Embed Size (px)

Citation preview

Building a scorecard can help managers link today'sactions with tomorrow's goals.

Using the BalancedScorecard as a Strategic

Management System

by Rohert S. Kaplan and David P. Norton

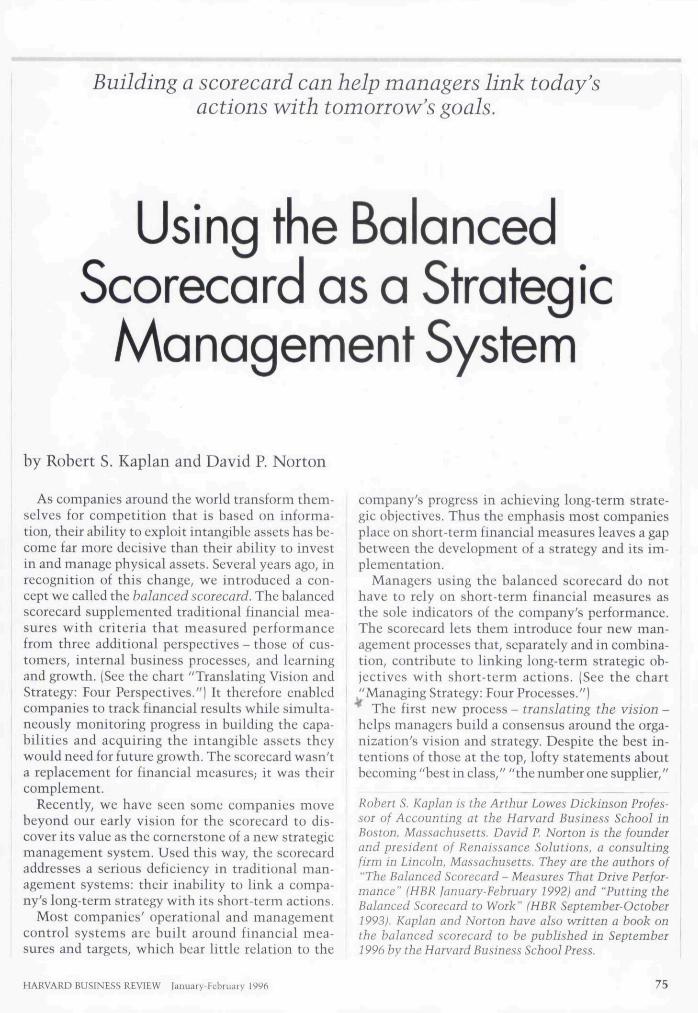

As companies around the world transform them-selves for competition that is based on informa-tion, their ability to exploit intangible assets has be-come far more decisive than their ability to investin and manage pbysical assets. Several years ago, inrecognition of this change, we introduced a con-cept we called the balanced scorecard. The balancedscorecard supplemented traditional financial mea-sures witb criteria tbat measured performancefrom three additional perspectives - those of cus-tomers, internal business processes, and learningand growth. (See the cbart "Translating Vision andStrategy: Four Perspectives.") It therefore enabledcompanies to track financial results wbile simulta-neously monitoring progress in building the capa-bilities and acquiring the intangible assets tbcywould need for future growth. Tbe scorecard wasn'ta replacement for financial measures; it was tbeircomplement.

Recently, we bave seen some companies movebeyond our early vision for the scorecard to dis-cover its value as the cornerstone of a new strategicmanagement system. Used tbis way, the seorecardaddresses a serious deficiency in traditional man-agement systems: tbeir inability to link a compa-ny's long-term strategy with its short term actions.

Most companies' operational and managementcontrol systems are built around financial mea-sures and targets, wbicb bear little relation to the

company's progress in achieving long-term strate-gic objectives. Tbus tbe emphasis most companiesplace on short-term financial measures leaves a gapbetween the development of a strategy and its im-plementation.

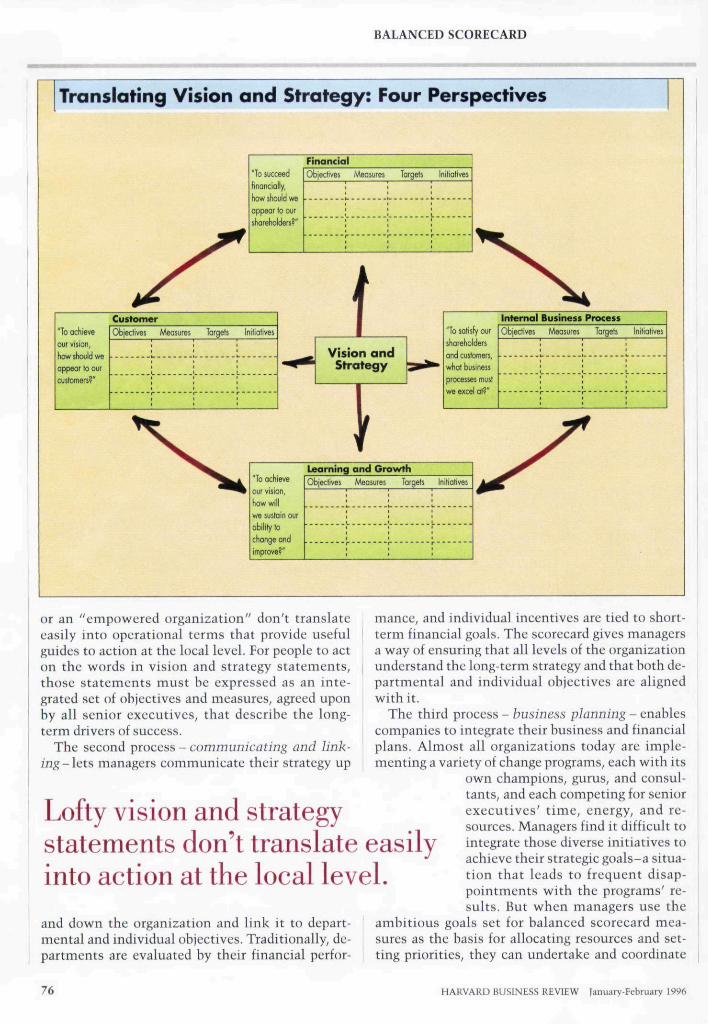

Managers using tbe balaneed scorecard do notbave to rely on sbort-term financial measures astbe sole indicators of tbe company's performance.Tbe seoreeard lets them introduce four new man-agement processes that, separately and in combina-tion, contribute to linking long-term strategie ob-jectives with sbort-term actions. (See tbe chart''Managing Strategy: Four Processes.")

The first new process - translating the vision -helps managers build a consensus around the orga-nization's vision and strategy. Despite the best in-tentions of tbose at tbe top, lofty statements aboutbecoming "best in class/' "the number one supplier,"

Robert S. Kaplan is the Arthur Lowes Dickinson Profes-sor of Accounting at the Harvard Business School inBoston. Massachusetts. David P. Norton is the founderand president of Renaissance Solutions, a consultingfirm in Lincoln. Massachusetts. They are the authors of"The Balanced Scorecard - Measures That Drive Perfor-mance" (HBR January-February 1992} and "Putting theBalanced Scorecard to Work" (HBR September-October1993). Kaplan and Norton have also written a book onthe balanced scorecard to be published in September1996 by the Harvard Business School Press.

HARVARD BUSINESS REVIEW Uiniiiary-Fcbruary 19% 75

BALANCED SCORECARD

Translating Vision and Strategy: Four Perspectives

'To succeed

financially,

Kow should we

appear ro out

shorekildefs?'

FinancialObjectives Measures Targets Initiatives

1 1 '•

"Ta achieve

our viiion,

how should we

appeal to our

customers?"

CustomerObjectives Measures Targets Initiatives t

Vision atidStrategy

"To satisfy our

shareholders

and customers,

what business

processes must

we excel at?"

Intemal Business ProcessObjectives Measures Targets Initiotives

To achieve

our vision.

wesustoinour

ability lo

change and

improve?"

Learning and Orovrth,t,.-:^?^i-;:^ .Objectives Meosures Torgets Initiatives

or an "empowered organization" don't translateeasily into operational terms that provide usefulguides to aetion at the local level. For people to acton the words in vision and strategy statements,those statements must be expressed as an inte-grated set of objectives and measures, agreed uponby all senior executives, that describe the long-term drivers of success.

The second process - communicating and link-managers communicate their strategy up

mance, and individual incentives are tied to sbort-term financial goals. The scorecard gives managersa way of ensuring tbat all levels of tbe organizationunderstand tbe long term strategy and tbat botb de-partmental and individual objectives are alignedwitb it.

Tbe tbird process - business planning - enablescompanies to integrate their business and financialplans. Almost all organizations today are imple-menting a variety of cbange programs, eacb witb its

own cbampions, gurus, and consul-tants, and eacb competing for seniorexecutives' time, energy, and re-

,^ sources. Managers find it difficult to

d o n t t r a n s l a t e e a s i l y integrate tbose diverse initiatives to• acbieve tbeir strategic goals-a situa-

tion tbat leads to frequent disap-pointments witb tbe programs' re-sults. But wben managers use tbe

ambitious goals set for balanced scorecard mea-sures as tbe basis for allocating resources and set-ting priorities, tbey can undertake and coordinate

Lofty vision and strategy

into action at the local level.

and down tbe organization and link it to depart-mental and individual objectives. Traditionally, de-partments are evaluated by tbeir financial perfor-

m HARVARD BUSINESS REVIEW lanuary-february 1996

only tbose initiatives that move them toward theirlong-term strategic objectives.

The fourth proeess - feedhack and learning -gives companies the capacity for wbat we call stra-tegic learning. Existing feedback and review pro-cesses focus on wbetber the company, its depart-ments, or its individual employees have met tbeirbudgeted financial goals. With tbe balanced score-card at tbe center of its management systems, acompany can monitor sbort-term results from thethree additional perspectives - customers, internalbusiness processes, and learning and growth - andevaluate strategy in the light of recent perfor-mance. Tbe seoreeard thus enables eompanies tomodify strategies to reflect real-time learning.

None of tbe more than 100 organizations that wehave studied or with which we have worked imple-mented tbeir first balanced seoreeard witb the in-tention of developing a new strategic managementsystem. But in eacb one, the senior exeeutives dis-covered that tbe scorecard supplied a frameworkand thus a focus for many critical managementprocesses: departmental and individual goal set-ting, business planning, capital allocations, strate-gic initiatives, and feedback and learning. Previous-ly, those processes were uncoordinated and oftendirected at short-term operational goals. By build-ing the scorecard, the senior executives started aprocess of change tbat bas gonewell beyond tbe original idea ofsimply broadening tbe company'sperformance measures.

For example, one insurancecompany - let's call it NationalInsurance-developed its first bal-anced scorecard to create a newvision for itself as an underwrit-ing specialist. But once Nationalstarted to use it, tbe seoreeard al-lowed tbe CEO and tbe seniormanagement team not only to in-troduee a new strategy for the or-ganization but also to overhaulthe company's management sys-tem. Tbe CEO subsequently toldemployees in a letter addressed tothe wbole organization tbat Na-tional would thencefortb use thebalanced scorecard and the pbilos-opby tbat it represented to man-age the business.

National built its new strategicmanagement system step-by-stepover 30 montbs, witb each steprepresenting an incremental im-

provement. [See the chart "How One CompanyBuilt a Strategic Management System.") The itera-tive sequence of actions enabled tbe company toreconsider each of tbe four new management pro-cesses two or three times before the system sta-bilized and became an establisbed part of National'soverall management system. Tbus the CEO wasable to transform tbe company so that everyonecould focus on achieving long-term strategie objec-tives - something tbat no purely financial frame-work could do.

Translating the Vision

Tbe CEO of an engineering construction com-pany, after working witb his senior managementteam for several months to develop a mission state-ment, got a phone call from a project manager in thefield. "I want you to know," the distraught managersaid, "that I believe in the mission statement. Iwant to aet in accordance with tbe mission state-ment. I'm bere witb my customer. What am I sup-posed to do?"

Tbe mission statement, like tbose of many otberorganizations, had declared an intention to "usehigh-quality employees to provide services thatsurpass customers' needs." But tbe project managerin tbe field with his employees and his customer

Managing Strategy: Four Processes

Translatingfhe Vision

D Clarifying tiie visionD Gainif>g consensus

Communicatingand Linking

C CommunicaNngand educatingD Setting goalsQ linking rewards taperformonce measures

Feedbackand Learning

n Articulating theshared vision

n Supplying srrategicfeedbackD Facilitating stralagyreview and learning

BusinessPlanning

D Setting targetspAligning strategicinitiatives• Allocating resources• Establishingmilestones

HARVARD BUSINESS REVIEW January-February 1996 77

BALANCED SCORECARD

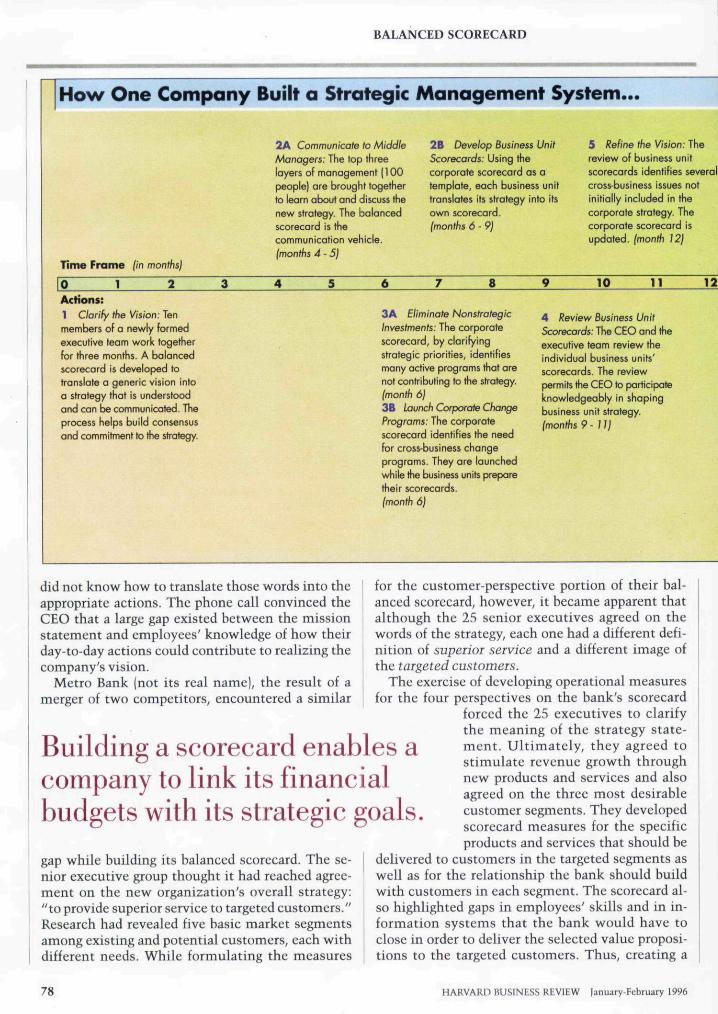

How One Company Built a Strategic Management System...

Time Frame (Irj months}

0 1 2 3Actions:1 Clarify the Vision: Tenmembers of a newly formedexecutive team work togetherfor tfiree months. A balancedscorecard is developed totranslate a generic vision intoa strategy tfiot is understoodand can be communicated. Theprocess helps build consensusand commitment to the strategy.

2A Communicate to Middle 2B Develop BusinessManagers: The top three Scorecards: Using thelayers of management (100 corporate scorecard aspeople) are brought together template, each busines

Unit 5 Refine the Vision: Tfiereview of business unit

a scorecards identifies severals unit cross-business issues not

to learn obout and discuss the translates its strategy into Its initially included in thenew strategy. The balanced own scorecard.scorecard is tfie (months 6 - 9)communication vehicle.(months 4 - 5]

4 5 6 7 8

3A Eliminate NonstrategicInvestments: The corporatescorecard, by clarifyingstrategic priorities, identifiesmany active programs that arenot contributing lo tfie strategy.(month 6)3B launch Corporate ChangePrograms: Tfie corporatescorecard identifies tfie needfor cross-business cfiangeprograms. Tfiey are launchedwhile tfie business units preparetheir scorecards.(month 6)

corporate strategy. Thecorporate scorecord isupdated, (month 12)

9 10 11 12

4 Review Business UnitScorecards: The CEO and theexecutive team review theindividual business units'scorecards. The reviewpermits the CEO to participateknowledgeably in shapingbusiness unit strategy.(months 9 - U j

did not know how to translate those words into theappropriate actions. The phone call convinced theCEO that a large gap existed between the missionstatement and employees' knowledge of how theirday-to-day actions could contrihute to realizing thecompany's vision.

Metro Bank (not its real name), the result of amerger of two competitors, encountered a similar

Building a scorecard enables acompany to link its financial

for the customer-perspective portion of their bal-anced scorecard, however, it became apparent thatalthough the 25 senior executives agreed on thewords of the strategy, each one had a different defi-nition of superior service and a different image ofthe targeted customers.

The exercise of developing operational measuresfor the four perspectives on the bank's scorecard

forced the 25 executives to clarifythe meaning of the strategy state-ment. Ultimately, they agreed tostimulate revenue growth throughnew products and services and also

, ^ , , 1 agreed on the three most desirable

with its strategic goals. customer segments They developed0 0 crnrprarn mpaQiirp*; rnr tfip sneririr

gap while huilding its balanced scorecard. The se-nior executive group thought it had reached agree-ment on the new organization's overall strategy;"to provide superior service to targeted customers."Research had revealed five basic market segmentsamong existing and potential customers, each withdifferent needs. While formulating the measures

scorecard measures for the specificproducts and services that should be

delivered to customers in the targeted segments aswell as for the relationship the bank should buildwith customers in each segment. The scorecard al-so highlighted gaps in employees' skills and in in-formation systems that the bank would have toclose in order to deliver the selected value proposi-tions to the targeted customers. Thus, creating a

78 HARVARD BUSINESS REVIEW Ianuary-February 1996

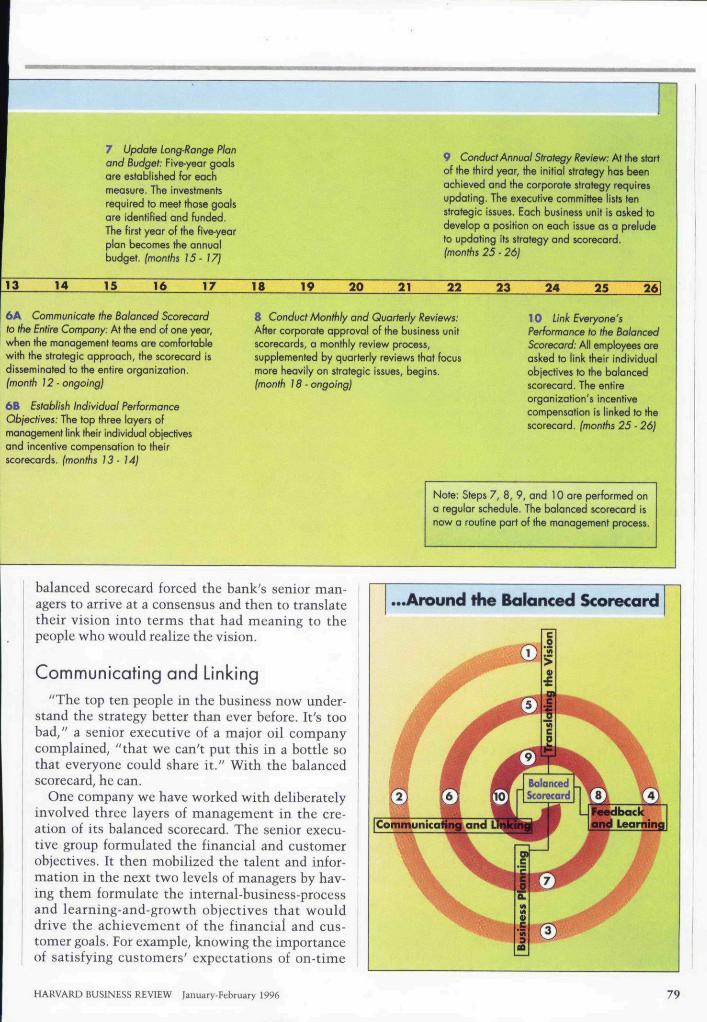

7 Update Long-Range Planand Budget: Five-year goalsare established for eachmeasure. The investmentsrequired to meet those goalsare identified and funded.The first year of tfie five-yearplan becomes the annualbudget, (months 15- 17)

9 Conduct Annual Strategy Review; At the startofthe third year, the initial strategy has beenachieved and the corporate strategy requiresupdating. The executive committee lists tenstrategic issues. Each business unit is asked tadevelop a position on each issue as a preludeto updating its strategy and scorecard.(months 25 - 26)

13 14 15 16 17 18 19 22 23 24 25 26

6A Communicate the Balanced Scorecardto tbe Entire Company: At the end of one year,when the management teems are comfortablev/ith the strategic approach, the scorecard isdisseminated to the entire organization.(month ) 2 - ongoing)

6B Establish Individual PerformanceObjectives: The top three layers ofmanagement link their individual objectivesand incentive compensation to theirscorecards. (months 13- 14)

8 Conduct Monthly and Quarterly Reviews:After corporate approval of the business unitscorecards, a monthly review process,supplemented by quarterly reviews that focusmore heavily on strategic issues, begins.(month 18 - ongoing)

10 Link Everyone'sPerformance to the BalancedScorecard: All employees areasked to link their individualobjectives lo the balancedscorecard. The entireorganization's incentivecompensation is linked to thescorecard. (months 25 - 26}

Note: Steps 7, 8, 9, and 10 are performed ona regular schedule. The balanced scorecard isnow a routine part of the management process.

balanced scorecard forced the bank's senior man-agers to arrive at a consensus and then to translatetheir vision into terms that had meaning to thepeople who w ould realize the vision.

Communicating and Linking"The top ten people in the business nov ' under-

stand the strategy better than ever before. It's toobad," a senior executive of a major oil companycomplained, "that we can't put this in a bottle sothat everyone could share it." With the balancedscorecard, he can.

One company we have worked with deliberatelyinvolved three layers of management in the cre-ation of its balanced scorecard. The senior execu-tive group formulated the financial and customerobjectives. It then mobilized tbe talent and infor-mation in the next two levels of managers by hav-ing them formulate the internal-business-processand learning-and-growth objectives tbat woulddrive the achievement of the financial and cus-tomer goals. For example, knowing the importanceof satisfying customers' expectations of on-time

...Around the Balanced Scorecard

[Communicating and L

HARVARD BUSINESS REVIEW January-February 1996 79

BALANCED SCORECARD

delivery, the broader group identified several inter-nal business processes - such as order processing,scheduling, and fulfillment-in which the companyhad to excel. To do so, tbe company would have toretrain frontline employees and improve the infor-mation systems available to them. The group de-veloped performance measures for those criticalprocesses and for staff and systems capabilities.

Broad participation in creating a scorecard takeslonger, but it offers several advantages: Informationfrom a larger number of managers is incorporatedinto the internal ohjectives; the managers gain abetter understanding of the company's long-termstrategic goals; and such broad participation buildsa stronger commitment to achieving those goals.But getting managers to buy into the scorecard isonly a first step in linking individual actions to cor-porate goals.

The balanced scorecard signals to everyone whatthe organization is trying to achieve for sharehold-ers and customers alike. But to align employees' in-dividual performances witb the overall strategy,scorecard users generally engage in tbree activities:communicating and educating, setting goals, andlinking rewards to performance measures.

Communicating and Educating. Implementing astrategy begins with educating those who have toexecute it. Whereas some organizations opt to holdtheir strategy close to the vest, most believe thatthey should disseminate it from top to bottom. Abroad-hased communication program sbares withall employees the strategy and the critical objec-tives they have to meet if the strategy is to succeed.

The personal scorecard helpsto communicate corporate andunit objectives to the peopleand teams performing the work.

Onetime events such as the distribution of hro-chures or newsletters and the holding of "townmeetings" might kick off the program. Some orga-nizations post bulletin boards that illustrate andexplain the balanced scorecard measures, then up-date them with monthly results. Others use group-ware and electronic bulletin boards to distributethe scorecard to the desktops of all employees andto encourage dialogue about the measures. Thesame media allow employees to make suggestionsfor achieving or exceeding the targets.

The balanced scorecard, as the embodiment ofbusiness unit strategy, should also be communi-cated upward in the organization-to corporate head-quarters and to the corporate board of directors.With the scorecard, business units can quantify andcommunicate their long-term strategies to seniorexecutives using a comprehensive set of linked fi-nancial and nonfinancial measures. Such commu-nication informs the executives and the board inspecific terms that long-term strategies designedfor competitive success are in place. The measuresalso provide the basis for feedback and accountabil-ity. Meeting short-term financial targets should notconstitute satisfactory performance when othermeasures indicate that the long-term strategy is ei-ther not working or not being implemented well.

Should the balanced scorecard be communicatedbeyond tbe boardroom to external shareholders?We helieve that as senior executives gain confi-dence in tbe ability of the scorecard measures tomonitor strategic performance and predict futurefinancial performance, they will find ways to in-form outside investors about those measures with-out disclosing competitively sensitive information.

Skandia, an insurance and financial servicescompany based in Sweden, issues a supplement toits annual report called "The Business Navigator"-"an instrument to help us navigate into the futureand therehy stimulate renewal and development."The supplement describes Skandia's strategy andthe strategic measures the company uses to com-municate and evaluate the strategy. It also providesa report on the company's performance along those

measures during the year. The mea-sures are customized for each operat-ing unit and include, for example,market share, customer satisfactionand retention, employee compe-tence, employee empowerment, andtechnology deployment.

Communicating the balancedscorecard promotes commitmentand accountability to tbe business'slong-term strategy. As one executive

at Metro Bank declared, "The balanced scorecardis both motivating and obligating."

Setting Goals. Mere awareness of corporate goals,however, is not enough to cbange many people's be-havior. Somehow, the organization's high-levelstrategic objectives and measures must be trans-lated into objectives and measures for operatingunits and individuals.

The exploration group of a large oil company de-veloped a technique to enable and encourage indi-viduals to set goals for themselves that were consis-

80 HARVARD BUSINESS REVIEW January-February 1996

1

The Personal Scorecard

Corporate Objectives 1n Double ojr corporate value in seven years,n Increase our earnings by an average of 20% per year.D Achieve an internal rate of relurn 2% obave the cast of capital.n Increase bolh praduction ond reserves by 20% in the next decade.

Corporate Targets Scorecard Measures Business Unit Targets Team/Individual Objecttvssand InitiatTves

1995 19961199711998119991 |l995|l996|l997|l998|l999|Financial

100IOO100

12045085

160?0080

18021075

25022570

Earninqs (in millions oF dollars]Net cosh HowOverhead and operatinq expenses

I.

1 2Operotinq

100100100

7597105

7393108

7090lOfi

64B?no

Production costs per barrelDevelopment costs per barrelTatql annual production

111 3

Team/Individual Measures Tarqets1.2,3,A5.Name:

Location:

14.

5.

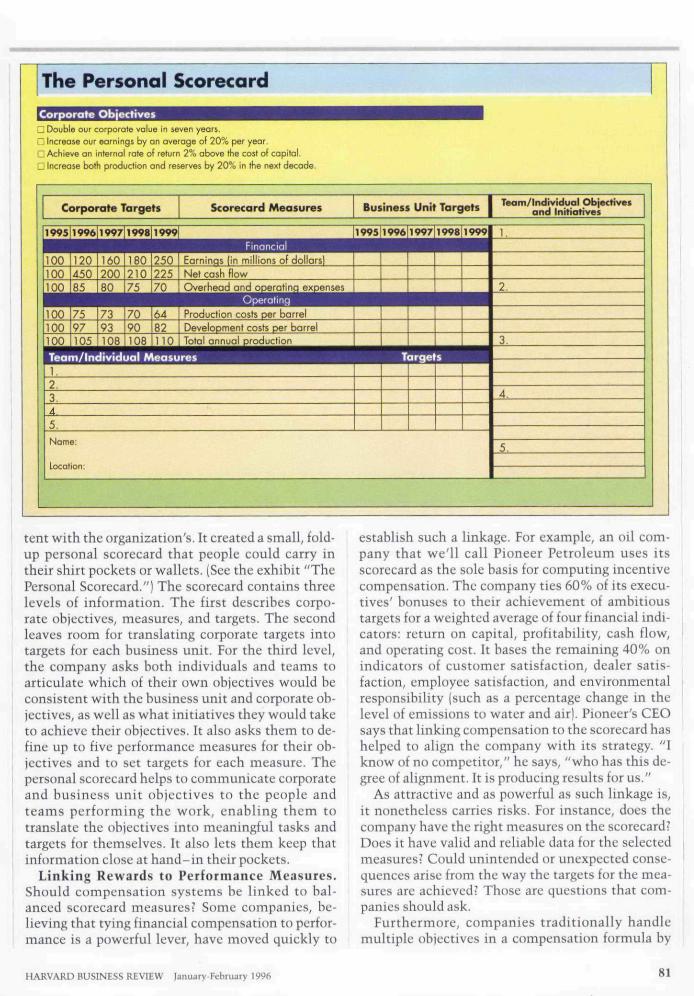

tent with the organization's. It created a small, fold-up personal scorecard that people could carry intheir shirt pockets or wallets. (See the exhihit "ThePersonal Scorecard.") The scorecard contains threelevels of information. The first descrihes corpo-rate ohjectives, measures, and targets. The secondleaves room for translating corporate targets intotargets for each husiness unit. For the third level,the company asks hoth individuals and teams toarticulate which of their own ohjectives would heconsistent with the husiness unit and corporate oh-jectives, as well as what initiatives they would taketo achieve their objectives. It also asks them to de-fine up to five performance measures for their oh-jectives and to set targets for each measure. Thepersonal scorecard helps to communicate corporateand husiness unit ohjectives to the people andteams performing the work, enahling them totranslate the ohjectives into meaningful tasks andtargets for themselves. It also lets them keep thatinformation close at hand-in their pockets.

Linking Rewards to Performance Measures.Should compensation systems be linked to hal-anced scorecard measures? Some companies, he-lieving that tying financial compensation to perfor-mance is a powerful lever, have moved quickly to

establish such a linkage. For example, an oil com-pany that we'll call Pioneer Petroleum uses itsscorecard as the sole basis for computing incentivecompensation. The company ties 60% of its execu-tives' honuses to tbeir achievement of ambitioustargets for a weighted average of four finaneiai indi-cators: return on capital, profitahility, cash flow,and operating cost. It hases the remaining 40% onindicators of customer satisfaction, dealer satis-faction, employee satisfaction, and environmentalresponsibility [such as a percentage cbange in tbelevel of emissions to water and air). Pioneer's CEOsays tbat linking compensation to the scorecard hashelped to align tbe company with its strategy. "Iknow of no competitor," he says, "who has this de-gree of alignment. It is producing results for us."

As attractive and as powerful as such linkage is,it nonetheless carries risks. For instance, does tbecompany bave the right measures on the scorecard?Does it bave valid and reliable data for tbe selectedmeasures- Could unintended or unexpected conse-quenees arise from the way the targets for the mea-sures are achieved? Those are questions that com-panies should ask.

Furthermore, companies traditionally handlemultiple objectives in a compensation formula by

HARVARD BUSINESS REVIEW |anuary-February 1996 81

BALANCED SCORECARD

assigning weights to each objective and calculatingincentive compensation by tbe extent to whicheach weighted objective was achieved. This prac-tice permits substantial incentive compensation tobe paid if the business unit overachicvcs on a fewobjectives even if it falls far sbort on others. A bet-ter approach would be to establish minimumthreshold levels for a critical subset of the strategicmeasures. Individuals would earn no ineentivecompensation if performance in a given period fellshort of any threshold. This requirement shouldmotivate people to achieve a more balanced perfor-mance across short- and long-term objectives.

Some organizations, bowever, have reduced theiremphasis on short-term, formula-based incentivesystems as a result of introducing the balancedscorecard. They have discovered that dialogueamong executives and managers about the score-card - both the formulation of the measures andobjectives and the explanation of actual versustargeted results - provides a better opportunity toobserve managers' performance and abilities. In-creased knowledge of their managers' abilitiesmakes it easier for executives to set incentive re-wards subjectively and to defend those subjectivecvaluations-a process that is less susceptible to thegame playing and distortions associated with ex-plicit, formula-based rules.

One company we have studied takes an interme-diate position. It bases bonuses for business unitmanagers on two equally weighted criteria: theirachievement of a financial objective - economicvalue added - over a three-year period and a sub-jective assessment of their performance on mea-sures dravk'n from the customer, intcrnal-business-process, and learning-and-growth perspectives ofthe balanced scorecard.

That the halanced scorecard has a role to play inthe determination of incentive compensation is notin doubt. Precisely what that role should be will be-come clearer as more companies experiment withlinking rewards to scorecard measures.

Business Planning

"Where the rubber meets the sky": That's howone senior executive describes his company's long-range-planning process. He might have said thesame of many other companies because their finan-cially based management systems fail to linkchange programs and resource allocation to long-term strategic priorities.

The problem is that most organizations haveseparate procedures and organizational units forstrategic planning and for resource allocation and

budgeting. To formulate their strategic plans, se-nior executives go off-site annually and engage forseveral days in active discussions facilitated by se-nior planning and development managers or exter-nal consultants. The outcome of this exercise is astrategic plan articulating where the company ex-pects (or hopes or prays) to be in three, five, and tenyears. Typically, such plans then sit on executives'bookshelves for the next 12 months.

Meanwhile, a separate resource-allocation andbudgeting process run by tbe finance staff sets fi-nancial targets for revenues, expenses, profits, andinvestments for the next fiscal year. The budget itproduces consists almost entirely of financial num-bers that generally bear little relation to the targetsin the strategic plan.

Which document do corporate managers discussin their monthly and quarterly meetings during thefollowing year; Usually only the budget, becausethe periodic reviews focus on a comparison of actu-al and budgeted results for every line item. Wben isthe strategic plan next discussed? Probably duringthe next annual off-site meeting, when the seniormanagers draw up a new set of three-, five-, and ten-year plans.

The very exercise of creating a balanced score-card forces companies to integrate their strategicplanning and budgeting processes and thereforehelps to ensure that their budgets support theirstrategies. Scorecard users select measures ofprogress from all four scorecard perspectives andset targets for each of them. Then tbey determinewhich actions will drive them toward their tar-gets, identify the measures they will apply to thosedrivers from the four perspectives, and establish theshort-term tnilestones that will mark their progressalong the strategic paths tbey have selected. Build-ing a scorecard thus enables a company to link itsfinancial budgets with its strategic goals.

For example, one division of the Style Company(not its real name] committed to achieving a seem-ingly impossible goal articulated by the CEO: todouble revenues in five years. The forecasts builtinto the organization's existing strategic plan fell$1 billion short of this objective. The division'smanagers, after considering various scenarios,agreed to specific increases in five different perfor-mance drivers: the number of new stores opened,the number of new customers attracted into newand existing stores, the percentage of shoppers ineach store converted into actual purchasers, theportion of existing customers retained, and averagesales per customer.

By helping to define the key drivers of revenuegrowth and by committing to targets for each of

HARVARD BUSINESS REVIEW |anuaiy-Fcbniar>' 1996

them, the division's managerseventually grew comfortable withthe CEO's ambitious goal.

The process of building a bal-anced scorecard - clarifying thestrategic objectives and then iden-tifying the few critical drivers -also creates a framework for man-aging an organization's variouschange programs. These initia-tives - reengineering, employeeempowerment, time-based man-agement, and total quality man-agement, among others - promiseto deliver results but also com-pete with one another for scarceresources, including the scarcestresource of all: senior managers'time and attention.

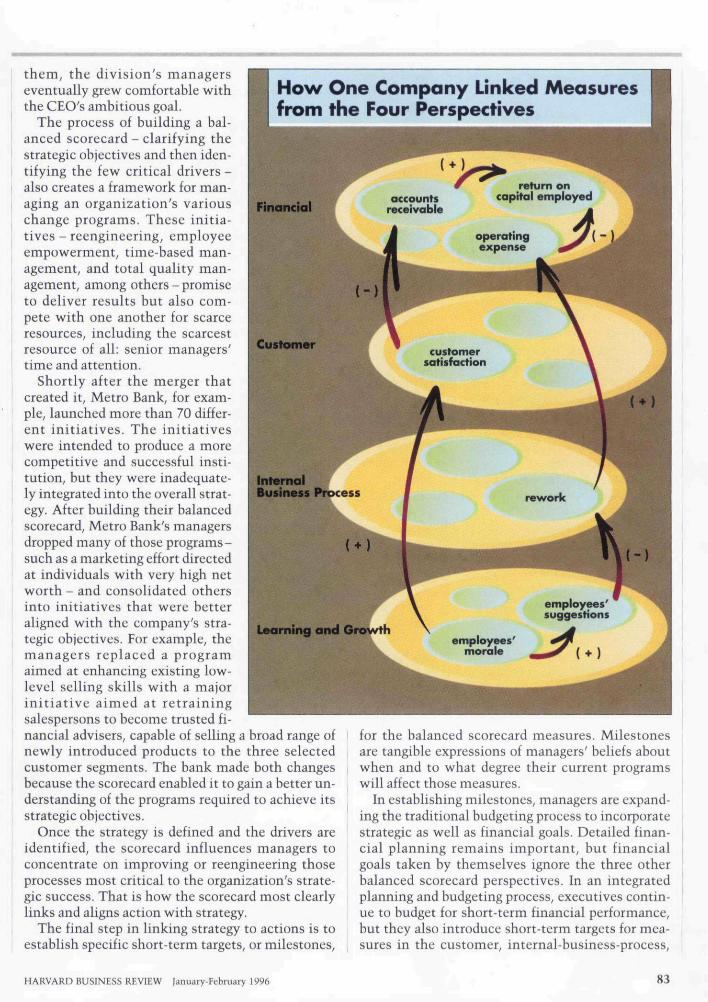

Shortly after the merger thatcreated it, Metro Bank, for exam-ple, launched more than 70 differ-ent initiatives. The initiativeswere intended to produce a morecompetitive and successful insti-tution, but they were inadequate-ly integrated into the overall strat-egy. After huilding their balancedscorecard, Metro Bank's managersdropped many of those programs-such as a marketing effort directedat individuals with very high networth - and consolidated othersinto initiatives that were betteraligned with the company's stra-tegic objectives. For example, themanagers replaced a programaimed at enhancing existing low-level selling skills with a majorinitiative aimed at retrainingsalespersons to become trusted fi-nancial advisers, capable of selling a broad range ofnewly introduced products to the three selectedcustomer segments. The bank made both changesbecause the scorecard enabled it to gain a better un-derstanding of the programs required to achieve itsstrategic objectives.

Once the strategy is defined and the drivers areidentified, the scorecard influences managers toconcentrate on improving or reengineering thoseprocesses most critical to the organization's strate-gic success. That is how the scorecard most clearlylinks and aligns action with strategy.

The final step in linking strategy to actions is toestablish specific short-term targets, or milestones.

One Company Linked Measuresfram the Four Perspectives

return oncapital employed

InternalBusiness Process

employees'suggestions

Learning and Grovsrth

for the balanced scorecard measures. Milestonesare tangible expressions of managers' beliefs aboutwhen and to what degree their current programswill affect those measures.

In establishing milestones, managers are expand-ing the traditional budgeting process to incorporatestrategic as well as financial goals. Detailed finan-cial planning remains important, but financialgoals taken by themselves ignore the three otherbalanced scorecard perspectives. In an integratedplanning and budgeting process, executives contin-ue to budget for short-term financial performance,but they also introduce short-term targets for mea-sures in the customer, imernal-business-process.

HARVARD BUSINESS REVIEW lanuary-Febniary 1996 83

BALANCED SCORECARD

and learning-and-growth perspectives. With thosemilestones establisbed, managers can continuallytest botb the theory underlying the strategy and thestrategy's implementation.

At the end of the business planning process, man-agers should have set targets for the long-termobjectives they would like to achieve in all fourscorecard perspectives; they should have identifiedthe strategic initiatives required and allocatedtbe necessary resources to tbose initiatives,- andthey should have established milestones for themeasures that mark progress toward achievingtheir strategic goals.

Feedback and Learning"With tbe balanced scorecard," a CEO of an engi-

neering company told us, "I can continually testmy strategy. It's like performing real-time re-search." That is exactly the capability that thescorecard should give senior managers: tbe abilityto know at any point in its implementation wheth-er the strategy they have formulated is, in fact,working, and if not, why.

The first tbree management processes - translat-ing the vision, communicating and linking, andbusiness planning - are vital for implementingstrategy, but they are not sufficient in an unpre-dictable world. Together they form an importantsingle-loop-learning process - single-loop in thesense that the objective remains constant, and anydeparture from the planned trajectory is seen as adefect to be remedied. Tbis single-loop process doesnot require or even facilitate reexamination of ei-ther the strategy or the techniques used to imple-ment it in light of current conditions.

Most companies today operate in a turbulent en-vironment witb complex strategies that, thoughvalid wben they were launched, may lose their va-Udity as business conditions cbange. In this kind ofenvironment, where new threats and opportunitiesarise constantly, companies must become capableof what Chris Argyris calls double-loop learning-learning that produces a change in people's assump-tions and theories about cause-and-effect relation-ships. (See "Teaching Smart People How to Learn,"HBR May-June 1991.)

Budget reviews and other financially hased man-agement tools cannot engage senior executives indouble-loop learning - first, because these toolsaddress performance from only one perspective,and second, because they don't involve strategiclearning. Strategic learning consists of gatheringfeedback, testing the hypotheses on which strategywas based, and making the necessary adjustments.

The balanced scorecard supplies three elementsthat are essential to strategic learning. First, it ar-ticulates tbe company's shared vision, defining inclear and operational terms the results that thecompany, as a team, is trying to achieve. The score-card communicates a holistic model that links in-dividual efforts and accomplishments to businessunit objectives.

Second, the scorecard supplies the essential stra-tegic feedback system. A business strategy can beviewed as a set of hypotheses about cause-and-effect relationships. A strategic feedhack systemshould be able to test, validate, and modify the hy-potheses embedded in a business unit's strategy. Byestablishing short-term goals, or milestones, with-in the business planning process, executives areforecasting the relationship between changes inperformance drivers and the associated changes inone or more specified goals. For example, execu-tives at Metro Bank estimated the amount of timeit would take for improvements in training and inthe availability of information systems before em-ployees could sell multiple financial products effec-tively to existing and new customers. They alsoestimated how great tbe effect of that selling capa-bility would be.

Another organization attempted to validate itshypothesized cause-and-effeet relationships in thebalanced scorecard by measuring the strength ofthe linkages among measures in the different per-spectives. (See the chart "How One CompanyLinked Measures from the Four Perspectives.") Thecompany found significant correlations betweenemployees' morale, a measure in the learning-and-growth perspective, and customer satisfaction, animportant customer perspective measure. Cus-tomer satisfaction, in turn, was correlated withfaster payment of invoices - a relationship that ledto a substantial reduction in accounts receivableand hence a higher return on capital employed. Tbecompany also found correlations between employ-ees' morale and the number of suggestions made byemployees (two learning-and-growth measures) aswell as between an increased number of sugges-tions and lower rework (an internal-business-pro-cess measure). Evidence of such strong correlationshelp to confirm the organization's business strat-egy. If, however, the expected correlations are notfound over time, it should be an indication to exec-utives that the theory underlying the unit's strategymay not be working as they had anticipated,• Especially in large organizations, accumulatingsufficient data to document significant correlationsand causation among balanced scorecard measurescan take a long time - montbs or years. Over the

84 HARVARD BUSINESS REVIEW (anuary-February 1996

short term, managers' assessment of strategic im-pact may have to rest on subjective and qualitativejudgments. Eventually, however, as more evidenceaccumulates, organizations may be able to providemore objectively grounded estimates of cause-and-effect relationships. But just getting managers tothink systematically about tbe assumptions under-lying their strategy is an improvement over the cur-rent practice of making decisions based on short-term operational results.

Third, tbe scorecard facilitates tbe strategy re-view that is essential to strategic learning. Tradi-tionally, companies use the monthly or quarterlymeetings between corporate and division execu-tives to analyze the most recent period's financialresults. Discussions focus on past performance andon explanations of why financial objectives werenot achieved. The balanced scorecard, with itsspecification of the causal relationships betweenperformance drivers and objectives, allows corpo-rate and business unit executives to use their peri-odic review sessions to evaluate the validity of theunit's strategy and the quality of its exeeution. Ifthe unit's employees and managers have deliveredon the performance drivers (retraining of employ-ees, availability of information systems, and new fi-nancial products and services, for instance), thentheir failure to achieve the expected outcomes(higher sales to targeted customers, for example)signals that the theory underlying the strategy maynot be valid. The disappointing sales figures are anearly warning.

Managers sbould take such disconfirming evi-dence seriously and reconsider their shared conclu-sions about market conditions, customer valuepropositions, competitors' behavior, and internalcapabilities. The result of sueh a review may be adecision to reaffirm their belief in the current strat-egy but to adjust tbe quantitative relationshipamong the strategic measures on the balancedscorecard. But they also might conclude that tbeunit needs a different strategy (an example of dou-ble-loop learning) in light of new knowledge aboutmarket conditions and internal capabilities. In anycase, the scorecard will bave stimulated key execu-tives to learn about the viabihty of their strategy.Tbis capacity for enabling organizational learningat the executive level - strategic learning-is what

distinguishes tbe balanced scorecard, making it in-valuable for those who wish to create a strategicmanagement system.

Toward a New Strategic ManagementSystem

Many companies adopted early balanced-score-card concepts to improve their performance mea-surement systems. They achieved tangible but nar-row results. Adopting those concepts providedclarification, consensus, and focus on the desiredimprovements in performance. More recently, webave seen companies expand their use of tbe bal-anced scorecard, employing it as the foundation ofan integrated and iterative strategic managementsystem. Companies are using the scorecard to• clarify and update strategy,n communicate strategy throughout the company,D align unit and individual goals witb the strategy,ni ink strategic objectives to long-term targets andannual budgets,

n identify and align strategic initiatives, andD conduet periodic performance reviews to learnabout and improve strategy.

Tbe balanced scorecard enables a company toalign its management processes and focuses the en-tire organization on implementing long-term strat-egy. At National Insurance, the scorecard providedthe CEO and his managers with a central frame-work around which they could redesign each pieceof the company's management system. And be-cause of the cause-and-effect linkages inherent inthe scorecard framework, changes in one compo-nent of the system reinforced earlier changes madeelsewhere. Therefore, every change made over tbe30-month period added to the momentum that keptthe organization moving forward in the agreed-upon direction.

Witbout a balanced scorecard, most organiza-tions are unable to achieve a similar consistency ofvision and action as they attempt to change direc-tion and introduce new strategies and processes.The balanced scorecard provides a framework formanaging the implementation of strategy whilealso allowing the strategy itself to evolve in re-sponse to ehanges in the company's competitive,market, and technological environments. ^

Reprint 96107 For ordering information, seepage 172.

HARVARD BUSINESS REVIEW lanuary-Febmary 1996 85