Embed Size (px)

Citation preview

US Economic OutlookAhmad Ijaz

Center for Business and Economic Research

Culverhouse College of Commerce

The University of Alabama

Composite Can and Tube Institute Annual Meeting

Point Clear, Alabama | May 19, 2017

Overview: U.S. Economy

• The current economic recovery (now into its 8thyear) has been the slowest recovery in postwar history.

• Compared to its peak in 4th quarter 2007, GDP is only about 12 percent higher while the number of employed is only 3.5 million higher.

• Advance estimate of inflation adjusted GDP growth in the first quarter of 2017 was only 0.7 percent – the weakest in

three years, with consumer spending and inventory accumulation slowing sharply.

• Growth in second half is expected to be around 3.4 percent, led primarily by consumer spending. For the year, the

rate of growth is estimated to be around 2.2 percent, followed by approximately 2.7 percent in 2018. The economy

grew by 1.6 percent in 2016.

• Consumer spending will remain the main source of growth, rising by 2.5 percent in 2017.

• After dropping by 0.5 percent, nonresidential business spending will increase by 4.5 percent in both 2017 and 2018. .

• However, weak wage growth in some sectors of the economy and relatively high debt levels ($12.7 trillion) will

continue to keep consumers cautious, despite the job growth seen in recent months, historically employment growth

is still relatively sluggish, and most of the jobs being added are either temporary (about 30 to 40 percent), part-time

and/or in low wage sectors of the economy.

• After a 1.2 percent drop in 2016, industrial production index will rise 1.9 percent in 2017 and 2.9 percent in 2018.

Industrial production in paper and related products will rise by 0.7 percent in 2017, following a 2.6 percent drop in

2016. Payroll employment in paper and related products industry will rise 0.4 percent, at about the same pace as

2016.

Post-recession Average Real GDP Growth

Time period Average growth

1976 - 1980 2.59%

1983 - 1989 3.75%

1992 - 1998 3.17%

2002 - 2007 2.39%

2010 - 2016 1.72%Source: U.S. Bureau of Economic Analysis

Post-recession Average Real GDP Growth

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

'76-'80 '83-'89 '92-'98 '02-'07 '10-'16

Source: U.S. Bureau of Economic Analysis

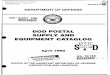

Post-recession Average Employment Growth

Time period Average growth

1976 - 1980 2.48%

1983 - 1989 2.40%

1992 - 1998 2.21%

2002 - 2007 0.99%

2010 - 2016 1.51%Source: U.S. Bureau of Labor Statistics

Post-recession Average Employment Growth

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

'76-'80 '83-'89 '92-'98 '02-'07 '10-'16

Source: U.S. Bureau of Labor Statistics

Labor Force Participation Rate

55.0

57.0

59.0

61.0

63.0

65.0

67.0

69.0

United States

Source: Bureau of Labor Statistics

Labor Productivity in the U.S.

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012 2015

Source: Bureau of Labor Statistics and Bureau of Economic Analysis Data

GDP Growth

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

10 States with highest GDP growth in 2016

-7.0%

-6.0%

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

No

rth D

akota

Wyo

min

g

Oklah

om

a

West V

irginia

Lou

isiana

Ne

w M

exico

Mo

ntan

a

Kan

sas

De

laware

Texas

10 States with lowest GDP growth in 2016

Source: Bureau of Economic Analysis

Shares of U.S. Gross Domestic Product and Nonfarm Employment by Industry (2016)

21.3414.24

3.95

4.65

8.5015.67

19.77

5.74

12.01

15.40

3.86

10.82

11.698.56

12.82

13.95

6.0610.97

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

100.00

Share of GDP Share of Non-farm Employment

Retail trade

Professional andbusiness services

Manufacturing

Leisure and hospitality

Government

Finance activities

Education and healthservices

Construction

All Other

Source: Estimates based on Bureau of Labor Statistics and Bureau of Economic Analysis Data

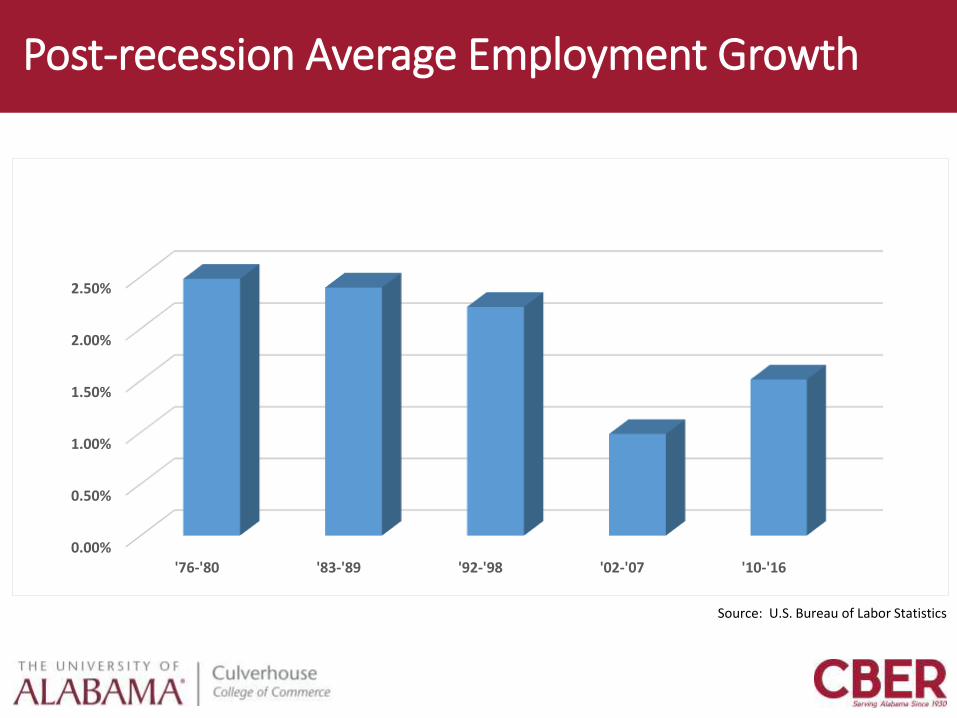

Inflation Adjusted Chained 2009 Dollars

(Annual Percent Change)

Source: Bureau of Economic Analysis and IHS Global Insight.

-30

-25

-20

-15

-10

-5

0

5

10

15

20

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

GDP

CONS. SPENDING

NON-RESIDENTIALINVESTMENTS

RESIDENTIALINVESTMENTS

U.S. Economy(GDP, Consumer Spending and Investments)

Gross Domestic Product: Expansion remains on Track(Inflation Adjusted Annual Percent Change)

-4

-3

-2

-1

0

1

2

3

4

5

6

1/1

/90

1/1

/91

1/1

/92

1/1

/93

1/1

/94

1/1

/95

1/1

/96

1/1

/97

1/1

/98

1/1

/99

1/1

/00

1/1

/01

1/1

/02

1/1

/03

1/1

/04

1/1

/05

1/1

/06

1/1

/07

1/1

/08

1/1

/09

1/1

/10

1/1

/11

1/1

/12

1/1

/13

1/1

/14

1/1

/15

1/1

/16

1/1

/17

1/1

/18

1/1

/19

1/1

/20

1/1

/21

1/1

/22

1/1

/23

1/1

/24

1/1

/25

Source: U.S. Department of Commerce and IHS Global Insight.

Consumer Spending, Total and Nondurables(Annual Percent Change, 2009 Chained Dollars)

-3

-2

-1

0

1

2

3

4

5

6

1/1

/90

1/1

/91

1/1

/92

1/1

/93

1/1

/94

1/1

/95

1/1

/96

1/1

/97

1/1

/98

1/1

/99

1/1

/00

1/1

/01

1/1

/02

1/1

/03

1/1

/04

1/1

/05

1/1

/06

1/1

/07

1/1

/08

1/1

/09

1/1

/10

1/1

/11

1/1

/12

1/1

/13

1/1

/14

1/1

/15

1/1

/16

1/1

/17

1/1

/18

1/1

/19

1/1

/20

1/1

/21

1/1

/22

1/1

/23

1/1

/24

1/1

/25

Total Nondurable GoodsSource: U.S. Department of Commerce and IHS Global Insight.

Consumer Sentiment Index(supported by improving household finances)

Source: University of Michigan and IHS Global Insight

40

60

80

100

120

1/1

/90

1/1

/91

1/1

/92

1/1

/93

1/1

/94

1/1

/95

1/1

/96

1/1

/97

1/1

/98

1/1

/99

1/1

/00

1/1

/01

1/1

/02

1/1

/03

1/1

/04

1/1

/05

1/1

/06

1/1

/07

1/1

/08

1/1

/09

1/1

/10

1/1

/11

1/1

/12

1/1

/13

1/1

/14

1/1

/15

1/1

/16

1/1

/17

1/1

/18

1/1

/19

1/1

/20

1/1

/21

1/1

/22

1/1

/23

1/1

/24

1/1

/25

Factors Affecting Consumer Spending

• Positive• Employment growth

• Wage acceleration

• Rising asset Values

• Income tax cuts in 2018

• Expansion of e-commerce sales

• Positive

• Negative• High consumer and student debt burdens

• Payroll cycle economics

• Asset and income inequality (significant increase in part-time and temporary jobs)

Nonfarm Employment, Nondurable Goods and Paper Product (Annual Percent Change)

-10

-8

-6

-4

-2

0

2

1/1

/91

1/1

/92

1/1

/93

1/1

/94

1/1

/95

1/1

/96

1/1

/97

1/1

/98

1/1

/99

1/1

/00

1/1

/01

1/1

/02

1/1

/03

1/1

/04

1/1

/05

1/1

/06

1/1

/07

1/1

/08

1/1

/09

1/1

/10

1/1

/11

1/1

/12

1/1

/13

1/1

/14

1/1

/15

1/1

/16

1/1

/17

1/1

/18

1/1

/19

1/1

/20

1/1

/21

1/1

/22

1/1

/23

1/1

/24

1/1

/25

Nondurable Manufacturing Paper Products

Source: U.S. Department of Commerce and IHS Global Insight.

Change in Inventories, Total and Manufacturing(Billions of Chained 2009 Dollars)

-200

-150

-100

-50

0

50

100

1/1

/90

1/1

/91

1/1

/92

1/1

/93

1/1

/94

1/1

/95

1/1

/96

1/1

/97

1/1

/98

1/1

/99

1/1

/00

1/1

/01

1/1

/02

1/1

/03

1/1

/04

1/1

/05

1/1

/06

1/1

/07

1/1

/08

1/1

/09

1/1

/10

1/1

/11

1/1

/12

1/1

/13

1/1

/14

1/1

/15

1/1

/16

1/1

/17

1/1

/18

1/1

/19

1/1

/20

1/1

/21

1/1

/22

1/1

/23

1/1

/24

1/1

/25

Total Business Total Manufacturing

Source: U.S. Department of Commerce and IHS Global Insight.

Industrial Production Index(Annual Percent Change)

-20

-15

-10

-5

0

5

10

15

20

1/1

/90

1/1

/91

1/1

/92

1/1

/93

1/1

/94

1/1

/95

1/1

/96

1/1

/97

1/1

/98

1/1

/99

1/1

/00

1/1

/01

1/1

/02

1/1

/03

1/1

/04

1/1

/05

1/1

/06

1/1

/07

1/1

/08

1/1

/09

1/1

/10

1/1

/11

1/1

/12

1/1

/13

1/1

/14

1/1

/15

1/1

/16

1/1

/17

1/1

/18

1/1

/19

1/1

/20

1/1

/21

1/1

/22

1/1

/23

1/1

/24

1/1

/25

Paper and Paper Products Converted Paper Products

Bags, Coated and Treated Paper Residual Paper Products

Source: U.S. Department of Commerce and IHS Global Insight.

Nonresidential and Residential Business Investments(Annual Percent Change, Chained 2009 Dollars)

-30

-25

-20

-15

-10

-5

0

5

10

15

20

1/1

/90

1/1

/91

1/1

/92

1/1

/93

1/1

/94

1/1

/95

1/1

/96

1/1

/97

1/1

/98

1/1

/99

1/1

/00

1/1

/01

1/1

/02

1/1

/03

1/1

/04

1/1

/05

1/1

/06

1/1

/07

1/1

/08

1/1

/09

1/1

/10

1/1

/11

1/1

/12

1/1

/13

1/1

/14

1/1

/15

1/1

/16

1/1

/17

1/1

/18

1/1

/19

1/1

/20

1/1

/21

1/1

/22

1/1

/23

1/1

/24

1/1

/25

Nonresidential ResidentialSource: U.S. Department of Commerce and IHS Global Insight.

U.S. Recessions: Total Non-farm Employment

90

92

94

96

98

100

102

104

0 10 20 30 40 50 60 70 80 90

Months

Jan-80

Jul-81

Jul-90

Mar-01

Dec-07

Source: Estimates based on Bureau of Labor Statistics Data

U.S. Economic Forecast

(Percent change unless otherwise noted) 2016 2017 2018 2019 2020

Real GDP 1.6 2.2 2.7 2.4 2.2

Consumption 2.7 2.5 3.2 2.8 3.2

Residential Investment 3.5 11.7 4.7 2.7 3.1

Commercial, Healthcare Structures 12.9 10.1 15.4 6.1 5.1

Nonresidential Fixed Investment 6.0 2.1 -0.2 4.6 4.5

Federal Government -2.5 0.0 0.7 0.3 -0.8

State & Local Government 0.2 2.9 0.9 0.8 1.4

Exports 4.3 0.1 -0.3 3.1 3.1

Imports 4.4 4.6 1.2 4.9 4.9

Payroll Employment 1.9 2.1 1.7 1.2 1.2

Unemployment Rate 6.2 5.3 4.9 4.7 4.7

CPI Inflation 1.6 0.1 1.2 2.5 2.5

Light Vehicle Sales (Millions) 16.44 17.39 17.47 17.78 17.78

Paperboard Manufacturing Snapshot

2002 2007

Number of establishments 2,669 2,409

Value of shipments ($ Millions) 43,494 50,935

Annual payroll ($ Millions) 7,091 7,385

Total employment 184,884 165,978

Value of shipments per establishment ($1,000)

16,296 21,144

Value of shipments per employee ($1,000) 235 307

Value of shipments per $ of payroll ($) 6.13 6.9

Payroll per employee ($) 38,355 44,493

Employees per establishment 69.27 68.9

Value of shipments per capita ($) 151 169

Population per establishment 107,765 125,044

Value of Shipments: United States

Source: U.S. Census Bureau

Employees Per Establishments: United States

Source: U.S. Census Bureau

Number of Establishments: United States

2,345

2,241

2,205

2,1312,117

2,088

1,950

2,000

2,050

2,100

2,150

2,200

2,250

2,300

2,350

2,400

2008 2009 2010 2011 2012 2013

Source: U.S. Census Bureau

Number of Employees: United States

162,515

147,593

142,868141,159

137,468138,684

120,000

125,000

130,000

135,000

140,000

145,000

150,000

155,000

160,000

165,000

2008 2009 2010 2011 2012 2013

Source: U.S. Census Bureau

U.S. Recessions- Paperboard Container Manufacturing Employment

70.0

75.0

80.0

85.0

90.0

95.0

100.0

105.0

0 20 40 60 80 100 120

Months

Jul-90

Mar-01

Dec-07

Source: Estimates based on Bureau of Labor Statistics Data

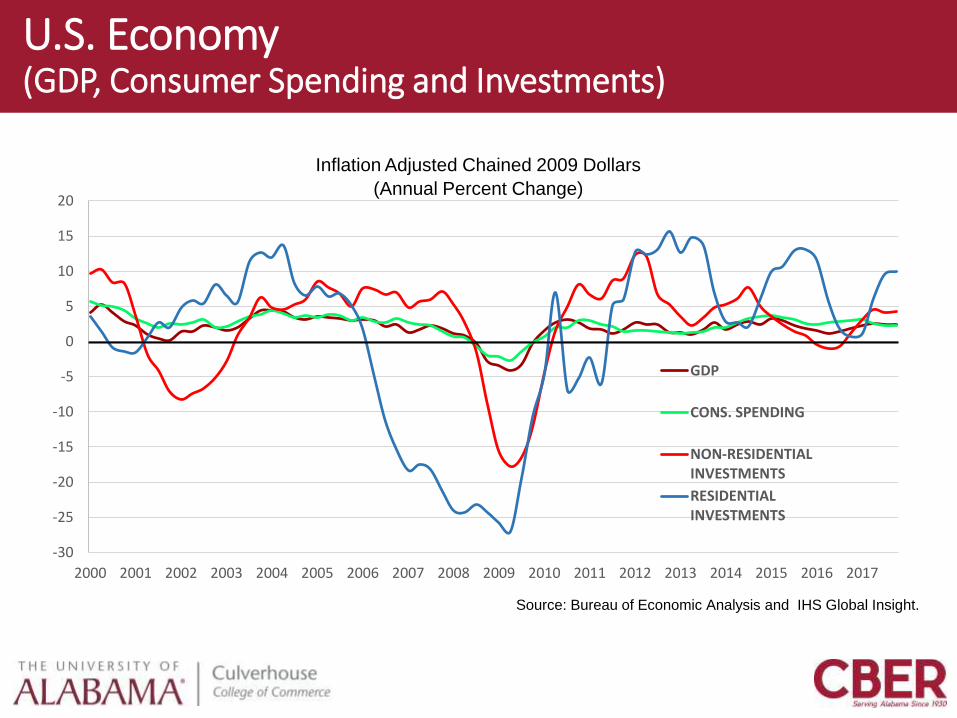

Payroll per Employee: United States (Dollars)

46,995

45,136

48,128

49,293

51,525

52,634

40,000

42,000

44,000

46,000

48,000

50,000

52,000

54,000

2008 2009 2010 2011 2012 2013

Source: U.S. Census Bureau

Average Weekly Earnings, 2016

$882

$1,058

$1,112

$1,041

$990

$0 $200 $400 $600 $800 $1,000 $1,200

All private sector industries

Manufacturing

Paper and paper products

Converted paper products

Paperboard containers

Source: Bureau of Labor Statistics, CES

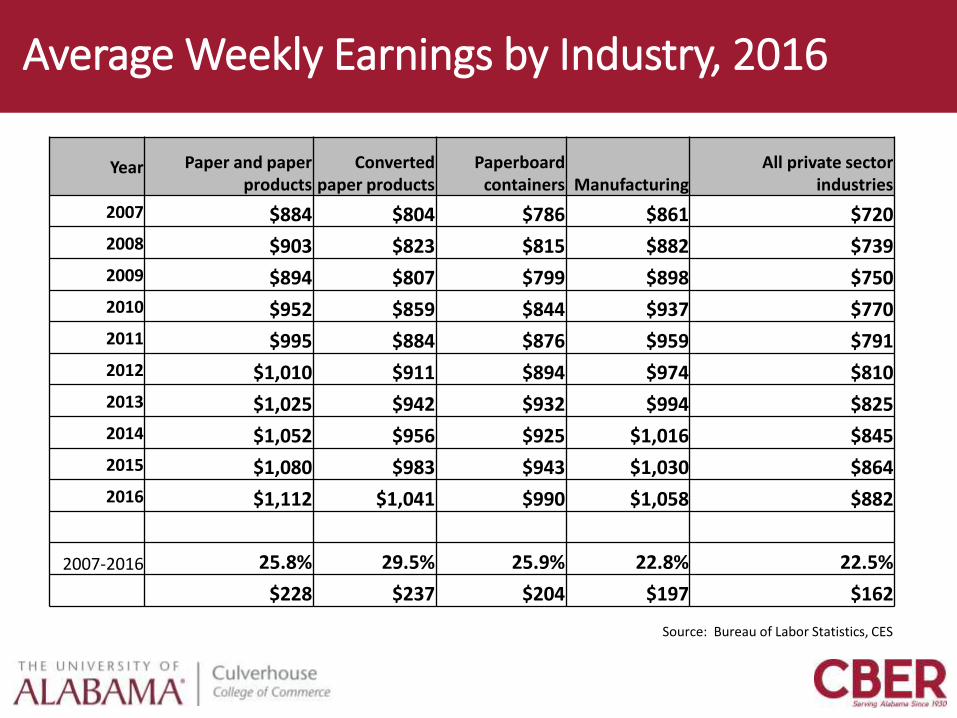

Average Weekly Earnings by Industry, 2016

Year Paper and paper products

Converted paper products

Paperboard containers Manufacturing

All private sector industries

2007 $884 $804 $786 $861 $720

2008 $903 $823 $815 $882 $739

2009 $894 $807 $799 $898 $750

2010 $952 $859 $844 $937 $770

2011 $995 $884 $876 $959 $791

2012 $1,010 $911 $894 $974 $810

2013 $1,025 $942 $932 $994 $825

2014 $1,052 $956 $925 $1,016 $845

2015 $1,080 $983 $943 $1,030 $864

2016 $1,112 $1,041 $990 $1,058 $882

2007-2016 25.8% 29.5% 25.9% 22.8% 22.5%

$228 $237 $204 $197 $162

Source: Bureau of Labor Statistics, CES

Average Weekly Earnings by Industry, 2016

$600

$700

$800

$900

$1,000

$1,100

$1,200

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Paper and paper products Converted paper products Paperboard containers Manufacturing All private sector industries

Source: Bureau of Labor Statistics, CES

Employment by Industry (Thousands)

Year

Industries

Paper andPaper

products

Pulp, paper, and

paperboard mills

Converted paper

products

Paperboard containers

Corrugated and solid

fiber boxes

Folding boxes and

miscellaneous paperboard

containers

Paper bags and coated and

treated paper

Stationery and other converted

paper products

ManufacturingAll private

sector industries

2007 458 132 326 172 110 62 73 81 13,878 115,778

2008 445 126 318 167 106 60 71 80 13,403 114,737

2009 407 117 290 151 94 56 65 75 11,848 108,747

2010 395 112 282 147 93 54 62 73 11,529 107,864

2011 387 109 278 145 92 53 63 70 11,727 109,848

2012 380 108 272 142 90 52 61 68 11,927 112,251

2013 378 107 271 144 90 53 61 66 12,020 114,531

2014 373 104 269 143 91 52 60 65 12,185 117,062

2015 373 101 271 147 93 54 59 65 12,335 119,789

2016 371 100 271 148 93 55 60 63 12,348 122,0772007-2016 -19.1% -24.3% -17.0% -14.0% -15.3% -11.9% -18.3% -22.0% -11.0% 5.4%

-87 -32 -55 -24 -17 -7 -13 -18 -1,530 6,300

Source: Bureau of Labor Statistics, CES

Change in Employment (Percent)

-14.00

-12.00

-10.00

-8.00

-6.00

-4.00

-2.00

0.00

2.00

4.00

2008 2009 2010 2011 2012 2013 2014 2015 2016

Paperboard containers Paper bags and coated and treated paper

Stationery and other converted paper products Manufacturing

All private sector industries Source: Bureau of Labor Statistics, CES

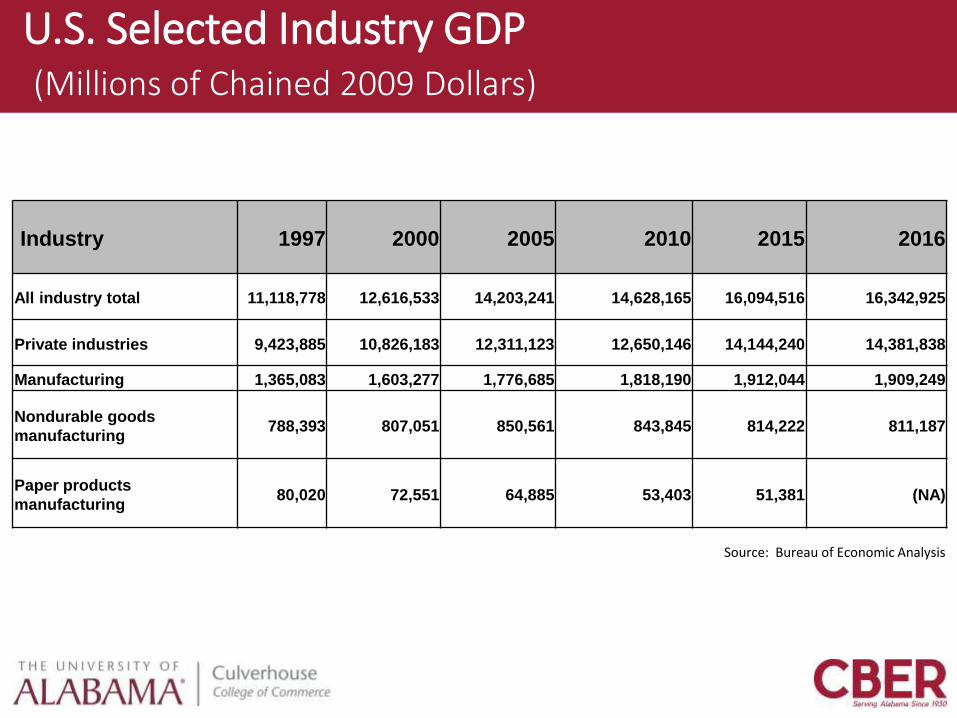

U.S. Selected Industry GDP(Millions of Chained 2009 Dollars)

Industry 1997 2000 2005 2010 2015 2016

All industry total 11,118,778 12,616,533 14,203,241 14,628,165 16,094,516 16,342,925

Private industries 9,423,885 10,826,183 12,311,123 12,650,146 14,144,240 14,381,838

Manufacturing 1,365,083 1,603,277 1,776,685 1,818,190 1,912,044 1,909,249

Nondurable goods

manufacturing788,393 807,051 850,561 843,845 814,222 811,187

Paper products

manufacturing80,020 72,551 64,885 53,403 51,381 (NA)

Source: Bureau of Economic Analysis

Annual Percent Change in GDP

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

All industry total Manufacturing Nondurable goods manufacturing Paper products manufacturing

Source: Bureau of Economic Analysis

Paper Industry Share of Total GDP (Percent)

0.00%

0.10%

0.20%

0.30%

0.40%

0.50%

0.60%

0.70%

0.80%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Source: Bureau Economic Analysis

Paper Industry Forecast (Industrial Production)

(Percent change unless otherwise noted)

2016 2017 2018 2019 2020

Paper and Paper Products -2.4 -1.2 0.0 0.7 0.7

Pulp and Paper Mills -3.3 -2.1 -0.5 0.1 0.3

Converted Paper Products -1.5 -0.4 0.5 0.9 0.9

Bags, Coated and Treated

Paper -6.3 -2.7 0.4 0.9 1.0

Other Paper Products -0.4 0.9 1.3 1.7 1.5

Source: IHS Global Insight

Economy will continue to grow at around 2 to 2.5 percent rate for the next two to three years

Thank youCenter for Business and Economic Research

Culverhouse College of Commerce

The University of Alabama

205-348-6191

http://cber.cba.ua.edu