Embed Size (px)

Citation preview

Bundesverband Solarwirtschaft e.V. (BSW-Solar)

Value Chain Analysis of the PV Market in Pakistan

Project “Pakistan Solar Quality Potential“

Content

Project “Pakistan Solar Quality Potential“

The value chain analysis

• Energy situation & key stakeholders for PV development

• Key actors in the value chain

• PV import data

• Feedback from interviews & market research

• Market segments & perceptions

• Business environment for German PV companies

• Target segments for German PV companies

© BSW-Solar

German Solar Association:

© BSW-Solar

TASK To represent the solar industry in Germany in the

thermal and photovoltaic and storage sector

VISION A sustainable global energy supply provided by solar

(renewable) energy

ACTIVITIES Lobbying, political advice, public relations, market

observation, standardization

EXPERIENCE Active in the solar energy sector for over 30 years

REPRESENTS More than 800 solar producers, suppliers, wholesalers,

installers and other companies active in the solar

business from all over the world

HEADQUARTERS Berlin

Equipment Materials System

components

Wholesale & Distri-bution

Project Develop-

ment

Con-structi

on O&M

3

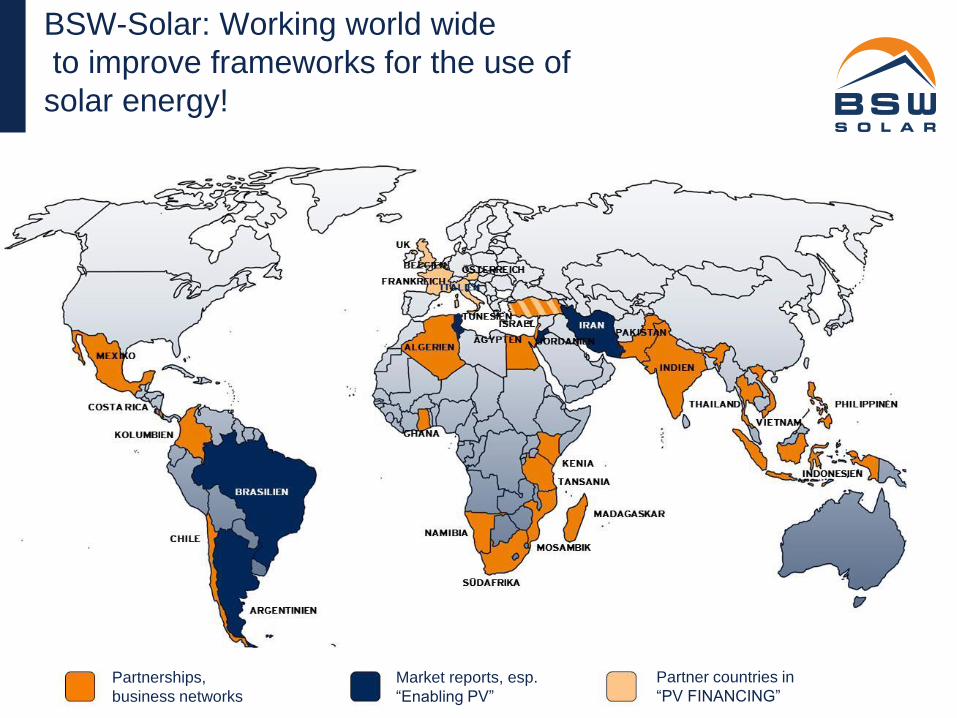

BSW-Solar: Working world wide

to improve frameworks for the use of

solar energy!

Partnerships,

business networks

Market reports, esp.

“Enabling PV”

Partner countries in

“PV FINANCING”

© BSW-Solar

The project: Pakistan Solar Quality

Potential

Objective

To achieve a sustainable quality demand of PV products,

through the improvement of the capacity building of local

institutions helping them to achieve an organizational structure

that allows them to continue with the dissemination of quality

standards and norms in Pakistan

• Duration: August – December 2016

• On behalf of the GIZ

• Partners: Pakistan Solar Association

© BSW-Solar

Project activities & outcomes

© BSW-Solar

Analyze the value chain of PV in Pakistan

Identification of the PV market potential & the needs of local stakeholders

Development of a training concept & awareness campaign

Target group of the trainings are installers and of the awareness campaign are the end customers

Identification of the key multipliers for dissemination

The pilot region is Lahore. Nevertheless, the training material will be generic and able to be used in all the country

Project activities & outcomes

© BSW-Solar

Conduction of trainings

To qualify key Pakistani multipliers for the application of the standards and norms. Focused on installers.

Strength cooperation between Pakistan & Germany

Bringing together relevant stakeholders including training institutions and industries in both countries

& disseminate the results with relevant stakeholders in both

countries

© BSW-Solar

The value chain analysis

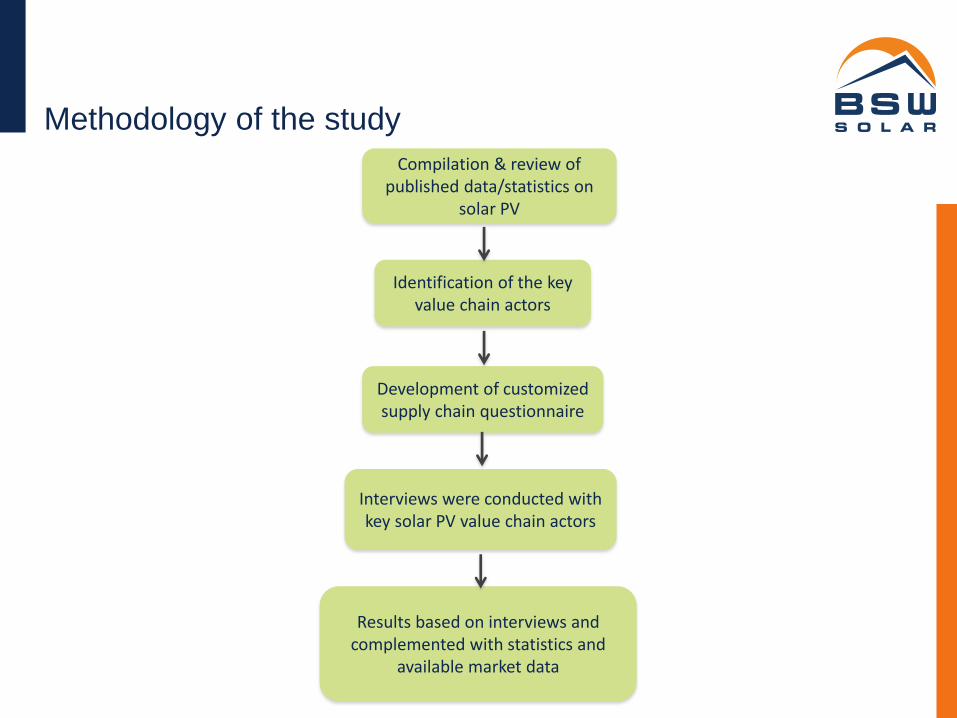

Methodology of the study

Development of customized supply chain questionnaire

Compilation & review of published data/statistics on

solar PV

Identification of the key value chain actors

Interviews were conducted with key solar PV value chain actors

Results based on interviews and complemented with statistics and

available market data

Solar irradiation levels - Pakistan

© BSW-Solar

High irradiation levels

Across the country (4.5-7.0 kWh/m2/day)

In particular: Punjab & Sindh provinces:

4.5 – 6.0 kWh/m2/day

High PV potential in both rural and

urban areas. Industry concentrated in

Punjab & Sindh provinces.

Source: CPPA, NEPRA and AEDB

Share of RES steadily

increasing each year

1136 MW of RES

installed by 2016,

mainly PV, wind and

micro/mini hydropower

2010 2011 2012 2013 2014 2015 2016

RE 50 106 408 1136

Nuclear 462 787 787 787 787 787 1.127

Thermal 14.240 15.753 15.888 15.852 16.963 16.963 16.814

Hydro 6.555 6.627 6.627 6.928 7.097 7.097 7.121

21,257 MW 23,167 MW 23,302 MW 23,617 MW 24,953 MW 25,255 MW 26,197 MW

RE

Nuclear

Thermal

Hydro

Power sector in Pakistan: installed capacity

Power sector in Pakistan: supply & demand scenario

Source: MoWP

The power deficit was near 5 GW in

summer 2016

Multiple power generation projects

from various sources are currently

in the pipeline and are envisaged to

eliminate the power deficit by 2019

- if expected projects are

completed on time

PV based projects can play a key

role in the elimination of the power

deficit, particularly in the industrial

and residential sectors.

19917

21599

25080

27600

30938

17500

14121

21096

18738

26590

23107

17107

24262

18262

25961

Capacity

Availability

Demand

Power sector in Pakistan: higher demand in the

domestic & industrial sector

© BSW-Solar

Source: Pakistan Energy Yearbook 2015

Increase of 11,000

GWh in the last 5

years, specially in the

domestic and industrial

sector

Significant and increasing energy demand in the country

Policy on FITs (Feed in tariffs) catalyzing project development

Introduction of net metering

Introduction of import quality standards

Financing available for PV

Rationale for PV development

Key stakeholders for PV development

Other stakeholders for PV development

• PSA (Pakistan Solar Association) : National trade body of Pakistan’s PV industry. The

association represents and promotes PV businesses in the country

• REAP (Renewable Energy Association of Pakistan): Non-profit organization currently

representing 400 members with the aim to promote renewable energy sources in Pakistan

• International donors/technical assistance programs

BMZ (German Ministry of Economic Cooperation)

GIZ (implementers on behalf of BMZ)

KfW bank

ADB (Asian Development Bank)

USAID (United States Agency for International Development)

JICA (Japan International Cooperation Agency)

ADB (Asian Development Bank)

European Commission

World Bank

UNDP (United Nations Development Program)

UNIDO

DFID

PV Value Chain Actors

Trend of import of PV panels: Oct’14 - Sept’15 vs.

Oct’15 - Sept’16

• Federal Board of Revenue (FBR), GoP, 2016

• Panel volume imported (MW) calculated based on 0.7 USD/Watt (FBR Valuation Ruling No. 620/2013)

Chinese PV panels have the highest share of imports into Pakistan which has increased between 2014 and 2016.

This is attributed to price competitiveness with similar products from other countries, extensive customer outreach

through dealership networks and a large variation in product quality/pricing which caters to different economic

classes of customers.

95.60% (975.3 MW)

0.62% (6.3 MW)

1.39% (14.1 MW)

0.40% (4 MW) 0.53% (5.4 MW)

1.47% (15 MW)

Oct'15 - Sept'16

China

UAE

Malaysia

Germany

HongKong

Others

94.98% (497 MW)

3.20% (16.7 MW)

0.22% (1.1 MW) 0.21% (1.1 MW)

1.40% (7.3 MW)

Oct'14 - Sept'15

China

UAE

Germany

Korea

Others

Trend of import of inverters: Oct’14 - Sept’15 vs.

Oct’15 - Sept’16

• Federal Board of Revenue (FBR), GoP, 2016 • Inverter volume imported (MW) calculated based on 37.5 USD/kW (FBR Valuation Ruling No. 751/2015) • Inverter statistics presented are for all inverters imported into country (i.e. for use with PV systems and also for use as

UPS for charging only from the grid )

Chinese inverters have highest share of imports into Pakistan which has increased between 2014 and 2016. The

reasons behind this dynamic are the same as in the case of import of PV panels i.e. price competitiveness with

similar products from other countries, extensive dealership networks and a large variation in product quality/pricing which caters to different economic classes of customers.

65.01% (1007.4 MW)

3.11% (48.1 MW)

2.86% (44.3 MW)

6.01% (93.2 MW)

2.55% (39.5 MW)

20.46% (317.1 MW)

Oct'14-Sept'15

China

UAE

UK

Germany

Finland

Others

71.54% (1328.8 MW)

6.93% (128.8 MW)

4.21% (78.3 MW)

3.17% (58.9 MW)

2.58% (47.9 MW)

2.16% (40.1 MW)

2.13% (39.5 MW)

7.28% (135.1 MW)

Oct'15-Sept'16

China

Germany

Finland

UAE

Other EUStates

UK

Italy

Others

Trend of import of charge controllers: Oct’14 - Sept’15

vs. Oct’15 - Sept’16

• Federal Board of Revenue (FBR), GoP, 2016 • Charge controller volume imported (MW) calculated based on 37.5 USD/kW (FBR Valuation Ruling No. 751/2015)

High proportion of ‘Chinese’ Charge controllers being imported into the country with the same reasons behind

this dynamic as those already cited above for the case of PV panels and inverters. Overall volume of Charge

controllers imported from Germany has increased over the last year, although there has been a minor decrease in the market share

36.03 % (211.1 MW)

25.86 % (151.5 MW)

23.58 % (138.1 MW)

4.47 % (26.2 MW)

3.35 % (19.6 MW) 6.72 % (39.4 MW)

Oct'14 - Sept'15

China

Germany

USA

Singapore

Italy

Others

32.78 % (237.7 MW)

21.98 % (159.4 MW)

19.37 % (140.5 MW)

7.02 % (50.9 MW)

5.96 % (43.2 MW)

2.60 % (18.9 MW)

2.41 % (17.5 MW)

2.04 % (14.8 MW)

5.83 % (42.3 MW)

Oct'15 - Sept'16

China

Germany

USA

Italy

Other EUstates

UAE

Turkey

Sweden

Others

• Federal Board of Revenue (FBR), GoP, 2016 • Deep cycle battery volume imported (tonnes) calculated based on 1.72 USD/ kg (FBR Valuation Ruling No. 723/2015)

High proportion of Chinese ‘deep cycle’ batteries being imported into the country with the same reasons

behind this dynamic as those already cited above for the case of PV panels and inverters. Overall volume of

batteries imported from Germany has increased over the last year, although there has been a minor decrease in the market share

85.13% (24,970 t)

3.24% (950.0 t)

3.03% (888.1 t)

3.70% (1086.6 t)

1.81% (530.6 t) 0.98% (286.4 t) 0.47% (137 t)

1.65% (483.2 t)

Oct'15 - Sept'16

China

Vietnam

USA

Korea

Singapore

Other EUstatesGermany

Others

Trend of import of deep cycle’ batteries: Oct’14 -

Sept’15 vs. Oct’15 - Sept’16

82.44 % (19,900 tonnes)

5.17% (1249 t)

2.62% (634.3 t)

1.97% (475.2 t)

2.57% (621.3 t)

1.03% (247.9 t)

0.49% (117.4 t)

3.71% (899.8 t)

Oct'14 - Sept'15

China

USA

Vietnam

France

Korea

UK

Germany

Others

Results based on interviews and market

research

© BSW-Solar

Results based on interviews with PV key value chain actors (wholesalers, importers, installers, retailers etc.) and on market research. The list is not exhaustive and may not include all available brands. The component brands are listed in no particular order. Considering the scope of this study, it was not possible to assess the specific market share of each respective brand mentioned here. Classification of equipment into ‘Tiers’ is currently not possible, due to the lack of quality standards in Pakistan.

Inverters Batteries PV panels

Yingli (China)

Kyocera (Japan)

Rene Sola (China)

LG (Korean)

JA Solar (China)

Canadian Solar (China)

Alfa Solar (Germany)

Hitek (UK)

Jinko Solar (China)

GH (Belgium)

Trina Solar (China)

Solar World (Germany)

Phono (China)

Beyond PV (Taiwan)

Eurener (Spain)

Hanergy (China)

Shanghai Solar (China)

Long (Vietnam)

Hoppeke (German)

Powersonic (China)

Trojan (USA)

Narada (China)

Baykee (China)

JTE (China)

CSB (Taiwan)

Huawei (China)

Sunny Power (China)

Inti Power (China)

Voltronic (Taiwan)

Schneider Electric (French)

Sacred Sun (China)

SMA (Germany)

ABB (Swedish-

Swiss)

Outback (USA)

Nedap (Holland)

Sungrow (China)

Baykee (China)

Studer (Swiss)

TBB Power (China)

Fronius (Austria)

Victron (Holland)

I-Energy (Taiwan)

Kaco New Energy (Germany)

PV products & service range in Pakistan

imported brands available

* Results based on interviews with PV key value chain actors (importers, wholesalers, retailers, installers etc.) and on market research

PV products & service range in Pakistan

• Chinese products have a considerable market share of the PV market in the country

with over 90 % of the PV panels and over 80 % of the ‘deep cycle’ batteries. This is

attributed to the price competitiveness with similar products from other countries, extensive

dealership networks and a large variation in product quality/pricing which caters to different

economic classes of customers.

• Considerable variation in quality and price of PV products (panels, batteries, inverters)

being imported from China

• There is a niche in every market sector (industrial, commercial and residential) that

requires high quality and reliable PV products, particularly inverters and batteries. These

elements of the market constitute the target customer group for European products.

• Most existing and potential users of PV from the industrial sector in Pakistan claim to prefer

European products since they are bankable and more reliable. However, currently they

purchase Chinese products (PV panels and inverters) due to the high costs of the

European products and the limited offer of after-sales services in comparison to the

Chinese ones.

Local ‘assembly’ of panels being conducted by five companies in Pakistan. However, imported panels manufactured by reputed brands are currently preferred due to the higher reliability and trust enjoyed by foreign brands

No

Panels

Local manufacturing

Yes

Limited volumes and questionable quality

Import of PV panels

Low quality panels (low cost brands & smuggled) High quality panels (reputed brands)

Customers NOT satisfied with performance of local panels (efficiency versus price)

* Results based on interviews with PV key value chain actors (wholesalers, importers, retailers, installers etc.)

Local assembly

PV products & service range in Pakistan: panels

Manufacturing of AGM batteries is expected to commence soon in Pakistan with four different industrial groups

setting up factories in the southern Pakistani city of Karachi:

Daewoo Group

Treet Group

Eco Star (DWP & GREE Groups)

Homage

* Results based on interviews with PV key value chain actors (wholesalers, importers, installers, retailers etc.) ** Rough estimates based on feedback collected during interviews and market research. Detailed surveys are necessary to determine more accurate statistics regarding the battery landscape in Pakistan.

Imported battery

(≅40%)**

Sub-standard (≅70%) ** (Low grade Chinese)

High quality (≅30%)** (High-end European, American,

Chinese)

Local battery (≅60%)**

Landscape of batteries for PV systems in Pakistan

Sub-standard (≅100%)** (Lead acid car batteries)

High quality (Yet to start manufacturing)

PV products & service range in Pakistan: batteries

Results: customer awareness

Question: What is the general level of ‘Customer awareness’ related to PV products in Pakistan?

:

• ‘Low’ level of awareness (≤2) : 23%

• ‘Moderate’ level of awareness (>2≤5): 67%

• ‘High’ level of awareness (>5≤10): 10%

Note: ‘Customers’ collectively refers to clients from the residential, commercial, industrial and public sectors

Awareness scale (0 to 10) 0: Unaware 10: Aware

23%

67%

10%

≤2

>2≤5

>5≤10

Results based on interviews with PV key value chain actors (wholesalers, importers, installers, retailers etc.)

Results: payback expectations

Question: What are the ‘Payback expectations’ from PV products of the different customer segments in the

Pakistani market?

Note: ‘Customers’ collectively refers to clients from the residential, commercial, industrial and public sectors

The shortest payback expectations

are for the commercial sector (3.5

years), followed by the industrial

sector (4.5 years)

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

5,0

Commercial Residential Industrial Public Sector

3.5 years

5 years

4.5 years

5 years

Pay

bac

k Ti

me

(ye

ars)

Target Sector for PV Products

Results based on interviews with PV key value chain actors (wholesalers, importers, installers, retailers etc.)

Question: What is the proportion of ‘Certified’ PV components in the local market?

0

2

4

6

8

10

12

14

16

18

20

Inverter Battery Panel

14%

9%

20%

Pro

po

rtio

n o

f C

ert

ifie

d C

om

po

ne

nts

in P

ak M

arke

t

Solar system components

Exact statistics on the specific brands and their respective volumes being imported into Pakistan are only available with the customs authorities. However, this information is

restricted and classified.

Low proportion of ‘certified’ PV components available in the local market

Results based on interviews with PV key value chain actors (wholesalers, importers, installers, retailers etc.)

Results: certified PV components

Perception of the PV market segments

http://www.sbp.org.pk/smefd/circulars/2016/C3.htm

Commercial Industrial

Typical installation size

1 MW – 10 MW

High potential industries & locations

• Textile (spread across Punjab province)

• Sports (focused in Sialkot city)

• Food industry (across the country)

• Pharmaceutical industry (Karachi)

Possible project financing models

• Financing through recently announced scheme for

RE project financing by State bank of Pakistan.

Loans being offered at 6% for solar PV projects up to

50 MW

• Conventional financing through lending from bank

along with equity from project developer

Product preferences

Based on past trends, industry prefers to install reliable

and high quality components to ensure project

bankability.

SMA, Schneider and ABB quite popular in terms of

reliability compared to Chinese products

Typical installation size

100 kW – 1 MW

High potential segments & locations

• Hospitals (across the country)

• Private educational institutions

• Hotels & restaurants (across the country)

• General provision stores (across the country)

Possible project financing models

• Financing through recently announced Scheme

for RE project financing by State bank of

Pakistan. Loans being offered at 6% for solar PV

projects up to 50 MW

• Conventional financing through lending from

bank along with equity from project developer

• Equity

Product preferences

In the past, tendency to install cheaper and less

reliable quality Chinese brands. However, slowly

trend moving towards increasing awareness leading

to installation of SMA, Schneider and ABB due to

high level of reliability

Results based on interviews with PV key value chain actors (wholesalers, importers, installers, retailers etc.)

Perception of the PV market segments

1. http://www.sbp.org.pk/smefd/circulars/2016/C3.htm

Residential Public sector (Government funded)

Typical installation size

1 kW – 20 kW

High potential locations

• Urban centers (Karachi, Lahore, Islamabad, Rawalpindi,

Faisalabad, Multan, Hyderabad)

• 40,000 un-electrified off-grid villages across the country

• Agricultural areas across Punjab, Sindh and KPK

provinces owned by farmers with land holdings of different

sizes

Possible Project Financing Models

• Financing through recently announced scheme for RE

project financing by State bank of Pakistan. Loans being

offered at 6 percent1 for solar PV projects up to 50 MW

• Equity

• Funding through donor projects in off-grid areas

Product Preferences

High price sensitivity exists with niche market for ‘high

quality’ and certified products. Large proportions of clients in

this sector opting for Chinese products although increasing

interest in ‘certified’ high quality products as result of ‘lessons

learnt’

Typical installation size

50 kW – 200 kW

High potential segments & locations

• Public hospitals & health facilities

• Government educational institutions (across the

country)

• Public parks and recreation facilities (across the

country)

• Public offices (across the country)

Possible project financing models

• Public financing from national approved budget as per PC-

1 document

• Grant aid from international donor agencies

Product preferences

Tendency remains to maximize project size within allocated

budget. Also, ‘open’ tenders bidding mechanism based on

awarding project to ‘lowest’ bidder results in high quality and

durable products losing out to competitors offering lower

quality products

* Results based on interviews with PV key value chain actors (wholesalers, importers, installers, retailers etc.)

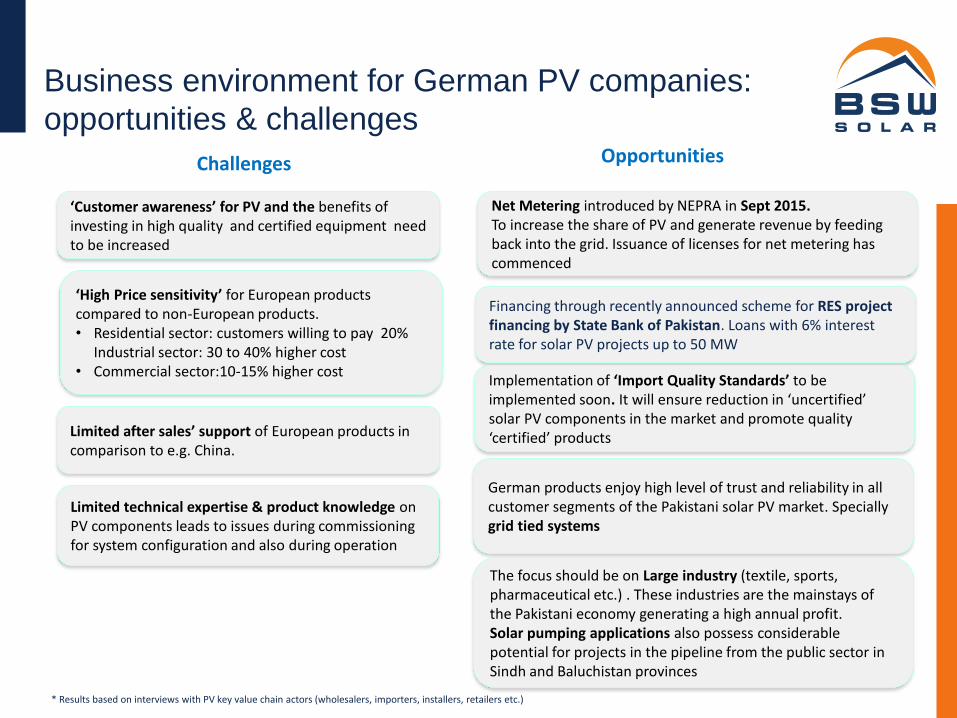

Net Metering introduced by NEPRA in Sept 2015. To increase the share of PV and generate revenue by feeding back into the grid. Issuance of licenses for net metering has commenced

Challenges Opportunities

Financing through recently announced scheme for RES project financing by State Bank of Pakistan. Loans with 6% interest rate for solar PV projects up to 50 MW Implementation of ‘Import Quality Standards’ to be implemented soon. It will ensure reduction in ‘uncertified’ solar PV components in the market and promote quality ‘certified’ products

Limited technical expertise & product knowledge on PV components leads to issues during commissioning for system configuration and also during operation

Limited after sales’ support of European products in comparison to e.g. China.

‘High Price sensitivity’ for European products compared to non-European products. • Residential sector: customers willing to pay 20%

Industrial sector: 30 to 40% higher cost • Commercial sector:10-15% higher cost

‘Customer awareness’ for PV and the benefits of investing in high quality and certified equipment need to be increased

German products enjoy high level of trust and reliability in all customer segments of the Pakistani solar PV market. Specially grid tied systems

The focus should be on Large industry (textile, sports, pharmaceutical etc.) . These industries are the mainstays of the Pakistani economy generating a high annual profit. Solar pumping applications also possess considerable potential for projects in the pipeline from the public sector in Sindh and Baluchistan provinces

* Results based on interviews with PV key value chain actors (wholesalers, importers, installers, retailers etc.)

Business environment for German PV companies:

opportunities & challenges

Technical consulting services

(techno-economic feasibility studies, grid

connection studies, support in project tendering process, monitoring of

commissioned projects, maintenance and operation of large scale grid connected &

medium scale PV projects) Batteries (Flooded or AGM) The residential, off-grid & the commercial sector installations requiring battery back up. Installed system are expected to scale

up to use the economic benefits of net metering and will require larger battery

banks. (Potential for high quality batteries exists but price competitiveness will other comparable products will be critical)

‘Grid tied’ inverters for use in medium scale (100kW-1 MW) and large scale (>1 MW) grid connected projects being set up by industrial and commercial sectors. (Price competitiveness with comparable products from other countries will be critical)

Products Services

PV testing & monitoring equipment (battery testers, PV panel testers, PV

analyzers, PV panel flash test equipment)

EPC Companies for developing both commercial sector

(kW scale) and large scale (>1 MW) grid connected projects

EPC contracting companies with a strong profile of developing large scale projects are in high demand

Results based on interviews with PV key value chain actors (wholesalers, importers, installers, retailers etc.)

Target segments for German PV products & services

Nr. IEC Standards Title

1 IEC 61646:2008 Thin-film terrestrial photovoltaic (PV) modules design qualification and type approval

2 IEC 61439-1:2011 Low-voltage switchgear and Control gear assemblies – Part 1: General rules

3 IEC 60947-

3:2008+A1:2012

Low voltage switchgear and control gear – Part 3: switches, disconnections, switch

disconnections and fuse combination units

4 IEC: 62103:2003 Electronic equipment for use in power installations (e.g. EN 50178:1998)

5 IEC: 62930 Electric cables for photovoltaic systems (BT(DE/NOT)258)(e.g EN 50618)

6 IEC 62103 (2003-07)

Ed.1.0

Electronic equipment for use in power installations

7 IEC 61701:2011 Salt mist corrosion testing of photovoltaic (PV) modules

8 IEC 62116:2014 Protection against islanding of Grid (Utility-interconnected photovoltaic inverters –

procedure of islanding prevention measures)

9 IEC 61683: 1999 Photovoltaic systems – Power conditioners – Procedure for measuring efficiency

10 IEC 62509:2010 Battery charge controllers for photovoltaic systems – Performance and functioning

Adopted as Pakistan standard in 94th electro-technical national standards committee meeting held on October 21st, 2015. Implementation of these standards has yet to commence.

IEC quality standards

Nr. IEC Standards Title

11 IEC 62093:2005 Balance-of-system components for photovoltaic systems – natural

environments

12 IEC 62124: 2004 Photovoltaic (PV) stand alone systems – Design verification

13 IEC 62253: 2011 Photovoltaic pumping systems – Design qualification and

measurements

14 IEC 62257 (2013) Recommendations for small renewable energy and hybrid systems for

electrification – Part 1: General introduction to IEC 62257 series and

electrification

15 IEC/TS 62257-9-5: 2013 (E) Recommendations for small renewable energy and hybrid systems for

electrification – Part 9-5: Integrated system – Selection of stand-alone

lighting kits for rural electrification

Adopted as Pakistan standard in 94th electro-technical national standards committee meeting held on October 21st, 2015. Implementation of these standards has yet to commence.

IEC quality standards

Nr. IEC Standards Title

1 IEC 62109-1:2010 Safety of power converters for use in photovoltaic power systems –

General requirements

2 IEC 62109-2:2011 Safety of power converters for use in photovoltaic power systems –

Particular requirements for inverters

3 IEC 61730-1:2004 Photovoltaic (PV) module safety qualification – Part 1: Requirements

construction

4 IEC 61730-2:2004 Photovoltaic (PV) module safety qualification – Part 2: Requirements

testing

5 IEC 61439-1: 2011 Low-voltage switchgear and Control gear assemblies – Part 1:

Adopted as Pakistan standard in 94th electro-technical national standards committee meeting held on October 21st, 2015. Implementation of these standards has yet to commence.

IEC safety standards

Nr. IEC Standards Title

1 IEC 61000-6-4:2006 + A1:2010 Electromagnetic compatibility (EMC) – Part 6-4: Generic standards –

Emission standard for industrial environments

2 IEC 61000-6-1:2006+ A1:2010 Electromagnetic compatibility (EMC) – Part 6-1: Generic standards –

Immunity for residential, commercial and light-industrial

applicable)

3 IEC 61000-6-3:2006 + A1:2010 Electromagnetic compatibility (EMC) – Part 6-3: Generic standards –

Emission standard for residential, commercial and light industrial

environments (if applicable)

4 IEC 60068-2 Environmental Testing (more than 70 standards in this series (From

2-1 to 60068-2-83)

Adopted as Pakistan standard in 94th electro-technical national standards committee meeting held on October 21st, 2015. Implementation of these standards has yet to commence.

IEC environmental standards

Luz Alicia Aguilar

International Project Manager

German Solar Association

Phone: +49 (30) 29 777 88-40

E-Mail: [email protected]

© BSW-Solar