Embed Size (px)

Citation preview

US Regulatory change

and Surplus lines

Steve Yates, Manager, International Regulatory Affairs

Giles Taylor, Manager, International Regulatory Affairs

27 July 2011

© Lloyd’s2

Agenda Focus on surplus lines implications of the Non-Admitted

And Reinsurance Reform Act (Title V, Subtitle B, Part I,

of Dodd-Frank)

Legislative intent and implementation

Tax

Impact on doing surplus lines business Exempt Commercial Purchaser

MAT Exemptions

Independent Procurement

Group schemes

Admitted business

Eligibility filings

What are Lloyd’s expectations of how this will continue to develop?

© Lloyd’s3

NRRA: Intent & Implementation Gives the insured’s ‘Home State’ exclusive authority:

for tax, statutory and regulatory requirements

Congress placed a tight deadline for implementation (330 days) of interstate agreement on how to implement NRRA

Intent was to create uniformity:

"the letter and spirit of the NRRA [are] to provide a simpler, uniform tax reporting and payment process....“, Rep Dennis Moore, sponsor of the NRRA Bill

‘Congress intends that each State adopt nationwide uniform requirements, forms and procedures….’, Dodd-Frank S.521 (b) 4.

The reality of how NRRA has been implemented has made several changes to an already complicated surplus lines landscape

© Lloyd’s4

Tax Implications NRRA says: ‘The States may enter into a compact or

otherwise establish procedures to allocate among the States the premium taxes paid to the insured’s home State.’

Pressure of a 330 day deadline and budget crises

Key states keeping 100% of tax (e.g. NY, TX, CA)

NIMA: Backed by NAIC leadership, opposed by industry - establishing a clearing house to handle tax monies but requiring more data

SLIMPact-Lite: Backed by NCOIL and NAPSLO – clearing house allocates tax using existing data

Biggest challenge is going to be balancing all three in various scenarios

© Lloyd’s5

‘Industrial Insured’ to ‘Exempt Commercial Purchaser’

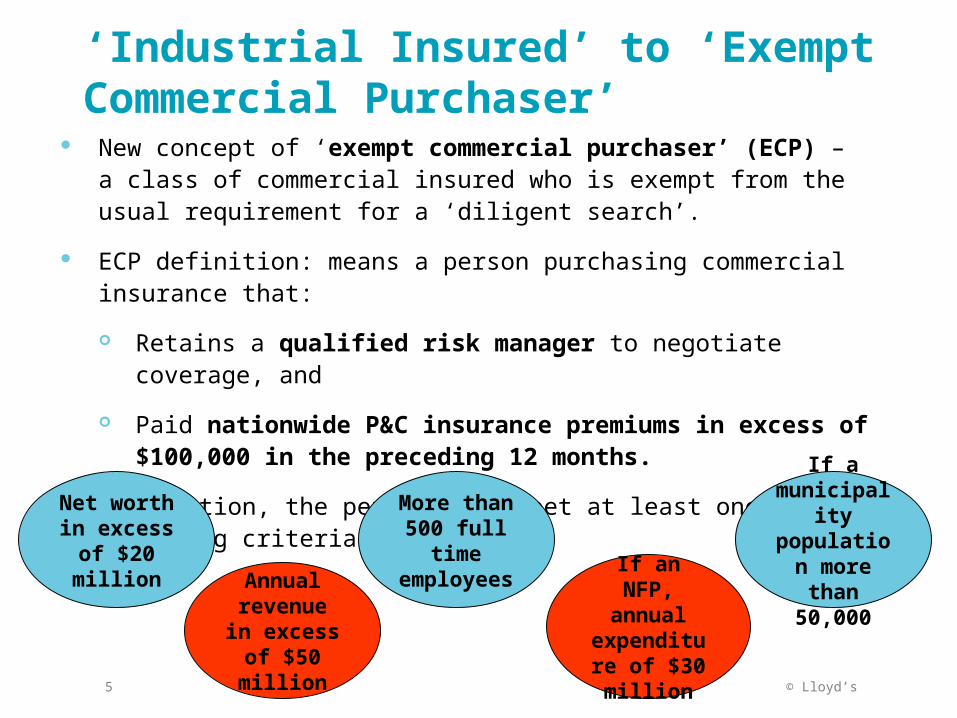

New concept of ‘exempt commercial purchaser’ (ECP) – a class of commercial insured who is exempt from the usual requirement for a ‘diligent search’.

ECP definition: means a person purchasing commercial insurance that:

Retains a qualified risk manager to negotiate coverage, and

Paid nationwide P&C insurance premiums in excess of $100,000 in the preceding 12 months.

In addition, the person must meet at least one of the following criteria.

Net worth in excess

of $20 million

Annual revenue in excess of

$50 million

More than 500 full

time employees

If a municipalit

y population more than

50,000If an NFP,

annual expenditure

of $30 million

© Lloyd’s6

‘Industrial Insured’ to ‘Exempt Commercial Purchaser’

Surplus lines brokers must get the ECP to sign a disclosure acknowledging cover may be available in the admitted market.

ECP is still treated as a surplus lines transaction, unlike industrial insured which is exempt business.

Some states have replaced industrial insured exemptions with the ECP standard, some states now have both an industrial insured and an ECP exemption

Need to review individual state pages on Crystal to determine which is available, or if both are.

© Lloyd’s7

MAT Exemptions Originally, some states were going to repeal their MAT exemption

States who had this in their bill have since removed this from their NRRA legislation

All states who had an MAT exemption prior to the NRRA have kept this exemption

© Lloyd’s8

Independent Procurement Independent procurement is defined as ‘non admitted’ insurance

(like surplus lines) and is therefore impacted by the NRRA.

However, independent procurements are permitted by virtue of federal case law, therefore the eligibility of independent procurement is not affected by the NRRA.

The requirements for tax are impacted by the NRRA.

Only the ‘home state’ may regulate and tax independent procurements.

© Lloyd’s9

Group Schemes Group schemes may be impacted in some states, were they

have included the definition of ‘home state’ found in the Nonadmitted Insurance Multistate Agreement (‘NIMA’)

The definition requires individual regulatory compliance (i.e. a diligent search of the admitted market) for every group member

These states cannot be covered under a group policy, post-NRRA

Further information will be issued shortly by Lloyd’s

© Lloyd’s10

Group Schemes However, the NRRA may result in improvements in states where group

schemes have in the past been problematic, ‘problem states’.

Historically, some states have required premium for group members in their state to be carved out and premium tax paid.

After NRRA implementation on July 21, these states can no longer require this because only the ‘home state’ can tax the transaction.

Premium tax paid 100% to the home state – i.e. State where master policy is issued

Again, revised information from Lloyd’s will be issued shortly

© Lloyd’s11

Admitted / Licensed Business Lloyd’s is an admitted (licensed) insurer in Kentucky, Illinois and the USVI.

Multistate Risks

Multistate risk surplus lines placements sometimes include risks located in Kentucky, Illinois or the USVI.

For these risks the portion of the premium allocated to Kentucky or Illinois may be carved out and premium tax paid on an admitted basis for that portion of the premium.

Admitted Business will continue to be carved cut

Brokers will need to continue reporting Kentucky, Illinois & USVI admitted business and allocating premium so that Lloyd’s can pay the appropriate licensed tax

© Lloyd’s12

Surplus lines: Eligibility Under NRRA states cannot prevent brokers from placing surplus lines business

with insurers listed on the NAIC Quarterly Listing of Alien Insurers (“White List”)

Current Position of State Filings

Many states have adopted this in their NRRA implementation legislation and will no longer require filings from Lloyd’s

But this doesn’t necessarily mean an end to all state filings

For now, Lloyd’s will continue to make filings, but will include a disclosure that the filing is done on a voluntary basis

Filing Run-off – the goal is to reduce the number of filings in line with NRRA intent

NAIC International Insurers Department (IID) Filing more important

Role of the IID office will be more significant for alien surplus lines insurers that are listed on the White List

Lloyd’s is working with IID to discuss filing requirements

© Lloyd’s13

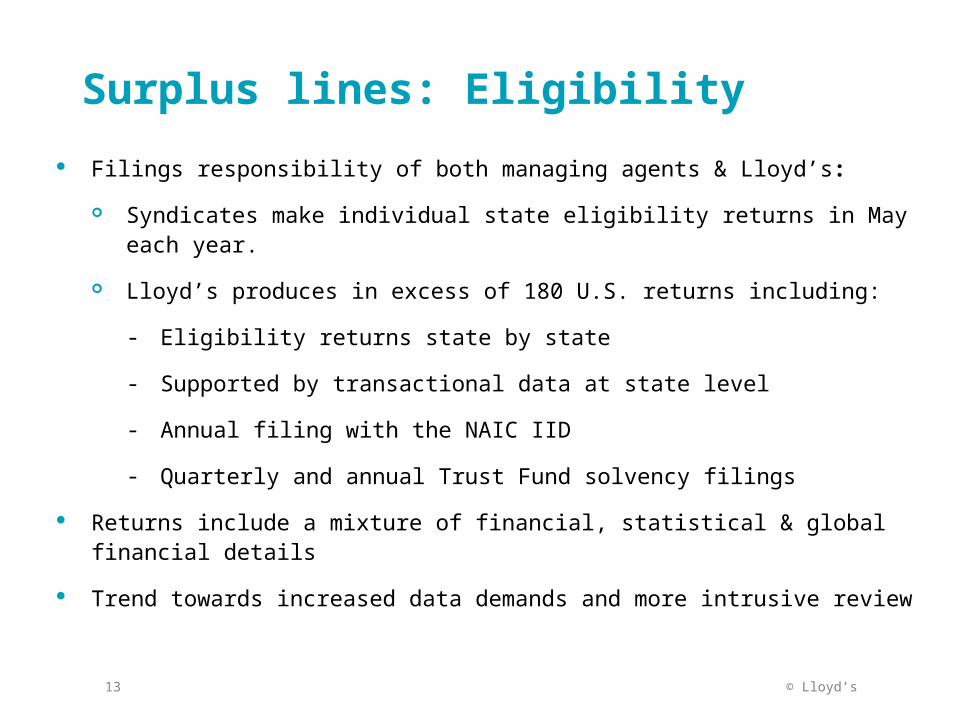

Surplus lines: Eligibility

Filings responsibility of both managing agents & Lloyd’s:

Syndicates make individual state eligibility returns in May each year.

Lloyd’s produces in excess of 180 U.S. returns including:

- Eligibility returns state by state

- Supported by transactional data at state level

- Annual filing with the NAIC IID

- Quarterly and annual Trust Fund solvency filings

Returns include a mixture of financial, statistical & global financial details

Trend towards increased data demands and more intrusive review

© Lloyd’s14

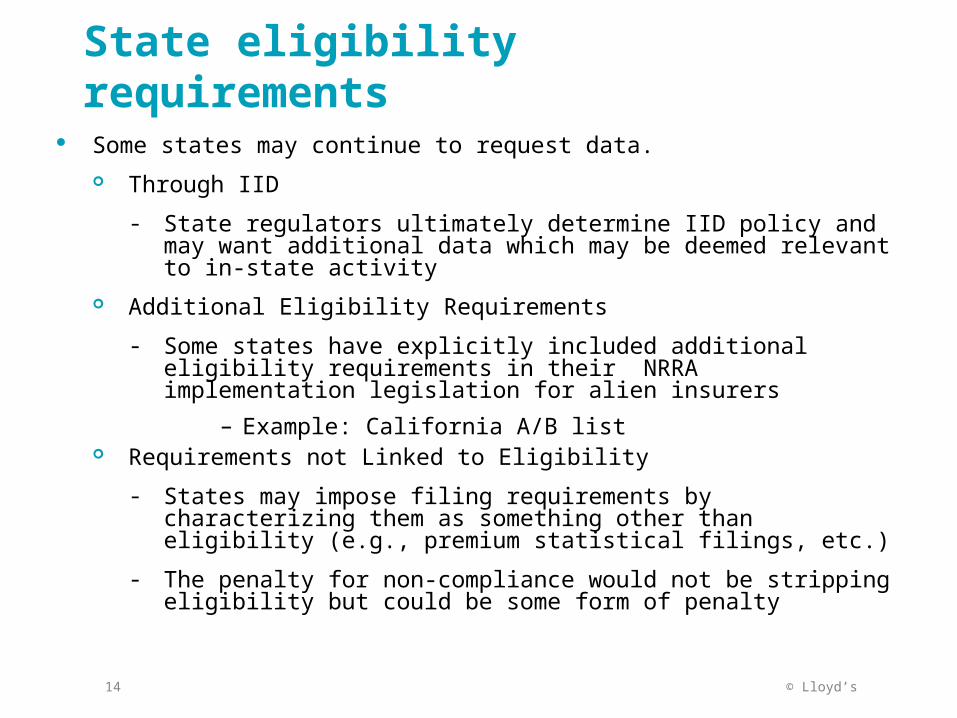

State eligibility requirements Some states may continue to request data.

Through IID

- State regulators ultimately determine IID policy and may want additional data which may be deemed relevant to in-state activity

Additional Eligibility Requirements

- Some states have explicitly included additional eligibility requirements in their NRRA implementation legislation for alien insurers

– Example: California A/B list Requirements not Linked to Eligibility

- States may impose filing requirements by characterizing them as something other than eligibility (e.g., premium statistical filings, etc.)

- The penalty for non-compliance would not be stripping eligibility but could be some form of penalty

© Lloyd’s15

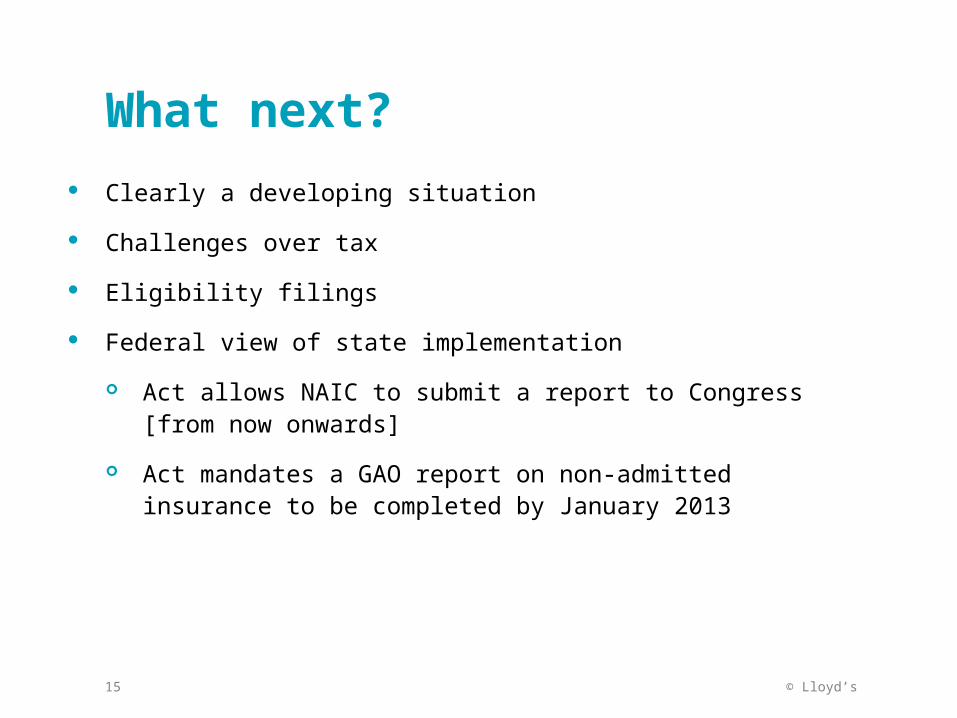

What next?

Clearly a developing situation

Challenges over tax

Eligibility filings

Federal view of state implementation

Act allows NAIC to submit a report to Congress [from now onwards]

Act mandates a GAO report on non-admitted insurance to be completed by January 2013

© Lloyd’s16