Embed Size (px)

Citation preview

US Renewable Energy Markets: Financial

Perspective

ByMichael D. Ware

Advance Capital Markets, Inc.Washington Council of Governments

Washington, DCJune 22, 2005

2

“The way we produce and consume energy hasn’t

changed much in decades.”

Business Week

October 11, 2004

3

Overview

• Financial Markets for RE are Driven by Key Factors

•Economic•Financial•Political

• Review of RE in the U.S.• Potential Local Applications

4

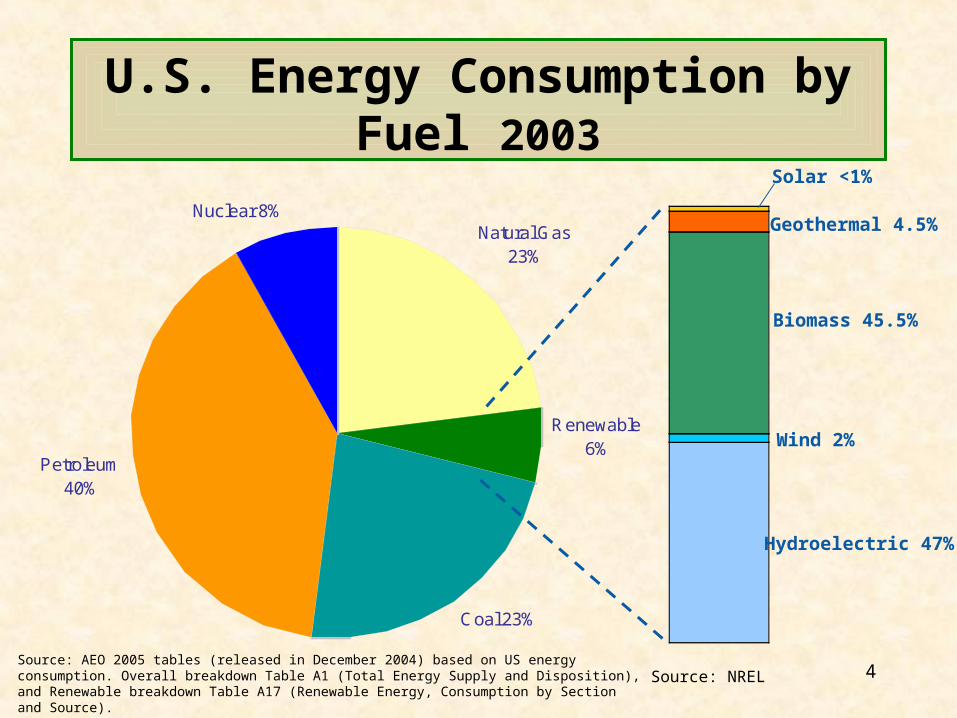

U.S. Energy Consumption by Fuel 2003

Source: NREL

Coal 23%

Petroleum 40%

Renewable 6%

Natural Gas 23%

Nuclear 8%

Wind 2%

Biomass 45.5%

Hydroelectric 47%

Geothermal 4.5%

Solar <1%

Source: AEO 2005 tables (released in December 2004) based on US energy consumption. Overall breakdown Table A1 (Total Energy Supply and Disposition), and Renewable breakdown Table A17 (Renewable Energy, Consumption by Section and Source).

5

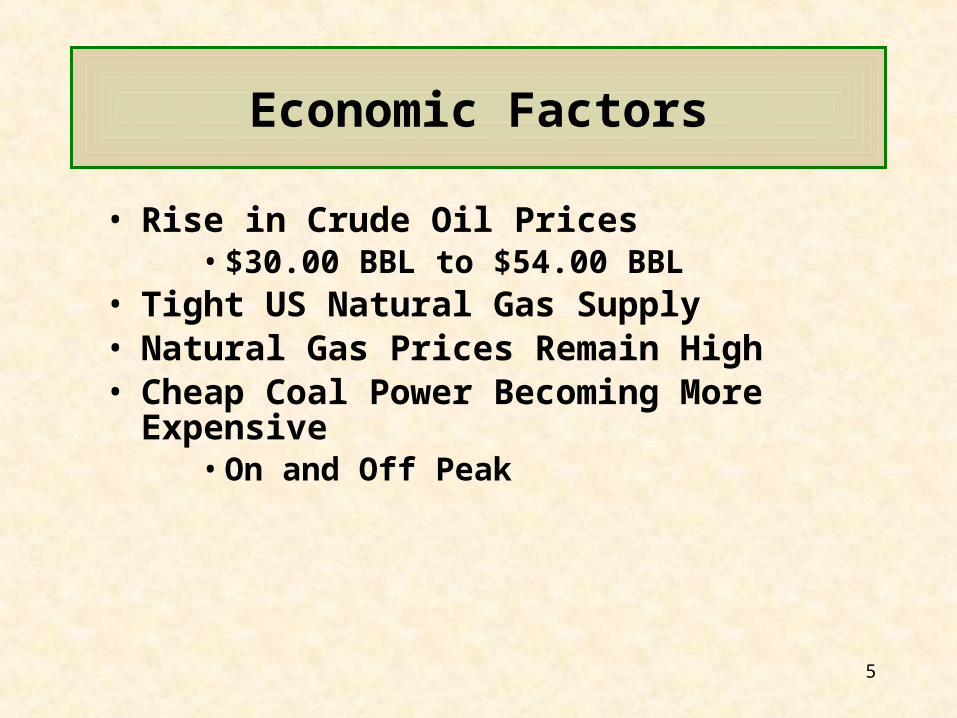

Economic Factors

• Rise in Crude Oil Prices•$30.00 BBL to $54.00 BBL

• Tight US Natural Gas Supply• Natural Gas Prices Remain High• Cheap Coal Power Becoming More

Expensive•On and Off Peak

6

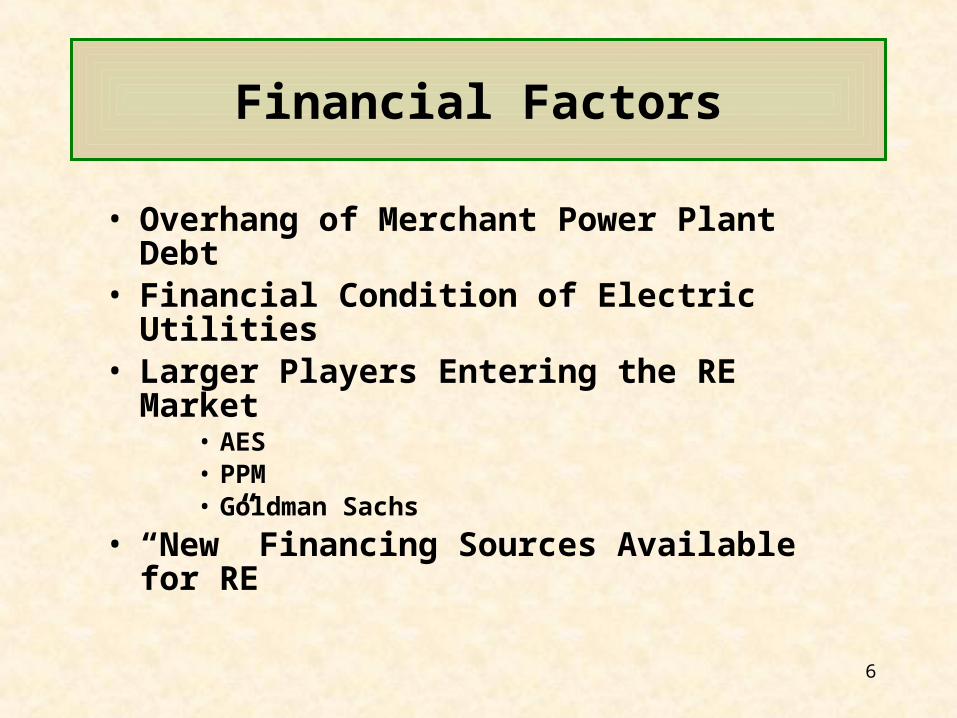

Financial Factors

• Overhang of Merchant Power Plant Debt

• Financial Condition of Electric Utilities

• Larger Players Entering the RE Market

• AES• PPM• Goldman Sachs

• “New” Financing Sources Available for RE

7

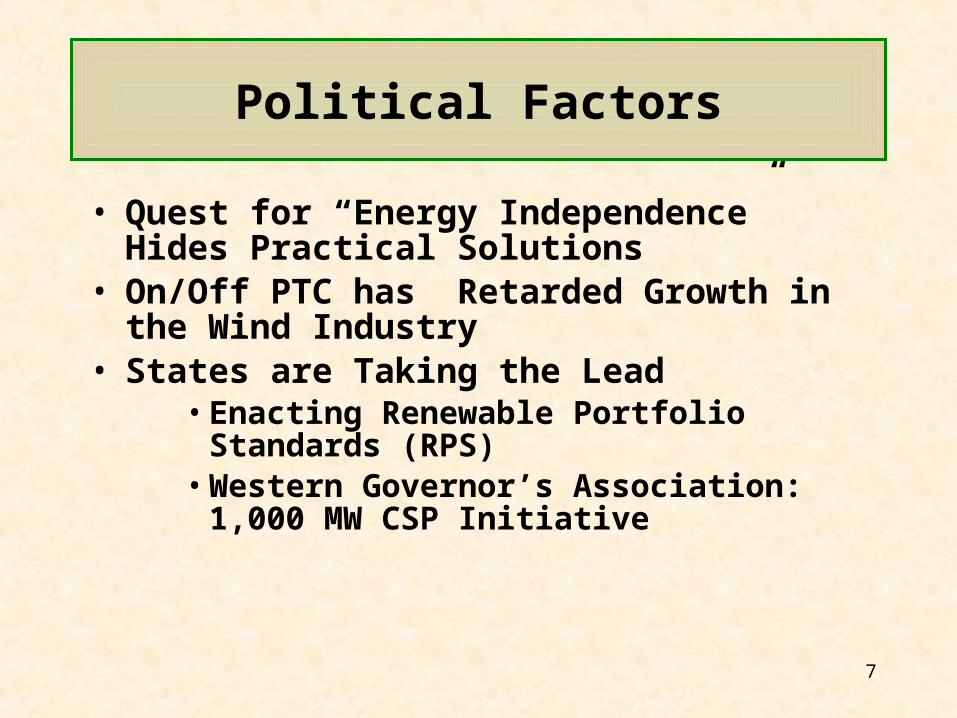

• Quest for “Energy Independence” Hides Practical Solutions

• On/Off PTC has Retarded Growth in the Wind Industry

• States are Taking the Lead•Enacting Renewable Portfolio

Standards (RPS)•Western Governor’s Association:

1,000 MW CSP Initiative

Political Factors

8

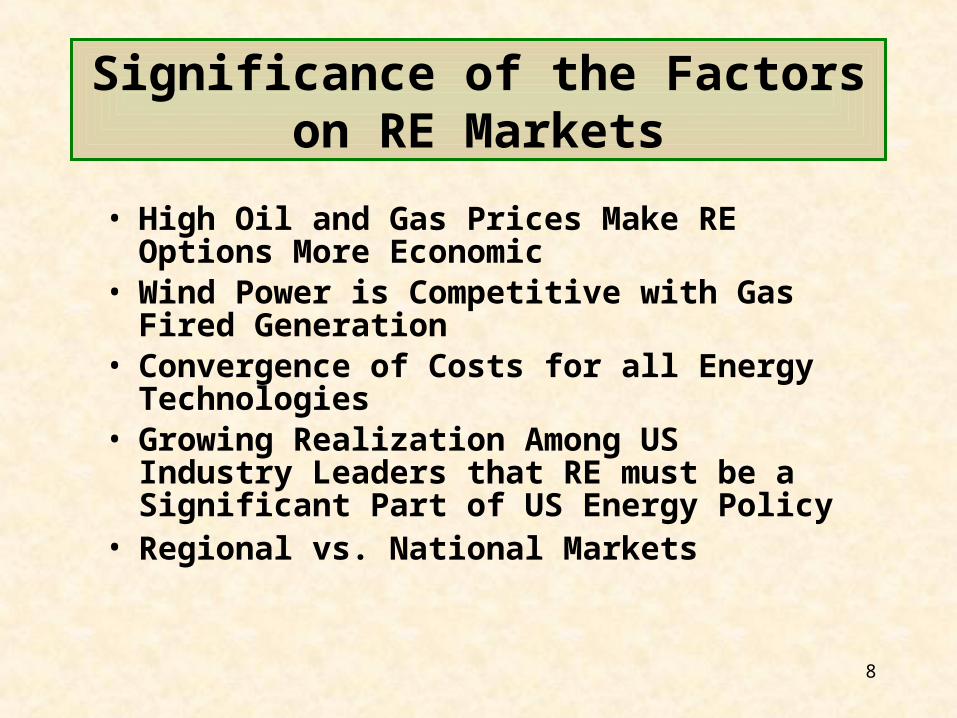

Significance of the Factors on RE Markets

• High Oil and Gas Prices Make RE Options More Economic

• Wind Power is Competitive with Gas Fired Generation

• Convergence of Costs for all Energy Technologies

• Growing Realization Among US Industry Leaders that RE must be a Significant Part of US Energy Policy

• Regional vs. National Markets

9

Review of RE in the US

10

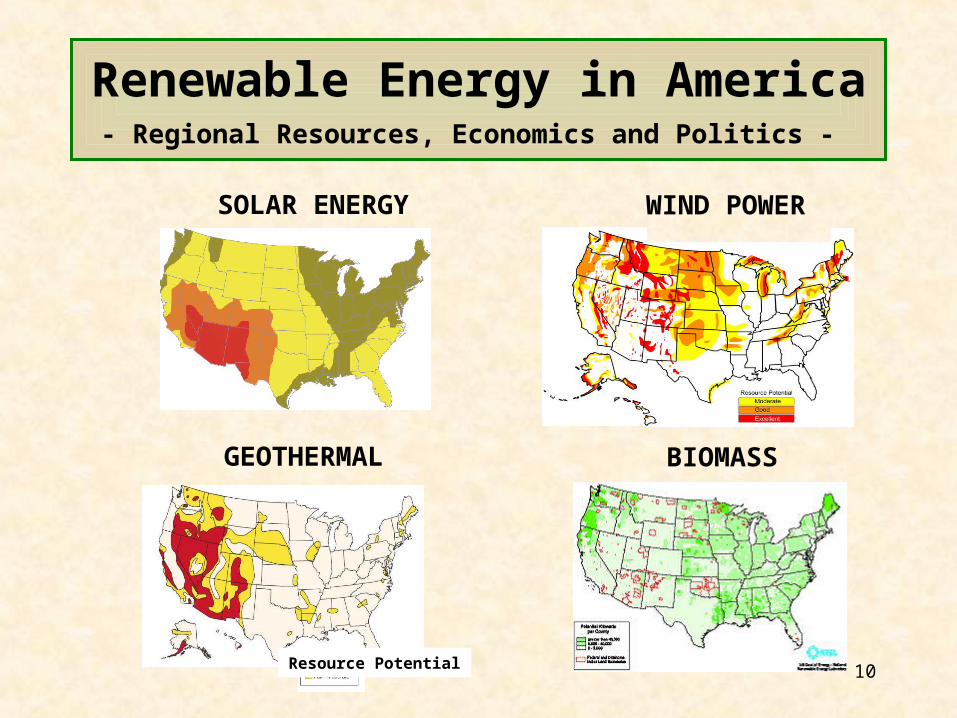

Renewable Energy in America

- Regional Resources, Economics and Politics -

Resource Potential

SOLAR ENERGY WIND POWER

GEOTHERMAL BIOMASS

11

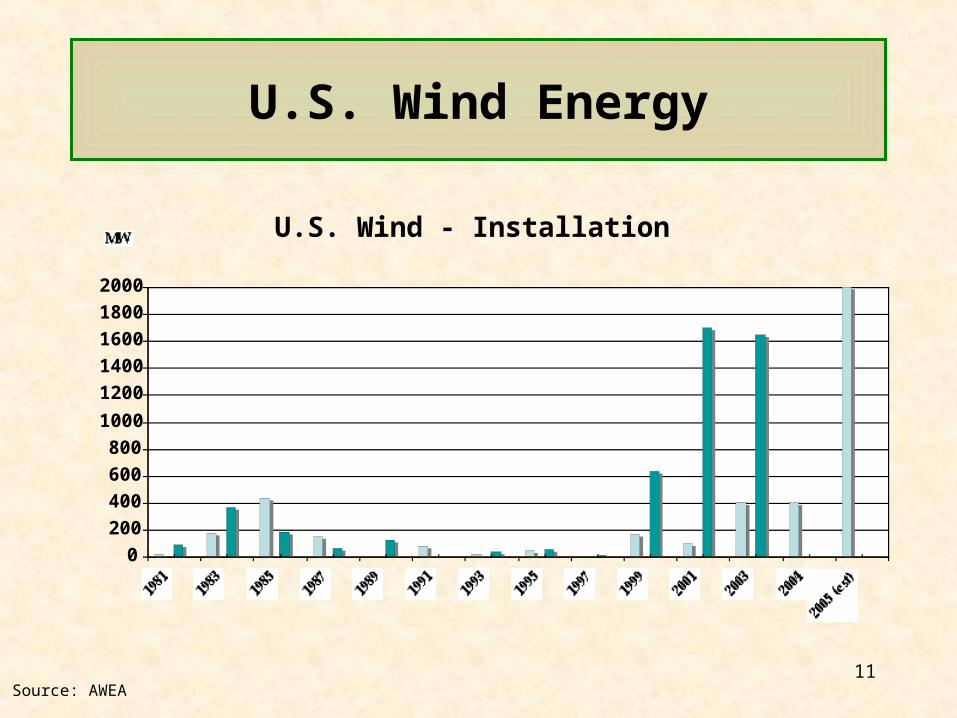

U.S. Wind Energy

U.S. Wind - Installation by Year

0200400600800

1000

12001400160018002000

1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2004

2005 (est)

MW

Source: AWEA

12

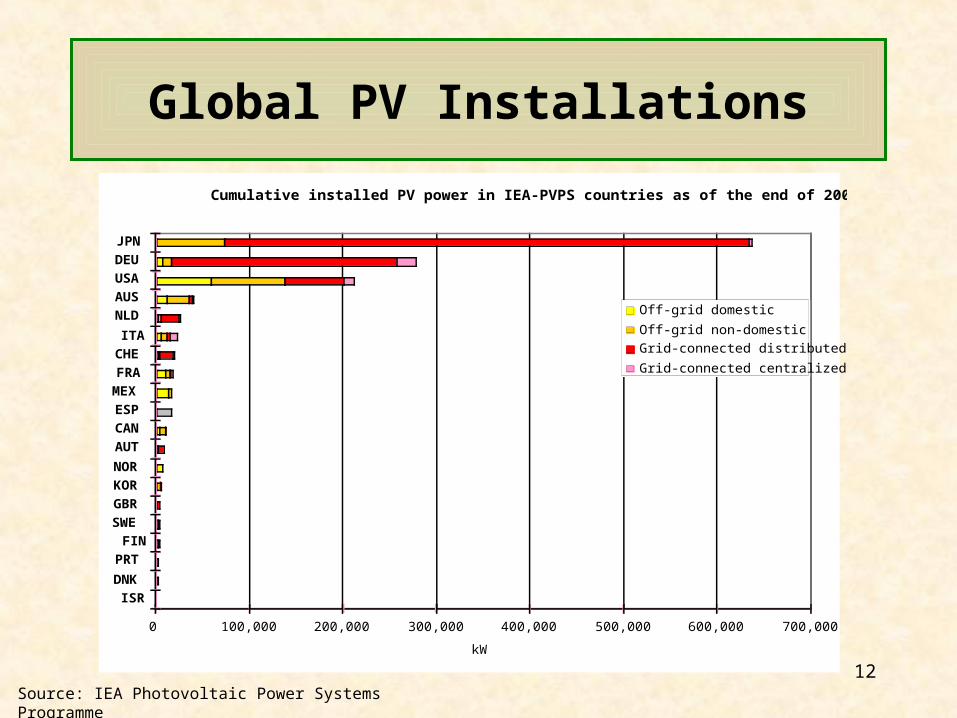

Global PV Installations

Cumulative installed PV power in IEA-PVPS countries as of the end of 2002

0 100,000 200,000 300,000 400,000 500,000 600,000 700,000

ISR

DNK

PRT

FIN

SWE

GBR

KOR

NOR

AUT

CAN

ESP

MEX

FRA

CHE

ITA

NLD

AUS

USA

DEU

JPN

kW

Off-grid domestic

Off-grid non-domestic

Grid-connected distributed

Grid-connected centralized

Source: IEA Photovoltaic Power Systems Programme

13

U.S. Geothermal Energy

Source: Geothermal Energy Association

14

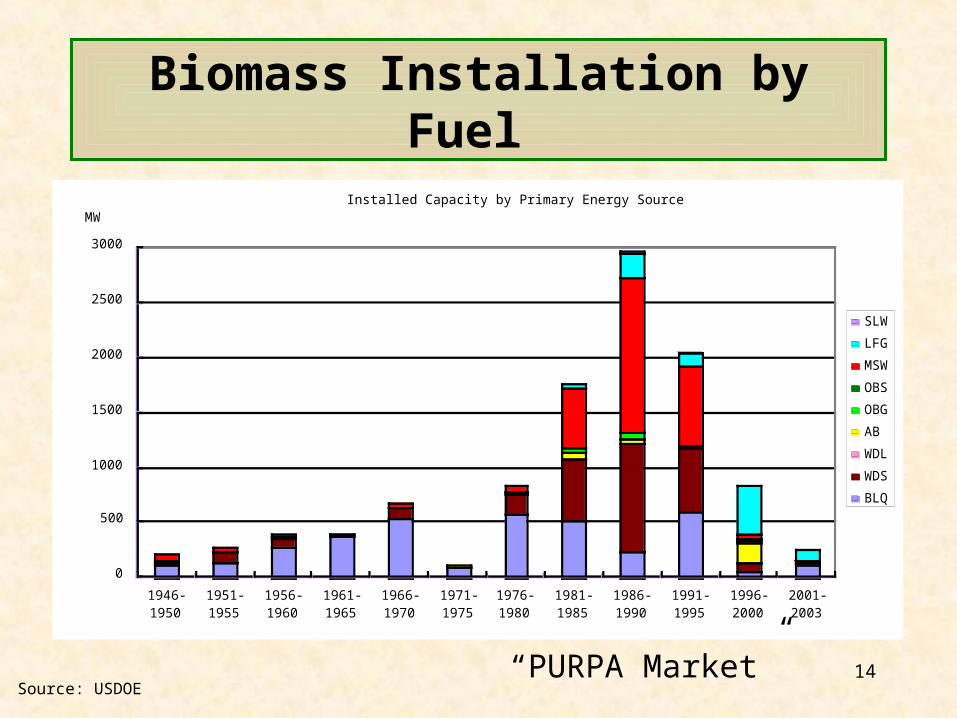

Biomass Installation by Fuel

Source: USDOE

Installed Capacity by Primary Energy Source

0

500

1000

1500

2000

2500

3000

1946-1950

1951-1955

1956-1960

1961-1965

1966-1970

1971-1975

1976-1980

1981-1985

1986-1990

1991-1995

1996-2000

2001-2003

MW

SLW

LFG

MSW

OBS

OBG

AB

WDL

WDS

BLQ

“PURPA Market”

15

Fuel Ethanol Production

Source: Renewable Fuel Association

16

Key Trends in Financial Markets

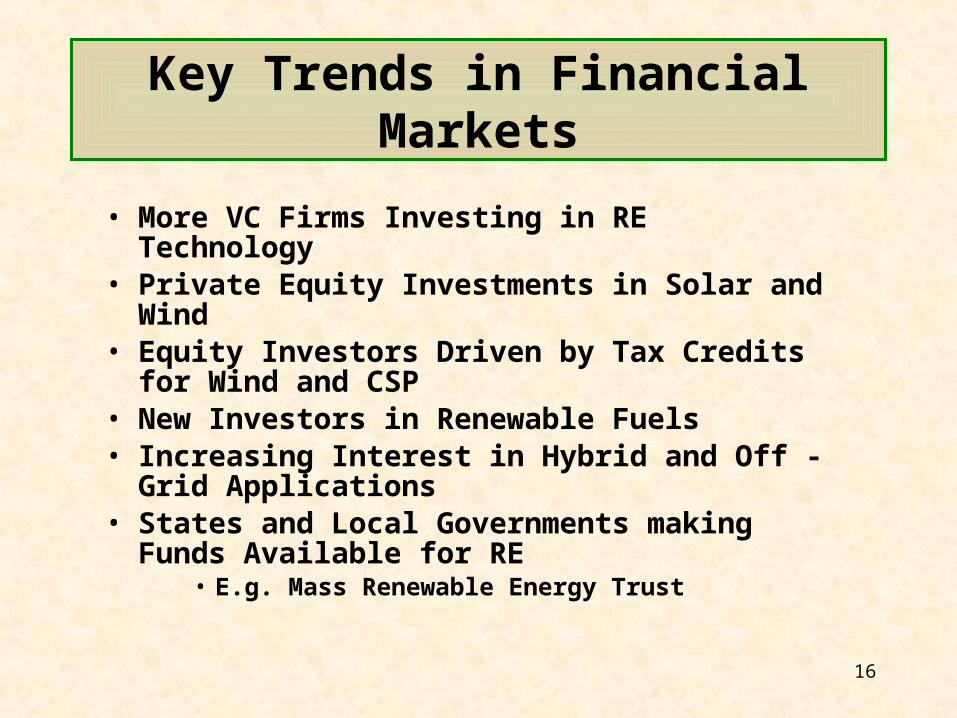

• More VC Firms Investing in RE Technology

• Private Equity Investments in Solar and Wind

• Equity Investors Driven by Tax Credits for Wind and CSP

• New Investors in Renewable Fuels• Increasing Interest in Hybrid and Off -

Grid Applications• States and Local Governments making

Funds Available for RE• E.g. Mass Renewable Energy Trust

17

ACORE Call for “Phase II”

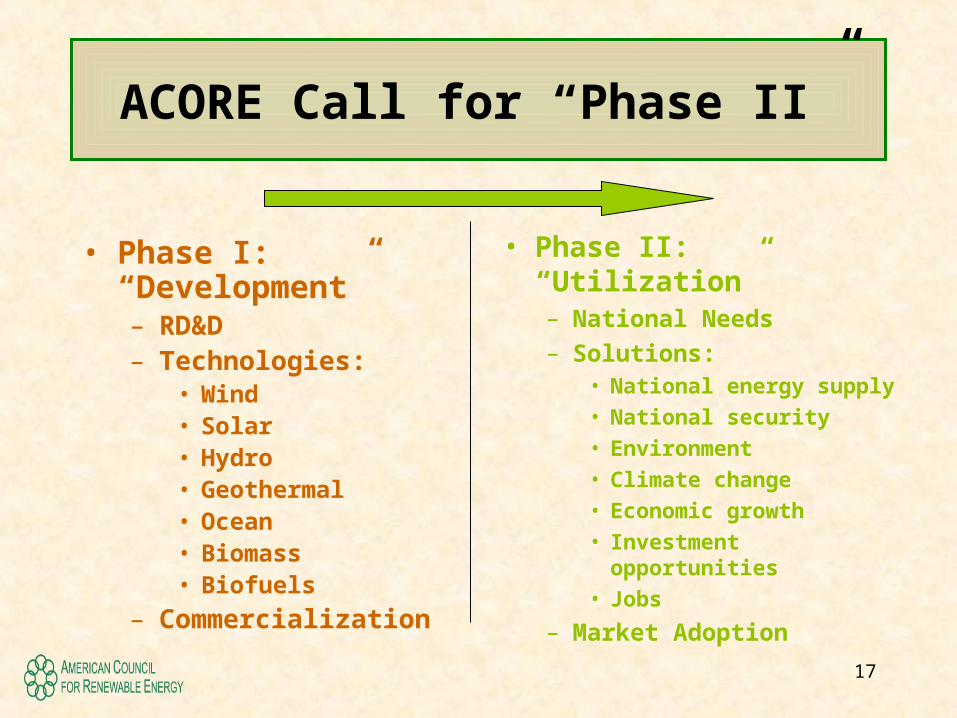

• Phase I: “Development”– RD&D– Technologies:

• Wind • Solar• Hydro• Geothermal• Ocean• Biomass• Biofuels

– Commercialization

• Phase II: “Utilization”– National Needs

– Solutions:• National energy supply

• National security

• Environment

• Climate change

• Economic growth

• Investment opportunities

• Jobs

– Market Adoption

18

Potential RE Options

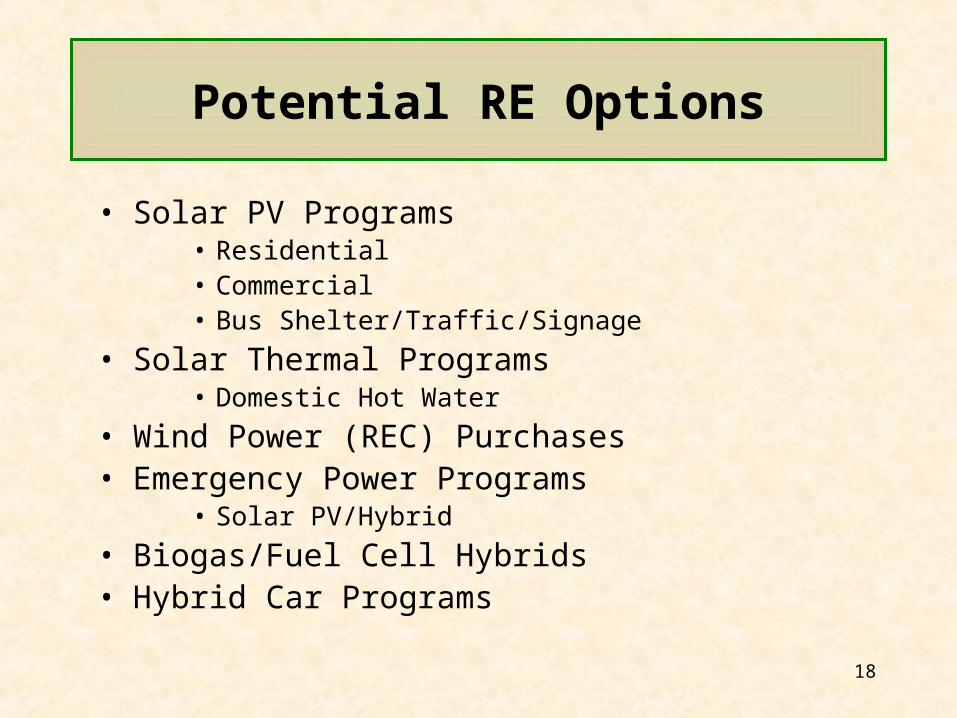

• Solar PV Programs• Residential• Commercial• Bus Shelter/Traffic/Signage

• Solar Thermal Programs• Domestic Hot Water

• Wind Power (REC) Purchases• Emergency Power Programs

• Solar PV/Hybrid

• Biogas/Fuel Cell Hybrids• Hybrid Car Programs

Extra Slides

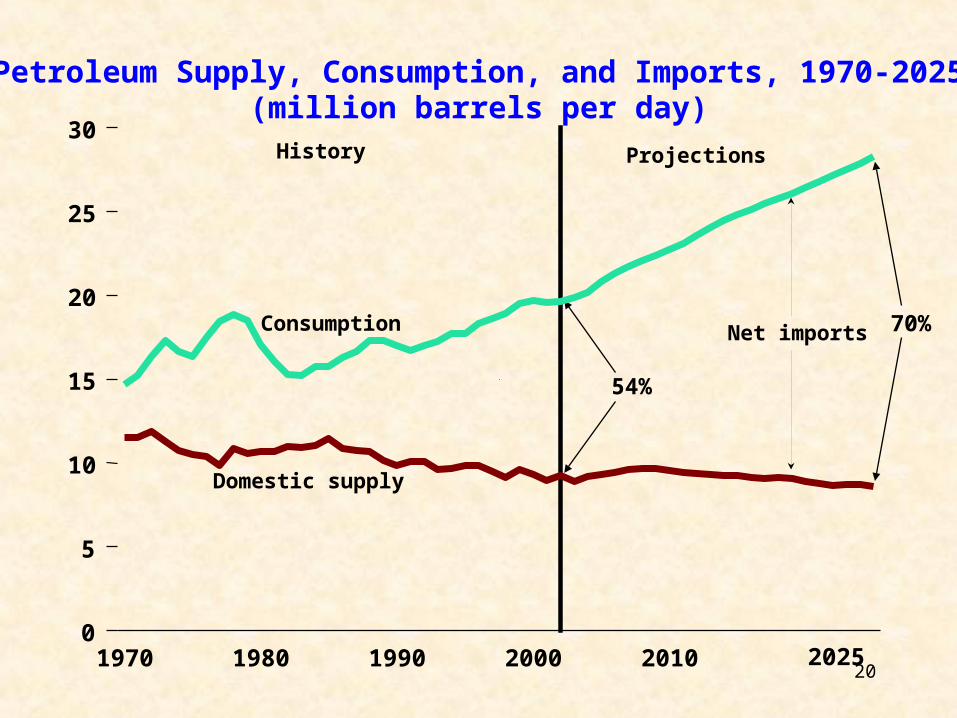

20

54%

70%

1970 1980 1990 2000 2010 20250

5

10

15

20

25

30

Domestic supply

Consumption

History Projections

Net imports

Petroleum Supply, Consumption, and Imports, 1970-2025(million barrels per day)

Primary Driver of Increased Consumption

• Power sector consumption of natural gas projected to increase significantly every year:

Source: Energy Ventures Group

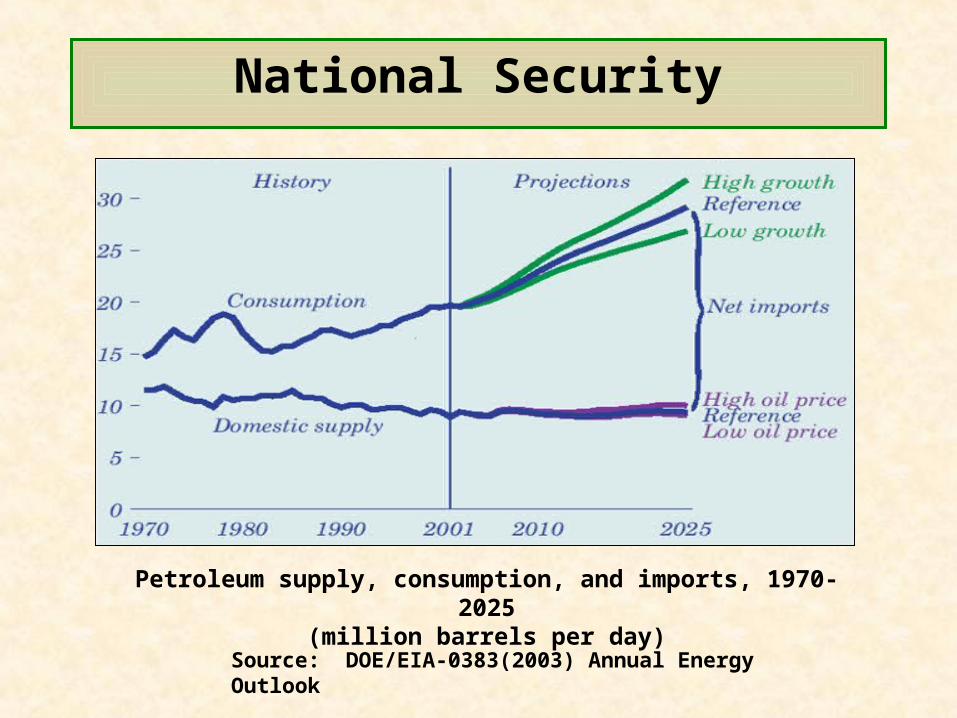

Petroleum supply, consumption, and imports, 1970-2025(million barrels per day)

Source: DOE/EIA-0383(2003) Annual Energy Outlook

National Security