Embed Size (px)

Citation preview

U.S. MOBILE PAYMENTS LANDSCAPE

AND OPPORTUNITIES FOR THE FUTURE

AFP PAYMENTS ADVISORY GROUP November 4, 2009

Marianne CroweFederal Reserve Bank of Boston

AGENDA2

Mobile Definitions U.S. Mobile Landscape Mobile Banking & Payments Applications Risks & Regulations Future of Mobile Payments

MOBILE DEFINITIONS

Source: NACHA, Mobile Channel Terminology .August 2008Source: Mobile Marketing Association, Mobile Marketing Industry Glossary 2008

3

Mobile Banking Use of mobile device to connect to a financial institution to conduct customer self-

service (CCS) View account balances, transfer funds between accounts, pay bills or receive

account alertsMobile Payments Use of a mobile device to make a purchase or other payment-related transaction Payments can be initiated in the physical or virtual worlds, and can be conducted

via SMS, MMS, mobile Internet, downloadable application, and contactless NFC chips

Purchases and payments may include digital content, goods and services at POS or Internet, transportation fares, P2P

Mobile Commerce Extends e-commerce to a variety of hand held mobile devices to buy and sell

goods and servicesMobile Marketing Marketing, messages, coupons, and other content delivered via wireless (mobile

media)

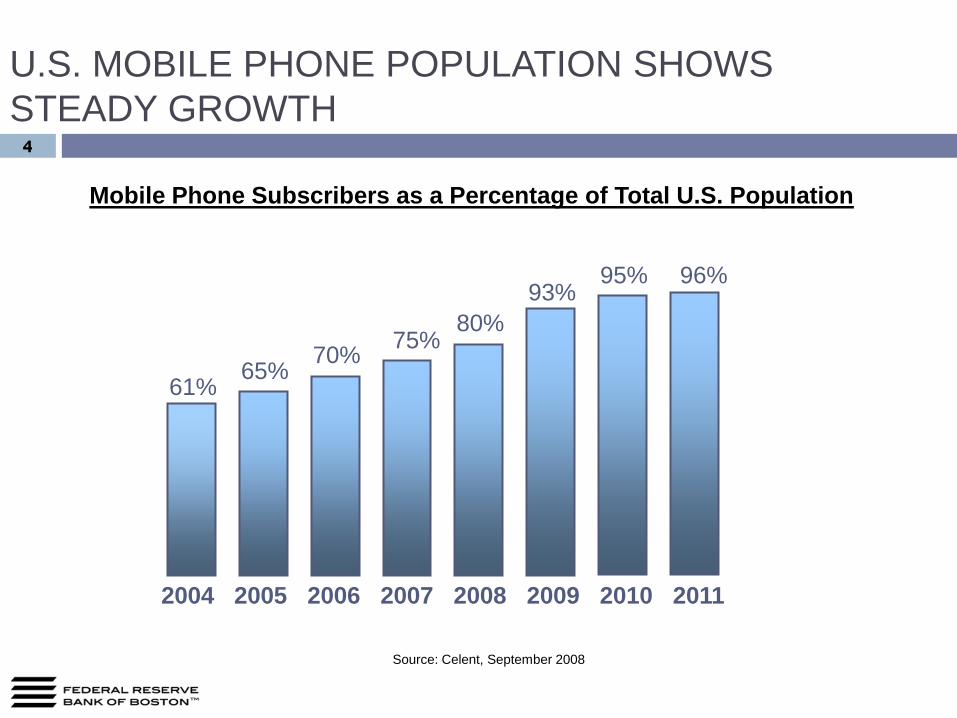

4

U.S. MOBILE PHONE POPULATION SHOWS STEADY GROWTH

Mobile Phone Subscribers as a Percentage of Total U.S. Population

2004 2005 2006 2007 2008 2009 2010 2011

Source: Celent, September 2008

65%61%

70% 75%80%

93% 95% 96%

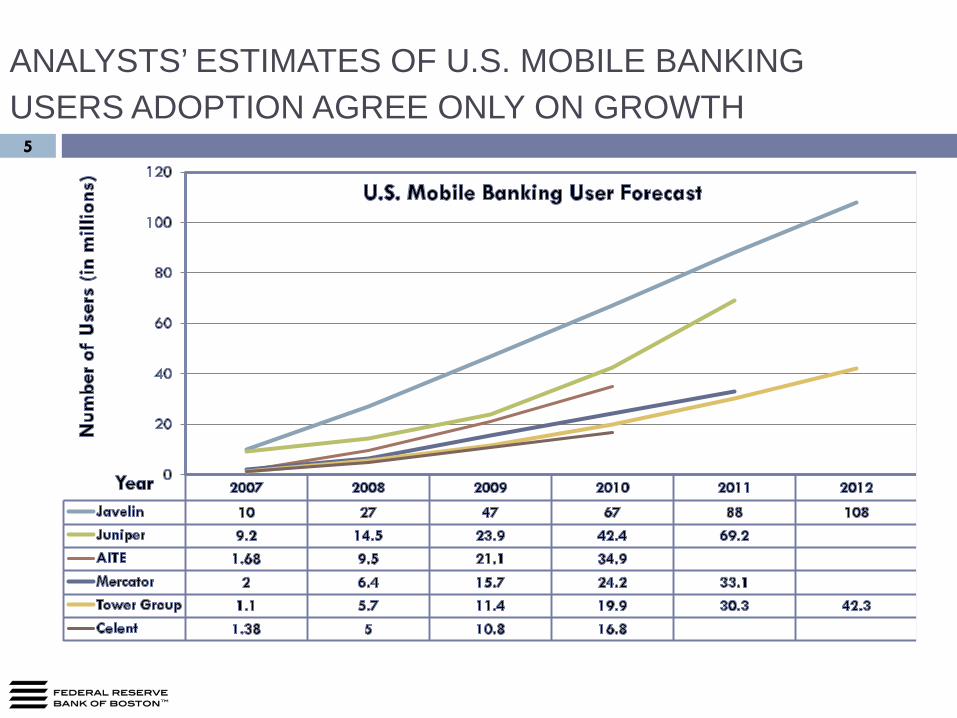

ANALYSTS’ ESTIMATES OF U.S. MOBILE BANKING USERS ADOPTION AGREE ONLY ON GROWTH

5

6

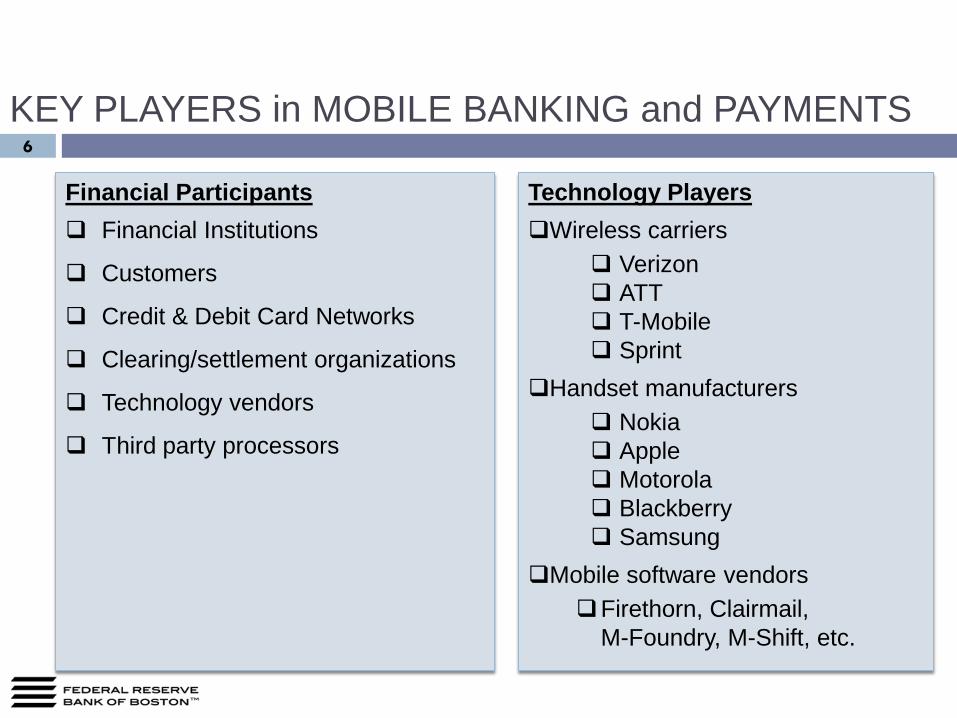

KEY PLAYERS in MOBILE BANKING and PAYMENTS

Financial Participants Financial Institutions

Customers

Credit & Debit Card Networks

Clearing/settlement organizations

Technology vendors

Third party processors

Technology PlayersWireless carriers

Verizon ATT T-Mobile Sprint

Handset manufacturers Nokia Apple Motorola Blackberry Samsung

Mobile software vendorsFirethorn, Clairmail,

M-Foundry, M-Shift, etc.

7

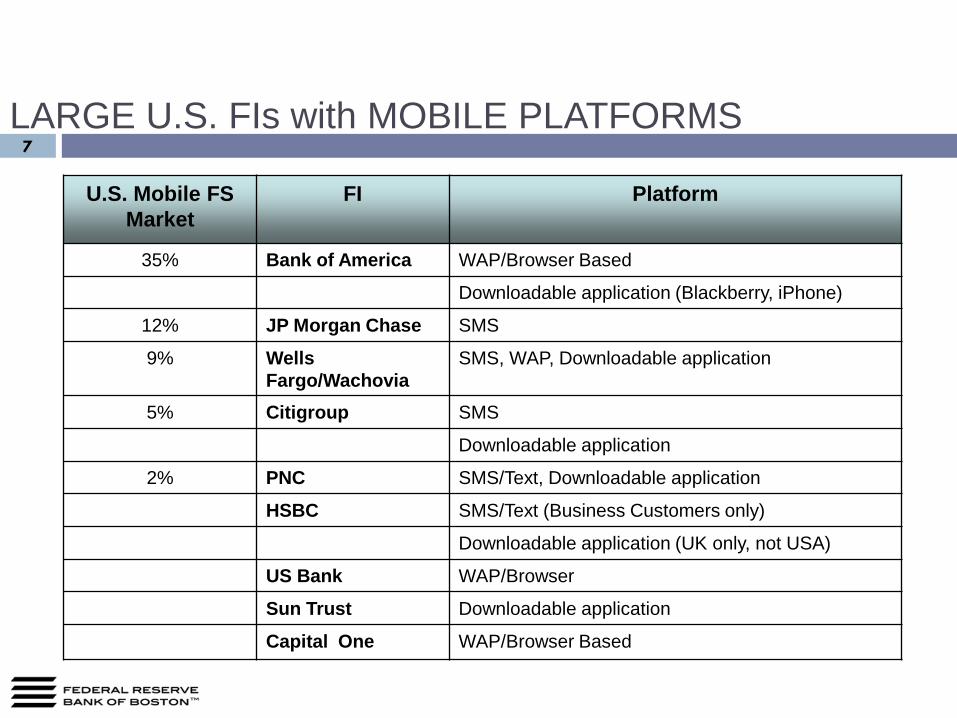

U.S. Mobile FS Market

FI Platform

35% Bank of America WAP/Browser Based

Downloadable application (Blackberry, iPhone)

12% JP Morgan Chase SMS

9% Wells Fargo/Wachovia

SMS, WAP, Downloadable application

5% Citigroup SMS

Downloadable application

2% PNC SMS/Text, Downloadable application

HSBC SMS/Text (Business Customers only)

Downloadable application (UK only, not USA)

US Bank WAP/Browser

Sun Trust Downloadable application

Capital One WAP/Browser Based

LARGE U.S. FIs with MOBILE PLATFORMS

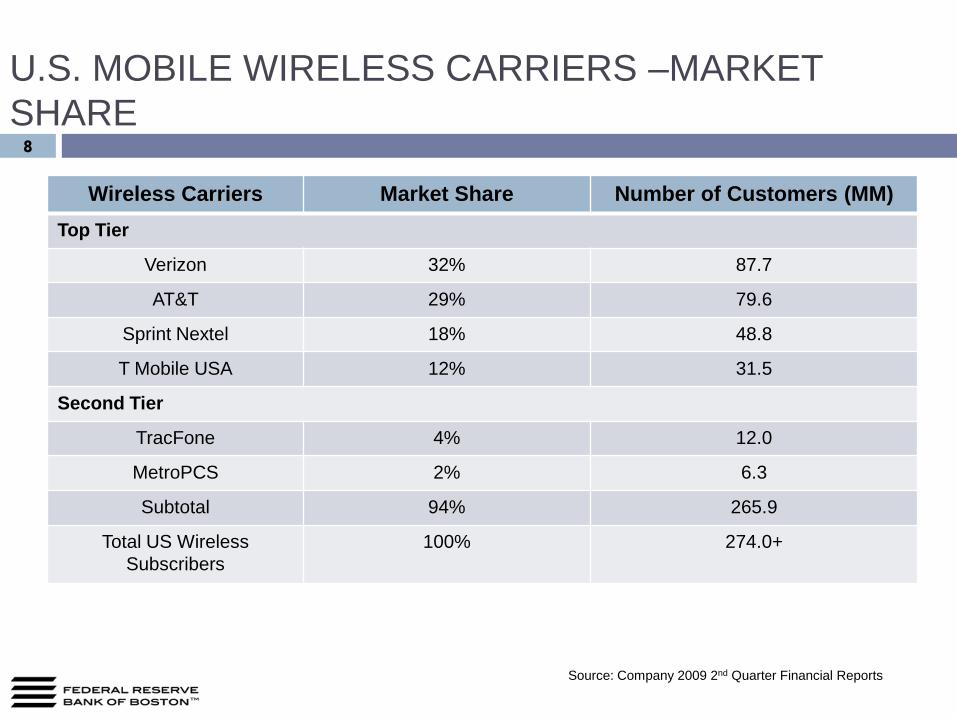

U.S. MOBILE WIRELESS CARRIERS –MARKET SHARE

Wireless Carriers Market Share Number of Customers (MM)Top Tier

Verizon 32% 87.7

AT&T 29% 79.6

Sprint Nextel 18% 48.8

T Mobile USA 12% 31.5

Second Tier

TracFone 4% 12.0

MetroPCS 2% 6.3

Subtotal 94% 265.9

Total US Wireless Subscribers

100% 274.0+

Source: Company 2009 2nd Quarter Financial Reports

8

8

MOBILE TECHNOLOGY PLATFORMS9

SMS (Short Message Service) Text message format allows mobile phone users to send/receive simple text messages to each

other MMS (Multimedia Messaging Service) is an extension of SMS that enables messages to include

multimedia content such as photos and videosWireless Application Protocol (WAP)/Browser WAP: Secure specification that allows users to access information instantly, particularly Internet

content, via mobile phones

Browser software enables user to display and interact with text, images, videos, music, etc. on Internet pages

Downloadable Application Customized software loaded onto mobile phone to enable customer to navigate through

functions more quickly

Considered more secure method for complex transactions (payments or fund transfers).

90% SMS capable

60% WAP accessible

30% Downloadable

Application

Handsets lack platform commonality in the U.S.

OTHER MOBILE TECHNOLOGY10

Over-the-air (OTA) Transaction or transfer that takes place wirelessly using the cellular network. Usually for

downloading content or software applications to mobile handsets.

NFC (Near Field Communication) A short-range wireless proximity technology that uses radio frequency to enable

communication between two devices.

NFC chips are embedded in mobile phones (or credit/debit cards) to enable this contactless ‘tap and go’ payment technology.

Value of NFC Enables proximity payments to buy physical goods at retail POS locations or for Transit

services NFC can speed purchase process; make more convenient for consumer M-Wallet: Ability to download (via OTA) virtual payment card method(s)

NFC sticker being implemented as a short-term solution to bridge gap to NFC, build user acceptance

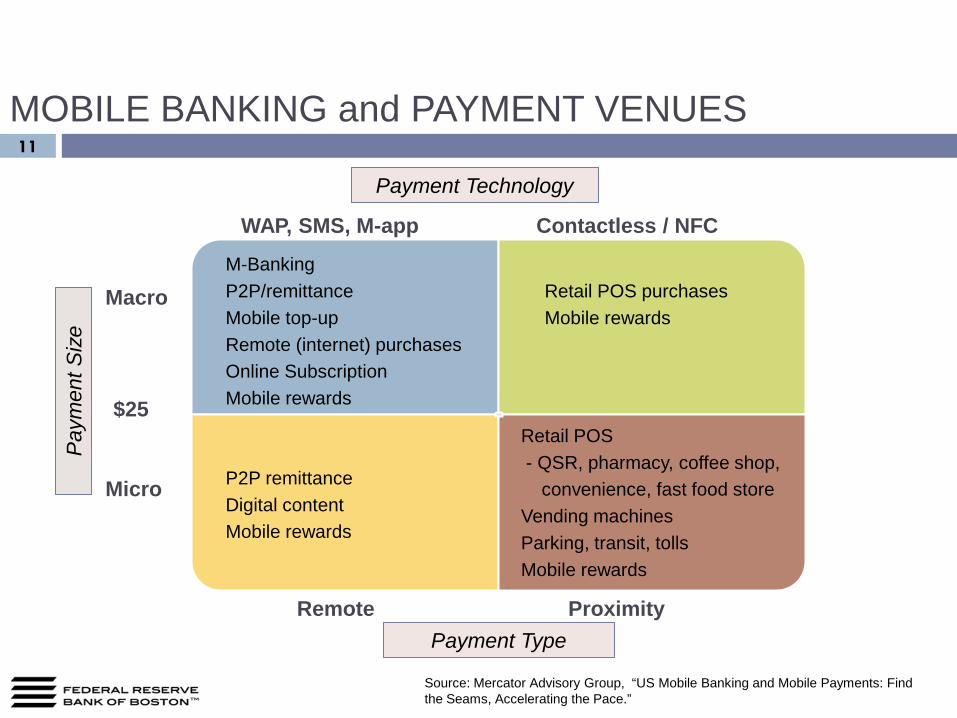

MOBILE BANKING and PAYMENT VENUES11

M-BankingP2P/remittanceMobile top-upRemote (internet) purchases Online SubscriptionMobile rewards

Retail POS purchasesMobile rewards

P2P remittanceDigital contentMobile rewards

Retail POS- QSR, pharmacy, coffee shop,

convenience, fast food storeVending machinesParking, transit, tollsMobile rewards

Macro

Micro

Contactless / NFCWAP, SMS, M-app

ProximityRemote

$25

Source: Mercator Advisory Group, “US Mobile Banking and Mobile Payments: Find the Seams, Accelerating the Pace.”

Payment Type

Payment Technology

Pay

men

t Siz

e

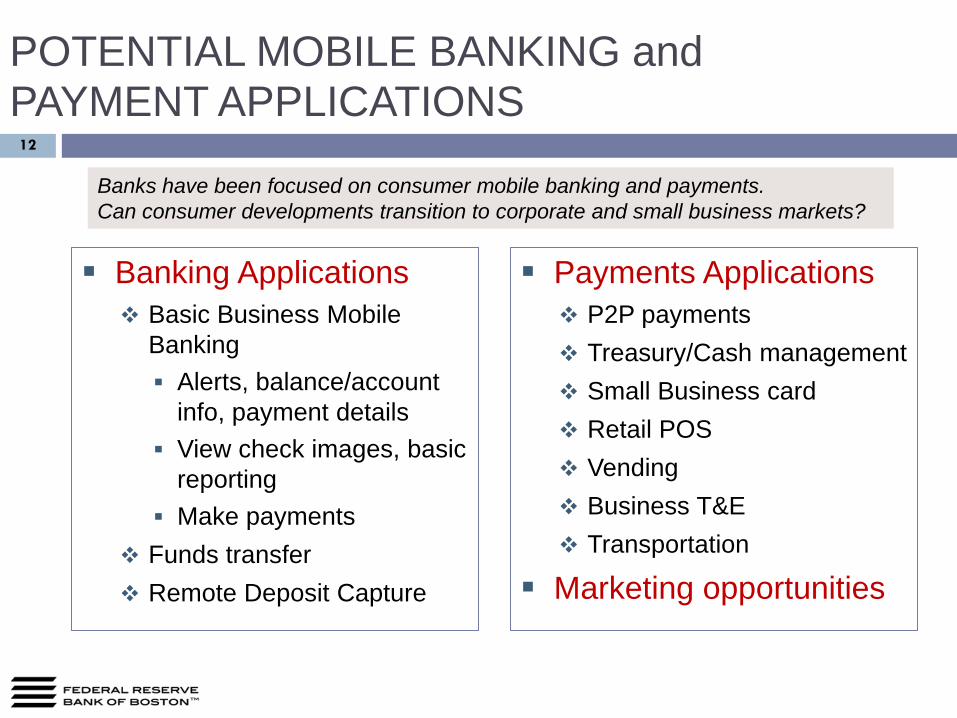

POTENTIAL MOBILE BANKING and PAYMENT APPLICATIONS

Banking Applications Basic Business Mobile

Banking Alerts, balance/account

info, payment details View check images, basic

reporting Make payments

Funds transfer Remote Deposit Capture

Payments Applications P2P payments Treasury/Cash management Small Business card Retail POS Vending Business T&E Transportation

Marketing opportunities

12

Banks have been focused on consumer mobile banking and payments.Can consumer developments transition to corporate and small business markets?

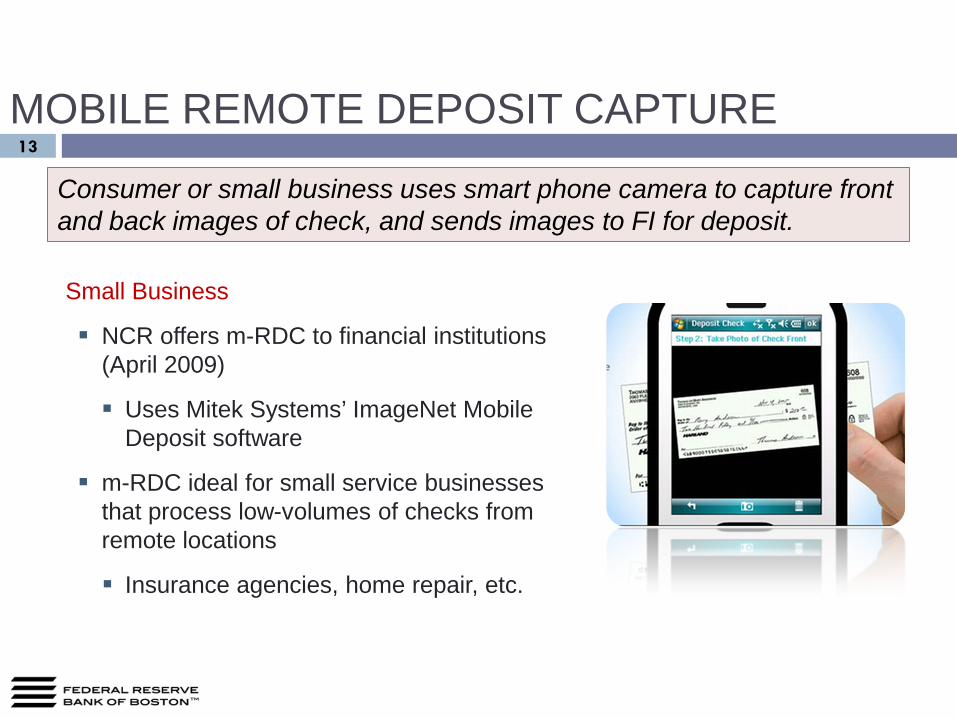

MOBILE REMOTE DEPOSIT CAPTURE13

Small Business

NCR offers m-RDC to financial institutions (April 2009)

Uses Mitek Systems’ ImageNet Mobile Deposit software

m-RDC ideal for small service businesses that process low-volumes of checks from remote locations

Insurance agencies, home repair, etc.

Consumer or small business uses smart phone camera to capture front and back images of check, and sends images to FI for deposit.

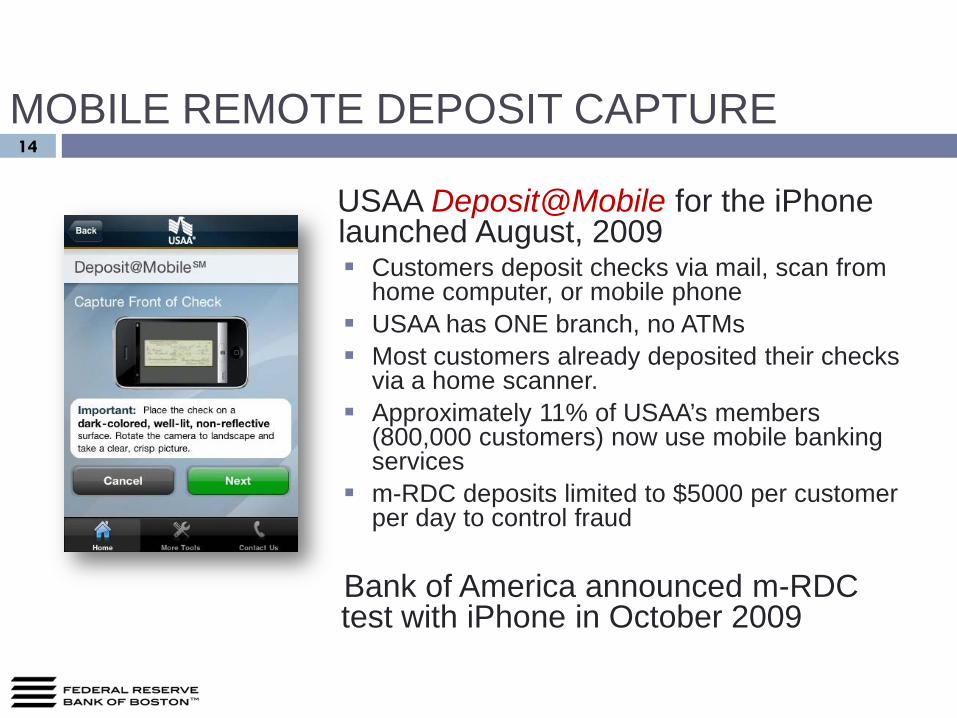

MOBILE REMOTE DEPOSIT CAPTURE14

USAA Deposit@Mobile for the iPhonelaunched August, 2009 Customers deposit checks via mail, scan from

home computer, or mobile phone USAA has ONE branch, no ATMs Most customers already deposited their checks

via a home scanner. Approximately 11% of USAA’s members

(800,000 customers) now use mobile banking services

m-RDC deposits limited to $5000 per customer per day to control fraud

Bank of America announced m-RDC test with iPhone in October 2009

Corporate Mobile Banking & Treasury Cash Management Services

Wells Fargo CEO Mobile Banking for Executives• Monitor accounts & perform treasury management functions through

mobile browser on smart phone Initiate, approve, reject wires View account balances Monitor cash flows in multiple accounts Manage fraud protection services Administer users & reset passwords

Wall Street Systems Treasury on the Move• Payment initiation, authorization and release• Verification of investments• Short term borrowings• FX transactions• Intercompany loans

15

Mobile Financial Trading

E-Trade Mobile Pro Trade stocks and options Check balances and account details Check watch list and portfolios Real time streaming stock/option quotes Move money between e-Trade accounts and to/from

outside FI accounts Access via WAP/browser

16

MOBILE P2P PAYMENTS17

Exchange funds between individuals via mobile interface number Involves intermediary (PayPal or FI) and online component Usually settles via ACH Sender must register for service and activate mobile phone Cash/check replacement for informal, low dollar payments

between established relationships Babysitter, housekeeper, landscaper Family/college students; school or sports club fees Future? Small professional services – medical, legal, etc.

U.S. non-banks currently offer mobile service (PayPal, Obopay) U.S. banks just beginning to enter online P2P market (BoA)

Very limited mobile P2P Wells Fargo offers mobile P2P only between Wells Fargo customers

MOBILE CARD APPLICATION FOR SMALL BUSINESS

Smartphone payment application Converts mobile phone

to POS terminal Less costly than

wireless-enabled POS terminals Allows card acceptance

for ‘remote’ services Trade shows, kiosks Plumbers, carpenters

Expands consumer payment options beyond cash & check

May increase revenue

Risk Mobile device may or

may not be PCI compliant, depending on software used

18

18

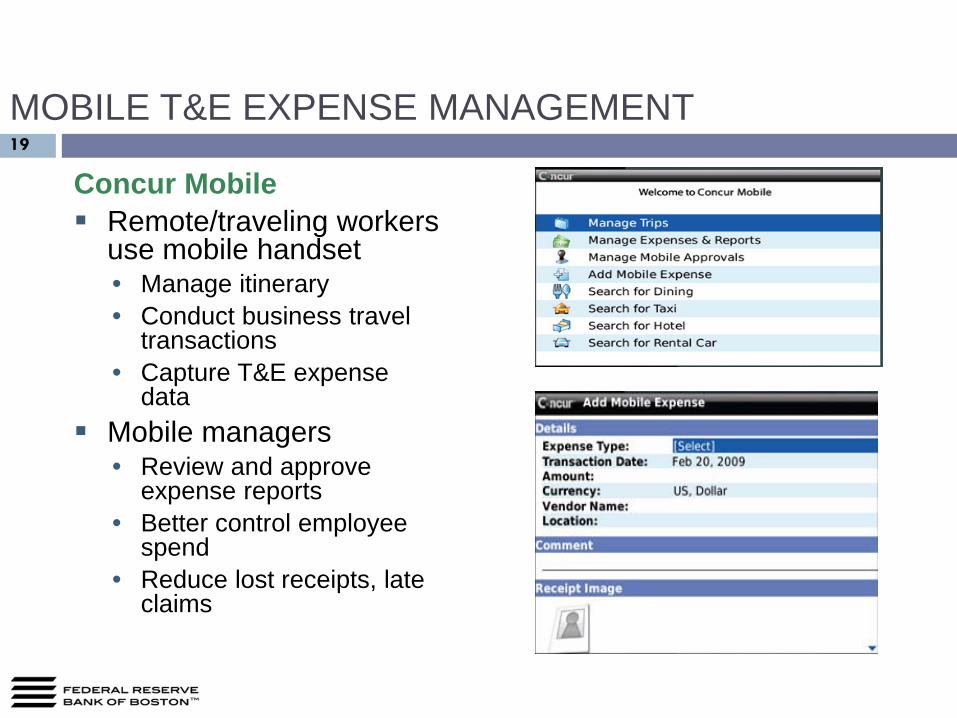

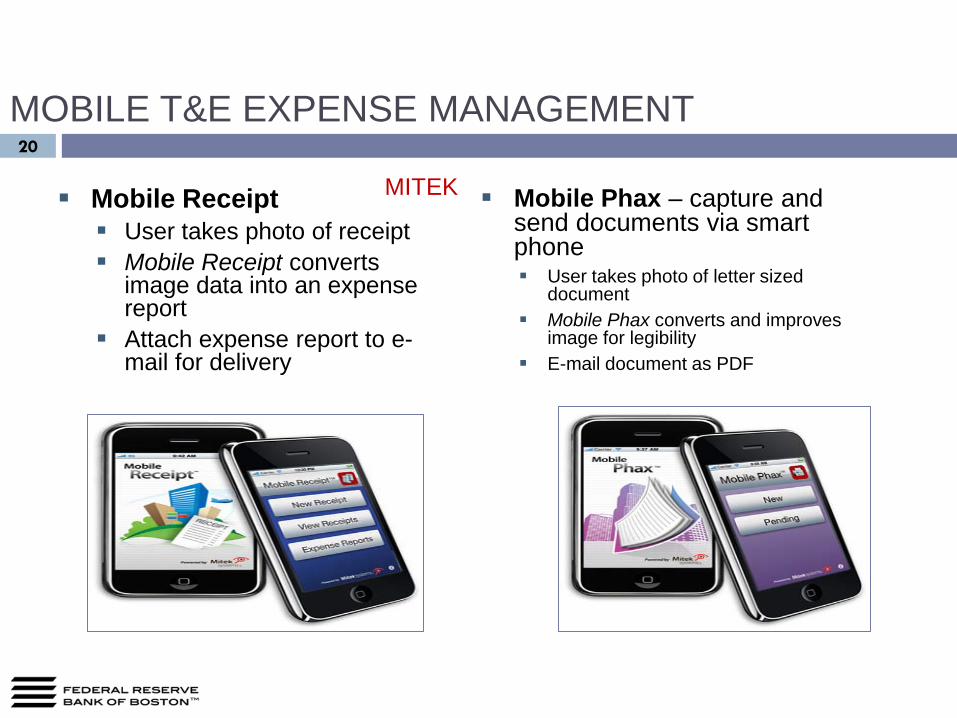

MOBILE T&E EXPENSE MANAGEMENT

Concur Mobile Remote/traveling workers

use mobile handset• Manage itinerary• Conduct business travel

transactions• Capture T&E expense

data Mobile managers

• Review and approve expense reports

• Better control employee spend

• Reduce lost receipts, late claims

19

MOBILE T&E EXPENSE MANAGEMENT20

Mobile Receipt User takes photo of receipt Mobile Receipt converts

image data into an expense report

Attach expense report to e-mail for delivery

Mobile Phax – capture and send documents via smart phone User takes photo of letter sized

document Mobile Phax converts and improves

image for legibility E-mail document as PDF

MITEK

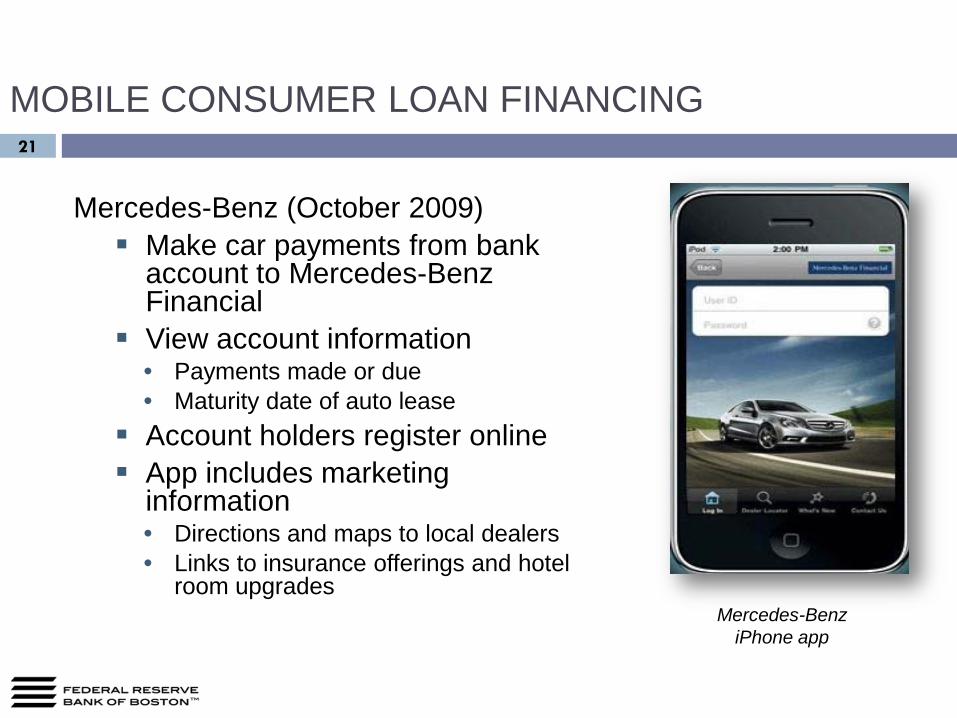

MOBILE CONSUMER LOAN FINANCING21

Mercedes-Benz (October 2009) Make car payments from bank

account to Mercedes-Benz Financial

View account information• Payments made or due• Maturity date of auto lease

Account holders register online App includes marketing

information• Directions and maps to local dealers• Links to insurance offerings and hotel

room upgradesMercedes-Benz

iPhone app

22

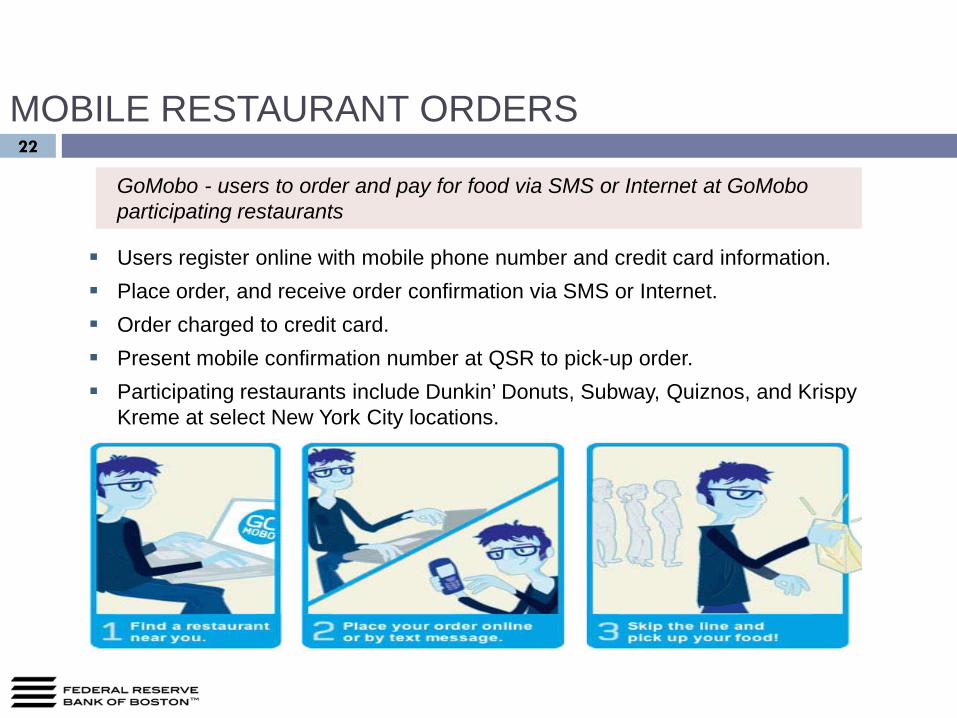

Users register online with mobile phone number and credit card information. Place order, and receive order confirmation via SMS or Internet. Order charged to credit card. Present mobile confirmation number at QSR to pick-up order. Participating restaurants include Dunkin’ Donuts, Subway, Quiznos, and Krispy

Kreme at select New York City locations.

MOBILE RESTAURANT ORDERS

GoMobo - users to order and pay for food via SMS or Internet at GoMoboparticipating restaurants

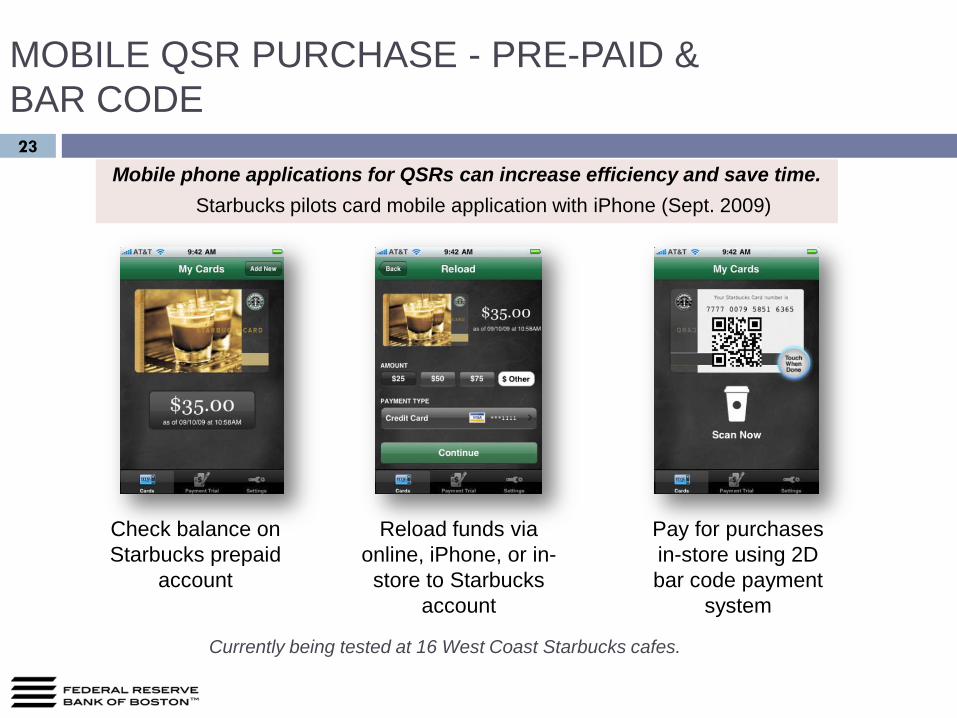

MOBILE QSR PURCHASE - PRE-PAID & BAR CODE23

Mobile phone applications for QSRs can increase efficiency and save time. Starbucks pilots card mobile application with iPhone (Sept. 2009)

Currently being tested at 16 West Coast Starbucks cafes.

Check balance on Starbucks prepaid

account

Reload funds via online, iPhone, or in-store to Starbucks

account

Pay for purchases in-store using 2D bar code payment

system

MOBILE RETAIL PAYMENTS – NFC STICKER24

FirstData’s GO-Tag is a contactless payment technology based on an open loop prepaid card infrastructure. Customer must register; load funds to prepaid account. GO-Tag can be a sticker, mini-card, or wristband. Sticker applied to mobile phone to acclimate

consumers to use of mobile phone as payment method.

Customer waves or taps GO-Tag at merchant’s POS contactless reader to complete purchase.

Can be used wherever VISA prepaid debit cards are accepted.

Initial card issuance fee is $6.95 Reloading fees range from $1 to $2+ depending on

retailer and/or payment type.

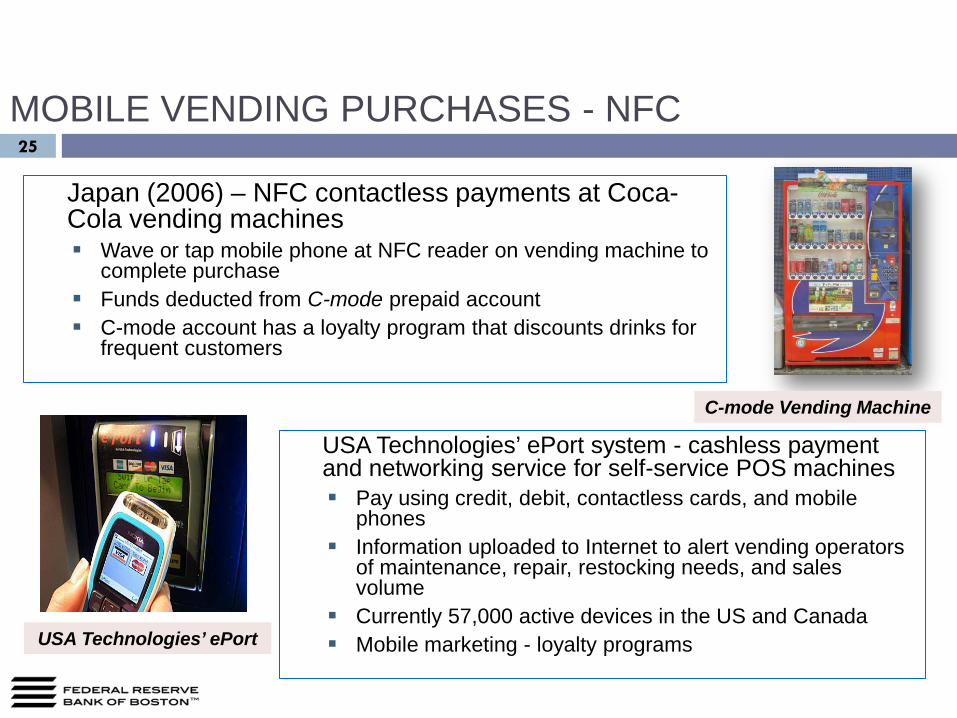

MOBILE VENDING PURCHASES - NFC25

USA Technologies’ ePort system - cashless payment and networking service for self-service POS machines Pay using credit, debit, contactless cards, and mobile

phones Information uploaded to Internet to alert vending operators

of maintenance, repair, restocking needs, and sales volume

Currently 57,000 active devices in the US and Canada Mobile marketing - loyalty programs

Japan (2006) – NFC contactless payments at Coca-Cola vending machines Wave or tap mobile phone at NFC reader on vending machine to

complete purchase Funds deducted from C-mode prepaid account C-mode account has a loyalty program that discounts drinks for

frequent customers

USA Technologies’ ePort

C-mode Vending Machine

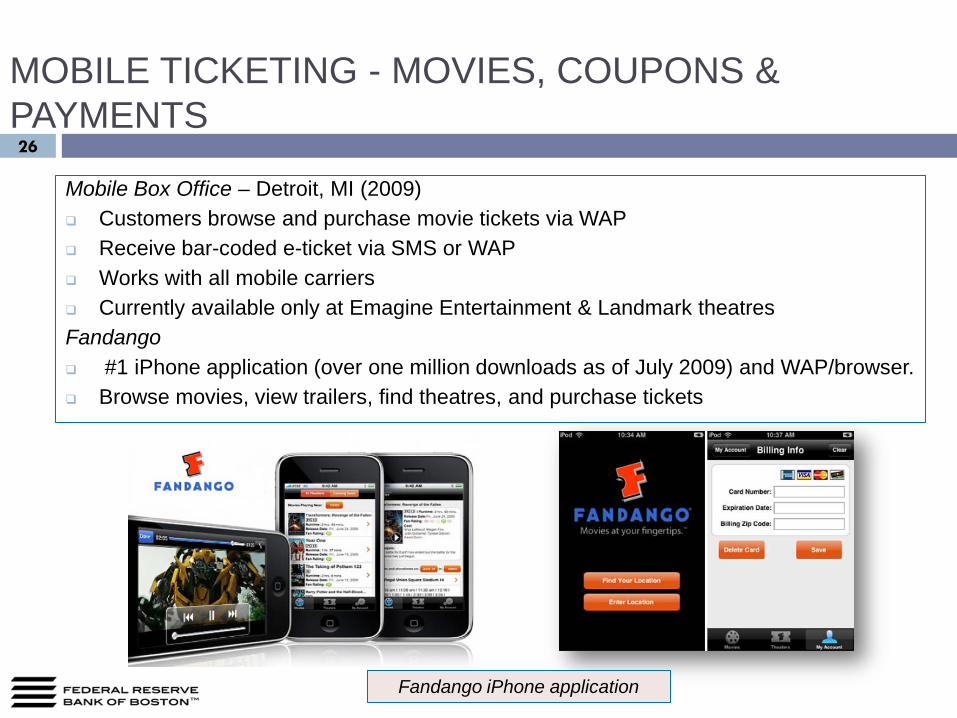

MOBILE TICKETING - MOVIES, COUPONS & PAYMENTS26

Mobile Box Office – Detroit, MI (2009) Customers browse and purchase movie tickets via WAP Receive bar-coded e-ticket via SMS or WAP Works with all mobile carriers Currently available only at Emagine Entertainment & Landmark theatresFandango #1 iPhone application (over one million downloads as of July 2009) and WAP/browser. Browse movies, view trailers, find theatres, and purchase tickets

Fandango iPhone application

MOBILE TICKETING - AIRLINES 27

Airline tickets purchased at airline mobile websites• Southwest, American, Delta, US

Airways Boarding pass barcode loaded on

mobile phone and scanned to board• IATA (International Air Transport

Association) mandates Bar Coded Boarding Pass standard by 2011 Currently 18 airlines offer mobile

(BCBP) ticketing• Lufthansa, Cathay Pacific, Air France,

Northwest, Continental, Delta, and American Airlines.

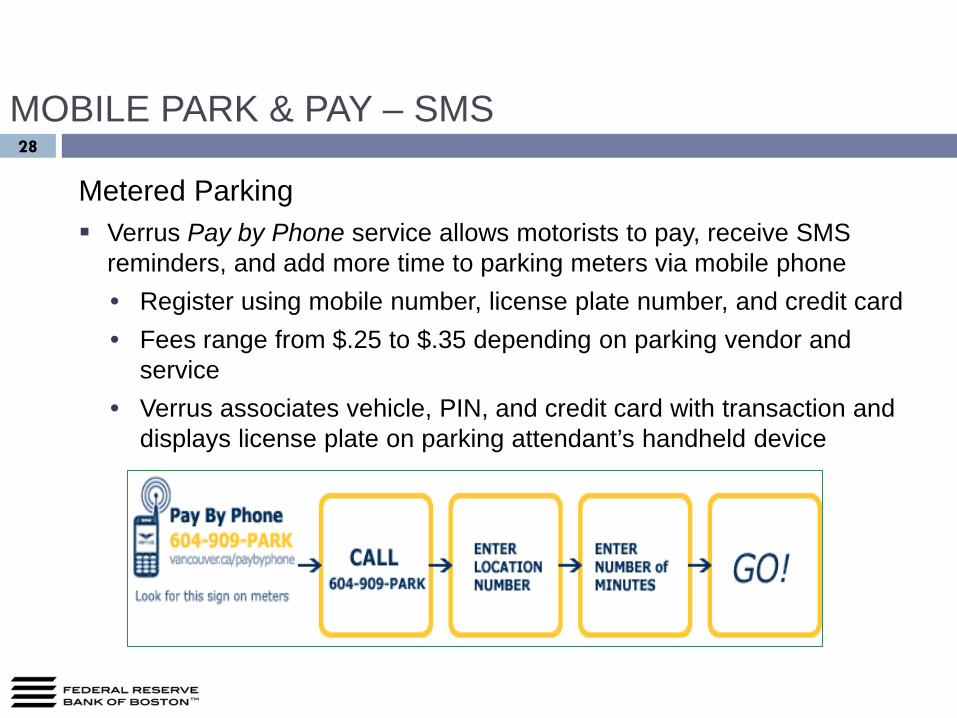

MOBILE PARK & PAY – SMS28

Metered Parking Verrus Pay by Phone service allows motorists to pay, receive SMS

reminders, and add more time to parking meters via mobile phone• Register using mobile number, license plate number, and credit card • Fees range from $.25 to $.35 depending on parking vendor and

service• Verrus associates vehicle, PIN, and credit card with transaction and

displays license plate on parking attendant’s handheld device

MOBILE TRANSIT PAYMENTS -NFC29

Debit or prepaid (open or closed loop) account to pay for public transit (subway, bus, light rail)

Funds are loaded onto mobile device with an embedded NFC chip Primary implementations in Southeast Asia and UK

Japan: Osaifu-Keitai “Mobile Wallet” service (2004) Cash card, credit card, train pass, plane ticket, and identity card services

South Korea: SK Telecom MONETA Card (2007) Visa cash e-purse, loyalty programs, and public transportation payment

China: China Unicom and Chongqing Yucheng Transportation (2009) SIM-pass enabled custom-made mobile phones to pay for bus, cable car rides, hotels,

parks, and restaurants

UK: Nokia and O2 Wallet trial (2007) Micro-payments at retail retail outlets, access to events, and Oyster card

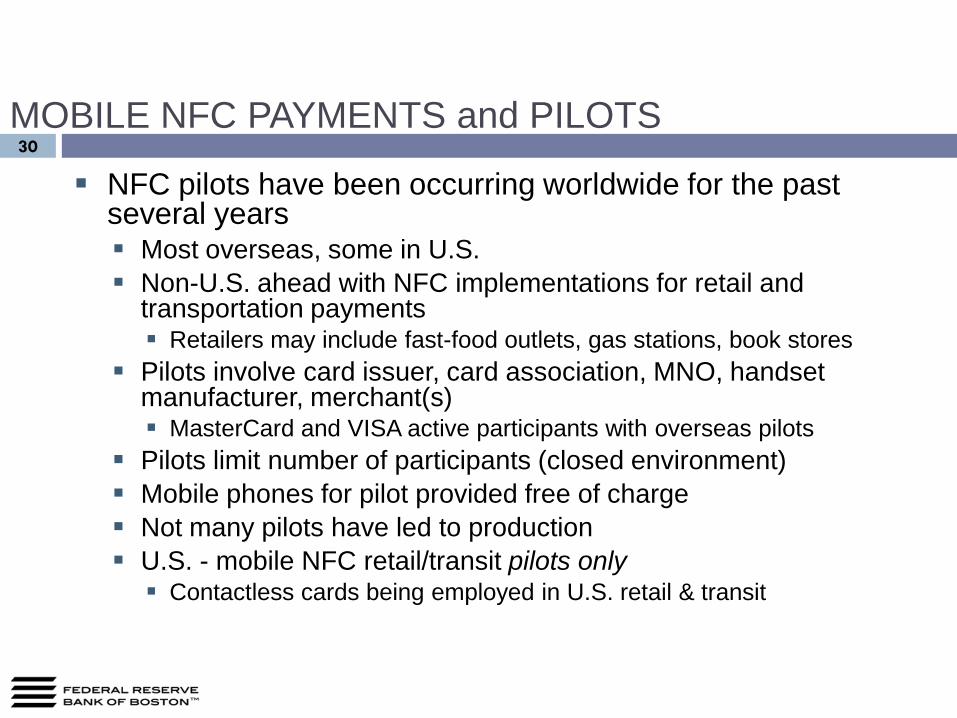

30

NFC pilots have been occurring worldwide for the past several years Most overseas, some in U.S. Non-U.S. ahead with NFC implementations for retail and

transportation payments Retailers may include fast-food outlets, gas stations, book stores

Pilots involve card issuer, card association, MNO, handset manufacturer, merchant(s) MasterCard and VISA active participants with overseas pilots

Pilots limit number of participants (closed environment) Mobile phones for pilot provided free of charge Not many pilots have led to production U.S. - mobile NFC retail/transit pilots only Contactless cards being employed in U.S. retail & transit

MOBILE NFC PAYMENTS and PILOTS

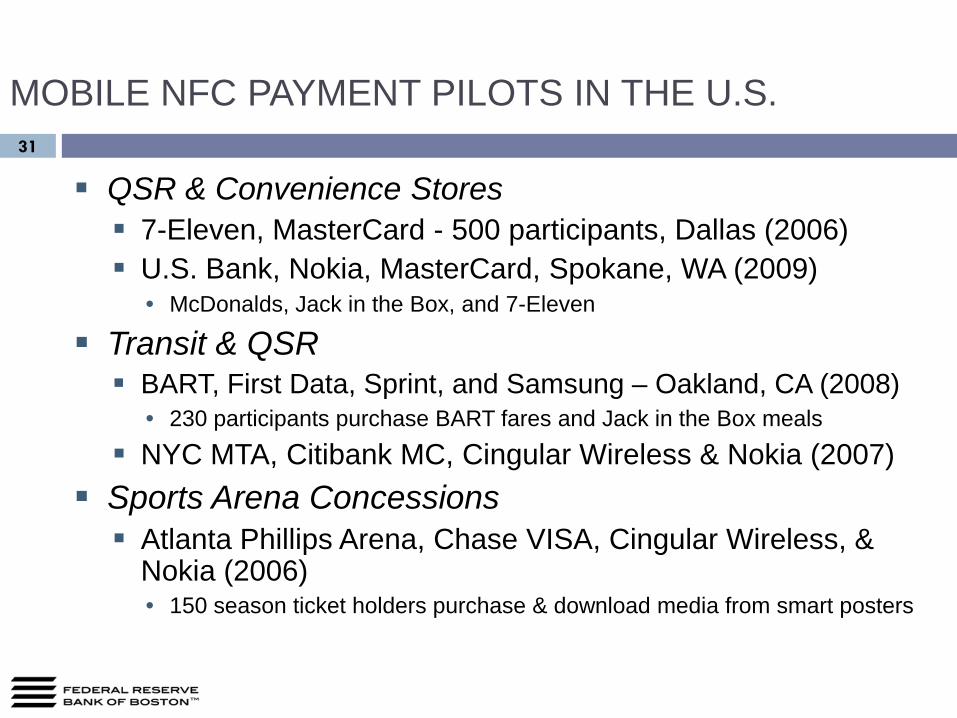

31

QSR & Convenience Stores 7-Eleven, MasterCard - 500 participants, Dallas (2006) U.S. Bank, Nokia, MasterCard, Spokane, WA (2009)

• McDonalds, Jack in the Box, and 7-Eleven

Transit & QSR BART, First Data, Sprint, and Samsung – Oakland, CA (2008)

• 230 participants purchase BART fares and Jack in the Box meals

NYC MTA, Citibank MC, Cingular Wireless & Nokia (2007) Sports Arena Concessions Atlanta Phillips Arena, Chase VISA, Cingular Wireless, &

Nokia (2006)• 150 season ticket holders purchase & download media from smart posters

MOBILE NFC PAYMENT PILOTS IN THE U.S.

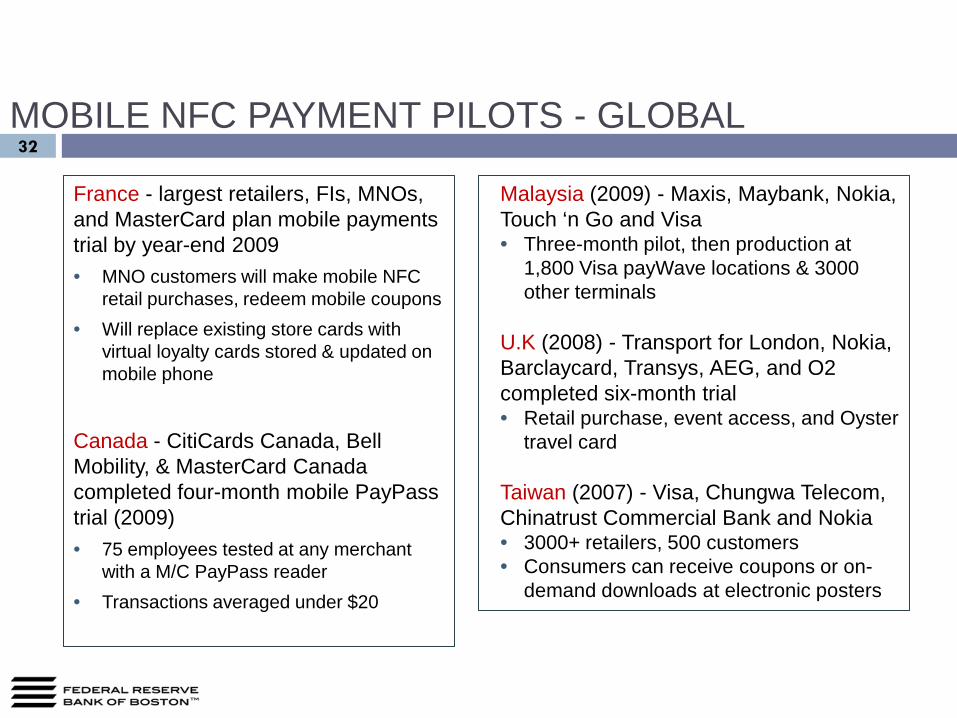

32

France - largest retailers, FIs, MNOs, and MasterCard plan mobile payments trial by year-end 2009• MNO customers will make mobile NFC

retail purchases, redeem mobile coupons• Will replace existing store cards with

virtual loyalty cards stored & updated on mobile phone

Canada - CitiCards Canada, Bell Mobility, & MasterCard Canada completed four-month mobile PayPasstrial (2009)• 75 employees tested at any merchant

with a M/C PayPass reader• Transactions averaged under $20

MOBILE NFC PAYMENT PILOTS - GLOBAL

Malaysia (2009) - Maxis, Maybank, Nokia, Touch ‘n Go and Visa • Three-month pilot, then production at

1,800 Visa payWave locations & 3000 other terminals

U.K (2008) - Transport for London, Nokia, Barclaycard, Transys, AEG, and O2 completed six-month trial• Retail purchase, event access, and Oyster

travel card

Taiwan (2007) - Visa, Chungwa Telecom, Chinatrust Commercial Bank and Nokia• 3000+ retailers, 500 customers • Consumers can receive coupons or on-

demand downloads at electronic posters

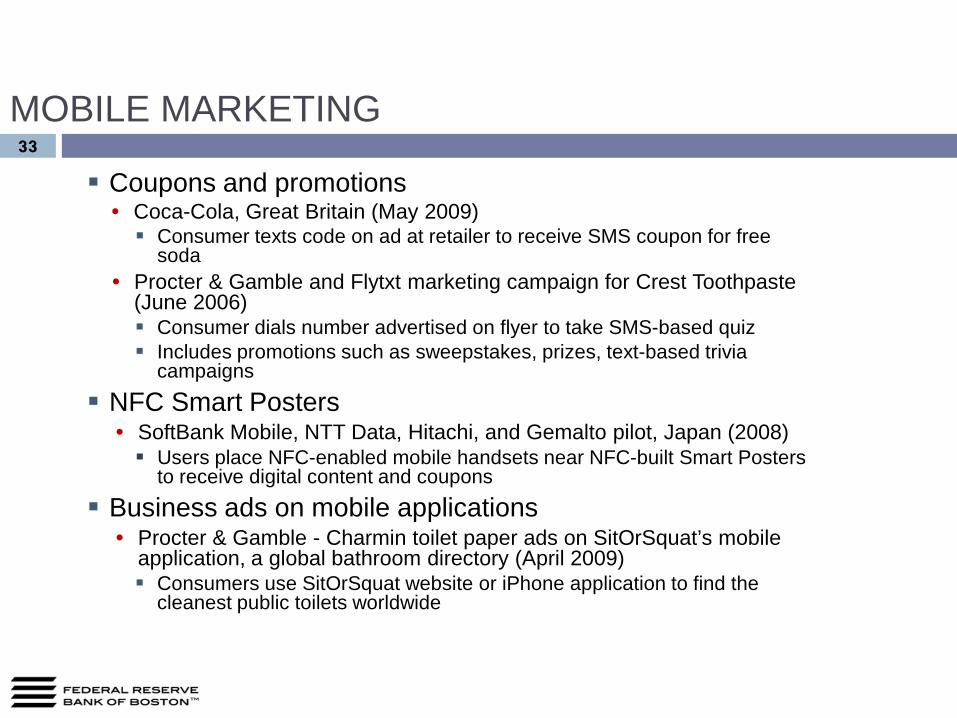

MOBILE MARKETING33

Coupons and promotions• Coca-Cola, Great Britain (May 2009) Consumer texts code on ad at retailer to receive SMS coupon for free

soda• Procter & Gamble and Flytxt marketing campaign for Crest Toothpaste

(June 2006) Consumer dials number advertised on flyer to take SMS-based quiz Includes promotions such as sweepstakes, prizes, text-based trivia

campaigns

NFC Smart Posters• SoftBank Mobile, NTT Data, Hitachi, and Gemalto pilot, Japan (2008) Users place NFC-enabled mobile handsets near NFC-built Smart Posters

to receive digital content and coupons

Business ads on mobile applications• Procter & Gamble - Charmin toilet paper ads on SitOrSquat’s mobile

application, a global bathroom directory (April 2009) Consumers use SitOrSquat website or iPhone application to find the

cleanest public toilets worldwide

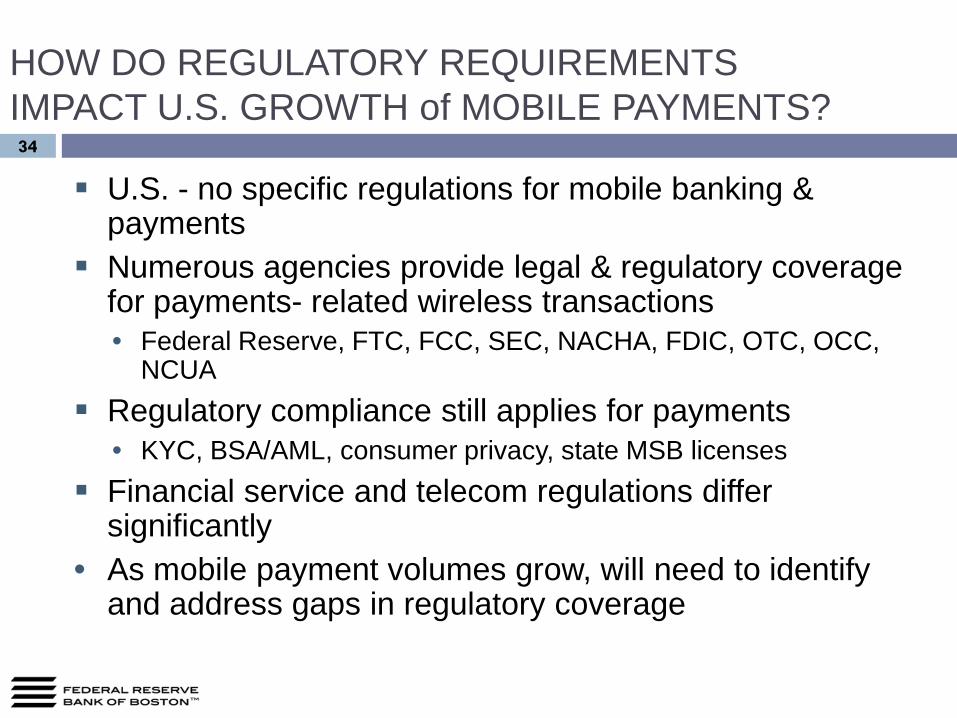

HOW DO REGULATORY REQUIREMENTS IMPACT U.S. GROWTH of MOBILE PAYMENTS?34

U.S. - no specific regulations for mobile banking & payments

Numerous agencies provide legal & regulatory coverage for payments- related wireless transactions• Federal Reserve, FTC, FCC, SEC, NACHA, FDIC, OTC, OCC,

NCUA Regulatory compliance still applies for payments

• KYC, BSA/AML, consumer privacy, state MSB licenses Financial service and telecom regulations differ

significantly• As mobile payment volumes grow, will need to identify

and address gaps in regulatory coverage

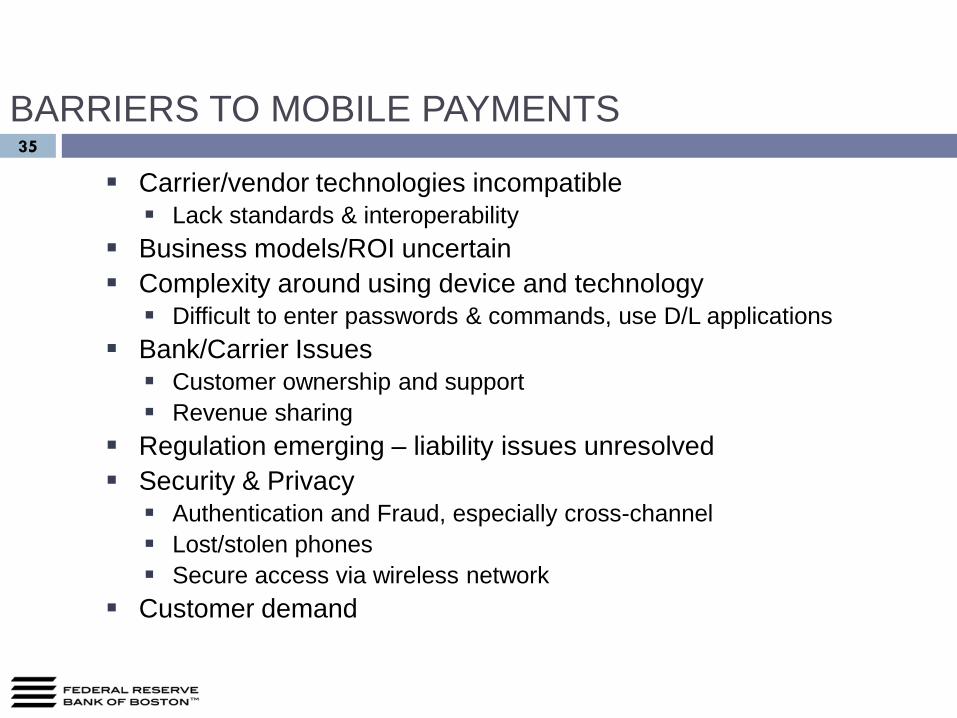

BARRIERS TO MOBILE PAYMENTS35

Carrier/vendor technologies incompatible Lack standards & interoperability

Business models/ROI uncertain Complexity around using device and technology Difficult to enter passwords & commands, use D/L applications

Bank/Carrier Issues Customer ownership and support Revenue sharing

Regulation emerging – liability issues unresolved Security & Privacy Authentication and Fraud, especially cross-channel Lost/stolen phones Secure access via wireless network

Customer demand

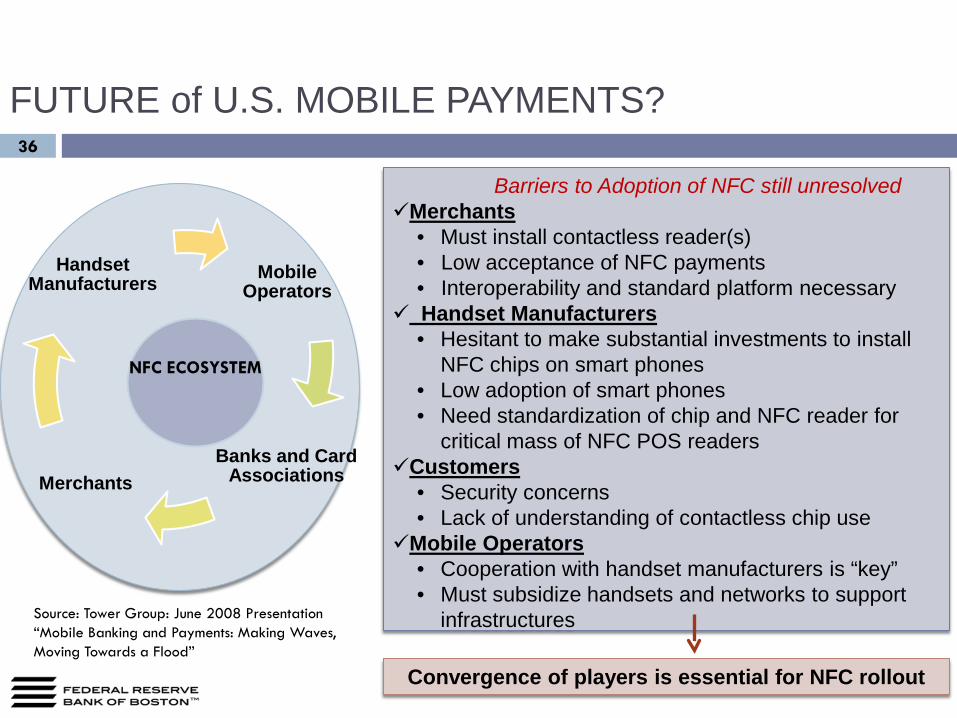

FUTURE of U.S. MOBILE PAYMENTS?

Barriers to Adoption of NFC still unresolvedMerchants

• Must install contactless reader(s)• Low acceptance of NFC payments• Interoperability and standard platform necessary

Handset Manufacturers• Hesitant to make substantial investments to install

NFC chips on smart phones• Low adoption of smart phones• Need standardization of chip and NFC reader for

critical mass of NFC POS readersCustomers

• Security concerns• Lack of understanding of contactless chip use

Mobile Operators• Cooperation with handset manufacturers is “key”• Must subsidize handsets and networks to support

infrastructures

Convergence of players is essential for NFC rollout

Mobile Operators

Banks and Card AssociationsMerchants

Handset Manufacturers

NFC ECOSYSTEM

Source: Tower Group: June 2008 Presentation “Mobile Banking and Payments: Making Waves, Moving Towards a Flood”

36

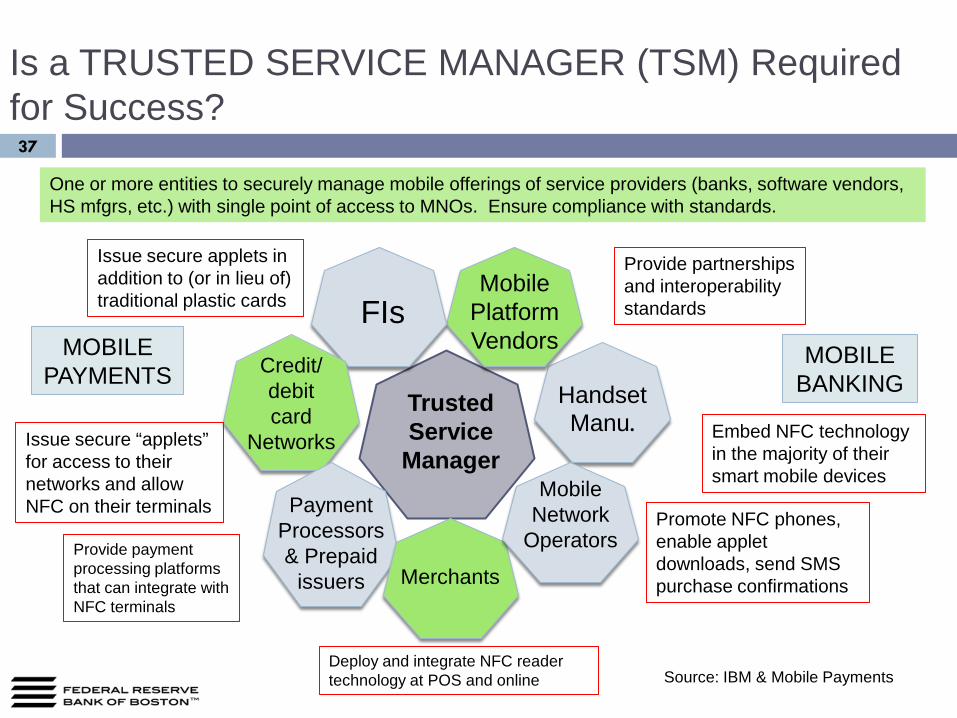

Is a TRUSTED SERVICE MANAGER (TSM) Required for Success?37

Trusted Service

Manager

Credit/ debit card

Networks

FIs Mobile

Platform Vendors

Merchants

Payment Processors & Prepaid

issuers

Mobile Network

Operators

Handset Manu.

Issue secure “applets” for access to their networks and allow NFC on their terminals

Provide payment processing platforms that can integrate with NFC terminals

Issue secure applets in addition to (or in lieu of) traditional plastic cards

Embed NFC technology in the majority of their smart mobile devices

One or more entities to securely manage mobile offerings of service providers (banks, software vendors, HS mfgrs, etc.) with single point of access to MNOs. Ensure compliance with standards.

Promote NFC phones, enable applet downloads, send SMS purchase confirmations

Deploy and integrate NFC reader technology at POS and online

Provide partnerships and interoperability standards

MOBILE BANKING

MOBILE PAYMENTS

Source: IBM & Mobile Payments

Thank You38

Marianne CroweConsumer Payments Research CenterFederal Reserve Bank of [email protected]