Embed Size (px)

Citation preview

6/15/2021

1

© SASB

Update on SASB and the ESG Reporting LandscapePresentation for SCCE ESG and Compliance Conference

Neil Stewart, Director of Corporate Outreach; [email protected]

June 17, 2021

77 industry-specific disclosure standards

Used by companies and investors globally

SASB Standards connect businesses and investors on the financial impacts of sustainability

The Value Reporting Foundation and SASB StandardsNon-profit standards-setting organization for financially material ESG information

6/17/2021 © SASB2

1

2

6/15/2021

2

A major advancement towards building a comprehensive and

holistic reporting system.

Introducing the Value Reporting FoundationSASB and the IIRC have merged

6/17/2021 © SASB3

• Simplify the field• Globalize both organizations• Support the needs of investors and other

stakeholders• Focus on reporting as a means to changing

behaviour• Achieve interoperability with the GRI

standards• Advance the adoption of integrated

reporting and integrated thinking• Accelerate progress towards a

comprehensive corporate reporting system.

The merger of IIRC and SASB will:

Investor DemandTargeted Calls from Large Asset Managers for SASB Disclosure

6/17/2021 © SASB4

“…This year, we are asking the companies that we invest in on behalf of our clients to: (1) publish a disclosure in line with industry-specific SASB guidelines by year-end…”

“…leveraging the Sustainability Accounting Standards Board (SASB) materiality framework, R-Factor … allows us to evaluate a company’s performance against both regional and global industry peers …

Source: Morrow Sodali 2020 Institutional Investor Survey

“As a starting point companies can report industry specific SASB metrics to account for financially material risks and opportunities…”

3

4

6/15/2021

3

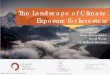

Momentum: International Investor Support for SASB StandardsDramatic increase in investors around the world using and licensing the SASB standards, representing $70T+ in AUM

© SASB

Investor Supporters# of SASB Alliance/Investor Advisory Group Members and Licensees

# of Countries Represented 9 146 22

Updated March 2021

207 firms in

22 countries with

$70T+ AUM

-25

25

75

125

175

225

2017 2018 2019 2020 YTD 2021

21

6/17/20215

X

x

• ISS Climate International

• Luxembourg Stock Exchanges

• Morgan Stanley Investment Management

• Neuberger Berman

• Northern Trust Investments

• PCJ Investment Council

• Pensions and Lifetime Savings Association

• QMA

• SSgA Funds Management

• T Rowe Price

• Aberdeen Standard Investments

• Aviva Investors

• BCI Investments

• BlackRock

• Calvert Research & Management

• Capital Group

• Columbia Threadneedle

• CPP Investments

• Dimensional Investing

• Goldman Sachs Asset Management

Growing Number of Investor Policy Guidelines Call for SASB DisclosureAt least 30 stewardship, proxy voting, and/or policy guidelines reference SASB, often along with TCFD

6/17/2021 © SASB6

5

6

6/15/2021

4

Use of SASB Standards by businesses

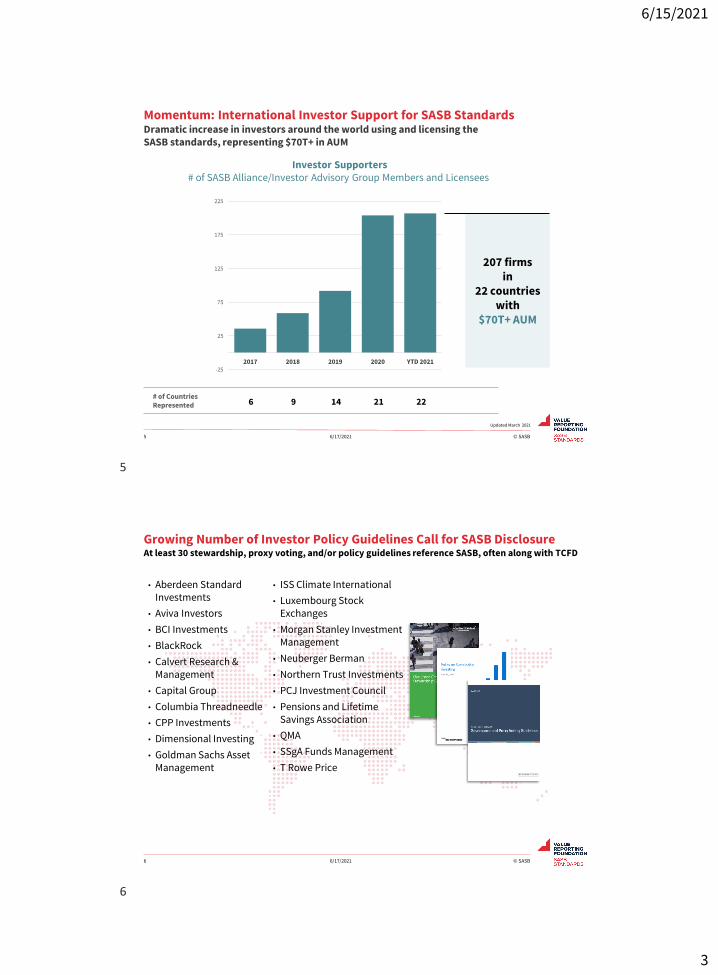

Corporate Adoption of SASB Standards in the U.S.

Source: ‘Telling all: Regulators want firms to own up to climate risks’. The Economist, March 13, 2021 edition

6/17/2021 © SASB8

7

8

6/15/2021

5

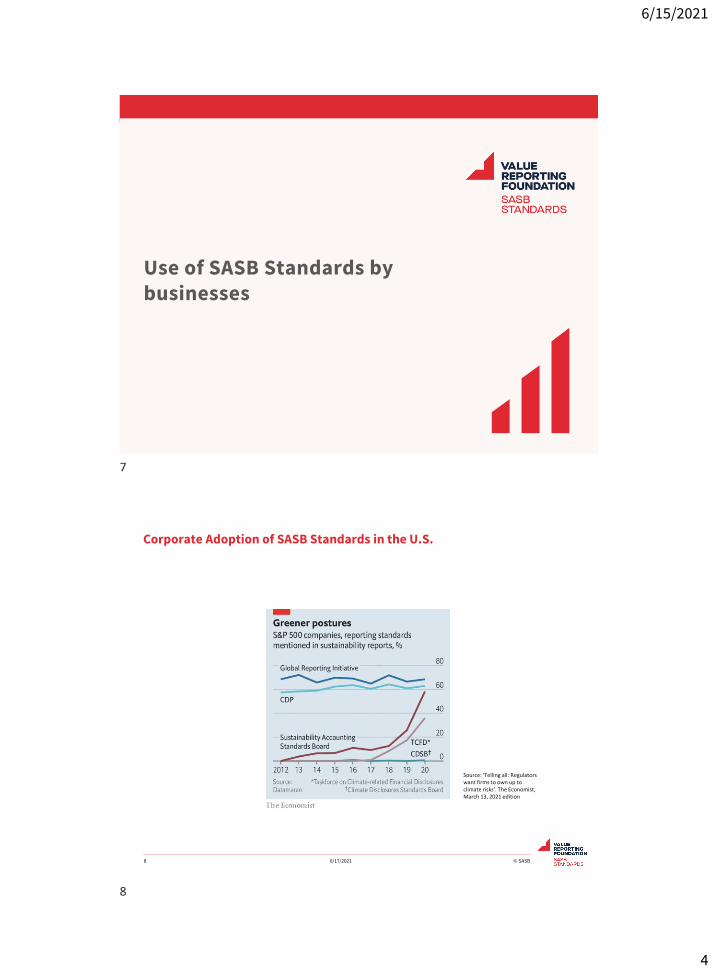

More Than 1,030 SASB Reporters World-wide – as of end of May 2021More than half of the S&P 500 and one third of the S&P Global 1200 are reporters

6/17/2021 © SASB9

Examples:

Complete list: https://www.sasb.org/company-use/

SASB Reporters since 2019

U.S.50%

International50%

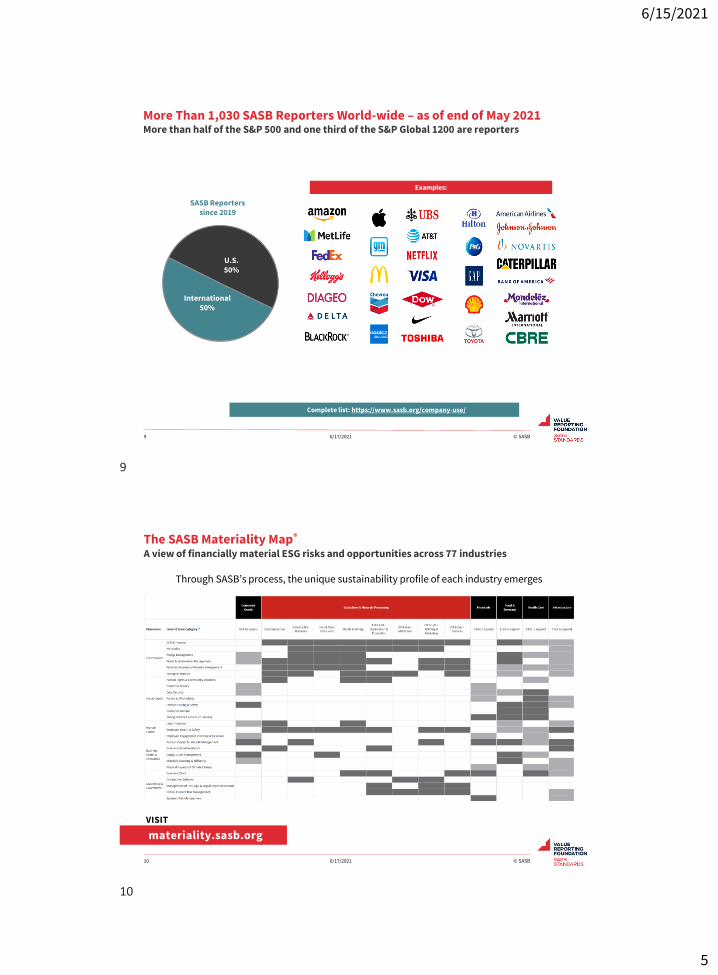

The SASB Materiality Map®

A view of financially material ESG risks and opportunities across 77 industries

6/17/2021 © SASB10

materiality.sasb.org

VISIT

Through SASB’s process, the unique sustainability profile of each industry emerges

9

10

6/15/2021

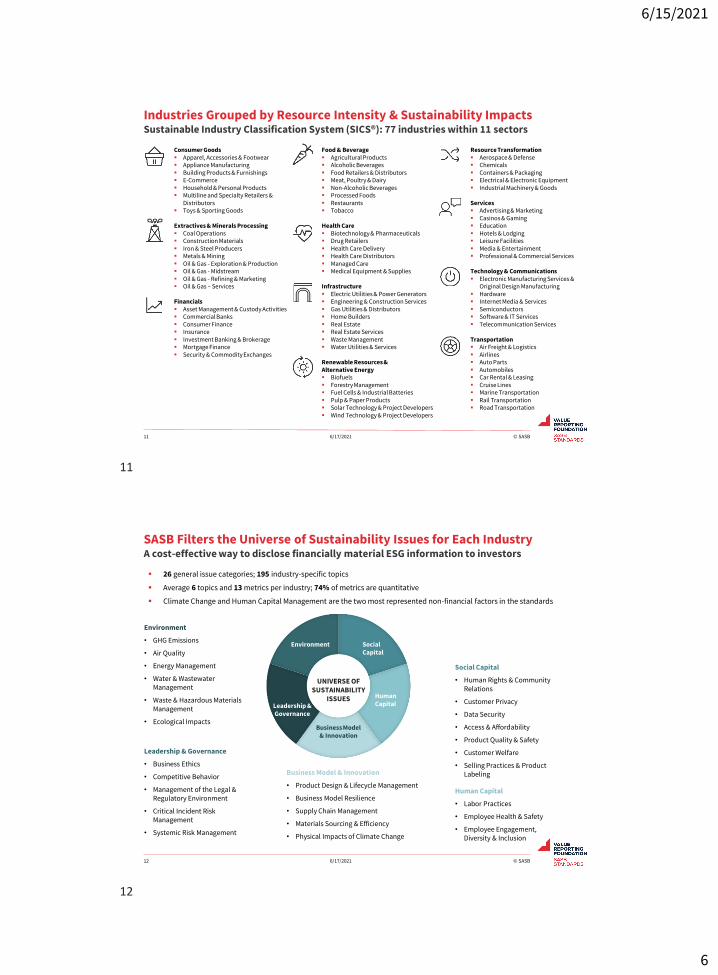

6

Consumer Goods▪ Apparel, Accessories & Footwear▪ Appliance Manufacturing▪ Building Products & Furnishings▪ E-Commerce▪ Household & Personal Products▪ Multiline and Specialty Retailers &

Distributors▪ Toys & Sporting Goods

Extractives & Minerals Processing▪ Coal Operations▪ Construction Materials▪ Iron & Steel Producers▪ Metals & Mining▪ Oil & Gas - Exploration & Production▪ Oil & Gas - Midstream▪ Oil & Gas - Refining & Marketing▪ Oil & Gas – Services

Financials▪ Asset Management & Custody Activities▪ Commercial Banks▪ Consumer Finance▪ Insurance▪ Investment Banking & Brokerage▪ Mortgage Finance▪ Security & Commodity Exchanges

Food & Beverage▪ Agricultural Products▪ Alcoholic Beverages▪ Food Retailers & Distributors▪ Meat, Poultry & Dairy▪ Non-Alcoholic Beverages▪ Processed Foods▪ Restaurants▪ Tobacco

Health Care▪ Biotechnology & Pharmaceuticals▪ Drug Retailers▪ Health Care Delivery▪ Health Care Distributors▪ Managed Care▪ Medical Equipment & Supplies

Infrastructure▪ Electric Utilities & Power Generators▪ Engineering & Construction Services▪ Gas Utilities & Distributors▪ Home Builders▪ Real Estate▪ Real Estate Services▪ Waste Management▪ Water Utilities & Services

Renewable Resources & Alternative Energy▪ Biofuels▪ Forestry Management▪ Fuel Cells & Industrial Batteries▪ Pulp & Paper Products▪ Solar Technology & Project Developers▪ Wind Technology & Project Developers

Resource Transformation▪ Aerospace & Defense▪ Chemicals▪ Containers & Packaging ▪ Electrical & Electronic Equipment▪ Industrial Machinery & Goods

Services▪ Advertising & Marketing▪ Casinos & Gaming▪ Education▪ Hotels & Lodging▪ Leisure Facilities▪ Media & Entertainment▪ Professional & Commercial Services

Technology & Communications▪ Electronic Manufacturing Services &

Original Design Manufacturing▪ Hardware▪ Internet Media & Services▪ Semiconductors▪ Software & IT Services▪ Telecommunication Services

Transportation▪ Air Freight & Logistics▪ Airlines▪ Auto Parts▪ Automobiles▪ Car Rental & Leasing▪ Cruise Lines▪ Marine Transportation▪ Rail Transportation▪ Road Transportation

Industries Grouped by Resource Intensity & Sustainability ImpactsSustainable Industry Classification System (SICS®): 77 industries within 11 sectors

6/17/2021 © SASB11

SASB Filters the Universe of Sustainability Issues for Each IndustryA cost-effective way to disclose financially material ESG information to investors

6/17/2021 © SASB12

▪ 26 general issue categories; 195 industry-specific topics

▪ Average 6 topics and 13 metrics per industry; 74% of metrics are quantitative

▪ Climate Change and Human Capital Management are the two most represented non-financial factors in the standards

Environment

• GHG Emissions

• Air Quality

• Energy Management

• Water & Wastewater Management

• Waste & Hazardous Materials Management

• Ecological Impacts

Leadership & Governance

• Business Ethics

• Competitive Behavior

• Management of the Legal & Regulatory Environment

• Critical Incident Risk Management

• Systemic Risk Management

Social Capital

• Human Rights & Community Relations

• Customer Privacy

• Data Security

• Access & Affordability

• Product Quality & Safety

• Customer Welfare

• Selling Practices & Product Labeling

Human Capital

• Labor Practices

• Employee Health & Safety

• Employee Engagement, Diversity & Inclusion

Business Model & Innovation

Social Capital

Human CapitalLeadership &

Governance

Environment

UNIVERSE OF SUSTAINABILITY

ISSUES

• Product Design & Lifecycle Management

• Business Model Resilience

• Supply Chain Management

• Materials Sourcing & Efficiency

• Physical Impacts of Climate Change

11

12

6/15/2021

7

SASB metrics are aligned with more than 200 existing frameworks, regulations, and certifications

SASB standards average 6 topics and 13 metrics (74 percent quantitative) per industry

Efficient and Cost-Effective for BusinessesSASB provides a cost-effective way to report on financially material ESG topics

6/17/2021 © SASB13

Standalone SASB Report Regulatory Filing Integrated Report

Excel Download

sasb.org/company-use/sasb-reporters/

SASB Table or Index

Reporting Channel is Determined by the Reporting CompanySASB-reporting companies use a variety of different channels and formats

6/17/2021 © SASB14

13

14

6/15/2021

8

SASB Reporters: Most Common Use CaseSASB table in a sustainability report or standalone

6/17/2021 © SASB15

Towards a global system of comprehensive corporate reporting

15

16

6/15/2021

9

A Shifting Landscape Key players in the move towards a comprehensive system of corporate reporting

• The European Commission announced intent to develop European non-financial reporting standards with focus on ‘double materiality’. Legislative proposal for Corporate Sustainability Reporting Directive (CSRD) published April 21, 2021

• The United States Securities and Exchange Commission has launched a consultation on climate change disclosure and is evaluating the development of a rule to drive climate-risk and/or broader ESG reporting

• IFRS Foundation Trustees announced expectations to establish Sustainability Standards Board. SASB will sit on a technical working group, along with IIRC, TCFD, CDSB and WEF. A roadmap and timeline for the SSB will be launched in September 2021

• IOSCO has established a Technical Experts Group chaired by the US SEC and the Monetary Authority of Singapore to assess the IFRS effort to establish a Sustainability Standards Board and evaluate the Prototype Climate Standard developed by the “Group of 5” private sector frameworks and standards-setters.

• WEF IBC Stakeholder Capitalism Metrics Project has proposed 21 cross-industry metrics to demonstrate company contribution to the SDGs, along with calling for a global system of standards. WEF is publicly supporting the IFRS effort.

• “Group of Five” private sector frameworks and standards-setters articulate a vision for a comprehensive corporate reporting system and offer to provide technical support to IFRS and the European Commission.

6/17/2021 © SASB17

SASB’s Comment Letter on Climate-related Disclosure

• Simplifying the Landscape: A Common Structure for Sustainability Disclosure Leveraging Existing Frameworks and Standards

• Disclosure Location and Reliability • International Considerations

6/17/2021 © SASB18

17

18

6/15/2021

10

IFRS Foundation is Evaluating its Role in Sustainability ReportingRoadmap and timeline for global Sustainability Standards Board expected in Sept. 2021

▪ IFRS Foundation has announced its strategic direction for a Sustainability Standards Board (SSB).

▪ Focus on enterprise value creation and on the information needs of investors, lenders, and other creditors.

▪ Committed to a building block approach that enables both global comparability and regional specificity.

▪ The new SSB will initially focus its efforts on climate-related reporting then expand to a holistic view of ESG.

▪ Considering the “group of five’s” prototype climate standard as a starting point.

6/17/2021 © SASB19

Governance & internal controls for ESG reporting

19

20

6/15/2021

11

Assess

Respond

Monitor

Report

Identify

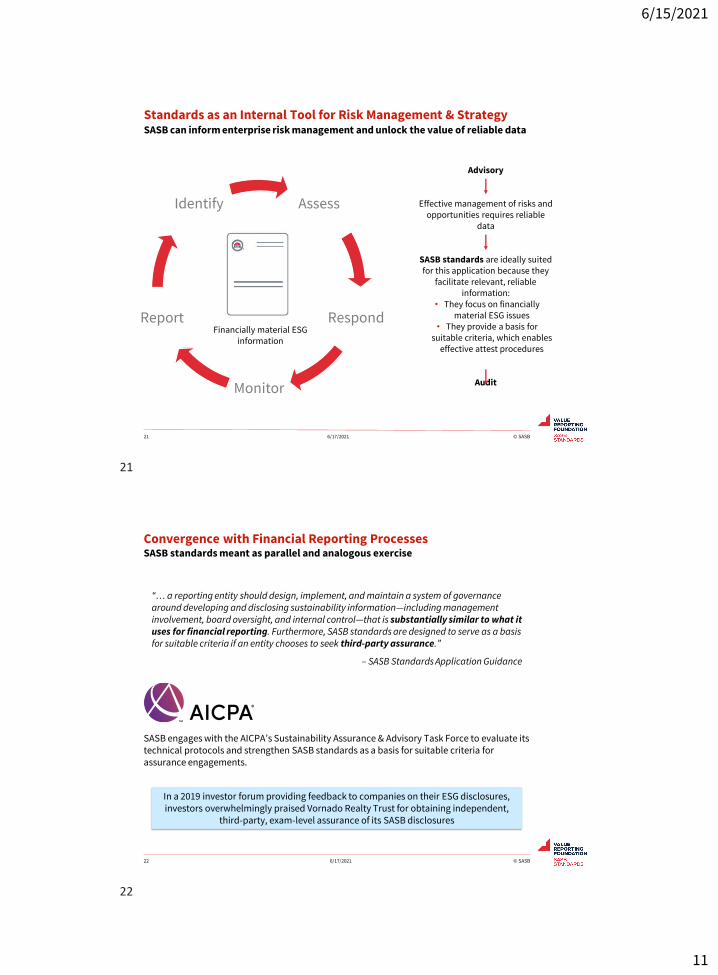

Standards as an Internal Tool for Risk Management & StrategySASB can inform enterprise risk management and unlock the value of reliable data

21 © SASB

Financially material ESG information

Advisory

Effective management of risks and opportunities requires reliable

data

SASB standards are ideally suited for this application because they

facilitate relevant, reliable information:

• They focus on financially material ESG issues

• They provide a basis for suitable criteria, which enables

effective attest procedures

Audit

6/17/2021

“… a reporting entity should design, implement, and maintain a system of governance around developing and disclosing sustainability information—including management involvement, board oversight, and internal control—that is substantially similar to what it uses for financial reporting. Furthermore, SASB standards are designed to serve as a basis for suitable criteria if an entity chooses to seek third-party assurance.”

– SASB Standards Application Guidance

© SASB22

Convergence with Financial Reporting ProcessesSASB standards meant as parallel and analogous exercise

In a 2019 investor forum providing feedback to companies on their ESG disclosures, investors overwhelmingly praised Vornado Realty Trust for obtaining independent,

third-party, exam-level assurance of its SASB disclosures

SASB engages with the AICPA’s Sustainability Assurance & Advisory Task Force to evaluate its technical protocols and strengthen SASB standards as a basis for suitable criteria for assurance engagements.

6/17/2021

21

22

6/15/2021

12

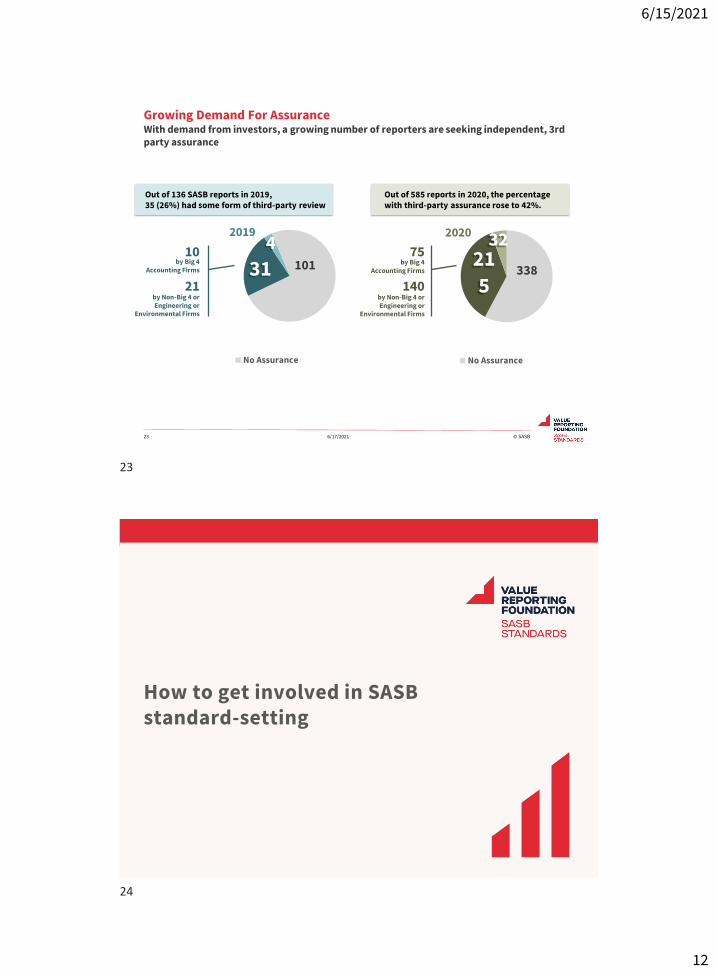

Growing Demand For AssuranceWith demand from investors, a growing number of reporters are seeking independent, 3rd party assurance

© SASB23 6/17/2021

by Non-Big 4 or Engineering or

Environmental Firms

by Big 4 Accounting Firms 338

21

5

322020

No Assurance

10131

42019

No Assurance

by Non-Big 4 or Engineering or

Environmental Firms

by Big 4 Accounting Firms

Out of 136 SASB reports in 2019, 35 (26%) had some form of third-party review

Out of 585 reports in 2020, the percentage with third-party assurance rose to 42%.

10

21

75

140

How to get involved in SASB standard-setting

23

24

6/15/2021

13

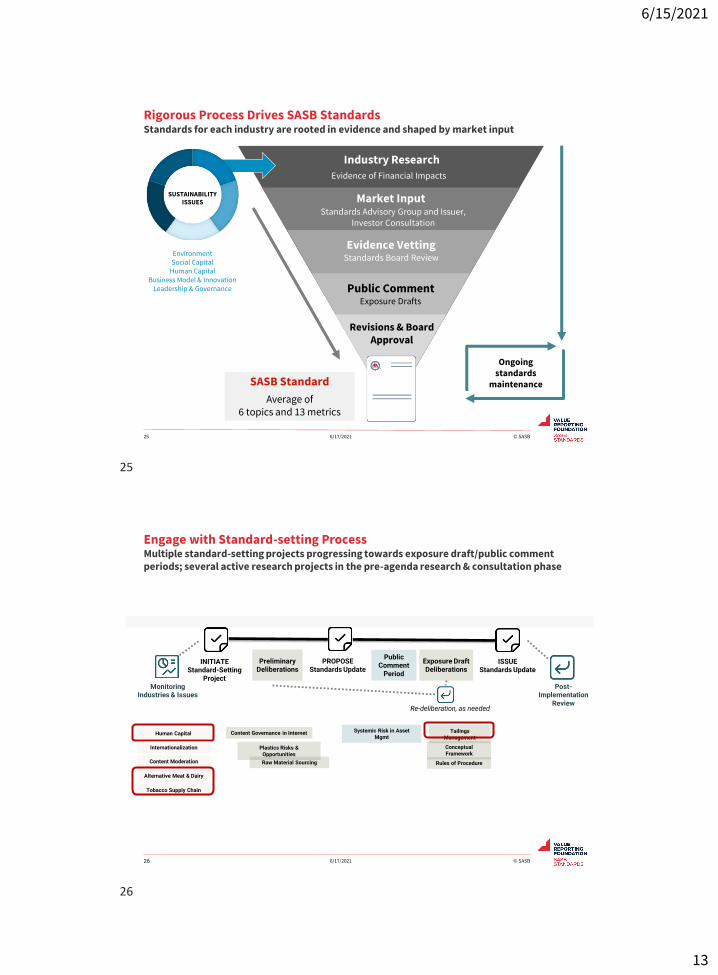

Rigorous Process Drives SASB StandardsStandards for each industry are rooted in evidence and shaped by market input

6/17/2021 © SASB25

UNIVERSE OF ESG

ISSUESSUSTAINABILITY

ISSUES

Industry Research

Market Input

Evidence VettingStandards Board Review

Public Comment

Revisions & Board Approval

SASB Standard

Average of 6 topics and 13 metrics

Ongoing standards

maintenance

Standards Advisory Group and Issuer, Investor Consultation

Evidence of Financial Impacts

Exposure Drafts

EnvironmentSocial Capital

Human CapitalBusiness Model & Innovation

Leadership & Governance

Re-deliberation, as needed

INITIATE Standard-Setting

Project

ISSUE Standards Update

PROPOSE Standards Update

Monitoring Industries & Issues

Preliminary Deliberations

Public Comment

Period

Post-Implementation

Review

Exposure Draft Deliberations

Engage with Standard-setting ProcessMultiple standard-setting projects progressing towards exposure draft/public comment periods; several active research projects in the pre-agenda research & consultation phase

Conceptual Framework

Tailings Management

Plastics Risks & Opportunities

Systemic Risk in Asset Mgmt

Raw Material Sourcing Rules of Procedure

Content Governance in InternetHuman Capital

Tobacco Supply Chain

Alternative Meat & Dairy

Internationalization

Content Moderation

26 6/17/2021 © SASB

25

26

6/15/2021

14

Commitment to Market Feedback, Transparency, and EngagementSignificant advancements to solicit market feedback on the Standards

6/17/2021 © SASB27

12

3

sasb.org/standards/process/active-projects/

VISIT

SASB AllianceMembership for Individuals and Organizations Who Benefit from a Market Standard

sasb.org/alliance

MEMBERS JOIN SASB ALLIANCE TO

EXPLORE BEST PRACTICES TO INTEGRATE ESG INFORMATION

SUPPORT A STANDARD TO BENEFIT THE MARKET

Organizational Membership

• Exclusive convenings

• Engage with SASB leadership

• Educational resources

• More

Individual Membership

• Latest research

• $700 in discounts

• Annual member reception

“The SASB Alliance makes it easier for me to tapinto the wealth of resources that SASB hascreated, which strengthens my ability to offerleading and value-creating ESG integrationservices to companies and investors.”

MARIE-JOSÉE PRIVYK, CFA, SIPC

SASB Alliance Individual Member

MEMBERS INCLUDE:

6/17/2021 © SASB28

27

28

6/15/2021

15

29