Methods 51

4.1. Research setting 51

4.2. Sample and data 52

4.3. Methods 56

4.4. Variable description 57

4.4.1. Dependent variable: partners’ abnormal returns 57

4.4.2. Independent variables 58

4.4.3. Moderator: environnemental munificence 61

x

4.4.4. Interaction variables 61

4.4.5. Control variables 62

Chapter 5. Results 67

5.1. Descriptive statistics 67

5.2. Hypothesis tests 67

5.2.1. Main effects 69

5.2.2. Interaction effects 70

5.2.3. Control variables 70

Chapter 6. Discussion and Conclusions 73

6.1. Findings and discussion 73

6.2. Limitations and directions for future research 75

6.3. Contributions to research 77

6.4. Managerial implications 78

6.5. Summary and conclusions 82

References 83

xi

List of Tables

Table Page

Table 1. Key perspectives on the motivations for alliance formation 8

Table 2. Key empirical research on the performance implications of

strategic alliances 15

Table 3. Key empirical research on the role of environmental munificence 31

Table 4. Sample and data 55

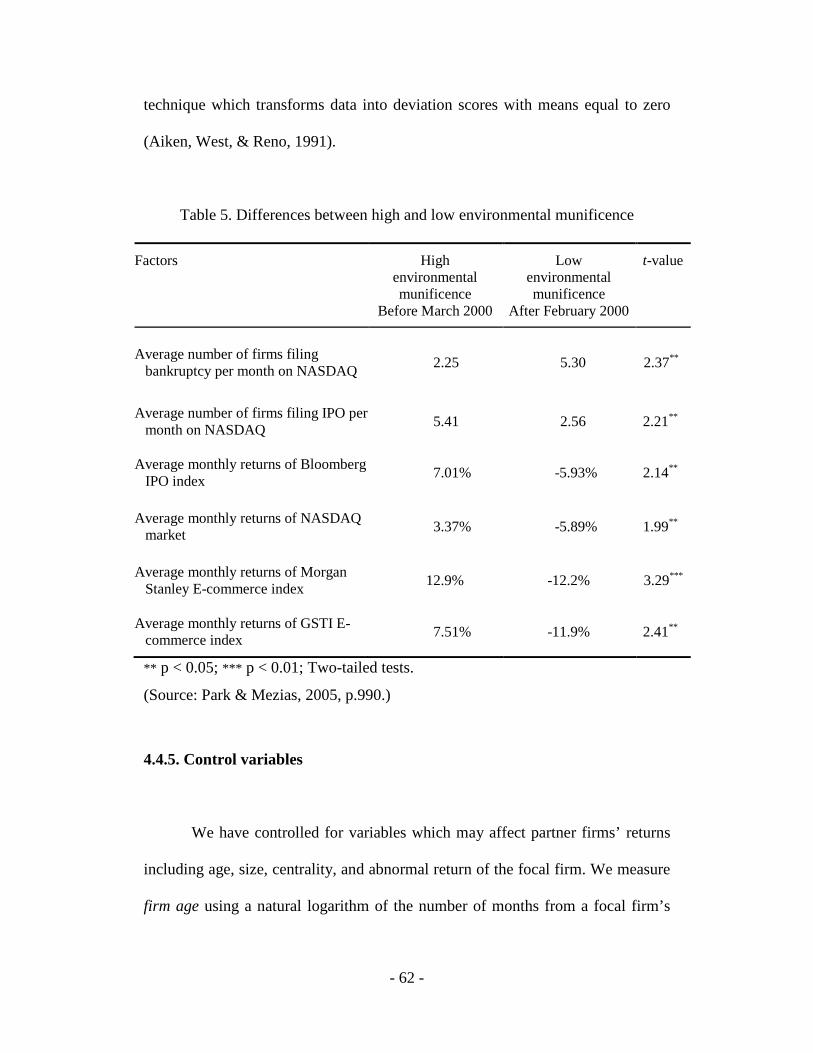

Table 5. Differences between high and low environmental munificence 62

Table 6. Descriptions of variables 65

Table 7. Means, standard deviation, and correlations 68

Table 8. Results of regression analysis 69

List of Figures

Figure Page

Figure 1. Three analysis levels: Dyadic, Networks, and Portfolios 11

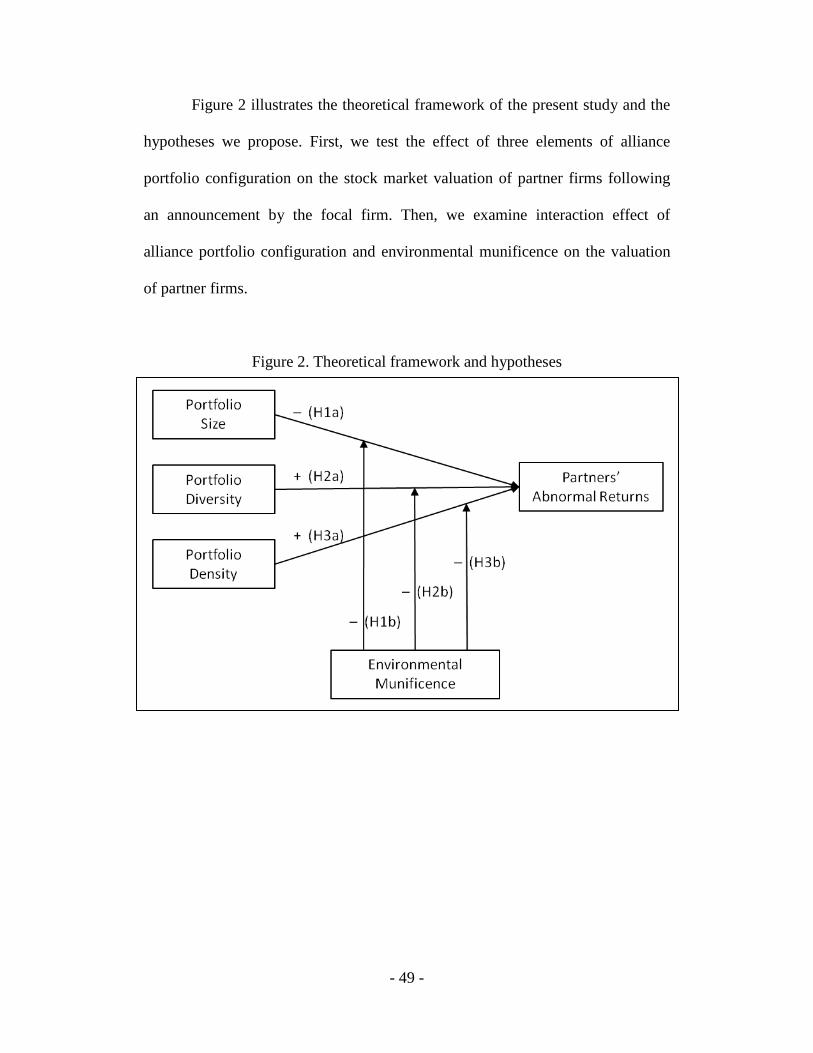

Figure 2. Theoretical framework and hypotheses 49

Figure 3. Research setting 52

Figure 4. Results of hypothesis tests 71

xii

This page left intentionally blank.

- 1 -

Chapter 1. Introduction

Strategic alliances have long been touted as a corporate resource, which

can affect the growth, performance, or even survival of firms. The strategic

significance of such inter-organizational forms has grown rapidly in recent years

as business environments have become increasingly turbulent and competitive.

The formation of strategic alliances (Gulati & Gargiulo, 1999; Pfeffer, 1987) and

their impacts on firm performance (Baum, Calabrese, & Silverman, 2000; Stuart,

2000) have long been investigated from varied perspectives including transaction

cost economics (Williamson, 1975, 1985), resource dependence perspective

(Pfeffer, 1981, 1987; Pfeffer & Salancik, 1978), resource-based view (Barney,

1991; Eisenhardt & Schoonhoven, 1996; Wernerfelt, 1984), social capital theory

(Coleman, 1988; Knoke, 2009; Koka & Prescott, 2002), and social network

theory (Burt, 1992; Granovetter, 1985; Gulati, 1998).

The levels of analysis in prior research are, however, also varied. In the

present study, we review extant research on strategic alliances and firm

performance across the three levels of analysis: micro- (i.e., dyadic alliances),

macro- (i.e., alliance networks), and mezo-level (i.e., alliance portfolios). And, for

the purpose of the study, we concentrate on the alliance portfolios which are

comprised of “all the alliances of the focal firm” (Hoffmann, 2007), and their

association with firm performance.

Although variations exist in their specific objectives and expectations,

firms generally engage in alliances in pursuit of creating benefits and sharing of

- 2 -

risks (Das & Teng, 1999; Mitchell & Singh, 1996). Strategic alliances are fraught

with risk and typically require a significant amount of resources and commitment

for long periods of time (White & Lui, 2005). Given that directly or indirectly

allied firms within an alliance portfolio are “in the same boat” in that they co-

create the rewards and share the risks (Das & Teng, 1999), any major event,

whether positive or negative, that impacts on one firm is likely to impact on

others. In particular, an event that is strategically important to a focal firm may

influence the investors’ valuations of not only the focal firm itself but also the

partner firms with which the focal firm allied. For example, if Yahoo! announces

that its earnings are strikingly lower (or higher) than expected, this performance is

likely to shatter (or boost) investors’ confidence in the alliance initiatives formed

by Yahoo! and, subsequently, negatively (or positively) affect the expected

profitability of its alliance partners. Consequently, a value-creation and a risk-

sharing will take place among the firms embedded in an alliance portfolio.

Previous studies have revealed that the structure and composition of

alliance portfolios have an important performance implication for the focal firm

because they play a crucial role in mobilizing and activating resources within, as

well as across, its firm boundaries (Dyer & Singh, 1998; Gulati, 1998; 1999). By

contrast, little is known about how the configuration of the focal firm’s alliance

portfolio influences the future profitability of its partner firms who determine, to a

large extent, the structural and relational characteristics of the alliance portfolio

(Stuart, 2000).

The thesis therefore examines the following research questions:

- 3 -

• How does the size of the alliance portfolio affect the value of the

partners upon the announcement of new events by the focal firm?

• What role does the partners’ diversity play in creating value for them?

• To what extent does the alliance portfolio density impact the value of

the partner firms?

Our study seeks to fill this void to shed light on the alliance portfolio from the

perspective of the impact on partners rather than the focal firm or rivals.

The extant literature indicates that when environmental munificence, the

given level of resources in a particular environment (Randolph & Dess, 1984;

Staw & Szwajkowski, 1975), is high (resources available outside the firm are

abundant), the firm can exploit the resources to its own benefit and, therefore,

becomes more capable and competent (Castrogiovanni, 1991). In contrast, when

environmental munificence is low (resources are scarcely available), the firm is

forced to compete more intensely, and consequently, its performance or even

survival can be jeopardized (Khandwalla, 1973; Staw & Szwajkowski, 1975).

Drawing on this perspective, Park and Mezias (2005) assess how environmental

munificence governs the stock market’s reaction to e-commerce alliances by

focusing on two distinct periods, that is, before and after the technology sector

crash in 2000.

Extending this line of research, we examine the following additional

research question:

- 4 -

• How does environmental munificence moderate the interplay between

the properties of alliance portfolios and the valuation of the partner

firms?

To address these questions, we first explore the essential configuration

parameters of the alliance portfolio which most affect the valuation of the partners

that are members of the alliance portfolio. Then, based on the event study method,

we investigate how the configuration parameters affect the market value of the

partners following the announcement of a new major event involving the focal

firm. Furthermore, through the lens of environmental munificence, we examine

whether the relationship between portfolio characteristics and the stock market

reaction to partner firms is moderated by the extent of environmental munificence.

This study makes the following contributions to research. First, contrary to

most event studies in the strategy literature which have focused only on the

valuation impact on a focal firm, we identify the extent to which value-creation

taken place between a focal firm and its partner firms upon the occurrence of a

major event involving the focal firm. Second, our research contributes to the

literature on alliance portfolios by monitoring the partners’ valuation in

conjunction with a focal firm’s alliance portfolio. By conceptualizing the alliance

portfolio as the ego-network, our study seeks to explore the recursive and

cooperative dynamics embedded in the alliance portfolio with particular reference

to the partners’ valuation. Finally, we uncover how environmental munificence

moderates the impact of the properties of alliance portfolios on the stock market’s

reactions to the partner firms when a focal firm announces corporate events. This

- 5 -

approach helps to integrate two research streams: the effects of portfolio alliances

on firm performance and the impact of environmental munificence on value-

creation.

The results of this study provide practitioners with a deeper understanding

of the value of the proposed alliances contingent on the configuration of the

alliance portfolios of the potential partner firms, thus help executives or managers

identify the alliance partners that can maximize their firm’s value. In addition, our

study gives hints to practitioners regarding the better timing to enter into alliances

with a particular partner, in terms of the level of environmental munificence.

Moreover, the results imply practical guidelines as to how to construct and

configure an alliance portfolio in such a way that creates as much value as

possible.

The thesis is structured as follows. The second chapter surveys the major

streams of research, i.e., the motivation for alliance formation, performance

implications of strategic alliances across three levels of analysis, and

environmental munificence, all of which provide concerted theoretical building

blocks for this research. The third chapter outlines the research model and

presents the research hypotheses. The fourth chapter details data and methods,

and the fifth chapter describes the results of the study. In the final chapter, the

thesis concludes with a discussion of the results, contributions and implications,

and limitations as well as directions for future research.

- 6 -

This page left intentionally blank.

- 7 -

Chapter 2. Literature Review

2.1. Motivations for alliance formation

Strategic alliances, which are commonly defined as voluntary

arrangements between firms involving exchange, sharing, or co-development of

products, technologies, or services (Gulati, 1998), have been one of the central

topics in the management research for several decades. When strategic alliances

emerged and increased as one of the popular inter-organizational forms in the

early 1980s, many researchers began to investigate the motivations for alliance

formation; why do firms engage in strategic alliances? Diverse perspectives have

contributed to theoretical and empirical explanations of alliance formation (for a

review, see Auster, 1994; Barringer & Harrison, 2000; Glaister & Buckley, 1996;

Ireland, Hitt, & Vaidyanath, 2002; Kogut, 1988). Table 1 summarizes key

perspectives and their explanations of the motivation for alliance formation.

Viewing strategic alliances as hybrid governance structures, transaction

cost economics posits that firms establish strategic alliances in order to reduce

transaction costs (Hennart, 1988, 1991; Williamson, 1975, 1985). According to

transaction cost economics, organizations exist to mediate economic transactions

among members inside or outside of the organization (Ulrich & Barney, 1984).

Since strategic alliances are more efficient than markets or hierarchies when they

minimize the transaction costs (Jarillo, 1988), they are the product of a firm’s

- 8 -

activities to minimize the sum of its transaction costs (Barringer & Harrison,

2000).

Table 1. Key perspectives on the motivation for alliance formation

Perspective Motivation Representative research

Transaction cost economics

To reduce transaction costs Hennart (1988, 1991), Williamson (1975, 1985)

Resource dependence theory

To maximize power and/or autonomy

Pfeffer (1987), Pfeffer & Salancik (1978)

Resource-based view To acquire resources Das & Teng (2000), Eisenhardt & Schoonhoven (1996), Stuart (2000), Wernerfelt (1984)

Organizational ecology To survive environmental conditions over time

Aldrich (1979), Hannan & Carroll (1992), Hannan & Freeman (1989), Miner, Amburgey, & Stearns (1990)

Institutional theory To appear legitimate and conform to social norms

Baum & Oliver (1991), Dimaggio & Powell (1983), Kraatz (1998)

Positioning school To strengthen competitive position

Harrigan (1987, 1988), Porter (1980, 1985)

Organizational learning perspective

To absorb knowledge, thus to increase competencies and ultimately add value to the firm

Doz (1996), Doz & Hamel (1998), Gulati (1999), Inkpen & Crossan (1995), Inkpen & Tsang (2005), Kogut (2000), Powell, Koput, & Smith-Doerr (1996), Prahalad & Hamel (1990)

The resource dependence theory asserts that firms establish linkages with

other firms to maximize power, mitigate environmental control, and acquire

- 9 -

resources (Pfeffer, 1981, 1987; Pfeffer & Salancik, 1978). In order to survive,

organizations need to obtain resources from the environment, which is uncertain

and unstable (Katz & Kahn, 1966). One way organizations cope and try to gain

power is to establish inter-organizational linkages to acquire resources and

information about their environment, coordinate competitive interdependence, or

reduce competitive uncertainty (Pfeffer, 1987).

The resource-based view of the firm suggests that strategic alliances are

formed in the quest for resources (Eisenhardt & Schoonhoven, 1996; Stuart,

2000). According to the resource-based view, the firm is a collection of

heterogeneous resources (Barney, 1991; Penrose, 1959; Wernerfelt, 1984), and

sustained resource heterogeneity is a potential source of competitive advantage

(Das & Teng, 2000). Therefore, a firm forms strategic alliances to develop a

collection of value-creating resources that the firm cannot create independently

(Lavie, 2006; Park, Mezias, & Song, 2004).

Diverse explanations in the strategy and organization literature also help

us to understand motivations of firms to form alliances. It has been suggested that

firms enter into strategic alliances to survive environmental conditions over time

(Aldrich, 1979; Hannan & Carroll, 1992; Hannan & Freeman, 1989; Miner,

Amburgey, & Stearns, 1990), to appear legitimate and conform to social norms

(Baum & Oliver, 1991; Dimaggio & Powell, 1983; Kraatz, 1998), to strengthen

competitive position by influencing industry structure (Harrigan, 1987, 1988;

Porter, 1980, 1985), and to absorb knowledge that is difficult to obtain by other

means (Doz, 1996; Gulati, 1999; Inkpen & Crossan, 1995; Kogut, 2000; Powell,

- 10 -

Koput, & Smith-Doerr, 1996), thus to increase core competencies and ultimately

add value to the firm (Doz & Hamel, 1998; Prahalad & Hamel, 1990).

Having reviewed key perspectives on motivations for alliance formation,

all of which pertain directly or indirectly to firm survival (resource dependence,

organizational ecology, institutional theory) or other measures of performance

(transaction costs, resource-based view, positioning school and organizational

learning), we turn to the literature focusing on the relationship between alliances

and performance.

2.2. Strategic alliances and firm performance

As explanations for the motivation for strategic alliances began to be

provided, a question soon followed; what are the consequences of strategic

alliances? To provide answers to this question, varied perspectives have long

examined performance implications of alliances accruing to the participating

firms in alliances. This literature review focuses on those studies that investigate

the relationship between strategic alliances and firm performance.

Extant studies on this research theme can be categorized in three streams

based on the levels of analysis: (1) micro-level or single, dyadic alliances, (2)

macro-level or alliance networks, and (3) meso-level or alliance portfolios. Figure

1 illustrates the three analysis levels. There are six firms in total, and four dyadic

alliances are established among five firms; one firm (F) is not connected any other

firms (or isolated). From the focal firm’s perspective, every firm that has at least

- 11 -

one dyadic alliance has its own alliance portfolio; thus we have five alliance

portfolios. For example, the dotted triangle in Figure 1 shows firm B’s alliance

portfolio, which is composed of B as the focal firm and its partners A, C, and D.

By contrast, all these entities, including isolated firm F, and alliance relationships

together constitute an alliance network, the dashed line rectangle (for the

illustration of dyadic alliances and alliance networks, see also Das & Teng, 2002:

447).

Figure 1. Three analysis levels: Dyadics, Networks, and Portfolios

Note: Individual firms: A, B, C, D, E, F.

Dyadic alliances: A-B, B-C, B-D, D-E.

Alliance Portfolios: (A-B), (B+A+C+D), (C-B), (D-B-E), (E-D).

An Alliance Network: A, B, C, D, E, F, A-B, B-C, B-D, D-E,

(A-B), (B+A+C+D), (C-B), (D-B-E), (E-D).

- 12 -

From varied perspectives, the three research streams related to these levels

of analysis together help us to understand diverse aspects of relationships between

strategic alliances and firm performance. An overview of key empirical research

on the performance implications of strategic alliances is presented in Table 2.

2.2.1. Dyadic alliances and firm performance

Researchers have found that strategic alliances have significant effects on

the performance of participating firms. Concerning the unit of analysis, however,

early studies on strategic alliances were mostly focused on the single, individual

and dyadic alliances (e.g., Dyer & Singh, 1998; Madhok & Tallman, 1998).

Insights from this approach have enhanced our understanding of dyadic alliances.

Several research strands have shown that properties of individual dyadic alliances

are associated with firm performance. Some concentrate on (a) the strength of ties,

while others focus on (b) the attributes of the partners to which a focal firm ties.

In the social network literature, one of the considerable debates is between

two opposite perspectives on the strength of ties 1

1 In social network literature, the “strength of ties” often referred to as a key characteristics of the “relational embeddedness,” as compared to the “structural embeddedness” (Gulati, 1998; Rowley, Behrens, & Krackhardt, 2000). We review it detailedly in chapter 2.2.2.

: “strength of strong ties” versus

“strength of weak ties” (Kilduff & Tsai, 2003; Lin, 2001). The debate was

triggered by Granovetter’s seminal article (1973), in which he argued that more

diverse information is likely to derive from weak ties than from strong ties.

However, Granovetter also pointed out that strong ties may play an important role,

- 13 -

remarking that “weak ties provide people with access to information and

resources beyond those available in their own social circles; but strong ties have

greater motivation to be of assistance and are typically more easily available”

(1982: 113). On the other hand, subsequent research has followed which finds

evidence for the argument of the strength of strong ties (Krackhardt, 1992; Nelson,

1989). Ever since Granovetter identified and proposed the strength of weak ties

(1973), a large volume of research has been dedicated to contend which argument

has better evidence.

Several studies examined dyadic tie strength or the “linkage intensity” in

the context of inter-firm settings (Hoffmann, 2007). For example, strong ties

enhance coordination and resource sharing while weak ties enlarge ability to

access to diverse information (Uzzi, 1996). Furthermore, strong ties appear to be

important for exploitation and weak ties for exploration, though weak ties

generally enhance profitability (Rowley, Behrens, & Krackhardt, 2000). Although

the strength of dyadic ties research is focus on a single relationship level of

analysis, it has been frequently involved to examine the performance implications

of alliance networks and alliance portfolios as well (Wassmer, 2010).

Some researchers have explained that performance differentials of focal

firms are derived from their partners’ attributes such as reputation, capabilities,

and rivalry. For instance, Stuart and his colleagues find that young firms with

prominent partners go to IPO faster and earn greater valuations at IPO than firms

that lack such connections (Stuart, Hoang, & Hybels, 1999). Similarly, firms with

large and innovative alliance partners perform better than otherwise comparable

- 14 -

firms that lack such partners (Stuart, 2000). Also, alliances with potential rivals

have positive effects on biotech startups’ initial performance, because those

alliances provide more opportunity for learning and less risk of intra-alliance

rivalry (Baum, Calabrese, & Silverman, 2000).

These studies have offered a rich perspective on what benefits accrue from

alliances. However, this perspective may not fully explain the impact of alliances

on firm performance, because the analysis is conducted mostly at the dyadic level

thus each alliance considered as an isolated event rather than as an interdependent

element in a set of multiple alliances (Lavie, 2007).

- 15 -

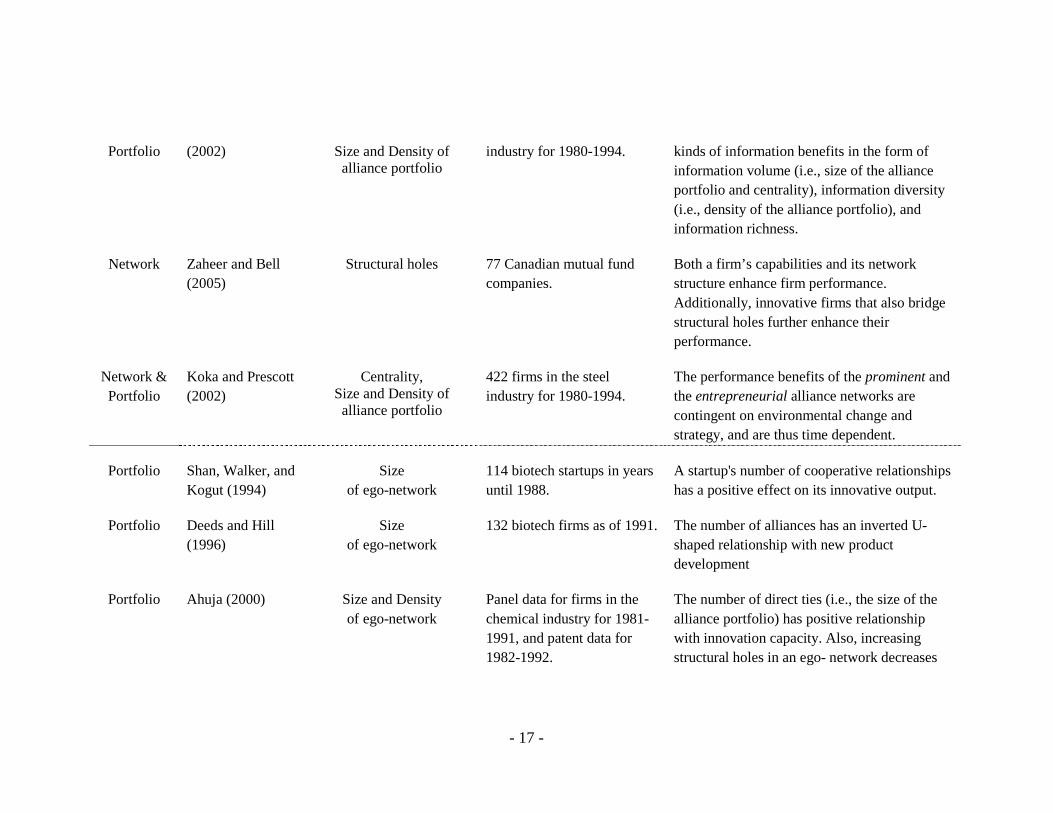

Table 2. Key empirical research on the performance implications of strategic alliances

Level of analysis Authors Explanations for

performance differential Data and sample Main proposals/findings

Dyad Uzzi (1996) Strength of ties

43 interviews from 23 New York apparel firms.

Arm’s-length ties (i.e., weak ties) encourage wide access to information circulating in the market; embedded ties (i.e., strong ties) enhance benefits from trust, joint problem solving and thick information exchange, which in turn enhance coordination and resource sharing.

Dyad Stuart, Hoang, and Hybels (1999)

Partners’ attributes (status)

IPO data of 301 DBF (dedicated biotechnology firms) for 1978-1991.

Young and small firms with prominent strategic alliance partners and organizational equity investors go to IPO faster and earn greater valuations at IPO than firms that lack such connections.

Dyad Stuart (2000) Partners’ attributes (capabilities)

Patent citation data among 150 firms in the semiconductor industry for 1985-1991.

Firms (especially young and small firms) with large and innovative alliance partners perform better than otherwise comparable firms that lack such partners.

Dyad & Portfolio

Rowley, Behrens, and Krackhardt (2000)

Strength of ties, Density of ego-network

Secondary data on the 132 semiconductor firms and 138 steel firms for 1990-1997.

There is a general positive relationship between the number of weak ties and ROA. However, strong ties are important for exploitation, and

- 16 -

weak ties for exploration. Additionally, density of ego-network does not have any significant effect on ROA.

Dyad & Portfolio

Baum, Calabrese, and Silverman (2000)

Partners’ attributes (rivalry),

Size of alliance portfolio

142 Canadian biotech startups for 1991-1996.

Startups can enhance their early performance by establishing alliances with potential rivals that provide more opportunity for learning and less risk of intra-alliance rivalry. Also, their initial performance increases with the size of its alliance network at founding.

Network Powell, Koput, and Smith-Doerr (1996)

Centrality 225 DBFs for 1990-1994. The greater the firm’s centrality in an alliances network, the more rapid its subsequent growth.

Network Gulati (1999) Centrality 166 firms in new materials, industrial automation, and automotive products for 1908-1989.

Firms that are centrally located in the alliance network are more likely to form new alliances.

Network McEvily and Zaheer (1999)

Structural holes Field data from 227 job shop manufacturers located in the Midwest U.S.

Firms embedded in geographical clusters that maintain a network rich in bridging ties to regional institutions are well-positioned to access new information, ideas, and opportunities.

Network & Koka and Prescott Centrality, 422 firms in the steel Social capital yields three distinctly different

- 17 -

Portfolio (2002) Size and Density of alliance portfolio

industry for 1980-1994. kinds of information benefits in the form of information volume (i.e., size of the alliance portfolio and centrality), information diversity (i.e., density of the alliance portfolio), and information richness.

Network Zaheer and Bell (2005)

Structural holes 77 Canadian mutual fund companies.

Both a firm’s capabilities and its network structure enhance firm performance. Additionally, innovative firms that also bridge structural holes further enhance their performance.

Network & Portfolio

Koka and Prescott (2002)

Centrality, Size and Density of alliance portfolio

422 firms in the steel industry for 1980-1994.

The performance benefits of the prominent and the entrepreneurial alliance networks are contingent on environmental change and strategy, and are thus time dependent.

Portfolio Shan, Walker, and Kogut (1994)

Size of ego-network

114 biotech startups in years until 1988.

A startup's number of cooperative relationships has a positive effect on its innovative output.

Portfolio Deeds and Hill (1996)

Size of ego-network

132 biotech firms as of 1991. The number of alliances has an inverted U-shaped relationship with new product development

Portfolio Ahuja (2000) Size and Density of ego-network

Panel data for firms in the chemical industry for 1981-1991, and patent data for 1982-1992.

The number of direct ties (i.e., the size of the alliance portfolio) has positive relationship with innovation capacity. Also, increasing structural holes in an ego- network decreases

- 18 -

the ego’s innovation output. (i.e., density of the alliance portfolio increases the focal firm’s innovation output.)

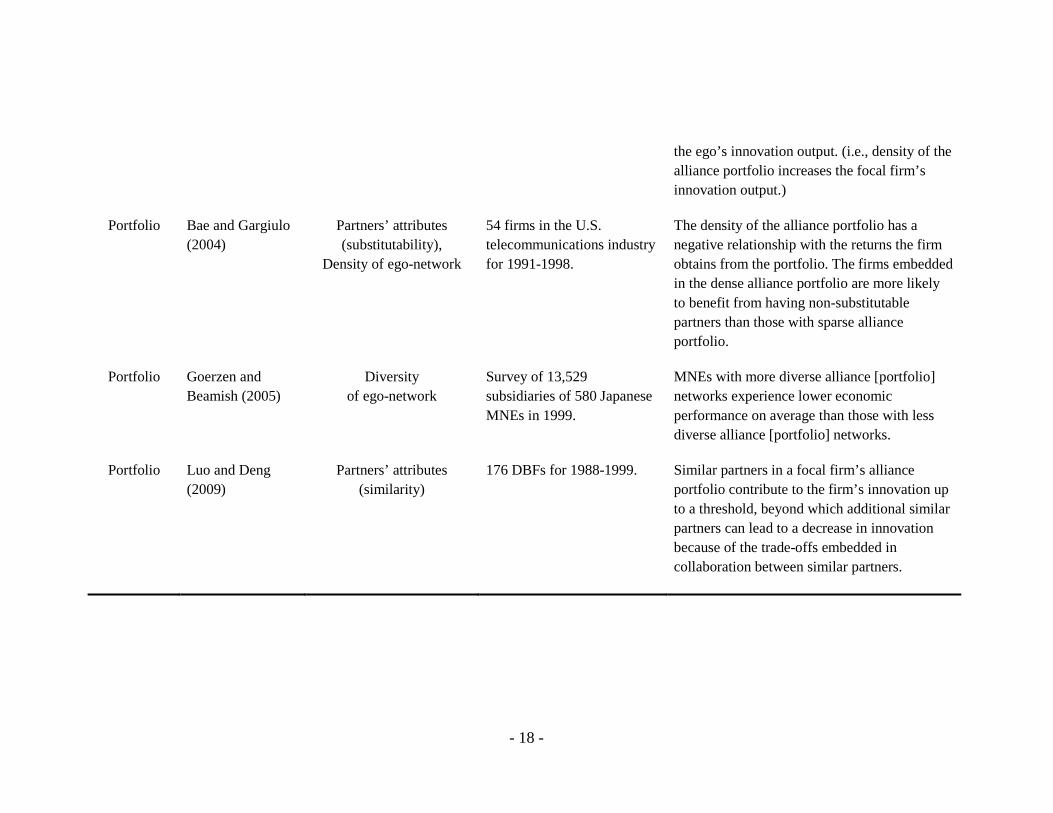

Portfolio Bae and Gargiulo (2004)

Partners’ attributes (substitutability),

Density of ego-network

54 firms in the U.S. telecommunications industry for 1991-1998.

The density of the alliance portfolio has a negative relationship with the returns the firm obtains from the portfolio. The firms embedded in the dense alliance portfolio are more likely to benefit from having non-substitutable partners than those with sparse alliance portfolio.

Portfolio Goerzen and Beamish (2005)

Diversity of ego-network

Survey of 13,529 subsidiaries of 580 Japanese MNEs in 1999.

MNEs with more diverse alliance [portfolio] networks experience lower economic performance on average than those with less diverse alliance [portfolio] networks.

Portfolio Luo and Deng (2009)

Partners’ attributes (similarity)

176 DBFs for 1988-1999. Similar partners in a focal firm’s alliance portfolio contribute to the firm’s innovation up to a threshold, beyond which additional similar partners can lead to a decrease in innovation because of the trade-offs embedded in collaboration between similar partners.

- 19 -

2.2.2. Alliance networks and firm performance

While the causes and consequences of dyadic inter-firm relationships have

long been the main focus of the studies on strategic alliances, less attention has

been paid to the structure of large strategic alliance networks at the holistic level

resulting from numerous dyadic alliances (Gemser, Leenders, & Wijnberg, 1996;

Gulati, 1998; Knoke, Yang, & Granados, 2002; Nohria, 1992). Apart from the

direct dyadic ties between two firms, firms are typically involved in the complex

network of indirectly connected relationships, through “partners of partners” by

participating in various alliances with different partners (Knoke, Yang, &

Granados, 2002).

Research on the macro-level alliances networks is more recent including

what has been termed as the alliance web (Doz & Hamel, 1998), the alliance

network (Baum, Calabrese, & Silverman, 2000; Koka & Prescott, 2002), the

alliance constellation (Das & Teng, 2002; Gomes-Casseres, 1996), the networks

of strategic alliances (Hargedoorn & Schakenraad, 1992), or the strategic alliance

network (Knoke, 2001; Knoke, Yang, & Granados, 2002). Theories of social

embeddedness, social capital, and social network, among many others, have

provided diverse theoretical and empirical explanations on these complex

networks.

Triggered by the seminal work by Mark Granovetter (1985), a new

research approach called the “new economic sociology” has emerged in academic

circles (Swedberg, 2003). As its name indicates, the new economic sociology

- 20 -

analyzes core economic phenomena with the help of sociological approaches,

mainly social network theory, organization theory, and cultural sociology

(Swedberg, 2003). Granovetter’s embeddedness theory, as the central concept of

the new stream, posits that an “economic action” is in principle always

“embedded” in some form or another of “social structure” (1985). The concept of

social embeddedness provides theoretical basis for further research on social

capital and social network perspectives on strategic alliances.

Through the social structure (i.e., the social ties), actors – be they

individuals, groups, or organizations – exchange resources such as wealth,

information, knowledge, status, prestige, power, or access to others. Since social

ties serve as conduits of resources, an actor’s performance may depend on his

possession and control of the social ties (Burt, 1992). Therefore, possession and

control of the social ties create strategic advantages for actors. In this vein, social

capital theorists argue that an actor’s potential resources are inherent in the actor’s

social ties (Kilduff & Tsai, 2003). Further, it has been argued that “something

about the structure of the player’s network and the location of the player’s

contacts in the social structure of the arena provides a competitive advantage in

getting higher rates of return on investment” (Burt, 1992: 8).

In a similar vein, the social network framework suggests that a firm’s

strategic conduct within an industry is influenced not only by the properties of

their direct relationships, but also by the collective structure of inter-firm

relationships (Madhavan, Koka, & Prescott, 1998). Therefore, in contrast to the

traditional theoretical framework in management, which attributes the

- 21 -

performance differentials to the individual firm’s internal resources and

capabilities (the resource-based view), the social network perspective suggests

that the extent to which firms are embedded within networks of relationships

helps determine their performance (Gulati, 1998; Uzzi, 1996). In this vein, Gulati

(2007) named this network embeddedness as the “network resource” in a sense

that it arises outside a firm’s boundaries and within its social networks distinct

from the resources that reside within a firm’s boundaries. Further, he made it clear

that two distinct components of network resources are relevant that accrue to firm

performance: the relational component and the structural component (Gulati,

1998, 2007). Relational embeddedness refers to direct ties a firm links to others,

and studies on this theme have focused mainly on investigating the effect of

strength of ties on organizational performance, as we reviewed earlier. Structural

embeddedness, in turn, refers to the structural position actors occupy in the

overall network, and researchers have examined the relationship between firm

performance and various structural properties such as centrality (Freeman, 1978;

Ibarra, 1993), density (Coleman, 1988), and structural holes (Burt, 1992).

To date, evidence from the structural embeddedness perspective has

covered various benefits derived from the firms’ structural properties within

alliance networks. For example, centrality increases firms’ growth (Powell, Koput,

& Smith-Doerr, 1996) and social capital (Koka & Prescott, 2002); density

increases firms’ innovation output (Ahuja, 2000) and social capital (Koka &

Prescott, 2002); and structural holes increase firms’ returns and access to

information (Burt, 1992; McEvily & Zaheer, 1999).

- 22 -

Notably, however, extant research contains opposite claims on the

network structure: an “open network” versus a “closed network” (Lin, Cook, &

Burt, 2001). Both approaches are largely grounded on and developed from social

capital theory. The open network or the structural holes argument is that social

capital is created by a network in which actors can broker connections between

otherwise disconnected segments (Burt, 1992), whereas the closed network

argument is that social capital is created by a network of strongly interconnected

elements (Coleman, 1988). Varied theoretical and empirical studies have followed

which support either one of the claims or explain them as contingent on other

factors (e.g., Ahuja, 2000; McEvily & Zaheer, 1999; Zaheer & Bell, 2005).

However, the network perspective also may offer only a partial account of the

impact of alliances on firm performance, because it focuses mainly on ties while

assuming away differences in the inherent attributes of actors (Lavie, 2007).

2.2.3. Alliance Portfolios and firm performance

As strategic alliances have become an important strategic resource for

firms, most firms are engaged in multiple alliances with different partners.

Although extant research stream has predominantly focused on either simple

dyadic alliances or complex alliance networks, several researchers have pointed

out that a set of multiple alliances as a level of analysis raises new and important

issues for further research (Gulati, 1998, 2007; Kale & Singh, 2009; Khanna,

1998; Lavie, 2007; Parise & Casher, 2003; Wassmer, 2010). This unit of analysis

- 23 -

refers to the alliance portfolio, which is commonly defined as the aggregate of all

direct strategic alliances of a focal firm (Bae & Gargiulo, 2004; Doz & Hamel,

1998). From the social network perspective, this is akin to the notion of the

egocentric network (Das & Teng, 2002; Lavie, 2007), which encompasses the

focal firm (ego), its set of partners (alters), and their connecting ties (Wasserman

& Faust, 1994). In other words, an alliance portfolio considers an alliance

network from the perspective of a focal firm – i.e., focusing on all alliances that

the focal firm has (Hoffmann, 2007).

Ozcan and Eisenhardt (2009) posit that the level of analysis for alliance

portfolios is theoretically important in several aspects. First, firms establish

alliances in the context of building portfolios, thus the logic of portfolio building

is central to understanding alliance formation. Second, portfolios have aggregate

properties that affect performance but are not meaningful for single ties. Lastly,

portfolios are engines of network evolution; firms adjust their portfolios, thereby

changing the networks in which they operate.

To implement strategies successfully and maximize the benefits from

alliances, firms often rely not only on single high-profile alliances but also on

several coordinated alliances (Gomes-Casseres, 1996). What really matters is not

the success or failure of a single alliance but that the firm will accomplish its

strategic goals with the bundle of its alliances, thus placing the structure and

strategic orientation of the whole alliance portfolio at the center of interest

(Hoffmann, 2007: 828). In this light, researchers have investigated what are the

- 24 -

characteristics of the high-performing portfolios and how to build and manage the

high-performing portfolios.

The characteristics or properties of alliance portfolios are referred as the

portfolio configuration (Hoffmann, 2007; Lavie, 2007; Wassmer, 2010), to which

researchers have recently started to give attention. The portfolio configuration

determines the quality and quantity of external resources the focal firm can access,

thereby influencing its performance (Baum, Calabrese, & Silverman, 2000;

Hoffmann, 2007). Several authors have sought to identify the key elements of the

portfolio configuration. Hoffmann (2007) posits that the alliance portfolio

configuration is comprised of four parameters: the number, dispersion,

redundancy, and the linkage intensity of alliances within the alliance portfolio.

Adding partner-related characteristics to Hoffman’s parameters, Wassmer (2010)

later denotes the alliance portfolio configuration as a complex concept comprising

four dimensions: the size, the structural, the relational, and the partner dimensions.

An alliance portfolio, by definition, embraces the characterisitcs of both

dyadic alliances and alliance networks. Therefore, the elements of portfolio

configuration include those from multiple and mixed levels. For instance,

relational properties (i.e., the strength of ties) and partner atributes (i.e., diversity

of partners) comprise the characteristics of dyadic alliances. In contrast, the size

and the structural properties (i.e., density) of alliance portfolios target the

properties of egocentric networks. These elements of alliance portfolios, alone or

mixed, are reported to affect the focal firm’s performance (for a review, see

Wassmer, 2010).

- 25 -

Stuart and his coauthors (1999) and Stuart (2000), for example, assert that

strategic alliances are access relationships, and therefore the advantages which a

focal firm derives from a portfolio of strategic coalitions depend on the resource

profiles of its alliance partners. Ahuja (2000) finds that the number of partners

(i.e., the size of the alliance portfolio) and density of the alliance portfolio affect

the firm’s capacity to innovate. Baum, Calabrese and Silverman (2000) suggest

that startups can enhance their early performance by establishing many alliances,

and especially by allying with potential rivals that provide more opportunity for

learning and less risk of intra-alliance rivalry. Goerzen and Beamish (2005)

investigate the impact of the diversity of the alliance portfolio on fhe firm’s

performance and find a negative relationship between them. Koka and Prescott

(2002; 2008) have examined the performance implications of network centrality

and size, density, and diversity of a firm’s alliacne portfolio.

Although prior research offers a clear description of the characteristics of

the high-performing portfolio configurations, however, it is not yet clear whether

the benefits accrue to all members of the portfolio. Previous findings have been

limited to only one particular member of the portfolio, the focal firm. An alliance

is established between two or more firms, thus an alliance portfolio is comprised

of multiple firms: a focal firm and its partner firms. Therefore, it can be inferred

that the benefits and the risks derived from an alliance portfolio accrue to all the

member firms in the alliance portfolio, i.e., not only the focal firm but also its

partners.

- 26 -

Surprisingly, however, extant research on the performance implications of

alliance portfolios has concentrated on the focal firm. In a few exceptions, some

researchers shift their focus from focal firms to their rival firms, and test the

impact of focal firms’ alliance announcements (Oxley, Sampson, & Silverman,

2009) or increases in R&D expenditure (Zantout & Tsetsekos, 1994) on their

rivals’ market valuation. In the present study, we seek to shift the focus from the

focal firms to alliance partners, and fill this gap in extant research by investigating

how the configuration of the alliance portfolio influences the expected

profitability of partner firms.

2.3. Environmental munificence

The environment can be viewed as a stock of resources (Aldrich, 1979),

and organizations must import resources from their environments in order to

function (Katz & Kahn, 1966). Therefore, the environment and its interaction with

the organization constitute one of the central research issues in the management

literature (Cyert & March, 1963; Pfeffer & Salancik, 1978; Thompson, 1967).

Environments are multidimensional, and the range of dimensions is indeed wide.

For example, Child (1972) identifies three important environmental conditions:

illiberality, variability, and complexity. Aldrich (1979) reviews previous studies

and codifies six dimensions: capacity, homogeneity-heterogeneity, stability-

instability, concentration-dispersion, domain consensus-dissensus, and turbulence.

Dess and Beard (1984) and McArthur and Nystrom (1991) propose three

- 27 -

dimensions as a more parsimonious set: munificence, dynamism, and complexity.

Similarly, Rajagopalan, Rasheed, and Datta (1993) list three aspects of the

environment: uncertainty, complexity, and munificence.

All these diverse dimensions may be considered almost equally important

in examining the environmental influence. However, Castrogiovanni has

recommended that researchers find and examine a few environmental elements

which are more salient to a given research topic (1991: 543-544, quotation marks

in original).

In a sense, environment is “everything else” outside of a particular

organization (Boulding, 1978). It is impossible to examine

everything, however, and some environmental elements are more

relevant to a particular organization and to the particular issue at

hand than others (cf. Osborn & Hunt, 1974). Thus, theorists have

found it useful to stratify environment according to levels of

specificity, immediacy, and relevance to the organizational

phenomenon of interest (cf. Beard & Dess, 1988; Child, 1972; Dill,

1958; McKelvey, 1982; Starbuck, 1976; Ulrich, 1987).

Following his recommendation for parsimony and salience, we concentrate solely

on the dimension of environmental munificence as the most relevant to our

research.

Environmental munificence is defined as “the extent to which the industry

can support present organizations, enable the present organizations to grow and

prosper, and enable new organizations to gain entrance into the industry”

- 28 -

(Randolph & Dess, 1984: 121). In other words, it is the scarcity or abundance of

critical resources needed by firms operating within an environment

(Castrogiovanni, 1991), thus it has a critical effect on firm behaviors and

outcomes (Dess & Beard, 1984; Wan & Hoskisson, 2003).

As presented in Table 3, research has demonstrated significant

relationships between environments, strategy, and the performance of

organizations (Hansen & Wernerfelt, 1989; Porter, 1980; Scherer & Ross, 1990).

In the strategic management literature, two streams exist in this research area:

those which examine the direct environmental influences on strategy, and those

which focus on the moderating role of the environment in the relationship

between strategy and performance outcomes (Rajagopalan, Rasheed, & Datta,

1993). The same may be said of the research streams on environmental

munificence.

The direct impact of environmental munificence on organizational

strategic behaviors and performance has been the subject of a limited number of

studies. Staw and Szwajkowski (1975), for example, have suggested that the less

munificent the organization’s environment, the more likely it engages in legally

questionable activities, because when the organization’s environment is less

munificent the organization exerts more effort to obtain resources from that

environment. Koberg (1987) has also investigated the relationship between the

level of environmental munificence and organizational behaviors, and posited that

declines in the level of environmental munificence bring about changes in budgets,

planning and control systems, equipment and facilities, and departmentation in

- 29 -

schools. Baum and Wally (2003) have recently asserted that high munificence

environments allow firms to speed up strategic decision-making, thus enhancing

firm performance.

Strategy is considered to be under the control of managers, while

environments are considered to be constraints in that in certain situations

managers cannot proactively change (Pfeffer & Salancik, 1978). Thus, much of

the strategic management literature has considered environments as moderators of

the relationship between strategy and performance (Prescott, 1986). Examining

the effect of environmental munificence on firms, prior research supports the

moderating effect of the environmental munificence on firm strategy in regards to

firm performance. For example, McArthur and Nystrom (1991) find that there is

no direct effect of environemntal munificene on firm performance but there is a

significant positive effect by environmental munificene on the strategy-

performance relationship. Goll and Rasheed (1997, 2004) show that environmetal

munificence moderates the relationship between rationality and performance and

that rationality is strongly associated with performance in a high munificent

environment. Payne and his colleages also find that environmental munificence

has no direct impact on firm performance but it affects performance in the three-

way interaction with firm specialization and rivalry intensity (Payne, Kennedy, &

Davis, 2009). Wan and Yiu (2009) find that corporate acquisitions in high

munificence environments are negatively related to firm performance, because

firms may act imprudently in high munificence environments (Lubatkin &

Chatterjee, 1991) thus engage in inappropriate acquisitions which easily lead to

- 30 -

hurting firm performance. The authors find also that, on the contrary, the same

relationship is positive in low munificence environments because firms can get

significant benefits from low munificence environments by taking new

opportunities through corporate acquisitions (Chattopadhyay, Glick, & Huber,

2001; Meyer, 1982).

Although a large volume of research has investigated the relationship

between environmental munificence and organizational performance, relatively

few empirical studies have examined the effect of environmental munificence on

the stock market response (Park & Mezias, 2005). In the present study, we seek to

make an empirical contribution by examining how environmental munificence

moderates the effect of alliance portfolio properties on the stock market valuation

of the alliance partners in response to major corporate events announced by the

focal firm.

- 31 -

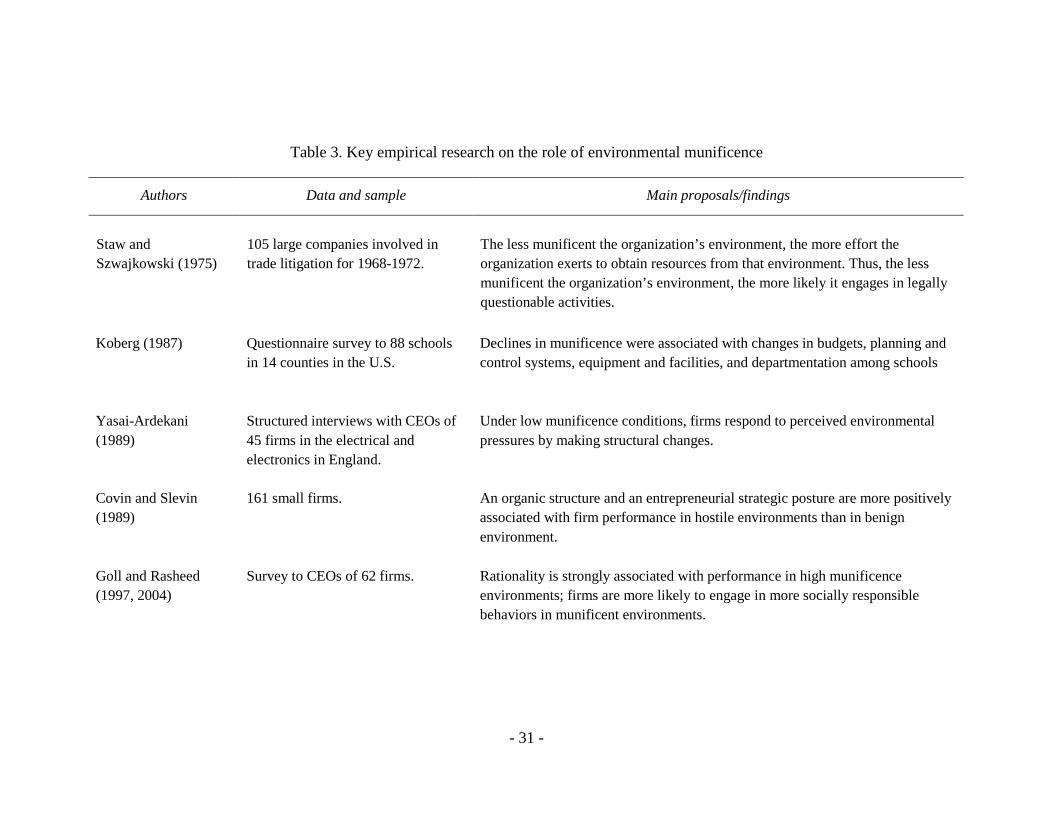

Table 3. Key empirical research on the role of environmental munificence

Authors Data and sample Main proposals/findings

Staw and Szwajkowski (1975)

105 large companies involved in trade litigation for 1968-1972.

The less munificent the organization’s environment, the more effort the organization exerts to obtain resources from that environment. Thus, the less munificent the organization’s environment, the more likely it engages in legally questionable activities.

Koberg (1987) Questionnaire survey to 88 schools in 14 counties in the U.S.

Declines in munificence were associated with changes in budgets, planning and control systems, equipment and facilities, and departmentation among schools

Yasai-Ardekani (1989)

Structured interviews with CEOs of 45 firms in the electrical and electronics in England.

Under low munificence conditions, firms respond to perceived environmental pressures by making structural changes.

Covin and Slevin (1989)

161 small firms. An organic structure and an entrepreneurial strategic posture are more positively associated with firm performance in hostile environments than in benign environment.

Goll and Rasheed (1997, 2004)

Survey to CEOs of 62 firms. Rationality is strongly associated with performance in high munificence environments; firms are more likely to engage in more socially responsible behaviors in munificent environments.

- 32 -

Wan and Hoskisson (2003)

799 firms in western Europe. In more munificent environments, there is a negative relationship between product diversification and performance; in less munificent environments, there is a positive relationship between product diversification and performance.

Baum and Wally (2003)

Survey to 318 firms for 1996-2001. The greater the environmental munificence, the higher the firm’s performance; the greater the environmental munificence, the faster the strategic decision-making.

Park and Mezias (2005)

408 alliance announcements of 75 e-commerce firms for 1995-2001.

Stock market responds more favorably to alliances during the less munificent period. Stock market response to alliance partner and type is also affected by the change in environmental munificence between the two periods.

Payne, Kennedy, and Davis (2009)

Survey to 1,030 SMEs. Environmental munificence moderates the relationship between firm specialization and firm performance; performance increases with firm specialization, at a faster rate with increased munificence.

Latham (2009) Survey to 137 software executives for 2001-2003.

In low munificence environments, smaller firms adopt revenue generating strategies but larger firms adopt cost reduction strategies.

Wan and Yiu (2009) 234 M&As among 78 firms in Hong Kong and Singapore for 1994-2002.

In low munificence environments, acquisitions are positively related to firm performance, but the same relationship in high munificence environments is negative in comparison.

Rosenzweig (2009) Web survey to 50 manufacturers. Environmental munificence weakens the relationship between e-collaboration and performance.

- 33 -

Chapter 3. Theory and Hypotheses

3.1. Value-creation in alliance portfolios

Strategic alliances are both access relationships and pathways for the

exchange of resources and signals that convey social status and recognition

(Stuart, 2000). The following metaphor may clarify this inter-firm relationship.

Surely this patterned exchange looks more like a marriage than a

one-night stand, but there is no marriage license, no common

household, no pooling of assets (Powell, 1990: 301).

However, alliances are fraught with risks as well as benefits, and typically require

a significant amount of resources and commitment for long periods of time

(White & Lui, 2005). When outcomes from alliances are positive, the alliances

convey social capital, but when they obstruct strategic actions, they produce

“social liability”, i.e., negative social capital (Leenders & Gabbay, 1999: 3).

When positive or negative outcomes are produced from dyadic alliances,

those outcomes may be shared between two firms, whether evenly or unevenly

(Khanna, 1998). Therefore, the benefits and the risks which derive from an

alliance portfolio may accrue not only to a focal firm but also to all the other firms

within the alliance portfolio (i.e., the partners of the focal firm). Since the partners

of a focal firm within an alliance portfolio are interdependent and affect one

another, they together create synergies or conflicts (Parise & Casher, 2003), which

make the total value created in the alliance portfolio greater or smaller than the

- 34 -

sum of the values created by individual dyadic alliances in the portfolio (Vassolo,

Anand, & Folta, 2004). In other words, since allied firms are “in the same boat” in

that they co-create rewards and share the risks (Das & Teng, 1999), value-

creation, whether positive or negative, will occur among those firms in the

corporate marriage (Oxley, Sampson, & Silverman, 2009).

The market signaling perspective posits that investors may respond to

corporate announcements by buying or selling the stock (Asquith & Mullins,

1986). For example, investors react to corporate announcements such as dividends

and earnings announcements (Eddy & Seifert, 1992), mergers and acquisitions

(Datta, Pinches, & Narayanan, 1992), strategic alliances (Das, Sen, & Sengupta,

1998), lawsuits (Bhagat, Brickley, & Coles, 1994), proactive layoffs (Lee, 1997),

and corporate name changes (Lee, 2001). Such corporate announcements can

generate positive abnormal returns when investors expect great potential in the

firm’s action, or negative abnormal returns when investors disapprove of

managerial decisions (Asquith & Mullins, 1986).

We posit that, when a firm announces major events which are strategically

important to the firm, the announcements may have impact on its partner firms, i.e.

all the firms in the same boat, as well as the announcing firm itself. For example,

if Yahoo! announces that its earnings are noticeably higher than expected, this

performance is likely to boost investors’ confidence in the alliance initiatives

formed by Yahoo! as well as Yahoo! itself. Thus, subsequently, the

announcement will positively affect the expected future profitability of its alliance

partners. In the same vein, when an event negatively affects the stock price of the

- 35 -

announcing firm, it also is likely to have a negative effect on the stock prices of

partner firms.

By this line of thinking, we presume that a corporate announcement in an

efficient capital market influences the investors’ valuation of not only the

announcing firm itself but also its partner firms as reflected in their stock prices.

3.2. The configuration of alliance portfolios

Firms establish and maintain alliances expecting these will enhance

performance. However, all alliances may not have an equal value for performance.

For instance, at the dyadic alliance level, whom to ally with and whether to seek

strong or weak alliances may be major determinants of firm performance (Baum,

Calabrese, & Silverman, 2000; Uzzi, 1996).

Together with these findings, firm performance can be better understood

by also examining strategic alliance networks in which the firm is embedded

(Gulati, 1998; Gulati, Nohria, & Zaheer, 2000). However, all alliance networks,

like dyadic alliances, may not be equally valuable for firm performance. For

example, at a collective network level, central positioning in the network may also

be a major determinant of firm performance (Burt, 2001; Powell, Koput, &

Smith-Doerr, 1996).

As such, all alliance portfolios may not contribute equally to performance.

It is the portfolio configuration that determines the performance differentials

(Baum, Calabrese, & Silverman, 2000; Hoffmann, 2007). The portfolio

- 36 -

configuration is comprised of varied parameters such as the number, dispersion,

redundancy, and the strength of ties within the alliance portfolio (Hoffmann,

2007), or the size, structural, and relational characteristics of ties within the

alliance portfolio, and partner-related characteristics (Wassmer, 2010). Among

these, we select three characteristics as essential parameters of the alliance

portfolio configuration: (a) the size, (b) diversity, and (c) density of the alliance

portfolio. We believe that these parameters best represent the structured properties

of the unit of ego-network, and thus most affect performance of the partners

which are embedded in the alliance portfolio. Further, we believe also that these

parameters affect stock market valuation to the partners in the same alliance

portfolio when a focal firm announces major corporate events.

3.2.1. Portfolio size

One of the essential configuration parameters of alliance portfolios is the

size of the portfolio. Most prior studies suggest that the bigger the size of an

alliance portfolio the better the focal firm’s performance. Since firms possessing a

large alliance portfolio have better access to large volume of external resources

and information (Gulati, 1999; Koka & Prescott, 2002; 2008), they may yield

better performance than those with a smaller alliance portfolio. Evidence also

suggests that the size of the portfolio has a positive effect on innovative output

(Ahuja, 2000; Baum, Calabrese, & Silverman, 2000; Shan, Walker, & Kogut,

- 37 -

1994) or an inverted U-shaped relationship with new product development (Deeds

& Hill, 1996).

However, we may need different lenses when we examine performance of

a focal firm that possesses an alliance portfolio if we investigate the performance

of partners embedded in the alliance portfolio. Also, if we shift our perspective

from a focal firm to its partners, the predominant argument may not necessarily be

true at the shifted perspective. Regarding the size of alliance portfolios, we argue

that the small size may be more valuable especially in the value creation of the

partners in an alliance portfolio for the following reasons.

In alliance portfolios, both value-creation mechanisms and value-

appropriation mechanisms are in play (Lavie, 2007). Value-appropriation

mechanisms determine the relative share of benefits to individual partners

(Khanna, Gulati, & Nohria, 1998) and competition for the distribution of benefits

increases conflicts between partners, which may lead to alliance failure (Park &

Russo, 1996). Therefore, as the number of dyadic alliances increases in an

alliance portfolio, i.e., as the size of an alliance portfolio increases, the potential

for multilateral conflicts also increases. Moreover, as the number of partners in an

alliance portfolio increase, so do coordination costs, monitoring costs, and

managerial complexity (Gulati & Singh, 1998).

By contrast, small alliance portfolios may provide firms with better

environment to have frequent interactions than large ones (Kraatz, 1998). Also,

the increasing chances of interactions may lead to formation of direct ties between

otherwise indirectly connected firms. Then, the newly established stronger ties

- 38 -

make it easier for the firms to share and exchange complex knowledge and

valuable information (Hansen, 1999; Krackhardt, 1992; Uzzi, 1996). The

potential for direct dyadic interactions between any two parties in an alliance

portfolio is likely to decline as network size grows. Subsequently, investors in an

efficient capital market will perceive that the firms embedded in small alliance

portfolios have better chances to enhance their future performance. Consequently,

we argue for the negative relationship between the size of an alliance portfolio

and performance of the partners embedded in the alliance portfolio.

Hypothesis 1a: When a focal firm announces corporate events, the partner firms’

abnormal returns will be negatively associated with the size of the alliance

portfolio.

3.2.2. Portfolio size and environmental munificence

However, investor perceptions on the portfolio size may be contingent on

environmental munificence. Munificent environments provide firms with

abundant resources necessary to sustain growth and stability (Dess & Beard,

1984). Thus, even without alliances with others, in munificent environments firms

can easily secure resources to improve brand awareness, create demand, and

secure future growth (Aldrich, 1979; Pfeffer, 1987; Randolph & Dess, 1984).

Thus, in a munificent environment, strategic alliances may signal weakness

because firms are not trying to operate independently even though resources are

- 39 -

plentiful. Therefore, alliance announcements in the period of low environment

munificence result in higher abnormal returns than those in the period of high

environment munificence (Park & Mezias, 2005).

Firms find it more difficult and have fewer options to obtain resources in a

less munificent environment (Castrogiovanni, 1991; Dess & Beard, 1984).

Therefore, a firm possessing a large set of partners in low munificence may signal

strength because firms may more easily obtain resources thus more likely to

sustain growth. By contrast, it is quite likely that, in munificent environments,

being a member of a large alliance portfolio thus possessing a great number of

indirectly allied partners may signal weakness. Consequently, we argue the

following:

Hypothesis 1b: The negative relationship between portfolio size and partners’

abnormal returns will be stronger in high munificence environments than in low

munificence environments.

3.2.3. Portfolio diversity

Diversity of the alliance portfolio is the breadth, dispersion, heterogeneity,

or dissimilarites among the partners in an alliance portfolio (Goerzen & Beamish,

2005; Hoffmann, 2007). Research on partner diversity was investigated initially at

the individual level. However, prior studies have conflicting arguments on the

relationship between partner diversity and performance. For example, Granovetter

- 40 -

demonstrates that job-seekers find better jobs faster when they maintain diverse

acquaintances (1973). On the other hand, people are more likely to learn complex

things from others when they are embedded in a homophilous social circle

(Bandura, 1977), because individuals in homophilic relationships share common

characteristics (e.g., beliefs, values, and education) that make communication and

relationship formation easier and more frequent (McPherson, Smith-Lovin, &

Cook, 2001).

Exploration of the effects of the partner similarity at the inter-firm

alliances level has also been researched. Darr and Kurtzberg (2000) have shown

that collaboration between similar partners leads to better knowledge transfer,

because their identies and routines are similar so that they can cooperate and

coordinate easier. Also, social similarity within a network promotes frequent

communications as well as liking and intimacy between actors (Rogers, 1995). On

the other hand, others have argued that collaboration between partners possessing

dissimilar resources are likely to enhance firm performance by integrating

complementary resources (Das & Teng, 2000; Harrison, Hitt, Hoskisson, &

Ireland, 2001).

The literature review therefore shows opposing and inconclusive results

about the effects of partner diversity on performance, at many different levels of

analysis such as the individual, inter-personal, intra-, and inter-organizational.

This may result from the studies’ focus on the dyad relations rather than the social

contexts in which such a dyad embedded (Luo & Deng, 2009: 1006). It may also

be due to the studies’ focus only on the focal firms. We attempt to advance the

- 41 -

debate and enlarge the perspective by examining the phenomenon at the level of

the alliance portfolio and from the viewpoint of the partners of a focal firm.

Diversity of the alliance portfolio can affect the performance of partners in

several aspects. First, a diverse portfolio provides the firms with access to various

benefits including information, knowledge, technologies, skills, and markets,

which are new and fresh that homogeneous portfolios may not provide. Firms

with diverse partners may have access to a variety of ideas and perspectives (Burt,

1992; Granovetter, 1982). In this vein, “a portfolio of alliances consisting of ties

to organizations in a variety of different market niches may be more valuable than

an otherwise similar portfolio of alliances with firms in the same or similar niches”

(Stuart, 2000: 809). Furthermore, information and innovations are spread faster

and effectively in diverse (or “heterophilious” in his own use) networks (Rogers,

1995). The benefits derive from a diverse alliance portfolio, in turn, may provide

the firms with better chances to solve the problems, enhance social capital, and

explore new business opportunities (Fleming & Sorenson, 2001; Koka & Prescott,

2002; 2008; March, 1991).

Second, a diverse portfolio may facilitate creation of synergies among the

partners by combining complementary resources and capabilities (Madhok &

Tallman, 1998). A firm establishes alliances with other firms in its own industry

as well as across industries for strategic and social purposes (Eisenhardt &

Schoonhoven, 1996). When a focal firm has multiple partners that operate in the

same product markets or offer similar services and thus play a similar role in its

alliance portfolio, multilateral competition evolves in the alliance portfolio (Lavie,

- 42 -

2007: 1195). Given that alliance partners that operate in the same industry or in

the same market niche may be the current or the potential rivals who compete

with one another for limited resources and markets (Baum, Calabrese, &

Silverman, 2000), suspicion may replace trust in their relationship (Inkpen &

Tsang, 2005) and the looming competition may hinder collaboration between

them (Luo & Deng, 2009).

Either synergy- or conflict-creating interdependencies can occur between

partners within an alliance portfolio (Parise & Casher, 2003). Synergies between

partners in an alliance portfolio occur when partners affect one another positively,

while conflicts occur when partners affect one another negatively. According to

Parise and Casher (2003), conflicts are created because partners are rivals in an

industry or they promote competing technologies. Subsequently conflicts may be

more likely to occur in the alliance portfolios comprised of current or potential

rivals. On the other hand, in diverse portfolios that are composed of partners

across industries and market niches, cooperation rather than competion may

encourgae collaboration between partners, and thus synergies may be more likely

to occur. Integrating these insights, we suggest that diversity of an alliance

portfolio will have a positive effect on the partners in the alliance portfolio.

Hypothesis 2a: When a focal firm announces corporate events, the partner firms’

abnormal returns will be positively associated with diversity of the alliance

portfolio.

- 43 -

3.2.4. Portfolio diversity and environmental munificence

Firms secure resources from their environments in order to survive (Katz

& Kahn, 1966), and they can more easily obtain such needed resources in high

munificence than in low munificence environments (Randolph & Dess, 1984).

Therefore, the less munificent a firm’s environment the more effort the firm will