Embed Size (px)

Citation preview

USAGE OF MOBILE BANKING AND ITS EFFECTS ON

CONSUMER BEHAVIOR IN THAILAND

BY

MR. CHANA SILPARCHA

AN INDEPENDENT STUDY SUBMITTED IN PARTIAL

FULFILLMENT OF

THE REQUIREMENTS FOR THE DEGREE OF

MASTER OF SCIENCE PROGRAM IN MARKETING

(INTERNATIONAL PROGRAM)

FACULTY OF COMMERCE AND ACCOUNTANCY

THAMMASAT UNIVERSITY

ACADEMIC YEAR 2017

COPYRIGHT OF THAMMASAT UNIVERSITY

Ref. code: 25605902040087AGC

USAGE OF MOBILE BANKING AND ITS EFFECTS ON

CONSUMER BEHAVIOR IN THAILAND

BY

MR. CHANA SILPARCHA

AN INDEPENDENT STUDY SUBMITTED IN PARTIAL

FULFILLMENT OF

THE REQUIREMENTS FOR THE DEGREE OF

MASTER OF SCIENCE PROGRAM IN MARKETING

(INTERNATIONAL PROGRAM)

FACULTY OF COMMERCE AND ACCOUNTANCY

THAMMASAT UNIVERSITY

ACADEMIC YEAR 2017

COPYRIGHT OF THAMMASAT UNIVERSITY

Ref. code: 25605902040087AGC

(1)

Independent Study Title USAGE OF MOBILE BANKING AND ITS

EFFECTS ON CONSUMER BEHAVIOR IN

THAILAND

Author Mr. Chana Silparcha

Degree Master of Science Program in Marketing

(International Program)

Major Field/Faculty/University Faculty of Commerce and Accountancy

Thammasat University

Independent Study Advisor Associate Professor Kenneth E. Miller, Ph.D.

Academic Year 2017

ABSTRACT

“What is the first thing you do when you wake up in the morning?” it

is highly likely that the answer is you looked at your smartphone. In 2016, Deloitte

conducted a global mobile consumer survey and discovered that 61 percent of people

check their phones within 5 minutes after waking up. Dubbed “the most innovative

invention in the 21st century”, smartphones impacted our lives in many ways and

revolutionized multiple industries. One of the industries disrupted is the banking

industry as mobile banking empowered us to conduct banking activities anywhere at

any time through the comfort of our smartphones. Similar to other ASEAN countries,

Thailand experienced exponential growth in usage of mobile banking as a result of e-

commerce expansion and improved e-payment infrastructure.

Ref. code: 25605902040087AGC

(2)

Although studies on the underlying factors that influence mobile banking

adoption has been extensively conducted, research to examine after-adoption behavior

has been neglected. Thus, this research captures the current situation of mobile

banking in Thailand and categorizes mobile banking users into different segments.

Banks and government sectors alike will benefit from this comprehensive research as

they can apply insights to generate suitable products for banking customers and

develop Thailand’s electronic payment infrastructure.

Secondary research from multiple journals and academic articles has been

collected to gain fundamental background knowledge. Later, primary research through

in-depth interviews and an online survey was conducted; statistical analysis was

performed with the help of Statistical Package for the Social Sciences (SPSS)

program.

Results show the majority of respondents likely have a positive perception

towards mobile banking. Furthermore, findings suggest that Thai mobile banking

users can be categorized into 3 segments. The largest segment is made up of heavy

users called “Middle Aged Go-Getter” who seek mobile banking application

reliability and useful features. Another heavy user called “Youthful Minimalist”

values application ease of use and convenience. Finally, “Old School Veterans” are

lights users whose service adoption heavily relies on recommendation from peers and

online reviews.

With the above findings it is recommended that commercial banks should

consistently improve the performance and user friendliness of mobile banking

applications in order to increase usage frequency among current heavy user segments.

In addition, an untapped opportunity with the older user segment is ripe. Commercial

banks need to educate and increase service adoption rate in order to reach the tipping

point.

Keywords: mobile banking, Thai mobile banking user behavior, Thai mobile banking

user segment

Ref. code: 25605902040087AGC

(3)

ACKNOWLEDGEMENTS

I would like to express the highest gratitude to my advisor, Professor

Kenneth E. Miller, Ph.D., for his continuous guidance and valuable feedback. His

enormous input and support largely contributed to the success of this research.

Furthermore, I would like to thank all interviewees, respondents, friends

and family members who gave me endless support of throughout the research. Also, a

special thanks to Ms. Thanyathorn Pattana-Amorn who was kind enough to give

consultation and constructive feedback on this report.

Mr.Chana Silparcha

Ref. code: 25605902040087AGC

(4)

TABLE OF CONTENTS

Page

ABSTRACT (1)

ACKNOWLEDGEMENTS (3)

LIST OF TABLES (7)

LIST OF FIGURES (8)

CHAPTER 1 INTRODUCTION 1

1.1 Research Purpose 1

1.2 Research Objectives 1

CHAPTER 2 REVIEW OF LITERATURE 3

2.1 Definition of Mobile Banking 3

2.1.1 Positive Impacts of Mobile Banking 4

2.1.2 Negative Impacts of Mobile Banking 5

2.2 Mobile Banking in South East Asia (ASEAN) 5

2.2.1 Mobile Banking Adoption 5

2.2.2 Mobile Banking Penetration 6

2.3 Mobile Banking in Thailand 7

2.3.1 Mobile Banking Trends 9

2.3.2 Challenges of Mobile Banking Adoption 10

CHAPTER 3 RESEARCH METHODOLOGY 11

3.1 Exploratory Research Design 11

3.1.1 Secondary Data Research 11

Ref. code: 25605902040087AGC

(5)

3.1.2 In-depth Interview 12

3.2 Descriptive Research Design 12

3.2.1 Survey Questionnaire 12

3.3 Sampling Plan 13

3.3.1 Sample Selection Criteria 13

3.3.2 Recruiting Plan 13

3.3.3 Data Analysis Plan 14

CHAPTER 4 RESULTS AND DISCUSSION 15 4.1 In-depth Interview Analysis 15

4.2 Survey Result Analysis 16

4.2.1 Respondent Profile 16

4.2.2 Mobile Banking Awareness and Usage 18

4.2.3 Segmentation 20

CHAPTER 5 CONCLUSIONS AND RECOMMENDATIONS 23 5.1 Conclusions and Managerial Implications 23

5.1.1 Managerial Implication for Commercial Banks 23

5.2 Research Limitations 24

5.3 Suggestions for future studies 24

REFERENCES 26

APPENDICES

APPENDIX A: In-depth Interview Guideline 32

APPENDIX B: Example of Questionnaire 34

APPENDIX C: Respondent Demographic 38

APPENDIX D: Frequency Analysis - Perception 39

APPENDIX E: Attributes Correlation 40

Ref. code: 25605902040087AGC

(6)

APPENDIX F: Factor Analysis 41

APPENDIX G: Cluster Analysis 42

APPENDIX H: Cluster Analysis with Respondent Perception 43

BIOGRAPHY 45

Ref. code: 25605902040087AGC

(7)

LIST OF TABLES Tables Page

Table 4.1: Respondent’s perception towards mobile banking based 17

on 4 level Likert scale frequency analysis

Table 4.4: Correlation between “Security & Reliability” and 20

“Recommendation from peers & Online reviews”

Table 4.5: Results from cluster analysis with respondent’s perception 22

Table 4.6: Anova results from cluster analysis with respondent’s perception 22

Ref. code: 25605902040087AGC

(8)

LIST OF FIGURES Figures Page

Figure 2.2: Digital banking penetration in SEA (%) 6

Figure 2.3: Overview of financial digitization in Thailand 8

Figure 4.2: Top 3 mobile banking brand conversion rate 18

Figure 4.3: Top 3 mobile banking service conversion rate 19

Figure 4.5: Heavy and light user cluster analysis 21

Ref. code: 25605902040087AGC

1

CHAPTER 1

INTRODUCTION

1.1 Research Purpose

The purpose of this research is to study Thai users’ mobile banking behavior

and identify various user segments. This research is beneficial to commercial banks,

non-bank players (eg. E-wallet companies) as well as the government sector

responsible for shaping digital banking policy. This study is a contemporary topic in

applied marketing

1.2 Research Objectives

The first objective of this study is to determine the current users of mobile

banking as well as their usage patterns and overall trends. Consequently, the second

objective is to categorize mobile banking users into different segments. Lastly, this

study will identify whether there is a change in consumer behavior for each segment.

The sub-objectives of this study are as follows:

Ø To identify awareness and usage among current mobile banking users

• To identify mobile banking usage frequency

• To identify service awareness

Ø To categorize behavior of current mobile banking users

• To determine behavior in usage purpose

• To determine importance of available services that drive usage

• To determine usage occasion

• To determine average transaction amount

Ref. code: 25605902040087AGC

2

Ø To identify mobile banking user segment

• To explore demographic profile, lifestyle and behavior of each

user segment

• To identify mobile banking needs of each segment

Ø To identify any changes in consumer behavior influenced by mobile banking

Key variables of this study are 1) Mobile banking users’ characteristics such as

age, income, education and occupation 2) Consumer behaviors such as: service

awareness relative to usage rate, service usage frequency relative to branch banking,

purpose of usage, average amount per transaction 3) Psychographic variables such as

personalities, lifestyles, interests, opinions and social class.

Secondary and primary data was collected from both qualitative and

quantitative methodologies. Target respondents are Thais between the age of 15- 54

years old who are current users of mobile banking services.

Ref. code: 25605902040087AGC

3

CHAPTER 2

REVIEW OF LITERATURE

2.1 Definition of Mobile Banking

Banks around the world are currently interacting with their customers through

multiple channels such as Automated Teller Machines (ATMs), branch banking,

telephone banking, internet banking and mobile banking. (Hoehle, 2012) claimed that

customers select branch banking for complex product categories (e.g. mortgages and

loans) and select mobile banking for simple operations (e.g. bill payment and fund

transfer.)

Mobile-banking or commonly referred to as “M-Banking” is an extension of

internet banking which offers financial services such as balance checking, fund

transfer, stock market transactions, bill payments and top up (Munongo, 2013). Banks

are encouraging customers to adopt mobile banking with the goal of improving

customer relationship management, reducing operational costs and utilizing analytics

to enhance cross-selling (Laukkanen, 2007). Mobile devices applicable for mobile

banking usage includes smart-phone, personal digital assistant devices (PDAs),

wireless tablets and any other devices that can connect to mobile telecommunication

networks (Deshwal, Dr. Parul, 2015).

In recent years, numerous comprehensive research was conducted to determine

the underlying factors that influence mobile banking adoption. (Carlos T., 2017)

highlighted these factors as perceived usefulness, perceived ease of use, perceived

risk, trust, social influence and self-efficacy.

Ref. code: 25605902040087AGC

4

Regarding factors that undermine the growth of mobile banking, (P. Dupas,

2012) identified security and privacy issues as the two biggest challenges for

consumers to adopt mobile banking. However, these two factors prove to be

insignificant among younger banking customers as (Rammile, 2012) argued that

university students do not consider mobile banking to be prone to risk if operated with

caution. The reason being younger consumers are generally more familiar with the use

of mobile technology thus perceived benefits outweighs perceived risks.

As mobile banking systems become more prevalent throughout the world,

businesses and consumers alike, look forward to how it would revolutionize the

banking industry. However, it is crucial to recognize what this revolution means and

understand both sides of the coin to gain a larger perspective of its implications.

2.1.1 Positive Impacts of Mobile Banking

Cost Reduction: Fundamentally, mobile banking enables banks to provide

services to more customers anywhere at any time at minimal costs. In a

comprehensive report, (Deloitte, 2010) claim that banks can significantly cut

operational costs with mobile banking as branch banking is approximately 50 times

more costly.

Revenue Expansion: (David T., 2013) noted that through mobile banking,

banks are able to collect vast amounts of data and monetize the value of each

customer through big data analytics. Banks will be equipped with insights to enhance

customer satisfaction and improve prospects of acquiring new customers, thus

generating more revenue.

Ref. code: 25605902040087AGC

5

Enhance customer satisfaction: As mentioned above, utilizing mobile

banking as a channel for important reminders can significantly increase customer

satisfaction. Banking customers will be better informed about outstanding loan

repayments as well as payment of monthly installments. Moreover, banking customers

are provided with real-time updates of their account balance which allows them to be

more flexible when conducting transactions. Lastly, mobile banking can reduce the

risk of credit card fraud by keeping card holders well informed about the purchase

amount for each credit card transaction (Deshwal, Dr. Parul, 2015).

2.1.2 Negative Impact of Mobile Banking

Risk of Security Threats: The number one concern for mobile banking users

is the security of data transmission and user privacy. IBM security expert (Charles,

2017) advise mobile banking users to protect their smart-phones carefully as you

would protect your desktop or personal computers. This is because there is a

possibility that mobile devices can become a victim of targeted malware which may

consist of viruses, Trojan and spyware. Moreover, it is advised that users do not use

mobile banking applications when they are connected to unsecured Wi-Fi networks

such as public Wi-Fi. Hackers can breach the network and gain access to your

unencrypted transactions.

2.2 Mobile Banking in South East Asia (ASEAN)

2.2.1 Mobile Banking Adoption

The evolution of digital banking in ASEAN can be traced back to the

introduction of ATMs (Automated Teller Machine) in the 1980s. Subsequently, in the

Ref. code: 25605902040087AGC

6

1990s internet banking became more common among affluent desktop and personal

computer owners (DBS Group Research, 2015). In spite of internet banking popularity

in developed Asian countries, the biggest limitation to internet banking is the

requirement of desktop or personal computer computers which were relatively

expensive and inaccessible to many ASEAN citizens at that time.

Interestingly, unlike other developed Asian countries, the majority of ASEAN

countries did not adopt internet banking and later migrated to mobile banking as

ASEAN citizens tend to use smartphones as their primary channel to connect with the

internet. Further fueling the development of mobile banking in ASEAN is the

advancement in broadband cellular network technology and the smartphone

technology.

2.2.2 Mobile Banking Penetration

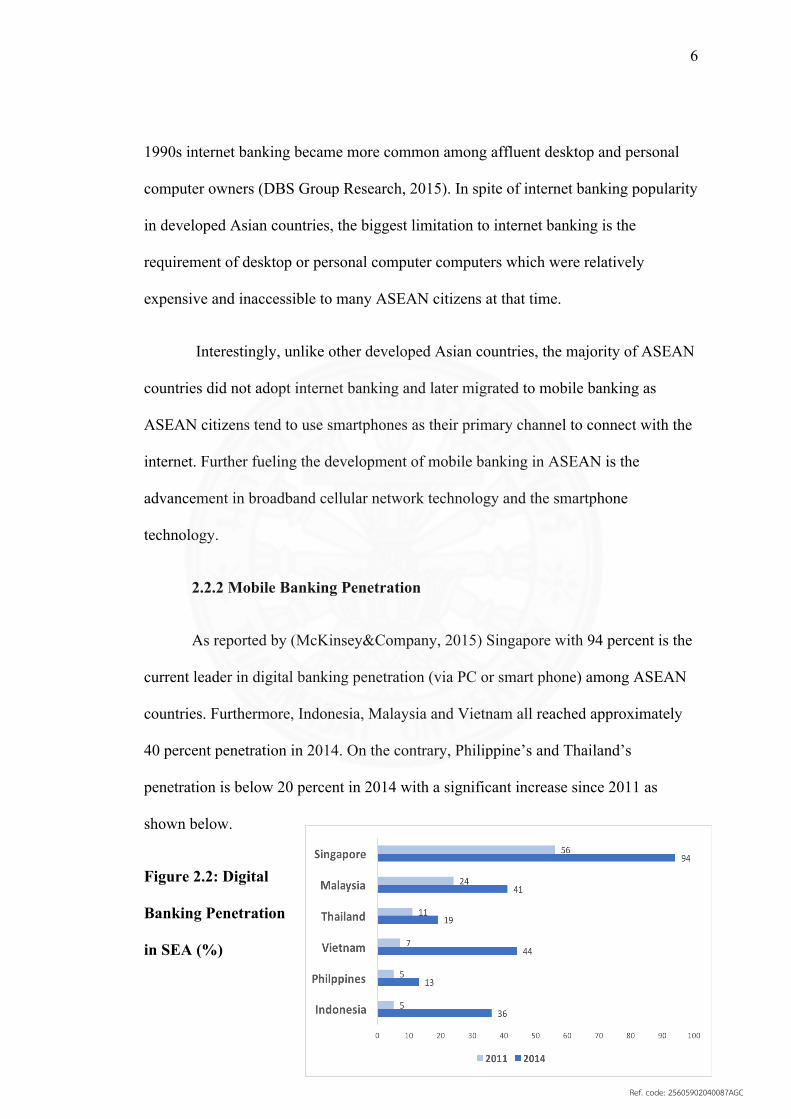

As reported by (McKinsey&Company, 2015) Singapore with 94 percent is the

current leader in digital banking penetration (via PC or smart phone) among ASEAN

countries. Furthermore, Indonesia, Malaysia and Vietnam all reached approximately

40 percent penetration in 2014. On the contrary, Philippine’s and Thailand’s

penetration is below 20 percent in 2014 with a significant increase since 2011 as

shown below.

Figure 2.2: Digital

Banking Penetration

in SEA (%)

Ref. code: 25605902040087AGC

7

Moreover, with the exception of Singapore where digital banking penetration

was high in all income segments and age groups, the young and affluent segments are

the early adopters and users of digital banking in ASEAN.

These statistics show that there is a major shift in ASEAN banking industry

which represents an opportunity for both existing banks and new entrants alike.

Existing banks can utilize advanced analytics to leverage existing data to promote

stronger customer satisfaction and solidifying their strong position. On the other hand,

new entrants can solely focus on developing digital capabilities and save costs

establishing expensive branch banking networks (McKinsey&Company, 2015).

2.3 Mobile Banking in Thailand

Thailand is experiencing a rapid increase in smartphone subscription as well

as mobile banking users. According to the (Bangkok Post, 2016) Thailand’s

smartphone subscription is expected to reach 80 million by 2021.

Additionally, Thailand experienced exponential growth in the number of

mobile banking users, number of transactions as well as the value of transactions

between 2011 and 2015. With a CAGR of 81 percent, the number of new mobile

banking users grew from 706,439 to 13,918,815. In accordance to the increasing

number of mobile banking users, the number of transactions also increased

significantly at 67 percent CAGR. Lastly, the value of transactions grew from 187

billion Thai baht to 2,800 billion Thai baht (Bank of Thailand, 2017). The most up to

date info graphic of Thailand’s overall financial digitization is provided in Figure 2.3

below.

Ref. code: 25605902040087AGC

8

Figure 2.3: Overview of Financial Digitization in Thailand (Source: Bangkok Post)

According to (The Nation, 2016), the number of mobile banking transactions

is continuously outgrowing the number of branch banking transactions. This

represents the digitization of banking in Thailand. Despite the fact that mobile

banking transaction value is only a portion of the total financial technology (fin-tech)

market, according to (Statista, 2017) the transaction value of the Thai fin-tech market

would reach US$23,434 million in 2021, with a projected CAGR of 19 percent.

As one of segments of the Thailand 4.0 initiative, the Thai government aims to

digitize Thailand’s payment infrastructure and transform Thailand into a cashless

society. Thailand E-Payment Trade Association (TEPA) believed that Thailand is on

track to become a cashless society by 2020 (The Nation, 2017). A compelling

indicator of this milestone can be observed from the newly launched “Prompt Pay”

under the national e-payment program. By the end of 2016, 48 percent of all

employees in Thailand registered to the Prompt Pay program (Kasikorn Research,

2017). It can be said that the Prompt Pay program established a new standard for all

banks to accept lower transfer fees in order to reap other benefits in the long run.

Ref. code: 25605902040087AGC

9

Download statistics from Apple’s App store and Google’s Play Store in 2016

identified, the top 3 mobile banking applications to be K Plus at 41 percent (Kasikorn

Bank), SCB Easy at 12 percent (Siam Commercial Bank) and Bualuang mBanking at

12 percent (Bangkok Bank.) Besides standard services such as balance checking and

money transfer, tech-savvy banks such as Kasikorn Bank and Siam Commercial Bank

also offer extended services such as credit card details and mutual fund purchase via

mobile banking. Notably, telecommunication companies such as True Corporation

and AIS (Advance Info Service) are also emerging as competitors in the mobile

banking market.

2.3.1 Mobile Banking Trends in Thailand

Decreased Dependency on Cash: (Nielsen, 2014) conducted a “Global

Survey of Saving and Investment Strategies” and discovered that 68 percent of Thai’s

preferred form of payment is cash. However, in recent years there has been a decline

in cash dependency as younger generation of Thais become more familiar to cashless

payments through various e-payment channels and mobile banking. Additionally,

Kasikorn and Siam Commercial Bank recently introduced “QR Code Payment” which

will reduce transaction friction between buyers and sellers in the retail sector.

Small and Medium-sized Enterprise (SME) Mobile Banking: As Thailand

has the biggest SME lending volume among ASEAN countries (Deloiotte, 2015), it is

conceivable that multiple banks are trying to capture this large and emerging market

segment. Currently, Kasikorn Bank and Siam Commercial Bank are the only two

banks offering specialized mobile banking services for the SME segment.

Ref. code: 25605902040087AGC

10

2.3.2 Challenges of Mobile Banking Adoption in Thailand

Adoption Hurdle: Comparable to other ASEAN countries, security and trust

remains a big challenge for mobile banking adoption and usage in Thailand. Based on

an empirical study on mobile banking by (XinLuo, 2010) banks must create more

awareness regarding the benefits of mobile banking, while simultaneously, increase

institutional trust as both factors can increase the adoption rate.

Regulatory Challenges: Although some may argue that the government’s

introduction of “Prompt Pay” program gained modest success, others are anticipating

forthcoming programs such as e-tax payment and overall development in Thailand’s

payment infrastructure. Furthermore, unlike other developed countries in Asia, there

are no incentive schemes implemented to promote e-payments in Thailand. These

schemes may introduce higher VAT rates for cash purchases and reduced tax rates for

e-payment users (SCB Economic Intelligence Center, 2016).

Throughout the literature review a clear definition of mobile banking has been

defined. In addition, the advantages such as cost reduction and disadvantages such as

security risks has been highlighted. Compared to other neighboring countries,

Thailand’s mobile banking penetration is relatively low, nevertheless, there is 1.7

times growth since 2011. This growth will likely continue in accordance with rising

smartphone penetration and introduction of new electronic payment systems

(McKinsey&Company, 2015)

Ref. code: 25605902040087AGC

11

CHAPTER 3

RESEARCH METHODOLOGY

3.1 Exploratory Research Design

Qualitative and quantitative methodologies have been used for this research.

With the intention to identify user behavior, awareness and usage frequency, the

research was conducted with exploratory research design and descriptive research

design. Findings from exploratory research was later used as a basis to develop an

online questionnaire.

3.1.1 Secondary Data Research

Secondary data research was used to gather background information regarding

current mobile banking usage rate and mobile banking services offered by Thai

commercial banks. Information from reliable online sources such as Thai Bankers

Association (TBA), Bank of Thailand (BOT) and Thailand Board of Investment (BOI)

databases were also collected to statically pinpoint Thailand’s mobile banking

advancement. Multiple academic journals were studied to gain a better understanding

of mobile banking definition, implications and future trends. Additionally, journals

and online articles from leading consultancies such as Deloitte, McKinsiey&Co. and

Kasikorn Research Center served as reliable sources to determine the global mobile

banking landscape and its market potential.

Ref. code: 25605902040087AGC

12

3.1.2 In-depth Interview

In order to validate and explore the findings from secondary research, a total of

10 in-depth interviews was conducted from November 8, 2017 to December 1, 2017.

The interview length varies from 30 minutes to 1 hour. Each respondent discussed

their current mobile banking usage behaviors, past positive and negative experiences

and ranked attributes they value most in a mobile banking application. A moderator

conducted the all interviews according to predesigned guidelines to make respondents

feel more comfortable, resulting in more insightful responses.

3.2 Descriptive Research Design

Descriptive research design played an important role in systematically

describing the facts and characteristics of a given population of interest. The purpose

of descriptive research was to describe characteristics of Thai mobile banking user’s

behavior and preferences.

3.2.1. Survey Questionnaire

An online questionnaire was constructed to collect information from the target

population to describe commonalities and differences. It consists of five sections,

namely, screening, awareness, usage behavior, perception and demographic. After

respondents qualify as a current mobile banking user within the right age group,

respondents were asked about their mobile banking brand and services awareness.

Next, mobile banking behaviors such as frequency, usage date & time and average

transaction amount was inquired. Later on, respondents had to rank important mobile

banking attributes. In conjunction with the demographic section, the above sections

were used to segment current users and define users profile. Various social media

Ref. code: 25605902040087AGC

13

outlets such as Line application and Facebook was used and a total of 200 completed

questionnaires was obtained. Questionnaire sample is displayed in Appendix B.

3.3 Sampling Plan

A total of ten people was recruited for the in-depth interview and 240

respondents answered the online questionnaire. Prior to the questionnaire launch, five

pilot tests were conducted to ensure understandability of the questionnaire and the

amount of time required for completion.

3.3.1 Sample Selection Criteria

Ø Gender: Both male and female

Ø Age: 15-54 years’ old

Ø All Socio-Economics Status

Ø Current mobile banking user (last usage not exceeding 3 months)

3.3.2 Recruiting plan

Due to time constraints, non-probability convenience sample was applied for

all in-depth interviews and online surveys. All respondents were recruited through

personal contacts. Screening questions were applied in order to qualify whether the

respondent is a current mobile banking user within the right age group. Target

respondents group were 1) Teenagers 2) Working Adults 3) Retirees.

Ref. code: 25605902040087AGC

14

3.3.2 Data Analysis Plan

The analysis focused on the result from both qualitative and quantitative

methods. Qualitative data was transcribed with the reduction method while preserving

respondent’s verbatim. The data was used to investigate usage behavior and

perception towards mobile banking. The transcription data was used to gain a better

understanding of consumer language and explore further insights. Regarding

quantitative survey, Statistical Package for Social Sciences (SPSS) was employed to

initially run frequencies, forming a big picture of the data set. Subsequently

correlations between variables was identified and factor analysis was conducted.

Finally cluster analysis was used to conduct segmentation of mobile banking users.

Ref. code: 25605902040087AGC

15

CHAPTER 4

RESULTS AND DISCUSSION

4.1 In-Depth Interview Analysis

A total of 10 in-depth interviews was conducted to identify current mobile

banking user behavior and to investigate user’s perception toward mobile banking

application. Diverse responses were collected from teenagers (aged 17 and 21 and 22),

young adults (aged 25 and 28 and 29), working adults (aged 39 and 42) and retirees

(aged 64 and 67). All interviewees are Thai and each age group consisted of at least

one male and one female respondent. With the exception of retirees who were aware

of mobile banking applications but never used it, every other age group are current

mobile banking users.

In terms of usage frequency, 5 out of 8 teenagers, young adults and working

adults use mobile banking applications up to 5 times a week. Interestingly, 4

respondents out of 10, use mobile banking multiple times a day to check account

balance, split the bill when eating out with friends and making QR code payment to

various vendors. For young and working adults, mobile banking applications serves as

a tool for both work related transactions as well as personal activities. This indicates a

potential growth trend of online-based entrepreneurs that heavily rely on money

transfer from e-commerce transactions. Furthermore, all young and working adult

respondents prefer to use mobile banking over branch banking as it saves time and

money. On the contrary, the male retiree respondent expressed “I am not familiar with

applications on smartphones, let alone trust it to transfer my money. All my retirement

Ref. code: 25605902040087AGC

16

collectables are made directly to my accounts and none of my friends use it so I don’t

use it either.”

As highlighted above, with the exception of retirees, all other age group

express positive perception towards mobile banking. Moreover, it is also useful in

emergencies as the male working adult respondent disclosed “My aunt who was living

outside of Bangkok urgently needed money to undergo a medical procedure in the

middle of the night and mobile banking truly helped me.” Despite this, 4 out of 10

respondents raised concerns for functionality of some mobile banking applications as

they experienced minor malfunctions in the past. As for the female retiree, the most

pressing concerns were security risks followed by user friendliness “Although I agree

that mobile banking provides advantages, but I just don’t know where to start.”

4.2 Survey Result Analysis

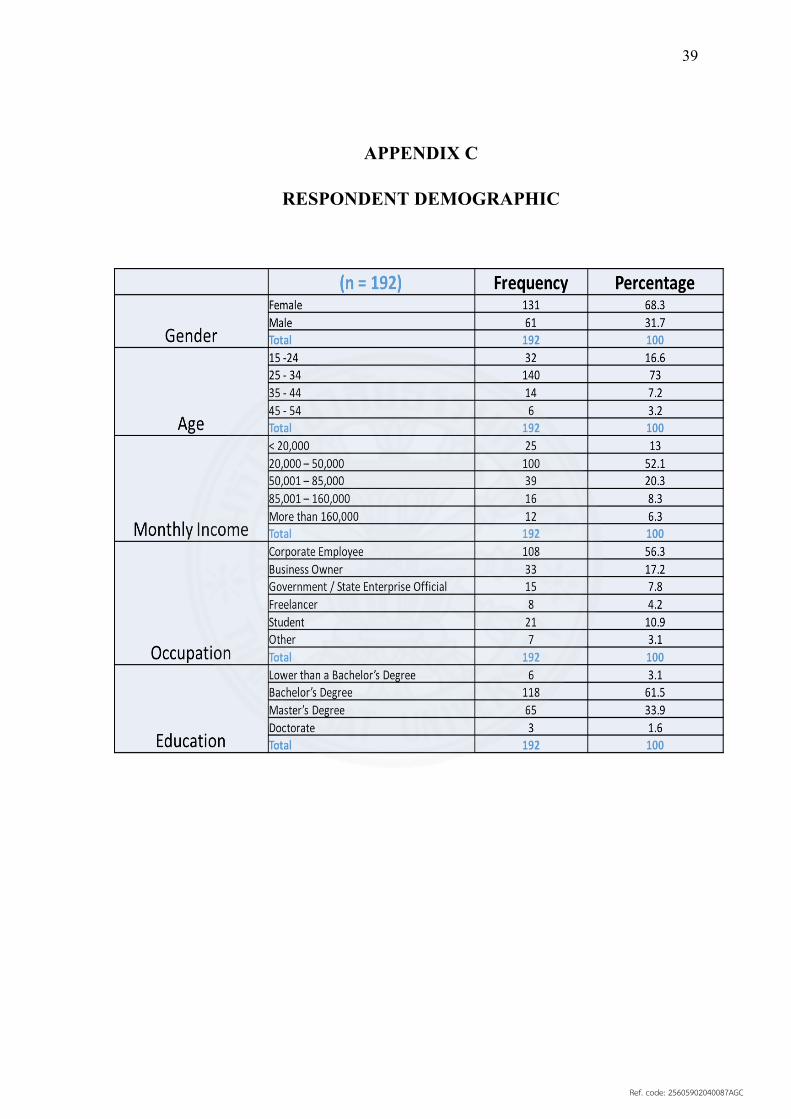

4.2.1 Respondent Profile

With 240 completed surveys, 192 surveys qualified the screening process. 94

percent of all respondents are smartphone owners who have at least one mobile

banking application installed on their smartphone. The demographic of the 192

qualified respondents are 68 percent female, 95 percent either have a bachelor or a

master’s degree. 73 percent is made up of corporate employee or business owners with

50 percent monthly income of 20,000-50,000. Only respondents aged 15-54 years old

were included in the research, representing 60 percent of the the Thai population

(Index Mundi, 2018). See appendix C for Respondent’s Demographic Profile.

Ref. code: 25605902040087AGC

17

Regarding mobile banking usage behavior, usage peaks hours are during

evening times with 42 percent. In addition, 56 percent of the average mobile banking

transaction per usage is below 5,000 THB and 70 percent of respondents use mobile

banking applications on both weekdays and weekends. Furthermore, 79 percent of

respondents have used mobile banking within the past week. This classifies them as

heavy users because the majority of them use mobile banking several times per week.

On the other hand, the remaining 21 percent of respondents are regarded as light users

that use mobile banking application a few times per month. Heavy and light users will

be used for further factor and cluster analysis.

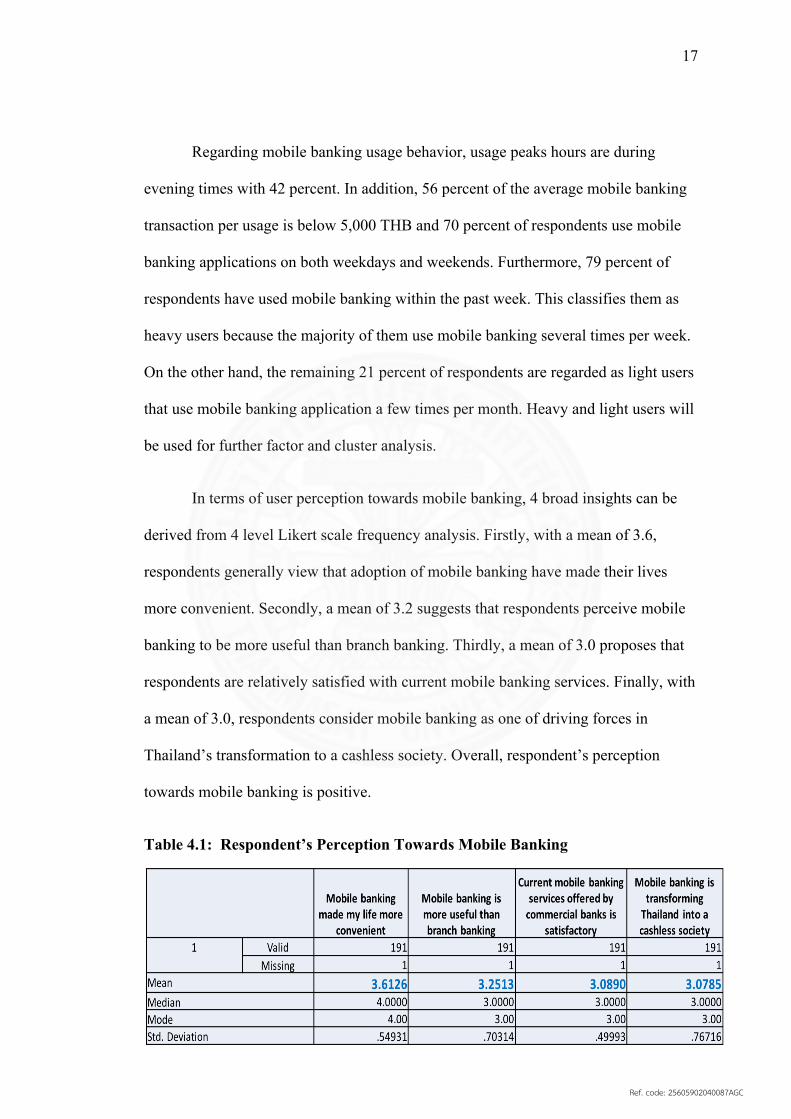

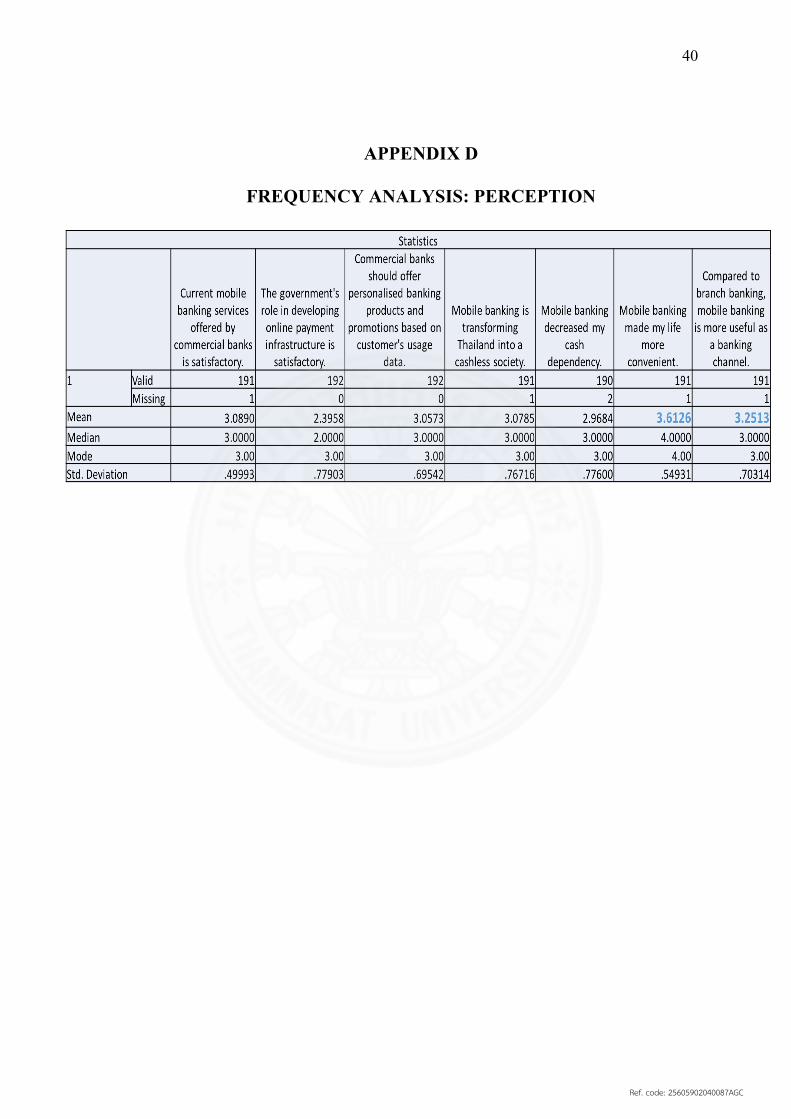

In terms of user perception towards mobile banking, 4 broad insights can be

derived from 4 level Likert scale frequency analysis. Firstly, with a mean of 3.6,

respondents generally view that adoption of mobile banking have made their lives

more convenient. Secondly, a mean of 3.2 suggests that respondents perceive mobile

banking to be more useful than branch banking. Thirdly, a mean of 3.0 proposes that

respondents are relatively satisfied with current mobile banking services. Finally, with

a mean of 3.0, respondents consider mobile banking as one of driving forces in

Thailand’s transformation to a cashless society. Overall, respondent’s perception

towards mobile banking is positive.

Table 4.1: Respondent’s Perception Towards Mobile Banking

Ref. code: 25605902040087AGC

18

4.2.2 Mobile Banking Brand Awareness and Usage

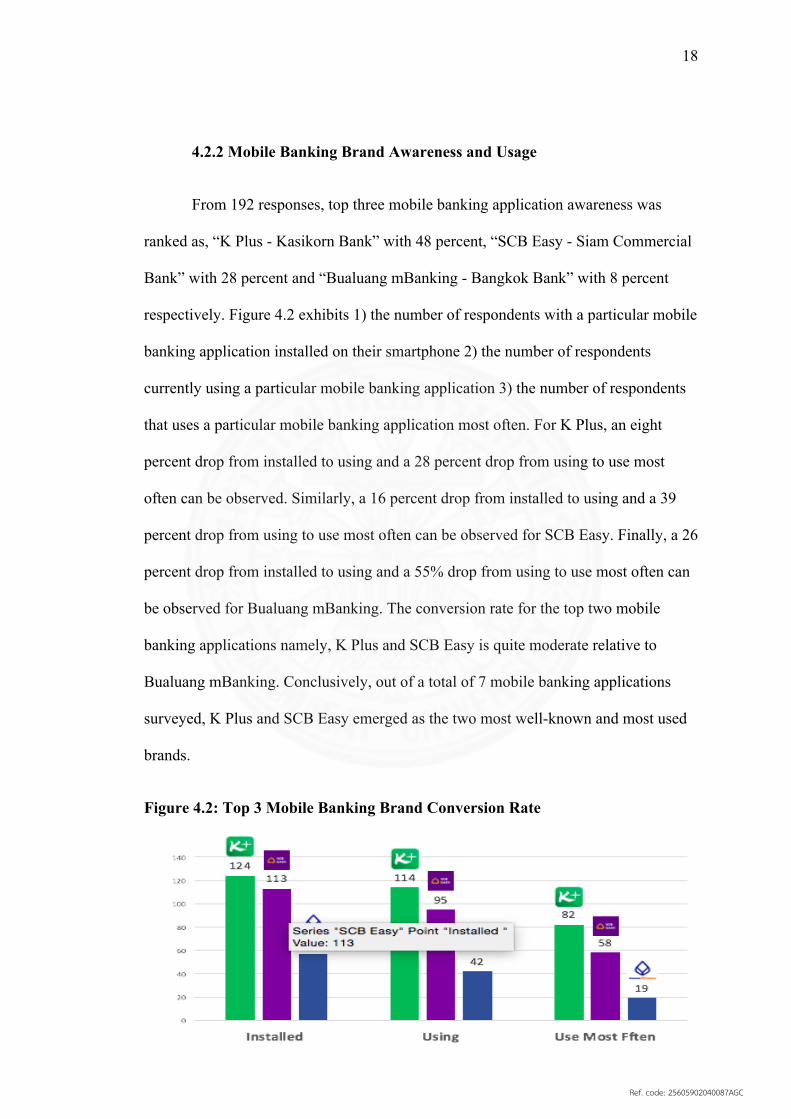

From 192 responses, top three mobile banking application awareness was

ranked as, “K Plus - Kasikorn Bank” with 48 percent, “SCB Easy - Siam Commercial

Bank” with 28 percent and “Bualuang mBanking - Bangkok Bank” with 8 percent

respectively. Figure 4.2 exhibits 1) the number of respondents with a particular mobile

banking application installed on their smartphone 2) the number of respondents

currently using a particular mobile banking application 3) the number of respondents

that uses a particular mobile banking application most often. For K Plus, an eight

percent drop from installed to using and a 28 percent drop from using to use most

often can be observed. Similarly, a 16 percent drop from installed to using and a 39

percent drop from using to use most often can be observed for SCB Easy. Finally, a 26

percent drop from installed to using and a 55% drop from using to use most often can

be observed for Bualuang mBanking. The conversion rate for the top two mobile

banking applications namely, K Plus and SCB Easy is quite moderate relative to

Bualuang mBanking. Conclusively, out of a total of 7 mobile banking applications

surveyed, K Plus and SCB Easy emerged as the two most well-known and most used

brands.

Figure 4.2: Top 3 Mobile Banking Brand Conversion Rate

Ref. code: 25605902040087AGC

19

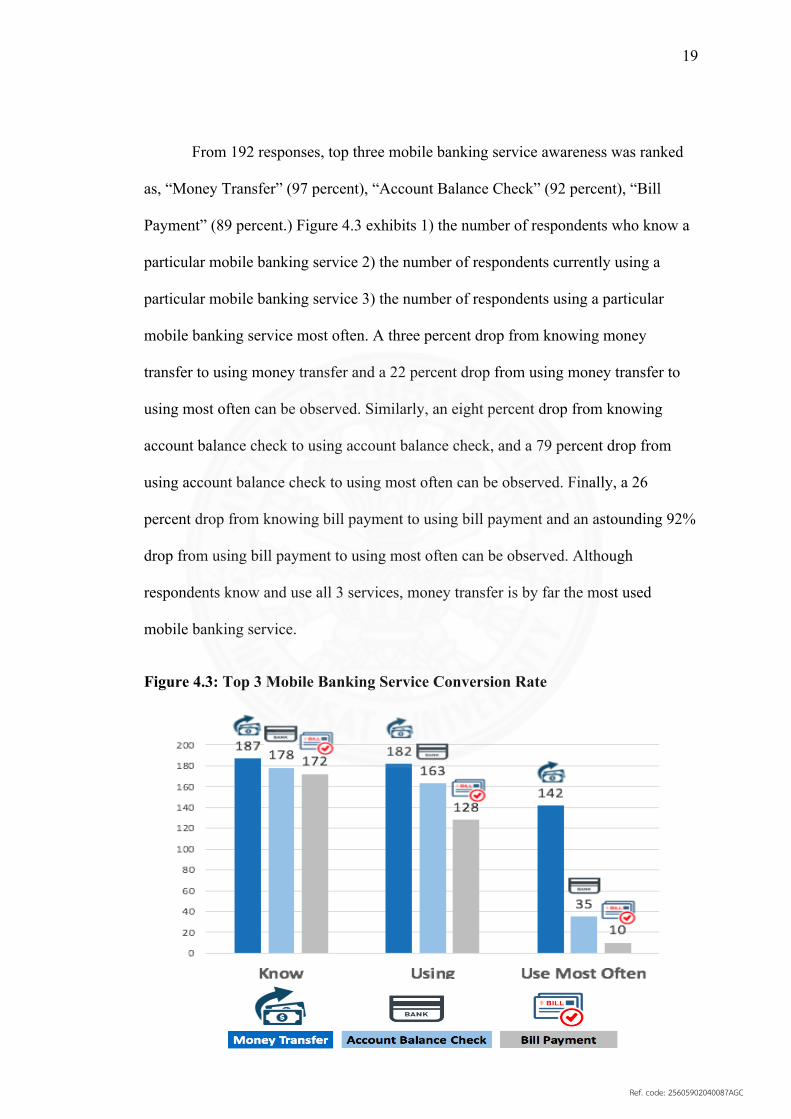

From 192 responses, top three mobile banking service awareness was ranked

as, “Money Transfer” (97 percent), “Account Balance Check” (92 percent), “Bill

Payment” (89 percent.) Figure 4.3 exhibits 1) the number of respondents who know a

particular mobile banking service 2) the number of respondents currently using a

particular mobile banking service 3) the number of respondents using a particular

mobile banking service most often. A three percent drop from knowing money

transfer to using money transfer and a 22 percent drop from using money transfer to

using most often can be observed. Similarly, an eight percent drop from knowing

account balance check to using account balance check, and a 79 percent drop from

using account balance check to using most often can be observed. Finally, a 26

percent drop from knowing bill payment to using bill payment and an astounding 92%

drop from using bill payment to using most often can be observed. Although

respondents know and use all 3 services, money transfer is by far the most used

mobile banking service.

Figure 4.3: Top 3 Mobile Banking Service Conversion Rate

Ref. code: 25605902040087AGC

20

4.2.3 Segmentation

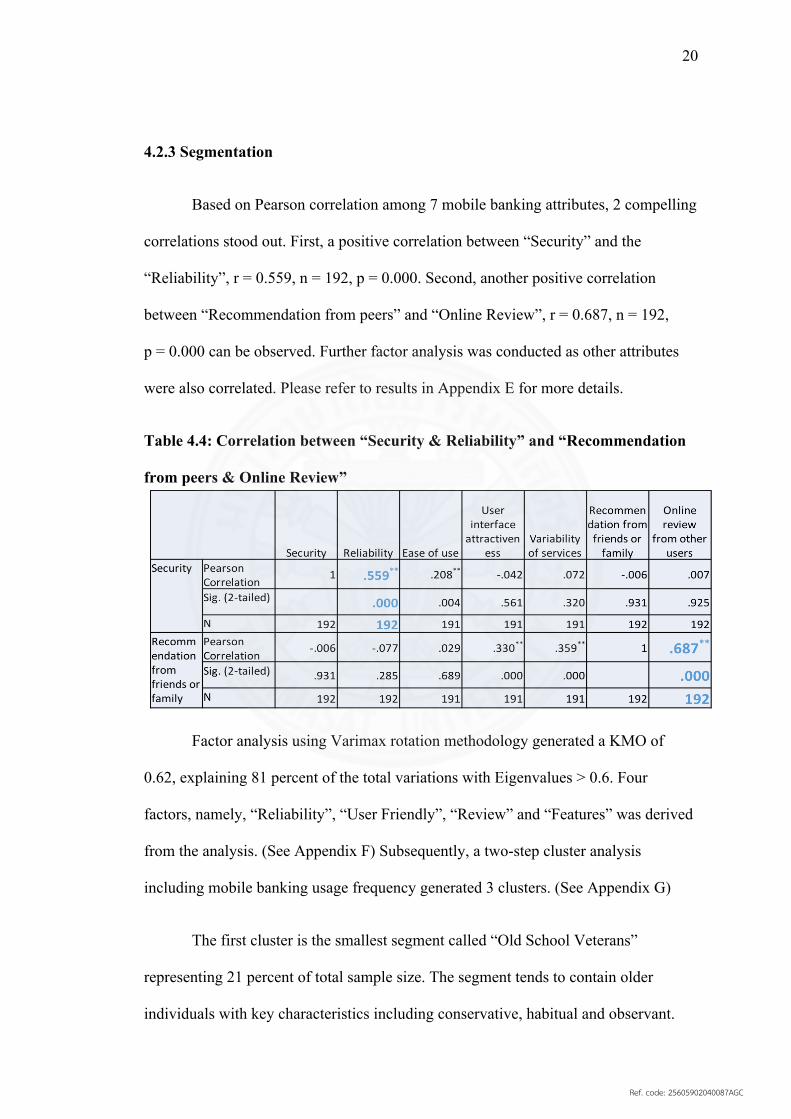

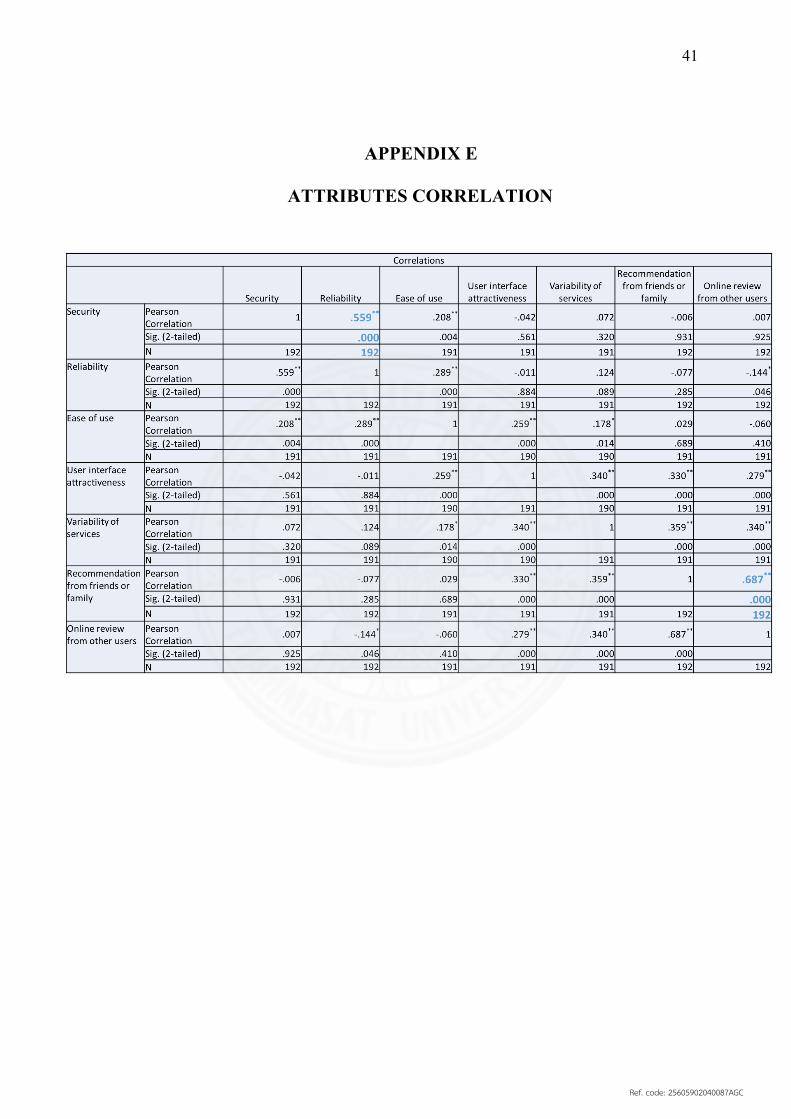

Based on Pearson correlation among 7 mobile banking attributes, 2 compelling

correlations stood out. First, a positive correlation between “Security” and the

“Reliability”, r = 0.559, n = 192, p = 0.000. Second, another positive correlation

between “Recommendation from peers” and “Online Review”, r = 0.687, n = 192,

p = 0.000 can be observed. Further factor analysis was conducted as other attributes

were also correlated. Please refer to results in Appendix E for more details.

Table 4.4: Correlation between “Security & Reliability” and “Recommendation

from peers & Online Review”

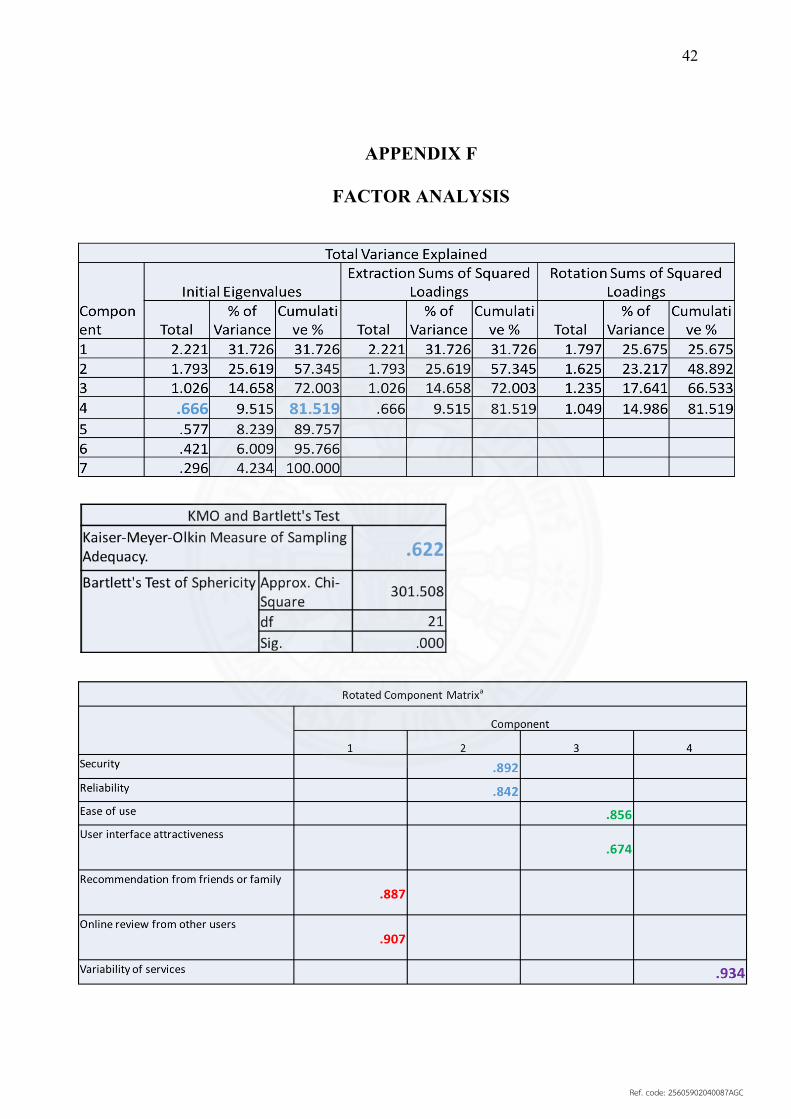

Factor analysis using Varimax rotation methodology generated a KMO of

0.62, explaining 81 percent of the total variations with Eigenvalues > 0.6. Four

factors, namely, “Reliability”, “User Friendly”, “Review” and “Features” was derived

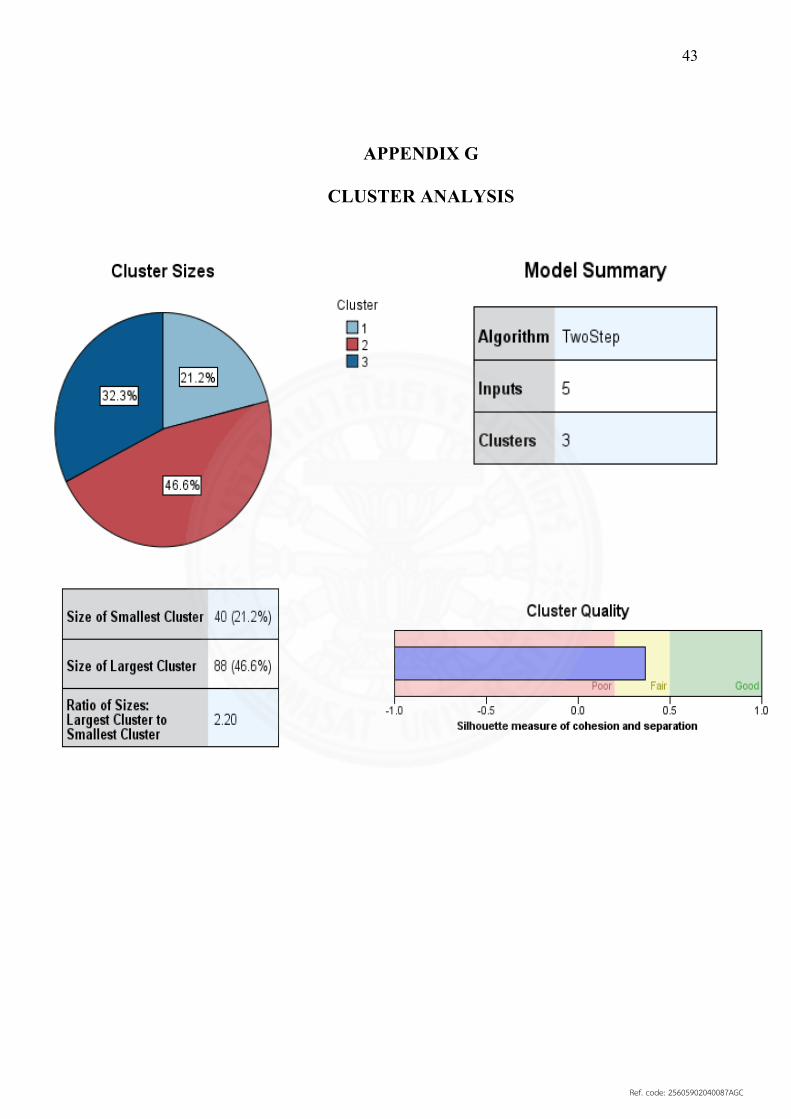

from the analysis. (See Appendix F) Subsequently, a two-step cluster analysis

including mobile banking usage frequency generated 3 clusters. (See Appendix G)

The first cluster is the smallest segment called “Old School Veterans”

representing 21 percent of total sample size. The segment tends to contain older

individuals with key characteristics including conservative, habitual and observant.

Ref. code: 25605902040087AGC

21

The second cluster is the largest segment called “Middle Aged Go-Getter”

representing 46 percent of the total sample size. This segment is made up of working

adults who are logical, practical and have systematic thinking. Finally, a segment

called “Youthful Minimalist”, which is the second largest cluster, representing 32

percent of the total sample size. Individuals in this segment tend to be younger,

tasteful, emotional and spontaneous. “Middle Aged Go-Getter” and “Youthful

Minimalist” are classified as heavy users and “Old School Veterans” is classified as

light users.

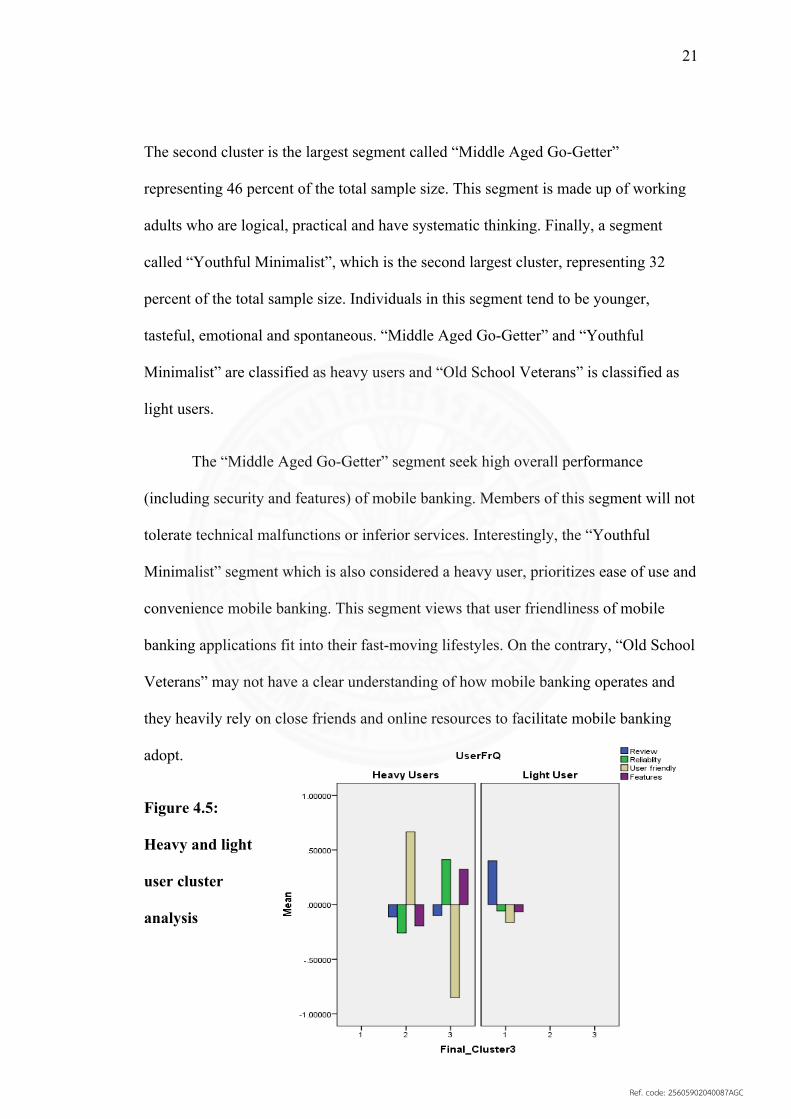

The “Middle Aged Go-Getter” segment seek high overall performance

(including security and features) of mobile banking. Members of this segment will not

tolerate technical malfunctions or inferior services. Interestingly, the “Youthful

Minimalist” segment which is also considered a heavy user, prioritizes ease of use and

convenience mobile banking. This segment views that user friendliness of mobile

banking applications fit into their fast-moving lifestyles. On the contrary, “Old School

Veterans” may not have a clear understanding of how mobile banking operates and

they heavily rely on close friends and online resources to facilitate mobile banking

adopt.

Figure 4.5:

Heavy and light

user cluster

analysis

Ref. code: 25605902040087AGC

22

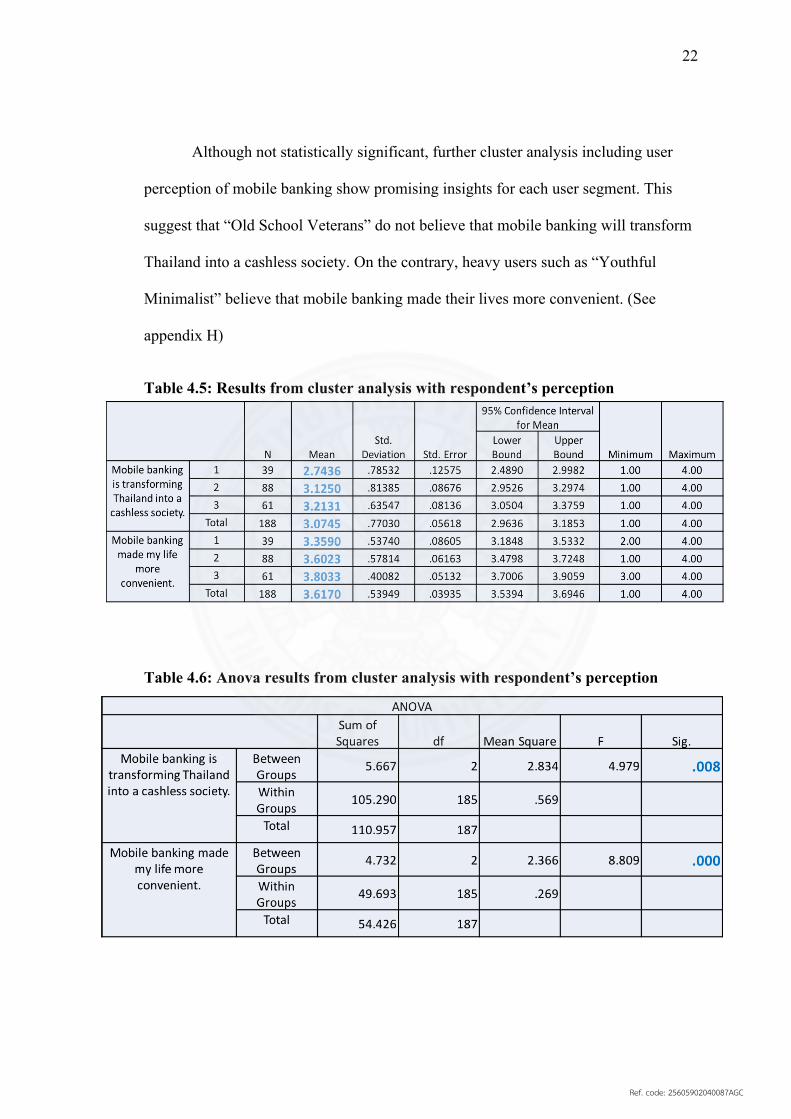

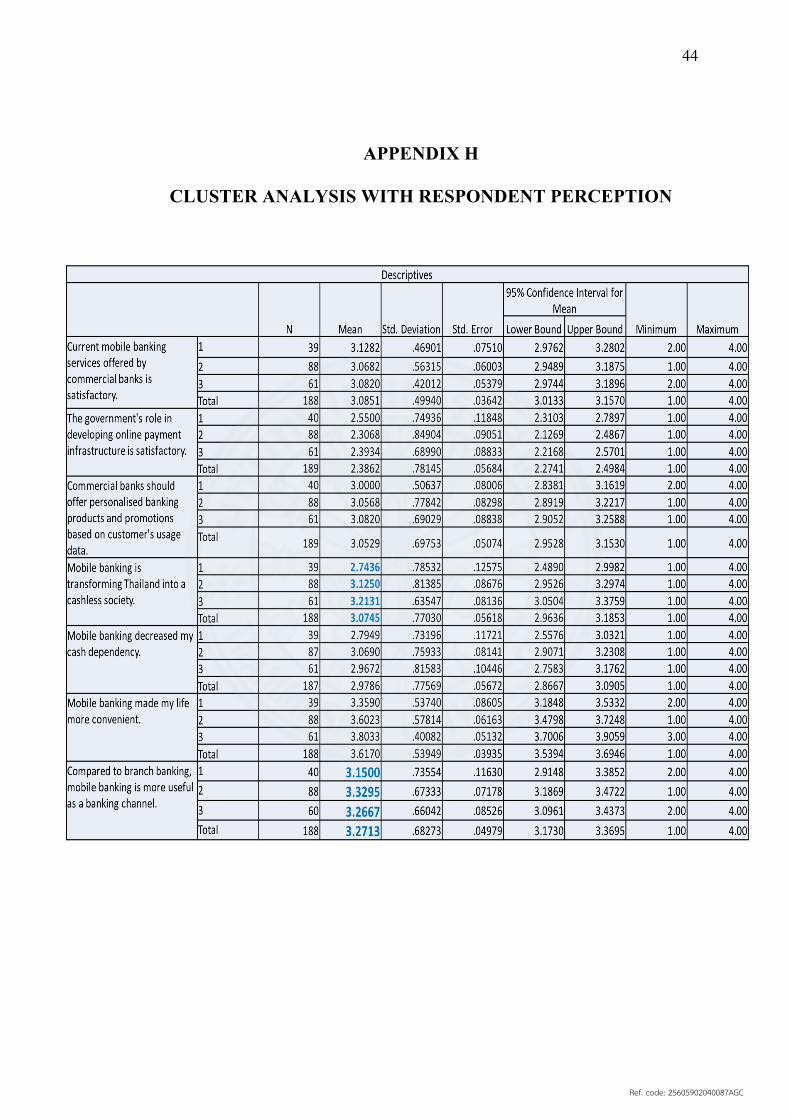

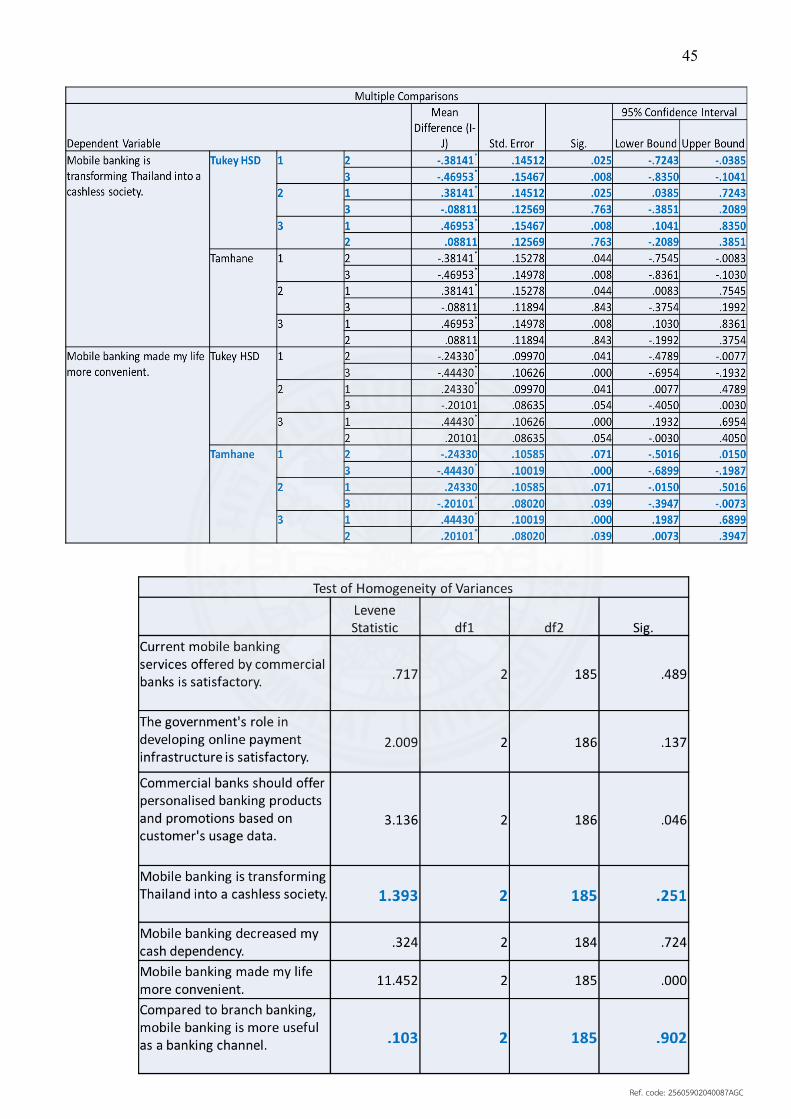

Although not statistically significant, further cluster analysis including user

perception of mobile banking show promising insights for each user segment. This

suggest that “Old School Veterans” do not believe that mobile banking will transform

Thailand into a cashless society. On the contrary, heavy users such as “Youthful

Minimalist” believe that mobile banking made their lives more convenient. (See

appendix H)

Table 4.5: Results from cluster analysis with respondent’s perception

Table 4.6: Anova results from cluster analysis with respondent’s perception

Ref. code: 25605902040087AGC

23

CHAPTER 5

CONCLUSIONS AND RECOMMENDATIONS

5.1 Conclusion and Managerial Implication

According to qualitative research as well as frequency, factor and cluster

analysis, the majority of Thais have a positive perception towards mobile banking.

Furthermore, 2 out of 3 user segments identified by the research are heavy users that

highly value reliability and user friendliness. Interestingly, the remaining cluster of

light users who value word of mouth and online review has the potential to turn into a

heavy user if they were better educated about the product. As Thailand’s smartphone

penetration increases, more Thais will likely adopt mobile banking and the following

implications for commercial banks can be implemented.

5.1.1 Managerial Implication for Commercial Banks

Firstly, there are only 2 dominant brands in the market and the remaining

5 banks must compete more aggressively in terms of brand awareness and usage

frequency. Although the research identified 3 top-of-mind mobile banking brands, it

was clear that, K Plus and SCB Easy were the only two that dominated the market.

This finding is not surprising as Kasikorn Bank and Siam Commercial Bank invested

heavily in their digital banking infrastructure. However, this is a wake-up call for the

remaining 5 banks. One possible solution is to reduce traditional banking channels

costs and increase invest in innovative banking solutions such as QR code payment

infrastructure to catch up with technological advancement. Another solution is to

secure user’s Prompt Pay registration as a means of obtaining a user’s “Primary

Ref. code: 25605902040087AGC

24

Account.” Users will prefer to use the primary account to transfer money rather than

secondary accounts because Prompt Pay is more convenient. This strategy will attract

more traffic to the mobile banking application and create a ripple effect to generate

more awareness among prospect users.

Secondly, offering a wide range of services is not a sustainable competitive

advantage. Research findings suggests money transfer is the most commonly used

service, followed by account balance check and bill payment. However, the majority

of users do not use the remaining 13 services currently offered by various commercial

banks. As a result, it would be impractical to invest and roll out insignificant service

extensions such as insurance purchase and branch location. Rather, commercial banks

should integrate and reinvent their mobile banking application into user’s daily lives.

This will transform mobile banking from a payment channel into a multi-purpose

lifestyle platform capable of ride hailing, food delivery and online shopping. Higher

usage frequency also translates to a bigger potential in monetizing user data.

Ultimately, commercial banks will have to compete against non-bank players such as

e-wallet companies that are aiming to disrupt the banking industry.

5.2 Research Limitations

Although this research was carefully planned and executed, 2 main limitations

emerged. Firstly, the diversity of respondents’ profiles was limited. This is because

the majority of respondents are corporate employees living in Bangkok with similar

education background. Collecting more response from other population groups such

as the working class as well as senior management could have generated other

insightful findings.

Ref. code: 25605902040087AGC

25

Secondly, with limited time and resources, the research failed to gasp a better

understanding of non-bank players which represents a considerable portion of

Thailand’s Fintech industry. Moreover, a deeper study of the government sector will

produce a holistic understanding of the industry as they are a responsible for shaping

digital banking policies and infrastructure.

5.3 Suggestions for Future Studies

The intention of this research was to identify overall user behavior and to

identify consumer segments; however, the findings are relatively generalized.

Therefore, future studies should specifically target one out of three user segments

defined by this study or other potential segments including teenagers, entrepreneurs

and pensioners. It is also important to investigate how to increase usage frequency

among current heavy users or how to transform light users into heavy users.

Furthermore, commercial banks will find financial profiles and user profitability of

each segments highly useful. Aside from Thai mobile banking users, other potential

user segments to conduct further study on are Chinese tourists who heavily rely on e-

payment at home and abroad. Further studies have the potential to increase usage

frequency and satisfaction of heavy users, increase mobile banking adoption for light

users and ultimately transform Thailand into a cashless society.

Ref. code: 25605902040087AGC

26

REFERENCES

Alker, T. (2016). CROWDFUNDING SUCCESS FACTORS IN THAILAND. Colleg e of Management, Master of Management. Bangkok, Thailand: Mahdiol University. Retrieved October 14, 2017, from Globalbizresearch: http://globalbizresearch.org/Bangkok_Thailand_Conference_2017_feb1/docs/doc/2.%20Finance,%20Account%20&%20Banking/T744.pdf

Allison, A. L. (2016, November 1). The Hierarchy of Effects Model in Advertising. Retrieved March 7, 2018, from Propaganda For Change: http://persuasion-and-influence.blogspot.com/2016/11/the-hierarchy-of-effects-model_1.html

Bangkok Post. (2016, June 28). Smartphone subscriptions near 50m. Retrieved from Bangkok Post Technology: https://www.bangkokpost.com/tech/local-news/1021773/smartphone-subscriptions-near-50m

Bank of Thailand. (2017, August 31). Use of mobile banking and internet banking. Retrieved from Bank of Thailand Official Web Site: http://www2.bot.or.th/statistics/ReportPage.aspx?reportID=688&language=eng

Bank of Thailand. (2017, August 31). Use of mobile banking and internet banking. Retrieved from Bank of Thailand Official Website: http://www2.bot.or.th/statistics/ReportPage.aspx?reportID=688&language=eng

Bayus, B. L., & Kuppuswamy, V. (2015, October 28). A REVIEW OF CROWDFUNDING RESEARCH AND FINDINGS. (D. Mitra, Ed.) Retrieved September 14, 2017, from SSRN: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2685739

Boonperm, J., Wayuparb, S., Mutraden, A., & Tangpoolcharoen, J. (2016, March). Thailand Internet User Profile 2015. Retrieved November 24, 2017, from Electronic Transactions Development Agency: http://unctad.org/meetings/en/Contribution/dtl_eweek2016_ETDA_IUP_en.pdf

Carlos T., T. O. (2017). Literature review of mobile The current issue and full text archive of this journal is available on Emerald Insight. International Journal of Bank Marketing, 1048.

Charles, B. S. (2017, June 6). Security Intelligence. (IBM, Producer, & IBM) Retrieved from Securityintelligence.com: https://securityintelligence.com/is-mobile-banking-safe/

Chung, K. C. (2009, December ). Understanding factors affecting trust in and satisfaction with mobile banking in Korea: A modified DeLone and McLean’s model perspective. Interacting With Computers, 385-392.

Ref. code: 25605902040087AGC

27

Crowdsourcing.org. (2012, May). CROWDFUNDING INDUSTRY REPORT : Market Trends, Composition and Crowdfunding Platforms. Retrieved November 14, 2017, from Crowdfunding: http://www.crowdfunding.nl/wp-content/uploads/2012/05/92834651-Massolution-abridged-Crowd-Funding-Industry-Report1.pdf

Cumming, D., Schwienbacher, A., & Leboeuf, G. (2014, January). Crowdfunding Models: Keep-it-All vs. All-or-Nothing. Retrieved December 3, 2017, from Researchgate: https://www.researchgate.net/publication/272306935_Crowdfunding_Models_Keep-it-All_vs_All-or-Nothing

David T., M. S. (2013). Analytics: The real-world use of big data in financial services. Saïd Business School at the University of Oxford . New York: IBM Global Business Services .

DBS Group Research. (2015). Regional Industry Focus ASEAN Banks. Singapore: DBS Vickers Securities.

Deloiotte. (2015). Digital banking for small and medium-sized enterprises Improving access to finance for the underserved. Deloiotte Southeast Asia .

Deloitte. (2010). Mobile banking A catalyst for improving bank performance. Deloitte Development.

Deshwal, Dr. Parul. (2015, December). A Study of Mobile Banking in India. International Journal of Adcanced Research in IT and Engineering, 6-7.

Deshwal, Dr. Parul. (2015, December). A Study of Mobile Banking in India. International Journal of Advanced Research in IT and Engineering, 2-4.

Education, M. o. (2017, August). Aveage Education Years for Thai Population 2012-2017. Retrieved March 26, 2018, from Ministry of Education: http://backoffice.onec.go.th/uploads/Book/1554-file.pdf

Gerber, E., Hui, J., & Kuo, P.-Y. (2012, Febuary). Crowdfunding: Why People are Motivated to Post and Fund Projects on Crowdfunding Platforms. Retrieved September 17, 2017, from ResearchGate: https://www.researchgate.net/publication/261359489_Crowdfunding_Why_People_are_Motivated_to_Post_and_Fund_Projects_on_Crowdfunding_Platforms

Hoehle, H. H. (2012). Advancing task-technology fit theory: a formative measurement approach to determining task-channel fit for electronic banking channels. Information Systems Foundations: Theory Building in Information Systems, 133-169.

index mundi. (2018, January 20). Thailand Demographics Profile 2018. Retrieved March 26, 2018, from index mundi: https://www.indexmundi.com/thailand/demographics_profile.html

Ref. code: 25605902040087AGC

28

Index Mundi. (2018, January 20). Thailand Demographics Profile 2018. Retrieved April 1, 2018, from Index Muni : https://www.indexmundi.com/thailand/demographics_profile.html

Investopedia. (2018, March 7). Hierarchy-Of-Effects Theory. Retrieved from Investorpedia: https://www.investopedia.com/terms/h/hierarchy-of-effects-theory.asp#ixzz5936AAmxa

Investopedia. (n.d.). Herd Instinct. Retrieved December 5, 2017, from Investopedia: https://www.investopedia.com/terms/h/herdinstinct.asp

Kasikorn Research. (2017). PromptPay to Help Create Cashless Society and Long-Term Economic Benefits Despite Cutting Banks’ Fee Income . Bangkok: Kasikorn Research.

Kuppuswamy, V., & Bayus , B. L. (2013, March 16). CROWDFUNDING CREATIVE IDEAS: THE DYNAMICS OF PROJECT BACKERS IN KICKSTARTE. Retrieved October 14, 2017, from https://funginstitute.berkeley.edu/wp-content/uploads/2013/11/Crowdfunding_Creative_Ideas.pdf

Laukkanen, T. (2007). Internet vs mobile banking: comparing customer value perceptions. Business Process Management Journal, 788-797.

Lor, M. J. (2017, September 9). Asiola Performance as a leading Crowdfunding in Thailand. (P. Kangwankit, Interviewer)

Massolution. (2015, March 31). 2015 Massolution Report Released: Crowdfunding Market Grows 167% in 2014, Crowdfunding Platforms Raise $16.2 Billion. Retrieved November 14, 2017, from NCFA : National Crowdfunding Association of Canada: http://ncfacanada.org/2015-massolution-report-released-crowdfunding-market-grows-167-in-2014-crowdfunding-platforms-raise-16-2-billion/

McKinsey&Company. (2015). Digital Banking in ASEAN: Increasing Consumer Sophistication and Openness. Asia Consumer Insights Center. McKinsey&Company.

McKinsey&Company. (2015). Digital Banking in Asia: What do consumers really want? . McKinsey&Company.

Meyskens, M., & Bird, L. (2015, January). Crowdfunding and Value Creation. Retrieved December 5, 2017, from Researchgate: https://www.researchgate.net/publication/277637559_Crowdfunding_and_Value_Creation

Mollick, E. (2013, June 26). The Untold story behind Kickstarter stats. Retrieved September 26, 2017, from Appsblogger: http://www.appsblogger.com/behind-kickstarter-crowdfunding-stats/

Ref. code: 25605902040087AGC

29

Moritz, A., & Block, J. H. (2014, August 11). Crowdfunding: A Literature Review and Research Directions. Retrieved November 9, 2017, from SSRN: https://papers.ssrn.com/sol3/Papers.cfm?abstract_id=2554444

Munongo, S. K. (2013, November 1). Extending the Technology Acceptance Model to Mobile Banking Adoption in Rural Zimbabwe. Journal of Business Administration and Education, 51-79.

Nielsen. (2014, Febuary 12). Nielsen Pressroom. Retrieved from Nielsen Official Website: http://www.nielsen.com/my/en/press-room/2014/preferred-payment-methods.html

P. Dupas, S. G. (2012, Febuary). CHALLENGES IN BANKING THE RURAL POOR: EVIDENCE FROM KENYA'S WESTERN PROVINCE. National Bureau of Economic Research Working Paper Series.

Philipp Haas, I. B. (2014). An empirical taxonomy of crowdfunding. Conference: International Conference on Information Systems (ICIS) 2014, (p. 18). Auckland, New Zealand. Retrieved November 17, 2017, from Paper presented at the International Conference on Information Systems: https://www.alexandria.unisg.ch/234893/1/Haas%20et%20al%20-%20An%20Empirical%20Taxonomy%20of%20Crowdfunding%20Intermediaries.pdf

Prive, T. (2012, November 27). What Is Crowdfunding And How Does It Benefit The Economy. Retrieved November 9, 2017, from Forbes: https://www.forbes.com/sites/tanyaprive/2012/11/27/what-is-crowdfunding-and-how-does-it-benefit-the-economy/#2f57fbc1be63

Pual Belleflamme, T. L. (2012, April 25). Crowdfunding: Tapping the Right Crowd. Retrieved November 9, 2017, from Innovation & Regulation Chair: http://innovation-regulation2.telecom-paristech.fr/wp-content/uploads/2012/10/Belleflamme-CROWD-2012-06-20_SMJ.pdf

Qiu, C. (2013, October 27). Issues in Crowdfunding: Theoretical and Empirical Investigation on Kickstarter. Retrieved November 15, 2017, from SSRN: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2345872

Rammile, N. &. (2012). Understanding resistance to cell phone banking adoption through the application of the technology acceptance model (TAM). African Journal of Business Management, 86-97.

SCB Economic Intelligence Center. (2016, October 13). EIC Analysis / Interesting Topics. Retrieved from SCB Economic Intelligence Center: https://www.scbeic.com/en/detail/product/2913

STARTUP FUNDING BOOK. (2017, November 17). TYPES OF CROWDFUNDING RELEVANT FOR STARTUPS. Retrieved from STARTUP FUNDING BOOK: https://startupfundingbook.com/category/crowdfunding/

Ref. code: 25605902040087AGC

30

Statista. (2017). Crowdfunding : Thailand. Retrieved November 15, 2017, from Statista: https://www.statista.com/outlook/335/126/crowdfunding/thailand#

Statista. (2017). Thailand Fintech Overview. Retrieved from www.statista.com: https://www.statista.com/outlook/295/126/fintech/thailand#

Taylor, B. (2015, May 22). 6 things almost every viral Kickstarter has in common. Retrieved October 14, 2017, from PCWorld: https://www.pcworld.com/article/2924327/web-social/6-things-almost-every-viral-kickstarter-has-in-common.html

Team, T. (2017, December 27). Here’s What Happened in Thailand’s Startup Ecosystem in 2017. Retrieved March 29, 2018, from Techsauce: https://techsauce.co/en/country-en/thailand-en/heres-happened-thailands-startup-ecosystem-2017/

Technavio Research. (2017, August 14). Global Crowdfunding Market - Segmentation and Forecast by Technavio. Retrieved September 30, 2017, from BusinessWire: http://www.businesswire.com/news/home/20170814005545/en/Global-Crowdfunding-Market---Segmentation-Forecast-Technavio

The Asian Banker. (2017, July 4). The Asian Banker Official Website. Retrieved from Research Note: http://www.theasianbanker.com/updates-and-articles/mobile-banking-seen-to-overtake-internet-banking

The Nation. (2016, December 23). Digitisation of banking system to continue in 2017. Retrieved from www.nationmultimedia.com: http://www.nationmultimedia.com/news/business/EconomyAndTourism/30302676

The Nation. (2017, August 31). The Nation, Thailand Portal. Retrieved from The Nation Official Website: http://www.nationmultimedia.com/detail/Economy/30325327

Thuy, N. N. (2017, August). The Impact of Project and Founder Quality on funding success. CROWDFUNDING IN VIETNAM: The Impact of Project and Founder Quality on funding success., 59. Retrieved January 20, 2018, from http://essay.utwente.nl/73270/1/Nguyen_MA_BMS.pdf

Ward, C., & Ramachandran, V. (2010). Crowdfunding the next hit: Microfunding online experience. Retrieved November 15, 2017, from In Workshop on Computational Social Science and the Wisdom of Crowds at NIPS2010: http://people.cs.umass.edu/~wallach/workshops/nips2010css/papers/ward.pdf

XinLuo, H. J. (2010, May). Examining Multi- Dimensional Trust and Multi-Faceted Risk in Initial Acceptance of Emerging Technologies: An Empirical Study of Mobile Banking Services. Decision Support Systems, 222-234.

Yeh, A. (2015, October 6). New Research Study: 7 Stats from 100,000 Crowdfunding Campaigns. Retrieved November 17, 2017, from Indiegogo:

Ref. code: 25605902040087AGC

31

https://go.indiegogo.com/blog/2015/10/crowdfunding-statistics-trends-infographic.html

Ref. code: 25605902040087AGC

32

APPENDICES

Ref. code: 25605902040087AGC

33

APPENDIX A

IN-DEPTH INTERVIEW GUIDELINE

1.1 Interview ice breaking and set up

Hi! I want to thank you for taking the time to meet with me today. My name is

Win and I would like to talk to you about your perception and past experience

regarding mobile banking in Thailand. The interview should take less than an hour. I

hope you don’t mind me voice recording the session because I don’t want to miss any

of your comments. All of your responses will be kept confidential and I will ensure

that any information I include in my report does not identify you as the respondent.

Remember, you don’t have to talk about anything you don’t want to and you may end

the interview at any time. Feel free to ask any questions before we begin the session.

1.2 Questions

1) Describe the top 3 words that comes to your mind when you think about mobile banking (e.g. convenient, money transfer, Prompt Pay)

2) Identify all mobile banking services that you are aware of (e.g. money transfer, bank balance check, bill payment.)

3) Describe your mobile banking usage frequency and time of usage (e.g. weekly, mid-day.)

4) Describe mobile banking purpose of use (e.g. online shopping, work-related, personal affairs)

5) Describe mobile banking services that you have used and the average amount per transaction (e.g. money transfer, bill payment, approximately 2,000 THB per transaction)

6) Describe any positive perceptions or experiences that you have towards mobile banking, if any (e.g. convenient, cashless society, diverse service offerings.) Please provide justification for your response.

Ref. code: 25605902040087AGC

34

7) Describe any negative perceptions or experiences that you have towards mobile banking, if any (e.g. security concerns, application malfunction, hard to use.) Describe how did you overcame those negative experiences.

8) To what extend did the adoption and advancement of mobile banking change your behavior as a consumer (e.g. less cash dependent, subconsciously spend more money, increased trust in e-commerce)

9) If you could give any recommendations to commercial banks or government agencies regarding mobile banking, what are the top 3 recommendations you would give?

1.3 Interview closing

Feel free to add any additional comments before we end the interview. I’ll be

analyzing the information you and others gave me and I’ll be happy to send you a

copy of my research, if you are interested. Thank you for your time.

Ref. code: 25605902040087AGC

35

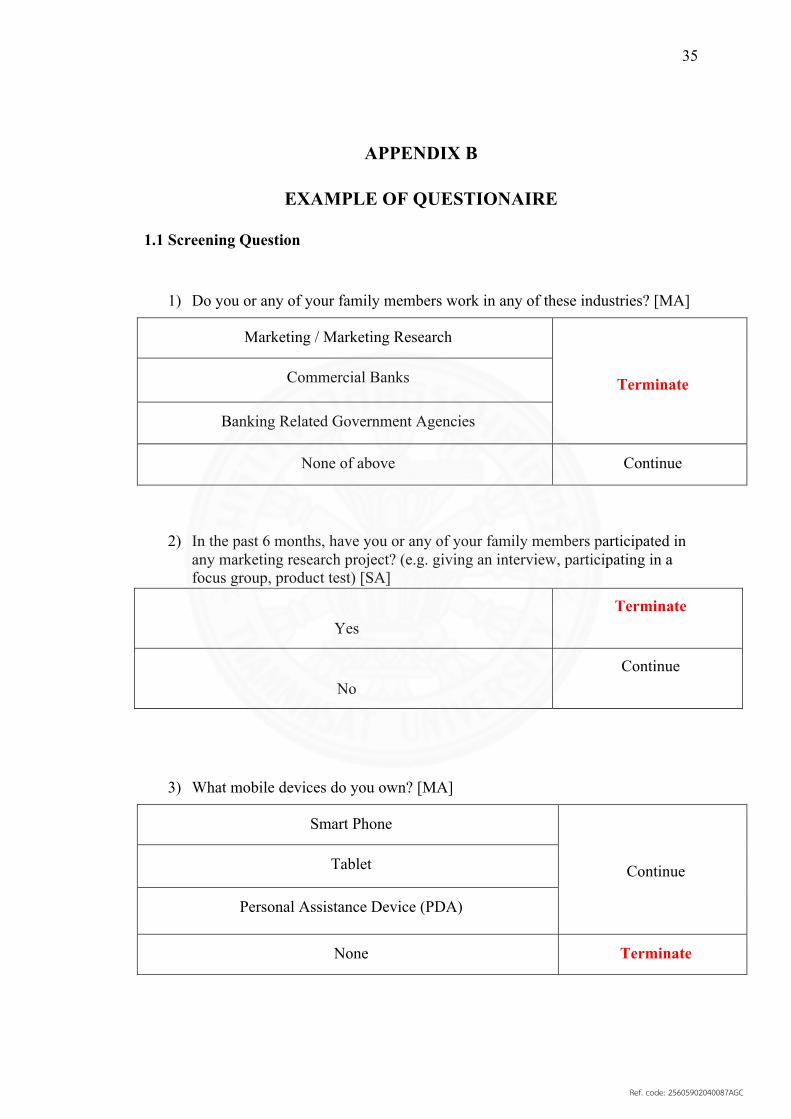

APPENDIX B

EXAMPLE OF QUESTIONAIRE

1.1 Screening Question

1) Do you or any of your family members work in any of these industries? [MA]

Marketing / Marketing Research

Terminate Commercial Banks

Banking Related Government Agencies

None of above Continue

2) In the past 6 months, have you or any of your family members participated in any marketing research project? (e.g. giving an interview, participating in a focus group, product test) [SA]

Yes

Terminate

No

Continue

3) What mobile devices do you own? [MA]

Smart Phone

Continue Tablet

Personal Assistance Device (PDA)

None Terminate

Ref. code: 25605902040087AGC

36

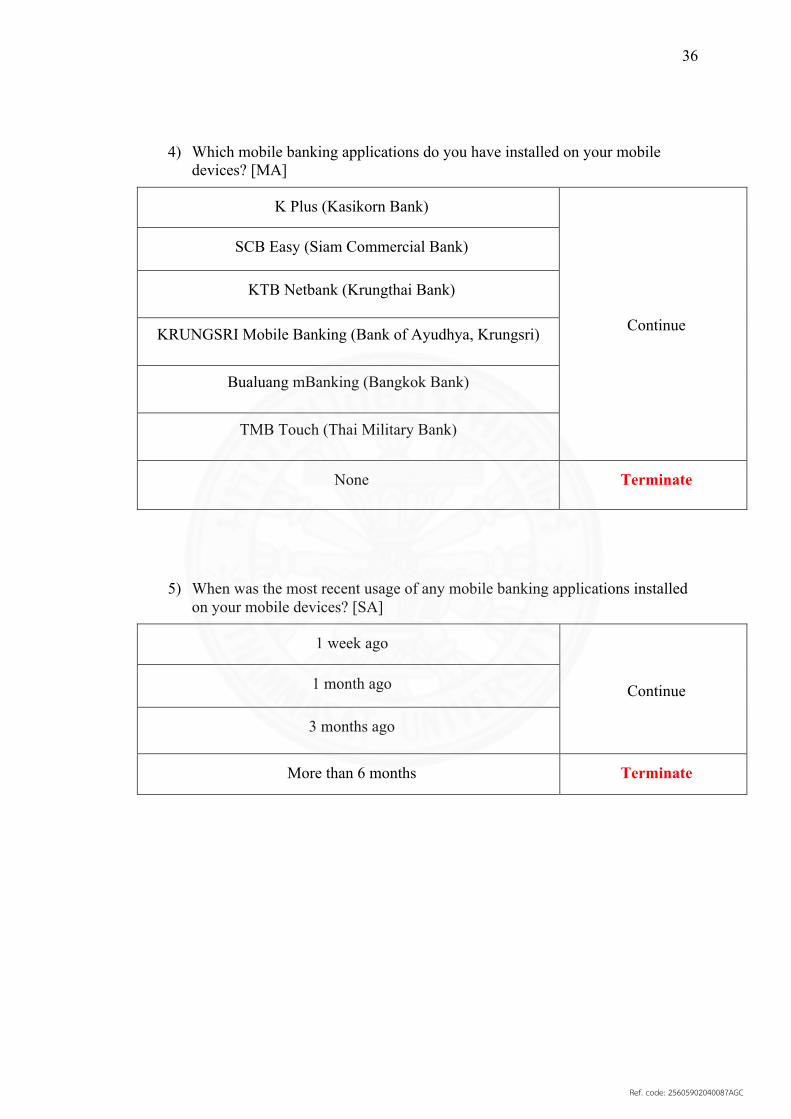

4) Which mobile banking applications do you have installed on your mobile devices? [MA]

K Plus (Kasikorn Bank)

Continue

SCB Easy (Siam Commercial Bank)

KTB Netbank (Krungthai Bank)

KRUNGSRI Mobile Banking (Bank of Ayudhya, Krungsri)

Bualuang mBanking (Bangkok Bank)

TMB Touch (Thai Military Bank)

None Terminate

5) When was the most recent usage of any mobile banking applications installed on your mobile devices? [SA]

1 week ago

Continue 1 month ago

3 months ago

More than 6 months Terminate

Ref. code: 25605902040087AGC

37

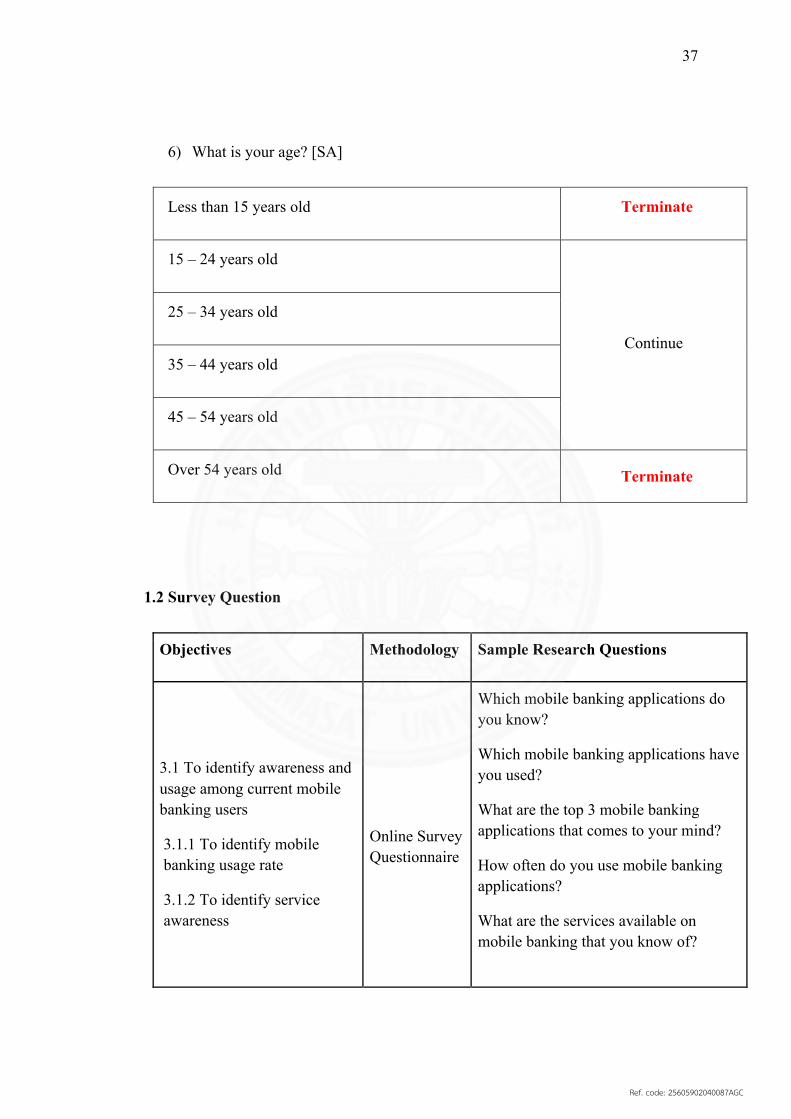

6) What is your age? [SA]

Less than 15 years old Terminate

15 – 24 years old

Continue

25 – 34 years old

35 – 44 years old

45 – 54 years old

Over 54 years old Terminate

1.2 Survey Question

Objectives Methodology Sample Research Questions

3.1 To identify awareness and usage among current mobile banking users

3.1.1 To identify mobile banking usage rate

3.1.2 To identify service awareness

Online Survey Questionnaire

Which mobile banking applications do you know?

Which mobile banking applications have you used?

What are the top 3 mobile banking applications that comes to your mind?

How often do you use mobile banking applications?

What are the services available on mobile banking that you know of?

Ref. code: 25605902040087AGC

38

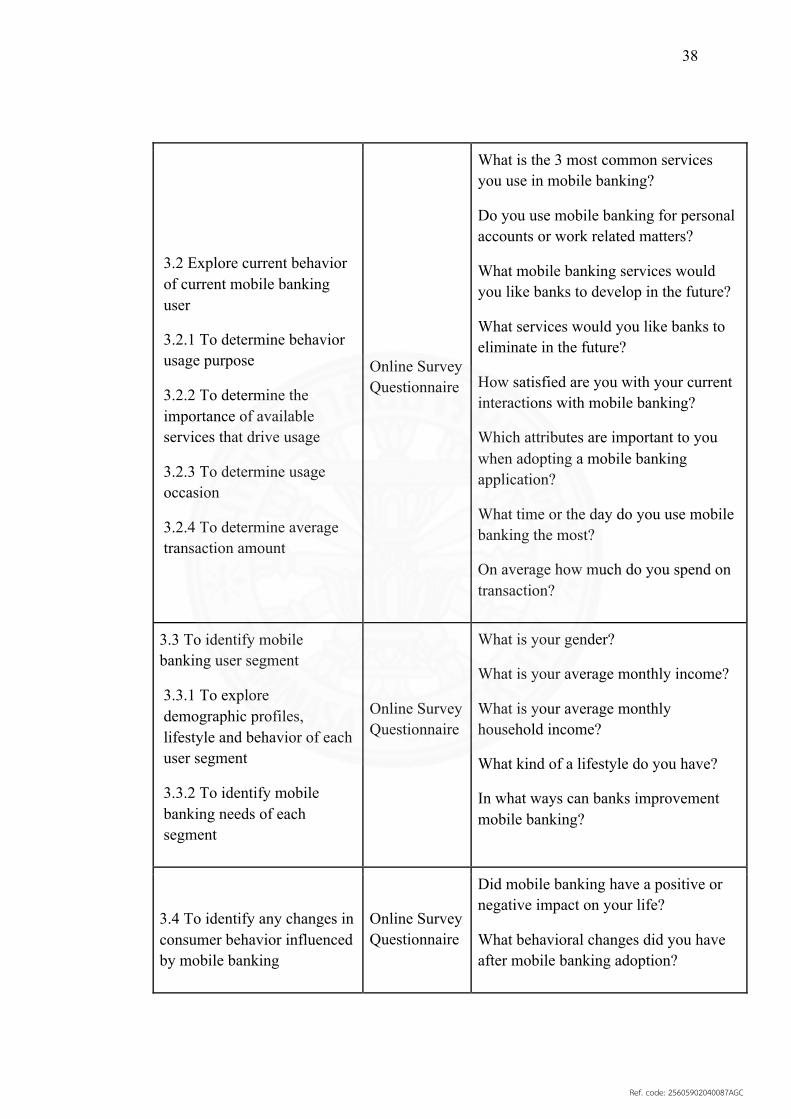

3.2 Explore current behavior of current mobile banking user

3.2.1 To determine behavior usage purpose

3.2.2 To determine the importance of available services that drive usage

3.2.3 To determine usage occasion

3.2.4 To determine average transaction amount

Online Survey Questionnaire

What is the 3 most common services you use in mobile banking?

Do you use mobile banking for personal accounts or work related matters?

What mobile banking services would you like banks to develop in the future?

What services would you like banks to eliminate in the future?

How satisfied are you with your current interactions with mobile banking?

Which attributes are important to you when adopting a mobile banking application?

What time or the day do you use mobile banking the most?

On average how much do you spend on transaction?

3.3 To identify mobile banking user segment

3.3.1 To explore demographic profiles, lifestyle and behavior of each user segment

3.3.2 To identify mobile banking needs of each segment

Online Survey Questionnaire

What is your gender?

What is your average monthly income?

What is your average monthly household income?

What kind of a lifestyle do you have?

In what ways can banks improvement mobile banking?

3.4 To identify any changes in consumer behavior influenced by mobile banking

Online Survey Questionnaire

Did mobile banking have a positive or negative impact on your life?

What behavioral changes did you have after mobile banking adoption?

Ref. code: 25605902040087AGC

39

APPENDIX C

RESPONDENT DEMOGRAPHIC

Ref. code: 25605902040087AGC

40

APPENDIX D

FREQUENCY ANALYSIS: PERCEPTION

Ref. code: 25605902040087AGC

41

APPENDIX E

ATTRIBUTES CORRELATION

Ref. code: 25605902040087AGC

42

APPENDIX F

FACTOR ANALYSIS

Ref. code: 25605902040087AGC

43

APPENDIX G

CLUSTER ANALYSIS

Ref. code: 25605902040087AGC

44

APPENDIX H

CLUSTER ANALYSIS WITH RESPONDENT PERCEPTION

Ref. code: 25605902040087AGC

45

Ref. code: 25605902040087AGC

46

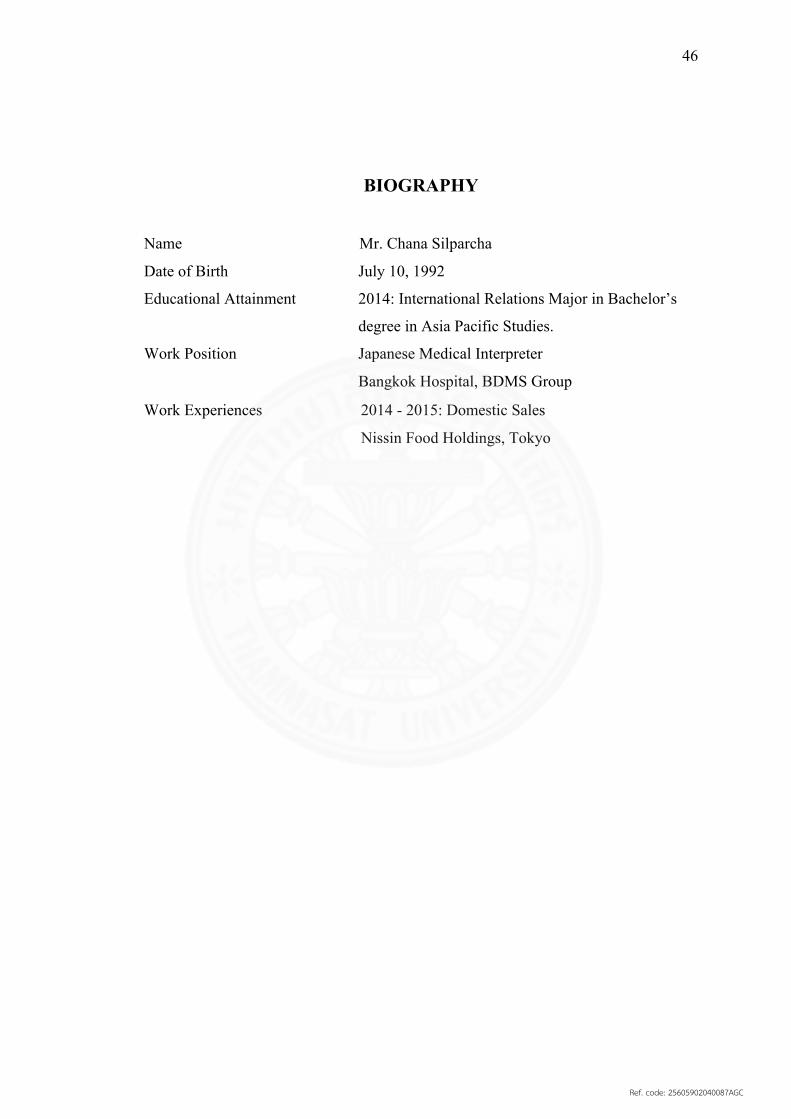

BIOGRAPHY

Name Mr. Chana Silparcha

Date of Birth July 10, 1992

Educational Attainment

2014: International Relations Major in Bachelor’s

degree in Asia Pacific Studies.

Work Position Japanese Medical Interpreter

Bangkok Hospital, BDMS Group

Work Experiences 2014 - 2015: Domestic Sales

Nissin Food Holdings, Tokyo

Ref. code: 25605902040087AGC