Embed Size (px)

Citation preview

UNIT 1 - FINANCE

AQA GCSE Business Studies

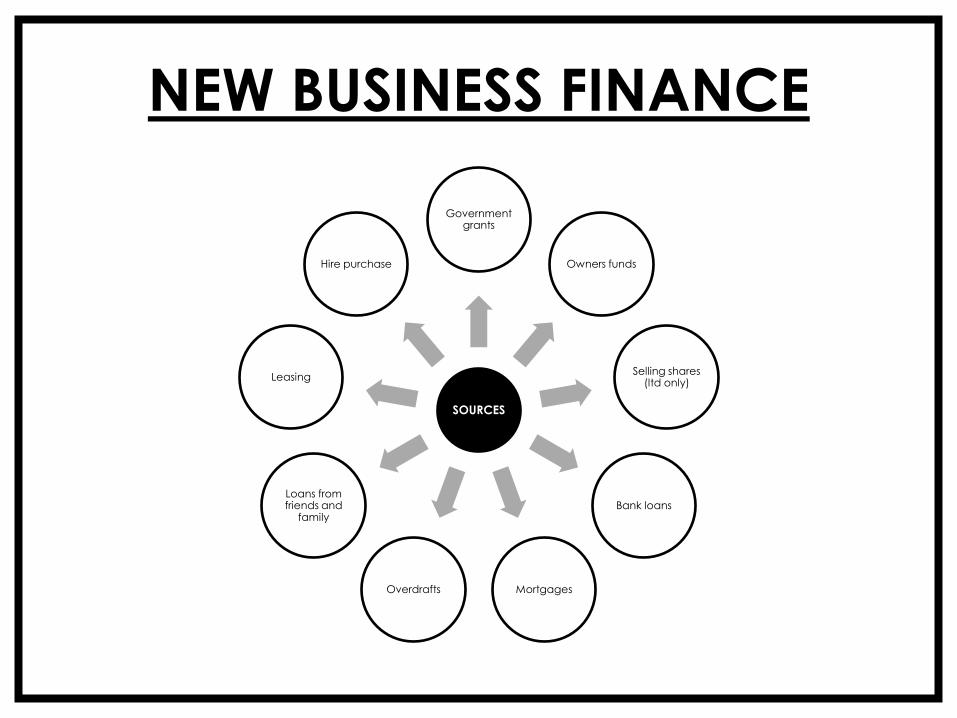

NEW BUSINESS FINANCE

SOURCES

Government grants

Owners funds

Selling shares (ltd only)

Bank loans

Mortgages Overdrafts

Loans from friends and

family

Leasing

Hire purchase

BANK LOAN

Bank agrees to lend a set sum of money

for an agreed period of time. In return

the bank will charge interest. The Halifax

charge 5.9% interest on a £10,000 loan

paid back over 5 years. The total loan

repayable would be £11,500, the bank

making £1,500 in interest.

ADVANTAGES DISADVANTAGES

Good for budgeting – payments

spread over loan term.

Expensive – interest must be paid

on the amount borrowed.

Quick – application process is

usually short

May not get approval – if have no

history of borrowing finance

SELLING SHARES (LTD)

Private individuals (friends and

family) are invited to become

part owners in the business.

They will purchase a specific

amount of shares in the business.

ADVANTAGES DISADVANTAGES

Permanent – does not have to be

repaid.

May lose control – if do not own

majority of the shares (51%).

Cheap – no interest charges. Less profits – dividends (% of profits)

may need to be paid to new

shareholders.

LEASING

ADVANTAGES DISADVANTAGES

Asset maintained by leasing

company – reduces maintenance

costs.

Never own the asset – belongs to

the finance company.

Have up-to-date equipment – can

be exchanged when newer

equipment become available.

Payments are high – include profits

for the finance company.

This allows a business to rent

assets such as vehicles,

computers and photocopiers

etc over a set period of time

e.g. 3 years.

LOAN FROM FRIENDS/FAMILY

ADVANTAGES DISADVANTAGES

Easy and quick to arrange – simple

bank transfer.

Lead to arguments – if loan is paid

back slowly or if no payments are

made at all.

Cheap – often lent free of interest

payments.

Confusion over control - may feel

that they are now part owners and

have the right to make decisions.

Family/friends agree to lend

a fixed sum of money.

MORTGAGES

ADVANTAGES DISADVANTAGES

Allows a business to purchase

expensive assets such as land and

buildings.

Bank can repossess asset – if loan

repayment are not paid.

Good for budgeting – payments

spread over loan term.

Interest must be paid – if mortgage

is taken over a long-term period i.e.

30 years, this will be costly.

Loans from banks that are used to

buy land and buildings. They are

normally very long-term loans of up to 30 years. The business will have to

make regular monthly payments until

the money and any interest is repaid.

GOVERNMENT GRANTS

ADVANTAGES DISADVANTAGES

Does not have to be repaid – no

accumulation of debt.

Can be difficult to obtain – business

has to meet a number of

conditions.

Cheap – no interest payments. Process is time consuming – lots of

forms have to be completed and

possibly an interview,

A grant is a sum of money given to an

entrepreneur or a business for a

specific reason. Grants from the UK

government are usually given if a

business creates jobs. Usually the

business has to put in a sum of money

equal to the government grant.

OVERDRAFTS

ADVANTAGES DISADVANTAGES

Flexible – can use overdraft facility

when it is needed.

Expensive - interest rates can be

high.

Interest is only paid on the amount

overdrawn.

Not permanent - bank can ask for

the overdraft to be repaid at very

short notice.

Overdrafts are flexible loans as

businesses only use them when

required. Bank will allow a business

to spend more than what they

have in their business account to

an agreed limit.

OWNERS FUNDS

ADVANTAGES DISADVANTAGES

Quick – no application process to

go through.

Not appropriate – may not have

enough savings to contribute.

Cheap – no interest payments. Risk – may lose savings if business

fails.

The owner(s) of a new

business may use their own

savings to invest in the

business.

WHAT IS CASH FLOW?

Is the money that

flows into and

out of a business

on a day-to-day

basis.

CASH INFLOW Money that becomes available to a

business:

• Income from sales

• Loans from banks

• Owners savings

CASH OUTFLOW Payments made by a business causes

an outflow of cash:

• Buying raw materials

• Wages

• Interest on loans

• Electricity and gas

CASH FLOW DOCUMENTS

CASH FLOW FORECAST

A plan of the expected inflows and

outflows to and from a business over a

period of time.

CASH FLOW STATEMENT

A historical record of the cash inflows

and outflows that have taken place

over a period of time.

IMPORTANCE

REASON 1 Cash flow forecasts help

entrepreneurs:

• Identify times when the

business might be short of

cash.

REASON 2 Cash flow forecasts help

entrepreneurs:

• Take action to avoid

cash shortages

becoming a major

problem.

CONSEQUENCES

INSOLVENCY If a business does not

have enough cash to pay

its bills it cannot trade. It is

said to be insolvent.

RECEIVERSHIP A business will go into

receivership when this

happens. A ‘receiver’

will be appointed to

administer the business.

They will try and sell the

business as a going

concern or close the

business down and sell its

assets.

CASH FLOW FORECAST Peter and Sue’s cash flow forecast

December January February

Cash inflows

Peter and Sue’s savings £5,000

Bank loan £7,500

Sales revenue from Sue’s £3,800 £6,000 £8,800

Total cash inflows (A) £16,300 £6,000 £8,800

Cash outflows

Purchases of stocks of food and drink £8,000 £4,250 £3,900

Wages £4,000 £3,500 £3,700

Interest on bank loan £250 £250 £250

Rent (3 months) £4,250 - -

Electricity and gas £250 £220 £210

Total cash outflow (B) £16,750 £8,220 £8,060

Net cash flow (C = A - B) (£450) (£2,220) £740

Opening balance (D) £1,000 £550 (£1,670)

Closing balance (E = D + C) £550 (£1,670) (£930)

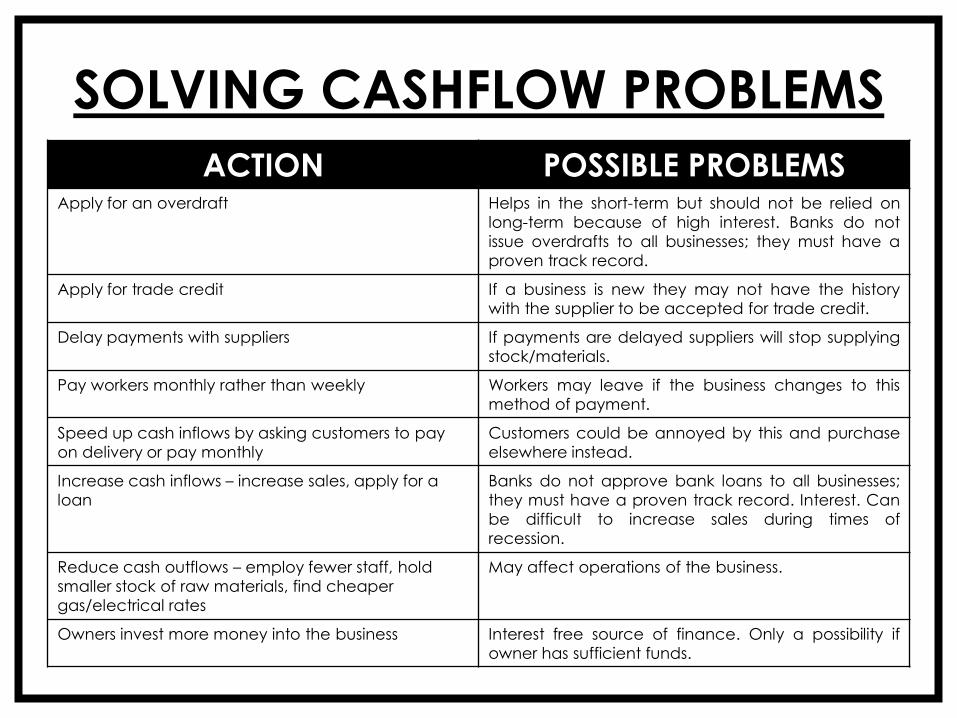

SOLVING CASHFLOW PROBLEMS

ACTION POSSIBLE PROBLEMS Apply for an overdraft

Helps in the short-term but should not be relied on

long-term because of high interest. Banks do not

issue overdrafts to all businesses; they must have a

proven track record.

Apply for trade credit If a business is new they may not have the history

with the supplier to be accepted for trade credit.

Delay payments with suppliers If payments are delayed suppliers will stop supplying

stock/materials.

Pay workers monthly rather than weekly Workers may leave if the business changes to this

method of payment.

Speed up cash inflows by asking customers to pay

on delivery or pay monthly

Customers could be annoyed by this and purchase

elsewhere instead.

Increase cash inflows – increase sales, apply for a

loan

Banks do not approve bank loans to all businesses;

they must have a proven track record. Interest. Can

be difficult to increase sales during times of

recession.

Reduce cash outflows – employ fewer staff, hold

smaller stock of raw materials, find cheaper

gas/electrical rates

May affect operations of the business.

Owners invest more money into the business Interest free source of finance. Only a possibility if

owner has sufficient funds.

PRICE

DEFINITION Price is the amount a

business asks a

customer to pay for a single product. When

you go into a shop,

most items for sale

have a price attached

so you know how much

you have to pay.

WHAT PRICE? A business must consider the

following:

• What competitors are charging

• How much is costs to produce

the good/service that the

business sells

• Popularity of good/service –

high price

• Amount of stock left – low price

(sales)

• What customers can afford

and are willing to pay

SALES

DEFINITION

Number of

products sold by

a business over

some time

period, normally

a week, a month

or year.

EXAMPLE

A dressmaker

sells 12 dresses a

month.

SALES

Revenue

=

selling price x number of products sold

Is the income that a business receives

from selling its goods or services.

EXAMPLE

A dressmaker sells dresses at a standard price of

£110. If the business sells 12 dresses a month, the

monthly revenue will be £1,320.

£110 x 12 = £1,320

REVENUE

Revenue

=

selling price x number of products sold

Is the income that a business receives

from selling its goods or services.

EXAMPLE

A dressmaker sells dresses at a standard price of

£110. If the business sells 12 dresses a month, the

monthly revenue will be £1,320.

£110 x 12 = £1,320

COSTS

FIXED COSTS Fixed costs do not change

when a business changes its

output (how much it

produces).

VARIABLE COST Variable costs vary directly

with the business’s level of

output and sales.

EXAMPLES

Management Salaries

Insurance

Rent

EXAMPLES

Factory Labour

Raw Materials

Packaging

Total cost = Fixed cost + Variable cost

OTHER COSTS

START-UP COSTS One off costs when

starting a business.

RUNNING COSTS Are expenses that a

business has to pay

regularly as a normal

part of trading.

EXAMPLES Rent

Raw materials

Wages

Business taxes

EXAMPLES Buildings

Machinery and equipment

Market research

CALCULATING PROFIT

Sales – the number of

products sold

Price – what customers

pay

Revenue – the

businesses income

x

Total costs – fixed costs

and variable costs

Profits (or losses)

gives

minus

gives

CALCULATING PROFIT EXAMPLE

Sales

10,000 pens

Price

£1 per pen

Revenue

£10,000

x

Total costs

£5,000

Profits

£5,000

gives

minus

gives

FINANCE ADVICE

SOURCE OF

ADVICE

EXPLANATION

Business Link Organisation run by the government that operates in all

parts of the UK. Has 445 branches. Helps new and existing

business. Offers advise and support.

Private Websites Smallbusines.co.uk best known private website. Sponsored

by Lloyds TSB. Offers advise on starting a business, finance,

marketing, employing people and the law for small

businesses.

Banks • Help with writing business plans

• How to find suitable buildings for the business

• The issues involved in employing people

• How

Accountants Give support in financial matters such as borrowing money

and paying taxes.

Solicitor Offer help with legal matters such as setting up a private

limited company or signing a franchise agreement.