Embed Size (px)

Citation preview

UNION PACIFIC CORPORATIONOCTOBER 24, 2013Alex Johansson, Dan Kleeman & Qianwen Wu

Agenda

Introduction Macroeconomic Outlook Industry Overview Company Overview Earnings Report Financial Analysis Valuation Recommendation

Macroeconomic Outlook

Increasing Growth of Shale Sands Emerging Market in South Inbound – Frac Sand &

Pipe Outbound – Crude Oil

Increasing U.S. Population Base Stimulate Long-Term

Growth

Source: 2012 10-K (Pg. 2)

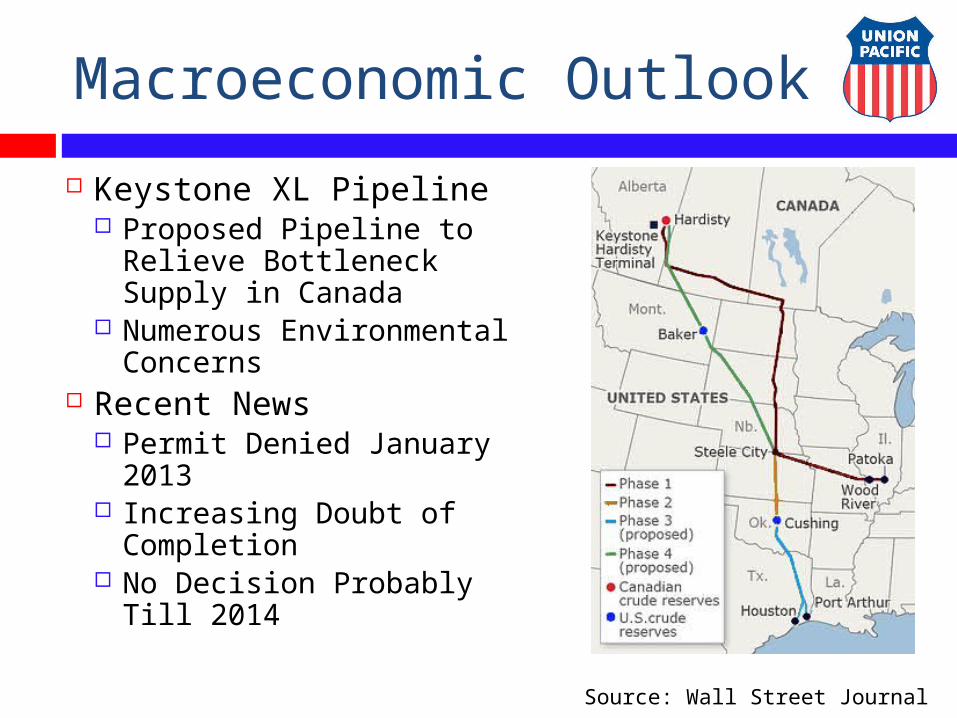

Macroeconomic Outlook

Keystone XL Pipeline Proposed Pipeline to

Relieve Bottleneck Supply in Canada

Numerous Environmental Concerns

Recent News Permit Denied January

2013 Increasing Doubt of

Completion No Decision Probably Till

2014

Source: Wall Street Journal

Macroeconomic Outlook

Industry Catalysts Automotive

Largest Automotive Carrier West of the Mississippi

Chemical – Shale Commodity Group Emerging Market – Offsets Decreased Coal

GrowthCoal

Coal Made Up 20% of 2012 Revenues Decreased Growth Domestically – EPA &

President Obama Proposals Indirect Growth Relationship w/Natural Gas Prices Decreased Growth In Imports To China We Proposed Minimal Growth In Our Model

Source: Wall Street Journal, 2012 10-K (Pg. 5 &23)

Industry Forces Analysis

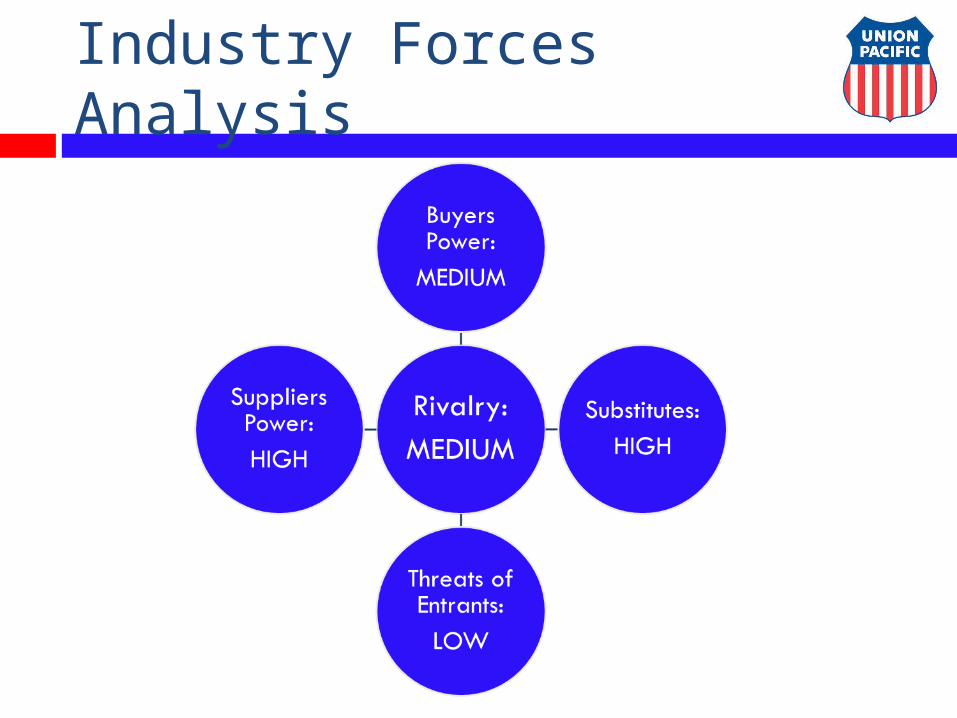

Industry Forces Analysis

Threat of Substitutes: High Other Alternatives Include Transportation Via:

River Barge, Trucking & Pipeline (Keystone XL)

Bargaining Power of Buyers: Medium Few Competitors Many Alternatives

Threat of New Entrants: Low Very Capital Intensive High Barriers of

Entrance Geographic specificity

Industry Forces Analysis

Bargaining Power of Suppliers: High Very Little Pricing Power Over Fuel Few Suppliers of Trains and Rail Supplies

Switching Cost May Be High

Rivalry among Competitors: Medium Limited Amount of Competitors Specific to Service & Geographic Region

Comparison between Dow Jones Railroad Index and S&P 500

Source: Google Finance

Company Overview

Source: Union Pacific Website

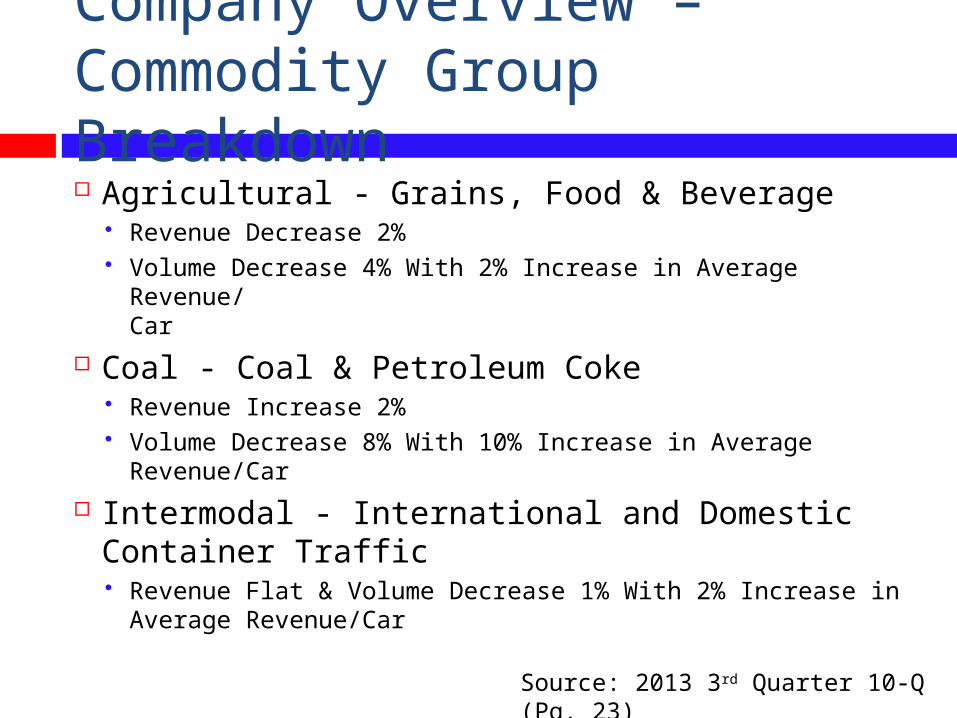

Company Overview – Commodity Group Breakdown Agricultural - Grains, Food & Beverage

Revenue Decrease 2% Volume Decrease 4% With 2% Increase in Average Revenue/

Car

Coal - Coal & Petroleum Coke Revenue Increase 2% Volume Decrease 8% With 10% Increase in Average

Revenue/Car

Intermodal - International and Domestic Container Traffic Revenue Flat & Volume Decrease 1% With 2% Increase in

Average Revenue/Car

Source: 2013 3rd Quarter 10-Q (Pg. 23)

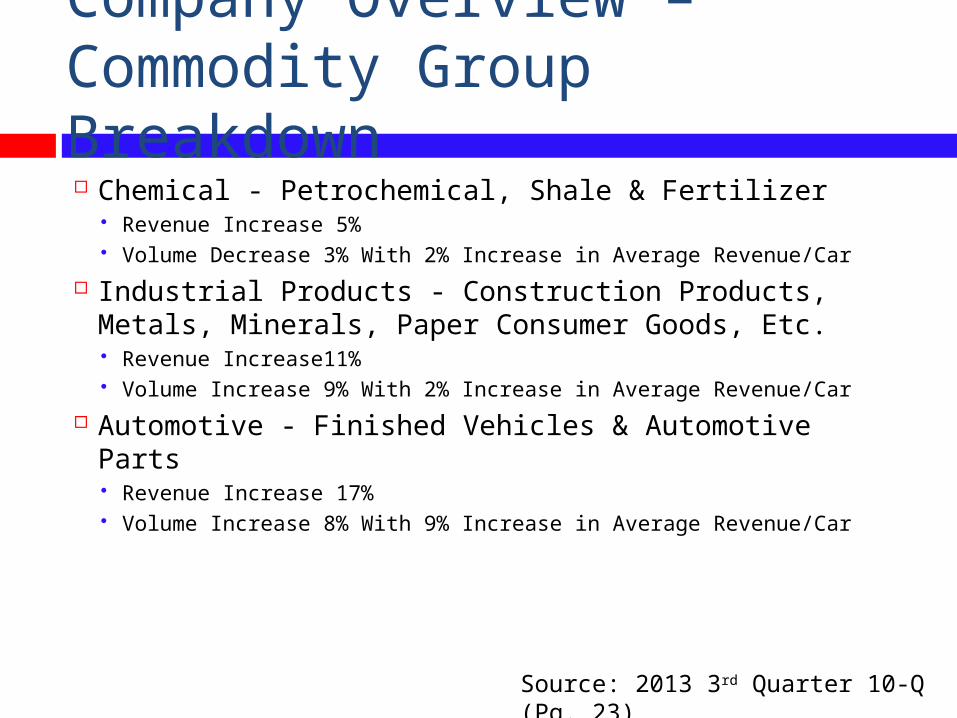

Company Overview – Commodity Group Breakdown Chemical - Petrochemical, Shale & Fertilizer

Revenue Increase 5% Volume Decrease 3% With 2% Increase in Average Revenue/Car

Industrial Products - Construction Products, Metals, Minerals, Paper Consumer Goods, Etc. Revenue Increase11% Volume Increase 9% With 2% Increase in Average Revenue/Car

Automotive - Finished Vehicles & Automotive Parts Revenue Increase 17% Volume Increase 8% With 9% Increase in Average Revenue/Car

Source: 2013 3rd Quarter 10-Q (Pg. 23)

Company Overview – Revenue Breakdown 9 Months Ended September 2013

% of Revenue 2013

% of Revenue 2012

Agricultural 15% 17%

Automotive 10% 9%

Chemicals 17% 16%

Coal 19% 20%

Industrial Products

19% 18%

Intermodal 20% 20%

Source: 2012 10-K (Pg. 5), 2013 10-Q (Pg. 8)

Business Risk Analysis

Source: Union Pacific 2012 10-K (Pg. 6 & 11)

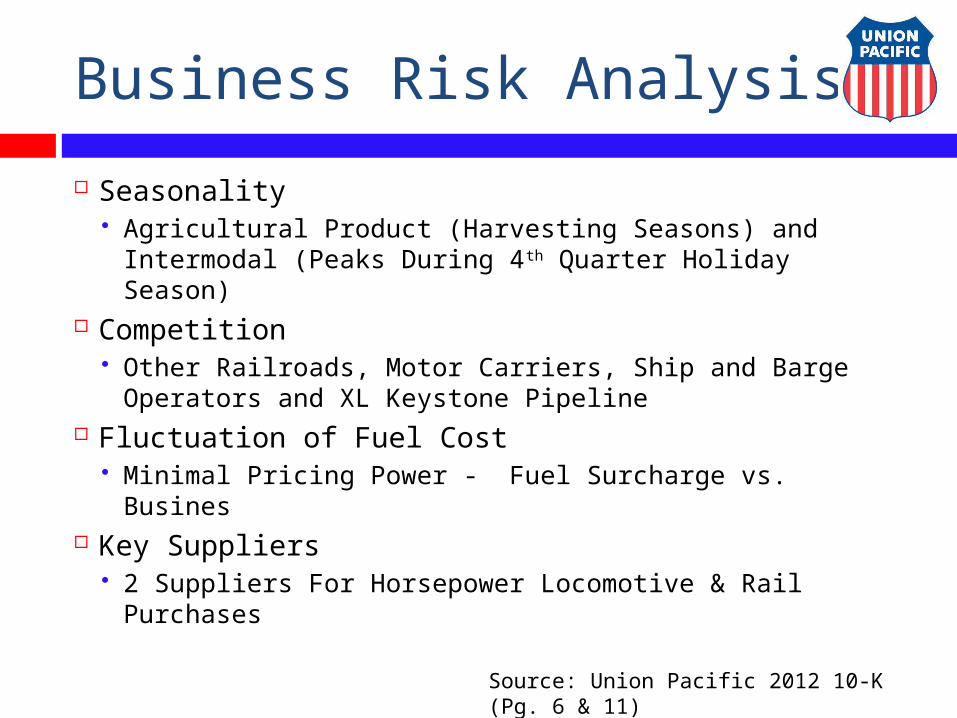

Seasonality Agricultural Product (Harvesting Seasons) and

Intermodal (Peaks During 4th Quarter Holiday Season) Competition

Other Railroads, Motor Carriers, Ship and Barge Operators and XL Keystone Pipeline

Fluctuation of Fuel Cost Minimal Pricing Power - Fuel Surcharge vs. Busines

Key Suppliers 2 Suppliers For Horsepower Locomotive & Rail

Purchases

Business Risk Analysis

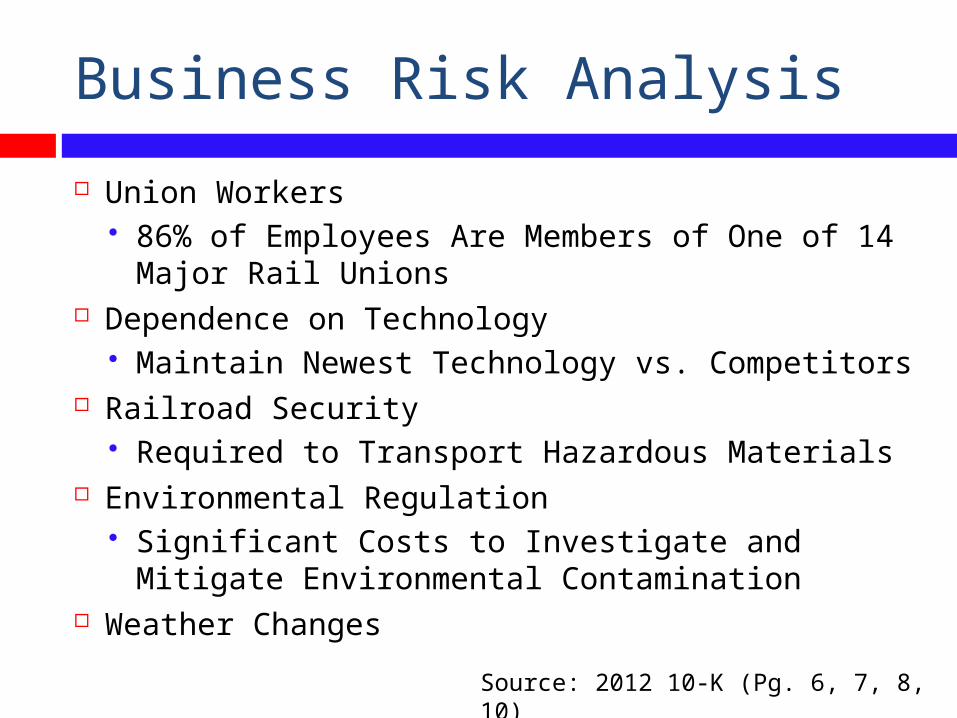

Union Workers 86% of Employees Are Members of One of 14

Major Rail Unions Dependence on Technology

Maintain Newest Technology vs. Competitors Railroad Security

Required to Transport Hazardous Materials Environmental Regulation

Significant Costs to Investigate and Mitigate Environmental Contamination

Weather ChangesSource: 2012 10-K (Pg. 6, 7, 8, 10)

SWOT Analysis

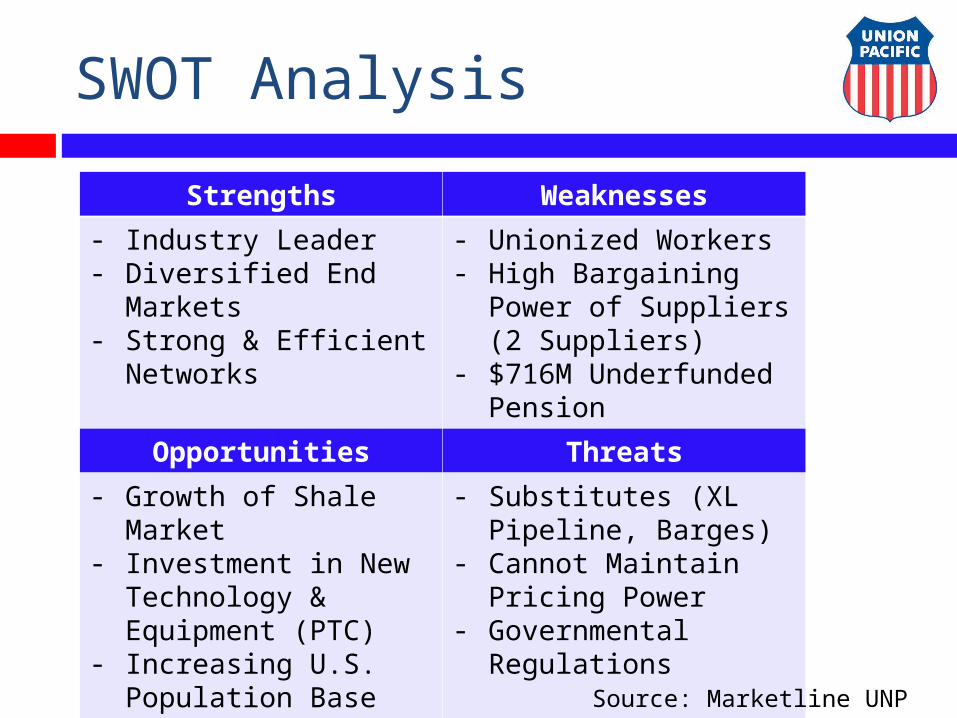

Strengths Weaknesses

- Industry Leader- Diversified End

Markets- Strong & Efficient

Networks

- Unionized Workers- High Bargaining

Power of Suppliers (2 Suppliers)

- $716M Underfunded Pension

Opportunities Threats

- Growth of Shale Market

- Investment in New Technology & Equipment (PTC)

- Increasing U.S. Population Base (Long-Term)

- Substitutes (XL Pipeline, Barges)

- Cannot Maintain Pricing Power

- Governmental Regulations

Source: Marketline UNP Report

Strategy

Focusing on Creating Value for Our Customers By Providing Safe, Efficient and Reliable Services.

Continued Capital Investment to Support Long-Term Functionality

Expand Network in the South Increase Shale Related Presence

Maintain a Diverse Franchise of Operations

Source: Union Pacific 2013 10-Q (Pg. 15), 2012 10-K (Pg. 2)

Management Outlook

Positive 2012 Performance Reaches All-Time High Diversified Portfolio of Business Providing

Hedging Against Each Other Invest Intensively in Technology and Equipment

Enhancement Growth in the Southern Region of the Network

(Shale-Related Energy Arena) Increase in U.S. Population Base

Concerns Fuel Price Fluctuation

Source: 2013 3rd Quarter 10-Q (Pg. 15, 22), 2012 10-K (Pg. 2)

Recent News – Earnings Report Earnings Report – October 17, 2013

Record Quarterly Earnings of $2.48/Share From $2.19 2nd Quarter

Net Income Increased to $1.2B From $1.0B Dividend Declared $0.79/Share Record Quarterly Operating Margin of

64.8% Flat Volumes With Increase in Core Pricing

Power

Source: Union Pacific Website News Releases

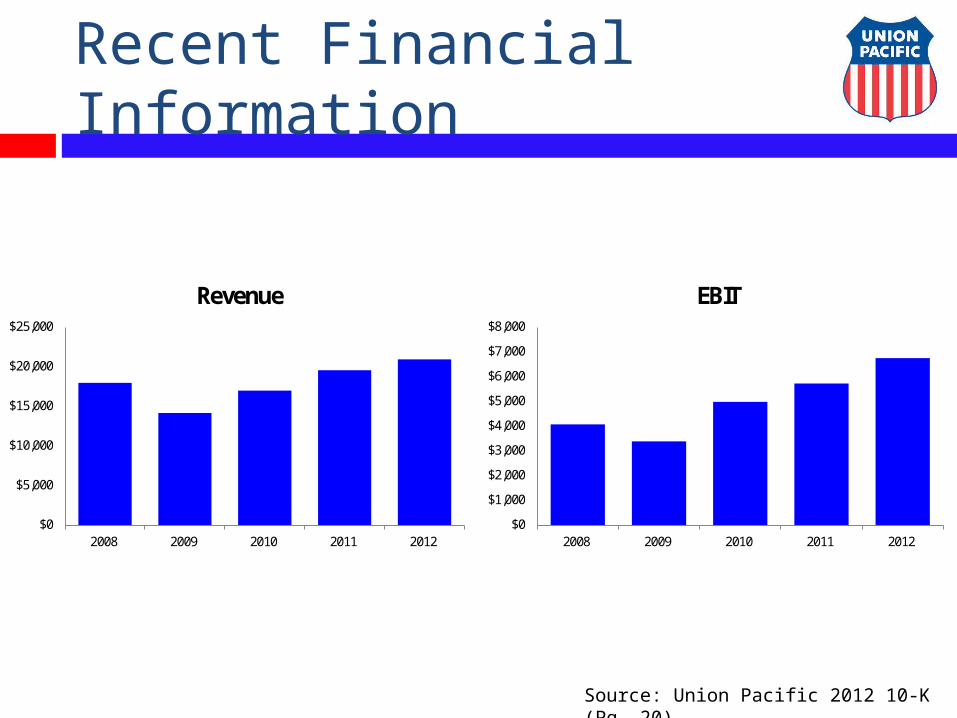

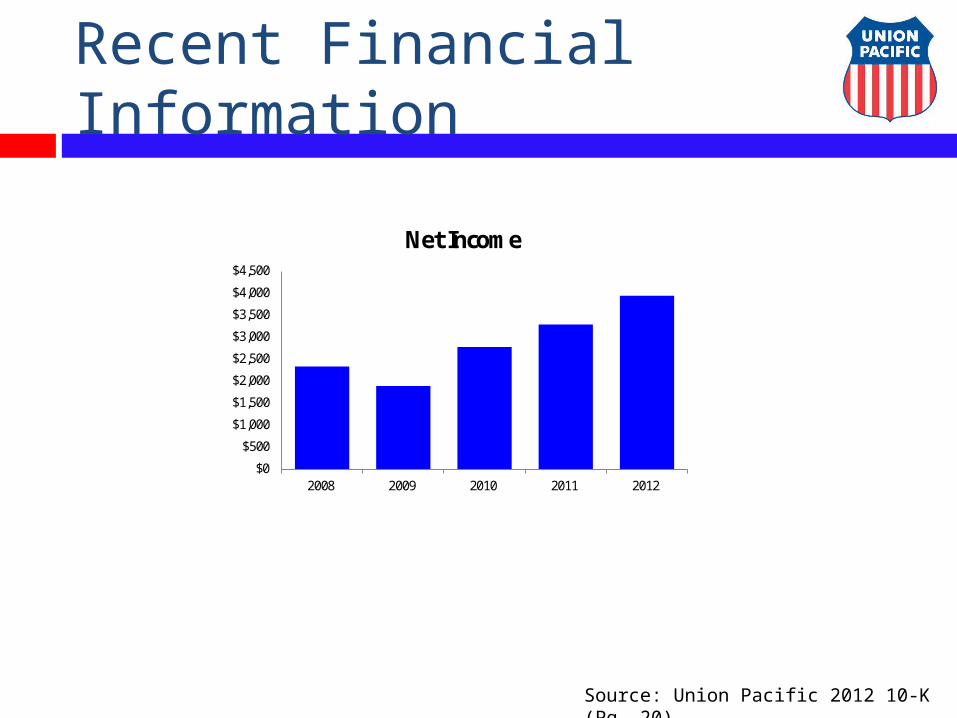

Recent Financial Information

Source: Union Pacific 2012 10-K (Pg. 20)

$0

$5,000

$10,000

$15,000

$20,000

$25,000

2008 2009 2010 2011 2012

Revenue

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

2008 2009 2010 2011 2012

EBIT

Recent Financial Information

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

2008 2009 2010 2011 2012

Net Income

Source: Union Pacific 2012 10-K (Pg. 20)

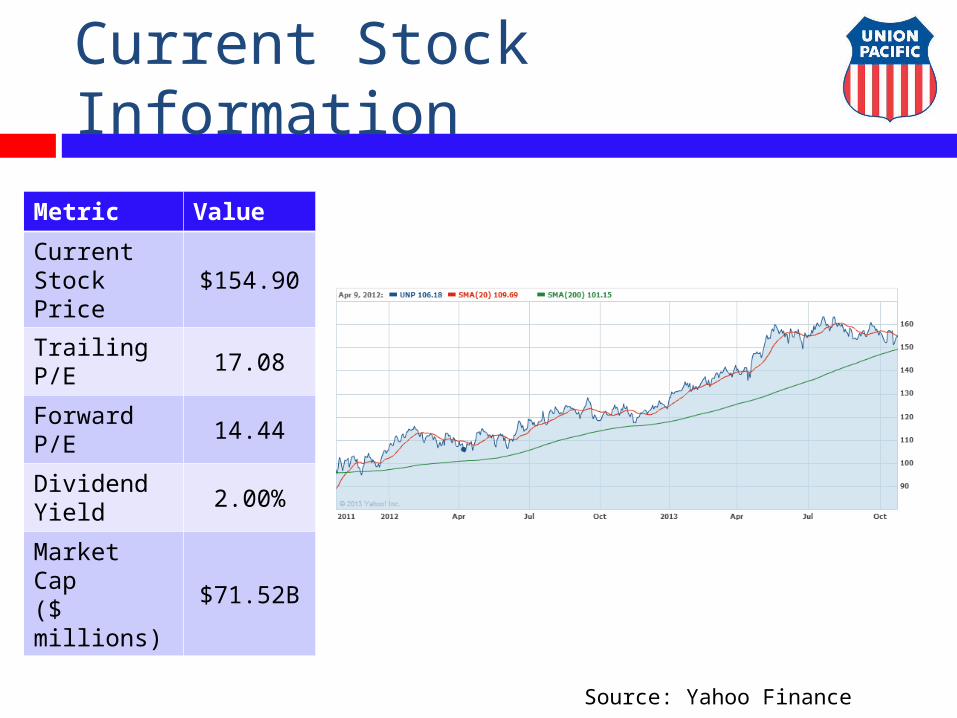

Current Stock Information

Source: Yahoo Finance

Metric Value

Current Stock Price $154.90

Trailing P/E17.08

Forward P/E 14.44

Dividend Yield 2.00%

Market Cap($ millions) $71.52B

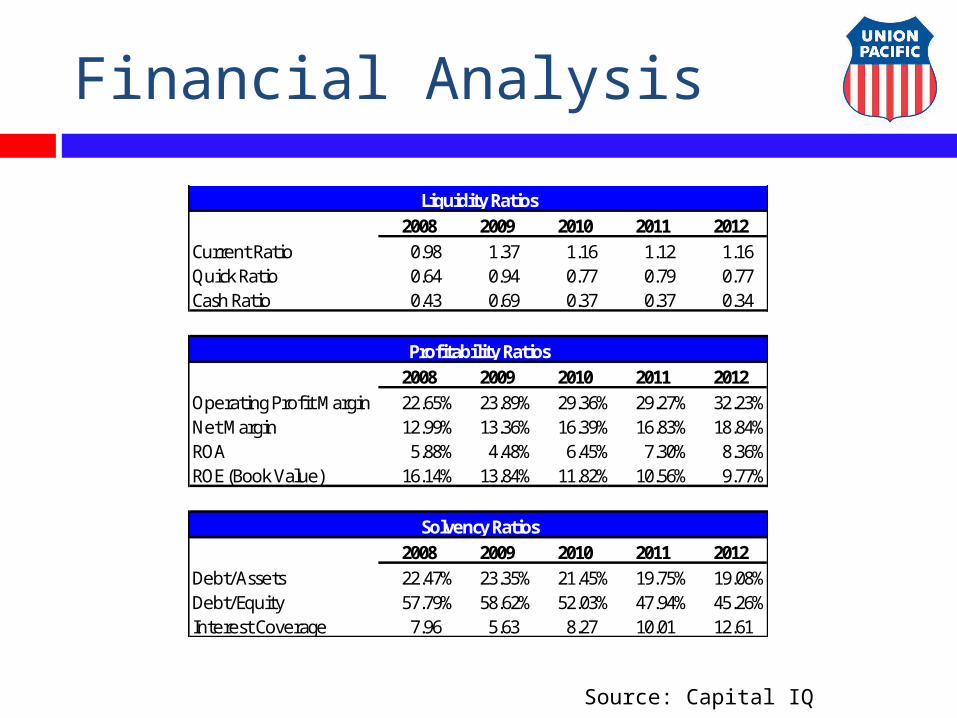

Financial Analysis

2008 2009 2010 2011 2012Current Ratio 0.98 1.37 1.16 1.12 1.16Quick Ratio 0.64 0.94 0.77 0.79 0.77Cash Ratio 0.43 0.69 0.37 0.37 0.34

2008 2009 2010 2011 2012Operating Profit Margin 22.65% 23.89% 29.36% 29.27% 32.23%Net Margin 12.99% 13.36% 16.39% 16.83% 18.84%ROA 5.88% 4.48% 6.45% 7.30% 8.36%ROE (Book Value) 16.14% 13.84% 11.82% 10.56% 9.77%

2008 2009 2010 2011 2012Debt/Assets 22.47% 23.35% 21.45% 19.75% 19.08%Debt/Equity 57.79% 58.62% 52.03% 47.94% 45.26%Interest Coverage 7.96 5.63 8.27 10.01 12.61

Profitability Ratios

Solvency Ratios

Liquidity Ratios

Source: Capital IQ

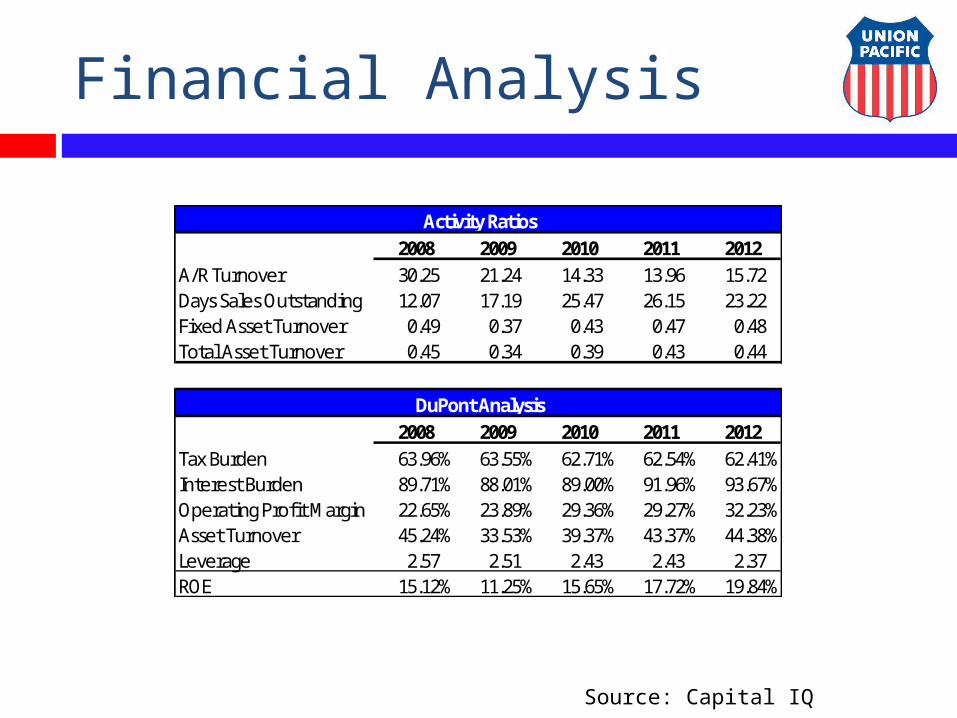

Financial Analysis

2008 2009 2010 2011 2012A/R Turnover 30.25 21.24 14.33 13.96 15.72Days Sales Outstanding 12.07 17.19 25.47 26.15 23.22Fixed Asset Turnover 0.49 0.37 0.43 0.47 0.48Total Asset Turnover 0.45 0.34 0.39 0.43 0.44

2008 2009 2010 2011 2012Tax Burden 63.96% 63.55% 62.71% 62.54% 62.41%Interest Burden 89.71% 88.01% 89.00% 91.96% 93.67%Operating Profit Margin 22.65% 23.89% 29.36% 29.27% 32.23%Asset Turnover 45.24% 33.53% 39.37% 43.37% 44.38%Leverage 2.57 2.51 2.43 2.43 2.37ROE 15.12% 11.25% 15.65% 17.72% 19.84%

Activity Ratios

DuPont Analysis

Source: Capital IQ

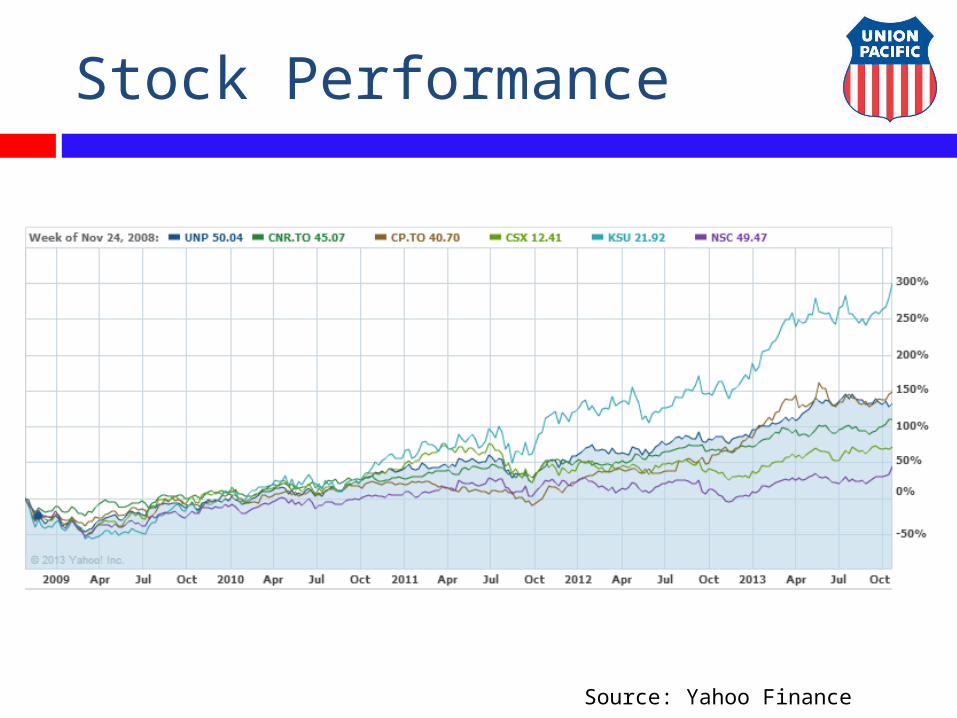

Stock Performance

Source: Yahoo Finance

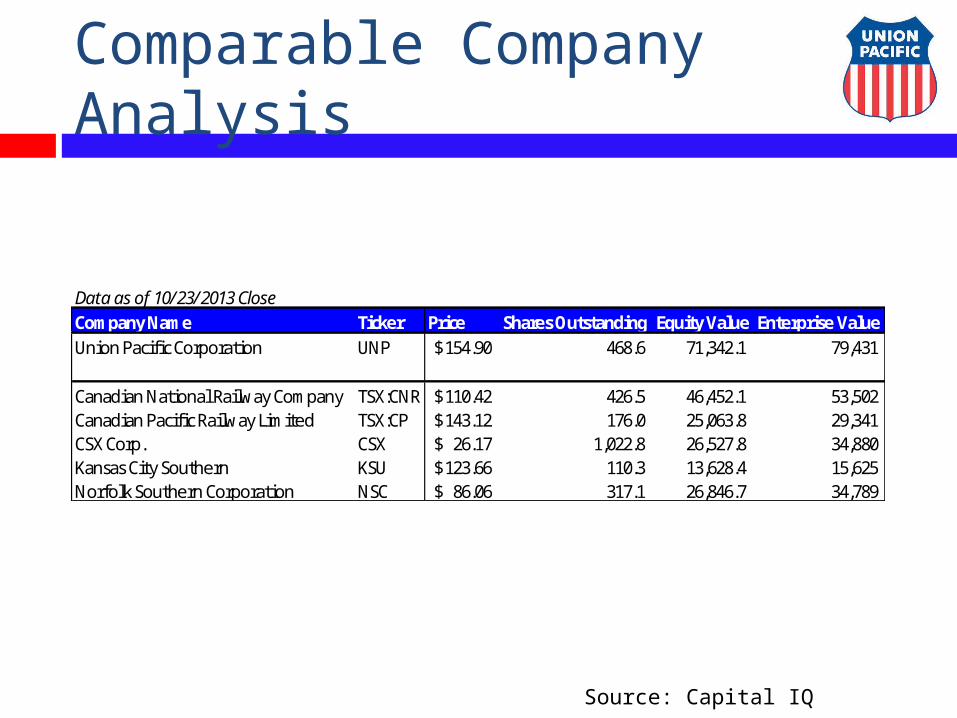

Comparable Company Analysis

Source: Capital IQ

Data as of 10/23/2013 CloseCompany Name Ticker Price Shares Outstanding Equity Value Enterprise ValueUnion Pacific Corporation UNP 154.90$ 468.6 71,342.1 79,431

Canadian National Railway Company TSX:CNR 110.42$ 426.5 46,452.1 53,502 Canadian Pacific Railway Limited TSX:CP 143.12$ 176.0 25,063.8 29,341 CSX Corp. CSX 26.17$ 1,022.8 26,527.8 34,880 Kansas City Southern KSU 123.66$ 110.3 13,628.4 15,625 Norfolk Southern Corporation NSC 86.06$ 317.1 26,846.7 34,789

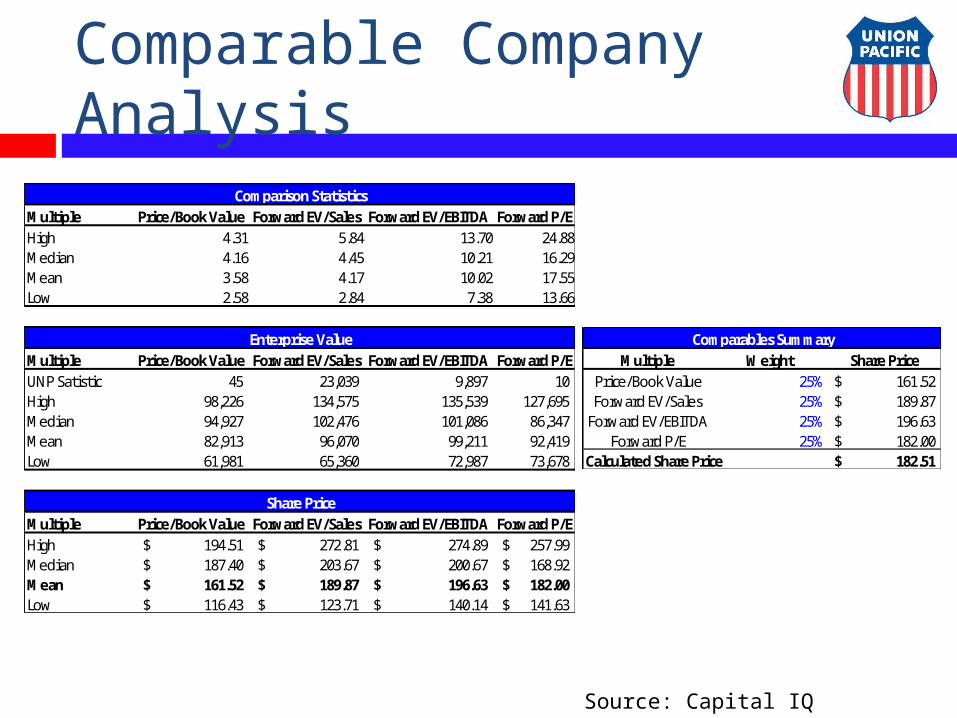

Comparable Company Analysis

Source: Capital IQ

Multiple Price/Book Value Forward EV/Sales Forward EV/EBITDA Forward P/EHigh 4.31 5.84 13.70 24.88Median 4.16 4.45 10.21 16.29Mean 3.58 4.17 10.02 17.55Low 2.58 2.84 7.38 13.66

Multiple Price/Book Value Forward EV/Sales Forward EV/EBITDA Forward P/EUNP Satistic 45 23,039 9,897 10 High 98,226 134,575 135,539 127,695 Median 94,927 102,476 101,086 86,347 Mean 82,913 96,070 99,211 92,419 Low 61,981 65,360 72,987 73,678

Multiple Price/Book Value Forward EV/Sales Forward EV/EBITDA Forward P/EHigh 194.51$ 272.81$ 274.89$ 257.99$ Median 187.40$ 203.67$ 200.67$ 168.92$ Mean 161.52$ 189.87$ 196.63$ 182.00$ Low 116.43$ 123.71$ 140.14$ 141.63$

Comparison Statistics

Enterprise Value

Share Price

Multiple Weight Share PricePrice/Book Value 25% 161.52$ Forward EV/Sales 25% 189.87$

Forward EV/EBITDA 25% 196.63$ Forward P/E 25% 182.00$

Calculated Share Price 182.51$

Comparables Summary

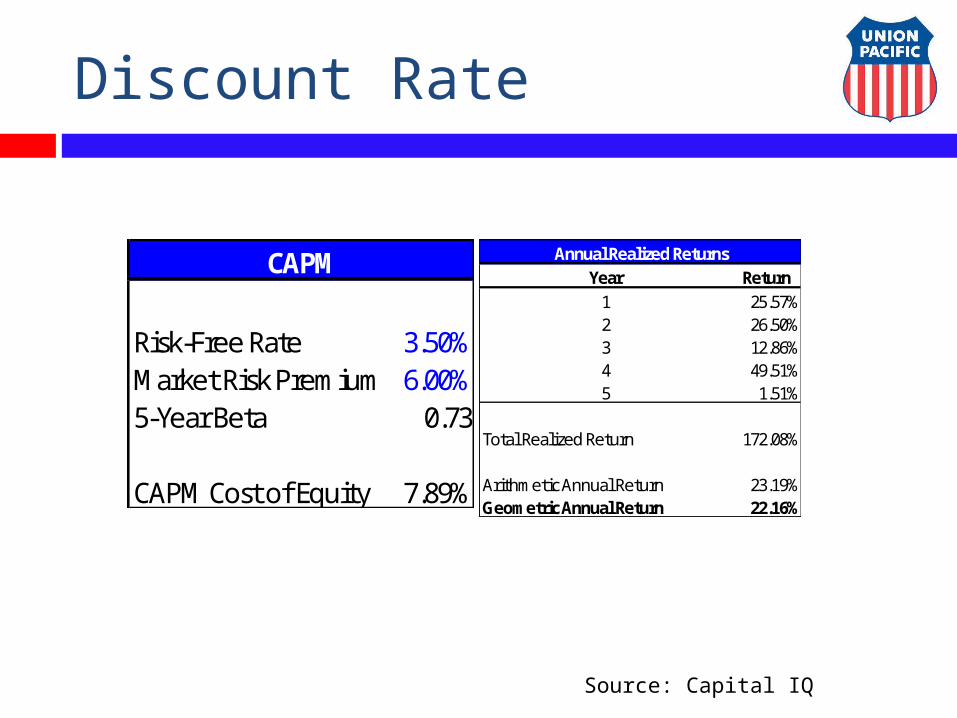

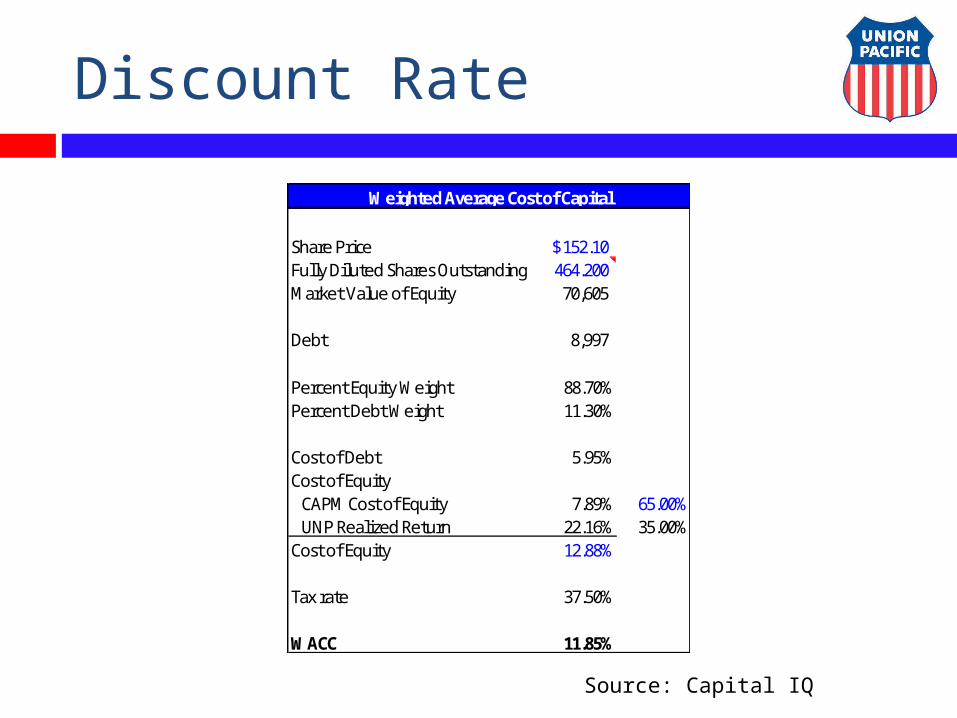

Discount Rate

Year Return1 25.57%2 26.50%3 12.86%4 49.51%5 1.51%

Total Realized Return 172.08%

Arithmetic Annual Return 23.19%Geometric Annual Return 22.16%

Annual Realized Returns

Risk-Free Rate 3.50%Market Risk Premium 6.00%5-Year Beta 0.73

CAPM Cost of Equity 7.89%

CAPM

Source: Capital IQ

Discount Rate

Share Price 152.10$ Fully Diluted Shares Outstanding 464.200 Market Value of Equity 70,605

Debt 8,997

Percent Equity Weight 88.70%Percent Debt Weight 11.30%

Cost of Debt 5.95%Cost of Equity

CAPM Cost of Equity 7.89% 65.00%UNP Realized Return 22.16% 35.00%

Cost of Equity 12.88%

Tax rate 37.50%

WACC 11.85%

Weighted Average Cost of Capital

Source: Capital IQ

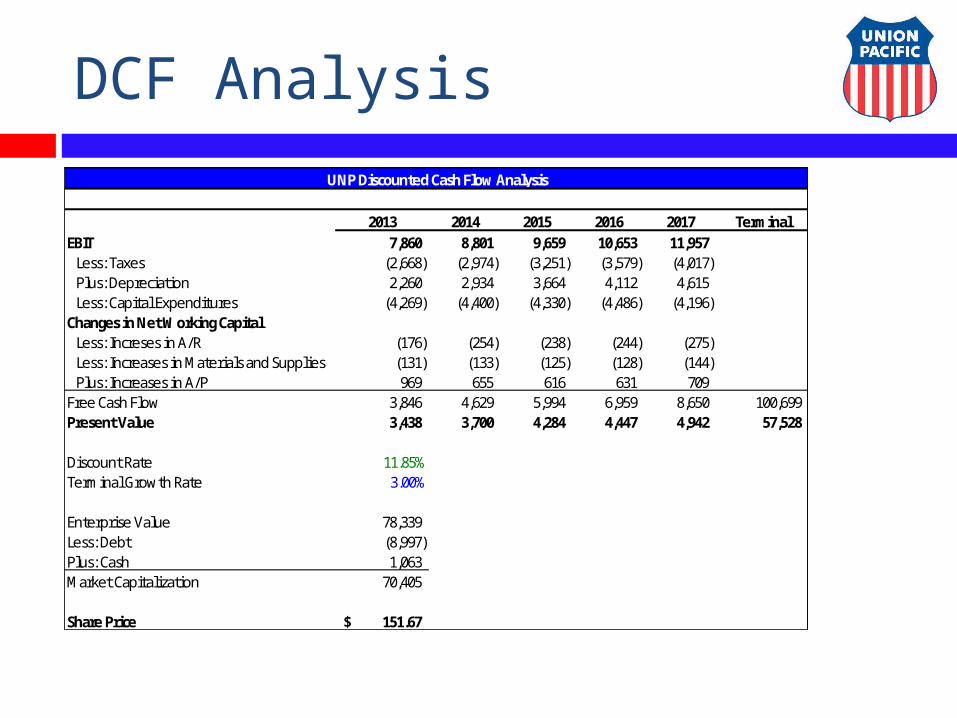

DCF Analysis

2013 2014 2015 2016 2017 TerminalEBIT 7,860 8,801 9,659 10,653 11,957

Less: Taxes (2,668) (2,974) (3,251) (3,579) (4,017) Plus: Depreciation 2,260 2,934 3,664 4,112 4,615 Less: Capital Expenditures (4,269) (4,400) (4,330) (4,486) (4,196)

Changes in Net Working CapitalLess: Increses in A/R (176) (254) (238) (244) (275) Less: Increases in Materials and Supplies (131) (133) (125) (128) (144) Plus: Increases in A/P 969 655 616 631 709

Free Cash Flow 3,846 4,629 5,994 6,959 8,650 100,699 Present Value 3,438 3,700 4,284 4,447 4,942 57,528

Discount Rate 11.85%Terminal Growth Rate 3.00%

Enterprise Value 78,339 Less: Debt (8,997) Plus: Cash 1,063 Market Capitalization 70,405

Share Price 151.67$

UNP Discounted Cash Flow Analysis

Decision Drivers

Strengths Record Operating Margin of 65% Record Quarterly Earnings of $2.48/Share &

Record Quarterly Dividend of $0.78/Share Industry Diversification – Growth of Shale Automobile Industry Resurgence

Concerns Decrease in Coal Growth Crude Oil Fluctuations

Source: Union Pacific Website News Releases,2012 10-K (Pg. 2)

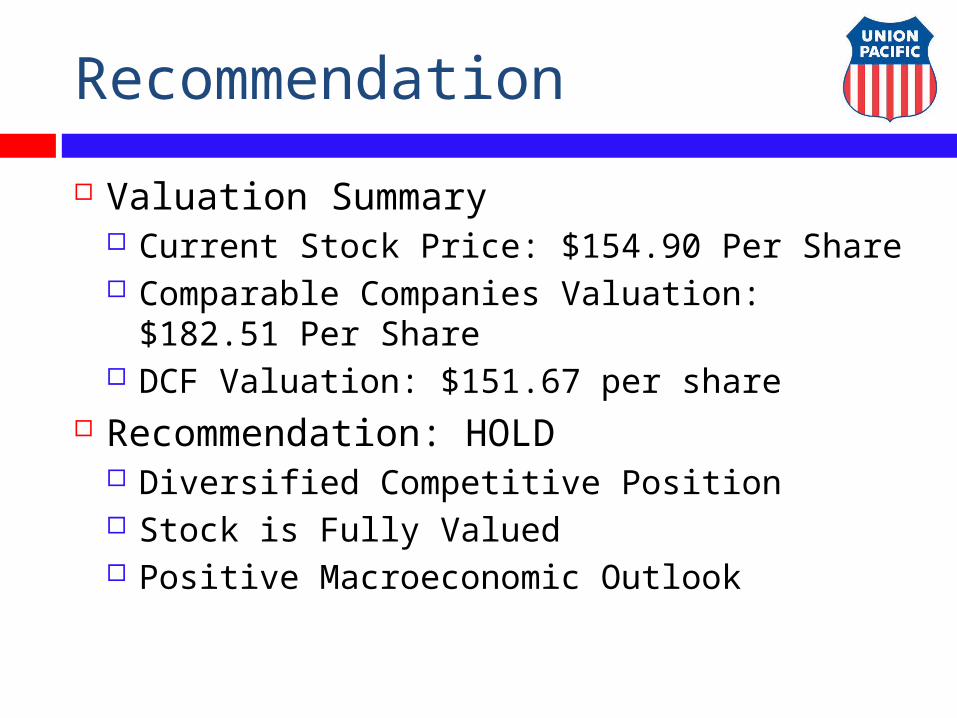

Recommendation

Valuation Summary Current Stock Price: $154.90 Per Share Comparable Companies Valuation: $182.51

Per Share DCF Valuation: $151.67 per share

Recommendation: HOLD Diversified Competitive Position Stock is Fully Valued Positive Macroeconomic Outlook

Questions?