Embed Size (px)

Citation preview

Upcoming Advancesin the Hybrid Vehicle Market

No. 114 February 1, 2007

Yuki TANAKA, Yukio SHIGETA

Copyright 2007 by Nomura Research Institute, Ltd. 1

NRI Papers No. 114February 1, 2007

Upcoming Advancesin the Hybrid Vehicle Market

Yuki TANAKA, Yukio SHIGETA

The market for hybrid vehicles has been growing explosively. These vehicles first appeared on

the market ten years ago, in 1997, when they were touted as a means of suppressing growing

CO2 emissions. Against a background of increased environmental awareness and higher oil prices,

2004 proved to be the second consecutive year in which sales of hybrid cars doubled, and 2005

saw sales reach about 300,000 units.

Despite these figures, even after being on the market for ten years, hybrid cars still account for

less than 2 percent of all new car sales. To determine the factors that would lead to a faster spread

of hybrid vehicles, NRI conducted a questionnaire-based consumer survey. As a result, we identi-

fied three main factors, namely, (1) lower cost, (2) wider product lineups and (3) more opportuni-

ties to actually experience using hybrid vehicles. If manufacturers could respond to these demands,

we estimate that the market for hybrid vehicles would rise to 2.2 million vehicles by 2012, while

giving birth to a hybrid-related component market amounting to 760 billion yen.

Unfortunately, however, it is not easy to reduce the cost and size of the components used in

hybrid vehicles. If this were to be realized, the vehicle manufacturers and parts suppliers would

have to establish some kind of open development system.

Previous Trends in the IndustryHybrid vehicle market expands rapidly as more and more manufacturers maketheir entry

Current TopicsApproach varies depending on the manufacturer

Market ProspectsReductions in costs and wider product lineups seen as keys to expanding themarket

Changes in Industrial StructureMarket growth offers new opportunities to manufacturers of electricalequipment and components

Suggestions for the IndustryMotor manufacturers should establish an open development system with relatedsuppliers

Copyright 2007 by Nomura Research Institute, Ltd. 2

Previous Trends in the Industry

Hybrid vehicle market expands rapidly asmore and more manufacturers make theirentry

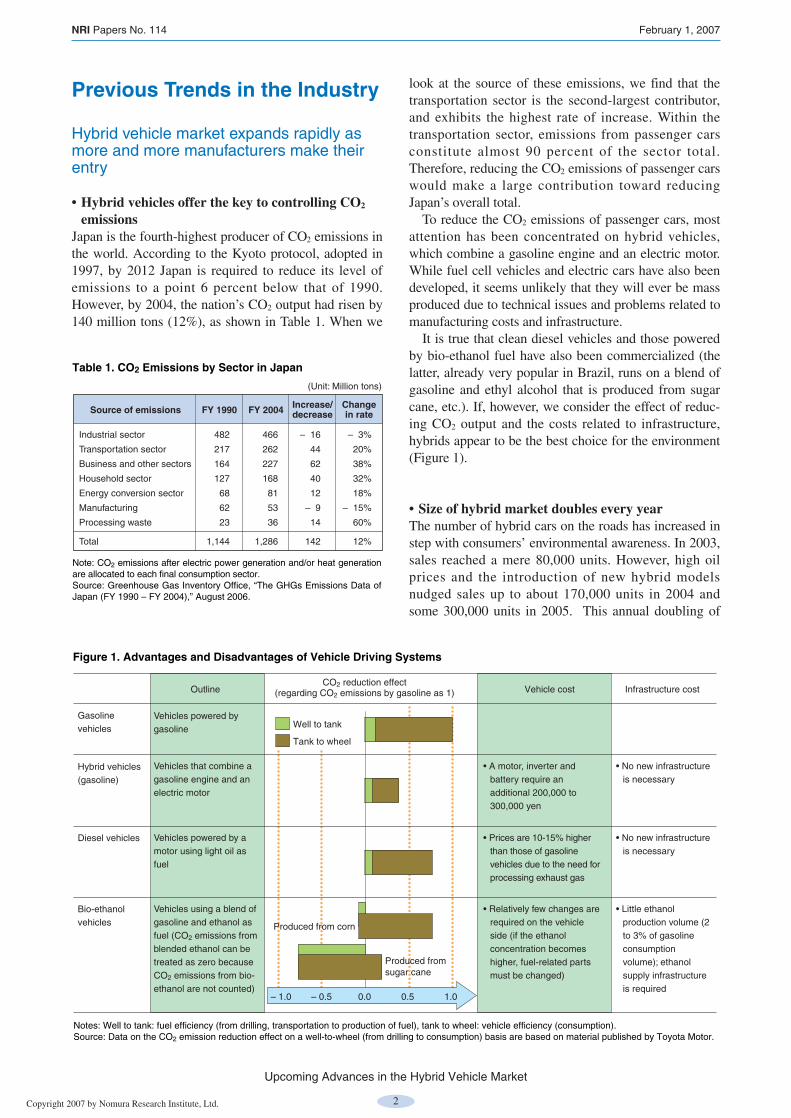

• Hybrid vehicles offer the key to controlling CO2

emissionsJapan is the fourth-highest producer of CO2 emissions inthe world. According to the Kyoto protocol, adopted in1997, by 2012 Japan is required to reduce its level ofemissions to a point 6 percent below that of 1990.However, by 2004, the nation’s CO2 output had risen by140 million tons (12%), as shown in Table 1. When we

look at the source of these emissions, we find that thetransportation sector is the second-largest contributor,and exhibits the highest rate of increase. Within thetransportation sector, emissions from passenger carsconstitute almost 90 percent of the sector total.Therefore, reducing the CO2 emissions of passenger carswould make a large contribution toward reducingJapan’s overall total.

To reduce the CO2 emissions of passenger cars, mostattention has been concentrated on hybrid vehicles,which combine a gasoline engine and an electric motor.While fuel cell vehicles and electric cars have also beendeveloped, it seems unlikely that they will ever be massproduced due to technical issues and problems related tomanufacturing costs and infrastructure.

It is true that clean diesel vehicles and those poweredby bio-ethanol fuel have also been commercialized (thelatter, already very popular in Brazil, runs on a blend ofgasoline and ethyl alcohol that is produced from sugarcane, etc.). If, however, we consider the effect of reduc-ing CO2 output and the costs related to infrastructure,hybrids appear to be the best choice for the environment(Figure 1).

• Size of hybrid market doubles every yearThe number of hybrid cars on the roads has increased instep with consumers’ environmental awareness. In 2003,sales reached a mere 80,000 units. However, high oilprices and the introduction of new hybrid modelsnudged sales up to about 170,000 units in 2004 andsome 300,000 units in 2005. This annual doubling of

NRI Papers No. 114 February 1, 2007

Upcoming Advances in the Hybrid Vehicle Market

Note: CO2 emissions after electric power generation and/or heat generation are allocated to each final consumption sector.Source: Greenhouse Gas Inventory Office, “The GHGs Emissions Data of Japan (FY 1990 – FY 2004),” August 2006.

Table 1. CO2 Emissions by Sector in Japan

FY 1990 FY 2004 Increase/decrease

Changein rateSource of emissions

(Unit: Million tons)

Industrial sector 482 466 – 16 – 3%

Transportation sector 217 262 44 20%

Business and other sectors 164 227 62 38%

Household sector 127 168 40 32%

Energy conversion sector 68 81 12 18%

Manufacturing 62 53 – 9 – 15%

Processing waste 23 36 14 60%

Total 1,144 1,286 142 12%

– 1.0 – 0.5 0.0 1.00.5

Produced from corn

Produced from sugar cane

Well to tank

Tank to wheel

Notes: Well to tank: fuel efficiency (from drilling, transportation to production of fuel), tank to wheel: vehicle efficiency (consumption).Source: Data on the CO2 emission reduction effect on a well-to-wheel (from drilling to consumption) basis are based on material published by Toyota Motor.

Figure 1. Advantages and Disadvantages of Vehicle Driving Systems

Vehicles powered by gasoline

Vehicles that combine a gasoline engine and an electric motor

Vehicles powered by a motor using light oil as fuel

Vehicles using a blend of gasoline and ethanol as fuel (CO2 emissions from blended ethanol can be treated as zero because CO2 emissions from bio-ethanol are not counted)

• A motor, inverter and battery require an additional 200,000 to 300,000 yen

• Prices are 10-15% higher than those of gasoline vehicles due to the need for processing exhaust gas

• Relatively few changes are required on the vehicle side (if the ethanol concentration becomes higher, fuel-related parts must be changed)

• No new infrastructure is necessary

• No new infrastructure is necessary

• Little ethanol production volume (2 to 3% of gasoline consumption volume); ethanol supply infrastructure is required

Gasolinevehicles

Hybrid vehicles (gasoline)

Diesel vehicles

Bio-ethanolvehicles

OutlineCO2 reduction effect

(regarding CO2 emissions by gasoline as 1) Vehicle cost Infrastructure cost

Copyright 2007 by Nomura Research Institute, Ltd. 3

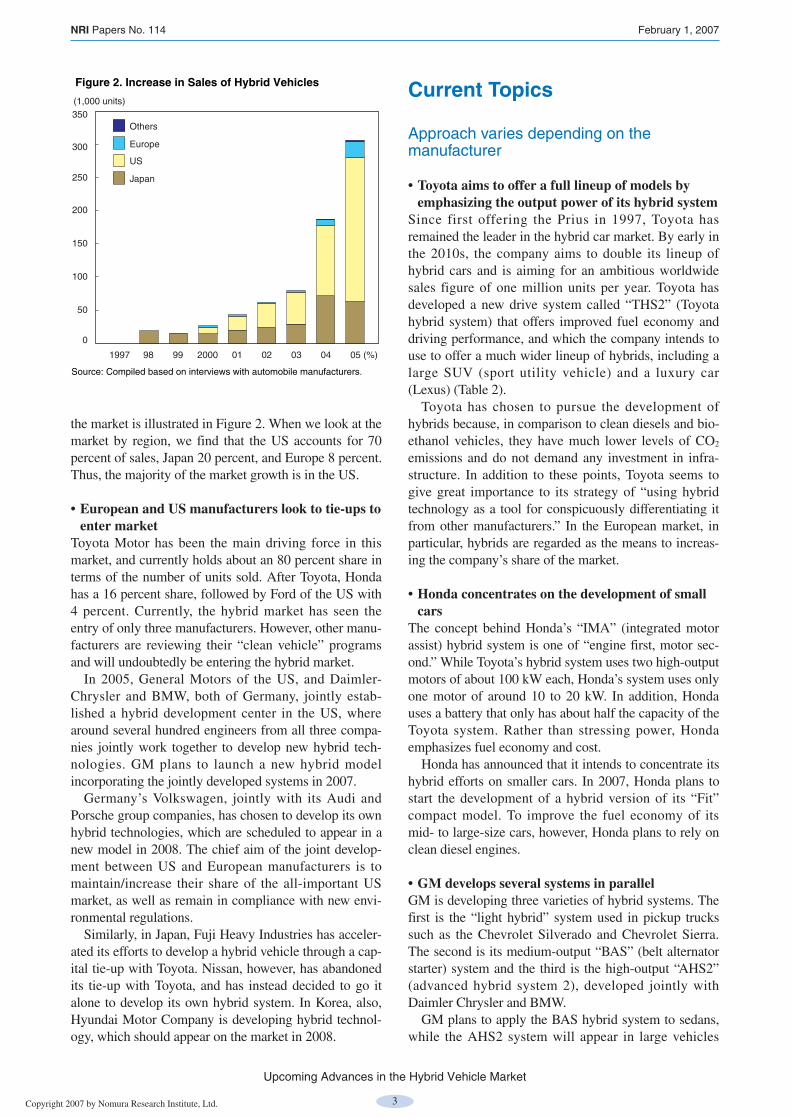

the market is illustrated in Figure 2. When we look at themarket by region, we find that the US accounts for 70percent of sales, Japan 20 percent, and Europe 8 percent.Thus, the majority of the market growth is in the US.

• European and US manufacturers look to tie-ups toenter market

Toyota Motor has been the main driving force in thismarket, and currently holds about an 80 percent share interms of the number of units sold. After Toyota, Hondahas a 16 percent share, followed by Ford of the US with4 percent. Currently, the hybrid market has seen theentry of only three manufacturers. However, other manu-facturers are reviewing their “clean vehicle” programsand will undoubtedly be entering the hybrid market.

In 2005, General Motors of the US, and Daimler-Chrysler and BMW, both of Germany, jointly estab-lished a hybrid development center in the US, wherearound several hundred engineers from all three compa-nies jointly work together to develop new hybrid tech-nologies. GM plans to launch a new hybrid modelincorporating the jointly developed systems in 2007.

Germany’s Volkswagen, jointly with its Audi andPorsche group companies, has chosen to develop its ownhybrid technologies, which are scheduled to appear in anew model in 2008. The chief aim of the joint develop-ment between US and European manufacturers is tomaintain/increase their share of the all-important USmarket, as well as remain in compliance with new envi-ronmental regulations.

Similarly, in Japan, Fuji Heavy Industries has acceler-ated its efforts to develop a hybrid vehicle through a cap-ital tie-up with Toyota. Nissan, however, has abandonedits tie-up with Toyota, and has instead decided to go italone to develop its own hybrid system. In Korea, also,Hyundai Motor Company is developing hybrid technol-ogy, which should appear on the market in 2008.

Current Topics

Approach varies depending on themanufacturer

• Toyota aims to offer a full lineup of models byemphasizing the output power of its hybrid system

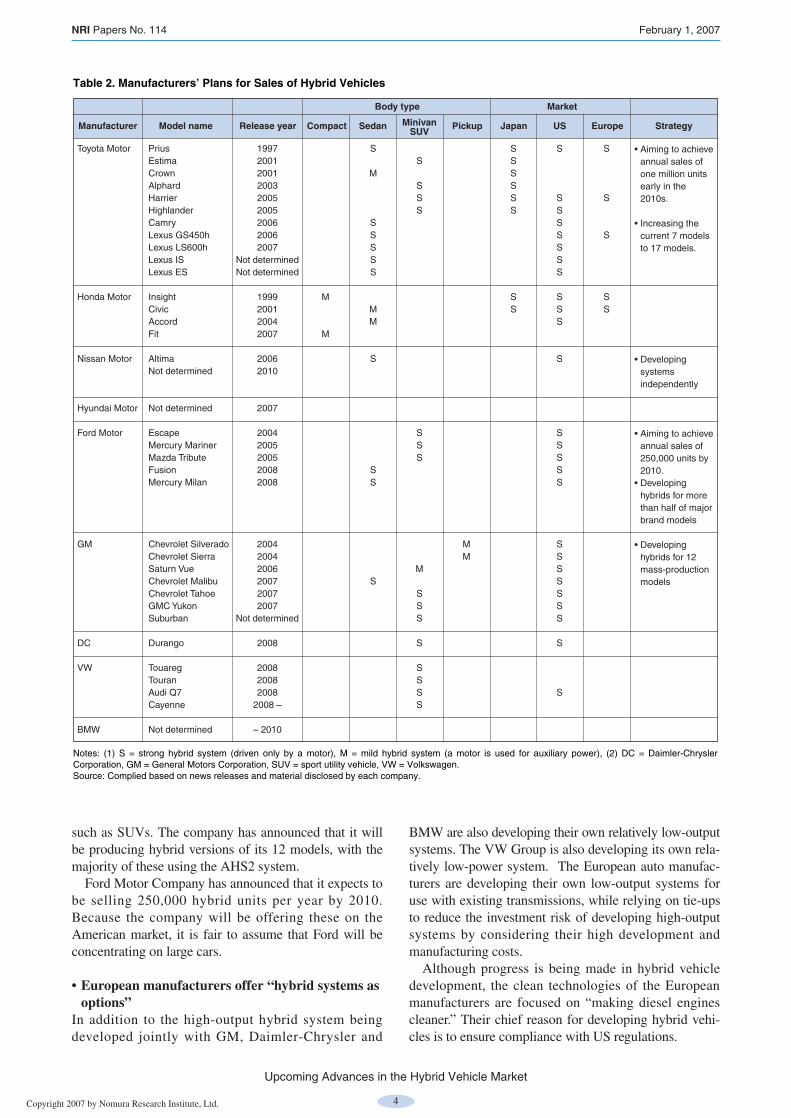

Since first offering the Prius in 1997, Toyota hasremained the leader in the hybrid car market. By early inthe 2010s, the company aims to double its lineup ofhybrid cars and is aiming for an ambitious worldwidesales figure of one million units per year. Toyota hasdeveloped a new drive system called “THS2” (Toyotahybrid system) that offers improved fuel economy anddriving performance, and which the company intends touse to offer a much wider lineup of hybrids, including alarge SUV (sport utility vehicle) and a luxury car(Lexus) (Table 2).

Toyota has chosen to pursue the development ofhybrids because, in comparison to clean diesels and bio-ethanol vehicles, they have much lower levels of CO2

emissions and do not demand any investment in infra-structure. In addition to these points, Toyota seems togive great importance to its strategy of “using hybridtechnology as a tool for conspicuously differentiating itfrom other manufacturers.” In the European market, inparticular, hybrids are regarded as the means to increas-ing the company’s share of the market.

• Honda concentrates on the development of smallcars

The concept behind Honda’s “IMA” (integrated motorassist) hybrid system is one of “engine first, motor sec-ond.” While Toyota’s hybrid system uses two high-outputmotors of about 100 kW each, Honda’s system uses onlyone motor of around 10 to 20 kW. In addition, Hondauses a battery that only has about half the capacity of theToyota system. Rather than stressing power, Hondaemphasizes fuel economy and cost.

Honda has announced that it intends to concentrate itshybrid efforts on smaller cars. In 2007, Honda plans tostart the development of a hybrid version of its “Fit”compact model. To improve the fuel economy of itsmid- to large-size cars, however, Honda plans to rely onclean diesel engines.

• GM develops several systems in parallelGM is developing three varieties of hybrid systems. Thefirst is the “light hybrid” system used in pickup truckssuch as the Chevrolet Silverado and Chevrolet Sierra.The second is its medium-output “BAS” (belt alternatorstarter) system and the third is the high-output “AHS2”(advanced hybrid system 2), developed jointly withDaimler Chrysler and BMW.

GM plans to apply the BAS hybrid system to sedans,while the AHS2 system will appear in large vehicles

NRI Papers No. 114 February 1, 2007

Upcoming Advances in the Hybrid Vehicle Market

350(1,000 units)

300

250

200

150

100

50

0

Others

Europe

US

Japan

1997 98 99 2000 01 02 03 04 05 (%)

Source: Compiled based on interviews with automobile manufacturers.

Figure 2. Increase in Sales of Hybrid Vehicles

Copyright 2007 by Nomura Research Institute, Ltd. 4

such as SUVs. The company has announced that it willbe producing hybrid versions of its 12 models, with themajority of these using the AHS2 system.

Ford Motor Company has announced that it expects tobe selling 250,000 hybrid units per year by 2010.Because the company will be offering these on theAmerican market, it is fair to assume that Ford will beconcentrating on large cars.

• European manufacturers offer “hybrid systems asoptions”

In addition to the high-output hybrid system beingdeveloped jointly with GM, Daimler-Chrysler and

BMW are also developing their own relatively low-outputsystems. The VW Group is also developing its own rela-tively low-power system. The European auto manufac-turers are developing their own low-output systems foruse with existing transmissions, while relying on tie-upsto reduce the investment risk of developing high-outputsystems by considering their high development andmanufacturing costs.

Although progress is being made in hybrid vehicledevelopment, the clean technologies of the Europeanmanufacturers are focused on “making diesel enginescleaner.” Their chief reason for developing hybrid vehi-cles is to ensure compliance with US regulations.

NRI Papers No. 114 February 1, 2007

Upcoming Advances in the Hybrid Vehicle Market

Notes: (1) S = strong hybrid system (driven only by a motor), M = mild hybrid system (a motor is used for auxiliary power), (2) DC = Daimler-Chrysler Corporation, GM = General Motors Corporation, SUV = sport utility vehicle, VW = Volkswagen.Source: Complied based on news releases and material disclosed by each company.

Table 2. Manufacturers’ Plans for Sales of Hybrid Vehicles

Toyota Motor Prius 1997 S S S SEstima 2001 S SCrown 2001 M SAlphard 2003 S SHarrier 2005 S S S SHighlander 2005 S S SCamry 2006 S SLexus GS450h 2006 S S SLexus LS600h 2007 S SLexus IS Not determined S SLexus ES Not determined S S

Honda Motor Insight 1999 M S S SCivic 2001 M S S SAccord 2004 M SFit 2007 M

Nissan Motor Altima 2006 S SNot determined 2010

Hyundai Motor Not determined 2007

Ford Motor Escape 2004 S SMercury Mariner 2005 S SMazda Tribute 2005 S SFusion 2008 S SMercury Milan 2008 S S

GM Chevrolet Silverado 2004 M SChevrolet Sierra 2004 M SSaturn Vue 2006 M SChevrolet Malibu 2007 S SChevrolet Tahoe 2007 S SGMC Yukon 2007 S SSuburban Not determined S S

DC Durango 2008 S S

VW Touareg 2008 STouran 2008 SAudi Q7 2008 S SCayenne 2008 – S

BMW Not determined – 2010

• Aiming to achieve annual sales of one million units early in the 2010s.

• Increasing the current 7 models to 17 models.

• Developing systems independently

• Aiming to achieve annual sales of 250,000 units by 2010.

• Developing hybrids for more than half of major brand models

• Developing hybrids for 12 mass-production models

Manufacturer Model name Release year Compact Sedan Pickup Japan US Europe StrategyMinivanSUV

Body type Market

Copyright 2007 by Nomura Research Institute, Ltd. 5

Accordingly, it is impossible to deny that they are tak-ing a passive stance of “only offering the required mini-mum” in the first instance. The European manufacturershave not announced any specific plans to introducehybrid models.

Because the European manufacturers are positioninghybrid systems as just another option, it is thought thatthey are not placing as much emphasis on the develop-ment of their own systems. This also points to their pas-sive attitude toward hybrid vehicles.

Market Prospects

Reductions in costs and wider productlineups seen as keys to expanding themarket

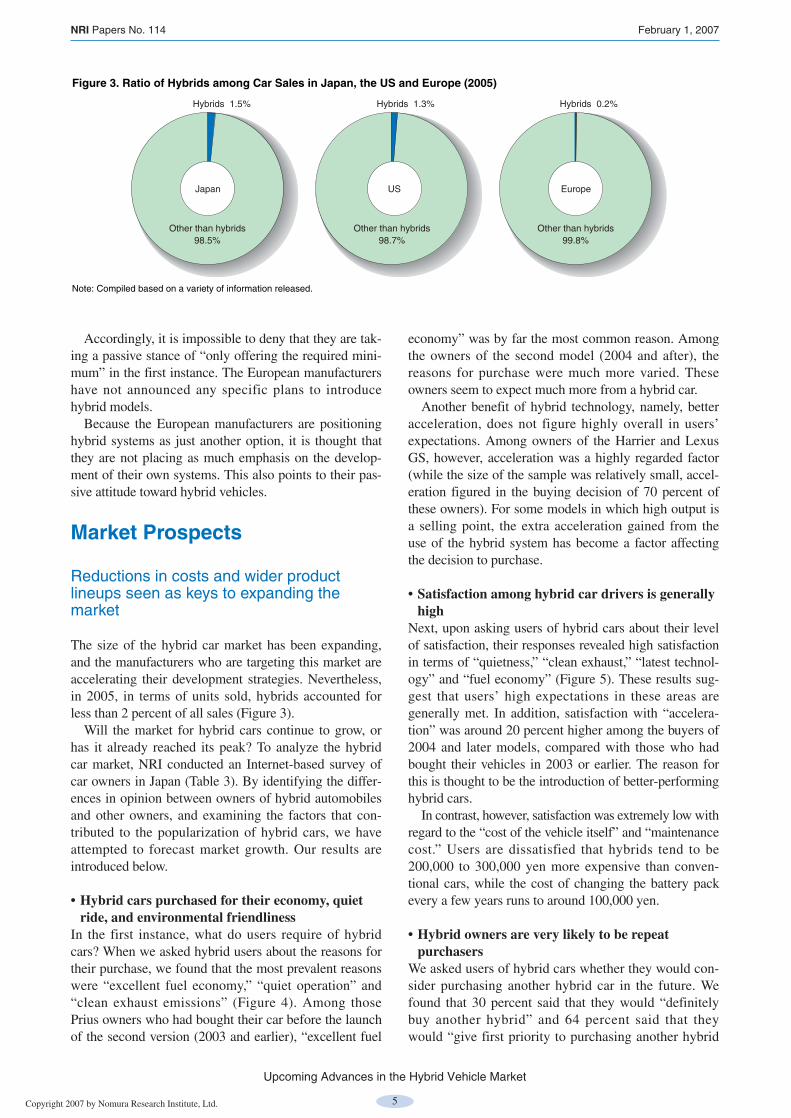

The size of the hybrid car market has been expanding,and the manufacturers who are targeting this market areaccelerating their development strategies. Nevertheless,in 2005, in terms of units sold, hybrids accounted forless than 2 percent of all sales (Figure 3).

Will the market for hybrid cars continue to grow, orhas it already reached its peak? To analyze the hybridcar market, NRI conducted an Internet-based survey ofcar owners in Japan (Table 3). By identifying the differ-ences in opinion between owners of hybrid automobilesand other owners, and examining the factors that con-tributed to the popularization of hybrid cars, we haveattempted to forecast market growth. Our results areintroduced below.

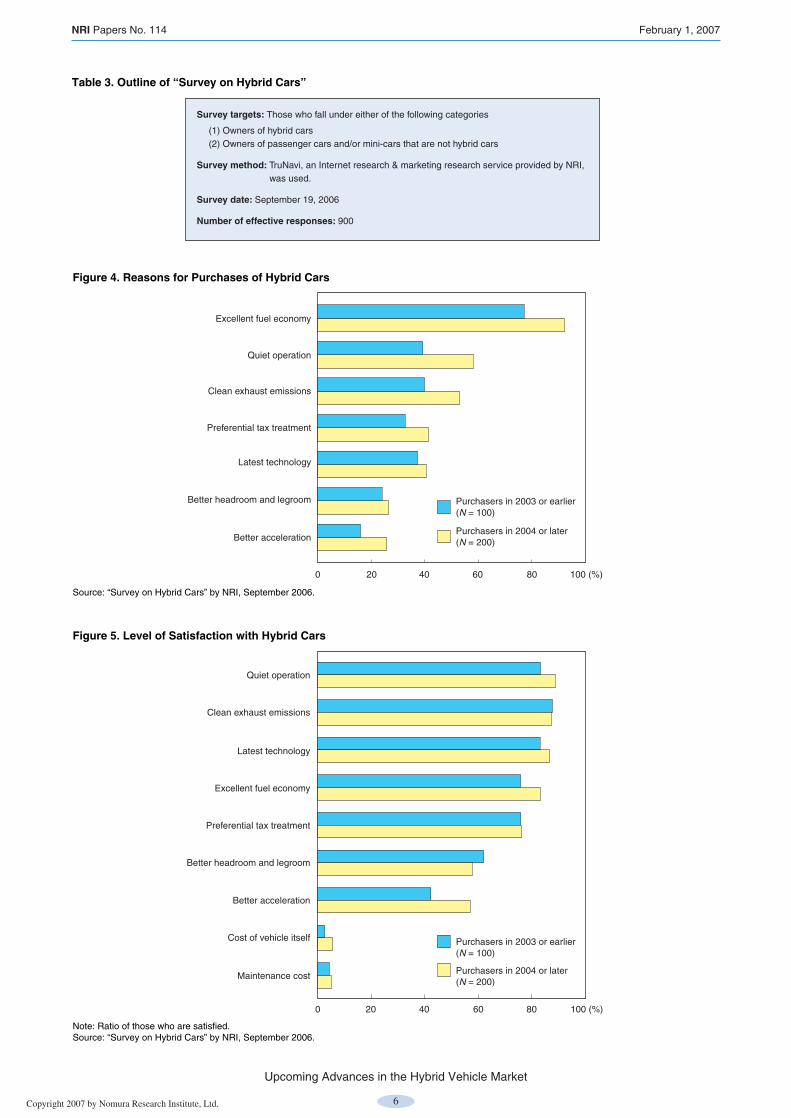

• Hybrid cars purchased for their economy, quietride, and environmental friendliness

In the first instance, what do users require of hybridcars? When we asked hybrid users about the reasons fortheir purchase, we found that the most prevalent reasonswere “excellent fuel economy,” “quiet operation” and“clean exhaust emissions” (Figure 4). Among thosePrius owners who had bought their car before the launchof the second version (2003 and earlier), “excellent fuel

economy” was by far the most common reason. Amongthe owners of the second model (2004 and after), thereasons for purchase were much more varied. Theseowners seem to expect much more from a hybrid car.

Another benefit of hybrid technology, namely, betteracceleration, does not figure highly overall in users’expectations. Among owners of the Harrier and LexusGS, however, acceleration was a highly regarded factor(while the size of the sample was relatively small, accel-eration figured in the buying decision of 70 percent ofthese owners). For some models in which high output isa selling point, the extra acceleration gained from theuse of the hybrid system has become a factor affectingthe decision to purchase.

• Satisfaction among hybrid car drivers is generallyhigh

Next, upon asking users of hybrid cars about their levelof satisfaction, their responses revealed high satisfactionin terms of “quietness,” “clean exhaust,” “latest technol-ogy” and “fuel economy” (Figure 5). These results sug-gest that users’ high expectations in these areas aregenerally met. In addition, satisfaction with “accelera-tion” was around 20 percent higher among the buyers of2004 and later models, compared with those who hadbought their vehicles in 2003 or earlier. The reason forthis is thought to be the introduction of better-performinghybrid cars.

In contrast, however, satisfaction was extremely low withregard to the “cost of the vehicle itself” and “maintenancecost.” Users are dissatisfied that hybrids tend to be200,000 to 300,000 yen more expensive than conven-tional cars, while the cost of changing the battery packevery a few years runs to around 100,000 yen.

• Hybrid owners are very likely to be repeatpurchasers

We asked users of hybrid cars whether they would con-sider purchasing another hybrid car in the future. Wefound that 30 percent said that they would “definitelybuy another hybrid” and 64 percent said that theywould “give first priority to purchasing another hybrid

NRI Papers No. 114 February 1, 2007

Upcoming Advances in the Hybrid Vehicle Market

Hybrids 0.2%

Other than hybrids99.8%

Europe

Hybrids 1.3%

Other than hybrids98.7%

US

Hybrids 1.5%

Other than hybrids98.5%

Japan

Note: Compiled based on a variety of information released.

Figure 3. Ratio of Hybrids among Car Sales in Japan, the US and Europe (2005)

Copyright 2007 by Nomura Research Institute, Ltd. 6

NRI Papers No. 114 February 1, 2007

Upcoming Advances in the Hybrid Vehicle Market

0 20 40 60 80 100 (%)

Purchasers in 2003 or earlier(N = 100)

Purchasers in 2004 or later(N = 200)

Excellent fuel economy

Quiet operation

Clean exhaust emissions

Better acceleration

Preferential tax treatment

Latest technology

Better headroom and legroom

Source: “Survey on Hybrid Cars” by NRI, September 2006.

Figure 4. Reasons for Purchases of Hybrid Cars

0 20 40 60 80 100 (%)

Note: Ratio of those who are satisfied.Source: “Survey on Hybrid Cars” by NRI, September 2006.

Figure 5. Level of Satisfaction with Hybrid Cars

Purchasers in 2003 or earlier(N = 100)

Purchasers in 2004 or later(N = 200)

Quiet operation

Clean exhaust emissions

Latest technology

Excellent fuel economy

Preferential tax treatment

Better headroom and legroom

Better acceleration

Cost of vehicle itself

Maintenance cost

Table 3. Outline of “Survey on Hybrid Cars”

Survey targets: Those who fall under either of the following categories

(1) Owners of hybrid cars(2) Owners of passenger cars and/or mini-cars that are not hybrid cars

Survey method: TruNavi, an Internet research & marketing research service provided by NRI,was used.

Survey date: September 19, 2006

Number of effective responses: 900

Copyright 2007 by Nomura Research Institute, Ltd. 7

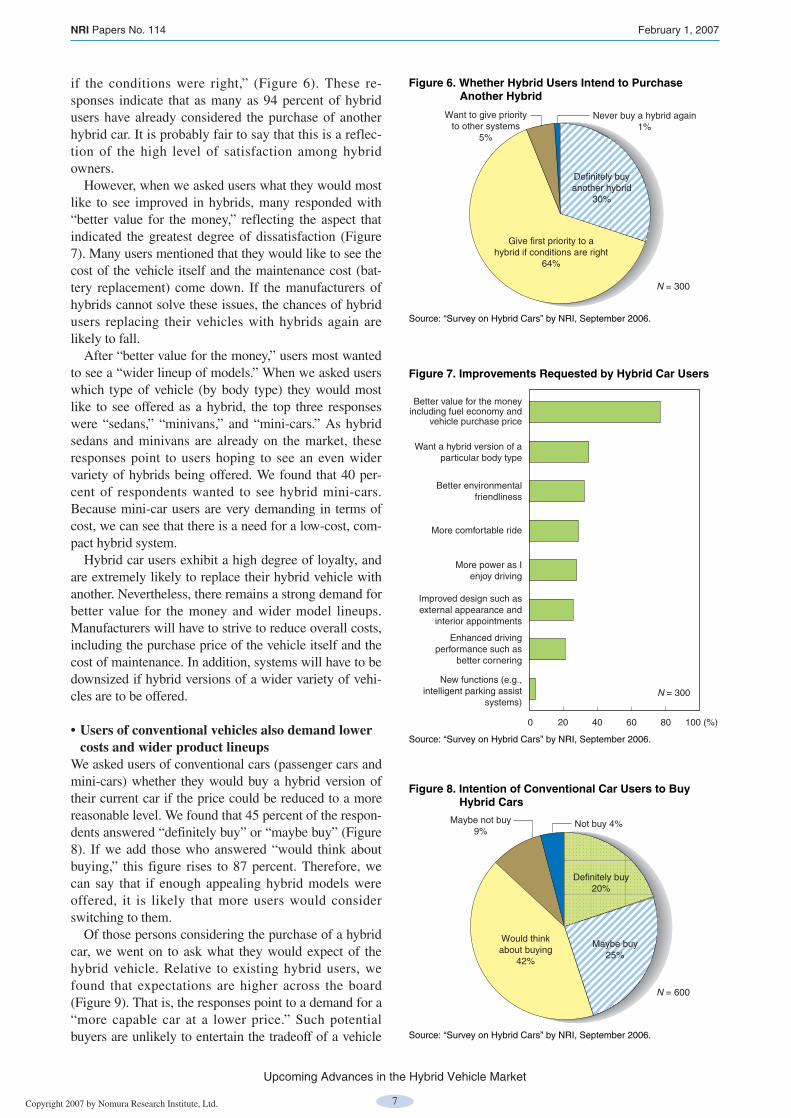

if the conditions were right,” (Figure 6). These re-sponses indicate that as many as 94 percent of hybridusers have already considered the purchase of anotherhybrid car. It is probably fair to say that this is a reflec-tion of the high level of satisfaction among hybridowners.

However, when we asked users what they would mostlike to see improved in hybrids, many responded with“better value for the money,” reflecting the aspect thatindicated the greatest degree of dissatisfaction (Figure7). Many users mentioned that they would like to see thecost of the vehicle itself and the maintenance cost (bat-tery replacement) come down. If the manufacturers ofhybrids cannot solve these issues, the chances of hybridusers replacing their vehicles with hybrids again arelikely to fall.

After “better value for the money,” users most wantedto see a “wider lineup of models.” When we asked userswhich type of vehicle (by body type) they would mostlike to see offered as a hybrid, the top three responseswere “sedans,” “minivans,” and “mini-cars.” As hybridsedans and minivans are already on the market, theseresponses point to users hoping to see an even widervariety of hybrids being offered. We found that 40 per-cent of respondents wanted to see hybrid mini-cars.Because mini-car users are very demanding in terms ofcost, we can see that there is a need for a low-cost, com-pact hybrid system.

Hybrid car users exhibit a high degree of loyalty, andare extremely likely to replace their hybrid vehicle withanother. Nevertheless, there remains a strong demand forbetter value for the money and wider model lineups.Manufacturers will have to strive to reduce overall costs,including the purchase price of the vehicle itself and thecost of maintenance. In addition, systems will have to bedownsized if hybrid versions of a wider variety of vehi-cles are to be offered.

• Users of conventional vehicles also demand lowercosts and wider product lineups

We asked users of conventional cars (passenger cars andmini-cars) whether they would buy a hybrid version oftheir current car if the price could be reduced to a morereasonable level. We found that 45 percent of the respon-dents answered “definitely buy” or “maybe buy” (Figure8). If we add those who answered “would think aboutbuying,” this figure rises to 87 percent. Therefore, wecan say that if enough appealing hybrid models wereoffered, it is likely that more users would considerswitching to them.

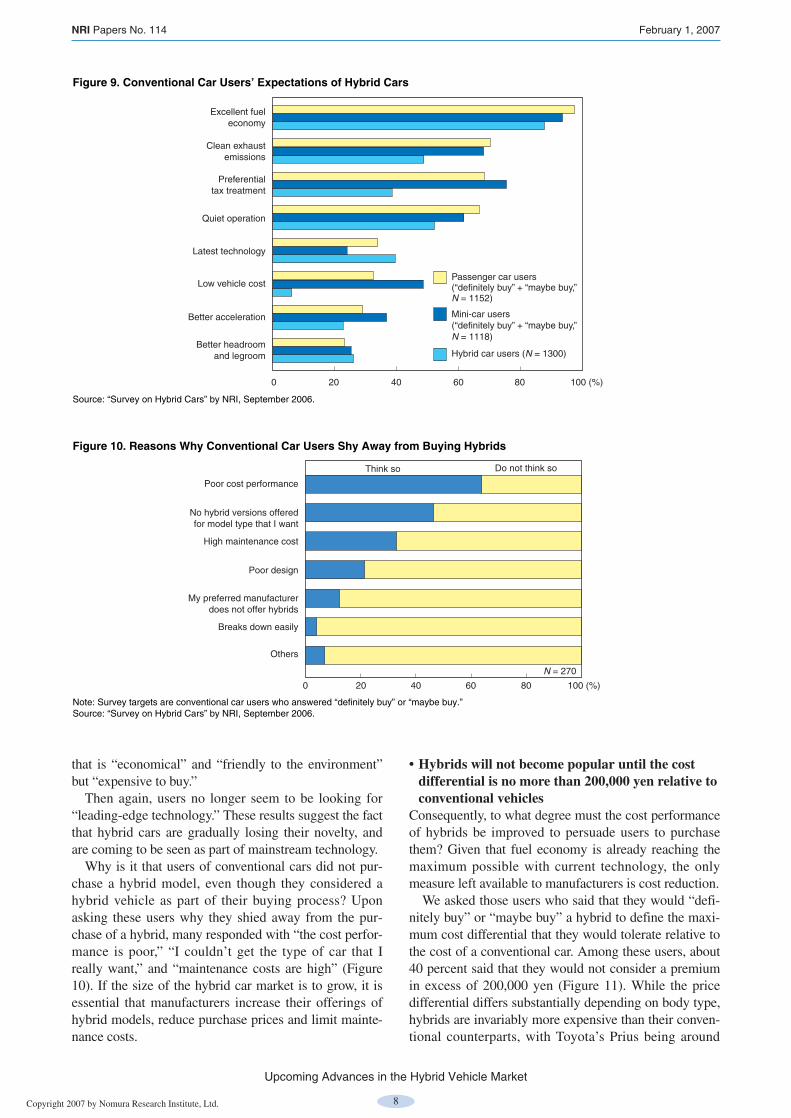

Of those persons considering the purchase of a hybridcar, we went on to ask what they would expect of thehybrid vehicle. Relative to existing hybrid users, wefound that expectations are higher across the board(Figure 9). That is, the responses point to a demand for a“more capable car at a lower price.” Such potential buyers are unlikely to entertain the tradeoff of a vehicle

NRI Papers No. 114 February 1, 2007

Upcoming Advances in the Hybrid Vehicle Market

Give first priority to ahybrid if conditions are right

64%

N = 300

Definitely buyanother hybrid

30%

Never buy a hybrid again1%

Want to give priorityto other systems

5%

Source: “Survey on Hybrid Cars” by NRI, September 2006.

Figure 6. Whether Hybrid Users Intend to Purchase Another Hybrid

Definitely buy20%

Maybe buy25%

Not buy 4%

Would thinkabout buying

42%

N = 600

Source: “Survey on Hybrid Cars” by NRI, September 2006.

Maybe not buy9%

Figure 8. Intention of Conventional Car Users to Buy Hybrid Cars

200 40 60 80 100 (%)

N = 300

Better value for the money including fuel economy and

vehicle purchase price

Want a hybrid version of a particular body type

Better environmental friendliness

More power as Ienjoy driving

Improved design such as external appearance and

interior appointments

Enhanced driving performance such as

better cornering

New functions (e.g., intelligent parking assist

systems)

More comfortable ride

Source: “Survey on Hybrid Cars” by NRI, September 2006.

Figure 7. Improvements Requested by Hybrid Car Users

Copyright 2007 by Nomura Research Institute, Ltd. 8

that is “economical” and “friendly to the environment”but “expensive to buy.”

Then again, users no longer seem to be looking for“leading-edge technology.” These results suggest the factthat hybrid cars are gradually losing their novelty, andare coming to be seen as part of mainstream technology.

Why is it that users of conventional cars did not pur-chase a hybrid model, even though they considered ahybrid vehicle as part of their buying process? Uponasking these users why they shied away from the pur-chase of a hybrid, many responded with “the cost perfor-mance is poor,” “I couldn’t get the type of car that Ireally want,” and “maintenance costs are high” (Figure10). If the size of the hybrid car market is to grow, it isessential that manufacturers increase their offerings ofhybrid models, reduce purchase prices and limit mainte-nance costs.

• Hybrids will not become popular until the costdifferential is no more than 200,000 yen relative toconventional vehicles

Consequently, to what degree must the cost performanceof hybrids be improved to persuade users to purchasethem? Given that fuel economy is already reaching themaximum possible with current technology, the onlymeasure left available to manufacturers is cost reduction.

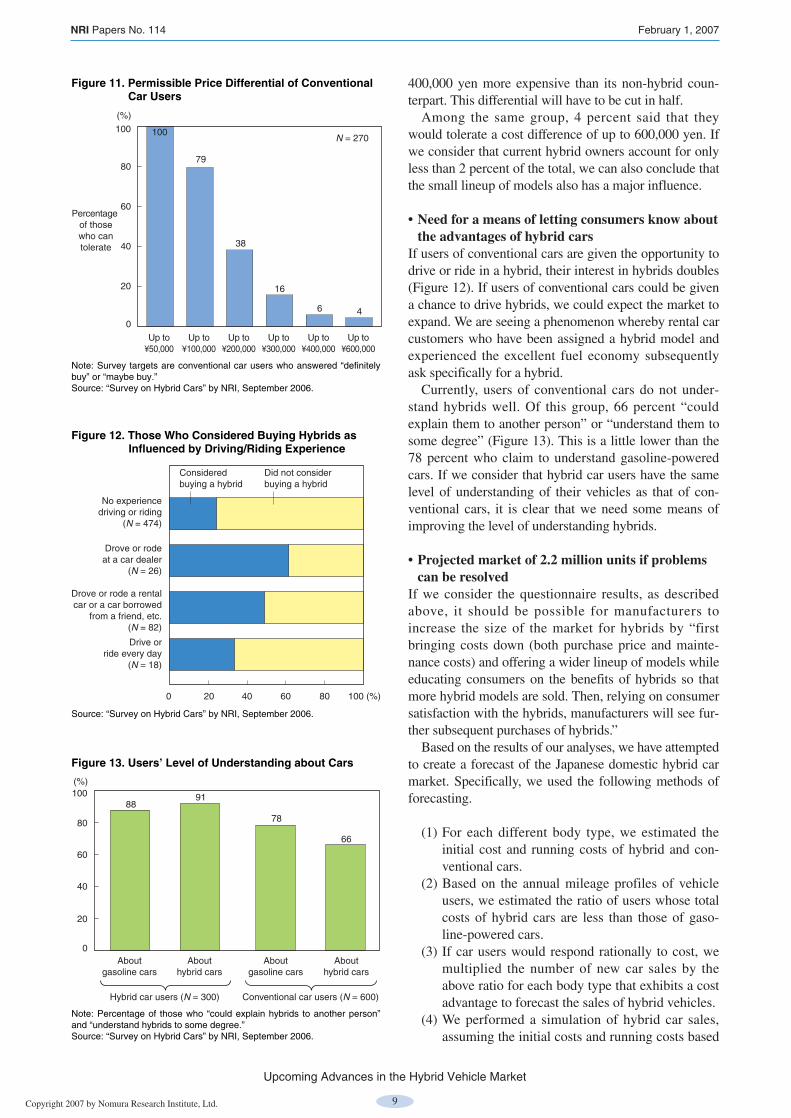

We asked those users who said that they would “defi-nitely buy” or “maybe buy” a hybrid to define the maxi-mum cost differential that they would tolerate relative tothe cost of a conventional car. Among these users, about40 percent said that they would not consider a premiumin excess of 200,000 yen (Figure 11). While the pricedifferential differs substantially depending on body type,hybrids are invariably more expensive than their conven-tional counterparts, with Toyota’s Prius being around

NRI Papers No. 114 February 1, 2007

Upcoming Advances in the Hybrid Vehicle Market

0 20 40 60 80 100 (%)

Excellent fueleconomy

Clean exhaustemissions

Preferentialtax treatment

Quiet operation

Latest technology

Low vehicle cost

Better acceleration

Better headroomand legroom

Source: “Survey on Hybrid Cars” by NRI, September 2006.

Figure 9. Conventional Car Users’ Expectations of Hybrid Cars

Passenger car users (“definitely buy” + “maybe buy,” N = 1152)

Mini-car users (“definitely buy” + “maybe buy,” N = 1118)

Hybrid car users (N = 1300)

Think so Do not think so

0 20 40 60 80 100 (%)

Note: Survey targets are conventional car users who answered “definitely buy” or “maybe buy.”Source: “Survey on Hybrid Cars” by NRI, September 2006.

Figure 10. Reasons Why Conventional Car Users Shy Away from Buying Hybrids

Poor cost performance

No hybrid versions offeredfor model type that I want

High maintenance cost

Poor design

My preferred manufacturerdoes not offer hybrids

Breaks down easily

Others

N = 270

Copyright 2007 by Nomura Research Institute, Ltd. 9

400,000 yen more expensive than its non-hybrid coun-terpart. This differential will have to be cut in half.

Among the same group, 4 percent said that theywould tolerate a cost difference of up to 600,000 yen. Ifwe consider that current hybrid owners account for onlyless than 2 percent of the total, we can also conclude thatthe small lineup of models also has a major influence.

• Need for a means of letting consumers know aboutthe advantages of hybrid cars

If users of conventional cars are given the opportunity todrive or ride in a hybrid, their interest in hybrids doubles(Figure 12). If users of conventional cars could be givena chance to drive hybrids, we could expect the market toexpand. We are seeing a phenomenon whereby rental carcustomers who have been assigned a hybrid model andexperienced the excellent fuel economy subsequentlyask specifically for a hybrid.

Currently, users of conventional cars do not under-stand hybrids well. Of this group, 66 percent “couldexplain them to another person” or “understand them tosome degree” (Figure 13). This is a little lower than the78 percent who claim to understand gasoline-poweredcars. If we consider that hybrid car users have the samelevel of understanding of their vehicles as that of con-ventional cars, it is clear that we need some means ofimproving the level of understanding hybrids.

• Projected market of 2.2 million units if problemscan be resolved

If we consider the questionnaire results, as describedabove, it should be possible for manufacturers toincrease the size of the market for hybrids by “firstbringing costs down (both purchase price and mainte-nance costs) and offering a wider lineup of models whileeducating consumers on the benefits of hybrids so thatmore hybrid models are sold. Then, relying on consumersatisfaction with the hybrids, manufacturers will see fur-ther subsequent purchases of hybrids.”

Based on the results of our analyses, we have attemptedto create a forecast of the Japanese domestic hybrid carmarket. Specifically, we used the following methods offorecasting.

(1) For each different body type, we estimated theinitial cost and running costs of hybrid and con-ventional cars.

(2) Based on the annual mileage profiles of vehicleusers, we estimated the ratio of users whose totalcosts of hybrid cars are less than those of gaso-line-powered cars.

(3) If car users would respond rationally to cost, wemultiplied the number of new car sales by theabove ratio for each body type that exhibits a costadvantage to forecast the sales of hybrid vehicles.

(4) We performed a simulation of hybrid car sales,assuming the initial costs and running costs based

NRI Papers No. 114 February 1, 2007

Upcoming Advances in the Hybrid Vehicle Market

N = 270100

Percentage of thosewho cantolerate

(%)

80

60

40

20

0

100

38

16

6 4

79

Up to¥50,000

Up to¥100,000

Up to¥200,000

Up to¥300,000

Up to¥400,000

Up to¥600,000

Note: Survey targets are conventional car users who answered “definitely buy” or “maybe buy.”Source: “Survey on Hybrid Cars” by NRI, September 2006.

Figure 11. Permissible Price Differential of Conventional Car Users

Considered buying a hybrid

Did not consider buying a hybrid

0 20 40 60 80 100 (%)

Source: “Survey on Hybrid Cars” by NRI, September 2006.

Figure 12. Those Who Considered Buying Hybrids as Influenced by Driving/Riding Experience

No experiencedriving or riding

(N = 474)

Drove or rodeat a car dealer

(N = 26)

Drive orride every day

(N = 18)

Drove or rode a rentalcar or a car borrowed

from a friend, etc.(N = 82)

100

80

60

40

20

0

Hybrid car users (N = 300) Conventional car users (N = 600)

66

78

9188

Aboutgasoline cars

Abouthybrid cars

Aboutgasoline cars

Abouthybrid cars

(%)

Note: Percentage of those who “could explain hybrids to another person” and “understand hybrids to some degree.”Source: “Survey on Hybrid Cars” by NRI, September 2006.

Figure 13. Users’ Level of Understanding about Cars

Copyright 2007 by Nomura Research Institute, Ltd. 10

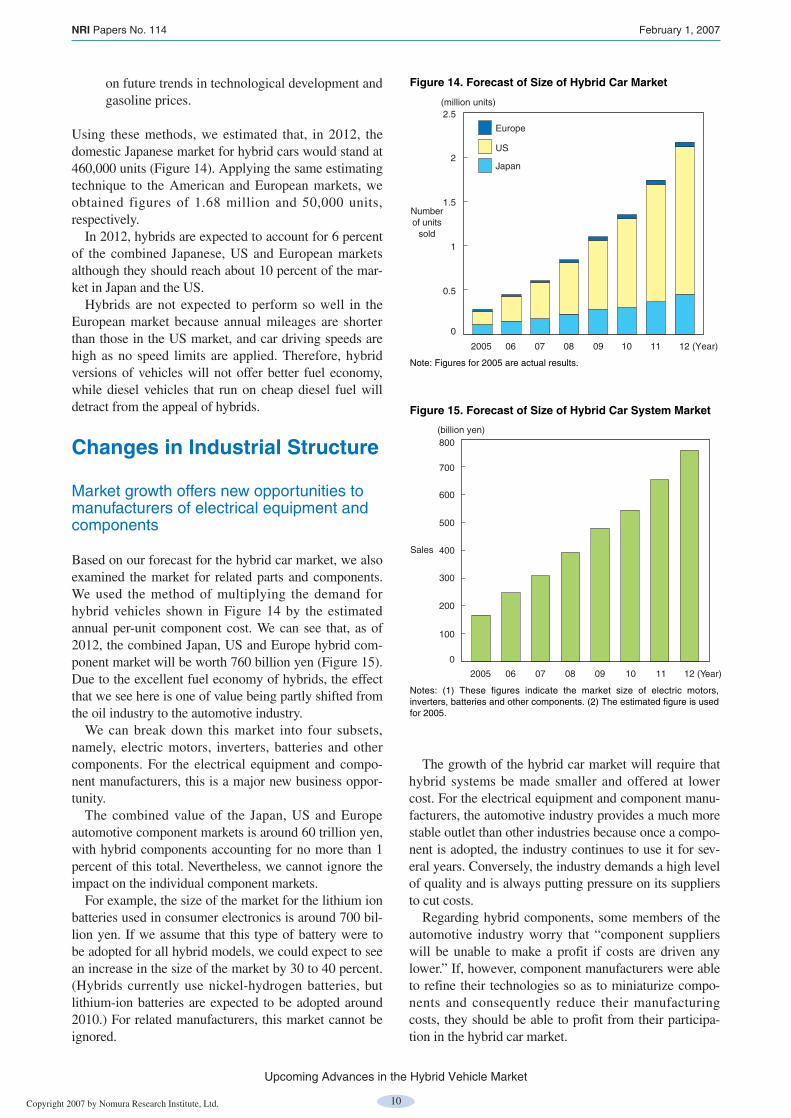

on future trends in technological development andgasoline prices.

Using these methods, we estimated that, in 2012, thedomestic Japanese market for hybrid cars would stand at460,000 units (Figure 14). Applying the same estimatingtechnique to the American and European markets, weobtained figures of 1.68 million and 50,000 units,respectively.

In 2012, hybrids are expected to account for 6 percentof the combined Japanese, US and European marketsalthough they should reach about 10 percent of the mar-ket in Japan and the US.

Hybrids are not expected to perform so well in theEuropean market because annual mileages are shorterthan those in the US market, and car driving speeds arehigh as no speed limits are applied. Therefore, hybridversions of vehicles will not offer better fuel economy,while diesel vehicles that run on cheap diesel fuel willdetract from the appeal of hybrids.

Changes in Industrial Structure

Market growth offers new opportunities tomanufacturers of electrical equipment andcomponents

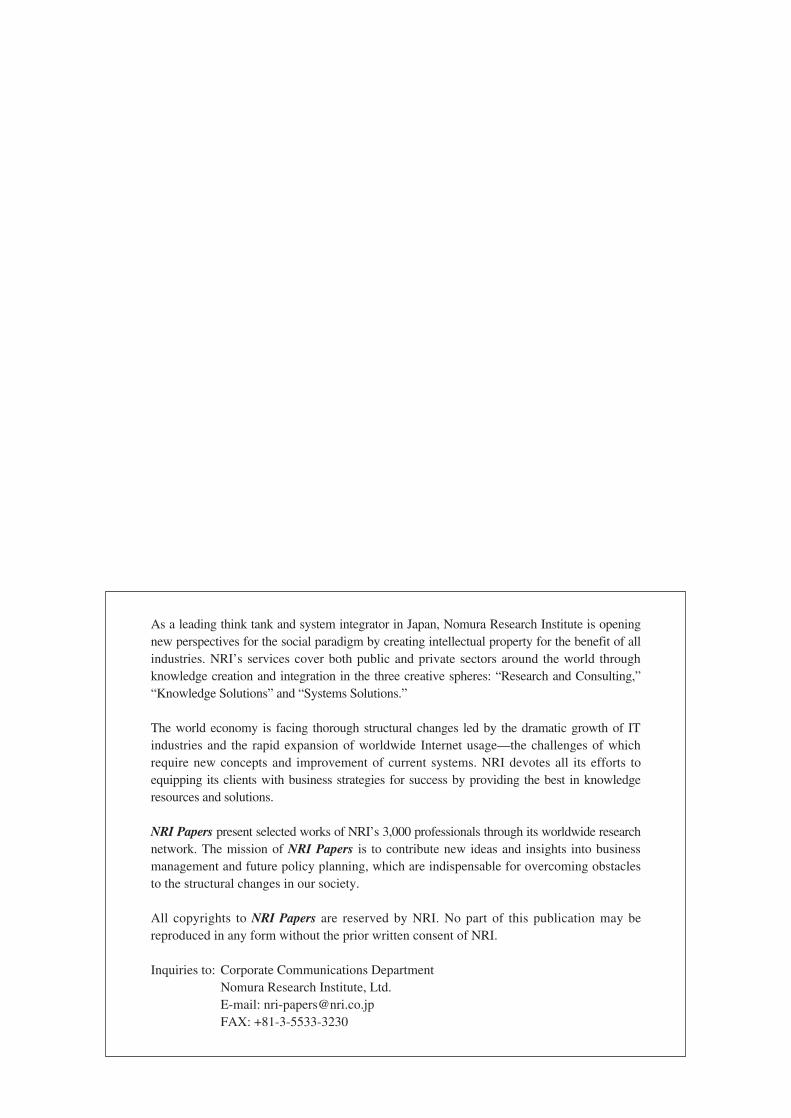

Based on our forecast for the hybrid car market, we alsoexamined the market for related parts and components.We used the method of multiplying the demand forhybrid vehicles shown in Figure 14 by the estimatedannual per-unit component cost. We can see that, as of2012, the combined Japan, US and Europe hybrid com-ponent market will be worth 760 billion yen (Figure 15).Due to the excellent fuel economy of hybrids, the effectthat we see here is one of value being partly shifted fromthe oil industry to the automotive industry.

We can break down this market into four subsets,namely, electric motors, inverters, batteries and othercomponents. For the electrical equipment and compo-nent manufacturers, this is a major new business oppor-tunity.

The combined value of the Japan, US and Europeautomotive component markets is around 60 trillion yen,with hybrid components accounting for no more than 1percent of this total. Nevertheless, we cannot ignore theimpact on the individual component markets.

For example, the size of the market for the lithium ionbatteries used in consumer electronics is around 700 bil-lion yen. If we assume that this type of battery were tobe adopted for all hybrid models, we could expect to seean increase in the size of the market by 30 to 40 percent.(Hybrids currently use nickel-hydrogen batteries, butlithium-ion batteries are expected to be adopted around2010.) For related manufacturers, this market cannot beignored.

The growth of the hybrid car market will require thathybrid systems be made smaller and offered at lowercost. For the electrical equipment and component manu-facturers, the automotive industry provides a much morestable outlet than other industries because once a compo-nent is adopted, the industry continues to use it for sev-eral years. Conversely, the industry demands a high levelof quality and is always putting pressure on its suppliersto cut costs.

Regarding hybrid components, some members of theautomotive industry worry that “component supplierswill be unable to make a profit if costs are driven anylower.” If, however, component manufacturers were ableto refine their technologies so as to miniaturize compo-nents and consequently reduce their manufacturingcosts, they should be able to profit from their participa-tion in the hybrid car market.

NRI Papers No. 114 February 1, 2007

Upcoming Advances in the Hybrid Vehicle Market

Numberof units

sold

(million units)

2

2.5

1.5

1

0.5

0

11 12 (Year)2005 06 07 08 09 10

Europe

US

Japan

Note: Figures for 2005 are actual results.

Figure 14. Forecast of Size of Hybrid Car Market

800

Sales

(billion yen)

700

600

500

400

300

200

100

0

11 12 (Year)2005 06 07 08 09 10

Notes: (1) These figures indicate the market size of electric motors, inverters, batteries and other components. (2) The estimated figure is used for 2005.

Figure 15. Forecast of Size of Hybrid Car System Market

Copyright 2007 by Nomura Research Institute, Ltd. 11

Suggestions for the Industry

Motor manufacturers should establish anopen development system with relatedsuppliers

Through only efforts in which car dealers offer consult-ing services to conventional car users, it is likely that wewould be able to see some increase in the size of thehybrid car market. However, there is no escaping the factthat the market must have a wider lineup of modelsoffered at prices that are more competitive. To this end,the major issue facing the industry is how to offersmaller-sized components that can be manufactured forlower cost. However, because motor manufacturers donot necessarily have the experience or expertise neededto manufacture these parts, there is a need for a systemwhereby components are jointly developed by motormanufacturers and electrical equipment and componentsuppliers.

Many electrical equipment and component manufac-turers are showing interest in the growing market. This isnot just limited to those manufacturers who are “familiarwith the auto market.” While many major electricalequipment and component manufacturers have set updedicated automotive marketing divisions and researchcenters, they do not have any means of identifying theneeds of the motor manufacturers. Without knowingwhat motor manufacturers actually need, it is impossible

to set clear component development objectives. If trulyneeded development objectives cannot be identified, thespecifications are likely to become excessive, makingcost-cutting difficult.

Some electrical equipment and component manufac-turers believe that “if they can learn exactly how a vehi-cle is to be used, they can develop optimum componentsat the lowest possible cost.” Other electrical equipmentand component manufacturers have a stance of “if theautomotive manufacturers will take the componentmanufacturers under their wing from the componentdesign stage, the chances of a breakthrough are greatlyimproved.”

Given the importance of their core technologies, it isdifficult to expect motor manufacturers to make thisinformation available. However, there is surely a need toestablish a relationship whereby the electrical equipmentand component manufacturers are involved in more ofthe process from the initial stages of development withboth sides striving to reduce costs so as to produce morecompact hybrid components at the lowest possible cost.

Yuki TANAKA is a consultant at NRI’s Technological andIndustrial Consulting Department I. His specialties includebusiness strategies and operational support for the materialsprocess technology, industrial machinery and automotivefields.Yukio SHIGETA is a consultant at NRI’s Technologicaland Industrial Consulting Department I. His specialtiesinclude business strategies and operational support for theenergy, battery, vehicle and chemical fields.

NRI Papers No. 114 February 1, 2007

Upcoming Advances in the Hybrid Vehicle Market

As a leading think tank and system integrator in Japan, Nomura Research Institute is openingnew perspectives for the social paradigm by creating intellectual property for the benefit of allindustries. NRI’s services cover both public and private sectors around the world throughknowledge creation and integration in the three creative spheres: “Research and Consulting,”“Knowledge Solutions” and “Systems Solutions.”

The world economy is facing thorough structural changes led by the dramatic growth of ITindustries and the rapid expansion of worldwide Internet usage—the challenges of whichrequire new concepts and improvement of current systems. NRI devotes all its efforts toequipping its clients with business strategies for success by providing the best in knowledgeresources and solutions.

NRI Papers present selected works of NRI’s 3,000 professionals through its worldwide researchnetwork. The mission of NRI Papers is to contribute new ideas and insights into businessmanagement and future policy planning, which are indispensable for overcoming obstaclesto the structural changes in our society.

All copyrights to NRI Papers are reserved by NRI. No part of this publication may bereproduced in any form without the prior written consent of NRI.

Inquiries to: Corporate Communications DepartmentNomura Research Institute, Ltd.E-mail: [email protected]: +81-3-5533-3230