Embed Size (px)

Citation preview

EUR Prev. 2016A Prev. 2017E Prev. 2018E Prev. 2019E

Organic RevGrowth

-- 3.7% -- 3.8% -- 4.1% -- 4.3%

EBIT Margin -- 15.3% 15.7% 16.0% 16.3% 16.8% 16.9% 17.6%

EPS -- 1.88 2.02 2.11 2.22 2.34 2.42 2.59

Div Yield -- 3.30% -- 3.50% -- 3.80% -- 4.10%

FCF Yield

FY Dec -- 4.80% -- 5.30% -- 5.80% -- 6.40%

GBp Prev. 2016A Prev. 2017E Prev. 2018E Prev. 2019E

FY Dec -- 153.34 172.11 180.44 188.63 200.54 206.50 221.92

FY P/E 26.4x 22.4x 20.2x 18.2x

Price Performance

MAR-16 JUL-16 NOV-16 MAR-17

50

45

40

35

^Prior trading day's closing price unlessotherwise noted.

COMPANY NOTE

Target | Estimate Change

Europe | Consumer | Food & HPC 15 March 2017

Unilever NV (UNA NA)A Marmite Stock No Longer. And Still APositive Spread From Here.

EQU

ITY R

ESEARC

H EU

ROPE

BUYPrice target €51.50

(from €44.00)Price €46.10^

Price target 4,490.00p(from 3,700.00p)Price 4,042.00p^

Bloomberg AEX: UNA NABloomberg LSE: ULVR LN

Financial SummaryNet Debt (MM): €10,230.4

Market Data52 Week Range: €46.22 - €36.22Total Entprs. Value (MM): €141,813.6Market Cap. (MM): €131,583.2Institutional Ownership: 77.2%Shares Out. (MM): 2,854.3Float (MM): NAAvg. Daily Vol.: 4,543,914

Martin Deboo *Equity Analyst

+44 (0) 20 7029 8670 [email protected] Letten *

Equity Analyst+44 (0)20 7029 8020 [email protected]

* Jefferies International Limited

Key Takeaway

The NV is up 15% post-KHC and ahead of a review in April. We stay on boardand counsel investors not to underestimate the value of the galvanising shockthat has been administered. Our Buy case assumes faster progress on margins,but not a spin/split, which we think offers insufficient risk/reward from here.But the ultimate end-game remains one of building a New World Order in HPCby acquiring Colgate. April's review should be seen as a staging post to that.

A profound wake-up call, the positive impact of which should not be under-estimated. As the shockwaves abate, the galvanising impact of Kraft's (KHC's) approach forULVR shouldn't be underestimated, in our view. Despite an NV/plc share price up 15%/20%since Feb 16, we continue to see upside from here, with April's review a first staging post.

Buying Colgate our preferred end-game. Argues for a 'keep and improve'stance in April. We identify 3 end-games for ULVR, of which building a New World Orderin HPC (via Colgate) is most attractive. We project fair value across 4 scenarios of €53-€56per share, but it's a stretch without disposals. Better, we think, to hold on to non-HPC assets,in pursuit of selling a control premium later, when the time is right to pay for one on Colgate.

Upgrading stand-alone numbers to top-end of current margin guidance.Results in FY19E EPS of €259c (€279c inc. buyback). In the meantime, and witheyelids suitably fluttered at CAGNY, ULVR need to demonstrate renewed impetus on costs.We think progress beyond the top end of 40-80bps margin guidance would be a stretch.But even that offers a 7% EPS uplift by FY19 (relative to our previous high-end numbers &a 15% uplift including a €6bn annual buyback), with growth in EPS/FCF of 11%/12% paalong the way. Which can be owned for the current 21.3x PER, relative to NESN 21.0x, P&G22.5x & Colgate 24.8x.

No further upside from a spin. Costs as well as benefits. We have been advocatesof a spin/split...until we counted the costs. While we can scope an incremental c.€10bnof benefit from a spin (of Foods or Foods & Refreshment), predicated on improved valuediscovery, plus an indicative €2.75 special dividend, we also scope c.€10bn costs to achieve.The risk/reward feels unattractive and there is an opportunity cost in the form of a controlpremium foregone on any eventual sale.

Valuation/RisksOur PT of €51.50 reflects a target 15x EBITDA (was 14x) which equates to 21.6x PER, adiscount to peers at 22.8x. Risks include i.) EM demand ii.) fx.

Please see analyst certifications, important disclosure information, and information regarding the status of non-US analysts on pages 52 to 56 of this report.

Contents SCENARIOS SUMMARY ........................................................................................................................ 3 A WAKE-UP CALL THAT IS FUNDAMENTALLY GOOD NEWS FOR INVESTORS ......................................... 4

A profound shock… ............................................................................................................................4 …that is likely to inspire more radical and decisive action .................................................................4 A significant and valuable catalyst for change internally ..................................................................4 Working back to April from three distinct end-games .......................................................................6 Allowing for ULVR’s belief system .....................................................................................................7

VALUE ON THE TABLE, DESPITE RAISED BAR ........................................................................................ 8 Shares up by 15%/20% since the approach .......................................................................................8 Raises the bar to additional value creation relative to undisturbed price .........................................8 Footnote: what is ULVR’s market cap? ............................................................................................10

MOVING TO THE TOP END OF MARGIN GUIDANCE. BUT CAUTIOUS BEYOND THAT ............................ 11 ULVR’s cost base: myth and reality .......................................................................................................11 SG&A efficiency not best-in-class, but not dramatically out-of-line of either .......................................11 But progress on SG&A reduction limited to date..................................................................................12

UK case study: steady work in a mature market .............................................................................13 Seeing margin progress beyond upper bound of current guidance as a challenge...............................15

ZBB programme suitably aggressive ...............................................................................................15 Not a conspicuously under-earning business relative to mix ...........................................................16

Upgrading stand-alone forecasts to the top end of guidance range. Modelling a return to Buybacks .20 Upgrading margin forecasts to the top end of the current guidance range ....................................20 Scoping a potential €18bn cumulative buyback to 2019 .................................................................20 Stand-alone forecast scenarios summary ........................................................................................21

NO FURTHER UPSIDE FROM A SPLIT, ONCE COSTS & COMPLEXITIES ARE WEIGHED ............................ 23 The case for a split ................................................................................................................................23

Questionable returns from scale and diversification .......................................................................23 But costs as well as benefits ............................................................................................................23 Potentially significant upsides: Cadbury & other case studies .........................................................24

Material potential upsides for ULVR from enhanced valuation perception, prior to any costs ............26 Still unconvinced by the synergy arguments in Developed Markets ....................................................28

UK case study: largely un-integrated other than back office? .........................................................29 Separation in the UK un- problematic, with scale diseconomies limited .........................................30

But Emerging Markets more complicated ............................................................................................31 India case study: manufacturing separability, distribution complexity............................................32

Options for a split: Gradations of Foods, DM’s vs. EM’s. The question of Refreshment .......................34 The complexity of Foods ..................................................................................................................35 The question of Refreshment...........................................................................................................36 Appraising the split options .............................................................................................................36

Limited upsides from here, once the costs and risks are properly weighed? .......................................37 Modelling two spin scenarios with a target multiple of 16.2x EBITDA ............................................38 Scoping €10-12bn of offsetting value destruction ...........................................................................38 Scoping a special dividend of €2.75 per ULVR share ........................................................................38 Limited upsides relative to our base case ........................................................................................39

ACQUIRING COLGATE ........................................................................................................................ 41 Potential ULVR/CL combinations .....................................................................................................41

Strong strategic logic ............................................................................................................................41 Good strategic fit. Competition issues manageable ........................................................................41

Modelling a deal ...................................................................................................................................43 Valuation gap currently relative unattractive .................................................................................43 Colgate, Unilever and Universal merger assumptions .....................................................................43 Colgate assumptions .......................................................................................................................43

Resultant accretion & impact on ULVR .................................................................................................44 Implications on leverage and return ................................................................................................44 Earnings accretion & valuation .......................................................................................................44 Colgate not realistically do-able for cash without offsetting disposals............................................44 Towards a pure play HPC business ..................................................................................................44 Scenario impact on geographic mix ................................................................................................45 Puts combined entity on a potentially compelling valuation ...........................................................45 No ULVR disposals sensitivity analysis .............................................................................................46 Colgate plus ULVR Foods disposal sensitivity analysis .....................................................................47 Colgate plus ULVR Foods & Refreshment disposal sensitivity analysis ............................................48

CHANGES TO FORECASTS .................................................................................................................. 49 DIVISIONAL SALES & MARGIN DRIVERS ............................................................................................. 49 DETAILED FINANCIAL FORECASTS ...................................................................................................... 50

UNA NA

Target | Estimate Change

15 March 2017

page 2 of 56 , Equity Analyst, +44 (0) 20 7029 8670, [email protected] Deboo

Please see important disclosure information on pages 52 - 56 of this report.

Scenarios Summary

Summary of Scenarios

New stretch case is basis for published PT of €51.50 on a rounded basis

Scenario Previous

forecast

& PT

New

Stretch

case

Stretch case

plus

buyback

Spin out

Foods/Foods

& Refresh,

plus Special

Div

Buy Colgate

for cash - no

disposals

Buy Colgate -

with new

equity

Buy Colgate -

dispose

Foods

Buy Colgate -

dispose Foods

& Refresh

Key metrics,

events &

assumptions

As published

27 Jan

80bps pa

margin

progress to

FY19 (FY19

margin 17.6%)

As previous

plus Euro 6bn

pa buyback to

FY19 (net

debt:EBITDA

2.0x)

Foods and/or

Foods &

Refreshment

spun out.

€2.75 special

div.

Net

debt:EBITDA

post-deal of

5.1x

New ULVR

equity

equivalent to

13% of total.

Net debt:

EBITDA 4.0x

Sell Foods for

11x EBITDA

Sell Foods &

Refreshment for

13x EBITDA

NV EPS (Euros)

FY16A 188 188 188

FY17E 202 211 213

FY18E 222 234 244 213 297 275 240 234

FY19E 242 259 279

CAGR 19 vs. 16 9% 11% 14% n/a n/a n/a n/a n/a

Net debt:EBITDA1 0.8x 0.7x 1.8x 1.5x 5.1x 4.0x 3.8x 1.6x

Valuation metrics

Projected price

per NV share

44.00 51.60 50.89 48.50 55.98 54.84 53.00 53.75

EV:EBITDA 14.0x 15.0x 15.0x 16.2x 15.6x 15.6x 16.5x 16.6x

PER 19.8x 21.6x 20.4x 22.7x 18.9x 20.0x 22.1x 23.0x

FCF yield 4.2% 3.9% 4.0% n/a n/a n/a n/a n/a

Valuation metrics at current share price (prospective 12 mths basis)

EV:EBITDA 15.3x 14.6x 14.6x n/a n/a n/a n/a n/a

PER 22.5x 21.2x 20.9x n/a n/a n/a n/a n/a

FCF yield 4.0% 4.5% 4.5% n/a n/a n/a n/a n/a

Source: Jefferies analysis & estimates 1 FY18 basis for comparability. Colgate scenarios exclude synergies i.e. leverage is pro-forma peak immediately after acquisition

UNA NA

Target | Estimate Change

15 March 2017

page 3 of 56 , Equity Analyst, +44 (0) 20 7029 8670, [email protected] Deboo

Please see important disclosure information on pages 52 - 56 of this report.

A Wake-Up Call That Is Fundamentally

Good News for Investors ‘This has certainly been a trigger moment for Unilever and we will not waste it’

Graham Pitkethly, ULVR CFO

A profound shock…

We return to the Unilever (ULVR) beat, in anticipation of their strategic review due in April

and in profoundly altered circumstances to those prevailing prior to February 17, the day

when ULVR received an initial bid approach from Kraft Heinz (KHC).

Our bullishness on ULVR notwithstanding, it’s fair to say that a bid for the company

wasn’t on our radar, or was part of our Buy case. Nor, evidently, was it on ULVR’s radar

either. The shock – of being the subject of a bid of any kind, let alone one from such

arrivistes as KHC/3G (the horror, the horror) – will have been profound. And will no doubt

still be resonating around the walls of 100 Victoria Embankment (100VE), ULVR’s mighty

bastion on the banks of the Thames.

Any initial humiliation has been on the Kraft Heinz (KHC)/3G side. The collapse of their

approach within 48 short hours has left their reputation for sharp and persistent deal-

making and bear-hugging damaged. Their $50 per share offer looked less an invitation to

treat and more a piece of hastily-contrived opportunism. One that was a long way short

of what would have been required to engage shareholders. They would appear to have

under-estimated both ULVR’s strategic and economic significance in Europe and the likely

complexities of seizing control of a dual-listed entity, with strong roots in Holland, a

nation with a more muscular model of stakeholder capitalism than the UK. The fawning

obsequieties of KHC’s walk-away notice must have been painful to pen.

But neither has the experience been comfortable for ULVR either. Their reluctance to be

more aggressive towards their cost base had left their P&L dangerously vulnerable to

arbitrage from an alternative owner with radically different cultural norms and margin

aspirations. An unleveraged balance sheet meant that a less well-capitalised buyer could

contemplate acquiring control, by utilising ULVR’s own debt capacity. A diverse portfolio

left plenty of potential to reduce that debt with subsequent asset disposals.

…that is likely to inspire more radical and decisive action

KHC’s incursion will mean that all three of the above issues (which have all been germane

to the shareholder debate on ULVR in the decade that this analyst has covered the stock)

must now be re-addressed. Whatever conclusions are ultimately reached, this must surely

be both good and healthy.

Such dilemmas have conditioned this analyst’s views over the years. In September 2014

we were Sellers of ULVR on the grounds of frustration with slow progress on margins and

over-dependence on slowing Emerging Markets. In January 2016 we kicked the tyres on

ZBB and found the targets to be credible. But our confidence in the willingness to do the

hard yards on cost was wanting. In December 2016 we turned Buyers, predicated on

ULVR’s growing confidence in delivery a year down the track and a depressed stock price.

But we would be lying if we didn’t confess to feeling a certain tremulousness in our new

found conviction, something which the weak Q4 did little to dissipate.

A significant and valuable catalyst for change internally

ULVR now has precisely the catalyst it needed to shift the terms of debate internally and

align the culture with more radical action. This can and should be a firm-wide process.

The tendency at times like these is to see the actors in the drama as those on the Board

and ExComm. They will be the lead players, sure enough. But change and improvement

only washes through an organisation of 170,000 employees if there is buy-in to the goals

and imperatives at the middle and bottom of the organisation.

We return to ULVR post the KHC

approach

We think this will have been a

profound shock to ULVR

Any initial embarrassment was on

the KHC side

But the experience has highlighted

ULVR’s vulnerabilities too

We expect the event to prompt more

decisive action on costs and margins,

a recurring source of frustration for

us

UNA NA

Target | Estimate Change

15 March 2017

page 4 of 56 , Equity Analyst, +44 (0) 20 7029 8670, [email protected] Deboo

Please see important disclosure information on pages 52 - 56 of this report.

Prior to 17 February it’s conceivable that this buy-in wasn’t as strong as it might have

been. ULVR’s white collar troops were being realigned into the new Connected For

Growth (‘C4G’) organisational structure, which gelled as recently as last December. A

structure that demands new ways of working and different reporting lines. This on the

back of the long march from a region-led, to a category-led, organisation that has been

underway for the past decade and a half. On top of this has come Zero-Based Budgeting

(ZBB), a source of both incremental workload (all those tiresome task force meetings) and,

no doubt, some challenge to the level of individual perquisites that do so much to ease

the stresses of the working day. Down on the shop floor, it’s been only five years since

ULVR’s sizeable UK workforce were on strike over curtailed pension benefits.

Our sense has been that both C4G and ZBB have been placing additional burdens on an

already change-weary organisation. So they might be expected to encounter some

pushback. But now any recalcitrance has been met with a counterfactual and counter-

cultural vision of the most dramatic kind.

Ratings and feedback on ULVR & KHC from glassdoor.com corroborate the anecdotes that

have featured in the newspapers over the past two weeks. These are two companies that

couldn’t be more different in terms of internal cultural norms and morale.

Exhibit 1: ULVR vs. KHC employee feedback on glassdoor.com

ULVR KHC

Sample size 2,251 2,145

Would recommend to a friend 81% 29%

Approve of CEO 94% 28%

Positive Business Outlook 68% 26%

Satisfaction scores (where 5 is best)

Culture & values 4.0 2.2

Work/life balance 3.5 2.1

Senior Management 3.3 2.1

Compensation & benefits 3.5 2.9

Career Opportunities 3.5 2.7

Overall score 3.8 2.5

Trend in overall score Up Down

Source: glassdoor.com; Jefferies analysis

Exhibit 2: Verbatim reviews from glassdoor.com

ULVR KHC

Positive ‘Fantastic brands. Great People. Collaborative, friendly, culture.

International scale. High integrity. True to their sustainability

mission.'

‘People are great. Brands are strong. Opportunities to work across

departments and develop knowledge and skills in Grocery. Have

become more shopper-focussed over time.'

‘Beautiful office. Nice perks. Nice canteen. Exposure to senior

stakeholders. Systems generally work well. Professional atmosphere.

Prestigious company to work for.’

‘Fast growth opportunity. Lean structure. Easy to be noticed.’

‘Good work culture. Smart people.’ ‘Culture is very specific and not for everyone.’

Negative/critical ‘A huge company with all the complexity and politics you would

expect.’

‘The merger completely killed the culture of a great CPG company.’

‘Be prepared for plenty of structured processes and lots of

stakeholder management.’

‘An unsustainable business model…cutting costs to the point where

some functions barely run.’

‘The same English & Dutch ‘club’ that got us here may not be the

right one to take us to the next level.’

‘Haphazard leadership and dysfunctional culture. 3G mantra

inspirational in theory but in practice targets unachievable and

leadership style brutal - miss your number and you are exited, which

happens regularly.’

Source: glassdoor.com; Jefferies analysis

The value of the KHC approach as an

internal catalyst for change will have

been enormous

glassdoor.com ratings illuminate the

cultural divide

UNA NA

Target | Estimate Change

15 March 2017

page 5 of 56 , Equity Analyst, +44 (0) 20 7029 8670, [email protected] Deboo

Please see important disclosure information on pages 52 - 56 of this report.

The implication for the typical mid-level ULVR staffer is clear. Prior to February 17 he or

she was no doubt cavilling, as one might, over the level and pace of disruption to their

internal comfort zone that C4G and ZBB was requiring. Now they have been invited to

contemplate a fate worse than 10,000 deaths. The impact will be electrifying. Not since

the dark days of 2004/2005 will senior management have enjoyed such latitude to drive

change and raise the level of expectation. They must make the most of it.

Working back to April from three distinct end-games

So rather than focus on the April review in isolation, we think it’s appropriate to start by

outlining what we think are the long term strategic end games for ULVR. We then propose

to work back from there to what they might say in April. We think there are three such

end-games, per Exhibit 4.

We think these end games both gel the debates unfolding in the market as we write and

highlight the choices that need to be made by ULVR. As it happens we don’t think the

choices have fundamentally altered since February 17. But the urgency of confronting

them, and the need for decisive and credible action, has.

Exhibit 3: Potential strategic end-games for ULVR

Source: Jefferies

And so to ULVR’s April review. Investors are right to fixate on it and the sequential market

announcements made on 22nd February have raised the level of anticipation. But we

would urge investors to keep those expectations in check: ULVR in our experience is a

conservative company that is managed for long term value, in harness to a longer term

vision and purpose.

1. Optimise & bid-proof the broad status quo

2. Split the business3. Build a New World

Order in HPC

End games for ULVR

• Increased aggression on costs & margins

• Pursue enhanced cash returns

• Continue to reposition portfolio incrementally in favour of HPC, most obviously via a spin-out of Spreads

• Spin out the Foods business as a separate listing

• Buy Colgate (or RB as a secondary option)

• Fund via a sale or carve-out of Foods

Both these options incremental to (1)Question mark over Refreshment in both scenarios

Choices

Questions

• How much harder can margins be pushed?

• How big a cash distribution?

• What is there left to sell short of a complete exit from Foods?

• Would a split create net incremental value?

• Is Refreshment a keep or a spin?

• Is there a strategic logic?• Would a ‘megadeal’ create

value?• Is there a strategic buyer

for Foods/Refreshment?

Having contemplated a fate worse

than 10,000 deaths, ULVR’s body

politic should have been galvanised

We counsel a focus on the ultimate

end-game for ULVR, not just April’s

review

But we do think that the urgency of

resolving the ultimate end-game has

increased

UNA NA

Target | Estimate Change

15 March 2017

page 6 of 56 , Equity Analyst, +44 (0) 20 7029 8670, [email protected] Deboo

Please see important disclosure information on pages 52 - 56 of this report.

If that longer-term vision is, for example, to acquire a Colgate and build a New World

Order in HPC, then we think we are unlikely to see that unveiled in April. But, should it be

the vision, any announcements made in April mustn’t preclude it and must be consistent

with it. Otherwise ULVR will lay themselves open to the charge of precipitate behaviour

that was famously levelled at Cadbury in 2007, by senior fund manager Anthony Bolton,

as they took the decision to split their business in response to activist pressure.

Allowing for ULVR’s belief system

What end-game ULVR might choose is partly a function of analysis and hard-headed

calculation. But it will also be a function of the belief system that operates within ULVR,

one that we think reflects a strong sense of mission, inclines to scale and business

diversity, rather than focus, and which reflects strong fiscal conservatism. None of this is

to argue that ULVR won’t be feeling the need to change and evolve. But is to argue that

the choices will be carefully weighed, and that long-standing beliefs won’t be abrogated

by current exigencies. What we think of the belief system is essayed below.

Belief in the virtue of independence for its own sake. The vehemence of the

response to the KHC approach signals strongly that ULVR want to retain their

independence. Any company, performing basically well, and faced with a lowball offer,

would have responded similarly. But we sense that the desire to remain independent runs

deeper within ULVR than in most companies. Not, we would suggest, for venal or self-

seeking reasons amongst the current Board and Senior Management team. But because of

the sense of purpose and manifest destiny that arises from ULVR’s long history and deep

values. Much has been made over the past two weeks around the similarities with the

Cadbury take-out in 2009/10. But then Cadbury Chairman Roger Carr said at the outset

that the debate ‘would be about (shareholder) value, and only value.’ While Cadbury

fought hard and nobly for its independence, the implication was that the company was

always for sale at the right price. We question whether we will be hearing similar rhetoric

from ULVR Chairman Marijn Dekkers. The implication is that ULVR will be wary of moves,

most obviously a split, that would make it more vulnerable to takeover.

Belief in the value of multi-category scale and risk diversification. This analyst

has argued consistently that there are limited returns to multi-category scale in Developed

Markets with a strong, consolidated Modern Trade. The case will be argued again later in

this note. Your analyst was also taught at the London Business School that ‘investors can

diversify risk more cheaply and efficiently than managers.’ ULVR, by their actions and

commentary, would appear to dance to a different drum. We might not like the beat, but

we think that they are sincere in their adherence to it. The implication, similar to the point

above, is that ULVR will be relatively reluctant to shrink its portfolio too aggressively.

A ‘DCF’, rather than earnings, mindset. ULVR’s M&A culture, on both the sell and

buy-side of deals, reflects in our experience a strong mindset around value to the

company versus value to the acquirer/vendor, reflecting Discounted Cash Flow (DCF)

analysis. The most obvious example of this has been the apparent reluctance to

contemplate a sale of the Spreads business on the grounds that it is an important

generator of cash. The implication is that ULVR don’t, or won’t evaluate deals purely on

the basis of earnings accretion/dilution and will be relatively resistant to the sort of EPS

‘grandstanding’ that might arise from a return to buybacks of pursuit of ‘megadeals’ that

are light on strategic logic and economic synergy.

A conservative approach to the balance sheet. ULVR have struck a consistently

conservative tone on balance sheet management and CEO Paul Polman has voiced his

dislike of buybacks, despite almost continuous pressure from elements in the investment

community to adopt them (on which score this analyst agrees with ULVR). ULVR hasn’t

had a buyback programme in place since 2008 and net debt:EBITDA has been below 1x

for more than 50% of the time over the past twenty years. This is not so say that ULVR

won’t gear up for the right big acquisition (they were briefly >3x net debt:EBITDA post-

Bestfoods in November 2000) or that they won’t consider buybacks as a defensive

response to a bid. But we think they will weigh carefully the risks as well as the benefits.

ULVR need to avoid seeming

precipitate or reactive

UNA NA

Target | Estimate Change

15 March 2017

page 7 of 56 , Equity Analyst, +44 (0) 20 7029 8670, [email protected] Deboo

Please see important disclosure information on pages 52 - 56 of this report.

Value on the table, despite raised bar Shares up by 15%/20% since the approach

The previous section has argued that KHC’s intervention has been unequivocally good

news for ULVR shareholders. The complication is that the good news is directionally in the

price, with the NV and PLC listings up 15% and 20% respectively relative to the close on

16 February. Relative to which we are upgrading our FY17 forecasts by c.5% to reflect

both the margin guidance upgrade of 22 February and slightly better fx.

Exhibit 4: ULVR NV forecasts & valuation pre- & post-KHC

As at 13 March. Prospective 12 mths. basis. Now reflects fx & 22 Feb guidance upgrade

16 Feb Now

NV share price €39.57c €45.60c

Market value

Market cap €110275m €129490m

Net debt (end FY17) €10511m €10230m

IAS19 deficit (end FY17) €2902m €2902m

Gross EV €123688m €142622m

Less JV's & Associates at fair value (€3283m) (€3100m)

Add non-controlling interests at fair value €16391m €16311m

Adjusted EV (for EV:EBITDA purposes) €136796m €155833m

Forecast metrics (NTM basis)

EBITDA €10073m €10546m

EPS €202.5c €214.3c

DPS €132.3c €134.9c

FCF per share €183.0c €202.0c

Valuations (NTM basis)

EV:EBITDA 13.6x 14.8x

PER 19.5x 21.3x

Dividend yield 3.3% 3.0%

FCF yield 4.6% 4.4%

Source: FactSet; Jefferies analysis

Raises the bar to additional value creation relative to undisturbed price

The impact has been to add more than a turn to ULVR’s Enterprise multiple, nearly two

turns to PER and to reduce both dividend & FCF yield by 20-30bps. So any contemplation

of what might be on the table in April needs to be compared to this higher hurdle.

Or should it? The counter-argument, advanced by some in the market, and ULVR

themselves at CAGNY the other week, is that the valuation immediately prior to KHC was

at some sort of unreasonable trough. Indeed, at that point, the NV share price had come

down by 7% from its 12 month high (achieved in early September 2016) of €42.70. This

equated to a PER of 22.4x, relative to only 19.5x on 16 February.

We’re not persuaded by this argument (of unreasonableness), for a couple of reasons.

First, almost all of ULVR’s share price decline was a function of the defensive counter-

rotation that occurred in October and November 2016: ULVR’s share price relative to the

SX3P (EuroStoxx Food & Beverage index) barely moved from early September to February

161. Second, the price on 16 February was the price of what is a well-researched and well-

understood stock. Sure we might have disagreed with it, having a Buy recommendation

and a then price target of €44. But that was just one opinion, in an efficient market.

1 ULVR fell by 3-4% relative to the SX3P on the weak Q4 on 26 January. This loss had been

regained by Feb 16, reflecting we think the subsequent weak Q4 across the sector

The NV & PLC listings are up 15% &

20% since 16 Feb

This has added more than 1 turn of

EBITDA & nearly 2 turns of PER to

valuation

We are not persuaded by the

argument that ULVR was

anomalously cheap on 16 Feb

UNA NA

Target | Estimate Change

15 March 2017

page 8 of 56 , Equity Analyst, +44 (0) 20 7029 8670, [email protected] Deboo

Please see important disclosure information on pages 52 - 56 of this report.

Exhibit 5: PER vs. EPS growth

Prospective 12-24 months1, per consensus. As at 9 March

Source: FactSet; Jefferies analysis 1 EPS growth is 12-24 mths out (‘2TM’) to minimise fx distortions

Exhibit 6: PER vs. organic sales growth

Prospective 12 months, per consensus. As at 9 March

Source: FactSet; Jefferies analysis

Exhibit 7: EV:EBITDA vs. organic profit growth

Prospective 12 mths., per consensus. Adjusted for JV’s & minorities

Source: FactSet; Jefferies analysis

Exhibit 8: EV: operating cashflow vs. organic profit growth

Prospective 12 mths., per consensus. Adjusted for JV’s & minorities

Source: FactSet; Jefferies analysis

Exhibit 9: EPS growth vs. FCF yield

Prospective 12 months, per consensus. As at 9 March

Source: FactSet; Jefferies analysis

DGE

RI

BFI

RCO

BATS

PMIMO

RAI

ULVR - consNESN

BN

RBPG

CLOR

HEN3

BEI

ABI

HEIA

CARL.B

ULVR - JEFe

16.0x

18.0x

20.0x

22.0x

24.0x

26.0x

28.0x

30.0x

6% 8% 10% 12% 14%

PE

R

EPS growth in reporting currency

DGE

RI

BFI

RCO

BATS

IMB

PMI

MORAI

ULVR - consNESN

BN

RBPG

CL

OR

HEN3

BEI

ABI

HEIACARL.B

ULVR - JEFe

12.0x

14.0x

16.0x

18.0x

20.0x

22.0x

24.0x

26.0x

28.0x

30.0x

0% 2% 4% 6%

PE

R

Organic sales growth

DGERI

BFI RCO

IMB

PMIMO

RAIULVR - cons

NESN BN

RBPG

CL

OR

HEN3

BEIABI

HEIA

CARL.B

ULVR - JEFe

8.0x

10.0x

12.0x

14.0x

16.0x

18.0x

20.0x

0% 2% 4% 6% 8% 10% 12%

Ad

just

ed

EV

:EB

ITD

A

Organic profit growth next 12 mths.

DGE

RI

BFI

IMB

PMI

MO

RAI

ULVR - cons

NESN

BN

RBPG

CLOR

HEN3

BEI

ABI

HEIA

CARL.B

ULVR - JEFe

10.0x

15.0x

20.0x

25.0x

30.0x

35.0x

40.0x

45.0x

0% 2% 4% 6% 8% 10% 12%EV

: o

pe

rati

ng

ca

shfl

ow

po

st c

ap

ex

& t

ax

Organic profit growth next 12 mths.

DGE

RI

BFI

RCO

BATS

IMB

PMI

MO

RAI

ULVR - consNESN

BN

RBPG

CLOR

HEN3

BEI

ABIHEIA

CARL.B

ULVR - JEFe

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

4% 5% 6% 7% 8% 9% 10% 11% 12% 13% 14%

FC

F y

ield

EPS growth in reporting currency

UNA NA

Target | Estimate Change

15 March 2017

page 9 of 56 , Equity Analyst, +44 (0) 20 7029 8670, [email protected] Deboo

Please see important disclosure information on pages 52 - 56 of this report.

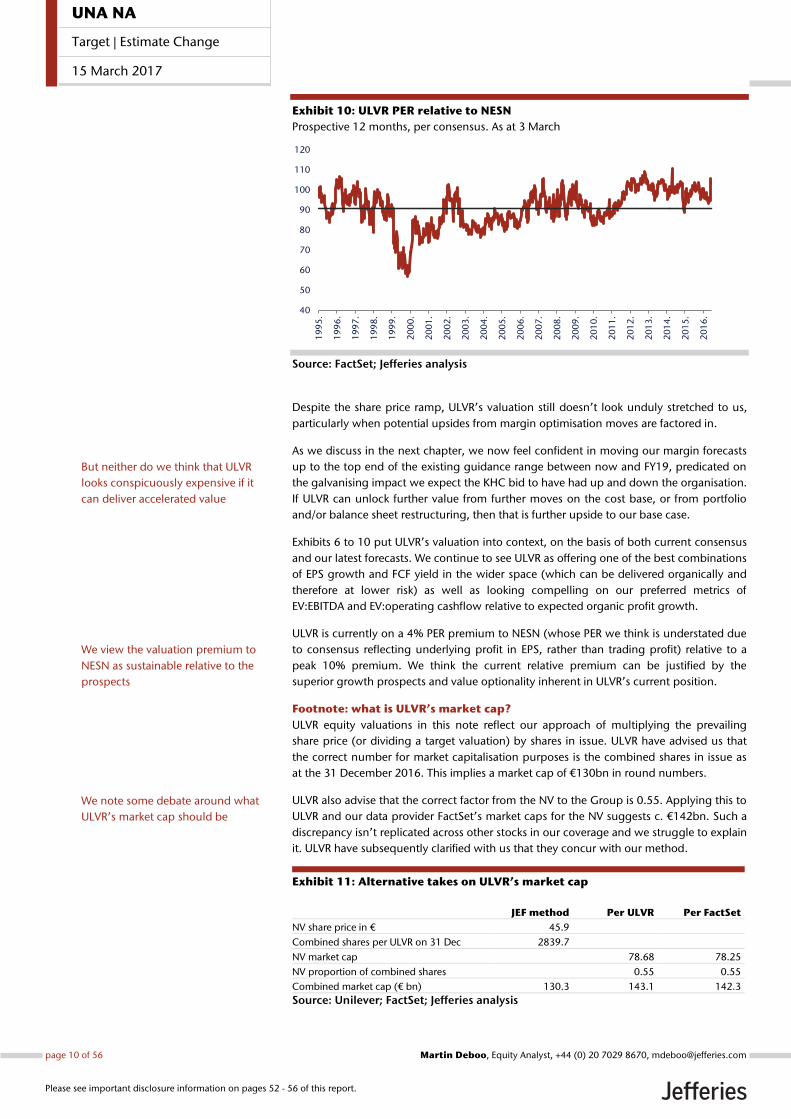

Exhibit 10: ULVR PER relative to NESN

Prospective 12 months, per consensus. As at 3 March

Source: FactSet; Jefferies analysis

Despite the share price ramp, ULVR’s valuation still doesn’t look unduly stretched to us,

particularly when potential upsides from margin optimisation moves are factored in.

As we discuss in the next chapter, we now feel confident in moving our margin forecasts

up to the top end of the existing guidance range between now and FY19, predicated on

the galvanising impact we expect the KHC bid to have had up and down the organisation.

If ULVR can unlock further value from further moves on the cost base, or from portfolio

and/or balance sheet restructuring, then that is further upside to our base case.

Exhibits 6 to 10 put ULVR’s valuation into context, on the basis of both current consensus

and our latest forecasts. We continue to see ULVR as offering one of the best combinations

of EPS growth and FCF yield in the wider space (which can be delivered organically and

therefore at lower risk) as well as looking compelling on our preferred metrics of

EV:EBITDA and EV:operating cashflow relative to expected organic profit growth.

ULVR is currently on a 4% PER premium to NESN (whose PER we think is understated due

to consensus reflecting underlying profit in EPS, rather than trading profit) relative to a

peak 10% premium. We think the current relative premium can be justified by the

superior growth prospects and value optionality inherent in ULVR’s current position.

Footnote: what is ULVR’s market cap?

ULVR equity valuations in this note reflect our approach of multiplying the prevailing

share price (or dividing a target valuation) by shares in issue. ULVR have advised us that

the correct number for market capitalisation purposes is the combined shares in issue as

at the 31 December 2016. This implies a market cap of €130bn in round numbers.

ULVR also advise that the correct factor from the NV to the Group is 0.55. Applying this to

ULVR and our data provider FactSet’s market caps for the NV suggests c. €142bn. Such a

discrepancy isn’t replicated across other stocks in our coverage and we struggle to explain

it. ULVR have subsequently clarified with us that they concur with our method.

Exhibit 11: Alternative takes on ULVR’s market cap

JEF method Per ULVR Per FactSet

NV share price in € 45.9

Combined shares per ULVR on 31 Dec 2839.7

NV market cap 78.68 78.25

NV proportion of combined shares 0.55 0.55

Combined market cap (€ bn) 130.3 143.1 142.3

Source: Unilever; FactSet; Jefferies analysis

40

50

60

70

80

90

100

110

120

19

95

.

19

96

.

19

97

.

19

98

.

19

99

.

20

00

.

20

01

.

20

02

.

20

03

.

20

04

.

20

05

.

20

06

.

20

07

.

20

08

.

20

09

.

20

10

.

20

11

.

20

12

.

20

13

.

20

14

.

20

15

.

20

16

.

But neither do we think that ULVR

looks conspicuously expensive if it

can deliver accelerated value

We view the valuation premium to

NESN as sustainable relative to the

prospects

We note some debate around what

ULVR’s market cap should be

UNA NA

Target | Estimate Change

15 March 2017

page 10 of 56 , Equity Analyst, +44 (0) 20 7029 8670, [email protected] Deboo

Please see important disclosure information on pages 52 - 56 of this report.

Moving to the top end of margin

guidance. But cautious beyond that

ULVR’s cost base: myth and reality ULVR is a fat, complacent, high-cost organisation isn’t it? Why the evidence is there for all

to see: Its monumental Thames-side gaff at 100 Victoria Embankment, nearly half of which

is an atrium, all indulgent thin air funded at Prime London rental rates. Not to mention its

multi-£millions renovation in the mid-noughties, courtesy of en vogue architectural

hotshot Kohn Pederson Fox. And don’t even get us started on the lavish Four Acres

‘Leadership Development Facility’ in Singapore (what was wrong with a bulk discount at

Insead?), opened at a cost of €50m in 2013.

In contrast Reckitt Benckiser make do with a nondescript 80s block at the wrong end of

Slough, while bêtes noires Kraft Heinz have moved their people out of a glossy out-of-

town campus into five open plan floors in a downtown skyscraper. Why, something must

be done to control ULVR’s largesse, angry investors might say (and do).

Well yes and no. We’d by lying if, like many, we didn’t admit to a few twinges of cynicism

and wonderment as we have toured the various demesnes of ULVR’s global empire over

the past few years. But going the other way is that ULVR is a big global business, one that

benefits from significant economies of scale in SG&A. It is a business engaged in a global

war for talent and one that believes in treating its people with care and respect, in the

interests of their longer-term wellbeing and ability to perform. And ULVR are far from the

only multinational to feel the need to erect the occasional symbol to their greatness,

including one or two investment banks we could mention.

So any debate on the cost reduction potential available to ULVR needs to stay rooted in

the facts and the analysis, not the comforting mythology. So let’s go there now.

SG&A efficiency not best-in-class, but not dramatically out-of-line of either Let’s commence at the logical starting point of Selling, General & Admin (SG&A) cost as a

percentage of sales, which is the heart of the debate about the ‘3G’ versus ‘ULVR’ way of

doing things. Exhibit 13 analyses this ratio for the usual suspect large consumer

multinationals, including ULVR. The analysis is complicated by different approaches to

cost (particularly distribution cost) allocation. However we believe that the ratios for the

key comparators of ULVR, RB, KHC & Nestle (NESN) are comparable.

The immediately striking thing about Exhibit 13 is that there is no evidence of returns to

scale in SG&A. The relative cheapskates, RB, are the smallest company in the sample while

the biggest, company, NESN, sports a relatively high ratio. We suspect that Colgate &

P&G’s ratio might include distribution costs, which typically run at 5 to 10% of sales2. We

think the lack of the intuitive inverse correlation is partly because of differences in culture

but also because Food companies have a lower sales value per unit (and hence higher

SG&A as a percentage) than HPC ones.

ULVR runs on an SG&A:sales ratio of 13%, relative to the best-in-class benchmark of RB, at

8%, which is of course a much smaller player, albeit an HPC (and Health) one. The two

‘3G’ players, KHC and ABI, run on about 10% SG&A to sales, although we can’t be sure in

KHC’s case whether this includes an element of distribution cost.

2 We have been unable to validate this from 10-K disclosures for P&G and Colgate

There is plenty of mythology in the

market around ULVR’s purported

high cost base…

..which sits in contrast to the likes of

RB and of course KHC

But we urge a focus on the facts of

efficiency, not the myths

We focus on SG&A cost, the

heartland of any ZBB programme

There is little compelling evidence of

returns to scale in SG&A across large

staples players

ULVR runs a higher SG&A ratio than

best-in-class, but is also far from

worst-in-class

UNA NA

Target | Estimate Change

15 March 2017

page 11 of 56 , Equity Analyst, +44 (0) 20 7029 8670, [email protected] Deboo

Please see important disclosure information on pages 52 - 56 of this report.

Exhibit 12: SG&A costs as a percentage of sales, relative to overall scale

Based on the most recent reported financial year with detailed cost disclosure

Source: Company data; Jefferies analysis Note: In some cases SG&A to sales has been calculated by derivation from gross margin, operating margin and A&P to sales. The picture is complicated by the fact that definitions of gross margin differ, particularly around where and how distribution costs are accounted for. But we think the ratios for ULVR, RB, DGE & NESN are comparable. NESN’s ratio rests on an assumption of A&P:sales of 7%,which is not disclosed and is our estimate

So the facts would suggest that there is potential for ULVR to make savings in SG&A.

Given its scale, we would have thought that a high single digit percentage of sales should

be attainable, equivalent to a reduction of at least 30% from current levels. Whether ULVR

want to deliver this is a question primarily of their appetite. Let’s return to that below.

But progress on SG&A reduction limited to date Our long-standing critique of ULVR has been that operating margins haven’t progressed

as strongly as we would like, relative to what has been achieved by best-performing peers

and the imperative to buttress weak top line with compensating improvement in margin.

In fairness to ULVR, the rate of progress has improved, with the five year average

improving from 18bps in 2013, to 21bps in 2014 and 36 bps now. This has been driven

by two years of above-trend improvement in 2015 & 2016. However these have arguably

been relatively ‘easy’ years, where input cost pressures have been subdued and US

players have been obliged to take a benign pricing stance given adverse $ fx.

Exhibit 13: Average progress in adjusted/core operating margins

In basis points. Most recent five financial years. At actual fx

Source: Company data; Jefferies analysis

NESN

ULVR

RB

CL

PG

ABIKHC

DGE

0%

5%

10%

15%

20%

25%

30%

0 10 20 30 40 50 60 70 80 90 100S

G&

A %

of

sale

s

Sales (USDbn)

119

74

36

126

(5)

RB CL ULVR NESN PG Danone

While margin progression has

accelerated, ULVR remains middle of

our performance table

UNA NA

Target | Estimate Change

15 March 2017

page 12 of 56 , Equity Analyst, +44 (0) 20 7029 8670, [email protected] Deboo

Please see important disclosure information on pages 52 - 56 of this report.

So ULVR still remains #3 in our table, albeit now ahead of NESN. RB and Colgate have

higher base margins, but it remains the case that RB’s 120bps of progress and Colgate’s

75bps amount to an incremental one to two points faster earnings growth over five years.

Turning to the principal moving parts of core margin, namely gross margin, SG&A and

Brand & Marketing Investment (BMI) it can be seen that ULVR’s operating margin

progress has come solely from improvement in gross margin. BMI was increasing as a

percentage of sales prior to 2016, while SG&A started to climb again in 2015 & 2016,

having fallen in the two years prior to that. While this was partly due to adverse fx on

SG&A in 2015, it’s hard to argue that ULVR have taken really decisive action on its SG&A

base prior to the unveiling of Zero-Based Budgeting (‘ZBB’) in December 2015.

Exhibit 14: ULVR margin moving parts since 2004

% of sales

Source: Unilever; Jefferies analysis 1 Gross margin prior to 2010 includes distribution & selling costs to improve comparability to post-2010 margin. SG&A prior to 2010 is Admin Expenses per old ULVR reporting

UK case study: steady work in a mature market

There is a lot going on in ULVR’s global SG&A cost line. So in order to undertake a

‘cleaner’ analysis, in a single market, we have drilled down in the UK. This has been

possible because ULVR’s UK trading entity, Unilever UK Ltd, files annual returns.

The UK is ULVR’s fourth biggest market worldwide (behind the USA, Brazil and India) and

is its largest European market by some margin. The business was extensively re-organised

in 2007-2009, when three operating companies headquartered respectively in Kingston-

upon-Thames (Home and Personal Care), Crawley (Foods) and Walton-on-Thames (Ice

Cream) were amalgamated into one new Head Office at Leatherhead, Surrey, under the

auspices of then Chairman in the UK, Dave Lewis. Lewis offered extensive disclosures at

the 2008 Investor Seminar at Port Sunlight to the effect that the move to Leatherhead was

facilitating extensive overhead reduction following a detailed cost benchmarking study.

This is apparent in the data. Ignoring the transitional year of 2007 (Unilever UK was

formed only in the middle of 2007), the business started life with close to 4400 heads in

2008, including nearly 600 in admin. By 2014 this had been reduced to under 4000

heads, despite 20% cumulative organic growth in the intervening years and the

integration of the acquired Alberto Culver and Sara Lee businesses in 2010 /2011. Sales

per employee accordingly rose, by c.3% pa between 2008 and 2014. Headcount fell

further in 2015 but this reflected in part the carve-out the Baking, Cooking and Spreads

(BCS) Company into a separate entity in April 2015, with close to 200 associated heads.

41.0%38.9% 39.8% 40.0%

38.4% 39.5%41.5%

39.9% 40.5% 41.6% 41.4% 42.2% 42.7%

13.7%

11.4%

12.5% 12.4% 11.4%11.5% 14.2% 13.3%

12.5% 12.7% 12.1% 12.4% 12.7%11.7%

12.8%

13.1% 13.2% 12.5% 13.3% 13.7% 13.1%

14.2% 14.8% 14.8% 15.0% 14.7%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Gross margin SG&A BEI

New 'core profit' definitionOld definition

Operating margin progress has

come from GM, not SG&A

We case study the UK in more

detail…

…where overheads were extensively

rationalised in 2007-2009

UK headcount has fallen consistently

despite rising sales

UNA NA

Target | Estimate Change

15 March 2017

page 13 of 56 , Equity Analyst, +44 (0) 20 7029 8670, [email protected] Deboo

Please see important disclosure information on pages 52 - 56 of this report.

Like many of ULVR’s Developed Market businesses, UK sales slowed markedly in 2014 &

2015 as demand remained subdued and commodity inflation cycled out. Margins fell by

several percentage points to c.4%.3

Exhibit 15: ULVR UK LFL sales growth

Source: Unilever; Jefferies analysis Note: 2008 to 2012 is as disclosed in Companies House accounts. 2013 & 2014 is based change in domestic sales. 2015 is based on change in continuing ops sales ex BCS

Exhibit 16: ULVR UK adjusted operating margin

Source: Unilever; Jefferies analysis

Exhibit 17: ULVR UK headcount

Source: Unilever; Jefferies analysis

Exhibit 18: ULVR UK admin costs to sales ratio

Source: Unilever; Jefferies analysis

Behind the scenes, admin costs as a percentage of sales fell consistently from 2009 to

2012, reflecting, we assume, efficiencies. Since 2012 they have stayed fairly constant as a

percentage of sales, despite tough conditions4.

So we find both positive and negative messages from our UK case study. On the positive

side, SG&A has flatlined as a percentage of sales in recent years. This suggests potential

for improvement, facilitated by ZBB and new C4G ways of working. On the other hand it

might suggest that ULVR have already maxed out on SG&A efficiencies, having

undertaken a de facto ZBB exercise in 2007-2009, facilitated by a move to a greenfield

site.

3 We don’t consider the absolute level of operating margin for ULVR UK to be meaningful,

reflecting as it does transfer pricing in from ULVR’s Unilever Supply Chain Company AG

(‘USCC’). We do however assume the margin trend to be meaningful 4 We can’t explain the fall in admin heads and costs that occurred in 2013.

-1%

0%

1%

2%

3%

4%

5%

2008 2009 2010 2011 2012 2013 2014 2015

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

2007 2008 2009 2010 2011 2012 2013 2014 2015

2101 2277 2065 2064 2230 2245 2157 2061 1895

1018

15371621 1585

1685 1698 15811409

1279

715

573397 336

395 397329

356351

2007 2008 2009 2010 2011 2012 2013 2014 2015

Production Marketing & Selling Admin0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

2007 2008 2009 2010 2011 2012 2013 2014 2015

UK SG&A:sales fell from 2009-2012,

but have flatlined since

We think our UK case study signals

renewed potential for improvement

UNA NA

Target | Estimate Change

15 March 2017

page 14 of 56 , Equity Analyst, +44 (0) 20 7029 8670, [email protected] Deboo

Please see important disclosure information on pages 52 - 56 of this report.

Seeing margin progress beyond upper bound of current guidance as a challenge To advance the analysis, and the argument, we return to and refresh some detailed

analysis at the Group level that we undertook initially in January 2016, as we appraised

ZBB for the first time. We have updated this analysis for the FY16 out-turn and firmer

guidance commentary given at last December’s Port Sunlight seminar.

We continue to probe the upsides on margin through two complementary perspectives:

Bottom up, in terms of the structure of the current cost base and the relative

aggression of the current ZBB savings programme in this context

Top down, in terms of the evolving mix of categories, peer group benchmarks

in these categories and ULVR’s track record on margin progression

A re-review of this analysis leads us to stick to our conclusion that progress beyond the

upper bound of current 3 year guidance of between 40bps and 80bps will be challenging

for ULVR. This implies a terminal (FY19) margin of between 17.5% and 18.0%.

Let’s start by looking bottom up, at ULVR’s cost base by line item. As we have already

observed above, ULVR has a generally good record on gross margins (GM’s) to date as a

result of ongoing gross supply chain savings in the €1bn+ range, structural change in the

portfolio in favour of higher GM HPC and incremental ‘maxing the mix’ initiatives at sub-

category level.

ZBB programme suitably aggressive

So the focus of the current ZBB programme has been the SG&A cost base. The core of this

is the €5.7bn or so of ‘pure’ SG&A cost (essentially white collar staff functions and

associated overhead such as property and IT costs). Also in scope for ZBB will be R&D cost

of around €1bn and the ‘non-working media’ (how this analyst’s former advertising

colleagues hate that term) component of Brand & Marketing Investment (BMI). We think

this will be around 20% of total BMI spend of €7.7bn, say around €1.5bn. So there is

around €8bn of total cost in-scope for the ZBB programme.

Exhibit 19: ULVR’s cost base by component

Based on FY16A

Source: Unilever; Jefferies analysis

€52.7bn

€21.1bn

€1.5bn

€7.6bn

€7.7bn

€1.0bn

€5.7bn

€8.0bn

Sales Raw & Pack D&A Oth. COGs BMI R&D SG&A Core Profit

40% 3% 14% 15% 2% 11% 15%% sales

€1bn+ ZBB goal as % of:Sales: 200-250bps

All costs: 250-300bpsSG&A costs: 20-25%

We review and refresh our integrated

analysis of margins from 2016

We think that progress on a 3 year

view above the top end of current

guidance will be tough to achieve

The €1bn+ ZBB target needs to come

out of a c.€8bn target cost base

UNA NA

Target | Estimate Change

15 March 2017

page 15 of 56 , Equity Analyst, +44 (0) 20 7029 8670, [email protected] Deboo

Please see important disclosure information on pages 52 - 56 of this report.

ULVR’s delivery partner in ZBB, consulting firm Accenture, cite savings of between 10%

and 40% of SG&A cost from ZBB, depending on line item. They claim resultant

improvements in EBITDA of between 25% to 50%.

Exhibit 20: Accenture’s view of potential ZBB savings

Source: Accenture: ‘Closed Loop Cost Management’

ULVR’s implied ZBB target of 20 to 25% of SG&A cost looks suitably aggressive to us in

this context. It’s well in the mid-range of Accenture’s claims. And while it implies a much

lower improvement in EBITDA than Accenture claim (c.10%, even if all the savings go to

the bottom line) that calculation depends acutely on what starting point SG&A:sales and

EBITDA margins are.

ULVR’s consistent commentary on ZBB has been to the effect that it’s not a ‘full on’ 3G

style programme and is instead targeted at looking at cost more insightfully and creatively

in a way that inspires better ways of working, not just cost savings. We have also opined

that ULVR won’t want to fracture their internal ‘social contract’ with white collar staff such

as would occur if an ultra-aggressive programme was instituted. Some will argue that this

calculation has altered fundamentally since February 17. We are not so sure: ULVR have

many levers to pull to unlock value, of which ZBB is just one.

Not a conspicuously under-earning business relative to mix

A complementary top-down analysis reinforces our caution around margin progress

going beyond the upper bound of current guidance. Our core argument is that, contrary

to myth, ULVR is not a conspicuously under-earning business relative to its mix of

categories, geographic exposures and competitive challenges.

Exhibit 22 compares operating margins across the broad peer group. ULVR is a mid-table

player in a peer group that tends to have large multinational HPC businesses at the high

end and a mix of smaller multinational HPC’s and local Food businesses at the low end.

The reality is that ULVR is a hybrid Foods & HPC business with characteristics of both

groupings. It is also a business more heavily exposed to Emerging Markets than most,

where peer margins tend to be lower and the need to invest is higher.

ULVR’s ZBB goal looks suitably

stretching relative to partner

Accenture’s benchmarks…

…particularly when the nature of

ULVR’s ‘social contract’ with its staff

is factored in

We stick to our view that ULVR isn’t

an under-earning business relative to

its mix

UNA NA

Target | Estimate Change

15 March 2017

page 16 of 56 , Equity Analyst, +44 (0) 20 7029 8670, [email protected] Deboo

Please see important disclosure information on pages 52 - 56 of this report.

Exhibit 21: Peer group operating margins in broadly comparable business to Unilever

FY16 for ULVR, NESN & KHC. Latest reported FY for peers. Reflects margins in broadly comparable businesses to ULVR (see notes)

Source: Companies; Jefferies analysis & estimates Notes 1. Danone excludes Medical Nutrition, 2. Edgewell excludes Wet Shave, 3. Henkel excludes adhesives, 4. Kao excludes Speciality Chemicals & Health Care, 5. L’Oreal excludes Body Shop

We frame the debate by looking at ULVR’s mix of sales by region and category (Exhibit 23)

and our estimates of margins in each region/category (Exhibit 24). This reveals that ULVR

tends to have some mature businesses earning exceptionally high margins (e.g. Spreads

in Europe) and some growth businesses earning much lower ones (e.g. the nascent parts

of the Home Care and Refreshment empire). Advancing margins via category mix and

margin improvement is therefore a non-trivial challenge.

Exhibit 22: ULVR sales value map by geography & category

Chart areas proportionate to sales in €bn at ULVR selling prices. Estimated, consistent with FY16A totals

Source: Jefferies analysis & estimates

ULVR Predominantly HPC Predominantly Foods

0.0

42

5.5

% 7.7

%

8.5

% 11

.3%

11

.9%

12

.0%

12

.2%

12

.9%

13

.3%

13

.3%

13

.9%

14

.0%

14

.8%

14

.8%

15

.3%

15

.3%

15

.5%

15

.8%

17

.1%

17

.2% 20

.5%

21

.9%

24

.0%

24

.7%

1.50.3

2.51.3 3.7 0.8

2.1

1.0 5.2

3.2

1.5

6.2

1.01.7

0.6

2.1

1.1

1.2

2.3

1.04.3

0.41.1

0.41.2

1.8 0.41.0 0.3 0.8 0.7

0.1 0.1 0.1 Spreads€2.9bn

Other Foods€9.6bn

Refreshment€10.0bn

Personal Care€20.2bn

Home Care€10.0bn

W. Europe€10.7bn

NorthAm€9.1bn

LatAm€8.0bn

Emerging Asia€14.0bn

AME€3.2bn

CEE€2.5bn

Dev Asia€5.3bn

Total€52.7bn

We explore the question of a fair rate

of margin starting with the current

sales and margin mix

UNA NA

Target | Estimate Change

15 March 2017

page 17 of 56 , Equity Analyst, +44 (0) 20 7029 8670, [email protected] Deboo

Please see important disclosure information on pages 52 - 56 of this report.

Exhibit 23: ULVR estimated margins by geography & category

Estimated, consistent with FY16A. Chart areas proportionate to sales. Omits margin estimates for segments with low materiality

Source: Jefferies analysis & estimates

Exhibits 25-30 look at ULVR margins relative to peers in related categories and

geographies. This supports the thesis that ULVR aren’t conspicuously under-margined:

Margins in Foods are upper quartile (Spreads margins are even higher). Ditto Personal

Care. Home Care margins are low and therefore a big source of upside. Refreshment

wants for benchmarks but probably also has upside. Emerging Market and Europe

margins are average and North American margins are low end. But much depends on

category mix in the market and overall local scale.

Spreadsc.19%

Other Foodsc.17.5%

Refreshment9.9%

Personal Care19.1%

Home Care9.7%

W. Europec.16%

NorthAmc.16%

LatAmc.15%

Emerging Asiac.16%

AMEc.10%

CEEc.12%

Dev. Asiac.16%

c.8%

c.19%

c.11%

c.19%

c.19%

c.12%

c.10%

c.11%

c.17%

c.11%

c.11%

c.10%

c.8%

c.15%

c.7%

Group15.3%

c.20%

c.20%

c.21%

c.18%

c.19%

c.8%

c.18%

c.10%

c.20% c.20%

Margins are peer superior or peer

comparable ex Home Care

UNA NA

Target | Estimate Change

15 March 2017

page 18 of 56 , Equity Analyst, +44 (0) 20 7029 8670, [email protected] Deboo

Please see important disclosure information on pages 52 - 56 of this report.

Exhibit 24: Peer margins in Foods ex. Spreads

Source: Companies; Jefferies analysis & estimates Note: ULVR is estimated. NESN is underlying, not trading, margin

Exhibit 25: Peer margins in Personal Care

Source: Companies; Jefferies analysis & estimates Note: RB is estimated excluding Foods & Healthcare

Exhibit 26: Peer margins in Home Care

Source: Companies; Jefferies analysis & estimates Note: RB includes some Personal Care businesses

Exhibit 27: Peer margins in North America

Source: Companies; Jefferies analysis & estimates Note: RB is Europe & North America combined

Exhibit 28: Peer margins in Europe

Source: Companies; Jefferies analysis & estimates Note: RB is Europe & North America combined

Exhibit 29: Peer Margins in Emerging Markets

Source: Companies; Jefferies analysis & estimates Note: ULVR is estimated. Peer margins reflect either overall EM averages or reported margins from LatAm, Asia or Africa

This top down analysis corroborates some of our caution from the ZBB perspectives and

leads us to question whether ULVR can put any more margin guidance on the table than

they already are.

5.5%

8.5%

11.3%

12.0%

12.2%

14.8%

17.1%

17.2%

17.5%

18.6%

22.1%

24.0%

26.9%

Bimbo

Tingyi

Mondelez

Brasil Foods

Danone

Campbells

Premier Foods

Gen. Mills

Unilever

Nestle

Heinz

Kraft

RB

4.2%

7.7%

9.7%

11.9%

13.3%

13.9%

14.0%

14.8%

15.3%

16.8%

19.1%

20.5%

21.2%

Shisheido

Oriflame

Kao

Beiersdorf

Johnson Johnson

Natura

PZ Cussons

Edgewell

Henkel

P&G

Unilever

L'Oreal

RB

9.7%

16.2%

16.4%

18.8%

21.2%

Unilever

Henkel

P&G

Kao

RB

8.6%

14.8%

16.0%

20.6%

26.0%

27.2%

28.2%

Danone

Campbells

Unilever

Gen. Mills

Kraft

Colgate

RB

12.7%

14.9%

15.3%

15.7%

16.0%

17.1%

22.0%

23.3%

25.5%

28.2%

Mondelez

Dairy Crest

Nestle

Danone

Unilever

Premier Foods

PZ Cussons

Colgate

Heinz

RB

8.4%

8.5%

10.8%

11.6%

12.9%

13.9%

14.0%

18.7%

19.8%

24.0%

Mondelez

Tingyi

Bimbo

Danone

Brasil Foods

Heinz

Unilever

Nestle

RB

Colgate

UNA NA

Target | Estimate Change

15 March 2017

page 19 of 56 , Equity Analyst, +44 (0) 20 7029 8670, [email protected] Deboo

Please see important disclosure information on pages 52 - 56 of this report.

Upgrading stand-alone forecasts to the top end of guidance range. Modelling a return to Buybacks Upgrading margin forecasts to the top end of the current guidance range

We now integrate these perspectives to inform a new forecast. The increase in FY17

guidance is a clear signal that ULVR plan to accelerate capture of ZBB savings and, we

suspect, increase the retention rate on those savings. We expect this to drive an

accelerated rate of margin progress beyond FY17, with the biggest gains being made in

the under-margined categories of Home Care and Refreshment. This gives us confidence

that ULVR can continue to bat at the upper end of the 40-80bps guidance range.

But not beyond it, in our view. Exhibit 31 highlights the extent of the challenge.

On the upside, we assume that Home Care can continue to grow margins at close to its

recent and high rate of 150-200bps. This projects an FY19 margin of 14.9%, which we see

as directionally consistent with Home Care EVP Nitin Paranjpe’s assertion at Port Sunlight

to the effect that he saw no reason why Home Care margins couldn’t exceed the group

average at some point in the future. Our FY19 forecast assumes that they achieve the

current group average (more or less) in three years.

We also assume accelerated margin progress in Refreshment (Ice Cream and Tea).

Consistent margin progress has been made in the past two and a half years and ULVR

seem to be getting to grips with low levels of ROIC in Ice Cream via mix improvement and

cabinet management initiatives. ROIC in Ice Cream improved by 300bps between 2013

and 2016, around half of which was margin, according to EVP Kevin Havelock.

We also assume that Personal Care can deliver a higher rate of margin growth than it has

in recent years as organic growth recovers, mix continues to improve and the category

benefits from its share of ZBB savings. But there are risks here: starting point margins are

high, the category is competitively intense and ULVR has some performance-fixing to do.

Exhibit 30: Projected FY19 core margins & 3 year progression

2015/16

avg. LFL

2015/16

Core

margin

pa

2016A

Core

margin

Projected

LFL

Projected

Core

Margin

pa

2019E

core

margin

Personal Care 4.2% 20bps 19.1% 5.0% 50bps 20.8%

Home Care 5.4% 170bps 9.7% 5.0% 150bps 14.9%

Refreshment 4.5% 55bps 9.9% 4.0% 100bps 13.3%

Foods 1.8% (35bps) 17.9% 2.0% 10bps 18.2%

Total 3.9% 40bps 15.3% 4.1% 80bps 17.6%

Source: Company data; Jefferies analysis & estimates

On the (relative) downside, we assume that Foods margins progress only slowly, given

the high starting point relative to the peer group and the need to invest in defending the

top line. Our forward projection of 15bps of annual progress reflects significant

improvement relative to the most recent two years.

Scoping a potential €18bn cumulative buyback to 2019

ULVR’s April review remit has made explicit reference to the Balance Sheet. We read this as

an open-ness to fresh thinking around enhanced cash returns to shareholders.

ULVR’s CEO Paul Polman has of course vigorously resisted Buybacks over the years. We

have some sympathy with his position, taking the view that headline earnings accretion is

largely offset by PER compression, as the result of the higher cost of leveraged equity.

However we now expect more pragmatic counsels to prevail, post-KHC. Partly as the

result of shareholder pressure and the symbolism inherent in such a shareholder friendly

move. More critically, because one of the hard lessons from KHC was that a smaller

Our peer analysis informs our new

medium term margin forecasts

We think that core margins of 17-

18% by FY19 is a realistic target

We model a buyback scenario that

reflects a target net debt:EBITDA at

end FY19 of 2.0x

UNA NA

Target | Estimate Change

15 March 2017

page 20 of 56 , Equity Analyst, +44 (0) 20 7029 8670, [email protected] Deboo

Please see important disclosure information on pages 52 - 56 of this report.

predator was able to contemplate taking out ULVR using its own under-leveraged balance

sheet. We expect this to shift hearts and minds inside 100VE.

We accordingly model an upside (for EPS) case that has ULVR buying back to hit a target

net debt:EBITDA multiple of 2.0x by the end of 2019. This implies a c.€6bn annual

programme between now and then.

Stand-alone forecast scenarios summary

Exhibit 32 summarises our forecast scenarios based on the above discussion. We reference

as a baseline our previous published forecast from January 27, which resolved to an FY17

EPS of €202c rising to €243c by FY19. This forecast reflected c.40bps of margin

progression in FY17, rising to c.60bps in FY19, the latter the mid-upper range of

guidance. Subsequent fx movements would have been a c.2% upgrading influence.

Exhibit 31: Summary forecasts (published forecast shaded grey)

Organic growth

FY16A FY17E FY18E FY19E FY20E CAGR

19 vs.16

Previous published forecast 3.7% 3.8% 4.1% 4.3% 4.3% 4.1%

Above at latest fx 3.7% 3.8% 4.1% 4.3% 4.3% 4.1%

New stretch margin forecast 3.7% 3.8% 4.1% 4.3% 4.3% 4.1%

New forecast plus buyback 3.7% 3.8% 4.1% 4.3% 4.3% 4.1%

Core margins

FY16A FY17E FY18E FY19E FY20E Delta pa

19 vs.16

Previous published forecast 15.3% 15.7% 16.3% 16.9% 17.3% 56bps

Above at latest fx 15.3% 15.7% 16.3% 16.9% 17.3% 55bps

New stretch margin forecast 15.3% 16.0% 16.8% 17.6% 18.4% 76bps

New forecast plus buyback 15.3% 16.0% 16.8% 17.6% 18.4% 76bps

Net debt:EBITDA

FY16A FY17E FY18E FY19E FY20E

Previous published forecast 1.3x 1.0x 0.8x 0.6x 0.4x

Above at latest fx 1.3x 1.0x 0.8x 0.6x 0.3x

New stretch margin forecast 1.3x 1.0x 0.7x 0.5x 0.2x

New forecast plus buyback 1.3x 1.6x 1.8x 2.0x 2.0x

NV EPS (in Euro c)

FY16A FY17E FY18E FY19E FY20E CAGR

19 vs.16

Previous published forecast 188.1 202.1 221.5 242.5 261.6 9%

Above at latest fx 188.1 206.6 226.9 248.4 267.9 10%

New stretch margin forecast 188.1 210.5 233.8 258.6 285.2 11%

New forecast plus buyback 188.1 213.2 243.8 278.9 319.0 14%

PLC EPS (in GBp)

FY16A FY17E FY18E FY19E FY20E CAGR

19 vs.16

Previous published forecast 153.3 172.1 188.6 206.5 222.7 10%

Above at latest fx 153.3 177.0 194.5 212.8 229.6 12%

New stretch margin forecast 153.3 180.4 200.5 221.9 244.9 13%

New forecast plus buyback 153.3 182.7 209.0 239.0 273.4 16%

% EPS deltas relative to previous published forecast

FY16A FY17E FY18E FY19E FY20E

Latest fx 0% 2% 2% 2% 2%

New stretch margin forecast 0% 4% 6% 7% 9%

New forecast plus buyback 0% 5% 10% 15% 22%

Source: Jefferies analysis & estimates

Our best case optimised forecasts

indicates FY19 EPS 15% higher at

€279c

UNA NA

Target | Estimate Change

15 March 2017

page 21 of 56 , Equity Analyst, +44 (0) 20 7029 8670, [email protected] Deboo

Please see important disclosure information on pages 52 - 56 of this report.

Our new published forecasts (shaded grey in the Exhibit and set out in detail at the end of

this note) now assume consistent margin progress at the very top end of the range i.e.

80bps pa. This is consistent with new ULVR guidance for FY17 issued on 22 February and

our own analysis and conjecture as set out above in the out years. The effect is to upgrade

FY19 EPS by 7% relative to our previous published forecast of 5% at constant fx.

Our speculative Buyback case projects FY19 EPS of €279c, being a 15% upgrade to our

previous published forecast (13% at constant fx) and a cumulative 8% upgrade to our

new stretch margin case forecast.

UNA NA

Target | Estimate Change

15 March 2017

page 22 of 56 , Equity Analyst, +44 (0) 20 7029 8670, [email protected] Deboo

Please see important disclosure information on pages 52 - 56 of this report.

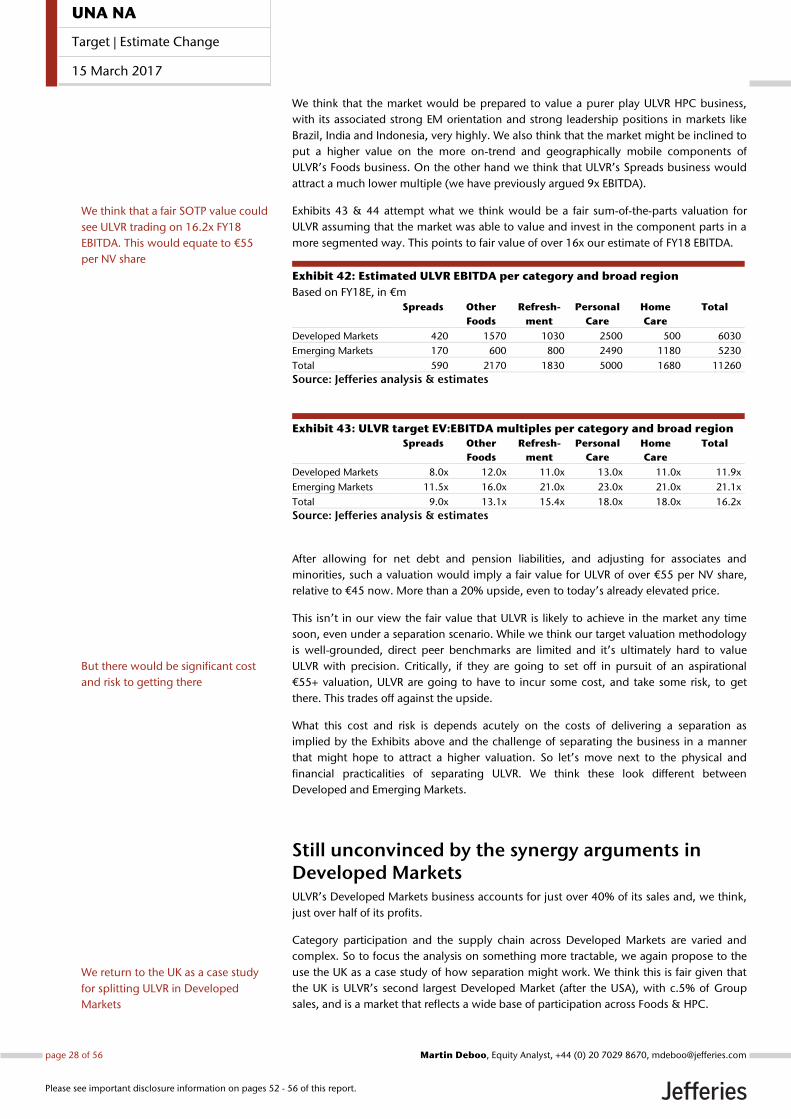

No further upside from a split, once

costs & complexities are weighed

The case for a split Questionable returns from scale and diversification

KHC’s intervention has put the question of whether ULVR should break itself up in some

way firmly back on the table. ‘Portfolio’ has now been identified by ULVR as one of the

four legs of its strategic review process. While this might not be intended to allude to the

idea of a split, the market is abuzz with that kind of speculation. So the issue needs to be

tackled, as comprehensively and analytically as possible.

This analyst has been a long term advocate of a ULVR split, for virtually the whole of the

ten years he has covered the stock. This reflects two strong convictions.

The first and most important is that we are simply unconvinced by the returns from multi-

category scale: manufacturing synergy is non-existent and distribution synergy is limited