Embed Size (px)

Citation preview

US tax reform, tax policy and IRS updates

Michael Mundaca, Ray Beeman,

Heather Maloy

Page 2

Disclaimer

► EY refers to the global organization, and may refer to one or more, of the member firms of Ernst &

Young Global Limited, each of which is a separate legal entity. Ernst & Young LLP is a client-serving

member firm of Ernst & Young Global Limited operating in the U.S.

► This presentation is © 2017 Ernst & Young LLP. All rights reserved. No part of this document may

be reproduced, transmitted or otherwise distributed in any form or by any means, electronic or

mechanical, including by photocopying, facsimile transmission, recording, rekeying, or using any

information storage and retrieval system, without written permission from Ernst & Young LLP. Any

reproduction, transmission or distribution of this form or any of the material herein is prohibited and

is in violation of U.S. and international law. Ernst & Young LLP expressly disclaims any liability in

connection with use of this presentation or its contents by any third party.

► Views expressed in this presentation are those of the speakers and do not necessarily represent the

views of Ernst & Young LLP.

► This presentation is provided solely for the purpose of enhancing knowledge on tax matters. It does not provide tax

advice to any taxpayer because it does not take into account any specific taxpayer’s facts and circumstances

► These slides are for educational purposes only and are not intended, and should not be relied upon, as accounting

advice.

3

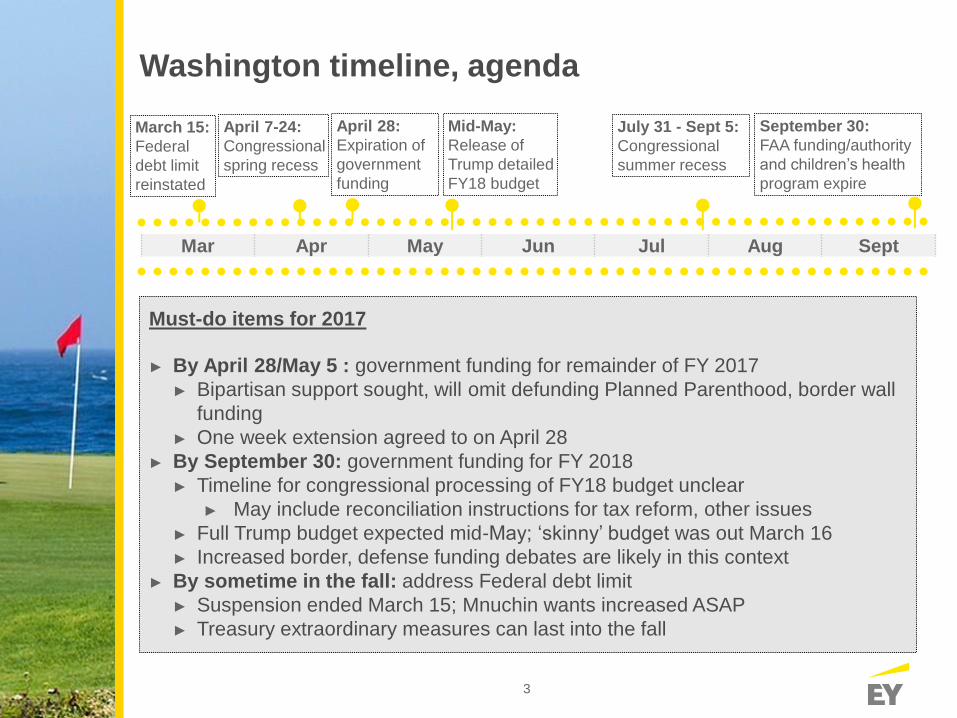

April 7-24:

Congressional

spring recess

Washington timeline, agenda

Mar Apr May Jun Jul Aug Sept

March 15:

Federal

debt limit

reinstated

September 30:

FAA funding/authority

and children’s health

program expire

Must-do items for 2017

► By April 28/May 5 : government funding for remainder of FY 2017

► Bipartisan support sought, will omit defunding Planned Parenthood, border wall

funding

► One week extension agreed to on April 28

► By September 30: government funding for FY 2018

► Timeline for congressional processing of FY18 budget unclear

► May include reconciliation instructions for tax reform, other issues

► Full Trump budget expected mid-May; ‘skinny’ budget was out March 16

► Increased border, defense funding debates are likely in this context

► By sometime in the fall: address Federal debt limit

► Suspension ended March 15; Mnuchin wants increased ASAP

► Treasury extraordinary measures can last into the fall

July 31 - Sept 5:

Congressional

summer recess

April 28:

Expiration of

government

funding

Mid-May:

Release of

Trump detailed

FY18 budget

4

Trump/Republican priorities, 2017

ACA repeal

► House bill pulled from consideration due to insufficient GOP support

► Would have repealed most ACA taxes beginning in 2017

► President says negotiations continue, wants to do before tax reform

Tax reform

► Administration at “beginning phases” of developing a new proposal

► NEC’s Cohn: We’re “going to launch with one cohesive plan together”

► Trump: doesn’t like term “border adjustment,” prefers reciprocal tax

Infrastructure

► Trump: very big infrastructure bill coming very soon

► “See it as part perhaps of the healthcare plan” to get Democratic votes

► Senate Democrats proposed $1T plan, includes closing tax loopholes

Regulatory

reform

► March 28 executive order calls for rolling back Obama climate policies,

including Clean Power Plan regulations for electric power plants

► January executive order calls for 2 regulations out for every new 1 in; April executive order requires review of all 2016 “significant” tax regs

Immigration► Trump calling for wall on Mexico border: $15-25b cost

► Budget bill unlikely to include wall funding that Democrats oppose

Trade

► Trump withdrew US from TPP; new USTR not yet confirmed

► Wants NAFTA renegotiated quickly; farmers, others concerned

► Did not act to deem China a currency manipulator

5

Effects of health bill outcome on tax reform

$/Process

Leadership

►Highlights awareness of the difficulty of advancing a major bill

►Trump, House GOP under greater pressure for legislative achievement

►Could increase wariness for including controversial tax elements

►GOP could seek Democratic tax reform votes with infrastructure tie-in

►GOP likely to try to line up support for tax proposal earlier in the

process

►Health bill would’ve repealed most ACA taxes in 2017 = $1 trillion cut

►If ACA taxes cut in tax reform, $1 trillion needed for revenue neutrality

►GOP could abandon revenue neutrality in favor of tax cut

►Health bill was crafted in House, Speaker Ryan was main advocate

►Administration has now asserted it take lead on tax reform

►OMB Dir. Mulvaney: “It will be the President’s plan,” we will drive debate

►Press Sec. Spicer: “Obviously, we’re driving the train on this.”

Politics

6

Tax reform: overall state of play

► House Republican Blueprint for tax reform:► Reduced individual tax rates: 12%, 25%, and 33%; standard deduction increased, other

deductions repealed, limited; capital gains, etc. effectively taxed at one-half of otherwise

applicable rate (NIT assumed repealed as part of healthcare reform)

► 20% corporate income tax rate/25% rate for business income of pass-throughs

► Immediate expensing of capital expenditures with no interest expense deduction

► Business provisions eliminated, except for R&D Credit and LIFO

► Territorial system of taxing future foreign earnings

► Mandatory tax (8.75%/3.5%) on accumulated foreign earnings

► Destination-basis tax system exempts exports while fully taxing imports

► Hearings in May?

House

Senate

Trump

Admin.

► Trump Administration:► Reduced individual tax rates: 10%, 25%, and 35%; double standard deduction; deductions, etc.

other than for charitable giving and home ownership, could be eliminated; tax relief for families

with child and dependent care expenses; current law rates for capital gains and dividends

maintained; 3.8% NIT repealed; AMT repealed; estate tax repealed

► 15% corp. tax rate, 15% pass-through business rate (for small- and medium-sized businesses?)

► “Eliminate tax breaks for special interests”

► Territorial system, with mandatory one-time tax on accumulated foreign earnings

► Senate: ► Does not have a companion to the House Blueprint

► Senate Finance Chairman Hatch: Senate will conduct its own tax reform process after the

House acts. Will not just accept House bill

► Hatch and other Senators have reservations about border adjustability and starting to question

need for revenue neutral bill

► Staff currently reviewing all options, including corporate integration

7

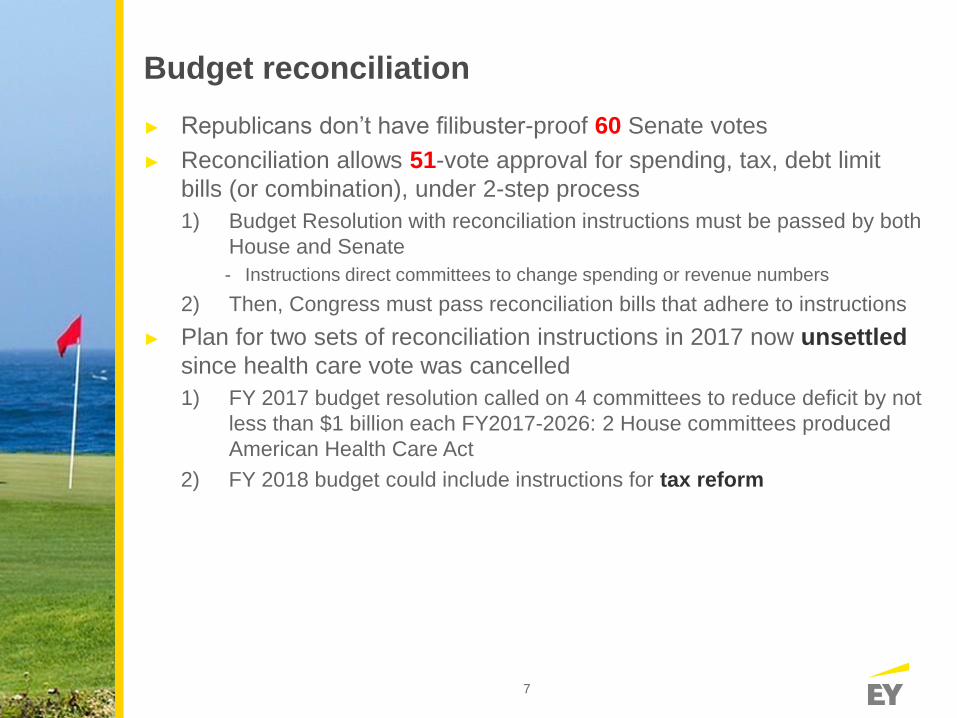

Budget reconciliation

► Republicans don’t have filibuster-proof 60 Senate votes

► Reconciliation allows 51-vote approval for spending, tax, debt limit

bills (or combination), under 2-step process

1) Budget Resolution with reconciliation instructions must be passed by both

House and Senate

- Instructions direct committees to change spending or revenue numbers

2) Then, Congress must pass reconciliation bills that adhere to instructions

► Plan for two sets of reconciliation instructions in 2017 now unsettled

since health care vote was cancelled

1) FY 2017 budget resolution called on 4 committees to reduce deficit by not

less than $1 billion each FY2017-2026: 2 House committees produced

American Health Care Act

2) FY 2018 budget could include instructions for tax reform

8

Budget reconciliation limitations

“Byrd Rule” protects views of minority party, prohibits extraneous matter

Six tests for matters to be considered extraneous and thus require 60 Senate votes to

waive point of order, applicable to provisions that:

Do not produce a change in outlays or revenues

Produce changes in outlays or revenue which are merely incidental to the non-

budgetary components of the provision

Are outside the jurisdiction of the committee that submitted the title or provision for

inclusion in the reconciliation measure

Increase outlays or decrease revenue if the provision's title, as a whole, fails to

achieve the Senate reporting committee's reconciliation instructions

Increase net outlays or decrease revenue during a fiscal year after the years covered

by the reconciliation bill unless the provision's title, as a whole, remains budget neutral

Contain recommendations regarding the OASDI (Social Security) trust funds

These limitations on reconciliation have practical effects, including:

► The 2001 Bush tax cuts were subject to a sunset after 10 years, and required subsequent legislation to make many provisions permanent

► The Affordable Care Act cannot be completely repealed under reconciliation

9

Key issues in tax reform debate

Border adjustability Individual taxes Interest deductibility

Pass-throughs Revenue/politics

► House Rs: Imports exempt from tax with cost of goods sold deductible; costs, including costs of goods sold, for imports non-deductible

► House proposal faces opposition from retailers, others, including Senate, maybe Trump

► Reform may be “revenue neutral”

► Democrats may or may not participate

► Reconciliation could require provisions to sunset after 10 years

► GOP can lose only two Senate votes if using reconciliation

► Trump proposed expensing for manufacturers, who then lose interest deductibility

► House Rs: expensing, eliminate deductibility of net interest expense

► Expensing may or may not be worth losing interest deductions

► Trump: 15% pass-through rate, 15% corporate rate

► House Republicans: 25% pass-through rate, 20% corporate rate

► Elimination of deductions, etc. to pay for rate cuts affects pass-through entities

► Trump and House Republicans propose top individual rate of 33%

► Lower tax rates on investment income

► Cuts to key individual tax benefits may create political fallout

► Payroll tax cut?

New international tax system

► Move from a global tax system to a territorial system?

► Eliminate income deferral?

► Mandatory tax on accumulated earnings

10

For and against border adjustability

Arguments for:

► Provides level playing field for

US companies; would bring

jobs, investment to US

► Eliminates incentive for profit-

shifting

► No need for anti-base erosion

provisions

► $1 trillion-plus in revenue

toward tax reform bill

► Exchange rate adjustment

would offset increased

taxes/prices for imported goods

► Advocates think WTO challenge

can be won

Arguments against:

► Too complicated

► Too much uncertainty

► Increased taxes for imported goods hits

retailers, passed to consumers

► May create negative net tax liability for

large exporters

► Wage deduction may violate WTO rule

that income taxes cannot favor exports

► Countries could retaliate outside of WTO,

arguing BAT is export subsidy

► Exchange rate adjustment uncertain,

could take a while

► And would reduce value of foreign

investments held by US investors, such as

pension funds, retirees

11

Senate Republicans on border adjustability

► Finance Chairman Hatch (R-UT): “at least a handful” of Senators have serious

reservations. Questions:

► Who will bear the tax? Consistent with WTO obligations? Burden on industries?

► Senate GOP Whip (#2 in charge) Cornyn (R-TX):

► Concerned about constituent refiners, manufacturers in supply chains with Mexico

► Don’t want the House to get momentum behind something that won’t pass Senate

► Scholars disagree on impact: “doesn’t seem to be any consensus”

► Senator Perdue (R-GA), former Reebok CEO:

► BAT “regressive, hammers consumers… Increase in consumer prices”

► “[C]urrency revaluation = multi-trillion dollar reduction in the value of foreign

investments held by US investors,” including pension funds, retirees

► Senator Cotton (R-AR): affects prices of food, apparel, toys, gas

► Taxes working class “to lower marginal rates for corporations”

► Senator Rounds (R-SD): need to know impact on economy

► Senator Moran (R-KS): worries over constituents paying tax, trade war

► “I assume you get into a battle with other countries… and it affects the exporters.”

12

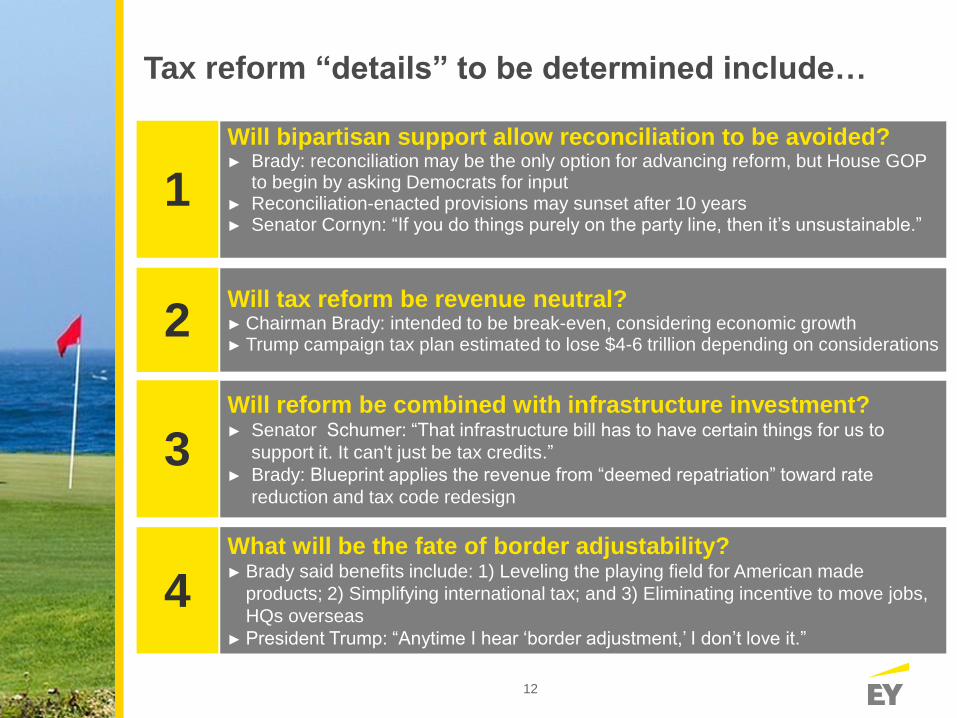

Tax reform “details” to be determined include…

1

Will tax reform be revenue neutral?► Chairman Brady: intended to be break-even, considering economic growth► Trump campaign tax plan estimated to lose $4-6 trillion depending on considerations

2

3

4What will be the fate of border adjustability?► Brady said benefits include: 1) Leveling the playing field for American made

products; 2) Simplifying international tax; and 3) Eliminating incentive to move jobs,

HQs overseas

► President Trump: “Anytime I hear ‘border adjustment,’ I don’t love it.”

Will reform be combined with infrastructure investment?► Senator Schumer: “That infrastructure bill has to have certain things for us to

support it. It can't just be tax credits.”

► Brady: Blueprint applies the revenue from “deemed repatriation” toward rate

reduction and tax code redesign

Will bipartisan support allow reconciliation to be avoided?► Brady: reconciliation may be the only option for advancing reform, but House GOP

to begin by asking Democrats for input► Reconciliation-enacted provisions may sunset after 10 years► Senator Cornyn: “If you do things purely on the party line, then it’s unsustainable.”

13

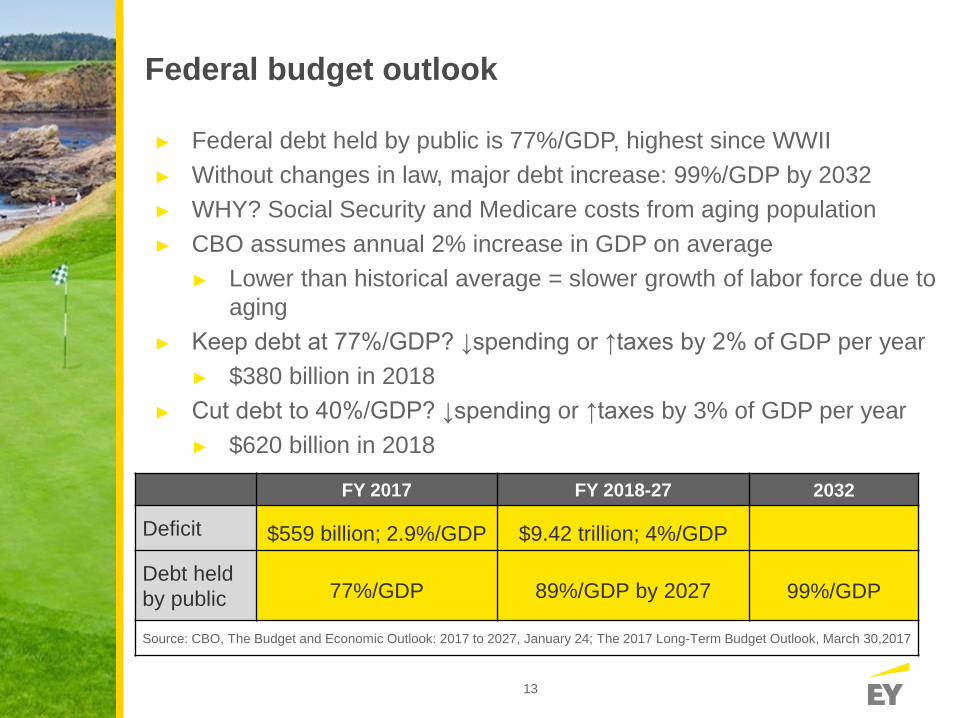

Federal budget outlook

FY 2017 FY 2018-27 2032

Deficit $559 billion; 2.9%/GDP $9.42 trillion; 4%/GDP

Debt held

by public 77%/GDP 89%/GDP by 2027 99%/GDP

Source: CBO, The Budget and Economic Outlook: 2017 to 2027, January 24; The 2017 Long-Term Budget Outlook, March 30,2017

► Federal debt held by public is 77%/GDP, highest since WWII

► Without changes in law, major debt increase: 99%/GDP by 2032

► WHY? Social Security and Medicare costs from aging population

► CBO assumes annual 2% increase in GDP on average

► Lower than historical average = slower growth of labor force due to

aging

► Keep debt at 77%/GDP? ↓spending or ↑taxes by 2% of GDP per year

► $380 billion in 2018

► Cut debt to 40%/GDP? ↓spending or ↑taxes by 3% of GDP per year

► $620 billion in 2018

14

Trump budget perspectives

► Trump promised not to cut Social Security or Medicare

► Trump has focused comments more on tax cuts than reform

► Unclear if Administration’s plan is revenue neutral

► ‘Skinny’ budget cut discretionary to boost defense $54B

► Would not achieve any deficit reduction

► Tax cut could add to deficit, but arguably increase growth

“We believe we can be competitive and get back to sustainable

growth at 3% or more. There’s going to be a lot of things that

will impact it. I think the first issue … is going to be tax reform.”

Treasury Secretary Mnuchin, February 27

15

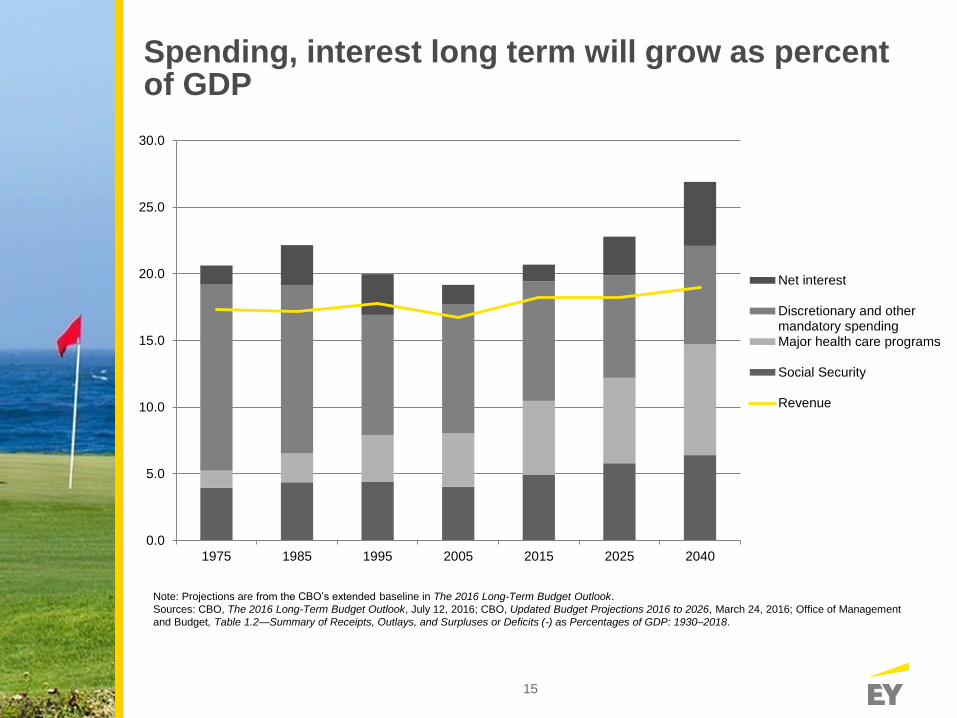

Spending, interest long term will grow as percent of GDP

Note: Projections are from the CBO’s extended baseline in The 2016 Long-Term Budget Outlook.

Sources: CBO, The 2016 Long-Term Budget Outlook, July 12, 2016; CBO, Updated Budget Projections 2016 to 2026, March 24, 2016; Office of Management

and Budget, Table 1.2—Summary of Receipts, Outlays, and Surpluses or Deficits (-) as Percentages of GDP: 1930–2018.

0.0

5.0

10.0

15.0

20.0

25.0

30.0

1975 1985 1995 2005 2015 2025 2040

Net interest

Discretionary and othermandatory spendingMajor health care programs

Social Security

Revenue

16

Federal debt, long term

0

20

40

60

80

100

120

140

160

2017:

77% of GDP

2018–2027:

89% of GDP

Projected annual average

2028–2037:

113% of GDP

Projected annual average

2038–2047:

150% of GDP

Projected annual average

Source: CBO, The 2017 Long-Term Budget Outlook, March 30,2017

40% = average of past 50 years

100%

17

Internal Revenue Service update

18

IRS budget challenges

Even though there was a small $290 million increase in 2016, it was

barely enough to keep up with inflation. As a result, IRS funding was still

17 percent below the 2010 level, adjusted for inflation.

$0 $2 $4 $6 $8 $10 $12 $14

19

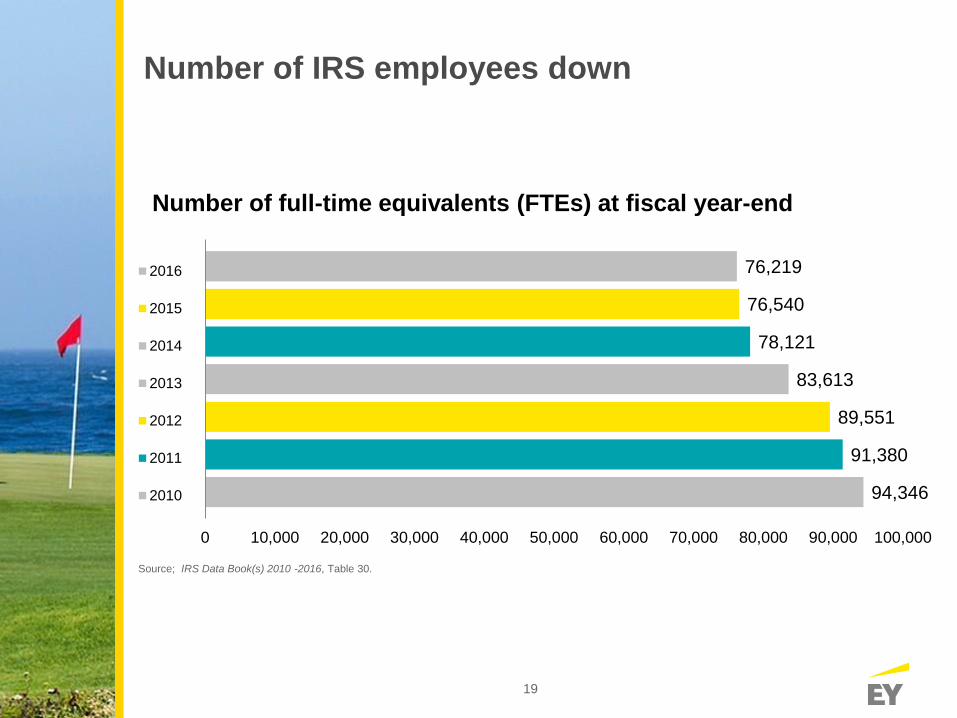

Number of IRS employees down

Source; IRS Data Book(s) 2010 -2016, Table 30.

94,346

91,380

89,551

83,613

78,121

76,540

76,219

0 10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000 90,000 100,000

Number of full-time equivalents (FTEs) at fiscal year-end

2016

2015

2014

2013

2012

2011

2010

20

IRS workforce composition

► In the next several years, close to 35% of IRS workforce will be

eligible to retire

► 40% of managers

► 50% of executives

► Number of Revenue Agents has fallen 25% since 2010

► Only 122 full-time employees 25 years old or younger out of a

workforce of about 77,000, less than one-half of one percent.

21

Changing controversy landscapeImpact on taxpayers

► Large Business & International Division (LB&I)

Campaigns

► Update on LB&I’s Examination Process

► Update on Appeals

22

Questions?

EY | Assurance | Tax | Transactions | Advisory

About EY

EY is a global leader in assurance, tax, transaction and advisory

services. The insights and quality services we deliver help build trust

and confidence in the capital markets and in economies the world

over. We develop outstanding leaders who team to deliver on our

promises to all of our stakeholders. In so doing, we play a critical role

in building a better working world for our people, for our clients and

for our communities.

EY refers to the global organization, and may refer to one

or more, of the member firms of Ernst & Young Global Limited, each

of which is a separate legal entity. Ernst & Young

Global Limited, a UK company limited by guarantee, does not

provide services to clients. For more information about our

organization, please visit ey.com.

Ernst & Young LLP is a client-serving member firm of

Ernst & Young Global Limited operating in the US.

© 2017 Ernst & Young LLP.

All Rights Reserved.

ED None

This material has been prepared for general informational purposes

only and is not intended to be relied upon as accounting, tax or other

professional advice. Please refer to your advisors for specific advice.

ey.com