Embed Size (px)

Citation preview

1

Unilever Q1 2008 Roadshow

20Hellmann’s Light11Big Global Brands

18

16Rexona5Commodity Costs

19

19

Heart Health

16

10Strong Category Positions

Knorr Bouillon GelGrowth Strategy

14Innovation Driving Growth4Growth by Region

13Accelerate Restructuring Programme – Simplification3Highlights

13Accelerate Restructuring Programme – Progress to Date3Strong Organic Growth

7

12

12

11

9

8

8

6

5

4

Magnum Temptation

Moo

Lipton

Small & Mighty in Europe

Comfort Fresh Release

Dove Go Fresh

Dove Pro.Age

Ponds Age Miracle

Clear

Innovation

21Shaping the portfolio

21Acceleration of Unilever’s Growth Agenda

20Unilever’s Strategic Priorities

Returning Cash to Shareholders

182008 Outlook

17Business Priorities

17Commodity Costs – Tea and SMP

Commodity Costs – Oil Charts

15Q1 2008 Operating Margin

Growth by Category

INDEX - Unilever Q1 2008 Results

2

Safe Harbour Statement

This presentation may contain forward-looking statements, including 'forward-looking statements' within the meaning of the United States Private Securities Litigation Reform Act of 1995. Words such as 'expects', 'anticipates', 'intends' or the negative of these terms and other similar expressions of future performance or results, including financial objectives to 2010, and

their negatives are intended to identify such forward-looking statements. These forward-looking statements are based upon current expectations and assumptions regarding anticipated

developments and other factors affecting the Group. They are not historical facts, nor are they guarantees of future performance. Because these forward-looking statements involve risks and uncertainties, there are important factors that could cause actual results to differ materially from

those expressed or implied by these forward-looking statements, including, among others, competitive pricing and activities, consumption levels, costs, the ability to maintain and manage key customer relationships and supply chain sources, currency values, interest rates, the ability to integrate acquisitions and complete planned divestitures, physical risks, environmental risks,

the ability to manage regulatory, tax and legal matters and resolve pending matters within current estimates, legislative, fiscal and regulatory developments, political, economic and social

conditions in the geographic markets where the Group operates and new or changed priorities of the Boards. Further details of potential risks and uncertainties affecting the Group are described

in the Group's filings with the London Stock Exchange, Euronext Amsterdam and the US Securities and Exchange Commission, including the Annual Report & Accounts on Form 20-F.

These forward-looking statements speak only as of the date of this presentation

3

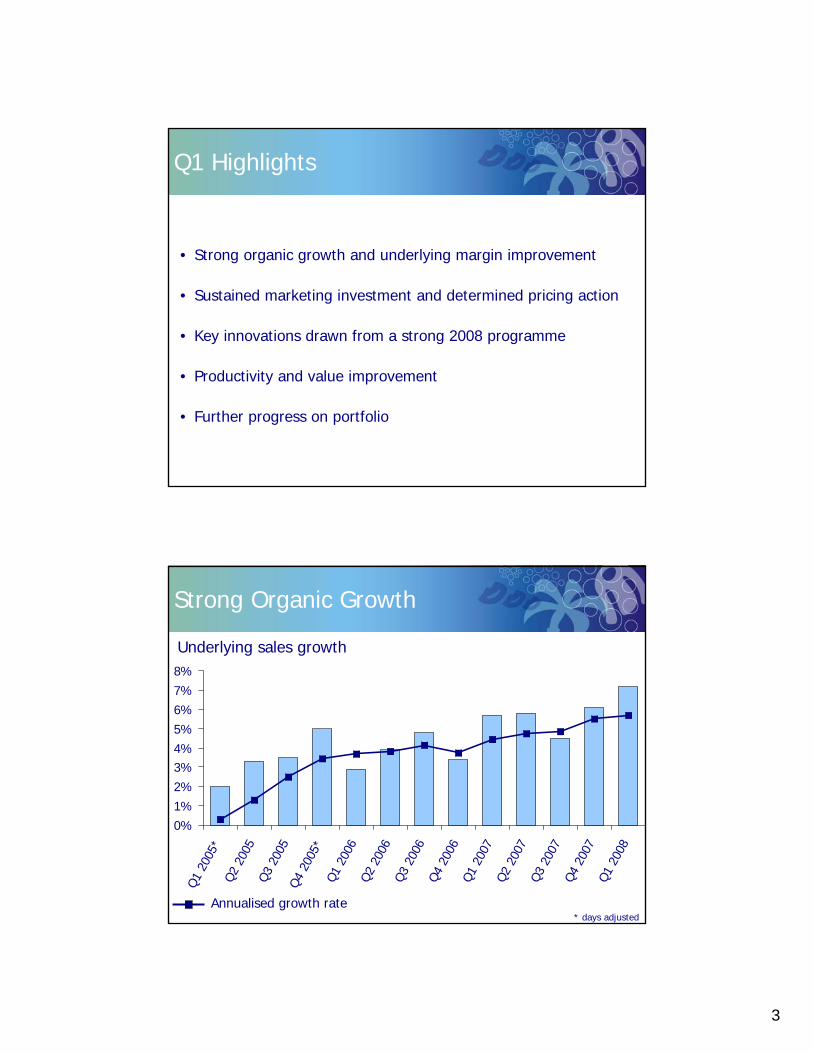

Q1 Highlights

• Strong organic growth and underlying margin improvement

• Sustained marketing investment and determined pricing action

• Key innovations drawn from a strong 2008 programme

• Productivity and value improvement

• Further progress on portfolio

0%1%2%3%4%5%6%7%8%

Q1 2

005*

Q2 2

005

Q3 2

005

Q4 2

005*

Q1 2

006

Q2 2

006

Q3 2

006

Q4 2

006

Q1 2

007

Q2 2

007

Q3 2

007

Q4 2

007

Q1 2

008

Strong Organic Growth

* days adjusted

Underlying sales growth

Annualised growth rate

4

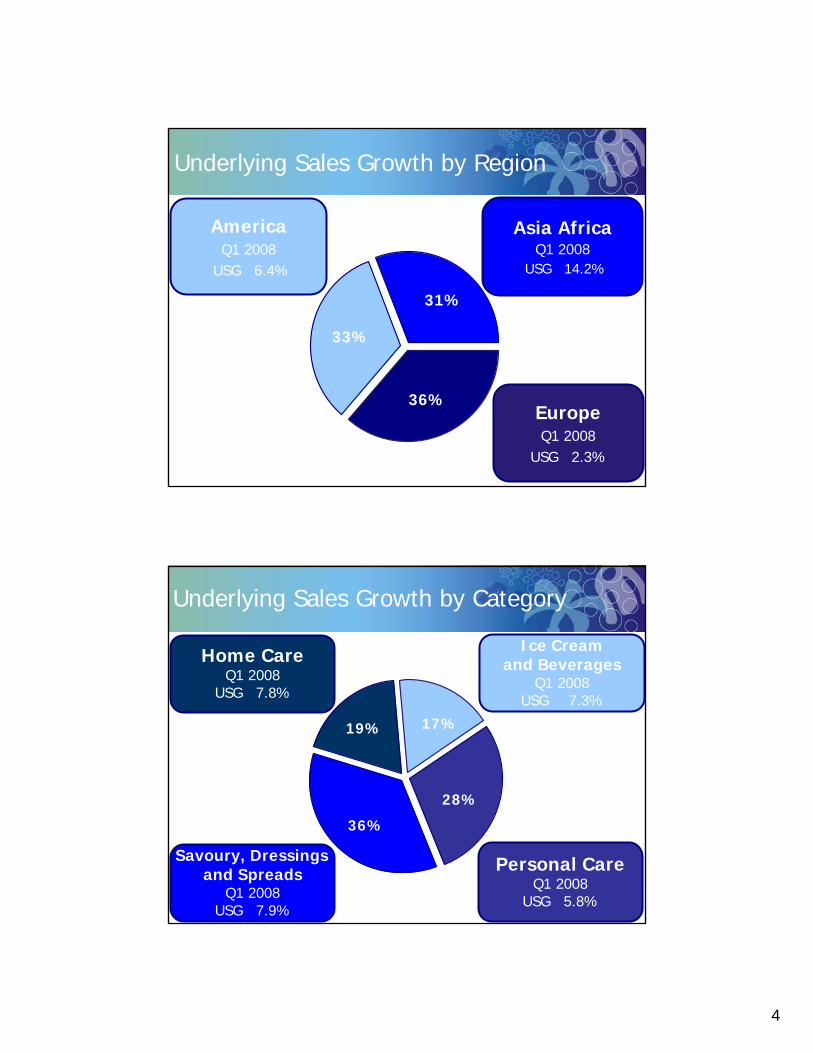

33%

36%

31%

Underlying Sales Growth by Region

AmericaQ1 2008

USG 6.4%

EuropeQ1 2008

USG 2.3%

Asia AfricaQ1 2008

USG 14.2%

Underlying Sales Growth by Category

36%

17%

28%

19%

Ice Cream and Beverages

Q1 2008USG 7.3%

Home CareQ1 2008

USG 7.8%

Savoury, Dressingsand Spreads

Q1 2008USG 7.9%

Personal CareQ1 2008

USG 5.8%

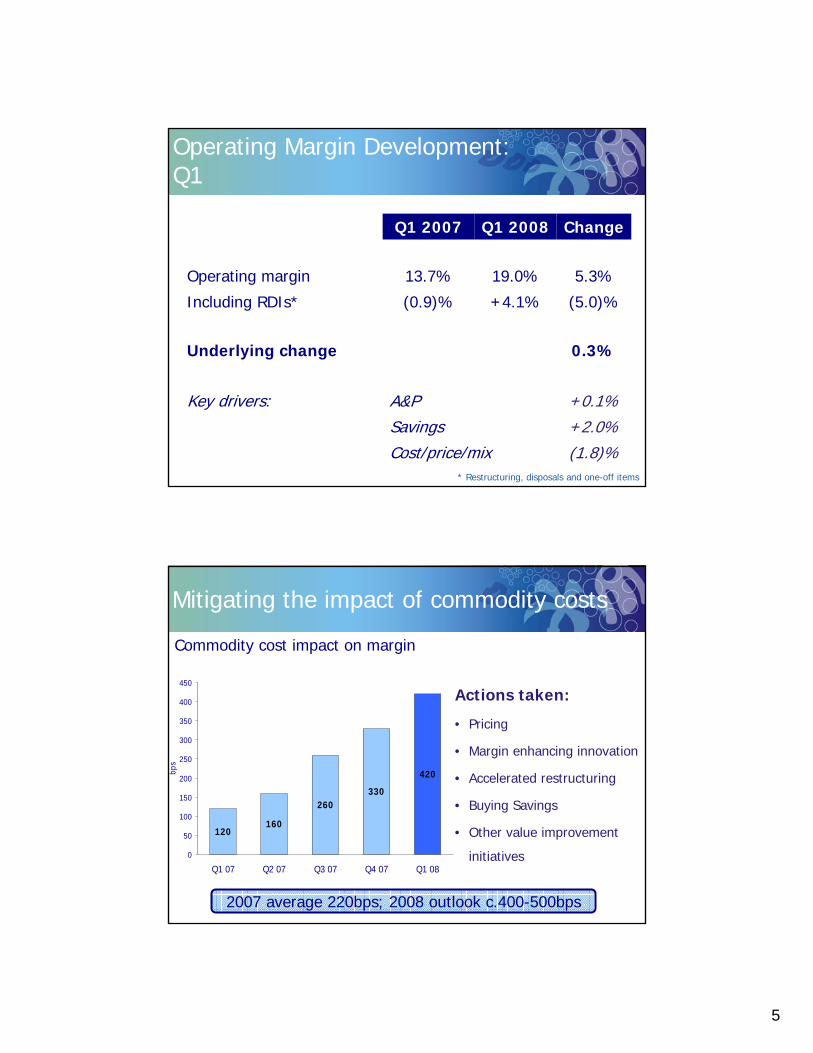

5

(5.0)%+4.1%(0.9)%Including RDIs*

+0.1%A&PKey drivers:

0.3%Underlying change

+2.0%Savings(1.8)%Cost/price/mix

5.3%19.0%13.7%Operating margin

ChangeQ1 2008Q1 2007

Operating Margin Development: Q1

* Restructuring, disposals and one-off items

Mitigating the impact of commodity costs

Actions taken:

• Pricing

• Margin enhancing innovation

• Accelerated restructuring

• Buying Savings

• Other value improvement

initiatives

Commodity cost impact on margin

420

330260

160120

0

50

100

150

200

250

300

350

400

450

Q1 07 Q2 07 Q3 07 Q4 07 Q1 08

bps

2007 average 220bps; 2008 outlook c.400-500bps

6

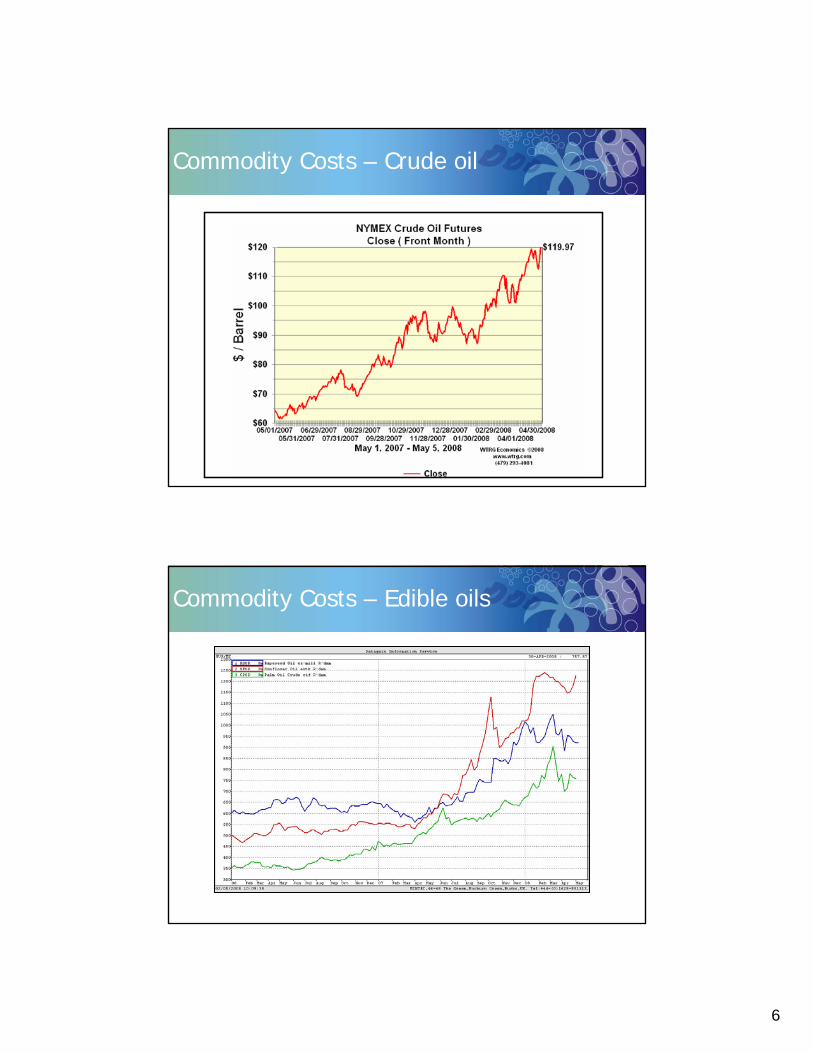

Commodity Costs – Crude oil

Commodity Costs – Edible oils

7

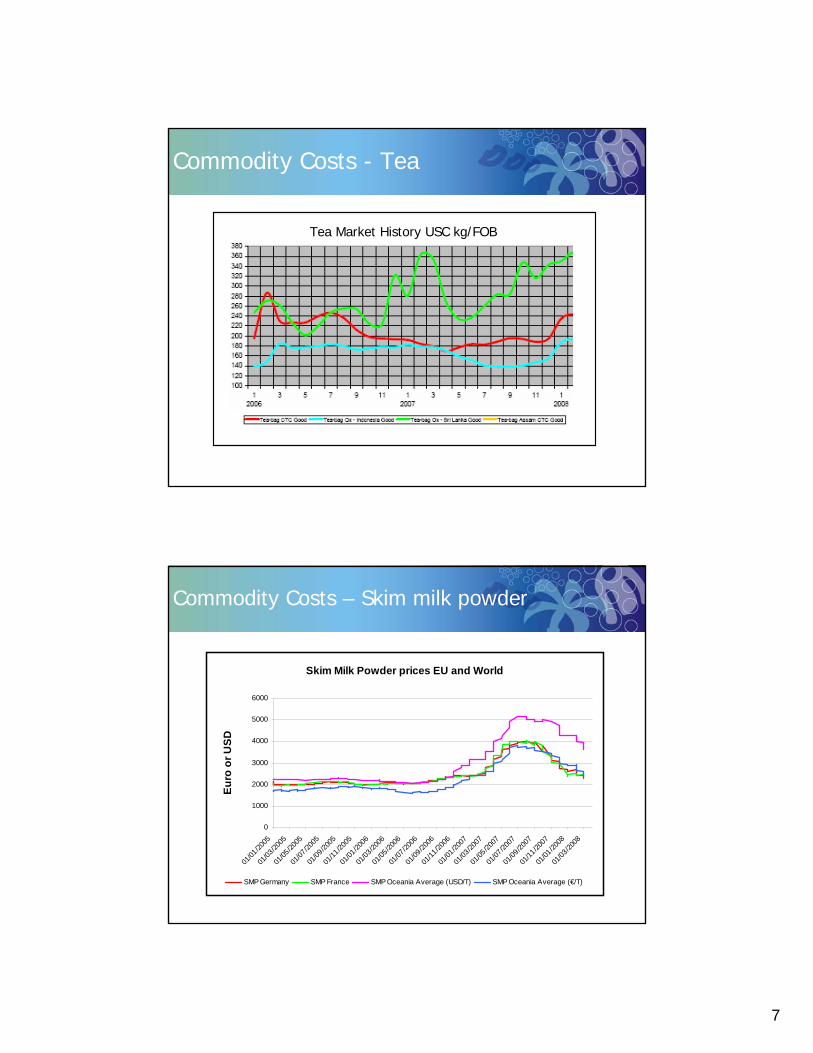

Commodity Costs - Tea

Tea Market History USC kg/FOB

Commodity Costs – Skim milk powder

Skim Milk Powder prices EU and World

0

1000

2000

3000

4000

5000

6000

01/01

/2005

01/03

/2005

01/05

/2005

01/07

/2005

01/09

/2005

01/11

/2005

01/01

/2006

01/03

/2006

01/05

/2006

01/07

/2006

01/09

/2006

01/11

/2006

01/01

/2007

01/03

/2007

01/05

/2007

01/07

/2007

01/09

/2007

01/11

/2007

01/01

/2008

01/03

/2008

Euro

or U

SD

SMP Germany SMP France SMP Oceania Average (USD/T) SMP Oceania Average (€/T)

8

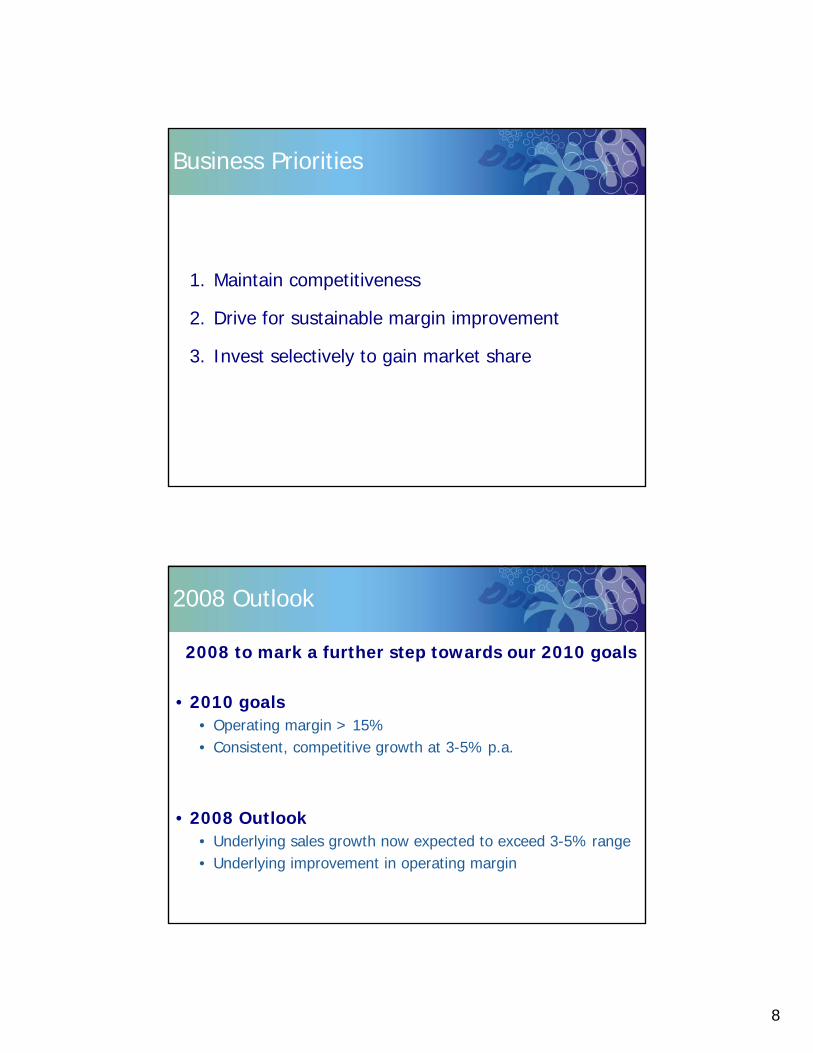

Business Priorities

1. Maintain competitiveness

2. Drive for sustainable margin improvement

3. Invest selectively to gain market share

2008 Outlook

2008 to mark a further step towards our 2010 goals

• 2010 goals• Operating margin > 15%• Consistent, competitive growth at 3-5% p.a.

• 2008 Outlook• Underlying sales growth now expected to exceed 3-5% range• Underlying improvement in operating margin

9

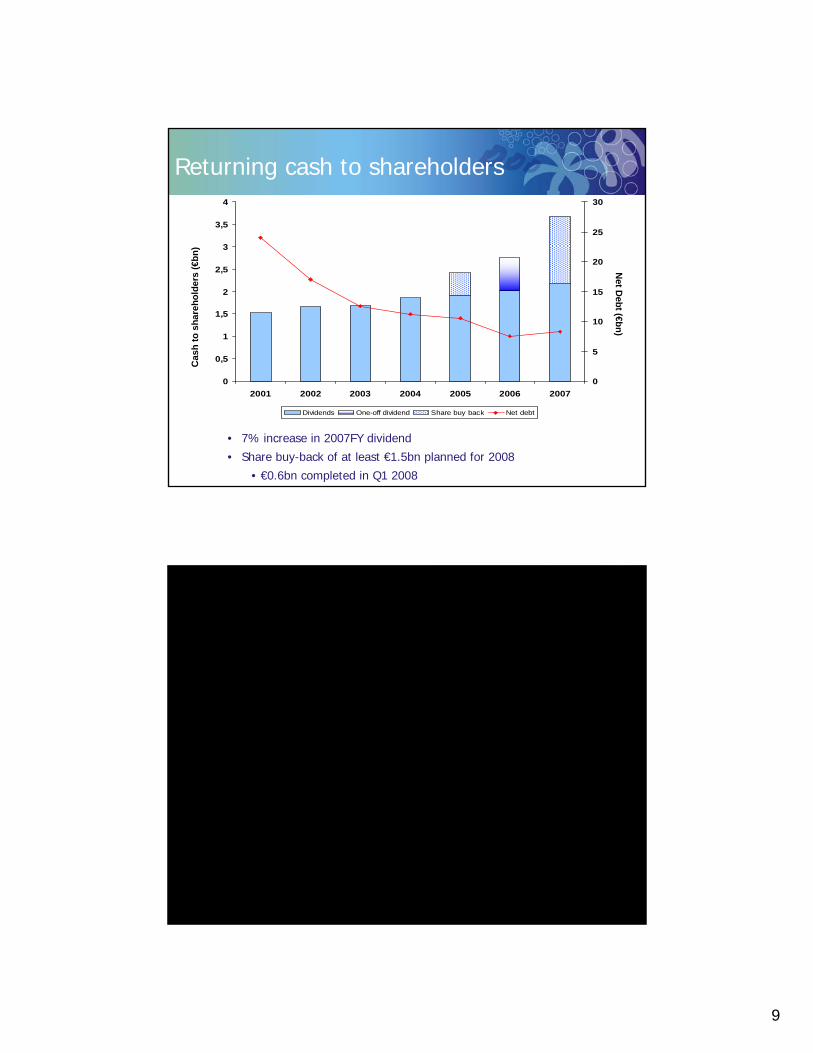

Returning cash to shareholders

• 7% increase in 2007FY dividend

• Share buy-back of at least €1.5bn planned for 2008

• €0.6bn completed in Q1 2008

0

0,5

1

1,5

2

2,5

3

3,5

4

2001 2002 2003 2004 2005 2006 20070

5

10

15

20

25

30

Dividends One-off dividend Share buy back Net debt

Cas

h to

sha

reho

lder

s (€

bn)

Net D

ebt (€bn)

10

Growth Strategy

Strong category positions

Laundry

Household Cleaning

Daily Hair Care

Oral Care

Savoury

Dressings

Ice Cream

Deodorants

Spreads

TeaMass Skin

World Number 1

World Number 2

Local Strength

11

Big global brands

Top 25 brands = ¾ of Unilever’s sales

12 billion euro + brands

Unilever’s strategic priorities

Personal Care D&E Vitality

12

Acceleration of Unilever’s Growth Agenda

•Shaping the portfolio

•Simplification

• Innovation driving growth

Shaping the portfolio

* completed 1 Jan 2008

Disposal

UnderwayNA

Laundry

Acquisitions Indonesia

Fruit Drinks

Russia

Ice Cream

Disposals completed/ announced Brazil Spreads Brands US Seasonings

*

France Cheese

JV Extended Global

RTD Tea

13

Accelerated Restructuring Programme -Simplification

• Organisational simplification• 14 MCOs in place• 4 new MCOs in Europe

- Belgium, Netherlands, Luxembourg- UK, Ireland- Germany, Austria, Switzerland- Czech Republic, Hungary

• Supply chain rationalisation• Streamline or closure of 14 sites

- UK, France, Spain, Sweden, Netherlands, Czech Republic

• Centralisation of European transport management

Accelerated Restructuring Programme –Progress to Date• Savings

• Target of €1.5bn reduction p.a. by end 2010• Achieved €0.3bn in 2007- Other savings realised via buying and local efficiency programmes takes

total savings to €1bn in 2007

• Restructuring Costs• Target of c. 250bps p.a. over 2007-2009: c. €1bn p.a., €3bn total

- €875m charged in 2007, cash outflow of c. €700m

• c. €1bn restructuring charges expected in 2008

• Headcount Reduction• Target of 20,000 reduction by end of 2010

- 5,300 reduction achieved during 2007

• Turnover per employee up by 10% in 2007

14

Innovation Driving Growth

Rapid roll-outs across key markets

Vitality-focused innovation

Faster deployment of new technologies

Transfer of proven mixes

15

Innovation

Clear

Complete antidandruff and scalp care regime

Centrally developed, identically presented simultaneously across China, Brazil, Russia, Arabia and Turkey

16

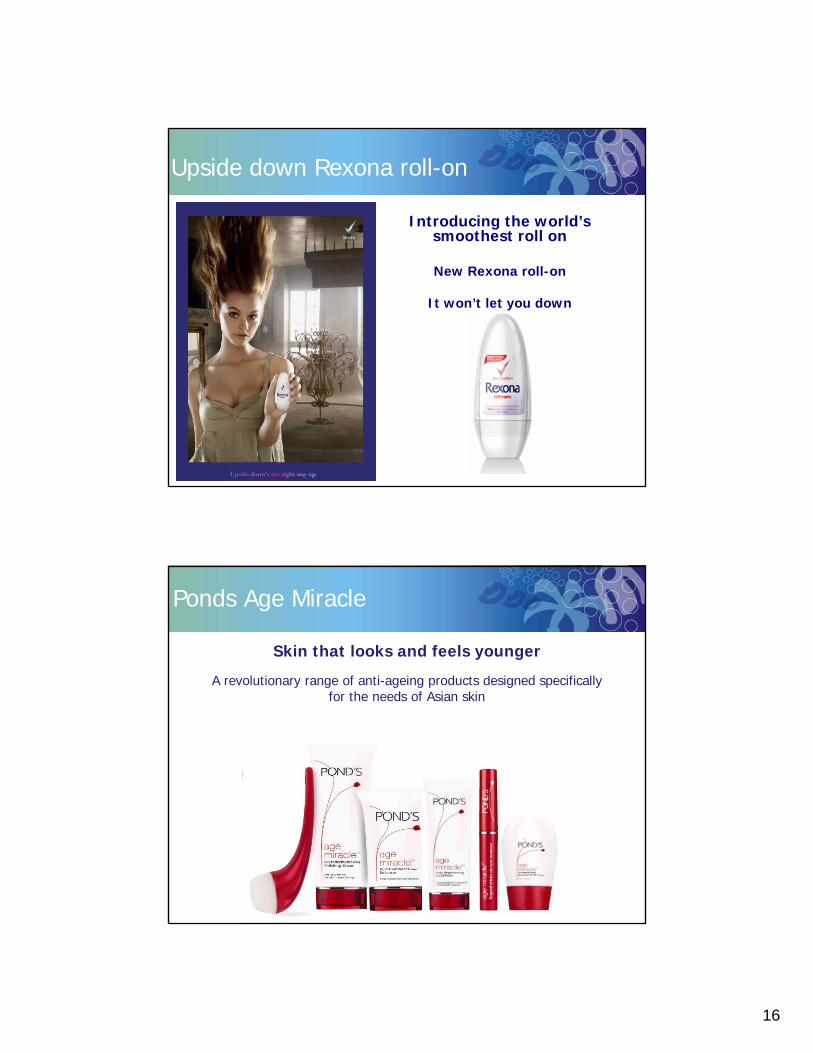

Upside down Rexona roll-on

Introducing the world’s smoothest roll on

New Rexona roll-on

It won’t let you down

Ponds Age Miracle

Skin that looks and feels younger

A revolutionary range of anti-ageing products designed specifically for the needs of Asian skin

17

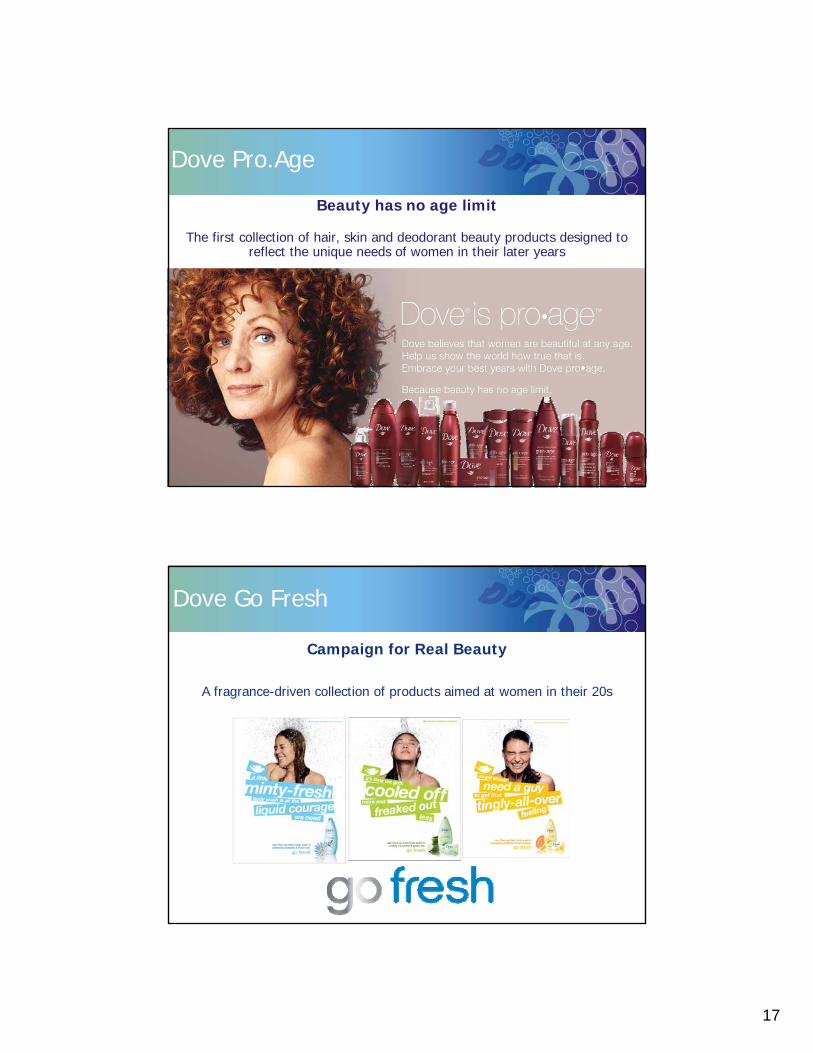

Dove Pro.Age

Beauty has no age limit

The first collection of hair, skin and deodorant beauty products designed to reflect the unique needs of women in their later years

Dove Go Fresh

Campaign for Real Beauty

A fragrance-driven collection of products aimed at women in their 20s

18

Strategy

Comfort Fresh Release

Breakthrough technology to outperform any fabric conditioner

present in the marketplace

Do the moves to release the freshness

Small & Mighty in Europe

A revolutionary 3-times-moreconcentrated laundry detergent

A new breakthrough product with perceivably better cleaning,

and better convenience, at the same price per wash

Cleans a whole wash-load with just one small capful

19

Knorr Bouillon Gel

Launched in China with local insight into soup preparation

Omega 3 plusPacked with more omega 3 than any other spread or

minidrink

pro.activ (Promise activ)Spreads, milk, yoghurt

and mini-drinks clinically proven to lower cholesterol

Heart Health

“Goodness of Margarine”

20

Hellmann’s Light

With unique citrus fibre technology

Delicious extra light mayonnaise now with only 3% fat

Lipton

A unique slimming tea twice as rich in catechins

to help maintain your silhouette

Sustainably sourced tea certified by the Rainforest Alliance

21

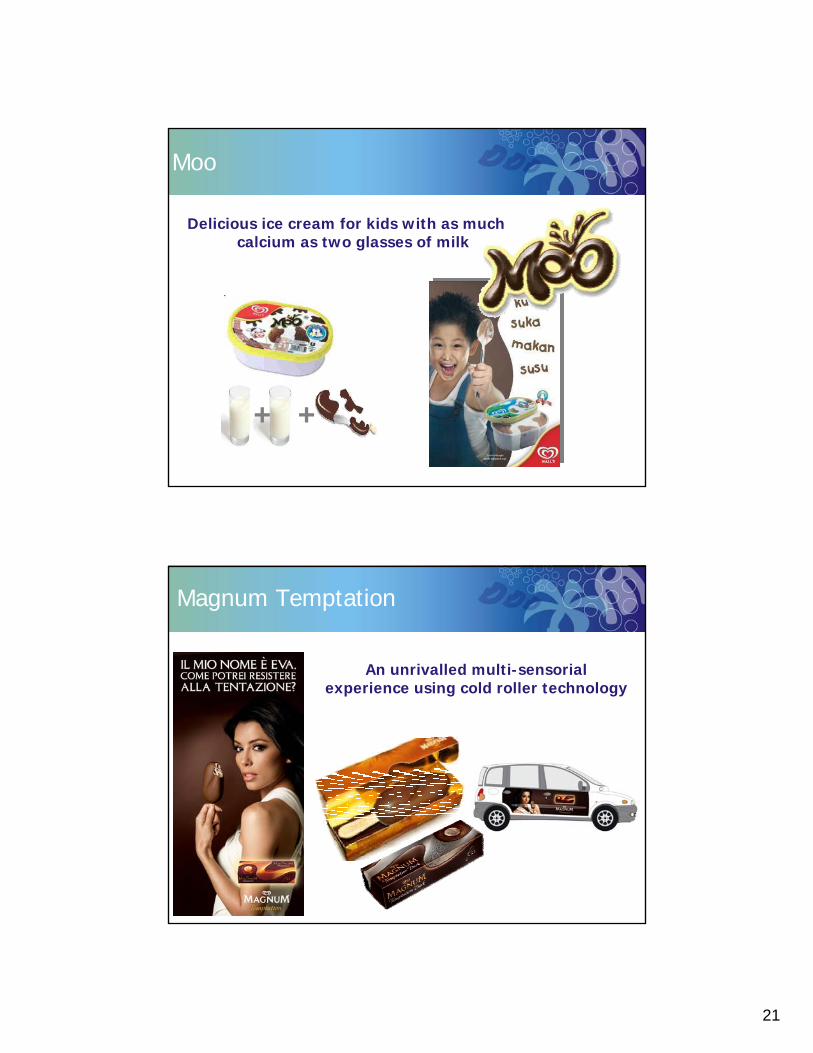

Moo

+ +

Delicious ice cream for kids with as much calcium as two glasses of milk

Magnum Temptation

An unrivalled multi-sensorial experience using cold roller technology