Embed Size (px)

Citation preview

Unit 1: Planning and financing a business

Financial planning

Calculating costs, revenues and profits

Chapter 11

Unit 1: Planning and financing a business

Financial planning

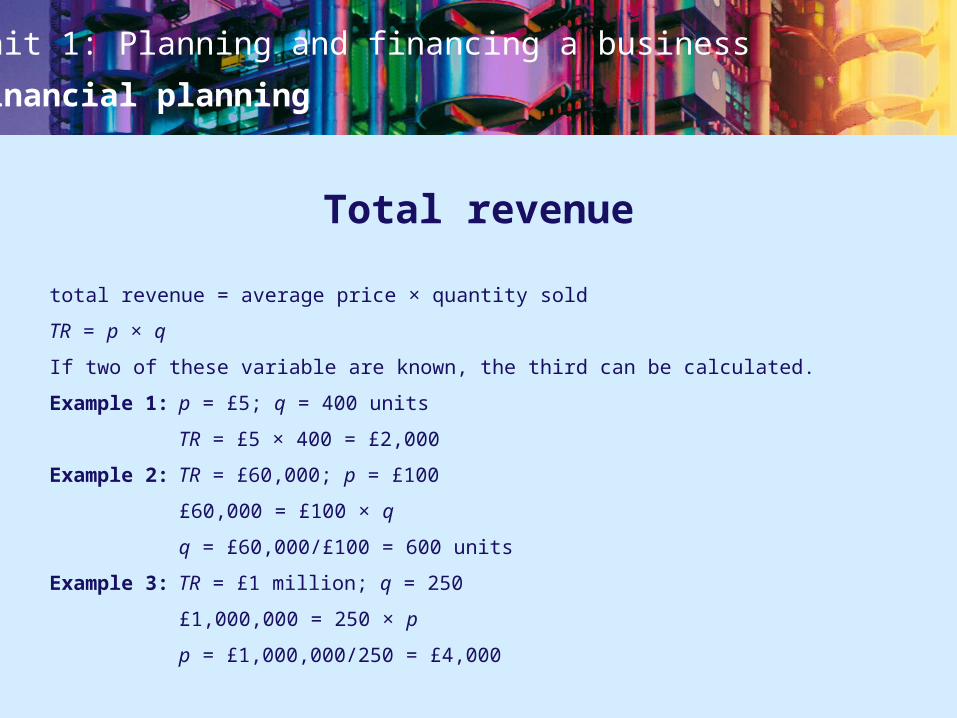

Total revenue

total revenue = average price × quantity sold

TR = p × q

If two of these variable are known, the third can be calculated.

Example 1: p = £5; q = 400 units

TR = £5 × 400 = £2,000

Example 2: TR = £60,000; p = £100

£60,000 = £100 × q

q = £60,000/£100 = 600 units

Example 3: TR = £1 million; q = 250

£1,000,000 = 250 × p

p = £1,000,000/250 = £4,000

Unit 1: Planning and financing a business

Financial planning

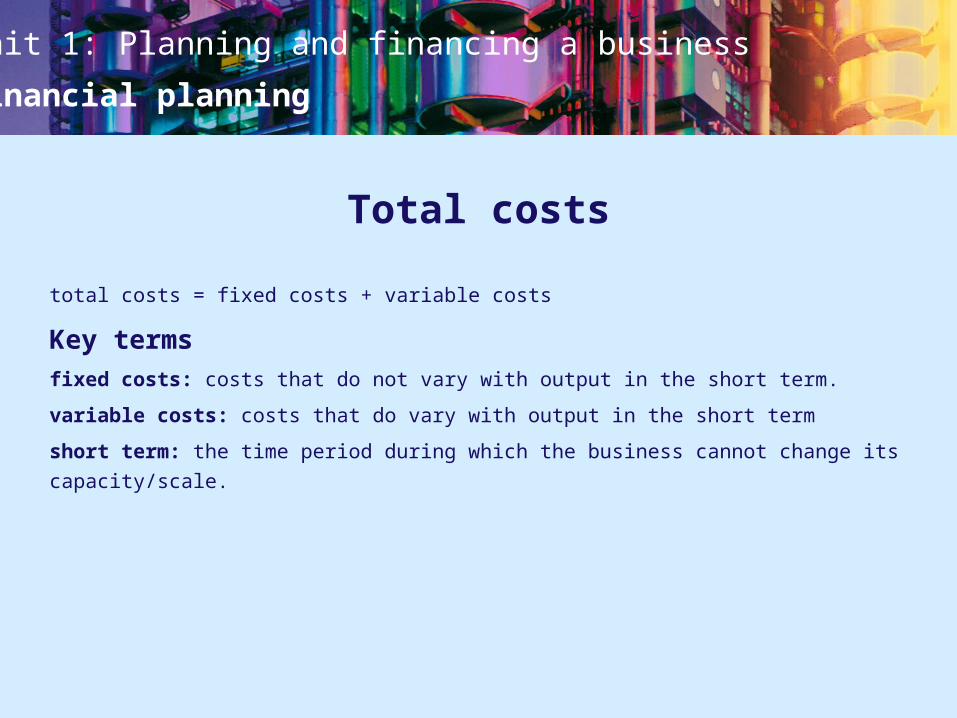

Total costs

total costs = fixed costs + variable costs

Key termsfixed costs: costs that do not vary with output in the short term.

variable costs: costs that do vary with output in the short term

short term: the time period during which the business cannot change its

capacity/scale.

Unit 1: Planning and financing a business

Financial planning

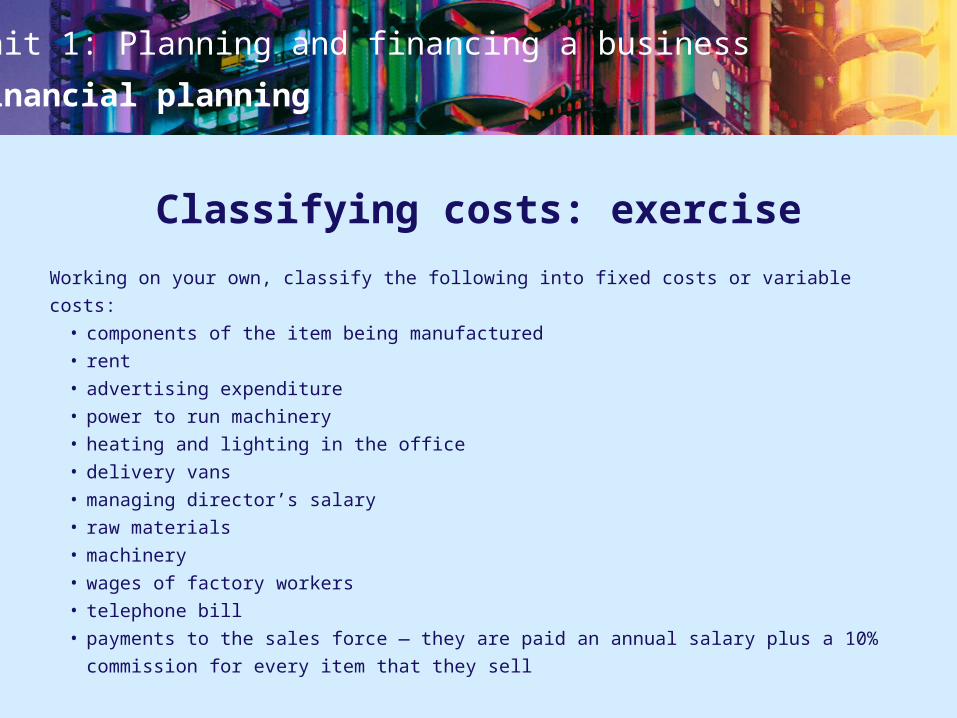

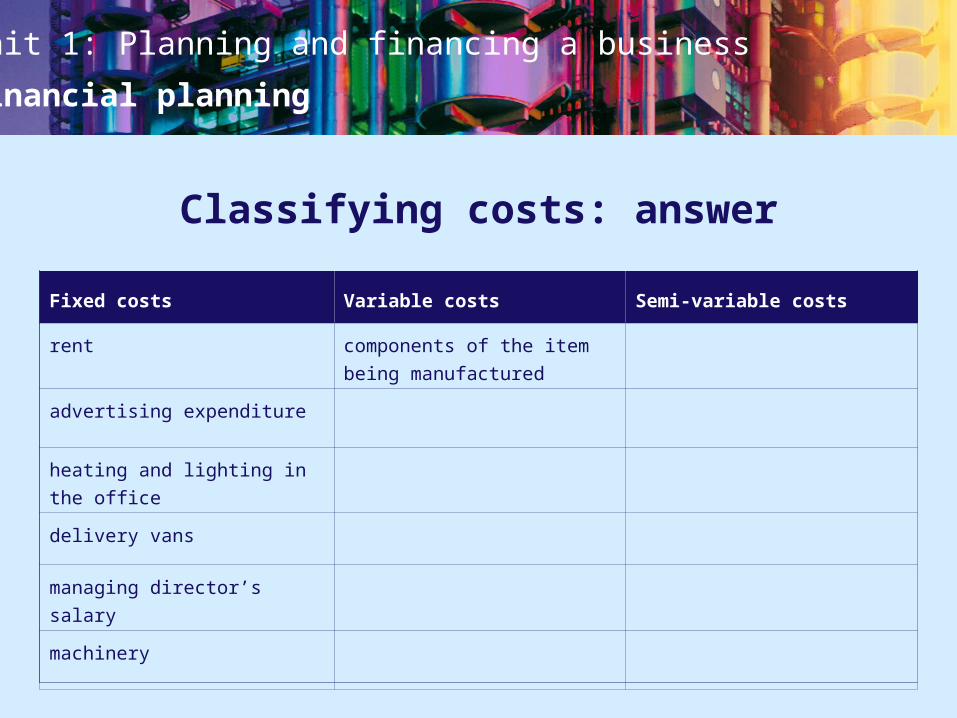

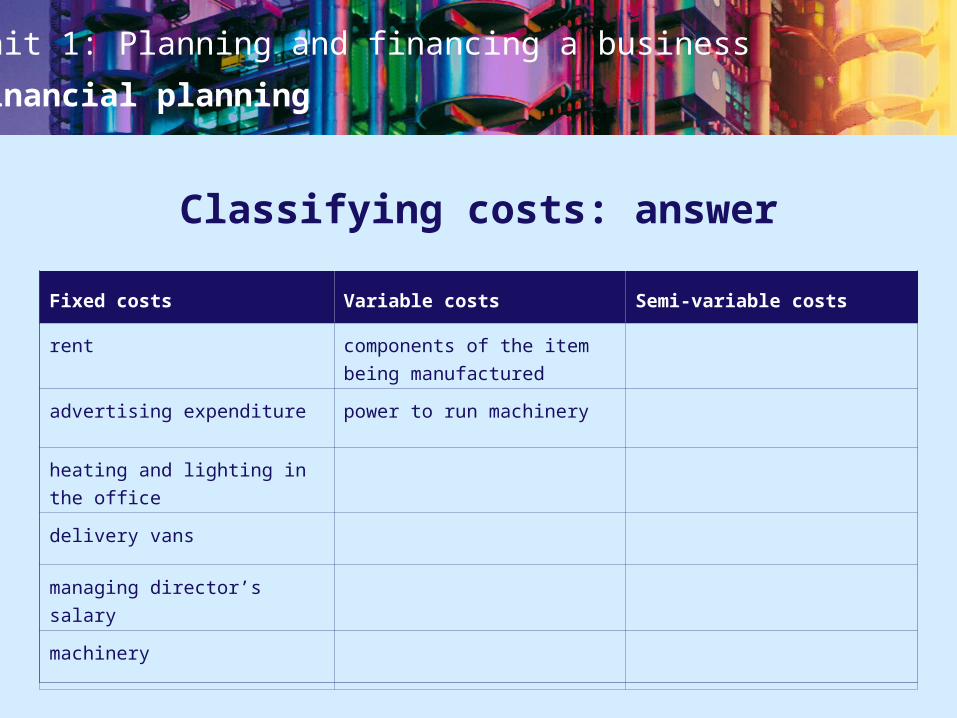

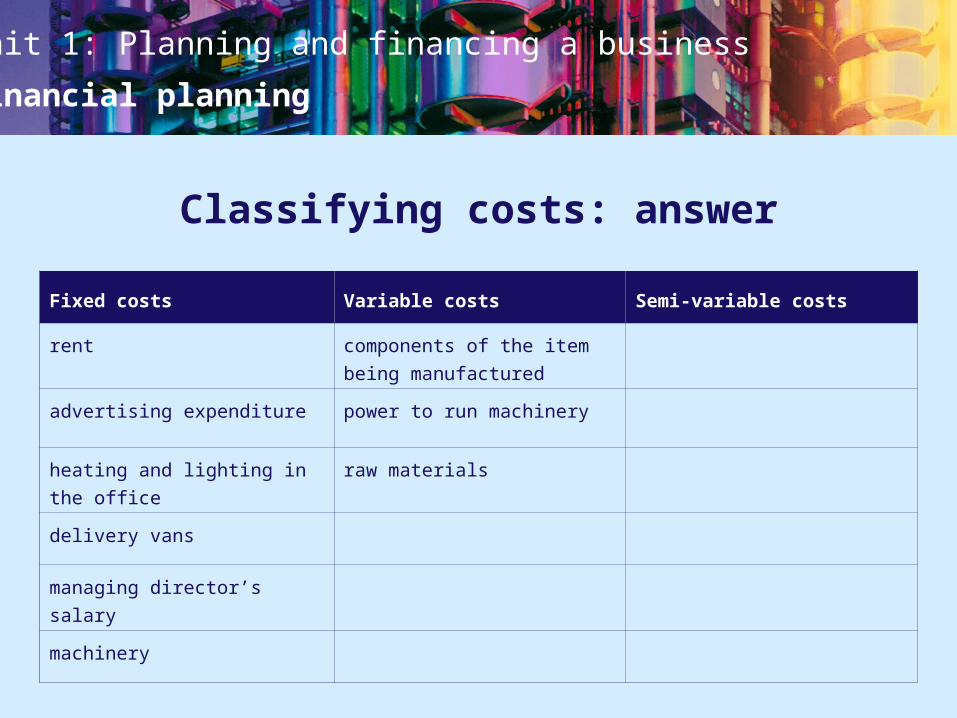

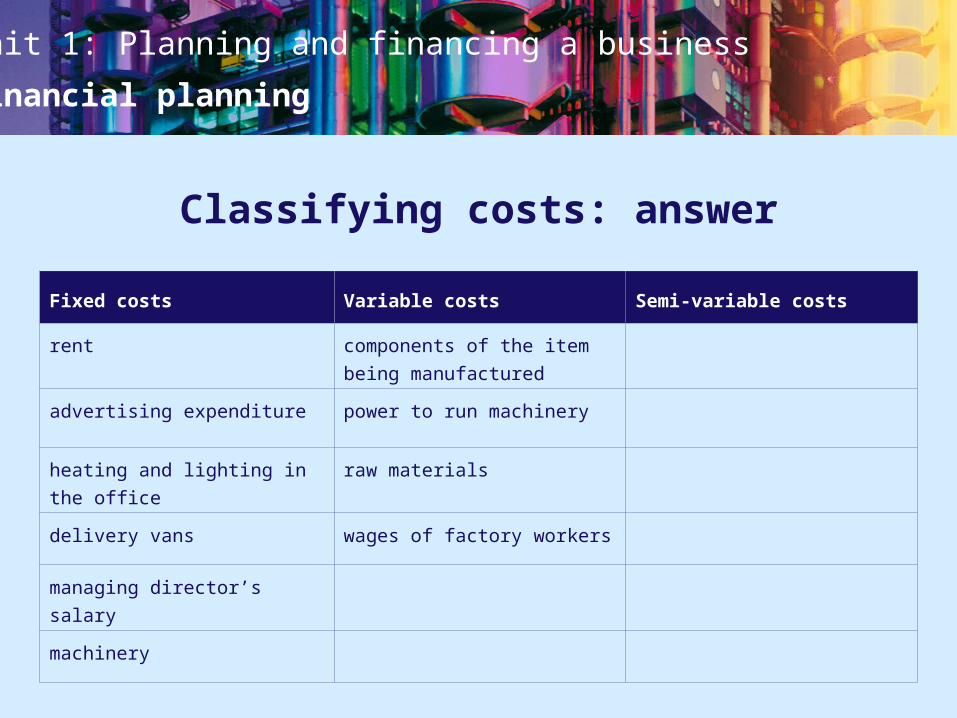

Classifying costs: exercise

Working on your own, classify the following into fixed costs or variable costs:• components of the item being manufactured• rent• advertising expenditure• power to run machinery• heating and lighting in the office• delivery vans• managing director’s salary• raw materials• machinery• wages of factory workers• telephone bill• payments to the sales force — they are paid an annual salary plus a 10%

commission for every item that they sell

Unit 1: Planning and financing a business

Financial planning

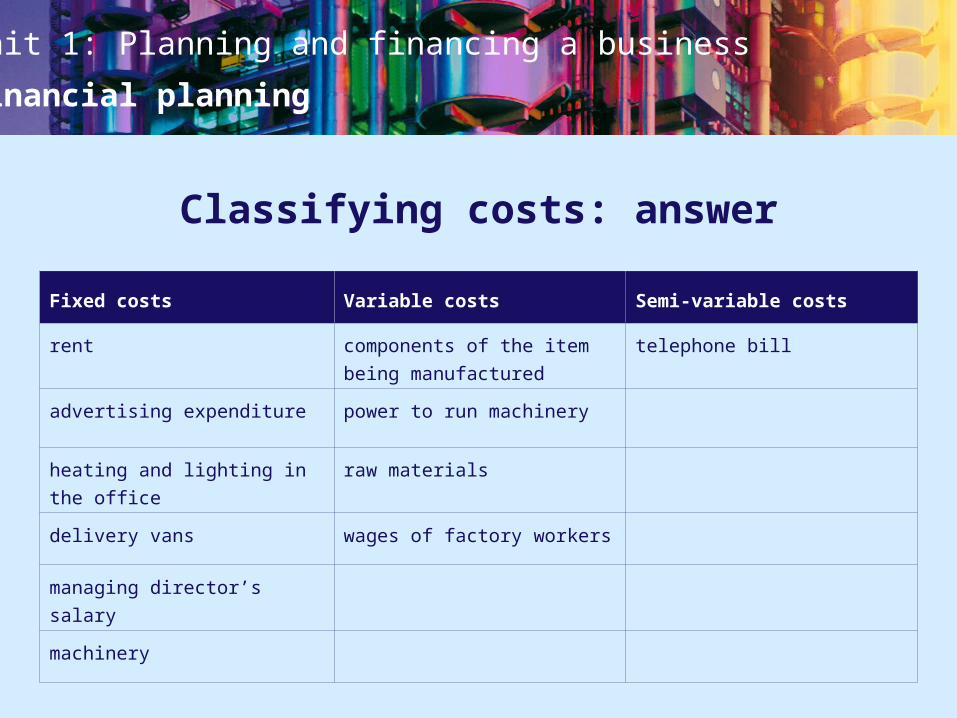

Classifying costs: answer

Fixed costs Variable costs Semi-variable costs

rent

advertising expenditure

heating and lighting in the

office

delivery vans

managing director’s salary

machinery

Unit 1: Planning and financing a business

Financial planning

Classifying costs: answer

Fixed costs Variable costs Semi-variable costs

rent components of the item

being manufactured

telephone bill

advertising expenditure power to run machinery payments to the sales force

heating and lighting in the

office

raw materials

delivery vans wages of factory workers

managing director’s salary

machinery

Fixed costs Variable costs Semi-variable costs

rent components of the item

being manufactured

advertising expenditure power to run machinery

heating and lighting in the

office

raw materials

delivery vans wages of factory workers

managing director’s salary

machinery

Fixed costs Variable costs Semi-variable costs

rent components of the item

being manufactured

advertising expenditure power to run machinery

heating and lighting in the

office

raw materials

delivery vans

managing director’s salary

machinery

Fixed costs Variable costs Semi-variable costs

rent components of the item

being manufactured

advertising expenditure power to run machinery

heating and lighting in the

office

delivery vans

managing director’s salary

machinery

Fixed costs Variable costs Semi-variable costs

rent components of the item

being manufactured

advertising expenditure

heating and lighting in the

office

delivery vans

managing director’s salary

machinery

Unit 1: Planning and financing a business

Financial planning

Classifying costs: answer

Fixed costs Variable costs Semi-variable costs

rent components of the item

being manufactured

telephone bill

advertising expenditure power to run machinery payments to the sales force

heating and lighting in the

office

raw materials

delivery vans wages of factory workers

managing director’s salary

machinery

Fixed costs Variable costs Semi-variable costs

rent components of the item

being manufactured

advertising expenditure power to run machinery

heating and lighting in the

office

raw materials

delivery vans wages of factory workers

managing director’s salary

machinery

Fixed costs Variable costs Semi-variable costs

rent components of the item

being manufactured

advertising expenditure power to run machinery

heating and lighting in the

office

raw materials

delivery vans

managing director’s salary

machinery

Fixed costs Variable costs Semi-variable costs

rent components of the item

being manufactured

advertising expenditure power to run machinery

heating and lighting in the

office

delivery vans

managing director’s salary

machinery

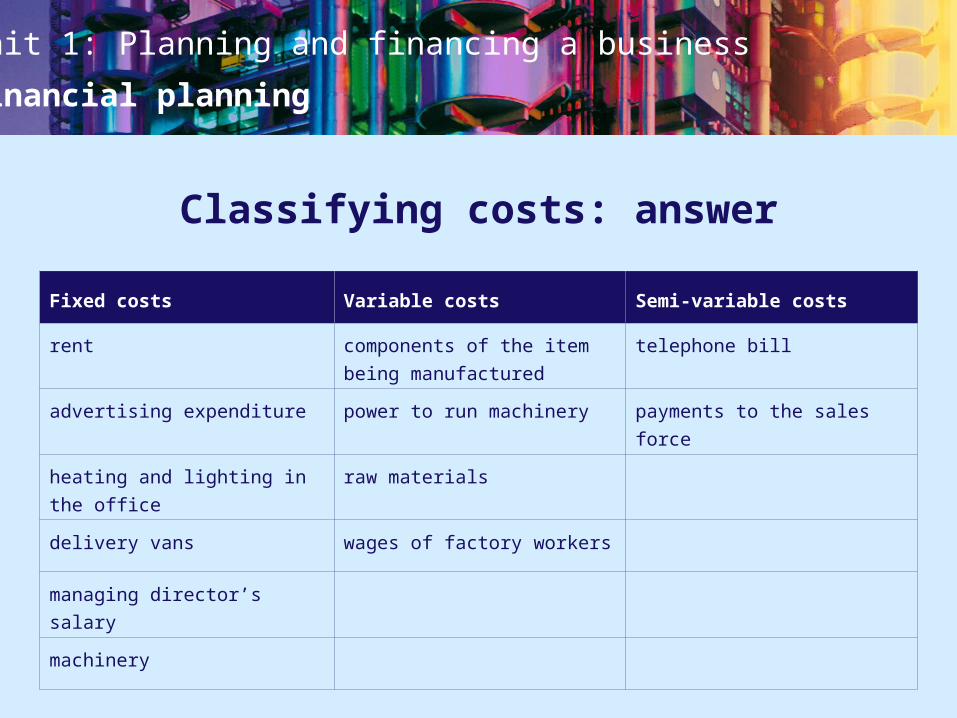

Unit 1: Planning and financing a business

Financial planning

Classifying costs: answer

Fixed costs Variable costs Semi-variable costs

rent components of the item

being manufactured

advertising expenditure power to run machinery

heating and lighting in the

office

raw materials

delivery vans wages of factory workers

managing director’s salary

machinery

Fixed costs Variable costs Semi-variable costs

rent components of the item

being manufactured

advertising expenditure power to run machinery

heating and lighting in the

office

raw materials

delivery vans

managing director’s salary

machinery

Unit 1: Planning and financing a business

Financial planning

Classifying costs: answer

Fixed costs Variable costs Semi-variable costs

rent components of the item

being manufactured

advertising expenditure power to run machinery

heating and lighting in the

office

raw materials

delivery vans wages of factory workers

managing director’s salary

machinery

Unit 1: Planning and financing a business

Financial planning

Classifying costs: answer

Fixed costs Variable costs Semi-variable costs

rent components of the item

being manufactured

telephone bill

advertising expenditure power to run machinery

heating and lighting in the

office

raw materials

delivery vans wages of factory workers

managing director’s salary

machinery

Unit 1: Planning and financing a business

Financial planning

Classifying costs: answer

Fixed costs Variable costs Semi-variable costs

rent components of the item

being manufactured

telephone bill

advertising expenditure power to run machinery payments to the sales force

heating and lighting in the

office

raw materials

delivery vans wages of factory workers

managing director’s salary

machinery

Unit 1: Planning and financing a business

Financial planning

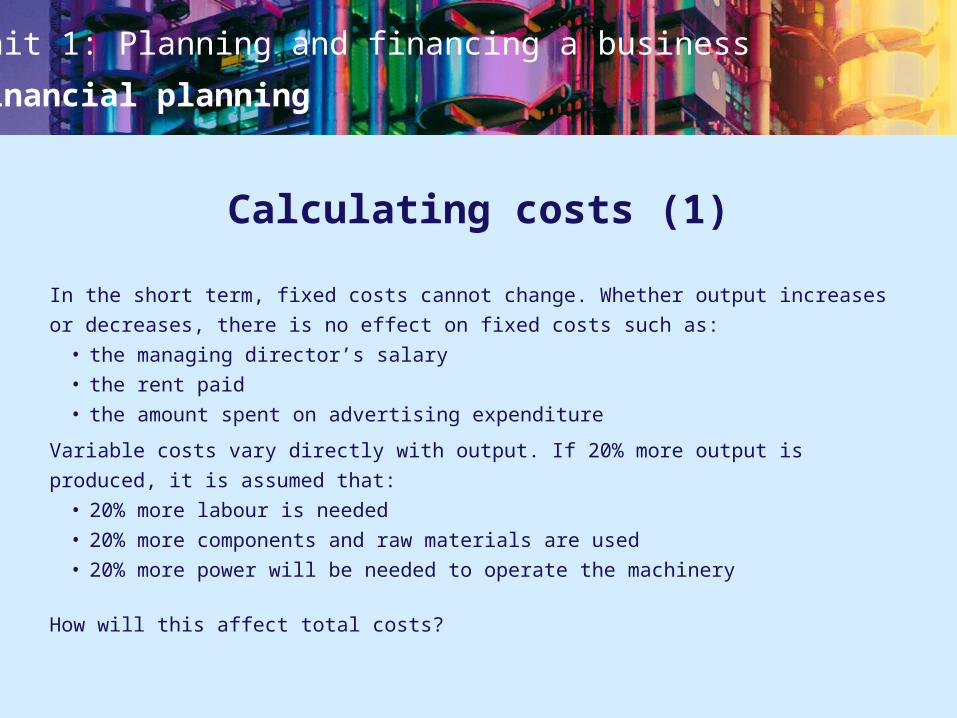

Calculating costs (1)

In the short term, fixed costs cannot change. Whether output increases or decreases,

there is no effect on fixed costs such as:• the managing director’s salary• the rent paid• the amount spent on advertising expenditure

Variable costs vary directly with output. If 20% more output is produced, it is

assumed that:• 20% more labour is needed• 20% more components and raw materials are used• 20% more power will be needed to operate the machinery

How will this affect total costs?

Unit 1: Planning and financing a business

Financial planning

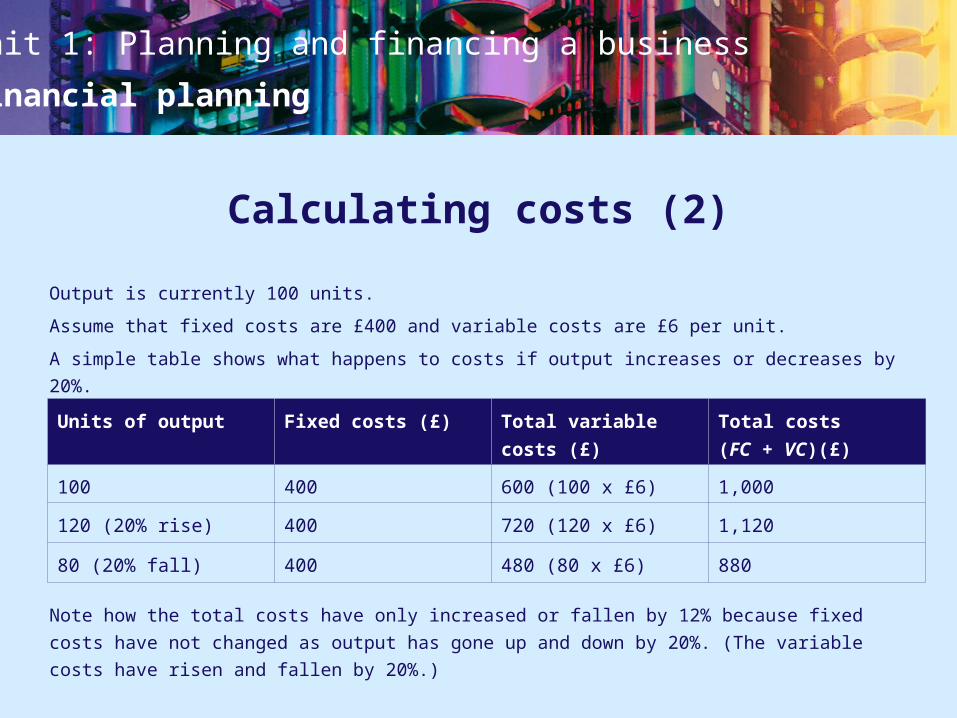

Calculating costs (2)

Output is currently 100 units.

Assume that fixed costs are £400 and variable costs are £6 per unit.

A simple table shows what happens to costs if output increases or decreases by 20%.

Note how the total costs have only increased or fallen by 12% because fixed costs

have not changed as output has gone up and down by 20%. (The variable costs have

risen and fallen by 20%.)

Units of output Fixed costs (£) Total variable

costs (£)

Total costs

(FC + VC)(£)

100 400 600 (100 x £6) 1,000

120 (20% rise) 400 720 (120 x £6) 1,120

80 (20% fall) 400 480 (80 x £6) 880

Unit 1: Planning and financing a business

Financial planning

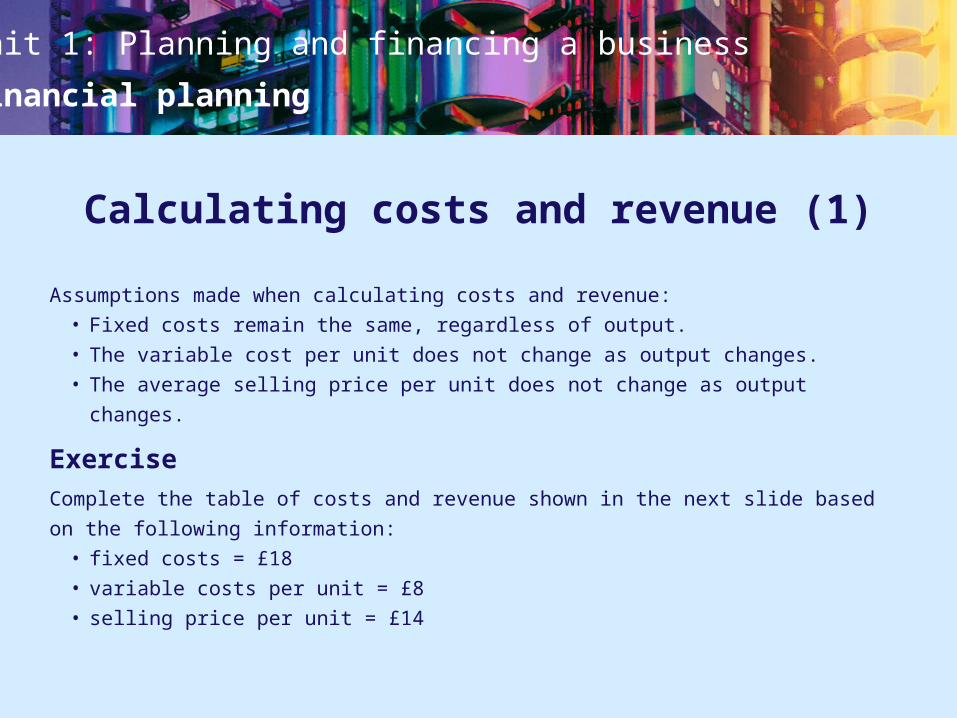

Calculating costs and revenue (1)

Assumptions made when calculating costs and revenue:• Fixed costs remain the same, regardless of output.• The variable cost per unit does not change as output changes.• The average selling price per unit does not change as output changes.

ExerciseComplete the table of costs and revenue shown in the next slide based on the

following information:• fixed costs = £18• variable costs per unit = £8• selling price per unit = £14

Unit 1: Planning and financing a business

Financial planning

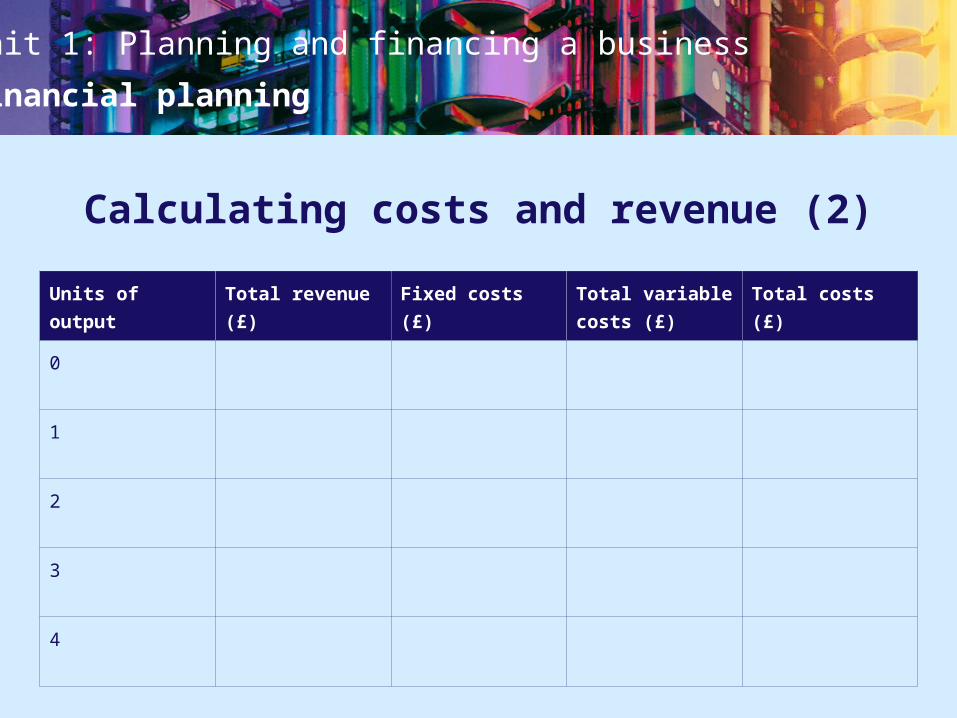

Calculating costs and revenue (2)

Units of

output

Total revenue

(£)

Fixed costs (£) Total variable

costs (£)

Total costs (£)

0

1

2

3

4

Unit 1: Planning and financing a business

Financial planning

Calculating costs and revenue (2): answer

Units of

output

Total revenue

(£)

Fixed costs (£) Total variable

costs (£)

Total costs (£)

0 0 18 0 18

1 14 18 8 26

2 28 18 16 34

3 42 18 24 42

4 56 18 32 50

Unit 1: Planning and financing a business

Financial planning

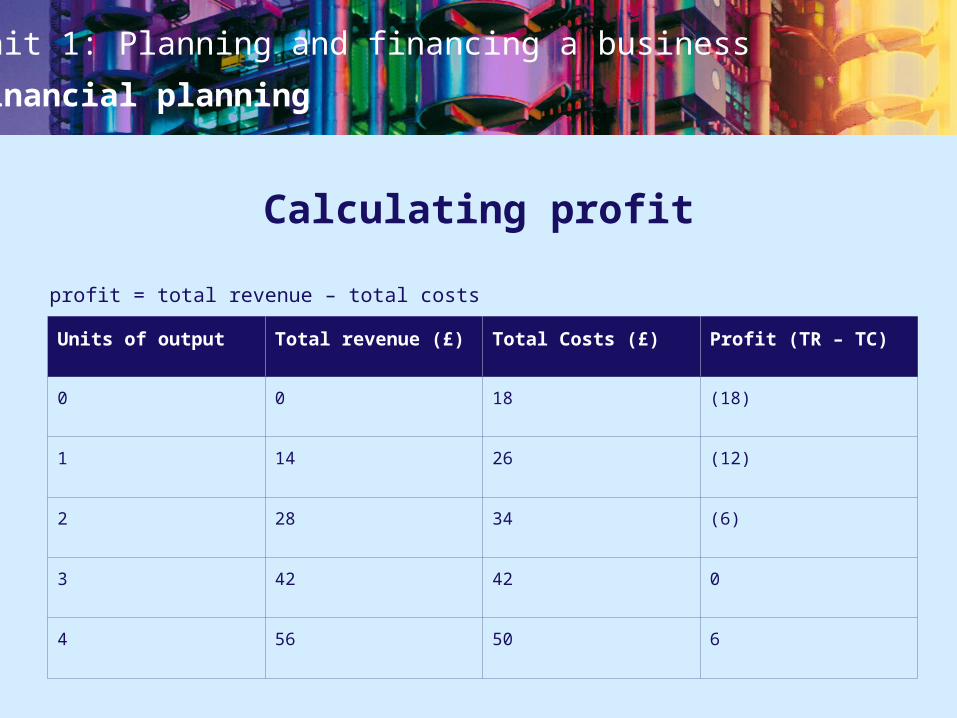

Calculating profit

profit = total revenue – total costs

Units of output Total revenue (£) Total Costs (£) Profit (TR – TC)

0 0 18 (18)

1 14 26 (12)

2 28 34 (6)

3 42 42 0

4 56 50 6

Unit 1: Planning and financing a business

Financial planning

Units of

output

Total

revenue (£)

Fixed costs

(£)

Total variable

costs (£)

Total

costs (£)

Profit (£)

0

1

2 40

3

4 100

5 60

6

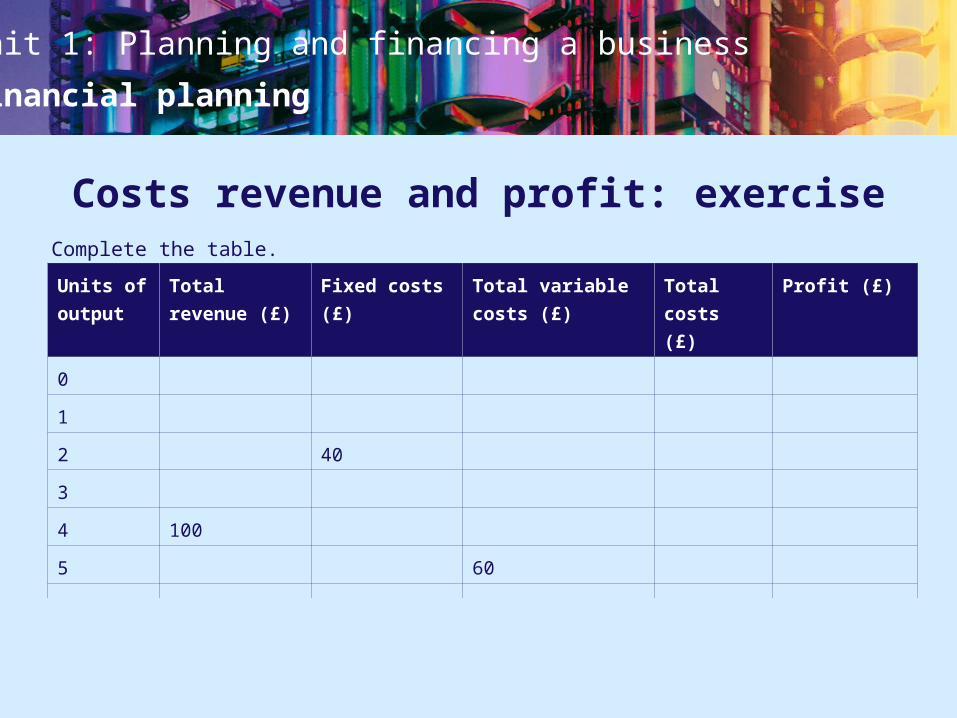

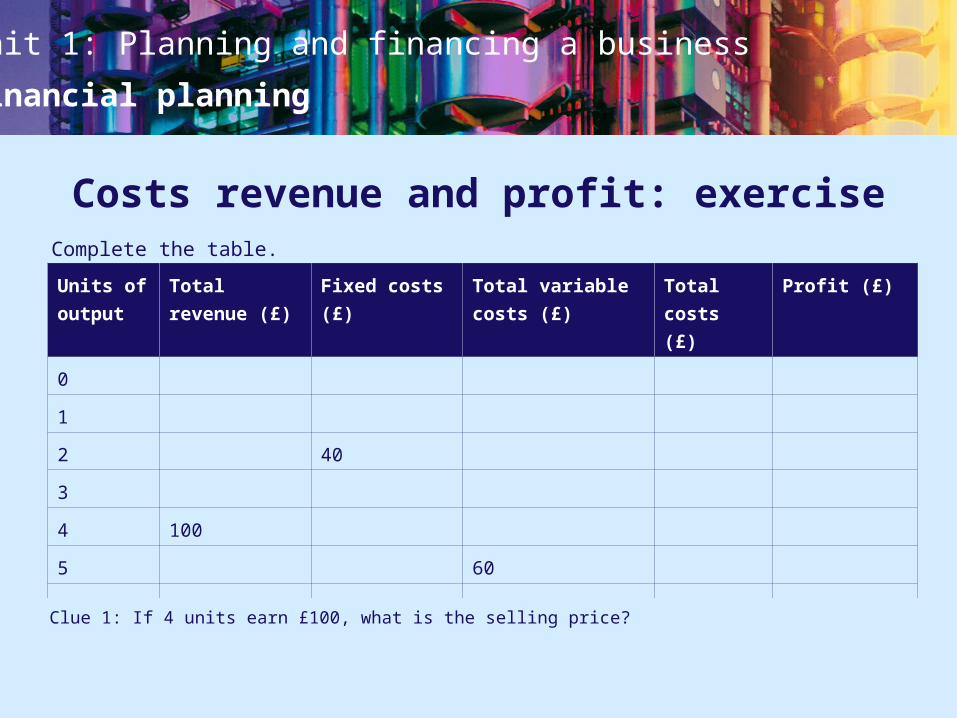

Costs revenue and profit: exercise

Clue 1: If 4 units earn £100, what is the selling price?

Clue 2: In the short term, fixed costs are…?

Clue 3: Use the logic in Clue 1 to work out the variable cost per unit.

Clue 1: If 4 units earn £100, what is the selling price?

Clue 2: In the short term, fixed costs are…?

Clue 1: If 4 units earn £100, what is the selling price?

Complete the table.

Unit 1: Planning and financing a business

Financial planning

Units of

output

Total

revenue (£)

Fixed costs

(£)

Total variable

costs (£)

Total

costs (£)

Profit (£)

0

1

2 40

3

4 100

5 60

6

Costs revenue and profit: exercise

Clue 1: If 4 units earn £100, what is the selling price?

Clue 2: In the short term, fixed costs are…?

Clue 3: Use the logic in Clue 1 to work out the variable cost per unit.

Clue 1: If 4 units earn £100, what is the selling price?

Clue 2: In the short term, fixed costs are…?

Clue 1: If 4 units earn £100, what is the selling price?

Complete the table.

Unit 1: Planning and financing a business

Financial planning

Units of

output

Total

revenue (£)

Fixed costs

(£)

Total variable

costs (£)

Total

costs (£)

Profit (£)

0

1

2 40

3

4 100

5 60

6

Costs revenue and profit: exercise

Clue 1: If 4 units earn £100, what is the selling price?

Clue 2: In the short term, fixed costs are…?

Clue 3: Use the logic in Clue 1 to work out the variable cost per unit.

Clue 1: If 4 units earn £100, what is the selling price?

Clue 2: In the short term, fixed costs are…?

Complete the table.

Unit 1: Planning and financing a business

Financial planning

Units of

output

Total

revenue (£)

Fixed costs

(£)

Total variable

costs (£)

Total

costs (£)

Profit (£)

0

1

2 40

3

4 100

5 60

6

Costs revenue and profit: exercise

Clue 1: If 4 units earn £100, what is the selling price?

Clue 2: In the short term, fixed costs are…?

Clue 3: Use the logic in Clue 1 to work out the variable cost per unit.

Complete the table.

Unit 1: Planning and financing a business

Financial planning

Costs and profit: answer

Units of

output

Total

revenue (£)

Fixed costs

(£)

Total

variable

costs (£)

Total costs

(£)

Profit (£)

0 0 40 0 40 (40)

1 25 40 12 52 (27)

2 50 40 24 64 (14)

3 75 40 36 76 (1)

4 100 40 48 88 12

5 125 40 60 100 25

6 150 40 72 112 38

Unit 1: Planning and financing a business

Financial planning

Costs, revenue and profit: follow-up exercise

Complete the practice exercises and the case study questions at the end of Chapter

11 of the textbook.

Unit 1: Planning and financing a business

Financial planning

Chapter 12

Using breakeven analysis to make decisions

Unit 1: Planning and financing a business

Financial planning

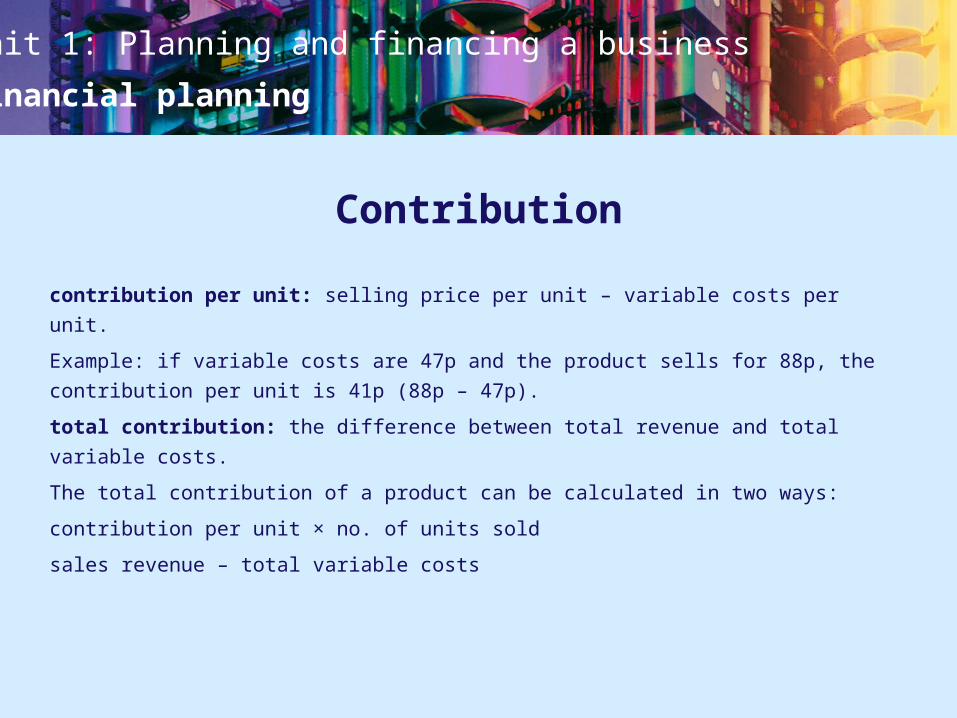

Contribution

contribution per unit: selling price per unit – variable costs per unit.

Example: if variable costs are 47p and the product sells for 88p, the contribution per

unit is 41p (88p – 47p).

total contribution: the difference between total revenue and total variable costs.

The total contribution of a product can be calculated in two ways:

contribution per unit × no. of units sold

sales revenue – total variable costs

Unit 1: Planning and financing a business

Financial planning

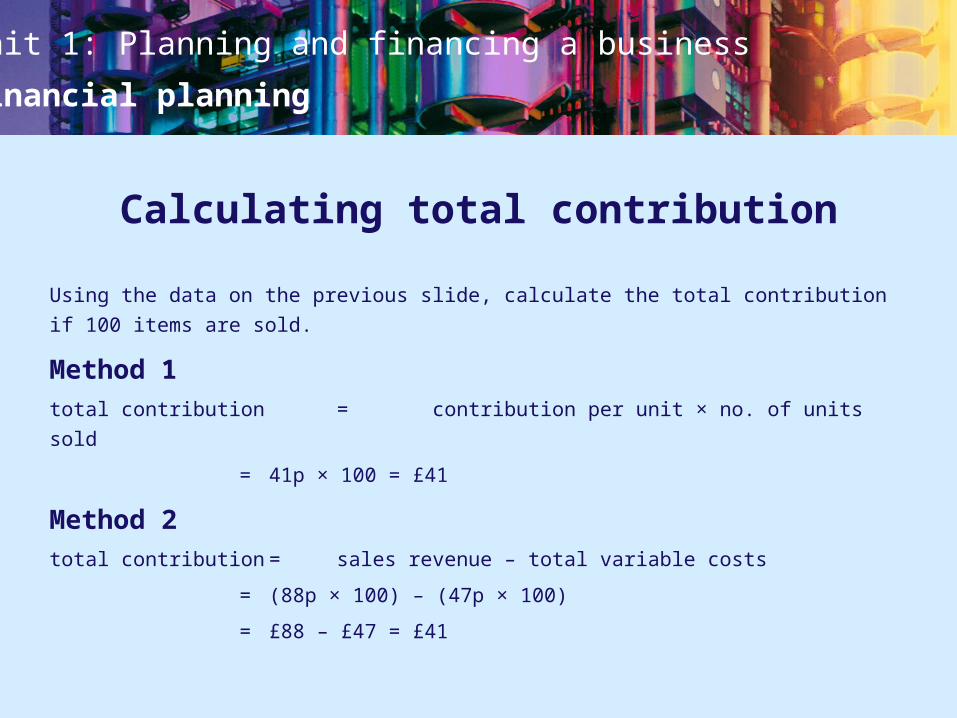

Calculating total contribution

Using the data on the previous slide, calculate the total contribution if 100 items are

sold.

Method 1total contribution = contribution per unit × no. of units sold

= 41p × 100 = £41

Method 2total contribution = sales revenue – total variable costs

= (88p × 100) – (47p × 100)

= £88 – £47 = £41

Unit 1: Planning and financing a business

Financial planning

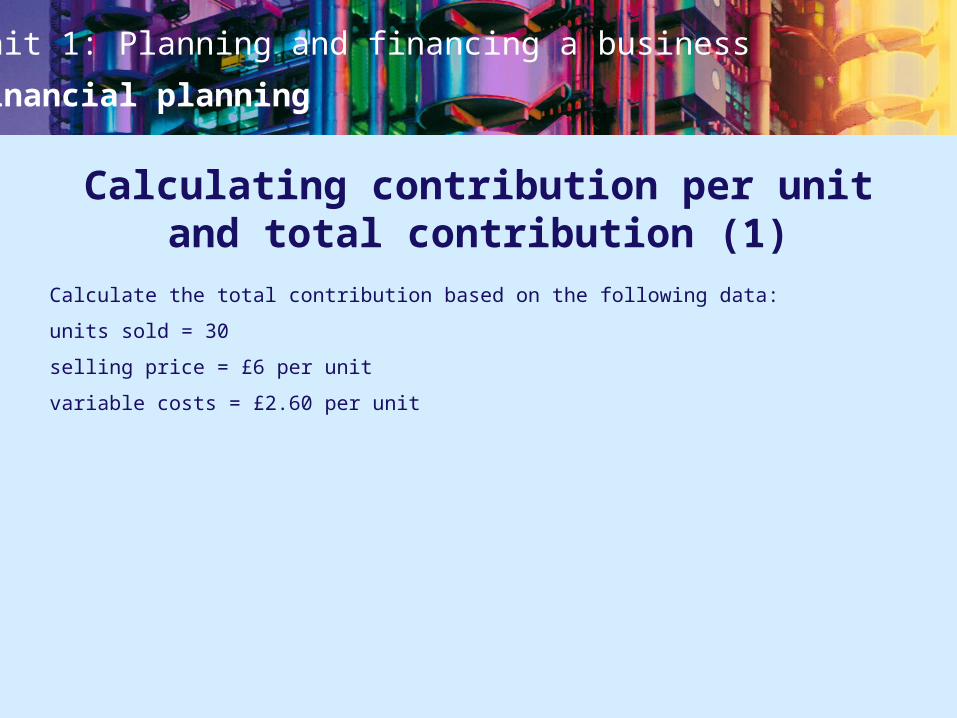

Calculating contribution per unit and total contribution (1)

Calculate the total contribution based on the following data:

units sold = 30

selling price = £6 per unit

variable costs = £2.60 per unit

Unit 1: Planning and financing a business

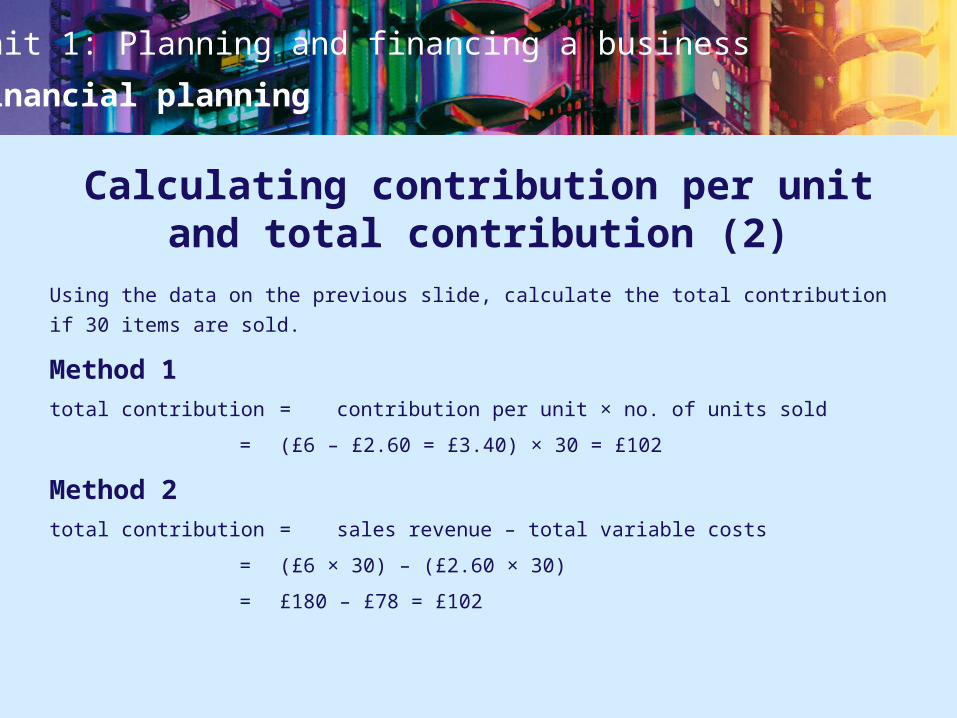

Financial planning

Calculating contribution per unit and total contribution (2)

Using the data on the previous slide, calculate the total contribution if 30 items are

sold.

Method 1total contribution = contribution per unit × no. of units sold

= (£6 – £2.60 = £3.40) × 30 = £102

Method 2total contribution = sales revenue – total variable costs

= (£6 × 30) – (£2.60 × 30)

= £180 – £78 = £102

Unit 1: Planning and financing a business

Financial planning

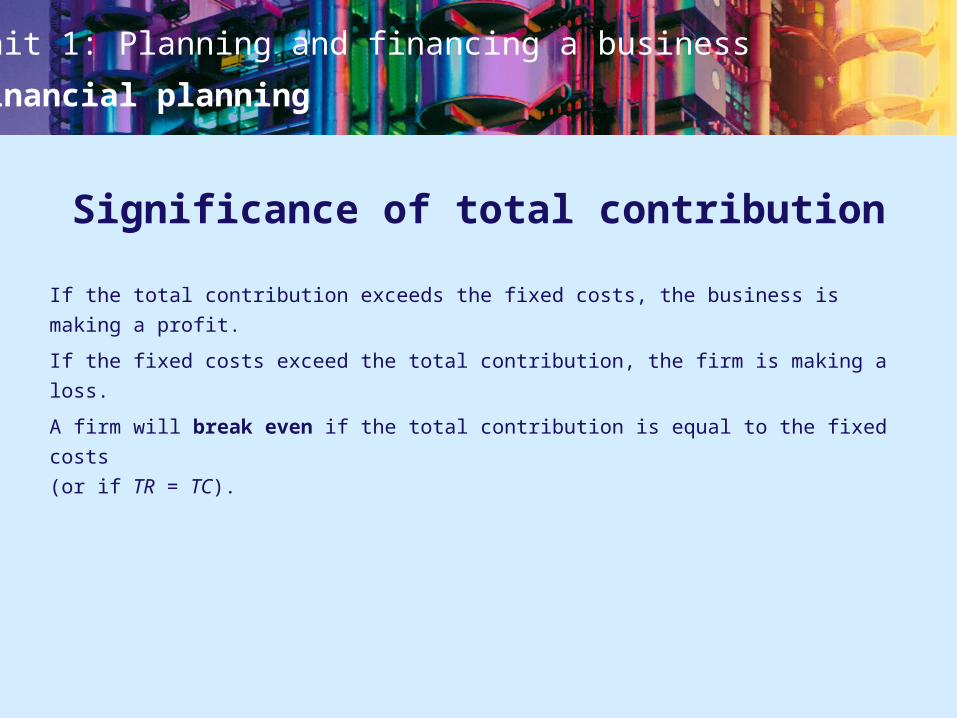

Significance of total contribution

If the total contribution exceeds the fixed costs, the business is making a profit.

If the fixed costs exceed the total contribution, the firm is making a loss.

A firm will break even if the total contribution is equal to the fixed costs

(or if TR = TC).

Unit 1: Planning and financing a business

Financial planning

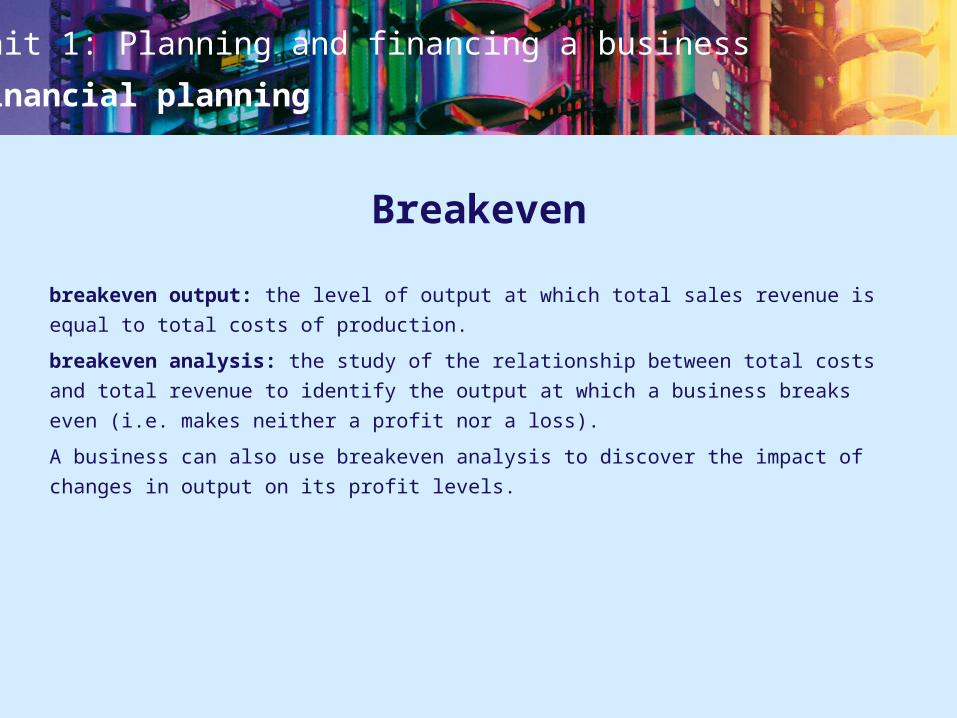

Breakeven

breakeven output: the level of output at which total sales revenue is equal to total

costs of production.

breakeven analysis: the study of the relationship between total costs and total

revenue to identify the output at which a business breaks even (i.e. makes neither a

profit nor a loss).

A business can also use breakeven analysis to discover the impact of changes in

output on its profit levels.

Unit 1: Planning and financing a business

Financial planning

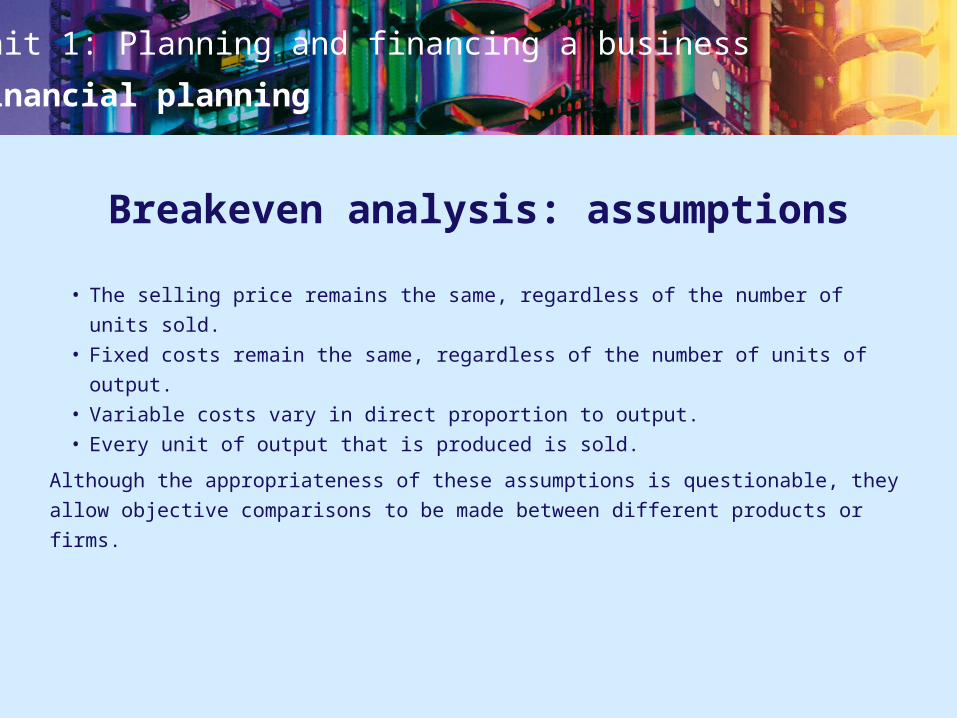

Breakeven analysis: assumptions

• The selling price remains the same, regardless of the number of units sold.• Fixed costs remain the same, regardless of the number of units of output.• Variable costs vary in direct proportion to output. • Every unit of output that is produced is sold.

Although the appropriateness of these assumptions is questionable, they allow

objective comparisons to be made between different products or firms.

Unit 1: Planning and financing a business

Financial planning

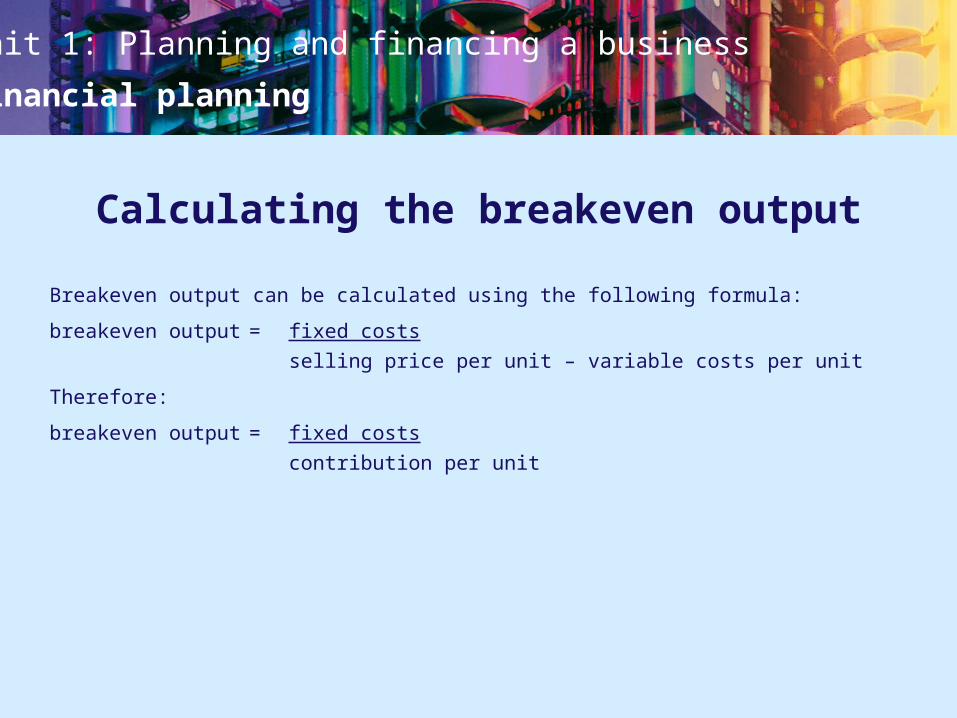

Calculating the breakeven output

Breakeven output can be calculated using the following formula:

breakeven output = fixed costs

selling price per unit – variable costs per unit

Therefore:

breakeven output = fixed costs

contribution per unit

Unit 1: Planning and financing a business

Financial planning

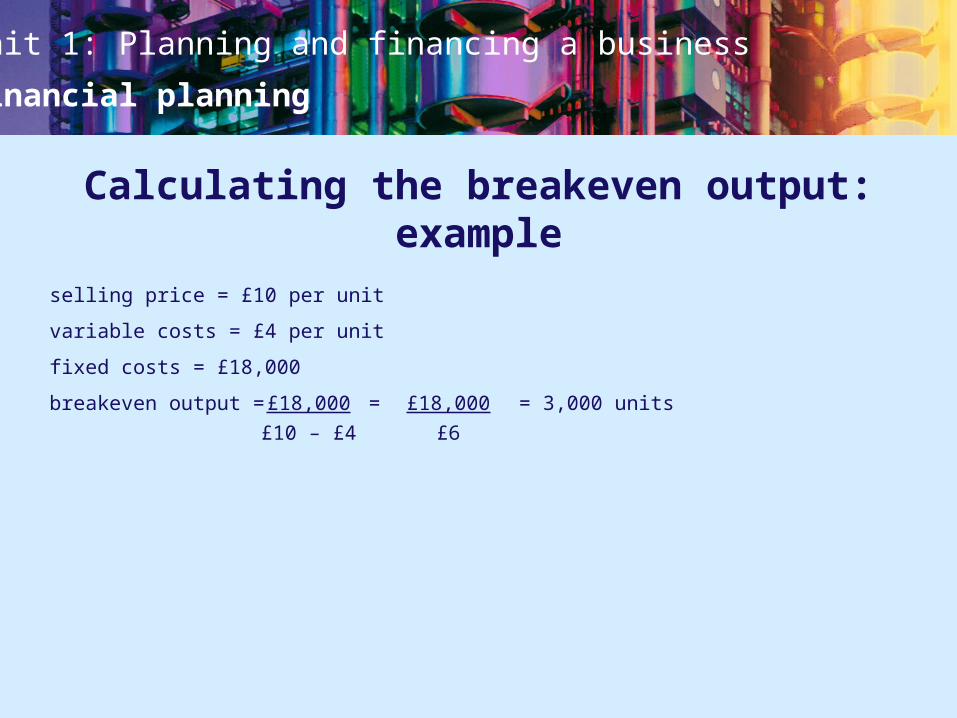

Calculating the breakeven output: example

selling price = £10 per unit

variable costs = £4 per unit

fixed costs = £18,000

breakeven output = £18,000 = £18,000 = 3,000 units

£10 – £4 £6

Unit 1: Planning and financing a business

Financial planning

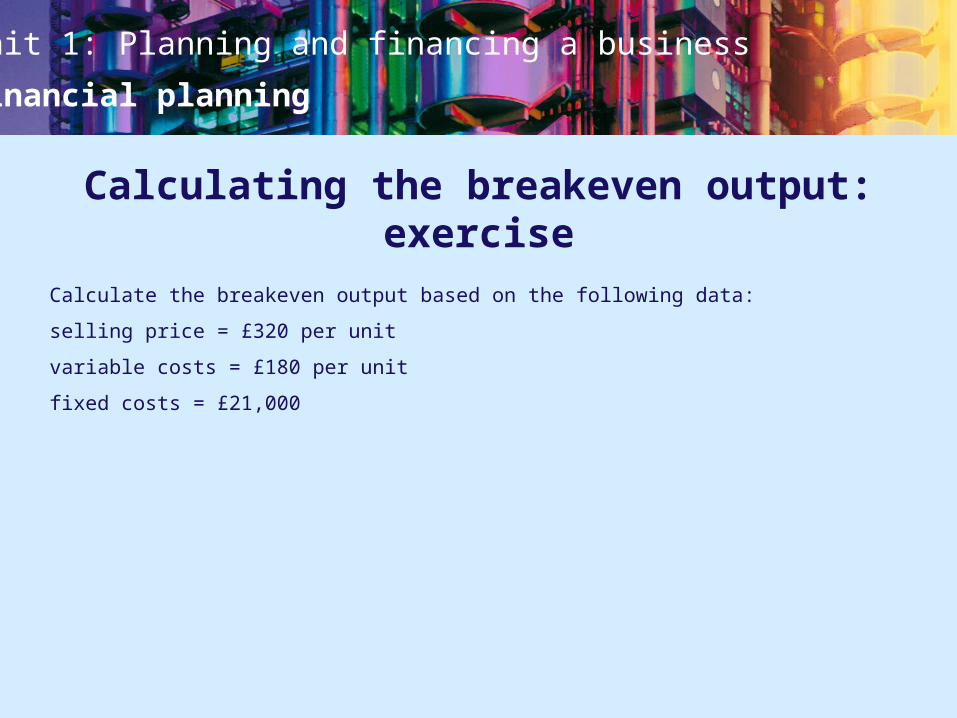

Calculating the breakeven output: exercise

Calculate the breakeven output based on the following data:

selling price = £320 per unit

variable costs = £180 per unit

fixed costs = £21,000

Unit 1: Planning and financing a business

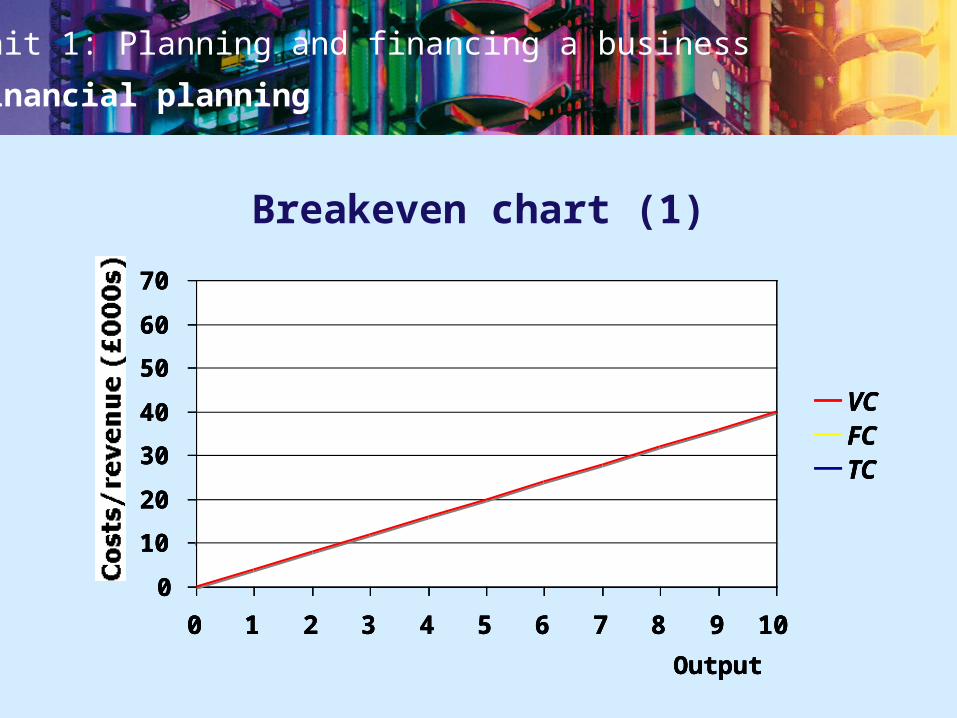

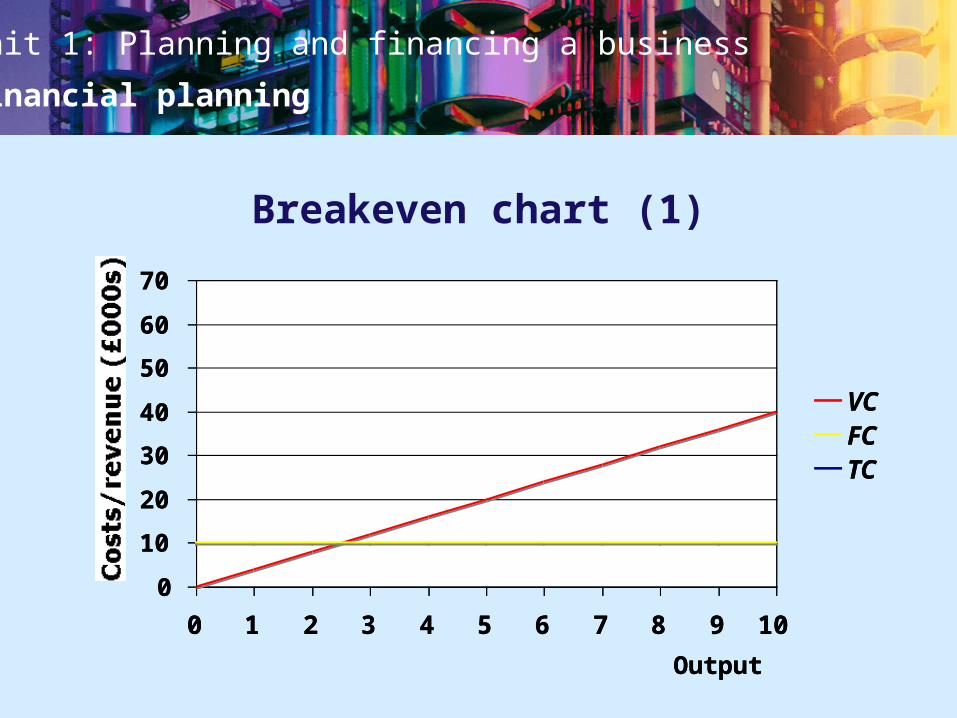

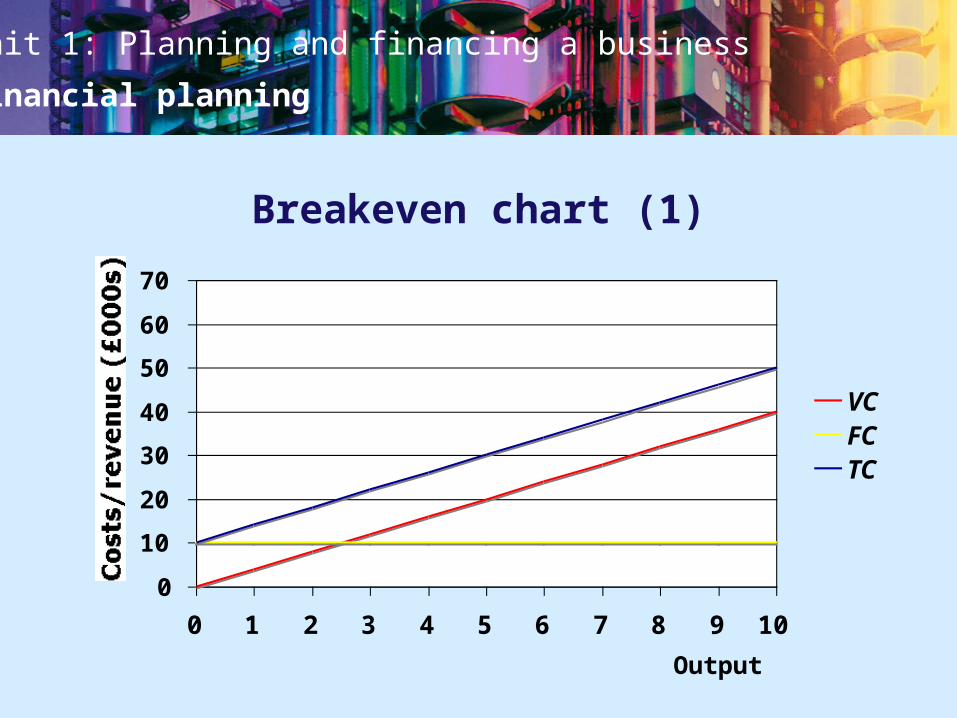

Financial planning

0

10

20

30

40

50

60

70

0 1 2 3 4 5 6 7 8 9 10

Output

Costs/revenue (£000s)

VCFCTC

Breakeven chart (1)

Unit 1: Planning and financing a business

Financial planning

0

10

20

30

40

50

60

70

0 1 2 3 4 5 6 7 8 9 10

Output

Costs/revenue (£000s)

VCFCTC

0

10

20

30

40

50

60

70

0 1 2 3 4 5 6 7 8 9 10

Output

Costs/revenue (£000s)

VCFCTC

0

10

20

30

40

50

60

70

0 1 2 3 4 5 6 7 8 9 10

Output

Costs/revenue (£000s)

VCFCTC

Breakeven chart (1)

Unit 1: Planning and financing a business

Financial planning

0

10

20

30

40

50

60

70

0 1 2 3 4 5 6 7 8 9 10

Output

Costs/revenue (£000s)

VCFCTC

0

10

20

30

40

50

60

70

0 1 2 3 4 5 6 7 8 9 10

Output

Costs/revenue (£000s)

VCFCTC

Breakeven chart (1)

Unit 1: Planning and financing a business

Financial planning

0

10

20

30

40

50

60

70

0 1 2 3 4 5 6 7 8 9 10

Output

Costs/revenue (£000s)

VCFCTC

Breakeven chart (1)

Unit 1: Planning and financing a business

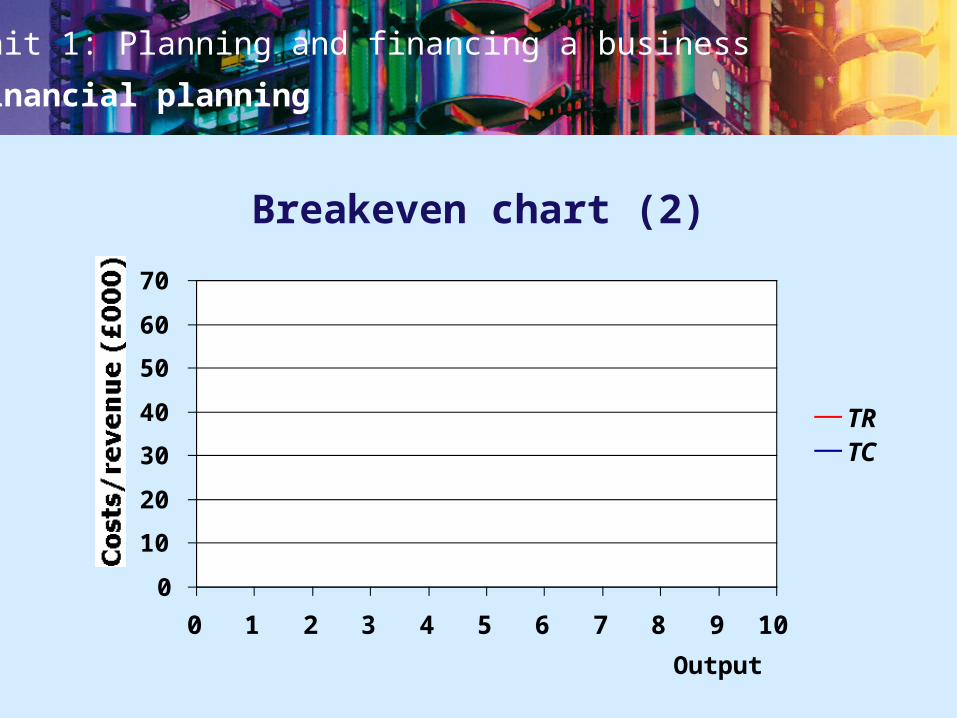

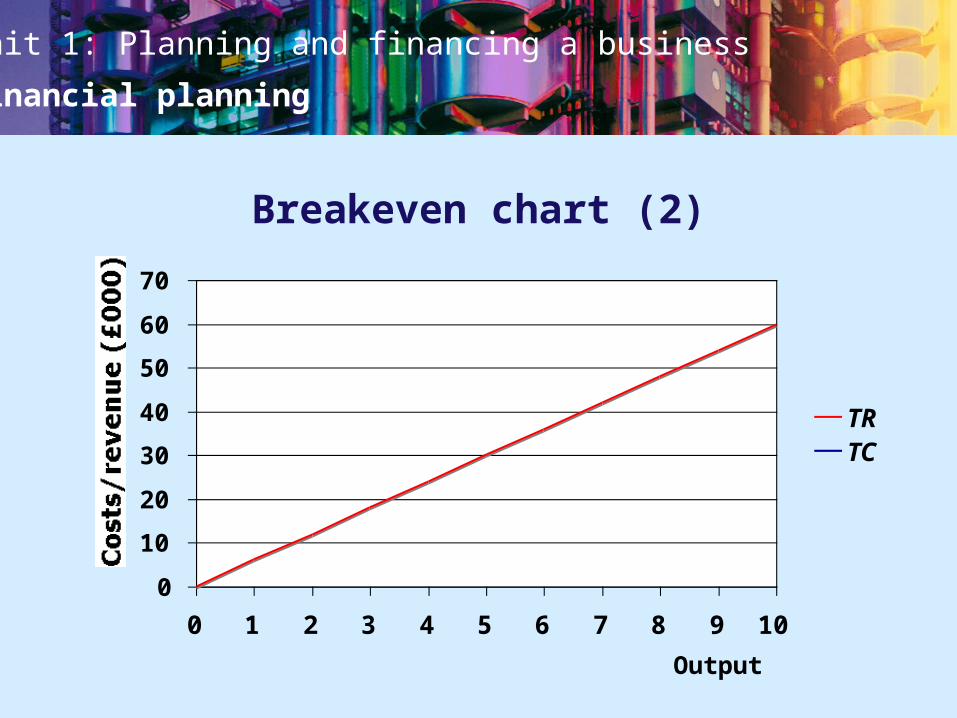

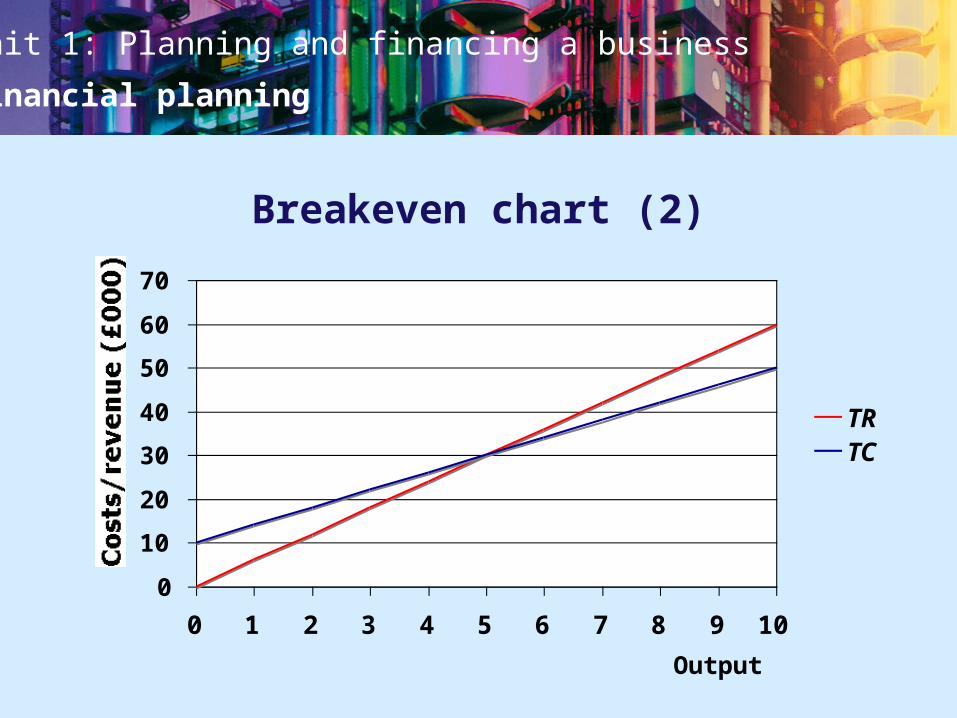

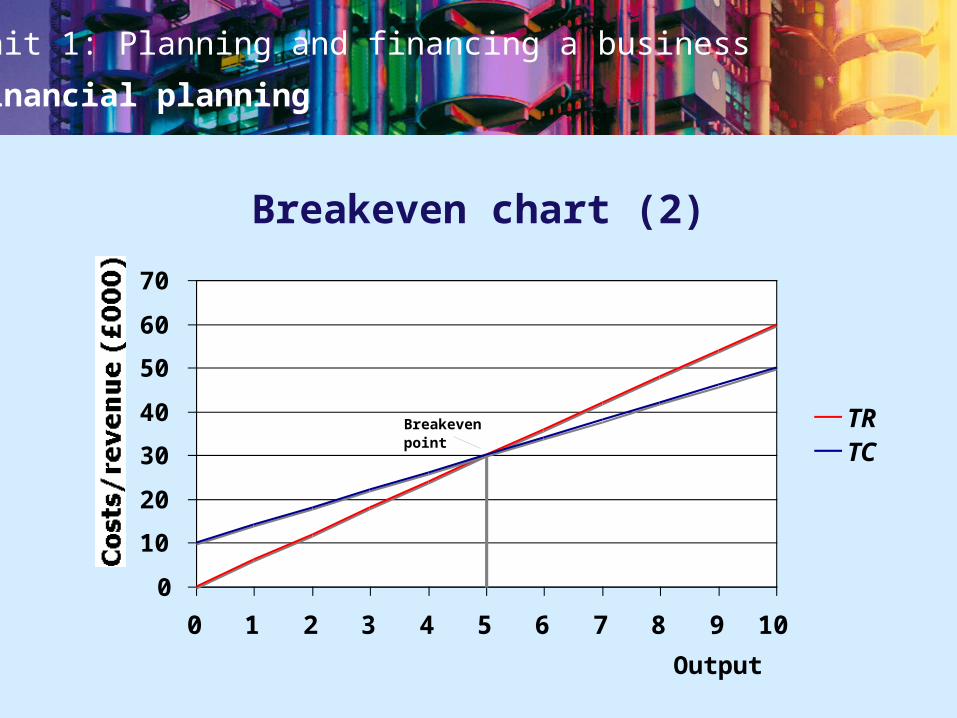

Financial planning

Breakeven chart (2)

0

10

20

30

40

50

60

70

0 1 2 3 4 5 6 7 8 9 10

Output

Costs/revenue (£000)

TRTC

Unit 1: Planning and financing a business

Financial planning

0

10

20

30

40

50

60

70

0 1 2 3 4 5 6 7 8 9 10

Output

Costs/revenue (£000)

TRTC

Breakeven chart (2)

Unit 1: Planning and financing a business

Financial planning

0

10

20

30

40

50

60

70

0 1 2 3 4 5 6 7 8 9 10

Output

Costs/revenue (£000)

TRTC

Breakeven chart (2)

Unit 1: Planning and financing a business

Financial planning

0

10

20

30

40

50

60

70

0 1 2 3 4 5 6 7 8 9 10

Output

Costs/revenue (£000)

TRTC

Breakevenpoint

Breakeven chart (2)

Unit 1: Planning and financing a business

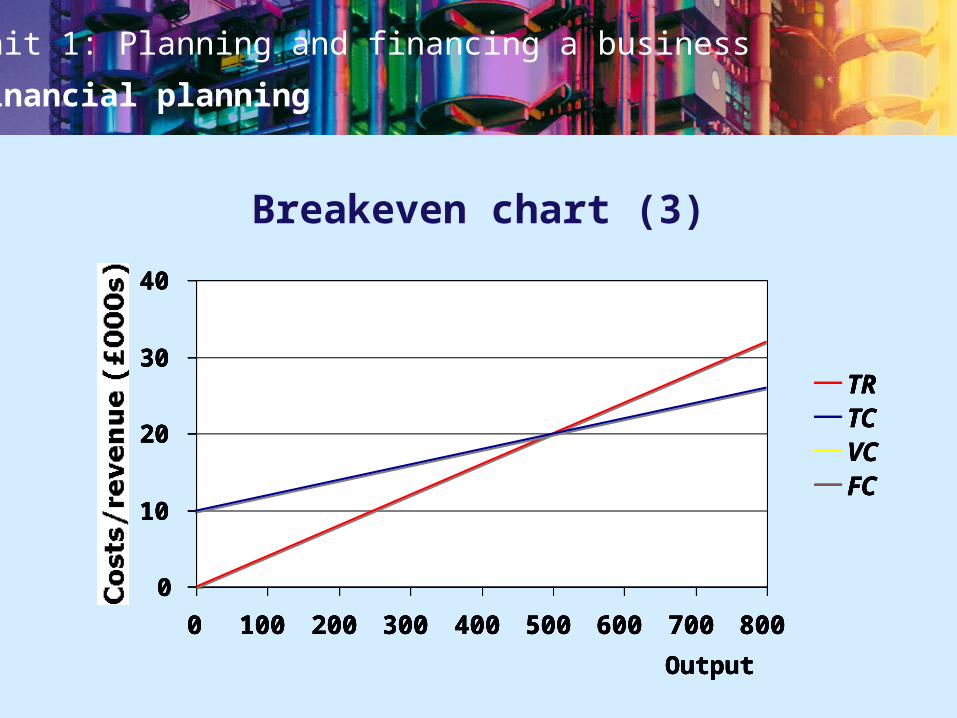

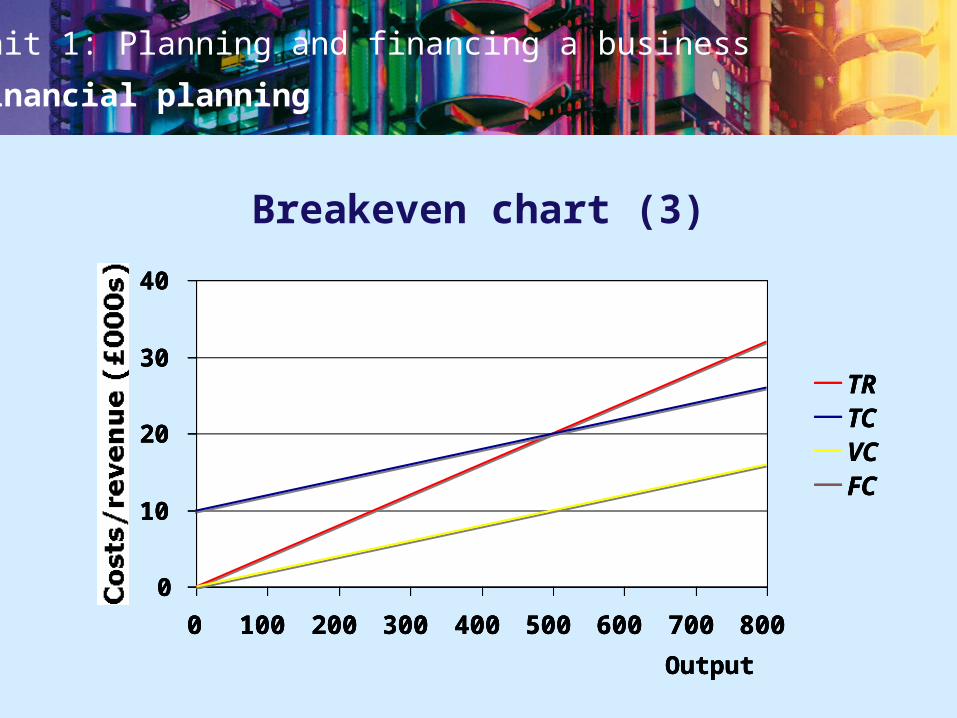

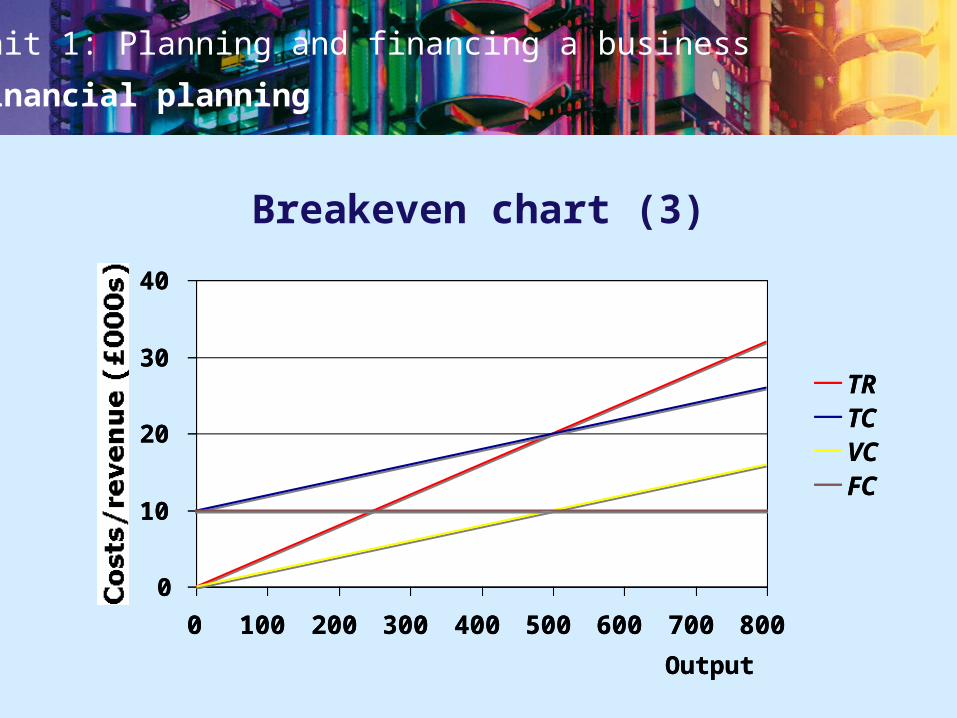

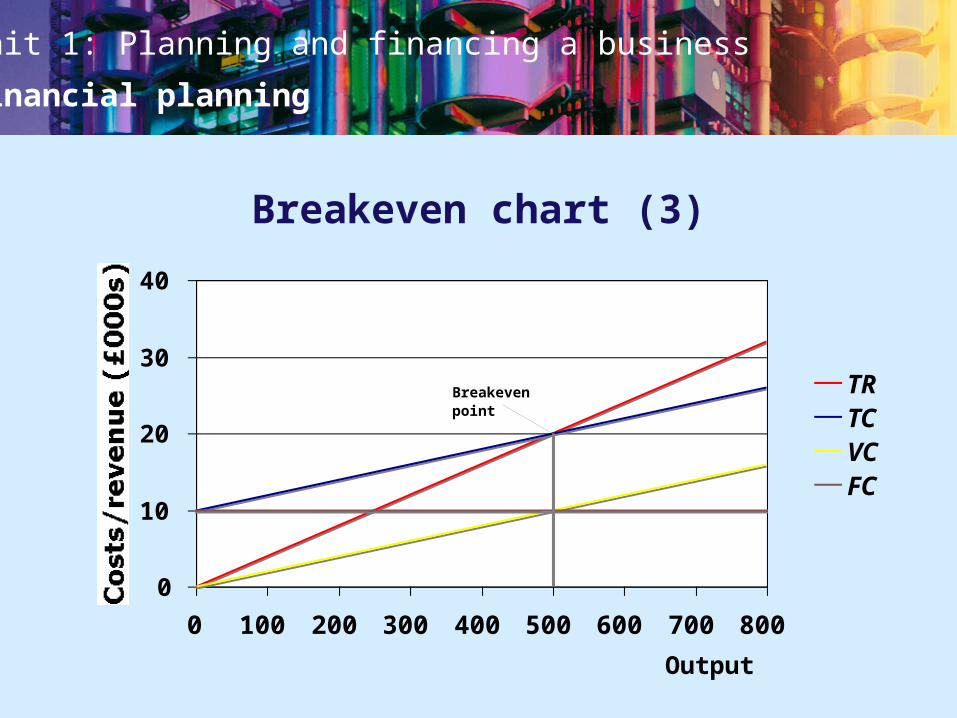

Financial planning

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue (£000s)

TRTCVCFC

Breakeven chart (3)

Unit 1: Planning and financing a business

Financial planning

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue (£000s)

TRTCVCFC

Breakeven point

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue (£000s)

TRTCVCFC

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue (£000s)

TRTCVCFC

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue (£000s)

TRTCVCFC

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue (£000s)

TRTCVCFC

Breakeven chart (3)

Unit 1: Planning and financing a business

Financial planning

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue (£000s)

TRTCVCFC

Breakeven point

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue (£000s)

TRTCVCFC

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue (£000s)

TRTCVCFC

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue (£000s)

TRTCVCFC

Breakeven chart (3)

Unit 1: Planning and financing a business

Financial planning

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue (£000s)

TRTCVCFC

Breakeven point

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue (£000s)

TRTCVCFC

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue (£000s)

TRTCVCFC

Breakeven chart (3)

Unit 1: Planning and financing a business

Financial planning

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue (£000s)

TRTCVCFC

Breakeven point

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue (£000s)

TRTCVCFC

Breakeven chart (3)

Unit 1: Planning and financing a business

Financial planning

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue (£000s)

TRTCVCFC

Breakeven point

Breakeven chart (3)

Unit 1: Planning and financing a business

Financial planning

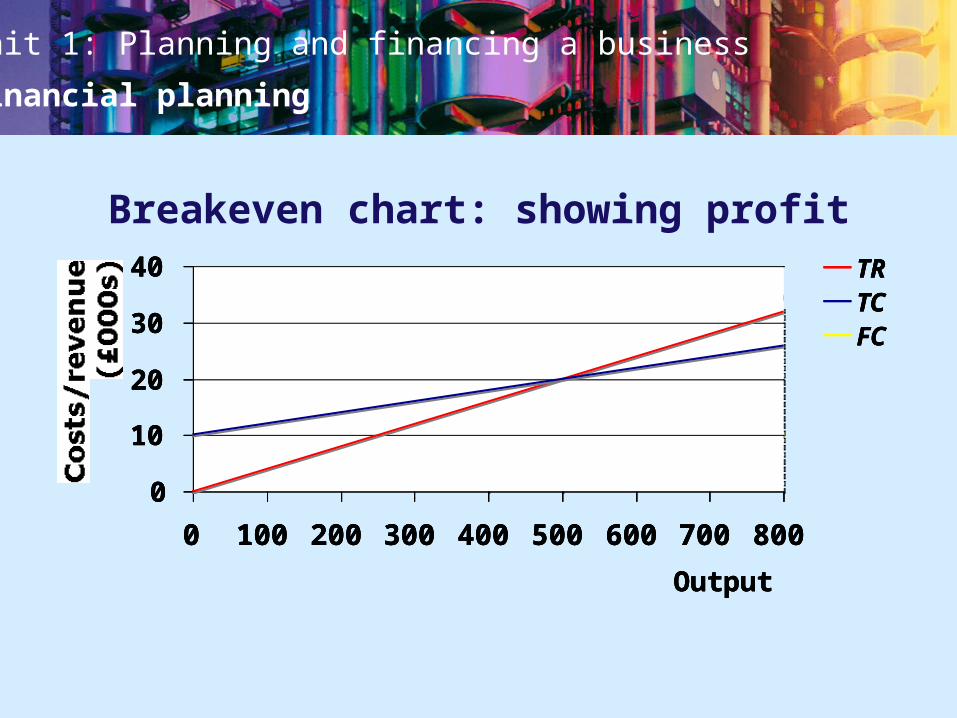

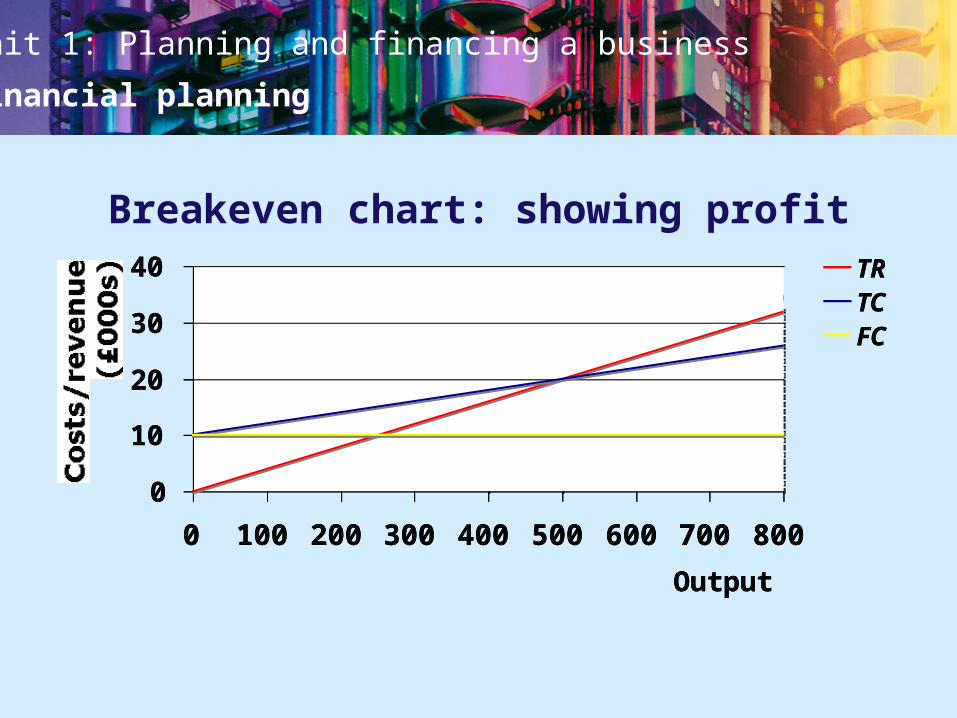

Breakeven chart: showing profit

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue

(£000s)

TRTCFC

Unit 1: Planning and financing a business

Financial planning

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue

(£000s)

TRTCFC

(a)

(b)(c)

(d)

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue

(£000s)

TRTCFC

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue

(£000s)

TRTCFC

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue

(£000s)

TRTCFC

Breakeven chart: showing profit

Unit 1: Planning and financing a business

Financial planning

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue

(£000s)

TRTCFC

(a)

(b)(c)

(d)

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue

(£000s)

TRTCFC

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue

(£000s)

TRTCFC

Breakeven chart: showing profit

Unit 1: Planning and financing a business

Financial planning

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue

(£000s)

TRTCFC

(a)

(b)(c)

(d)

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue

(£000s)

TRTCFC

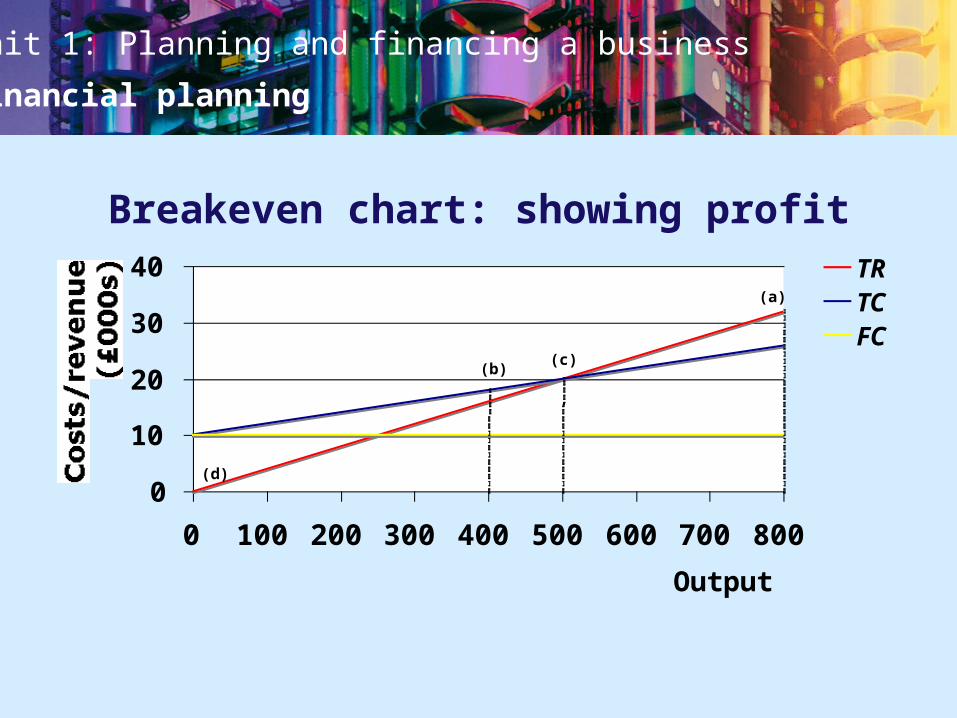

Breakeven chart: showing profit

Unit 1: Planning and financing a business

Financial planning

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue

(£000s)

TRTCFC

(a)

(b)(c)

(d)

Breakeven chart: showing profit

Unit 1: Planning and financing a business

Financial planning

What is the profit (loss) at the following levels of output?

(a)

(b)

(c)

(d)

Conclusion: profit (loss) is the vertical distance between the TR and TC curves at the

output given.

Unit 1: Planning and financing a business

Financial planning

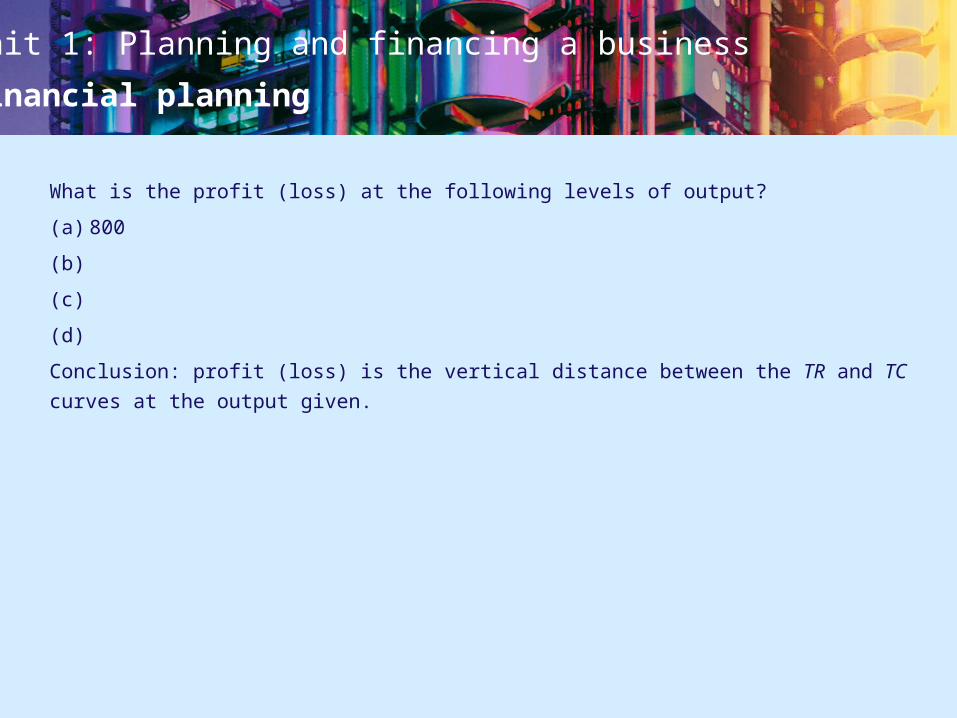

What is the profit (loss) at the following levels of output?

(a) 800

(b) 400

(c) 500

(d) 0

Conclusion: profit (loss) is the vertical distance between the TR and TC curves at the

output given.

What is the profit (loss) at the following levels of output?

(a) 800

(b) 400

(c) 500

(d)

Conclusion: profit (loss) is the vertical distance between the TR and TC curves at the

output given.

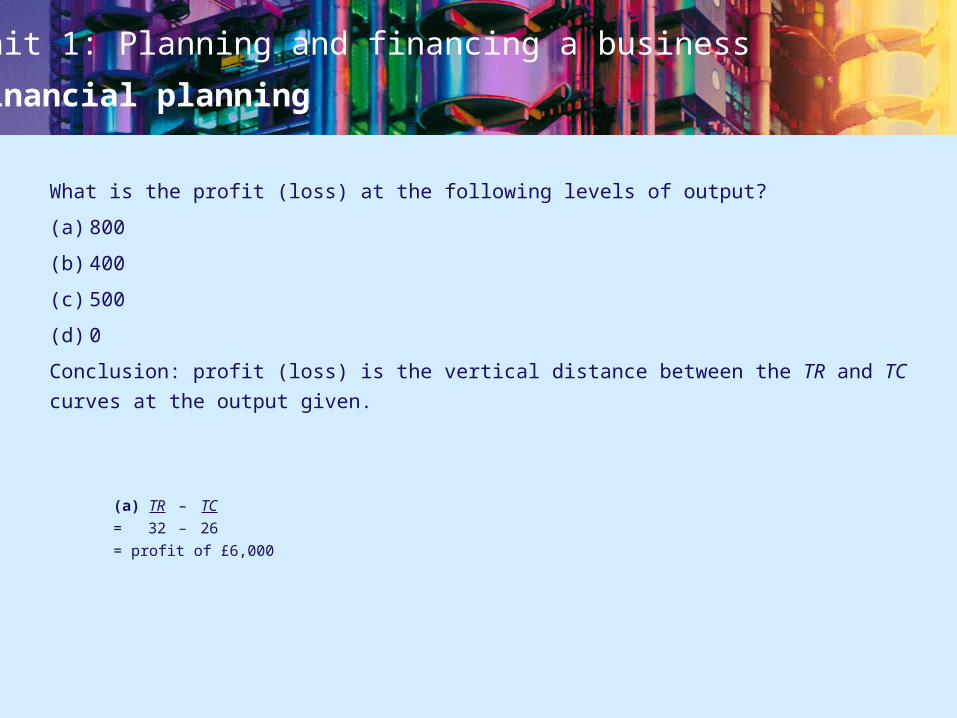

What is the profit (loss) at the following levels of output?

(a) 800

(b) 400

(c)

(d)

Conclusion: profit (loss) is the vertical distance between the TR and TC curves at the

output given.

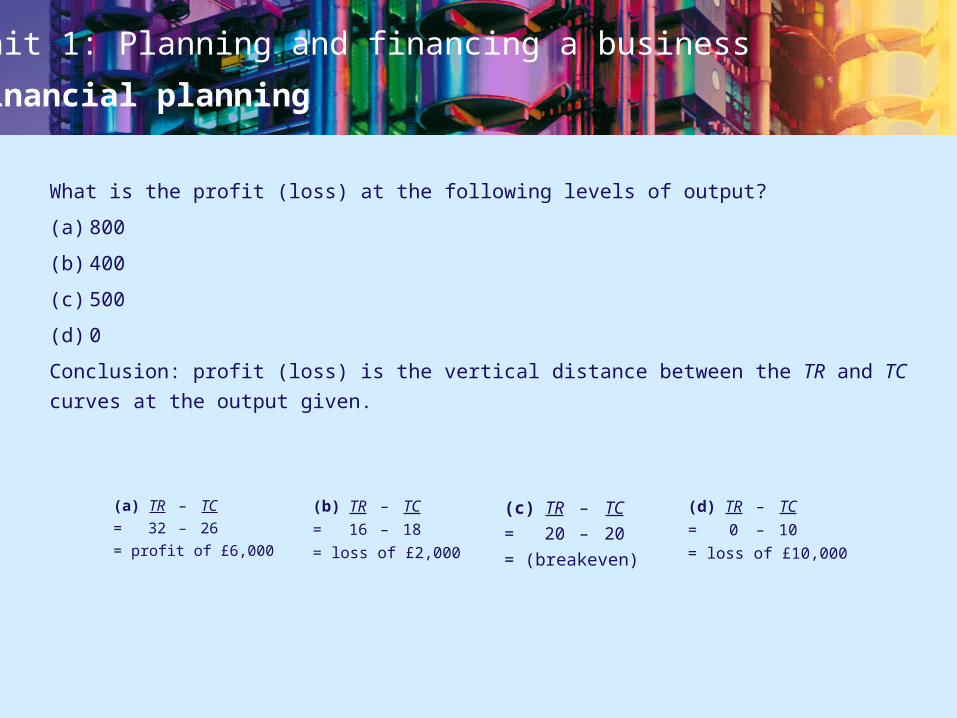

What is the profit (loss) at the following levels of output?

(a) 800

(b)

(c)

(d)

Conclusion: profit (loss) is the vertical distance between the TR and TC curves at the

output given.

(a) TR – TC

= 32 – 26

= profit of £6,000

(b) TR – TC

= 16 – 18

= loss of £2,000

(c) TR – TC

= 20 – 20

= (breakeven)

(d) TR – TC

= 0 – 10

= loss of £10,000

Unit 1: Planning and financing a business

Financial planning

What is the profit (loss) at the following levels of output?

(a) 800

(b) 400

(c) 500

(d) 0

Conclusion: profit (loss) is the vertical distance between the TR and TC curves at the

output given.

What is the profit (loss) at the following levels of output?

(a) 800

(b) 400

(c) 500

(d)

Conclusion: profit (loss) is the vertical distance between the TR and TC curves at the

output given.

What is the profit (loss) at the following levels of output?

(a) 800

(b) 400

(c)

(d)

Conclusion: profit (loss) is the vertical distance between the TR and TC curves at the

output given.

(a) TR – TC

= 32 – 26

= profit of £6,000

(b) TR – TC

= 16 – 18

= loss of £2,000

(c) TR – TC

= 20 – 20

= (breakeven)

(d) TR – TC

= 0 – 10

= loss of £10,000

Unit 1: Planning and financing a business

Financial planning

What is the profit (loss) at the following levels of output?

(a) 800

(b) 400

(c) 500

(d) 0

Conclusion: profit (loss) is the vertical distance between the TR and TC curves at the

output given.

What is the profit (loss) at the following levels of output?

(a) 800

(b) 400

(c) 500

(d)

Conclusion: profit (loss) is the vertical distance between the TR and TC curves at the

output given.

(a) TR – TC

= 32 – 26

= profit of £6,000

(b) TR – TC

= 16 – 18

= loss of £2,000

(c) TR – TC

= 20 – 20

= (breakeven)

(d) TR – TC

= 0 – 10

= loss of £10,000

Unit 1: Planning and financing a business

Financial planning

What is the profit (loss) at the following levels of output?

(a) 800

(b) 400

(c) 500

(d) 0

Conclusion: profit (loss) is the vertical distance between the TR and TC curves at the

output given.

(a) TR – TC

= 32 – 26

= profit of £6,000

(b) TR – TC

= 16 – 18

= loss of £2,000

(c) TR – TC

= 20 – 20

= (breakeven)

(d) TR – TC

= 0 – 10

= loss of £10,000

Unit 1: Planning and financing a business

Financial planning

What is the profit (loss) at the following levels of output?

(a) 800

(b) 400

(c) 500

(d) 0

Conclusion: profit (loss) is the vertical distance between the TR and TC curves at the

output given.

(a) TR – TC

= 32 – 26

= profit of £6,000

(b) TR – TC

= 16 – 18

= loss of £2,000

(c) TR – TC

= 20 – 20

= (breakeven)

(d) TR – TC

= 0 – 10

= loss of £10,000

Unit 1: Planning and financing a business

Financial planning

What is the profit (loss) at the following levels of output?

(a) 800

(b) 400

(c) 500

(d) 0

Conclusion: profit (loss) is the vertical distance between the TR and TC curves at the

output given.

(a) TR – TC

= 32 – 26

= profit of £6,000

(b) TR – TC

= 16 – 18

= loss of £2,000

(c) TR – TC

= 20 – 20

= (breakeven)

(d) TR – TC

= 0 – 10

= loss of £10,000

Unit 1: Planning and financing a business

Financial planning

What is the profit (loss) at the following levels of output?

(a) 800

(b) 400

(c) 500

(d) 0

Conclusion: profit (loss) is the vertical distance between the TR and TC curves at the

output given.

(a) TR – TC

= 32 – 26

= profit of £6,000

(b) TR – TC

= 16 – 18

= loss of £2,000

(c) TR – TC

= 20 – 20

= (breakeven)

(d) TR – TC

= 0 – 10

= loss of £10,000

Unit 1: Planning and financing a business

Financial planning

What is the profit (loss) at the following levels of output?

(a) 800

(b) 400

(c) 500

(d) 0

Conclusion: profit (loss) is the vertical distance between the TR and TC curves at the

output given.

(a) TR – TC

= 32 – 26

= profit of £6,000

(b) TR – TC

= 16 – 18

= loss of £2,000

(c) TR – TC

= 20 – 20

= (breakeven)

(d) TR – TC

= 0 – 10

= loss of £10,000

Unit 1: Planning and financing a business

Financial planning

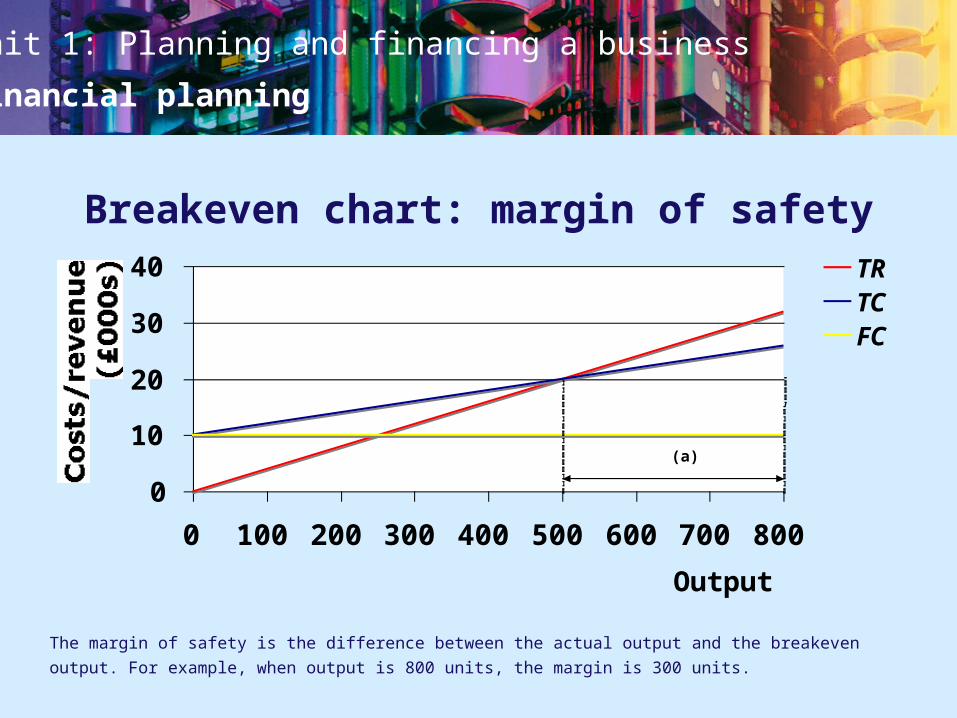

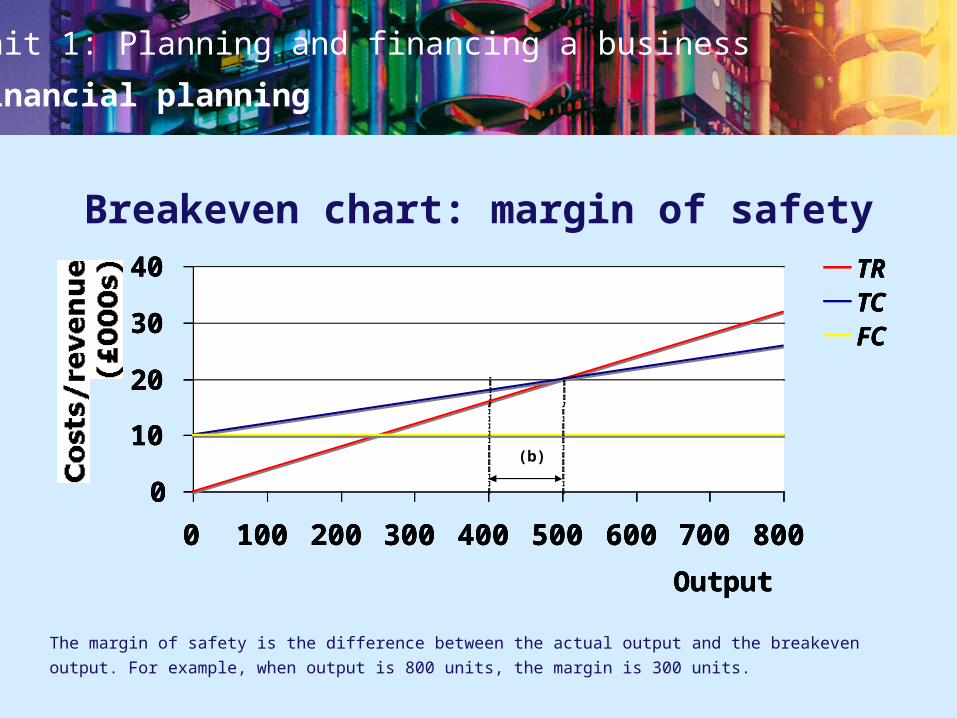

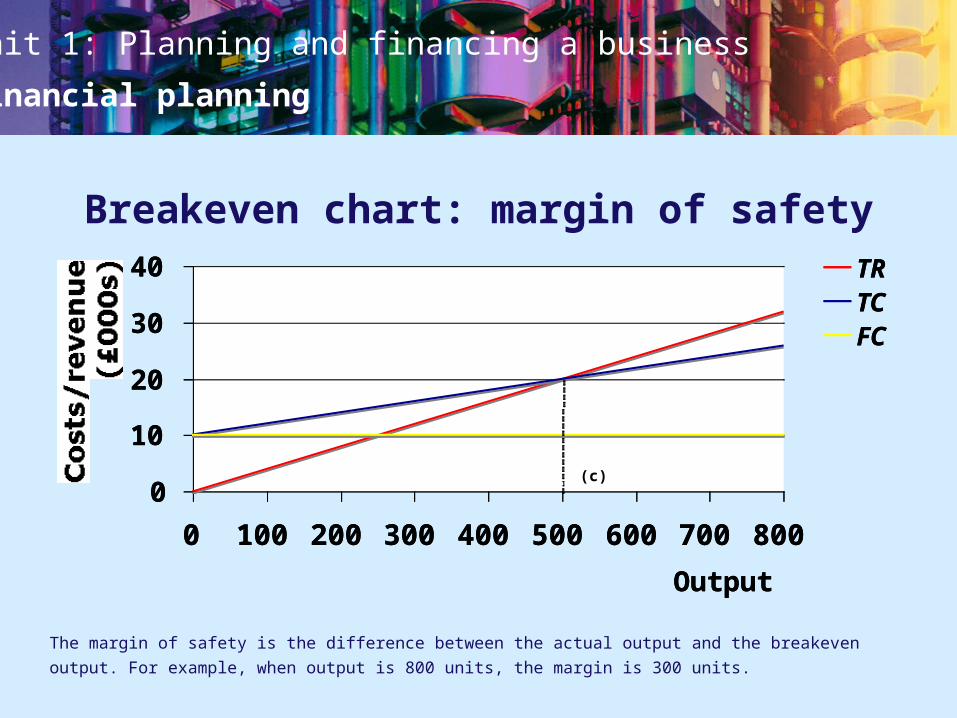

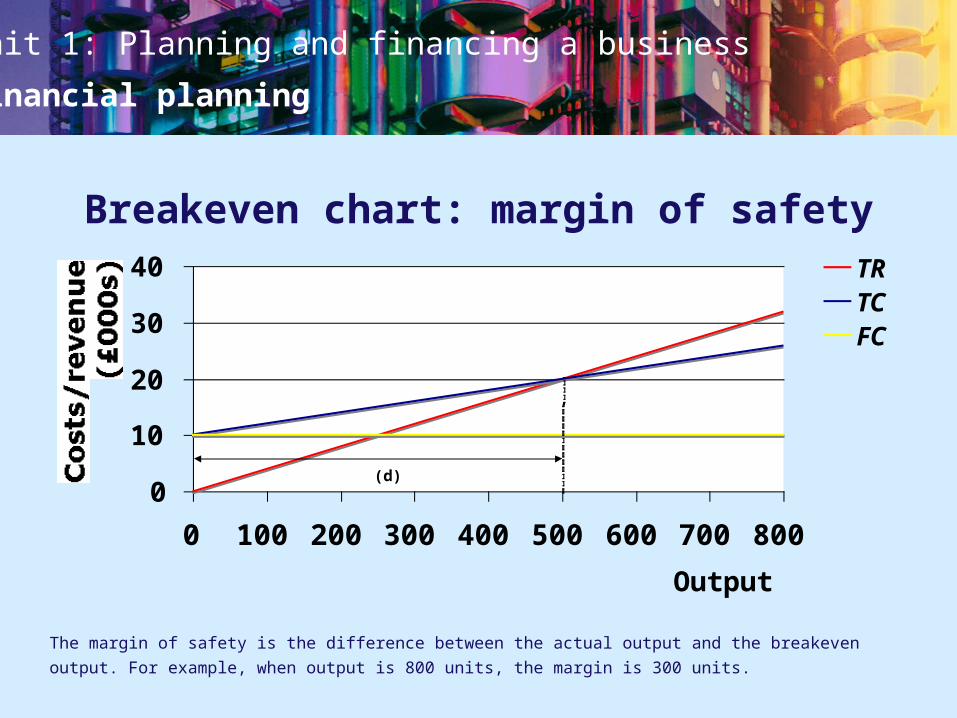

Breakeven chart: margin of safety

The margin of safety is the difference between the actual output and the breakeven

output. For example, when output is 800 units, the margin is 300 units.

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue

(£000s)

TRTCFC

(a)

Unit 1: Planning and financing a business

Financial planning

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue

(£000s)

TRTCFC

(d)0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue

(£000s)

TRTCFC

(c)0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue

(£000s)

TRTCFC

(b)

Breakeven chart: margin of safety

The margin of safety is the difference between the actual output and the breakeven

output. For example, when output is 800 units, the margin is 300 units.

Unit 1: Planning and financing a business

Financial planning

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue

(£000s)

TRTCFC

(d)0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue

(£000s)

TRTCFC

(c)

The margin of safety is the difference between the actual output and the breakeven

output. For example, when output is 800 units, the margin is 300 units.

Breakeven chart: margin of safety

Unit 1: Planning and financing a business

Financial planning

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue

(£000s)

TRTCFC

(d)

The margin of safety is the difference between the actual output and the breakeven

output. For example, when output is 800 units, the margin is 300 units.

Breakeven chart: margin of safety

Unit 1: Planning and financing a business

Financial planning

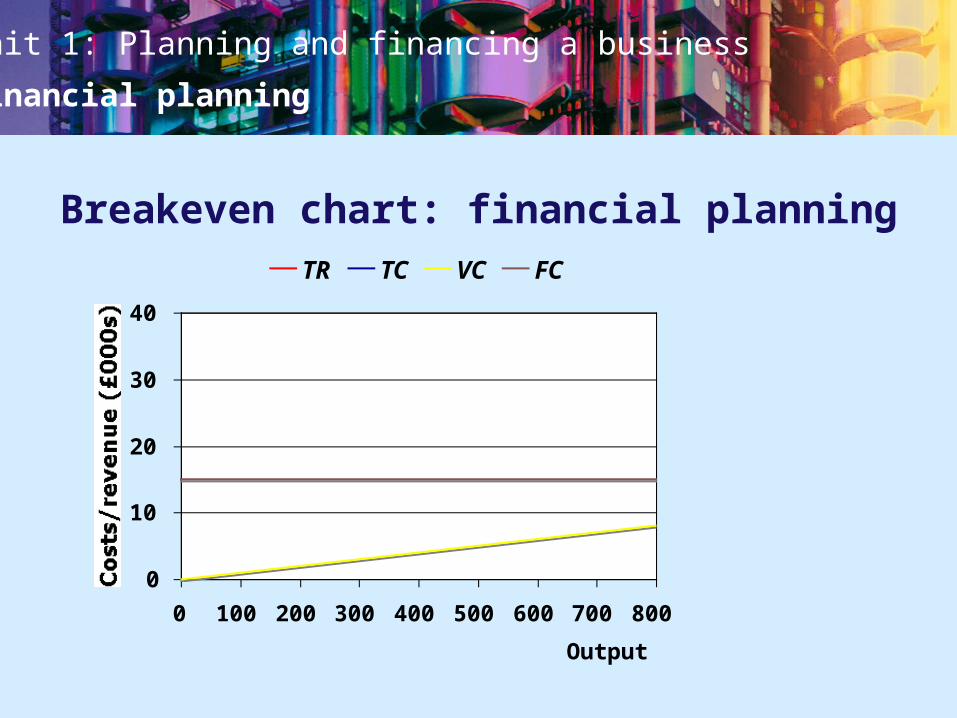

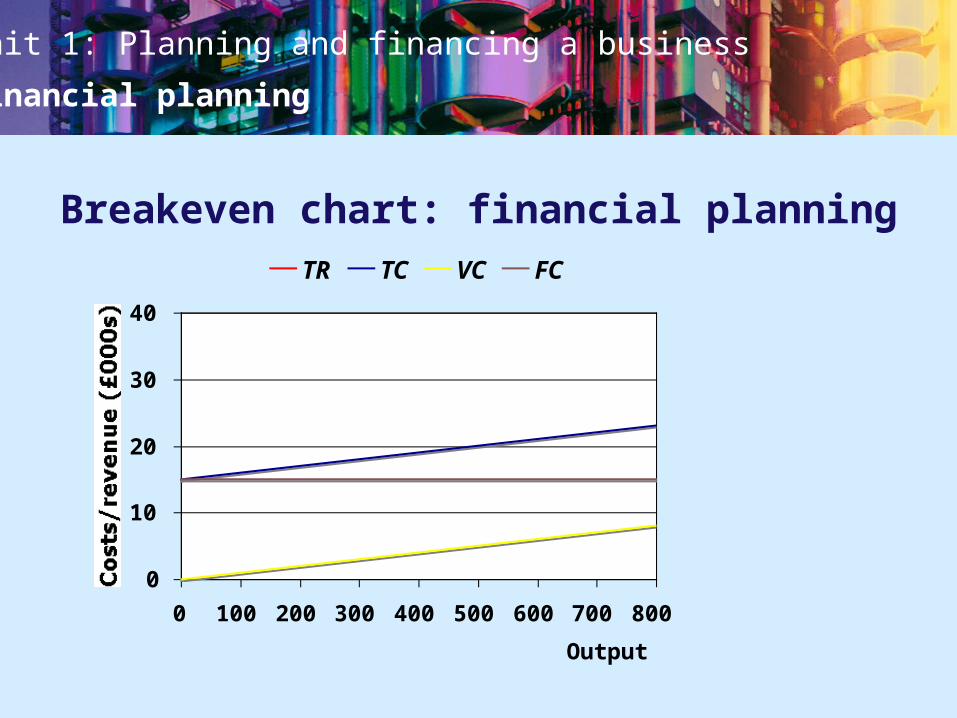

Breakeven chart: ‘what if?’ analysis

Breakeven charts can be used to see what happens if one of the variables is

changed: for example, what happens if:• price increases to £50• variable costs fall to £10 per unit• fixed costs increase to £15,000

Unit 1: Planning and financing a business

Financial planning

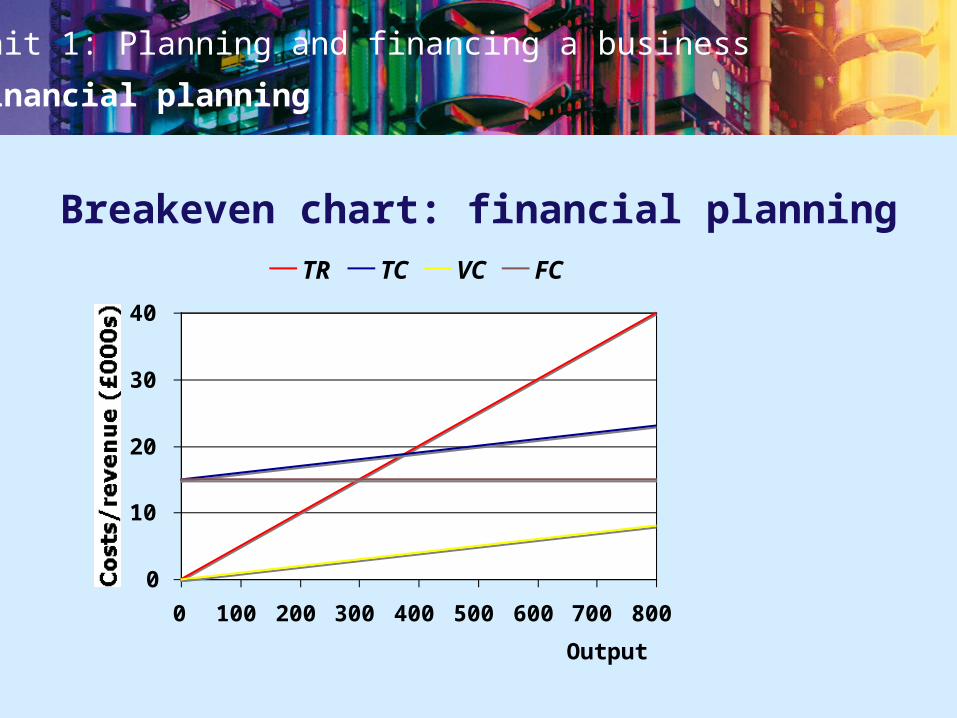

Breakeven chart: financial planning

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue (£000s)

TR TC VC FC

Unit 1: Planning and financing a business

Financial planning

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue (£000s)

TR TC VC FC

Breakeven chart: financial planning

Unit 1: Planning and financing a business

Financial planning

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue (£000s)

TR TC VC FC

Breakeven chart: financial planning

Unit 1: Planning and financing a business

Financial planning

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue (£000s)

TR TC VC FC

Breakeven chart: financial planning

Unit 1: Planning and financing a business

Financial planning

0

10

20

30

40

0 100 200 300 400 500 600 700 800

Output

Costs/revenue (£000s)

TR TC VC FC

Breakeven chart: financial planning

Unit 1: Planning and financing a business

Financial planning

0

10

20

30

40

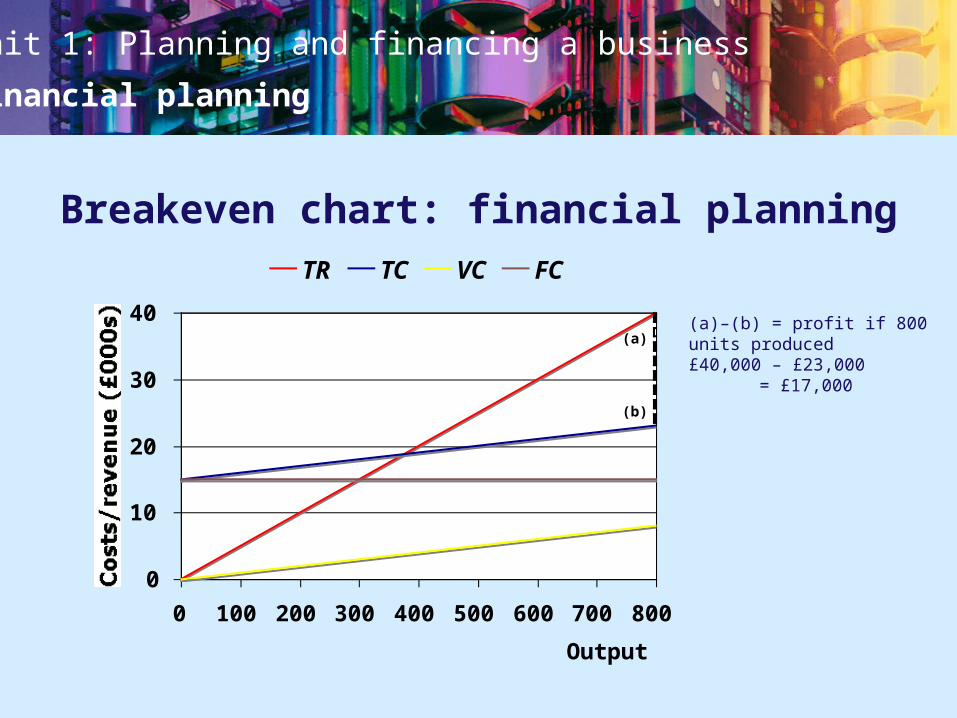

0 100 200 300 400 500 600 700 800

Output

Costs/revenue (£000s)

TR TC VC FC

(a)

(b)

Breakeven chart: financial planning

(a)–(b) = profit if 800units produced £40,000 – £23,000 = £17,000

Unit 1: Planning and financing a business

Financial planning

0

10

20

30

40

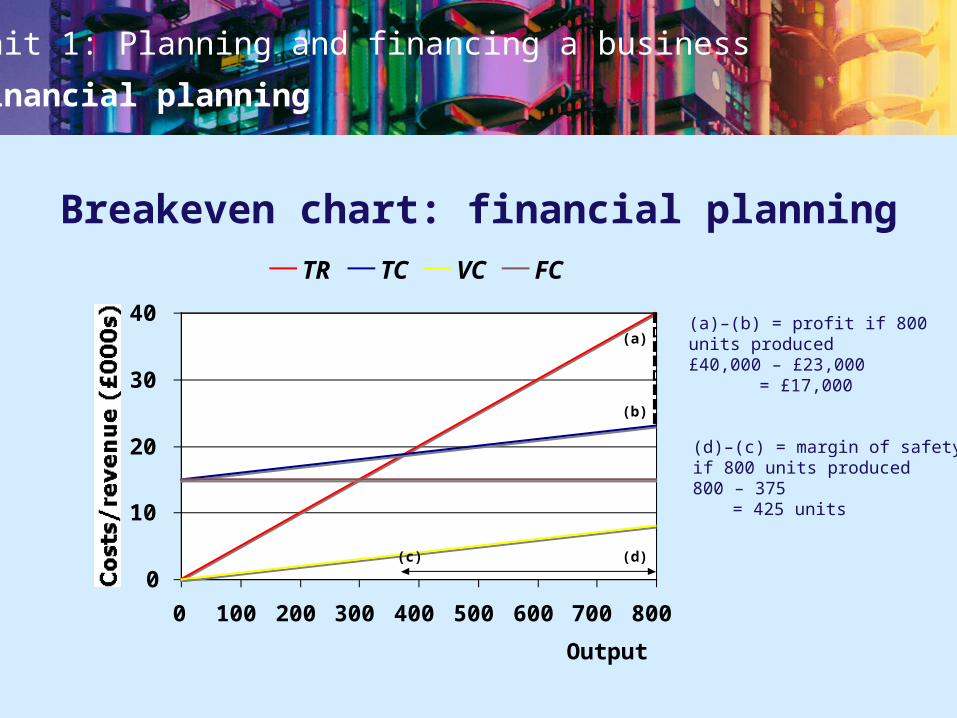

0 100 200 300 400 500 600 700 800

Output

Costs/revenue (£000s)

TR TC VC FC

(a)

(b)

(c) (d)

Breakeven chart: financial planning

(d)–(c) = margin of safetyif 800 units produced800 – 375 = 425 units

(a)–(b) = profit if 800units produced £40,000 – £23,000 = £17,000

Unit 1: Planning and financing a business

Financial planning

0

10

20

30

40

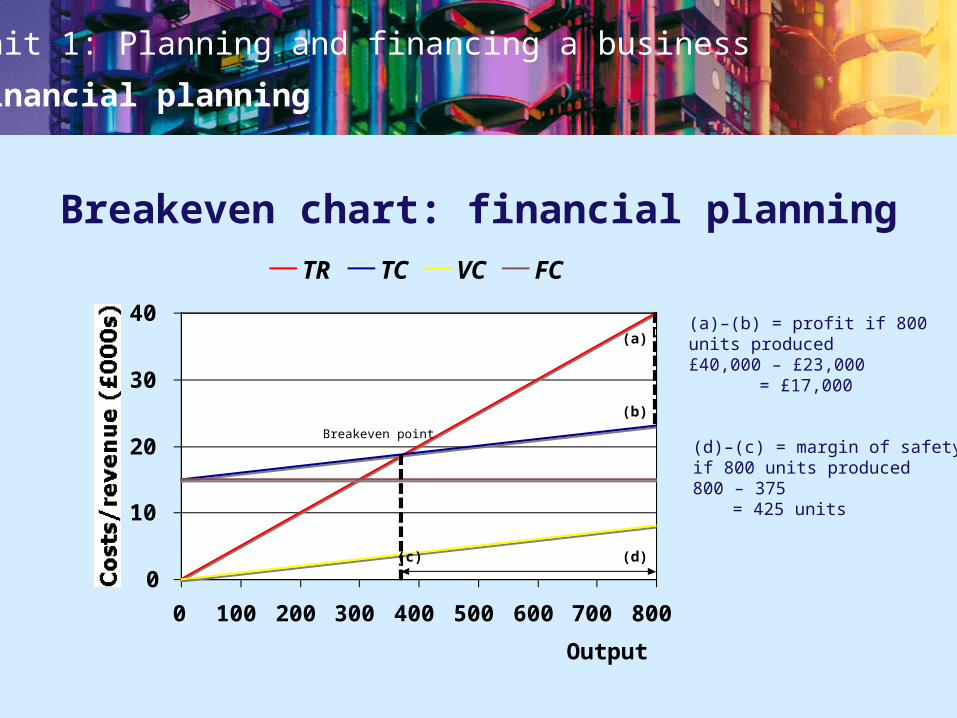

0 100 200 300 400 500 600 700 800

Output

Costs/revenue (£000s)

TR TC VC FC

Breakeven point

(a)

(b)

(c) (d)

(a)–(b) = profit if 800units produced £40,000 – £23,000 = £17,000

Breakeven chart: financial planning

(d)–(c) = margin of safetyif 800 units produced800 – 375 = 425 units

Unit 1: Planning and financing a business

Financial planning

Usefulness of breakeven analysis to start-up businesses

• To calculate how long it will take to reach the level of output needed to make a

profit. This will help it to assess whether the business is viable or not.• To get financial support, such as a bank overdraft.• To assess the probability of success and to gain some idea of the level of risk,

using the margin of safety.• To use ‘what if?’ analysis to show the different breakeven outputs and changes in

levels of profit that might arise from changes in prices, variable costs and fixed

costs.

Unit 1: Planning and financing a business

Financial planning

Strengths of breakeven analysis as a technique

• It is flexible — it can show the different levels of profit arising from various levels

of output.• The calculations are quick and easy to complete, thus saving businesses time. • Businesses that foresee future changes (e.g. higher wage costs or lower prices)

can examine the impact on individual products in their range.• For firms that have a target profit level, breakeven analysis can be adapted

to discover at which point a company can reach a particular profit level

(see the next slide).

Unit 1: Planning and financing a business

Financial planning

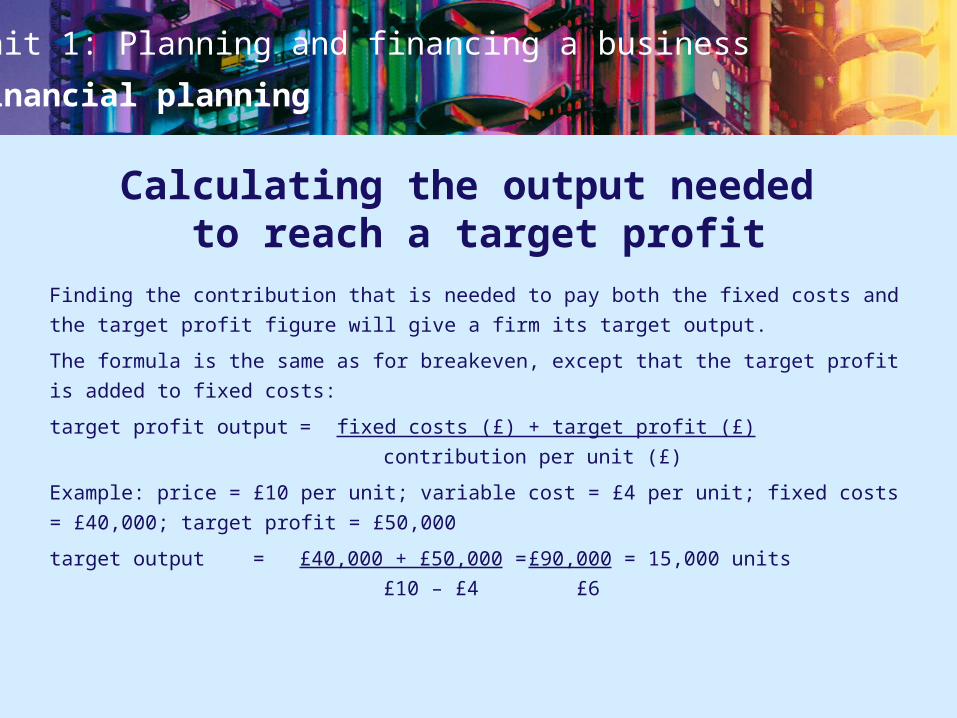

Calculating the output needed to reach a target profit

Finding the contribution that is needed to pay both the fixed costs and the target

profit figure will give a firm its target output.

The formula is the same as for breakeven, except that the target profit is added to

fixed costs:

target profit output = fixed costs (£) + target profit (£)

contribution per unit (£)

Example: price = £10 per unit; variable cost = £4 per unit; fixed costs = £40,000;

target profit = £50,000

target output = £40,000 + £50,000 = £90,000 = 15,000 units

£10 – £4 £6

Unit 1: Planning and financing a business

Financial planning

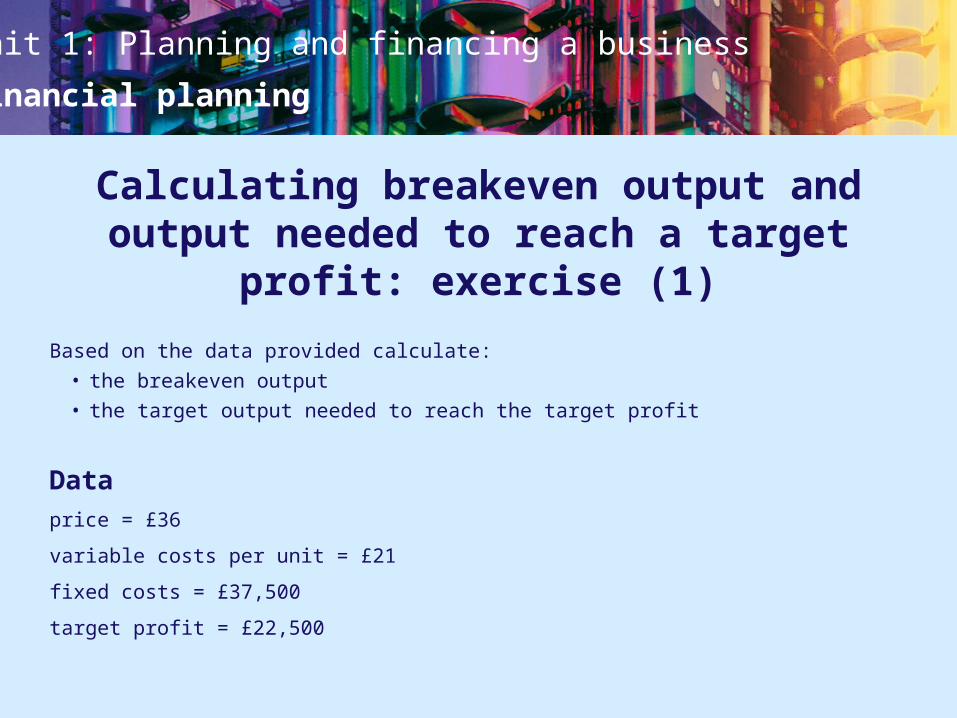

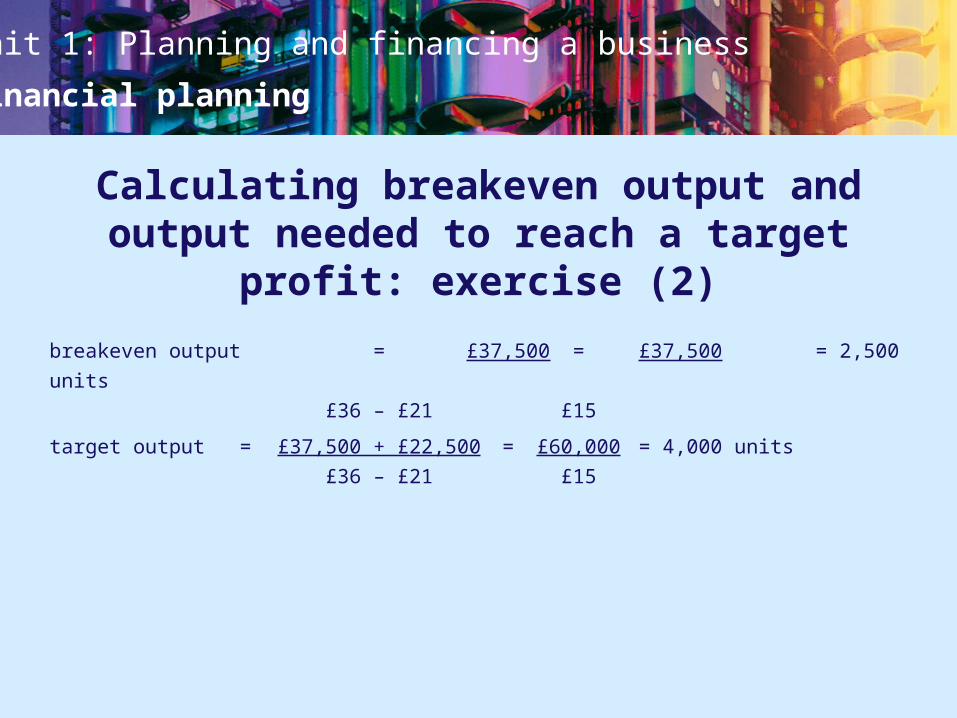

Calculating breakeven output and output needed to reach a target

profit: exercise (1)

Based on the data provided calculate:• the breakeven output• the target output needed to reach the target profit

Dataprice = £36

variable costs per unit = £21

fixed costs = £37,500

target profit = £22,500

Unit 1: Planning and financing a business

Financial planning

Calculating breakeven output and output needed to reach a target

profit: exercise (2)

breakeven output = £37,500 = £37,500 = 2,500 units

£36 – £21 £15

target output = £37,500 + £22,500 = £60,000 = 4,000 units

£36 – £21 £15

Unit 1: Planning and financing a business

Financial planning

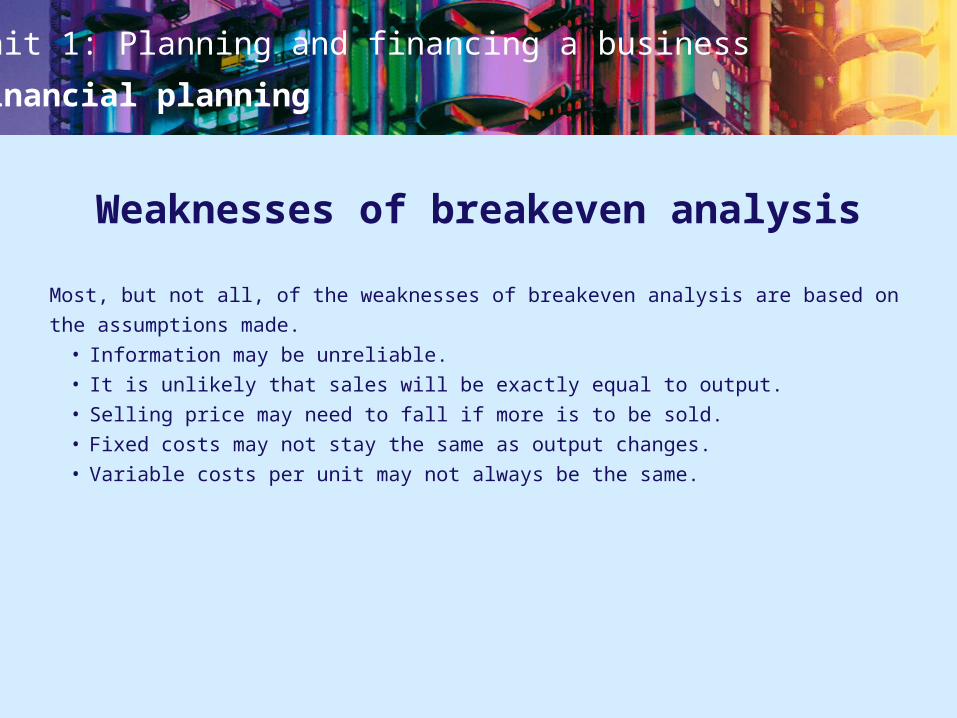

Weaknesses of breakeven analysis

Most, but not all, of the weaknesses of breakeven analysis are based on the

assumptions made.• Information may be unreliable.• It is unlikely that sales will be exactly equal to output.• Selling price may need to fall if more is to be sold. • Fixed costs may not stay the same as output changes. • Variable costs per unit may not always be the same.

Unit 1: Planning and financing a business

Financial planning

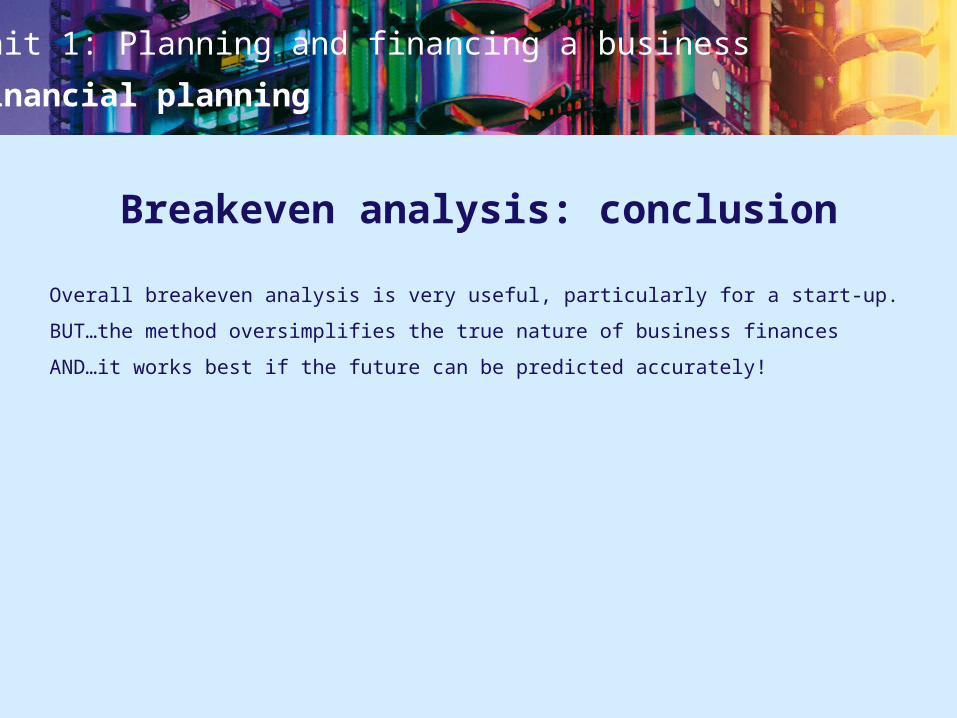

Breakeven analysis: conclusion

Overall breakeven analysis is very useful, particularly for a start-up.

BUT…the method oversimplifies the true nature of business finances

AND…it works best if the future can be predicted accurately!

Unit 1: Planning and financing a business

Financial planning

Chapter 13

Using cash-flow forecasting

Unit 1: Planning and financing a business

Financial planning

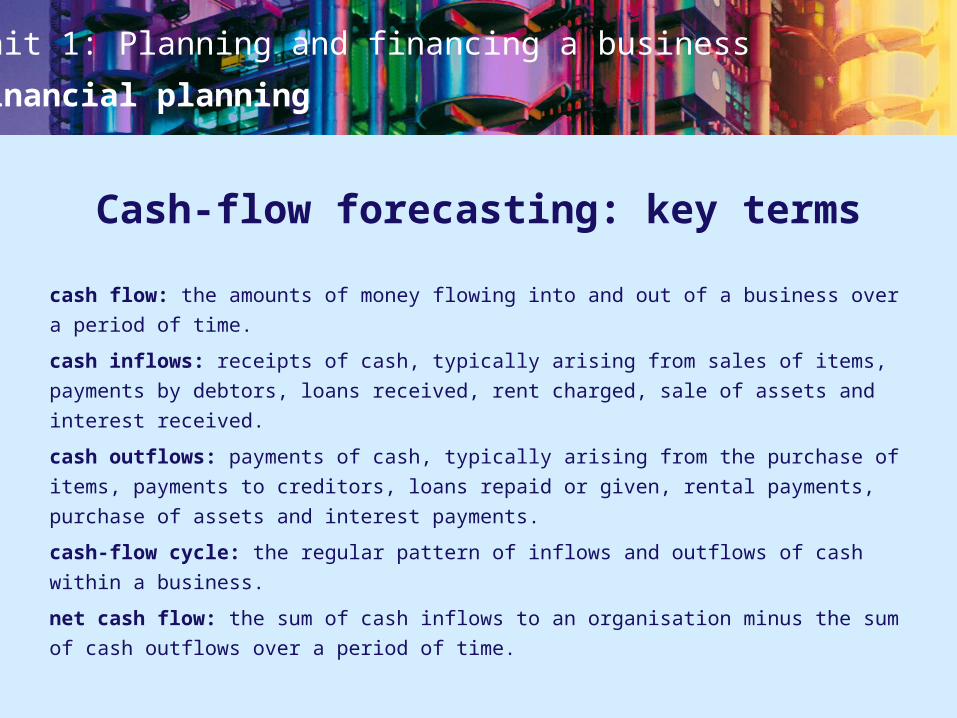

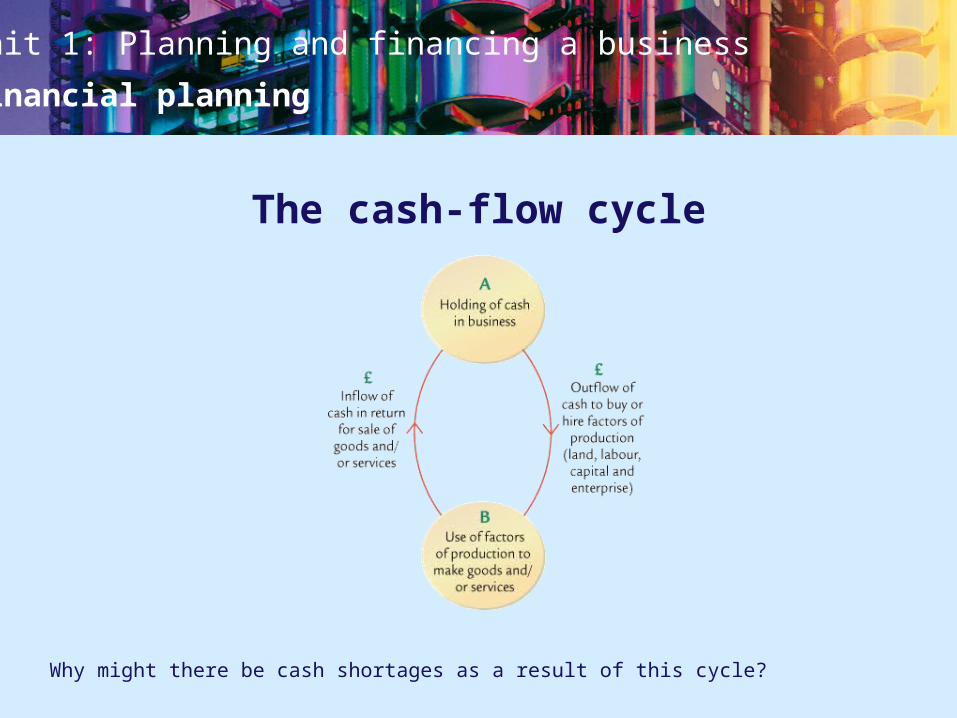

Cash-flow forecasting: key terms

cash flow: the amounts of money flowing into and out of a business over a period of

time.

cash inflows: receipts of cash, typically arising from sales of items, payments by

debtors, loans received, rent charged, sale of assets and interest received.

cash outflows: payments of cash, typically arising from the purchase of items,

payments to creditors, loans repaid or given, rental payments, purchase of assets

and interest payments.

cash-flow cycle: the regular pattern of inflows and outflows of cash within a

business.

net cash flow: the sum of cash inflows to an organisation minus the sum of cash

outflows over a period of time.

Unit 1: Planning and financing a business

Financial planning

The cash-flow cycle

Why might there be cash shortages as a result of this cycle?

Unit 1: Planning and financing a business

Financial planning

Cash-flow forecasts and cash-flow statements

cash-flow forecasting: the process of estimating the expected cash inflows and

cash outflows over a period of time. Cash flow is often seasonal, so it is advisable to

forecast for a period of 1 year.

cash-flow statement: a description of how cash flowed into and out of a business

during a particular period of time.

A cash-flow forecast attempts to predict the future whereas a cash-flow statement

describes what actually happened in the past.

Unit 1: Planning and financing a business

Financial planning

Sources of information for cash-flow forecasts

Where can a business get information from in order to forecast cash flow?

Possible ideas include:• previous cash-flow forecasts• cash-flow statements• consumer research• competitors• contacting potential suppliers for quotes• banks• consultants

Unit 1: Planning and financing a business

Financial planning

Possible causes of inaccuracy in cash-flow forecasts

• changes in levels of consumer spending in the economy• changes in consumer tastes• inaccurate market research• changing levels of competition• unexpected changes in costs

Unit 1: Planning and financing a business

Financial planning

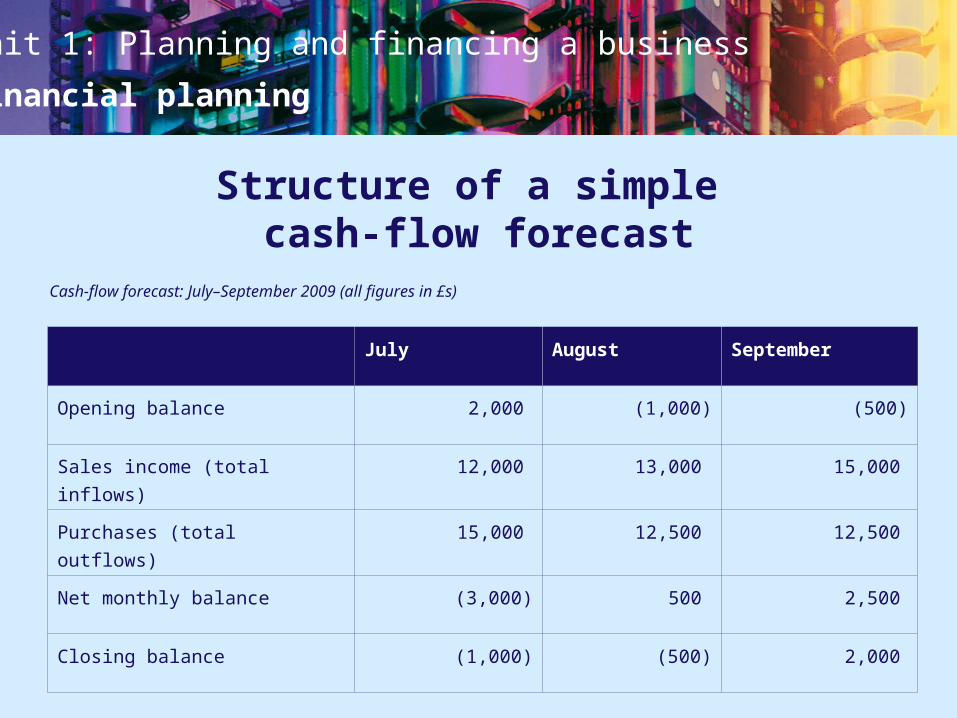

Structure of a simple cash-flow forecast

Cash-flow forecast: July–September 2009 (all figures in £s)

July August September

Opening balance 2,000 (1,000) (500)

Sales income (total inflows) 12,000 13,000 15,000

Purchases (total outflows) 15,000 12,500 12,500

Net monthly balance (3,000) 500 2,500

Closing balance (1,000) (500) 2,000

Unit 1: Planning and financing a business

Financial planning

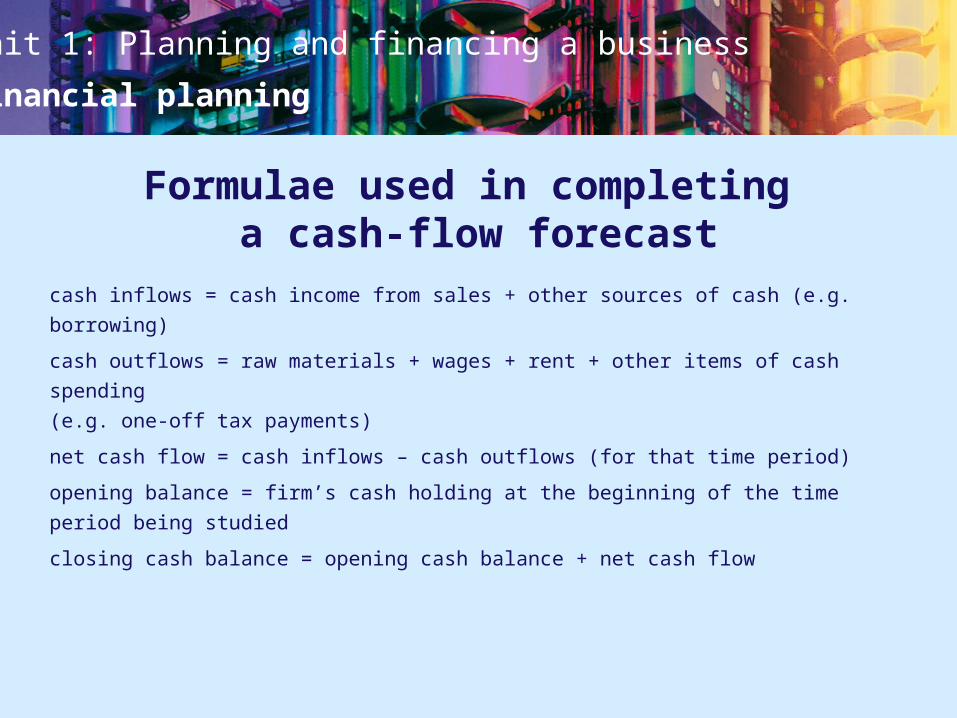

Formulae used in completing a cash-flow forecast

cash inflows = cash income from sales + other sources of cash (e.g. borrowing)

cash outflows = raw materials + wages + rent + other items of cash spending

(e.g. one-off tax payments)

net cash flow = cash inflows – cash outflows (for that time period)

opening balance = firm’s cash holding at the beginning of the time period being

studied

closing cash balance = opening cash balance + net cash flow

Unit 1: Planning and financing a business

Financial planning

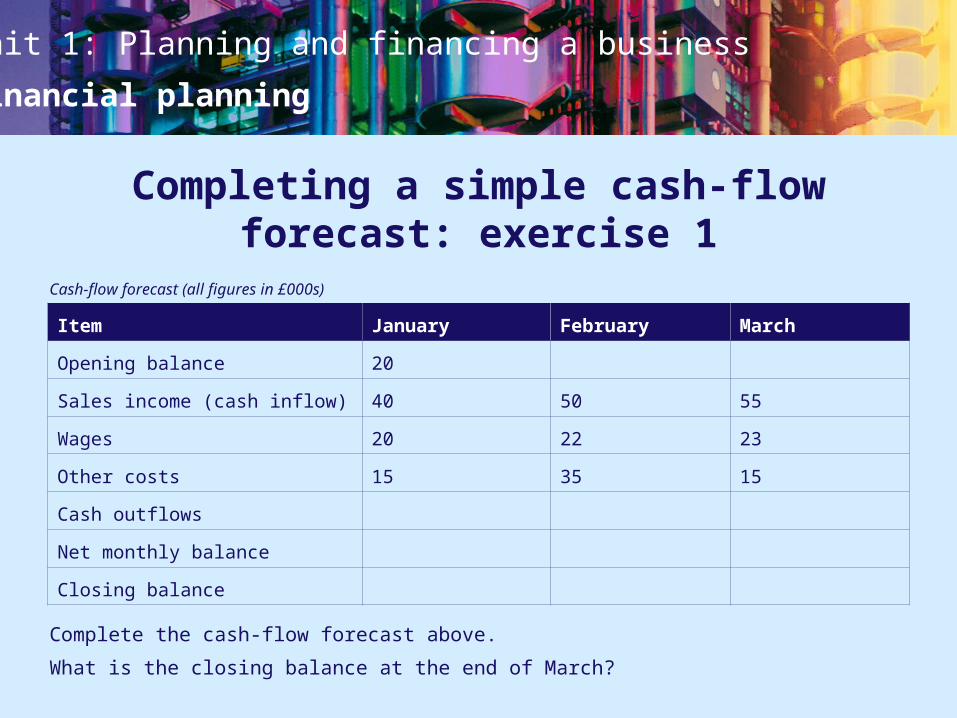

Completing a simple cash-flow forecast: exercise 1

Cash-flow forecast (all figures in £000s)

Complete the cash-flow forecast above.

What is the closing balance at the end of March?

Item January February March

Opening balance 20

Sales income (cash inflow) 40 50 55

Wages 20 22 23

Other costs 15 35 15

Cash outflows

Net monthly balance

Closing balance

Unit 1: Planning and financing a business

Financial planning

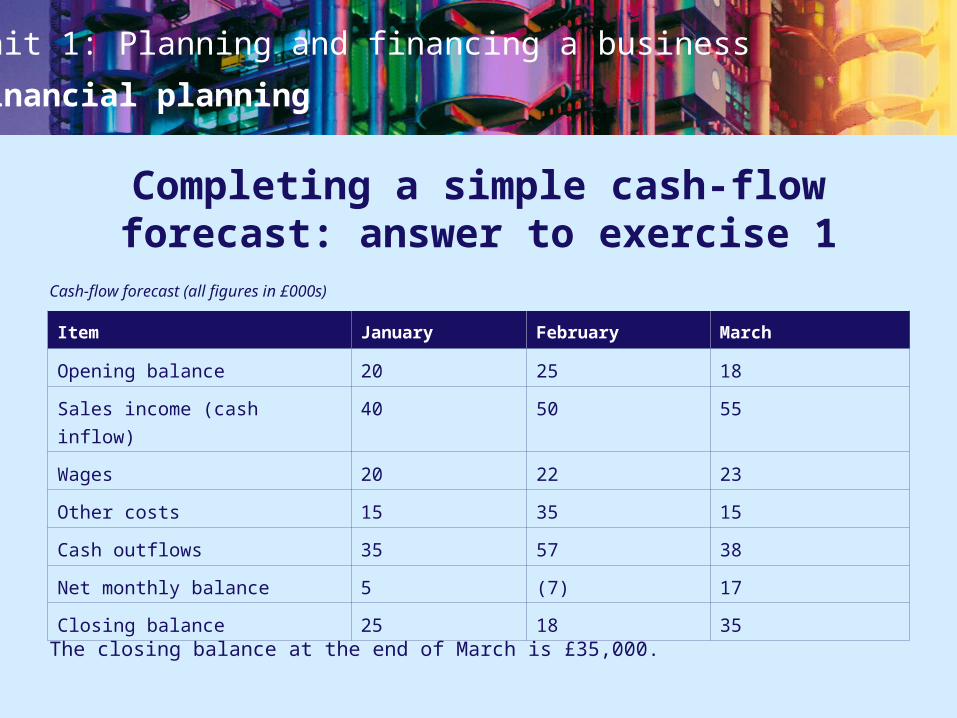

Completing a simple cash-flow forecast: answer to exercise 1

Cash-flow forecast (all figures in £000s)

The closing balance at the end of March is £35,000.

Item January February March

Opening balance 20 25 18

Sales income (cash inflow) 40 50 55

Wages 20 22 23

Other costs 15 35 15

Cash outflows 35 57 38

Net monthly balance 5 (7) 17

Closing balance 25 18 35

Unit 1: Planning and financing a business

Financial planning

Completing a simple cash-flow forecast: exercise 2

Complete the blank cash-flow forecast template on the next slide, based on the

following information: • The opening balance is £4,000.• Sales income is £20,000 in January and increases by 10% per month on the

previous month.• Wages are £3,000 per month.• Raw materials are half the value of sales income each month. • Other costs are £6,000 in January and March but £15,000 in February.

Unit 1: Planning and financing a business

Financial planning

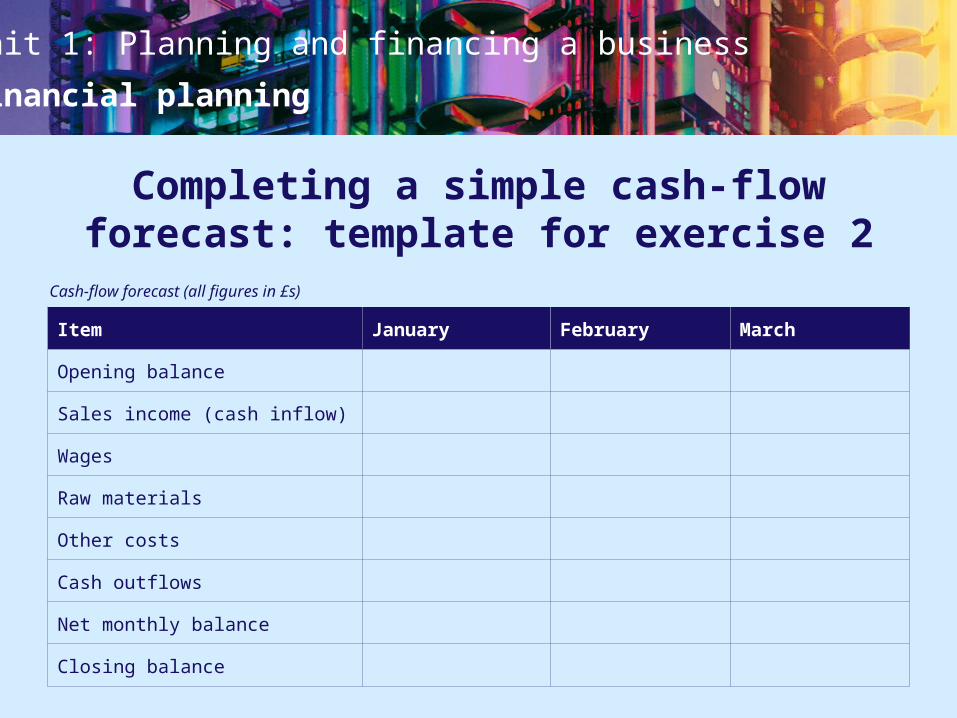

Completing a simple cash-flow forecast: template for exercise 2

Cash-flow forecast (all figures in £s)

Item January February March

Opening balance

Sales income (cash inflow)

Wages

Raw materials

Other costs

Cash outflows

Net monthly balance

Closing balance

Unit 1: Planning and financing a business

Financial planning

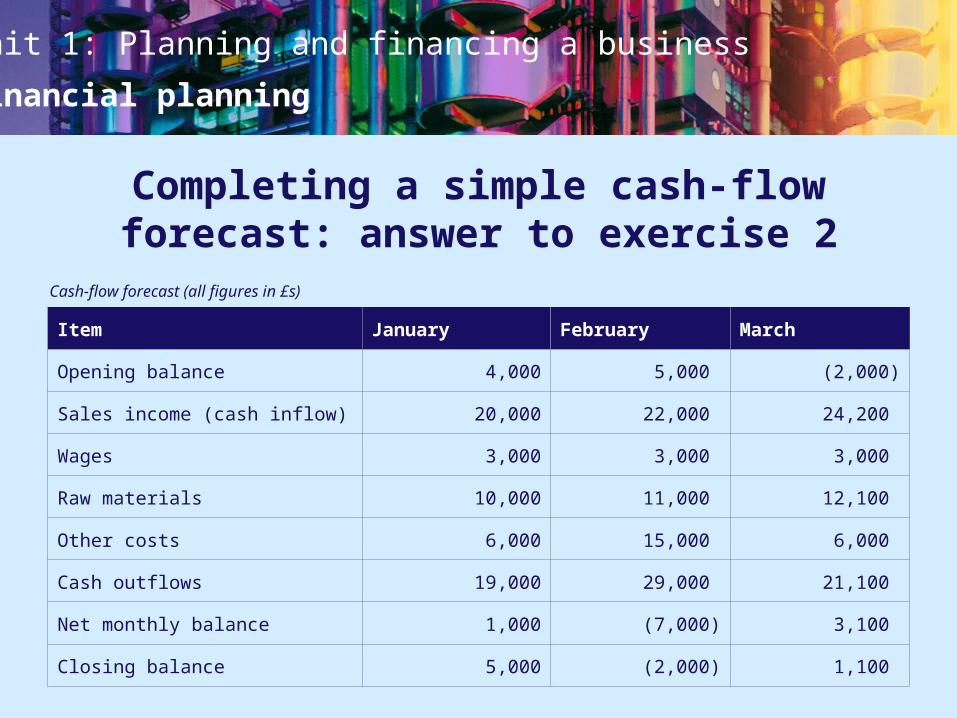

Completing a simple cash-flow forecast: answer to exercise 2

Cash-flow forecast (all figures in £s)

Item January February March

Opening balance 4,000 5,000 (2,000)

Sales income (cash inflow) 20,000 22,000 24,200

Wages 3,000 3,000 3,000

Raw materials 10,000 11,000 12,100

Other costs 6,000 15,000 6,000

Cash outflows 19,000 29,000 21,100

Net monthly balance 1,000 (7,000) 3,100

Closing balance 5,000 (2,000) 1,100

Unit 1: Planning and financing a business

Financial planning

Significance of cash-flow forecasting

Liquidity is the ability to convert an asset into cash without loss or delay.

The most liquid asset that a business can possess is cash. All firms, however

profitable, must manage their cash to guarantee their survival.

The significance of cash-flow forecasts is that they enable a firm to see times

in the future when it may be short of liquidity, so that measures can be taken

to prevent this from happening.

Unit 1: Planning and financing a business

Financial planning

Reasons for cash-flow forecasting

• to identify potential cash-flow problems in advance• to guide the firm towards appropriate action• to make sure that there is sufficient cash available to pay suppliers etc.• to provide evidence in support of a request for financial assistance

(e.g. asking a bank for an overdraft)• to avoid the possibility of the company being forced out of business

(into liquidation)• to identify the possibility of holding too much cash

Unit 1: Planning and financing a business

Financial planning

Using cash-flow forecasting: follow-up exercises

Complete the practice exercises and case study questions at the end of Chapter 13.

Unit 1: Planning and financing a business

Financial planning

Chapter 14

Setting budgets

Unit 1: Planning and financing a business

Financial planning

Budgeting: key terms

budget: an agreed plan establishing, in numerical or financial terms, the policy to

be pursued and the anticipated outcomes of that policy.

Types of budgetincome budget: the agreed, planned income of a business (or division of a

business) over a period of time. It may also be described as a revenue budget or

sales budget.

expenditure budget: the agreed, planned expenditure of a business (or division of

a business) over a period of time.

profit budget: the agreed, planned profit of a business (or division of a business)

over a period of time.

Unit 1: Planning and financing a business

Financial planning

Income budget

Key points:• It links to the marketing targets of the business.• It is subdivided into different elements to allow analysis of different sources —

particularly in multi-product firms.• It helps the business to assess expenditure needs, especially raw materials.• It includes other sources of income, such as rent received.

Unit 1: Planning and financing a business

Financial planning

Expenditure budget

The expenditure budget can be more complex than the income budget, as there are

many different items of expenditure in a business — for example: • raw materials/components• labour costs• marketing expenditure• administration costs• rent• capital costs

Unit 1: Planning and financing a business

Financial planning

Profit budget

profit budget = income budget – expenditure budget

• The profit budget usually has an annual focus to avoid seasonal distortions.• It is important for regular review to assess whether budget targets are being hit.

Unit 1: Planning and financing a business

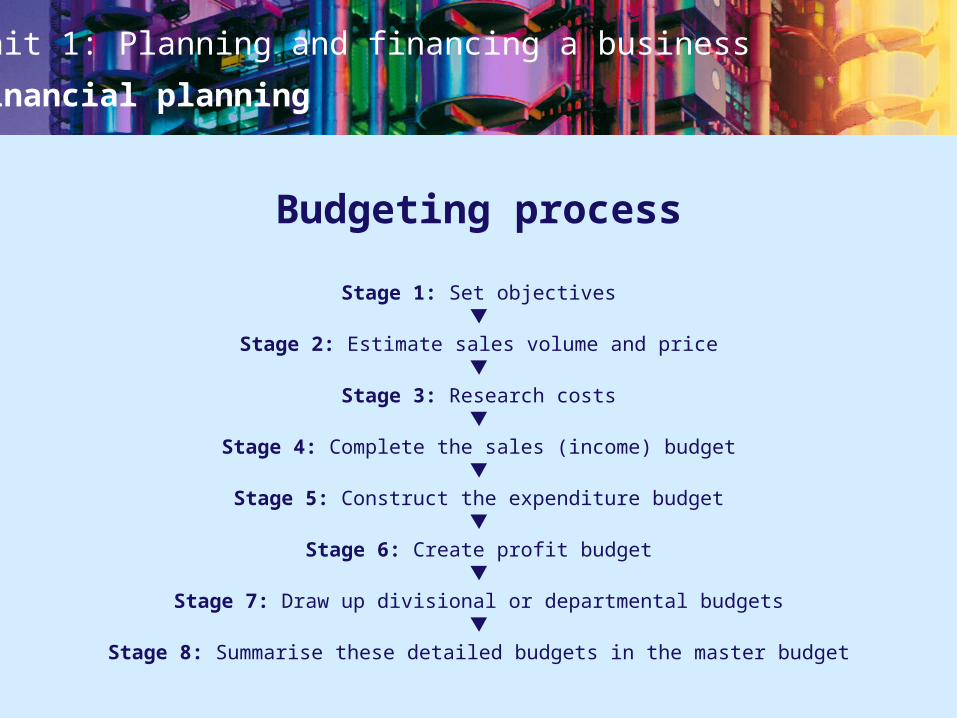

Financial planning

Budgeting process

Stage 1: Set objectives

Stage 2: Estimate sales volume and price

Stage 3: Research costs

Stage 4: Complete the sales (income) budget

Stage 5: Construct the expenditure budget

Stage 6: Create profit budget

Stage 7: Draw up divisional or departmental budgets

Stage 8: Summarise these detailed budgets in the master budget

Unit 1: Planning and financing a business

Financial planning

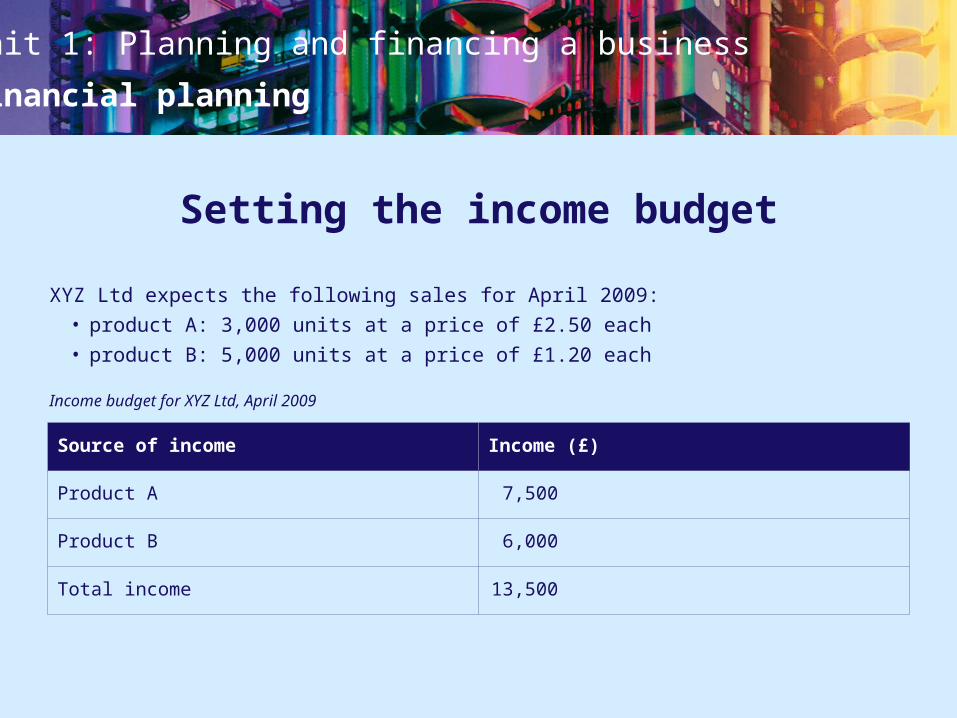

Setting the income budget

XYZ Ltd expects the following sales for April 2009:• product A: 3,000 units at a price of £2.50 each• product B: 5,000 units at a price of £1.20 each

Income budget for XYZ Ltd, April 2009

Source of income Income (£)

Product A 7,500

Product B 6,000

Total income 13,500

Unit 1: Planning and financing a business

Financial planning

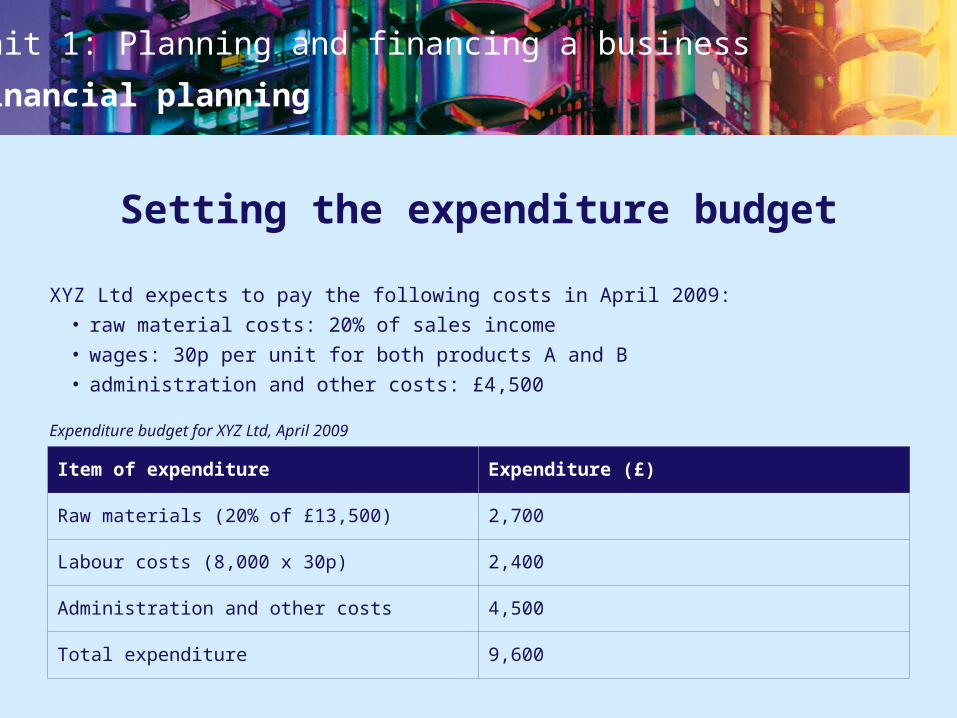

Setting the expenditure budget

XYZ Ltd expects to pay the following costs in April 2009:• raw material costs: 20% of sales income• wages: 30p per unit for both products A and B• administration and other costs: £4,500

Expenditure budget for XYZ Ltd, April 2009

Item of expenditure Expenditure (£)

Raw materials (20% of £13,500) 2,700

Labour costs (8,000 x 30p) 2,400

Administration and other costs 4,500

Total expenditure 9,600

Unit 1: Planning and financing a business

Financial planning

Setting the profit budget

profit = income – expenditure

The profit budget is constructed by taking the income budget and subtracting the

expenditure budget.

Profit budget for XYZ Ltd, April 2009

Item of income/expenditure (£)

Total income 13,500

Total expenditure 9,600

Budgeted profit 3,900

Unit 1: Planning and financing a business

Financial planning

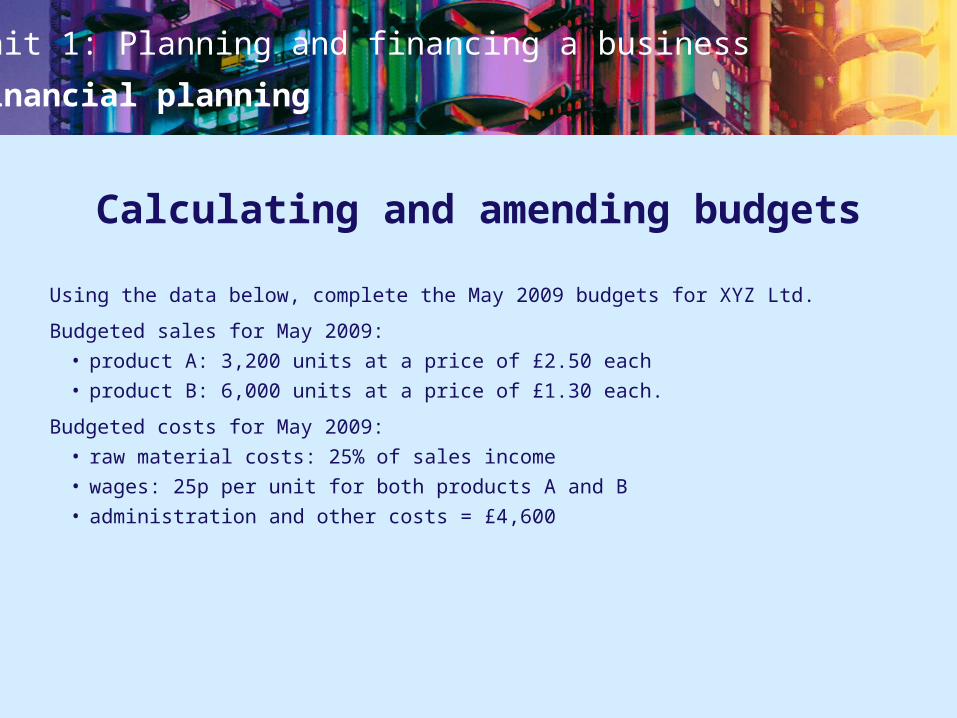

Calculating and amending budgets

Using the data below, complete the May 2009 budgets for XYZ Ltd.

Budgeted sales for May 2009:• product A: 3,200 units at a price of £2.50 each• product B: 6,000 units at a price of £1.30 each.

Budgeted costs for May 2009:• raw material costs: 25% of sales income• wages: 25p per unit for both products A and B• administration and other costs = £4,600

Unit 1: Planning and financing a business

Financial planning

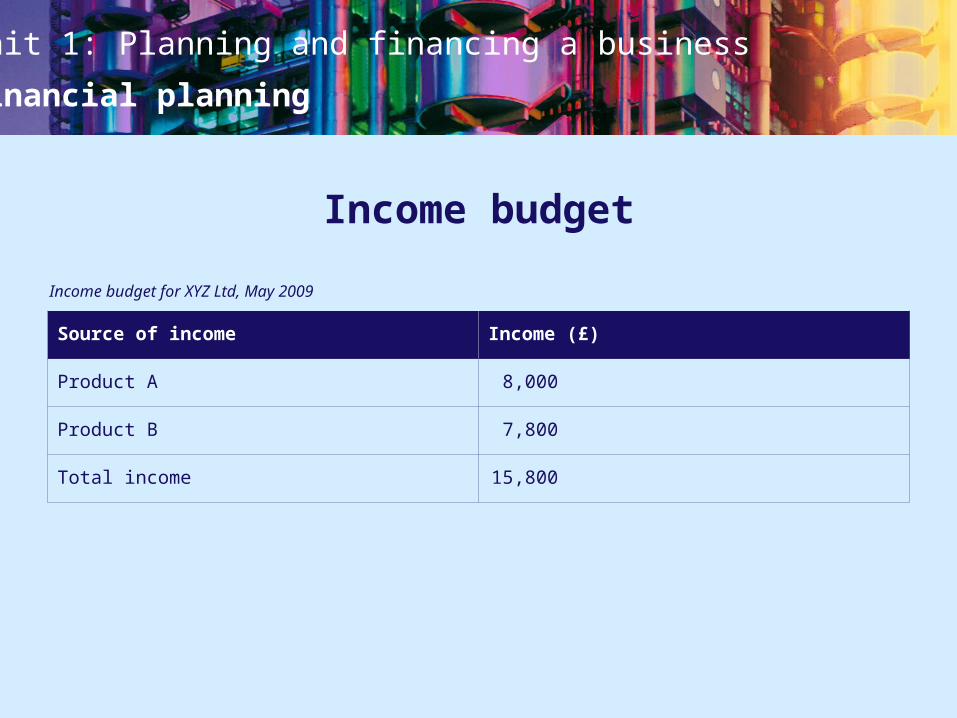

Income budget

Income budget for XYZ Ltd, May 2009

Source of income Income (£)

Product A 8,000

Product B 7,800

Total income 15,800

Unit 1: Planning and financing a business

Financial planning

Expenditure budget

Expenditure budget for XYZ Ltd, May 2009

Item of expenditure Expenditure (£)

Raw materials (25% of £15,800) 3,950

Labour costs (9,200 x 25p) 2,300

Administration and other costs 4,600

Total expenditure 10,850

Unit 1: Planning and financing a business

Financial planning

Item of income/expenditure (£)

Total income 15,800

Total expenditure 10,850

Budgeted profit 4,950

Profit budget

Profit budget for XYZ Ltd, May 2009

Unit 1: Planning and financing a business

Financial planning

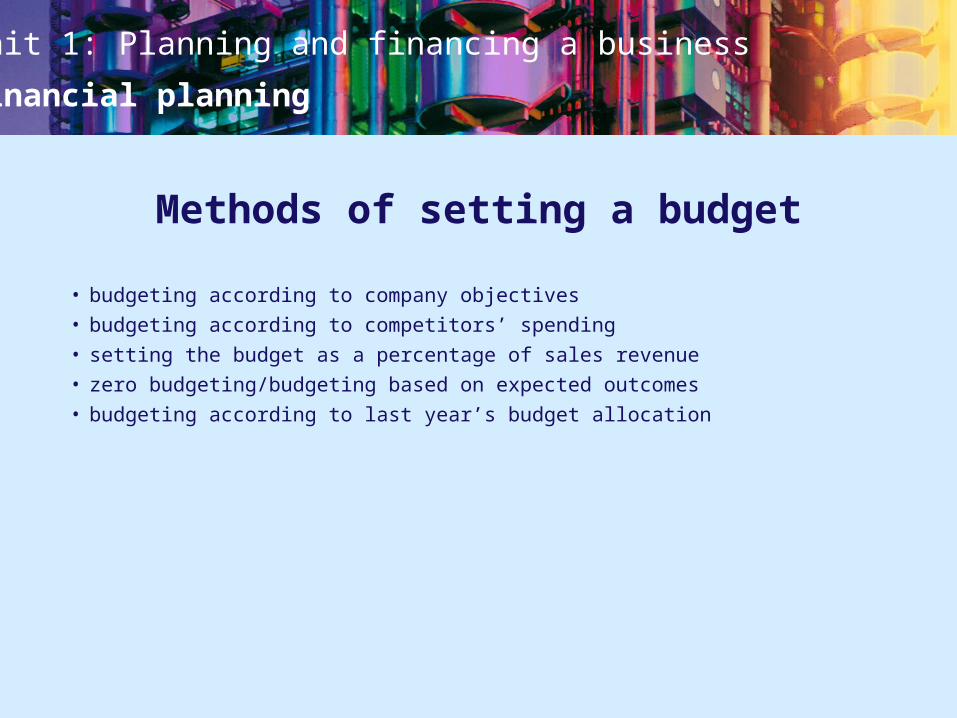

Methods of setting a budget

• budgeting according to company objectives• budgeting according to competitors’ spending• setting the budget as a percentage of sales revenue• zero budgeting/budgeting based on expected outcomes • budgeting according to last year’s budget allocation

Unit 1: Planning and financing a business

Financial planning

Reasons for setting budgets

• to gain financial support• to ensure that a business does not overspend• to establish priorities• to encourage delegation and responsibility, and to motivate staff• to assign responsibility• to improve efficiency

Unit 1: Planning and financing a business

Financial planning

Problems of setting budgets

• managers not knowing enough about the division or department• difficulties in gathering information• unforeseen changes• changes in prices that are difficult to foresee• problems arising from budgets being imposed • the time taken in setting budgets

Unit 1: Planning and financing a business

Financial planning

Setting budgets: follow-up exercises

Complete practice exercise 2 and the case study questions from Chapter 14.

Unit 1: Planning and financing a business

Financial planning

Chapter 15

Assessing business start-ups

Unit 1: Planning and financing a business

Financial planning

Assessing the business idea or plan

Possible issues to consider include:• what the business objectives are• which product or service is to be provided and whether it can be produced and

supplied profitably• customers’ needs and wants, and which market segment to target• the possibility of competition and an appropriate pricing and selling strategy• finance for day-to-day and longer-term operations, and the time scales between

start-up and breakeven• who will be involved, what they will be doing and what skills, expertise and

experience they have• the risks involved

Unit 1: Planning and financing a business

Financial planning

Refer to the Tribal Woods case study on page 165 of the textbook and discuss the

following questions: • Is there anything special, new or different about the Bill’s products that would

make them appeal to consumers? • Could the products compete successfully with other products on the market?

Assessing the business start-up: exercise

Unit 1: Planning and financing a business

Financial planning

Common reasons for business failure

• poor cash-flow management• lack of effective market research• lack of effective planning• lack of skills needed to run a

business and lack of business

training• problems in coordinating all the

different aspects of the business

• failure to turn what looks like a

good idea into a profitable business• lack of finance to fund the business• the actions of bigger competitors• difficulties in developing a solid

customer base• difficulties in acquiring affordable

premises

In addition, business failure can result from:• unexpected changes in demand for the product or service• unexpected changes in costs• delays and unavailability of supplies

Unit 1: Planning and financing a business

Financial planning

Working in groups, take one of the following areas: finance, marketing, operations,

personnel, external factors. Investigate the main problems that might occur in your

allocated area for a business start-up in relation to this area and, in particular, why

such problems might lead to the failure of the business. Share your findings with the

rest of the class and assess how interrelated the problems are.

Investigating problems of business start-ups

Unit 1: Planning and financing a business

Financial planning

Financial difficulties

Raising financeOver a quarter of all start-up businesses in the government’s Annual Small Business

Survey said they experienced difficulty in obtaining the finance they needed. Discuss

the likely impact of this on a new business.

Cash flowIn the government’s Annual Small Business Survey, nearly 30% of all businesses

thought late payment was a factor that might cause cash-flow problems. Discuss why

this might be the case.

Why do even profitable firms sometimes find it impossible to continue trading

because they are unable to meet their current debts?

Unit 1: Planning and financing a business

Financial planning

Competition

The success of a business start-up will be determined by its ability to attract and

retain its customers. To do this it will have to offer something more than any of its

competitors. In the government’s Annual Small Business Survey, over 40% of all

businesses thought competition in the market was an obstacle to their success —

especially larger competitors with more influence and resources.

Working in groups, take any type of product or service and explore how a new, small,

local firm could compete successfully with an established, large, national firm. Share

your findings with the class.

Unit 1: Planning and financing a business

Financial planning

Difficulties of building a customer base

Satisfied customers are likely to recommend the business to others; such

recommendation is the most effective but least expensive form of advertising.

Factors to consider when trying to encourage customer loyalty include:• providing customers with service that is efficient and meets their expectations • providing a good after-sales service and dealing effectively and positively with

customer complaints • understanding customers’ buying habits and ensuring that stock and staff

availability are in tune with this• ensuring that contact between customers and staff is always friendly and

efficient

Working in groups, develop each of the above points by providing a business

example that illustrates the impact on a business if it fails to ensure these factors are

present in the service it offer to customers.

Unit 1: Planning and financing a business

Financial planning

Regulations and ‘red tape’

A business must meet legal requirements relating to employment, health and safety,

consumer protection and environmental protection as well as the requirements

relating to taxation and other financial issues.

Much of this is very complex to comply with and costly, both financially and in terms

of time.

New legislation on age discrimination, which came into force in October 2007, adds

another layer of red tape for small firms to deal with. Why do you think that this

legislation might cause problems for a small business?