Embed Size (px)

Citation preview

Value-Added Taxation in Canada: Advanced Topics

April 28, 2016

(This page is intentionally left blank)

April 2016

Value-Added Taxation in Canada: Advanced Topics

Contents Page numbers

1) Introduction 2

2) Place of Supply Rules a) Taxable supplies made in Canada 6 b) HST and QST place of supply 9

(1) Real property 10 (2) Intangible personal property 11 (3) Service in respect of tangible personal property or real property 17

3) Taxation of imports

a) Importation of goods 24 b) Services and intangible personal property 28 c) Self-assessing HST and QST on imports 30

4) Recovery of tax on import 33

5) Taxation of exports

a) Export of goods 46 b) Export of services 48 c) Export of intangible personal property 57 d) Export trading house 59 e) Exporters of processing services 60

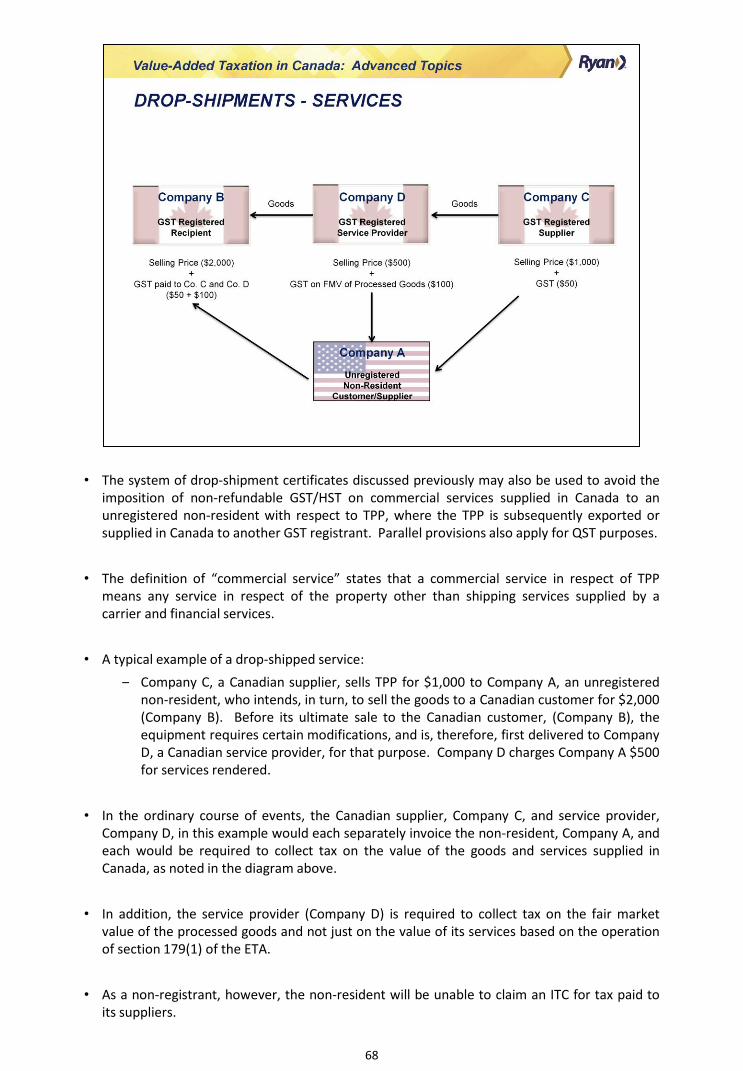

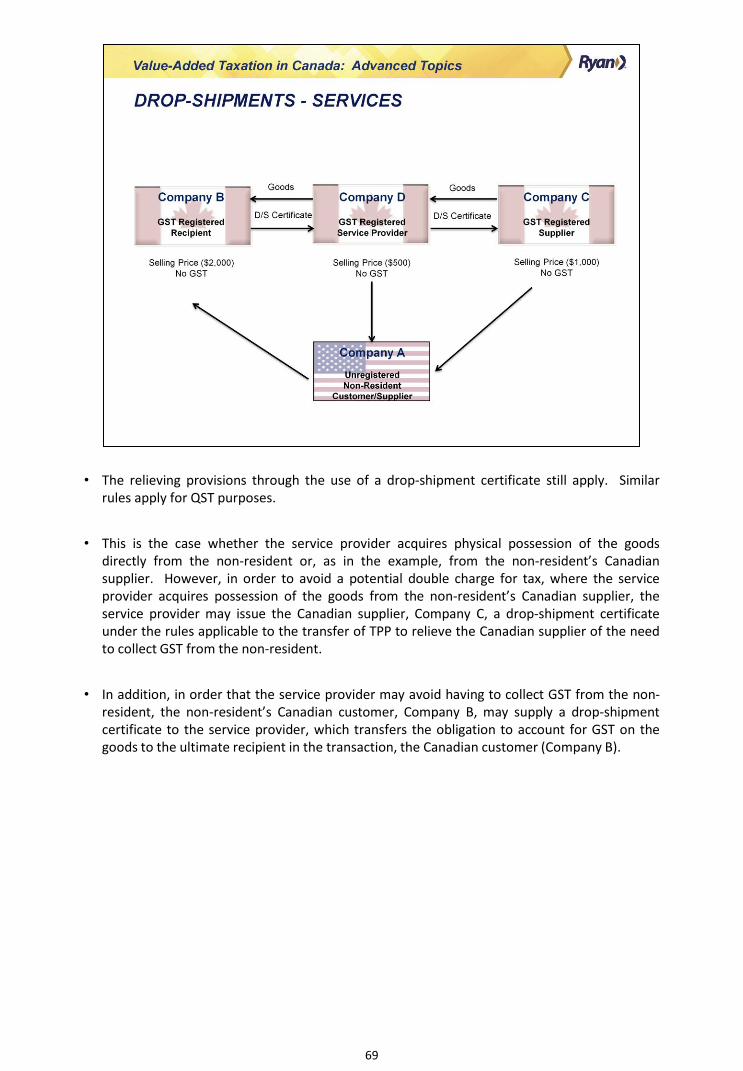

6) Drop-shipments 61

7) Pension plans 70

April 2016

Value-Added Taxation in Canada: Advanced Topics

Reference Materials

A. Excerpts of Canada Revenue Agency, Draft GST/HST Technical Information Bulletin B-103, June 2012, “Harmonized Sales Tax - Place of supply rules for determining whether a supply is made in a province”

B. GST Memoranda, 300-9 “Imported Services and Intangible Property”

C. GST/HST Memoranda Series, 4.5.3 “Exports – Services and Intellectual Property”

D. GST/HST Memoranda Series, 3.3.1 “Drop-Shipments”, June 2008 – Appendix B only (drop-

shipment certificate)

E. GST/HST Technical Information Bulletin, B-108 “Changes to GST/HST Rules for Pension Plans – New Section 157 and Amendments to Section 172.1”

April 2016

Value-Added Taxation in Canada: Advanced Topics

Glossary of Terms CBSA: Canada Border Services Agency CRA: Canada Revenue Agency ETA: Excise Tax Act GST: Goods and Services Tax HST: Harmonized Sales Tax IPP: Intangible personal property ITA: Income Tax Act ITC: input tax credit ITR: input tax refund PSB: public service body PVAT: provincial component of HST QST: Québec Sales Tax QSTA: an Act respecting the Québec sales tax RITC: recapture of input tax credits (provincial component) SAM: Special Attribution Method SLFI: Selected Listed Financial Institution TPP: Tangible personal property

(This page is intentionally left blank)

1

2

3

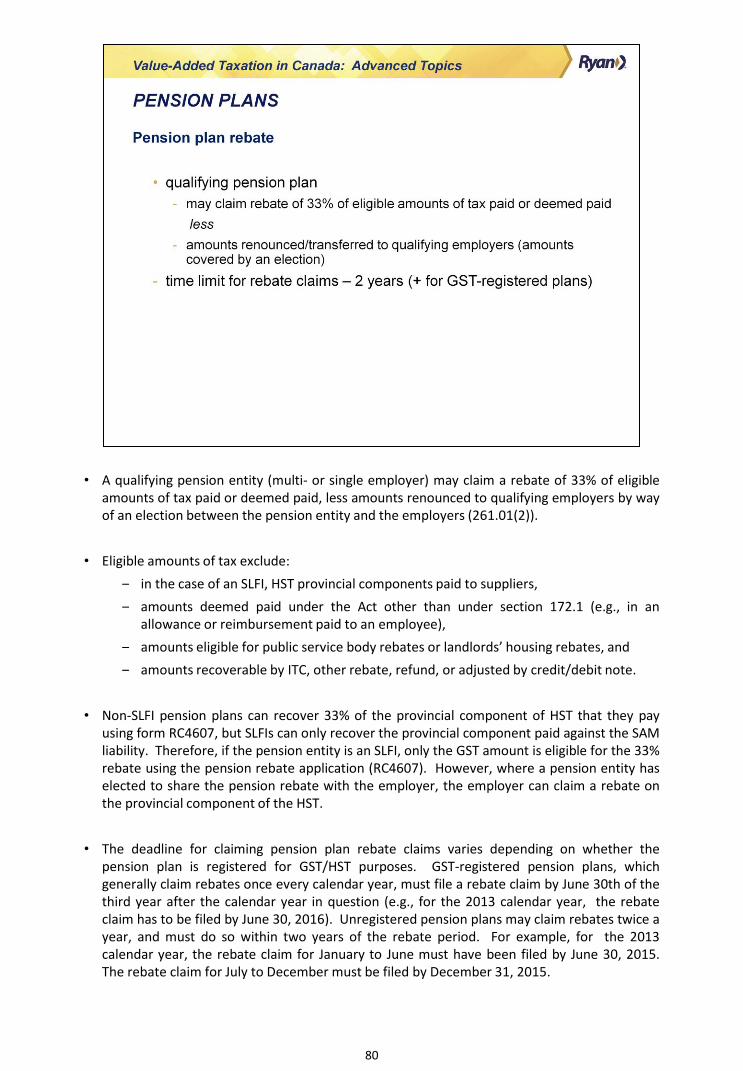

• The GST is a value-added tax which applies to most goods and services sold at every level in the production, marketing and distribution chain. It is designed to be paid by the ultimate consumer or purchaser, but since it is levied at every stage in the business cycle, it impacts almost every organization doing business in Canada.

• GST/HST is collected on supplies of property and services made in, and imported into, Canada. Tax is payable by the recipient of a supply at the time the consideration is paid or becomes payable. A supply can include goods, services, intangibles and real property. Services include everything other than property (including goods, real property and intangibles), money and salaries or wages.

• The participating (or “harmonized” provinces), meaning provinces that have adopted HST, receive federal transfer payments for having surrendered their right to collect provincial sales taxes. They do not receive the provincial component of the HST directly.

• HST is effectively GST at a higher rate, and generally applies to the same tax base. Its application includes supplies made, or deemed to be made, in the five participating provinces (Prince Edward Island (14%, effective April 1, 2013), Newfoundland and Labrador (13% [increasing to 15% effective January 1, 2016]), New Brunswick (13%), Nova Scotia (15%), and Ontario [13%, effective July 1, 2010]). In its 2016 budget, the province of New Brunswick announced that they will be increasing their HST rate to 15%, effective July 1, 2016.

• HST is remitted with an organization’s GST remittances to the federal government. Most registrants are not required to separately track the tax paid or collected at each rate.

• To accommodate further provincial harmonization, legislative amendments were made to the HST to permit other provinces to join the system at an agreed-upon rate.

4

• Québec was the first province to attempt a synchronization of its provincial sales tax with the GST. Like GST, QST is designed to be paid by the ultimate consumer or purchaser. This tax is also levied at each stage in the production, marketing, and distribution chain. It is collected by QST registrants on the value of the consideration for the supply. QST registrants engaged in commercial activities are generally eligible to recover QST paid on inputs, subject to certain restrictions.

• As of January 1, 2013, the QST rate is 9.975%, and is no longer calculated on the GST-included amount. This new rate is equal to the effective tax rate when the tax rate was 9.5% and charged on the GST-included amount. Without this increase, Québec would likely have faced declining tax revenue from the QST.

• Under an agreement that took effect on January 1, 2013, although Revenu Québec continues to administer the QST, the GST/HST and QST rules and tax bases became more harmonized, and as a result, outcomes produced by the QST legislation are almost identical to those produced by the GST/HST rules, with some limited exceptions.

• One major difference that still exists is Québec’s temporary restrictions on input tax refund (“ITR”) claims for large businesses. In addition, due to unique aspects of Québec’s Civil Code, terminology used in an Act respecting the Québec sales tax (“QSTA”) differs from terms used in the Excise Tax Act (“ETA”). Although not exactly synonymous, several terms used in the QSTA have rough equivalents in the ETA, including: corporeal movable property and tangible personal property (“TPP”); immovables and real property; and incorporeal movable property and intangible personal property (“IPP”).

5

Reference:

• Canada Revenue Agency Draft GST/HST Technical Information Bulletin B-103, June 2012, “Harmonized Sales Tax – Place of Supply Rules for Determining Whether a Supply is Made in a Province”.

6

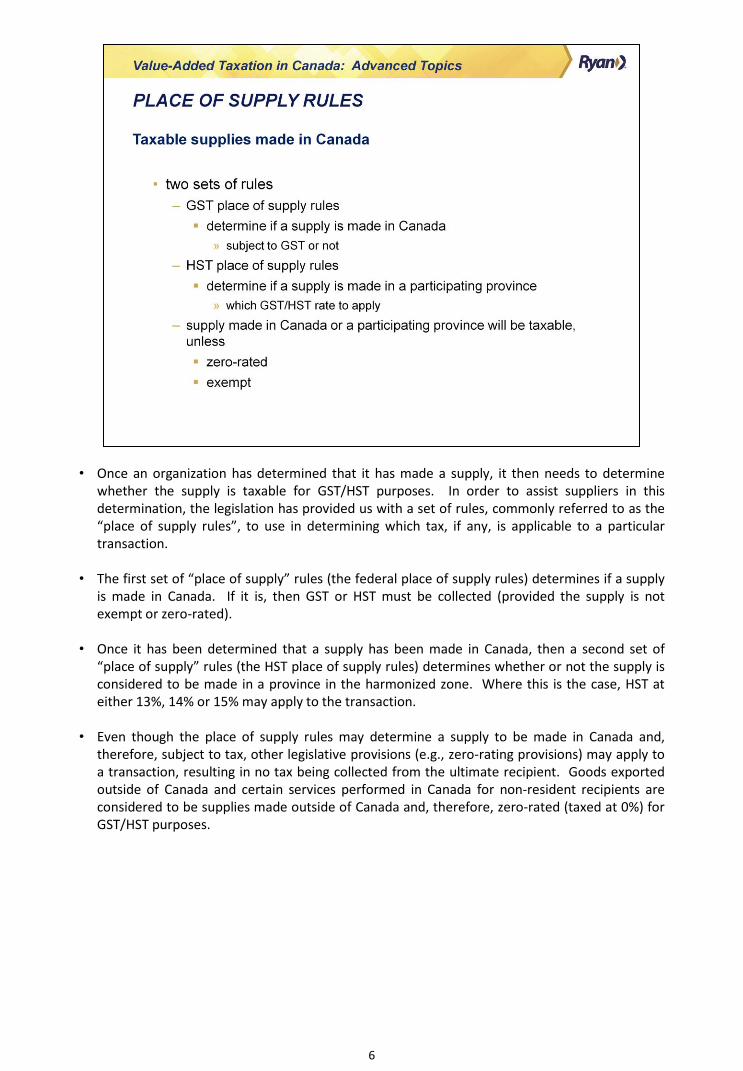

• Once an organization has determined that it has made a supply, it then needs to determine whether the supply is taxable for GST/HST purposes. In order to assist suppliers in this determination, the legislation has provided us with a set of rules, commonly referred to as the “place of supply rules”, to use in determining which tax, if any, is applicable to a particular transaction.

• The first set of “place of supply” rules (the federal place of supply rules) determines if a supply is made in Canada. If it is, then GST or HST must be collected (provided the supply is not exempt or zero-rated).

• Once it has been determined that a supply has been made in Canada, then a second set of “place of supply” rules (the HST place of supply rules) determines whether or not the supply is considered to be made in a province in the harmonized zone. Where this is the case, HST at either 13%, 14% or 15% may apply to the transaction.

• Even though the place of supply rules may determine a supply to be made in Canada and, therefore, subject to tax, other legislative provisions (e.g., zero-rating provisions) may apply to a transaction, resulting in no tax being collected from the ultimate recipient. Goods exported outside of Canada and certain services performed in Canada for non-resident recipients are considered to be supplies made outside of Canada and, therefore, zero-rated (taxed at 0%) for GST/HST purposes.

7

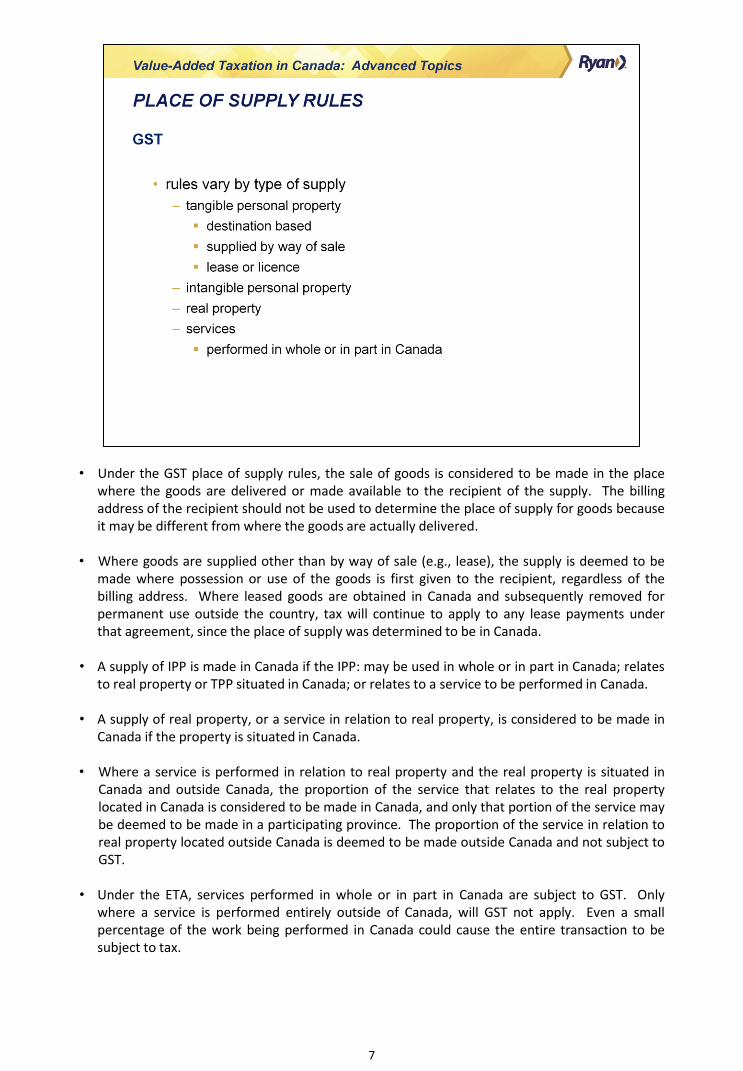

• Under the GST place of supply rules, the sale of goods is considered to be made in the place where the goods are delivered or made available to the recipient of the supply. The billing address of the recipient should not be used to determine the place of supply for goods because it may be different from where the goods are actually delivered.

• Where goods are supplied other than by way of sale (e.g., lease), the supply is deemed to be made where possession or use of the goods is first given to the recipient, regardless of the billing address. Where leased goods are obtained in Canada and subsequently removed for permanent use outside the country, tax will continue to apply to any lease payments under that agreement, since the place of supply was determined to be in Canada.

• A supply of IPP is made in Canada if the IPP: may be used in whole or in part in Canada; relates to real property or TPP situated in Canada; or relates to a service to be performed in Canada.

• A supply of real property, or a service in relation to real property, is considered to be made in Canada if the property is situated in Canada.

• Where a service is performed in relation to real property and the real property is situated in Canada and outside Canada, the proportion of the service that relates to the real property located in Canada is considered to be made in Canada, and only that portion of the service may be deemed to be made in a participating province. The proportion of the service in relation to real property located outside Canada is deemed to be made outside Canada and not subject to GST.

• Under the ETA, services performed in whole or in part in Canada are subject to GST. Only where a service is performed entirely outside of Canada, will GST not apply. Even a small percentage of the work being performed in Canada could cause the entire transaction to be subject to tax.

8

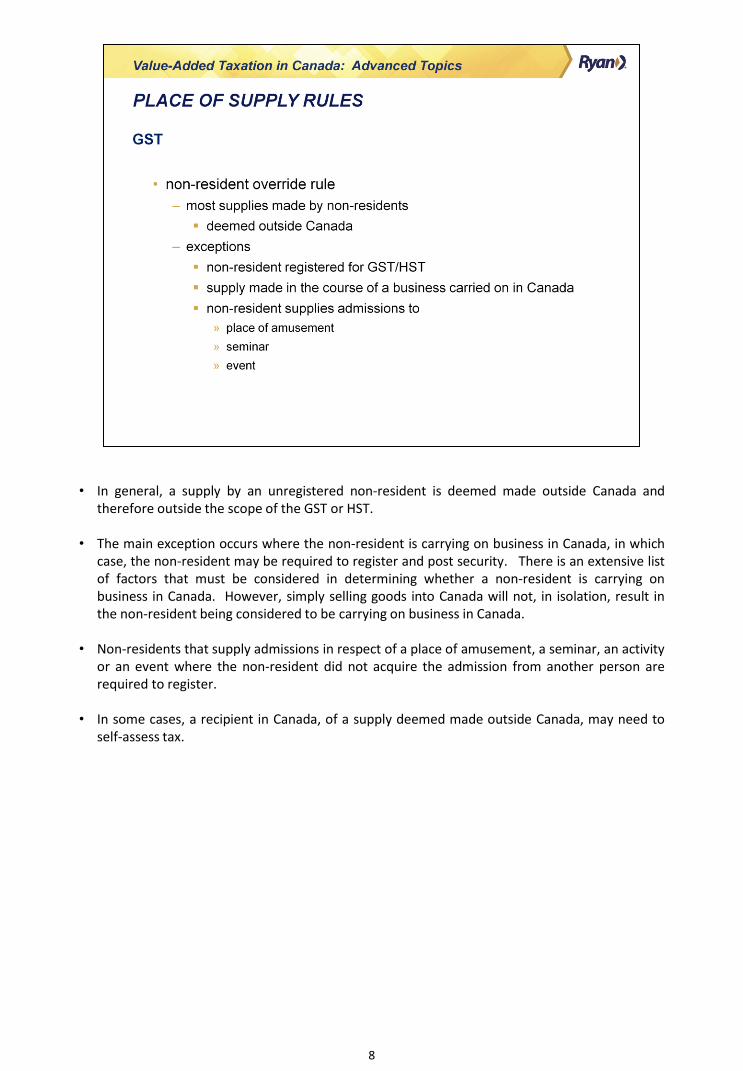

• In general, a supply by an unregistered non-resident is deemed made outside Canada and

therefore outside the scope of the GST or HST.

• The main exception occurs where the non-resident is carrying on business in Canada, in which case, the non-resident may be required to register and post security. There is an extensive list of factors that must be considered in determining whether a non-resident is carrying on business in Canada. However, simply selling goods into Canada will not, in isolation, result in the non-resident being considered to be carrying on business in Canada.

• Non-residents that supply admissions in respect of a place of amusement, a seminar, an activity or an event where the non-resident did not acquire the admission from another person are required to register.

• In some cases, a recipient in Canada, of a supply deemed made outside Canada, may need to self-assess tax.

9

• The place of supply rules for HST and QST are similar. Where a supply that is made in Canada is made in a participating province or Québec, the supply will be subject to HST or QST (plus GST), depending upon the province in which the supply has been made.

• As with the GST place of supply rules, the HST and QST place of supply rules vary by type of supply.

• The HST and QST place of supply rules for TPP and a general supply of services is explained in our introductory Value-Added Taxation in Canada seminar.

• This seminar will introduce the rules for supplies of real property, IPP and several of the place of supply rules that apply to many specific services.

10

• Tax applies to most goods and services, including supplies of real property. Certain exemptions exist for qualifying supplies of real property, but they are generally limited to used residential real property and certain personal-use real property sold by individuals.

• Complicating the tax treatment of supplies of real property are the “reverse collection” rules in place for most supplies of real property. Under the general rule, a supplier is required to collect and remit tax on the value of a supply. For suppliers of real property, the rule is often reversed and it is the purchaser who is required to remit the tax. This will occur where:

‒ the supplier is a non-resident; or ‒ the recipient is registered for the tax, provided the sale is not a residential complex or a

cemetery plot or similar site made to an individual.

• Where the purchaser is required to remit tax in respect of the acquisition of real property, it may be remitted by most organizations on the regular GST/HST return for the reporting period in which the tax becomes payable.

• A recipient may not relieve itself of its obligation to self-assess tax on supplies of real property by paying it to the supplier. Tax paid to the supplier in this situation would be considered tax paid in error.

11

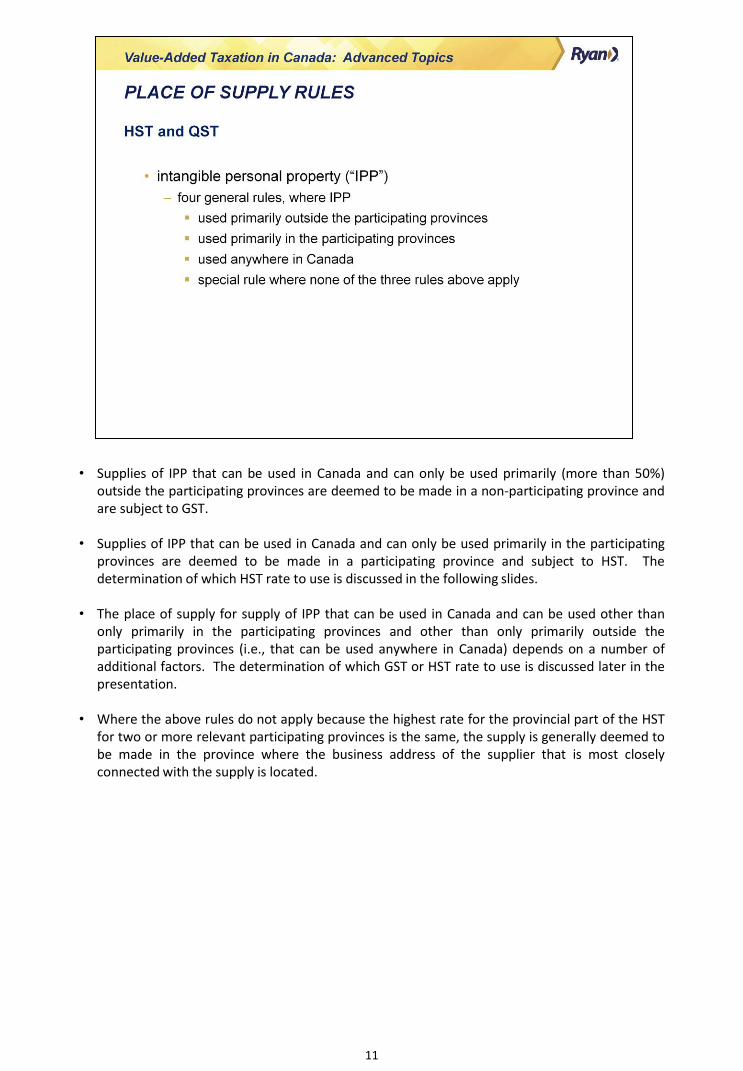

• Supplies of IPP that can be used in Canada and can only be used primarily (more than 50%) outside the participating provinces are deemed to be made in a non-participating province and are subject to GST.

• Supplies of IPP that can be used in Canada and can only be used primarily in the participating provinces are deemed to be made in a participating province and subject to HST. The determination of which HST rate to use is discussed in the following slides.

• The place of supply for supply of IPP that can be used in Canada and can be used other than only primarily in the participating provinces and other than only primarily outside the participating provinces (i.e., that can be used anywhere in Canada) depends on a number of additional factors. The determination of which GST or HST rate to use is discussed later in the presentation.

• Where the above rules do not apply because the highest rate for the provincial part of the HST for two or more relevant participating provinces is the same, the supply is generally deemed to be made in the province where the business address of the supplier that is most closely connected with the supply is located.

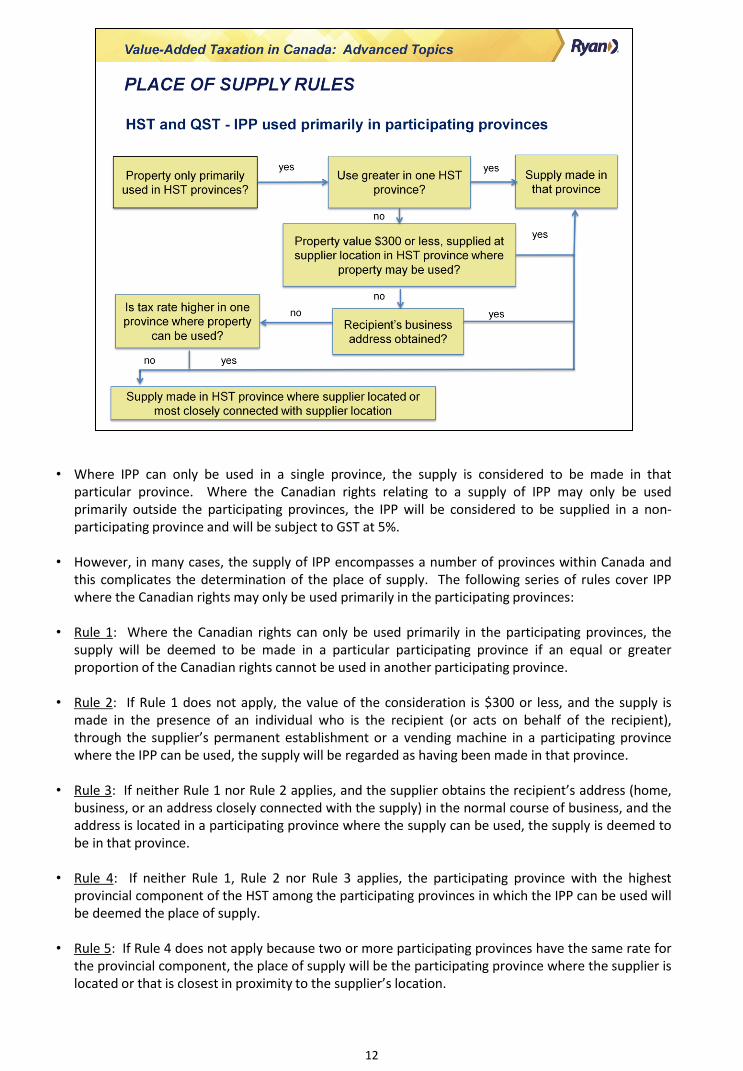

12

• Where IPP can only be used in a single province, the supply is considered to be made in that particular province. Where the Canadian rights relating to a supply of IPP may only be used primarily outside the participating provinces, the IPP will be considered to be supplied in a non-participating province and will be subject to GST at 5%.

• However, in many cases, the supply of IPP encompasses a number of provinces within Canada and this complicates the determination of the place of supply. The following series of rules cover IPP where the Canadian rights may only be used primarily in the participating provinces:

• Rule 1: Where the Canadian rights can only be used primarily in the participating provinces, the supply will be deemed to be made in a particular participating province if an equal or greater proportion of the Canadian rights cannot be used in another participating province.

• Rule 2: If Rule 1 does not apply, the value of the consideration is $300 or less, and the supply is

made in the presence of an individual who is the recipient (or acts on behalf of the recipient), through the supplier’s permanent establishment or a vending machine in a participating province where the IPP can be used, the supply will be regarded as having been made in that province.

• Rule 3: If neither Rule 1 nor Rule 2 applies, and the supplier obtains the recipient’s address (home, business, or an address closely connected with the supply) in the normal course of business, and the address is located in a participating province where the supply can be used, the supply is deemed to be in that province.

• Rule 4: If neither Rule 1, Rule 2 nor Rule 3 applies, the participating province with the highest provincial component of the HST among the participating provinces in which the IPP can be used will be deemed the place of supply.

• Rule 5: If Rule 4 does not apply because two or more participating provinces have the same rate for the provincial component, the place of supply will be the participating province where the supplier is located or that is closest in proximity to the supplier’s location.

13

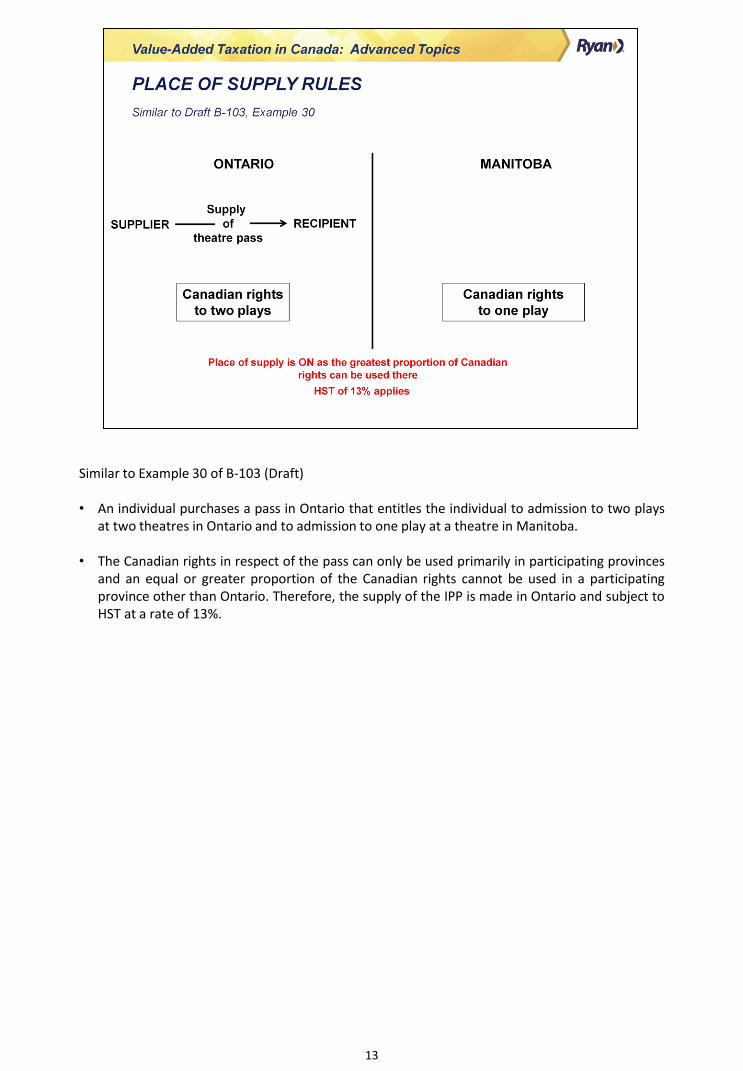

Similar to Example 30 of B-103 (Draft)

• An individual purchases a pass in Ontario that entitles the individual to admission to two plays at two theatres in Ontario and to admission to one play at a theatre in Manitoba.

• The Canadian rights in respect of the pass can only be used primarily in participating provinces and an equal or greater proportion of the Canadian rights cannot be used in a participating province other than Ontario. Therefore, the supply of the IPP is made in Ontario and subject to HST at a rate of 13%.

14

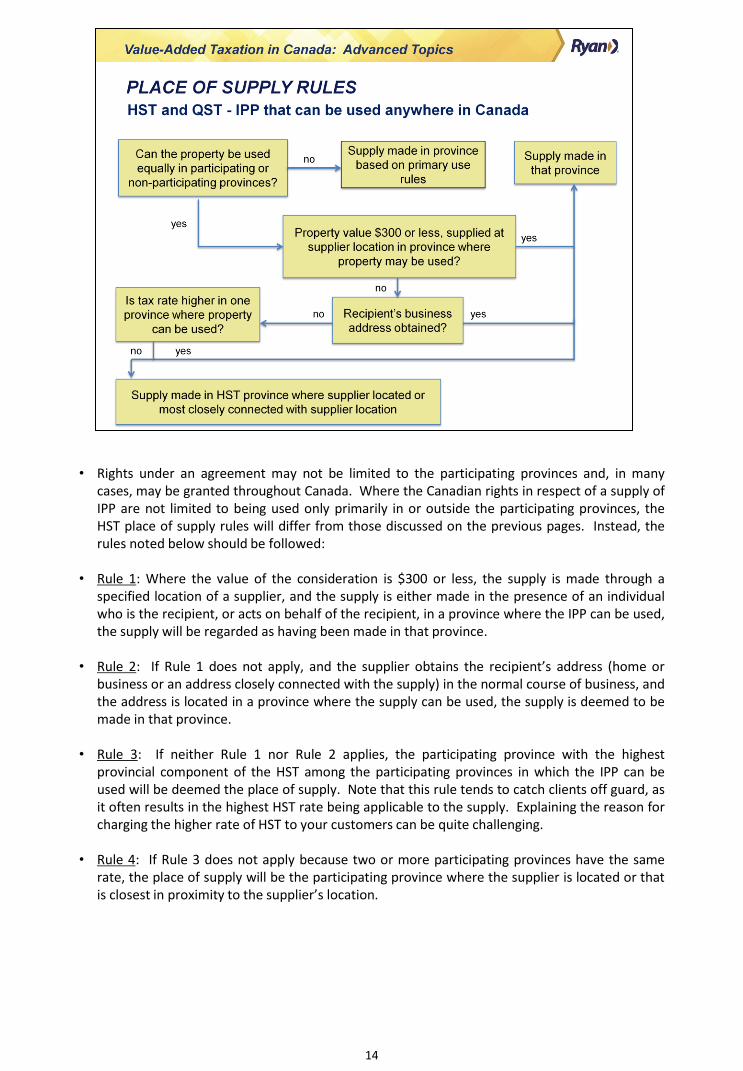

• Rights under an agreement may not be limited to the participating provinces and, in many cases, may be granted throughout Canada. Where the Canadian rights in respect of a supply of IPP are not limited to being used only primarily in or outside the participating provinces, the HST place of supply rules will differ from those discussed on the previous pages. Instead, the rules noted below should be followed:

• Rule 1: Where the value of the consideration is $300 or less, the supply is made through a specified location of a supplier, and the supply is either made in the presence of an individual who is the recipient, or acts on behalf of the recipient, in a province where the IPP can be used, the supply will be regarded as having been made in that province.

• Rule 2: If Rule 1 does not apply, and the supplier obtains the recipient’s address (home or business or an address closely connected with the supply) in the normal course of business, and the address is located in a province where the supply can be used, the supply is deemed to be made in that province.

• Rule 3: If neither Rule 1 nor Rule 2 applies, the participating province with the highest provincial component of the HST among the participating provinces in which the IPP can be used will be deemed the place of supply. Note that this rule tends to catch clients off guard, as it often results in the highest HST rate being applicable to the supply. Explaining the reason for charging the higher rate of HST to your customers can be quite challenging.

• Rule 4: If Rule 3 does not apply because two or more participating provinces have the same rate, the place of supply will be the participating province where the supplier is located or that is closest in proximity to the supplier’s location.

15

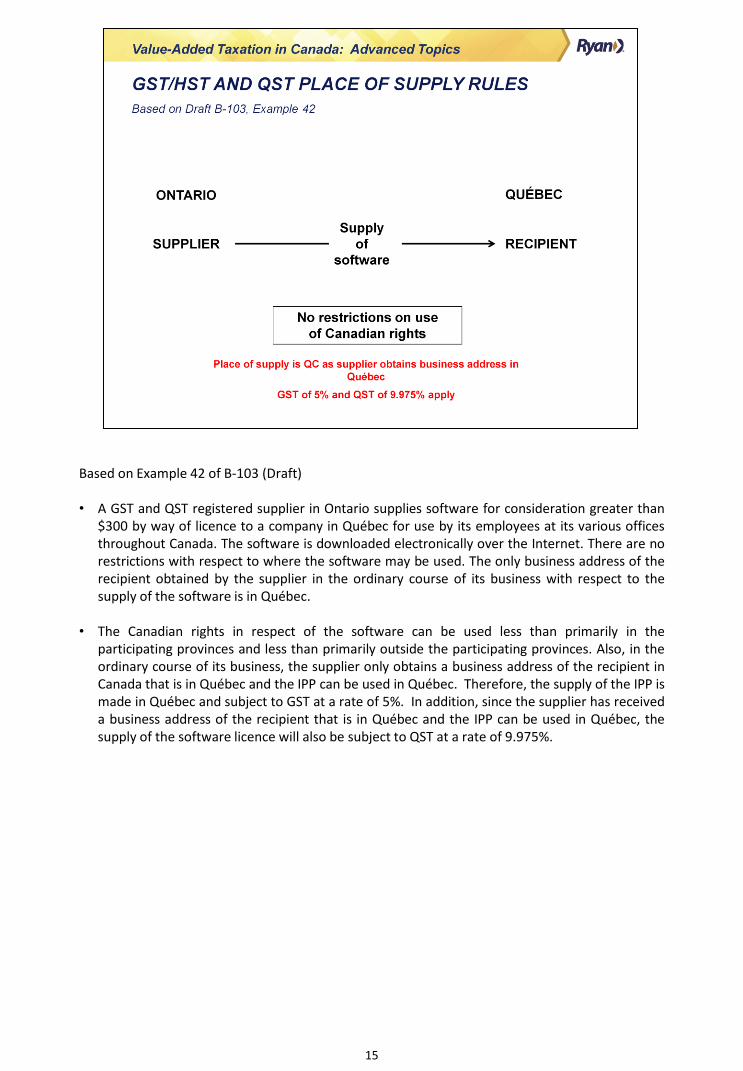

Based on Example 42 of B-103 (Draft)

• A GST and QST registered supplier in Ontario supplies software for consideration greater than $300 by way of licence to a company in Québec for use by its employees at its various offices throughout Canada. The software is downloaded electronically over the Internet. There are no restrictions with respect to where the software may be used. The only business address of the recipient obtained by the supplier in the ordinary course of its business with respect to the supply of the software is in Québec.

• The Canadian rights in respect of the software can be used less than primarily in the participating provinces and less than primarily outside the participating provinces. Also, in the ordinary course of its business, the supplier only obtains a business address of the recipient in Canada that is in Québec and the IPP can be used in Québec. Therefore, the supply of the IPP is made in Québec and subject to GST at a rate of 5%. In addition, since the supplier has received a business address of the recipient that is in Québec and the IPP can be used in Québec, the supply of the software licence will also be subject to QST at a rate of 9.975%.

16

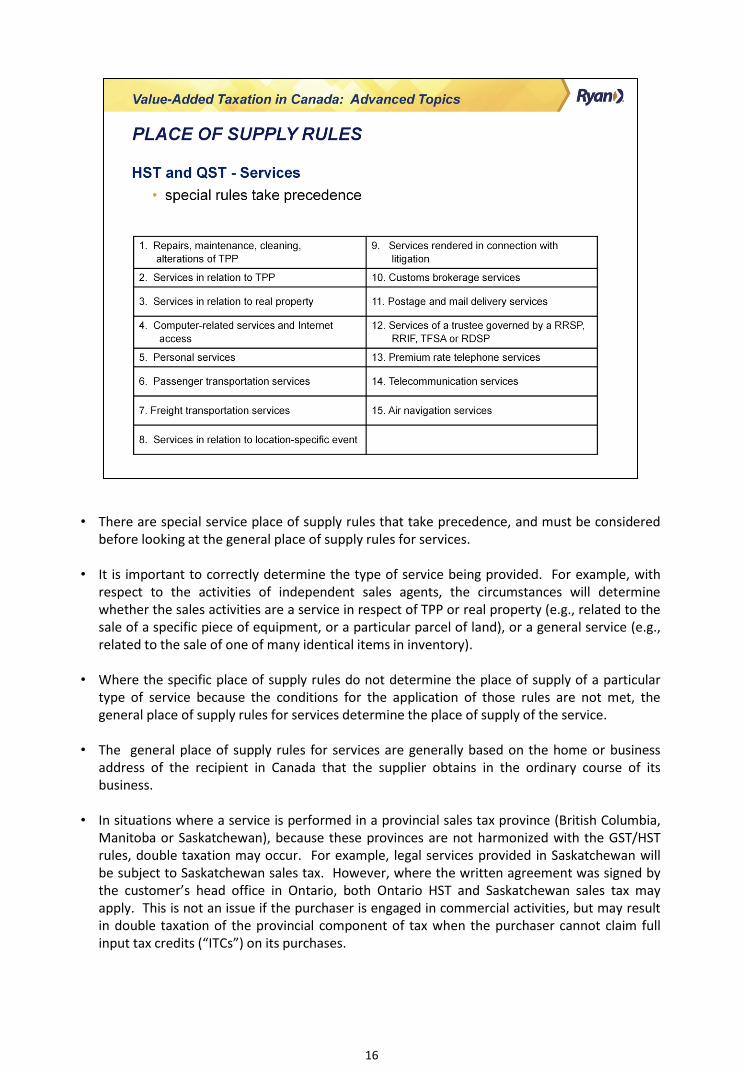

• There are special service place of supply rules that take precedence, and must be considered before looking at the general place of supply rules for services.

• It is important to correctly determine the type of service being provided. For example, with respect to the activities of independent sales agents, the circumstances will determine whether the sales activities are a service in respect of TPP or real property (e.g., related to the sale of a specific piece of equipment, or a particular parcel of land), or a general service (e.g., related to the sale of one of many identical items in inventory).

• Where the specific place of supply rules do not determine the place of supply of a particular type of service because the conditions for the application of those rules are not met, the general place of supply rules for services determine the place of supply of the service.

• The general place of supply rules for services are generally based on the home or business address of the recipient in Canada that the supplier obtains in the ordinary course of its business.

• In situations where a service is performed in a provincial sales tax province (British Columbia, Manitoba or Saskatchewan), because these provinces are not harmonized with the GST/HST rules, double taxation may occur. For example, legal services provided in Saskatchewan will be subject to Saskatchewan sales tax. However, where the written agreement was signed by the customer’s head office in Ontario, both Ontario HST and Saskatchewan sales tax may apply. This is not an issue if the purchaser is engaged in commercial activities, but may result in double taxation of the provincial component of tax when the purchaser cannot claim full input tax credits (“ITCs”) on its purchases.

17

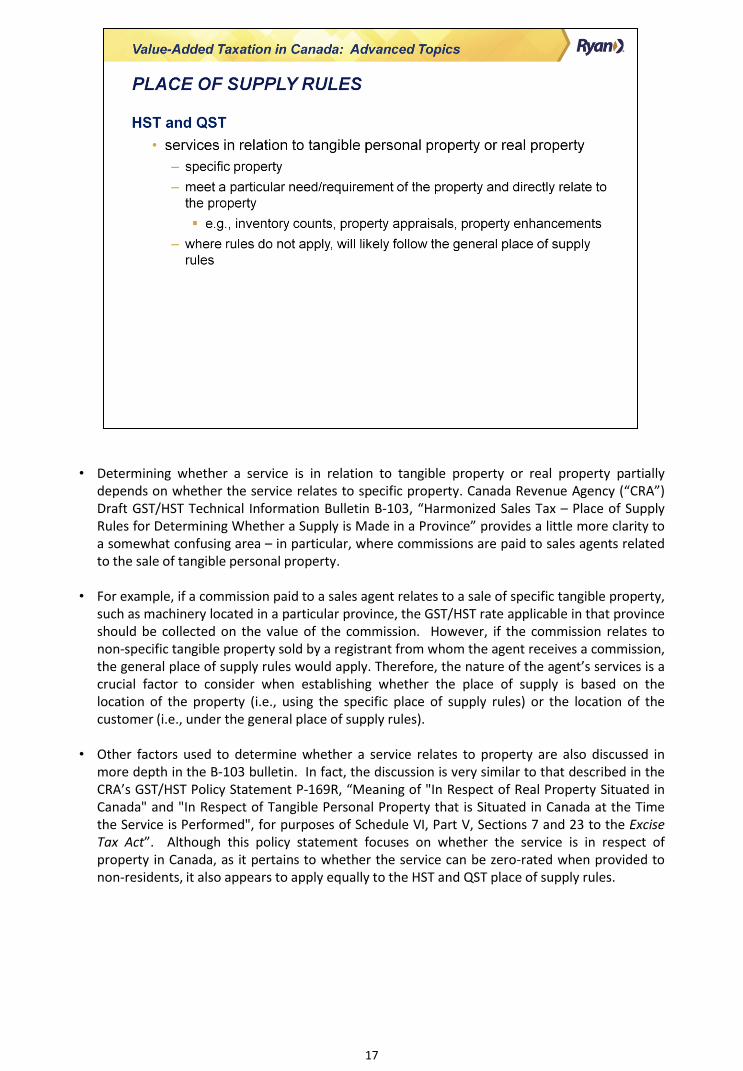

• Determining whether a service is in relation to tangible property or real property partially depends on whether the service relates to specific property. Canada Revenue Agency (“CRA”) Draft GST/HST Technical Information Bulletin B‐103, “Harmonized Sales Tax – Place of Supply Rules for Determining Whether a Supply is Made in a Province” provides a little more clarity to a somewhat confusing area – in particular, where commissions are paid to sales agents related to the sale of tangible personal property.

• For example, if a commission paid to a sales agent relates to a sale of specific tangible property, such as machinery located in a particular province, the GST/HST rate applicable in that province should be collected on the value of the commission. However, if the commission relates to non-specific tangible property sold by a registrant from whom the agent receives a commission, the general place of supply rules would apply. Therefore, the nature of the agent’s services is a crucial factor to consider when establishing whether the place of supply is based on the location of the property (i.e., using the specific place of supply rules) or the location of the customer (i.e., under the general place of supply rules).

• Other factors used to determine whether a service relates to property are also discussed in

more depth in the B-103 bulletin. In fact, the discussion is very similar to that described in the CRA’s GST/HST Policy Statement P-169R, “Meaning of "In Respect of Real Property Situated in Canada" and "In Respect of Tangible Personal Property that is Situated in Canada at the Time the Service is Performed", for purposes of Schedule VI, Part V, Sections 7 and 23 to the Excise Tax Act”. Although this policy statement focuses on whether the service is in respect of property in Canada, as it pertains to whether the service can be zero-rated when provided to non-residents, it also appears to apply equally to the HST and QST place of supply rules.

18

• Generally, the service must meet a particular need or requirement of the property, and directly relate to the property, in order to be considered “in relation to” the property. Examples include inventory counts, property appraisals, and enhancements made to property. Note that this concept also applies to IPP in relation to tangible or real property.

• For both IPP and services, one key point made in the bulletin is that the general place of supply rules are to be used when specific place of supply rules do not apply.

• For example, where a commission relates to sales of both tangible property and real property under a single agreement, the general place of supply rules for services should apply, since neither the place of supply rules for services in relation to tangible property nor the place of supply rules for services in relation to real property would apply (i.e., it is a service in relation to the sale of both tangible and real property, not one or the other).

19

• The rules for services in relation to TPP are based on whether the TPP remains in the same province while the service is performed. Note that these rules do not apply where the goods to be repaired are shipped to the supplier’s location for the performance of specific repairs and maintenance services.

• The supply of a service in relation to TPP will be made in a participating province if the TPP is situated primarily (more than 50%) in the participating province(s) when the Canadian element of the service begins and the goods remain in that province or provinces while the service is performed. The supply of the service is considered to be made in the participating province in which the greatest proportion of the TPP is located.

• Where services are performed in relation to TPP in one or more provinces and the property does not remain situated in that province or those provinces while the Canadian element of the service is performed, the service will be considered to be made in a participating province if:

‒ the property is situated primarily (more than 50%) in participating provinces at any time the Canadian element of the service is performed;

‒ the service is performed primarily in participating provinces; and ‒ the greatest proportion of the service performed in participating provinces is performed

in that participating province.

• If the TPP is situated otherwise than primarily in participating provinces (e.g., situated primarily in non-participating provinces or situated equally in participating and non-participating provinces) when the Canadian element of the service is performed, or the service is performed otherwise than primarily in participating provinces, the supply will be regarded as having been made in a non-participating province.

20

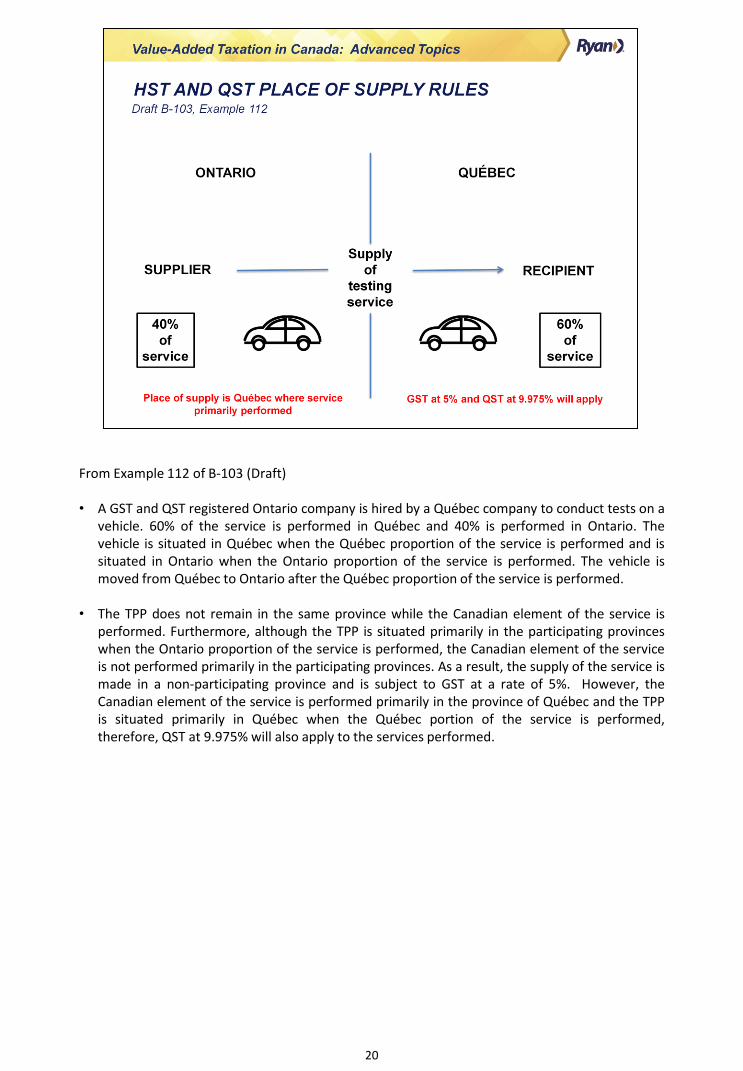

From Example 112 of B-103 (Draft)

• A GST and QST registered Ontario company is hired by a Québec company to conduct tests on a vehicle. 60% of the service is performed in Québec and 40% is performed in Ontario. The vehicle is situated in Québec when the Québec proportion of the service is performed and is situated in Ontario when the Ontario proportion of the service is performed. The vehicle is moved from Québec to Ontario after the Québec proportion of the service is performed.

• The TPP does not remain in the same province while the Canadian element of the service is performed. Furthermore, although the TPP is situated primarily in the participating provinces when the Ontario proportion of the service is performed, the Canadian element of the service is not performed primarily in the participating provinces. As a result, the supply of the service is made in a non-participating province and is subject to GST at a rate of 5%. However, the Canadian element of the service is performed primarily in the province of Québec and the TPP is situated primarily in Québec when the Québec portion of the service is performed, therefore, QST at 9.975% will also apply to the services performed.

21

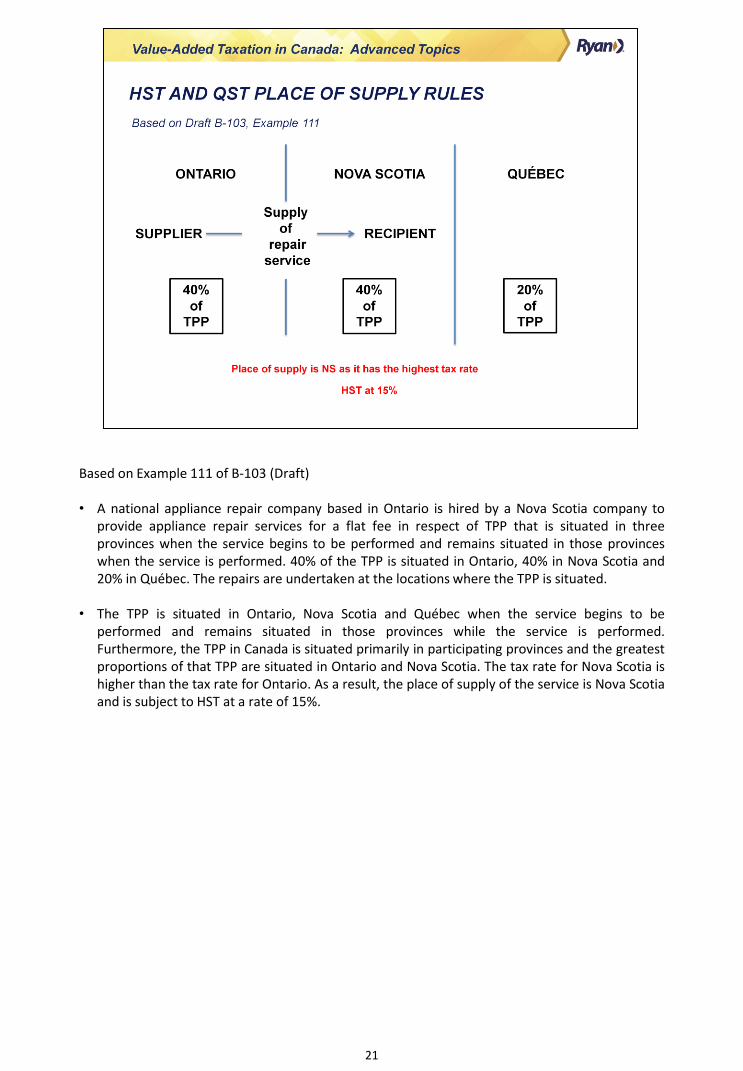

Based on Example 111 of B-103 (Draft)

• A national appliance repair company based in Ontario is hired by a Nova Scotia company to provide appliance repair services for a flat fee in respect of TPP that is situated in three provinces when the service begins to be performed and remains situated in those provinces when the service is performed. 40% of the TPP is situated in Ontario, 40% in Nova Scotia and 20% in Québec. The repairs are undertaken at the locations where the TPP is situated.

• The TPP is situated in Ontario, Nova Scotia and Québec when the service begins to be performed and remains situated in those provinces while the service is performed. Furthermore, the TPP in Canada is situated primarily in participating provinces and the greatest proportions of that TPP are situated in Ontario and Nova Scotia. The tax rate for Nova Scotia is higher than the tax rate for Ontario. As a result, the place of supply of the service is Nova Scotia and is subject to HST at a rate of 15%.

22

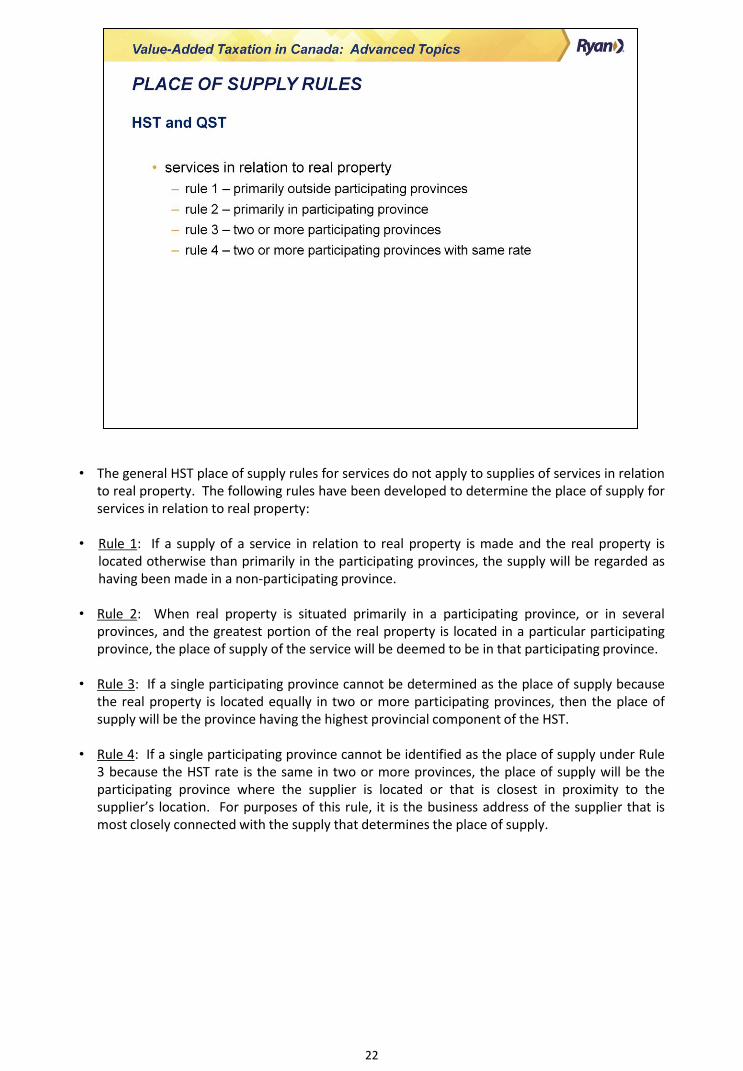

• The general HST place of supply rules for services do not apply to supplies of services in relation to real property. The following rules have been developed to determine the place of supply for services in relation to real property:

• Rule 1: If a supply of a service in relation to real property is made and the real property is located otherwise than primarily in the participating provinces, the supply will be regarded as having been made in a non-participating province.

• Rule 2: When real property is situated primarily in a participating province, or in several provinces, and the greatest portion of the real property is located in a particular participating province, the place of supply of the service will be deemed to be in that participating province.

• Rule 3: If a single participating province cannot be determined as the place of supply because

the real property is located equally in two or more participating provinces, then the place of supply will be the province having the highest provincial component of the HST.

• Rule 4: If a single participating province cannot be identified as the place of supply under Rule

3 because the HST rate is the same in two or more provinces, the place of supply will be the participating province where the supplier is located or that is closest in proximity to the supplier’s location. For purposes of this rule, it is the business address of the supplier that is most closely connected with the supply that determines the place of supply.

23

References:

• GST Memorandum 300-8, “Imported Goods”.

• GST Memorandum 300-9, “Imported Services and Intangible Property”.

24

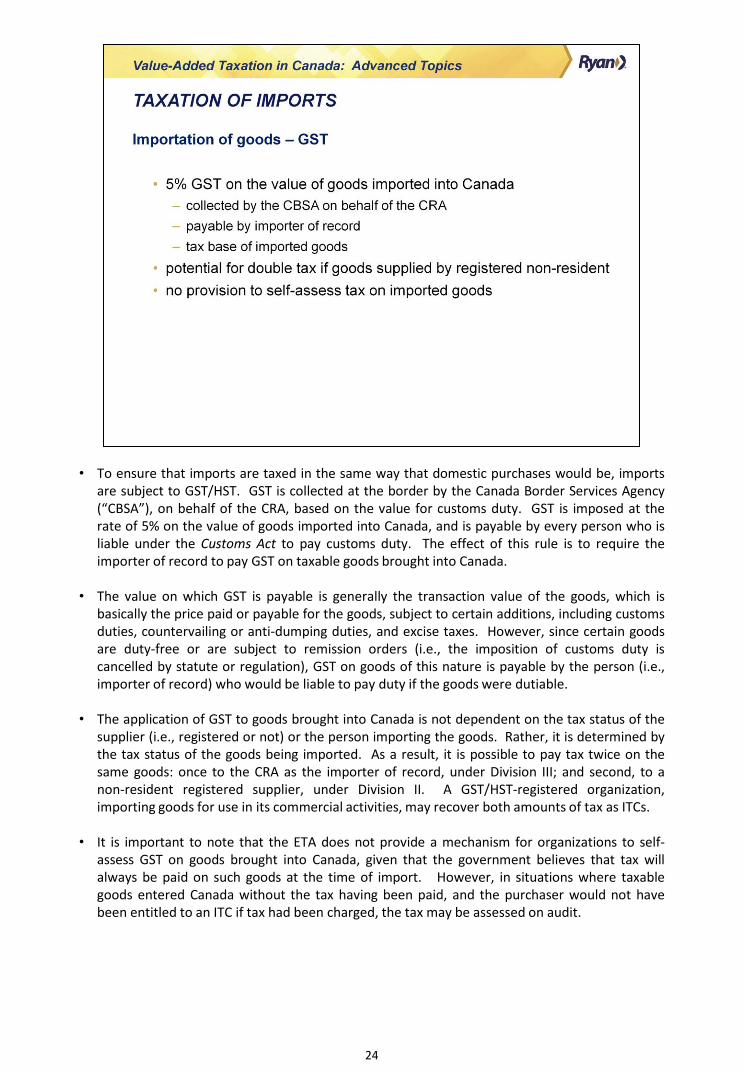

• To ensure that imports are taxed in the same way that domestic purchases would be, imports are subject to GST/HST. GST is collected at the border by the Canada Border Services Agency (“CBSA”), on behalf of the CRA, based on the value for customs duty. GST is imposed at the rate of 5% on the value of goods imported into Canada, and is payable by every person who is liable under the Customs Act to pay customs duty. The effect of this rule is to require the importer of record to pay GST on taxable goods brought into Canada.

• The value on which GST is payable is generally the transaction value of the goods, which is basically the price paid or payable for the goods, subject to certain additions, including customs duties, countervailing or anti-dumping duties, and excise taxes. However, since certain goods are duty-free or are subject to remission orders (i.e., the imposition of customs duty is cancelled by statute or regulation), GST on goods of this nature is payable by the person (i.e., importer of record) who would be liable to pay duty if the goods were dutiable.

• The application of GST to goods brought into Canada is not dependent on the tax status of the supplier (i.e., registered or not) or the person importing the goods. Rather, it is determined by the tax status of the goods being imported. As a result, it is possible to pay tax twice on the same goods: once to the CRA as the importer of record, under Division III; and second, to a non-resident registered supplier, under Division II. A GST/HST-registered organization, importing goods for use in its commercial activities, may recover both amounts of tax as ITCs.

• It is important to note that the ETA does not provide a mechanism for organizations to self-assess GST on goods brought into Canada, given that the government believes that tax will always be paid on such goods at the time of import. However, in situations where taxable goods entered Canada without the tax having been paid, and the purchaser would not have been entitled to an ITC if tax had been charged, the tax may be assessed on audit.

25

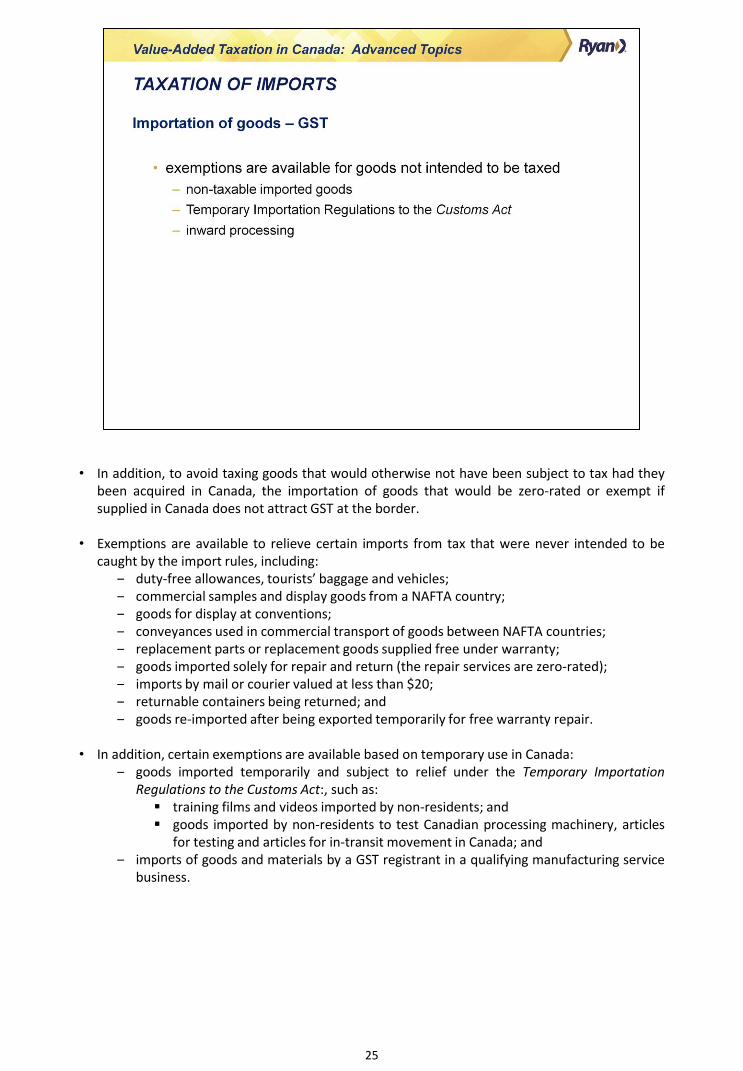

• In addition, to avoid taxing goods that would otherwise not have been subject to tax had they been acquired in Canada, the importation of goods that would be zero-rated or exempt if supplied in Canada does not attract GST at the border.

• Exemptions are available to relieve certain imports from tax that were never intended to be caught by the import rules, including:

‒ duty-free allowances, tourists’ baggage and vehicles; ‒ commercial samples and display goods from a NAFTA country; ‒ goods for display at conventions; ‒ conveyances used in commercial transport of goods between NAFTA countries; ‒ replacement parts or replacement goods supplied free under warranty; ‒ goods imported solely for repair and return (the repair services are zero-rated); ‒ imports by mail or courier valued at less than $20; ‒ returnable containers being returned; and ‒ goods re-imported after being exported temporarily for free warranty repair.

• In addition, certain exemptions are available based on temporary use in Canada:

‒ goods imported temporarily and subject to relief under the Temporary Importation Regulations to the Customs Act:, such as:

training films and videos imported by non-residents; and goods imported by non-residents to test Canadian processing machinery, articles

for testing and articles for in-transit movement in Canada; and ‒ imports of goods and materials by a GST registrant in a qualifying manufacturing service

business.

26

• Although GST is collected on goods imported into Canada, the provincial component of the HST is not collected at the border on commercial imports into the harmonized provinces from places outside Canada. HST is, however, collected on non-commercial imports for individuals residing in any of the harmonized provinces.

• Furthermore, GST/HST registrants who are entitled to claim full ITCs are not required to self-assess the provincial component of the HST on goods imported into the harmonized provinces.

• In contrast, tax must generally be self-assessed on imports into the participating provinces by persons who are not entitled to claim full ITCs, including non-commercial organizations such as public service bodies (e.g., hospitals, universities and school boards).

• However, selected listed financial institutions (“SLFIs”) are not required to self-assess tax under these provisions, since the provincial component of the HST is taken into account in their annual special attribution method calculation (SAM calculation).

27

• QST is not collected at the border by the CBSA on behalf of the Québec government on commercial imports into Québec from a place outside Canada. However, QST is collected on non-commercial imports (i.e., goods brought in by individuals) based on the person’s place of residence. Therefore, organizations importing taxable supplies into Québec are generally required under the QSTA to self-assess QST. However, exceptions to this rule including situations where tax has been collected by a QST registrant or where goods are imported for exclusive commercial use.

• Where goods are imported into Québec from a non-QST registered supplier, there is no mechanism to collect QST on the importation of goods into Québec from other provinces. Similar to imports from a place outside Canada, registrants importing goods into Québec from other provinces are not required to self-assess QST if the goods are imported for exclusive use in commercial activities.

• In addition, there are specific exclusions from the imposition of QST on the importation of goods under conditions which parallel those found in the federal provisions of Schedule VII of the ETA and in the Non-Taxable Imported Goods (GST) Regulations and Value of Imported Goods (GST/HST) Regulations.

28

• It is impractical, if not impossible, for the CRA to collect tax on imported services and intangible properties at the border. Instead, imported services and intangibles are taxable on a self-assessment basis in accordance with the imported taxable supply rules (Division IV).

• The main objective in taxing imported services and intangible property is to ensure that persons engaged in non-commercial activities cannot avoid tax on, for example, engineering, management, data processing, and other services for use in Canada by acquiring such services outside Canada or from unregistered non-resident suppliers. The CRA has also ruled that GST/HST applies to training services rendered in Canada by an unregistered non-resident and to charges for advertising a Canadian employment opportunity in a foreign publication. Common examples of imported taxable supplies of IPP include intellectual property (such as patents, trade secrets, trade-marks and trade names), contractual rights, options, and software.

• However, tax does not need to be self-assessed on: ‒ services or intangibles purchased for the exclusive consumption, use or supply in the

commercial activities of a registrant; ‒ services or intangibles purchased for consumption, use or supply in the course of

activities engaged in exclusively outside of Canada; ‒ services or intangibles in respect of real property situated outside Canada; or ‒ intangible property that may not be used in Canada.

• Administratively, the CRA interprets exclusive use as 90% or more. However, in the case of

financial institutions (“FIs”), exclusive use means 100%. The exclusion from the tax on services imported for use exclusively in commercial activities ensures registrants do not have to self-assess tax on an importation where they would otherwise be entitled to recover any tax paid by claiming ITCs.

29

• Québec recipients are required to self-assess QST in these same circumstances. Prior to January 1, 2013, the supply of financial services was zero-rated in Québec and, therefore, qualified as commercial activity.

• Effective January 1, 2013, financial services are exempt services and no longer qualify as commercial activity, meaning that financial institutions may now have to self-assess QST on their imported taxable supplies.

30

• Although GST is collected on goods imported into Canada, the provincial component of the HST is not collected at the border on commercial imports into the harmonized provinces. Supplies that are made outside a participating province and that are brought into a participating province from outside Canada or from a non-participating province may be subject to self-assessment of the provincial component of the HST. Generally, the self-assessment rules apply to persons engaged in non-commercial activities and consumers who have not been charged the provincial component of the HST by the supplier.

• Furthermore, registrants who are entitled to claim full ITCs/ITRs are not required to self-assess the provincial component of the HST/QST on goods imported into the harmonized provinces or Québec, unless the goods are specified expenses for ITC recapture or restricted ITR purposes. Failure to self-assess HST/QST on imported supplies subject to ITC recapture/ITR restrictions will cause an additional sales tax exposure.

• In contrast, tax must generally be self-assessed on imports into the HST provinces/Québec by persons who are not entitled to claim full ITCs/ITRs, including non-commercial organizations, such as municipalities, hospitals, universities, school boards and financial institutions.

• However, the HST self-assessment rules dealing with goods and services imported into, or removed from, a participating province generally do not apply to listed financial institutions that qualify as an SLFI. This is because, as previously mentioned, SLFIs account for the provincial component of HST on their purchases through adjustments to their net tax calculation as determined by the special attribution method formula (SAM calculation).

• Note that QST must be self-assessed on insurance premiums acquired from unregistered vendors for risks in Québec. Where the Québec tax on insurance has not been charged on insurance related to risks in Québec, the tax on insurance may be self-assessed by completing both the Special-Purpose Return (FP-505-V) and the Return Respecting the tax on Insurance Premiums (FP-505.D.H-V).

31

• In situations where TPP is brought into a participating province from another participating province, with a lower HST rate, a person will generally be required to self-assess the difference between the provincial component of the HST in the destination province and the originating province based on the lesser of the consideration paid for the property and the fair market value of the property at the time of import.

• In circumstances where services and IPP are supplied in a province and subsequently consumed 10% or more in a participating province with a higher HST provincial component than the acquisition province, the person must self-assess an amount based on the difference between the provincial components of the HST.

• In both cases, relief is provided so that a person will not be required to self-assess tax on the difference if the amount of tax that is payable by the person is less than $25 in a calendar month.

• Self-assessment of HST by registrants involved in exempt activities for IPP and services acquired outside Canada will be required where 10% or more of the supply will be consumed in a participating province. If self-assessment is required, it is provided that an amount of tax be calculated with regard to the extent to which the IPP or service will be consumed in each participating province.

32

• An expansion to existing rebate mechanisms has been provided to allow registrants that acquire TPP that is subsequently removed from a participating province to a participating province with a lower provincial component tax rate to recover a portion or all of the provincial component of the HST, provided that the TPP is removed within 30 days of delivery to the original participating province. A similar rebate is provided for services and intangibles supplied in a participating province for use in another participating province. No 30-day time limit applies to this rebate.

• The rebate amount would be based on the difference between the provincial component of the HST paid and the provincial component of the HST that would have been paid in the destination province.

• The provisions discussed on the last two pages will only apply to organizations engaged in non-

commercial activities (e.g., financial institutions), as organizations engaged in commercial activity would be entitled to claim full ITCs for the HST paid on similar purchases.

33

Reference: • Policy Statement P-125R, “Input Tax Credit Entitlement for Tax on Imported Goods”.

34

• There are several factors that must be taken into consideration before determining whether the entity that pays the 5% GST on importation of the goods is permitted to claim an input tax credit.

• GST is payable on the excise and duty-paid value of taxable goods at the time of importation. GST paid or payable on imported goods is included in determining the registrant’s ITC entitlement in the same manner as for goods and services acquired from Canadian sources.

• Registrants may also claim an ITC if they import another person’s goods for the purpose of performing a commercial service, other than shipping, on the imported goods. However, registrants are not eligible for an ITC where GST was not payable upon importation.

• In the past, the CRA had indicated that the only person entitled to claim an ITC for tax paid or payable at the time of importation was the de facto importer of the goods. The de facto importer is the person in Canada who caused the goods to be brought into Canada (generally the owner of the goods). However, the de facto importer is not necessarily the person named on the customs accounting documents and required to pay GST at the border as the importer of record.

• For instance, a supplier may have acted as the importer of record and paid applicable taxes at the border on its own account where the actual supply of the goods was considered to be made outside of Canada (e.g., at a non-resident supplier’s dock). Depending on the circumstances, this type of situation may create an issue for the recovery of tax paid at the border on imports.

35

• To address the de facto importer issue, and to simplify the recovery of tax paid at the border on imports, section 178.8 to the ETA was enacted and applies to goods imported on or after October 3, 2003.

• In order to meet the section 178.8 conditions, the goods must be supplied outside of Canada and then imported into Canada.

• The constructive importer is defined by section 178.8(2) as a recipient of a specified supply of goods made outside of Canada where the recipient does not, at any time before the release of the goods, supply the goods outside of Canada and the recipient or any other person imported the goods for consumption, use or supply by the recipient. In other words, the constructive importer is the last person to whom a supply of the goods is made outside of Canada, before they are released (but not necessarily the importer of the goods).

‒ a specified supply means a supply of goods that: (a) are, at any time after the supply is made, imported; or (b) have been imported in circumstances in which the supply is deemed to be made outside Canada.

• The specified importer is referred to in subsection 178.8(5) as the person who was identified for the purposes of the Customs Act as the importer of the goods when the goods were accounted for under section 32 of that Act. In essence, it is the person who is the importer of record of the goods.

• Since QST is not typically collected at the border by CBSA when goods are imported into Canada, a similar provision as discussed above is not required for QST purposes.

36

• Section 178.8 deems the tax to have been paid by the constructive importer, regardless of who acts as the importer of record. The constructive importer is the last person to whom a supply of goods is made outside Canada prior to import for the person’s consumption, use or re-supply. However, the constructive importer is not the person that the goods are accounted for under the Customs Act at the time of importation.

• These rules potentially apply whenever goods are supplied outside of Canada and are subsequently imported into Canada. They are not limited only to a situation where a registered non-resident vendor imports goods that it has delivered outside of Canada.

• If the supplier pays the tax, acting as the importer of record, it is considered to be doing so only as an agent on behalf of the constructive importer. These rules operate by denying the supplier the ITC for the Division III tax paid at the border. Where the goods are supplied outside of Canada, the ITC will only be available to the recipient of the supply. For these rules to work, the supplier must pass prescribed documentation on to the constructive importer (i.e., recipient) to enable it to claim the ITC.

• In an attempt to further simplify the recovery of tax on imports, this legislation permits a registered supplier and the constructive importer to agree that the supplier will collect tax on the supply as if it were made in Canada, thereby allowing the recipient to claim an ITC for the amount of tax charged, and the supplier to claim an ITC for any tax paid at the border. This election must be made in writing, but need not be filed with the CRA.

37

• Given that specified goods are being imported for use in the constructive importer's activities, these activities will determine eligibility for recovery of tax on the imported goods. However, in some cases, the constructive importer may not meet all of the conditions for recovery.

• To solve this problem, the default rule in subsection 178.8(2) deems the imported goods supplied outside Canada to be imported by the constructive importer. It also deems any amount of tax paid or payable under Division III of Part IX of the ETA to be paid or payable by the constructive importer.

• In order for the default rule to apply all the following conditions must be satisfied:

‒ a specified supply of the goods is made outside of Canada (i.e., supply made outside of Canada of goods that are subsequently imported into Canada);

‒ the recipient of the specified supply of goods made outside of Canada does not, at any time before the release of the goods, supply the goods outside of Canada; and

‒ the goods are imported for the consumption, use or supply by the recipient.

• Therefore, where the above conditions are satisfied the following is deemed to occur:

‒ the constructive importer (i.e., the recipient) is deemed to have imported the goods; and

‒ the constructive importer is deemed to have paid the Division III tax at the border, no one else.

• These deeming rules ensure that the constructive importer is the only the person eligible to claim any ITC in respect of the tax at the border. However prior to claiming an ITC, the constructive importer must obtain appropriate documentation (e.g. B3) from the importer of record supporting the payment of tax.

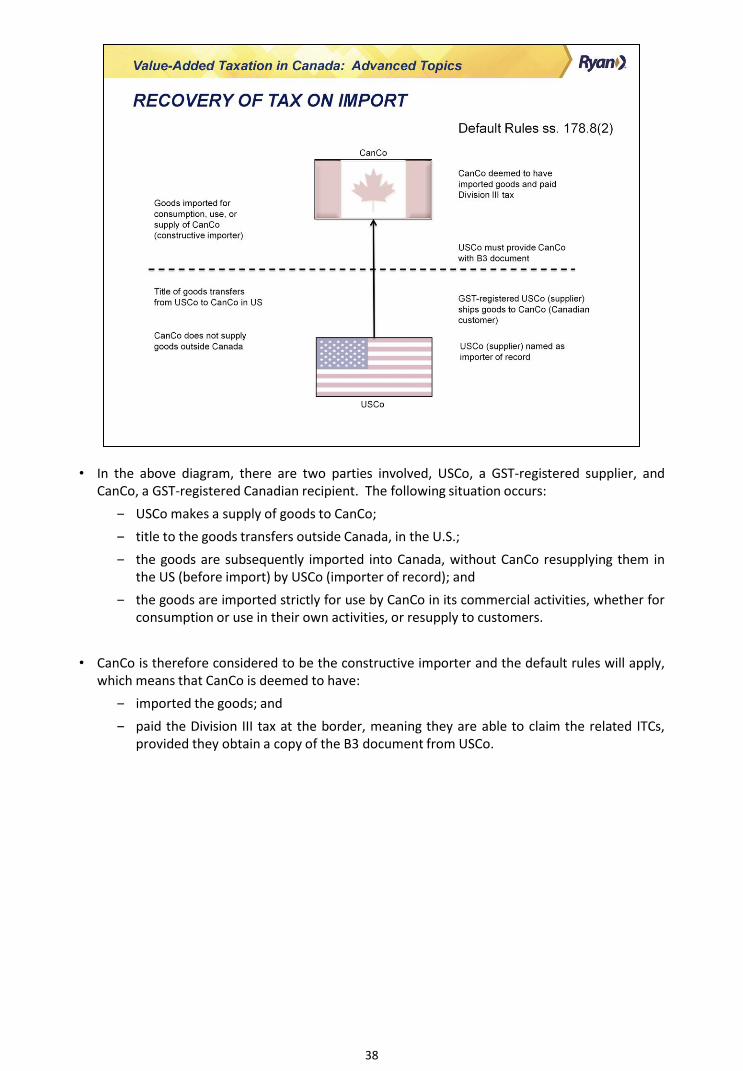

38

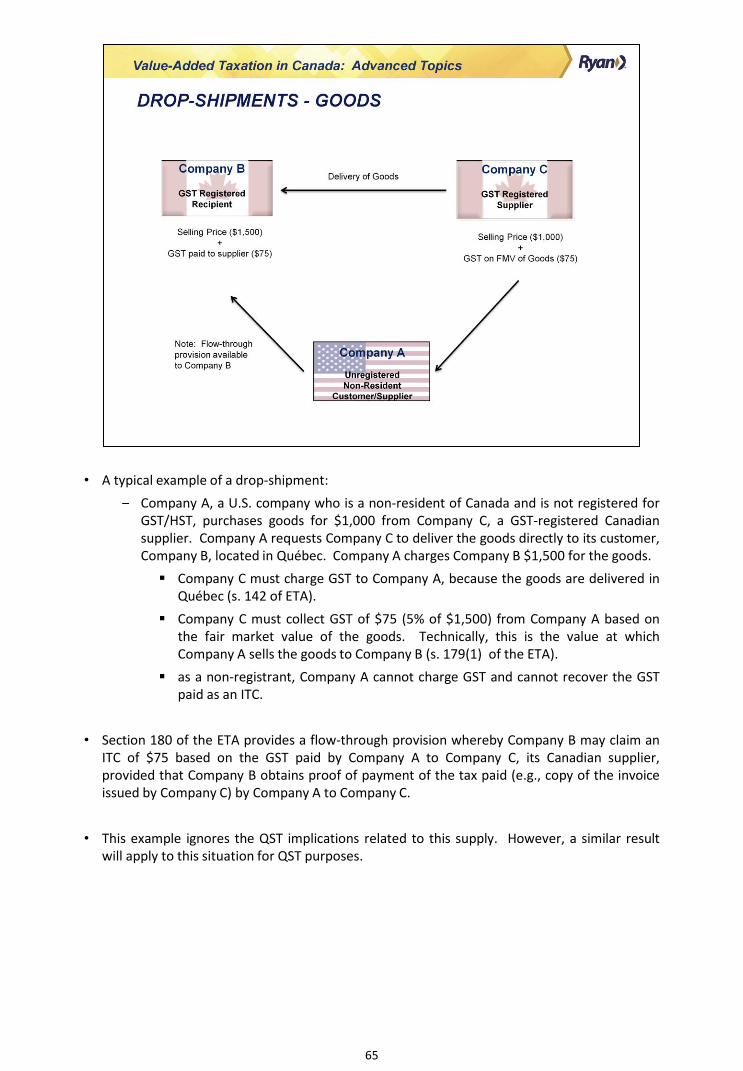

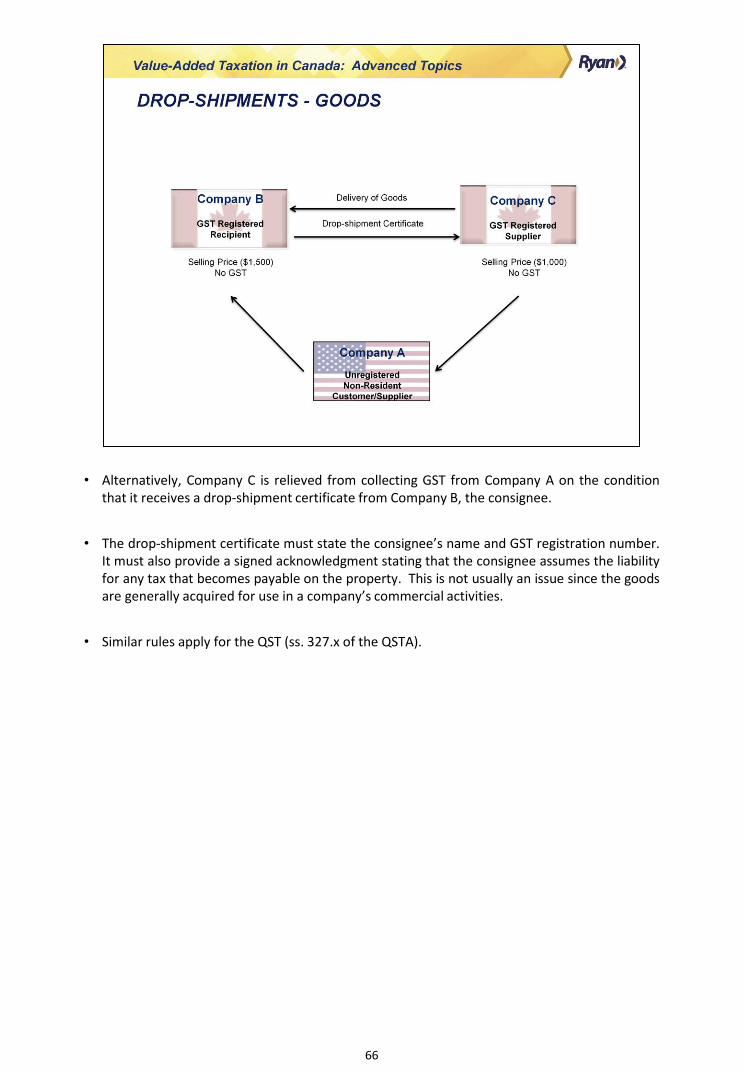

• In the above diagram, there are two parties involved, USCo, a GST-registered supplier, and CanCo, a GST-registered Canadian recipient. The following situation occurs:

‒ USCo makes a supply of goods to CanCo;

‒ title to the goods transfers outside Canada, in the U.S.;

‒ the goods are subsequently imported into Canada, without CanCo resupplying them in the US (before import) by USCo (importer of record); and

‒ the goods are imported strictly for use by CanCo in its commercial activities, whether for consumption or use in their own activities, or resupply to customers.

• CanCo is therefore considered to be the constructive importer and the default rules will apply, which means that CanCo is deemed to have:

‒ imported the goods; and

‒ paid the Division III tax at the border, meaning they are able to claim the related ITCs, provided they obtain a copy of the B3 document from USCo.

39

• Subsections 178.8(3) and (4) of the ETA provide a mechanism whereby a registered supplier can avoid the need to pass on the import documentation to the constructive importer for purposes of recovering the tax paid on the goods.

• The following conditions must be met:

‒ a registered vendor makes a taxable supply outside of Canada that will be imported;

‒ the registered vendor pays the Division III tax;

‒ the recipient of the supply must be the constructive importer; and

‒ the registered vendor and the constructive importer elect to have subsection 178.8(4) apply. (This election doesn’t need to be filed, but must be available for review during an audit.)

• Provided all of the conditions under subsection 178.8(3) are met, subsection 178.8(4) deems the following to have occurred:

‒ the supply by the registered vendor to the constructive importer is deemed to have been made in Canada. As a result, the registered vendor is required to collect Division II tax (tax required to be collected by registered vendors) from the constructive importer;

‒ consideration for the supply is deemed to be the consideration otherwise determined plus any amount that the constructive importer pays the registered vendor in respect of customs duties or excise tax or duties that are levied at the time of importation; and

‒ the registered vendor is deemed to have paid the Division III tax and imported the goods for the purpose of supply in the course of a commercial activity. Therefore, the registered vendor is allowed to claim an ITC for the Division III tax paid at the time the goods are imported into Canada. In fact, no one else is permitted to claim the ITC.

40

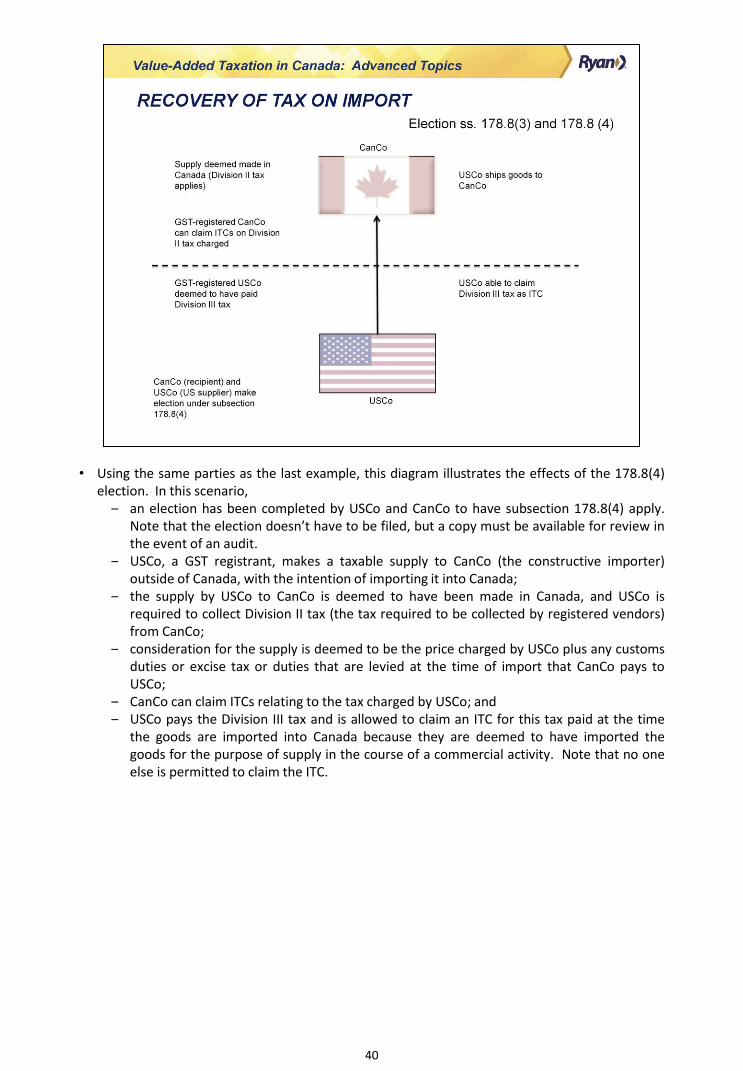

• Using the same parties as the last example, this diagram illustrates the effects of the 178.8(4) election. In this scenario,

‒ an election has been completed by USCo and CanCo to have subsection 178.8(4) apply. Note that the election doesn’t have to be filed, but a copy must be available for review in the event of an audit.

‒ USCo, a GST registrant, makes a taxable supply to CanCo (the constructive importer) outside of Canada, with the intention of importing it into Canada;

‒ the supply by USCo to CanCo is deemed to have been made in Canada, and USCo is required to collect Division II tax (the tax required to be collected by registered vendors) from CanCo;

‒ consideration for the supply is deemed to be the price charged by USCo plus any customs duties or excise tax or duties that are levied at the time of import that CanCo pays to USCo;

‒ CanCo can claim ITCs relating to the tax charged by USCo; and ‒ USCo pays the Division III tax and is allowed to claim an ITC for this tax paid at the time

the goods are imported into Canada because they are deemed to have imported the goods for the purpose of supply in the course of a commercial activity. Note that no one else is permitted to claim the ITC.

41

• Usually, when GST registrants import the goods of an unregistered non-resident to provide a commercial service in respect of those goods, the registrant pays the GST on the value of the goods at the time of importation.

• Registrants in this situation can recover the GST paid at the time of importation as an ITC, as long as they provide a taxable supply of a commercial service in respect of the goods.

• A commercial service is any service performed in respect of the goods, except for financial or shipping services. There must be a direct functional relationship between the commercial service and the goods. Generally, a functional relationship exists where the commercial service is performed to, or on, the goods themselves.

• The CRA considers assembling, blending, testing, repairing, maintaining, modifying and packaging or repackaging imported property to be qualifying commercial services. However, it does not consider the provision of services necessary to clear goods through customs, or to arrange for a common carrier to deliver the goods, to constitute a commercial service.

• Since QST is not typically collected at the border by CBSA when goods are imported into Canada, a similar provision, as discussed above, is not required for QST purposes.

42

• Where an unregistered non-resident acts as the importer of record for goods brought into Canada, it will pay GST at the border. If the goods are sold to a Canadian customer, the tax is normally passed on as part of the cost of the goods sold or shown on the invoice as GST, but without some special relief, the Canadian customer, even if a GST registrant, will be unable to claim the tax back as an ITC, given that the Canadian recipient has not paid GST to a registered supplier.

• It is specifically provided, therefore, that the Canadian recipient will be treated as having paid the tax itself where either the goods have been sold to the Canadian customer, or possession of the goods has been acquired for the purposes of performing a commercial service in respect of the goods for the non-resident.

• In order for the Canadian recipient to recover the tax, the non-resident must provide them with proof that the tax has been paid (e.g., a copy of the customs B3 document). The Canadian recipient may then claim an ITC for the tax paid as though it has acquired the goods from a registrant for consumption, use or supply in the course of its commercial activity.

• The flow-through provision will also permit a GST-registered person, who has acquired goods from an unregistered non-resident for use in commercial activity or for further processing, to recover the tax, where the non-resident has paid GST on the purchase of these goods from a Canadian supplier. However, the use of this provision in these circumstances is infrequent because it requires that the non-resident supplier divulge their markup in order for an accurate calculation of GST to be made. In addition, the payment of tax can generally be avoided entirely by relying on the drop-shipment rules.

• Québec provides equivalent flow-through relief to a QST registrant in the rare circumstance where QST has been paid by an unregistered person on the importation of goods.

43

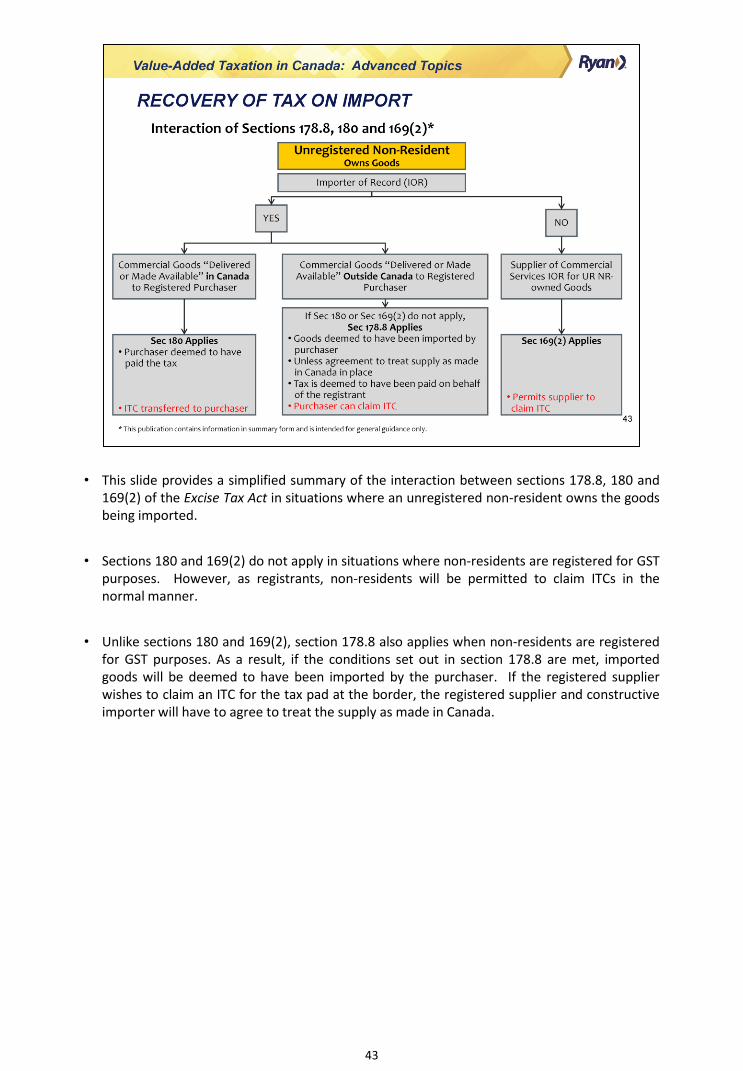

• This slide provides a simplified summary of the interaction between sections 178.8, 180 and 169(2) of the Excise Tax Act in situations where an unregistered non-resident owns the goods being imported.

• Sections 180 and 169(2) do not apply in situations where non-residents are registered for GST purposes. However, as registrants, non-residents will be permitted to claim ITCs in the normal manner.

• Unlike sections 180 and 169(2), section 178.8 also applies when non-residents are registered for GST purposes. As a result, if the conditions set out in section 178.8 are met, imported goods will be deemed to have been imported by the purchaser. If the registered supplier wishes to claim an ITC for the tax pad at the border, the registered supplier and constructive importer will have to agree to treat the supply as made in Canada.

44

• Rebates of tax paid at the border, or otherwise, are available where a person is not able to recover the tax by means of an ITC or refund in the following circumstances:

‒ goods are acquired on consignment, approval or sale-or-return terms, and are returned within 60 days of release from customs; or

‒ goods were damaged, of inferior quality, defective, did not include the correct quantity or were not the goods ordered, and the person is not entitled to a tax-free warranty replacement (no QST equivalent).

• The rebate is proportional to the abatement or refund of duty on the duty-paid value, on the assumption that the goods were subject to duty.

• The rebate is subject to a 2-year claim period.

45

References:

• GST/HST Memorandum 4.5.2 “Exports – Tangible Personal Property”.

• GST/HST Memorandum 4.5.3 “Exports – Services and Intellectual Property”.

• RBA Sales Tax Review™, May 1998, “GST and PST on Exports: a Vendor’s Dilemma”, and RBA Sales Tax Review™, September 1996, “Goods Delivered in Québec for Subsequent Export”.

• RBA Sales Tax Review™, September 1998, “GST and PST on Exports, Part II: “Exported Services”.

• Canada Revenue Agency GST/HST Info Sheet GI-034, “Exports of Intangible Personal Property”.

46

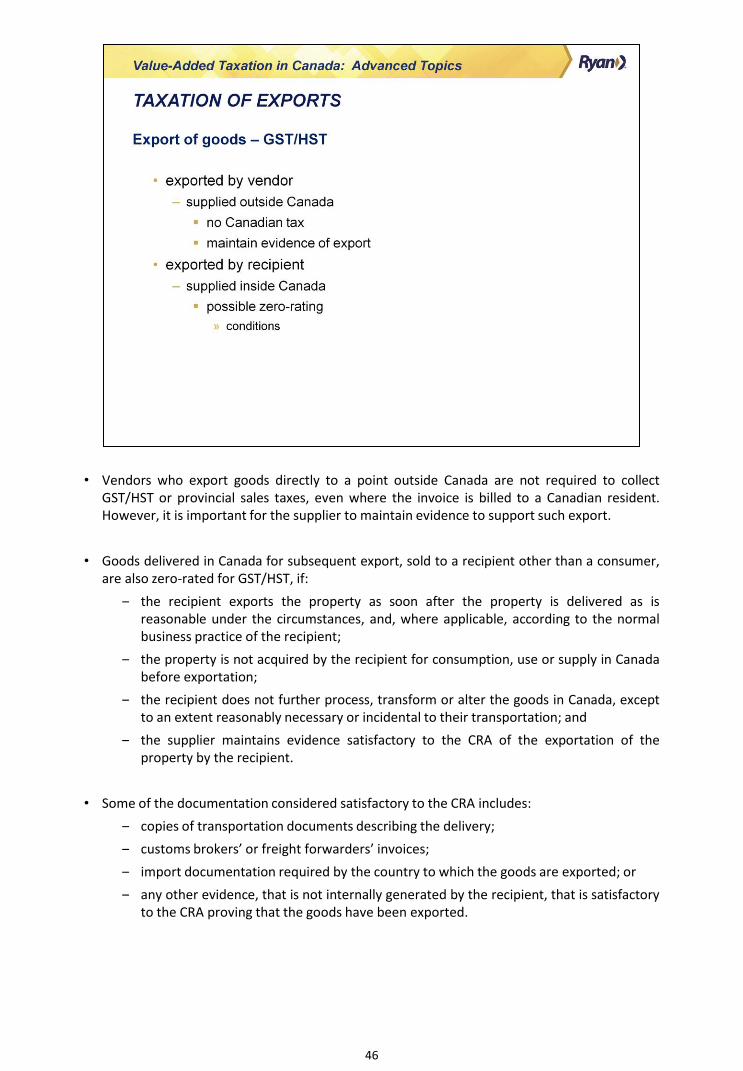

• Vendors who export goods directly to a point outside Canada are not required to collect GST/HST or provincial sales taxes, even where the invoice is billed to a Canadian resident. However, it is important for the supplier to maintain evidence to support such export.

• Goods delivered in Canada for subsequent export, sold to a recipient other than a consumer, are also zero-rated for GST/HST, if:

‒ the recipient exports the property as soon after the property is delivered as is reasonable under the circumstances, and, where applicable, according to the normal business practice of the recipient;

‒ the property is not acquired by the recipient for consumption, use or supply in Canada before exportation;

‒ the recipient does not further process, transform or alter the goods in Canada, except to an extent reasonably necessary or incidental to their transportation; and

‒ the supplier maintains evidence satisfactory to the CRA of the exportation of the property by the recipient.

• Some of the documentation considered satisfactory to the CRA includes:

‒ copies of transportation documents describing the delivery;

‒ customs brokers’ or freight forwarders’ invoices;

‒ import documentation required by the country to which the goods are exported; or

‒ any other evidence, that is not internally generated by the recipient, that is satisfactory to the CRA proving that the goods have been exported.

47

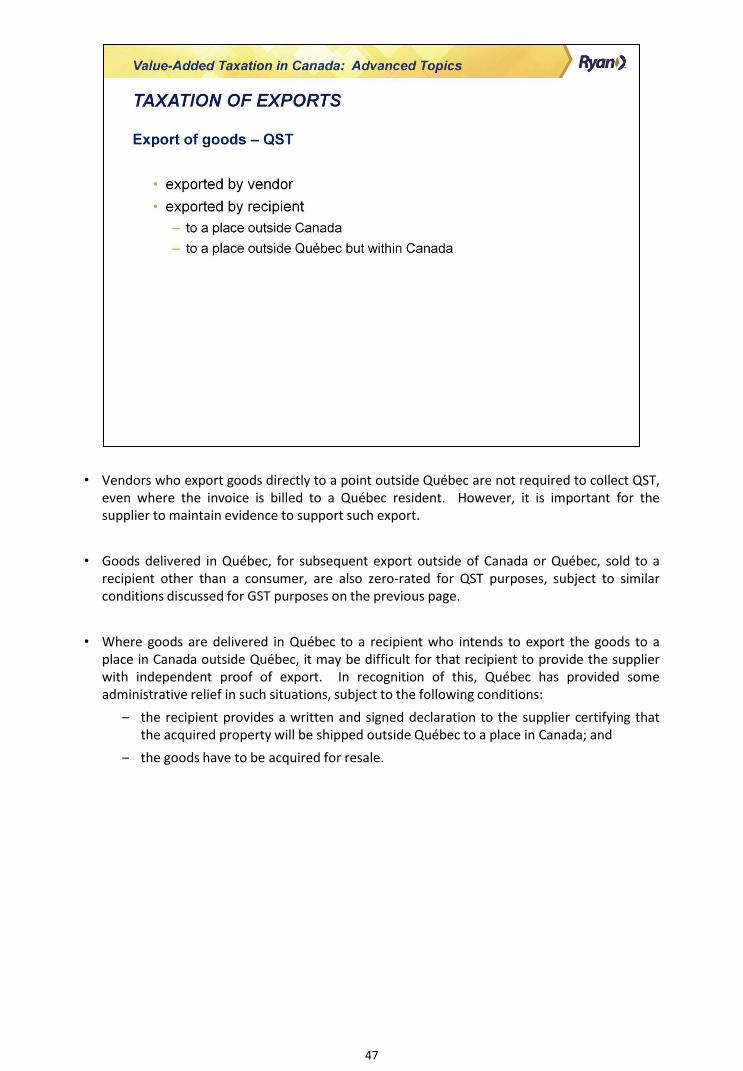

• Vendors who export goods directly to a point outside Québec are not required to collect QST, even where the invoice is billed to a Québec resident. However, it is important for the supplier to maintain evidence to support such export.

• Goods delivered in Québec, for subsequent export outside of Canada or Québec, sold to a recipient other than a consumer, are also zero-rated for QST purposes, subject to similar conditions discussed for GST purposes on the previous page.

• Where goods are delivered in Québec to a recipient who intends to export the goods to a place in Canada outside Québec, it may be difficult for that recipient to provide the supplier with independent proof of export. In recognition of this, Québec has provided some administrative relief in such situations, subject to the following conditions:

‒ the recipient provides a written and signed declaration to the supplier certifying that the acquired property will be shipped outside Québec to a place in Canada; and

‒ the goods have to be acquired for resale.

48

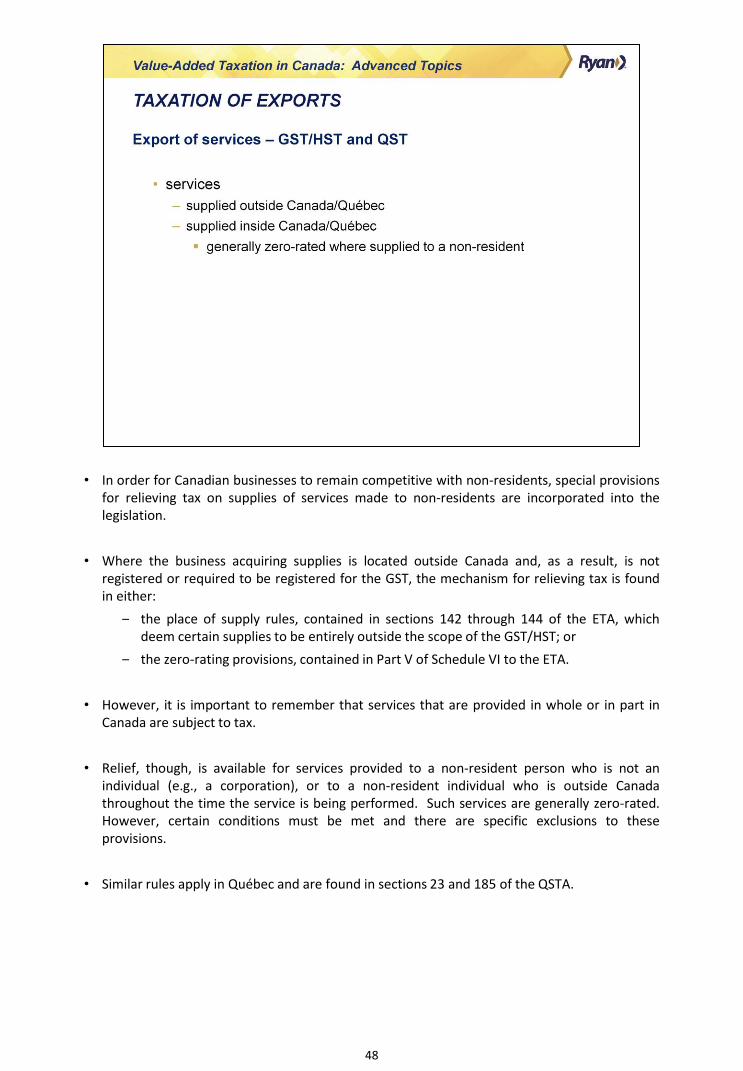

• In order for Canadian businesses to remain competitive with non-residents, special provisions for relieving tax on supplies of services made to non-residents are incorporated into the legislation.

• Where the business acquiring supplies is located outside Canada and, as a result, is not registered or required to be registered for the GST, the mechanism for relieving tax is found in either:

‒ the place of supply rules, contained in sections 142 through 144 of the ETA, which deem certain supplies to be entirely outside the scope of the GST/HST; or

‒ the zero-rating provisions, contained in Part V of Schedule VI to the ETA.

• However, it is important to remember that services that are provided in whole or in part in Canada are subject to tax.

• Relief, though, is available for services provided to a non-resident person who is not an individual (e.g., a corporation), or to a non-resident individual who is outside Canada throughout the time the service is being performed. Such services are generally zero-rated. However, certain conditions must be met and there are specific exclusions to these provisions.

• Similar rules apply in Québec and are found in sections 23 and 185 of the QSTA.

49

• A general provision zero-rates services provided to non-residents of Canada, with a number of specific exceptions, as follows:

‒ a service made to an individual who is in Canada at any time when the individual has contact with the supplier in relation to the supply;

‒ a service that is rendered to an individual, though the supply may be billed to a non-resident corporation while that individual is in Canada (e.g., call centers and support desks);

‒ an advisory, consulting or professional service1;

‒ a postal service1;

‒ a service in respect of TPP or real property situated in Canada at the time the service is performed1;

‒ a service of acting as an agent of the non-resident person or of arranging for, procuring or soliciting orders for supplies by or to the person1;

‒ a transportation service1; or

‒ a telecommunication service1.

1 It is important to note that even though these services may be excluded from the general zero- rating provision as outlined above, other provisions in the legislation may specifically zero-rate

these services, as noted in the following pages.

• Similar rules apply for services to movable (TPP) and immovable corporeal property (real property) situated in Québec and for services provided by a mandatory (agent).

50

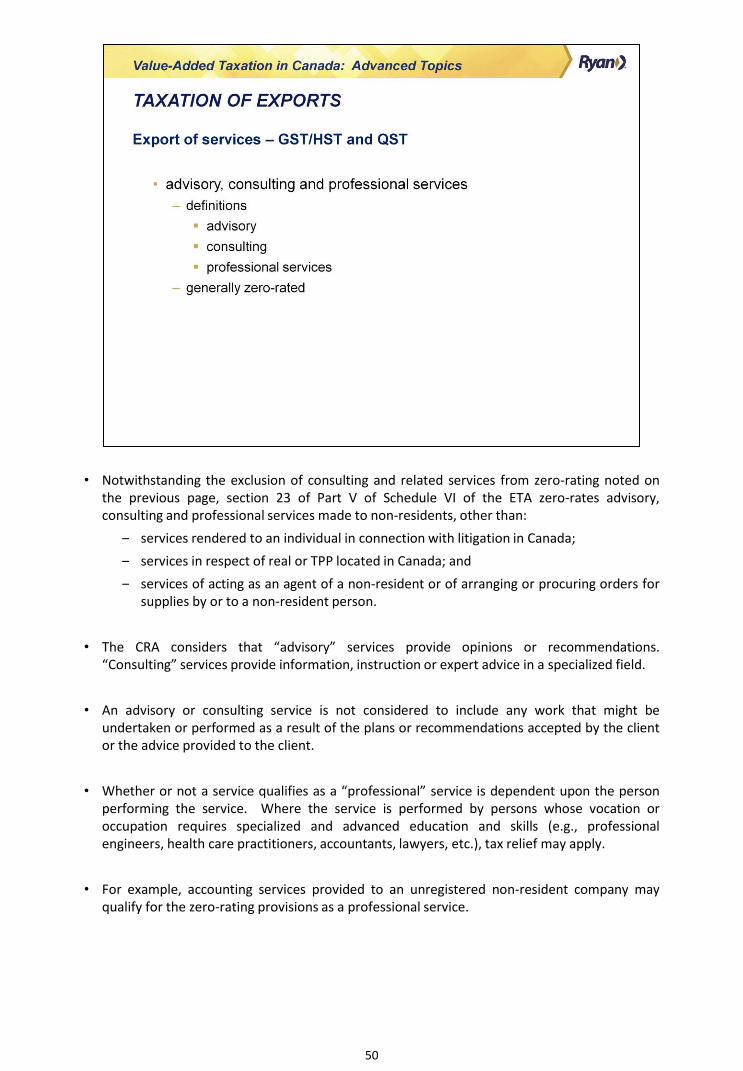

• Notwithstanding the exclusion of consulting and related services from zero-rating noted on the previous page, section 23 of Part V of Schedule VI of the ETA zero-rates advisory, consulting and professional services made to non-residents, other than:

‒ services rendered to an individual in connection with litigation in Canada;

‒ services in respect of real or TPP located in Canada; and

‒ services of acting as an agent of a non-resident or of arranging or procuring orders for supplies by or to a non-resident person.

• The CRA considers that “advisory” services provide opinions or recommendations. “Consulting” services provide information, instruction or expert advice in a specialized field.

• An advisory or consulting service is not considered to include any work that might be undertaken or performed as a result of the plans or recommendations accepted by the client or the advice provided to the client.

• Whether or not a service qualifies as a “professional” service is dependent upon the person performing the service. Where the service is performed by persons whose vocation or occupation requires specialized and advanced education and skills (e.g., professional engineers, health care practitioners, accountants, lawyers, etc.), tax relief may apply.

• For example, accounting services provided to an unregistered non-resident company may qualify for the zero-rating provisions as a professional service.

51

• As previously noted, if the service is in respect of real or TPP located in Canada, the service remains taxable. The same taxing provisions exist for QST purposes. Where the service relates to immovable or corporeal movable property located in Québec, the service remains taxable for QST purposes.

• Note that there is no exclusion to the zero-rating provision when a consulting, advisory or professional service is rendered to an individual while that individual is in Canada, unlike the exclusion under the general zero-rating provision. For example, income tax services rendered to an individual in Canada, but invoiced to an un-registered non-resident, are zero-rated.

• CRA has ruled that the following types of services are taxable where they are in respect of property located in Canada:

‒ physically counting the property;

‒ appraising the property;

‒ physically protecting or securing the property;

‒ enhancing the value of the property; or

‒ facilitating the transfer of ownership of the property.

• Generally, CRA tends to have a broad definition of the term “in respect of”. The relationship between the service and the property must be sufficiently direct for the service to be considered “in respect of” the property.

• For example, rental fees charged to a non-resident for inventory kept in a storage facility that is situated in Canada are taxable for GST/HST purposes as the service is in respect of TPP that is situated in Canada at the time the service is performed. Therefore, storage services do not qualify for relief under the general zero-rating provisions. The same rules apply in Québec.

52

• Though most services related to real property and TPP located in Canada are taxable, there are a number of exceptions. They include:

‒ services in respect of TPP ordinarily located outside of Canada that is brought into Canada temporarily for the sole purposes of having that particular service performed, provided that the property is exported as soon as is feasible after the service is performed (also covers parts supplied along with the service);

‒ services and related parts provided to unregistered non-residents in respect of a warranty provided by the non-resident;

‒ a service of testing or inspecting TPP on behalf of an unregistered non-resident that has been brought into Canada for that sole purpose, where the property is destroyed or discarded after the service is performed;

‒ a service of destroying or discarding TPP located in Canada on behalf of an unregistered non-resident;

‒ a service of dismantling TPP on behalf of an unregistered non-resident for the purpose of export; and

‒ emergency repair services in respect of transportation equipment used by non-resident transportation companies.

• Similar QST rules apply related to corporeal movable property.

53

• It is common for non-residents of Canada to pay commissions to Canadian marketing and sales representatives related to sales of the non-resident’s goods or services.

• Where the non-resident is not registered for GST/HST, it is not in a position to claim ITCs for any of the tax potentially payable on these services.

• After a protracted public debate, followed by a moratorium on assessments of Canadian sales representatives for not collecting GST/HST on commissions received from non-residents, the taxing authorities finally agreed to retroactively amend the GST/HST legislation to zero-rate these services.

• This section also covers services provided by purchasing representatives acting on behalf of non-residents, as well as most services of acting as a legal agent of a non-resident of Canada.

• This zero-rating provision applies even if goods are delivered in Canada by an unregistered non-resident, since most supplies made by an unregistered non-resident are deemed to be made outside of Canada.

• Revenu Québec has adopted the same policy.

54

• A separate provision in Part V of Schedule VI of the ETA zero-rates advertising services supplied to non-residents of Canada who are not registered for GST/HST.

• An advertising service is generally considered by the CRA to be:

‒ a service of creating a message oriented towards soliciting business, or calling public attention by any means including oral, written or graphic statements and representations disseminated by any means, including:

in a newspaper or other publication;

on radio or television;

in a notice, handbill, sign, catalogue, or letter, and

on a billboard or on real property; and

‒ a service directly related to the communication of such a message (e.g., air time on a broadcasting service, space in a publication) where:

the communication service is supplied as part of the supply of a message as defined in the paragraph above; or

the person providing the communication service can demonstrate that, at the time the supply is made, the service is in relation to a supply of a message as defined in the paragraph above.

• Similar rules are found in section 186 of the QSTA.

55

• Other specific services for which zero-rating provisions have been provided include:

‒ custodial and nominee services in respect of securities or precious metals of a non-resident;

‒ services of instructing non-resident individuals in certain qualifying courses; and

‒ postal and telecommunication services supplied by organizations in the industry where they are supplied to non-residents operating in the same industry.

• Cross-border transportation services are generally zero-rated under provisions contained in Part VII of Schedule VI to the ETA and Division VII of the QSTA with special rules covering, among other things, continental air travel.

56

• For most of the zero-rating provisions discussed on the previous pages, there are two key components in determining their application.

• The first is verifying that the service in question is a qualifying service based on the nature of the supply.

• The second is determining that the purchaser is in fact a non-resident, or an unregistered non-resident, as the case requires.

• It is not completely within a supplier’s ability to determine a recipient’s registration and residency status. As a result, both the CRA and Revenu Québec permit a supplier to obtain a certificate from the recipient attesting to the purchaser’s status. This certification must be retained by the supplier for inspection by a CRA or Revenu Québec auditor. Both taxing authorities will generally consider this sufficient to support the non-collection of tax.

• Failure to obtain this documentation may result in an assessment for tax and interest.

57

• A supply of IPP made to a non-resident was previously zero-rated only where the non-resident was not registered at the time the supply was made and the supply was one of intellectual property or of any right, licence or privilege to use such property. Intellectual property includes an invention, patent, trade secret, trade-mark, trade-name, copyright or industrial design. Therefore, supplies of other intangibles such as memberships and franchise rights, that are not included in the definition of intellectual property, remained taxable.

• The CRA considers a supply of software that is IPP delivered electronically to qualify for zero-rating under this provision. Software supplied by way of physical media, such as CD-ROM, is considered to be TPP and would not be covered by these provisions and would likely be zero-rated by the zero-rating provisions for exported goods discussed earlier.

• The ETA currently zero-rates all supplies of IPP provided to unregistered non-residents of Canada, effective for supplies made on or after March 20, 2007.

• However, exceptions to this zero-rating provision include supplies of IPP that:

‒ are made to an individual who is in Canada at the time the supply is made;

‒ are related to real or tangible personal property normally located in Canada;

‒ are related to a service rendered in Canada that is not a zero-rated exported service; and

‒ may only be used in Canada.

58

• In order to zero-rate a supply of IPP to a non-resident, a supplier must verify the registration status, the residency and/or physical location (if an individual) of their customer.

• Verification of registration status of customers:

‒ suppliers must maintain evidence that the supplies are made to customers who are not registered when the supplies are made.

‒ for purposes of zero-rating supplies of IPP made over the internet, CRA will generally accept an online self-declaration by customers that they are not registered.

• Verification of residency status of customers:

‒ suppliers must maintain evidence that the supplies are made to non-residents of Canada when the supplies are made.

‒ CRA will generally accept an online self-declaration by non-resident customers along with their complete home address as proof of residency, provided it is supported by another verification method.

‒ examples of other methods include the comparison of declared address versus billing address per credit/debit card company records and the use of geo-location software.

• Verification of physical location of non-resident customers who are individuals:

‒ suppliers must maintain evidence that individuals are physically outside Canada when the supplies are made.

‒ CRA will accept the use of geo-location software to verify that the individual is outside Canada when the supply is made.

59

• An export trading house is an organization that is engaged exclusively, 90% or more, in export trading activities. An export certificate issued by an export trading house is a written representation that the trading house will export the goods in the circumstances and under the conditions required for zero-rating to apply.

• Generally, a registered supplier is required to collect tax on goods delivered in Canada. Where the recipient of a supply is an export trading house that has been authorized by the Minister to issue export certificates, the supplier may accept such a certificate as sufficient proof of export for purposes of zero-rating. Under the Export Trading House Program, if an export trading house issues a certificate that is not in effect or does not export the property, tax applies to the supply.

• However, a supplier is absolved of the liability to collect and account for the tax, provided the supplier did not know and could not reasonably be expected to have known that the goods would not be exported. If this condition is met, the supply is treated as being zero-rated.

• An export trading house must apply, in prescribed form, to the CRA or Revenu Québec for authorization to issue export certificates, which are valid for three years only. The Minister may so authorize a person if it is reasonable to expect that the person will meet the following two tests during the next 12-month period:

‒ at least 90% of the inventory the person purchases in Canada or Québec for resale will qualify for zero-rating as sales for export; and

‒ 90% of the person’s sales outside Canada or Québec of items of inventory that were acquired or imported into Canada or Québec will be of items that were sold without having been consumed, used, processed, transformed, or altered by the person.

60

• Exporters of processing services, or inward processors, can be described as manufacturing service companies. Manufacturing service companies perform manufacturing services (i.e., assembly, manufacture, alteration, etc.) on goods or materials that they do not own for which they charge a fee.

• Relief is available under this provision to both GST/HST and QST registered exporters of processing, storage and distribution services where the services are provided to a non-resident. Imported goods or materials that qualify to be imported or purchased tax-free under the “inward processing relief” provision include:

‒ goods that are to be processed, distributed or stored in Canada or Québec and subsequently exported;

‒ goods to be incorporated or transformed into, attached to, or combined or assembled with other goods that are processed in Canada or Québec and subsequently exported; or

‒ materials (other than fuel, lubricants or plant equipment) directly consumed or expended in the processing in Canada or Québec of other goods that are subsequently exported.

• In each case, the goods that are being exported may not be used or consumed in Canada or Québec prior to export for any purpose except to the extent reasonably necessary or incidental to their transportation. The exportation of the imported goods or materials being processed in Canada/Québec must occur within four years from the day on which the goods are accounted for under section 32 of the Customs Act. The registrant cannot be closely related to the non-resident person on whose behalf the processing is being done.

• In order to take advantage of the relief, qualifying GST/HST-registered and QST-registered organizations must apply for a letter of authorization.

61

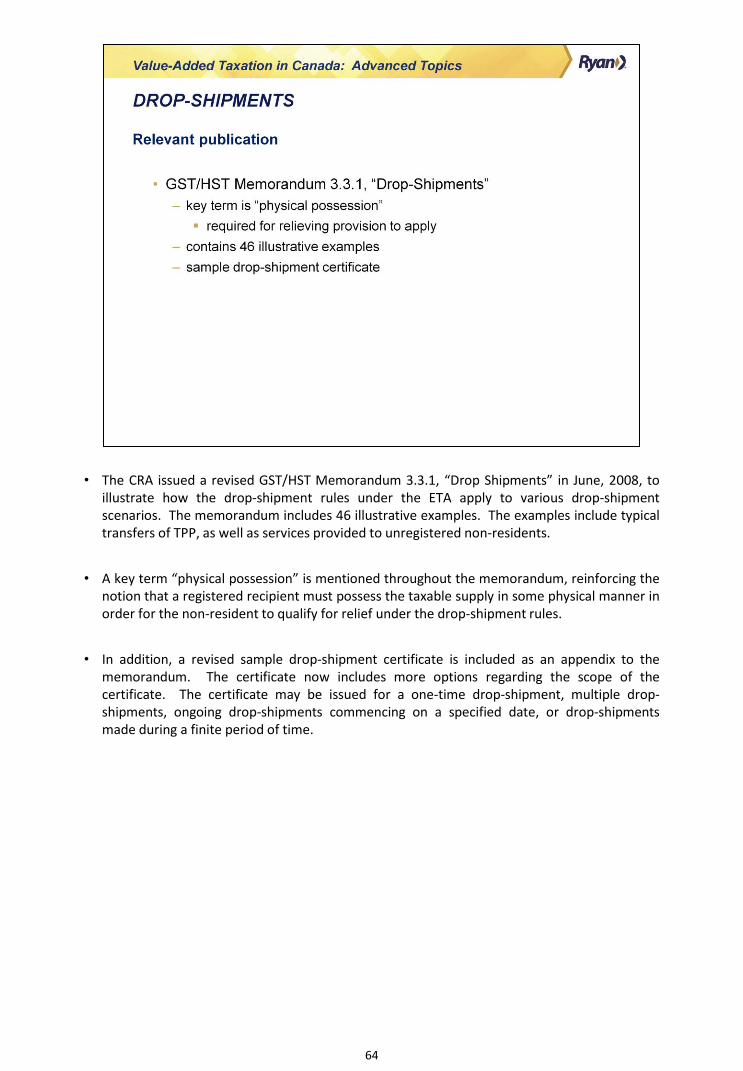

References: • GST/HST Memorandum 3.3.1, “Drop-Shipments”.

• RBA Sales Tax Review™, March 1999, “GST and QST on Drop-shipments”.

• RBA Sales Tax Review™, September 2000, “GST and QST on Drop-shipments: Commercial

Services”.

62

• From the inception of the GST, the federal government realized that in order to assure the international competitiveness of Canadian businesses, from a sales tax perspective, special rules were needed for certain transactions involving non-residents, particularly from the U.S. Canada does not have the ability to require non-residents to register and many are not prepared to do so voluntarily.