Embed Size (px)

Citation preview

Welcome!The Return of the Tone at the Top

Gerard Zack, CFE, CPA, CIA, CCEPManaging Director, Global Forensics

BDO USA, LLP

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc.

Gerard M. Zack, CFE, CPA, CIAManaging Director, Global Forensics

BDO USA, LLP

Washington, DC

The Return of the Tone at the TopSessions 2B/5B

3 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 3 of 40

Session Objectives

1. Understand how tone at the top affects:

• Financial statement fraud

• Nonfinancial reporting fraud

• Corruption schemes

• Asset misappropriation schemes

2. Identify different elements of corporate culture

in our organizations that can increase the risk

of fraud and corruption.

3. Determine practical action steps we can take

to improve tone at the top.

4 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 4 of 40

Corporate Culture—2002

CEO Bernie Ebbers “created, and the [then] board

permitted, a corporate environment in which

pressure to meet numbers was high, the

departments that served as controls were weak,

and the word of senior management was final and

not to be challenged.”

5 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 5 of 40

Corporate Culture-2015

Toshiba

“A corporate culture at Toshiba where it was

impossible to go against the boss’s will” and “a

systematic involvement including by top

management, with the goal of intentionally inflating

the appearance of net profits.”

6 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 6 of 40

Poor Tone at the Top Identified

as an Internal Control Weakness

22.9% of financial statement frauds

16.9% of corruption cases

9.5% of asset misappropriation cases

Source:

2016 ACFE Report to the Nations on Occupational Fraud and Abuse

7 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 7 of 40

CASE STUDIES

8 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 8 of 40

Toshiba Profit Inflation Scheme

Pre-tax profit inflated by

$1.9 billion (USD)

Senior management

pressured employees to

meet targets

Employees interpreted as

implicit direction to cook

the books

CEO denies giving explicit

instruction

9 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 9 of 40

Toshiba

CEO instructed executives to “use every

possible measure to achieve profitability.”

Culture in place made it impossible for

employees to go against the will of their

superiors.

Profit targets became more and more

aggressive.

Division heads were told their business might

be closed if results did not improve.

Accounting department intentionally misled

auditors to cover up the scheme.

10 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 10 of 40

37 PERCENT OF MANAGEMENT

ACCOUNTANTS HAVE FELT

PRESSURE FROM MANAGERS OR

PEERS TO COMPROMISE

CORPORATE ETHICS

Source: Chartered Global Management Accountant (2015)

11 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 11 of 40

Tesco Inflated Profits by £263m

Problem can be traced to expansion beyond

traditional grocery business in early 2000s– clothing,

garden centers, banking, etc.

2006–open U.S. chain, part supermarket, discount,

convenience store

Back in home market–competition heats up

Pressure to maintain profitability rises

12 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 12 of 40

Tesco Profit Inflation

Improper accounting for supplier credits

Can be traced to overly aggressive tactics in

dealing with suppliers as a method of

meeting profit goals

In one email, direction was given to “maintain

[Tesco’s] margin at key financial reporting

periods” by “not paying back money owed” to

a supplier.

13 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 13 of 40

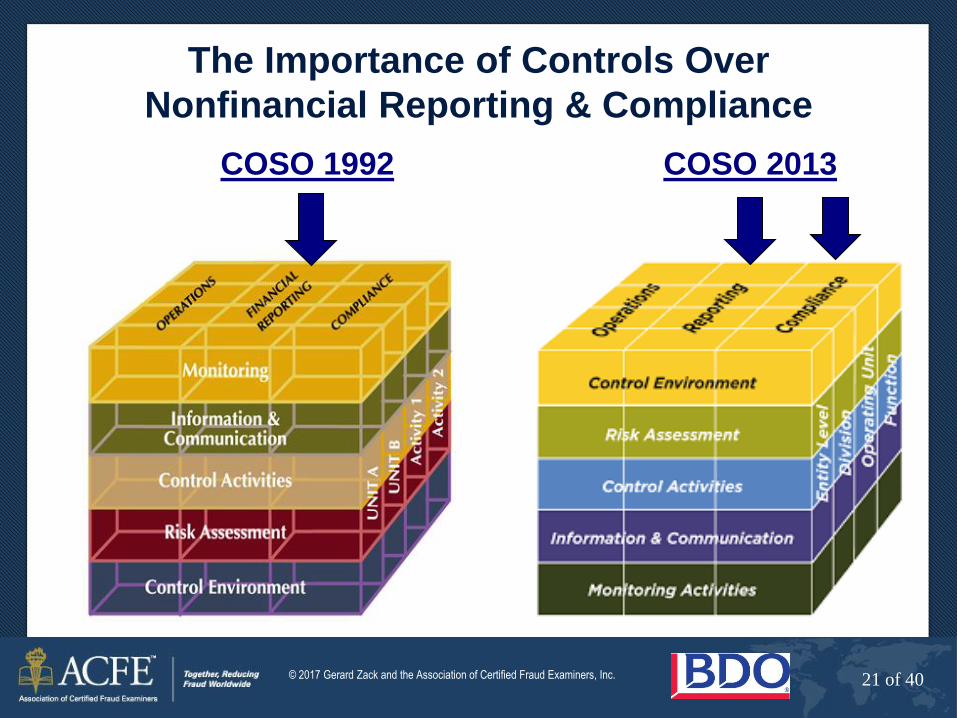

Multiple Accounting

Errors

Fifteen separate areas of the company’s 2012

and 2013 financials required restatement.

Investigation identified weaknesses in four of

the five COSO components of internal controls:

• Control environment

• Risk assessment

• Control activities

• Information and communication

• Monitoring

14 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 14 of 40

Hertz Control Environment

An “inconsistent and sometimes inappropriate tone at

the top.”

“Our former chief executive officer’s management

style and temperament created a pressurized

operating environment at the company, where

challenging targets were set and achieving those

targets was a key performance expectation.”

“There was in certain instances an inappropriate

emphasis on meeting internal budgets, business

plans, and current estimates.”

Also cited lack of expertise, training, and reporting

structure.

15 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 15 of 40

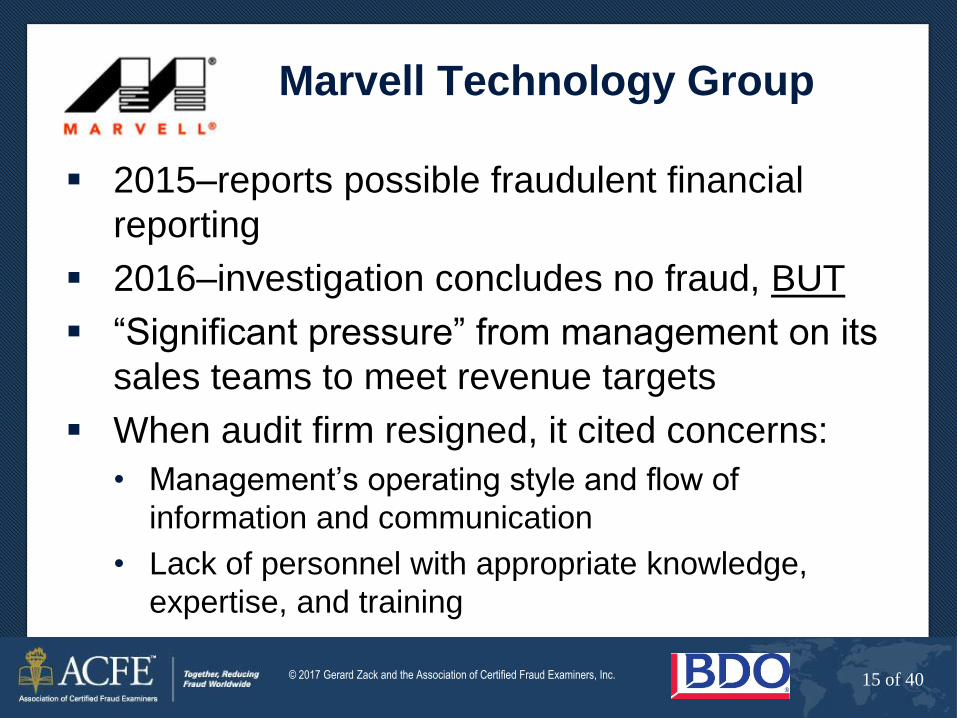

Marvell Technology Group

2015–reports possible fraudulent financial

reporting

2016–investigation concludes no fraud, BUT

“Significant pressure” from management on its

sales teams to meet revenue targets

When audit firm resigned, it cited concerns:

• Management’s operating style and flow of

information and communication

• Lack of personnel with appropriate knowledge,

expertise, and training

16 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 16 of 40

It’s Not All About Financial Reporting

This is the story of the president of Mount St. Mary’s

University.

One metric for the university involves the success

rate of students.

The denominator of this rate is “enrolled” students.

“Enrolled” is measured on September 25, after

students have been in classes for about three

weeks.

If the president could get the professors to weed out

the students most likely to fail by September 25, the

success rate would get a boost!

17 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 17 of 40

The Plan Is Hatched

By email: “My short-term goal is to have 20–

25 people leave by the 25th.”

“This one thing will boost our retention 4–5%.”

“A larger committee or group needs to work

on the details…

But I think you get the idea.”

“There will be some collateral damage.”

But there was a problem:

• Professors tend to develop strong bonds with their

students.

18 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 18 of 40

Mount St. Mary’s University

“This is hard for you,

because you think of

the students as

cuddly bunnies.”

“You just have to

drown the bunnies…”

19 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 19 of 40

The Collateral Damage

The president resigned from Mount St.

Mary’s University, even though he had

widespread student support for many of the

changes he had brought to the university in

the sort time he was there.

But this one incident involving a single-

minded focus on achieving a performance

metric led to his demise.

20 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 20 of 40

Other Frauds Linked to Corporate Culture

“Diesel Gate”–Volkswagen

Other automakers–emissions, etc.

Environmental claims

Product safety claims

Wells Fargo new account fraud

21 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 21 of 40

The Importance of Controls Over

Nonfinancial Reporting & Compliance

COSO 1992 COSO 2013

22 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 22 of 40

Corruption Cases

The link to the highest levels of an

organization is clearest in financial and

nonfinancial reporting frauds.

Next clearest link is with corruption schemes.

Least obvious link is with asset

misappropriations.

23 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 23 of 40

Avon China

In December 2014, Avon agrees to $135m

SEC/DOJ settlement over FCPA charges.

From 2004–2008, Avon China provided $8

million in value to government officials.

Initially identified by internal audit in 2005

Avon self-reported, but not until 2008.

24 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 24 of 40

Avon China (AC) AC executives directed IA to delete FCPA references

from the audit report, saying it “fell within purview of

Legal, and not Internal Audit.”

IA team was told to retrieve and destroy draft reports.

Avon HQ failed to instruct AC to cease the conduct

identified in the draft report.

No remedial measures were ever taken, even though

the decision was made to remediate.

In March 2006, AC adopted a “zero penalty policy,”

but it’s not what you might think!

Pay bribes to reduce or eliminate fines and to prevent

any negative media.

25 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 25 of 40

Asset Misappropriation Schemes

The least obvious link to a branch of the Fraud

Tree

Poor tone at the top often linked to

rationalization for employees who commit asset

misappropriations:

• Perceived greed of executives

• Perceived transgressions/violations perpetrated by

executives

• Perceived lack of enforcement against coworkers

• Perceived poor treatment by executives

26 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 26 of 40

COMMON THEMES IN POOR

TONES AT THE TOP

27 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 27 of 40

Is It Merely Lip Service?

91% of FTSE annual reports reference ethics and

integrity

• Only 8% provided any metrics on ethics

82% of companies surveyed have a code of ethics,

and 80% indicate that bribery was an ethical issue for

their organizations

• Only 57% have specific anti-corruption guidelines

59% have hotlines

• 26% say management views users as “trouble makers”

Sources:

• U.K.’s Chartered Institute of Internal Auditors (CICA)

• CGMA’s Managing Responsible Business – 2015 Edition

28 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 28 of 40

Signs of Toxic Corporate Culture(Tone at the Top, February 2016)

1. Favoritism

2. Walking on eggshells (constant fear of

discipline from supervisors)

3. Bad workplace behavior (competitiveness,

cliques, etc.)

4. Lack of development (no training)

5. Information hoarding by managers

6. Lack of accountability (no consequences for

ethics violations)

29 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 29 of 40

Additional Red Flags

Overly aggressive goal-setting

Pressure cooker environment for achieving

goals

One-way communication from executives

Decision-making driven by attempts to hide

problems rather than address them

The “Enron culture”

30 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 30 of 40

What Is the Enron Culture?

A focus on finding the loophole in a rule or

contract

Strategizing ways to comply with the letter

of the rule, while violating its spirit

31 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 31 of 40

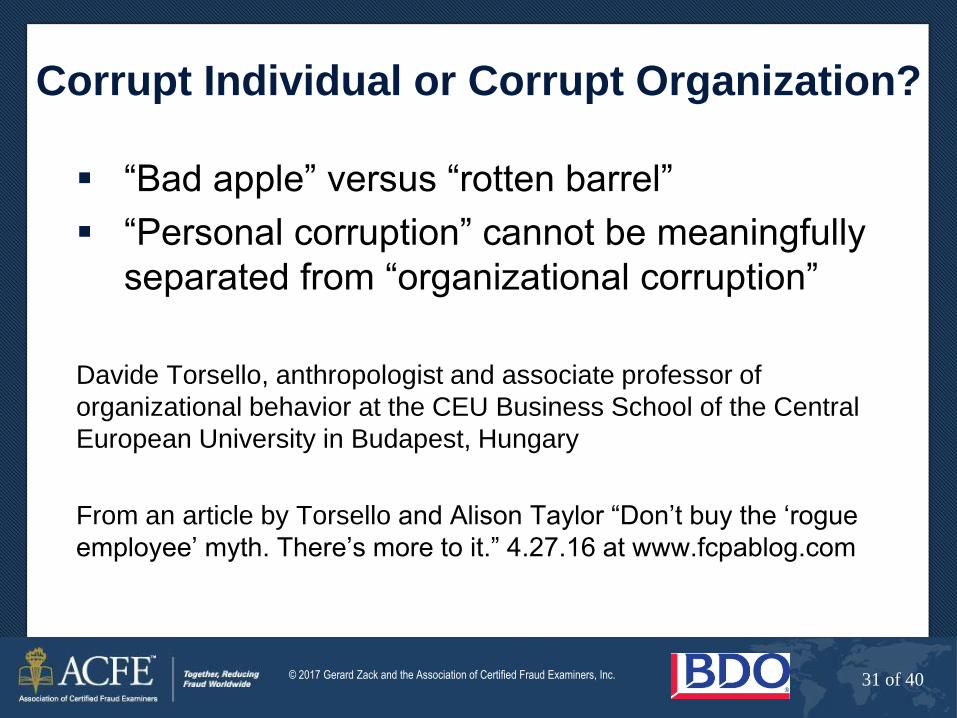

Corrupt Individual or Corrupt Organization?

“Bad apple” versus “rotten barrel”

“Personal corruption” cannot be meaningfully

separated from “organizational corruption”

Davide Torsello, anthropologist and associate professor of

organizational behavior at the CEU Business School of the Central

European University in Budapest, Hungary

From an article by Torsello and Alison Taylor “Don’t buy the ‘rogue

employee’ myth. There’s more to it.” 4.27.16 at www.fcpablog.com

32 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 32 of 40

Why Not? Five Reasons

1. Leadership–Management is responsible for

integrating employees by communicating

rules, norms, processes, etc.

2. Motivation–What cultural condition allows

unethical motivations (achieve goals no

matter how) to take precedence over

integrity?

3. Socialization–Workers spend a third of their

lives at work; work environment affects

personal vision, individual choices.

33 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 33 of 40

Why Not? Five Reasons

4. Rules and norms–Cognitive mechanisms

enable workers to accept and justify

differences between workplace and personal

norms; cognitive dissonance; rationalization.

5. Reciprocity–Is the sense of reciprocity built

towards individuals? Or is it built more

towards the organization?

34 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 34 of 40

WHAT CAN BE DONE TO

IMPROVE THINGS?

35 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 35 of 40

It Starts at the Top!

Is ethics a regular item on the board’s agenda?

• Make it an active, on-going discussion at the board

level.

Are ethics metrics tracked?

• People participating in training programs

• Surveys of employee opinions

Exec compensation linked to ethics

Consider external measures

• Dow Jones Sustainability Index

• FTSE4Good

36 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 36 of 40

Understanding Culture

Rarely is there a single culture.

Understand micro-cultures that exist due to:

• Geographic differences

• Mergers and acquisitions

• Job categories

Senior execs need to be proactive to ensure

their tone at the top is transferred to each

layer of micro-culture.

37 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 37 of 40

Enhance the “Speak Up” Line

Well communicated through the organization

Availability

Multiple languages

Provide guidance, not only a tool for reporting

Clear protocol for handling information

Confidentiality

Consistency in enforcement

Protection for providers of information

38 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 38 of 40

Managing Pressure

Pressure is a fact of doing business, but it

can be better managed.

There is no one single step to this, but rather

a series of incremental steps:

• Good two-way communication between managers

and employees

• Manager awareness of pressures on employees

• Managers not imposing their own schedules and

pressures on employees

39 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 39 of 40

Other Characteristics of Strong Culture

Managers demonstrate interest in staff well-being• Including investment in training and development of individuals

Lots of social interaction among coworkers and

between levels

Leaders provide clear guidance • Workers have a strong understanding of their roles and where the

organization is going

Workers are focused on customer needs (rather than

their own needs or those of the boss)• Focus on mission of the organization

Departments are interdependent and have high group

identification

Group participation in goal-setting

40 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 40 of 40

Questions??

My contact information

Gerry Zack, CFE, CIA, CPA

Managing Director – Global Forensics

BDO USA, LLP

Washington, DC

https://www.linkedin.com/in/gerryzack

41 of 34© 2014 Association of Certified Fraud Examiners, Inc.

© 2017 Gerard Zack and the Association of Certified Fraud Examiners, Inc. 41 of 40

Welcome!The Return of the Tone at the Top

Gerard Zack, CFE, CPA, CIA, CCEPManaging Director, Global Forensics

BDO USA, LLP