Embed Size (px)

Citation preview

UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF IOWA

CENTRAL DIVISION

JUDITH CURRAN and MICHAEL EARP, for the use and benefit of the Principal Funds, Inc. Strategic Asset Management (SAM) Balanced Portfolio, Principal Strategic Growth Portfolio, et al.,

Plaintiffs,

v.

Principal Management Corporation and Principal Funds Distributor, Inc.,

Defendants.

Case No. 09-cv-00433-RP-CFB

Action filed: October 28, 2009

MEMORANDUM IN SUPPORT OF DEFENDANTS’ MOTION FOR SUMMARY JUDGMENT

A. Robert Pietrzak [email protected] Andrew W. Stern [email protected] Alex. J. Kaplan [email protected] Sidley Austin LLP 787 Seventh Ave. New York, NY 10019 Telephone: (212) 839-5300 Facsimile: (212) 839-5599

Mark B. Blocker [email protected] Sarah H. Newman [email protected] Sidley Austin LLP One South Dearborn St. Chicago, IL 60603 Telephone: (312) 853-7000 Facsimile: (312) 853-7036

Brian L. Campbell [email protected] Whitfield & Eddy P.L.C. 317 Sixth Avenue, Suite 1200 Des Moines, IA 50309-8002 Telephone: (515) 246-5503 Facsimile: (515) 246-1474

Counsel for Defendants Principal Management Corporation

and Principal Funds Distributor, Inc.

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 1 of 48

TABLE OF CONTENTS Page

TABLE OF AUTHORITIES .......................................................................................................... ii

I. PRELIMINARY STATEMENT ........................................................................................ 1

II. STATEMENT OF FACTS ................................................................................................. 3

A. The Funds At Issue. ................................................................................................ 3

B. The Parties. ............................................................................................................. 4

C. The Relevant Time Period ...................................................................................... 5

D. The SAM Funds Have an Independent Board ........................................................ 6

E. Defendants’ Compensation and the SAM Funds’ Performance ............................. 8

1. The SAM Funds’ Expense Ratios ............................................................... 8

2. The SAM Funds’ 12b-1 Fees .................................................................... 11

3. The SAM Funds’ Investment Performance .............................................. 11

F. The SAM Funds’ Board Requested and Received Extensive Information Annually ................................................................................................................ 13

1. Between March and May, the Board Requested and Received Substantial Information ............................................................................. 13

2. Vedder Price Provided Advice to the Independent Directors in Connection with the 15(c) Process ........................................................... 14

3. The Board’s 15(c) Task Force Met Five Times Per Year ......................... 14

4. In August and September, the Board Conducted Annual Deliberations Regarding the Renewal of PMC’s Advisory Contract ....... 15

5. In December, the Board Conducted Annual Deliberations Regarding the Renewal of PFD’s Contract ............................................... 16

G. PMC, Edge, and PFD Provided Extensive Services to the SAM Funds............... 17

III. ARGUMENT .................................................................................................................... 20

A. Section 36(b) and Binding Authority Impose a Heavy Burden that Plaintiffs Cannot Satisfy ....................................................................................... 20

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 2 of 48

-ii-

B. The Fees Paid by the SAM Funds Were Within the Arms’ Length Range .......... 22

1. PMC Provided High-Quality Services to the SAM Funds ....................... 22

2. The Independent Directors Approved PMC’s Fees Following a Robust Review .......................................................................................... 24

3. The Fees Charged to the SAM Funds Compare Favorably to Other Fee Structures............................................................................................ 26

4. PMC Adequately Shared Economies of Scale with the SAM Funds’ Shareholders.................................................................................. 36

5. PMC’s Profitability Fell Within A Range Courts Have Uniformly Regarded As Acceptable. .......................................................................... 38

6. Any Fall-Out Benefits Were Reasonable and Were Disclosed to the Board. .................................................................................................. 39

C. The SAM Funds’ 12b-1 Fees were within an Arms’ Length Range .................... 39

IV. CONCLUSION ................................................................................................................. 41

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 3 of 48

-iii-

TABLE OF AUTHORITIES

Page(s) CASES

Anderson v. Liberty Lobby, Inc., 477 U.S. 242 (1986) .................................................................................................................20

Benak v. Alliance Capital Mgmt., No. Civ. A. 01-5734, 2004 WL 1459249 (D.N.J. Feb. 9, 2004) .................................21, 22, 28

Braden v. Wal-Mart Stores, Inc., 588 F.3d 585 (8th Cir. 2009) .............................................................................................21, 28

Celotex Corp. v. Catrett, 477 U.S. 317 (1986) .................................................................................................................20

Gallus v. Ameriprise Fin., Inc., 497 F. Supp. 2d 974 (D. Minn. 2007), rev’d on other grounds, 561 F.3d 816 (8th Cir. 2009), vacated, 130 S. Ct. 2340 (2010), reinstated on remand, 2010 WL 5137419 (D. Minn. Dec. 10, 2010), aff’d, 675 F.3d 1173 (8th Cir. 2012) .............................................23, 27

Gallus v. Ameriprise Financial, Inc., 675 F.3d 1173 (8th Cir. 2012) ......................................................................................... passim

Gartenberg v. Merrill Lynch Asset Mgmt., Inc., 694 F.2d 923 (2d Cir. 1982)............................................................................................. passim

Hecker v. Deere & Co., 556 F.3d 575 (7th Cir. 2009) .........................................................................................8, 20, 28

In re Am. Mut. Funds Fee Litig., No. CV 04-5593, 2009 WL 5215755 (C.D. Cal. Dec. 28, 2009) .................................... passim

Jones v. Harris Assocs. L.P., 130 S. Ct. 1418 (2010) ..................................................................................................... passim

Jones v. Harris Assocs. L.P., No. 04 C 8305, 2007 WL 627640 (N.D. Ill. Feb. 27, 2007), aff’d on other grounds, 527 F.3d 627 (7th Cir. 2007), vacated and remanded, 130 S. Ct. 1418 (2010) ................27, 38

Kalish v. Franklin Advisers, Inc., 742 F. Supp. 1222 (S.D.N.Y. 1990), aff’d, 928 F.2d 590 (2d Cir. 1991) ........................ passim

Kasilag v. Hartford Inv. Fin. Serv., LLC, No. 11-1083, 2012 WL 6568409 (D.N.J. Dec. 17, 2012) ..................................................11, 40

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 4 of 48

-iv-

Krinsk v. Fund Asset Mgmt., Inc., 715 F. Supp. 472 (S.D.N.Y. 1988), aff’d, 875 F.2d 404 (2d Cir. 1989) ......................26, 27, 36

Matsushita Elec. Indus. Co., Ltd. v. Zenith Radio Corp., 475 U.S. 574 (1986) .................................................................................................................20

Meyer v. Oppenheimer Mgmt. Corp., 707 F. Supp. 1394 (S.D.N.Y. 1988), aff’d, 895 F.2d 861 (2d Cir. 1990) ................................38

Schuyt v. Rowe Price Prime Reserve Fund Inc., 663 F. Supp. 962 (S.D.N.Y. 1987), aff’d per curiam, 835 F.2d 45 (2d Cir. 1987) ...........37, 38

Strougo v. BEA Assocs., 188 F. Supp. 2d 373 (S.D.N.Y. 2002)......................................................................................27

STATUTES

15 U.S.C. §§ 80a-2(a) ......................................................................................................................6

15 U.S.C. § 80a-10(a) ......................................................................................................................6

15 U.S.C. § 80a-12 .....................................................................................................................3, 28

15 U.S.C. § 80a-15 .........................................................................................................................13

15 U.S.C. § 80a-35 .................................................................................................................5, 6, 24

OTHER AUTHORITIES

17 C.F.R. 270.0-1(a)(7)....................................................................................................................6

17 C.F.R. § 274.11 ...........................................................................................................................8

Fed. R. Civ. P. 56 ...........................................................................................................................20

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 5 of 48

-1-

Defendants Principal Management Corporation (“PMC”) and Principal Funds

Distributor, Inc. (“PFD”) (collectively, “Defendants”), by their undersigned counsel, respectfully

submit this Memorandum in support of their Motion for Summary Judgment.

I. PRELIMINARY STATEMENT

Plaintiffs own a small number of shares in two high performing mutual funds managed

by PMC and distributed by PFD. Despite the solid performance of these funds and the

reasonableness of the total fees that Defendants charged for their services, Plaintiffs assert in this

action that Defendants received excessive compensation in breach of their fiduciary duties under

Section 36(b) of the Investment Company Act of 1940 (the “ICA”), 15 U.S.C. § 80a-35(b). The

record demonstrates that Plaintiffs cannot satisfy the stringent standard imposed by Congress and

the United States Supreme Court; i.e., Plaintiffs cannot raise a genuine issue of material fact that

would permit the Court to conclude that the fees Defendants charged were “so disproportionately

large that [they] bear[] no reasonable relationship to the services rendered and could not have

been the product of arm’s length bargaining.” Jones v. Harris Assocs. L.P., 130 S. Ct. 1418,

1426 (2010) (citation omitted). Moreover, the critical evidence to the contrary dooms Plaintiffs’

claims and compels summary judgment in favor of Defendants.

During the relevant period (October 29, 2008 – October 28, 2011), the two funds in

which Plaintiffs invested – the Principal Funds, Inc. Strategic Asset Management Balanced

Portfolio ( “SAM Balanced”) and the Strategic Asset Management Strategic Growth Portfolio

(“SAM Strategic Growth”) (collectively, the “SAM Funds”) – provided investors with solid

long-term investment performance; were consistently ranked among the best in their respective

mutual fund peer groups; were run by portfolio managers who employed carefully designed and

sophisticated investment processes; and paid fees to PMC and PFD that were within the range

paid by similar but lower-performing mutual funds. Indeed, in 2011, the performance of the two

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 6 of 48

-2-

SAM Funds over the previous five years, net of fees (i.e., subtracting fees from performance),

placed them in the top 28 percent and 42 percent of their respective Morningstar comparative

categories. Moreover, the SAM Funds’ expense ratios (i.e., the total, all-in cost paid by

investors) were particularly favorable for their investors; for example, in 2011, the SAM

Balanced Fund’s expense ratio was in the 38th percentile for its peer group (or lower than 62

percent of the funds in its category), and the SAM Strategic Growth Fund’s expense ratio was in

the 50th percentile. These competitive fees, particularly in light of the SAM Funds’ investment

performance, are plainly not “so disproportionately large” that they bear “no reasonable

relationship to the services rendered.” Jones, 130 S. Ct. at 1426.

All of this information, along with a substantial amount of data and documents, including

“15(c) Materials” (which will be described herein), was supplied to the SAM Funds’ Board of

Directors, who in turn reached informed conclusions that Defendants’ fees were reasonable and,

therefore, annually renewed PMC’s investment management contracts and PFD’s distribution

contracts. Under these circumstances, Section 36(b) does not “permit a compensation agreement

to be reviewed in court for ‘reasonableness,’” nor does it call for “second-guessing of informed

board decisions” approving an advisor’s fees. Id. at 1423, 1430. Moreover, as discussed herein,

the substantial record in this action otherwise demonstrates as a matter of law that all of the

“Gartenberg factors” (the six considerations that the fees paid to PMC and PFD were not

disproportionately large) weigh decisively in favor of Defendants.

Prior to the production of this evidence, this Court suggested in response to Defendants’

motion to dismiss that this case is “unlikely” to be resolved on summary judgment because

Defendants’ arguments in favor of their motion to dismiss raised “what appear to be fact-

intensive inquiries.” Dkt. 38 at 20. Defendants understand the Court’s earlier concern, but in

light of the extremely heavy burden the Supreme Court and Eighth Circuit have imposed on

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 7 of 48

-3-

plaintiffs in Section 36(b) cases, the undisputed material facts of the case demonstrate that

Plaintiffs cannot prove an excessive fee claim under Section 36(b). Indeed, under similar

circumstances, the Eighth Circuit recently affirmed the grant of summary judgment in favor of

the defendant investor advisors in Gallus v. Ameriprise Financial, Inc., 675 F.3d 1173 (8th Cir.

2012). The critical and indisputable facts here are that Defendants have delivered good

performance to its shareholders at a price well within the range of the SAM Funds’ peers.

Accordingly, summary judgment should be granted in favor of Defendants, and all of Plaintiffs’

claims should be dismissed with prejudice.

II. STATEMENT OF FACTS1

A. The Funds At Issue.

This case involves two Principal mutual funds: the SAM Balanced and the SAM

Strategic Growth Funds (collectively, the “SAM Funds”). SUF ¶ 1; Am. Compl. ¶ 1: A4. The

SAM Funds are “funds of funds” that invest in other Principal Financial, Inc. (“PFI”) mutual

funds, in accordance with Section 12 of the ICA (permitting the creation of “funds of funds” that

acquire the shares of other mutual funds within the same family of funds). SUF ¶ 2; see also 15

U.S.C. § 80a-12, Dkt. 38 at 2 n.2. The SAM Funds are “target risk” funds, which are funds that

allow investors the ability to invest based on their risk tolerance. SUF ¶ 3. PFI offers five

different SAM funds (including the two SAM Funds at issue in this case), each with a different

level of risk, depending on the mix of funds emphasizing stocks and funds emphasizing bonds.

Id. ¶ 4. The SAM Balanced Fund offers a medium degree of risk among the five SAM funds, in

1 Throughout this brief, “SUF” refers to the Defendants’ Statement of Undisputed Facts, which has been submitted in support of this motion. Deposition transcripts are referred to with the deponent’s name and “Tr.”; for example, the deposition of Judith Curran is referenced as “Curran Tr.” References to “Am. Compl. ¶ _” refer to particular paragraphs in Plaintiffs’ Amended Complaint (Dkt. No. 17), filed on January 15, 2010. References to “A__” are specific page numbers in the Appendix.

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 8 of 48

-4-

that its portfolio is more “balanced” between shares of funds that emphasize stocks and funds

that emphasize bonds; the SAM Strategic Growth Fund offers the highest risk among the five

SAM funds because it is heavily weighted toward funds that emphasize investment in stocks. Id.

¶¶ 6-7. By investing in one of the SAM Funds, an investor can obtain a diversified portfolio

tailored to the amount of risk the investor is willing to bear. Id. ¶ 8.

The SAM Funds are diversified portfolios of PFI, an investment company originally

incorporated under Maryland law, headquartered in Des Moines, and registered under the ICA,

15 U.S.C. § 80a-1, et seq. SUF ¶ 9; Am. Compl. ¶ 8: A5. In 2006, PFI2 acquired the SAM funds

from Washington Mutual. SUF ¶ 10.

Each of the SAM Funds has ten share classes: A, B, C, J, Institutional, R-1, R-2, R-3, R-

4, and R-5. Id. ¶ 12. Share classes A, B, and C primarily target retail markets; share class J is

reserved for IRA rollovers from members of retirement plans serviced by Principal Life

Insurance Company; Institutional share class is reserved for large institutional investors; and

share classes R-1 through R-5 are designed to be held in employer-sponsored retirement plans.

Id. ¶ 13.

B. The Parties.

Plaintiffs. Plaintiffs Judith Curran (“Curran”) and Michael Earp (“Earp”) (collectively,

“Plaintiffs”) purport to bring this action derivatively on behalf of the SAM Balanced and the

SAM Strategic Growth Funds. SUF ¶ 1; Am. Compl. ¶ 1: A4. Prior to 2006, Ms. Curran

invested in the SAM Balanced Fund. SUF ¶ 14. She has maintained an investment in the SAM

Balanced Fund throughout the Relevant Time Period (defined in Section II-B, infra). SUF ¶ 15;

Am. Compl. ¶ 6: A4. Since 2010, Plaintiffs’ counsel, Keller Rohrback, has paid the brokerage

2 Principal Investors Fund, Inc. (“PIF”) changed its name to Principal Funds, Inc. (“PFI”) in June 2008. SUF ¶ 11.

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 9 of 48

-5-

fees for Ms. Curran’s account. SUF ¶ 16. In or about late 2006, Mr. Earp invested in the SAM

Strategic Growth Fund, and he has maintained the investment to date. SUF ¶¶ 17-18; Am.

Compl. ¶ 7: A4.

PMC. Defendant Principal Management Corporation (“PMC”) serves as the investment

adviser to each of the SAM Funds. SUF ¶¶ 19-20; Am. Compl. ¶ 10: A5. Each year, PMC

enters into a contract with PFI that governs the terms of its relationship with the SAM Funds and

dictates the fees that PMC can charge (the “Advisory Agreements” or “Agreements”).3 SUF ¶

20. The SAM Funds’ Board of Directors (described below) approved the continuation of the

Agreements for one-year periods in September 2008, September 2009, September 2010, and

September 2011. Id. ¶ 23. As of 2011, the SAM Funds were two of the 98 funds in the Principal

mutual fund complex, which includes both PFI mutual funds and Principal Variable Contracts

(“PVC”) mutual funds. Id. ¶ 21.

PFD. Principal Funds Distributor (“PFD”) is a registered broker-dealer under the

Securities Exchange Act of 1934. SUF ¶ 24; Am. Compl. ¶ 12: A5. PFD, which is affiliated

with PMC, receives compensation from the SAM Funds as the distributor and principal

underwriter of the SAM Funds. SUF ¶¶ 25-26; Am. Compl. ¶ 12: A5. Each year, the Board

approves a distribution plan and agreements (the “Distribution Agreements”) that set forth the

amount of 12b-1 fees that PFD may charge the SAM Funds. Id. ¶ 27.

C. The Relevant Time Period

The initial complaint in this action was filed on October 28, 2009. SUF ¶ 28; Dkt. No. 1.

Section 36(b)(3) of the ICA provides that a claim for damages is limited to the one-year period

3 PMC serves as the investment advisor to all of the PFI funds and PVC funds, including the three other PFI SAM portfolios, which are not the subject of this lawsuit: SAM Flexible Income Portfolio, SAM Conservative Balanced Portfolio, and SAM Conservative Growth Portfolio. SUF ¶¶ 21-22.

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 10 of 48

-6-

prior to the date of the commencement of an action. See 15 U.S.C. § 80a-35(b)(3). Accordingly,

the relevant time period for this case begins on October 28, 2008. SUF ¶ 29. To preserve their

arguments regarding purported damages for successive years, Plaintiffs filed “anniversary

complaints” on October 28, 2010 (Case No. 10-508 Dkt. 1); October 28, 2011 (Dkt. 93)4; and

October 28, 2012 (Case No. 12-513 Dkt. 1). SUF ¶ 30. The October 28, 2010 and October 28,

2011 anniversary complaints were consolidated with this case. SUF ¶ 31; see Dkt. Nos. 62 and

96. Because there was no discovery on the period from October 28, 2011 to October 28, 2012,

the parties have agreed that this period is not currently at issue. SUF ¶ 33. Thus, the relevant

time period for this action is from October 29, 2008 to October 28, 2011 (“Relevant Time

Period”). Id. ¶ 34.

D. The SAM Funds Have an Independent Board

The SAM Funds in which Plaintiffs invested were and continue to be subject to the ICA

and regulations promulgated thereunder, which establish a number of operational, recordkeeping

and disclosure requirements for mutual funds, and also govern the relationship between a mutual

fund and its investment adviser. SUF ¶¶ 35-36. For example, the ICA requires a mutual fund to

have a board of directors, at least 40 percent of whom must be independent. See 15 U.S.C. §§

80a-2a(19), 80a-10(a) (defining “independent” as not owning or controlling 5 percent or more of

the company’s securities and not being an officer, director, partner, employee, or investment

adviser of such company); SUF ¶ 37. In addition, at least 75 percent of a mutual fund’s board is

required to be independent in order for the fund to avail itself of certain exemptions. See 17

C.F.R. 270.0-1(a)(7). Plaintiffs concede that 75 percent of the Board of Directors that oversaw

4 Plaintiffs initially filed the Second Anniversary Complaint as Dkt. No. 93. The Court ordered this complaint to be stricken from the case, re-filed as a new case, and then consolidated with the original case. SUF ¶ 32.

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 11 of 48

-7-

the SAM Funds (the “Board”) was independent during the Relevant Time Period. SUF ¶ 39;

Am. Compl. ¶ 96: A45.

In September of each year during the Relevant Time Period, the Board approved the

Advisory Contracts with PMC. SUF ¶ 23. Each time, the Board was comprised of twelve

directors, including nine who were not affiliated with PMC. Id. ¶ 40. The nine independent

directors were Elizabeth Ballantine, Kristianne Blake, Craig Damos, Richard W. Gilbert, Mark

A. Grimmett, Fritz S. Hirsch, William C. Kimball, Barbara Lukavsky, and Daniel Pavelich

(collectively, the “Independent Directors”). Id. ¶ 41. The remaining three directors, who also

served as officers of PMC, were Ralph C. Eucher, Nora M. Everett, and William G. Papesh.5 Id.

¶ 44.

The Board is comprised of highly qualified and experienced individuals with

distinguished business careers. See SUF ¶¶ 53-82. All Independent Directors have served as

senior executives (id. ¶¶ 61-62, 65, 69, 73, 77, 80, 83, 85, 88); five have served as Chief

Executive Officers of publicly-held companies (id. ¶¶ 69, 80, 83, 85, 88), one has served as

Chief Operating Officer (id. ¶ 73), and two have served as Chief Financial Officer (id. ¶¶ 69, 77).

Eight have served as directors in other companies (SUF ¶¶ 62, 66, 70, 74, 77, 80, 83, 88), one

served as director of another mutual fund (id. ¶ 66), and another served on the board of a mutual

fund advisor (id. ¶ 74). Three Independent Directors have advanced degrees in business or law

(id. ¶¶ 60, 76, 79); five have CPA licenses (id. ¶¶ 64, 68, 76, 79, 87); and one is a certified

financial planner (id. ¶ 64).

Throughout the Relevant Time Period, the Independent Directors received legal advice

from investment management attorneys with Vedder Price, a large national law firm with

5 Larry Zimpleman served on the Board until Dec. 8, 2008. SUF ¶¶ 42-43. Upon Mr. Zimpleman’s retirement, Nora Everett was appointed to the Board. Id. ¶ 43.

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 12 of 48

-8-

extensive and nationally-recognized expertise in the representation of mutual funds and their

directors or trustees. SUF ¶¶ 89-90. For example, Cathy O’Kelly, a partner at Vedder Price who

has served as counsel to the Independent Directors, has achieved a number of distinctions in her

career representing mutual funds and their boards. Id. ¶ 91.

E. Defendants’ Compensation and the SAM Funds’ Performance

1. The SAM Funds’ Expense Ratios

The SAM Funds disclosed their expense ratios – which is a ratio calculated as the total

fees charged to a fund’s shareholders expressed as a percentage of that fund’s average net assets

– in materials provided to investors, and in accordance with governing regulations. See SUF ¶¶

92, 94 (disclosed in prospectuses, annual and semi-annual reports, website, and third-party

sources). The expense ratio, which is also referred to as the annual fund operating expenses,

includes, among other things, the management fees that PMC charges to manage the SAM

Funds’ investment portfolios, any non-management fees, and the 12b-1 distribution fees that

PFD charges in connection with the marketing, selling, and distribution of mutual fund shares

(and all of these fee components were disclosed to investors). Id. ¶¶ 92, 95. While not all

mutual fund advisers choose to provide the same services under the umbrella of what is labeled a

“management fee,” every fund is required to calculate and publish its total expense ratio (which

the SEC and funds also refer to as “total annual fund operating expenses”). See, e.g., SUF ¶ 93;

17 C.F.R. § 274.11 (directing funds to file disclosures on SEC Form N-1A); SEC Form N-1A

Instructions, Item 3 at 11-16 (requiring disclosure of “total annual fund operating expenses”);

U.S. Securities and Exchange Commission, “Invest Wisely: An Introduction to Mutual Funds”

(“SEC’s Introduction to Mutual Funds”), available at

http://www.sec.gov.investor/pubs/inwsmf.htm (last visited February 20, 2013), at 9 (defining

total annual fund operating expenses as “expense ratio”). This permits investors to make apples-

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 13 of 48

-9-

to-apples comparisons of the total expenses paid by shareholders of various funds. See, e.g.,

Hecker v. Deere & Co., 556 F.3d 575, 586 (7th Cir. 2009) (The “total fee . . . is the critical figure

for someone interested in the cost of including a certain investment in her portfolio and the net

value of that investment.”); SEC’s Introduction to Mutual Funds at 9 (informing investors that

“[l]ooking at the expense ratio can help you make comparisons among funds”).

During the Relevant Time Period, the Board was provided independent analyses of fund

expenses prepared by Lipper, Inc. (“Lipper”), a well-recognized, independent source of mutual

fund industry data, which included the following information regarding the expense ratio for

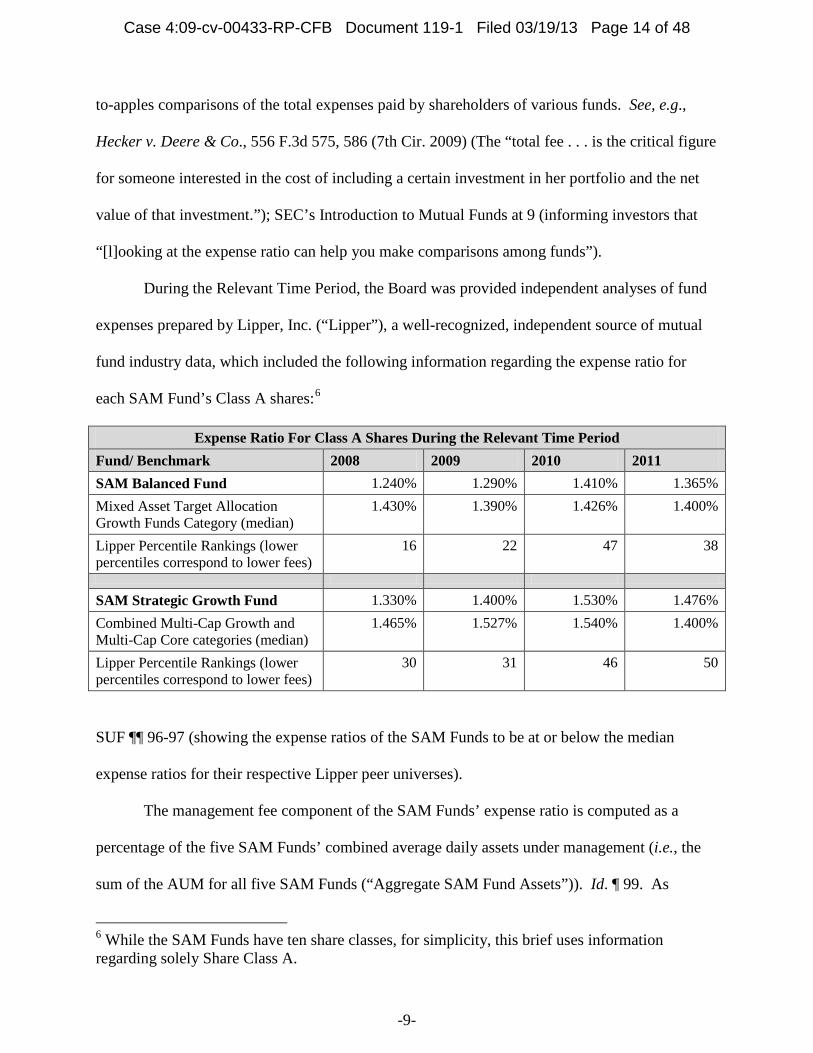

each SAM Fund’s Class A shares:6

Expense Ratio For Class A Shares During the Relevant Time Period Fund/ Benchmark 2008 2009 2010 2011 SAM Balanced Fund 1.240% 1.290% 1.410% 1.365% Mixed Asset Target Allocation Growth Funds Category (median)

1.430% 1.390% 1.426% 1.400%

Lipper Percentile Rankings (lower percentiles correspond to lower fees)

16 22 47 38

SAM Strategic Growth Fund 1.330% 1.400% 1.530% 1.476% Combined Multi-Cap Growth and Multi-Cap Core categories (median)

1.465% 1.527% 1.540% 1.400%

Lipper Percentile Rankings (lower percentiles correspond to lower fees)

30 31 46 50

SUF ¶¶ 96-97 (showing the expense ratios of the SAM Funds to be at or below the median

expense ratios for their respective Lipper peer universes).

The management fee component of the SAM Funds’ expense ratio is computed as a

percentage of the five SAM Funds’ combined average daily assets under management (i.e., the

sum of the AUM for all five SAM Funds (“Aggregate SAM Fund Assets”)). Id. ¶ 99. As

6 While the SAM Funds have ten share classes, for simplicity, this brief uses information regarding solely Share Class A.

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 14 of 48

-10-

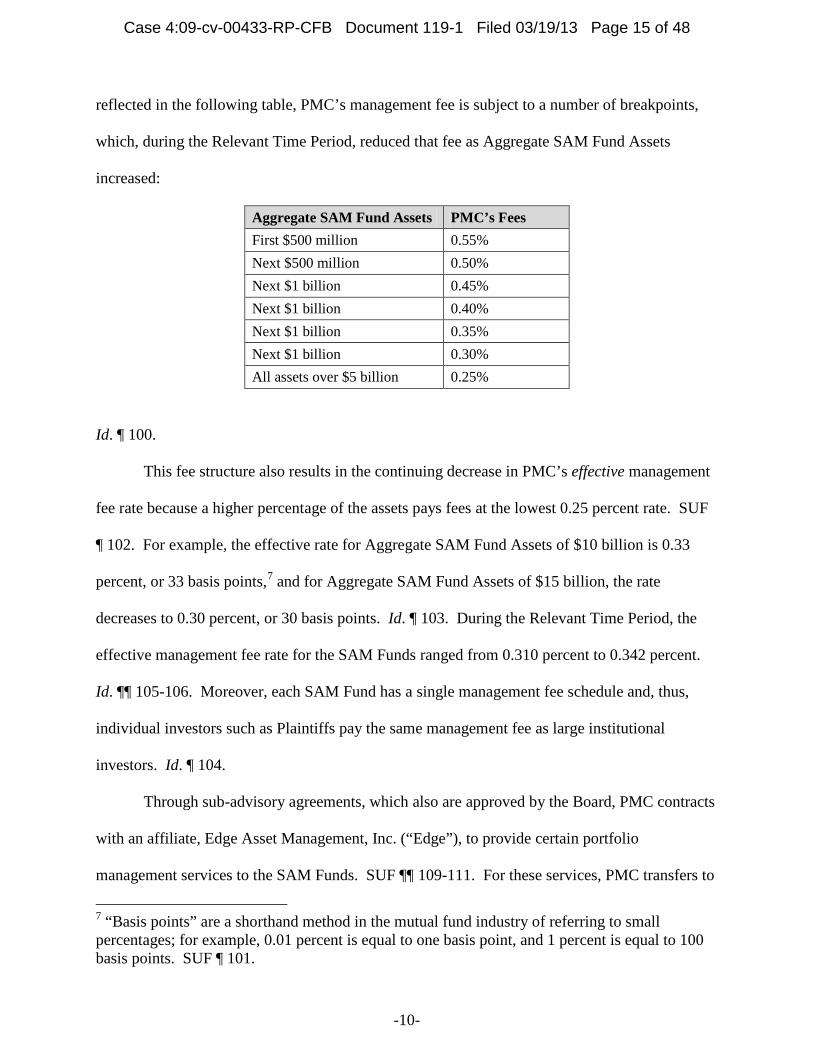

reflected in the following table, PMC’s management fee is subject to a number of breakpoints,

which, during the Relevant Time Period, reduced that fee as Aggregate SAM Fund Assets

increased:

Aggregate SAM Fund Assets PMC’s Fees First $500 million 0.55% Next $500 million 0.50% Next $1 billion 0.45% Next $1 billion 0.40% Next $1 billion 0.35% Next $1 billion 0.30% All assets over $5 billion 0.25%

Id. ¶ 100.

This fee structure also results in the continuing decrease in PMC’s effective management

fee rate because a higher percentage of the assets pays fees at the lowest 0.25 percent rate. SUF

¶ 102. For example, the effective rate for Aggregate SAM Fund Assets of $10 billion is 0.33

percent, or 33 basis points,7 and for Aggregate SAM Fund Assets of $15 billion, the rate

decreases to 0.30 percent, or 30 basis points. Id. ¶ 103. During the Relevant Time Period, the

effective management fee rate for the SAM Funds ranged from 0.310 percent to 0.342 percent.

Id. ¶¶ 105-106. Moreover, each SAM Fund has a single management fee schedule and, thus,

individual investors such as Plaintiffs pay the same management fee as large institutional

investors. Id. ¶ 104.

Through sub-advisory agreements, which also are approved by the Board, PMC contracts

with an affiliate, Edge Asset Management, Inc. (“Edge”), to provide certain portfolio

management services to the SAM Funds. SUF ¶¶ 109-111. For these services, PMC transfers to

7 “Basis points” are a shorthand method in the mutual fund industry of referring to small percentages; for example, 0.01 percent is equal to one basis point, and 1 percent is equal to 100 basis points. SUF ¶ 101.

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 15 of 48

-11-

Edge a portion of the management fee, here a flat fee of 0.0416 percent on all assets of the SAM

Funds, with no breakpoints, computed on a monthly basis. Id. ¶ 112. At all times during the

Relevant Time Period, PMC maintained responsibility for all of Edge’s portfolio management

decisions. Id. ¶ 114.

2. The SAM Funds’ 12b-1 Fees

Each SAM Fund’s Share Class A also pays 12b-1 distribution fees to PFD for marketing,

selling and distributing mutual fund shares, and for shareholder services. SUF ¶¶ 26, 116. This

fee is included in the total expense ratio and fully disclosed to shareholders. Id. ¶¶ 94-95, 115.

Moreover, 12b-1 distribution fees are approved on an annual basis by the Independent Directors.

Id. ¶ 27. Each Class A share of the SAM Funds charges a 12b-1 fee of 0.25 percent of the

average daily net assets of the SAM Funds. Id. ¶ 117. A 12b-1 fee of 25 basis points is

“customary” for Class A shares. See, e.g., Kasilag v. Hartford Inv. Fin. Serv., LLC, No. 11-

1083, 2012 WL 6568409, at *8 (D.N.J. Dec. 17, 2012) (quoting SEC Proposed Rules, Mutual

Fund Distrib. Fees, 75 Fed. Reg. 47064, 47070 (proposed Aug. 4, 2010) (“Class ‘A’ shares . . .

often have a 12b-1 fee of about 25 basis points.”)).

3. The SAM Funds’ Investment Performance

During the Relevant Time Period, the SAM Funds generated strong investment returns.

SUF ¶¶ 119-130. Each year, the Board received performance data compiled by Morningstar,

Inc. (“Morningstar”), a well-recognized, independent source of mutual fund industry data,

showing the one-year, three-year, and five-year performance of the SAM Funds, along with their

ranking in their Morningstar categories. Id. ¶ 120. In 2011, for example, the Board received a

number of data points regarding performance during that year, calculated net of fees (i.e.,

subtracting fees from performance), including (a) the results of the index that the Board used as a

benchmark for the fund; (b) the median performance of funds in the Morningstar category or

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 16 of 48

-12-

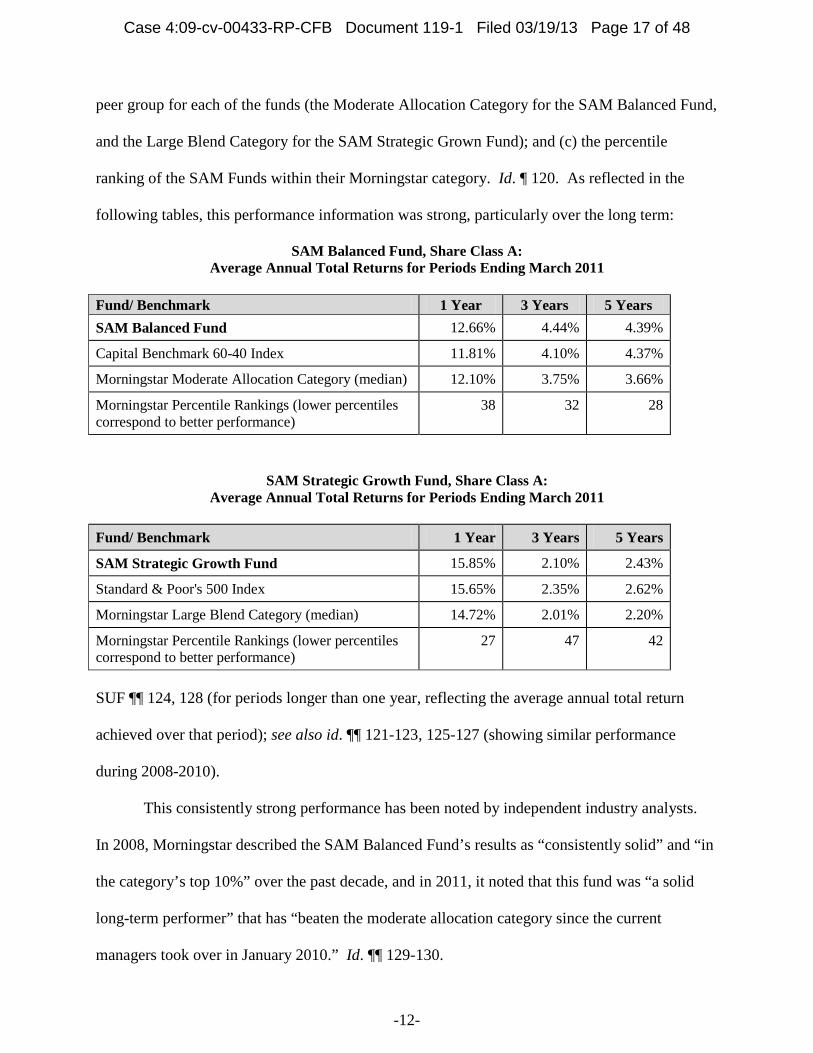

peer group for each of the funds (the Moderate Allocation Category for the SAM Balanced Fund,

and the Large Blend Category for the SAM Strategic Grown Fund); and (c) the percentile

ranking of the SAM Funds within their Morningstar category. Id. ¶ 120. As reflected in the

following tables, this performance information was strong, particularly over the long term:

SAM Balanced Fund, Share Class A: Average Annual Total Returns for Periods Ending March 2011

Fund/ Benchmark 1 Year 3 Years 5 Years SAM Balanced Fund 12.66% 4.44% 4.39%

Capital Benchmark 60-40 Index 11.81% 4.10% 4.37%

Morningstar Moderate Allocation Category (median) 12.10% 3.75% 3.66%

Morningstar Percentile Rankings (lower percentiles correspond to better performance)

38 32 28

SAM Strategic Growth Fund, Share Class A: Average Annual Total Returns for Periods Ending March 2011

Fund/ Benchmark 1 Year 3 Years 5 Years

SAM Strategic Growth Fund 15.85% 2.10% 2.43%

Standard & Poor's 500 Index 15.65% 2.35% 2.62%

Morningstar Large Blend Category (median) 14.72% 2.01% 2.20%

Morningstar Percentile Rankings (lower percentiles correspond to better performance)

27 47 42

SUF ¶¶ 124, 128 (for periods longer than one year, reflecting the average annual total return

achieved over that period); see also id. ¶¶ 121-123, 125-127 (showing similar performance

during 2008-2010).

This consistently strong performance has been noted by independent industry analysts.

In 2008, Morningstar described the SAM Balanced Fund’s results as “consistently solid” and “in

the category’s top 10%” over the past decade, and in 2011, it noted that this fund was “a solid

long-term performer” that has “beaten the moderate allocation category since the current

managers took over in January 2010.” Id. ¶¶ 129-130.

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 17 of 48

-13-

F. The SAM Funds’ Board Requested and Received Extensive Information Annually

As explained, PMC serves as investment adviser to each of the SAM Funds pursuant to

Advisory Agreements between PMC and PFI. See Section II.A, supra. The ICA requires these

Advisory Agreements to be approved annually by a majority of the independent members of the

SAM Funds’ Board, as well as a majority of the directors comprising the full Board. SUF ¶ 131;

15 U.S.C. §§ 80a-15(a), (c). To that end, the ICA requires that fund directors request and

evaluate, and that the mutual fund’s adviser supply, information “reasonably . . . necessary” to

evaluate the terms of the agreement. SUF ¶ 132; 15 U.S.C. § 80a-15(c). This annual process is

known as the “15(c) Process” and it occurs over a number of months, as described below. SUF ¶

132.

1. the Board Requested and Received Substantial Information

SUF ¶¶ 133-136. In response, PMC provided

extensive materials to the Independent Directors, including, among other things, information on

the absolute and relative performance of the SAM Funds and the other Principal Funds; the fees

charged and services provided to PFI and the SAM Funds; economies of scale;

fallout benefits, such as trading, brokerage, and commission recapture, including soft dollar

arrangements; 8 Id. ¶ 137. The Independent Directors were also

provided an analysis reflecting PMC’s profitability with respect to each of the SAM Funds,

8 The Form ADV is a regulatory disclosure that details information concerning an investment adviser’s business, ownership, clients, employees, business practices, affiliations, and any disciplinary action taken with respect to the adviser. See SUF ¶ 138.

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 18 of 48

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 19 of 48

-15-

4. In August and September, the Board Conducted Annual Deliberations Regarding the Renewal of PMC’s Advisory Contract

Each August and September, the Independent Directors conducted contract renewal

deliberations during three to four days of meetings. SUF ¶¶ 159-162.

Id. During these meetings, the

Independent Directors reviewed information

, as well as information provided by Lipper and Morningstar. Id. ¶ 163. The

Independent Directors also discussed with PMC representatives the operations for each of the

SAM Funds; the nature, extent, and quality of the advisory and other services provided by PMC

to the SAM Funds, including the performance of the SAM Funds; the overall expense ratios of

each class of shares of the SAM Funds; and any economies of scale and other benefits derived by

PMC from its relationship with the SAM Funds. Id. ¶ 164.

Id. ¶ 165.

Each September, following careful consideration of the foregoing information, the Board

concluded that the quality of services that PMC provided to the SAM Funds was consistently

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 20 of 48

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 21 of 48

-17-

G. PMC, Edge, and PFD Provided Extensive Services to the SAM Funds

During the Relevant Time Period, PMC, Edge, and PFD provided extensive portfolio

management and non-portfolio management services to the SAM Funds. Through a process

known as the “Principal Due Diligence Program,” PMC vetted, selected, and monitored the

menu of funds available for investment by the SAM Funds, as well as the subadvisors of those

funds. SUF ¶ 177. Under the Principal Due Diligence Program, PMC conducted comprehensive

research and analysis to identify, retain, monitor and evaluate subadvisors for the Principal

Funds, including Edge. Id. ¶ 178.

In accordance with each SAM Fund’s defined investment strategy, portfolio managers at

Edge employed an active investment process,

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 22 of 48

-18-

At all times during the Relevant Time Period, PMC maintained responsibility for all of

Edge’s portfolio management decisions. Id. ¶ 114.

PMC also provided the following substantial accounting, regulatory, compliance, transfer

agency, and retirement plan services to the SAM Funds:

• Maintaining corporate financial records and determining the daily net asset value (“NAV”) on an aggregate and per share basis.

• Providing portfolio accounting services, including: o Providing trading services to fund subadvisors;

o Maintaining records for all securities owned by a fund;

o Coordinating portfolio adjustments with the custodian and trading staff;

o Ensuring the proper recording of dividends and interest on portfolio securities; and

o Assembling the daily values of portfolio securities for purposes of determining the daily NAV per share.

• Calculating taxable income and realized gains available to be distributed to fund shareholders.

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 23 of 48

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 24 of 48

-20-

III. ARGUMENT

Summary judgment should be granted in favor of Defendants because Plaintiffs cannot

“raise[] a genuine issue of material fact that [Principal] charged ‘a fee that is so

disproportionately large that it bears no reasonable relationship to the services rendered and

could not have been the product of arm’s length bargaining.’” Gallus, 675 F.3d at 1179

(citations omitted). Fed. R. Civ. P. 56 “mandates the entry of summary judgment, after adequate

time for discovery and upon motion, against a party who fails to make a showing sufficient to

establish the existence of an element essential to that party’s case, and on which that party will

bear the burden of proof at trial.” Celotex Corp. v. Catrett, 477 U.S. 317, 322 (1986). A genuine

dispute as to material facts exists only when those facts “might affect the outcome of the suit

under the governing law.” Anderson v. Liberty Lobby, Inc., 477 U.S. 242, 248 (1986). For the

following reasons, there is no “genuine” dispute such that a reasonable fact finder “could return a

verdict for the nonmoving” Plaintiffs. Id.; see also Matsushita Elec. Indus. Co., Ltd. v. Zenith

Radio Corp., 475 U.S. 574, 586-87 (1986) (non-movant must “do more than simply show that

there is some metaphysical doubt as to the material facts”); Gallus, 675 F.3d at 1179.

A. Section 36(b) and Binding Authority Impose a Heavy Burden that Plaintiffs Cannot Satisfy

Section 36(b) of the Investment Company Act of 1940 provides, in pertinent part:

[T]he investment adviser of a registered investment company shall be deemed to have a fiduciary duty with respect to the receipt of compensation for services, or of payments of a material nature, paid by such registered investment company, or by the security holders thereof, to such investment adviser or any affiliated person of such investment adviser.

15 U.S.C. § 80a-35(b). The total compensation paid to an investment adviser, including all fees

and costs, expressed as a percentage of the mutual fund’s average net assets, is called the

“expense ratio” or “annual fund operating expenses.” SUF ¶ 92; accord Hecker, 556 F.3d at

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 25 of 48

-21-

586 (noting that the prospectus disclosed the funds’ total annual operating expenses and stating

that the “total fee” is “the crucial figure”); Braden v. Wal-Mart Stores, Inc., 588 F.3d 585, 595-

96, n.5 & 6 (8th Cir. 2009) (applying same); Benak v. Alliance Capital Mgmt., No. Civ. A. 01-

5734, 2004 WL 1459249, at *9 (D.N.J. Feb. 9, 2004) (noting that ICA’s legislative history

directs that “court look at . . . all compensation and payments received”) (citation omitted).

Cases interpreting and applying Section 36(b), including the Supreme Court’s 2010

decision in Jones, have established a very high bar for suits claiming that fees are excessive: “to

face liability . . . . an investment adviser must charge a fee that is so disproportionately large

that it bears no reasonable relationship to the services rendered and could not have been the

product of arm’s length bargaining.” Jones, 130 S. Ct. at 1425 (emphasis added) (citing

Gartenberg, 694 F.2d at 928). The Supreme Court emphasized that, in contrast to a common law

action for breach of fiduciary duty, the ICA places the burden squarely on the plaintiff to prove

“that the fee is outside the range that arm’s-length bargaining would produce.” Jones, 130 S. Ct

at 1427. Likewise, the concurring opinion in Jones emphasized the “heavy burden of proof” that

the ICA requires. Id. at 1431.

In Jones, the Supreme Court also clarified that “Section 36(b) is sharply focused on the

question of whether the fees themselves were excessive.” Id. at 1430 (citation omitted). Thus,

an investment adviser is subject to liability only if its fees are deemed excessive by an objective

measure, and as the Eighth Circuit has concluded, “after Jones, a process-based failure alone

does not constitute an independent violation of § 36(b).” Gallus, 675 F.3d at 1179. To make this

objective determination, the Supreme Court endorsed the use of a non-exclusive list of the

following six factors (known as the “Gartenberg factors,” and named for the case that first

announced them): (1) “the nature and quality of the services provided to the fund and [its]

shareholders”; (2) the profitability to the adviser of its relationship with the fund; (3) “fall-out”

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 26 of 48

-22-

benefits to the adviser, i.e., collateral benefits accruing to the adviser because of its relationship

with the fund; (4) whether economies of scale are achieved and appropriately shared with fund

investors; (5) comparative fee structures; and (6) the independence, expertise, and

conscientiousness of the disinterested members of the board in evaluating the advisory fee.

Jones, 130 S. Ct. at 1426 n.5, 1430 (citing Gartenberg, 694 F.2d at 929-32). A plaintiff cannot

establish liability based on a single factor. See, e.g., Gartenberg, 694 F.2d at 928 (district court

must assess fees in “light of all of the surrounding circumstances”); Benak, 2004 WL 1459249,

at *9 (“Plaintiff has not pointed to a single case where allegations of excessive fees were

sustained on the basis of only one of the six factors.”).

B. The Fees Paid by the SAM Funds Were Within the Arms’ Length Range

On the record in this case, Plaintiffs cannot demonstrate that the fees the SAM Funds

paid to PMC were “so disproportionately large that [they] bear[] no reasonable relationship to the

services rendered” such that they “could not have been the product of arm’s-length bargaining.”

Jones, 130 S. Ct. at 1429-30. Indeed, the objective facts make clear that, not only has PMC

delivered good performance for each of the SAM Funds, but it has received fees that compare

favorably with other peer funds that did not match the SAM Funds’ performance. See Section

II.D, supra. These incontrovertible facts obviate any need for the Court to consider expert

testimony on issues far less central to the Section 36(b) analysis. Nevertheless, a point-by-point

application of the Gartenberg factors to the record in this case demonstrates that these factors

weigh decisively in favor of Defendants and confirm that Plaintiffs cannot carry their burden to

prove a violation of Section 36(b).

1. PMC Provided High-Quality Services to the SAM Funds

A key consideration for any analysis of whether a mutual fund’s fees are disproportionate

to the services rendered is the nature and quality of the services rendered. In considering this

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 27 of 48

-23-

Gartenberg factor, courts look predominantly to the investment performance of the funds at issue

compared to peer funds. “Given investors’ primary objective of making money, the most

significant indication of the quality of an investment adviser’s services is the fund’s performance

relative to other funds of the same kind.” Kalish v. Franklin Advisers, Inc., 742 F. Supp. 1222,

1229 (S.D.N.Y. 1990), aff’d, 928 F.2d 590 (2d Cir. 1991).

For example, the district court in Gallus relied upon Lipper performance data in granting

summary judgment, notwithstanding the plaintiff’s proffer of testimony from Dr. Steve

Pomerantz (also retained by Plaintiffs in this case) who claimed that the performance of the

funds at issue there was “poor.” Gallus v. Ameriprise Fin., Inc., 497 F. Supp. 2d 974, 977, 980-

81 (D. Minn. 2007), rev’d on other grounds, 561 F.3d 816 (8th Cir. 2009), vacated, 130 S. Ct.

2340 (2010), reinstated on remand, 2010 WL 5137419 (D. Minn. Dec. 10, 2010), aff’d, 675 F.3d

1173 (8th Cir. 2012); see also In re Am. Mut. Funds Fee Litig. (“American Funds”), No. CV 04-

5593, 2009 WL 5215755, at *48-49 (C.D. Cal. Dec. 28, 2009) (noting the “good to excellent”

fund performance over five-year, ten-year, and “lifetime” periods, and holding that plaintiff had

“failed to offer any evidence undermining the conclusion that [the adviser’s] investment advisory

services were anything other than high quality”).

By any measure, the performance of the SAM Funds has been consistently strong

throughout the Relevant Time Period. During the Relevant Time Period, the SAM Balanced

Fund ranked in the 20th to 48th percentile for one-year performance, 25th to 38th percentile for

three-year performance, and in the 28th to 44th percentile for five-year performance. SUF ¶¶

121-124. Similarly, the SAM Strategic Growth Fund ranked in the 27th to 53rd percentile for

one-year performance throughout the Relevant Time Period, 28th to 47th percentile for three-

year performance, and in the 21st to 42nd percentile for five-year performance. Id. ¶¶ 125-128.

It is this performance that, in 2008 and 2011, led Morningstar to describe the SAM Balanced

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 28 of 48

-24-

Fund as “in the category’s top 10%” over the past decade and “a solid long-term performer.”

SUF ¶¶ 129-130. This impressive performance, together with all of the other services PMC

provides (see Section II.F, supra), demonstrates the high quality of the services that PMC

provides to the SAM Funds.

2. The Independent Directors Approved PMC’s Fees Following a Robust Review

The ICA requires that “approval by the board of directors . . . shall be given such

consideration by the court as is deemed appropriate under all the circumstances.” 15 U.S.C. §

80a-35(b)(2). In other words, courts are prohibited from engaging in “judicial second-guessing

of informed board decisions.” Jones, 130 S. Ct. at 1430. Rather, “[w]here a board’s process for

negotiating and reviewing investment-adviser compensation is robust, a reviewing court should

afford commensurate deference to the outcome of the bargaining process . . . . Thus, if the

disinterested directors considered the relevant factors, their decision to approve a particular fee

agreement is entitled to considerable weight, even if a court might weigh the factors differently.”

Id. at 1429-30 (reasoning that “Congress rejected a ‘reasonableness’ requirement that was

criticized as charging the courts with rate-setting responsibilities. . . . Congress’ approach

recognizes that courts are not well suited to make such precise calculations.”) (citations omitted).

Plaintiffs concede that, during the relevant period, the SAM Funds’ Independent

Directors were in fact independent and not “interested,” as that term is defined in the ICA. Am.

Compl. ¶¶ 96, 98: A45. Moreover, the Independent Directors were indisputably well-qualified,

experienced, successful professionals who carefully considered the appropriate factors in

exercising their business judgment to approve PMC’s fees. See SUF ¶¶ 59-88 (of the nine

Independent Directors, five were CPAs and one was a Certified Financial Planner; three had

advanced business or law degrees; all had served as senior executives; six had served as CEO,

COO, or CFO of a publicly-held company; eight have served directors of other companies; one

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 29 of 48

-25-

served as director of another mutual fund, and another served on the board of a mutual fund

advisor).

The SAM Funds’ Board engages in a robust 15(c) process that is consistent with industry

standards.

Members of the Audit Committee, Nominating and Governance Committees, and

Operations Committee met once per quarter, while the Executive Committee met as needed. Id.

¶ 48.

As part of the 15(c) process, the Independent Directors were guided by and received

detailed and thorough advice from their independent counsel, Vedder Price. SUF ¶ 89; see

Kalish, 742 F. Supp. at 1242 (“An important element of the independent director’s informed

state is the advice they received from their independent counsel”).

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 30 of 48

-26-

The materials considered by the Board in this case were no less robust than those deemed

sufficient in other Section 36(b) cases. For example, in Kalish, the board received “financial

statements of [adviser] entities, performance comparisons with other funds, and statements of

fund expenses and expense ratios.” 742 F. Supp. at 1243. Likewise, in Krinsk v. Fund Asset

Management, Inc., 715 F. Supp. 472 (S.D.N.Y. 1988), aff’d, 875 F.2d 404 (2d Cir. 1989), the

board received information on “the Fund’s performance and expense ratios, its portfolio structure

and trading activities, the 12b-1 plan, including its impact on expense ratio, total income and

yield, as well as comparative information on other funds” and “presentations on such topics as

Fund portfolio management, financial consultant reactions to the 12b-1 plan, and profitability

studies.” 715 F. Supp. at 502. Similar documents and information were included in the 15(c)

materials provided to the SAM Funds’ Board. See Section II.E supra.

After a review of all of the material obtained from PMC bearing upon the Gartenberg

factors and other considerations the Board deemed to be relevant, including comparative

information prepared by Morningstar and Lipper, and following a number of discussions during

annual meetings , the SAM

Funds’ Board approved the Advisory Agreements. SUF ¶¶ 159-168. Accordingly, the well-

informed Board’s business judgment should not be second-guessed. See Jones, 130 S. Ct. at

1429-30; Gallus, 675 F.3d at 1180.

3. The Fees Charged to the SAM Funds Compare Favorably to Other Fee Structures

A comparison of the fees incurred by the SAM Funds to other relevant fee structures also

weighs against Plaintiffs’ claims. Indeed, the fees paid by the SAM Funds are well within the

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 31 of 48

-27-

range that might result from arm’s-length negotiations, which “extend[s] from a low-end figure

below what the institutional clients were paying and a high-end figure beyond the fees that other

mutual fund clients paid.” Jones v. Harris Assocs. L.P., No. 04 C 8305, 2007 WL 627640, at *8

(N.D. Ill. Feb. 27, 2007), aff’d on other grounds, 527 F.3d 627 (7th Cir. 2007), vacated and

remanded, 130 S. Ct. 1418 (2010). The performance realized by the SAM Funds also should be

taken into account in considering the fees paid because “[s]uperior performance operates to

justify a relatively high fee, which in turn increases profitability.” Kalish, 742 F. Supp. at 1250.

a. Comparisons to Peer Mutual Funds

Courts in Section 36(b) cases have considered “a comparison of the fees with those paid

by similar funds,” Jones, 130 S. Ct. at 1426 n.5, and rule consistently in favor of defendants

where advisory fees are “within the range of fees and expenses for similar funds.” Strougo v.

BEA Assocs., 188 F. Supp. 2d 373, 384 (S.D.N.Y. 2002) (granting summary judgment to

defendant); see also Gallus, 497 F. Supp. 2d at 982-83 (same); Kalish, 742 F. Supp. at 1230

(finding for defendant following bench trial); Krinsk, 715 F. Supp. at 503 (same); American

Funds, 2009 WL 5215755, at *53 (same). As explained, the incontrovertible evidence

demonstrates that the fees the SAM Funds paid to PMC during the Relevant Time Period were

well within the range paid by their peers. See Section II.D.1 supra.

In their Complaint and during discovery, however, Plaintiffs focused only on the

management fee component of the total expense ratio paid by the SAM Funds. Plaintiffs allege

that SAM Fund shareholders pay four “layers” of fees – to the adviser of the SAM Fund (PMC),

the subadvisor of the SAM Fund (Edge), the advisers of the underlying funds, and the

subadvisors of the underlying funds – and that the multi-layered nature of the fees alone show

that PMC’s fees are excessive. Am. Compl. ¶¶ 40-44: A16-19. This argument, which could be

made about any fund of funds that invests in affiliated mutual funds, absurdly suggests that a

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 32 of 48

-28-

structure specifically authorized by the ICA is nonetheless illegal. See, e.g., 15 U.S.C. § 80a-12;

Dkt. 38 at 2 n.2.

Moreover, the manner in which Plaintiffs focus on fees is misguided. The total expense

ratio is the only appropriate comparative measure of the fees paid by an investor because, among

other things, there is no industry-wide definition of the “management fee” component or other

standard that dictates what services should be reflected in any particular component of the total

expense ratio. See U.S. Securities and Exchange Commission, “Division of Investment

Management: Report on Mutual Fund Fees and Expenses,” December 2000, at 16 and n.60:

A1740-A1801;10 see Hecker, 556 F.3d at 586 (“The total fee . . . is the critical figure for

someone interested in the cost of including a certain investment in her portfolio and the net value

of that investment”); accord Braden, 588 F.3d at 595-96, n.5 & 6 (applying same in ERISA

context); Benak, 2004 WL 1459249, at *9 (the ICA’s legislative history directs that “court look

at . . . all compensation and payments received”) (citation omitted).11

10 The SEC has explained that “no standard method exists for classifying the services provided in connection with buying and owning a mutual fund.” Id. at 16: A1755. In addition:

Some funds define the term management fee narrowly, to cover only the cost of selecting portfolio securities. These funds pay for administration, record keeping, and other services under separate contracts with other service providers. Other funds define the management fee broadly, to cover a variety of administrative and other services, in addition to expenses associated with selecting portfolio securities. A few funds have ‘unified’ fees under which the management fee pays for all fund expenses ... Thus, if Fund A has a higher management fee than Fund B, it may mean that Fund A pays a higher fee to its adviser. Alternatively, it may mean that Fund A’s management fee pays for services that are provided and charged for separately by Fund B’s adviser, an affiliate of the adviser, or outside contractors.

Id. n.60: A1788. 11 Plaintiffs may argue that this Court may not look at the expense ratio, based on the district court’s statement in American Funds, 2009 WL 5215755, at *44, that “Section 36(b) does not require Plaintiffs to establish that the fees charged by Defendants were excessive in the aggregate.” But that conclusion cannot be squared with the plain language of Section 36(b), which creates a fiduciary duty with respect to an investment manager’s “compensation,” and not

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 33 of 48

-29-

Here, while the management fees paid by the SAM Balanced and SAM Strategic Growth

Funds for Share Class A in 2011 rank in the 96th and 86th percentile, respectively, the non-

management fees paid by the SAM Funds during the same period rank in the 17th and 21st

percentiles, respectively. SUF ¶¶ 105-108. But, using these components to compute the 2011

total expense ratio resulted in the SAM Balanced Fund ranking in the 38th percentile for fees in

Lipper’s Mixed Asset Target Allocation Growth Funds Category, and the SAM Strategic Growth

Fund ranking in the 50th percentile of the Lipper combined Multi-Cap Growth and Multi-Cap

Core categories. Id. ¶¶ 96-97; see also id. ¶¶ 96-97, 105-108 (reflecting the SAM Funds’

expense ratio, management fee, and non-management expense rankings in 2008-2010).

Accordingly, these total expense ratios, which, along with the aforementioned fee components,

were considered by the SAM Funds’ Board and disclosed to investors, are well within the range

of similar funds. See Section II.D supra.

Plaintiffs argue that the fees charged to the SAM Funds are “excessive” because they

consist of “four layers of fees.” Am. Compl. ¶¶ 40-44: A16-19. Not only is this argument

factually incorrect, but it ignores the important benefits that PMC and the SAM Fund portfolio

managers provide to the SAM Fund shareholders. As an initial matter, the SAM Funds pay a

single management fee to PMC, and PMC then transfers a portion of that fee to Edge; likewise,

the underlying funds pay a fee to PMC, and PMC then transfers a portion of that fee to the

subadvisors of those underlying funds. SUF ¶¶ 112-113. In other words, the subadvisor fees are

just the components of the compensation. See, e.g., Benak, 2004 WL 1459249, at *9 (noting that ICA’s legislative history directs that “court look at . . . all compensation and payments received”) (citation omitted). This makes sense because, as a number of courts of appeal have recognized, there is no industry-wide standard describing what services are covered by the management fee, as opposed to some other component of the expense ratio, and thus the only way to accurately compare the fees of different mutual funds is by looking at the expense ratio. Indeed, plaintiffs themselves have argued to this Court that the fees are excessive because of the so-called “four layers” of fees (Am. Compl. ¶¶ 40-44), and that argument is predicated on the notion that total compensation is the appropriate measure.

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 34 of 48

-30-

not in addition to the management fees. Id. In any event, as explained, the only appropriate

consideration is the SAM Funds’ expense ratios, which were well within the range of peer funds

during the Relevant Time Period. See Section II.E, supra.

Moreover, as a fund of funds, each SAM Fund provides its investors with a diversified

portfolio in a single mutual fund. SUF ¶ 8. The SAM Funds’ portfolio managers select the

underlying funds carefully pursuant to a designed investment strategy.

In short,

the SAM Funds’ portfolio managers provided valuable portfolio management services over and

above the services provided by the manager of the underlying funds. Likewise, PMC similarly

provided very valuable services to the SAM Funds, including through the Principal Due

Diligence Program, which vetted, selected, and monitored the menu of funds available for

investment by the SAM Funds. SUF ¶ 177. Under this Program, PMC also conducted

comprehensive research and analysis to identify, retain, monitor and evaluate subadvisors for the

SAM Funds. Id. ¶ 177-178. Thus, the Principal Due Diligence Program was designed to enable

the SAM Funds to meet their investment goals. Id. In short, PMC and the SAM Funds’

portfolio managers provided valuable services over and above the services provided by the

manager of the underlying funds.

b. Comparisons to Other Principal Funds

During discovery, Plaintiffs suggested that the fees charged to the SAM Funds were

excessive by comparing them to fees charged by two other Principal mutual funds: the Principal

LifeTime Funds and the PVC SAM Funds. The Supreme Court has instructed, however, that

Section 36(b) does not require mutual fund advisers to charge all clients the same fee, or to make

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 35 of 48

-31-

the same profit from each account: “[e]ven if the services provided and fees charged to an

independent fund are relevant, courts should be mindful that the Act does not necessarily ensure

fee parity between mutual funds and institutional clients contrary to petitioners’ contentions.”

Jones, 130 S. Ct. at 1429. Rather, courts may accord such comparisons “the weight that they

merit in light of the similarities and differences between the services that the clients in question

require, but courts must be wary of inapt comparisons.” Id. at 1428. In cases where “the

services rendered are sufficiently different that a comparison is not probative,” the “courts must

reject such a comparison.” Id. Applying this standard, and for the reasons that follow, the Court

should reject any attempt Plaintiffs make to compare the management fees charged to SAM

Funds with the fees charged to investors in the Principal LifeTime Funds or the PVC SAM

Funds.

(i) Comparisons to the Principal LifeTime Funds

The services provided to the SAM Funds and Principal LifeTime Funds are not alike, and

any fee comparison Plaintiffs present will be irrelevant and entitled to no weight under Jones.

While the SAM Funds and LifeTime Funds are both asset allocation funds, that is where the

similarity ends. The LifeTime Funds employ a completely different investment strategy than the

SAM Funds.

The LifeTime Funds are a series of “target date” funds whose assets are invested in

accordance with a pre-determined asset allocation that is changed on a set schedule as the date of

an investor’s expected retirement approaches. Id. ¶ 200. For example, the LifeTime 2050 Fund

is intended for investors who plan to retire in 2050. That fund starts with an asset allocation

heavily weighted toward equities, and as 2050 approaches, the asset mix is changed so that it is

more heavily weighted toward fixed income investments (like bonds), so that principal is

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 36 of 48

-32-

preserved in retirement. Id. ¶ 201. These pre-determined asset allocations are known as a “glide

path.” Id. ¶ 202. The managers of the LifeTime Funds rebalance quarterly to keep the asset

allocation at its pre-determined figures. Id. ¶ 203.

By comparison, the SAM Funds are “target risk” funds that are intended to provide

investors with a specific amount of risk at all times. The SAM Balanced Fund is intended to

provide a moderate level of risk, with a “balance” of stocks and bonds, and SAM Strategic

Growth is intended to be an aggressively invested portfolio for investors with a greater risk

tolerance. SUF ¶¶ 3, 6-7.

As this comparison demonstrates, the SAM Funds follow a more actively managed

approach. The portfolio managers for the LifeTime Funds rebalance the funds quarterly to keep

them at their predetermined asset allocation targets. SUF ¶ 203. This quarterly process is not as

active as the daily process used for the SAM Funds. Id. ¶ 203.

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 37 of 48

-33-

It should therefore come as no surprise that the more

actively managed SAM Funds are more expensive than the LifeTime Funds.

This conclusion is reinforced by examining industry sources. If SAM and LifeTime were

truly comparable, one would expect that Lipper and Morningstar would consider them peer

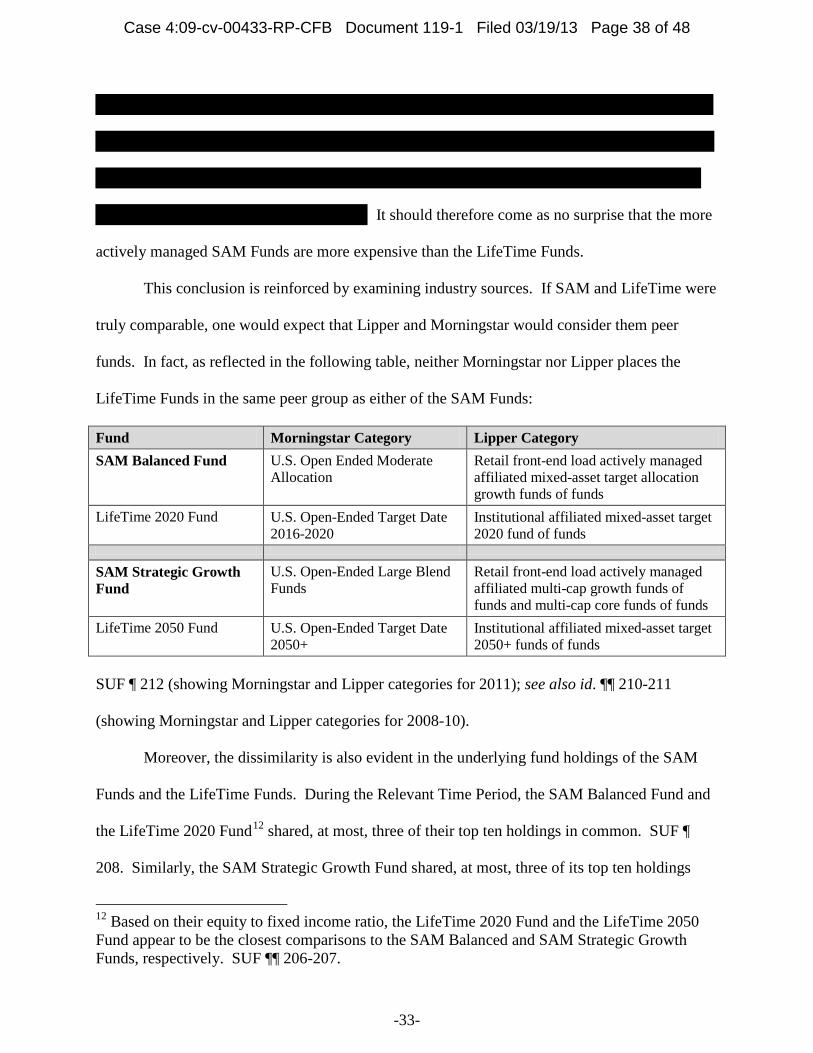

funds. In fact, as reflected in the following table, neither Morningstar nor Lipper places the

LifeTime Funds in the same peer group as either of the SAM Funds:

Fund Morningstar Category Lipper Category SAM Balanced Fund U.S. Open Ended Moderate

Allocation Retail front-end load actively managed affiliated mixed-asset target allocation growth funds of funds

LifeTime 2020 Fund U.S. Open-Ended Target Date 2016-2020

Institutional affiliated mixed-asset target 2020 fund of funds

SAM Strategic Growth Fund

U.S. Open-Ended Large Blend Funds

Retail front-end load actively managed affiliated multi-cap growth funds of funds and multi-cap core funds of funds

LifeTime 2050 Fund U.S. Open-Ended Target Date 2050+

Institutional affiliated mixed-asset target 2050+ funds of funds

SUF ¶ 212 (showing Morningstar and Lipper categories for 2011); see also id. ¶¶ 210-211

(showing Morningstar and Lipper categories for 2008-10).

Moreover, the dissimilarity is also evident in the underlying fund holdings of the SAM

Funds and the LifeTime Funds. During the Relevant Time Period, the SAM Balanced Fund and

the LifeTime 2020 Fund12 shared, at most, three of their top ten holdings in common. SUF ¶

208. Similarly, the SAM Strategic Growth Fund shared, at most, three of its top ten holdings

12 Based on their equity to fixed income ratio, the LifeTime 2020 Fund and the LifeTime 2050 Fund appear to be the closest comparisons to the SAM Balanced and SAM Strategic Growth Funds, respectively. SUF ¶¶ 206-207.

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 38 of 48

-34-

with the LifeTime 2050 Fund. Id. ¶ 209. These comparisons further demonstrate that the SAM

Funds and the LifeTime Funds employ completely different investment strategies.

Given these stark differences between the SAM Funds and the LifeTime Funds,

particularly with respect to the far more active management of the SAM Funds’ holdings, it is

not surprising that the management fees charged to the SAM Funds are higher than those

charged to the LifeTime Funds. Accordingly, any comparison that Plaintiffs attempt to press

would be erroneous.

(ii) Comparison to the PVC SAM Funds

Plaintiffs may also attempt to argue that the fees paid by the SAM Funds are excessive by

comparing them to the PVC SAM Funds. Once again, however, any such comparison would be

inappropriate.

The Principal Variable Contracts (“PVC”) Funds are mutual funds organized by Principal

Life Insurance Company (“Principal Life”). SUF ¶ 213. The PVC Funds include the PVC SAM

Balanced Fund and the PVC SAM Strategic Growth Fund, which are asset allocation mutual

funds whose asset allocation strategy shares some similarities with the SAM Funds. Id. ¶ 213.

But because the SAM Funds and PVC SAM Funds are different products that serve completely

different markets, any comparison of the fees charged by these funds has little value.

As an initial matter, PMC provides services to the PFI SAM Funds that it does not

provide to the PVC SAM Funds. For example, the SAM Funds have ten share classes, while the

PVC SAM Funds have only two share classes. Id. ¶ 216.

Moreover, unlike the SAM Funds, the PVC Funds are not

available to the general public directly. Rather, they can be purchased only through certain

variable life insurance policies or variable annuity contracts issued by life insurance companies.

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 39 of 48

-35-

SUF ¶ 214. Because of these differences, Lipper places the PVC SAM Funds in different peer

groups than the PFI SAM Funds. Id. ¶ 215.

Notwithstanding these differences, PMC charges fees to the PFI SAM Funds that are only

slightly higher than those charged to the PVC SAM Funds, particularly when accounting for

breakpoints. During the Relevant Time Period, the effective management fee for the PFI SAM

Funds was only seven to eleven basis points higher than the effective management fee for the

PVC SAM Funds. Id. ¶ 218. This minimal difference can hardly be said to result in fees for PFI

SAM that are “so disproportionately large that [they] bear[] no reasonable relationship to the

services rendered and could not have been the product of arm’s length bargaining.” Jones, 130

S. Ct. at 1426. Moreover, Plaintiffs cannot make the requisite “showing of relevance” with

respect to this slight differential, given that such “a showing of relevance requires courts to

assess any disparity in fees in light of the different markets for advisory services.” Id. at 1429

n.8. Here, the PFI SAM Funds and the PVC SAM Funds are different products that are

distributed through different channels to different customer segments. SUF ¶ 219.

c. Comparison to Fees Paid to Edge as Sub-Adviser

Plaintiffs also allege that the fees paid to PMC are excessive because Edge, a sub-adviser,

provides the portfolio management services to the SAM Funds. Am. Compl. ¶¶ 47-48: A25-28.

PMC transfers to Edge a fee of 4.16 basis points for its services (compared with PMC’s 2011

effective management fee of 34.2 basis points), and Plaintiffs have argued that this demonstrates

that PMC’s higher management fee is necessarily excessive. This argument is wrong.

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 40 of 48

-36-

As explained, investors are concerned primarily with overall performance and the total

expense ratio, and both the performance of the SAM Funds and the fees paid to PMC (which

include the portion paid to Edge) compare very favorably to their respective peer groups. See

Section II.D, supra. In any event, Plaintiffs’ comparison to Edge’s subadvisory fees ignores the

significant services that PMC provides under the management agreement. Those services

include the Due Diligence Program as well as substantial accounting, regulatory, compliance,

transfer agency, and retirement plan services. See Section II.E, supra. Further, Edge is a

wholly-owned subsidiary of PMC,

SUF ¶¶ 110, 221.

a non-Principal entity that sponsors a fund known as the Anchor

Series Trust, for which Edge is paid 20 to 40 basis points, an amount that is significantly higher

than the 4.16 basis points it receives for the SAM Funds. SUF ¶¶ 222-223.

4. PMC Adequately Shared Economies of Scale with the SAM Funds’ Shareholders

Plaintiffs contend that PMC achieved economies of scale – or lower per-transaction costs

as the SAM Funds’ assets increased – and that PMC did not adequately share any such

efficiencies with the SAM Funds’ shareholders. Again, Plaintiffs are wrong.

Indeed, Plaintiffs cannot prove “that the per unit cost of [SAM] Fund transactions . . .

decreases as the number of units increases.” Krinsk, 715 F. Supp. at 496 (granting summary

judgment in Section 36(b) case); accord American Funds, 2009 WL 5215755, at *51.

“Economies of scale do not exist in a vacuum. The concept is meaningful only if increased size

of a fund (more shareholders, more assets under management) directly reduces the manager’s

costs of processing each transaction and servicing each shareholder.” Kalish, 742 F. Supp. at

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 41 of 48

-37-

1239. It is insufficient to argue simply that the ratio of cost to assets decreased as assets

increased; rather, “Plaintiffs must ‘create a detailed analysis of each element of a transaction

surrounding [the Fund], over an extended period of time, over different levels of activity.’”

American Funds, 2009 WL 5215755, at *51 (quoting Krinsk, 715 F. Supp. at 496). Plaintiffs

have not even attempted to perform any such analysis with respect to the SAM Funds, and their

economies of scale allegations otherwise fails.

Moreover, it cannot be disputed that PMC shared with SAM Fund shareholders the

economies of scale that may have existed through the use of breakpoints. Breakpoints – or

automatic decreases in the management fee component of the total expense ratio when AUM

surpasses certain thresholds – are commonly cited by courts as a way for mutual fund

shareholders to participate in any cost savings achieved as a result of economies of scale. See,

e.g., Schuyt v. Rowe Price Prime Reserve Fund Inc., 663 F. Supp. 962, 979-80 (S.D.N.Y. 1987),

aff’d per curiam, 835 F.2d 45 (2d Cir. 1987). During the Relevant Time Period, the SAM Funds

benefited from seven breakpoints that were calculated using the Aggregate SAM Fund Assets (or

the total AUM of all five PFI SAM Funds), not just the assets of the two individual SAM Funds

at issue in this case, thereby enhancing the benefits to SAM Fund shareholders. SUF ¶ 99. The

SAM Funds’ management fee starts at 55 basis points on the first $500 million in Aggregate

SAM Fund Assets, but steadily declines as Aggregate SAM Fund Assets increases, and declines

to 25 basis points for Aggregate SAM Fund Assets greater than $5 billion. Id. ¶ 100. The SAM

Case 4:09-cv-00433-RP-CFB Document 119-1 Filed 03/19/13 Page 42 of 48

-38-

Funds’ breakpoints resulted in an effective management fee of 34 basis points in 2011, nearly 40

percent lower than the management fee at the first asset level. Id. ¶¶ 105-106.

Plaintiffs will not be able to provide any credible evidence that PMC’s sharing of

economies of scale was different from what might have resulted from arm’s-length negotiation,

as they are required to do. See, e.g., Jones, 2007 WL 627640, at *9 (granting summary judgment

where “Plaintiffs do not provide any evidence of what savings were gained from economies of

scale”). Accordingly, this factor also supports summary judgment in Defendants’ favor.

5. PMC’s Profitability Fell Within A Range Courts Have Uniformly Regarded As Acceptable.

During the Relevant Time Period, PMC’s profitability fell well within the range found to

be acceptable in other cases. Specifically, other courts have found pretax profit margins – or a