Embed Size (px)

Citation preview

Union Budget (Interim) 2014

(Prepared on Feb 17, 2014) Introduction As you know, the Union Finance Minister presented the Interim Budget on February 17, 2014. This being an election year, a new government will present a “proper budget” after the election results, probably around the middle of the year. The finance minister has made a serious attempt to control the fiscal deficit. By and large, he has avoided populist moves in an election year and also made attempts to revive growth by cuts in excise duties. But major concerns about the long term competitiveness of the economy remain. Here are some highlights and some key data points. This write up draws heavily from some recent research reports prepared by HDFC and CLSA and of course various media reports and government sources. Economic outlook

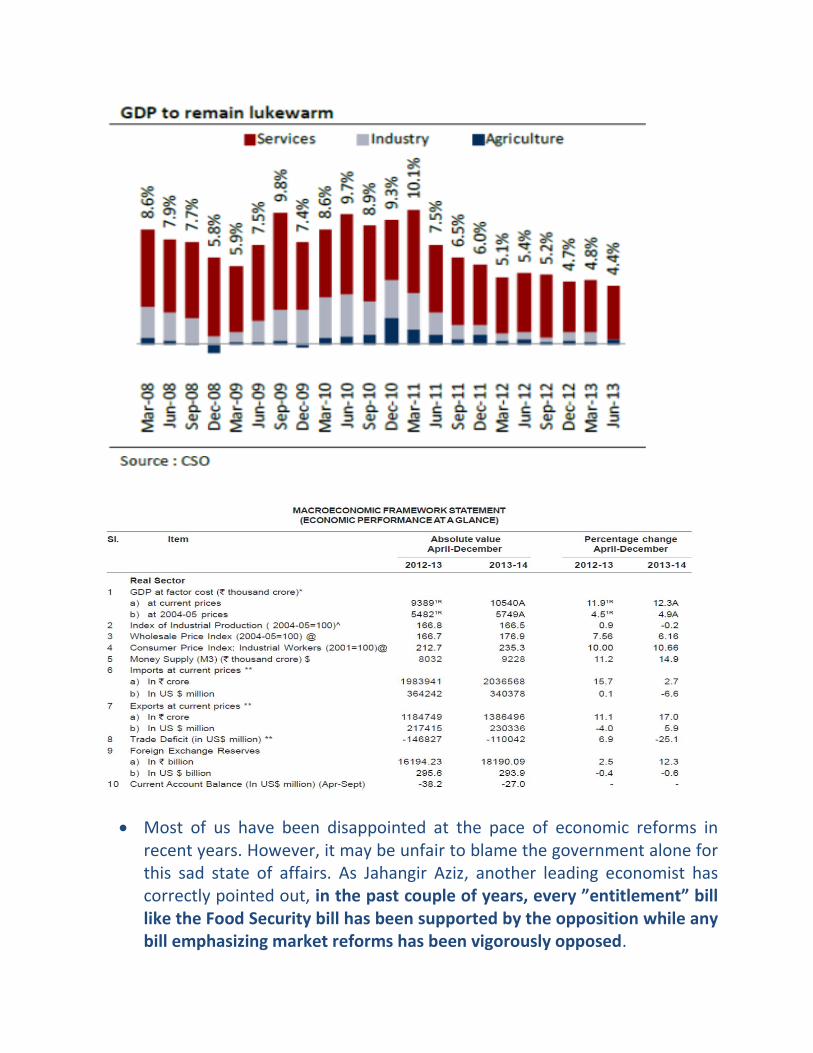

GDP (Gross Domestic Product, at factor cost at constant 2004-05 prices) growth slowed down from 8.9 per cent in 2010-11 to 6.7 per cent in 2011-12 and 4.5 per cent in 2012-13. With the economy projected to grow at 4.9 per cent in 2013-14, the government claims the declining trend in growth has been reversed. But we have to wait and see! In any case a sub 5% GDP growth is hardly a happy situation for us. It may be mentioned here, that it is for the first time in 28 years that the Indian economy will grow by less than 5 % for 2 consecutive years.

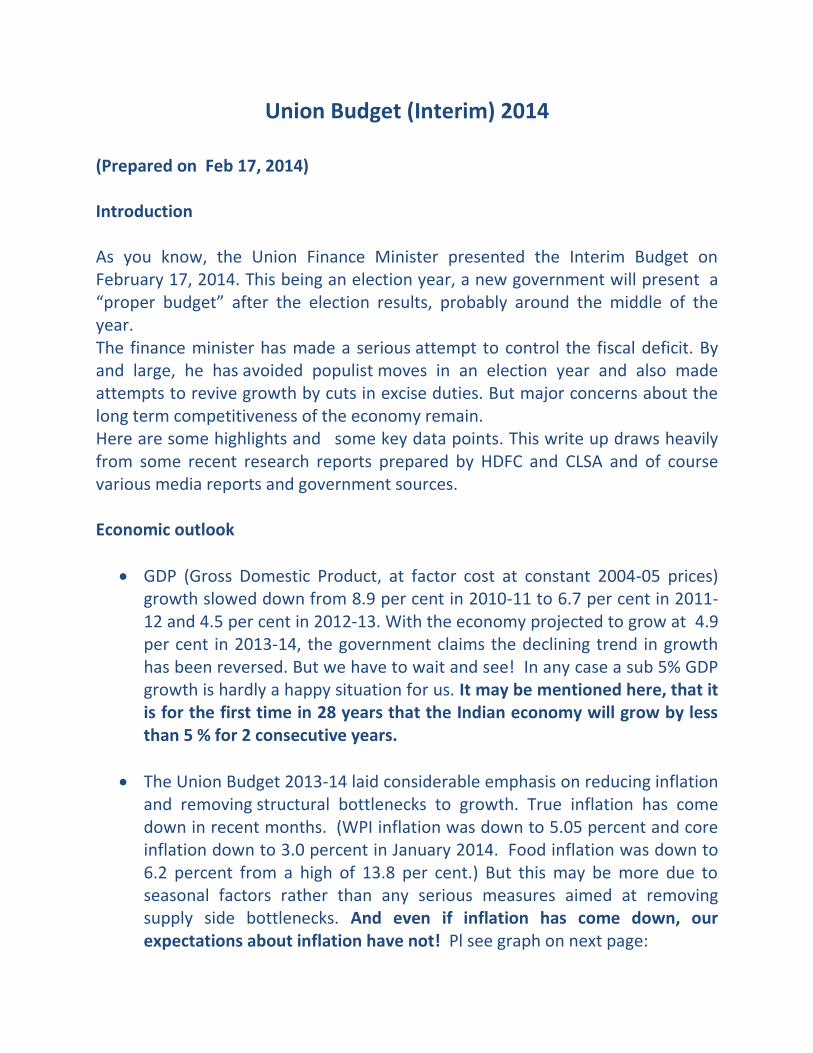

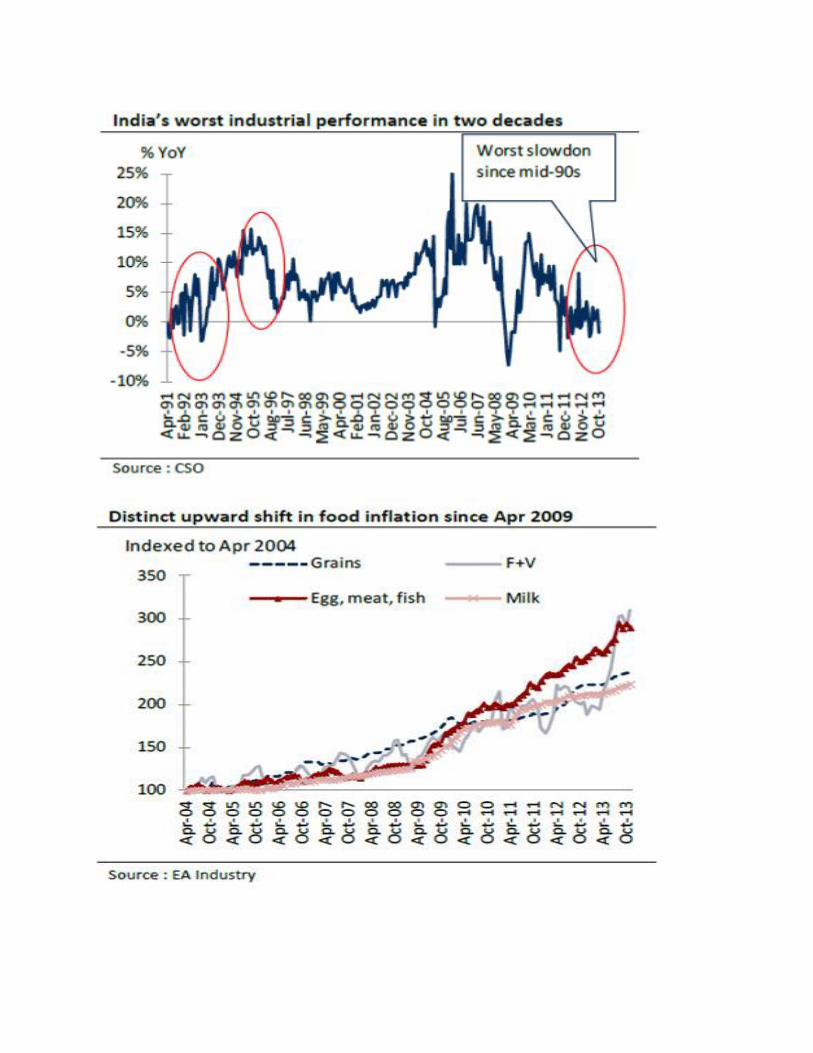

The Union Budget 2013-14 laid considerable emphasis on reducing inflation and removing structural bottlenecks to growth. True inflation has come down in recent months. (WPI inflation was down to 5.05 percent and core inflation down to 3.0 percent in January 2014. Food inflation was down to 6.2 percent from a high of 13.8 per cent.) But this may be more due to seasonal factors rather than any serious measures aimed at removing supply side bottlenecks. And even if inflation has come down, our expectations about inflation have not! Pl see graph on next page:

On a more positive note, a reduction in the trade deficit, supported by a rise in net invisibles receipts, led to a significant reduction in the current account deficit (CAD) in the first half of 2013-14. It may be mentioned that CAD was around 4.7% of GDP last year and now it is about 2%. Though this reduction has been achieved largely by imposing restrictions on gold imports, fiscal tightening has certainly helped. It may be noted that fiscal and current account deficits often tend to be strongly correlated.

The exchange rate, that breached the level of Rs 68/$ in August 2013, recovered to Rs 61.16/$ on October 11, 2013. The exchange rate averaged Rs 61.91/$ in December 2013.

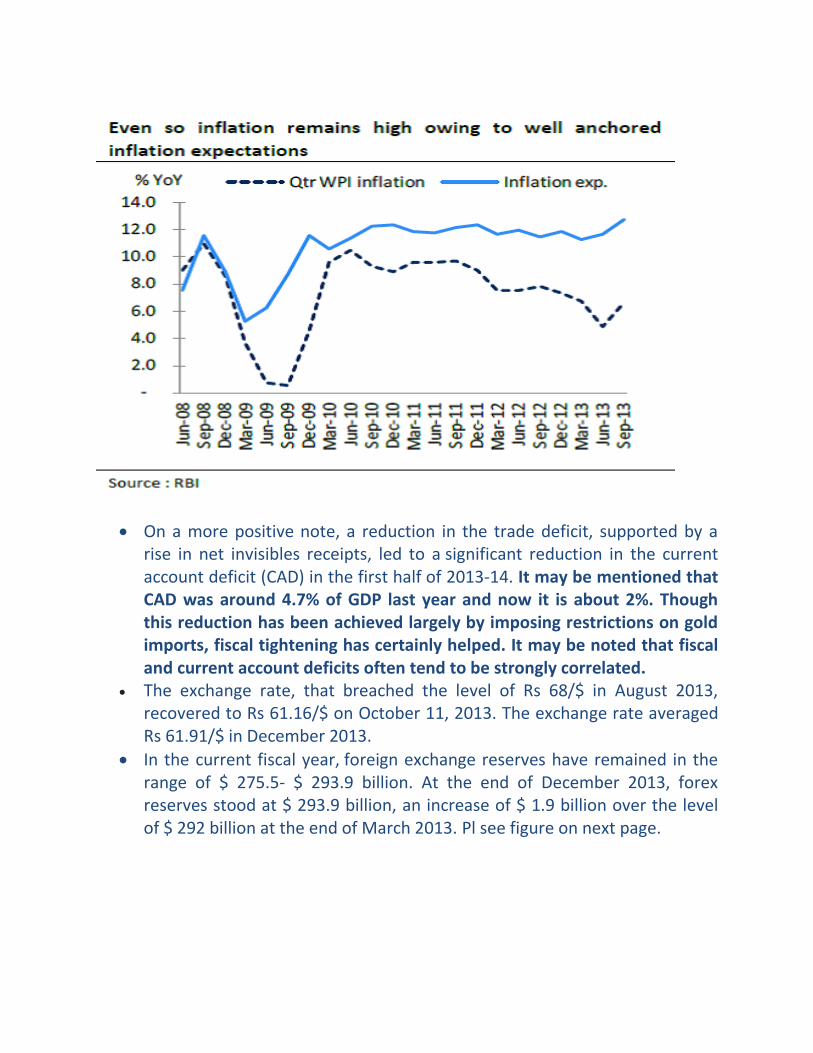

In the current fiscal year, foreign exchange reserves have remained in the range of $ 275.5- $ 293.9 billion. At the end of December 2013, forex reserves stood at $ 293.9 billion, an increase of $ 1.9 billion over the level of $ 292 billion at the end of March 2013. Pl see figure on next page.

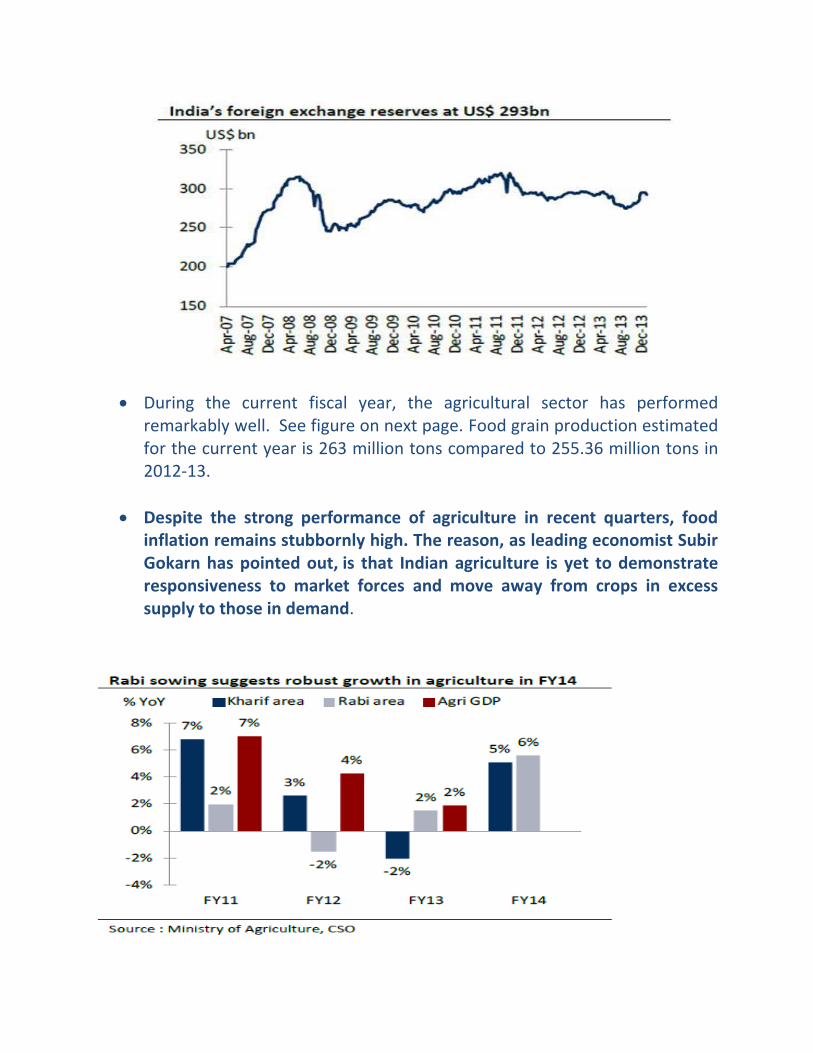

During the current fiscal year, the agricultural sector has performed remarkably well. See figure on next page. Food grain production estimated for the current year is 263 million tons compared to 255.36 million tons in 2012-13.

Despite the strong performance of agriculture in recent quarters, food inflation remains stubbornly high. The reason, as leading economist Subir Gokarn has pointed out, is that Indian agriculture is yet to demonstrate responsiveness to market forces and move away from crops in excess supply to those in demand.

The current government has been in power for about 10 years. How does the economy today compare with that 10 years ago?

In 2004, the fiscal deficit was 4.4%. Today, it is 4.6%.

Inflation rate which was about 3.8% in 2004 has been substantially higher during the past 5 years.

Then, the current account was in surplus. Today, the deficit is more than 2.0% of GDP.

True, in the past few years, the macroeconomic environment has become tougher. Oil prices were about $ 38 per barrel in 2004 and today, they are above $ 100. But then, the Government could have steadily raised fuel prices and kept the petroleum subsidies under check.

Moreover, much of the pressure on the current account in recent times has been due to reduction in iron ore exports and increase in coal imports. We learnt in our school geography text book that India is rich in iron ore and coal. ( My daughter is appearing for her ICSE exam next month and my interest in the subject has increased!) Logically, we should be exploiting these sectors to our advantage. But unfortunately, these sectors have become entangled in legal and environmental issues.

The performance of the manufacturing sector has significantly declined in the past 10 years while the overall growth has come down sharply in the past 8 years.

India’s corporate investment rate reached a high of 17% of GDP in 2007 -08. Since then, it has plummeted to 9%. To get growth back on track, we need private sector investments to be back on track. And to restore business confidence, excise duty cuts alone will not be enough. Various kinds of structural reforms will have to be implemented. And public infrastructure spending will clearly have to go up.

Most of us have been disappointed at the pace of economic reforms in recent years. However, it may be unfair to blame the government alone for this sad state of affairs. As Jahangir Aziz, another leading economist has correctly pointed out, in the past couple of years, every ”entitlement” bill like the Food Security bill has been supported by the opposition while any bill emphasizing market reforms has been vigorously opposed.

Budget overview

The Finance Minister has delivered a better than expected fiscal deficit of 4.6% of GDP for the current year. This is a pretty impressive achievement when we consider that the total deficit reduction over the past couple of years has been about 1.1% of GDP. This reduction has been achieved at a time of slowing GDP growth (below 5%) and poor progress on the public sector disinvestment front (less than 0.5% of GDP).

To put things in perspective, a couple of years back, the Indian economy was growing at 9% + and the disinvestment proceeds (including telecom spectrum sales) amounted to 2% of GDP. It was much easier to cut the deficit then but the deficit as a percentage of GDP was around the same level as today. So Mr. Chidambaram must get credit for making quite a bit of progress towards balancing the books of the government.

But the manner in which the deficit figure has been arrived at, raises some intriguing questions.

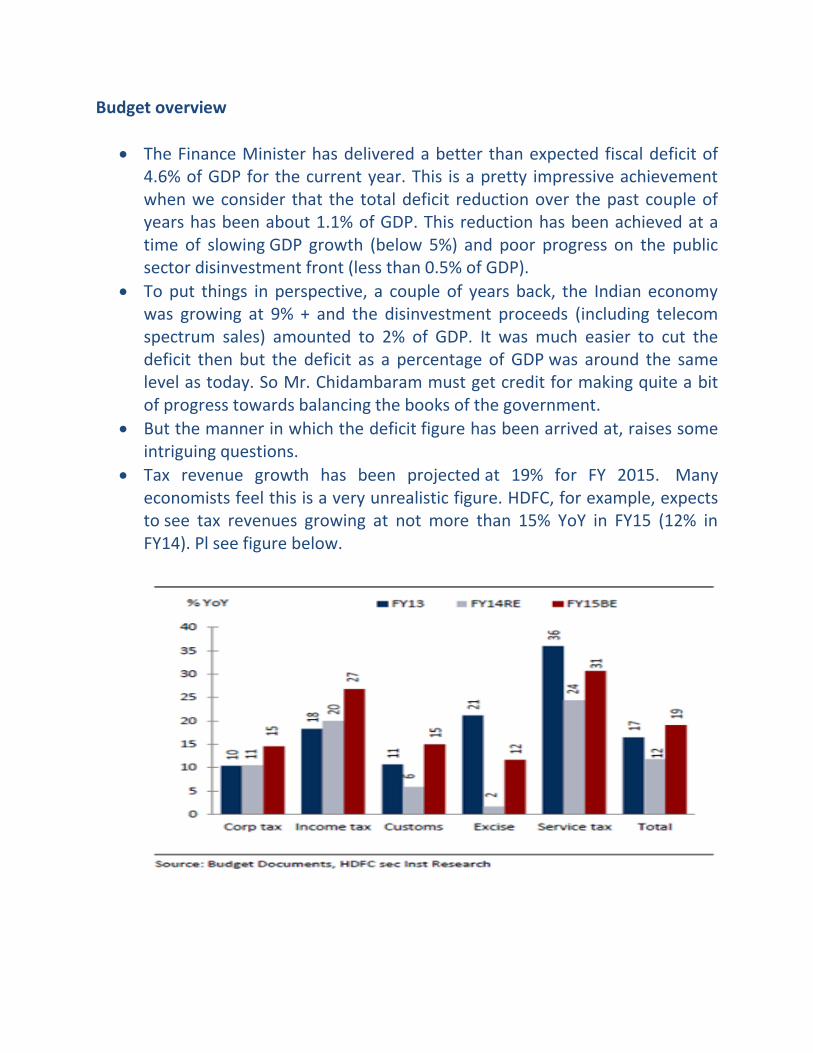

Tax revenue growth has been projected at 19% for FY 2015. Many economists feel this is a very unrealistic figure. HDFC, for example, expects to see tax revenues growing at not more than 15% YoY in FY15 (12% in FY14). Pl see figure below.

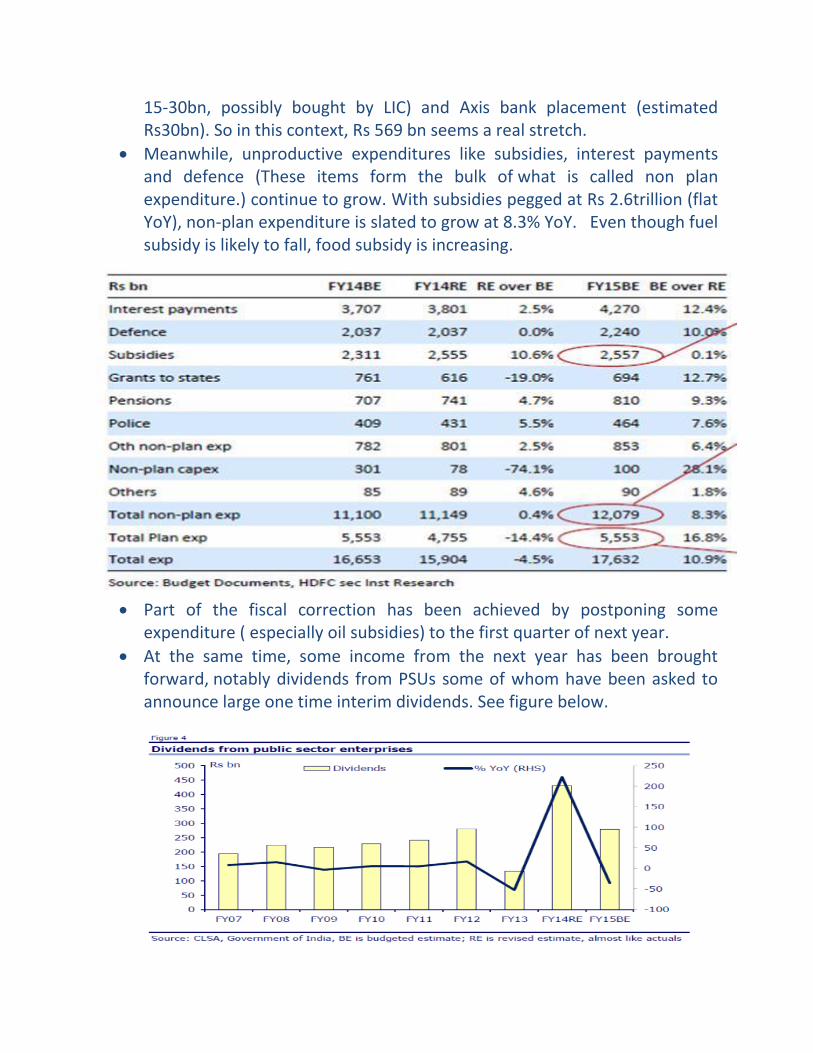

Disinvestment receipts may be far lower than the Rs 569 bn assumed in the budget estimates for FY15. In this context, it should be noted that the Government has significantly reduced the FY14 disinvestment target from Rs540bn to Rs 190bn. Of this only Rs 61bn of divestments have been closed so far. Over the next 6 weeks, the Government expects to conclude the disinvestment in IOC (Rs 55-60bn, to be bought by ONGC and OIL), BHEL (Rs

15-30bn, possibly bought by LIC) and Axis bank placement (estimated Rs30bn). So in this context, Rs 569 bn seems a real stretch.

Meanwhile, unproductive expenditures like subsidies, interest payments and defence (These items form the bulk of what is called non plan expenditure.) continue to grow. With subsidies pegged at Rs 2.6trillion (flat YoY), non-plan expenditure is slated to grow at 8.3% YoY. Even though fuel subsidy is likely to fall, food subsidy is increasing.

Part of the fiscal correction has been achieved by postponing some

expenditure ( especially oil subsidies) to the first quarter of next year.

At the same time, some income from the next year has been brought forward, notably dividends from PSUs some of whom have been asked to announce large one time interim dividends. See figure below.

Further reduction of the fisal deficit cannot be achieved by more cuts in plan spending (Plan spending is what boosts the long term productive potential of the economy.), running up arrears on subsidies and milking public sector companies by forcing them to pay high one time dividends. We need structural reforms. For example, the introduction of GST will unify India’s market, make the investment climate more favourable and ensure more efficient capital allocation. Similarly, a more effective and mandated use of Adhar will ensure that subsidies are better managed and reach the right people without much leakage.

The one rank one pension announcement , though a populist move aimed at mobilising the votes of ex defence services staff, has been received well, including opposition leaders like Narendra Modi. This means that our ex service men will receive the same pension for the same rank and for the same years of service, irrespective of when they retired.

A welcome move by the government towards decentralisation of spending powers and better governance is the proposal to transfer Rs 200,000 crores to the states and make them responsible for implementing programs related to school education, healthcare, women, child development and rural development.

Tax proposals

Income tax rates have been kept unchanged.

There is still no sign of the Goods and Services tax (GST) or the new Direct tax code (DTC).

To revive the manufacturing sector, the Government has cut excise duties by 4-6 points across segments. This should boost demand in the near-term as consumers prepone their purchases. But tinkering with excise duty rates is a backward step in the context of the GST Act which aims at harmonizing excise duties across goods.

Excise duty on small cars, motorcycles and commercial vehicles has been cut from 12 to 8 %.

Excise duty on SUVs has been cut from 30 to 24 %.

Excise duty on large and mid-segment cars has been reduced from 27-24 % to 24-20 %.

The expected relaxation of gold imports has not happened.

Concluding notes The budget has correctly identified ten top priorities. These priorities are :

Fiscal consolidation: We must achieve a fiscal deficit of 3 percent of GDP by 2016-17 and remain below that level always.

Current Account Deficit : CAD will be inevitable for some more years which can be financed only by foreign investment. Hence, we must be able to attract foreign investment in a big way.

Price Stability and Growth : In a developing economy, a high growth target entails a moderate level of inflation. RBI must strike a balance between price stability and growth while formulating the monetary policy. ( Current thinking in RBI, however, is that it must focus only on inflation.)

Financial Sector reforms must be completed as laid down by Financial Sector Legislative Reforms Commission.

Massive investment in infrastructure must be mobilized through the Public Private Partnership.

Manufacturing sector should form the base of India’s development. All taxes, Central and State that go into an exported product should be waived or rebated. There should be a minimum tariff protection to incentivize domestic manufacturing.

Subsidies, which are absolutely necessary should be chosen and targeted only at the absolutely deserving.

Urbanization must be managed to make cities governable and livable.

Skill development must be given priority at par with secondary and university education, sanitation and universal health care.

States must become partners in development and allow the Centre to focus on areas such as Defence, Railways, National Highways and Tele-communication.

A great vision and good intentions. Unfortunately, there is not too much in the budget that seems to indicate that decisive steps are being taken to move in this direction!