Embed Size (px)

Citation preview

U.S. private equity deal flow

0

100

200

300

400

500

600

700

800

900

0

20

40

60

80

100

120

140

160

180

200

2009 2010 2011 2012 2013 2014

US$ billions Count

Capital invested (left)

Deals closed (right)

Source: Pitchbook.

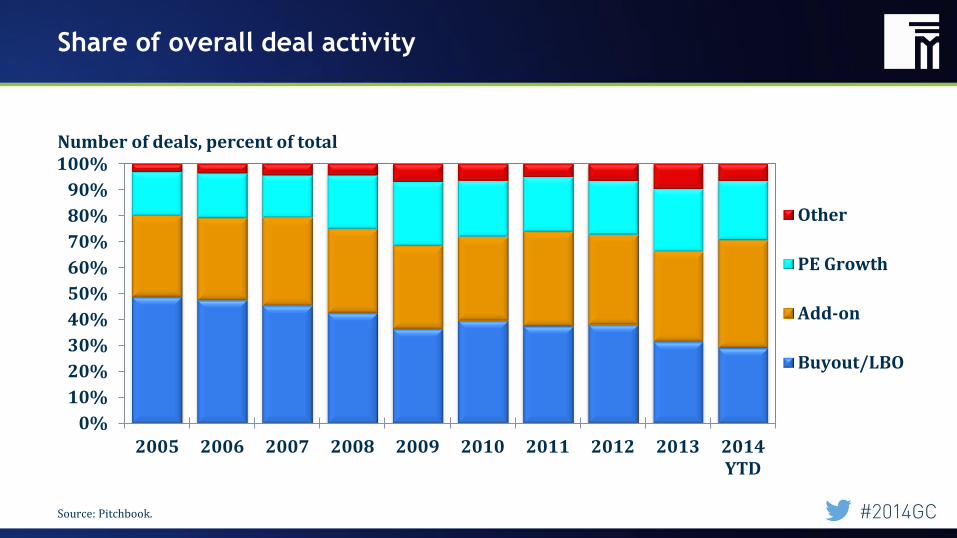

Share of overall deal activity

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014YTD

Other

PE Growth

Add-on

Buyout/LBO

Number of deals, percent of total

Source: Pitchbook.

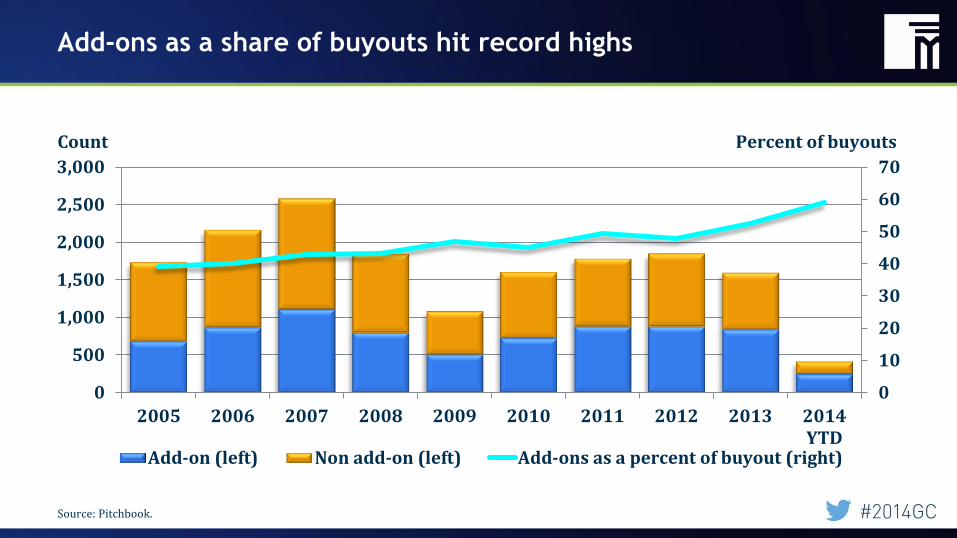

Add-ons as a share of buyouts hit record highs

0

10

20

30

40

50

60

70

0

500

1,000

1,500

2,000

2,500

3,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014YTD

Add-on (left) Non add-on (left) Add-ons as a percent of buyout (right)

Count Percent of buyouts

Source: Pitchbook.

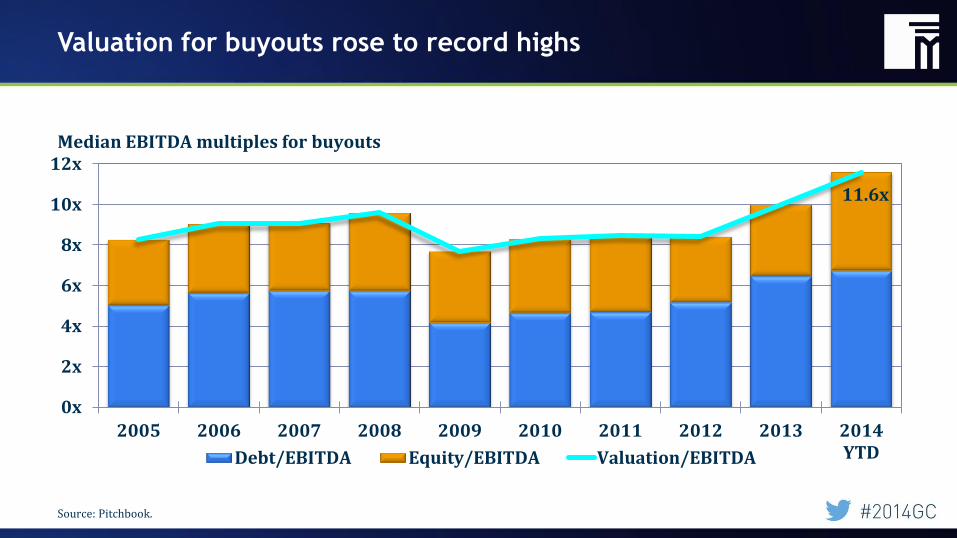

Valuation for buyouts rose to record highs

0x

2x

4x

6x

8x

10x

12x

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014YTDDebt/EBITDA Equity/EBITDA Valuation/EBITDA

Median EBITDA multiples for buyouts

11.6x

Source: Pitchbook.

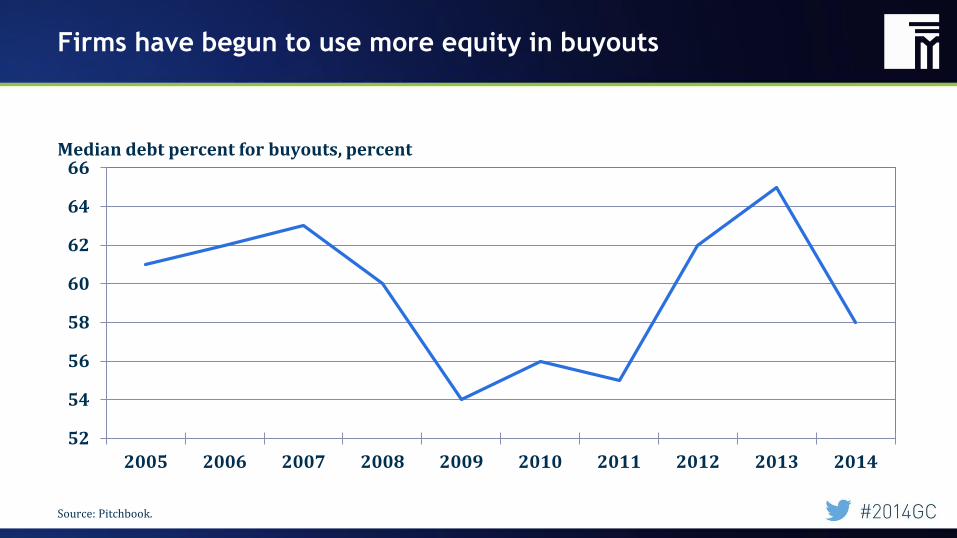

Firms have begun to use more equity in buyouts

52

54

56

58

60

62

64

66

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Median debt percent for buyouts, percent

Source: Pitchbook.

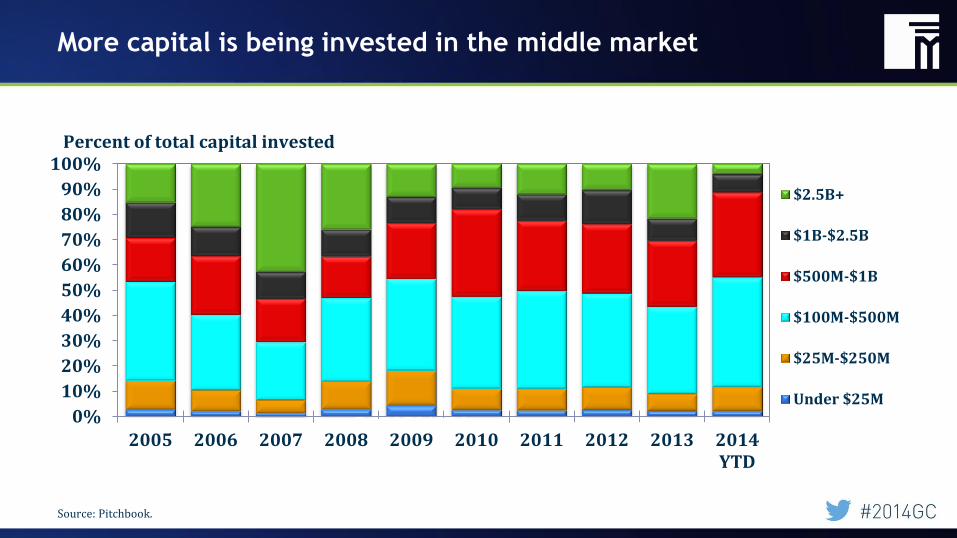

More capital is being invested in the middle market

8.197660441 9.821098686 10.94742011 9.657081486 7.069781081 9.334613163 9.607647915 11.36363048 9.957557606 2.305053263 0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014YTD

$2.5B+

$1B-$2.5B

$500M-$1B

$100M-$500M

$25M-$250M

Under $25M

Percent of total capital invested

Source: Pitchbook.

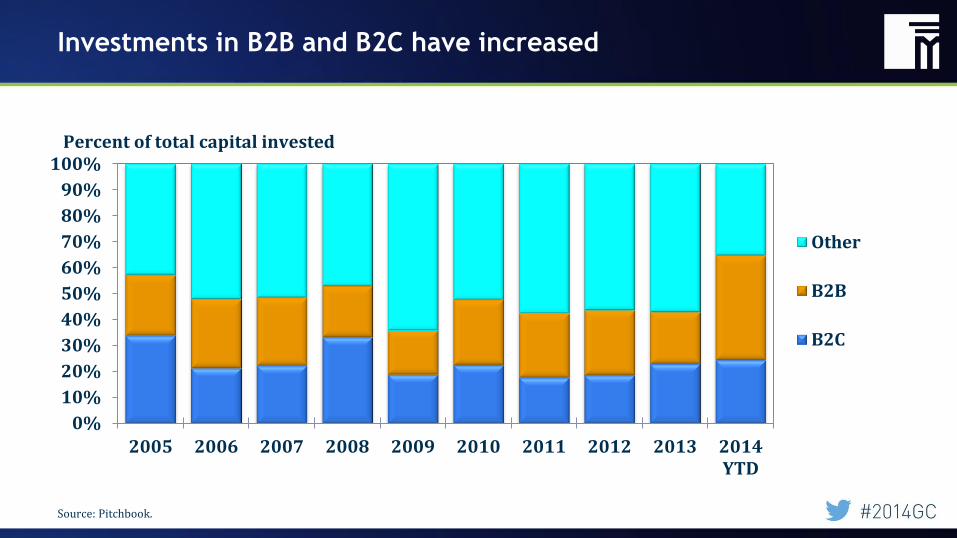

Investments in B2B and B2C have increased

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014YTD

Other

B2B

B2C

Percent of total capital invested

Source: Pitchbook.

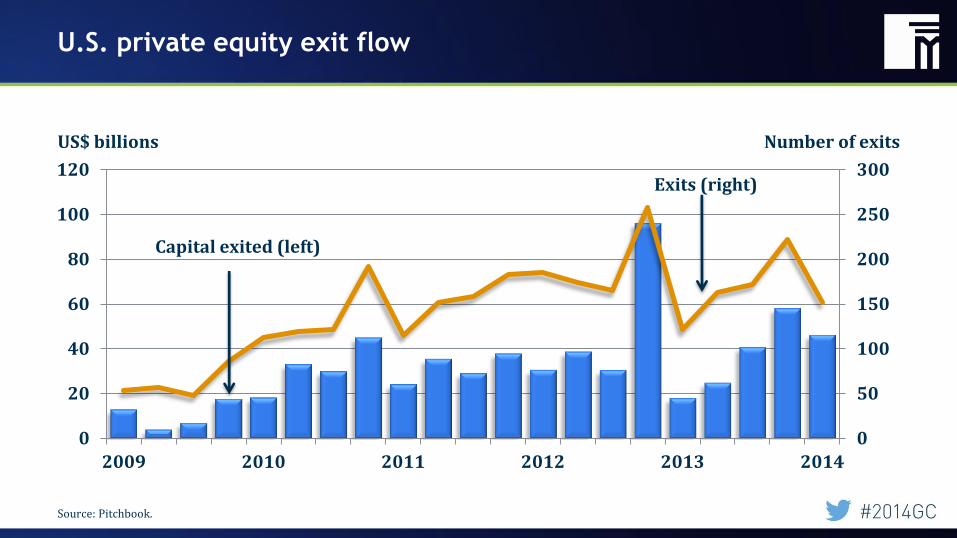

U.S. private equity exit flow

0

50

100

150

200

250

300

0

20

40

60

80

100

120

2009 2010 2011 2012 2013 2014

US$ billions Number of exits

Capital exited (left)

Exits (right)

Source: Pitchbook.

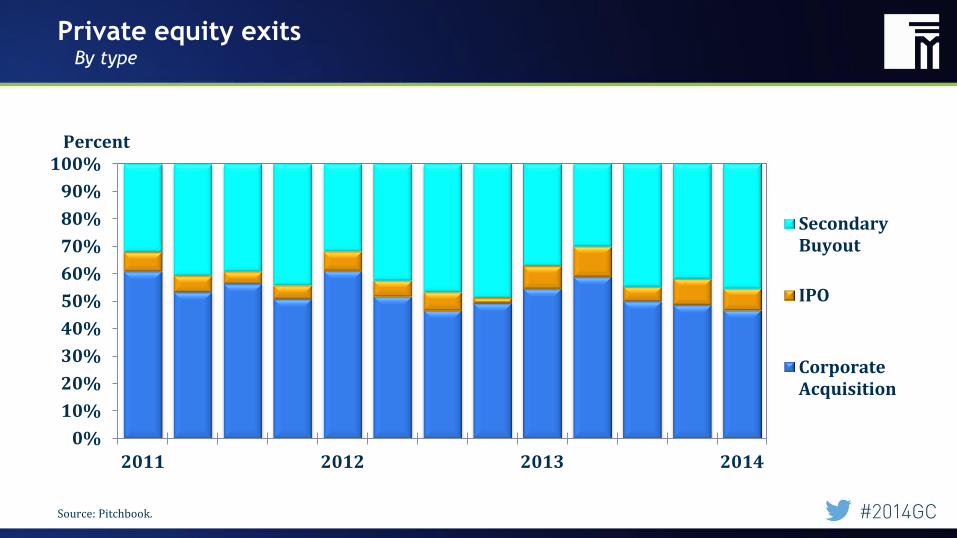

Private equity exits By type

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013 2014

SecondaryBuyout

IPO

CorporateAcquisition

Percent

Source: Pitchbook.

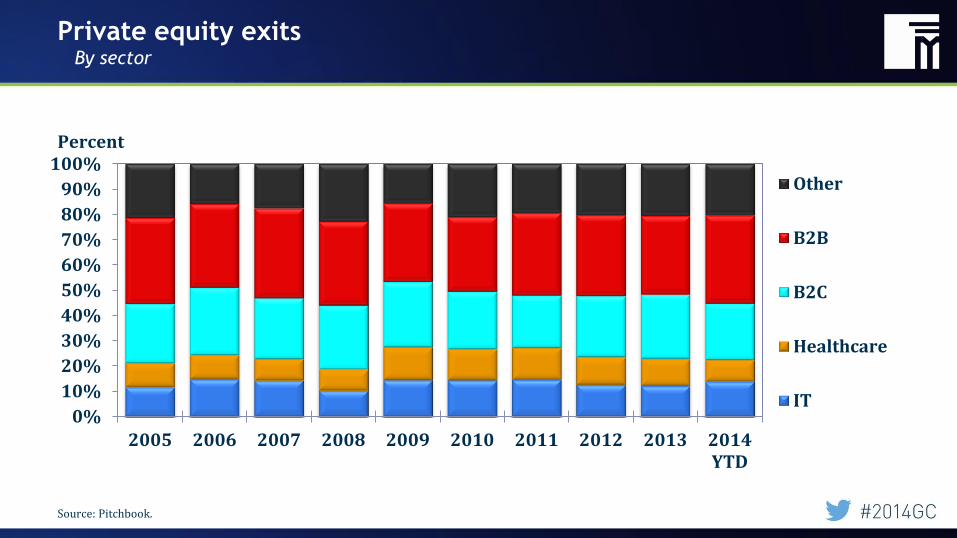

Private equity exits By sector

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014YTD

Other

B2B

B2C

Healthcare

IT

Percent

Source: Pitchbook.

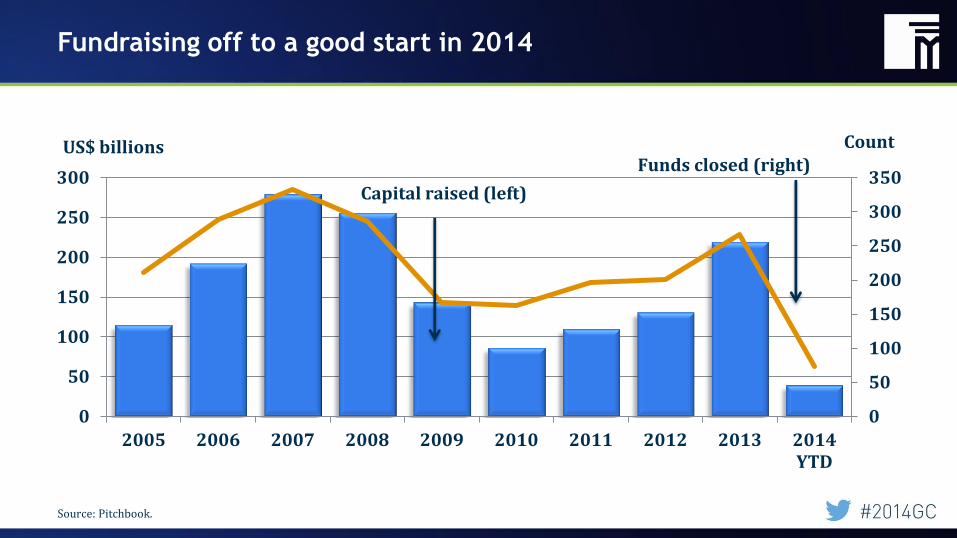

Fundraising off to a good start in 2014

0

50

100

150

200

250

300

350

0

50

100

150

200

250

300

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014YTD

US$ billions Count

Capital raised (left)

Funds closed (right)

Source: Pitchbook.

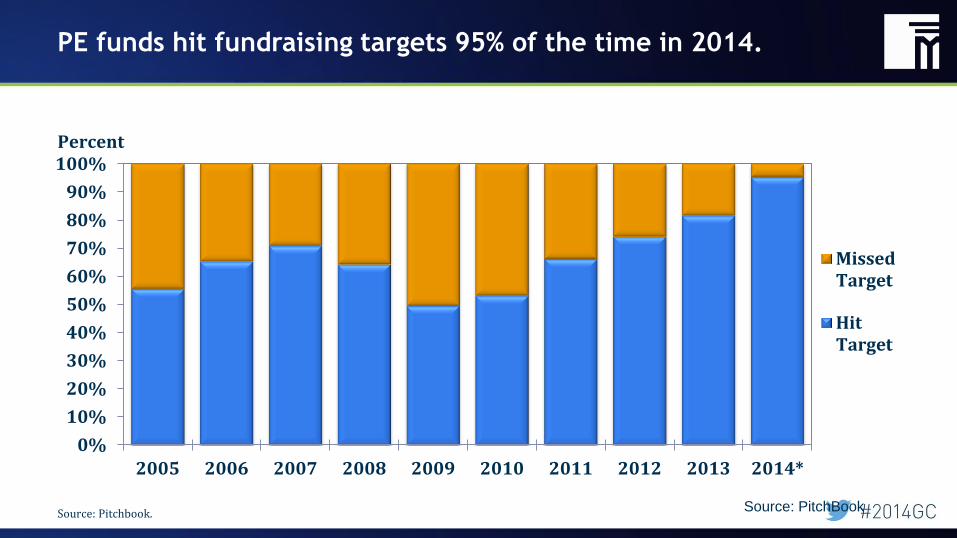

PE funds hit fundraising targets 95% of the time in 2014.

Source: PitchBook

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014*

MissedTarget

HitTarget

Percent

Source: Pitchbook.

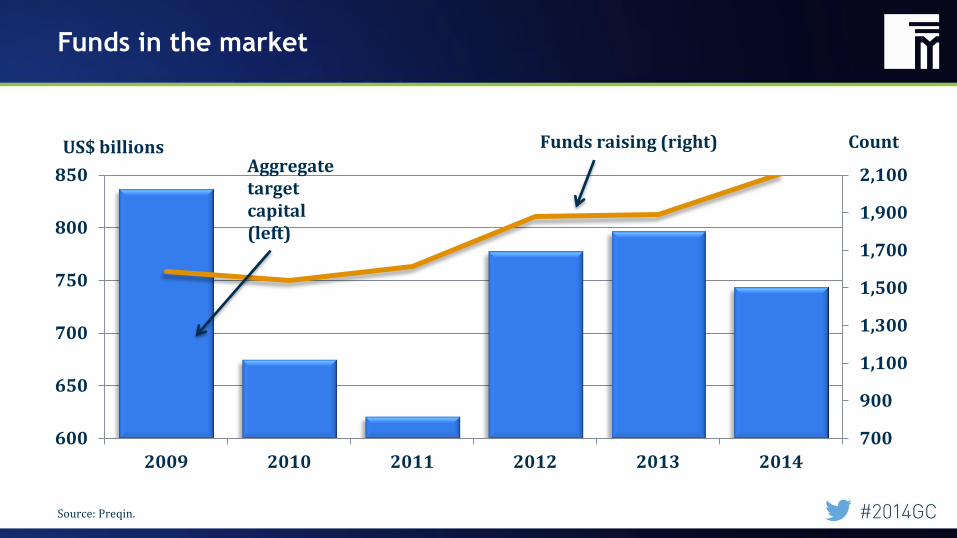

Funds in the market

700

900

1,100

1,300

1,500

1,700

1,900

2,100

600

650

700

750

800

850

2009 2010 2011 2012 2013 2014

US$ billions Aggregate target capital (left)

Funds raising (right) Count

Source: Preqin.

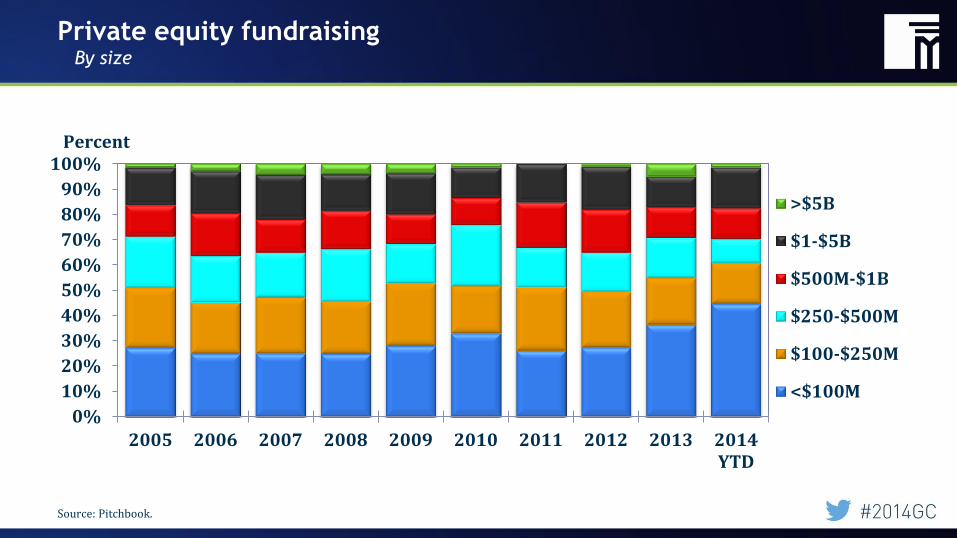

Private equity fundraising By size

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014YTD

>$5B

$1-$5B

$500M-$1B

$250-$500M

$100-$250M

<$100M

Percent

Source: Pitchbook.

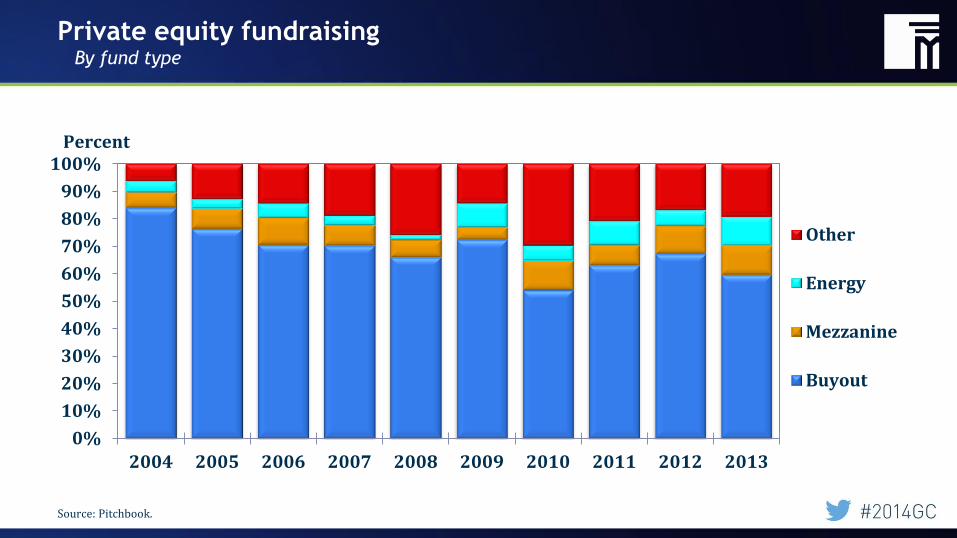

Private equity fundraising By fund type

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Other

Energy

Mezzanine

Buyout

Percent

Source: Pitchbook.

Global funds on the road

500

600

700

800

900

1000

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2008 2009 2010 2011 2012 2013 2014

US$ billions Aggregate target capital (left)

Funds on the road (right)

Count

Source: Preqin.

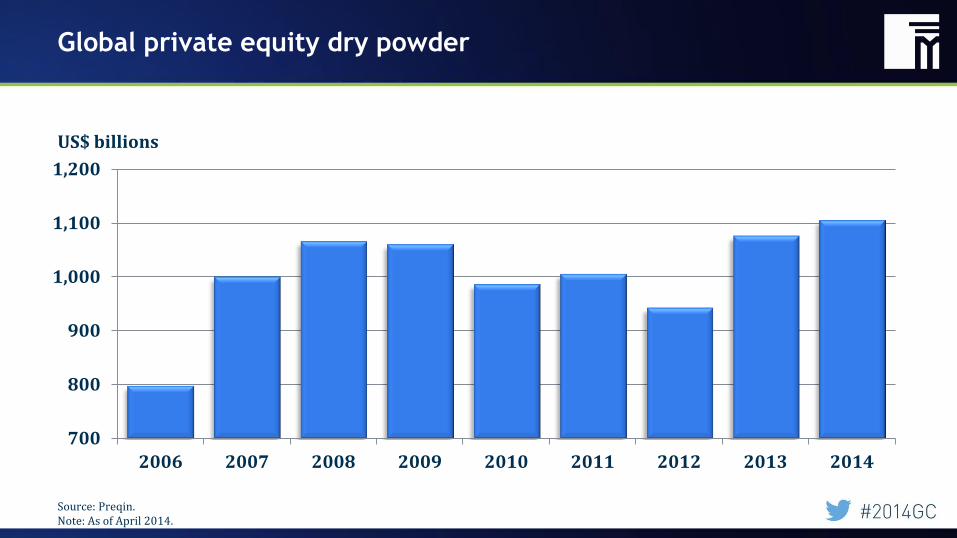

Global private equity dry powder

700

800

900

1,000

1,100

1,200

2006 2007 2008 2009 2010 2011 2012 2013 2014

US$ billions

Source: Preqin. Note: As of April 2014.

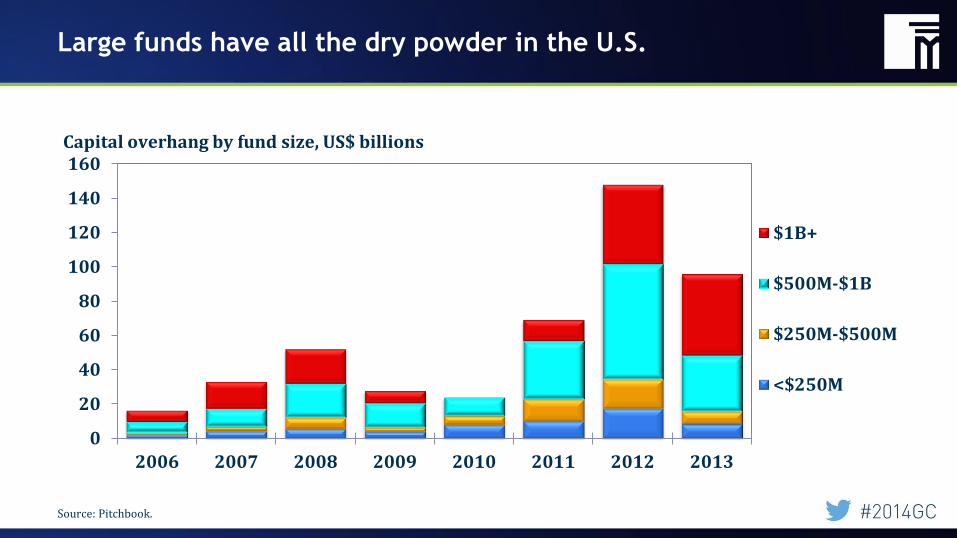

Large funds have all the dry powder in the U.S.

0

20

40

60

80

100

120

140

160

2006 2007 2008 2009 2010 2011 2012 2013

$1B+

$500M-$1B

$250M-$500M

<$250M

Capital overhang by fund size, US$ billions

Source: Pitchbook.

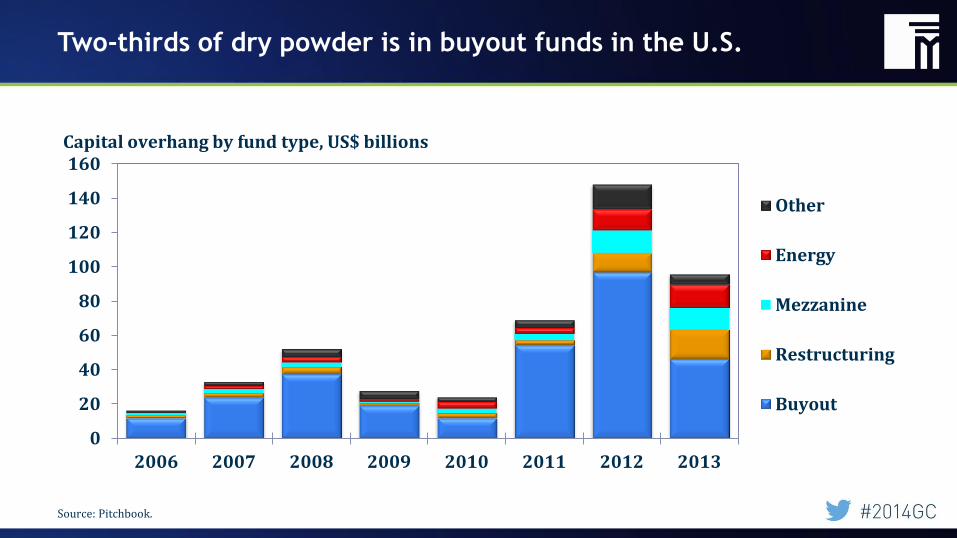

Two-thirds of dry powder is in buyout funds in the U.S.

0

20

40

60

80

100

120

140

160

2006 2007 2008 2009 2010 2011 2012 2013

Other

Energy

Mezzanine

Restructuring

Buyout

Capital overhang by fund type, US$ billions

Source: Pitchbook.

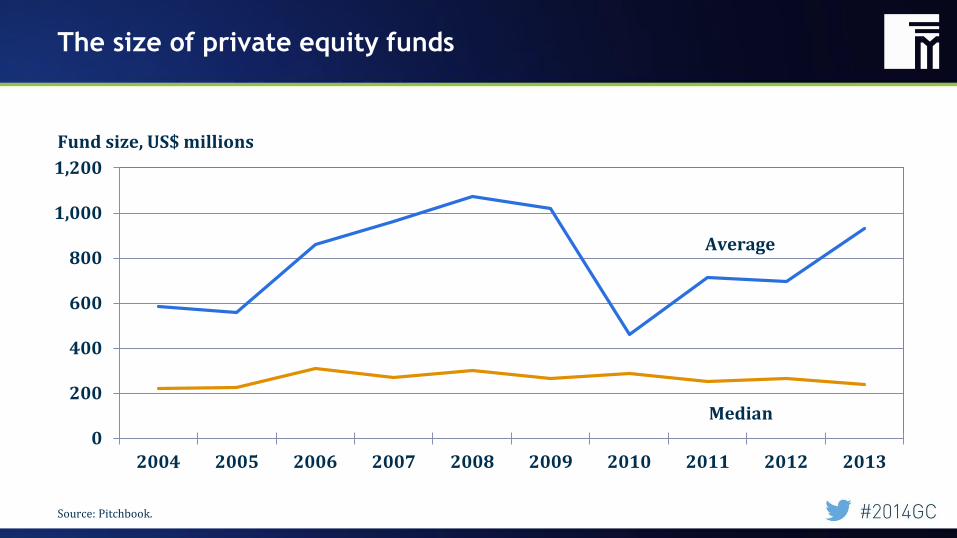

The size of private equity funds

0

200

400

600

800

1,000

1,200

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Fund size, US$ millions

Median

Average

Source: Pitchbook.

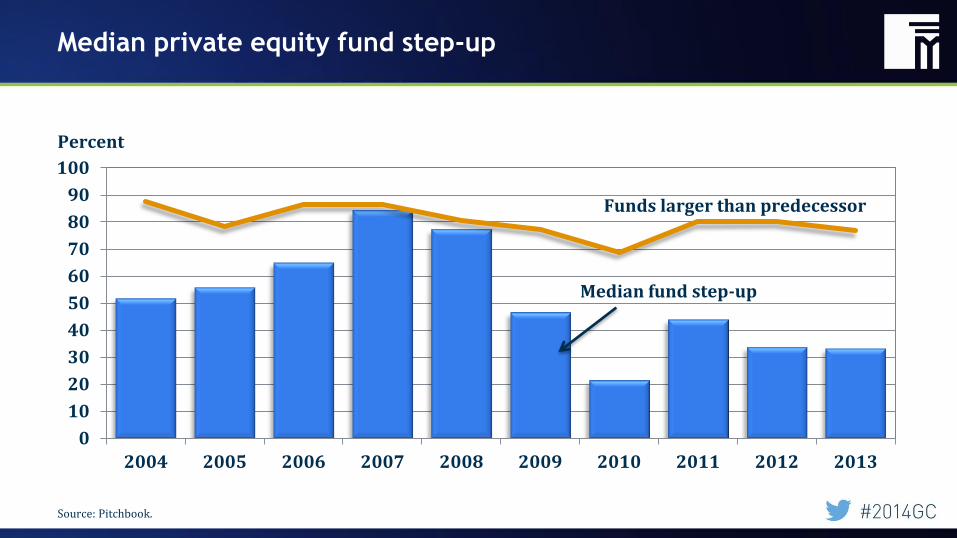

Median private equity fund step-up

0

10

20

30

40

50

60

70

80

90

100

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Percent

Funds larger than predecessor

Median fund step-up

Source: Pitchbook.

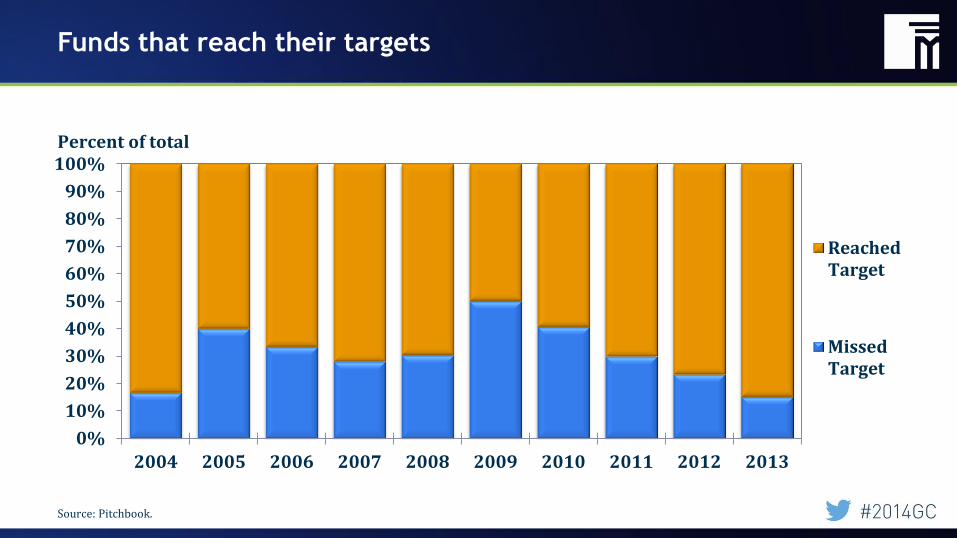

Funds that reach their targets

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

ReachedTarget

MissedTarget

Percent of total

Source: Pitchbook.

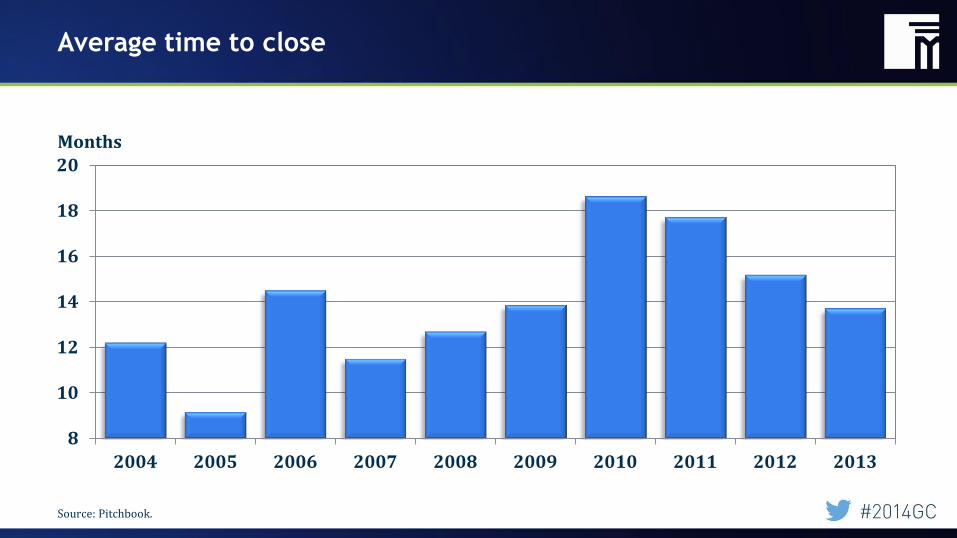

Average time to close

8

10

12

14

16

18

20

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Months

Source: Pitchbook.

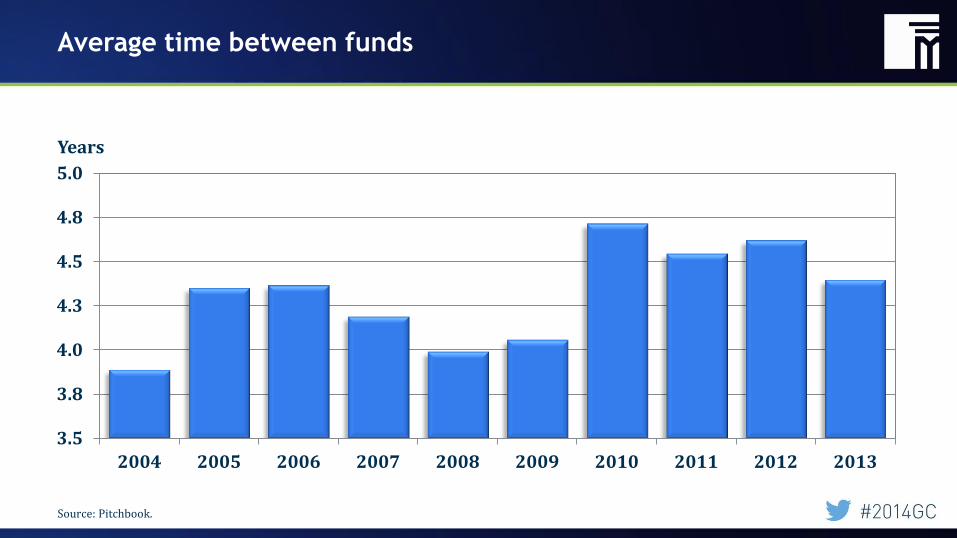

Average time between funds

3.5

3.8

4.0

4.3

4.5

4.8

5.0

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Years

Source: Pitchbook.

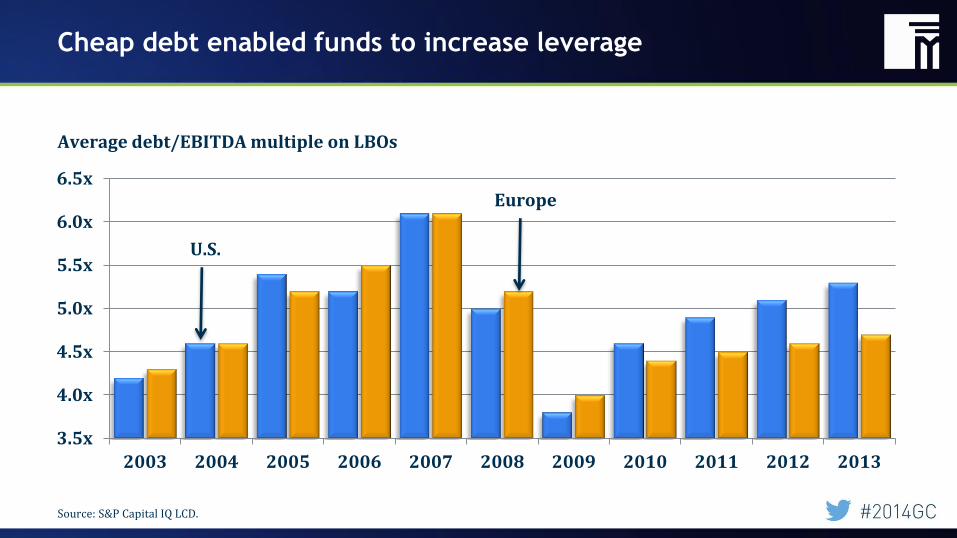

Cheap debt enabled funds to increase leverage

3.5x

4.0x

4.5x

5.0x

5.5x

6.0x

6.5x

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Average debt/EBITDA multiple on LBOs

U.S.

Europe

Source: S&P Capital IQ LCD.

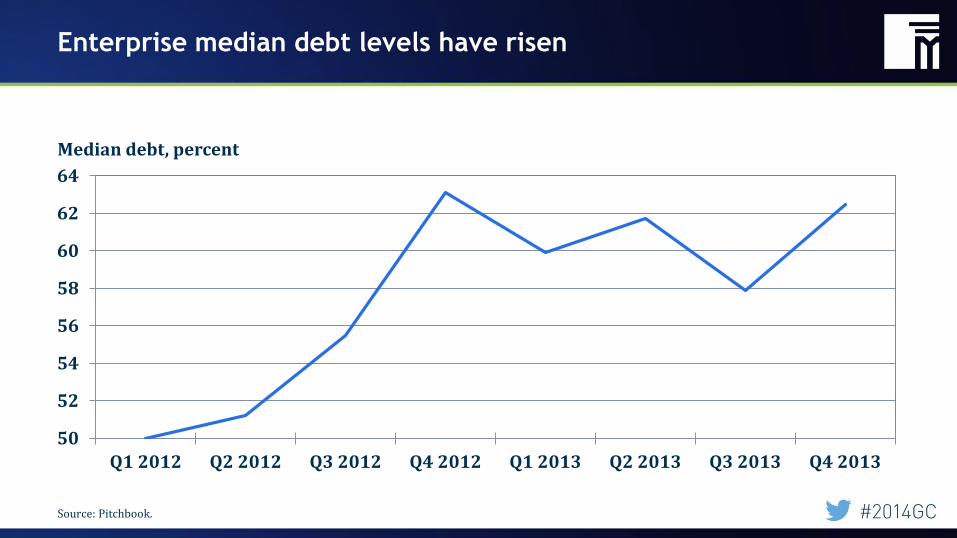

Enterprise median debt levels have risen

50

52

54

56

58

60

62

64

Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013

Median debt, percent

Source: Pitchbook.

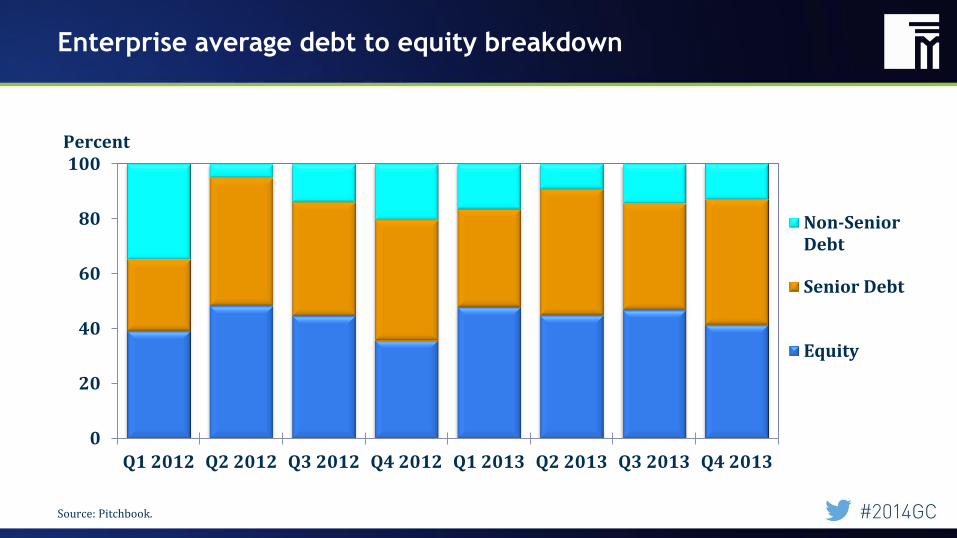

Enterprise average debt to equity breakdown

0

20

40

60

80

100

Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013

Non-SeniorDebt

Senior Debt

Equity

Percent

Source: Pitchbook.

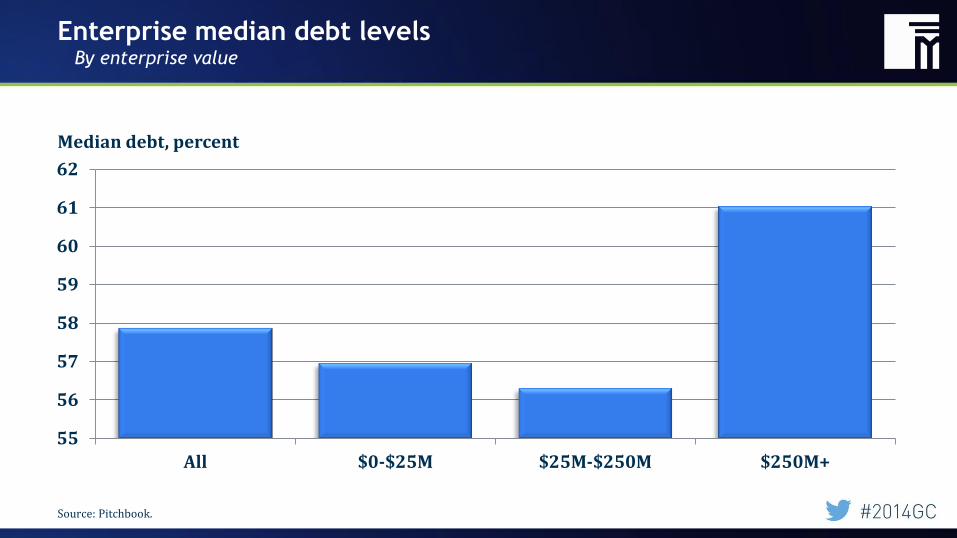

Enterprise median debt levels By enterprise value

55

56

57

58

59

60

61

62

All $0-$25M $25M-$250M $250M+

Median debt, percent

Source: Pitchbook.

The value of U.S. companies

By enterprise value

0

2

4

6

8

10

12

Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013

Median EV/EBITDA multiple

All $25-250M

$0-25M

$250M+

Source: Pitchbook.

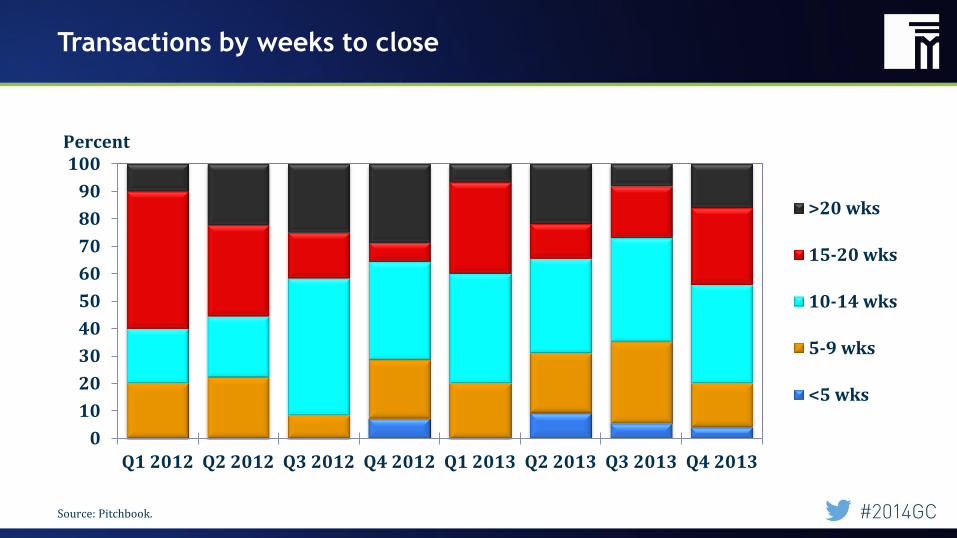

Transactions by weeks to close

0

10

20

30

40

50

60

70

80

90

100

Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013

>20 wks

15-20 wks

10-14 wks

5-9 wks

<5 wks

Percent

Source: Pitchbook.

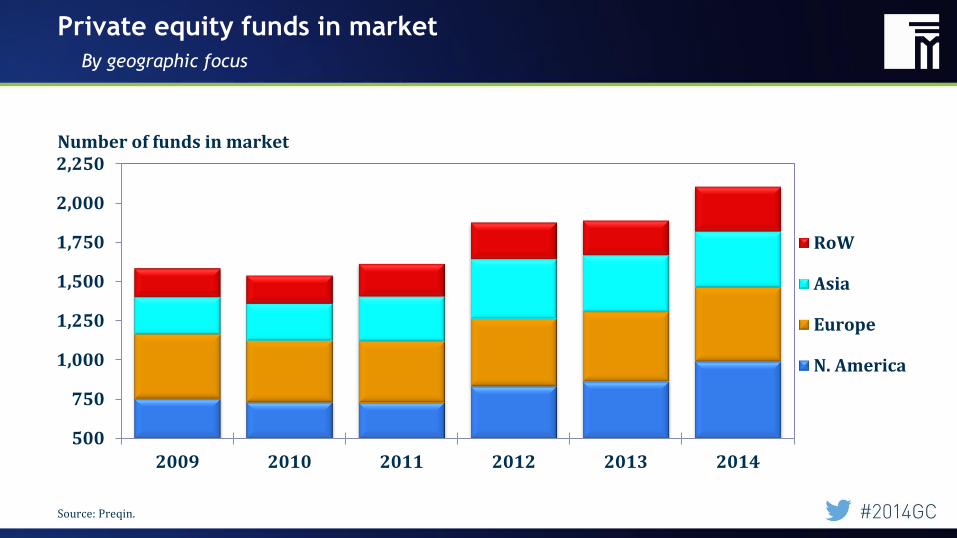

Private equity funds in market

By geographic focus

500

750

1,000

1,250

1,500

1,750

2,000

2,250

2009 2010 2011 2012 2013 2014

RoW

Asia

Europe

N. America

Number of funds in market

Source: Preqin.

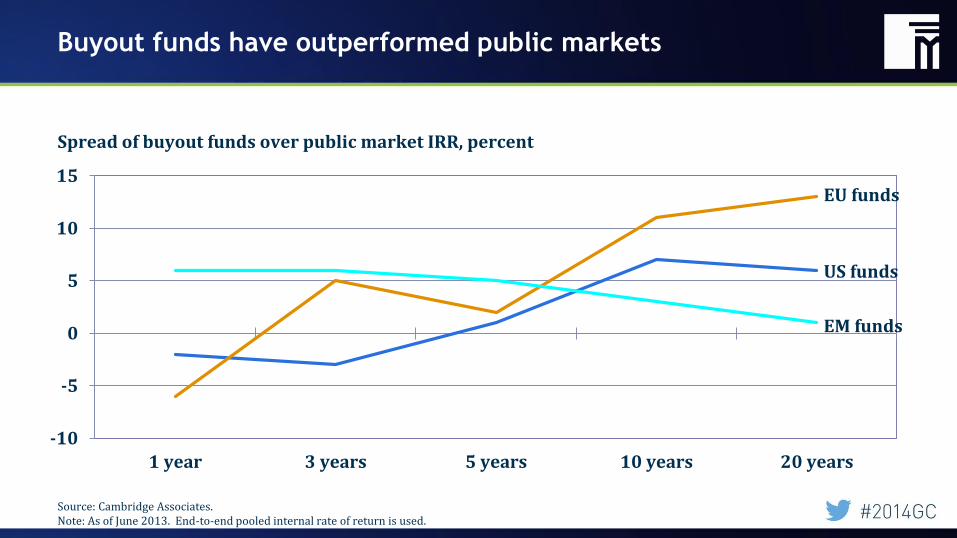

Buyout funds have outperformed public markets

-10

-5

0

5

10

15

1 year 3 years 5 years 10 years 20 years

Spread of buyout funds over public market IRR, percent

EU funds

US funds

EM funds

Source: Cambridge Associates. Note: As of June 2013. End-to-end pooled internal rate of return is used.

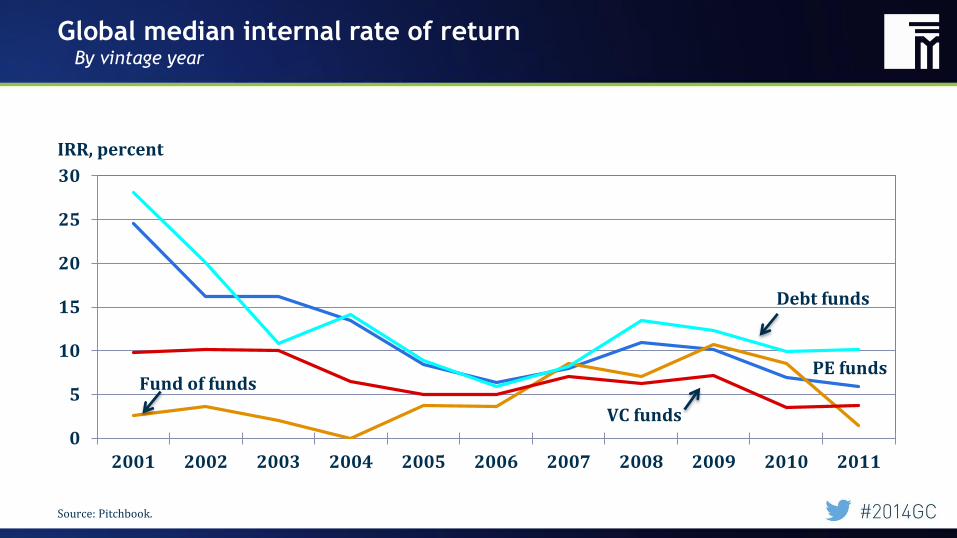

Global median internal rate of return By vintage year

0

5

10

15

20

25

30

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

IRR, percent

VC funds

PE funds Fund of funds

Debt funds

Source: Pitchbook.

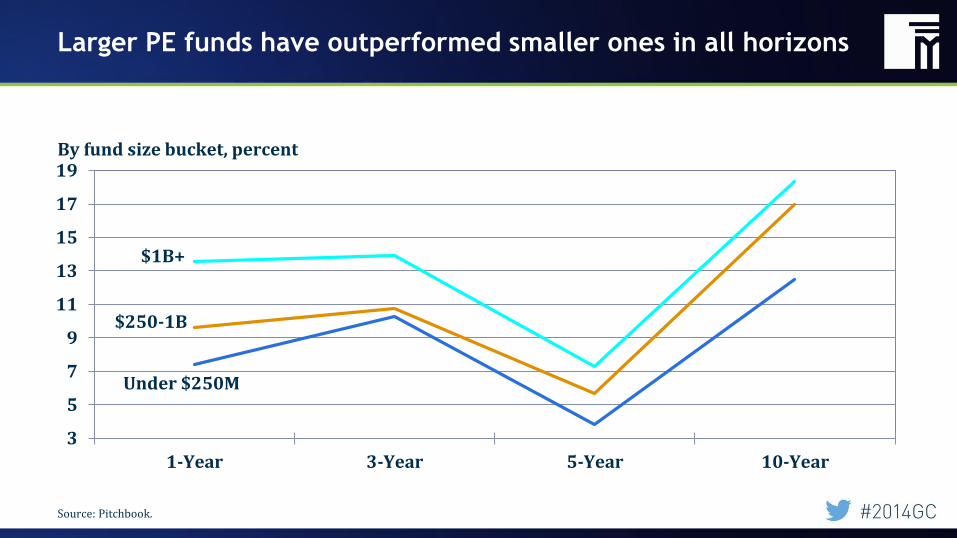

Larger PE funds have outperformed smaller ones in all horizons

3

5

7

9

11

13

15

17

19

1-Year 3-Year 5-Year 10-Year

By fund size bucket, percent

$1B+

$250-1B

Under $250M

Source: Pitchbook.

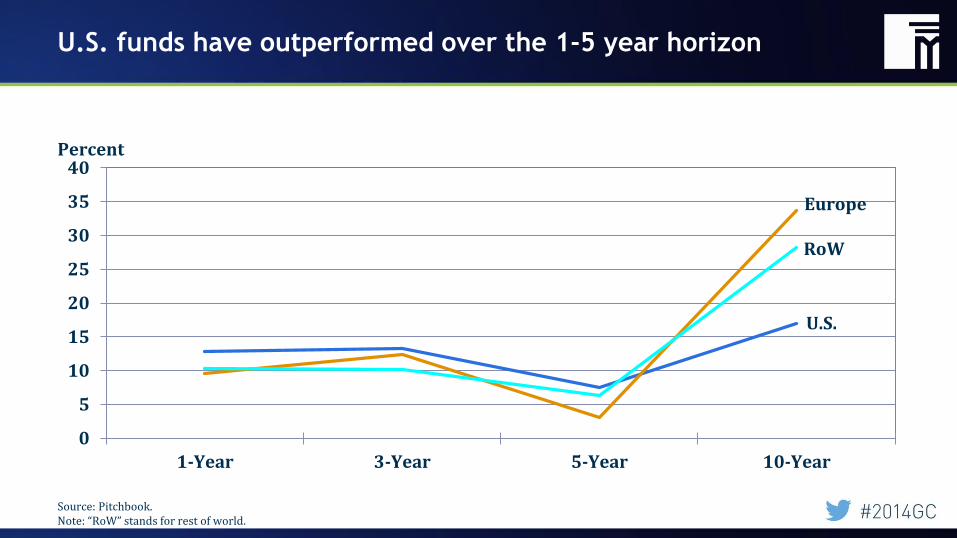

U.S. funds have outperformed over the 1-5 year horizon

0

5

10

15

20

25

30

35

40

1-Year 3-Year 5-Year 10-Year

Percent

U.S.

RoW

Europe

Source: Pitchbook. Note: “RoW” stands for rest of world.

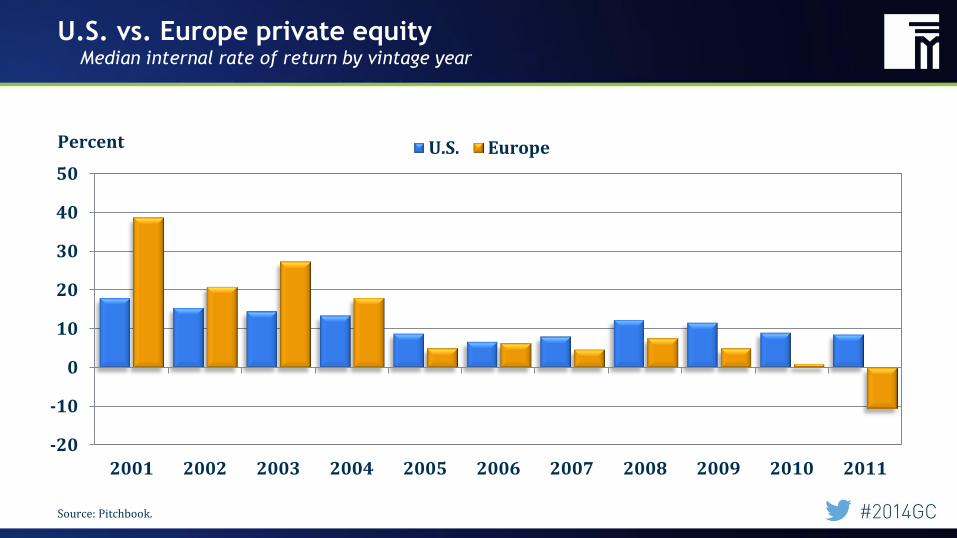

U.S. vs. Europe private equity Median internal rate of return by vintage year

-20

-10

0

10

20

30

40

50

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

U.S. EuropePercent

Source: Pitchbook.

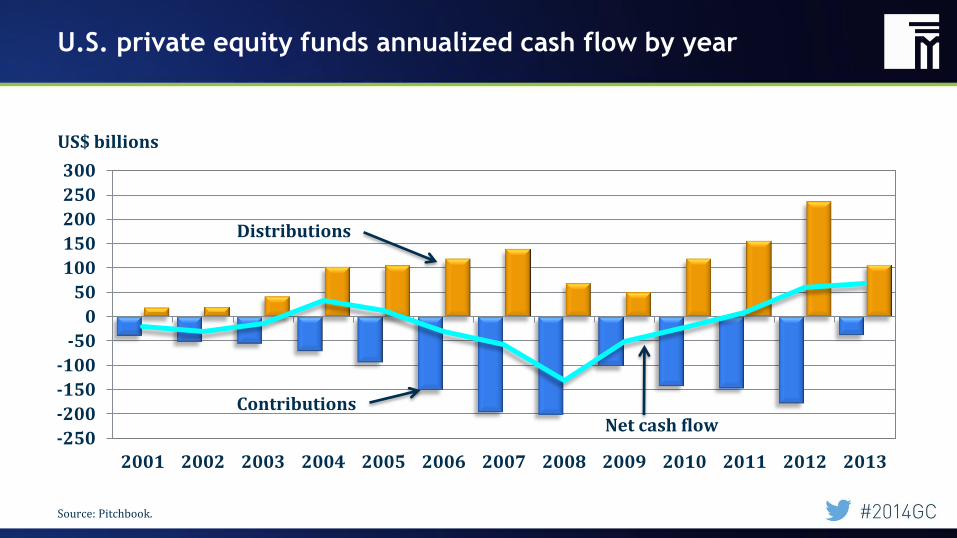

U.S. private equity funds annualized cash flow by year

-250

-200

-150

-100

-50

0

50

100

150

200

250

300

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

US$ billions

Contributions

Distributions

Net cash flow

Source: Pitchbook.

![SRZ 2011 Private Equity Buyer Public Target MA Deal Study 3rd Quarter[1]](https://img.pdfslide.us/doc/110x75/5448d9e6b1af9f5b618b4c1f/srz-2011-private-equity-buyer-public-target-ma-deal-study-3rd-quarter1.jpg)