Embed Size (px)

Citation preview

Universities Superannuation Scheme

Joint Negotiating CommitteeUCU Head Office, Old Bakery, Carlow Street, London, NW1 7LH

27 April 2018 15:00 - 27 April 2018 17:00

Overall Page 1 of 27

AGENDA

# Description Owner Time

1 ApologiesTO NOTE

Chair 3:00pm

2 Minutes of the last meetingTO APPROVE

JNC 153-2 Minutes of the meeting held on 28 Marc... 4

Chair

3 Matters arising TO NOTE

JNC 153-3 Matters arising.docx 12

Chair

4 ISSUES FOR DISCUSSION

4.1 Valuation update following the USSL board meeting on 10 April 2018

TO NOTE

JNC 153-4.1 Valuation update following the USSL b... 14

JNC 153-4.1 Annex.pdf 15

B Galvin 3.15pm

4.2 Practical implications of rule 76.4TO NOTE

JNC 153-4.2 Practical implications of rule 76.4.docx 18

JNC 153-4.2 Annex.pdf 22

S Golden 3.30pm

4.3 Response from UUK/UCU to the trustee letter of 17 April 2018 (oral)

TO COMMENT

UUK/UCU 3:45pm

4.4 Update on the formation of a Joint Expert Panel (oral)TO NOTE

UUK/UCU 4:00pm

4.5 Affirmation or revocation of the JNC resolution of 23 January 2018 (oral)

TO APPROVE

Chair 4.05pm

Overall Page 2 of 27

# Description Owner Time

4.6 Valuation communications (oral)TO NOTE

J Sawyer 4.20pm

4.7 Committee report for inclusion in the annual report and accounts

TO APPROVE

[P] JNC 153-4.7 Committee report for inclusion in Repo... 23

[P] JNC 153-4.7 Annex.docx 24

H Price 4.30pm

5 PAPERS TO NOTE 4.45pm

5.1 Regulatory updateTO NOTE

[P] JNC 153-5.1 Regulatory update.docx 25

S Golden

6 Any other business Chair 4:55pm

7 Date of next meeting: 10:00am on 14 June 2018 at USSL'sLondon office

Overall Page 3 of 27

Restricted Business Sensitive (RBS)JNC 153-2

(JNC 152-MO)Page 1 of 8

UNIVERSITIES SUPERANNUATION SCHEME LIMITED (‘USSL’ or the ‘trustee’)JOINT NEGOTIATING COMMITTEE (‘JNC’ or the ‘committee’)

Minutes of the 152nd meeting of the joint negotiating committee held on Wednesday 28 March 2018 at 2.00pm at USSL’s London office at 60 Threadneedle Street, London EC2R 8HP.

Present: Sir Andrew Cubie (chair) Mr P Harding (UUK) Mr W Spinks (UUK) Mr J Neilson (UUK) Ms M Lambe (UUK)) Mr C Vidgeon (UUK)

Ms C Haswell (UCU) Ms P Collins (UCU) (via conference call)

In attendance: Mr B GalvinMs M Duffield (USS)Mr S Golden (USS) Mrs L Howard (USS) (via conference call)

Mr J Sawyer (USS) Mr J Rowney (USS) Mrs H Price (USS)

1 Apologies for absence

The meeting commenced at 2.40pm to allow time for informal discussions to occur prior to the meeting commencing.

Apologies for absence were received from Dr Morelli, Dr Hersh and Dr Prendergast. The chair asked the secretary to confirm the quorum requirements for the meeting and she confirmed that the meeting was quorate.

The chair noted that it was the first committee meeting since 5 February and that he respected the strenuous efforts that had been made by both UUK and UCU since the last meeting (with ACAS support) to seek a further negotiated solution in relation to benefit change.

2 Updates on the UUK/UCU mandates for change

The chair requested, given the importance of the topic, that the UUK and UCU representatives provide updates on their respective mandates for change and responses to the letters issued by the trustee on 23 March (Trustee Letter) and the pensions regulator (TPR) on 27 March (TPR Letter).

The UUK representatives reported that:(a) A proposal (Proposal) had emerged from informal ACAS discussions to establish a joint expert panel

(Panel) to review (Review) the 2017 valuation methodology and offer recommendations (as more fully explained in UUK’s public announcement).

(b) The Proposal was presently being considered by UUK and UCU. (c) The UUK board was supportive of the Proposal and was presently consulting with employers; such

consultation being due to end at close of business on 28 March.(d) The UUK representatives were not inclined to revoke the committee’s resolution of 23 January 2018

(23 January Resolution). In order to revoke the 23 January Resolution they would need a mandate

Overall Page 4 of 27

Restricted Business Sensitive (RBS)JNC 153-2

(JNC 152-MO)Page 2 of 8

from UUK (which they did not currently have) and suspected that they would also need to consult with employers. Whilst it would be theoretically possible to replace the 23 January Resolution with an alternative proposal that could provide a backstop should an agreed benefit design proposal not be agreed by UUK and UCU within the necessary timeframes post the Review, UUK preferred not to do so as UUK considered that agreeing such a backstop might be inflammatory. Subject to being given the opportunity by the trustee and TPR, UUK’s preference was to wait to agree an alternative benefit proposal until after the Panel concluded the Review.

(e) UUK were however mindful of the trustee’s position and would like to gain a full understanding of the implications of the 23 January Resolution remaining in place or it being revoked and rule 76.4 applying.

The UCU representatives reported that:(a) UCU would like to see the dispute resolved in a way that satisfied the concerns of UCU members and

hoped a way forward would be found.(b) UCU were presently voting on whether to put the Proposal to a vote of UCU’s full membership.(c) UCU expected there to be no change to current benefits until after the Review concluded and the

outcomes been discussed.(d) UCU appreciated that the trustee was subject to duties. (e) Should rule 76.4 apply, UCU would be motivated to find a better valuation outcome because rule 76.4

would lead to an increase in member contributions in addition to an increase in employer contributions.

(f) They would like to hear more information in relation to the Trustee Letter and have the opportunity to discuss the TPR Letter.

Ms Haswell also shared her belief that UCU members would prefer it if the 23 January Resolution (and the move to a defined contribution (DC) only scheme) was revoked, though she noted that she had not consulted with UCU colleagues in relation to this.

The chair invited the executive to talk to the Trustee Letter and respond to UUK and UCU’s comments.

The executive explained that: (a) There were a lot of moving parts to the valuation and that it was important to ensure that everyone

had sufficient understanding to ensure that any decisions made were made in full knowledge of the consequences.

(b) The trustee recognised that everyone’s position was difficult and challenging and that there did not appear to be an easy or attractive solution to the valuation. Similarly the trustee itself was in a difficult and challenging space; it being subject to be both regulatory duties and obligations under the scheme rules. Failure to comply with regulatory duties would run the risk of TPR taking action against the trustee.

(c) Some of the particular challenges that the trustee was currently considering were:i. Economic challenges. In particular, the trustee was conscious that based on the valuation

(including the independent advice it had received) benefits were being accrued which were £800-900m per annum more than the contributions being received; the longer this situation continued the more difficult the trustee’s position.

ii. That the employer consultation (Employer Consultation) with affected members in relation to the 23 January Resolution had been paused. The trustee had taken legal advice which had concluded that it had been reasonable for the trustee to temporarily pause preparations for the Employer Consultation (in order that it could seek clarity and avoid wasted costs). However the trustee was increasingly uncomfortable as the 23 January Resolution constituted

Overall Page 5 of 27

Restricted Business Sensitive (RBS)JNC 153-2

(JNC 152-MO)Page 3 of 8

a formal instruction to the trustee under the rules and the trustee therefore needed the JNC to clarify how the trustee should proceed. Should the JNC not revoke the 23 January Resolution it would appear to indicate that the JNC was supporting that Resolution despite both UUK and UCU publicly saying that they did not support it.

(d) The trustee board was due to meet on 10 April and, subject to the matters discussed at the present meeting and any additional information that was provided to the trustee in advance of the board meeting, it appeared that the options open to the trustee were:

i. Option A – to conclude that the trustee must act on the extant 23 January Resolution. Were the trustee to conclude that it must act on the 23 January Resolution the trustee would issue a notice (Trigger Notice) to employers in relation to the Employer Consultation which would then trigger a requirement on the employers to undertake the Employer Consultation. The executive noted that in the TPR Letter, TPR had made it clear that it would tolerate the statutory deadline for the valuation being missed but only if there was a plan in place to progress the valuation. Should employers not undertake the Employer Consultation in this scenario they would be frustrating the statutory timetable and the trustee would have to look for alternative ways to complete the valuation.

ii. Option B – to follow the process under rules 76.4 to 76.8. This option would automatically apply if the 23 January Resolution were revoked by the JNC and not replaced. Were rule 76.4 to apply the first step would be for the JNC to consider DC accrual above the salary threshold. The trustee board would need to consider a schedule of contributions (based on cost sharing) and members would need to be consulted. Given the TPR letter, the trustee believed it could construct a reasonable timetable for the rule 76.4 process though the executive observed that TPR appeared keen for revised contributions to be implemented by 1 April 2019.

iii. Option C – to consider a new benefit design resolution passed by the JNC. As this option was considered relatively unlikely to occur before 10 April, it was not discussed in detail.

(e) The trustee would likely make a public statement post the board meeting on 10 April and that statement would likely be to the effect that:

i. To date the trustee had followed all requirements at law and under the scheme rules in relation to the valuation.

ii. The trustee wanted to make it clear that the valuation has been undertaken properly and with integrity.

iii. Subject to appropriate and acceptable terms of reference being settled, it proposed to engage with the Review.

iv. The trustee acts in the long term interests of beneficiaries of the scheme and always had that in the front of its mind. In that context and in the context of the trustee’s statutory obligations the trustee must proceed with the valuation but, with the support of TPR, increased contributions would be scheduled to be implemented in such a time frame as would hopefully allow agreement as to benefit design to be reached by the JNC following conclusion of the Review but before the revised contribution rates were implemented.

(f) Should the 23 January Resolution not be revoked by the JNC, the trustee would be in a difficult position as it was effectively being asked to frustrate the scheme rules and statute for what appeared to be procedural reasons given both UUK and UCU had publically resiled from the 23 January Resolution. Given this it appeared likely that the board would need to proceed to implement the 23 January Resolution and resolve that the Trigger Notice be served on Employers unless it had a good reason to do otherwise. The executive requested that UUK and UCU provide details of any such good reasons to them.

Overall Page 6 of 27

Restricted Business Sensitive (RBS)JNC 153-2

(JNC 152-MO)Page 4 of 8

In response to questions from the chair, it was confirmed by the UCU and UUK representatives that their intention was to convene the Panel and agree the terms of reference for the Review as soon as possible but in reality they expected it to take months rather than weeks for the Review to be completed (autumn 2018 being referred to as the possible timescale for conclusion of the Review). It was explained that they hoped that this would enable sufficient time post conclusion of the Review for due process to be followed to agree benefit changes and for those changes to be implemented from 1 April 2019 or as soon as reasonably possible thereafter.

The chair queried whether UUK’s view about leaving the 23 January Resolution extant was likely to change prior to the trustee board meeting on 10 April. In response the UUK representatives confirmed that they were unlikely to revoke the 23 January Resolution unless there was an alternative in place and that in turn it was unlikely that an alternative would be in place by 10 April, but UUK might be able to bring a proposal to the JNC meeting on 27 April. The importance of there being clear and reasonable timelines was emphasised by the executive.

The UCU representatives observed: (a) That whilst revoking the 23 January Resolution would put everyone in a difficult position, they thought

it would be preferable to revoke it and that this might encourage more UCU members to accept the Proposal.

(b) Given the trustee’s comments that it would likely need to issue the Trigger Notice should the 23 January Resolution not be revoked they thought that trust in the Review process might be negatively impacted should it appear that the Employer Consultation was to be commenced.

It was agreed that a meeting would be held between the executive and UUK (and separately with UCU should this be desired) to discuss the ramifications of the 23 January Resolution not being revoked and the options that were open to the trustee in this scenario (for example whether it could unilaterally increase contributions). Pending that, in response to questions received from the committee, some initial thoughts were shared by the executive in relation to such ramifications, including that:(a) It was for TPR to state what enforcement action it would take against employers who did not proceed

with the Employer Consultation following service of a Trigger Notice and were thus in breach of a statutory duty. Powers available to TPR included fines and the serving of enforcement notices. It was noted that there were 365 employers all of whom would need to make individual decisions as to whether to consult. It was reported by Will Spinks that were a Trigger Notice served on the University of Manchester that it would likely feel obliged to undertake the Employer Consultation and that it was unclear whether other employers would feel the same.

(b) TPR had made clear in the TPR Letter (paragraph 14) that in return for leniency in relation to completing the valuation by the statutory deadline it expected the trustee to have a plan in place for completing the valuation. Should the 23 January Resolution not be revoked but nor should the Employer Consultation occur, then the trustee would need to ensure that it was using its powers under scheme rules and statute to ensure there was a plan.

(c) The trustee was being placed in an uncomfortable position and that it was not tenable for it to remain in such an artificial position given both UUK and UCU had publicly resiled from the 23 January Resolution.

(d) The trustee board would need to consider the full ramifications of the 23 January Resolution not being revoked and all of the options open to it. The executive declined to speculate on what these options might be.

SGUUKUCU

Overall Page 7 of 27

Restricted Business Sensitive (RBS)JNC 153-2

(JNC 152-MO)Page 5 of 8

A number of questions were asked by the committee in relation to rule 76.4 and the executives’ responses confirmed that:(a) Whilst they had not had the opportunity to discuss it with the board ahead of the present meeting,

the executive thought that the board might be receptive to the executive’s recommendation that a reasonable timeline be used under rule 76.4 given that the trustee had some discretion as to timing under the rules. This was subject to:

i. Recognising TPR’s view that contribution increases/benefit changes should be implemented by 1 April 2019.

ii. Having certainty that any such timetable would be complied with.(b) There were a number of steps in the rule 76.4 process which included:

i. The JNC discussing DC contributions above the salary threshold. This would need to happen within a reasonable period and before the cost sharing provisions under rule 76.8 could be applied. The committee was referred to the 4 week period referred to in the Trustee Letter.

ii. A schedule of contributions would need to be prepared and consultations undertaken in relation to the proposed changes to member and employer contributions.

(c) One or possibly two JNC meetings would be required.(d) Whilst in order to confirm the contributions that would be definitively payable should rule 76.4 apply

detailed analysis (including as to strength of the employer covenant and the timing of increases) would be required, stakeholders could gain some understanding of the possible magnitude of contributions by having regard to the previously disclosed contribution rates for current benefits. It was noted that such contribution rates were broadly that an aggregate contribution rate of 37.4% of pay would be required of which approximately 0.8% of pay was attributable to the 1% match and c2.5% of pay was attributable to DC contributions above the salary threshold. Any increase to contributions would be split 35% by members and 65% by employers under the cost sharing provisions in rule 76.8.

The UUK representatives noted that they understood why the trustee was focused on its board meeting of 10 April but that realistically 27 April was the earliest date by which UUK could make a proposal. The executive reiterated that the trustee board would need a good reason not to issue the Trigger Notice should the 23 January Resolution not have been revoked by 10 April and that the onus was on UCU and UUK to provide that reason.

The chair expressed the view that: (a) By meeting and doing nothing to change the 23 January Resolution and showing no intention to

change it, the JNC was ipso facto validating that Resolution. (b) He was very sympathetic to the trustee’s position as the JNC had compelled the trustee to take action

by virtue of the 23 January Resolution which the trustee was not taking and that this led to the inequitable position of the trustee taking all of the regulatory risk in relation to the valuation.

(c) Whilst there were no easy answers, the JNC members should support the credibility of any request to the trustee board not to take precipitous action in relation to the 23 January Resolution by clarifying the position they hoped to reach by the end of April. He therefore suggested that a timeline for the steps to be taken by UUK and UCU during April be agreed.

The executive indicated that should UUK and UCU confirm an intent to revoke the 23 January Resolution prior to the trustee board meeting on 10 April, albeit that the formal revocation would be subject to review and confirmation at the JNC meeting on 27 April that it might give the trustee board sufficient comfort for it to resolve not to issue a Trigger Notice at its 10 April meeting. The executive did though observe that the trustee board may just see any such request as yet another postponement request.

Overall Page 8 of 27

Restricted Business Sensitive (RBS)JNC 153-2

(JNC 152-MO)Page 6 of 8

It was discussed that were UCU to ballot its members that such ballot would not close before the trustee board meeting on 10 April, but the UUK representatives agreed that UUK would write to the trustee to make its views clear ahead of the board meeting.

It was agreed that the executive would provide a paper in relation to the operation of rule 76.4 to UUK and UCU which set out the timescales and process that would apply and the contributions that may be payable should rule 76.4 apply. Such paper would also include a ‘right to left’ plan working back from 1 April 2019. UUK observed that it was critical that there was clarity as to the consequences of different courses of action and that it would be helpful to understand the impact of different courses of action on benefits, covenant strength, contributions, deficit recovery contributions and the legal consequences of regulatory obligations not being complied with. The executive responded that they would explain the process as they interpreted it from a procedural perspective (bearing in mind this procedure was set by the JNC). Some of the decision making elements (such as those relating to the strength of the covenant as it applied to contribution increases) were very complicated and would require external advice and consideration by the USSL Board.

3 Minutes of the meeting held on 23 January 2018

The minutes of the meeting held on 5 February 2018 were approved without amendment.

UUK

LHSGJR

4 Matters arising

The executive presented an update in relation to the matters arising. The executive drew the committee’s particular attention to the proposed closure of action 5 and the response of the USSL board to the request that the JNC be allowed access to certain information. It was agreed that this action could be closed. The committee also agreed that all other actions that had been marked as completed or proposed closed in the actions log could be closed.

The committee discussed:(a) Action 9 (which related to certain assumptions used by First Actuarial). The UUK representatives noted

that as the assumptions were based on there being no DC benefits above the scheme’s salary threshold that any modelling based on those assumptions which was then used in communications might be misleading. The UCU representatives agreed to feed this back to UCU.

(b) Action 13 (which related to the UCU representatives checking whether any information in UCU communications needed to be clarified or updated). The UCU representatives reported that they were unable to provide an update on this and agreed to raise this action with Paul Bridge.

CH

CH

5 Papers to Note

5.1 Regulatory update

The regulatory update was noted. The committee requested that the executive bring a more detailed update to the committee in relation to deferred debt arrangements (DDAs) under The Occupational Pension Schemes (Employer Debt and Miscellaneous Amendments) Regulations; such update to include the proposed timeline for the trustee’s assessment of the implications of DDAs.

SG

Overall Page 9 of 27

Restricted Business Sensitive (RBS)JNC 153-2

(JNC 152-MO)Page 7 of 8

5.2 Member insight and statistics

The executive presented the insight and statistics paper. In response to questions from the committee the executive: (a) Confirmed that whilst there was a big increase in transfers out, the increase did not appear to

be as marked as it was in other schemes and that no single independent financial adviser (IFA) appeared to have been involved in 20 or more recent transfers out.

(b) Explained that the level of opt-outs was likely due to the large number of members joining the scheme and that analysis undertaken by the executive showed that those opting-out tended to be younger lower earners.

The committee discussed that take up of the 1% match was relatively low and observed that this might be partly down to affordability concerns for members. The executive reported that there had though been an increase in take up of the match in recent months.

In addition, Ms Haswell provided feedback that she considered the annual member statement (AMS) to have been very well presented.

6 Matters For Discussion

6.1 Update following the USSL board meeting on 22 March 2018

As all pertinent matters had been discussed in the context of the UUK and UCU mandates for change (as set out in minute 2) the committee declined to discuss this agenda item further.

6.2 Employer Consultation Update

The consultation update was noted, the executive observing that: (a) The employer consultation had been on track to commence on 19 March, so from the

trustee’s perspective the project had been successfully implemented up until the point where it was paused.

(b) Should the JNC reach a new decision on benefit design it would take approximately 14-16 weeks from the date of that decision until the close of the requisite employer consultation (as explained in more detail in the paper).

6.3 Valuation Communications

The executive: (a) Provided an overview of the valuation communications activity that had been undertaken by

the trustee since the last committee meeting. (b) Explained that the trustee had taken a conscious decision to step back from proactive

communications whilst the ACAS discussions were publically continuing between UUK and UCU but had issued communications on 16 March to seek to address some of the inaccurate information that had been published about the valuation.

(c) Provided some statistical information in relation to the hits on the USS website and the number of ‘opens’ of member communications issued by the trustee in relation to the valuation.

(d) Requested feedback on its communications approach.

Overall Page 10 of 27

Restricted Business Sensitive (RBS)JNC 153-2

(JNC 152-MO)Page 8 of 8

No feedback or other comment was received from the committee.

7 Any other business

There being no further business the meeting closed at 4.15pm.

8 Date of next scheduled meeting

The next meeting will be held at 3.00pm on 27 April 2018 at UCU’s London Head Office.

Overall Page 11 of 27

Restricted Business Sensitive (RBS)JNC 153-3

Page 1 of 2

JOINT NEGOTIATING COMMITTEE - MATTERS ARISING

The committee is asked TO NOTE the following update on matters arising at the 27 April 2018 joint negotiating committee (JNC) meeting.

Action Date Minute ref

Matter arising Action owner

Due date Status

1. 19.10.2017 5.5 UCU and UUK are to notify the executive of any further specific benefit design modelling that they would like to be undertaken.

UCUUUK

ASAP Ongoing.

2. 23.01.2018 5.1 The executive is to confirm that accuracy of the data set out in section 2.1 of the Insight and Key Statistics Report provided to the meeting on 23.01.2018 including as to the breakdown of the number of members only taking up the 1% match.

Mel Duffield

April 2018 Ongoing. Capita have informed USS the data defect raised within the Hartlink contribution report has now been corrected. The report is presently being prioritised for testing by the Risk team to validate output.

3. 05.02.2018 4.1 The Secretary is to confirm meeting dates for the provisional JNC and FBSC meetings identified in the valuation timetable.

Helen Price April 2018 Complete. The dates presently scheduled for the remainder of 2018 are:JNC

- 27 April (2pm - 4pm)- 14 June (10am – 12pm)- 31 July (2pm - 4pm)- Week commencing 22 October TBC

FBSC

- 24 May (10am – 12pm)- 13 September (10am – 12pm)

4. 05.02.2018

28.03.2018

4.3 The UCU representatives are to check whether any information in the communications issued by UCU needs to be clarified or updated. At the meeting on 28 March, it was agreed that Christine Haswell would highlight this action to Paul Bridge.

Paul Bridge April 2018 Ongoing. Update requested from UCU on 18 April.

Overall Page 12 of 27

Restricted Business Sensitive (RBS)JNC 153-3

Page 2 of 2

Action Date Minute ref

Matter arising Action owner

Due date Status

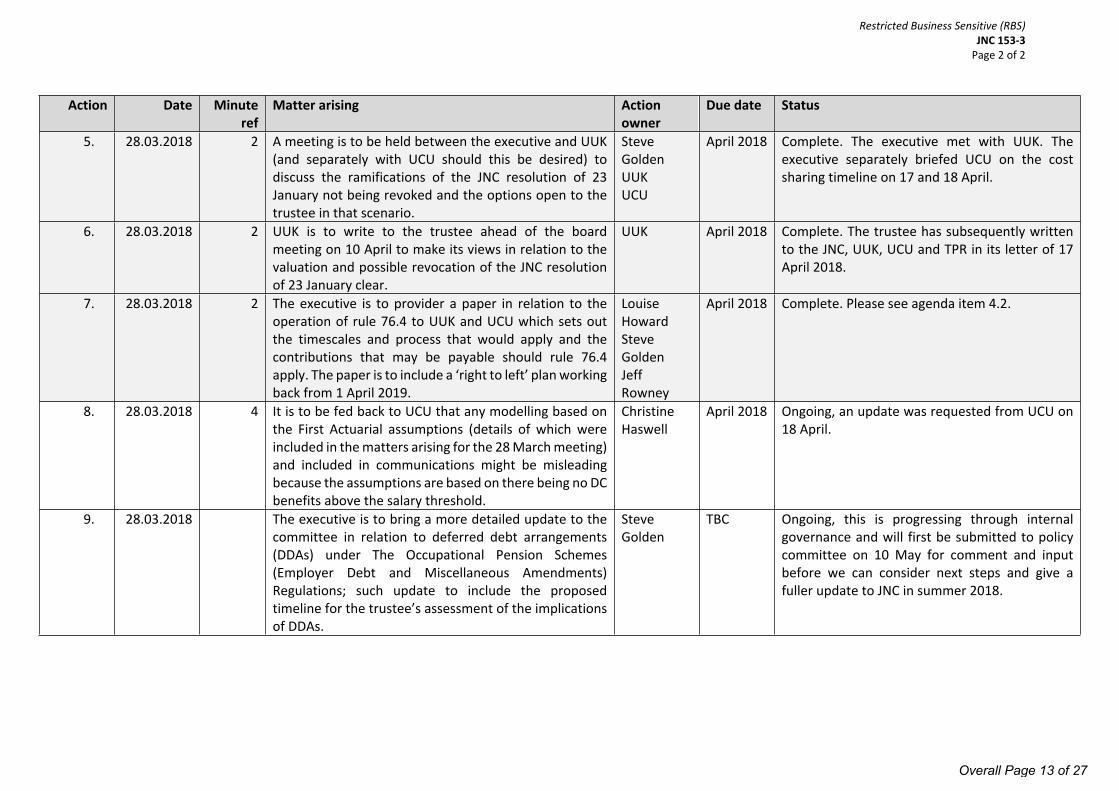

5. 28.03.2018 2 A meeting is to be held between the executive and UUK (and separately with UCU should this be desired) to discuss the ramifications of the JNC resolution of 23 January not being revoked and the options open to the trustee in that scenario.

Steve GoldenUUKUCU

April 2018 Complete. The executive met with UUK. The executive separately briefed UCU on the cost sharing timeline on 17 and 18 April.

6. 28.03.2018 2 UUK is to write to the trustee ahead of the board meeting on 10 April to make its views in relation to the valuation and possible revocation of the JNC resolution of 23 January clear.

UUK April 2018 Complete. The trustee has subsequently written to the JNC, UUK, UCU and TPR in its letter of 17 April 2018.

7. 28.03.2018 2 The executive is to provider a paper in relation to the operation of rule 76.4 to UUK and UCU which sets out the timescales and process that would apply and the contributions that may be payable should rule 76.4 apply. The paper is to include a ‘right to left’ plan working back from 1 April 2019.

Louise HowardSteve GoldenJeff Rowney

April 2018 Complete. Please see agenda item 4.2.

8. 28.03.2018 4 It is to be fed back to UCU that any modelling based on the First Actuarial assumptions (details of which were included in the matters arising for the 28 March meeting) and included in communications might be misleading because the assumptions are based on there being no DC benefits above the salary threshold.

Christine Haswell

April 2018 Ongoing, an update was requested from UCU on 18 April.

9. 28.03.2018 The executive is to bring a more detailed update to the committee in relation to deferred debt arrangements (DDAs) under The Occupational Pension Schemes (Employer Debt and Miscellaneous Amendments) Regulations; such update to include the proposed timeline for the trustee’s assessment of the implications of DDAs.

Steve Golden

TBC Ongoing, this is progressing through internal governance and will first be submitted to policy committee on 10 May for comment and input before we can consider next steps and give a fuller update to JNC in summer 2018.

Overall Page 13 of 27

Restricted Business Sensitive (RBS)JNC 153-4.1Page 1 of 1

Valuation update following the USSL board meeting on 10 April 2018 Executive Summary

Author: Helen PriceAuthorised by: Jonathan Taylor Purpose: NotingMeeting: Joint Negotiating Committee (“JNC” or “committee”), 27 April 2018ANNEX: Letter to the JNC chair dated 17 April 2018

Context:

Input sought/action requested:

Questions/Issues:

Conclusions:

Input received from the business/external advisers:

Input received from other boards/committees:

This paper provides the JNC with an update following the USSL board meeting on 10 April 2018.

The JNC is asked to NOTE this update.

1. What valuation update is provided following the USSL board meeting on 10 April 2018?

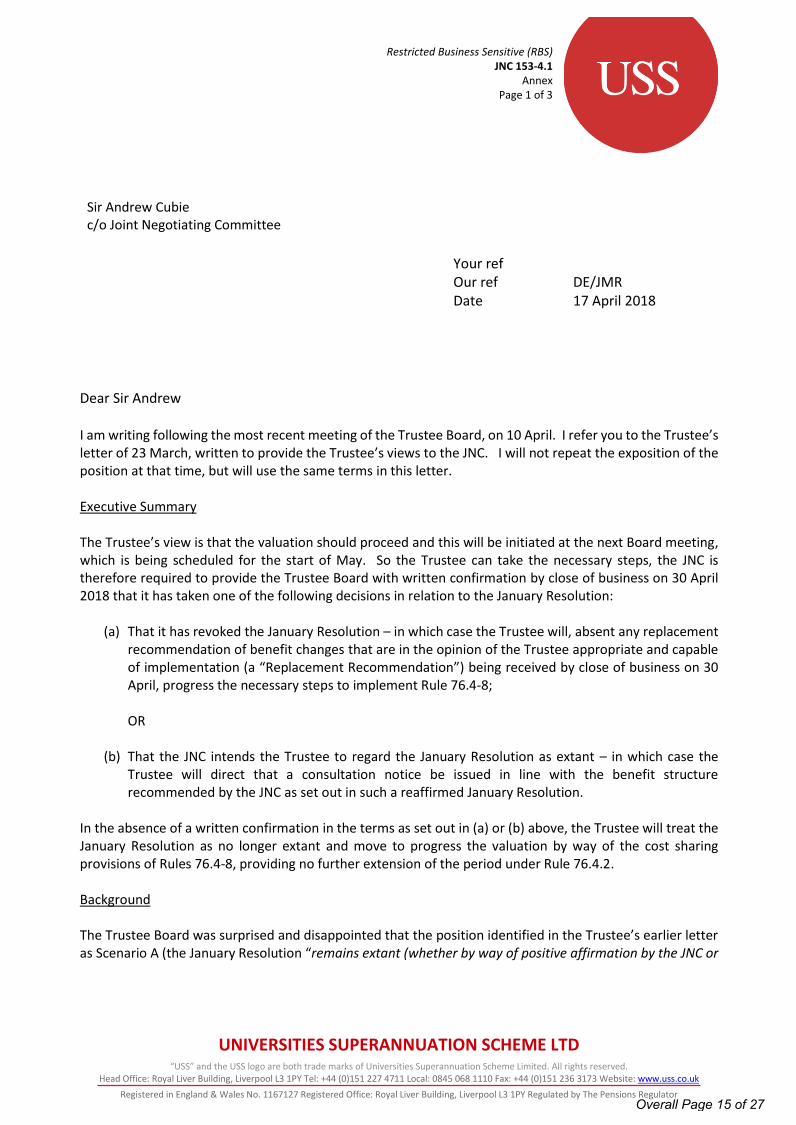

1. A letter dated 17 April 2018 was sent from Sir David Eastwood (chair of the USSL board) to the JNC chair summarising the USSL board’s views in relation to the valuation. A copy of the letter is annexed to this report.

None.

None.

Overall Page 14 of 27

UNIVERSITIES SUPERANNUATION SCHEME LTD “USS” and the USS logo are both trade marks of Universities Superannuation Scheme Limited. All rights reserved.

Head Office: Royal Liver Building, Liverpool L3 1PY Tel: +44 (0)151 227 4711 Local: 0845 068 1110 Fax: +44 (0)151 236 3173 Website: www.uss.co.uk

Registered in England & Wales No. 1167127 Registered Office: Royal Liver Building, Liverpool L3 1PY Regulated by The Pensions Regulator

Sir Andrew Cubie c/o Joint Negotiating Committee

Your ref Our ref Date

DE/JMR 17 April 2018

Dear Sir Andrew

I am writing following the most recent meeting of the Trustee Board, on 10 April. I refer you to the Trustee’s letter of 23 March, written to provide the Trustee’s views to the JNC. I will not repeat the exposition of the position at that time, but will use the same terms in this letter.

Executive Summary

The Trustee’s view is that the valuation should proceed and this will be initiated at the next Board meeting, which is being scheduled for the start of May. So the Trustee can take the necessary steps, the JNC is therefore required to provide the Trustee Board with written confirmation by close of business on 30 April 2018 that it has taken one of the following decisions in relation to the January Resolution:

(a) That it has revoked the January Resolution – in which case the Trustee will, absent any replacementrecommendation of benefit changes that are in the opinion of the Trustee appropriate and capableof implementation (a “Replacement Recommendation”) being received by close of business on 30April, progress the necessary steps to implement Rule 76.4-8;

OR

(b) That the JNC intends the Trustee to regard the January Resolution as extant – in which case theTrustee will direct that a consultation notice be issued in line with the benefit structurerecommended by the JNC as set out in such a reaffirmed January Resolution.

In the absence of a written confirmation in the terms as set out in (a) or (b) above, the Trustee will treat the January Resolution as no longer extant and move to progress the valuation by way of the cost sharing provisions of Rules 76.4-8, providing no further extension of the period under Rule 76.4.2.

Background

The Trustee Board was surprised and disappointed that the position identified in the Trustee’s earlier letter as Scenario A (the January Resolution “remains extant (whether by way of positive affirmation by the JNC or

Restricted Business Sensitive (RBS)JNC 153-4.1

Annex Page 1 of 3

Overall Page 15 of 27

Sir Andrew Cubie 17 April 2018

UNIVERSITIES SUPERANNUATION SCHEME LTD “USS” and the USS logo are both trade marks of Universities Superannuation Scheme Limited. All rights reserved.

Head Office: Royal Liver Building, Liverpool L3 1PY Tel: +44 (0)151 227 4711 Local: 0845 068 1110 Fax: +44 (0)151 236 3173 Website: www.uss.co.uk

Registered in England & Wales No. 1167127 Registered Office: Royal Liver Building, Liverpool L3 1PY Regulated by The Pensions Regulator

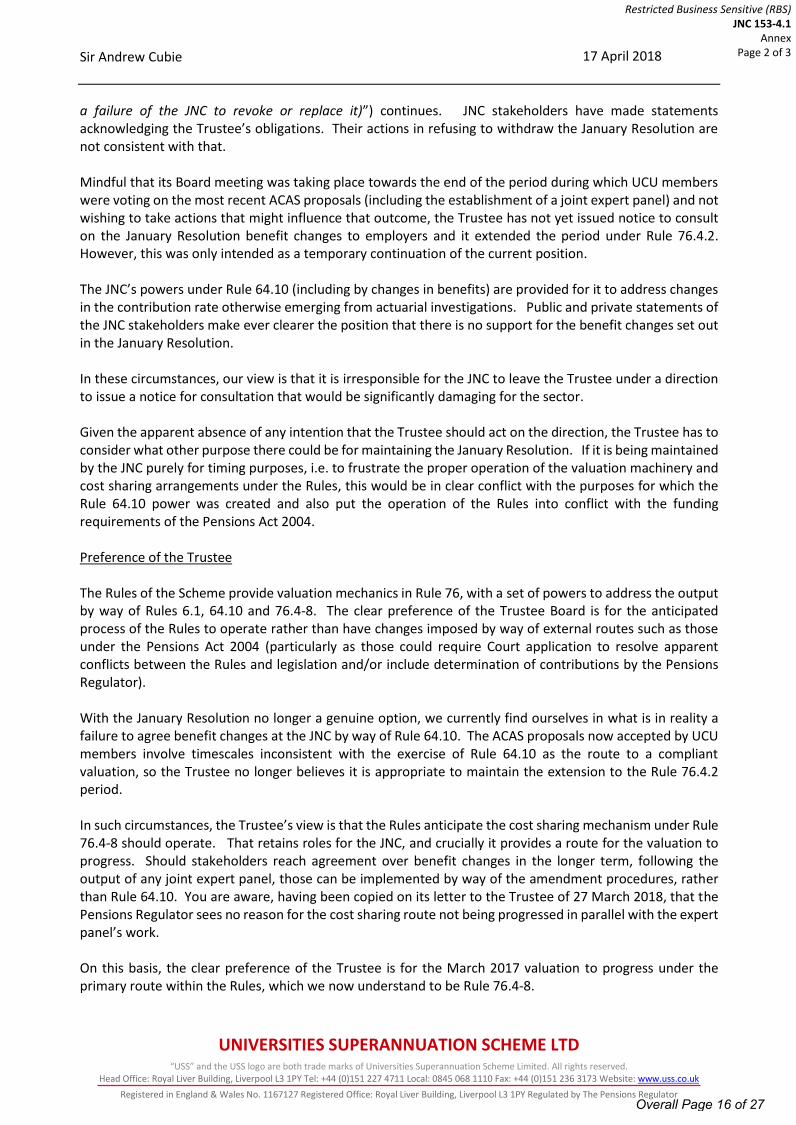

a failure of the JNC to revoke or replace it)”) continues. JNC stakeholders have made statements acknowledging the Trustee’s obligations. Their actions in refusing to withdraw the January Resolution are not consistent with that.

Mindful that its Board meeting was taking place towards the end of the period during which UCU members were voting on the most recent ACAS proposals (including the establishment of a joint expert panel) and not wishing to take actions that might influence that outcome, the Trustee has not yet issued notice to consult on the January Resolution benefit changes to employers and it extended the period under Rule 76.4.2. However, this was only intended as a temporary continuation of the current position.

The JNC’s powers under Rule 64.10 (including by changes in benefits) are provided for it to address changes in the contribution rate otherwise emerging from actuarial investigations. Public and private statements of the JNC stakeholders make ever clearer the position that there is no support for the benefit changes set out in the January Resolution.

In these circumstances, our view is that it is irresponsible for the JNC to leave the Trustee under a direction to issue a notice for consultation that would be significantly damaging for the sector.

Given the apparent absence of any intention that the Trustee should act on the direction, the Trustee has to consider what other purpose there could be for maintaining the January Resolution. If it is being maintained by the JNC purely for timing purposes, i.e. to frustrate the proper operation of the valuation machinery and cost sharing arrangements under the Rules, this would be in clear conflict with the purposes for which the Rule 64.10 power was created and also put the operation of the Rules into conflict with the funding requirements of the Pensions Act 2004.

Preference of the Trustee

The Rules of the Scheme provide valuation mechanics in Rule 76, with a set of powers to address the output by way of Rules 6.1, 64.10 and 76.4-8. The clear preference of the Trustee Board is for the anticipated process of the Rules to operate rather than have changes imposed by way of external routes such as those under the Pensions Act 2004 (particularly as those could require Court application to resolve apparent conflicts between the Rules and legislation and/or include determination of contributions by the Pensions Regulator).

With the January Resolution no longer a genuine option, we currently find ourselves in what is in reality a failure to agree benefit changes at the JNC by way of Rule 64.10. The ACAS proposals now accepted by UCU members involve timescales inconsistent with the exercise of Rule 64.10 as the route to a compliant valuation, so the Trustee no longer believes it is appropriate to maintain the extension to the Rule 76.4.2 period.

In such circumstances, the Trustee’s view is that the Rules anticipate the cost sharing mechanism under Rule 76.4-8 should operate. That retains roles for the JNC, and crucially it provides a route for the valuation to progress. Should stakeholders reach agreement over benefit changes in the longer term, following the output of any joint expert panel, those can be implemented by way of the amendment procedures, rather than Rule 64.10. You are aware, having been copied on its letter to the Trustee of 27 March 2018, that the Pensions Regulator sees no reason for the cost sharing route not being progressed in parallel with the expert panel’s work.

On this basis, the clear preference of the Trustee is for the March 2017 valuation to progress under the primary route within the Rules, which we now understand to be Rule 76.4-8.

Restricted Business Sensitive (RBS)JNC 153-4.1

Annex Page 2 of 3

Overall Page 16 of 27

Sir Andrew Cubie 17 April 2018

UNIVERSITIES SUPERANNUATION SCHEME LTD “USS” and the USS logo are both trade marks of Universities Superannuation Scheme Limited. All rights reserved.

Head Office: Royal Liver Building, Liverpool L3 1PY Tel: +44 (0)151 227 4711 Local: 0845 068 1110 Fax: +44 (0)151 236 3173 Website: www.uss.co.uk

Registered in England & Wales No. 1167127 Registered Office: Royal Liver Building, Liverpool L3 1PY Regulated by The Pensions Regulator

As I indicated previously, the Trustee will keep under review at all times what powers it has to move forward with the actuarial valuation under the Pensions Act 2004 alongside and/or without reference to the requirements of the Rules.

Next steps

The Trustee recognises the potential adverse consequences for members and the sponsoring institutions of a consultation notice at this time containing the changes set out in the January Resolution. However, it is not prepared to allow the uncertainty that has developed over the status of the January Resolution to delay further the 31 March 2017 valuation. Any uncertainty is the responsibility of the JNC and within its competence to resolve.

Accordingly, the Trustee now gives the JNC the opportunity to confirm the status of the January Resolution. The JNC is required to send written confirmation to the Trustee prior to the close of business on 30 April 2018 that either:

(a) It has revoked the January Resolution - in which case the trustee shall, absent any ReplacementRecommendation being received by close of business on 30 April, then progress the necessary stepsto implement Rule 76.4-8;

OR

(b) The JNC intends the Trustee to regard the January Resolution as extant - in which case the Trusteewill direct that a consultation notice be issued in line with the benefit structure recommended bythe JNC as set out in such a reaffirmed January Resolution.

For the avoidance of doubt, in the absence of written confirmation by the JNC to the Trustee Board in the terms set out above, the Trustee will treat the January resolution as no longer extant. The Trustee will consider the JNC’s failure to provide the confirmation requested as being inconsistent with the January Resolution continuing to have effect.

The Trustee is not willing to maintain further the period for JNC consideration under Rule 76.4.2, so the Trustee would, if the January Resolution has been revoked or otherwise fallen away without a Replacement Recommendation being notified in writing by close of business on 30 April, move to progress the valuation by way of the cost sharing provisions of Rules 76.4-8.

Kind regards

Yours sincerely

David Eastwood Chairman Universities Superannuation Scheme Limited

cc Phil Harding Paul Bridge The Pensions Regulator

Restricted Business Sensitive (RBS)JNC 153-4.1

Annex Page 3 of 3

Overall Page 17 of 27

Restricted Business Sensitive (RBS)JNC 153-4.2Page 1 of 4

Practical implications of rule 76.4-8

Author: Steve Golden Authorised by: Mel DuffieldPurpose: NOTE Meeting: Joint Negotiating Committee (JNC), 27 April 2018

Context:

Input sought/action requested:

Questions/Issues:

Conclusions:

Following the request at the last JNC to set out in greater detail how cost sharing and rule 76.4-8 works, this paper sets out the process and shows the interactions between the process to complete the valuation (including the employers’ consultation with affected employees), the timings for the work of the Joint Expert Panel (JEP) and the implementation cut-off dates for an April 2019 change to scheme benefits. Milestone dates have been aligned to support the trustee’s requirements of the JNC, commencing on 30 April 2018.

The JNC is asked to NOTE this paper.

1. How will the cost share process commence?2. What is required from the JNC immediately following the reactivation of 76.4?3. Will the changes in the contribution rate require a statutory consultation with affected employees and their

representatives?4. What would be the expected completion date?5. What are the latest dates by which a JNC recommendation proposing benefit changes can be implemented from 1

April 2019 and not require cost sharing to be used?6. What is the overall effect on benefits of the cost sharing rules?

1. The cost share rules (76.4 - 8) commence if the JNC is unable to decide on how required increases in the contribution rate are to be addressed following a scheme valuation. If the JNC decides to rescind the 23 January resolution (or otherwise fails to notify the trustee that it has affirmed such resolution by 30 April) then it is anticipated that the cost share process will re-commence from the end of April/early May (the date of the next trustee meeting).

2. Under the rules (76.5) it is for the JNC to consider whether there should be any changes to the employer contribution to USS Investment Builder (currently 12% of salary in excess of the salary threshold). In the timeline a maximum of four weeks has been allowed for the JNC to make this decision.

3. Yes, a consultation is required. Both a reduction in the amount of employer contributions and/or an increase to the member contribution rate are listed changes, thereby triggering a requirement to consult.

4. Based upon the 76.4-8 process commencing late April/early May 2018, the valuation process would complete at the end of the year or early in January 2019, in advance of implementation for 1 April 2019.

5. Given the consultation requirements and the practicalities of implementing changes and supporting member communications, mid-late June is the latest date for a JNC recommendation on benefit change with a credible implementation date of 1 April 2019. This timescale assumes that any changes would be simple parameter changes to the existing hybrid scheme structure (e.g. under 76.4) and not more fundamental changes to benefit structure. This is some months prior to the date it is assumed the JEP will produce any recommendations.

6. The trustee board would be expected to determine that the whole of the match would cease and, absent a decision by the JNC on benefit changes under 76.5, the remainder of the increased costs would be shared by increases in contributions in the ratio of 35:65 between members and employers respectively. The precise quantum of the increase will not be known until late June 2018 when the additional covenant review work is also complete.

Overall Page 18 of 27

Restricted Business Sensitive (RBS)JNC 153-4.2Page 2 of 4

Input received from the business/external advisers:

Input received from other boards/committees:

Funding and risk, Legal, Transformation.

N/A

Overall Page 19 of 27

Restricted Business Sensitive (RBS)JNC 153-4.2Page 3 of 4

Cost sharing – Rule 76.4-8

Summary

The cost share rules are invoked where a change in the aggregate contribution rate payable by employers is required following an actuarial valuation and the JNC is unable to decide how the cost of that increase is to be met (including by changes to contributions and/or benefits).

Given delays in deciding the final form of benefit changes, the timings are challenging as the Joint Expert Panel (JEP) is not expected to deliver any recommendations until September or October 2018 (this is subject to confirmation). However the cut-off date for a JNC recommendation proposing benefit changes to enable a 1 April 2019 implementation is mid-late June 2018.

The trustee will therefore have to progress the process to implement a contribution increase under the cost share rules to address the cost of benefits accruing (and which have accrued from April 2017) and the deficit no later than 1 April 2019, and run that process in parallel to the ongoing work of the JEP. The likely outcome therefore is that there will be a period of at least 12 months where the contribution rates will have increased but defined benefits remain largely unchanged (the match is removed), with the only credible date for scheme changes following the JEP process then likely to be 1 April 2020.

A further review of covenant is underway to consider affordability from an employer perspective and that work will conclude in June 2018 and inform the trustee board as to the rate to apply with effect from 1 April 2019. An oral update will be given on this element of the valuation process.

76.4-8 timeline

Attached as an annex to this paper is a timeline setting out the process for completing the 2017 valuation via the cost share route. The executive will give a detailed explanation of the process, however the key points are as follows:

The process will take 9-12 months: an assumed start date of end April/early May 2018, an end date of late December 2018/early January 2019 for completing the valuation, and an implementation date of 1 April 2019 for contribution and/or benefit changes.

The cut-off date for a JNC recommendation proposing benefit changes with a 1 April 2019 implementation is mid-late June 2018.

The timing of the JEP process is expected to mean that it will produce recommendation/outcomes during September/October 2018. A process to complete the valuation (reflecting the likely need to consult with affected employees on proposed changes to benefits/contributions, the governance steps around agreeing the final benefits after that consultation, and the actions around completion of the final signed Schedule of Contributions) with a JNC decision date in September would mean that the process would not finish until after 1 April 2019, and it will be too late by then to implement any benefit / contribution changes from 1 April 2019.

As the process extends past October 2018, the trustee’s ability to support members and employers to prepare for changes via communication and other means is increasingly diminished.

Overall Page 20 of 27

Restricted Business Sensitive (RBS)JNC 153-4.2Page 4 of 4

The timeline highlights the timing difficulties between three key elements namely i) the valuation process, ii) the work of the JEP and iii) the cut-off dates for implementation.

Given the timing conflict and the likely absence of a JNC recommendation over the coming weeks, the cost share provisions will have to apply from 1 April 2019 as it will not be possible to await the outcome of the JEP and any associated processes to enable a decision from the JNC; for instance the overall process will be extended further if there is a need to ballot members, consult with employers and then negotiate a joint proposal after the JEP concludes but before the JNC can be asked to decide on benefit change.

Rule 76.5 – contributions payable by employers in excess of the salary threshold

Under the rules (Rule 76.5) it is for the JNC to consider a reduction in the rate of employer contributions to USS Investment Builder (currently 12% of salary in excess of the salary threshold).

Four weeks have been allowed in the timeline for the JNC to reach a decision on the rate of employer contributions to USS Investment Builder (or other potential changes). If a decision is made earlier, this will have a positive effect on the completion date, and the date by which the trustee can start to more effectively communicate with members on the changes to apply under cost sharing from 1 April 2019.

Effect of the application of rule 76.4

Absent of any decision by the JNC on benefit changes under 76.5 (and subject to the outcome of the consultation) then the following will happen under the cost share rules:

The Trustee Board would be expected to determine that the whole of the match would cease.

The rates of salary above the threshold allocated to the USS Investment Builder for members earning above the threshold from member and employer contributions will remain 8% and 12% respectively.

The member contribution rate would increase by 35% of the remainder of the increased cost.

The employer contribution rate would increase by 65% of the remainder of the increased cost.

The impact of bullet two is important to understand, as it effectively means that for a member earning over the salary threshold, the amount paid to his/her USS Investment Builder account will be 20% (12% + 8%) i.e. the excess member contributions over 8% will be diverted to the main fund for DB benefits.

Overall Page 21 of 27

Review proposal and prepare consultation: shorter period as potentially simpler changes

(7 weeks)

Apr 16

Apr23

Apr 30

May 7

May 14

May 21

May 28

Jun4

Jun 11

Jun 18

Jun 25

Jul 2

Jul 9

Jul 16

Jul 23

Jul 30

Aug 6

Aug 13

Aug 20

Aug 27

Sep 3

Sep 10

Sep17

Sep 24

Oct 1

Oct 8

Oct 15

Oct22

Oct29

Nov 5

Nov 12

Nov 19

Nov 26

Dec3

Dec 10

Dec 17

Dec 24

Dec 31

Jan 6

“Revocation” of 23 January JNC resolution; Rule 76.4 invoked

Implementation : achievability ahead of 1 April 2019, based on reasonable approach to cost, risk

Rule 76.4 cost-sharing contributions

Alternative hybrid proposal (e.g. ACAS agreement)

27 April JNC.

End October: after this date, clear, actionable member communications, allowing time for consideration and action are at risk

Key Risk thresholds:

30 July

Start date of employer consultation

Consult with Affected Employees(9 weeks)

Analyse responses and

approvals (Trustee Board)

(4 weeks)

Consult with employers(4 weeks)

Finish / Submit Val’n

2 (weeks)

Discuss and agree final

proposals (JNC)(4 weeks)

23 November JNC have reconsidered recommendation for change/given approval.

Trustee letter

setting out

pos’n

28 SeptemberCompletion of 60 day consultation period (9 weeks).

JNC to consider, and discuss

contribution rates to USSIB on salary above threshold,

among other changes

(4 weeks)

Draft SoC &

RP(2 wks)

26 OctoberTrustee confirm consultation concluded and decides to amend rules. To JNC.

4 JanuaryTrustee completes formal SoC/RP consultation with employers

30 April Deadlineto confirm 23.1 resolution

21 JuneBoard agrees costs required for 76.8 including phasing

Joint Expert Panel (JEP) Terms of Reference drafted and agreed. Independent chair

appointed.

JEP review of Valuation methodology and assumptions

Commence engagement with employers and sector payroll providers re contribution and

payroll implementation requirements

Additional covenant review - estimated 6 weeks effort to inform June board before 1

April 2019 contribution rate set

Mid-late June: after this date, it becomes increasingly difficult for a credible plan to be proposed should there be a decision on benefit changes with the implementation date being 1 April 2019

Ongoing member communications, development and testing of process and system changes, implementation (testing and implementation will continue into the new year)

Restricted Business Sensitive (RBS)JNC 153-4.2

Annex Page 1 of 1

Overall Page 22 of 27

Restricted Business Sensitive (RBS)JNC 153-4.7Page 1 of 1

Committee report for inclusion in Report and Accounts

Executive Summary

Author: Helen PriceAuthorised by: Jonathan Taylor Purpose: ApprovalMeeting: Joint Negotiating Committee (“JNC” or “committee”), 27 April 2018ANNEX: JNC Report

Context:

Input sought/action requested:

Questions/Issues:

Conclusions:

Input received from the business/external advisers:

Input received from other boards/committees:

This paper provides the JNC with a draft of the annual report from the committee for inclusion in the 2018 USS Report and Accounts.

The committee is asked to APPROVE the draft report, for inclusion in the USS Report and Accounts, as at 31 March 2018.

1. Why is the report required?

2. What does the report cover?

3. When will the USS Report and Accounts for the year ending 31 March 2018 be approved?4.

1. The USS Report and Accounts will have a separate governance section available to access on the USS website to summarise the purpose of and key activities carried out by the USSL board and its principal committees.

2. The report provides an overview of the composition and role and responsibilities of the committee, as well as the key activities carried out during the 2017/18 reporting period.

3. The Report and Accounts will be approved by the USSL board at its meeting in July 2018.

The report was drafted by the Governance team with reference to the minutes from the 2017/18 reporting period.

None.

Overall Page 23 of 27

Restricted Business Sensitive (RBS)JNC 153-4.7

Annex APage 1 of 1

Joint negotiating committee reportIntroductionThe joint negotiating committee (JNC) is established under the rules of the scheme. Its constitution, powers and responsibilities are set out in the rules.

The JNC’s purpose is to initiate, consider and/or approve amendments proposed by the trustee to the scheme rules. If, following a valuation, the cost sharing provisions under the rules are triggered the JNC also has the power to decide on contribution increases or decreases and/or benefit changes in respect of the scheme. There are also a number of specific governance decisions that require the JNC’s approval (including the appointment or removal of independent directors to the trustee board and increases in fees for directors and certain other committee members, such as those sitting on the advisory and investment committees).

The JNC comprises five representatives of Universities UK (UUK) and five representatives of the University and College Union (UCU), together with an independent committee member who acts as Chair. Sir Andrew Cubie has chaired the committee since 1 September 2008.

The committee met 11 times during the year. Its funding and benefits sub-committee (FBSC) met formally 8 times and also met for a further informal training meeting. In addition to the training provided at the FBSC informal training meeting, the JNC and/or FBSC have received training during the year on a number of topics including reliance on employers, gilt yield forecasting and the respective roles of the Pensions Regulator, JNC and trustee board in relation to the valuation.

Key activities in 2017/18The JNC (and FBSC) have devoted a substantial amount of time to discussing the 2017 valuation process and proposed benefit design changes. As part of this the JNC and FBSC received regular updates on the progress of the valuation, the proposed valuation assumptions, the technical provisions consultation and the trustee’s interactions with the Pensions Regulator. The JNC and FBSC have also actively participated in discussions in relation to the trustee’s plans to communicate the valuation to members (and wider stakeholders). During the financial year, the JNC has considered (and consented to) amendments to the scheme rules. The JNC has also discussed flexible retirement, the work being undertaken by the trustee to develop member services and flexibilities and accessibility issues as well as receiving and considering detailed ‘insight’ in relation to the scheme’s membership.

MembershipIndependent committee member: Sir Andrew Cubie (Chair).

UUK appointees: Mr Phil Harding, Mr Cliff Vidgeon, Ms Mary Lambe, Mr John Neilson, and Mr Will Spinks.

UCU appointees: Ms Pauline Collins, Dr Marion Hersh, , Ms Christine Haswell, Dr Carlo Morelli, Dr R Prendergast (appointed during the year), Professor Jimmy Donaghey (retired during the year).

Overall Page 24 of 27

Restricted Business Sensitive (RBS)JNC 153-5.1Page 1 of 3

Regulatory update

Executive Summary

Author: Nathan Robinson Authorised by: Steve GoldenPurpose: NoteMeeting: Joint Negotiating Committee (JNC), 27 April 2018

Context:

Input sought/action requested:

Questions/Issues:

Conclusions:

Input received from the business/external advisers:

Input received from other boards/committees:

This paper provides an update on significant policy and regulatory issues that the committee should be aware of that are not covered elsewhere on the agenda.

The committee is requested to NOTE this update.

1. What are the key issues that the executive has been focusing on since the last regulatory update, and have any of these led to engagement with industry bodies or responses to public consultations?

1. This light-touch update provides news from the last four weeks, including i) the consultation issued by the Pensions Regulator (tPR) on the Code of Practice on the authorisation and supervision of Master Trusts, to which USS is drafting a response ii) the annual funding statement from the tPR, and iii) two separate updates from the Work and Pensions Committee (WPC) in Parliament.

This paper has been reviewed by Group Legal.

None.

Overall Page 25 of 27

Restricted Business Sensitive (RBS)JNC 153-5.1Page 2 of 3

The Report

1. Master Trusts

The Code of Practice was published in draft by tPR on 27 March, with tPR open to consultation responses until 8 May. The Code of Practice is extensive at 80 pages. USS is developing a response which involves multiple business areas. The application process for USS to be “authorised” as a master trust requires extensive information on USS systems and processes; the governance and management framework, including assurance on the competence of those running and influencing the scheme; and the scheme’s financial strength.

An oral update shall be provided at the meeting.

2. tPR Annual Funding Statement

Published this month, this set-piece statement is where tPR often seeks to comment on contemporary issues and re-iterate key policy objectives and how it operates as a regulator. It acknowledges the planned intention to review the DB funding code noted in section 4 below. In relation to transfer activity reported last month under the Member insight and statistics paper, tPR asks trustees to “keep records of transfer activity, including details of advisers and schemes to which transfers are made.” This is what USS is doing.

3. Pensions DashboardThe work on the pensions dashboard is progressing. The WPC passed on comment on this with two recommendations in a recent report:

That the Government introduces a single pensions dashboard, hosted by the forthcoming new single financial guidance body, funded by the industry levy and in place by April 2019, and

That the Government mandate all pension providers to provide necessary information to the pensions dashboard. To enable smaller legacy DB schemes sufficient time to comply, we recommend that Government consult with TPR on an implementation timetable. This should ensure that at least 80% of all DB pensions are visible on the dashboard by April 2019, with the remainder to follow.

There is a prototype dashboard in place at present but this is not the publicly hosted version WPC would like to see. The dashboard concept fits into a wider narrative about giving pension savers information to make decisions, and that needs supporting with guidance and advice infrastructure from multiple parties (e.g. individual schemes plus publicly funded bodies and private firms offering services at different fee levels). The WPC also comment on this in the 20+ pages of analysis.

4. Protecting Defined Benefit Pension Schemes

We reported the White Paper1 publication last month, to which the WPC responded with news of setting up an inquiry. WPC are seeking evidence from any “interested parties” on a defined set of questions, with a response date of 18 May. The questions are set out below.

To what extent is improving TPR's effectiveness a matter of greater powers, better use of resources or cultural change in the organisation?

1 Called ‘Security and Sustainability in Defined Benefit Schemes’

Overall Page 26 of 27

Restricted Business Sensitive (RBS)JNC 153-5.1Page 3 of 3

What can be done to strengthen the regime for clearing corporate transactions (like dividend payouts, selloffs, takeovers) that might weaken a pension scheme?

Will a criminal offence provide a meaningful deterrent? What should "prudent" and "appropriate" scheme funding mean? How can consolidation of the fragmented DB landscape be best achieved? Given the difficulties facing DB schemes, is a faster legislative timescale warranted?

.

Overall Page 27 of 27