Embed Size (px)

Citation preview

Using Budgets to Achieve Organizational Objectives

Chapter 10

Resource Flexibility• For decisions affecting the short-term, the firm’s

capacity-related costs are considered as given and fixed

• The supply of capacity resources is based on the amount needed to produce the projected volume of product

• The budgeting process makes clear that some resources, once acquired, cannot be disposed of easily if demand is less than expected

The Budgeting Process

• The process that determines the planned level of most flexible costs

• Budgeting also includes discretionary spending such as for R&D, advertising, and employee training These do not supply the firm with capacity but they do

provide support for the organization’s strategy by enhancing its performance potential

Once authorized, discretionary spending budgets are committed or fixed; they do not vary with level of production or service

The Budgeting Process• Budgets serve as a control for managers within

the business units of an organization• Budgets play a central role in the relationship

between planning and control• Budgets reflect in quantitative terms how to

allocate financial resources to each part of an organization, based on the planned activities and short-run objectives of that part of the organization

The Budgeting Process

• A budget is a quantitative expression of the money inflows and outflows that reveal whether a financial plan will meet organizational objectives

• Budgeting is the process of preparing budgets• Budgets provide a way to communicate the

organization’s short-term goals to its members

The Budgeting Process

• Budgeting the activities of each unit can Reflect how well unit managers understand

the organization’s goals Provide an opportunity for the organization’s

senior planners to correct misperceptions about the organization’s goals

• Budgeting also serves to coordinate the many activities of an organization

The Budgeting Process

• Budgets help to anticipate potential problems Budgeting reflects the cash cycle and

provides information anticipate borrowing needed to finance the inventory buildup early in the cash cycle

If budget planning indicates that the organization’s sales potential exceeds its manufacturing potential, then the organization can develop a plan to put more capacity in place or to reduce planned sales

Forecasting Demandfor Resources

Budgeting involves forecasting the demand for four types of resources over different time periods:

1. Flexible resources that create variable costs

2. Intermediate-term capacity resources that create capacity-related costs

3. Resources that, in the intermediate and long run enhance the potential of the organization’s strategy

4. Long-term capacity resources that create capacity-related costs

Master Budget• Two major types of budgets comprise the

master budget: Operating budgets - summarize the level of

activities such as sales, purchasing, and production

Financial budgets - identify the expected financial consequences of the activities summarized in the operating budgets

Operating Budgets

• Sales plan - identifies the planned level of sales for each product

• Capital spending plan - specifies the long-term capital investments that must be paid in the current budget period to meet activity objectives

• Production plan - schedules all required production

• Materials purchasing plan - schedules all required purchasing activities

Operating Budgets• Labor hiring and training plan - specifies the

number of people the organization must hire or release to achieve its activity objectives

• Administrative and discretionary spending plan - includes administration, staffing, research and development, and advertising

Operating Budgets

• Operations personnel use the operating budget to guide and coordinate the level of various activities during the budget period

• Operations personnel also record data from current operations that can be used to develop future budgets

Financial Budgets• Planners prepare the financial budgets to evaluate

the financial consequences of investment, production, and sales plans

• Planners use the projected statement of cash flows in two ways: To plan when excess cash will be generated To plan how to meet any cash shortages

Demand Forecast• An organization’s goals provide the starting point

and the framework for evaluating the budgeting process

• Comparison of the tentative operating plan’s projected financial results with the organization’s financial goals

• Influence of the demand forecast

Developing the Demand Forecast• Organizations develop demand forecasts in

many ways: Market surveys Statistical models Assume that demand will either grow or decline by

some estimated rate over previous demand levels

• Require a sales plan for each key line of goods and services

Importance of Sales Plans• The sales plans provide the basis for other plans

to acquire the necessary factors of production: Labor Materials Production capacity Cash

Level of Detail in Budget

• Choosing the amount of detail to present in the budget involves making trade-offs: More detail in the forecast improves the

ability of the budgeting process to identify potential bottlenecks and problems by specifying the exact timing of production flows

Forecasting and planning in great detail for each item can be extremely expensive and overwhelming to compute

Level of Detail in Budget

• Production planners use their judgment to strike a balance between The need for detail The cost and practicality of detailed

scheduling

• Planners do this by grouping products into pools

The Production Plan

• Planners determine a production plan by matching the completed sales plan with the organization’s inventory policy and capacity level

• The plan identifies the intended production during each of the interim periods comprising the annual budget period

Inventory Policy• The inventory policy is critical and has a unique

role in shaping the production plan• One policy is to produce goods for inventory and

attempt to keep a target number of units in inventory at all times Characteristic of an organization with highly

skilled employees or equipment dedicated to producing a single product

Reflects a lack of flexibility

Inventory Policy

• An alternative policy is to produce for planned sales in the next interim period within the budget period Organizations moving toward a just-in-time inventory

policy produce goods to meet the next interim period’s demand as an intermediate step in moving to a full just-in-time inventory system

Each interim period becomes shorter and shorter until the organization achieves just-in-time production

The scheduled production is the amount required to meet the inventory target of the level of the next interim period’s planned sales

Inventory Policy• Just-in-time (JIT) inventory policy:

Demand directly drives the production plan Production in each interim period equals the

next interim period’s planned sales• JIT requires:

Flexibility among employees, equipment, and suppliers

A production process with little potential for failure

Aggregate Planning• Aggregate planning compares:

The production plan The amount of available productive capacity

• Assesses the feasibility of the proposed production plan

The Spending Plan

• Once planners identify a feasible production plan, they may make tentative resource commitments

• The purchasing group prepares a plan to acquire the required raw materials and supplies

• Since sales and production plans change, the organization and its suppliers must be able to adjust their plans quickly based on new information

The Spending Plan

• The personnel and production groups prepare the labor hiring and training plans

• When an organization is contracting, it will: Use retraining plans to redeploy employees to

other parts of the organization, or Develop plans to discharge employees

The Spending Plan• Discretionary expenditures provide the required

infrastructure for the proposed production and sales plan “Discretionary” means the actual sales and

production levels do not drive the amount spent The senior managers in the organization determine

the amount of discretionary expenditures Once determined, the amount to be spent on

discretionary activities becomes fixed for the budget period and is unaffected by product volume and mix

The Spending Plan

• A long-term planning process rather than the one-year cycle of the operating budget drives the capital spending plan Capital spending projects usually involve time

horizons longer than the period of the operating budget

Choosing Capacity Levels

Three types of resources determine capacity:

1. Flexible resources that the organization can acquire in the short term

2. Capacity resources that the organization must acquire for the intermediate term

3. Capacity resources that the organization must acquire for the long term

Choosing Capacity Levels• Organizations develop sophisticated approaches

to balance the use of short, intermediate, and long-term capacity to minimize the waste of resources

• Three types of resource-consuming activities: Activities that create the need for resources

(and resource expenditures) in the short-term Activities undertaken to acquire capacity for the

intermediate-term Activities undertaken to acquire capacity

needed for the long-term

Choosing Capacity Levels

• Analysts evaluate short-term activities by considering efficiency and asking: Is this expenditure necessary to add to the product

value perceived by customers? Can the organization improve how it does this activity? Would changing the way this activity is done provide

more satisfaction to the customer?

• The production plan fixes the short-term expenditures that the master budget summarizes

Choosing Capacity Levels• Analysts evaluate intermediate- and long-term

activities by using efficiency and effectiveness considerations and asking: Are there alternative forms of capacity available that

are less expensive? Is this the best approach to achieve our goals? How can we improve the capacity selection decision

to make capacity less expensive or more flexible?

• The capacity plan commits the firm to its intermediate and long-term expenditures

Handling Infeasible Production Plans

• Planners use forecasted demand to plan activity levels and provide required capacity

• If planners find the tentative production plan infeasible, then they have to make provisions to: Acquire more capacity, or Reduce the planned level of production

Interpreting The Production Plan• Production is the lesser of:

Total demand Production capacity

• Demand is the quantity customers are willing to buy at the stated price

• Production capacity is the minimum of: The long-term capacity The intermediate-term capacity The short-term capacity

The Financial Plans• Financial summary of the tentative operating

plans The projected balance sheet serves as an

overall evaluation of the net effect of operating and financing decisions during the budget period

The projected income statement serves as an overall test of the profitability of the proposed activities

The projected cash flow forecast helps an organization identify if and when it will require external financing

The Cash Flow Statement

The cash flow statement has three sections:

1. Cash inflows from cash sales and collections of receivables

2. Cash outflows• For flexible resources that are acquired and

consumed in the short term• For capacity resources that are acquired and

consumed in the intermediate and long term

3. Results of financing operations

Financing Operations• Summarizes the effects on cash of transactions

that are not a part of the normal operating activities

• Includes the effects of: Issuing or retiring stock or debt Buying or selling capital assets Short-term financing

Using The Financial Plans• Organizations can raise money from outsiders

by borrowing from banks, issuing debt, or selling shares of equity

• Organizations can plan the appropriate mix of external financing to minimize the long-run cost of capital

Using The Financial Plans

• A cash flow forecast helps an organization Identify if and when it will require external

financing Determine whether any projected cash

shortage will be:• Temporary or cyclical• Permanent

What If Analysis• Explore the effects of alternative marketing,

production, and selling strategies

• Alternative proposals like these can be evaluated in a what-if analysis

• The structure and information required to prepare the master budget can be used easily to provide the basis for what-if analyses

Sensitivity Analysis

• What-if analysis is only as good as the model used to represent what is being evaluated

• Planners test planning models by varying the model estimates

• If small changes in an estimate used in the production plan have a dramatic effect on the plan, the model is said to be sensitive to that estimate

Sensitivity Analysis

• Sensitivity analysis is the process of selectively varying a plan’s or a budget’s key estimates for the purpose of identifying over what range a decision option is preferred

• Sensitivity analysis enables planners to identify the estimates that are critical for the decision under consideration

Variance Analysis

Variance analysis – comparison of planned (or budgeted) results with actual results Variance analysis has many forms and can

result in complex measures, but its basis is very simple: actual cost (or revenue) amount is compared with a target cost (or revenue) amount to identify the difference

Variance Analysis

• Variance – difference between planned and actual results

• Should be investigated to determine: What caused the variance What should be done to correct that variance

Sources of Budgeted Costs• Budgeted or planned costs can come from three

sources: Standards established by industrial engineers

Previous period’s performance

A benchmark, the best in class results achieved by a competitor

Variances• The financial numbers are the product of a price

and a quantity component: Budgeted amount = expected price * expected quantity Actual amount = actual price * actual quantity

• Variance analysis explains the difference between planned and actual costs by evaluating: Differences between planned and actual prices Differences between planned and actual quantities

Variances• Accountants focus separately on prices and

quantities because in most organizations: One department or division is responsible for

the acquisition of a resource and determining the actual price

A different department uses the resource and determining the quantity

• A variance is a signal that is part of a control system for monitoring results

Variances

• Supervisory personnel use variances as an overall check on how well employees managing day-to-day operations are performing

• When compared to the performance of other organizations engaged in comparable tasks, variances show the effectiveness of the control systems that operations

Variances

• If managers learn that specific actions they took helped lower the actual costs, then they can obtain further cost savings by repeating those actions on similar jobs in the future

• If the factors causing actual costs to be higher than expected can be identified, then actions may be taken to prevent those factors from recurring in the future

• If cost changes are likely to be permanent, cost information can be updated for future jobs

First-Level Variances• The first-level variance for a cost item is the

difference between the actual costs and the master budget costs for that cost item

• Variances are favorable (F) if the actual costs are less than estimated master budget costs

• Unfavorable (U) variances arise when actual costs exceed estimated master budget costs

Planning Variances• A flexible budget adjusts the forecast in the

master budget for the difference between planned volume and actual volume

• Cost differences between the master and the flexible budget are called planning variances Reflect the difference between planned output and

actual output Arise entirely because the planned volume of activity

was not realized

Flexible Budget Variances• Flexible budget variances are the differences

between the flexible budget and the actual results• Flexible budget variances reflect:

Quantity variances -- the difference between the planned and the actual use rates per unit of output

Cost variances -- the difference between the planned and the actual price or cost per unit of the various cost items

Second & Third-Level Variances• The second-level variances are the planning

variance and the flexible budget variance

• The direct material flexible budget variances and direct labor flexible budget variances can be decomposed further into third-level variances: Efficiency variances Price variances

Direct Material Variances

• The material quantity variance is calculated as:

Quantity variance = (AQ-SQ) x SP

Where:

AQ = actual quantity of materials used

SQ = standard (estimated) quantity of materials required

SP = standard (estimated) price of materials

Direct Material Variances

• The material price variance is calculated as:

Price variance = (AP-SP) x AQ

Where:

AP = actual price of materials

SP = standard (estimated) price of materials

AQ = actual quantity of materials used

The price variance may, however, be calculated using the quantity purchased rather than the quantity used

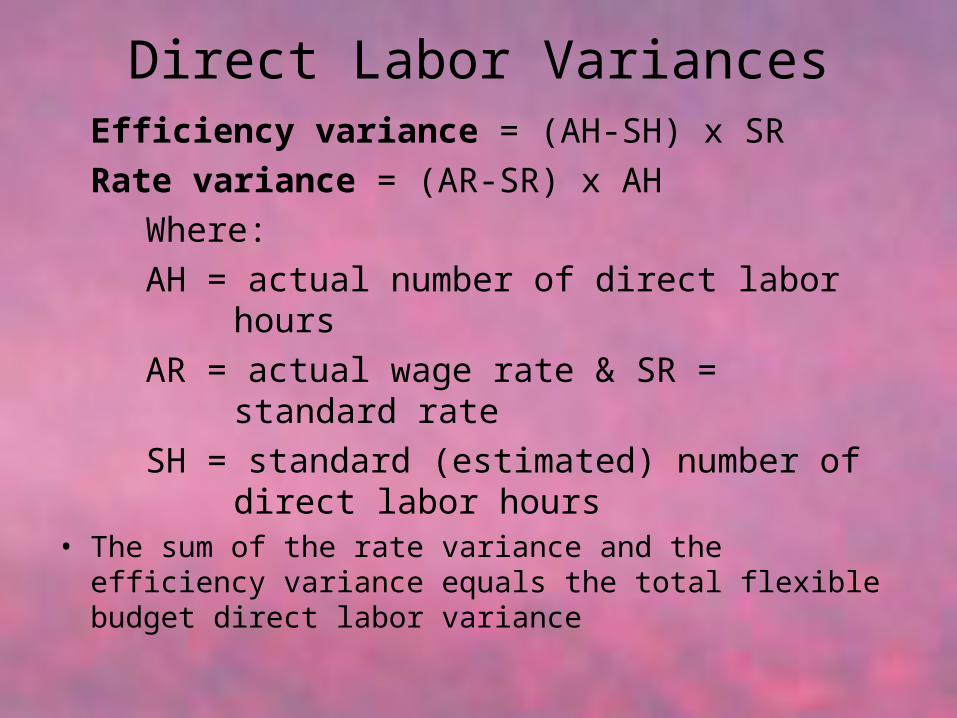

Direct Labor VariancesEfficiency variance = (AH-SH) x SR

Rate variance = (AR-SR) x AH

Where:

AH = actual number of direct labor hours

AR = actual wage rate & SR = standard rate

SH = standard (estimated) number of direct labor hours

• The sum of the rate variance and the efficiency variance equals the total flexible budget direct labor variance

Support Activity Cost Variances• Support costs can reflect either flexible or

capacity-related costs• The quantity of capacity-related costs may not

change from period to period, but the spending on them may fluctuate

• Monitoring spending variances on capacity-related resources is possible and desirable

Support Activity Cost Variances• Flexible support costs reflect behind-the-scenes

operations that are proportional to the volume of activity but are not directly a part of the product or service provided to the customer

• Flexible support costs consist of a quantity (or usage) component and a price component

• Flexible support cost variances may be analyzed in a manner similar to direct material or direct labor variances

Budgeting In Nonmanufacturing Organizations

• Budgeting helps nonmanufacturing organizations perform their planning function by coordinating and formalizing responsibilities and relationships and communicating the expected plans

• Budgeting serves a slightly different but equally relevant role in natural resource companies, service organizations, not-for-profit organizations, and government agencies

Budgeting In Nonmanufacturing Organizations

• In the natural resources sector, the focus is on balancing demand with the availability of natural resources Success requires managing the resource

base effectively to match supply with potential demand

• In the service sector, the focus is on balancing demand and the organization’s ability to provide services, which is determined by the organization’s level and mix of skills

Budgeting In Nonmanufacturing Organizations

• In not-for-profit organizations, the focus of budgeting has been to balance revenues raised by taxes or donations with spending demands

• In government agencies planned cash outflows, or spending plans, are called appropriations

Periodic Budgeting• In a periodic budget cycle, the planners prepare

budgets periodically for each planning period Periodic budgeting is typically performed once

per budget period—usually once a year Planners may, however, update or revise the

budgets

Continuous Budgeting• In continuous budgeting, as one budget period

passes, planners drop that budget period from the master budget and add a future budget period in its place

• The length of the budget period reflects the competitive forces, skill requirements, and technology changes that the organization faces

Periodic v. Continuous Budgeting• Advocates of periodic budgeting argue that

continuous budgeting takes too much time and effort and that periodic budgeting provides virtually the same benefits at a smaller cost

• Advocates of continuous budgeting argue that it keeps the organization planning, and assessing, and thinking, strategically year-round rather than just once a year at budget time

Controlling Discretionary Expenditures

• Organizations generally use one of three general approaches to budget discretionary expenditures: Incremental budgeting Zero-based budgeting Project funding

• Each has benefits distinct from the others

Incremental Budgeting• Incremental budgeting bases a period’s

expenditure level on the amount spent during the previous period

• If the total budget for discretionary items increases by 10%, then: Each discretionary item is allowed to increase

10%, or All items may experience an across-the-board

increase of, for example, 5% and the remaining 5% increase may be allocated based on merit

Zero-Based Budgeting (1 of 2)

• Zero-based budgeting (ZBB) requires that proponents of discretionary expenditures continuously justify every expenditure

• The starting point for each line item is zero• Zero-based budgeting arose, in part, to combat

indiscriminate incremental budgets where projects that take on a life of their own and resist going out of existence

Zero-Based Budgeting

• Organization’s resources are allocated to the spending proposals they think will best achieve the organization’s goals

• Used primarily to assess government expenditures• In profit-seeking organizations, ZBB has been

applied only to discretionary expenditures• For engineered costs, ZBB could be effective

when combined with the reengineering approach

Project Funding• Project funding – intermediate solution to mitigate

the disadvantages of ZBB and incremental budgeting A proposal is made for discretionary expenditures with a

specific time horizon or sunset provision Projects with indefinite lives (sometimes called

programs) should be continuously reviewed to ensure that they are living up to their intended purposes

Requests to extend or modify the project must be approved separately

Activity-Based Budgeting• Activity-based budgeting - based on activity-

based costing• Uses knowledge about the relationship between

the quantity of production units and the activities required to produce those units to develop detailed estimates of activity requirements underlying the proposed production plan

• Two main benefits of activity-based budgeting: Identifies situations when production plans

require new capacity Provides a more accurate way to project

future costs

Managing the Budgeting Process

• Many organizations use a budget team, headed by the organization’s budget director or the controller, to coordinate the budgeting process

• The budget team usually reports to a budget committee, which generally includes the chief executive officer, the chief operating officer, and the senior executive vice presidents

• The composition of the budget committee reflects the role of the budget as the planning document that reflects and relates to the organization’s strategy and objectives

Managing the Budgeting Process• Using a budget committee may signal to other

employees that budgeting is something that is relevant only for senior management

• Senior management must take steps to ensure that the organization members affected by the budget do not perceive the budget and the budgeting process as something beyond their control or responsibility

Behavioral Aspects of Budgeting• Because of the human factor involved in the

process, budgets often do not develop smoothly

• Two related areas are of particular importance with respect to the behavioral issues: Designing the budget process Influencing the budget process

Designing the Budget

• How should budgets be determined and who should be involved in the budgeting process?

• Three common methods of setting budgets: Authoritarian - superior simply tells subordinates what

their budget will be Participation - all parties agree about setting the

budget targets, using a joint decision-making process Consultation - managers ask subordinates to discuss

their ideas about the budget but determine the final budget alone

Designing the Budget (2 of 2)

• Research shows that the most motivating types of budgets are those that are tight With targets that are perceived as ambitious but

attainable

• Recently, some companies have implemented what are known as stretch targets Stretch targets exceed previous targets by a

significant amount and usually require an enormous increase in a goal over the next budgeting period

The theory is that only in this manner will companies completely reevaluate the ways in which they develop and produce products and services

Influencing The Budget Process• When incentives and compensation are tied to

the budget, some managers have been known to play budgeting games in which they attempt to manipulate information and targets to achieve as high a bonus as possible (or the best evaluation)

• Participation provides employees the opportunity to affect their budgets in ways that may not always be in the best interests of the organization

Budget Slack• Budget slack is created by requiring excess

resources or distorting performance information• If subordinates succeed in creating budget

slack, they will find it easy to meet or exceed their budgeted objectives

• Budgeting games can never be eliminated, although some organizations have devised methods to decrease the amount of budget slack