Embed Size (px)

Citation preview

Figure 3: TITAN‟s Stock Prices and Volumes period 4/1/2010 – 27/1/2011

Figure 2: TITAN‟s Market Share in Greece

Table 1: Fundamental Data and Valuation Ratios

Highlights:

1. We recommend TITAN stock as a “Buy” on the grounds that current

domestic market conditions in Greece rendered it as an undervalued asset

by a percentage of 15% (as of 27/1/2011). 2. TITAN Group has been transformed to a truly Multinational Company

over the last years, expanding its activities to markets other than Greece.

Being present in both emerging and mature markets, it has offset negative

impacts in regions that have been affected adversely by recent financial

crisis, such as Greece, reducing its dependence on them. 3. EASTMED: it is the strongest growing region of the Group over the last

two years, offsetting, to a great extent, decline in other regions, driving the

group‟s profitability and representing the company‟s cash flow steam

engine. Prospects are extremely positive due to Egypt‟s strong domestic

demand that is hardly accommodated in full by domestic supply and the

new plant that became operational in 2009. 4. USA: construction market presents signs of stabilizing in historical low

levels anticipating that TITAN has passed through the worse. US economy

is expected to bounce up in the following two years, with construction

market following suit, once surpluses in housing market are reduced. In the

long term, extremely positive demographic trends enhance construction

market growth predictions. 5. S.E. EUROPE: TITAN has expanded its activities in Albania and Kosovo.

The start of production activity in 03/2010 of the newly built cement plant

in Albania has already affected positively the group‟s results. Positive

future economic prospects coupled with the need for fundamental

infrastructure in the region leave plenty of room for business growth in the

near future.

6. Cash Flow Generator: TITAN has been generating positive free cash

flows, even during the financially turbulent recent years. 7. Net Debt Exposure Reduction: TITAN has focused in reducing its Net

Debt exposure. Since 2008 year end a decrease of €241 mil. has been

achieved (30/09/2010 latest figures).

Still being a TITAN

University of Piraeus Student Research

This report is published for educational purposes only

by students competing in the

Hellenic CFA Society Investment Research Challenge

TITAN Cement S.A.

27th of January 2011

TITAN Cement S.A.

January 2011

Company Stock Data

Reuters Code TTNr.AT

Bloomberg code TITK:GA

Market Cap 1344.75 as of

the 27th of

January 2011

No Shares outstand. 84,576m

1m 6m 12m

Absolute

Performance -1.42% -2.98% -22.54%

Relative

Performance 8.65% 4.95% 1.85%

Rating: Buy

Target Price: € 19.6 Current Price: € 15.9

ROE: 7.5%

Free float: 73%

Constructing

& Building Materials

Share Price Performance

Share Price Performance

Figure 1: TITAN‟s four-pronged Strategy

2009a 2010e 2011f 2012f

Net Profit 123.4 113 119 153

EV/EBITDA 8.2 6.63 6.27 5.38

P/E(x) 12.8 12.29 11.67 9.08

EV 2,186.5 2,260.1 2,179.3 2,101.2

Sales 1,361 1,342 1,402 1,508

EPS 1.46 1.34 1.41 1.81

DPS 0.18 0.40 0.42 0.54

EBITDA 329.8 341 347.4 390.7

1

University of Piraeus Investment Research Challenge Student Research 27/1/2011

2

Business Description

TITAN was founded in Greece in 1902. Its history spans in more than

100 years during which the company has been a strong player in the

Greek market. The group has been investing on modern technological

production methods and effective administrative patterns, focusing on

the human factor. With its headquarters in Greece –where the parent

company has been listed on the Athens Stock Exchange since 1912–

TITAN Group‟s vertically integrated ac tivity spans in 12 countries.

Since 1990‟s, it has been pursuing a twin expansion strategy of

geographical diversification and vertical integration; today, it has

operations in Greece, USA, South Eastern Europe and Eastern

Mediterranean carrying out its activities through wholly-owned

affiliated companies and joint ventures with other partners. The

company generates revenues from Cement, Ready Mix Concrete,

Aggregate and other material product Sales. All three are the main

products of the heavy building materials industry are Cement and

Concrete. Concrete (EBITDA Margin 5%-15%) is second only to water

as the most consumed substance on earth, with nearly one ton of the

material used annually for each person on the planet. Cement (EBITDA

Margin 30%-40%) is the critical ingredient in concrete, locking together

the sand and gravel constituents (Aggregates with EBITDA Margin

10%-30%) in an inert matrix; it is the „glue‟ which holds together much

of modern society‟s infrastructure. Over the last few years, TITAN

Group has increased its economic dependence on cement, both in

earnings and turnover.

TITAN Business Strategy

Geographic Diversification

It gives the opportunity for sales growth, mitigates the high transport

cost of this heavy, low-value material and spreads the risk of decline

across multiple regional markets.

Vertical Integration

In 2009, some 41% of TITAN‟s Turnover is in non-cement

products sales, such as ready-mix concrete, aggregates,

cement blocks, mortars and porcelain, spreading the risk

inherent in being a single product business.

TITAN Strategic Goals

Maintaining Cash Flow Level

Reduction of Net Debt

Reduction of Production Costs

Limiting Capital Needs - Withold Capex

Region Country Plants

Ready

Mix

Concrete

Stations

Cement

Distr.

Termin

als

% of Total

Cement

Production

Capacity

GRE &

W.EUR.

GRE 4 31 5 29.66%

UK 0 0 1

FRA 0 0 1

ITA 0 0 1

SUM W.EUR. 4 31 8 29.66%

USA USA 2 96 3 14.83%

SUM USA 2 96 3 14.83%

S.E.

EUR.

ALB 2 0 2 6.36%

SER 1 0 0 5.93%

KOS 1 0 0 2.54%

FYROM 1 1 0 3.39%

BULG 1 6 0 5.51%

SUM S.E.EUR. 6 7 2 23.73%

EASTER

N MED.

TUR 1 0 1 10.59%

EGY 2 1 0 21.19%

SUM EAST.MED 3 1 1 31.78%

TOTAL 15 135 14 100.00%

Figure 4: Regional % of Total Production Capacity 2009

Table 2: Regional Breakdown of Cement Production capacity

USA

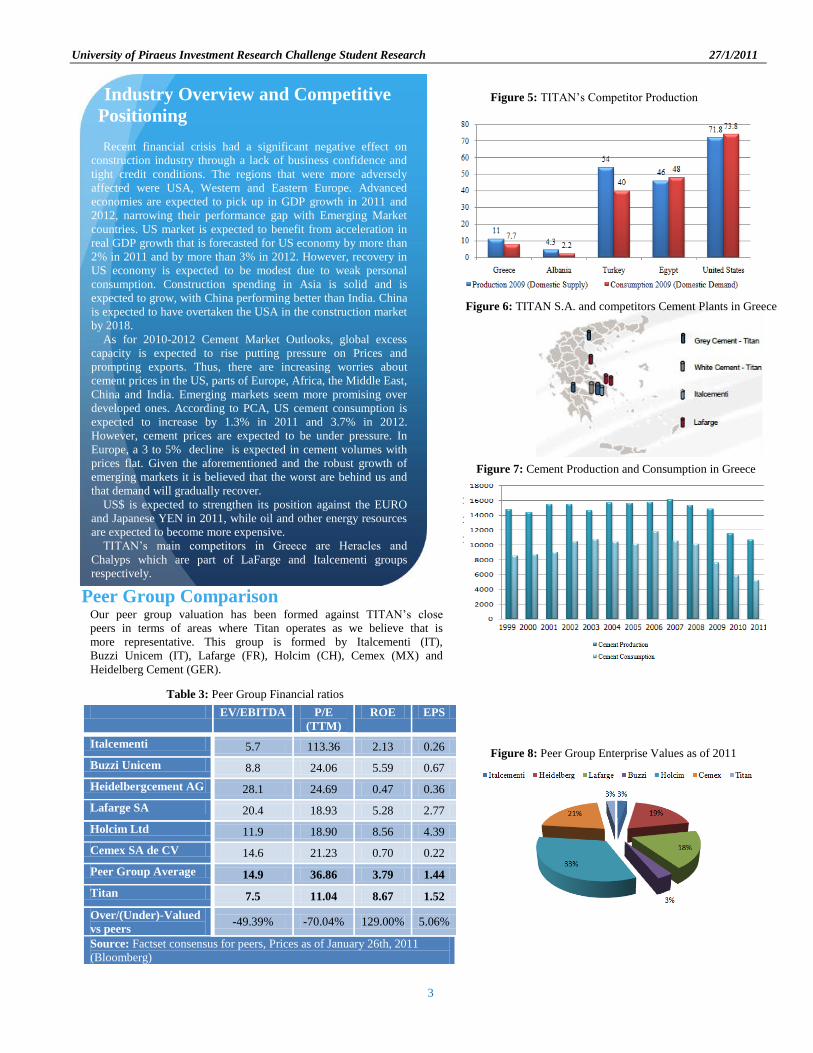

In 2009, more than half of TITAN Group‟s Non-Current

Assets were located in Western Europe, and in most part in

Greece. North America and Eastern Mediterranean account

for 1/5 of the group‟s non-current assets each, while South

Eastern Europe accounts only for 10% of the group‟s non-

current assets. In 2008 EastMed increased its share due to the

built up of a second cement production line in Beni Suef, as

the group aims at responding to Egypt‟s strong domestic

demand. Furthermore, the built up of a new cement

production plant in Albania was concluded, which will further

geographical diversification of the group‟s non current

Assets. Its production capacity is 1.5 mil. MT., enhancing

TITAN‟s presence in the region, boosting its Sales and

spreading the group‟s risk.

In 2009, more than half of TITAN Group‟s Non-Current

Assets were located in Western Europe, and in most part in

Greece. North America and Eastern Mediterranean account

for 1/5 of the group‟s non-current assets each, while South

Eastern Europe accounts only for 10% of the group‟s non-

current assets. In 2008 we note a significant increase in

Eastern Mediterranean‟s share due to the built up of a second

cement production line in Beni Suef, as the group aims at

responding to Egypt‟s strong domestic demand. Furthermore,

the built up of a new cement production plant in Albania was

concluded, which will rise the share of South Eastern Europe

in the group‟s non current Assets. Its production capacity is

1.5 mil. MT., enhancing TITAN‟s presence in the region and

boosting its Sales.

2

University of Piraeus Investment Research Challenge Student Research 27/1/2011

3

Industry Overview and Competitive

Positioning

Recent financial crisis had a significant negative effect on

construction industry through a lack of business confidence and

tight credit conditions. The regions that were more adversely

affected were USA, Western and Eastern Europe. Advanced

economies are expected to pick up in GDP growth in 2011 and

2012, narrowing their performance gap with Emerging Market

countries. US market is expected to benefit from acceleration in

real GDP growth that is forecasted for US economy by more than

2% in 2011 and by more than 3% in 2012. However, recovery in

US economy is expected to be modest due to weak personal

consumption. Construction spending in Asia is solid and is

expected to grow, with China performing better than India. China

is expected to have overtaken the USA in the construction market

by 2018.

As for 2010-2012 Cement Market Outlooks, global excess

capacity is expected to rise putting pressure on Prices and

prompting exports. Thus, there are increasing worries about

cement prices in the US, parts of Europe, Africa, the Middle East,

China and India. Emerging markets seem more promising over

developed ones. According to PCA, US cement consumption is

expected to increase by 1.3% in 2011 and 3.7% in 2012.

However, cement prices are expected to be under pressure. In

Europe, a 3 to 5% decline is expected in cement volumes with

prices flat. Given the aforementioned and the robust growth of

emerging markets it is believed that the worst are behind us and

that demand will gradually recover.

US$ is expected to strengthen its position against the EURO

and Japanese YEN in 2011, while oil and other energy resources

are expected to become more expensive.

TITAN‟s main competitors in Greece are Heracles and

Chalyps which are part of LaFarge and Italcementi groups

respectively.

Our peer group valuation has been formed against TITAN‟s close

peers in terms of areas where Titan operates as we believe that is

more representative. This group is formed by Italcementi (IT),

Buzzi Unicem (IT), Lafarge (FR), Holcim (CH), Cemex (MX) and

Heidelberg Cement (GER).

EV/EBITDA P/E

(TTM)

ROE EPS

Italcementi 5.7 113.36 2.13 0.26

Buzzi Unicem 8.8 24.06 5.59 0.67

Heidelbergcement AG 28.1 24.69 0.47 0.36

Lafarge SA 20.4 18.93 5.28 2.77

Holcim Ltd 11.9 18.90 8.56 4.39

Cemex SA de CV 14.6 21.23 0.70 0.22

Peer Group Average 14.9 36.86 3.79 1.44

Titan 7.5 11.04 8.67 1.52

Over/(Under)-Valued

vs peers -49.39% -70.04% 129.00% 5.06%

Source: Factset consensus for peers, Prices as of January 26th, 2011

(Bloomberg)

Figure 5: TITAN‟s Competitor Production plants in Greece

Figure 5

Figure 8: Peer Group Enterprise Values as of 2011

Table 3: Peer Group Financial ratios

Peer Group Comparison

Figure 6: TITAN S.A. and competitors Cement Plants in Greece

plants in Greece

Figure 7: Cement Production and Consumption in Greece

plants in Greece

3

University of Piraeus Investment Research Challenge Student Research 27/1/2011

4

TITAN’s Financial and Business Profile TITAN has been transforming to a multi-national group with affiliate companies in regions other than Greece, decreasing its dependence in the

challenging Greek market. The new cement plants in Albania and Egypt have furthered the group‟s geographical expansion, diversifying its risk

exposure. In this context, TITAN managed to sustain the same level of EBITDA Margin in 2009 compared to 2008, which is notable while

reckoning the difficulties it faces in its two main markets, namely Greece and USA.

Strong growth in Turnover and Profitability in EastMed has partly offset the decrease faced in Greece, USA and S.E. Europe countries. The

Group has noted a decline in sales of all three types of its products (cement, ready mixed concrete, aggregates), the most important being in

ready-mixed concrete. However, further increase in Sales in Egypt, slow recovery in US market in the mid-term and positive impact from new

plant in Albania are expected to enhance the geographical diversification positive impact on the Group‟s Sales and Profitability.

From 2006 onwards turnover and profitability of the Group has been increasingly relying on sales of cement. In 2009, cement had almost 70%

of total sales generating an overwhelming 80% of the group‟s operating profits.

TITAN operates with a Gross Profit Margin that is constantly over 30%, thanks to a remarkable relative stable analogy that the group achieves

between COGS and Turnover. TITAN has been facing a relative decline in Turnover and Profitability, thus pursuing a strategy of cost and

expenses reduction.

In 30/09/2010, Titan Group‟s Turnover was decreased by 1.7%, EBITDA was increased by 0.9% and EBITDA Margin increased by 0.7%

compared to the corresponding period of the previous year.

Investment Summary SWOT ANALYSIS

Strengths

Geographical Diversification of the Group with

presence in both mature and emerging markets

Vertical Integration of operations with economic

activity in several other markets than cement

(aggregates, ready mix concrete and other minor

products)

Strong Market Shares in all markets of Operation

Co-Leading Player in Greek Market

Sound, effective and experienced management team

Opportunities

Well foreseen penetration in Egypt which compensates

in part for decline in other markets.

Well placed in S.E. Europe, Turkey and USA to

benefit from future recovery.

Visionary project of substituting fossil fuels with bio-

fuels.

Signs of stability in low levels of cement consumption

in US market and expectations for recovery in the

near future.

Figure 9: 2009 Profit-Production Capacity

Figure 10: 2008 Profit-Production Capacity

Assets

Production

capacity

Non

Current

Assets

Turnover EBITDA EBITDA

Margin

Greece Greece USA USA S.E Eur. Eur.Euro

pe

S.E. Eur. East Med. East Med.

Weaknesses

Uncertainty concerning the period of recovery in

Greek economy and Greek market, which is

forecasted for further decline in 2011

Negative impact of economic crisis in weak

economies of S.E. Europe

Threats

Increased Costs (Fuel, Ocean Freights, Energy)

Increasing Trend in US$ Libor

Increased Export activity from Turkey with low cost

cement that put pressure on prices in Bulgaria.

Pressure on Prices in FYROM

Further decline in Greek economy and construction

market with weak domestic demand, consumption

and disposable income.

Gr &W.Eur. Gr &W.Eur.

University of Piraeus Investment Research Challenge Student Research 27/1/2011

5

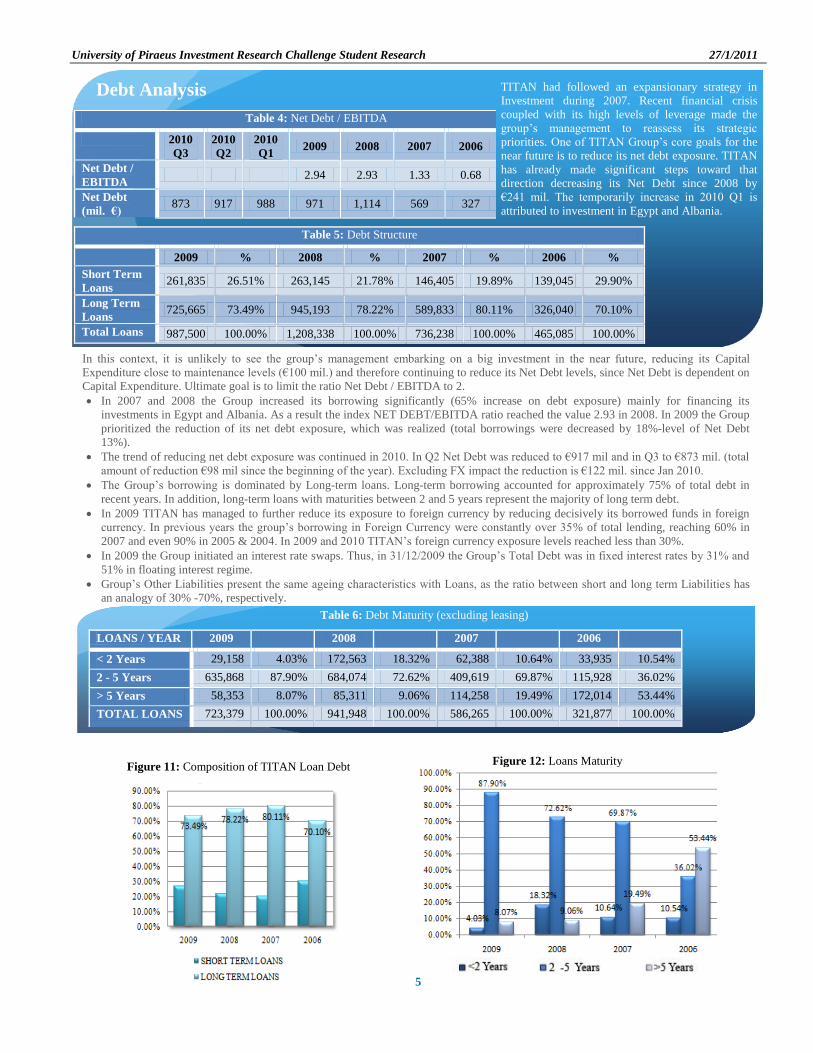

Table 5: Debt Structure

2009 % 2008 % 2007 % 2006 %

Short Term

Loans 261,835 26.51% 263,145 21.78% 146,405 19.89% 139,045 29.90%

Long Term

Loans 725,665 73.49% 945,193 78.22% 589,833 80.11% 326,040 70.10%

Total Loans 987,500 100.00% 1,208,338 100.00% 736,238 100.00% 465,085 100.00%

Table 6: Debt Maturity (excluding leasing)

Table 4: Net Debt / EBITDA

2010

Q3

2010

Q2

2010

Q1 2009 2008 2007 2006

Net Debt /

EBITDA 2.94 2.93 1.33 0.68

Net Debt

(mil. €) 873 917 988 971 1,114 569 327

Debt Analysis

In this context, it is unlikely to see the group‟s management embarking on a big investment in the near future, reducing its Capital

Expenditure close to maintenance levels (€100 mil.) and therefore continuing to reduce its Net Debt levels, since Net Debt is dependent on

Capital Expenditure. Ultimate goal is to limit the ratio Net Debt / EBITDA to 2.

In 2007 and 2008 the Group increased its borrowing significantly (65% increase on debt exposure) mainly for financing its

investments in Egypt and Albania. As a result the index NET DEBT/EBITDA ratio reached the value 2.93 in 2008. In 2009 the Group

prioritized the reduction of its net debt exposure, which was realized (total borrowings were decreased by 18%-level of Net Debt

13%).

The trend of reducing net debt exposure was continued in 2010. In Q2 Net Debt was reduced to €917 mil and in Q3 to €873 mil. (total

amount of reduction €98 mil since the beginning of the year). Excluding FX impact the reduction is €122 mil. since Jan 2010.

The Group‟s borrowing is dominated by Long-term loans. Long-term borrowing accounted for approximately 75% of total debt in

recent years. In addition, long-term loans with maturities between 2 and 5 years represent the majority of long term debt.

In 2009 TITAN has managed to further reduce its exposure to foreign currency by reducing decisively its borrowed funds in foreign

currency. In previous years the group‟s borrowing in Foreign Currency were constantly over 35% of total lending, reaching 60% in

2007 and even 90% in 2005 & 2004. In 2009 and 2010 TITAN‟s foreign currency exposure levels reached less than 30%.

In 2009 the Group initiated an interest rate swaps. Thus, in 31/12/2009 the Group‟s Total Debt was in fixed interest rates by 31% and

51% in floating interest regime.

Group‟s Other Liabilities present the same ageing characteristics with Loans, as the ratio between short and long term Liabilities has

an analogy of 30% -70%, respectively.

LOANS / YEAR 2009 2008 2007 2006

< 2 Years 29,158 4.03% 172,563 18.32% 62,388 10.64% 33,935 10.54%

2 - 5 Years 635,868 87.90% 684,074 72.62% 409,619 69.87% 115,928 36.02%

> 5 Years 58,353 8.07% 85,311 9.06% 114,258 19.49% 172,014 53.44%

TOTAL LOANS 723,379 100.00% 941,948 100.00% 586,265 100.00% 321,877 100.00%

TITAN had followed an expansionary strategy in

Investment during 2007. Recent financial crisis

coupled with its high levels of leverage made the

group‟s management to reassess its strategic

priorities. One of TITAN Group‟s core goals for the

near future is to reduce its net debt exposure. TITAN

has already made significant steps toward that

direction decreasing its Net Debt since 2008 by

€241 mil. The temporarily increase in 2010 Q1 is

attributed to investment in Egypt and Albania.

Figure 11: Composition of TITAN Loan Debt

Figure 12: Loans Maturity

University of Piraeus Investment Research Challenge Student Research 27/1/2011

6

WACC 9,0%

PV of Cash Flows 1,168.250

Residual Value 1,388.655

Firm Value 2,556.905

Less: Net Debt end 2010E 876.472

Less: Minority rights 20,830

Equity Value 1,659.603

Number of shares (in million) 84,576

Per share Year End 2011 19.6

Assumptions for Constant Growth Period

13 - '20

Expected growth in EBIT 4.0%

Return on capital 14.6%

Reinvestment rate 27.4%

(In mill except

stock price and

ratio)

Explicit

Estimates

Terminal

Value

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Risk Free rate 6.5% 6.5% 6.5% 6.5% 6.5% 6.5% 6.5% 6.5% 6.5% 6.5%

Risk premium 3.5% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5%

Market return 10.1% 10.1% 10.1% 10.1% 10.1% 10.1% 10.1% 10.1% 10.1% 10.1%

Beta 0.97 0.97 0.97 0.97 0.97 0.97 0.97 0.97 0.97 0.97

Rate on Debt 7.4% 7.4% 7.4% 7.4% 7.4% 7.4% 7.4% 7.4% 7.4% 7.4%

Debt/(Debt+Market

Value) 38.0% 38.0% 38.0% 38.0% 38.0% 38.0% 38.0% 38.0% 38.0% 38.0%

Ke=Rf+B(Rm-Rf) 10.0% 10.0% 10.0% 10.0% 10.0% 10,0% 10,0% 10,0% 10.0% 10.0%

WACC= 9.0% 9.0% 9.0% 9.0% 9.0% 9.0% 9.0% 9.0% 9.0% 9.0%

Discounting Factor 0.92 0.84 0.77 0.71 0.65 0.60 0.55 0.50 0.46 0.42

EBIT 225.301 267.994 278.714 289.862 301.457 313.515 326.056 339.098 352.662 366.768 381.439

Less: Tax 39.026 50.179 63.937 66.494 69.154 71.920 74.797 77.789 80.901 84.137 87.502

After tax EBIT 186.275 217.815 214.777 223.368 232.303 241.595 251.258 261.309 271.761 282.632 293.937

Less: Working

Capital additions 12.772 43.584 45.327 47.140 49.026 50.987 53.027 55.148 57.354 59.648 0.000

Plus: depreciation 122.100 122.711 127.619 132.724 138.033 143.554 149.296 155.268 161.479 167.938 0.000

Less: Cap ex 105.280 95.320 85.190 88.598 92.142 95.827 99.660 103.647 107.793 112.104 0.000

Free Cash Flow 190.323 201.621 155.979 162.218 168.707 175.455 182.473 189.772 197.363 205.258 293.937

Discounted Free

Cash Flows 174.660 169.801 120.551 115.056 109.810 104.804 100.026 95.466 91.114 86.960

We calculate our target price through the DCF Valuation method. Our

WACC assumption is 9%. We forecasted cash flows up to 2012 and by

considering a growth rate of 4% up to 2020 we structure the rest Cash

Flows. The risk free rate was calculated considering a weighted average

of the 10-year government bonds in the countries in which TITAN has

presence. A Risk Premium of 3.5% is assumed, based on the „sales per

region‟ used as a weighted factor multiplied by spreads of treasury bonds

(using the German T-bond as a basis) in the areas where TITAN S.A

operates. Our beta is calculated considering data provided by the Athens

Stock Exchange (where Titan S.A. is listed).

Our DCF Model

Valuation DCF Valuation Model

University of Piraeus Investment Research Challenge Student Research 27/1/2011

7

Table 7: Sales Breakdown by Region

€ m 2009 2010e 2011f 2012f

Greece

&W.Europe

504 430 400 409

% change -20% -15% -7% 2%

% of sales 37% 32% 29% 27%

USA (in €) 366 317 330 358

% change -24% -13% 4% 8%

% of sales 27% 24% 24% 24%

SE EUROPE 216 244 267 288

% change -25% 13% 9% 8%

% of sales 16% 18% 19% 19%

E. MED 275 351 405 453

% change 58% 28% 15% 12%

% of sales 20% 26% 29% 30%

Total Sales 1,361 1,342 1,402 1,508

% change -14% -1% 4% 8%

Titan 6.63 11.042 8.674 1.517

Over/(Under)-Valued vs peers -25.14% -70.04% 129.00% 5.06%

Source: Factset consensus for peers, Prices as at January 20, 2011

Table 8: EBITDA Breakdown by Region

€ m 2009 2010e 2011f 2012f

Greece &W.Europe 128 93 80 84

% change -24% -27% -13% 5%

% of EBITDA 39% 27% 23% 21%

EBITDA margin 25% 22% 20% 21%

USA (in €) 26 19 21 25

% change -40% -25% 8% 18%

% of EBITDA 8% 6% 6% 6%

EBITDA margin 7.0% 6% 6% 7%

SE EUROPE 74 80 58 55

% change -30% 8% -27% -5%

% of EBITDA 22% 23% 17% 14%

EBITDA margin 34% 33% 22% 19%

E. MED 103 149 188 227

% change 62% 45% 26% 21%

% of EBITDA 31% 44% 54% 58%

EBITDA margin 38% 42% 46% 50%

Total EBITDA 330 341 347 391

% change -13% 3% 2% 12%

EBITDA margin 24.3% 25.4% 24.8% 25.9%

Financial Analysis

GREECE& W. EUROPE

We expect that present market conditions will continue in 2011 with main characteristics being tight credit in mortgage loans, declining

construction market, both public and private, large excess of unsold properties in real estate and weak domestic demand. All these can be

seen in a wider context of negative growth, declining consumption and disposable income, high rate of unemployment and increasing

inflation rate.

USA

US economy was officially in recession in 2008-2009 having strong negative effects in the construction Market. As construction indices

have given signs of stabilizing in historical low levels, it is believed that the market has hit bottom and that the group has already passed

through the worse. PCA recently forecasted cement consumption to increase by 0,7% in 2010 and by 1.3% in 2011, following slight

upward trends in GDP growth. While robust recovery in the construction market is not visible before mid 2011, with building activity

and cement consumption remaining weak, yet it is anticipated that in a general context of a bounce up of the US economy in the

following two years, construction market will start to improve. Moreover, in the long term, positive prospects in the market are

reinforced by very positive demographic trends in the US.

S.E EUROPE

In 3Q 2010, S.E. Europe countries, in general, were still under the cloud of global financial crisis, with domestic demand noting

decreasing trends. Yet, the start of production activity in Albania and the expansion of activities in Kosovo led to improved results as

Turnover increased by 7.5% compared to 3Q 2009. In addition we assume that imports in Bulgaria from Turkey, will be reduced due to

the expected increase in domestic demand in Turkey for the period 2011-2012. Regarding future prospects positive economic growth

forecasts are coupled with increased infrastructure needs in this region given the fact that Bulgaria is already an EU country and the rest

are interested in joining the EU; the need for contemporary public transport infrastructures is imperative.

EAST. MED.

Eastern Mediterranean was the strongest growing region for the Group over the last two years, offsetting, to a great extent, decline in

other regions. The Group recorded a significant increase in profitability and sales due to continued high demand in Egypt and the

acquisitions in Egypt and Turkey. In the near future it is anticipated that the region should maintain the positive momentum of domestic

demand growth. Turkey is expected to continue its strong economic recovery with positive impact in private and public construction

activity. It will remain as one of major cement exporters, despite the fact that domestic demand is expected to increase. Yet, it is

expected to face increasing fuel costs. Egypt is expected to continue its increased demand for cement but in a more gently pace. Both

countries have extremely positive demographic and urbanization trends coupled with healthy banking systems with growing potentials in

mortgage market.

University of Piraeus Investment Research Challenge Student Research 27/1/2011

8

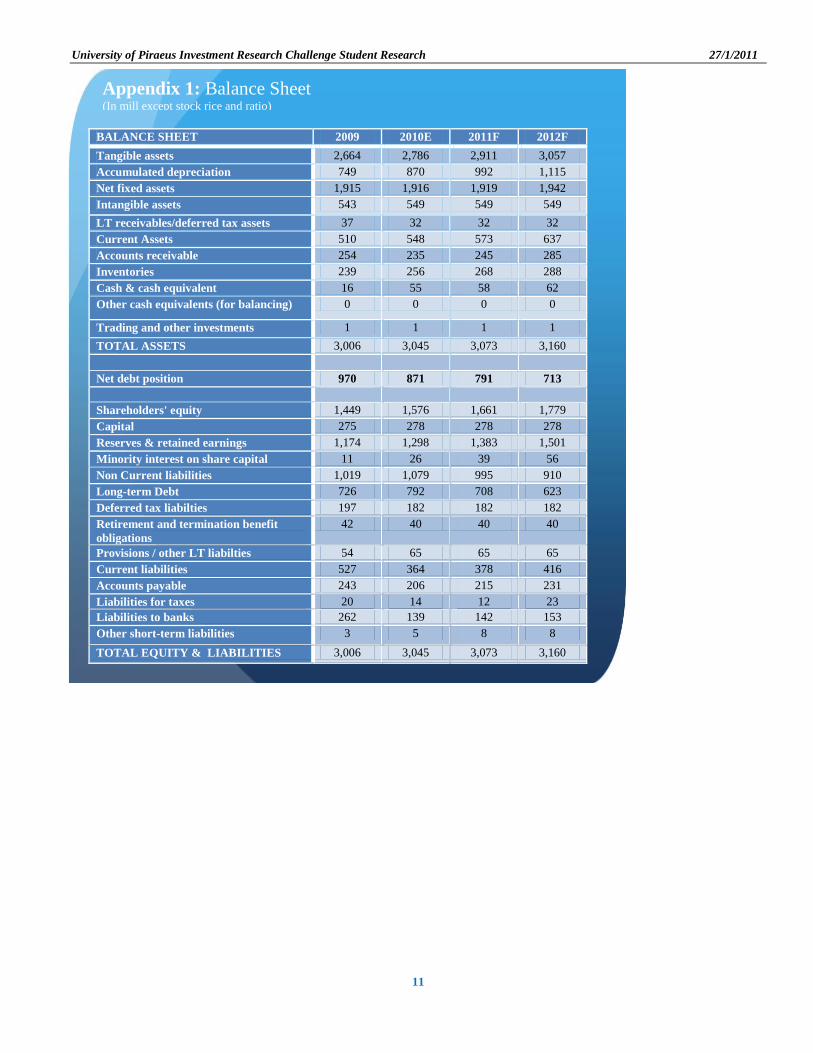

Table 9: Balance Sheet 2009 2010E 2011F 2012F

Net fixed assets 1,915 1,916 1,919 1,942

Current Assets 510 548 573 637

Cash & cash equivalent 16 55 58 62

TOTAL ASSETS 3,006 3,045 3,073 3,160

Net debt position 970 876 791 713

Shareholders' equity 1,449 1,576 1,661 1,779

Non Current liabilities 1,019 1,079 995 910

Long-term Debt 726 792 708 623

Current liabilities 527 364 378 416

Liabilities to banks 262 139 142 153

TOTAL EQUITY & LIABILITIES 3,006 3,045 3,073 3,160

Balance Sheet (In mill except stock rice and ratio)

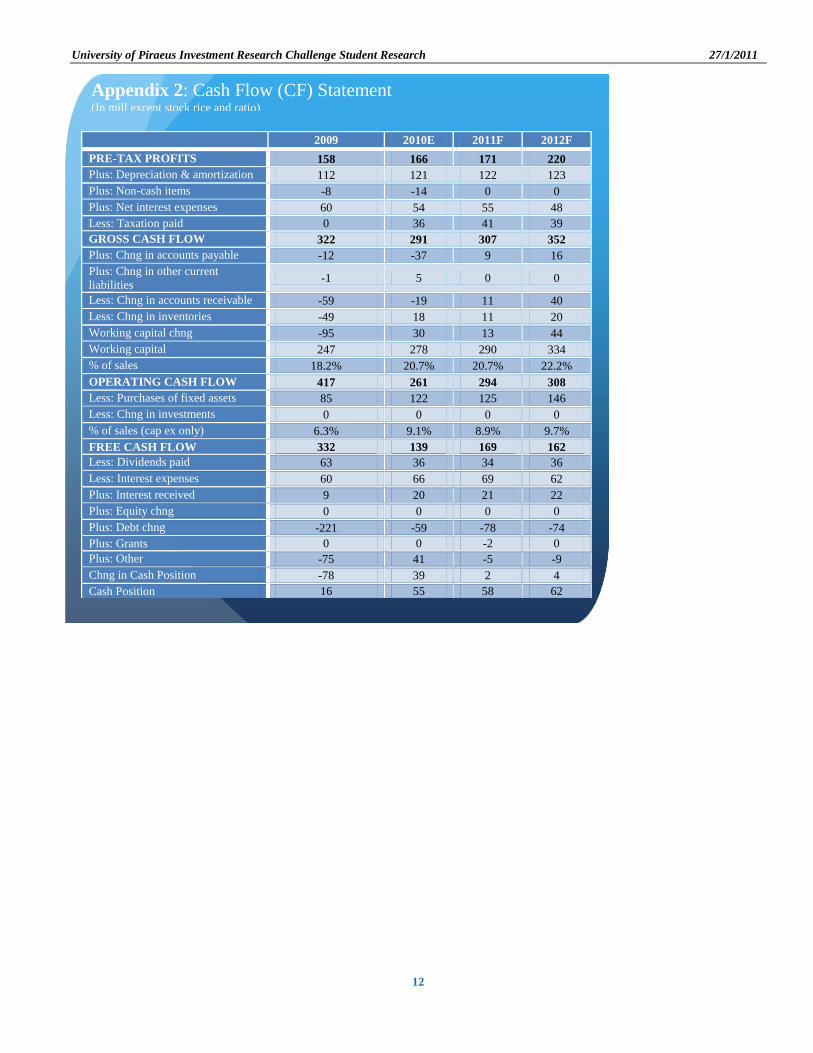

Table 10: Cash Flow (Cf) Statement 2009 2010E 2011F 2012F

Pre-tax profits 158 166 171 220

Gross cash flow 322 291 307 352

Operating Cash Flow 417 261 294 308

Free Cash Flow 332 139 169 162

Chng in Cash Position -78 39 2 4

Cash Position 16 55 58 62

Cash Flow (CF) Statement (In mill except stock rice and ratio)

Table 11: Profit & Loss (P&L) Items 2009 2010E 2011F 2012F

Sales 1,361 1,342 1,402 1,508

Total gross profit 485 494 507 563

EBITDA 330 341 347 391

Operating profit (EBIT) 217 219 225 268

Pre-tax profit 158 166 171 220

Profit after tax 123 113 119 153

Dividends 36 34 36 46

Profit & Loss (P&L) Items (In mill except stock rice and ratio)

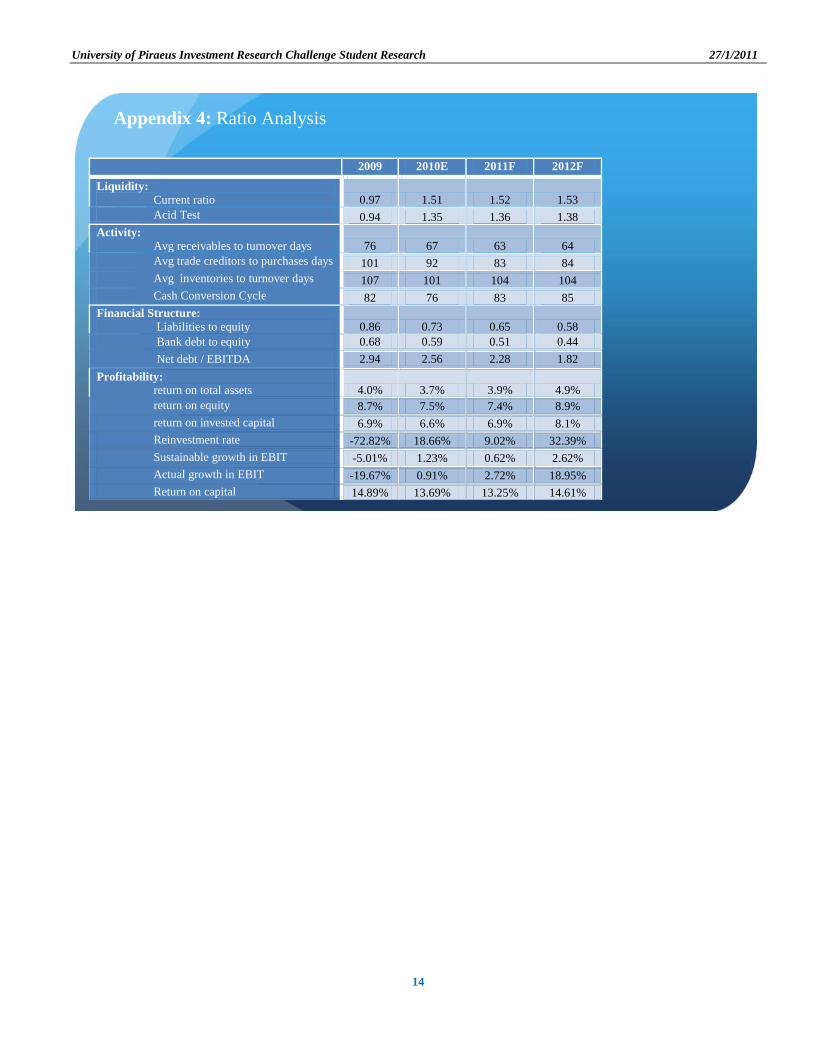

Table 12: Ratio Analysis 2009 2010E 2011F 2012F

Liquidity: Current ratio 0.97 1.51 1.52 1.53

Acid Test 0.94 1.35 1.36 1.38

Activity: Avg receivables to turnover days 76 67 63 64

Avg trade creditors to purchases days 101 92 83 84

Avg inventories to turnover days 107 101 104 104

Cash Conversion Cycle 82 76 83 85

Financial Structure: Liabilities to equity 0.86 0.73 0.65 0.58

Bank debt to equity 0.68 0.59 0.51 0.44

Net debt / EBITDA 2.94 2.56 2.28 1.82

Profitability: return on total assets 4.0% 3.7% 3.9% 4.9%

return on equity 8.7% 7.5% 7.4% 8.9%

return on invested capital 6.9% 6.6% 6.9% 8.1%

Reinvestment rate -72.82% 18.66% 9.02% 32.39%

Sustainable growth in EBIT -5.01% 1.23% 0.62% 2.62%

Actual growth in EBIT -19.67% 0.91% 2.72% 18.95%

Return on capital 14.89% 13.69% 13.25% 14.61%

University of Piraeus Investment Research Challenge Student Research 27/1/2011

9

Risk Assessment

WACC

19,6 -1,0% -0,5% 0,0% 0,5% 1,0% 1,5% 2,0% 2,5% 3,0% 3,5% 4,0% 4,5% 5,0% 5,5%

7,0% 22,8 23,4 24,0 24,7 25,3 26,0 26,7 27,4 28,2 28,9 29,7 30,6 31,4 32,3

7,5% 20,7 21,2 21,7 22,3 22,8 23,4 24,0 24,7 25,3 26,0 26,6 27,3 28,1 28,8

8,0% 18,8 19,2 19,7 20,2 20,7 21,2 21,7 22,2 22,8 23,4 23,9 24,5 25,2 25,8

8,5% 17,1 17,5 17,9 18,3 18,7 19,2 19,6 20,1 20,6 21,1 21,6 22,1 22,6 23,2

9,0% 15,6 15,9 16,3 16,7 17,0 17,4 17,8 18,2 18,6 19,1 19,5 19,9 20,4 20,9

9,5% 14,3 14,6 14,9 15,2 15,5 15,8 16,2 16,5 16,9 17,3 17,6 18,0 18,4 18,9

10,0% 13,1 13,3 13,6 13,9 14,1 14,4 14,7 15,0 15,3 15,7 16,0 16,3 16,7 17,0

10,5% 12,0 12,2 12,4 12,7 12,9 13,2 13,4 13,7 13,9 14,2 14,5 14,8 15,1 15,4

11,0% 11,0 11,2 11,4 11,6 11,8 12,0 12,2 12,5 12,7 12,9 13,2 13,4 13,7 13,9

11,5% 10,1 10,2 10,4 10,6 10,8 11,0 11,1 11,3 11,5 11,7 11,9 12,2 12,4 12,6

12,0% 9,2 9,4 9,5 9,7 9,8 10,0 10,2 10,3 10,5 10,7 10,8 11,0 11,2 11,4

12,5% 8,4 8,6 8,7 8,8 9,0 9,1 9,3 9,4 9,5 9,7 9,8 10,0 10,1 10,3

13,0% 7,7 7,8 8,0 8,1 8,2 8,3 8,4 8,5 8,7 8,8 8,9 9,0 9,2 9,3

13,5% 7,1 7,2 7,3 7,4 7,5 7,6 7,7 7,8 7,9 8,0 8,1 8,2 8,3 8,4

14,0% 6,5 6,5 6,6 6,7 6,8 6,9 6,9 7,0 7,1 7,2 7,3 7,4 7,4 7,5

14,5% 5,9 6,0 6,0 6,1 6,2 6,2 6,3 6,4 6,4 6,5 6,6 6,6 6,7 6,8

15,0% 5,3 5,4 5,5 5,5 5,6 5,6 5,7 5,7 5,8 5,8 5,9 5,9 6,0 6,0

Expected growth in EBIT

Risk

Risk Assessment

Figure 13: Probability density diagram of Titan share price

The outline of the risk assessment analysis provides support that the estimated price of 19.6 is indeed in the range of acceptable range of

confidence.

The diagram below defines the probability density of Titan‟s share according to Mode Carlo simulation with input parameter the expected

annual growth rate on EBIT from 2013 up to 2020. Based on our initial forecast of a 4% EBIT growth and assuming an annual volatility of

1.5% the target price of Titan‟s share is by 95% within the range of €18.8 and €20.5. …………………………

The current stock price is 15,9 which is less than the lower limit of the probability density diagram. This justifies our BUY

recommendation as we expect the value of Titans share to increase and stabilized within the 95% confident interval of the probability

diagram.

The outcome of the risk assessment analysis provide support for the estimated price of the 19.6 is within the range of acceptable range of

confidence.

Table 13: Titan share price according to various WACC and Expected growth in EBIT combinations

University of Piraeus Investment Research Challenge Student Research 27/1/2011

10

Risk Analysis

Our risk analysis can be affected by the following unexpected risks:

POLITICAL:

Recent developments in the Arab world, such as in Egypt where civil unrest broke out, creating a volatile political environment in the

group‟s strongest growing market.

Turkey‟s peculiar domestic political environment with the long-standing clash of the military versus the political power, always

comprises a factor of unpredictable developments in the region of Eastern Mediterranean.

GEOPOLITICAL:

TITAN‟s presence in the Balkan region is subjected to the risk of unforeseeable developments in respect to the Kosovo issue

ENVIROMNENTAL:

The Group keeps CO2 trade rights reserves in order to comply with future legislation and have the ability to trade in Climate Exchanges

whenever is necessary. …………………………………………………………………………………………………………………..

MACROECONOMIC:

One of the most important cost factors is energy. The inflation in energy prices, the increase of the fuel cost and freight rates could affect

the operational function of the Group. Mm mmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmm

Greek inflation rate that exceeds the Euroarea average figure, increased public debt and deficits in trade balance and balance of payments,

all comprise a very challenging macroeconomic environment for TITAN's base country.……………………………………………

An essential part of the analysis is the risk assessment section. That allows us a range of confidence of the static estimated share price.

FX:

The recent rally of EURO seems to go for an end, because of the positive announcement of the US GDP. This number reminds that the US

economy seems to retreat from the recent financial crisis and has an upside trend for the coming years. The debt problems of the peripheral

countries in EUROPE seems to weigh the euro in the near future, causing the single currency to level such as EURUSD=1.11.

CREDIT RISK:

Possible risk could be generated by lack of liquidity, rise of interest rates, transaction exposures and increase of outstanding accounts

receivables due to global slowdown.

University of Piraeus Investment Research Challenge Student Research 27/1/2011

11

BALANCE SHEET 2009 2010E 2011F 2012F

Tangible assets 2,664 2,786 2,911 3,057

Accumulated depreciation 749 870 992 1,115

Net fixed assets 1,915 1,916 1,919 1,942

Intangible assets 543 549 549 549

LT receivables/deferred tax assets 37 32 32 32

Current Assets 510 548 573 637

Accounts receivable 254 235 245 285

Inventories 239 256 268 288

Cash & cash equivalent 16 55 58 62

Other cash equivalents (for balancing) 0 0 0 0

Trading and other investments 1 1 1 1

TOTAL ASSETS 3,006 3,045 3,073 3,160

Net debt position 970 871 791 713

Shareholders' equity 1,449 1,576 1,661 1,779

Capital 275 278 278 278

Reserves & retained earnings 1,174 1,298 1,383 1,501

Minority interest on share capital 11 26 39 56

Non Current liabilities 1,019 1,079 995 910

Long-term Debt 726 792 708 623

Deferred tax liabilties 197 182 182 182

Retirement and termination benefit

obligations

42 40 40 40

Provisions / other LT liabilties 54 65 65 65

Current liabilities 527 364 378 416

Accounts payable 243 206 215 231

Liabilities for taxes 20 14 12 23

Liabilities to banks 262 139 142 153

Other short-term liabilities 3 5 8 8

TOTAL EQUITY & LIABILITIES 3,006 3,045 3,073 3,160

Appendix 1: Balance Sheet (In mill except stock rice and ratio)

University of Piraeus Investment Research Challenge Student Research 27/1/2011

12

Table 13

2009 2010E 2011F 2012F

PRE-TAX PROFITS 158 166 171 220

Plus: Depreciation & amortization 112 121 122 123

Plus: Non-cash items -8 -14 0 0

Plus: Net interest expenses 60 54 55 48

Less: Taxation paid 0 36 41 39

GROSS CASH FLOW 322 291 307 352

Plus: Chng in accounts payable -12 -37 9 16

Plus: Chng in other current

liabilities -1 5 0 0

Less: Chng in accounts receivable -59 -19 11 40

Less: Chng in inventories -49 18 11 20

Working capital chng -95 30 13 44

Working capital 247 278 290 334

% of sales 18.2% 20.7% 20.7% 22.2%

OPERATING CASH FLOW 417 261 294 308

Less: Purchases of fixed assets 85 122 125 146

Less: Chng in investments 0 0 0 0

% of sales (cap ex only) 6.3% 9.1% 8.9% 9.7%

FREE CASH FLOW 332 139 169 162

Less: Dividends paid 63 36 34 36

Less: Interest expenses 60 66 69 62

Plus: Interest received 9 20 21 22

Plus: Equity chng 0 0 0 0

Plus: Debt chng -221 -59 -78 -74

Plus: Grants 0 0 -2 0

Plus: Other -75 41 -5 -9

Chng in Cash Position -78 39 2 4

Cash Position 16 55 58 62

Appendix 2: Cash Flow (CF) Statement (In mill except stock rice and ratio)

University of Piraeus Investment Research Challenge Student Research 27/1/2011

13

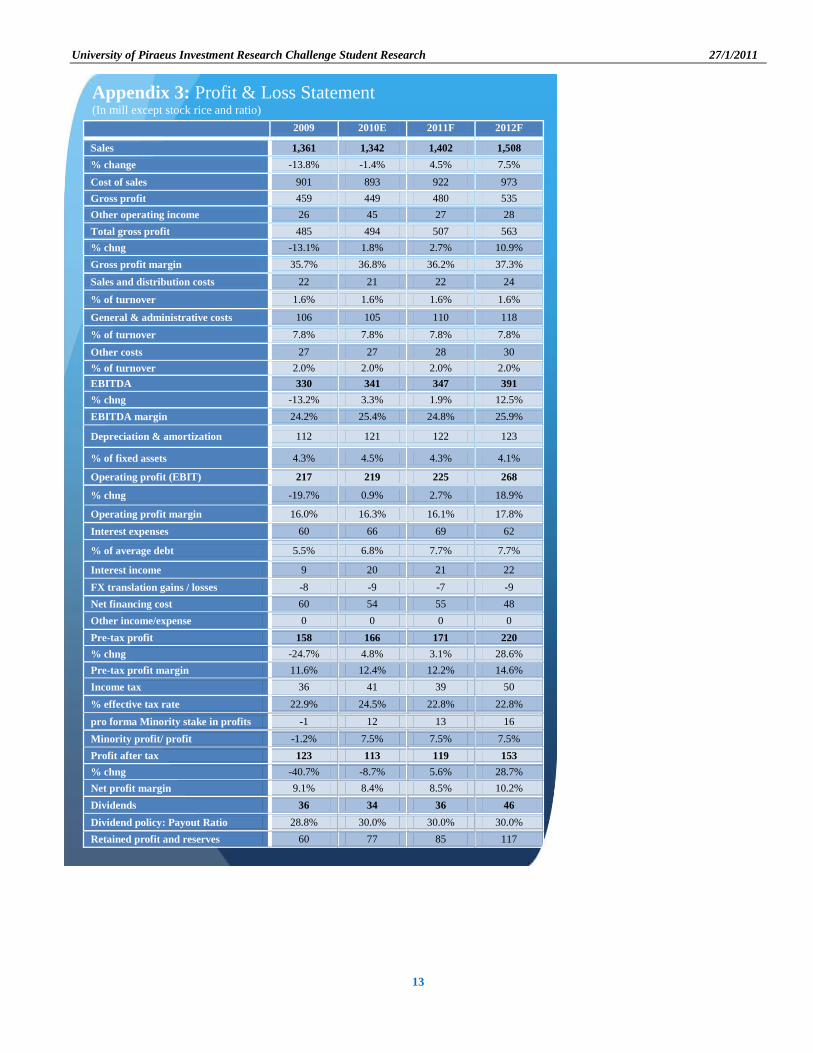

Appendix 3: Profit & Loss Statement (In mill except stock rice and ratio)

2009 2010E 2011F 2012F

Sales 1,361 1,342 1,402 1,508

% change -13.8% -1.4% 4.5% 7.5%

Cost of sales 901 893 922 973

Gross profit 459 449 480 535

Other operating income 26 45 27 28

Total gross profit 485 494 507 563

% chng -13.1% 1.8% 2.7% 10.9%

Gross profit margin 35.7% 36.8% 36.2% 37.3%

Sales and distribution costs 22 21 22 24

% of turnover 1.6% 1.6% 1.6% 1.6%

General & administrative costs 106 105 110 118

% of turnover 7.8% 7.8% 7.8% 7.8%

Other costs 27 27 28 30

% of turnover 2.0% 2.0% 2.0% 2.0%

EBITDA 330 341 347 391

% chng -13.2% 3.3% 1.9% 12.5%

EBITDA margin 24.2% 25.4% 24.8% 25.9%

Depreciation & amortization 112 121 122 123

% of fixed assets 4.3% 4.5% 4.3% 4.1%

Operating profit (EBIT) 217 219 225 268

% chng -19.7% 0.9% 2.7% 18.9%

Operating profit margin 16.0% 16.3% 16.1% 17.8%

Interest expenses 60 66 69 62

% of average debt 5.5% 6.8% 7.7% 7.7%

Interest income 9 20 21 22

FX translation gains / losses -8 -9 -7 -9

Net financing cost 60 54 55 48

Other income/expense 0 0 0 0

Pre-tax profit 158 166 171 220

% chng -24.7% 4.8% 3.1% 28.6%

Pre-tax profit margin 11.6% 12.4% 12.2% 14.6%

Income tax 36 41 39 50

% effective tax rate 22.9% 24.5% 22.8% 22.8%

pro forma Minority stake in profits -1 12 13 16

Minority profit/ profit -1.2% 7.5% 7.5% 7.5%

Profit after tax 123 113 119 153

% chng -40.7% -8.7% 5.6% 28.7%

Net profit margin 9.1% 8.4% 8.5% 10.2%

Dividends 36 34 36 46

Dividend policy: Payout Ratio 28.8% 30.0% 30.0% 30.0%

Retained profit and reserves 60 77 85 117

University of Piraeus Investment Research Challenge Student Research 27/1/2011

14

[Type a quote from the document or the summary of an interesting point. You can position the text box anywhere in the document. Use the Text Box Tools tab to change the formatting of the pull quote text box.]

2009 2010E 2011F 2012F

Liquidity:

Current ratio 0.97 1.51 1.52 1.53

Acid Test 0.94 1.35 1.36 1.38

Activity:

Avg receivables to turnover days 76 67 63 64

Avg trade creditors to purchases days 101 92 83 84

Avg inventories to turnover days 107 101 104 104

Cash Conversion Cycle 82 76 83 85

Financial Structure:

Liabilities to equity 0.86 0.73 0.65 0.58

Bank debt to equity 0.68 0.59 0.51 0.44

Net debt / EBITDA 2.94 2.56 2.28 1.82

Profitability:

return on total assets 4.0% 3.7% 3.9% 4.9%

return on equity 8.7% 7.5% 7.4% 8.9%

return on invested capital 6.9% 6.6% 6.9% 8.1%

Reinvestment rate -72.82% 18.66% 9.02% 32.39%

Sustainable growth in EBIT -5.01% 1.23% 0.62% 2.62%

Actual growth in EBIT -19.67% 0.91% 2.72% 18.95%

Return on capital 14.89% 13.69% 13.25% 14.61%

HELP ROWS

Appendix 4: Ratio Analysis