Embed Size (px)

Citation preview

NN.. CCHHRRYYSSSSOOCCHHOOIIDDIISS SSTTOOCCKK BBRROOKKEERRAAGGEE IINNVVEESSTTMMEENNTT SSEERRVVIICCEESS SS..AA..

Equity Research Department

EQU

ITY

RES

EAR

CH

(FU

ND

AM

ENTA

LS)

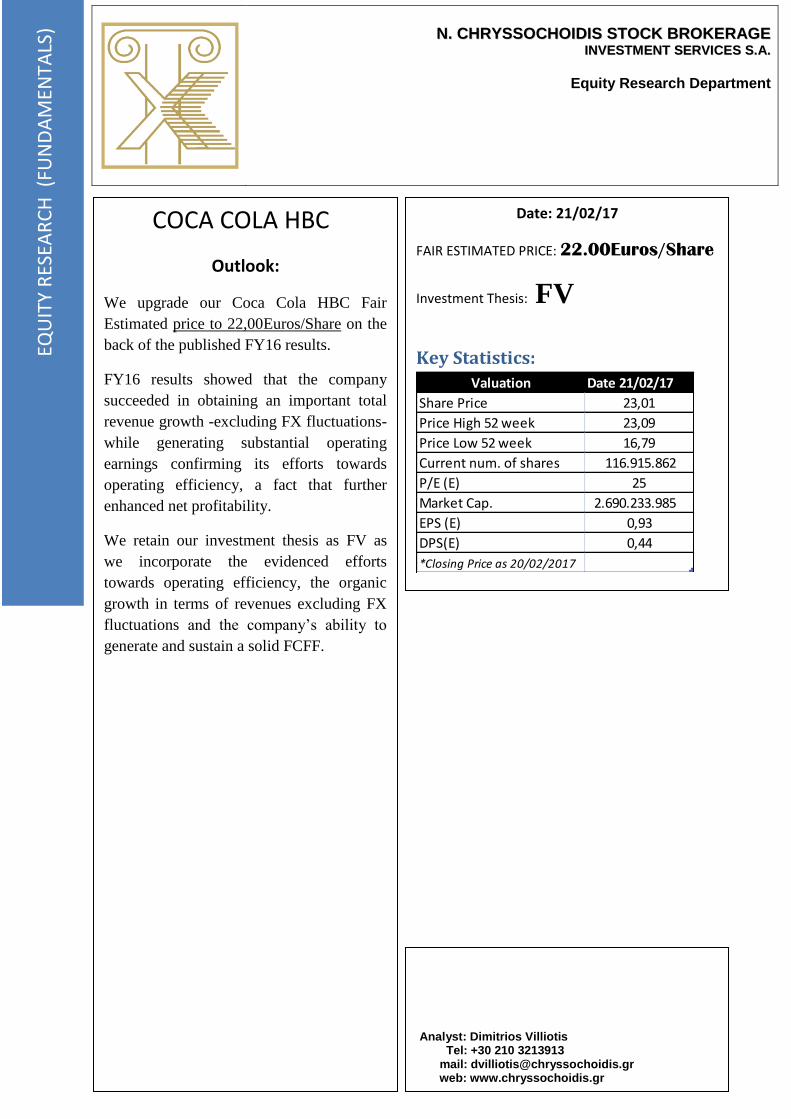

COCA COLA HBC

Outlook:

We upgrade our Coca Cola HBC Fair

Estimated price to 22,00Euros/Share on the

back of the published FY16 results.

FY16 results showed that the company

succeeded in obtaining an important total

revenue growth -excluding FX fluctuations-

while generating substantial operating

earnings confirming its efforts towards

operating efficiency, a fact that further

enhanced net profitability.

We retain our investment thesis as FV as

we incorporate the evidenced efforts

towards operating efficiency, the organic

growth in terms of revenues excluding FX

fluctuations and the company’s ability to

generate and sustain a solid FCFF.

Date: 21/02/17

FAIR ESTIMATED PRICE: 22.00Euros/Share

Investment Thesis: FV

Key Statistics:

Valuation Date 21/02/17

Share Price 23,01

Price High 52 week 23,09

Price Low 52 week 16,79

Current num. of shares 116.915.862

P/E (E) 25

Market Cap. 2.690.233.985

EPS (E) 0,93

DPS(E) 0,44

*Closing Price as 20/02/2017

Analyst: Dimitrios Villiotis Tel: +30 210 3213913 mail: [email protected] web: www.chryssochoidis.gr

COCA COLA HBC-GROWTH AND OPERATING EFFICIENCY

Coca Cola HBC’s FY16 results were characterized by the growth in total revenues

excluding FX impact, the sharp reduction of operating expenses reaching an eight year

low level and the FX volatility that affects the overall results.

Specifically, the unit cases volumes for the Emerging and Developing markets sector

increased with a more favorable package mix as evidenced by the increase in revenue

per case (excluding FX) but the substantial volatility of currency led to lower revenue

per case and decreased y-o-y revenues. In the Established market sector the unit cases

sold were 2.43% lower than the previous year reflecting the weaker sales in Water and

Sparkling Beverages. Despite that, the sector’s revenues per case were impacted from

the volatility of GBP during the period. In terms of operating performance the company

reaps the profits of the efforts towards operating efficiency as the company had the

lower operating expenses since FY08, a fact that enhances the FCFF and the

fundamental value of the company in combination with the Net profitability.

In our valuation model we apply a more normalized projected revenue growth (1% from

2% previously) as we take into consideration both the substantial impact of the

currencies and the macro environment of the regions that contribute to the overall

revenues and facing several challenges (Russia, Nigeria) and the evidenced softer

revenues in the Established markets region. We also incorporate the more efficient

operating performance which is the single most important factor for the generation of a

c.450mn. FCFF per annum especially in the case of a weaker overall revenues

environment.

In closing remarks we consider Coca Cola HBC’s as the most valuable pick among the

Hellenic Equities universe, we are satisfied from the share’s operating performance and

we consider it as an attractive investment case among its European peers as it is traded

10.35x in EV/EBITDA terms below the European average of 12.15x and 1.18x in

Price/Sales ratio vs the European Price/Sales average ratio of 2.63x.

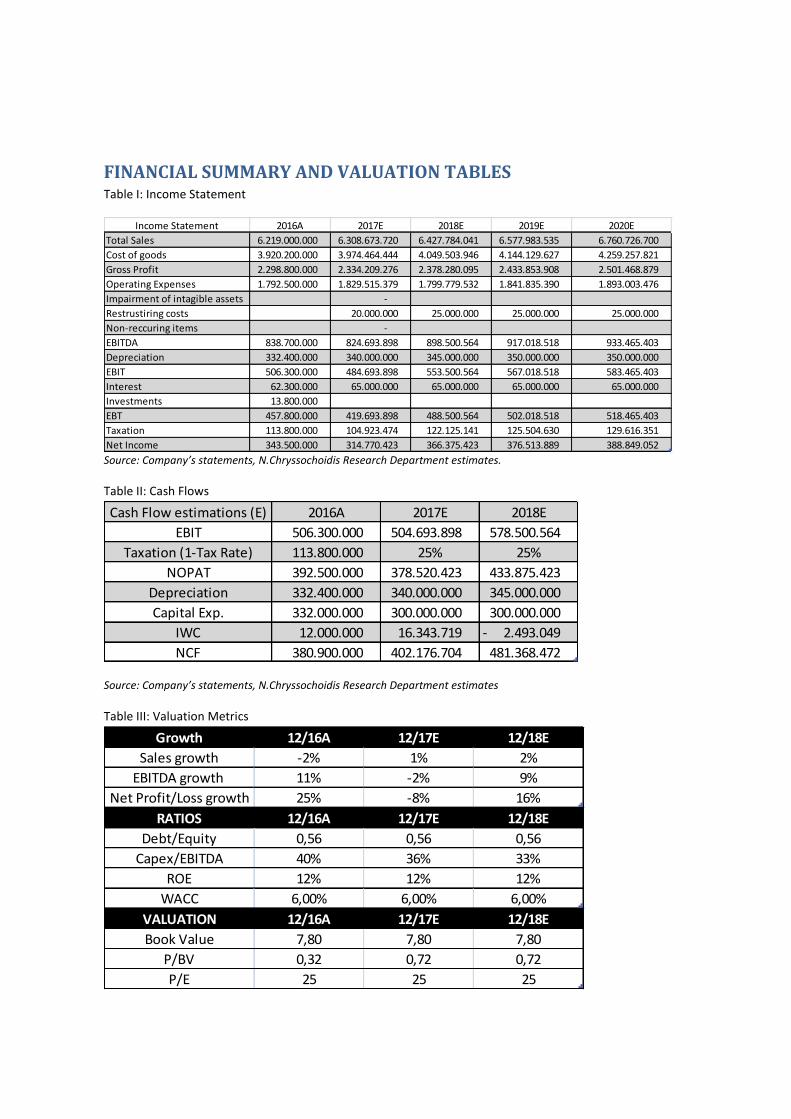

FINANCIAL SUMMARY AND VALUATION TABLES Table I: Income Statement

Income Statement 2016A 2017E 2018E 2019E 2020E

Total Sales 6.219.000.000 6.308.673.720 6.427.784.041 6.577.983.535 6.760.726.700

Cost of goods 3.920.200.000 3.974.464.444 4.049.503.946 4.144.129.627 4.259.257.821

Gross Profit 2.298.800.000 2.334.209.276 2.378.280.095 2.433.853.908 2.501.468.879

Operating Expenses 1.792.500.000 1.829.515.379 1.799.779.532 1.841.835.390 1.893.003.476

Impairment of intagible assets -

Restrustiring costs 20.000.000 25.000.000 25.000.000 25.000.000

Non-reccuring items -

EBITDA 838.700.000 824.693.898 898.500.564 917.018.518 933.465.403

Depreciation 332.400.000 340.000.000 345.000.000 350.000.000 350.000.000

EBIT 506.300.000 484.693.898 553.500.564 567.018.518 583.465.403

Interest 62.300.000 65.000.000 65.000.000 65.000.000 65.000.000

Investments 13.800.000

EBT 457.800.000 419.693.898 488.500.564 502.018.518 518.465.403

Taxation 113.800.000 104.923.474 122.125.141 125.504.630 129.616.351

Net Income 343.500.000 314.770.423 366.375.423 376.513.889 388.849.052

Source: Company’s statements, N.Chryssochoidis Research Department estimates.

Table II: Cash Flows

Cash Flow estimations (Ε) 2016A 2017E 2018E

EBIT 506.300.000 504.693.898 578.500.564

Taxation (1-Tax Rate) 113.800.000 25% 25%

NOPAT 392.500.000 378.520.423 433.875.423

Depreciation 332.400.000 340.000.000 345.000.000

Capital Exp. 332.000.000 300.000.000 300.000.000

IWC 12.000.000 16.343.719 2.493.049 -

NCF 380.900.000 402.176.704 481.368.472

Source: Company’s statements, N.Chryssochoidis Research Department estimates

Table III: Valuation Metrics

Growth 12/16A 12/17E 12/18E

Sales growth -2% 1% 2%

EBITDA growth 11% -2% 9%

Net Profit/Loss growth 25% -8% 16%

RATIOS 12/16A 12/17E 12/18Ε

Debt/Equity 0,56 0,56 0,56

Capex/EBITDA 40% 36% 33%

ROE 12% 12% 12%

WACC 6,00% 6,00% 6,00%

VALUATION 12/16A 12/17E 12/18Ε

Book Value 7,80 7,80 7,80

P/BV 0,32 0,72 0,72

P/E 25 25 25

Ρήηπα Πεπιοπιζμού Εςθύνηρ: Απαγνξεύεηαη ε αλαδεκνζίεπζε ηνπ παξόληνο ρσξίο ηελ άδεηα ηεο Ν. ΥΡΤΟΥΟΪΔΗ ΥΡΗΜΑΣΙΣΗΡΙΑΚΗ Α.Ε.Π.Ε.Τ. Οη απόςεηο πνπ πεξηέρνληαη βαζίδνληαη ζε πεγέο πνπ ζεσξνύληαη αμηόπηζηεο, σζηόζν ε Ν. ΥΡΤΟΥΟΪΔΗ ΥΡΗΜΑΣΙΣΗΡΙΑΚΗ Α.Ε.Π.Ε.Τ. δελ επζύλεηαη γηα ηελ εγθπξόηεηα, νξζόηεηα ή αμηνπηζηία ηνπο θαη δηαηεξεί ην δηθαίσκα αιιαγήο ηνπο ρσξίο πξόηεξε εηδνπνίεζε. Σόζν ε Ν. ΥΡΤΟΥΟΪΔΗ ΥΡΗΜΑΣΙΣΗΡΙΑΚΗ Α.Ε.Π.Ε.Τ. όζν θαη νη δηεπζύλνληεο θαη ππάιιεινη ηεο δελ θέξνπλ νπδεκία επζύλε γηα νπνηαδήπνηε ζπλέπεηα ησλ πιεξνθνξηώλ απηώλ. Το παπόν δεν αποηελεί πποζθοπά, πποηποπή ή επενδςηική ππόηαζη για αγοπά ή πώληζη μεηοσών ή άλλων κινηηών αξιών. Οι επενδύζειρ πος αναθέπονηαι ενδέσεηαι να µην είναι οι ενδεδειγμένερ για οπιζμένοςρ επενδςηέρ.

Disclaimer: This report has been issued by N. CHRYSSOCHOIDIS STOCK BROKERAGE I.S.S.A., a member of the Athens Stock Exchange, and may not be reproduced in any manner or provided to any other persons. Each person that receives a copy by

acceptance thereof represents and agrees that it will not distribute or provide it to any other person. The information contained herein has been obtained from sources believed to be reliable but has not been verified by N. CHRYSSOCHOIDIS

STOCK BROKERAGE I.S.S.A. The opinions expressed herein may not necessarily coincide with those of any member of N. CHRYSSOCHOIDIS STOCK BROKERAGE I.S.S.A. No representation or warranty (express or implied) is made as to

the accuracy, completeness, correctness, timeliness or fairness of the information or opinions herein, all of which are subject to change without notice. No responsibility of liability whatsoever or howsoever arising is accepted in relation to the

contents hereof by N. CHRYSSOCHOIDIS STOCK BROKERAGE I.S.S.A. or any of its directors, officers or employees. This report is not an offer to buy or sell or a solicitation of an offer to buy or sell securities mentioned herein. N.

CHRYSSOCHOIDIS STOCK BROKERAGE I.S.S.A. may effect transactions in or perform or seek to perform brokerage services for companies covered. The investments discussed in this report may be unsuitable for investors, depending on their

specific investment objectives and financial position.

Σημειώζεις/Notes Οδηγός Συζηάζεων/Ratings P: Τρέτοσζα Τιμή Market Price

MCAP: Κεθαλαιοποίηζη Capitalization UV Φαμηλή Αποηίμηζη/ Φαμηλός Κίνδσνος Underpriced/ Small Risk

EPS: Καθαρά Κέρδη Ανά Μεηοτή Earnings per Share

UV1

Φαμηλή Αποηίμηζη/ Κίνδσνος

Stock Price < 20% of Fair

Underpriced/ Risk

Stock Price < 10% of Fair

P/E: Λόγος Τιμής προς Κέρδη Price/Earnings Ratio FV Σωζηή Αποηίμηζη/ Φαμηλός Κίνδσνος Fairly Priced/ Small Risk

10%<Stock Price<10%

P/S: Λόγος Τιμής προς Πωλήζεις Price/Sales Ratio OV1 Σωζηή Αποηίμηζη/ Κίνδσνος Fairly Priced/ Risk

Stock Price >10% of Fair

D/A: Σσνολικός Δανειζμός προς Παθηηικό Total Debt/Assets

Ratio OV Υπερηιμημένη Μεηοτή Overvalued

Stock Price >20% of Fair

DY: Απόδοζη Μερίζμαηος Dividend Yield N/R Μη Αποηιμημένη Μεηοτή Not Rated

ROE: Απόδοζη Ιδίων Κεθαλαίων Return on Equity

FV: Τιμή Σωζηής Αποηίμηζης Fair Value Price