Embed Size (px)

Citation preview

U.S. Oil & Gas Industry

Chartbook

BBVA Research USA

Houston, TX March 2015

DISCLAIMER This document was prepared by Banco Bilbao Vizcaya (BBVA) BBVA Research U.S. on behalf of itself and its affiliated companies (each BBVA Group Company) for distribution in the United States and the rest of the world and is provided for information purposes only. Within the US, BBVA operates primarily through its subsidiary Compass Bank. The information, opinions, estimates and forecasts contained herein refer to the specific date and are subject to changes without notice due to market fluctuations. The information, opinions, estimates and forecasts contained in this document have been gathered or obtained from public sources, believed to be correct by the Company concerning their accuracy, completeness, and/or correctness. This document is not an offer to sell or a solicitation to acquire or dispose of an interest in securities.

Bottom Line

• The drastic fall in oil in prices continues to remain at the forefront of economic activity, with the potential for faster economic growth (via higher consumption)

• Although prices appear to be stabilizing, the continued imbalance between supply and demand is expected to keep oil prices low in the short-run

• There are downside risks for energy-dependent industries and states, such as Texas, but there will ultimately be a rebalancing among states and regions

• The decline in oil prices is a net positive to the U.S. economy, benefiting consumers and energy-intensive industries

3

Oil Prices

4

Spot Prices U.S. Crude Oil and Natural Gas Spot Prices (avg, $/bbl & $/MMBTU)

Source: Haver Analytics

0

2

4

6

8

10

12

14

16

18

0

20

40

60

80

100

120

140

160

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

WTI (lhs)

Natural gas (rhs)

Great Recession

U,.S economy expands 2.9% between 2004-2007 U.S. production of crude oil goes from 4.9

million B/D to 9 million B/D

5

Spot Prices U.S. WTI Spot Price (avg, $/bbl)

Source: Haver Analytics

0

20

40

60

80

100

120

Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14 Jan-15 Feb-15 Mar-15

Saudi Arabia refusal to boost

production

China reports faster GDP growth U.S. sanctions to Russia

OPEC announces weaker demand U.S. production reaches record

high

EIA cuts its oil price forecasts

Libyan production increases by more than 300% from June 2014. Iraqi production increases by 24%

from previous year.

Eurozone GDP flat in Q2 14 due to shock contraction in

Germany

Rig count falls to lowest level since

July 2011

WTI at $49.61 as of March 6, 2015

6 Projections are generated by simulation of the EIA Regional Short-Term Energy Model Source: Energy Information Administration/ Haver Analytics

Prices WTI Historical and EIA Forecast ($/bbl)

0

20

40

60

80

100

120

Forecast

7 Source: Haver Analytics

Futures Prices WTI Futures ($/bbl)

40

50

60

70

80

90

100

110

1st expiring contract (nearby) 2-month

3-month 4-month

6-month 1-year

2-year

8

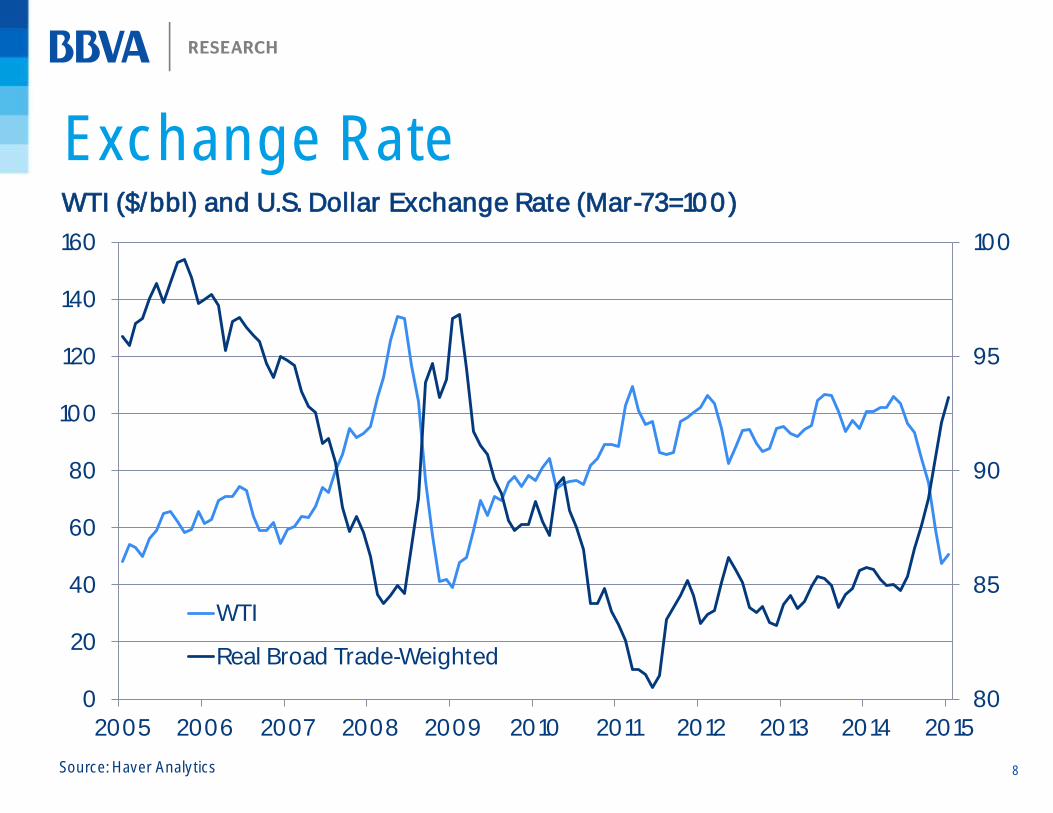

Exchange Rate WTI ($/bbl) and U.S. Dollar Exchange Rate (Mar-73=100)

Source: Haver Analytics

80

85

90

95

100

0

20

40

60

80

100

120

140

160

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

WTI

Real Broad Trade-Weighted

9

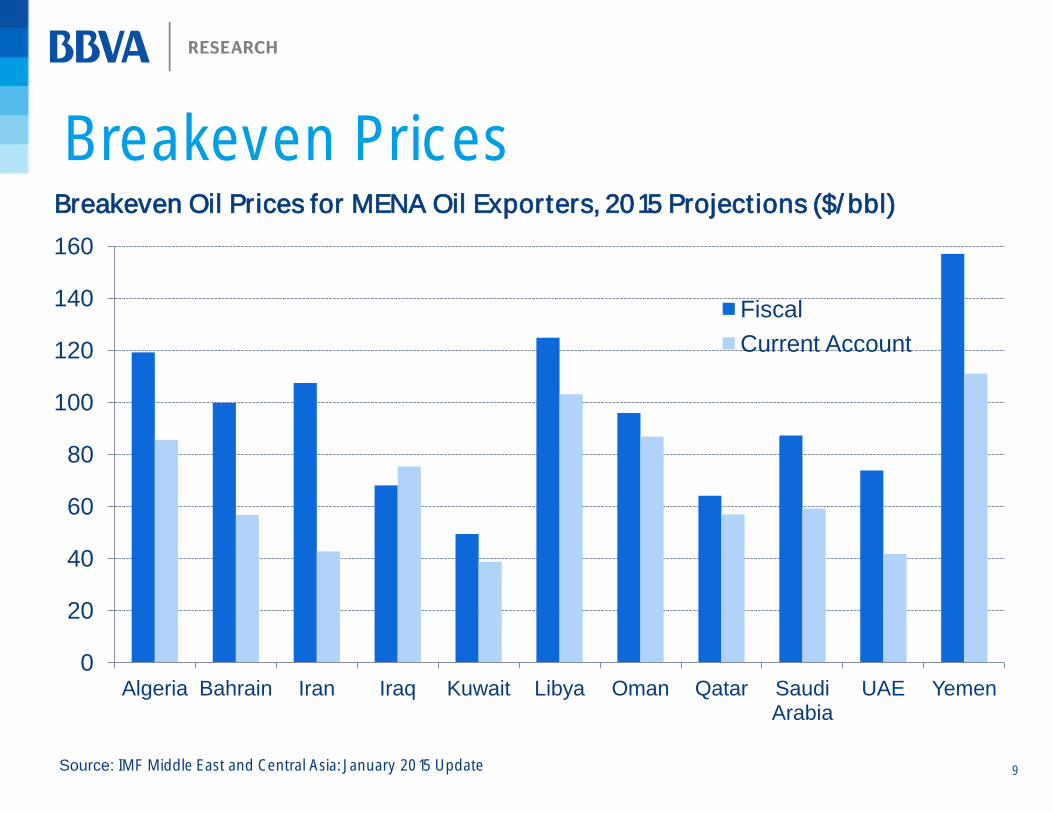

Breakeven Prices

0

20

40

60

80

100

120

140

160

Algeria Bahrain Iran Iraq Kuwait Libya Oman Qatar Saudi Arabia

UAE Yemen

Fiscal

Current Account

Breakeven Oil Prices for MENA Oil Exporters, 2015 Projections ($/bbl)

Source: IMF Middle East and Central Asia: January 2015 Update

10

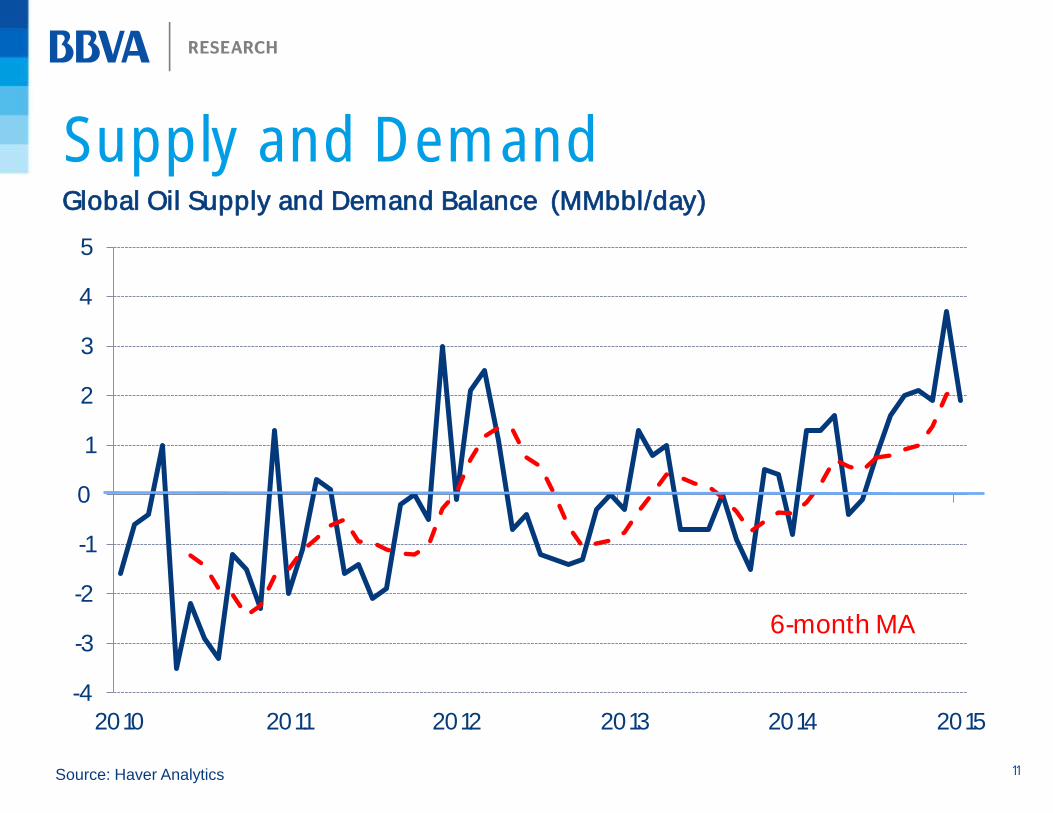

Global

Supply &

Demand

11

Supply and Demand Global Oil Supply and Demand Balance (MMbbl/day)

Source: Haver Analytics

-4

-3

-2

-1

0

1

2

3

4

5

2010 2011 2012 2013 2014 2015

6-month MA

12

Production Crude Oil Production (Mbbl/day, yoy % change)

Source: Haver Analytics

-10%

-5%

0%

5%

10%

15%

20%

25%

2010 2011 2012 2013 2014

OPEC U.S. Other Non-OPEC

13

Supply by Region Proved Crude Oil Reserves in 2013

(share of total, %)

Worldwide Production in 2013

(share of total, %)

Source: 2014 BP Statistical Review of World Energy & BP Energy Outlook 2035

19%

9%

20% 32%

10% 9%

North America Central and South America Europe Middle East Africa Asia Pacific

14%

20%

9% 48%

8%

2%

North America

Central and South America

Europe

Middle East

Africa

Asia Pacific

14

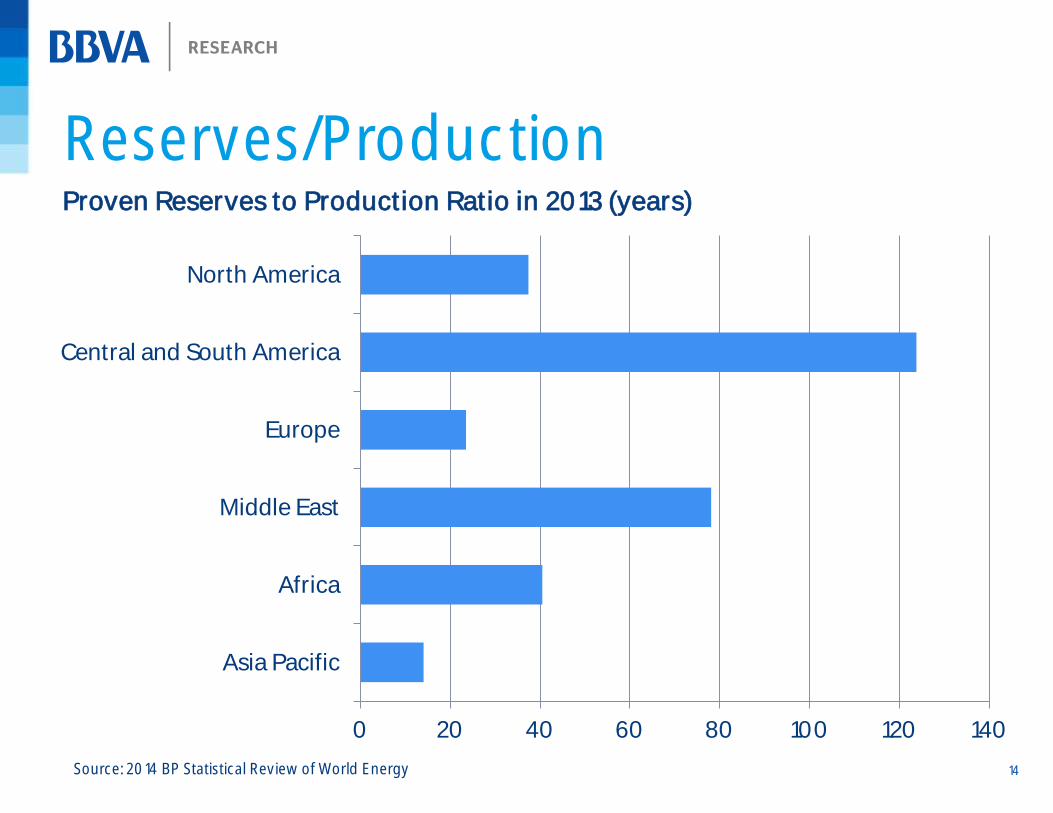

Reserves/Production Proven Reserves to Production Ratio in 2013 (years)

Source: 2014 BP Statistical Review of World Energy

0 20 40 60 80 100 120 140

Asia Pacific

Africa

Middle East

Europe

Central and South America

North America

15

Demand Oil Product Demand for Selected Regions (MMbbl/day)

Source: Haver Analytics

0

5

10

15

20

25

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

China EU-15 U.S. LatAm

16

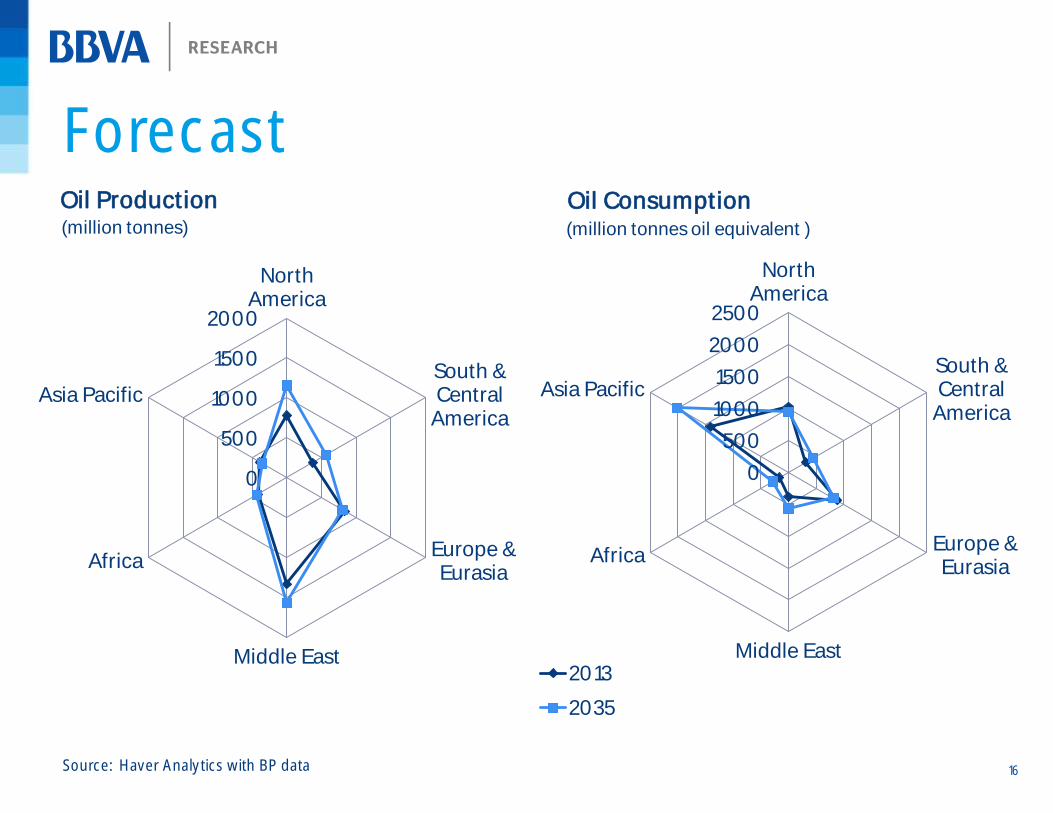

Forecast

Source: Haver Analytics with BP data

0

500

1000

1500

2000

North America

South & Central

America

Europe & Eurasia

Middle East

Africa

Asia Pacific

2013

2035

0

500

1000

1500

2000

2500

North America

South & Central

America

Europe & Eurasia

Middle East

Africa

Asia Pacific

Oil Production Oil Consumption (million tonnes) (million tonnes oil equivalent )

17

U.S. Supply

& Demand

18

Production U.S. Crude Oil Field Production (MMbbl/day)

Source: Haver Analytics

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Texas U.S.

19

Production U.S. Active Rig Count

Source: Haver Analytics

0

200

400

600

800

1000

1200

1400

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Horizontal Vertical

20

Net Imports

100

150

200

250

300

350

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Net Imports

Production

U.S. Production and Net Imports of Crude Oil (MMbbl/month)

Source: Haver Analytics

21

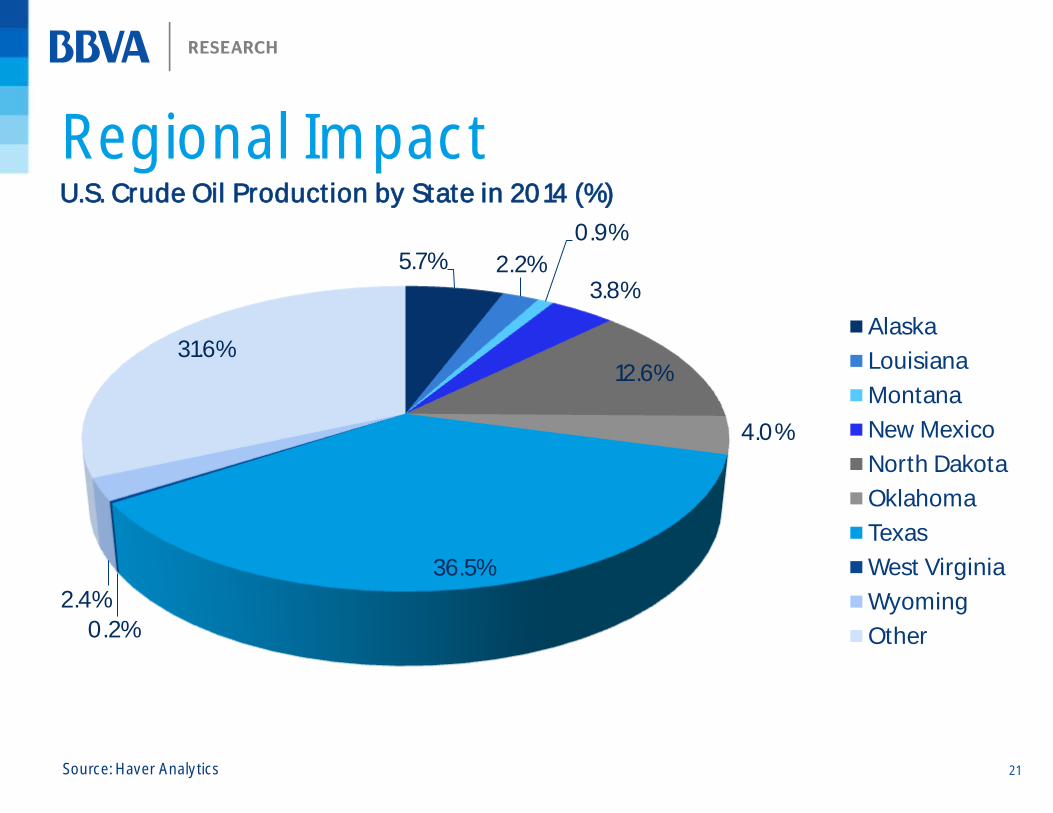

5.7% 2.2%

0.9%

3.8%

12.6%

4.0%

36.5%

0.2% 2.4%

31.6% Alaska

Louisiana

Montana

New Mexico

North Dakota

Oklahoma

Texas

West Virginia

Wyoming

Other

Regional Impact U.S. Crude Oil Production by State in 2014 (%)

Source: Haver Analytics

22

Impact on

U.S.

Economy

23

Consumer Spending U.S. Average Retail Gasoline Price vs. Real Retail Sales and Food Services (yoy % change)

Source: Haver Analytics

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

-60%

-40%

-20%

0%

20%

40%

60%

80%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Gas Price (lhs)

Sales (rhs)

24

Consumer Sentiment Consumer Sentiment (NSA, q1-66=100) vs. Average Retail Gasoline Prices ($/gallon)

Source: Haver Analytics

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

50

55

60

65

70

75

80

85

90

95

100

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Consumer Sentiment (lhs)

Gas Price (rhs)

25

Vehicle Miles Traveled

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Vehicle Miles of Travel (lhs)

Gas Prices (rhs)

Gasoline Prices and Vehicle Miles Traveled (yoy % change, 6-month MA)

Source: Haver Analytics

26

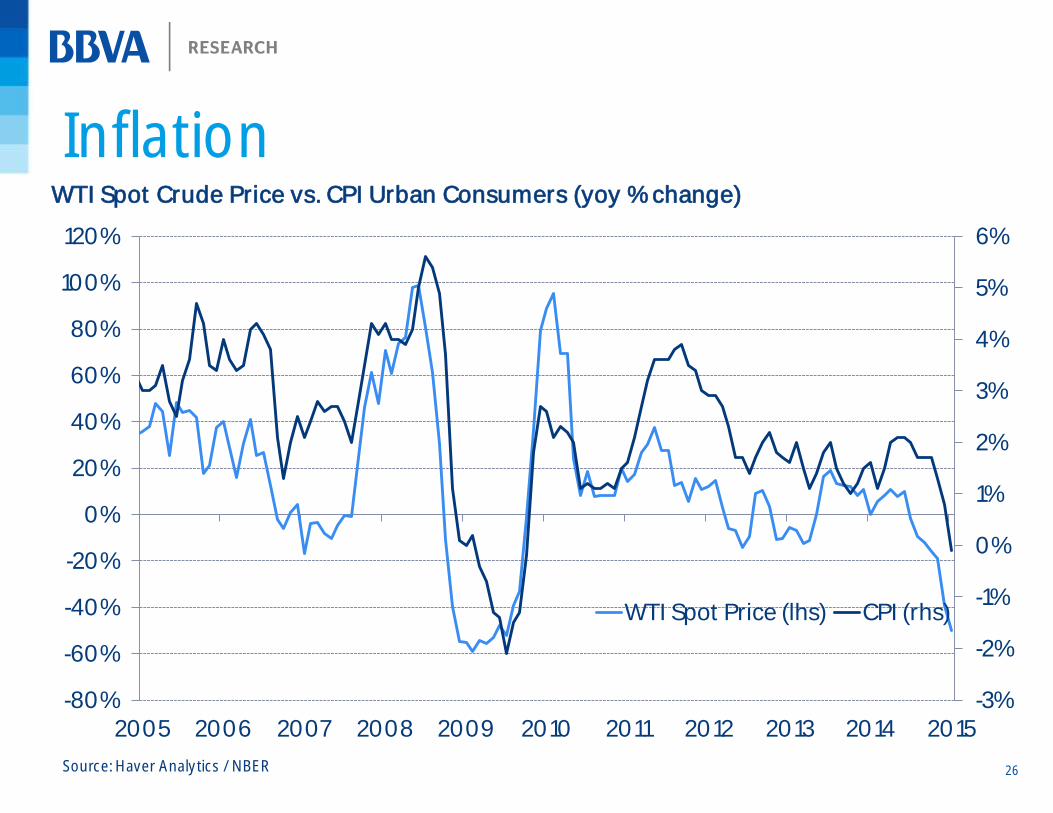

Inflation WTI Spot Crude Price vs. CPI Urban Consumers (yoy % change)

Source: Haver Analytics / NBER

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

WTI Spot Price (lhs) CPI (rhs)

27

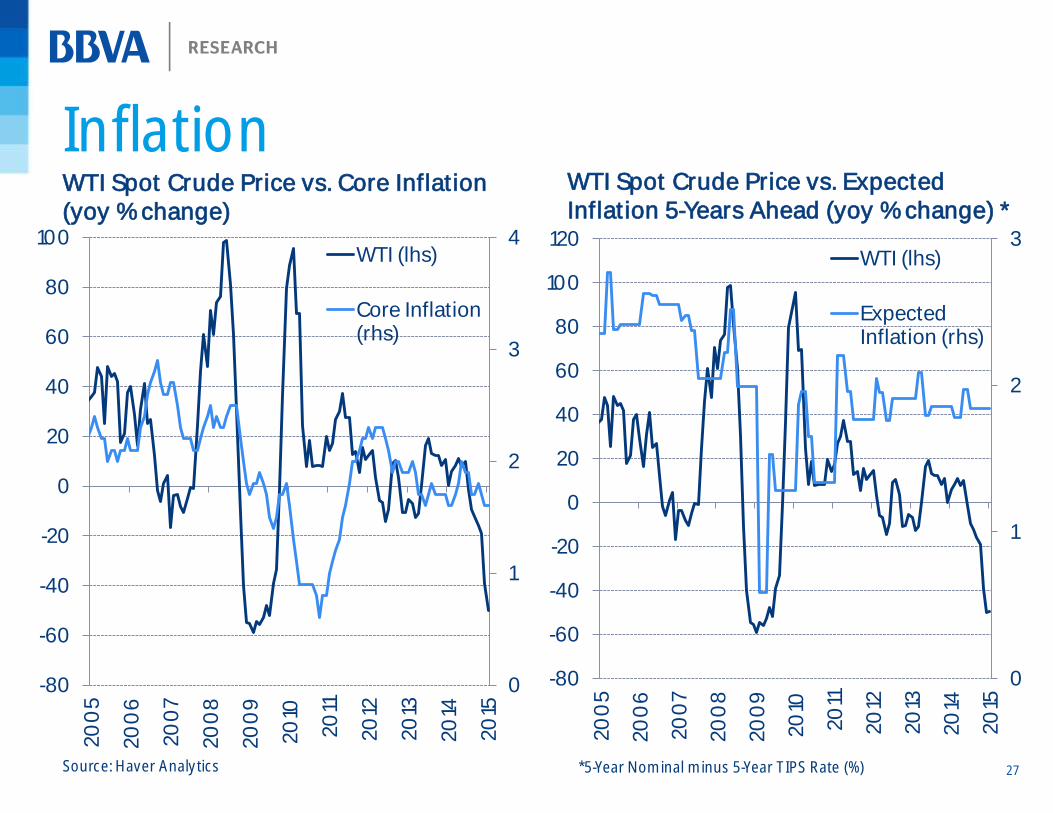

Inflation

Source: Haver Analytics

0

1

2

3

4

-80

-60

-40

-20

0

20

40

60

80

100

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

WTI (lhs)

Core Inflation (rhs)

0

1

2

3

-80

-60

-40

-20

0

20

40

60

80

100

120

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

WTI (lhs)

Expected Inflation (rhs)

WTI Spot Crude Price vs. Core Inflation (yoy % change)

WTI Spot Crude Price vs. Expected Inflation 5-Years Ahead (yoy % change) *

*5-Year Nominal minus 5-Year TIPS Rate (%)

28

Regional Impact Severance Tax as a Share of State Revenue for Selected States in 2013

Source: Haver Analytics/ Pew Charitable Trusts

0%

5%

10%

15%

20%

25%

30%

35%

Severance Tax: Tax imposed by state governments on the

removal of nonrenewable resources such as crude oil and

natural gas at their market value.

.

Share of TX State & Local Revenue from Oil and Gas Industry*

Sources: Haver Analytics, Texas Comptroller of Public Accounts, Texas Oil & Gas Association, BBVA Research

0%

2%

4%

6%

8%

10%

12%

14%

1982 1987 1992 1997 2002 2007 2012

*Includes property tax, sales and gross receipts, franchise tax,

severance tax, and land income

29

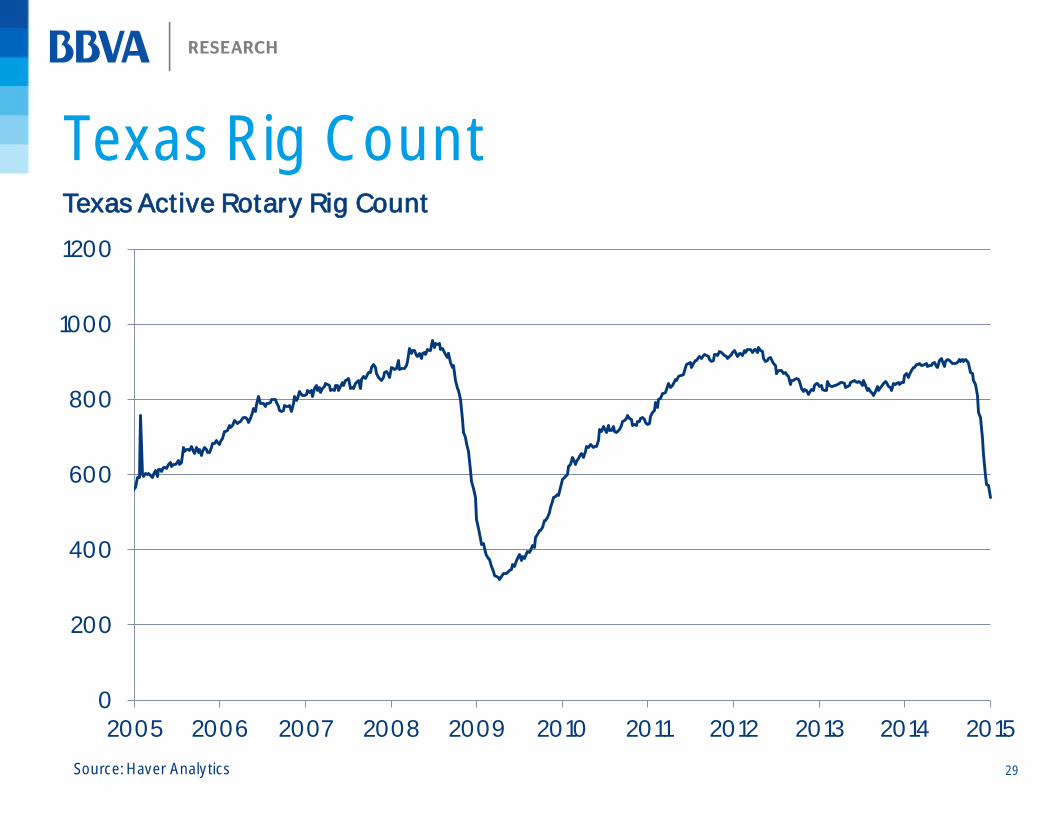

Texas Rig Count Texas Active Rotary Rig Count

Source: Haver Analytics

0

200

400

600

800

1000

1200

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

30

Texas Employment Location Quotients %

Location Quotients %

0% 20% 40% 60% 80%

100% 120% 140% 160% 180%

Construction

Manufacturing

Trade, Transp & Utilities

Information

Financial Activities

Professional & Business Svc

Educational & Health Services

Leisure & Hospitality

Other Services

Government

2014 2004 1994 0

2

4

6

8

10

12

14

16

Oil & Gas Extraction Support Activities for Mining

2014

2004

1994

Source: Haver Analytics

31

Energy

Industry

32

Debt High Yield Bonds (option adjusted spreads relative to U.S. treasuries)

0

200

400

600

800

1000

1200

Energy Total

Source: Bloomberg

33

Stock Markets S&P Daily Stock Market Capitalization (Bill.$)

Source: Haver Analytics

200

250

300

350

400

450

500

550

14000

15000

16000

17000

18000

19000

20000

S&P 500 (lhs)

E&P Index (rhs)

34

Stock Markets Market Weightings, S&P 500, 2015

Source: S&P Dow Jones Indices, Seeking Alpha

IT Financials

Healthcare Consumer Discretionary

Industrials Consumer Staples

Energy Utilities

Materials Telecom

0%

2%

4%

6%

8%

10%

12%

14%

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

%

Historical S&P Weighting, Energy Sector

35

M&A Activity U.S. M&A Number of Deals and Volume

Source: Bloomberg

0

5E+09

1E+10

1.5E+10

2E+10

2.5E+10

3E+10

3.5E+10

4E+10

4.5E+10

5E+10

0

20

40

60

80

100

120

2010 2011 2012 2013 2014

Deal Count (lhs)

Volume (rhs)

U.S. Oil & Gas Industry

Chartbook

BBVA Research USA

Houston, TX March 2015

DISCLAIMER This document was prepared by Banco Bilbao Vizcaya (BBVA) BBVA Research U.S. on behalf of itself and its affiliated companies (each BBVA Group Company) for distribution in the United States and the rest of the world and is provided for information purposes only. Within the US, BBVA operates primarily through its subsidiary Compass Bank. The information, opinions, estimates and forecasts contained herein refer to the specific date and are subject to changes without notice due to market fluctuations. The information, opinions, estimates and forecasts contained in this document have been gathered or obtained from public sources, believed to be correct by the Company concerning their accuracy, completeness, and/or correctness. This document is not an offer to sell or a solicitation to acquire or dispose of an interest in securities.