Embed Size (px)

Citation preview

U.S. Biodiesel Industry Growth in U.S. Biodiesel Industry Growth in U.S. Biodiesel Industry Growth in U.S. Biodiesel Industry Growth in

the Next Decadethe Next Decadethe Next Decadethe Next DecadeJ. Alan Weber

MARC-IV

September 30, 2011

Presentation Content

• Policy Background

• Industry Situation & Outlook

• Raw Material Supplies

• Growth Forecast• Growth Forecast

Policy Background

Renewable Fuel Standard (RFS 2)

• Energy Independence and Security Act of 2007 signed by the President on December 19, 2007– Increases RFS, to 9 billion gallons of renewable fuels in 2008 and to 36 billion gallons by 2022.

4 4

and to 36 billion gallons by 2022.

• Within the RFS, creates a minimum use requirement for “biomass-based diesel” which is a technology neutral classification, and includes biodiesel.

– Minimum usage requirements of 800 million gallons of biodiesel in 2011 up to 1 billion gallons in 2012.

• To qualify, the fuel must meet a 50 percent lifecycle To qualify, the fuel must meet a 50 percent lifecycle To qualify, the fuel must meet a 50 percent lifecycle To qualify, the fuel must meet a 50 percent lifecycle greenhouse gas emission requirementgreenhouse gas emission requirementgreenhouse gas emission requirementgreenhouse gas emission requirement

Important Issues

• Definition of “Renewable Biomass”.

• EPA approved pathways to meet the 50%

reduction in life-cycle greenhouse gas

emissions.emissions.

• Biomass-based diesel fuel volume obligation

for 2013 and beyond determined by the U.S.

EPA Administrator.

Renewable Biomass

• EISA’s definition of “renewable biomass”

incorporates land restrictions for planted crops

and trees.

– Planted crops and trees are to be harvested from

agricultural land cleared or cultivated at any time agricultural land cleared or cultivated at any time

prior to December 19, 2007, that is either actively

managed or fallow, and non-forested.

– Renewable fuel producers will need to have

information about the origin of the feedstock they

procure in order to generate RINs.

EPA Pathways

• Palm pathway under review by EPA.

• Palm based biodiesel can be marketed in the

U.S., however it cannot currently be marketed

as an advanced biofuel to meet the biomass-as an advanced biofuel to meet the biomass-

based diesel volume obligation.

– Due to the value differential of biomass-based

diesel RINs compared to conventional biofuel

RINs, it is difficult to market palm-based

biodiesel in the current marketplace.

Biomass-based Diesel

Volume Obligations

• Under the RFS2, EPA is tasked with setting the renewable fuel volume obligations each November for the following year.

• The statute also requires EPA to determine and promulgate the applicable volume of biomass-based diesel that will be required in 2013 and promulgate the applicable volume of biomass-based diesel that will be required in 2013 and beyond, as the statute does not specify the applicable volumes for years after 2012.– Notice of Proposed Rulemaking issued on July 1st.

– Biomass-based diesel fuel• 2012 volume obligation maintained at 1 billion gallons.

• 2013 volume obligation proposed at 1.28 billion gallons.

Industry Situation & Outlook

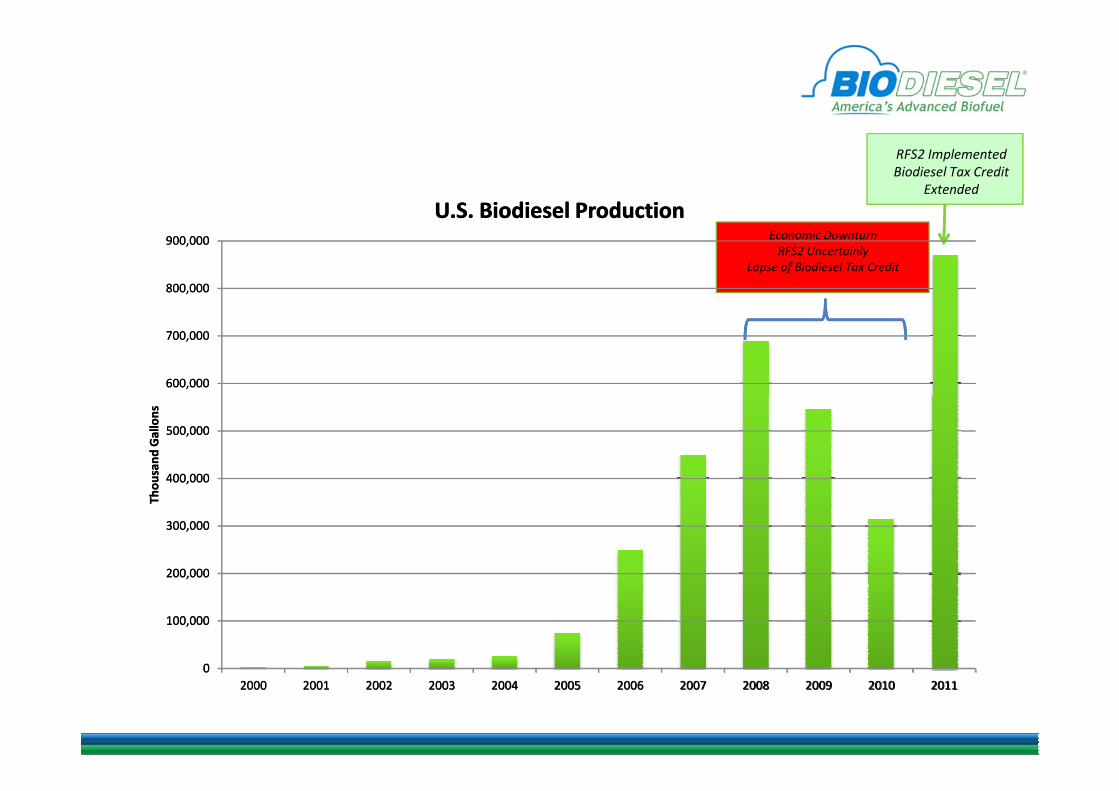

Industry Volatility

• Industry marked by significant growth from

2005 to 2008.

• Economic conditions, policy uncertainty, and

changing global trade policy led to downturn in changing global trade policy led to downturn in

production (2009-2010).

• Renewal of biodiesel blenders excise tax credit

coupled with full implementation of RFS2 has

led to renewed industry growth.

600,000

700,000

800,000

900,000

U.S. Biodiesel ProductionEconomic Downturn

RFS2 Uncertainly

Lapse of Biodiesel Tax Credit

RFS2 Implemented

Biodiesel Tax Credit

Extended

600,000

700,000

800,000

900,000

U.S. Biodiesel Production

0

100,000

200,000

300,000

400,000

500,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Th

ou

san

d G

all

on

s

0

100,000

200,000

300,000

400,000

500,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Th

ou

san

d G

all

on

s

2,000,000

2,500,000

3,000,000

U.S. Biodiesel Production

Looking to the future…..

0

500,000

1,000,000

1,500,000

2,000,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

(est)

2012 2013 2104 2015 2016 2017

Th

ou

san

d G

all

on

s

Raw Material Supplies

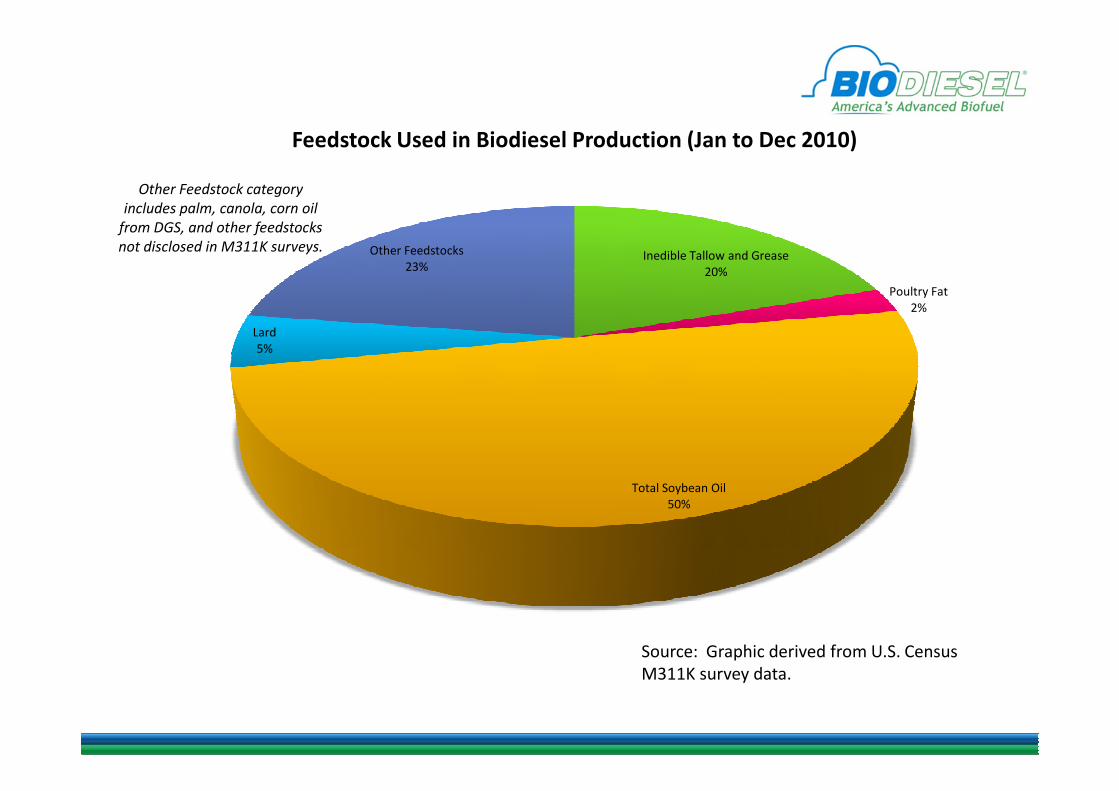

Feedstock OptionsEPA approved pathways or those under review

Corn Oil from DGS

Yellow Grease

Animal Fats

Soybean Oil

Palm Oil

Canola Oil

Inedible Tallow and Grease

20%

Poultry Fat

2%

Lard

5%

Other Feedstocks

23%

Feedstock Used in Biodiesel Production (Jan to Dec 2010)

Other Feedstock category

includes palm, canola, corn oil

from DGS, and other feedstocks

not disclosed in M311K surveys.

Total Soybean Oil

50%

Source: Graphic derived from U.S. Census

M311K survey data.

Progress with New

Feedstocks……

Low Ricin Castor

AlgaeJatropha

Pennycress

Seashore Mallow

Growth Forecasts

Economic Forecasting….

• Dr. John Kruse and IHS

Global Insight assisted the

biodiesel industry with

economic modeling efforteconomic modeling effort

– Partial equilibrium

econometric model that

includes both a domestic

and international

component

Key Assumptions

• Crude Oil Prices

• Public Policy

– Global

– Domestic– Domestic

• Edible Oil Demand

• Feedstock Options

Feedstock Assumptions

• Enhanced Yields from USDA Baseline for…

– Canola, corn, and soybeans

• Increased Extraction of Corn Oil from DGS

• Maintained Animal Fats & Yellow Grease • Maintained Animal Fats & Yellow Grease Availability at Current Forecasted Levels

• USDA Baseline Levels for Palm and Palm Oil Derivatives (e.g. PFAD)

• No new feedstocks (jatropha, camelina, algae, etc.) considered in the analysis

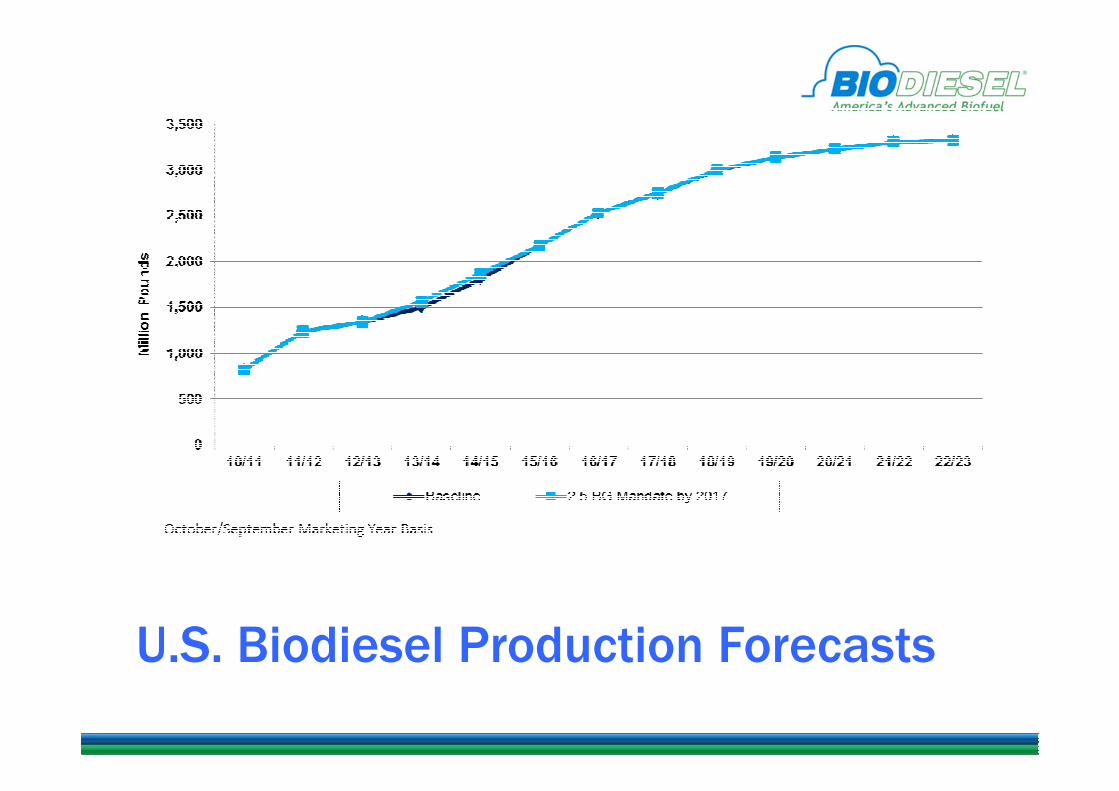

U.S. Biodiesel Production Forecasts

Report Conclusion

• “By using demonstrated yield technologies available to

farmers today in combination with consistent biofuels

policies and the DOE/EIA crude oil price forecast, biodiesel

production can reach 3.3 billion gallons by 2022. This can

be reached with growing global food demand for vegetable be reached with growing global food demand for vegetable

oils without dramatic increases in vegetable oil prices. A

modest expansion of the biodiesel mandate to 2.5 billion

gallons by 2017 would provide support for what the

industry can deliver given known feedstocks.”

U.S. Biodiesel Industry Growth in U.S. Biodiesel Industry Growth in U.S. Biodiesel Industry Growth in U.S. Biodiesel Industry Growth in

the Next Decadethe Next Decadethe Next Decadethe Next DecadeJ. Alan Weber

MARC-IV

September 30, 2011