Embed Size (px)

Citation preview

Exhibit 2

U.S. Small Business Administration

Office of Credit Risk Management

504 Loan Program

SMART Execution Guidance

THIS DOCUMENT IS STRICTLY CONFIDENTIAL

This review plan is the property of the U.S. Small Business Administration, Office of Credit Risk Management. Under no circumstances shall any recipient of this plan disclose or make public this document or any portion thereof. Unauthorized disclosure of any of the contents of this document is subject to the penalties in 18 USC 641. The Office of Credit Risk Management must be notified immediately if the examined entity receives a subpoena or other legal process calling for the production of this document.

Review Plan

Page | 2 of 27

Table of Contents

Subject Page

CDC Review Background 3

SCOPE 4

Prior Review Results & Areas of Concern 6

SCHEDULE, RESOURCE ESTIMATES AND AUTHORIZATIONS 6

ATTACHMENTS:

A - LEADSHEET SUMMARIES

1. Solvency and Financial Condition 8

2. Management and Board Governance: 9

3. Asset Quality and Servicing 14

4. Regulatory Compliance 20

5. Technical Issues and Mission 22

B – LOAN SAMPLE 25

C – Board of Directors Questions 26

D – File Deficiency and CDC Response 27

Review Plan

Page | 3 of 27

CDC Review Background

The purpose of this review plan is to outline the background, scope, objectives and approach for

reviewing [CDC NAME] the week of [DATE].

[CDC NAME] is an SBA Certified Development Company (CDC) located in [CITY, STATE]

NH. In addition to [STATE], [CDC NAME] has a multi-state lending authority or local economic

area expansion in [STATE].

As of [DATE], [CDC NAME] [provide description of SBA portfolio].

Active Balance by Delivery Method

Delivery

Method

Gross

Loans # Gross Loans $

Total

This was previously reviewed by the Office of Credit Risk Management on the week of [DATE] resulting in an assessment of [Assessment].

CDC has [PCLP and/or ALP] authority that expires on [DATE]. [Describe level of delegated authority].

SCOPE

The Review of [CDC NAME] is considered a [Full Risk Based Review or Targeted Risk Based

Review] that it is focus on the [ # of SMART components]: [Select Component to be Reviewed:

1) Solvency and Financial Condition, 2) Management and Board Governance, 3) Asset Quality and

Servicing, 4) Regulatory Compliance, and 5) Technical Issues and Mission]. The review will

specifically focus on the following areas regarding:

SOLVENCY AND FINANCIAL CONDITION– aka financial ability to operate,

including the following areas

Profitability

Net Asset Position

Adequacy of Reserves

Funds generated from 504 loans after payment of staff and overhead

Contributions from government or other sponsors

Cash Management

PCLP Loan Loss Reserve Amount

Authorize signers on Operating Account and other accounts

MANAGEMENT AND BOARD GOVERNANCE

Does the board properly govern the CDC?

Does board maintain an awareness of CDC’s performance?

Does board appear independent of management?

Review Plan

Page | 4 of 27

Did board establish an approved Internal Control Policy in accordance with

13 CFR 120.826(b)?

Are board and management receiving sufficient training on CDCs and the

SBA 504 program to properly fulfill their role and responsibility?

Is CDC management actively involved in day-to-day operations of CDC?

Are there conflicts of interest, self-dealing, or self-promoting form the

taxpayer supported CDC (or board)?

Loan committees

ASSET QUALITY AND SERVICING

Are performance metrics representative of acceptable risk?

Does the CDC have the proper systems for marketing, underwriting,

processing, closing, servicing and liquidating 504 loans?

Does CDC have prudent underwriting practices?

Are internal controls implemented to ensure SBA loan program

requirements are met regarding requesting, obtaining and analyzing annual

financial statements? Are they sending additional request letters and

obtaining credit reports?

Are policies, procedures and internal controls effectively implemented to

ensure compliance with all eligibility issues regarding EPC/OC eligibility?

Does the CDC have written credit policies?

Is the CDC proactive in managing its outstanding loan portfolio?

Was the underwriting repayment analysis adequate?

If debt service ability relied on sales projections, were the sales projections

reasonable and did the CDC question them?

Is there adequate analysis to justify deferments?

Were the “No Adverse Change” notices accurate for the three Early

Default loans?

REGULATORY COMPLIANCE

Is the CDC submitting all required reports to SBA in an accurate and

timely manner?

Is the CDC in compliance with SBA regulations concerning its 504

lending activities and operations?

Are policies, procedures and internal controls in place to ensure SBA Loan

Program Requirements are met?

Did CDC establish a periodic loan review function for its SBA loan

portfolio, to ensure management of its SBA loans in accordance with SBA

Loan Program Requirements?

Was the economic impact of loans adequately analyzed?

Is CDC in good standing with the IRS and all states in which it does

business (Check License)?

Are policies, procedures, and internal controls in place regarding the

annual risk rating of loan (timeliness) and CDC liquidation policy?

Were other compliance issues adequately addressed such as equity

injection verifications, the 51% occupancy requirement, environmental

assessments, and relevant owners guaranteed the loan?

Review Plan

Page | 5 of 27

Does the CDC’s D&O Insurance policy meet the requirements? Does it exclude

SBA? Is there a 20 day cancelation notice requirement?

Does the CDC have designated attorneys? Do they meet SBA requirements

(malpractice insurance, SBA training, proof of license in the state, etc.)?

TECHNICAL ISSUES AND MISSION

Is classifying its SBA loan in accordance with prudent lender practice?

Does the CDC adequately document its jobs created/retained numbers for all of its

loans?

Does the CDC participate in other economic development?

Does the CDC act as an LSP for other lenders?

Does the CDC have Professional Services Contracts?

Are there concentrations in the CDC’s portfolio? Does the CDC monitor and

manage these concentrations (Reporting to the Board)?

Does the CDC have a business plan for SBA lending, including SBA loan program

goals?

EVALUATIVE CRITERIA

Reviews will be conducted within the general parameters established by SBA’s Standard

Operating Procedures 51 00 – On-Site Lender Reviews/Reviews (SOP 51 00). SOP 51 00 will be

supplemented by other authoritative guidance, such as accounting standards or practices, or

auditing principles, as appropriate. The CDC’s operations will also be measured against other

SBA Standard Operating Procedures (SOPs), and sound business practices, as well as any

agreements between SBA and the CDC. The SBA’s SOPs are available online at www.sba.gov

under the library link.

Attachment A contains leadsheets that outline the specific objective, scope and approach, and

criteria for each Review area. Adjustments to the Review scope may be made, as determined

necessary by the contractor with concurrence of the SBA 504 oversight manager. As conditions

warrant, the Review scope and approach may be modified by the Reviewer in Charge, so long as

conclusions may be reached that adequately address the leadsheet objectives. Individual loan

findings and conclusions will be documented on an electronic workpaper. This workpaper will be

sent to each examiner before the pre-Review meeting.

Prior Review Results: The last Review was performed in [Year]. The summary assessment of

[CDC NAME] was [Assessment]. The Review identified [Findings] that needed management’s

attention.

Documentation Requirements: This Review will focus on the lender’s credit administration

processes (gathering, verifying, analysis, documentation, and/or controls and servicing processes)

on new loans.

Loan Selection: The loan portfolio is composed of [#] loans and SBA has chosen to review a

sample of [#] loans. [#] loans were [Judgmentally or Randomly] selected based on [Criteria].

ASSIGNMENTS AND WORKPAPER ORGANIZATION

The following table shows lead staff assignments and a workpaper index for this Review. The

staff assignments may be changed at the sole discretion of the Examiner in Charge (“EIC”). The

Review Plan

Page | 6 of 27

workpaper index will be used to organize the workpapers; however, flexibility exists to modify this

as circumstances dictate; however, workpapers will be cross referenced as prescribed in SOP 51

00. Any desired changes should be communicated to the EIC for concurrence.

Lead-

sheet

Work

Paper

Section

Assignment

Examiner(s)

Examiner in Charge

A Report of Review

B Review Planning

C Correspondence & other misc. materials

1 D Solvency and Financial Condition

2 E Management and Board Governance

3 F Asset Quality and Servicing

4 G Regulatory Compliance

5 H Technical Issues and Mission

6 I Loan workpaper support

7 J Quality Assurance

8 Supervisory Review

SCHEDULE, RESOURCE ESTIMATES AND AUTHORIZATIONS

The onsite Review schedule is based on a one-week onsite Review conducted by [#] contract

reviewers [Name of Contractors] from [Contracting Company], two representative from SBA’s

Office of Credit Risk Management [Name of SBA Employees], SBA District Counsel [Name]

from [State] District Office, and [Name] who is [Title] in SBA’s [Department Name] Servicing

Center.

The first onsite date will be [DATE] and the last onsite date is expected to be [DATE]. The

expected delivery date for the Risk Based Review Report (Report) to SBA is [DATE].

Adjustments to the schedule may be made, as determined necessary by [Contracting Company],

with concurrence of SBA.

.

Key Review dates are as follow:

ACTIVITY DUE DATES

Advance Letter

Draft Review Plan to Contractor

Approved Review Plan

Call with Contractors to go over PrePlan

Entrance Conference

Onsite Review Work

Exit Conference

Complete Section Summaries

Draft of Report Prepared by [Contracting

Company]

Draft Report from [FA] to [Supervisor]

Draft of Report to [OCRM Director]

Review Plan

Page | 7 of 27

Issue Report

[CDC NAME]Contact Info:

[CDC NAME]Board Members selected for Interviews:

[CDC NAME]Staff to interview:

Review Plan

Page | 8 of 27

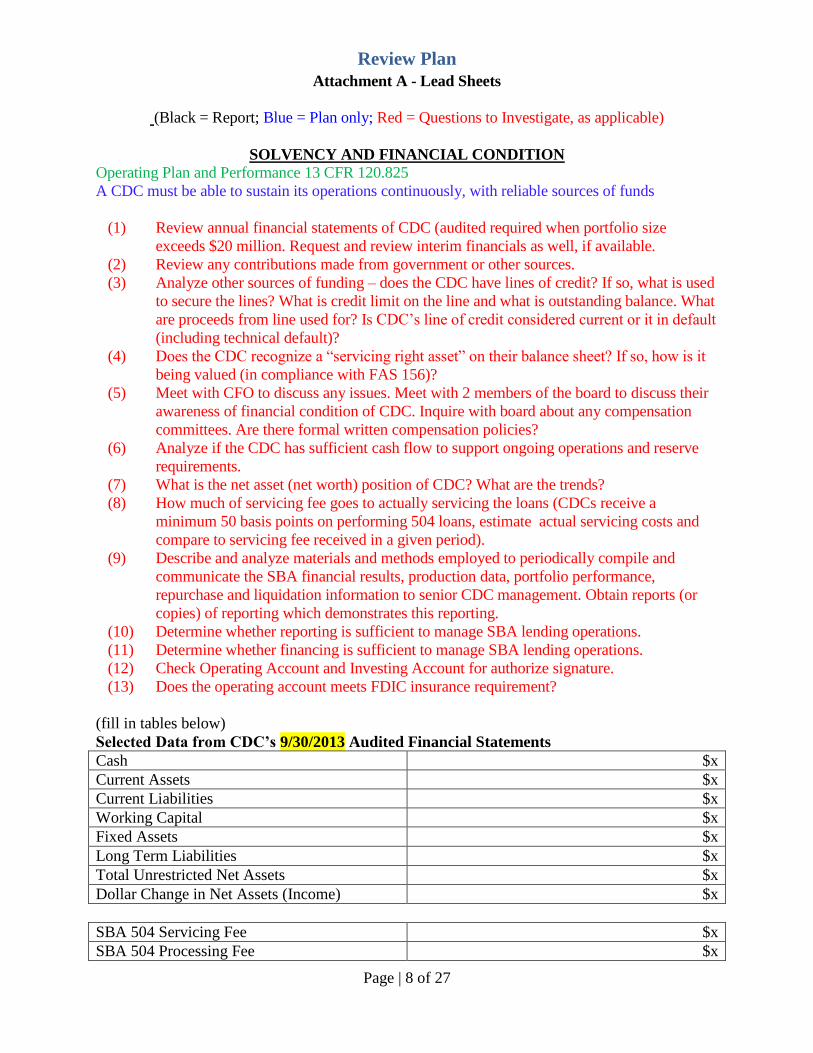

Attachment A - Lead Sheets

(Black = Report; Blue = Plan only; Red = Questions to Investigate, as applicable)

SOLVENCY AND FINANCIAL CONDITION

Operating Plan and Performance 13 CFR 120.825

A CDC must be able to sustain its operations continuously, with reliable sources of funds

(1) Review annual financial statements of CDC (audited required when portfolio size

exceeds $20 million. Request and review interim financials as well, if available.

(2) Review any contributions made from government or other sources.

(3) Analyze other sources of funding – does the CDC have lines of credit? If so, what is used

to secure the lines? What is credit limit on the line and what is outstanding balance. What

are proceeds from line used for? Is CDC’s line of credit considered current or it in default

(including technical default)?

(4) Does the CDC recognize a “servicing right asset” on their balance sheet? If so, how is it

being valued (in compliance with FAS 156)?

(5) Meet with CFO to discuss any issues. Meet with 2 members of the board to discuss their

awareness of financial condition of CDC. Inquire with board about any compensation

committees. Are there formal written compensation policies?

(6) Analyze if the CDC has sufficient cash flow to support ongoing operations and reserve

requirements.

(7) What is the net asset (net worth) position of CDC? What are the trends?

(8) How much of servicing fee goes to actually servicing the loans (CDCs receive a

minimum 50 basis points on performing 504 loans, estimate actual servicing costs and

compare to servicing fee received in a given period).

(9) Describe and analyze materials and methods employed to periodically compile and

communicate the SBA financial results, production data, portfolio performance,

repurchase and liquidation information to senior CDC management. Obtain reports (or

copies) of reporting which demonstrates this reporting.

(10) Determine whether reporting is sufficient to manage SBA lending operations.

(11) Determine whether financing is sufficient to manage SBA lending operations.

(12) Check Operating Account and Investing Account for authorize signature.

(13) Does the operating account meets FDIC insurance requirement?

(fill in tables below)

Selected Data from CDC’s 9/30/2013 Audited Financial Statements

Cash $x

Current Assets $x

Current Liabilities $x

Working Capital $x

Fixed Assets $x

Long Term Liabilities $x

Total Unrestricted Net Assets $x

Dollar Change in Net Assets (Income) $x

SBA 504 Servicing Fee $x

SBA 504 Processing Fee $x

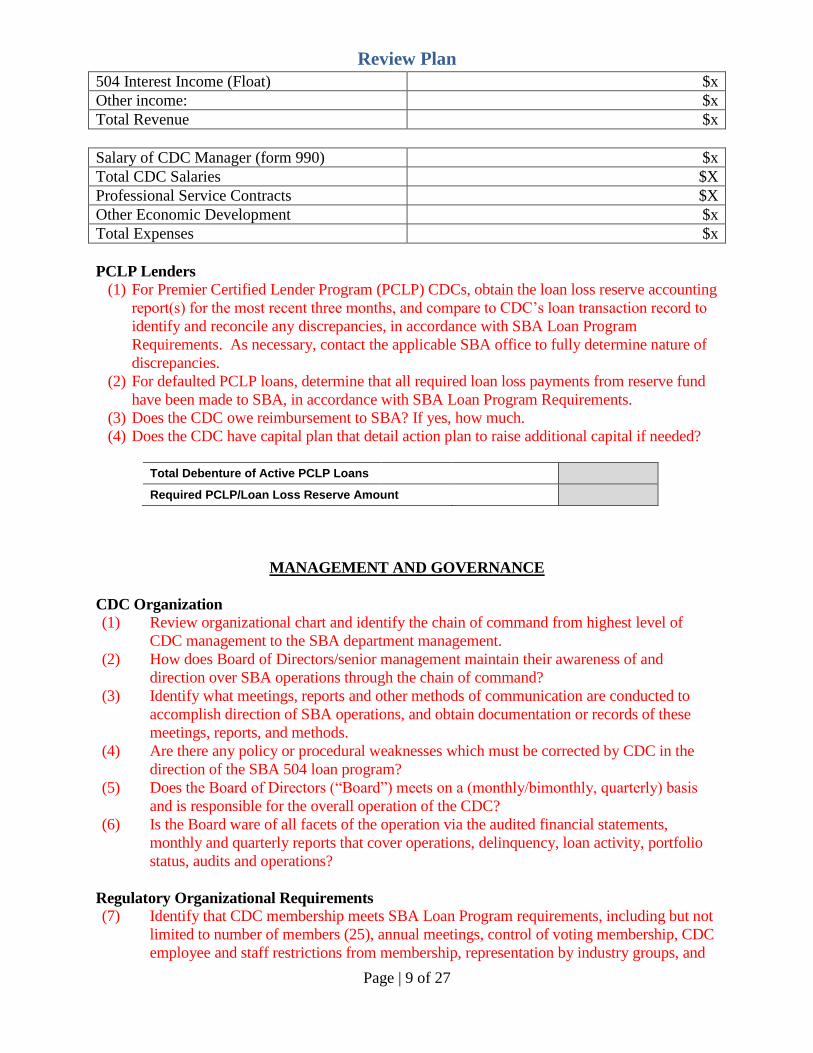

Review Plan

Page | 9 of 27

504 Interest Income (Float) $x

Other income: $x

Total Revenue $x

Salary of CDC Manager (form 990) $x

Total CDC Salaries $X

Professional Service Contracts $X

Other Economic Development $x

Total Expenses $x

PCLP Lenders

(1) For Premier Certified Lender Program (PCLP) CDCs, obtain the loan loss reserve accounting

report(s) for the most recent three months, and compare to CDC’s loan transaction record to

identify and reconcile any discrepancies, in accordance with SBA Loan Program

Requirements. As necessary, contact the applicable SBA office to fully determine nature of

discrepancies.

(2) For defaulted PCLP loans, determine that all required loan loss payments from reserve fund

have been made to SBA, in accordance with SBA Loan Program Requirements.

(3) Does the CDC owe reimbursement to SBA? If yes, how much.

(4) Does the CDC have capital plan that detail action plan to raise additional capital if needed?

Total Debenture of Active PCLP Loans

Required PCLP/Loan Loss Reserve Amount

MANAGEMENT AND GOVERNANCE

CDC Organization

(1) Review organizational chart and identify the chain of command from highest level of

CDC management to the SBA department management.

(2) How does Board of Directors/senior management maintain their awareness of and

direction over SBA operations through the chain of command?

(3) Identify what meetings, reports and other methods of communication are conducted to

accomplish direction of SBA operations, and obtain documentation or records of these

meetings, reports, and methods.

(4) Are there any policy or procedural weaknesses which must be corrected by CDC in the

direction of the SBA 504 loan program?

(5) Does the Board of Directors (“Board”) meets on a (monthly/bimonthly, quarterly) basis

and is responsible for the overall operation of the CDC?

(6) Is the Board ware of all facets of the operation via the audited financial statements,

monthly and quarterly reports that cover operations, delinquency, loan activity, portfolio

status, audits and operations?

Regulatory Organizational Requirements

(7) Identify that CDC membership meets SBA Loan Program requirements, including but not

limited to number of members (25), annual meetings, control of voting membership, CDC

employee and staff restrictions from membership, representation by industry groups, and

Review Plan

Page | 10 of 27

multi-state requirements. 13 CFR 120.822. Get list of CDC Members that shows

membership type and if the member is voting or non-voting.

(8) Identify that Board of Directors meet SBA Loan Program requirements, including but not

limited to membership group composition, control issues, no CDC staff except for CDC

manager, commercial lending experience requirements, quarterly meeting requirements,

quorum requirements, and/or Loan Committee requirements. 13 CFR 120.823

a. A CDC must have a Board of Directors chosen from the membership by the

members and representing at least three of the four membership groups.

b. No person who is a member of a CDC’s staff may be a voting member of the

Board except for the CDC manager.

c. At least one member other than the CDC manager must possess commercial

lending experience.

d. When the Board votes on SBA loan approval or servicing actions, at least one

Board Member with commercial loan experience acceptable to SBA, other than

the CDC manager, must be present and vote. There must be no actual or

apparent conflict of interest.

e. The Board may establish a Loan Committee of non- Board members that

reports to the Board. Loan Committee members must include at least 1 member

with commercial lending experience.

Get list of CDC Board Members that shows board membership type and if the board

member is voting or non-voting.

(9) Is there a loan committee or executive committee? If yes, does it meet 13 CFR 120.823?

(10) Identify that the professional management and staff meet SBA Loan Program

requirements, including but not limited to Executive Director requirement and

professional staff requirements and qualifications. 13 CFR 120.824

a. Members must be responsible for actively supporting economic development in

the Area of Operations and must be from one of the following groups:

government organizations responsible for economic development in the Area of

Operations; financial institutions that provide commercial long term fixed asset

financing in the Area of Operations; community organizations dedicated to

economic development in the Area of Operations such as chambers of

commerce, foundations, trade associations, college, universities, or small

business development centers; businesses in the Area of Operations

b. CDC must have at least one salaried professional employee who is employed

directly full time to manage the CDC. The CDC manager must be hired by the

CDC’s board of directors and subject to termination only by the board.

(11) Determine that the Operating CDC has met SBA Loan Program requirements, including

but not limited to professional staff requirements, SBA pre-approval for any contract

relationships, operating requirements, maintenance of records and documents and changes

in operations or location.

(12) Determine that the Operating CDC has met SBA Loan Program requirements regarding

Resumes, “Statement of Personal History” SBA Form 1081 and fingerprint cards Form

FD 258 on all associates and staff

(13) Identify that the CDC has filed quarterly service reports on each loan 60 days or more past

due.

(14) Determine CDC is in good standing in state incorporated, and any other state in which

CDC does business.

Review Plan

Page | 11 of 27

a. CDC must comply with all laws, including taxation requirements in the state in

which the CDC is incorporated or where it conducts business.

b. CDC must have satisfactory SBA performance as determined by SBA in its

discretion (e.g. consider CDC’s risk rating). Other factors include historical

performance measures (e.g. default rate, purchase rate, and loss rate), loan

volume to the extent that it impacts performance measures, and other

performance related measurements and information

(15) Identify any other deficiencies with regard to regulatory requirements.

(16) For Non-Profit CDCs: Determine if CDC meets the requirements of the Single Audit Act

Amendments of 1996 (31 USC 7501-7507) and revised OMB Circular A-133, Audits of

States, Local Governments, and Non-Profit Organizations.

(17) Determine if any long-range planning demonstrates a significant change to the CDC’s

approach to its SBA program. Describe the proposed change(s) and management’s intent.

Is it prudent?

(18) Determine if management is knowledgeable of SBA lending requirements.

Delegations of Authority

(19) Determine that delegations related to the SBA program for loan approval and servicing

authority are approved by the BOD or senior management, and that documentation related

to the delegations confirms this.

(20) Determine that the CDC is complying with its loan approval process. Senior

Management has to approve the loan before it’s presented to the Loan Committee

and Board.

(21) Analyze the approval timeline by the Senior Manager, Loan Committee and Board.

(22) Determine that CDC management communicated its delegations to the SBA portfolio staff

to meet the goals and objectives of senior direction?

(23) Assess what internal controls exist to ensure that exceptions to delegations are properly

handled?

(24) Determine what the CDC does to train and maintain proficiency in lending for its SBA

personnel.

Training

(25) What, if any, training opportunities does CDC offer to SBA personnel?

(26) How often, if ever, does CDC conduct training on its SBA program?

Legal Structure

(27) Current bylaws reviewed by the district and HQ?

(28) Current bylaws are in compliance?

Review Plan

Page | 12 of 27

Internal Controls and Oversight 13 CFR 120.826

(29) Each CDC’s board of directors must adopt internal control policy which provides

adequate direction for effective control over and accountability for operations, programs

and resources. At minimum it must include:

a. Assignment of responsibility for internal control function to an officer or

officers;

b. Adopt procedures for maintenance and periodic review of the internal control

function;

c. Direct a program to review and assess the CDC’s 504-related loans, specifically

including review standards, including standards for work papers and supporting

documentation; loan quality classification standards; specific control

requirements for oversight of Lender Service Providers; and standards for

training.

(30) Determine the nature and frequency of the internal activities that provide oversight data

and information to the SBA management.

(31) Determine that the CDC has an internal control policy which provides adequate direction

for effective control over and accountability for operations, programs, and resources and

meets SBA Loan Program Requirements, including but not limited to assigning

responsibility for the policy to an officer/officers, containing procedures for periodic

review of the policy, containing procedures for reviewing and assessing the 504-related

loans, specifying review standards including loan quality classification standards,

specifying procedures for the CDC’s oversight of Lender Service Provides, and specifying

standards of training to implement the loan review program.

(32) Determine that the Board of Directors has adopted the internal control policy in

accordance with SBA Loan Program Requirements.

(33) Determine whether CDC’s Board of Directors adopted an internal control policy which

provides adequate direction to the institution for effective control over and accountability

for operations, programs, and resources. Determine that the board adopting internal

control policy satisfies the following requirements at a minimum:

a. Direct management to assign the responsibility for the internal control function

(covering financial, credit, credit review, collateral and administrative matters)

to an officer of a CDC

b. Adopt and set forth procedures for maintenance and periodic review of the

internal control function

c. Direct the operation of a program to review and assess the CDC’s 504-related

loans.

(34) For the 504 review program, the internal control policies must specify the following:

b. Loan, loan-related collateral, and appraisal review standards, including

standards for scope of selection and standards for work papers and related

documents

c. Loan quality classification standards consistent with the standardized

classification systems used by the Federal Financial Institution Regulators

d. Specific control requirements for the CDC’s oversight of Lender Service

Providers

e. Standards for training to implement the loan review program

(35) Identify the types of independent review being used to oversee the SBA lending program

(i.e. internal and external audits). (This is not reporting, but review independent of the

loan program management).

Review Plan

Page | 13 of 27

(36) Review any internal audit reports or compliance Reviews of SBA lending operation and

review findings and recommendations for material deficiencies.

(37) Determine what action(s) have been taken by CDC to address any identified deficiencies.

Risk Rating System 13 CFR §120.826

(38) Determine whether CDC lender uses appropriate, prudent, and generally accepted industry

credit analysis processes and procedures.

(39) Evaluate policies for internal grading and/or risk rating SBA loans, and practices for rating

loans at regular intervals through life of loan (at least annually).

(40) Determine whether CDC lenders validate (and document) with appropriate and accepted

statistical methodologies that their business credit scoring model, if any, is predictive of

loan performance, and they must provide that documentation to SBA upon request.

(41) Determine how these rating systems affect CDC’s SBA portfolio management.

(42) Who is responsible for maintaining accurate risk ratings?

(43) Review management reports containing grades or risk ratings of all SBA loans.

(44) Determine whether CDC’s criteria for assigning each rating is clear and precisely defined

using objective and subjective factors.

(45) Determine whether the ratings reflect the risks posed by both the borrower’s expected

performance and the transaction.

(46) Determine whether assumptions implicit in the rating definitions accurately anticipate

outcomes.

External Oversight

(47) To what extent are the SBA program and/or the SBA loan portfolio subjected to third

party/independent Review, review or audit over past three years or since most recent SBA

review?

(48) Obtain and review copies of available independent reports, reviews or audits on CDC’s

SBA portfolio. Review report findings and recommendations for material deficiencies.

Determine what action(s) taken by CDC to address deficiencies and results achieved.

(49) Determine that CDC has submitted annual audited financial statements in accordance with

13 CFR § 120.826(c) and § 120.830, as applicable.

f. Each CDC with a 504 loan portfolio balance of $20 million or more must have

its financial statements audited annually by a certified public accountant that is

independent and experienced in auditing financial statements

g. For CDCs with a portfolio balance of less than $20million, the CDC’s annual

financial statements submitted to SBA must be reviewed by an independent

CPA in accordance with GAAP.

(50) Discuss all management and operations findings with CDC management.

(51) Note any relevant CDC input.

(52) Conclude on adequacy of SBA program management.

Review Plan

Page | 14 of 27

CDC Service Provider

(53) Any contracts for the managing, marketing, packaging, processing, closing, servicing or

liquidating functions at the CDC approved by SBA?

(54) Provide list of CDC Service Providers with name, job description, and when it was

approved by SBA HQ.

(55) What contracts does the principal have with other CDCs? Provide the name of the CDCs

and the work that is done.

(56) What time do they spend providing service for other CDCs?

Scott Gardiner got paid $55,706.98 on January 14, 2013 ($125 per hour total 446 hours)

Scott Gardiner got paid $49,325.48 on January 19, 2012 ($125 per hour total 395 hours)

Alan Abraham got paid $39,875.00 on March 30, 2012 ($125 per hour total 319 hours)

(57) Do you sign on any of these CDCs’ operating account or any other deposit account?

Findings and Corrective Actions

(1) Identify any Finding that requires a Corrective Action.

Identify the Corrective Action that corresponds to each Finding.

ASSET QUALITY AND SERVICING

Credit Underwriting Policies

(1) Determine that the CDC has established prudent underwriting practices for its SBA

program.

(2) Determine that the CDC’s SBA loan purpose clearly reflects actual use of the proceeds.

(3) Determine that the CDC maintains prudent credit underwriting practices for its SBA

program that meet the following criteria:

a. Are commensurate with the types of loans the institution will make and consider the

terms and conditions under which they will be made.

b. Consider the nature of the markets in which loans will be made.

c. Consider the borrower’s overall financial condition and resources, the financial

responsibility of any guarantor, the nature and value of any underlying collateral, and

the borrower’s character and willingness to repay as agreed.

d. Determine whether loan approval documentation contains sufficient analysis of

financial trends, industry trends, and risk mitigants.

e. Establish a system of independent, ongoing credit review of SBA loans and appropriate

communication to management and to the board of directors.

f. Take adequate account of concentration of credit risk (geographic and industry).

g. Are appropriate to the size of the institution and the nature and scope of its activities.

h. Are appropriate to the size of the CDC’s SBA portfolio.

Creditworthiness 13 CFR §120.150

Applicant must be creditworthy. Loans must be so sound as to reasonably assure

repayment. SBA will consider:

a. character, reputation, and credit history of the applicant, its associates, and

guarantors;

b. experience and depth of management;

c. strength of the business;

Review Plan

Page | 15 of 27

d. past earnings, projected cash flow, and future prospects;

e. ability to repay the loan with earnings from the business;

f. Sufficient invested equity to operate on a sound financial basis;

g. potential for long-term success;

h. nature and value of collateral (although inadequate collateral will not be the sole

reason for denial of a loan request);

i. the effect any affiliates may have on the ultimate repayment ability of applicant.

(4) Determine whether CDC’s SBA loan procedures establish requirements for

creditworthiness that, at minimum, include positive determination of repayment ability,

sufficient cash flow to fund operations, adequate management ability, adequate

capitalization and satisfactory credit history consistent with SBA Loan Program

Requirements.

(5) Determine whether CDC’s SBA credit policy demonstrates the ability to evaluate and

process SBA loans in accordance with SBA Loan Program Requirements.

(6) Review sample of loans to determine whether CDC is adhering to all loan policies and all

SBA loan policy requirements, and identify and provide examples of any material

deficiencies or patterns of deficiencies.

(7) Determine whether the CDC analyzes each application in a commercially reasonable

manner, consistent with prudent lending standards. The CDC’s analysis must include the

following:

b. A description of the history and nature of the business

c. A description of and comments on the business plan including financial condition

of the business, need for the business in the area (if new) and competition.

d. A discussion of the owners’ and managers’ relevant experience in the type of

business, as well as their personal credit histories.

e. A financial analysis of the Small Business Applicant’s current balance sheet before

and after the loan to include any required adjustments such as any equity injection,

including a discussion of its adequacy, or stand-by debt.

f. A financial analysis of repayment ability based on historical income statements

and/or tax returns (if an existing business) and projections, including the

reasonableness of the supporting assumptions.

g. A ratio analysis of the financial statements including comments on any trends and a

comparison with industry averages.

h. A discussion of lender’s credit experience with the applicant and a review of

business credit reports.

Eligibility

(8) Review each loan based upon applicant (borrower), project and lender file management.

Review issues include eligibility requirements, as applicable, to the type, delivery method,

size, and any other parameters defined by SBA in accordance with SBA Loan Program

Requirements. Compile individual incidences of deficiency, and analyze to determine if

any patterns of deficiency exist.

(9) Identify all compliance deficiencies in each sample file reviewed, and determine if there

are patterns of deficiencies among all files, reviewing for the following:

h. Determine whether the business is for profit, domestic operation, and otherwise

eligible in accordance with SBA Loan Program Requirements;

Review Plan

Page | 16 of 27

a. Review Articles of Incorporation, Articles of Organization, Corporate By-

Laws, Partnership Agreements, Association By-laws, and Tax Returns to

determine whether the business is for-profit.

i. Identify that the applicant business is small by SBA size standards;

a. The Small Business Applicant and its affiliates must have a maximum

tangible net worth not more than $15 million; AND the average net income

after Federal income taxes for the 2 full fiscal years before the date of the

application is not more than $5 million.

j. Identify that any franchise financing is eligible;

k. Determine whether credit is not otherwise available on reasonable terms from

non-Federal sources without guaranty provided by the SBA;

l. Determine whether some or the entire loan is not available from any of the

following sources: (a) the resources of the applicant business; or (b) the

personal resources of the principals of the applicant concern.

m. Determine whether desired funds are available from the personal resources of

any owner of 20% or more of the equity of the applicant, including limits on

outstanding personal liquid assets, and if available are injected;

n. Determine whether all principal owners of the business are eligible and of good

character as demonstrated on “Statement of Personal History”, SBA Form 912;

AND whether the Lender obtained SBA Form 912, Statement of Personal

History, on all persons required;

o. Determine whether the applicant has ever caused prior loss to the Government

from prior federal financial assistance;

p. Determine whether all principal owners of the business are U.S. citizens or

eligible resident aliens;

q. Identify all use of proceeds of the loan as eligible, including funds used to

purchase any portion of rental real estate, pay debts or change ownership of the

applicant business;

r. Determine whether 504 project meets specified economic development goals

and or job opportunity criteria in accordance with SBA Loan Program

Requirements;

a. At least one job for every $65,000 of project debenture ($100,000 for Small

Manufacturers)

b. A job opportunity does not have to be at the project facility, but 75% of the

jobs must be in the community where the project is located.

s. Identify any actual or apparent conflicts of interest or preferences;

t. Determine whether all SBA delegated program-specific eligibility issues (e.g.,

ALP, PCLP, etc.) are met; and

u. Identify any other SBA statutory, regulatory or SOP violations of eligibility.

(10) Determine that CDC has verified any required borrower contribution prior to disbursement

SBA Loan Program Requirements.

(11) Determine that CDC has obtained any required appraisals, environmental assessments,

flood insurance, or other required insurance, prior to disbursement in accordance with

SBA Loan Program Requirements;

(12) Determine that CDC required and reconciled IRS tax transcripts for any applicant when

required in accordance with SBA Loan Program Requirements;

(13) Determine that CDC obtained executed SBA Form 1506 Servicing Agent Agreement;

Review Plan

Page | 17 of 27

(14) Determine that CDC followed SBA requirement for site visit or other intensive servicing

activity when loan is 60-days or more past due, or there is other reasons for concern in

accordance with SBA Loan Program Requirements;

(15) As applicable to delegation of authority, determine that CDC has followed all SOP

requirements regarding management of liquidation cases, including preparation of a

liquidation plan, timely site visits, use of current appraisals, consideration of

environmental issues, and preparation of a wrap-up report at conclusion of liquidation in

accordance with SBA Loan Program Requirements; and

(16) Identify that CDC has forwarded all recoveries on repurchased loans with 15 days of

receipt in accordance with SBA Loan Program Requirements.

(17) Compile a list of all eligibility deficiencies by issue type and by errors per file, and

identify any trends of deficiencies which warrant lender attention.

(18) Compile a list of material eligibility deficiencies by loan file number and reason for

deficiency. A material deficiency is one which calls to question the validity of part or the

entire guaranty, if guaranty purchase should ever be requested, or which demonstrates

increased financial risk to SBA.

Early Defaults [13 CFR §120.938]

Use the loan detail report regarding early defaulted loans along with assessment of one or more

Early Defaulted (payment problem within 18 months of disbursement) loans to analyze and

address the following:

(19) Identify early debenture repurchases and analyze risk implications (early debenture

repurchase defined as repurchase within 18 months of disbursement). Verify that the SBA

borrower has not suffered any un-remedied adverse change since the 504 loan was initially

approved.

(20) Identify trend with early defaults by delivery method, industry and/or geographic

concentration (as data is available).

(21) Review one or more early defaulted loans and discuss credit underwriting observations in

Credit Administration section.

(22) If a CDC defaults on a Debenture, SBA generally shall limit its recovery to the payments

made by the small business to the CDC on the loan made from the Debenture proceeds,

and the collateral securing the defaulted loan.

(23) SBA will look to the CDC for the entire amount of the Debenture in the case of fraud,

negligence, or misrepresentation by the CDC.

(24) Determine whether CDC cooperates with SBA to cure defaults and initiate workouts.

Collateral 13 CFR§120. 934

(25) Determine whether CDC’s loan procedures establish requirements for SBA collateral that,

at minimum, meet all SBA collateral requirements contained in SBA Loan Program

Requirements.

(26) Review sample of loans to determine if CDC is adhering to SBA’s policy and

requirements regarding collateral, and identify and provide examples of any material

deficiencies or patterns of deficiencies.

Closing

(27) Determine whether the CDC’s policy and procedures define the requirements that must be

met before closing and funding is allowed, including use of authorized closing attorney in

preparation of all required closing instruments, obtaining all required executed loan

documents, meeting all loan authorization conditions, identification that all requirements

Review Plan

Page | 18 of 27

of the first lien holder are met, identification that the interim lien holder payoff is funded

appropriately, verification of borrower’s contribution, verification of correct use of

proceeds, verification of perfection of all lien and guaranty requirements, obtaining all

required insurance policies, including any applicable assignments and/or

acknowledgements; and verification that first lien holder has executed all required

agreements.

(28) Determine whether the CDC’s closing policy demonstrates the ability to close and

disburse SBA loans in accordance with SBA Loan Program Requirements.

(29) Determine if CDC confirmed that borrower made all required cash or property

contributions in accordance with SBA Loan Program Requirements.

(30) Review sample of loans to determine if CDC is adhering to loan policy and SBA

requirements regarding closing and disbursement, and identify and provide examples of

any material deficiencies or patterns of deficiencies.

(31) For each PCLP Loan, the PCLP CDC must document in its files the basis for its decisions

with respect to loan processing, closing, servicing, liquidating, and litigating.

Regular Servicing & Assessment of Continued Creditworthiness –13 CFR §120.970

(32) Describe CDC practices for evaluating continued creditworthiness, (e.g., annual financial

statement analysis, credit modeling for portfolio management purposes, etc.).

(33) Determine whether policy for continued monitoring of the SBA portfolio is, at minimum,

in accordance with any loan authorization requirements.

(34) Determine whether CDC’s policy for loan servicing is consistent with SBA Loan Program

Requirements.

i. The CDC is responsible for routine servicing including receipt and review of the

Borrower’s or Operating Company’s financial statements on an annual or more

frequent basis and monitoring the status of the Borrower and 504 loan collateral

(35) Determine whether adequate controls exist to ensure required insurance coverage in place,

including any applicable assignments and/or acknowledgements are obtained, and all

required insurance policies are renewed as necessary.

j. The CDC is responsible for assuring that the Borrower makes all required insurance

premium payments and has paid all taxes when due.

(36) Determine whether adequate controls exist to ensure required lien positions are obtained

and renewed, as necessary.

k. The CDC is responsible for filing renewals and extensions of security interests on

collateral for the 504, as required.

(37) Describe and determine procedures for processing borrower servicing requests.

(38) Review sample of loans to determine if CDC is adhering to loan policies and SBA

requirements, including those contained in SBA Loan Program Requirements regarding

regular servicing and portfolio management, and identify and provide examples of any

material deficiencies or patterns of deficiencies.

Intensive Servicing/Liquidation – 13 CFR §120.536

(39) The CDC must be approved by SBA to engage in workout, liquidation or litigation of 504

loans. Determine if the CDC lender has such authority, and if so, the following additional

procedures apply.

(40) SBA must give its prior written consent before a CDC does any of the following:

l. Increases the principal amount of a loan above that authorized by SBA at loan

origination

Review Plan

Page | 19 of 27

m. Confers a Preference on CDC or engages in an activity that creates a conflict of

interest

n. Compromises the principal balance of a loan

o. Transfers, sells, or pledges more than 90% of a loan

(41) Determine whether the CDC’s policy and procedure establish a basis upon which to

evaluate CDC’s collection practices including collection procedures for past due and

delinquent loans and procedures for collecting and deferring loans and for transferring

loans from regular servicing to intensive servicing and/or liquidation, and are consistent

with SBA Loan Program Requirements.

(42) Determine if CDC’s policy and procedures establish a basis upon which a loan will be

subjected to intensive servicing or liquidation action, and such intensive servicing or

liquidation includes workouts, site visits, liquidation plans, control, possession and/or

protection of collateral; and access to counsel, and are consistent with SBA Loan Program

Requirements.

p. All authorized CDC liquidators must submit liquidation plans for approval.

(43) Review a sample of loans to determine if CDC is adhering to loan policy and SBA

requirements regarding management of collections, intensive servicing and liquidation

accounts, and identify and provide examples of any material deficiencies or patterns of

deficiencies in accordance with SBA Loan Program Requirements.

(44) Determine whether authorized CDC liquidators are liquidating and conducting debt

collection litigation for 504 loans in their portfolio no less diligently than for their non-

SBA portfolio and in a prompt, cost-effective, and commercially reasonable manner

consistent with prudent lending standards. 13 CFR §120.535

(45) A CDC must not take any action in the liquidation or debt collection litigation of a 504

loan that would result in an actual or apparent conflict of interest between the CDC (or any

employee of the CDC) and any Third Party Lender, associate of a Third Party Lender, or

any person participating in a liquidation, foreclosure, or loss mitigation action

(46) Confirm that CDC received SBA consent before engaging in any of the following

activities:

q. Substantially altering the terms or conditions of any loan instrument

r. Releasing collateral having a cumulative market value in excess of 10% of the

Debenture amount of $10,000 whichever is less

s. Accelerating maturity of the note

t. Compromising or releasing any claim against any borrower or obligor or against

any guarantor, standby creditor, or any other person that is contingently liable for

moneys owed on the loan

u. Purchasing or paying off any indebtedness secured by the property that serves as

collateral for a defaulted 504 loan, such as payment of the debt(s) owed to a lien

holder or lien holders with priority over the lien securing the loan

v. Accepting a workout plan to restructure the material terms and conditions of a loan

that is in default or liquidation

(47) For all servicing/liquidation actions not requiring SBA’s prior written consent, CDCs must

document the justifications for their decisions and retain these and supporting documents

in their file for future SBA review to determine if the actions taken by the CDC were

prudent, commercially reasonable, and complied with all Loan Program Requirements.

Review Plan

Page | 20 of 27

Loans with Repurchased Debentures

(48) Determine that CDC’s policies and processes to manage purchased debentures are

consistent with non-purchased debenture financings.

(49) Review a selection of loans with repurchased debentures to determine that CDC has well-

defined action plan events for pursuit of payments, with timelines and responsibilities for

various categories of intensive attention.

Consistency/Conflict with SBA Policy

(50) Identify if any stated CDC policy is in conflict with SBA regulations, policies and/or

procedures. If any are so identified, what action(s), if any, must be taken to address the

conflict(s)? Reviewer must be mindful of this while conducting analysis of all CDC

policies and procedures related to the SBA loan portfolio and its individual SBA loans and

their administration.

Effectiveness of Internal Controls

(51) Review any checklists or other practices which assist in ensuring that all files are managed

consistently and correctly, and in accordance with policy.

(52) Describe any serious gaps in internal controls which indicate a material weakness.

Other Risk Characteristics

(53) Discuss all credit administration preliminary findings with management.

(54) Note any relevant lender input.

(55) Conclude on the effectiveness of Lender’s credit administration policies and practices. In

making these conclusions, the reviewer should identify mitigating circumstances such as

lending that, while being more risky, may further SBA’s mission in a positive manner.

However, additional risk in the SBA loan portfolio must be accompanied by more

rigorous credit administration practices in servicing and oversight. The conclusions shall

be presented to management at the exit conference along with an assessment of the

seriousness of the preliminary findings relative to the lender’s SBA activities.

Findings and Corrective Actions

(56) Identify any Finding that requires a Corrective Action.

Identify the Corrective Action that corresponds to each Finding.

REGULATORY COMPLIANCE

Annual Financial Statements

(14) Identify that CDC meets SBA Loan Program requirements for annual audited or reviewed

financial reports, any legal proceedings, any organizational status changes or any

condition changes that affect CDC’s eligibility to continue to participate. Audited financial

statements must at a minimum include:

Audited balance sheet

Audited statement of income (or receipts) and expense

Audited statement of source and application of funds

Auditor’s letter to management on internal control weaknesses

Auditor’s report

(15) Who is auditor? How long have they been the auditor? Does the board of directors receive

a copy of the audited financials? If there is an audit committee, how frequently does the

Review Plan

Page | 21 of 27

auditor meet with that committee? If no audit committee, when is the last time the auditor

met with the board of directors?

Reporting to SBA – 13 CFR §120.830

(16) Compare most recently submitted Annual Report to internal records and reports to

determine that it accurately reflects the status of the management, operations and financial

condition of the 504 CDC;

(17) Determine whether the Annual Report was submitted in accordance with time requirement

of SBA Loan Program Requirements, and if not, why not;

a. CDC must submit an annual report within 180 days after the end of the CDC’s

fiscal year (to include audited or reviewed financial statements of the CDC and

any affiliates or subsidiaries of the CDC prepared in accordance with

§120.826(c) and (d).

(18) CDC must report involvement in any legal proceedings (this has an impact on risk rating)

(19) CDC must report changes in organizational status (what is time frame?)

(20) Obtain the CSA monthly “45-day delinquent report” for the most recent three months, to

identify loans more than 45-days past due, and review a sample of these files to determine

that CDC has notified SBA of required analysis, plan and steps to be taken to bring

borrower current for any such 45-day delinquent accounts;

(21) Determine whether internal CDC records of servicing status of all problem loans (or a

sample) has been reported to Colson in a timely fashion on all negotiated catch-up

agreements;

State of Incorporation

(22) Which state is the CDC incorporated in?

(23) Is the CDC in good standing with state?

IRS

(24) Has CDC filed all its required tax returns?

Directors and Officers Liability Insurance (25) Does CDC have appropriate D/O insurance?

Designated Attorney

(26) Who are the designated Attorneys for the CDC?

(27) Are they licensed in the State where the CDC conducts business?

(28) Is their SBA required training up-to-date?

(29) Do they have Professional Liability Insurance?

CDC Corrective Action Response from prior RBR

(30) Did CDC adequately address the Findings in the prior RBR?

(31) Did the CDC adequately implement the Corrective Actions outlined in its Response Letter?

Findings and Corrective Actions

(32) Identify any Finding that requires a Corrective Action.

Identify the Corrective Action that corresponds to each Finding

Review Plan

Page | 22 of 27

TECHNICAL ISSUES AND MISSION

(1) Any funds generated from 503 and 504 loan activity by a CDC remaining after payment

to staff and payment of overhead expenses must be retained by the CDC as a reserve for

future operations and for investment in other local economic development activity in its

Area of Operations. Determine whether the CDC markets the 504 program, packages and

processes 504 loan applications, closes and services 504 loans, and if authorized by SBA,

liquidates and litigates 504 loan assets.

(2) Describe CDC’s business plan for SBA lending, including SBA loan program goals.

(3) Determine that CDC meets the annual approval requirements and/or portfolio average job

opportunity requirements.

Use of Loan Agents

(4) Does the CDC routinely or on an ad hoc basis use loan agents in originating its SBA loans?

(5) Determine whether CDC’s policies and procedures establish a basis for routine or ad hoc

use of loan agents (packagers, referral agents, brokers, etc.) in originating SBA loans.

(6) Determine how CDC tracks performance of loans generated by its loan agents.

(7) Determine whether CDC has policies (such as Code of Conduct) to require business

development officers and other lender personnel to disclose the involvement of loan

agents in generating or packaging loans.

(8) Determine whether loan agent-originated loans are fully meeting SBA standards, including

those regarding creditworthiness.

(9) For CDCs with active loan agent relationships, obtain list of loans referred by loan agents,

and analyze loans referred by loan agents to determine whether performance trends and/or

credit quality is comparable to book of business originated directly by CDC.

(10) Determine that SBA Form 159, “Fee Disclosure Form and Compensation Agreement” has

been completed, as applicable, for each loan in which a loan agent has had participation.

(11) Determine whether additional file review is appropriate to fully assess loan agent activity.

If so, review a small selection of loan files for loans originated by loan agents to determine

if each decision was reached in accordance with SBA’s policies and to better evaluate

CDC’s use of loan agents.

(12) Determine whether lender conducts an internal review and auditing functions to examine

the reasons why a particular lending official may have a significantly higher loan volume

than his/her colleagues, particularly if that lending official is known to work with a

particular loan agent or agents.

(13) Does lender have a system of identifying/monitoring potential fraud indicators:

a. The loan agent has a record of early defaults;

b. The loan agent controls of all communication between the lender and the

borrower;

c. The loan agent threatens to “shop” the loan elsewhere;

d. The loan agent provides a high numbers of “qualified” borrowers in a short

period of time;

e. The loan agent’s apparent ease in resolving seemingly difficult questions or

problems with a loan

f. The loan agent steers the lender to specific appraisers or title companies;

g. The borrower replies “no” when asked if a “packager” was paid to prepare the

loan application, when it is known a loan agent is involved in the process;

Review Plan

Page | 23 of 27

h. Multiple loan applications are submitted simultaneously to different lenders for

the same borrowers, as indicated in credit reports; and

i. The loan agent charges excessive fees.

(14) Discuss all credit administration findings with management.

(15) Note any relevant CDC input.

Concentrations

Use the loan detail report provided to provide chart, analyze and to address the following:

(16) Identify and analyze any notable concentration(s) (industry, geographic, Franchise, etc.)

within the CDC’s portfolio, and risk implications; i.e. significant percentage of dollars in

one or more industries.

(17) Compile a table of industry concentrations for loan portfolio (numbers and dollars).

(18) Compare to SBA portfolio and peer averages, if available.

(19) Analyze concentrations of 20% or more identifying the risk implications of such

concentrations.

(20) A CDC’s portfolio must maintain a minimum average of 1 Job Opportunity per an amount

of 504 loan funding that will be specified by SBA from time to time in Federal Register. A

CDC is permitted 2 years from its certification date to meet this average.

(21) A CDC must indicate in its annual report the Job Opportunities actually or estimated to be

provided by each project.

(22) If a CDC does not maintain the required average, it may retain its certification if it justifies

to SBA’s satisfaction its failure to do so in its annual report and shows how it intends to

attain the required average.

(23) Conclude on the adequacy of credit administration of the SBA portfolio.

Does the CDC meet the three years 20 applications requirement?

(24) If the CDC is an ALP, does it contain at least 30 active ALP loans?

(25) Does the CDC adequately market the SBA 504 Program in it area of operations?

(26) Is the CDC meeting its economic development mission?

If CDC has Lending Extension Area Authority (LEA):

(27) Does the CDC have sufficient staff to operate in the requested counties?

(28) Is the CDC's Designated Attorney license to practice in expansion area?

If CDC has Multi-State Authority:

(29) Does the CDC meets membership requirement in expansion state(s)?

(30) Is the CDC's Designated Attorney license to practice in expansion state(s)?

(31) Does the CDC have a separate loan committee in expansion state(s)?

Documentation of Jobs Created/Retained:

(32) Does the CDC receive written documentation from its borrowers with 2 years of

disbursement of 504 loan showing the number of jobs actually retained and/or created?

Review Plan

Page | 24 of 27

Attachment B - Loan Sample List

Sample

#

Loan

Number Borrower Name

Borrower

State

Delivery

Method Status Summary

Review Plan

Page | 25 of 27

Attachment C – Board of Directors Interview Questions

1. Tell me about your (business, job at bank/government/community)?

2. How did you become a member of the Board?

3. How long have you been on the Board?

4. What do you see as the role of the Board (whether chairman, chairman of loan

committee, or newest board member) in the financial oversight of the CDC?

5. Do you feel that the Board is aware of the CDC’s operations and its condition?

6. Is the board independent or a rubber stamp?

7. Do board members question the decisions of management?

8. Related to the board’s awareness of CDC matters -- have you seen/reviewed the SBA

Risk Based Review Report that SBA issued as part of its [DATE] CDC review? Do

you know what SBA’s summary assessment of CDC was? (answer: Acceptable)

9. Have you ever seen the CDC’s annual audited financial statements? Have you ever

met with the CDC’s auditor? What do you think of the financial condition of the

CDC?

10. Does the Board review and approve the CDC’s annual budget?

11. Are you on the committee?

12. How does the loan committee work? How often do you meet? Does the loan

committee ever decline loans? If so, how many do you think are actually declined?

13. Do you refer any business to the CDC?

14. What is the CDC’s conflict of interest policy?

15. Does the Board have an Executive Compensation Committee? Who is on that

Committee? Is there a written Compensation Policy? Does the entire Board vote on

the Compensation Committee’s decisions?

16. Are program education opportunities made available to Board Members? Have you

ever attended NADCO training? When?

17. What do you see as the biggest challenges for the CDC’s success?

Review Plan

Page | 26 of 27

Exceptions #____________

CDC:

Location:

Exam Date:

File Review Deficiencies

Sample #____________ SBA Loan #_______________________________________

Loan Name____________________________________________________________________

Reviewer’s Name_______________________________________________________________

DEFICIENCIES NOTED: (# refers to the item number on the Checklist)

1. #_____: _____________________________________________________________________

__________________________________________________________

2. #_____: ___________________________________________________

__________________________________________________________

3. #_____: ___________________________________________________

__________________________________________________________

4. #_____: ___________________________________________________

__________________________________________________________

5. #_____: ___________________________________________________

__________________________________________________________

6. #_____: ___________________________________________________

__________________________________________________________

__________________________________________________________

7. #_____: ___________________________________________________

__________________________________________________________

__________________________________________________________

8. #_____: ___________________________________________________

__________________________________________________________

__________________________________________________________

9. #_____: ___________________________________________________

__________________________________________________________

__________________________________________________________

Review Plan

Page | 27 of 27

File Deficiencies Response

MANAGEMENT RESPONSE:

1.____________________________________________________________________________

2.____________________________________________________________________________

3.____________________________________________________________________________

4.____________________________________________________________________________

5.____________________________________________________________________________

6.____________________________________________________________________________

7.____________________________________________________________________________

8.____________________________________________________________________________

9.____________________________________________________________________________

CDC’s Officer Signature: ________________________________________________________

Title:

Date: