Embed Size (px)

Citation preview

U R B I N A I G . C OM 1 3 0 1 E . B R OWA R D B LV D . S U I T E 2 6 0 � F T . L A U D E R D A L E , F L 3 3 3 0 1

9 5 4 - 6 0 6 - 0 7 3 0

BONDALERT

2/29/16 WhatInvestorsShouldKnow

Thisspecialreportwillhelpyouunderstandthecurrentenvironmentforbondsanddiscusshowthatenvironmentmaychangewithrisinginterestrates.Wewillalsodetailstrategiesinvestorsmayadopttohelpmitigatebondrisksandpotentiallyrepositiontheirportfolio.

UnderstandingBondsWH AT I N V E S T O R S S H O U L D K N OW

INTRODUCTION

Bondsaregenerallypopularwithinvestorswhoareseekingincomeandcanbeanexcellentadditiontoawell-roundedportfolioaspartofalong-term&inancialstrategy.Inrecentyears,theFederalReservehasaggressivelysoughteconomicgrowththroughbondpurchasesandultra-lowinterestratepolicies.Thesehistoricallylowinterestrateshavecreatedabullmarketforbondsissuedwithhigherstatedinterestrates.However,thesepolicieswilleventuallycometoanend,meaningbondinvestorsneedtounderstandthepotentialrisksandrewardsofholdingbondsduringaperiodofinterestrateincreases.

UnderstandingBonds

Page2

BONDBASICS

Bondsareessentiallyloansthatinvestorsmaketothebondissuer,whichcanbeacorporation,government,federalagencyorotherorganization.Asaresult,bondsarefrequentlyreferredtoasdebtsecuritiessincetheyareadebttheissuerowestoitsbondholders.Sinceinvestorswon’tlendtheirmoneywithoutcompensation,bondissuerspromisebondholdersinterestaswellasrepaymentoftheoriginalsum(thebondprincipal).Bondsarealsoknownas-ixed-incomesecuritiesbecausemanypayoutinterestatarateandintervalsetwhenthebondisissued.

Investorsmaybeattractedtobondsforseveralreasons,including:1

£ Theirincome-generatingability;

£ Capitalappreciationpotential.Positiveevents(suchasimprovementsinthecreditqualityoftheissuer,ordeclininginterestrates)canrewardinvestorswithincreasesinthemarketvalueofbonds;

£ Security.Ifacompanyisliquidated,bondholdersusuallyhavepriorityoverstockholdersinapaymentstructureandmaybemorelikelytoreceiverepayment;

£ Portfolioriskdiversi.ication.Bondscanhelpinvestorsspreadassetsacrossdifferentsegmentsofthe'inancialmarket,reducingtheirconcentrationinanysingleassetclass.2Diversi'icationcannoteliminateriskorprotectprincipalduringperiodsofwidespreadmarketdeclines.

Likeallinvestments,bondsofferabalancebetweenriskandpotentialreturn.Theriskthatconcernsmostinvestorsisthechancethattheywilllosesomeorallofthemoneytheyinvest;thereturnisthemoneyinvestorsstandtomakeontheinvestment.Thebalancebetweenriskandreturnvariesbasedontheinvestment,theentitythatissuesthesecurity,thestateoftheeconomy,largemarketmovements,andmanyotherfactors.Ingeneral,toearnhigherreturns,aninvestormusttakegreaterrisks.

Bondsaregenerallyconsideredtobelessriskythanstocksforafewreasons:3

1“TypesofBonds.”InvestinginBonds.http://www.investinginbonds.com/learnmore.asp?catid=5&subcatid=19&id=1913“WhatYouShouldKnow.”InvestinginBonds.http://www.investinginbonds.com/learnmore.asp?catid=3&id=383

CommonQuestionsAboutBondDuration

Whatisbondduration?

Durationisanumberthatmeasuresabondprice’ssensitivitytointerestrates.Thehigherabond’sduration,themoresensitiveabond’spriceistointerestratechanges.

HowcanI)indthedurationofanindividualbond?

Anumberoffactorscanaffectabond’sduration.Thesimplestwayto4indthisinformationistoaskyourinvestmentprofessionalorthebond’sissuer.Youcanalsoconsultanonlinebonddurationcalculator.

Doeslowdurationmeanlowrisk?

No.Justbecauseabond’sdurationislow,itdoesnotmeanyourinvestmentisrisk-free.Inadditiontodurationrisk,bondsaresubjecttoin1lationrisk,callrisk,defaultriskandotherriskfactors.

Whataffectsabond’sduration?

Variablessuchashowmuchinterestabondpaysduringitslifespan,thebond’scallorredemptionfeatures,yield,creditqualityoftheissuer,maturity,allplayaroleindurationcomputations.

UnderstandingBonds

Page3

£ Bondscarryanexplicitpromisetoreturnthefacevalue(principal)ofthesecuritytotheinvestoratmaturity.

£ Mostbondspromisetopayouta1ixedrateofinterestincometotheinvestor.Somestockspaydividends,butthereisnoexplicitpromisetodoso.

£ Historically,thebondmarkethasbeenlessvulnerabletopriceswingsandvolatilitythanthestockmarket.

UNDERSTANDINGBONDRISKS

Bondsplayanimportantroleinmanyportfolios,butit’simportanttounderstandthattheyaresubjecttocertaingeneralandspeci/icrisks.Whilenotexhaustive,herearesomerisksyoushouldbeawareofwheninvestinginbonds:4

Reinvestmentrisk:Wheninterestratesaredeclining,investorsmustreinvestanyinterestincomeandreturnofprincipalatlowerrates,reducingtheirinvestmentreturns.

In#lationrisk:In#lationcausesfuturedollarstobeworthlessthantoday’s.Sinceabond’sprincipaldoesnotgrowovertime,investorsriskareductioninthepurchasingpoweroffutureinterestincomeandprincipalovertime.

Marketrisk:Thisistheriskthatthebondmarketwilldeclineasawhole,bringingdownthevalueofindividualbonds,regardlessoftheirfundamentalcharacteristics.

Callrisk:Somebondscontaina“callprovision,”whichallowstheirissuerstoredeemthempriortomaturity,causinganinvestor’sprincipaltobereturnedsoonerthanexpectedandmakingthemloseoutonfutureinterestpayments.Declininginterestratesmaytriggertheredemptionofacallablebond,forcinginvestorstoreinvesttheprincipalatlowerinterestrates.

Interestraterisk:Generally,wheninterestratesrise,bondpricesfall.Conversely,wheninterestratesdecline,bondpricestypicallyrise.Investorswhosellbondspriortomaturitymaylosesomeoralloftheirprincipal.

Durationrisk:Thesensitivityofabond’spricechangesinprevailinginterestrates.Thehigherabond’sduration,themoresensitiveitspricetointerestratechanges.

Interestrateriskanddurationriskhavebecomeofparticularimportanceintoday’sultra-lowinterestrateenvironment.Currently,interestratesareathistoriclows,meaningthatthereisastronglikelihoodthatinterestratesmayriseinthefuture.

INTERESTRATESANDTHEFEDERALRESERVE

TheU.S.FederalReservehasthedualmandatetopromoteeconomicgrowthandlowunemploymentwhilemaintainingpricestability(asmeasuredbythein5lationrate.)Oneofthemostpowerfultoolsin4ibid.

UnderstandingBonds

Page4

theFed’sarsenalisitsabilitytosetthe“federalfundsrate,”whichistheratedepositoryinstitutionslendmoneytoeachother.Thisrateeffectivelysetsallotherinterestratesusedinbankingactivity,includingtheissuanceofbonds.

Inordertoboosteconomicactivityafterthe/inancialcrisis,theFedloweredthefederalfundsratetonearlyzero.Whenthisfailedtostimulatesustainedeconomicgrowth,theFedtookahistoricstepandembarkedonaseriesof“quantitativeeasing”programs,purchasingbothTreasurySecuritiesandMortgage-BackedSecuritiesinordertopushlong-terminterestrateslowerandsupport0inancialmarkets.QE3,thelatestroundofquantitativeeasing,targeted$85billioninmonthlygovernmentbondandmortgage-backedsecuritypurchases.Thesepurchasesaredesignedtoincreasedemandforthesebonds,pushingbondpricesupandinterestratesdown,boostingeconomicactivity.

Atsomepointinthefuture,theFedwillhavetoexitthesequantitativeeasingprogramsandbeginsellingofftheiraccumulatedbonds.Thepaceandtimingofthesesales,aswellasthetaperingoftheFed’saccommodativemonetarypolicywillaffectbondmarketsandbondinvestors.Asthequantitativeeasingprogramscometoanend,demandforbondsisexpectedtodrop,potentiallyresultinginadecreaseinbondvaluesandanincreaseinbondyields.Astheeconomyshowssustainedimprovement,theFedisalsoexpectedtoraiseinterestrates,pushingbondpricesstilllower.

UnderstandingBonds

Page5

THERELATIONSHIPBETWEENBONDVALUESANDINTERESTRATES

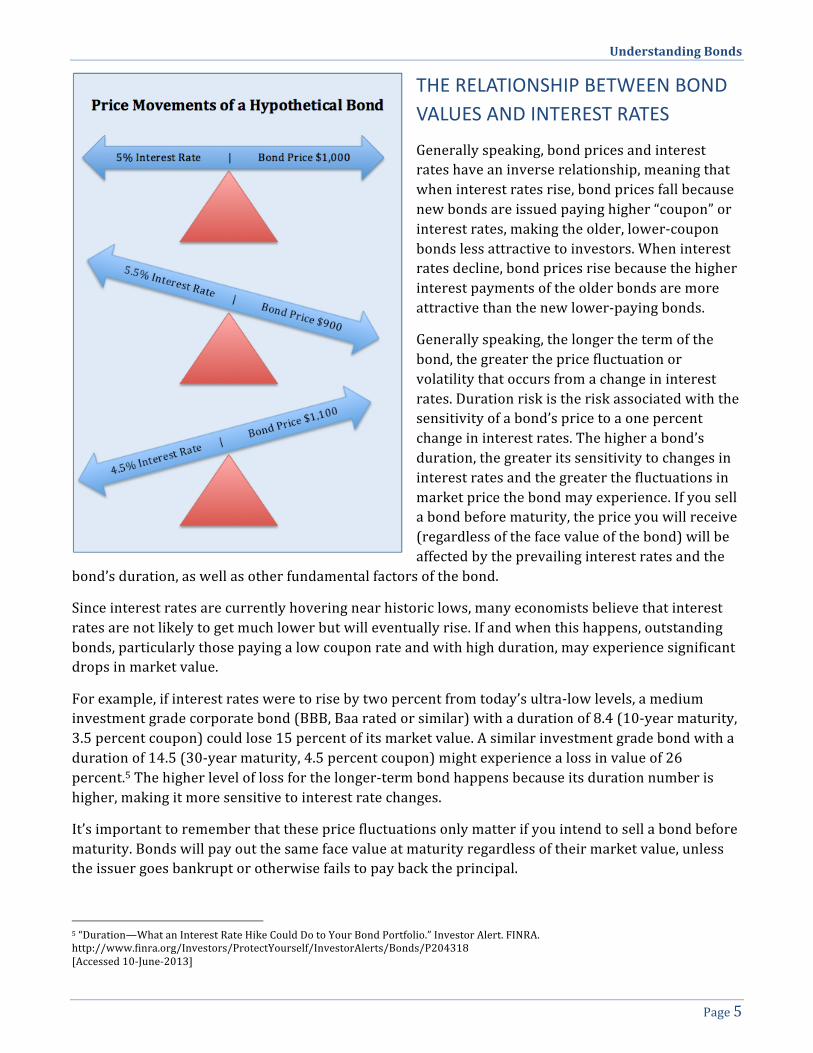

Generallyspeaking,bondpricesandinterestrateshaveaninverserelationship,meaningthatwheninterestratesrise,bondpricesfallbecausenewbondsareissuedpayinghigher“coupon”orinterestrates,makingtheolder,lower-couponbondslessattractivetoinvestors.Wheninterestratesdecline,bondpricesrisebecausethehigherinterestpaymentsoftheolderbondsaremoreattractivethanthenewlower-payingbonds.

Generallyspeaking,thelongerthetermofthebond,thegreatertheprice-luctuationorvolatilitythatoccursfromachangeininterestrates.Durationriskistheriskassociatedwiththesensitivityofabond’spricetoaonepercentchangeininterestrates.Thehigherabond’sduration,thegreateritssensitivitytochangesininterestratesandthegreaterthe,luctuationsinmarketpricethebondmayexperience.Ifyousellabondbeforematurity,thepriceyouwillreceive(regardlessofthefacevalueofthebond)willbeaffectedbytheprevailinginterestratesandthe

bond’sduration,aswellasotherfundamentalfactorsofthebond.

Sinceinterestratesarecurrentlyhoveringnearhistoriclows,manyeconomistsbelievethatinterestratesarenotlikelytogetmuchlowerbutwilleventuallyrise.Ifandwhenthishappens,outstandingbonds,particularlythosepayingalowcouponrateandwithhighduration,mayexperiencesigni7icantdropsinmarketvalue.

Forexample,ifinterestratesweretorisebytwopercentfromtoday’sultra-lowlevels,amediuminvestmentgradecorporatebond(BBB,Baaratedorsimilar)withadurationof8.4(10-yearmaturity,3.5percentcoupon)couldlose15percentofitsmarketvalue.Asimilarinvestmentgradebondwithadurationof14.5(30-yearmaturity,4.5percentcoupon)mightexperiencealossinvalueof26percent.5Thehigherleveloflossforthelonger-termbondhappensbecauseitsdurationnumberishigher,makingitmoresensitivetointerestratechanges.

It’simportanttorememberthattheseprice1luctuationsonlymatterifyouintendtosellabondbeforematurity.Bondswillpayoutthesamefacevalueatmaturityregardlessoftheirmarketvalue,unlesstheissuergoesbankruptorotherwisefailstopaybacktheprincipal.

5“Duration—WhatanInterestRateHikeCouldDotoYourBondPortfolio.”InvestorAlert.FINRA.http://www.(inra.org/Investors/ProtectYourself/InvestorAlerts/Bonds/P204318[Accessed10-June-2013]

UnderstandingBonds

Page6

STRATEGIESTOHELPMITIGATERISKIt’snotpossibletocompletelyeliminateinvestmentrisks,however,therearestrategieswecanemploytohelpreducetheimpactofcertainrisks.Whilefutureincreasesininterestratesposede3initeriskstobondinvestors,thecorrectsolutionmaynotbetoabandonthebondmarket;rather,investorsshouldseekoutsolutionsthathelpthempreparetheirportfoliosforrisinginterestrates.Indeed,risingratescanbepositiveforinvestorssincetheymayincreasetheavailabilityofhighquality,high-yieldbonds.

Oneofthestrongesttoolsinourarsenalisapersonalizedinvestmentstrategythatisneveronautopilot.Atanygiventime,therearemanyvariablesthatcanaffectthevalueofyourportfolioandweareconstantlyworkingtobalancereturnagainstrisk.Someofthestrategiesweemployinclude:

“Laddering”bonds,astrategyinwhichinvestorsbuybondswithdifferent,evenlyspacedmaturitiescanhelpreducetheeffectofrisinginterestratesonyouroverallbondportfolio.

Reducingmaturitiesthroughsellinglongerdurationbondsandbuyingshorterdurationdebtsecuritiescanhavetheeffectofreducingdurationandreducingyourportfolio’ssensitivitytointerestratechanges.

HoldinginternationalbondsfromcountrieswhereinterestratesarehigherthanintheU.S.canincreasebondyieldsandhelpreducedurations.However,ifconsideringthisstrategy,youmustbemindfulthatinternationalinvestingpresentsitsownuniquerisks,suchascurrency!luctuations,politicalrisks,anddifferencesinaccountingprocedures.

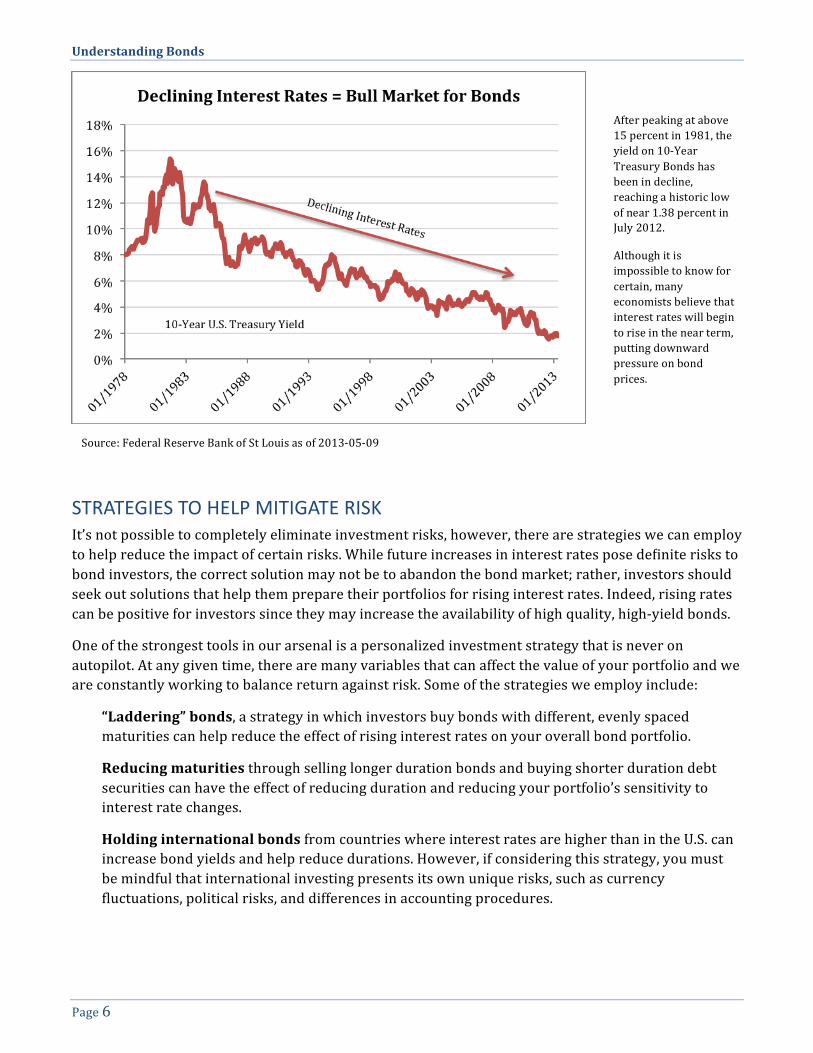

Afterpeakingatabove15percentin1981,theyieldon10-YearTreasuryBondshasbeenindecline,reachingahistoriclowofnear1.38percentinJuly2012.

Althoughitisimpossibletoknowforcertain,manyeconomistsbelievethatinterestrateswillbegintoriseinthenearterm,puttingdownwardpressureonbondprices.

Source:FederalReserveBankofStLouisasof2013-05-09

UnderstandingBonds

Page7

Buyingin(lation-adjustedsecuritiessuchasTreasuryInvestmentProtectedSecurities(TIPS),whosepayoutsareadjustedaccordingtotherateofin4lationcanhelptoreduceduration.Thisassumesthattherateofin.lationrisesinconcurrencewithanincreaseininterestrates,thustriggeringanincreaseinthepayoutrateofthebond.

Investorscanalsolookbeyondthebondmarketforopportunitiestoearnhigherratesofreturn.

Holdingdividend-payingstockscanofferanincomestreamthatmayincreaseovertimeascompaniesincreasedividendpayments.Stocksoffergrowthpotentialovertimethatcanhelp!ighttheeffectsofin!lation.Theseadvantagesshouldbebalancedagainstthepotentiallyhighervolatilityofequityinvestments.

Pursuingalternativeinvestmentstrategiesthatmayhavetheabilitytohedgeagainstrisinginterestratesorearnahigherreturninarisingrateenvironment.Ifyouhavequestionsaboutthesestrategies,pleasecontactus.

CONCLUSIONS&NEXTSTEPSWehopethatyou’vefoundthisspecialreportinformative,educational,andreassuring.Wefeelthatitisimportanttoeducateourclientsaboutthepotentialrisksandbene'itsofbondinvesting.However,havingsaidthat,wecertainlydon’tplantoabandon'ixedincomeinvestmentsshouldinterestratesincrease.Rather,weplantocontinuetomonitormarketsandseekouttheopportunitiesthatrisinginterestratesmaysendourway.

As$inancialguidesforourclients,weworkhardtoachieveresultswhilechartingacoursethroughshiftingeconomicconditions.Wealsowanttoofferourselvesasaresourcetoyou,yourfamily,andyourfriends.Wearehappytoanswerquestionsaboutyourcurrent4inancialsituationandfuturegoals,andweoffercomplimentaryconsultationsatanytime.Shouldyouhaveanyquestionsaboutbondinvestingormarketmovements,pleasereachout.Wewouldbedelightedtobeofservice.

Sincerely,

Christian Urbina

ChristianUrbina

President &CIO

UnderstandingBonds

Page8

Footnotes,disclosuresandsources:SecuritiesofferedthroughCapitalGuardian,LLC,memberFINRA/SIPC.InvestmentAdvisoryServicesofferedthroughCapitalGuardianWealthManagement,anSECregisteredInvestmentAdvisor.SecuritiesProductsarenotFDICinsured,arenotbankguaranteed,andmaylosevalue.

Opinions,estimates,forecastsandstatementsof.inancialmarkettrendsthatarebasedoncurrentmarketconditionsconstituteourjudgmentandaresubjecttochangewithoutnotice.

Thismaterialisforinformationpurposesonlyandisnotintendedasanofferorsolicitationwithrespecttothepurchaseorsaleofanysecurity.

Investinginvolvesriskincludingthepotentiallossofprincipal.Noinvestmentstrategycanguaranteeapro9itorprotectagainstlossinperiodsofdecliningvalues.

Fixedincomeinvestmentsaresubjecttovariousrisksincludingchangesininterestrates,creditquality,in7lationrisk,marketvaluations,prepayments,corporateevents,taxrami1icationsandotherfactors.

Opinionsexpressedarenotintendedasinvestmentadviceortopredictfutureperformance.

Pastperformancedoesnotguaranteefutureresults.

Consultyour+inancialprofessionalbeforemakinganyinvestmentdecision.

Opinionsexpressedaresubjecttochangewithoutnoticeandarenotintendedasinvestmentadviceortopredictfutureperformance.Allinformationisbelievedtobefromreliablesources;however,wemakenorepresentationastoitscompletenessoraccuracy.Pleaseconsultyour+inancialadvisorforfurtherinformation.

Investmentsinstocksinvolverisksincludinglossofentireprincipal.

Whilemanysecuritiesaimtoprovidestabledividends,dividendpaymentsaredependentonvariousfactorssuchasmarketconditionsandarenotguaranteed.Italsomaybediscontinuedormodi4iedatanytime.ThesearetheviewsofPlatinumAdvisorMarketingStrategies,LLC,andnotnecessarilythoseofthenamedrepresentative,BrokerdealerorInvestmentAdvisor,andshouldnotbeconstruedasinvestmentadvice.NeitherthenamedrepresentativenorthenamedBrokerdealerorInvestmentAdvisorgivestaxorlegaladvice.Allinformationisbelievedtobefromreliablesources;however,wemakenorepresentationastoitscompletenessoraccuracy.Pleaseconsultyour2inancialadvisorforfurtherinformation.

Byclickingonthelinks,youwillleaveourserver,astheyarelocatedonanotherserver.Wehavenotindependentlyveri7iedtheinformationavailablethroughthislink.Thelinkisprovidedtoyouasamatterofinterest.