Embed Size (px)

Citation preview

Filing Information: August 2013, IDC #242291, Volume: 1

Global Sourcing Strategies: Update

U P D A T E

E n g i n e e r i n g S e r v i c e s 2 . 0 : I n C o n v e r s a t i o n w i t h S a n d e e p K i s h o r e , H C L T e c h n o l o g i e s

Mukesh Dialani

I N T H I S U P D A T E

This IDC update presents the details of a conversation IDC had with Sandeep Kishore

(SK), who heads the Engineering and R&D Services (ERS) Practice at HCL

Technologies. IDC reached out to Sandeep to get his views and perspective on the

evolution and growth of engineering services. Through various leadership roles and

initiatives, he has seen these services evolve and grow to a $800+ million business at

HCL Technologies, and his responses to IDC's questions bear testimony to his and the

company's experience and thought leadership as they pertain to engineering services.

For many years, technology product companies across automotive, aerospace,

defense, medical, consumer, and other industries have managed to run an efficient

in-house operation, creating innovative new products and taking them to market.

However, in recent times they are being challenged by business issues such as talent

shortages, shrinking product life cycles, R&D budget challenges, increasing product

convergence, and so forth. This situation has inhibited their ability to focus on their

core competency, which is to create new innovative products for their customers. In

their quest to stay competitive, they have found an ally in R&D/product engineering

services providers that have in the past decade invested in building infrastructure to

service their customers' services needs.

The conversation and commentary that follow provide insight into the current state of

the engineering services market and HCL Technologies' strategy to build the

company's service offering as HCL partners with its customers' existing product

management and new product development initiatives. Technology product

companies can leverage the insights in this discussion and reach out to engineering

services providers for their product management/development needs.

Glo

bal H

eadquart

ers

: 5 S

peen S

treet F

ram

ingham

, M

A 0

1701 U

SA

P

.508.8

72.8

200 F

.508.9

35.4

015 w

ww

.idc.

com

2 #242291 ©2013 IDC

Q u e s t i o n s a n d A n s w e r s

IDC: What is your opinion about the evolution of engineering services? Where

in its life cycle does it stand today? Why?

SK: The global engineering services industry is evolving at a great pace right now.

Even though the industry itself is in its initial phases of maturity, the headroom for

growth is high, guided by disruptive changes in business and technology and

opportunities getting created at the intersection of technology convergence.

Today, the market is witnessing what we call Engineering Services 2.0, wherein

engineering service providers are being called on to play a critical role in their

technology customers' businesses. They are becoming true partners to customers in

their product development process by taking joint ownership of their customers'

products and associated ecosystems. In some cases, the provider's financial

business model is tied to the success associated with the customer's product in the

global market.

From a market perspective, global R&D investments are expected to increase in

absolute terms; they are expected to be in the range of remaining flat to moderately

declining as a percentage of the customer's product revenue over the decade.

Additionally, the convergence of industries and technologies is expected to drive

companies to launch their products faster and align to a highly connected world that

provides a great user experience across product categories, be it consumer or

industrial. Going forward, technology companies will need to drive significantly higher

effectiveness in their product and development processes and leverage the partner

ecosystem more than ever before.

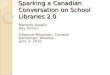

In light of the this current state of affairs, engineering services have come a long way

(see Figure 1) since their emergence over two decades ago, when it was largely a

staff augmentation delivery model from low-cost regions through tactical project-

based engagements. This included either development of noncore products or largely

sustenance-/life-cycle extension–based engagements for the more mature ones.

From an industry standpoint, these services witnessed some early adopters across

the semiconductor, telecom, software, automotive, and aerospace industries. They

are currently moving rapidly toward maturity, and industries such as medical,

industrial, and consumer are joining the fold.

As the engineering services industry moves into its next phase by consolidating and

building on its base, key success criteria will include product management, domain

expertise, the ability to deliver onsite services, newer business/delivery models, and

so forth.

©2013 IDC #242291 3

F I G U R E 1

T h e E v o l u t i o n o f E n g i n e e r i n g S e r v i c e s

Source: IDC, 2013

IDC: What is the timeline for these services to mature? Will customers ever

outsource their core products/engineering capabilities? If yes, what change is

required to accomplish this?

SK: It is a process driven by fast-changing end-customer needs, rapidly changing

technologies, and quick time to market in a globally competitive marketplace. These

are the most important considerations that we see driving this business. As I

mentioned earlier, the engineering services market is in initial phases of maturity, with

headroom for growth over the decade. This growth will depend on how new service

providers emerge and existing engineering services providers mature in terms of their

offerings, domain-specific solutions, business model alignment, and how much of a

true partner they become for their global customers. At the same time, product

companies also need to develop the necessary processes to integrate their

engineering services partners more closely into a true globally distributed product

development process. Given the confluence of shortening product life cycles, global

competition, and the convergence of industries, it is practically impossible to try and

have a closed system of engineering development. Partnerships are critical to

success, and most global companies are leveraging this strategy in some manner.

On the subject of core and noncore, many product companies are already

outsourcing what they consider is core to them. This partnership, however, requires

significant management commitment from both stakeholders and regular governance

in addition to all other elements of an engineering services partnership. There are

companies today that are effectively trying to make a transition from being a product

company to a platform and services company and are often leveraging engineering

services providers to free up their management and engineering assets bandwidth. In

many cases, we are developing next-generation products for our customers across

industries that include hi-tech, aerospace, medical, auto, and industrial. Customers

also need partners who have full capabilities to develop and take ownership of the

entire end-to-end systems without having to deal with multiple suppliers.

IDC: How do you accelerate your customers' product development?

SK: The approach is to work as our customers' partner and provide a deep business

and technical knowledge across multiple industries and technologies. In addition to

the traditional strength of deep technical knowledge, domain expertise, and skills at

global scale, we have created 25 Service Line Units (SLUs) such as rapid Android

development and migration, embedded device automation testing, automated testing

of large industrial products, accelerated functional testing framework, and M2M

Staff augmentation

Cost arbitrage Scale

Noncore projects

Outcome based Partnership

4 #242291 ©2013 IDC

framework, which help our customers in faster product launches. We have also

invested heavily in being closer to our customers through global delivery centers and

product and program management capabilities that function as an integral part of the

engineering and product management teams.

IDC: You talk a lot about convergence. As industries come closer to each other,

how in your view is the productization of services going to evolve, especially

for those services that are relevant across industries?

SK: Convergence is bringing industries closer to each other in a more overlapping

zone than what we have witnessed in a long time. In the past, as the dividing lines

between different industry functions were clear, services were often delivered in a

matrix model where industry experts worked with services experts in delivering the

right kind of solution for a particular problem. Although this approach was time and

resource intensive, it was a suitable way to provide value to technology customers.

However, with convergence, the interplay of devices, platforms, and software is

creating phenomenal opportunities for the industries. Many services are being

integrated into platforms that are being delivered across multiple industries. To

achieve the objective of differentiating engineering services in the market as well as

providing additional value to the customers, these services need to be prepackaged

along with the relevant IP/solutions — delivered faster, cheaper, and better in a

resource-independent way. That's the productization of services I am talking about,

and it's going to be the way to deliver services in future. This process will also enable

putting together the right kind of multiskilled teams to solve newer and emerging

problems faster and better. Our SLU approach and investment is a step in this

direction. We also see significant traction in platform-based development across

many industries — auto for example, where onboarding of new services can now be

done through the cloud and on an on-need basis.

IDC: How do you perceive engineering services providers such as HCL Tech to

partner with other business unit stakeholders (cloud, analytics, mobility, etc.)

from within the company to provide innovative solutions across different

industries?

SK: The common aspect in these technologies (cloud, analytics, mobility, etc.) is the

platform. Both device original equipment manufacturers (OEMs) and pure-play online

and software companies are using different kinds of platforms to provide experiences

as a service and charging on a pay-per-use model, right from downloading

applications/content to carrying out enterprise transactions on a smartphone.

The underlying ability of the engineering platform to provide a better user experience

by running big data analytics on the millions of concurrent transactions stored in the

cloud provides huge opportunities for engineering services providers across

industries.

We see a lot of disruptive growth in this area in the near and medium term.

IDC: How is HCL Tech assisting with its customers' innovation efforts?

SK: Great question — we are getting increasingly involved in our customers' innovation

efforts. In almost all our engineering services, a culture of providing innovation across

©2013 IDC #242291 5

products, processes, and technologies and using new business models is becoming an

integral part of customer engagements. For example, we have created three centers of

excellence (COEs) for one of our customers that include high-speed data analytics,

imaging, and control systems. Similarly, for another customer, a COE is created to drive

new thinking and innovation on implantable medical devices. Also, our Product

Intelligence SLU for online products and solutions across industries assists our

customers to gain critical business insights on user behavior.

In the telecom/communication sector, we have a large global engagement in

engineering services that includes technologies such as software-defined networking

(SDN), video, analytics, mobility, converged and self-healing networks, M2M, and so

forth.

Today, we are involved with more than 55% of the top 100 R&D spending companies

globally as a partner to develop next-generation products and platforms.

IDC: What is HCL Tech's philosophy to grow this business?

SK: We have adopted a multipronged strategy to grow. We are closely aligned to

creating business impact for our customers through:

Market launch and acceleration with respect to device, software, and

platform. To deliver the products/platforms and services to the market faster by

leveraging our solutions, SLUs, domain expertise, and integrated product

management and technical expertise

Operations optimization through testing, value engineering, and

sustenance. To deliver the best cost-to-benefit ratio

Adoption of emerging technologies, including mobility and smart products.

To provide cutting-edge solutions to the market and the extension of products to

adjacent markets and regions.

We have invested significantly in creating global delivery and operations capabilities

that are closer to customers and are an integral part of product development teams.

Integrated engineering is a key success factor for product launches, as customers

don't want to manage multiple partnerships.

We also believe that business impacts across products and market segments are

directly related to phenomenal end-user experience from all products, platforms, and

services. These can range from a simple software interface to complex industrial-

grade or mission-critical systems. Our "Engineering Experiences" approach and

processes bring this aspect in the overall design philosophy.

In addition to the U.S. market, we are also focused on growth opportunities in Europe

and Japan, which have a significant part of the overall global R&D. We have local

engineering development centers in these regions — closer to customers to provide

the interface for technical, product, and business aspects along with the local

leadership and language expertise.

6 #242291 ©2013 IDC

IDC: What roles do talent, infrastructure, and IP play in a customer's decision to

outsource versus keeping its product development/engineering functions in-

house?

SK: Talent, infrastructure, and IP have a huge bearing on any customer's decision on

whether they should partner for a particular program or do it in-house.

The talent pool of any technology product company should be focused on star and

future products that create and expand their market share and drive higher

profitability. However, we see that in many situations, higher R&D dollars are invested

toward managing current products that are end of life and not profitable. Collaborative

engineering partnerships with trusted companies are key to achieve this balance of

managing current products and investing into the future as well.

The infrastructure offered by the service provider to the customer obviously plays a

crucial role in the client's decision to partner as well. It is a clear choice depending on

whether the service provider has the required labs, tools, and infrastructure that can be

leveraged for the partnership. IP development and IP protection are both critical aspects

of any partnership and cannot be compromised. We also believe that proper and

regular executive-level governance is another important aspect of the relationship.

IDC: In the foreseeable future, which industries or product groups will

outsource the complete life cycle for their products, including supply chain,

and focus only on the sales and marketing functions?

SK: For many industries, this is already happening. For example, semiconductor

companies are outsourcing design services to India and manufacturing to China and

are taking up the responsibilities of overall strategy, sales, and marketing. However,

one key factor to note out here is they are keeping their design and manufacturing

ecosystems completely separate, and that's important to protect their IPs and retain

control. Not every company or industry will move in this direction though. Many of

them will keep a few elements of the value chain completely in-house, especially

where they excel, as they form part of their differentiator. As I mentioned earlier, they

will typically collaborate in areas of complementary strengths.

O b s e r v a t i o n s a n d S u m m a r y

This discussion validated the analyst's opinion about the growth and opportunity

provided to engineering services providers as well as the benefits that accrue to

technology product companies across a range of industries. The discussion provided

insight based on HCL Technologies' experience and strategy to grow this business.

As IDC's engineering services research has highlighted in the past, these services

need a very different set of capabilities, investment, and approach compared with the

traditional IT services companies.

©2013 IDC #242291 7

IDC is of the opinion that:

Competition will drive increased demand for engineering services. The stage

has been set, and the market needs a few other providers to begin or increase their

focus on these services — this activity will lead to market growth for R&D/product

engineering services. HCL Technologies and other engineering services providers

that currently offer these services need to be aware that new competitors that are

currently building this business can impact their current and future growth.

Engineering services delivery will begin to move onshore. As engineering

services providers such as HCL Tech move up the value chain, they will find it

difficult to source the kind of high-level talent that will be scarce in offshore

locations such as India. This trend coupled with customers' continued resistance

to outsource and especially offshore core intellectual property as well as

immigration policy issues will necessitate increasing engineering services

provider onshore presence.

SMAC will drive increased customer adoption of engineering services.

During one of our conversations with Kishore, he mentioned that the emergence

of the social-mobile-analytics-cloud (SMAC) services opportunity overlapped with

both the CIO's and the CTO's office. Each of these services requires a lot of

platform maturity and was being driven by a consortium of service providers,

technology stack providers, enterprise stack companies, and so forth. According

to IDC, the ability of the IT services and/or the engineering services providers to

build these platforms and/or solutions in partnership with other stakeholders will

increase awareness and market opportunity for these services.

G u i d a n c e f o r P o t e n t i a l S e r v i c e s P r o v i d e r s

a n d C u s t o m e r s

For services providers. It may seem daunting for those providers that do not

offer these services, but with careful planning and the acquisition of appropriate

skills and a reasonable investment commitment, this business can be built. If you

are already offering services across the SMAC stack, the good news is that you

are already providing some level of engineering services. These services will see

growth in the near term as well as in the long term. According to IDC's

R&D/product engineering services forecast (see Worldwide and U.S. Research

and Development/Product Engineering Services 2012–2016 Forecast, IDC

#238737, December 2012), the market is expected to grow at a five-year CAGR

of 9.1% and will reach an estimated $60.3 billion by 2016.

For customers. With shrinking R&D budgets and the urgent need to get your

products to market faster, you need to associate with engineering services

providers that will act as your business partner and help you achieve these

objectives. There are existing and emerging providers that have set up centers of

excellence across a host of functions/industries, hired the right kind of

engineering talent that will help you scale, and are infusing a significant amount

of technology in their service offering. These strategic partnerships will enable

you to free up budgets for additional R&D and new product/IP creation.

8 #242291 ©2013 IDC

L E A R N M O R E

R e l a t e d R e s e a r c h

Worldwide and U.S. Discrete Testing Services 2013–2017 Forecast: Cloud and

Mobility Drive Growth (IDC #241998, July 2013)

Worldwide and U.S. Research and Development/Product Engineering Services

2012–2016 Forecast (IDC #238737, December 2012)

R&D/Product Engineering Services — How Is HCL Technologies Thinking Out of

the Box and Providing Value to Technology Product Customers? (IDC #234586,

May 2012)

Worldwide Services 2012 Top 10 Predictions (IDC #233279, February 2012)

CSC Acquires AppLabs: Expands Its Testing Services Portfolio Footprint (IDC

#lcCA23046511, September 2011)

Mobility Testing Services: Providers' Cross-Platform and Usability Expertise

Helps Customers Build Strategic Advantage (IDC #229878, September 2011)

Strategies and Opportunities Driving Mobile Enterprise Application Development

Life-Cycle Services (IDC #229772, August 2011)

Mobile Product Development and Test Service Strategies — Where Are

Outsourcers Investing (IDC #226453, January 2011)

Symphony Services — Innovation at Work (IDC #225636, November 2010)

A Hot Bed of Testing Services — Mobile Apps and Devices Are Prime Validation

Targets (IDC #IcUS22556110, November 2010)

QuEST Global: Vendor Profile Series for Research and Development/Product

Engineering Services (IDC #224296, August 2010)

IDC MarketScape: Global Testing Services, 2010 Vendor Analysis (IDC

#223954, July 2010)

Moving Up the Value Chain: Tata Consultancy Services (TCS) to help Saab

Design and Develop "Gripen" Fighter Aircraft (IDC #lcUS21774609, April 2009)

2009 Research and Development/Product Engineering Services Needs with

Market Overview (IDC #217359, March 2009)

Wipro — Vendor Profile Series for Research and Development/Product

Engineering Services (IDC #215589, December 2008)

Accenture — Vendor Profile Series for Research and Development/Product

Engineering Services (IDC #215249, November 2008)

©2013 IDC #242291 9

Tata Consultancy Services — Vendor Profile Series for Research and

Development/Product Engineering Services (IDC #214088, November 2008)

HCL Technologies — Vendor Profile Series for R&D/Product Engineering

Services (IDC #214698, October 2008)

IBM: Harnessing the Global Ecosystem to Accelerate Time to Market — But Is

There More to Do? (IDC #IcUS21472908, October 2008)

Outsourcing Research and Development/Product Engineering Services — Is a

Hybrid Strategy the Way to Go? (IDC #211835, April 2008)

Outsourcing Research and Development — Customers Want to Cut Costs, and

Vendors Are Reaping the Benefits (IDC #209385, November 2007)

IDC's Worldwide R&D Product Engineering Services Taxonomy, 2007 (IDC

#209093, October 2007)

Research and Development/Product Engineering Services — A New Frontier of

Opportunities (IDC #208397, August 2007)

C o p y r i g h t N o t i c e

This IDC research document was published as part of an IDC continuous intelligence

service, providing written research, analyst interactions, telebriefings, and

conferences. Visit www.idc.com to learn more about IDC subscription and consulting

services. To view a list of IDC offices worldwide, visit www.idc.com/offices. Please

contact the IDC Hotline at 800.343.4952, ext. 7988 (or +1.508.988.7988) or

[email protected] for information on applying the price of this document toward the

purchase of an IDC service or for information on additional copies or Web rights.

Copyright 2013 IDC. Reproduction is forbidden unless authorized. All rights reserved.