Embed Size (px)

Citation preview

Valuation in GST

GST National Conference

ICAI-IDTC | SIRC-Chennai

Jun 2017

Basics for Valuation

• Relationship between:

– Consideration

– Price

– Value

• CGST Act refers:

– Levy and value

– Turnover and value

– Assessable value or

transaction value

• Value of supply:

– Means or is; or

– Shall e…..which is

• Key considerations:

– Cost impact by credit

– Relevance of Dai Ichi

– Income re-characterization

– Retention money

Express Provisions

• Key disqualifications:

– Price:

• Actually paid

• For the supply

– Unrelated parties

– Price is sole consideration

• Value to exclude:

– Discount on supply

– Discount allowed later:

• Est. by agreement

• Linked to invoice

• Value to include:

– Other taxes imposed

– Amounts owed by supplier

but paid by recipient

– Costs at / efore supply

– Interest or late charges

– Direct subsidies

Recourse to Rules

• Declaration or

prescription: ”…. alue of supply…..cannot be

determined under ss 1 ….”

• Reference to Rules:

– i all situatio s or – o ly i these situatio s

• Disqualified by s.15(1)

• Situations specified:

– Consideration not in

money terms

– Related persons

– Sole consideration

• Tariff value notified

Implied Provisions • Valuation for IGST to be

integrated with Customs

• Value of supplies with:

– Land and rights in land

– Excluded supplies

• Value for:

– Credit attri uta le

– Job-work (not u/s 143)

– Included consideration

– Any other consideration

– No consideration

– Incentive to distributor

• Key considerations:

– Leasing and HP

– Transport by rail

– Air-travel agents

– Insurance services

– Money changers

– Lottery distribution

– Reimbursable charges

– Chit fund activities

– Undivided share in land

– Inter-branch transfers

– Provision for bad-debts

Valuation Cases

• Reimbursable charges

• Warranty replacement

• Out-of-warranty

• Recovered parts

• Free or defaced samples

• Free-of-charge (project)

• Free replacements for:

– Transit-loss

– Quality defect

– Project delay

• Free-issue-material

• Part-B supplies • Demo/trial equipment

• Stand-by equipment

• Loss-leader produ ts

• Sale price below cost

• Bra hes at loss

• Pseudo discounts

• Sponsorship/subsidy

• Paid dis ou t oupo s

Place of Supply in GST

Jun 2017

Subject of GST

• Purpose of provision:

– Common provision

– Desti atio pri iple

• Relation to S.7 and 8

• Facts about:

– Place of supply ..shall be..

– Location of supplier – not

used

Goods

(S.10 &

11)

Services

(S.12 & 13)

Goods

as services

Place of Supply s. 10(1)(a)

• Supply i ol es movement:

– Supply i ol es

movement

– Supply i ol es o e e t

• Refer o asio s o e e t fro CST

Act

• Question of fact:

– fro ter s of supply

– fro ature of goods supplied

• Termination of

o e e t for delivery

Place of Supply s. 10(1)(b)

• Key considerations:

– Locus standii

– Recipient s.2(93)

– Overriding force

– Supply – limbs?

• Review supply model,

pre and post-GST

Supplier

Third

Party

Recipient

A

B

1 2

10(1)(b) 10(1)(c)

Place of Supply s. 10(1)(c)

• Supply does ot involve movement:

– …. hether y….

– ….supplier or re ipie t….

• Place is location of

goods at ti e of delivery

• Key considerations:

– What goods do ot involve movement?

– Where would they be

taken for consumption?

Place of Supply s. 10(1)(d)

• Assembly at site:

– Delivery to site for

assembly

– Assembly at site after

delivery

• Interpretation of:

– Where the goods are asse led….

– ….shall e pla e of su h asse ly

• Key considerations:

– Would works-contract be

covered s. 2(119)?

– Ho a y supplies i source-transfer-assemble?

– Which limb does clause

(d) address?

Place of Supply s. 10(1)(e)

• Supply o oard conveyance:

– Supply of goods to airline

– Supply to passenger by

airline

• Interpretation of:

– ….lo atio at hi h su h goods are taken on

board

• Key considerations:

– Differentiate between

supply to conveyance and

supply on-board conveyance

– Only one limb covered

Place of Supply s. 10(2)

• Residual provision

• Exclude other provisions

• Deter i e pla e of supply as pres ri ed

• Key considerations:

– Where….. a ot e deter i ed….

– Which circumstance?

International Supply

Imports

• Definition:

– Import

– Importer

• Place of supply is location of

importer

• Key considerations:

– Place of import

– Port of import

– Reimport of exports

– Warranty imports

Exports

• Definition:

– Export

– Exporter

• Place of supply is location

outside India

• Key considerations:

– Currency of transaction

– Location of recipient

– Merchanting trade

– High sea sales / SICOI

– Impact on credit

Subject of GST

Goods

(S.7 & 8)

Services

(S.9 & 10)

Goods

as services

• Identify services or goods

with caution

• Relation to s. 7 and 8

• Facts about:

– Legislative will – place

– Location of supplier of

services s. 2(15)

Place of Supply s. 12(3)

• Supply of:

– Immovable property –

grant-of-rights,

construction or use

– Vessel, etc.

– Ancillary services

• Place is location of

property

• Key considerations:

– Scope of i relatio to and y ay of

– Meaning of location

Place of Supply s. 12(4)

• Supply of:

– Restaurant and catering

– Personal grooming

– Fitness

– Beauty treatment

– Health service including

cosmetic and plastic

surgery

• Place is location of

a tual perfor a e

• Key considerations:

– Exhaustive or illustrative

– Specific or expansive

– Rule implies taxability of

new activities

– Implication to registered

recipient

Place of Supply s. 12(5)

• Supply of:

– Training and

performance appraisal

• Place is location of:

– registered recipient

– a tual perfor a e to unregistered recipient

• Key considerations:

– Location of such person

s. 2(14)

Place of Supply s. 12(6)

• Supply of admission to:

– Cultural & artistic

– Sporting

– Scientific & educational

– Entertainment &

amusement event

• Place is venue of event

• Key considerations:

– Admittance to viewer

– Ancillary services

Place of Supply s. 12(7)

• Supply of:

– Organizing event

– Ancillary services

• Place is location of:

– registered recipient

– venue of event if

recipient unregistered

• Key considerations:

– Assigning sponsorship

– Distribution by

proportion of large

events

Place of Supply s. 12(8) & 12(9)

• Supply of:

– Transport of goods

– Transport of passenger

• Place is location of:

– registered recipient

– loading or boarding if

unregistered recipient

• Key considerations:

– Mode of transportation

not specified

– Unspecified pre-booking

PLUS place not known

– Return booking, separate

Place of Supply s. 12(10)

• Supply of services on-

board

• Place is first poi t of departure

• Scope of supply:

– To conveyance operator

– By such operator

• Key considerations:

– Place of supply known

even before supply

– Will explanation in ss. 9

apply to return journey

Place of Supply s. 12(11)

• Supply of:

– Device-dependent telecom service

– Mobile telecom service:

• Post-paid basis

• Pre-paid basis

– Any other

• Place is:

– Location of in situ device

– Post-paid / e-pay billing address

– Pre-payment location

– Address-on-record

• Key considerations:

– Ownership of device

– Fixed-wireless telephone

– Data-card for laptop

Place of Supply s. 12(12)

• Supply of:

– Banking

– Financial and broking

service

• Place is:

– address i supplier s records

– location of supplier

(address not on records)

• Key considerations:

– Not ser i es y ut of

– Overlapping services –

financial v/s consulting

– Supplier-guided category

of services

Place of Supply s. 12(13)

• Supply of insurance

service

• Place is:

– location of registered

recipient

– address i supplier s records

• Key considerations:

– Ancillary services not

covered

– Services to insured not to

any others

Place of Supply s. 12(14)

• Supply of advertisement

service to Government

• Place is State of

dissemination in

proportion

• Key considerations:

– Ser i es to ot y

– Allocation by reasonable

asis i a se e of contract

Place of Supply s. 12(2)

• Supply of any other

service

• Place is:

– location of registered

recipient cl.(a)

– address i supplier s records cl.(b)(i)

– location of supplier

cl.(b)(ii)

• Key considerations:

– When not covered by

ss.3 to 14

– If none of above, then:

• To registered person cl.(a)

• To any other cl.(b)

International Supply

• Exports-imports (s.13)

• Supplier or Recipient

located outside India

• Location of recipient is

place of supply, unless:

– Location is determined

by other provisions or

– Location unknown then

it is location of supplier

• Services on goods:

– Goods made available

– Recipient present

• Service on immovables

• Services of admission

• Origin-of-supply (3)

• Transport service

• On-board services

• OIDAR

GST -Some Basic Concepts

Presented By:

CA Madhukar Hiregange

Necessity for GST

• Present system of indirect tax has multiplicity of taxes levied by Centre & State

• Tax on tax, increases cost - Cascading

• No uniformity of tax rates – Confusion when to pay, on what to pay

• Increase in compliance & administration costs

• Credit blockage due to restrictions under various laws – Luxury tax, VAT, ST

Example:

i. A Service provider cannot claim VAT , Luxury tax, SAD Credit...

ii. A VAT dealer cannot claim CST , luxury tax, Service tax Credit...

iii. A a ufacturer ca ot clai CST, Lu ur ta …Credit.

Hiregange 2

Does GST help India progress?

• GDP Growth go Up by about 2-4%

• International Competitiveness by about 5-8%

• Increased FDI- Already seen

• Common Market- Tax distorted locations and check post delays would not be there.

• All those who gain to be part of tax payment

• Lower transaction cost – reduced corruption

• Increased IDT + Direct Tax Revenue

Hiregange 3

What is GST (Goods and Service Tax)?

• Ta o Suppl of Goods & Services

• Destination based tax – Global Integration

• Goods – Every kind of movable property other than money and securities.

• Services – Anything other than goods

• Thus, GST has a wider coverage, and merges 11 Taxes.

• India proposes dual GST model – Federal Structure - CGST & SGST.

• Internationally, GST was first introduced in France and now more than 160 countries have introduced GST

Hiregange 4

Levy

• CGST/SGST - shall be levied on all intra-State supplies of goods

and/or services

• IGST - shall be levied on all inter-State supplies of goods

• Composition Levy – Not applicable to services ( Incl. WCT) - pay 0.5

1% for traders Restaurants – 2.5% - More later

• Reverse Charge – Goods ( URD ) & Services ( Unregistered,

Unorganised, Import) – Even those in Threshold as they will not be

registered.

Hiregange 5

Levy & Collection

18

• Services

• Goods

• Goods as services

1: Subject

• Included

• Implied

• Excluded

2: Supply

• Specified for goods

• Specified for services

4: Time

• Inter-State

• Intra-State

3: Place

© Indirect Taxes Committee, ICAI

Levy & Collection

© Indirect Taxes Committee, ICAI

19

Description Composite Supply Mixed Supply

Naturally bundled Yes No

Supplied together Yes Yes

Can be supplied separately No Yes

One is predominant supply for recipient Yes No

Other supply is not ‘aim in itself’ of recipient Yes No

Each supply priced separately No No

All supplies are goods Yes Yes

All supplies are services Yes Yes

One supply is goods and other supply is services Yes Yes

While, the above tests could be guiding principles in determining as to whether a supply is composite or mixed supply

the end user test could be adopted as one of the criteria; Every supply will have to be independently analysed.

COT

Eligible

Available

Availed

Allowed

Compliance

Hiregange

Composition Levy – Sec. 10 of CGST Act-2017

8

Composition Scheme For the person who has AGGREGATE TURNOVER equal or less than

50 lakhs IN PR. YR AND CURRENT YEAR

Rates – [1+1] = 2% in case of a manufacturer ( other than notified)

- [0.5+0.5] = 1% for Traders

- [2.5+2.5]= 5% for Small suppliers of food & beverages*

• Note: Not available for service providers other than food related.

• If not eligible then very very difficult.

• Quarterly return- Upload of purchases?

9 Hiregange

C

O

M

P

O

S

I

T

I

O

N

Composition SchOptional

emeO

• Optional Scheme: Not for B2 B suppliers

• Taxable person who affects any inter-state supplies of G & / S - not entitled for

composition scheme.

• No stock of goods procured interstate or Import

• Person having business in different places and separately registered all of them

should opt for composition scheme.

• Person cannot be in composition in one registration and outside in another

registration.

• A taxable person who pays tax under composition levy shall not collect any tax

from the recipient on supplies made by him nor shall he be entitled to any credit.

• Industry representation needed made to ease some of these conditions to

enable the survival of small business man without breaking the chain of credit.

Hiregange 10

Exemption

• Rs. 20 Lakhs Aggregate T.O. ( Rs. 10 Lakhs for Special smaller States)

• No credit without registration

• Transactions by CG/ SG/ Local Body – not a supply

• Goods/ Services exempted by CG/ SG to be notified.

• Very Few Exemption: Primary Health/ education, specific cereals..

• Tax expected on: textiles, defense, research ++

Hiregange 11

12

Pre - GST

Post - GST

Role of Chartered

Accountant

Role of CA

Pre-GST Period

Post-GST Period

13

Role as per Model GST Act, 2016

Overview Operational Consultancy

Network support & Infra.

Accounting & Taxation

Compliance requirement

Transitional Support Sr.

Centre/State Support Sr.

Audit & Assurance

Pre-GST Period Role as pre GST Act 2. Overview 3. Operational Consultancy 4. Network support & Infra. 5. Accounting & Taxation 6. Transitional Support Sr. 7. Centre/State Support Sr. 8. Global Opportunities

14

• Inspection/ Access to Business Premises

•Appearance by Authorised Representative

• Dept./ Special Audit

• Accounts and other records

• Audit –

• Rs.1 Cr. Section 35

35(5)

Section

65/ 66

Section 67

Other- Prof-

Better Fees

Section 152 – Disclosure of Information by Public Servant

Pre-GST Period 1. Role - pre -GST Act 2. Overview 3. Operational Consultancy 4. Network support & Infra. 5. Accounting & Taxation 6. Transitional Support Sr. 7. Centre/State Support Sr. 8. Global Opportunities

Being in a position to analyse the industry impact considering the global and Indian situation of the product / service;

In case of unintended hardship to some sectors- representation to the drafter would be in order as the level of listening presently is high; Akin to Companies Act

The clarity on the major impact on the client under GST due to in-depth understanding of the business; This presently service offering would provide the client with important information to plan the way forward under GST. This could be done as GST law is in place;

Being part of the core team of client for analysing, transiting into GST smoothly without business disruption & safeguarding of margins or as a knowledge advisor for s/w developers;

15

Pre-GST Period 1. Role as pre M-GST Act 2. Overview – Key Areas 3. Operational Consultancy 4. Network support & Infra. 5. Accounting & Taxation 6. Transitional Support Sr. 7. Centre/State Support Sr. 8. Global Opportunities

• Systems at client workplaces so as to provide appropriate advise on migrating to better systems/ ERP or suggest modification to make the existing systems GST compliant;

Understanding legacy tax

• For example supporting in decisions on: Closure/ reduction in godowns and branches; direct sale through e- commerce; evaluation of the working with C&F agents; in house/ outsourcing the distribution function to logistic companies; sourcing inputs at lowest cost within shorter time; linking to the ERP of the customer etc.;

Assisting in preparation of a strategic plan for procurement and

marketing systems of clients needed

under GST.

16

Pre-GST Period 1. Role as pre M-GST Act 2. Overview – Key Areas 3. Operational Consultancy 4. Network support & Infra. 5. Accounting & Taxation 6. Transitional Support Sr. 7. Centre/State Support Sr. 8. Global Opportunities

Changes in accounting software and internal control systems to suit GST. Test and guide & confirm the robustness;

GST awareness at initial stages and training for management, staff, vendors of clients.

Vetting and suggestion to modify agreements/ contracts/ major purchase orders overlapping or supplies to be made in GST regime;

17

Pre-GST Period 1. Role as pre M-GST Act 2. Overview – Key Areas 3. Operational Consultancy 4. Network support & Infra. 5. Accounting & Taxation 6. Transitional Support Sr. 7. Centre/State Support Sr. 8. Global Opportunities

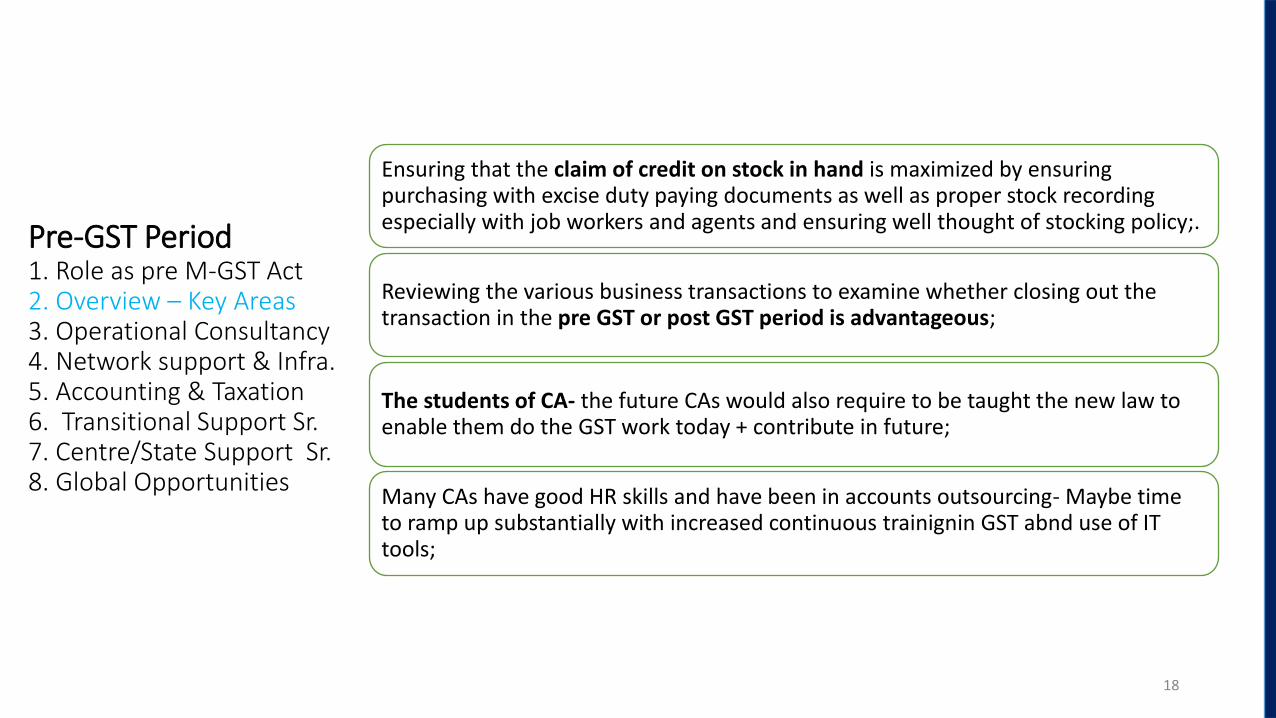

Ensuring that the claim of credit on stock in hand is maximized by ensuring purchasing with excise duty paying documents as well as proper stock recording especially with job workers and agents and ensuring well thought of stocking policy;.

Reviewing the various business transactions to examine whether closing out the transaction in the pre GST or post GST period is advantageous;

The students of CA- the future CAs would also require to be taught the new law to enable them do the GST work today + contribute in future;

Many CAs have good HR skills and have been in accounts outsourcing- Maybe time to ramp up substantially with increased continuous trainignin GST abnd use of IT tools;

18

Pre-GST Period 1. Role as pre M-GST Act 2. Overview – Key Areas 3. Operational Consultancy 4. Network support & Infra. 5. Accounting & Taxation 6. Transitional Support Sr. 7. Centre/State Support Sr. 8. Global Opportunities

19

• Revisit the pricing strategies with the distributors

• Renegotiate (if any) the pricing with suppliers

Pricing

• Alignment of all major contract terms and tax clauses with GST

• Discounts terms to be specifically brought out in the contracts executed with distributors

Review of contracts

• Making representation for lower rate of GST, taxability of promo products issued free

Representations

• Maintaining detailed registers of supply and procurements, input credits

• Timely filing of monthly and annual returns

Compliance and documentation

Pre-GST Period 1. Role as pre M-GST Act 2. Overview – Key Areas 3. Operational Consultancy 4. Network support & Infra. 5. Accounting & Taxation 6. Transitional Support Sr. 7. Centre/State Support Sr. 8. Global Opportunities

20

• Tracking GST developments and creating awareness on GST

GST developments – Sharing

• Mapping impact of GST on current supply chain and suggesting modifications from GST perspective

Impact on supply chain – Function wise

• Identifying impact on financials, working capital, credit chain, concessions, and suggesting controls/ Short proc + planning options

Imp.on bus./finance – Focus on SOP + controls

• GST awareness trainings, review of compliances, creation of manuals and access to GST updates/resolution to queries

Post implementation compliances

• Changes to ERP modules, MIS reports, statutory compliance support, and ongoing trouble shooting support

ERP Updation - Validation

Pre-GST Period 1. Role as pre M-GST Act 2. Overview – Key Areas 3. Operational Consultancy 4. Network support & Infra. 5. Accounting & Taxation 6. Transitional Support Sr. 7. Centre/State Support Sr. 8. Global Opportunities

Synchronising IT Systems & Old

data

Strong Management Information

System

System Reconciliations

Data Integration between Centre &

States

Automation of returns and other utilities at Centre as well as States

Updating Amendments in

IT Systems

Data management for State Jurisdiction

21

Pre-GST Period 1. Role as pre M-GST Act 2. Overview – Key Areas 3. Operational Consultancy 4. Network support & Infra. 5. Accounting & Taxation 6. Transitional Support Sr. 7. Centre/State Support Sr. 8. Global Opportunities

Treatment of Incentives / Discount

Process Documentations & Accounting Manuals

Branch Transfers

Budgetary Controls

Control & Dispute Settlement

22

Pre-GST Period 1. Role as pre M-GST Act 2. Overview – Key Areas 3. Operational Consultancy 4. Network support & Infra. 5. Accounting & Taxation 6. Transitional Support Sr. 7. Centre/State Support Sr. 8. Global Opportunities

Deregistration from Existing Laws

Managing Pending Litigations

Review & Certification of Stock on date of transition

Knowledge Sharing & Capacity Building

Credit Analysis and Utilization

Comparative Valuation Under GST

23

Pre-GST Period 1. Role as pre M-GST Act 2. Overview – Key Areas 3. Operational Consultancy 4. Network support & Infra. 5. Accounting & Taxation 6. Transitional Support Sr. 7. Centre/State Support Sr. 8. Global Opportunities

Representation - unintended hardship to sectors

Conscripting Legislation & Rules/ Procedures

Monitoring Transactions & Revenues

Cross –verification with Other Acts

Training & Education

Fixing Rate Based on RNR and Review

24

Pre-GST Period 1. Role as pre M-GST Act 2. Overview – Key Areas 3. Operational Consultancy 4. Network support & Infra. 5. Accounting & Taxation 6. Transitional Support Sr. 7. Centre/State Support Sr. 8. Global Opportunities

Tax Advisory Services

International Research Issues

Knowledge Process Outsourcing

Information & Knowledge Sharing

Capacity Building Services

Technology Support Services

25

Pre-GST Period 1. Role as pre GST Act 2. Overview – Key Areas 3. Operational Consultancy 4. Network support & Infra. 5. Accounting & Taxation 6. Transitional Support Sr. 7. Centre/State Support Sr. 8. Global Opportunities*

How to get awareness in GST?

• Start focused reading/practice in VAT, Central Excise or Service Tax till 1 July

or 1st September 2017 + Update on CGST / IGST/ UTGST + State Laws – Now

• Use online resources – [email protected] , gstclub, caclubindia, linkedin &

others.

• Form a small group for GST updates in your office

• Attend GST Cert. Course + focused workshops.

• Read books/ write articles for internal use…

Hiregange 26

How to get Expertise in GST?

• Write Articles – start with 1 small topic

• Do One Impact study for free or nominal fee

• Be part of future expert group – Mainly CA + 1/2 experienced advocates- meet 2 days a week with a paper presenter.

• Attend the weekly study circle in local branch/ RC.

• Analyse all the suggestions made to Govt by various authorities ( ICAI)

• Write a topics GST book on a sector or areas of concern

• Answer online forums with care/ in depth reading

Hiregange 27

INPUT TAX CREDIT

UNDER GST

1

2

GST on Goods

/service

Used/intended

to be used in the

course or

furtherance of

business

Restricted Items

INPUT TAX SCHEME

ITC

3

Input tax

Inputs

Capital Goods

Input services

TAX PAID ON

4

TAXES ON WHICH CREDIT IS ELIGIBLE

IGST, CGST, SGST / UTGST

IGST on import of goods or services

GST paid on reverse charge basis

Tax paid under composition does not qualify as input tax

a) Motor vehicles / other conveyances:

5

ITC for Motor

Vehicles will

NOT be

available

Except when they are used for:

Transportation of goods, or

Making the following taxable services:

i. Further supply of such vehicles/

conveyances, or

ii. Transportation of passengers, or

iii. Imparting training for driving/

flying/ navigating such vehicles/

conveyances

iv. Transportation of goods

RESTRICTED ITEMS

6

b) Supply of goods and services being:

Food and

Beverages

Outdoor

Catering

Beauty

Treatment

Health

Services

Cosmetic

and Plastic

Surgery ITC Not

allowed,

except

when used

in outward

supply of

same

category

Life/ health

Insurance Rent-a-cab

Govt notifies services obligatory for

employer to employees

RESTRICTED ITEMS

No credit shall be allowed for the following services:

Membership

of club

Health and

Fitness

Centre

Travel

Benefits to

employees

RESTRICTED ITEMS

8

c) Works Contract (other than plant & machinery)

d) Construction of Immovable Property (other than plant & machinery)

Works contract services,

Except where it is an input

service for further supply of

works contract service

Goods or services received by a taxable

person for construction of an

immovable property on his own account

including when used in course or furtherance

of business;

ITC not Available

Construction includes re-

construction, renovation,

addition or alteration or

repairs to the extent of

capitalisation.

RESTRICTED ITEMS

9

Other restrictions

e. GST paid under composition scheme under section 10;

f. Goods or services or both received by a non-resident taxable person except on

goods imported by him;

g. Goods or services or both used for personal consumption;

h. Goods lost or stolen/ written off/ disposed off by way of gift or free samples;

(Gifts to employees beyond Rs.50, 000 is considered as supply- what happens to

credit?)

i. Tax paid after adjudication where there involves fraud etc. (S. 74) / detention (S.129)

/ confiscation of goods (S. 130)

ITC – availment & utilisation

10

System for a seamless flow of credit

Extends to inter-State supplies

Credit utilization u/s 49 would be as follows:

CGST and SGST/UTGST

cannot be mutually set-off.

Tax To be adjusted with

IGST 1) IGST

2) CGST

3) SGST

CGST 1) CGST

2) IGST

SGST 1) SGST

2) IGST

UTGST 1) UTGST

2) IGST

11

Invoice • In possession of invoice or other document

Receipt

• Receipt of goods or services [Instalment supply - credit only upon

receipt of the last lot/ instalment.

• Goods deemed to be received by a registered person when the supplier delivers the goods to the recipient/ any other person, on the direction provided by the registered person.

Tax

• Tax payment and filing of returns by supplier

CONDITIONS FOR AVAILMENT

12

Payment

• Payment to supplier within 180 days of date of invoice

Depreciation

• No depreciation on credit amount of capital goods

Time limit

• Credit to be availed before filing of return for Sept month of next FY or before filing of annual return (earliest)

CONDITIONS FOR AVAILMENT

13

Regular supply

Invoice of supplier

Price variation

Debit note

Reverse charge

Invoice made by recipient

import

Bill of entry

ISD

Document issued by ISD

Document on the basis of which credit could be availed

APPORTIONMENT OF ITC

INPUT TAX CREDIT

14

15

Exempt supply

NIL rated Exemption Non

taxable supplies

“non-taxable supply” means a supply of goods or services which is not leviable to tax under this Act or under IGST

Supply to SEZ / SEZ unit or Exports are ZERO rated supplies and not

exempt supplies

S.17 - First apportion – partly used for business and partly for other purposes (non-business):

16

Use of input tax credit

Attributable to Business purposes

Credit available

Attributable to Other Purposes

Credit not available

Formula for apportion is given in Draft ITC Rules

S.17-Second apportion – partly used for taxable supplies and partly for exempted supplies:

17 Formula for apportion is given in Draft ITC Rules

Use of input tax credit: Partly for

Taxable Supplies

ITC Availabl

e

Zero-rated

Supplies

Credit available

Non-taxable Supplies

ITC not availabl

e

Exempt Supplies

ITC not availabl

e

Nil-rated

Supplies

Credit not available

18

Net credit

eligible

Total credit for

a period

Only on

inputs and

input services

not on capital

goods

Exclusively

used for

Personal purposes

Exempted supply

Credit not

eligible

Specified input credit - Invoice level segregation

19

Common

Credit

Total credit

less specified

credits

Personal purposes- 5% of the credit

Exempted supply – Proportionate basis

Common Credit- apportionment

Taxable supply – Proportionate basis

Reversal of credit on the basis of turnover

To be reversed on the monthly basis using monthly turnovers

Re-computation on annual basis within the month of September next FY

20

Special provision for banking companies & financial institutions:

In the case of banking companies or financial institutions including NBFCs could opt for availment of 50% of the total credit eligible in the tax period.

Where the aforesaid banking companies, NBFCs etc opt for availing 50% of total credit eligible, they have to follow the procedure contained in Rule 3 of Input Tax Credit Rules.

21

SPECIAL CIRCUMSTANCES

INPUT TAX CREDIT

22

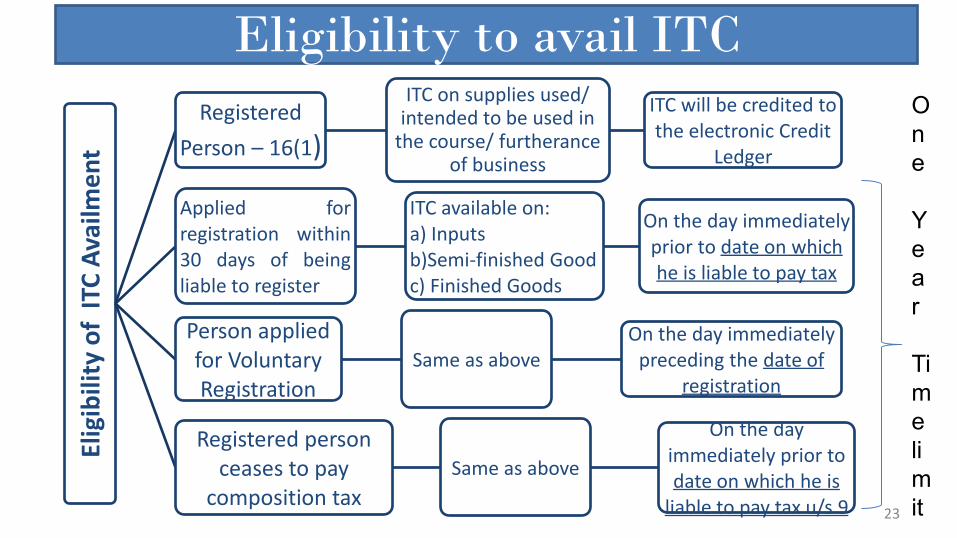

Eligibility to avail ITC

23

Eli

gib

ilit

y o

f I

TC

Av

ail

me

nt

Registered

Person – 16(1)

ITC on supplies used/ intended to be used in

the course/ furtherance of business

ITC will be credited to

the electronic Credit

Ledger

Applied for

registration within

30 days of being

liable to register

ITC available on:

a) Inputs

b)Semi-finished Good

c) Finished Goods

On the day immediately

prior to date on which

he is liable to pay tax

Person applied

for Voluntary

Registration

Same as above

On the day immediately

preceding the date of

registration

Registered person

ceases to pay

composition tax

Same as above

On the day

immediately prior to

date on which he is

liable to pay tax u/s 9

O

n

e

Y

e

a

r

Ti

m

e

li

m

it

Eligibility to avail ITC-Cap goods

24

Eli

gib

ilit

y o

f I

TC

Av

ail

me

nt

Composition to

regular scheme

Capital goods as on the

day immediately prior

to date of such

conversion

Cost less reduction of

5% per Quarter from

the date of invoice

Exemption to

taxable Same as above Same as above

Transfer of credit due to change in constitution

25

Change in

Constitution of

Registered

Person

On account of:

Sale,

Merger,

Demerger,

Amalgamation,

Lease, or

Transfer of

business

Transferee is allowed

to take credit of

unutilized ITC

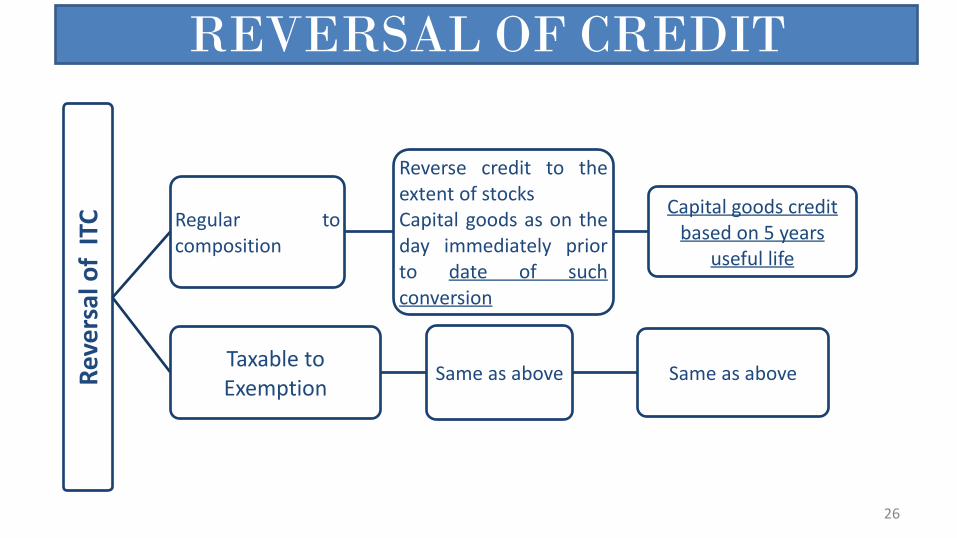

REVERSAL OF CREDIT

26

Re

ve

rsa

l o

f I

TC

Regular to

composition

Reverse credit to the

extent of stocks

Capital goods as on the

day immediately prior

to date of such

conversion

Capital goods credit

based on 5 years

useful life

Taxable to

Exemption Same as above Same as above

Removal of Cap. Goods

27

Removal of

Capital goods on

which credit is

availed

Pay higher of below:

A) Cost of Cap.

Goods less

depreciation

based on useful

life (assumed as

5 years)

B) Transaction value

Exception for

refractory bricks,

moulds an dies, jigs

and fixtures which

are supplied as

scrap, then tax has

to be paid on

tra sa tio alue only.

Input tax credit on inputs/CG sent for job work

28

Principal Job Worker

Inputs/ Capital Goods sent for job work

Received back or directly supplied from job-

orker s pre ises ithi 1 ear i puts or 3 years (capital goods) of being sent out

If not received/directly supplied in time: It is deemed that Principal has supplied

the input/capital goods on the day when input / capital goods were sent out.

He can reclaim this ITC on receiving back such inputs/ capital goods.

Where goods are directly sent to job worker, the period of one year shall

be counted from the date of receipt of inputs by the job worker.

29

INPUT SERVICE DISTRIBUTOR

(61) "Input Service Distributor" means an office of the supplier of

goods and / or services which receives tax invoices issued under

section 31 towards receipt of input services and issues a prescribed

document for the purposes of distributing the credit of CGST (SGST in

State Acts) and / or IGST paid on the said services to a supplier of

taxable goods and / or services having same PAN as that of the office

referred to above;

Input service distributor (Sec 20)

ISD shall distribute the credit subject to following conditions:

(a) the credit can be distributed to the recipients of credits against a

prescribed document;

(b) the amount of the credit distributed shall not exceed the amount of

credit available for distribution;

(c) the credit of tax paid on input services attributable to a recipient

shall be distributed only to that recipient;

30

31

Input service distributor (Sec 20)

(d) the credit of tax paid on input services attributable to more than

one recipient – e distri uted o l attri uta le re ipie ts o pro-

rata o the asis of the tur o er i a State or UT of su h re ipie t, during the relevant period, to the aggregate of the turnover of all

such recipients to whom such input service is attributable and which

are operational in the current year, during the said relevant period.

(e) where credit is attributable to all recipients, it shall be distributed

amongst such recipients on pro rata basis of turnover in a State or UT

of all recipients during the relevant period.

Explanation to Section 20-definitions

(a the rele a t period shall e––

1) if the recipients of credit have turnover in their States or Union

territories in the financial year preceding the year during which

credit is to be distributed, the said financial year; or

2) if some or all recipients of the credit do not have any turnover in

their States or Union territories in the financial year preceding the

year during which the credit is to be distributed, the last quarter for

which details of such turnover of all the recipients are available,

previous to the month during which credit is to be distributed;

(b the e pressio re ipie t of redit ea s the supplier of goods or services or both having the same Permanent Account Number as that of the

Input Service Distributor; 32

Recovery of ISD credit Sec 21

When ISD credit is distributed in excess of what is

available, it can be recovered with interest in manner

specified in section 73 or 74

33

Steps in availment and utilisation of credit

Avail credit provisionally after receipt of goods and invoice – S.41

Supplier to file returns along with supply details and pay taxes – S.37

Recipient to file return along with inward details and pay taxes – S.38

The credits are correlated with respective supplier returns – S. 42

Credits which match to the vendor details are treated as finalised

Credits not matched or excess on account of duplication etc. would be

treated as tax payable and intimated to the recipient. Vendors also would

be intimated about mismatch

The said amount of credits not matched would be paid along with interest in

the next month

Where the vendor rectifies and uploads, to such an extent credit would be

allowed and balance shall be payable with interest 34

Time and Tide wait for None

Date of/ Last date for

issue of Invoice Ref: Sec 31 (1)

Time of Supply of

Goods (Sec 12)

Date of payment received by

Supplier

Excess Amt Recd ≤ Rs 1000, when compared with Invoice value, supplier may opt to TOSG to be Date of Invoice

for such amount

E

A

R

L

I

E

S

T

Time and Tide wait for None

Tax too!

Explanation 1.––For the purposes of clauses (a) and (b), “supply” shall be deemed to have been made to the extent it is covered by the invoice or, as the case may be, the payment.

Explanation 2.––For the purposes of clause (b), “the date on which the supplier receives the payment” shall be the date on which the payment is entered in his books of account or the date on which the payment is credited to his bank account, whichever is earlier.

Few Explanations

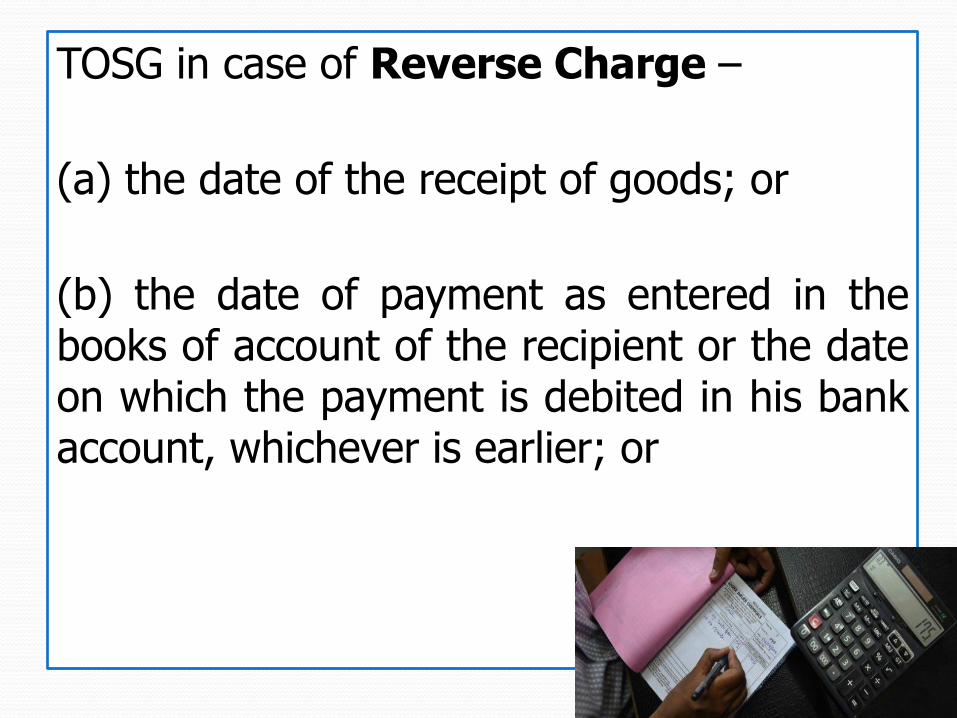

TOSG in case of Reverse Charge –

(a) the date of the receipt of goods; or

(b) the date of payment as entered in the books of account of the recipient or the date on which the payment is debited in his bank account, whichever is earlier; or

TOSG in case of Reverse Charge (Contd) –

(c) the date immediately following thirty days from the date of issue of invoice (??) or any other document, by whatever name called, in lieu thereof by the supplier:

TOSG in case of Reverse Charge (Contd) –

Provided that where it is not possible to determine the time of supply under clause (a) or clause (b) or clause (c), the time of supply shall be the date of entry in the books of account of the recipient of supply

Supply of Vouchers -

a) the date of issue of voucher, if the supply is identifiable at that point; or

(b) the date of redemption of voucher, in all other cases

TOSG when above mentioned could not be determined -

(a) in a case where a periodical return has to be filed, be the date on which such return is to be filed; or

(b) in any other case, be the date on which the tax is paid

TOSG in respect of Interest / Late Fee / Penalty for late payment of consideration -

The date on which the supplier receives such addition in value.

Date of Invoice - If issued as per Sec

31 (2)

Time of Supply of Services (Sec 13)

Date of Provision of Service if invoice

not issued as per Sec 31 (2)

Excess Amt Recd ≤ Rs 1000, when compared with Invoice value, supplier may opt to TOSS to be Date of Invoice for such excess amount

If both do not apply, Date of Receipt of service as recorded by recipient

E

A

R

L

I

E

S

T

(i) the supply shall be deemed to have been made to the extent it is covered by the invoice or, as the case may be, the payment;

(ii) “the date of receipt of payment” shall be the date on which the payment is entered in the books of account of the supplier or the date on which the payment is credited to his bank account, whichever is earlier.

Few Explanations

TOSS in case of Reverse Charge –

(a) the date of payment as entered in the books of account of the recipient or the date on which the payment is debited in his bank account, whichever is earlier; or

(b) the date immediately following sixty days from the date of issue of invoice or any other document, by whatever name called, in lieu thereof by the supplier

TOSS in case of Reverse Charge –

Provided that where it is not possible to determine the time of supply under clause (a) or clause (b), the time of supply shall be the date of entry in the books of account of the recipient of supply:

TOSS in case of Reverse Charge –

Provided further that in case of supply by associated enterprises, where the supplier of service is located outside India, the time of supply shall be the date of entry in the books of account of the recipient of supply or the date of payment, whichever is earlier.

Supply of Vouchers -

(a) the date of issue of voucher, if the supply is identifiable at that point; or

(b) the date of redemption of voucher, in all other cases

TOSS when above mentioned could not be determined -

(a) in a case where a periodical return has to be filed, be the date on which such return is to be filed; or

(b) in any other case, be the date on which the tax is paid

TOSS in respect of Interest / Late Fee / Penalty for late payment of consideration -

The date on which the supplier receives such addition in value.

Change in the rate of Goods / Services / Both –

(a) in case the goods or services or both have been supplied before the change in rate of tax,––

(i) where the invoice for the same has been issued and the payment is also received after the change in rate of tax, the time of supply shall be the date of receipt of payment or the date of issue of invoice, whichever is earlier; or

(ii) where the invoice has been issued prior to the change in rate of tax but payment is received after the change in rate of tax, the time of supply shall be the date of issue of invoice; or

(iii) where the payment has been received before the change in rate of tax, but the invoice for the same is issued after the change in rate of tax, the time of supply shall be the date of receipt of payment

Shall we quickly try to tabulate and simplify thereby –

For example

Old rate of GST – till 30.06.2018

New rate of GST – From 01.07.2018

Situations

Supplied on Invoice Raised

Payment Received by Supplier

Point of

Taxation (TOS)

A 28-06-2018 03-07-2018 10-07-2018 03-07-2018

B 28-06-2018 30-06-2018 10-07-2018 30-06-2018

C 28-06-2018 03-07-2018 30-06-2018 30-06-2018

D 03-07-2018 28-06-2018 05-07-2018 05-07-2018

E 03-07-2018 28-06-2018 30-06-2018 28-06-2018

F 03-07-2018 04-07-2018 28-06-2018 04-07-2018

When to refer bank account?

Provided that the date of receipt of payment shall be the date of credit in the bank account if such credit in the bank account is after four working days from the date of change in the rate of tax

What is the date of payment

The date on which the payment is entered in the books of account of the supplier or the date on which the payment is credited to his bank account, whichever is earlier.

QUESTIONS?

1

Levy & Composition,

Exemption from Tax

CA Ganesh Prabhu Balakumar B.Com, MFM, F.C.A, LL.B, DISA (ICAI)

2

Goods & Services Tax

Single Tax Payable on Taxable

Supply

Single Tax on the Supply of Goods

and Services

Multi Stage & Destination based Consumption Tax

GST

All About GST

3

GST is charged only

on the component of Value Addition

No (Reduce)

Cascading Effect

i.e tax on tax

All About GST

4

Dual GST

CGST & SGST or UTGST

IGST

GST Model - India

5

Section 7 - Supply

Sch 1 Activities w/o Consd.

Sch3 Activities - NOT

Activities by Govt or LA as Public Authorities

Notified by Govt + Co GST recom.

Sale, transfer, barter, exchange, license, rental, lease, disposal w/o consd

Import services w/ or w/o

Consd.

Scope of

Supply

Sch 2 Activities

By a person

For a consideration

In the course or furtherance of

Business

Sale/ Transfer/ Barter/ Exchange/License/

Rental/ Leases/ Disposal

Phrase To another person not incorporated

All form of Supply

Made or agreed to be made

Supply

Taxable Event

7

Sch – I Supply without Consideration

• Permanent Transfer of BA - ITC

• Supply Between Related or Distinct Person – FoB

• Gift by Employer to Employee – Rs.50,000/-

• Supply by Principal to Agent or

• Receipt of Goods by Agent on behalf of Principal

• Import of Service – Related Person - FoB

8

Sch II Supply of Goods or Services

• Transfer of title in Goods - SoG

• Right or UDS in Goods W/O Title Transfer – SoS

• Transfer of title in Goods - Future Date – HP/EMI -

SoG

• Right in Immovable Property W/O Title Transfer - SoS

• Treatment or Process – Another Person Goods - SoS

• Transfer of BA – No Longer Forms Part - SoG

9

Sch II Supply of Goods or Services

• If a BA – Private Use or Any Purpose other than

purpose of Business – SoS

• If a BA held by a taxable person who ceases to be a

taxable person –SoG

• Renting of IMP – SoS (DS)

• Construction of Complex – SoS - Except Entire Consd

• Temporary Transfer IPR – SoS

10

Sch II Supply of Goods or Services

• Information Technology Software – SoS

• Refrain from Act or Tolerate an Act – SoS

• Transfer of Right to use any Goods – SoS

• Composite Supply – WCS & Supply of Food

• Supply of Food by Club or Association - SoG

11

Sch III – Neither SoG or SoS

• Service - Employee to Employer – In Relation or Course

• Any Court or Tribunal, Functions – MP, MLA, etc.

• Post Recognized by CoI or CP, M, D of Board or

Commission of CG or SG or LA

• Funeral, Burial, Cremation, or Mortuary

• Sale of Land (except Construction of Complex)

• Actionable Claims (except Lottery, Betting, Gambling)

12

Sec 8 – TL on Mixed & Composite

Basis Mixed Supply

Composite Supply

Meaning Two or more supplies together, which is NOT a Composite Supply

Two or More supplies with 1 Principal Supply & Naturally Bundled

Treatment As supply of that supply w/ higher tax rate

As supply of that principal supply

13

Sec 9 (1) Levy of CGST & SGST

• Tax Levy of CGST (SGST Levy – Respective SGST

Act)

• All Intra-State Supply of G or S or B – Except Liquor

• Value determined as per Sec 15 of CGST Act

• Rate Notified by CG, SG

• Not Exceeding 20%

• Collected in Manner Prescribed (Sec 12 & 13)

14

Sec 9 (3) Levy of CGST & SGST - RCM

CG & SG – Recommendation GST Council

Specify Goods or Services or Both

Tax on which Payable under Reverse Charge

Tax shall be paid by Recipient

All provisions apply as if he is Supplier of such Goods or Services.

15

Sec 9 (4) Levy of CGST & SGST –URS

• Supply of taxable Goods or Services or Both

• By a Supplier, who is not registered under GST

• Tax on which Payable under Reverse Charge

• Tax shall be paid by such person as Recipient

• All provisions apply as if he is Supplier of such Goods or Services.

16

Sec 9 (5) Levy of CGST & SGST – ECom

• CG & SG on Recommendations of GST Council

• Specify category of Services (Goods – NA)

• Tax on which shall be paid by E-Commerce Operator

• If such services are supplied through them

• All provisions apply as if he is Supplier of such Goods or Services.

17

Sec 5 (1) of IGST - Levy of IGST

• Levy of IGST

• All Inter-State Supply

• Value determined as per Sec 15 of CGST

• Rate Notified by CG, SG - Not Exceeding 40%

• Collected in Manner Prescribed (Sec 12 & 13)

• IGST will be levied on Imported Goods

18

Sec 5(3) of IGST - Levy of IGST - RCM

• CG & SG on Recommendations of GST Council

• Specify Goods & Services

• Tax on which Payable under Reverse Charge

• Tax shall be paid by Recipient

• All provisions apply as if he is Supplier of such Goods or Services.

19

Sec 5(4) of IGST - Levy of IGST – URS

• Supply of taxable Goods & Services

• By a Supplier, who is not registered under GST

• Tax on which Payable under Reverse Charge

• Tax shall be paid by Recipient

• All provisions apply as if he is Supplier of such Goods or Services.

20

Sec 5(5) of IGST - Levy of IGST – E-Com

• CG & SG on Recommendations of GST Council

• Specify category of Services

• Tax on which shall be paid by E-Commerce Operator

• If such services are supplied through them

• All provisions apply as if he is Supplier of such Goods or Services.

21

Sec 10 Composition Levy - Eligibility

PY Aggregate Turnover ≤ Rs.50

Lakh

Engage in Supply of Services of Supply

of Foods

(Sch2 Para6 Clause (b))

Engage in making Supply of goods

which are liveable to tax under this

Act;

NOT Engaged

Inter-State Outward supplies of Goods;

NOT Engaged

Supply of goods through E Com

(Sec 52 of CGST Act)

22

Sec 10 Composition Levy - Eligibility

NOT Manufacturer of goods Notified*

If same PAN for more than 1 RP, eligible only if

both or all opt for Composition Levy

NOT collect any tax from Recipient & NOT entitled

to ITC

If RP opted without being eligible and PO has

reasons – Tax+ Penalty u/s 73 & 74

23

Sec 10 Composition Levy – Rate of Tax

Manufacturer 1% of State or UT

Turnover

Supply of Food

2 ½% of State/UT Turnover

Other Suppliers ½% of State/UT

Turnover

24

Conditions & Restrictions – Rules

Neither a CTP or a NRTP. Goods held in Stock as on AD are not

Inter State or Branch Transfer Imported Purchase Unregistered Person. (He shall pay tax under (3) & (4) of Sec 9

of CGST Act)

He should mention the word CTP - on every Bill, Notices & on Signboard He need not file a fresh intimation every year.

25

Validity of Composition Levy

Option to pay tax u/s 10 is valid only till all

conditions are fulfilled.

Conditions – Not satisfied then withdrawal is made

in FORM GST CMP 04 within 7 days of violation.

And liable to pay tax U/s 9 of CGST Act

26

Sec 11 of CGST Power to Exempt

Govt on GST Council recommendation in public interest may exempt:-

By notification, exempt partly or

wholly

By special order under exceptional nature

By Inserting explanation within one year of issue

with retrospective effect

27

Doubts / Questions ?

28

CA Ganesh Prabhu Balakumar Partner C.Ramasamy & B.Srinivasan Chartered Accountants, Chennai. Mobile: +91 98404 71139 E- Mail : [email protected] [email protected]