Embed Size (px)

Citation preview

Using Mixtures of Flexible Functional Forms to Estimate Factor Demand ElasticitiesAuthor(s): Stephen GordonSource: The Canadian Journal of Economics / Revue canadienne d'Economique, Vol. 29, No. 3(Aug., 1996), pp. 717-736Published by: Wiley on behalf of the Canadian Economics AssociationStable URL: http://www.jstor.org/stable/136259 .

Accessed: 16/06/2014 01:27

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

.

Wiley and Canadian Economics Association are collaborating with JSTOR to digitize, preserve and extendaccess to The Canadian Journal of Economics / Revue canadienne d'Economique.

http://www.jstor.org

This content downloaded from 188.72.126.55 on Mon, 16 Jun 2014 01:27:04 AMAll use subject to JSTOR Terms and Conditions

Using mixtures of flexible functional forms to estimate factor demand elasticities STEPHEN GORDON Universite Laval

Abstract. Researchers who wish to estimate factor demands using flexible functional forms may now choose from several candidates supplied by the theoretical literature. Unfortunately, the criteria for a priori model selection are not clear. This paper adopts the use of Bayesian methods and argues that there is in fact no need to choose; the optimal strategy is to use a mixture of functional forms to estimate the parameters of interest. Problems of overfitting are avoided by the imposition of the appropriate regulatory conditions. Practical irnplementation is greatly simplified by the use of Markov chain Monte Carlo techniques. In an example, three well-known functional forms for cost functions are applied to estimate factor demand elasticities in the Canadian manufacturing sector.

De l'utilisation de melanges de formes fonctionnelles flexibles dans l'estimation de 1'6da- sticite de la demande de facteurs de production. Les chercheurs qui d6sirent calibrer les fonctions de demande de facteurs de production en utilisant des formes fonctionnelles flex- ibles peuvent maintenant choisir clans un 6ventail de possibles pr6sent6s dans la litt6rature theorique. Malheureusement les criteres de s6lection a priori ne sont pas clairs. Ce m6moire utilise des m6thodes bayesiennes et suggere qu'on n'a pas besoin de choisir. La strat6gie optimale est d'utiliser un m6lange de formes fonctionnelles pour estimer les parametres qui nous interessent. On peut 6viter les problemes de surajustement en imposant les conditions de r6gularit6 appropri6es. L'utilisation pratique est grandement facilit6e par les techniques de Monte Carlo utilisant les chaines de Markov. Dans une illustration, on applique trois fonc- tionnelles bien connues dans le monde des fonctions de couts pour estimer les 6lasticit6s des demandes de facteurs de production dans le secteur manufacturier au Canada.

I. INTRODUCTION

A common theme in empirical applications of flexible functional forms is the need to choose between estimation strategies that fit the data and those that satisfy the regularity conditions suggested by the relevant economic theory. In the factor demand literature there are now several examples of functional forms for cost

Canadian Journal of Economics Revue canadienne d'Economique, xxlx, No. 3 August ao0t 1996. Printed in Canada Imprime au Canada

0008-4085 / 96 / 717-36 $1.50 ? Canadian Economics Association

This content downloaded from 188.72.126.55 on Mon, 16 Jun 2014 01:27:04 AMAll use subject to JSTOR Terms and Conditions

718 Stephen Gordon

functions that are flexible and for which the imposition of the appropriate regularity conditions is relatively straightforward.

It is not clear, however, which functional form is best suited for use in empirical applications. Theoretical studies (see, e.g., Caves and Christensen 1980; Barnett and Lee 1985; Lau 1986) address the properties of various functional forms across the entire sample space. Monte Carlo experiments (Wales 1977; Guilkey, Lovell, and Sickles 1983; Gagne and Ouellette 1994) examine the sampling properties of various functional form estimators in regions of the sample space covered by 'plausible' data-generating processes.

For empirical applications, the most pressing question is whether or not a partic- ular functional form is suitable for the data at hand. If the analyst were unconcerned with the regularity conditions, the appropriate functional form would be the one that best fit the data. Since flexible functional forms are typically characterized by a large number of parameters, however, the competing models are likely to overfit the data: such a strategy may end up simply choosing the model with the most free parameters. On the other hand, Barnett, Geweke, and Wolfe (1991) note that since a regular functional form cannot match perfectly the irregular patterns we observe, estimation strategies that incorporate regularity conditions will not overfit the data. If this is the case, the analyst need not be overly concerned with whether or not a functional form has a parameter vector that is too large.

The imposition of regularity conditions on cost functions often implies restric- tions on the estimated production technology. For example, global regularity in the Generalized Leontieff (Diewert 1971) and the Asymptotically Ideal Model (Bar- nett, Geweke, and Wolfe 1991) cost functions rules out the possibility that a pair of inputs might be complements. Obviously, conclusions on the usefulness of these functional forms depend crucially on whether or not the observed data display complementarity. If all of the inputs appear to be substitutes, then these functional forms may be appropriate; if not, then a functional form that allows for global regularity as well as complementarity (two examples are provided by Diewert and Wales 1987 and are examined below) may be more appropriate.

Since there does not appear to be a clear a priori criterion for choosing a functional form, it is natural to ask why it is even necessary to make such a choice before looking at the data. In the application of classicial methods of inference, there are efficiency gains to be made by restricting attention to the 'true' model, but actually making use of those gains appears problematic.

First, in order to identify the model that should be used to make inferences, the analyst would have to perform the appropriate hypothesis test and then estimate the chosen functional form. However, the statistical properties of this pre-test estimator are far from clear (see Leamer 1978 for more on this point). Motivating the model selection test poses extra problems: in the context of factor demands, the questions of interest are formulated usually in terms of demand elasticities, not necessarily in terms of the functional forms used to estimate them.

Second, it is not clear just how to interpret the notion of a 'true' flexible functional form, since the theoretical justifications of flexible forms are typically

This content downloaded from 188.72.126.55 on Mon, 16 Jun 2014 01:27:04 AMAll use subject to JSTOR Terms and Conditions

Flexible functional forms 719

couched in terms of how well the functional form under consideration can approxi- mate an unknown cost function. If models are considered to be simply useful para- metric representations of a complex phenomenon, it is difficult to avoid adopting a subjectivist Bayesian approach to the estimation problem; see, for example, Poirier (1988).

In the Bayesian framework presented below there is no reason to choose among the functional forms under consideration; optimal inference is based on a mixture of functional forms, where the weights associated with each functional form de- pend on prior and sample information. As noted above, if the analyst is willing to impose the appropriate regularity conditions on the model, there is no reason to limit the number of functional forms or the number of parameters associated with each functional form. The implementation of Bayesian methods is greatly simplified by the use of Gibbs sampling methods. An application to the Canadian manufacturing sector illustrates how this procedure can be used to estimate factor demand elasticities.

The paper has five sections. In section II the functional forms used in the ap- plication are described; how the data and the regularity conditions can be used to estimate and weight the various models are described in section III; the results of the empirical application are provided in section IV; and in section V conclusions are presented.

11. FLEXIBLE FUNCTIONAL FORMS FOR COST FUNCTIONS

Diewert (1974) defines a functional form as 'flexible' if it is capable of providing a second-order approximation to an arbitrary function at an arbitrary point in the sample space; two well-known examples are the translog and Generalized Leon- tieff (GL) forms. As discussed below, these functional forms are not well suited to the imposition of the appropriate regularity conditions. This difficulty is a pri- mary motivation for the development of functional forms that can incorporate both flexibility and the appropriate regularity conditions.

The functional forms for the cost functions used in this study can be represented by equation (1):

N N N

C(p, Q, t) = Q a a1pi + EYit + 6 + (t)), (1) i=1 i=1 i=1

where p is a vector of N input prices, Q is the (exogenous) output level, and 0(p) is a function of the prices. The possible dependence of the cost function on the time period t is incorporated in parameter vectors 'Y and 5. The regularity in the parameter conditions imposed upon C are that C(p, Q, t) be linearly homogeneous, non-decreasing and concave in p. The restriction that (1) be linearly homogeneous in p is satisfied if 0(p) is linearly homogeneous; this restriction is imposed by each of the models considered below. Note also that since C is linear in Q, the production technology displays constant returns to scale. Since the empirical application in

This content downloaded from 188.72.126.55 on Mon, 16 Jun 2014 01:27:04 AMAll use subject to JSTOR Terms and Conditions

720 Stephen Gordon

this paper makes use of aggregate data, the representative firm assumption is a maintained hypothesis in this study. The restriction that the production function displays constant returns to scale is a sufficient but not necessary condition for consistent aggregation; its use is adopted for simplicity.

When Shephard's Lemma is applied to (1), we obtain factor demand equations according to (2):

Zjl iaC(p, Q, t)(2 zi =] acp, Q t) of, +'y,t + b,t2 + dO(F)) i =1, . .. IN, (2)

where zi represents the quantity demand for input i. The factor demand equations form the basis for comparing the performance of

the competing models; more weight will be given to models that yield small devi- ations between (2) and observed factor demand. We now turn to a brief description of the functional forms considered in the empirical application.

1. Examples of flexible functional forms The first functional form considered is the Symmetric Generalized McFadden (SGM) cost function presented by Diewert and Wales (1987), where the expression for 0(p) in (1) is represented by

N N

E E oiupipi

0(p) (1/2) N' j (3)

i=1

where the ri terms are predetermined by the analyst.' For identification purposes, the restriction EN Oij = 0, j = 1, . .. I,N is imposed in the estimation.

Diewert and Wales (1987) also provide the second model considered in this paper, the Symmetric Generalized Barnett (SGB) cost function:

N N N N N

0(p) = 2 O ohip)124/2 O-h > Z Z jp2p-1/2p-1/2 (4) h=1 i=1,i>h h=1 i=1,i74h j=1,i74hj>i

The third and final example examined in this study is the Asymptotically Ideal Model (AIM) cost function, due to Barnett, Geweke, and Wolfe (1991). The sim- plest version (the AIM(1) functional form) is equivalent to the GL form, which is also a special case of the SGB functional form. Since both the AIM(2) and the SGB models can be interpreted as generalizations of the GL functional form, we consider the AIM(2) expansion. A problem is posed by the notation of the general

1 Following Diewert and Wales (1987), the values of -ri were set at the input levels of input i at the midpoint of the sample.

This content downloaded from 188.72.126.55 on Mon, 16 Jun 2014 01:27:04 AMAll use subject to JSTOR Terms and Conditions

Flexible functional forms 721

AIM form; since the data used in the estimation include series for capital (K), labour (L), energy inputs (E), and materials (M), equation (5) reports the AIM(2) expansion for these four inputs:

O(p) - olp~I4p)14 +Op~4p)4 +0p~4p)~4 +0p)2p I/2 0(P)-lP;/ L/ +02PL4U +03PL4S +094P L1/

+ 05p/2pL/I4p4 +06p!2pL1/4pf4 +07Pk'2p!2 +08pk/2pY4pj4 + O9pkk2pI2 +01 opk4p?14 +01 'Pk4PL12PY4 +012pP4pLl2pV4

+ OI3p)L/p/ 2 +014pI4pL4py4pj4 +015pk4pL/4P142 +9'6pV4pY4 + 017P(4p/2pj4 +018pk'4py4p)2 +0I19P/4p{4 +020P'P4/p4 (

+ 021PL 34pV4 +022P' 2plY2 +023pL'2pp4f4 +024PL'/2P2

+ 025pL 4pV4 + 426PL I2pj4 +027pLI/4p44pV42 +028pL14pV4

+ 2924p)~4 IF1P~2pV~2 +031p)f4p%4. + 029P P4 +030P;gP1 01XP

The models under consideration have several desirable properties: linear homo- geneity in prices is satisfied everywhere in the parameter space, the factor demand equations are linear in the parameters, and global concavity is easily imposed with the appropriate restrictions on the parameter space.

2. Imposing concavity One of the implications of Shephard's Lemma is that monotonicity is satisfied if input levels are positive. Since we observe only positive values for quantities, interest in regularity conditions is generally focused on the restriction that the cost function be concave in prices. There are two forms of concavity that the analyst may wish to impose: local concavity - due to Galland and Golub (1984) - and global concavity.

The weaker of the two restrictions is local concavity, in which the estimation imposes the restriction that the fitted cost function be concave at each data point. If the analyst is interested in simply measuring certain parameters of historical interest (say, the price elasticity of the demand for energy before and after the oil price shock), or if the object of the exercise is to generate forecasts flor a region of the sample space that is 'close' to what has been observed, then a cost function that is concave in the region of interest may be sufficient for the purposes of the analyst. Examples of this approach are provided by Gallant and Golub (1984) for the translog cost function, and by Koop, Osiewalski, and Steel (1994) for the AIM cost function.

If the analyst is interested in predicting behaviour in a region well outside the observed region of the sample space, however, or if the estimated parameters are to be incorporated into a general equilibrium model, then the analyst may wish to work with a cost function that is concave for all possible input price combina- tions. The restrictions on the parameters of 9(p) that are required by global con- cavity are:

This content downloaded from 188.72.126.55 on Mon, 16 Jun 2014 01:27:04 AMAll use subject to JSTOR Terms and Conditions

722 Stephen Gordon

Model Restriction for global regularity

SGM Matrix [9iw] is negative semi-definite

SGB Ohi, Ohij >O, Vh, i,j

AIM i >O, Vi

One consideration in the choice of a globally regular functional form is its degree of flexibility. Not all flexible forms can be globally concave; for example, the translog cost function can be made globally concave only at the expense of its flexibility. The three forms considered in this paper, however, can be globally concave while still retaining their flexibility. Even so, the functional forms do vary in their capacity-to incorporate flexibility and global concavity. Diewert and Wales (1987) note that a globally concave SGM functional form is flexible only at a certain point in the parameter space and that a globally concave SGB form can be said to be only 'quasi-flexible.' On the other hand, the AIM functional form can attain global flexibility as well as global concavity.

A second consideration is the effect that the imposition of global concavity has on the characteristics of the production technology. The GL form can be made glob- ally concave, but global concavity also implies that all input pairs must always be substitutes in production. The AIM functional form also shares this characteristic, but both the SGM and SGB functional forms allow for global concavity without excluding the possibility that two inputs might be complements.

There does not appear to be a compelling reason to choose one of the candi- date functional forms over the others based on the theoretical implications of the imposition of the regularity conditions. The choice of which form of concavity to impose largely depends on the analyst's focus of attention, but an evaluation of the appropriateness of a particular functional form depends on the available data.

111. MODEL ESTIMATION AND EVALUATION

This section describes how the implementation of Markov chain Monte Carlo (MCMC) techniques can be used to estimate the parameters of each model, the appropriate weights, and how mixtures of flexible functional forms can be used to estimate factor demand elasticities.

1. Overview of Bayesian methods It may be useful here to provide a brief outline of the Bayesian approach to pa- rameter estimation and model evaluation so that readers who are unfamiliar with Bayesian methods may appreciate the role of the MCMC techniques in addressing some of the computational issues involved in the current application. For a more detailed treatment see Bernardo and Smith (1994).

Suppose that there are K models, each indexed by m = 1, . . . , K. Let Mm be an indicator variable equal to 1 when the model is m and equal to 0 otherwise, and let the conditional distribution of the data x given model m and the parameter Am be

This content downloaded from 188.72.126.55 on Mon, 16 Jun 2014 01:27:04 AMAll use subject to JSTOR Terms and Conditions

Flexible functional forms 723

written as p(xIAm,Mm = 1). Conditional on model m, the application of Bayes's theorem yields

(xjIAin, IMm = 1)p(AmjMm 1) p(Am|x, Mm = 1) l (? m - 1)

p(xIA I Mm 1)p(ArmMm- 1)

p(x Am Mm l 1)p(AmIMm = 1)dAm

where p(Am Mmn = 1) represents prior beliefs about the parameters of model

m. The main computational challenge is posed by the marginalized likelihood

p(xIMm = 1), since analytic solutions for the integral involved exist for only a few special cases. A principal computational advantage of MCMC techniques is

that they provide estimates for expressions such as E[Amlx,Mm = 1] without cal- culating the marginalized likelihood.

The marginalized likelihood, however, also plays a role in model evaluatioll.

Given p(xIMm = 1), the posterior probability of model m is also provided by applying Bayes's theorem:

A(Mm i lx) A Plmt

- 1)p(Mm_ 1) K

Ep(xjM' = 1)p(M' = 1) j=1

in m _ AxVVn M m = 1)p(AmIMm =1)dA'np(Mm =1)

K,

E p(X|Ajl M' = 1)p(A IMJ = 1)dA'p(MJ 1) k=1

where p(Mm i) is the prior probability of model i.

In order to implement the Bayesian approach, the analyst much specify the prior

distributions p(AmjMm = 1) and p(Mm = 1) and must find a way to calculate - or to avoid calculating - the integrals associated with the marginalised likelihoods.

2. Parameter estimation As noted in section II, each of the competing models provides factor demand

equations that are linear in the parameters. Given a model m chosen from the K

candidates, at each observation t = 1, ... , T we can write

y =Xmm + u, (6)

where

Yt is the column vector [z,tI/Q1, z2,t/Qt IQ, I , ZN,t/Q]I

X7n is the N x km matrix of the covariates associated with model m

This content downloaded from 188.72.126.55 on Mon, 16 Jun 2014 01:27:04 AMAll use subject to JSTOR Terms and Conditions

724 Stephen Gordon

pm is the km x 1 vector of parameters associated with model m ut is an N-dimensional iid N(O, 2) vector of error terms.

Before going to the data, the analyst must specify prior beliefs about the param- eters in each model. Since model evaluation is an integral part of the analysis, there is a strong temptation to adopt the use of a conjugate prior, so that the posterior distribution has the same form as the prior distribution. An important advantage of this approach is that conjugate priors yield closed-form expressions for marginal- ized likelihoods. For the SUR model described in (6), the conjugate prior is of the normal-Wishart form, but Dreze and Richard (1983) note that there are two serious disadvantages with the normal-Wishart prior. First, prior beliefs about /3 and I cannot be independent. Secondly, the use of normal-Wishart prior imposes severe restrictions on the posterior covariance matrix of 1m*

Since the parameters of flexible functional forms have no intuitive economic interpretation, specifying prior beliefs is not straightforward. Since the functional forms are cost functions, however, we do have prior beliefs about certain combina- tions of the parameters, namely, the implications that a parameter combination has on the curvature of the cost function. As mentioned above, in order for a model to represent a cost function it must be concave in the price vector; such restric- tions rule out certain regions of the parameter space. It is in this context that the regularity conditions play a role in the estimation; this study adopts priors that are uniform across the regular parameter space. These priors are improper (in that they are not proper densities, and so the marginalized likelihood will not exist),2 which is a feature generally associated with so-called 'non-informative' priors that are designed to reflect complete ignorance about the parameter vector. Although these priors are improper, they are in fact informative, since zero prior mass is assigned to regions of the parameter space that do not conform to the regularity conditions.3 Two rounds of estimation will be carried out, one where local concavity is im- posed and one where concavity is imposed for all possible price combinations.4 Prior beliefs about z do not depend on a specific model and are independent of the distribution of pm. The standard 'non-informative' prior p(X) oc jXj-(N+1)/2 is adopted to describe prior beliefs about E. In the case of local concavity (LC), the prior beliefs are represented by

p(f m, xjMm = 1, LC) Oa Icrn(P)II-()/2

where P represents the set of observed prices, Cm(P) represents the region in the space of Om where the Hessian of the cost function is negative semi-definite at each

2 Note also that the use of an improper prior means that we cannot include the GL functional form in the estimation, since it is nested in both the AIM and SGB forms.

3 For example, imposing global concavity in the AIM model rules out all but one of the 2.1 billion orthants in the domain of 0.

4 The estimation procedure can also be applied to the case where the regularity conditions are not imposed, but the results are unlikely to be reliable. Since all the functional forms are heavily parameterized, all three unrestricted models are likely to overfit the data. Moreover, the demand elasticities derived from a cost function that is not concave will be difficult to interpret.

This content downloaded from 188.72.126.55 on Mon, 16 Jun 2014 01:27:04 AMAll use subject to JSTOR Terms and Conditions

Flexible functional forms 725

data point and where IC'(p) is an indicator function equal to one if Om E Cm(P) and equal to zero otherwise. Similarly, for the case in which global concavity (GC) is imposed, prior beliefs are represented by

P(f m XIMm| 1, GC) OIc" I I-(N+l)/2

where the concave region C' does not depend on observed prices. It is well known that the joint posterior distribution for (P', 1) is non-standard

(see, for example, Box and Tiao 1973). However, the model does yield conditional distributions that are much more easily dealt with. If the analyst knew the value of E. then the model (6) can be transformed into an OLS model. For the locally regular case, the conditional posterior distribution for /3' is of the normal form:

p(O' II, data, M' = 1, Lc) oa:fc-(pV(, (7))

where Am (_Xm'(IT 0 7 )Xm) X"n' ( X)y 0 -(I(TT ( T X-)

E -(XM (IT (9 2- )r)

and where y =yl ,y', . . . ,y' ]' is the stacked column of left-hand-side variables in (6), xm = [X1n X2m'',... X XTT']' is the stacked matrix of the regressors of model m, and IT is the identity matrix of dimension T.

Slimilarly, if the analyst knew the value of 3m C Cm(P), estimation of X is straightforward, since values for u, = y, -Xm/3om can be retrieved directly from (6). The conditional posterior distribution for I takes the inverse-Wishart form:

p(I- l )m, data, Mm 1, Lc) Wishart (S(n', data)-', T), (8)

where S(3', data) = ST UtU. Equations (7) and (8) form the basis of the Gibbs sampling estimation algorithm.

Since the normal and Wishart distributions are easily simulated, we can iterate between (7) and (8) to construct a random sequence {/3d, Id}Id according to

EI - xlom', Mm _ 1, data)

/3 'v p( mfX1 l Mm-=19 data) m

02, p(12mI 1,Mm-1, data) pm

' P(110ml2 Mm 1, data.)

2 ' P((mI22, Mm 1, data)

1, _p(XIf L1, Mm 1 data)

/37 'p(/3ml2j, Mm =1, data)

This content downloaded from 188.72.126.55 on Mon, 16 Jun 2014 01:27:04 AMAll use subject to JSTOR Terms and Conditions

726 Stephen Gordon

It can be shown (Gelfand and Smith 1990; Casella and George 1992) that this sequence is an irreducible and aperiodic Markov chain that converges in distribution to the joint posterior distribution of the pair (m', XIMI, data). Given D draws from this distribution, we can consistently estimate the posterior moments of g(f3,),

where g(-) is a function of interest. Note that since D is chosen by the analyst, any desired degree of accuracy can (in principle) be obtained.

This procedure is applied to each of the three models considered and for both the LC and GC cases.

3. Model evaluation For the LC case, the posterior probability of model m is given by

J J L(3m, XJdata)1X1-5/2dXdI3mp(Mm = 1)

p(M = 1jLC, data) = K

E '4 JECJ(P) jL(3', Ildata)III5/2dXdf'p(M'= 1) j=1 EPiCi(P) J

where L(3m, Xjdata) represents the likelihood function for the T observations of the multivariate normal density described in (6). While there is no analytic expression for the double integral with respect to both O3m and E, there is an analytic expression for the inner integral. Integrating with respect to I yields (Box and Tiao 1973, 428):

_ IS3Is(m, data)1T/2d3mp(Mm = 1) p(M m = 1 | Lc, data)- lEC (P) (9)

>1jiEC(P) |jS(Q3i, data)1-T/2d131p(Mj = 1) j=1 pECi(P)

where S(3m, data) is the matrix of the sum of the outer products of the residuals used in (8) above.

Since the parameter vectors are of fairly high dimension (a common feature of flexible functional forms), application of numerical integration techniques to (9) would be a cumbersome exercise. The use of Markov chain techniques, however, provides estimates for p(Mm = 1 JLc, data) directly.

The approach adopted in this paper is due to Carlin and Polson (1991); other extensions of Markov chains to model selection problems include George and McCulloch (1993) and Carlin and Chib (1995). In this application model evaluation is facilitated by adding the model indicator parameter to the model:

Y = Mm(Xtm3m) + ut. (10)

Given values for O3m C Cm(P) for each m, and integrating out I as above,5 the conditional posterior probability for model m is

P(M - l{I3'}'j LC, data)= IS(f3', data)| T/2p(Mm = 1ILC) (11)

E JS(j3, data) T/2p(Mj = 1|LC) i=l

5 We could also condition the model choice probabilities on S. While this poses no theoretical

This content downloaded from 188.72.126.55 on Mon, 16 Jun 2014 01:27:04 AMAll use subject to JSTOR Terms and Conditions

Flexible functional forms 727

Values for the model choice parameter can be simulated using the probabilities according to (11). Note also that the algorithm described in section 111.2 above provides a method for drawing values of /' from its marginal posterior distribution. The model evaluation algorithm is initiated by iterating between (7) and (8) for each model until convergence is ?eached, at which point the chain iterates between two steps: 1. Use (11) to select a model. 2. If model m is chosen in step 2, apply (7) and (8) to the chosen model to generate

a new value for /m. Values for /i, ] 7j m are not revised.6 The point estimate for p(Mm = 1 JLC, data) is simply the number of times the

chain visits model m divided by the number of iterations; this estimator has a maximum standard error of (4D) /2, where D is the number of iterations. The analysis for the case in which global concavity is imposed is done analagously.

4. Estimating price elasticities Given a model and the relevant parameter values, denote the elasticity of demand for factor i with respect to the price of input j at period t by

7Jt - q(3%", data),

where 77T depends on the parameters of the cost function as well as the data. The posterior mean of rlip given model m, the data and the local concavity prior, is

E[pij,tIMm = 1, LC, data]

j CCm( P) 4fQ(3m, data)p(mjMm = 1, LC7 data)dfm. (12) J C-( P)

Given a sample {/3}mD_ drawn from the posterior distribution p(QrIMm= 1,LC, data), a consistent estimate for the posterior mean is D-1: D 1Z77T(3d, data). Note that instead of basing estimates of elasticities on a point estimate of pm, this estimator integrates across the posterior uncertainty about the parameters of the cost function.

problem, it slows convergence of the Markov chain. For example, consider the case in which there are two bivariate models. Suppose that model A generates large errors in the first equation and generates small errors in the second, while the reverse is true for model B. If model A is used to start the chain, it would then be used to generate a new value of S. When the models are compared again, Model B would be penalized for the larger errors it generates in first equation. Since the normal density is decreasing in squared residuals, this will outweigh the credit it would receive for the smaller residuals generated in the other system. Since the conditional model probabilities will tend to favour the nmodel that had been used to generate X, the Markov chain will tend to stay with one model for longer periods of time. This problem is not encountered in univariate systems, where the criterion for model evaluation is unambiguous.

6 Carlin and Chib (1995) suggest a method of simulating draws for the parameters of the models that are not chosen. As we shall see, the support for one model is so overwhelming that the problem of staying with one model for too long does not appear in this application.

This content downloaded from 188.72.126.55 on Mon, 16 Jun 2014 01:27:04 AMAll use subject to JSTOR Terms and Conditions

728 Stephen Gordon

TABLE 1 Steps of the estimation

1 Generate draws for the parameters of each model by applying the Gibbs sampler using equations (7) and (8).

2 For each model, generate corresponding sequences of demand elasticities. The means of these sequences provide the estimates for the demand elasticities.

3 Estimate the posterior probabilities for each model according to the model selection Markov chain.

4 Use the model probabilities to weight the estimated elasticities.

The estimates in (12) are then weighted by the posterior probability of the model used to generate them:

K

E[?7ij,tILc, data] = ZEtE7itIMm- 1, LC, datajp(Mm = 1ILC, data) (13) m=1

Estimation of E[,qij,tGcC, data] is done using draws of pm that satisfy global regu- larity.

5. Summary of the estimation strategy The estimation strategy is summarized in table 1. Two rounds of estimation are performed, one imposing local concavity and the other imposing global concavity. For both the LC and the GC cases, the prior probabilities assigned to each of the three functional forms under consideration are set equal to 1/3.

IV. EMPIRICAL RESULTS

In this section the results of the application of the procedure outlined in table 1 are applied to annual data provided by Statistics Canada for the Canadian manufacturing sector for the period 1961-86. The levels of gross output and of the inputs are measured in constant 1986 dollars. As mentioned above, there are four input types: capital, labour, energy, and materials, denoted by K, L, E, and M, respectively. The capital measure incorporates both buildings and machinery inputs, the labour series combines both administrative and production employees, and the materials input series includes services and intermediate inputs. All combinations were done using the Tornqvist discrete-time approximation to the Divisia method.

Since the actual parameters of the various functional forms have little economic content, discussion of the results is based on the estimated price elasticities. The time series of the various estimated elasticities are presented in graph form; more detailed results are available from the author.

1. Local concavity In contrast to the globally concave case, there is no convenient way to characterize the locally concave region of the parameter space for each model; concavity must

This content downloaded from 188.72.126.55 on Mon, 16 Jun 2014 01:27:04 AMAll use subject to JSTOR Terms and Conditions

Flexible functional forms 729

be verified at each data point. In the application of the Gibbs sampler to the locally concave model, candidate values for Om were drawn from (7) and the concavity conditions were checked at each data point. If the candidate vector was in the locally regular region, it was accepted; if not, new draws were generated until a locally regular value of pm was found. Unfortunately, the rate of acceptance for an entire O3m vector was very small, reflecting the low probability assigned to the locally concave region in each model. It turned out to be faster to perform sequential univariate draws for each /T from the conditional distribution p(/3 l3mi,/ , Mm _ 1, data), where 3mi represents the set of elements in O3m other than 1T7. The increased acceptance rate for the draws more than compensated for the computational burden of the repeated calculation of the conditional means and variances of the resulting univariate normal distributions. For each model, 6,000 draws for Om were generated; the first 1,000 draws were discarded in estimating the demand elasticities.

In the model selection step the SGM model was found to receive overwhelming support from the data when compared with the SGB and AIM functional forms: the model selection chain always chose the SGM case in the first iteration and stayed there regardless of the starting values chosen in the other models. Other models were chosen only when the prior probability for the SGM functional form was set well below the floating point relative accuracy of the computer (2-52).7 The likely explanation for this dominance is that the local concavity restriction appears to be less binding for the SGM model than for the other models. In a round of estimation without the concavity restrictions, 54 of 5,000 draws of the SGM model were locally regular; none of the 5,000 draws generated by the unrestricted SGB or AIM specifications satisfied the local concavity conditions.

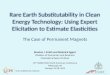

Although the posterior probabilities associated with the SGB and AIM functional forms are positive, their contribution to the posterior means in (13) is extremely small. If we limit the precision of our estimates to that of the data (five or six significant digits), then there is no loss in concentrating on the SGM results alone. The posterior means for the elasticities of demand for the four inputs with respect to their prices are plotted in figures 1-4. The numerical standard errors for the posterior means were calculated using the method described in Geweke (1992); in each case the numerical standard error was less than 0.5 per cent of the absolute value of its estimate.

Some features of the graphs are worth mentioning. Not surprisingly, the oil price shock in the 1970s significantly affected factor demands: many series have sharp spikes at the shock. It is also of interest to note that the sensitivity of labour demand with respect to changes in its own price increases over time, while the reverse is the case for the own-price elasticity of the demand for energy. Of the six input pair combinations only the capital-materials and labour-energy pairs are cornplements; the other four pairs are substitutes.

7 When the prior probability of the SGM model was set to zero, the SGB model was always chosen over the AIM functional form.

This content downloaded from 188.72.126.55 on Mon, 16 Jun 2014 01:27:04 AMAll use subject to JSTOR Terms and Conditions

730 Stephen Gordon

0.15

pL

0.1

0.05 - pE

0

-0.05 -

pK

-0.1 -

-0.15 1960 1965 1970 1975 1980 1985

FIGURE 1 Estimated price elasticities for the demand for capital - local concavity

0.25 ,

0.2 pM

0.15 /

0.1

0.05 - pK

0

-0.05 p

-0.1

-0.15

-0.2 - PL

-0.25 1960 1965 1970 1975 1980 1985

FIGURE 2 Estimated price elasticities for the demand for labour - local concavity

This content downloaded from 188.72.126.55 on Mon, 16 Jun 2014 01:27:04 AMAll use subject to JSTOR Terms and Conditions

Flexible functional forms 731

0.15 I -

0.1 pM

0.05

pK

0

-0.05 _- pL

pE

-0.1 1 1960 1965 1970 1975 1980 1985

FIGURE 3 Estimated price elasticities for the demand for energy - local concavity

0.068

pL-

0.06

0.04

0.02 pE

0-

-0.02 pK

-0.04

-0.06 -

-0.08 - pM

-0.1 1960 1965 1970 1975 1980 1985

FIGURE 4 Estimated price elasticities for the demand for materials - local concavity

This content downloaded from 188.72.126.55 on Mon, 16 Jun 2014 01:27:04 AMAll use subject to JSTOR Terms and Conditions

732 Stephen Gordon

2. Global concavity For the SGB and AIM models, global concavity is satisfied if the parameters in 0(p) are positive. Positivity was imposed by drawing values of /3 from the pos- itive tail of the univariate normal density p(/l. I3mi, ,M'- 1, data). Imposition of global regularity in the SGM model was imposed by accepting draws from

p(0TJ0:mi,1:,Mm = 1,data) that satisfied the global concavity restrictions.8 Since the concavity conditions did not need to be checked at each data point, estimation of the globally concave model was much more rapid.

The dominance of the SGM case in the model selection step was even more pronounced than in the locally concave case. Again, the likely explanation is the relatively higher probability associated with the globally concave region of the parameter space. Of the 5,000 locally regular draws of the SGM model just over half satisfied global concavity, while none of the locally regular draws for the SGB and AIM forms was consistent with global concavity.

Since the contribution of the other models is infinitesimal, the results graphed in figures 5-8 are those of the SGM model. In the case of the demand for cap- ital, the imposition of global concavity reduces the estimated price elasticities by roughly half, but aside from the scale, there are no remarkable differences between figures 1 and 5. This is not the case for the estimates for the elasticities of demand for labour graphed in figure 6. While the elasticity of demand with respect to the capital price is reduced by roughly half, the own-price labour demand elasticities increase by 25-30 per cent when global concavity is imposed. Furthermore, the signs of the estimated elasticities of demand for labour with respect to the price of energy change: labour and energy appear to be complements when local concavity is imposed, but when the estimation is done with global concavity imposed, the estimated posterior means suggest that they are substitutes. It should also be noted, however, that this apparent reversal is not complete; the estimated probability that labour and energy are complements is around 0.97 at each data point using the local concavity restriction, while the global concavity results provide an estimated posterior probability that the two inputs are substitutes of about 0.75. In the case of energy demand, the imposition of global concavity increases the own-price elas- ticity estimates by between 50-75 per cent, while the elasticity of energy demand with respect to the price of materials is roughly halved. It is interesting to note that energy is a substitute for all of the other inputs. The estimates for the demand

8 The most computationally efficient approach, due to Wiley, Schmidt, and Bramble (1973) and adopted by Diewert and Wales (1987), would be to reparametrize the model so that the estimation of is done in terms of the Cholesky root of the matrix -[Oij], i, j = 1, 2, 3. The conditional distribution of the new parameters is non-standard, but draws can be made by means of the Metropolis-Hastings algorithm (for an intuitive exposition, see Chib and Greenberg 1994). As it happens, the rate of acceptance for this case as quite high, so the computational cost in terms of the extra time for each draw turned out to be less than the extra programming time required to calibrate appropriate proposing distributions for the new parameters. A few preliminary rounds with the Metropolis-Hastings algorithm suggested that the results would be unaffected. Since all of the other Markov chains were based on the Gibbs sampler, it was felt that direct comparisons would be easier to motivate if the same estimation procedure was applied to each model.

This content downloaded from 188.72.126.55 on Mon, 16 Jun 2014 01:27:04 AMAll use subject to JSTOR Terms and Conditions

Flexible functional forms 733

0.08 , , ,

pL 0.06 -

0.04 -

0.02 - pE

0-

-0.02 -

pK -0.04 \

-0.06 -

PM -0.08

-0.1 . 1960 1965 1970 1975 1980 1985

FIGURE 5 Estimated price elasticities for the demand for capital - global concavity

0.3 _

0.2 pM

0.1

pE

0 pK

-0.1

-0.2 -

pL -0.3 1 L

1960 1965 1970 1975 1980 1985

FIGURE 6 Estimated price elasticities for the demand for labour - global concavity

This content downloaded from 188.72.126.55 on Mon, 16 Jun 2014 01:27:04 AMAll use subject to JSTOR Terms and Conditions

734 Stephen Gordon

0.1 , . . .

pM

0 pK

-0.05

-0.1

pE

-0.15 -

-0.2 1 . . 1960 1965 1970 1975 1980 1985

FIGURE 7 Estimated price elasticities for the demand for energy - global concavity

0.08 E , . .

pL 0.06

0.04

0.02

pE 0-

pK -0.02

-0.04

-0.06 -

PM

-0.08 1960 1965 1970 1975 1980 1985

FIGURE 8 Estimated price elasticities for the demand for materials - global concavity

This content downloaded from 188.72.126.55 on Mon, 16 Jun 2014 01:27:04 AMAll use subject to JSTOR Terms and Conditions

Flexible functional forms 735

elasticities for materials do not appear to be greatly affected by the imposition of global concavity.

V. CONCLUSION

There are certain conclusions that should not be drawn. First, it should be noted that the SGB and AIM functional forms were not 'rejected' in the estimation, since a model selection test is not performed. If the data warranted a high level of precision for the estimates of the price elasticities, all three models would have been used. Second, no general inferences should be drawn about the relative capabilities of the various functional forms to fit other data sets. Although Diewert and Wales (1987) also find that the SGM model does well, their estimation results are based on a data set that is similar to that used here: annual manufacturing data with KLEM inputs. The other functional forms may do quite well with other data sets; for instance, the data used by Bamett, Geweke, and Wolfe (1991) appear to be generally consistent with the AIM global concavity conditions.

The main point of this paper is that there is no need to condition inferences about factor demand elasticities on the choice of a particular flexible functional form. Since these flexible forms are generally interpreted as approximation to an unknown regular cost function, the best estimation strategy is to make use of as many models as possible and to allow the data to determine which functional form is best able to explain the data at hand.

REFERENCES

Barnett, W.A., J. Geweke, and M. Wolfe (1991) 'Seminonparametric Bayesian estimation of the asymptotically ideal production model.' Journal of Econometrics 49, 5-50

Barnett, W.A., and Y.W. Lee (1985) 'The global properties of the miniflex Laurent, generalized Leontieff and translog flexible forms.' Econometrica 53, 1421--37

Bernardo, J.M., and A.F.M. Smith (1994) Bayesian Theory (Chichester, UK: John Wiley) Box, G.F.P., and G.C. Tiao (1973) Bayesian Inference in Statistical Analysis (Reading,

MA: Addison-Wesley) Carlin, B.P., and S. Chib (1995) 'Bayesian model choice via Markov Chain Monte Carlo.'

Journal of the Royal Statistical Society-B 57, 473-84 Carlin, B.P., and N.G. Polson (1991) 'Inference for nonconjugate Bayesian models using

the Gibbs sampler.' Canadian Journal of Statistics 19, 399-405 Casella, G., and E. George (1992) 'Explaining the Gibbs sampler.' American Statistician

46, 167-74 Caves, D.W., and L.R. Christensen (1980) 'Global properties of flexible functional forms.'

American Economic Review 70, 322-32 Chib, S., and E. Greenberg (1994) 'Understanding the Metropolis-Hastings algorithm.'

Washington University working paper Diewert, W.E. (1971) 'An application of the Shephard duality theorem: a generalized

Leontieff production function.' Journal of Political Economy 79, 481-507 -(1974) 'Applications of duality theory.' In Frontiers of Quantitative Economics, Vol 1[,

ed. M.D. Intriligator and D.A. Kendrick (Amsterdam: North-Holland) Diewert, W.E., and T.J. Wales (1987) 'Flexible functional forms and global curvature

conditions.' Econometrica 55, 43-68

This content downloaded from 188.72.126.55 on Mon, 16 Jun 2014 01:27:04 AMAll use subject to JSTOR Terms and Conditions

736 Stephen Gordon

Dr&ze, J.H., and J.-F. Richard (1983) 'Bayesian analysis of simultaneous equation sys- tems.' In Handbook of Econometrics, Vol I, ed. Z. Griliches and M.D. Intriligator (Amsterdam: North-Holland)

Gagne, R., and P. Ouellette (1994) 'On the choice of functional forms: a Monte Carlo experiment.' Cahier de recherche IEA-94-04, Ecole des Hautes Etudes Commerciales (HEC), Montreal

Gallant, A.R., and G.H. Golub (1984) 'Imposing curvature restrictions on flexible func- tional forms.' Journal of Econometrics 26, 295-321

Gelfand, A., and A. Smith (1990) 'Sampling-based approaches to calculating marginal densities.' Journal of the American Statistical Association 85, 398-409

George, E.I., and R.E. McCulloch (1993) 'Variable selection via Gibbs sampling.' Journal of the American Statistical Association 88, 881-9

Geweke, J. (1992) 'Evaluating the accuracy of sampling-based approaches to the calcula- tion of posterior moments.' In Bayesian Statistics 4, ed. J.M. Bernardo, J.O. Berger, A.P. Dawid, and A.F.M. Smith (Oxford: Oxford University Press)

Guilkey, D.K., C.A.K. Lovel, and R.C. Sickles (1983) 'A comparison of the performance of three flexible forms.' International Economic Review 24, 591-616

Koop, G., J. Osiewalski, and M. Steel (1994) 'Bayesian efficiency analysis with a flexible form: the AIM cost function.' Journal of Business and Economic Statistics 12, 339-46

Lau, L.J. (1986) 'Functional forms in econometric model building.' In Handbook of Econometrics, Vol III, ed. Z. Griliches and M. Intriligator (Amsterdam: North-Holland)

Leamer, E.E. (1978) Specification Searches (New York: John Wiley) Poirier, D.J. (1988) 'Frequentist and subjectivist perspectives on the problems of model

building in economics.' Journal of Economic Perspectives 2, 121-70 Wales, T.J. (1977) 'On the flexibility of flexible functional forms.' Journal of Economet-

rics 5, 183-93 Wiley, D.E., W.H. Schmidt, and W.J. Bramble (1973) 'Studies of a class of covariance

structure models.' Journal of the American Statistical Association 68, 317-23

This content downloaded from 188.72.126.55 on Mon, 16 Jun 2014 01:27:04 AMAll use subject to JSTOR Terms and Conditions