Embed Size (px)

Citation preview

US Department of JusticeFair Lending Enforcement

Daniel P. MostellerActing Special Litigation Counsel for Fair Lending

Housing and Civil Enforcement Section, Civil Rights Division

US Department of Justice

2

Keynote Speaker

Daniel P. MostellerActing Special Litigation Counselfor Fair Lending

Housing and Civil EnforcementSection, Civil Rights DivisionUS Department of Justice

3

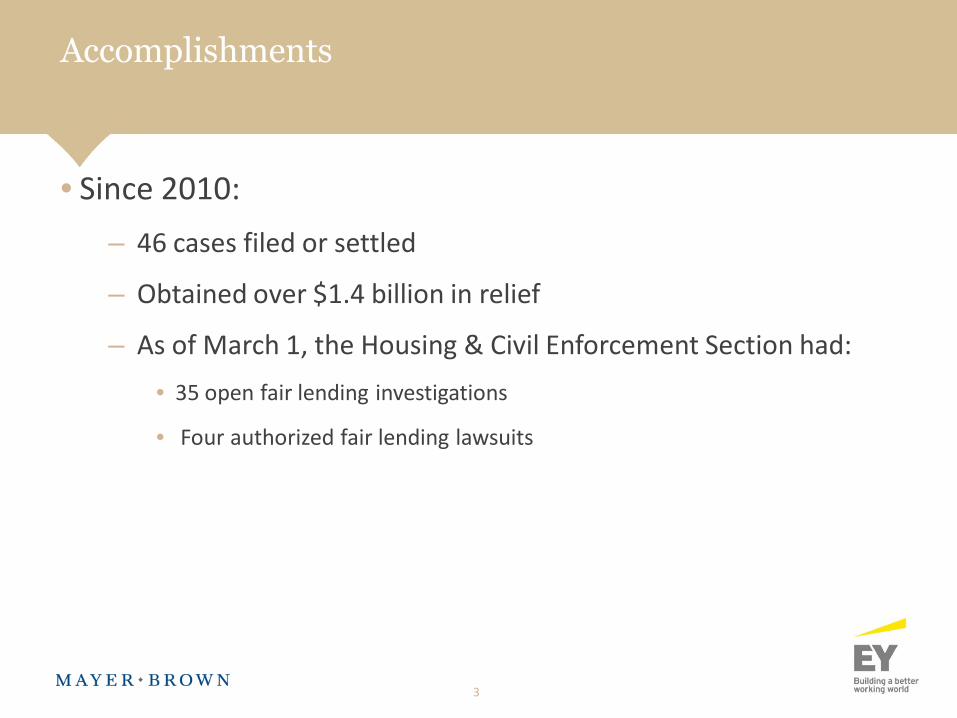

Accomplishments

• Since 2010:

– 46 cases filed or settled

– Obtained over $1.4 billion in relief

– As of March 1, the Housing & Civil Enforcement Section had:

• 35 open fair lending investigations

• Four authorized fair lending lawsuits

DISPARATE IMPACT

5

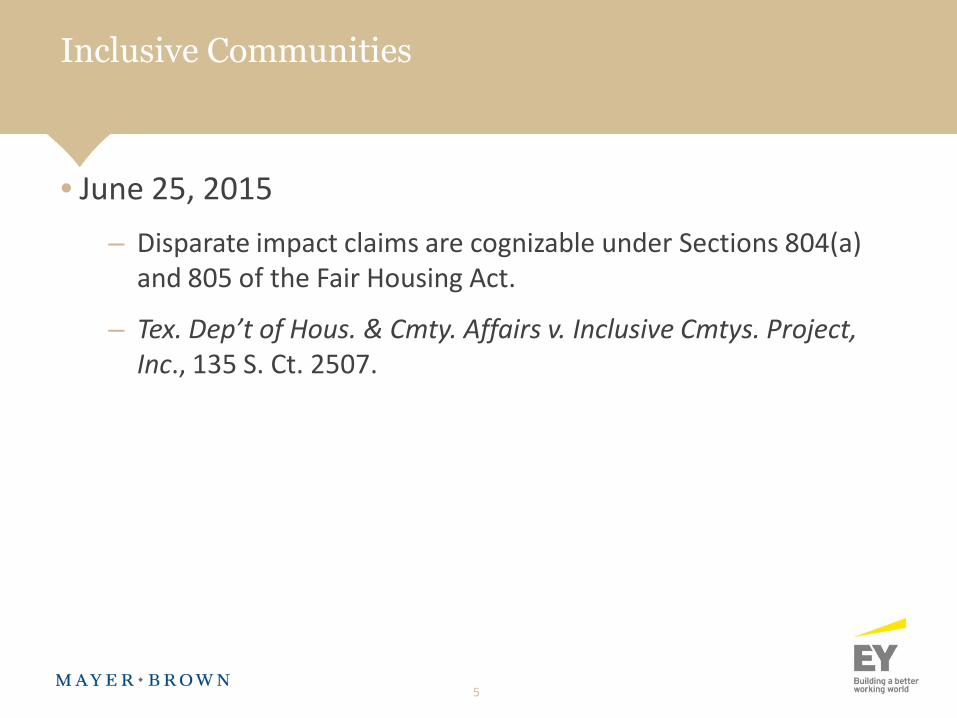

• June 25, 2015

– Disparate impact claims are cognizable under Sections 804(a)and 805 of the Fair Housing Act.

– Tex. Dep’t of Hous. & Cmty. Affairs v. Inclusive Cmtys. Project,Inc., 135 S. Ct. 2507.

Inclusive Communities

6

• “[V]estiges remain today, intertwined with the country’seconomic and social life,” of unconstitutional de jureresidential segregation by race.

• Disparate impact helps “counteract unconsciousprejudices and disguised animus that escape easyclassification as disparate treatment.”

Inclusive Communities

7

• Court finds multiple principles of statutory interpretationthat support the existence of disparate impact:

1. “otherwise make unavailable” language of 804(a), and the“discriminate against” language of 805, refer to theconsequences of actions and not just to the mindset ofactors.

2. 1988 amendments to the FHA came into effect against abackdrop of unanimous support in the Courts of Appeal fordisparate impact under FHA.

3. Court finds it “consistent with the FHA’s central purpose.”

Inclusive Communities

8

• “[D]isparate-impact liability has always been properlylimited in key respects.” (emphasis added)

• Plaintiff must identify policies causing disparity

• Analogue to “business necessity” defense

Inclusive Communities

9

• Inclusive Communities has been interpreted to have“implicitly adopted” HUD’s burden shifting approach andto require following HUD’s Rule instead of prior circuitcase law. MHANY Mgmt. v. Cnty. of Nassau, __ F.3d ___,2016 WL 1128424, at *31 (2d Cir. Mar. 23, 2016).

Inclusive Communities

10

• Compare FHA § 805(a) (“unlawful for any person . . . todiscriminate against any person in making available [alending] transaction”) with ECOA § 1691(a) (“unlawful forany creditor to discriminate against any applicant, withrespect to any aspect of a credit transaction”).

Inclusive Communities and ECOA

REDLINING

12

• Ten DOJ settlements involving allegations of redliningsince 2002.

• Regulatory and Enforcement Agency priority

• Recent settlements:

– CPFB and U.S. v. Hudson City Savings Bank (D.N.J.)

– U.S. v. Eagle Bank and Trust (E.D. Mo.)

A Persistent Fair Lending Issue

13

• Mortgage credit discrimination based on thecharacteristics of the would-be borrower’s neighborhood.

• Investigations focus on:

– CRA Assessment Areas

– Branch locations

– Marketing and advertising

– Statistical analyses

Redlining

14

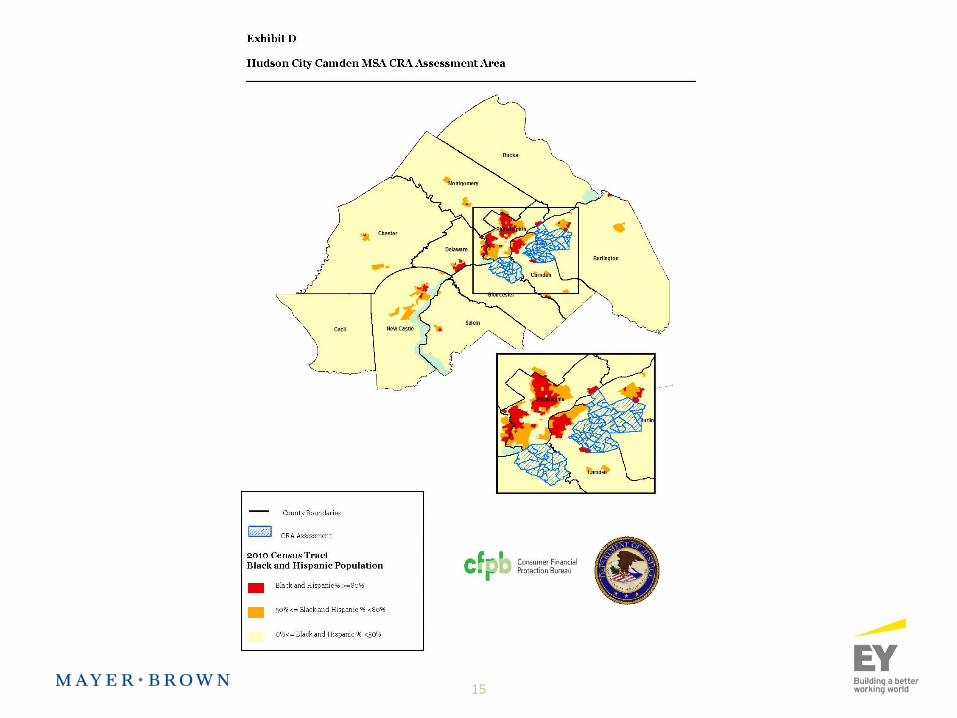

• Regulators use a bank’s delineated assessment areas inevaluating whether the institution is meeting the creditneeds of its entire community.

• A bank’s assessment area must consist generally of one ormore MSAs or one or more contiguous politicalsubdivisions such as a county or city.

• May not reflect illegal discrimination.

CRA Assessment Areas

15

16

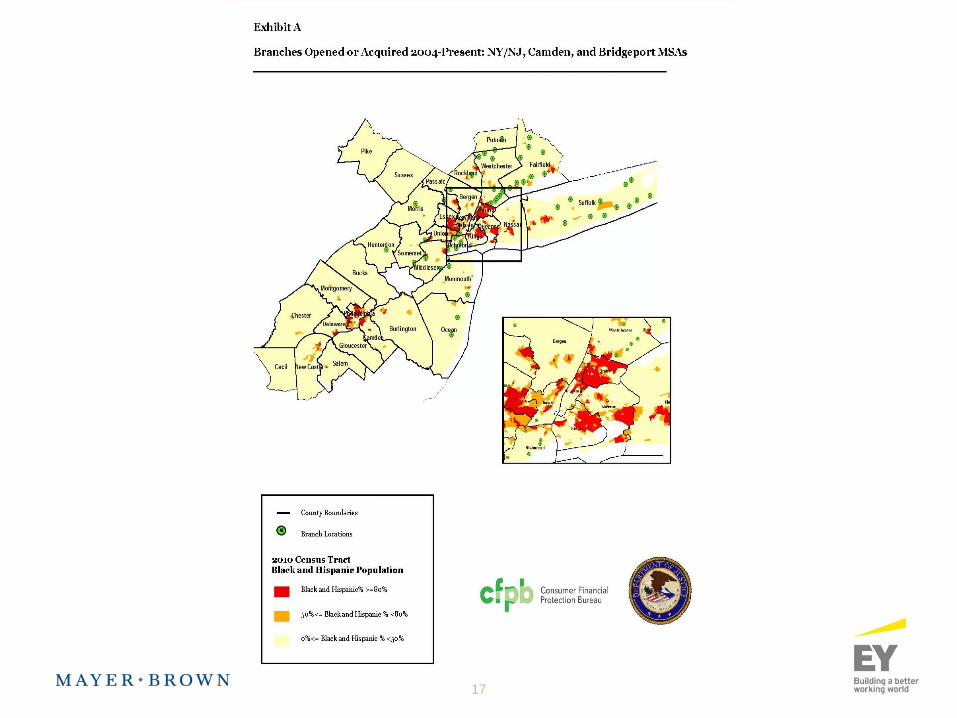

• Plotting the locations of a bank’s branch locationsprovides evidence as to locations the bank intends toserve.

• Historical analysis of branching decisions often showsdirections the bank is moving toward or away from.

Branch Locations

17

18

• We review past efforts in:

– Print media advertising

– Radio advertising

– Direct mailings

• We look at minority media outlets available in therelevant areas.

Marketing and Advertising

19

• Identify “peers” that are “similar” to target lender.

• Determine extent to which peer lenders provide servicesin majority minority neighborhoods of market areas.

• Expect similar behavior from the target lender and peerlenders.

Statistical Analyses

20

• Joint investigation and filing with CFPB

• 2009 to 2013

• Failure to provide its home mortgage lending services tomajority-Black-and-Hispanic neighborhoods on an equalbasis as to predominantly white neighborhoods

• Major market areas NJ, NY, CT, and PA

Hudson City Savings Bank

21

• $25 million in loan subsidies (interest rates, closing costs,down payment) for previously redlined areas

• Two new branches in previously redlined areas

• $1.5 million in targeted advertising, outreach, andconsumer education

• $750 thousand to partner with communities groups toassist residents of previously redlined areas

Hudson City Savings Bank

22

• Nondiscrimination provisions

• Expansion of CRA assessment areas

• Training and changes to bank procedures

• $5.5 million to CFPB Civil Penalty Fund

Hudson City Savings Bank

REDLININGSuccess Stories

24

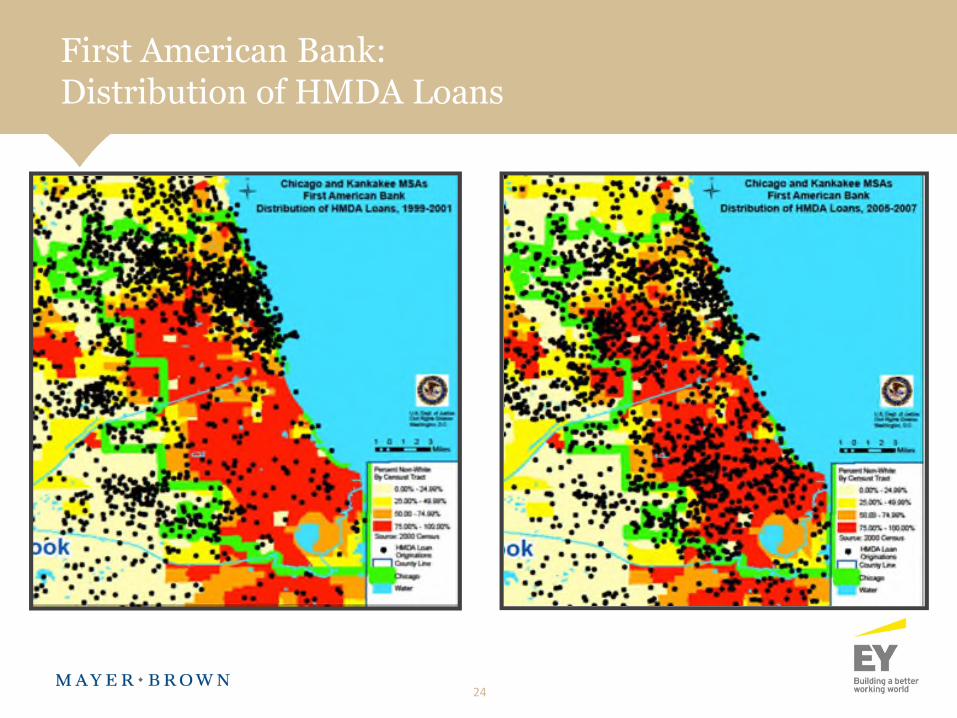

First American Bank:Distribution of HMDA Loans

25

• Opened branch in town with no bank branches

• After one year, hundreds of checking and savings accountsopened

• Fewer people relying on fringe lenders

• Bank proactively opening another branch in majority-minority neighborhood

Midwest BankCentre

INDIRECT AUTO LENDING

27

• Opened a series of investigations

• Different types of indirect auto lenders

• Several of the largest auto lenders in the United States

• Looked at markup disparities for:

– African-American, Hispanic, and Asian/Pacific Islanderborrowers

Joint DOJ-CFPB Effort

28

• Lender that funds the loan:

– Direct lenders

– Indirect lenders

• Independent financial institutions

• Captive lenders

• Individual dealership that arranges loan

• Individual dealership that funds the loan

Which Parties to Auto Lending Transaction AreCovered?

29

• Auto loan applications may not include race or ethnicityinformation.

• BISG method calculates race or ethnicity based on Censussurname information and neighborhood data.

• Comparable proxies used in voting, employment, andpolicing contexts.

Data Analysis

30

• Key terms:

– Buy rate

– Contract rate

– Markup, a/k/a dealer reserve

– Caps

Dealer Markup

31

• U.S. v. Ally Financial Inc. (Dec. 2013)

• U.S. v. Evergreen Bank Group (May 2015)

• U.S. v. American Honda Finance Corp. (July 2015)

• U.S. v. Fifth Third Bank (Sept. 2015)

• U.S. v. Toyota Motor Credit Corp. (Feb. 2016)

DOJ’s Dealer Markup Cases

32

• Complaints allege lenders charged minority borrowershigher interest rate markups on indirect auto loans.

• Lenders granted dealers broad and subjective discretionby lenders to mark up buy rate, subject to caps.

• Lenders did not conduct sufficient monitoring to detectrace or national origin disparities.

DOJ’s Dealer Markup Cases

33

• Enhanced Compliance Monitoring System

• Non-discretionary compensation

• Lower caps

Range of Remedies

34

• Joint investigation with CFPB

• CFPB entered into parallel consent order in itsadministrative process

Toyota Motor Credit Corp.

35

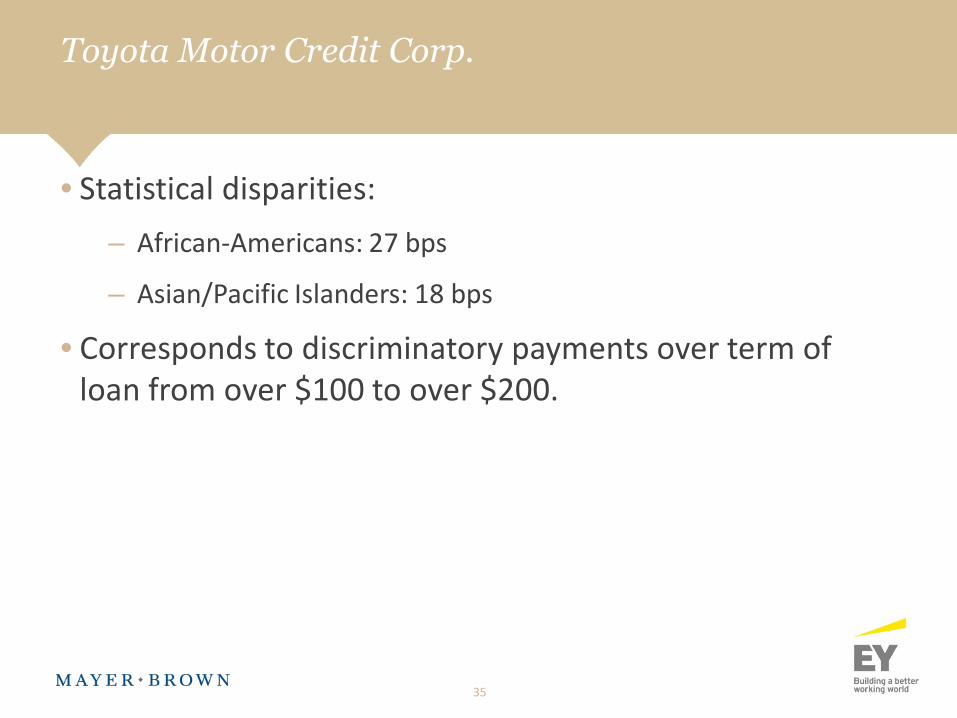

• Statistical disparities:

– African-Americans: 27 bps

– Asian/Pacific Islanders: 18 bps

• Corresponds to discriminatory payments over term ofloan from over $100 to over $200.

Toyota Motor Credit Corp.

36

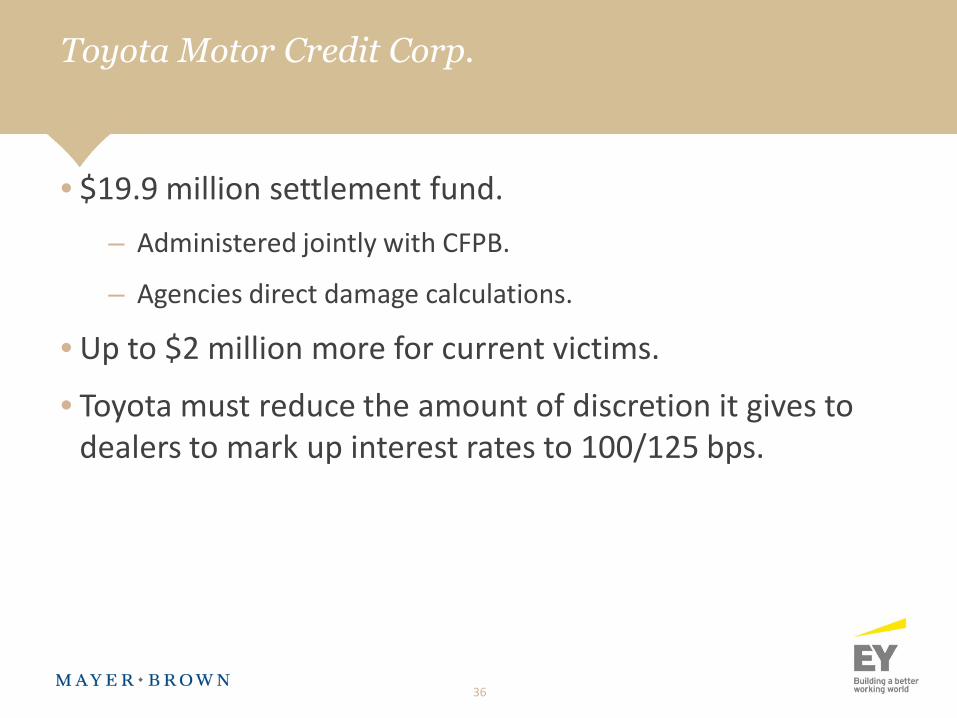

• $19.9 million settlement fund.

– Administered jointly with CFPB.

– Agencies direct damage calculations.

• Up to $2 million more for current victims.

• Toyota must reduce the amount of discretion it gives todealers to mark up interest rates to 100/125 bps.

Toyota Motor Credit Corp.

SERVICEMEMBERS CIVILRELIEF ACT

38

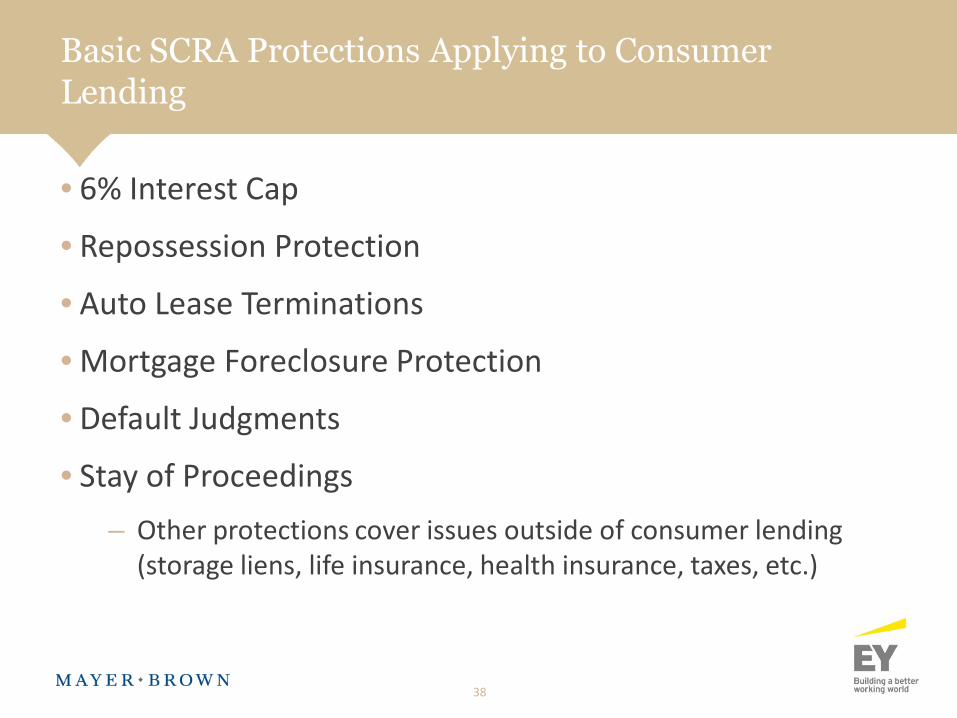

• 6% Interest Cap

• Repossession Protection

• Auto Lease Terminations

• Mortgage Foreclosure Protection

• Default Judgments

• Stay of Proceedings

– Other protections cover issues outside of consumer lending(storage liens, life insurance, health insurance, taxes, etc.)

Basic SCRA Protections Applying to ConsumerLending

39

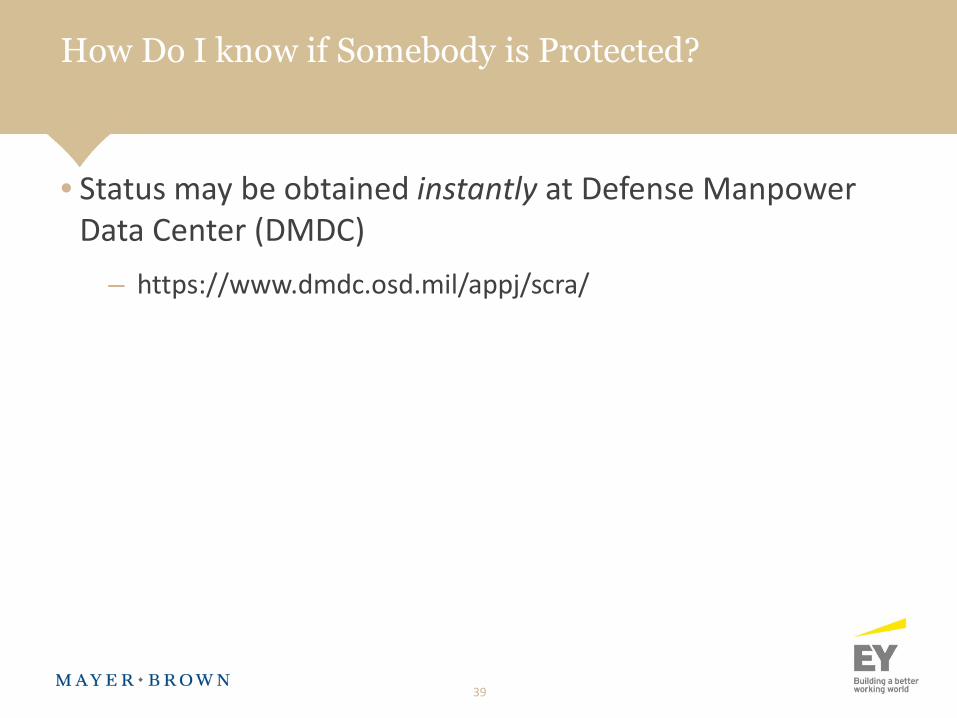

• Status may be obtained instantly at Defense ManpowerData Center (DMDC)

– https://www.dmdc.osd.mil/appj/scra/

How Do I know if Somebody is Protected?

40

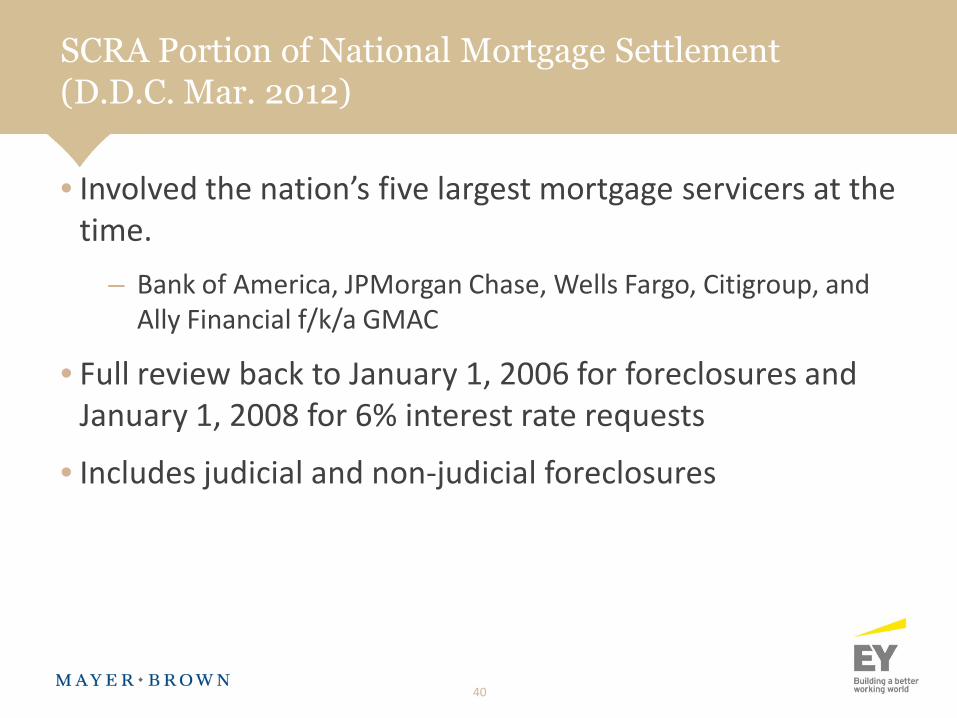

• Involved the nation’s five largest mortgage servicers at thetime.

– Bank of America, JPMorgan Chase, Wells Fargo, Citigroup, andAlly Financial f/k/a GMAC

• Full review back to January 1, 2006 for foreclosures andJanuary 1, 2008 for 6% interest rate requests

• Includes judicial and non-judicial foreclosures

SCRA Portion of National Mortgage Settlement(D.D.C. Mar. 2012)

41

• September 2015 announcement:

– 2,413 servicemembers and their co-borrowers are eligible toreceive over $311 million for illegal foreclosures.

SCRA Portion of National Mortgage Settlement(D.D.C. Mar. 2012)

42

• Payments overseen by DOJ

• Minimum payments per servicemember:

– $125,000 for a wrongful foreclosure

– Excess interest charged + greater of 3x that amount or $500 fora wrongful interest rate cap denial

SCRA Portion of National Mortgage Settlement(D.D.C. Mar. 2012)

SCRASuccess Stories

44

• At basic training; car was repossessed without courtorder. Complained to Army Legal Assistance.

• Complaint resulted in DOJ investigation

• Settlement with Santander Consumer, USA

• $9 million for 1,100 affected servicemembers

SPC Joshua Davis, USA

45

• One call from Davis-Monthan AFB to DOJ

• DOJ investigation

• Credit card company had not been lowering active dutyservicemember card rates to 6%

• Settlement with Capital One, N.A.

• $12 million for affected servicemembers

AF Servicemember

46

• Full text of statutes

• Annual ECOA Reports to Congress

• Principal DAAG Vanita Gupta’s speeches

• All press releases

– http://www.justice.gov/crt/housing-and-civil-enforcement-section

– http://www.servicemembers.gov

Want More Information?

QUESTIONS

Mayer Brown is a global legal services provider comprising legal practices that are separate entities (the "Mayer Brown Practices"). The Mayer Brown Practices are: Mayer Brown LLP and Mayer Brown Europe–Brussels LLP, both limited liability partnerships established in Illinois USA;Mayer Brown International LLP, a limited liability partnership incorporated in England and Wales (authorized and regulated by the Solicitors Regulation Authority and registered in England and Wales number OC 303359); Mayer Brown, a SELAS established in France; Mayer BrownJSM, a Hong Kong partnership and its associated legal practices in Asia; and Tauil & Chequer Advogados, a Brazilian law partnership with which Mayer Brown is associated. Mayer Brown Consulting (Singapore) Pte. Ltd and its subsidiary, which are affiliated with Mayer Brown, providecustoms and trade advisory and consultancy services, not legal services. "Mayer Brown" and the Mayer Brown logo are the trademarks of the Mayer Brown Practices in their respective jurisdictions.