Embed Size (px)

Citation preview

All Rights of Use and Reproduction ReservedCopyright © 2016 Marks Paneth LLP

ENSURING ORGANIZATIONAL COMPLIANCE WITH UNIFORM GUDANCE FOR FEDERAL AWARDS

OCTOBER 31, 2016

Marks Paneth LLP Presenters:

Sibi Thomas, CPA – PartnerJohn D’Amico, CPA – Director

Sibi Thomas, CPA, CFE, [email protected]

212 -201 -3004Sibi Thomas is a Partner within the Nonprofit and Government Group at Marks PanethLLP, with nearly 12 years of extensive accounting, auditing, tax and consultingexperience within the not-for-profit industry. Sibi plans, coordinates and conducts auditsof nonprofit organizations including: large social service organizations, third partyfunded organizations, educational institutions, charitable, and fundraising andmembership organizations including those requiring audits pursuant to UniformGuidance (Single Audit). Sibi performs audits of New York State cost reports,preparation and review of tax returns (Form 990, 990-PF, 990-T, CHAR 500) and auditsof pension plans (defined benefit and defined contribution).

Sibi has deepened his expertise as an adjunct faculty of not-for-profit accounting atNew York University. Mr. Thomas has authored several articles for the New YorkNonprofit Review that focused on helping nonprofit organizations evaluate their existinggovernance and financial reporting process. Recently, Mr. Thomas published an articleon FASB’s new proposed standards on not-for-profit financial reporting in AccountingToday. Sibi was awarded the CPA Practice Advisor “40 Under 40” for leading theaccounting profession.

Sibi is also a Certified Fraud Examiner and a Chartered Global ManagementAccountant. He volunteers his time as a board member of a nonprofit in New York City.

2

John D’Amico, [email protected]

212 -710 -1808John D'Amico, a Director with Marks Paneth LLP, has over 20 years of experience inproviding audit, accounting, and consulting services to not-for-profit organizations andgovernmental agencies. Prior to joining Marks Paneth LLP John worked at a Big 4firm and other regional accounting firms. His areas of expertise include Not-for-Profitaccounting, Single Audits, government auditing standards, cost allocations, andinternal controls. John is also an Instructor for the AICPA.

John has audited a significant number of not-for-profit clients including highereducation, social service agencies, religious organizations, professional organizations,and foundations. The majority of these organizations were government-fundedagencies.

Some of his clients that he as serviced are Fordham University, Wagner College, NYUMedical School, Wildlife Conservation Society (The Bronx Zoo), Heartshare HumanServices, American Arbitration Association, Safe Horizon, Public Health Solutions andAmerican Civil Liberties Union (ACLU). Also, the City of New York and the New YorkCity Board of Education. John has authored articles and conducted workshops andnumerous seminars on not-for-profit topics including OMB A-133/Uniform Guidancerequirements.

3

TODAY’S AGENDA

Background and Overview of Uniform Guidance Overall Auditee Responsibilities Internal Control Responsibilities Administrative Requirements

• Financial Management• Procurement Standards• Requirements of pass-through entities• Subrecepient and contractor determination • Equipment Standards • Cash Management

Allowable costs and cost principles

4

5

BACKGROUND AND OVERVIEW OF UNIFORM GUIDANCE

OMB UNIFORM GUIDANCE

Title 2 U.S. Code of Federal Regulations (CFR) Part 200Uniform Administrative Requirements, Cost Principles, and

Audit Requirements for Federal Awards

Electronic Code of Federal Regulations:http://www.ecfr.gov/cgi‐bin/text‐idx?SID=2d15215db570dfb78451488a5b1bd369&node=pt2.1.200&rgn=div5

6

OMB UNIFORM GUIDANCE (CONT’D.)

7

Subpart A - Acronyms and Definitions Subpart B - General Provisions Application request and mandatory

contact of federal audits Subpart C - Pre-Federal Award Requirements and Contents of Federal

Awards (Federal Agency) must follow in making federal audit Subpart D - Post Federal Award Requirements (300 series) Subpart E - Cost Principles (400 series) Subpart F - Audit Requirements (500 series)

2 CFR 300 & 400 series related to recipients

2 CFR 500 series relate to auditors

The 500 series Plus OMB’s annual compliance supplement is used to the audits

Today we will go over some of the main requirements in series AND what the auditors are required to do to test the requirements that you have to follow.

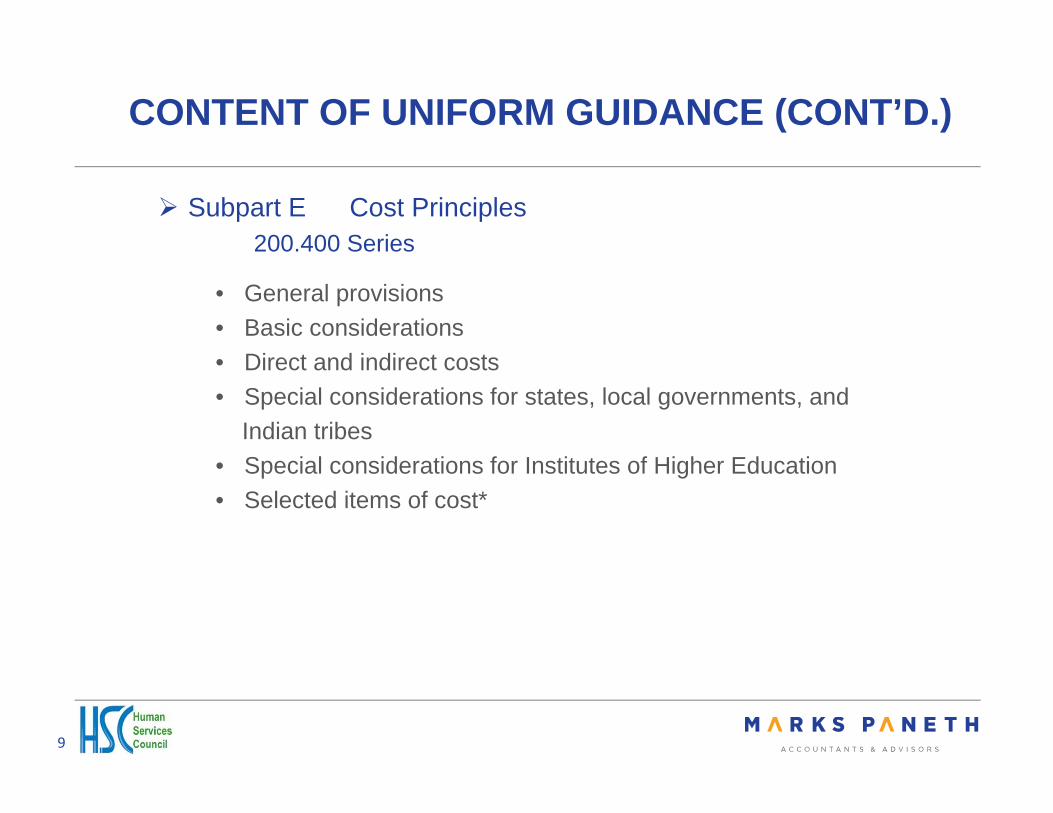

CONTENT OF UNIFORM GUIDANCE (CONT’D.)

8

Subpart D Post Federal Award Requirements (Administrative Requirements)

200.300 Series

• Standards for financial and program management• Procurement standards• Performance and financial monitoring and reporting• Subrecipient monitoring and management• Others

CONTENT OF UNIFORM GUIDANCE (CONT’D.)

9

Subpart E Cost Principles200.400 Series

• General provisions• Basic considerations• Direct and indirect costs• Special considerations for states, local governments, and

Indian tribes• Special considerations for Institutes of Higher Education• Selected items of cost*

CONSIDERATIONS RELATED TO THE ISSUANCE OF THE UNIFORM GUIDANCE

10

Effective Date of Uniform Guidance

• Subject to the Uniform Guidance Grant awarded received on or after 12/26/2014 and Funding increments received on or after 12/26/2014 in which the

funding agency considers the incremental funding actions to bean opportunity to revise award terms and conditions

• Subject to pre-Uniform Guidance OMB Circulars Awards and funding increments received before 12/26/2014 Funding increments received on or after 12/26/2014 in which the

funding agency doesn’t change the terms and conditions This can mean that a lot of your federal funding is still under the

OMB circulars.

UNDERSTANDING THE EFFECTIVE DATES IS KEY!

11

Implement policies and procedures by promulgating regulations to be effective

December 26, 2014

Implement the new administrative requirements

and cost principles for all new Federal awards made on or

after December 26, 2014, and to incremental funding made

after that date

Effective for audits of fiscal years beginning on or after December 26, 2014

•Not permitted to early implement any of the audit provisions

Federal Agencies

Non-federal entities

Audit requirements

12

OVERALL AUDITEE RESPONSIBILITIES

UNIFORM GUIDANCE RECIPIENT (AUDITEE) RESPONSIBILITY

13

Auditee is responsible for the following:

ID of federal programs and understanding and complying with compliance requirements

Establishing and maintaining internal control over compliance Evaluating and monitoring internal control over compliance Taking corrective action when needed To take reasonable measures to safeguard protected personally

identifiable information. 2 CFR 200.508(b) requires the auditee to prepare the SEFA in

accordance with 2 CFR 200.510(b) of the Uniform Guidance.

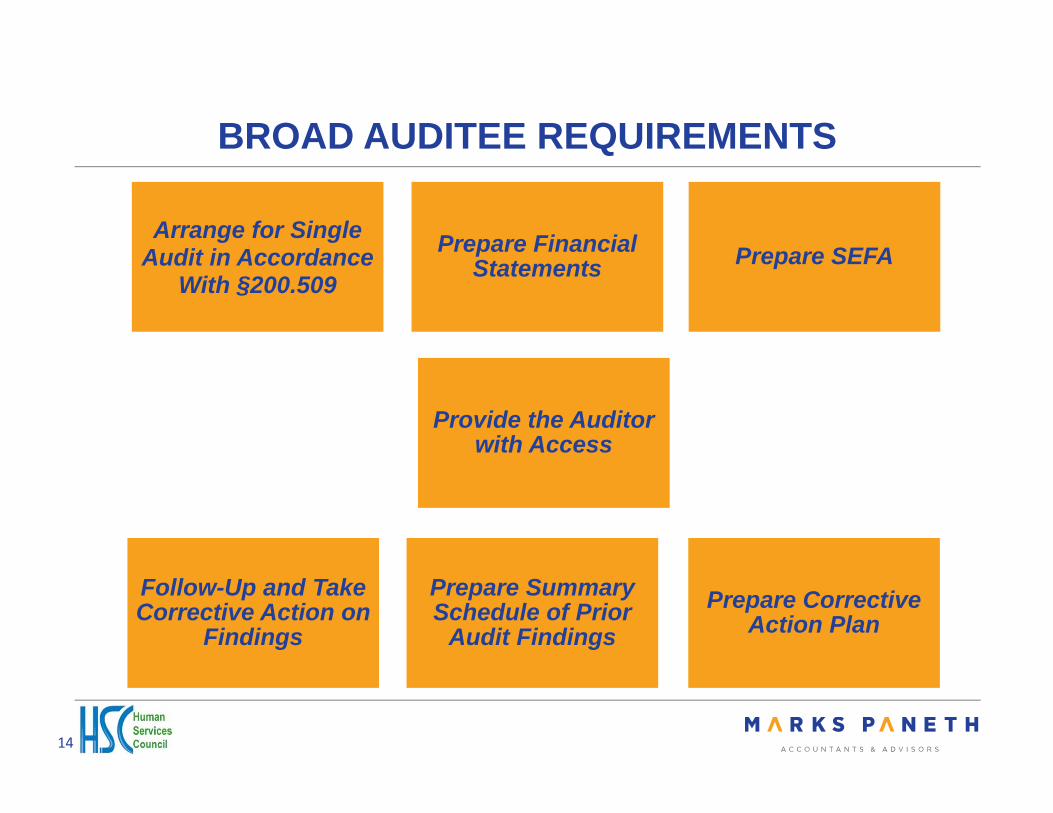

BROAD AUDITEE REQUIREMENTS

14

Arrange for Single Audit in Accordance

With §200.509Prepare Financial

Statements

Provide the Auditor with Access

Prepare SEFA

Follow-Up and Take Corrective Action on

Findings

Prepare Summary Schedule of Prior

Audit FindingsPrepare Corrective

Action Plan

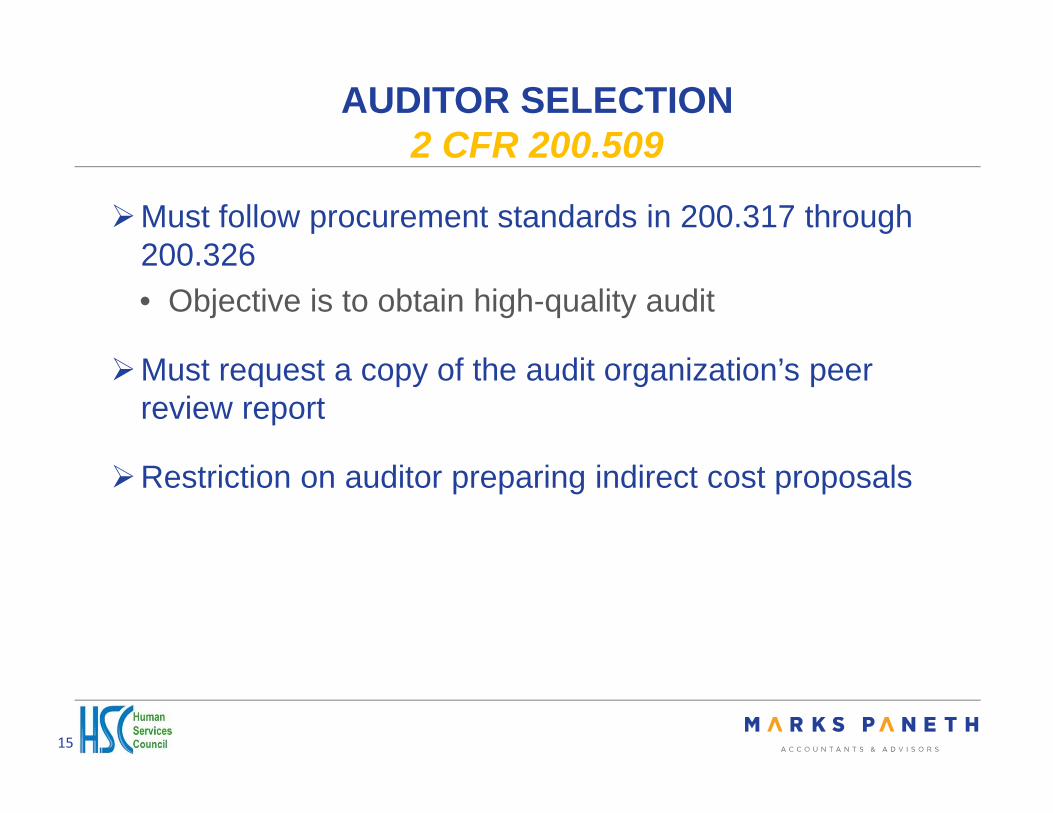

AUDITOR SELECTION2 CFR 200.509

15

Must follow procurement standards in 200.317 through 200.326• Objective is to obtain high-quality audit

Must request a copy of the audit organization’s peer review report

Restriction on auditor preparing indirect cost proposals

FINANCIAL STATEMENTS2 CFR 200.510

16

Must prepare financial statements for the fiscal year audited that reflect current: • Financial position• Results of operation or changes in net assets• Where appropriate, cash flows

Must be for same organizational unit and fiscal year that is chosen to meet the requirements of the Uniform Guidance

May include departments, agencies, and other organizational units that have separate audits under the Uniform Guidance

While preparing financial statements in accordance with generally accepted accounting principles (GAAP) not required, auditees cannot be considered a low-risk auditee by the auditor if they voluntarily follow a non-GAAP basis

SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS (SEFA) 2 CFR 200.510

17

Must also prepare a SEFA for the period covered by the auditee's financial statements • Must include the total federal awards expended as determined in

accordance with §200.502 “Basis for Determining Federal Awards Expended”

Important Notes about SEFA• Reconciles to accounting and other records used in preparing the

financial statements or the financial statements themselves• Auditor uses to base the performance of risk assessments and selection

of major programs• Completeness and accuracy critical to avoid missed programs!

18

INTERNAL CONTROL

AUDITEE INTERNAL CONTROL AND COMPLIANCE REQUIREMENTS 2.CFR 200.303

19

Establish and maintain internal

control over federal programs

Comply with federal statutes, regulations,

federal awardsEvaluate and monitor

compliance

Take prompt action when nocompliance

identified

Safeguard protected personally identifiable

information (PPII)

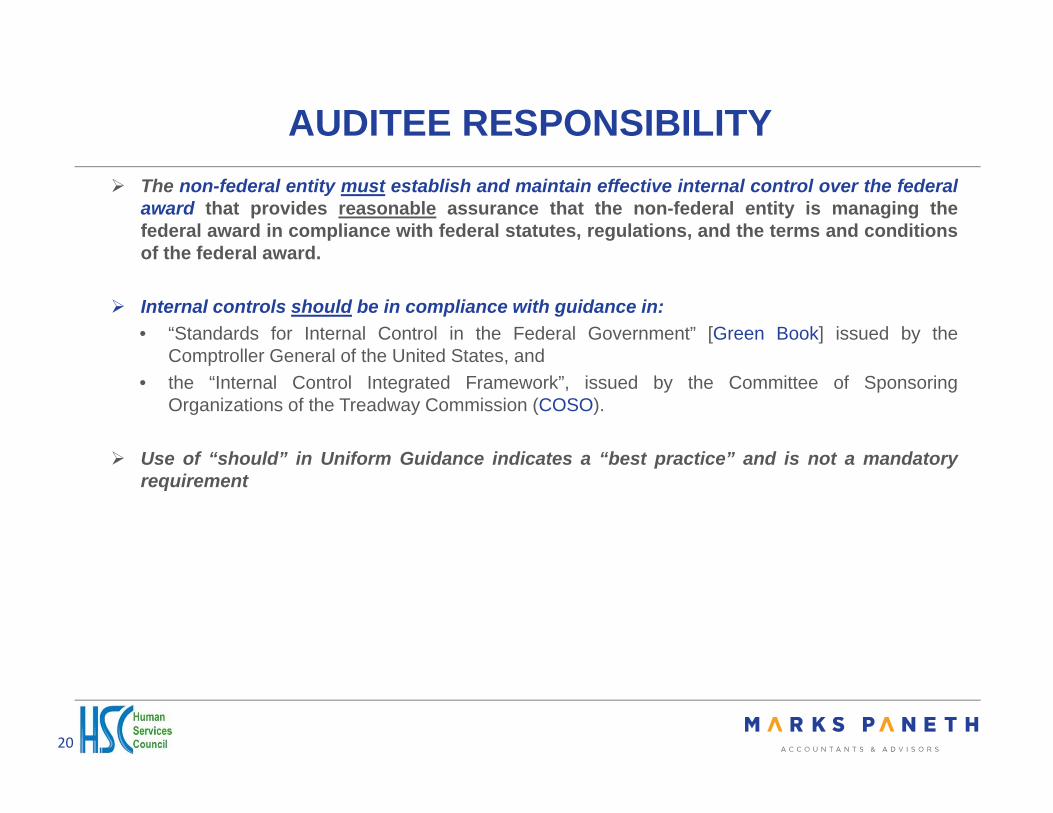

AUDITEE RESPONSIBILITY

20

The non-federal entity must establish and maintain effective internal control over the federalaward that provides reasonable assurance that the non-federal entity is managing thefederal award in compliance with federal statutes, regulations, and the terms and conditionsof the federal award.

Internal controls should be in compliance with guidance in:• “Standards for Internal Control in the Federal Government” [Green Book] issued by the

Comptroller General of the United States, and• the “Internal Control Integrated Framework”, issued by the Committee of Sponsoring

Organizations of the Treadway Commission (COSO).

Use of “should” in Uniform Guidance indicates a “best practice” and is not a mandatoryrequirement

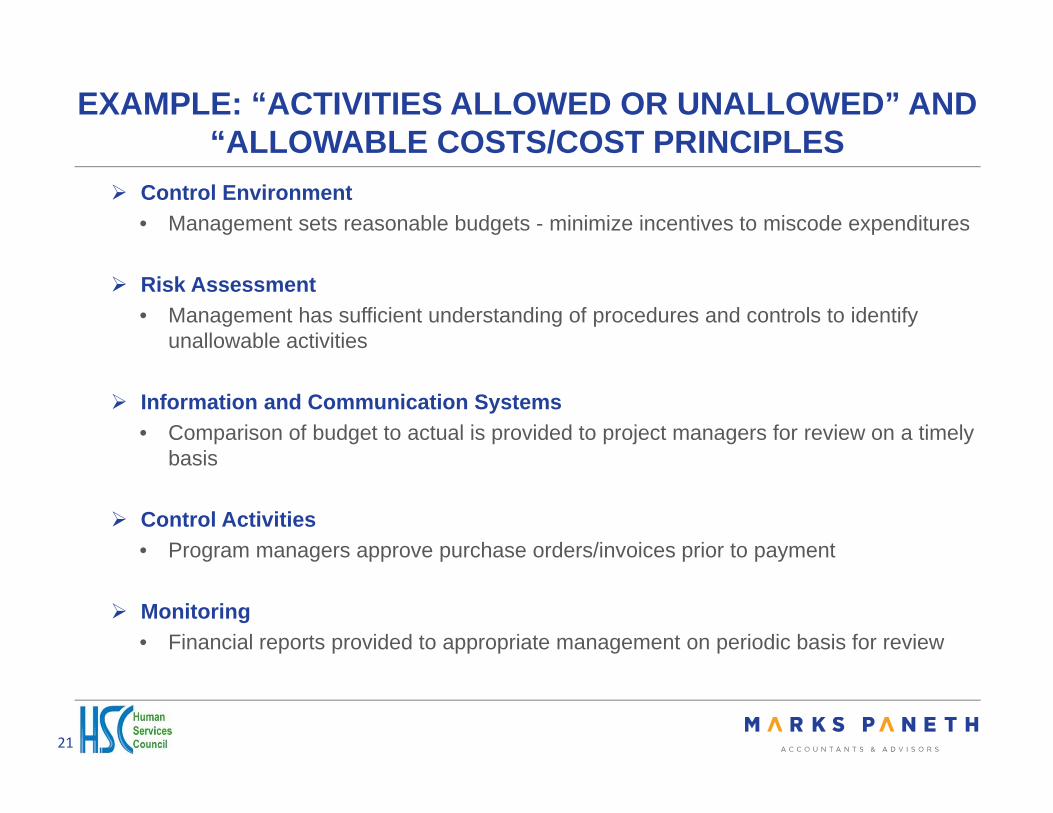

EXAMPLE: “ACTIVITIES ALLOWED OR UNALLOWED” AND “ALLOWABLE COSTS/COST PRINCIPLES

21

Control Environment• Management sets reasonable budgets - minimize incentives to miscode expenditures

Risk Assessment• Management has sufficient understanding of procedures and controls to identify

unallowable activities

Information and Communication Systems• Comparison of budget to actual is provided to project managers for review on a timely

basis

Control Activities• Program managers approve purchase orders/invoices prior to payment

Monitoring• Financial reports provided to appropriate management on periodic basis for review

INTERNAL CONTROL OVER COMPLIANCE –PROCESS VS. CONTROL

22

Processes• Procedures that originate, transfer or change data• Can introduce errors

Controls• Procedures designed to prevent, detect and correct errors

resulting from processing of accounting information• Cannot generate errors

INTERNAL CONTROL

23

Suggested Audit Procedures – Internal Control

1. Using the guidance provided in Part 6, “Internal Control,” perform procedures to obtainan understanding of internal control sufficient to plan the audit to support a lowassessed level of control risk for the program.

2. Plan the testing of internal control to support a low assessed level of control risk forprocurement and suspension and debarment requirements and perform the testing ofinternal control as planned. If internal control over some or all of the compliancerequirements is likely to be ineffective, see the alternative procedures in 2 CFRsection 200.514(c)(4), including assessing the control risk at the maximum andconsidering whether additional compliance tests are required because of ineffectiveinternal control.

3. Consider the results of the testing of internal control in assessing the remaining risk ofnoncompliance. Use this as the basis for determining the nature, timing, and extent(e.g., number of transactions to be selected) of substantive tests of compliance.

24

ADMINISTRATIVE REQUIREMENTS

FINANCIAL MANAGEMENT SYSTEM 2 CFR 200.302

25

Auditee financial management system must provide for the following:

Identification, in its accounts, of all federal awards received and expended and the federal programs under which they were received. Information should include, as applicable:• Catalog of Federal Domestic Assistance (CFDA) title and number• Federal award identification number and year• Federal awarding agency• Pass-through entity (PTE), if applicable

Accurate, current, and complete disclosure of the financial results of each federal award or program

FINANCIAL MANAGEMENT SYSTEM2 CFR 200.302

26

Must Include:• Records that identify the source and application of funds for federally-

funded activities

• Effective control over, and accountability for all funds, property, and other assets.

• Comparison of expenditures with budget amounts for each federal award

• Written procedures to implement the requirements cash management

• Written procedures for determining the allowability of costs in accordance with Cost Principles and terms and conditions of the federal awards

PROCUREMENT2 CFR 200.318 - 326

27

Auditees need to understand UG procurement requirements

States follow the same policies and procedures they use forprocurements from non-federal funds (i.e., state procurementstatues)

Other non-federal entities follow the five procurementmethods outlined in the Guidance

Small purchases, micro-purchases, sealed bids, competitiveproposals, and sole source

PROCUREMENT (CONT’D)2 CFR 200.318 - 326

28

Revised Procurement Categories

Micro-purchase – Under the new standards, micro-purchases are the acquisition of supplies orservices costing less than $3,000. They may be awarded without soliciting competitive quotations if thenonprofit considers the price to be reasonable.

Small purchase – Services, supplies or other property costing less than $150,000 are now considered“small purchase” and are subject to new relatively simple and informal procurement methods. Nonprofitsmust obtain price or rate quotations from an adequate number of qualified sources. The standards donot define “adequate number”.

Sealed bids – Sealed bids are used for purchases over $150,000 and primarily for constructioncontracts. Sealed bids are publicly solicited and a firm price contract is awarded to the responsiblebidder. Generally the lowest bid is selected.

Competitive proposals – Competitive proposals are used for procurements over $150,000 and requirea formal solicitation, and can be either fixed-price or cost-reimbursement contracts. Competitive bids areused when sealed bids are not appropriate. The contract is awarded to the proposal that is mostadvantageous to the program.

Sole source – This category applies to procurements where the item is only available from a singlesource or when there is a public emergency that makes a competitive proposal process too timeconsuming. Sole source procurements require approval from the federal or pass-through fundingsource.

PROCUREMENT (CONT’D)2 CFR 200.318 - 326

29

General Procurement Standards

Documented policies– Nonprofits must have documented procurement policies and procedures in placerelated to the purchase of goods and services with federal funds. These policies must be in accordancewith the federal, state and local regulations. Federal awards must be used only for necessary items andthere should be a full and open competitive procurement process.

Conflict of interest– There are now two types of conflict-of-interest policies required: employee conflict ofinterest and organizational conflict of interest. No employee, officer or agent may participate in theselection, award and or administration of a federally funded contract if there is an actual or apparent conflictof interest. Organizational conflict of interest is a new requirement, under which relationships with a parentcompany, affiliate or subsidiary organization must be identified if they appear to or actually render thenonprofit unable to be impartial in conducting a procurement action.

Documentation of cost and price analysis and vendor selection – There should be sufficientdocumentation on the process of vendor selection and how the nonprofit reached its final decision. Forexample, the organization must conduct a lease/purchase analysis to identify which is more cost effectivebefore entering into a lease or purchase contract.

PROCUREMENT (CONT’D)2 CFR 200.318 - 326

30

Suggested Audit Procedures – Compliance

(Procedures 2 – 5 apply to non-Federal entities other than States.)

2. Obtain the entity’s procurement policies and verify that the policiescomply with the compliance requirements highlighted above.

3. Verify that the entity has written standards of conduct covering conflictsof interest and governing the performance of its employees engaged inthe selection, award, and administration of contracts (2 CFR section200.318(c) and 48 CFR sections 52.203-13 and 52.303-16).

4. Ascertain if the entity has a policy to use statutorily or administrativelyimposed in-State or local geographical preferences in the evaluation ofbids or proposals. If yes, verify that these limitations were not appliedto federally funded procurements except where applicable Federalstatutes expressly mandate or encourage geographic preference (2CFR section 200.319(b)).

PROCUREMENT (CONT’D)2 CFR 200.318 - 326

31

5. Select a sample of procurements and perform the following procedures:

a. Examine contract files and verify that they document the history of the procurement,including the rationale for the method of procurement, selection of contract type, basisfor contractor selection, and the basis for the contract price (2 CFR section 200.318(i)and 48 CFR part 44 and section 52.244-2).

b. For grants and cooperative agreements, verify that the procurement method used wasappropriate based on the dollar amount and conditions specified in 2 CFR section200.320.

c. Verify that procurements provide full and open competition (2 CFR section200.319 and 48 CFR section 52.244-5).

d. Examine documentation in support of the rationale to limit competition in those caseswhere competition was limited and ascertain if the limitation was justified (2 CFRsections 200.319 and 200.320(f) and 48 CFR section 52.244-5).

e. Ascertain if cost or price analysis was performed in connection with all procurementactions exceeding the simplified acquisition threshold, including contractmodifications, and that this analysis supported the procurement action (2 CFR section200.323 and 48 CFR section 15.404-3).

PROCUREMENT (CONT’D)2 CFR 200.318 - 326

32

Note: A cost or price analysis is required for each procurement action, including each contractmodification, when the total amount of the contract and related modifications is greater than thesimplified acquisition threshold.)

f. Verify consent to subcontract was obtained when required by the terms and conditions of a costreimbursement contract under the FAR (48 CFR section 52.244-2).

(Procedures 6 and 7 apply to all non-Federal entities)

6. Review the non-Federal entity’s procedures for verifying that an entity withwhich it plans to enter into a covered transaction is not debarred, suspended,or otherwise excluded (2 CFR sections 200.212 and 200.318(h); 2 CFRsection 180.300; 48 CFR section 52.209-6).

7. Select a sample of procurements and subawards and test whether the non-Federal entity followed its procedures before entering into a coveredtransaction.

IMPORTANT COFAR FAQ ON EFFECTIVE DATE AND GRACE PERIOD FOR PROCUREMENT

33

FAQ .110-6 states, for compliance with the new procurement standardsonly, the federal government is providing a grace period of two full fiscalyears after the effective date of the Uniform Guidance for Federal Awards.

The FAQ goes on to provide information on certain documentation that thenon-federal entity will have to provide in this regard and how it will affect thesingle audit in its first year.

SUBRECIPIENT MONITORING: PASS- THROUGH ENTITY REQUIREMENTS

2 CFR 200.330 & .331

34

Determine if subrecipient or

contractor

Clearly identify subawards to subrecipients

Consider results of subrecipient audits

Provide certain subaward

information at time of subaward

Evaluate each subrecipient’s risk of noncompliance

Consider imposing specific subaward

conditions

Monitor activities of subrepcients

Verify subrecipientaudited

Consider taking enforcement action for noncompliant

subrecipients

SUBRECIPIENT MONITORING

35

PTE monitoring of the subrecipient must include:

Reviewing financial and performance reports required by the PTE

Following-up and ensuring that the subrecipient takes timely and appropriate action on all deficiencies pertaining to the federal award provided to the subrecipient• Includes deficiencies detected through audits, on-site reviews, and

other means. Issuing a management decision for audit findings pertaining to the

Federal award provided to the subrecipient from the PTE as required by §200.521 Management decision.

Depending on risk assessment results, may require additional monitoring procedures.

SUBAWARD REQUIREMENTS

36

Federal Award Identification

All requirements imposed by the PTE

Additional requirements that the PTE imposes on the subrecipient, includingidentification of any required financial or performance reports

An approved federally recognized indirect cost rate negotiated between thesubrecipient and the federal government or, if no such rate exists, either arate negotiated between the PTE and the subrecipient or a de minimisindirect cost rate as defined in section 200.414

A requirement that the subrecipient permit the PTE and auditors to haveaccess to the subrecipient’s records and financial statements, as necessary

Appropriate terms and conditions concerning the closeout of the subaward

SUBRECIPIENT MONITORING

37

Suggested Audit Procedures – Compliance

1. Review the PTE’s subrecipient monitoring policies and procedures to gain an understanding ofthe PTE’s process to identify subawards, evaluate risk of noncompliance, and perform monitoringprocedures based upon identified risks.

2. Review subaward documents including the terms and conditions of the subaward to ascertain if,at the time of subaward (or subsequent subaward modification), the PTE made the subrecipientaware of the award information required by 2 CFR section 200.331(a) sufficient for the PTE tocomply with Federal statutes, regulations, and the terms and conditions of the award.

3. Review the PTE’s documentation of monitoring the subaward and consider if the PTE’smonitoring provided reasonable assurance that the subrecipient used the subaward forauthorized purposes in compliance with Federal statutes, regulations, and the terms andconditions of the subaward.

4. Ascertain if the PTE verified that subrecipients expected to be audited as required by 2 CFR part200, subpart F, met this requirement (2 CFR section 200.331(f)). This verification may beperformed as part of the required monitoring under 2 CFR section 200.331(d)(2) to ensure thatthe subrecipient takes timely and appropriate action on deficiencies detected though audits.

EQUIPMENT STANDARDS2 CFR 200.313

38

Equipment Inventory:• Take inventory of all equipment that has been acquired with Federal

funds (at least once every two years)• Reconcile the inventory count to your property records

Property Records:• Make sure your property records include all of the required data elements

outlined in Subpart D

EQUIPMENT STANDARDS (CONT’D.)2 CFR 200.313

39

Suggested Audit Procedures – Compliance

Inventory Management of Equipment Acquired Under Federal Awards

a. Identify equipment acquired and trace selected purchases to the propertyrecords. Verify that the property records contain the required information.

b. Verify that the required physical inventory of equipment was performed.Test whether any differences between the physical inventory andequipment records were resolved.

c. Select a sample from all equipment identified as acquired under Federalawards from the property records and physically inspect the equipmentand determine whether the equipment is appropriately safeguarded andmaintained.

EQUIPMENT STANDARDS (CONT’D.)2 CFR 200.313

40

Suggested Audit Procedures – Compliance

Disposition of Equipment Acquired Under Federal Awards

a. Identify equipment dispositions for the audit period and performprocedures to verify that the dispositions of equipment acquired underFederal awards were properly reflected in the property records.

b. For dispositions of equipment acquired under grants and cooperativeagreements with a current per-unit fair market value of $5,000 or more,verify whether the Federal awarding agency was reimbursed for theFederal portion of the current market value or sales proceeds.

c. For dispositions of equipment acquired under cost-reimbursementcontracts, verify that the non-Federal entity followed Federal awardingagency disposition instructions.

EQUIPMENT STANDARDS (CONT’D.)2 CFR 200.313

41

Suggested Audit Procedures – Compliance

Disposition of Real Property Acquired Under Federal Awards

a. Identify real property dispositions for the audit period and determinewhether such real property was acquired or improved under Federalawards.

b. For dispositions of real property acquired or improved under Federalawards, perform procedures to verify that the non-Federal entity followedthe instructions of the Federal awarding agency or pass-through entity,which normally require reimbursement to the Federal awarding agencyfor the Federal portion of net sales proceeds or fair market value at thetime of disposition, as applicable.

CASH MANAGEMENT

42

For grants and cooperative agreements, all non-federal entities mustestablish written procedures to implement the requirements of 2 CFRsection 200.305

The “minimized elapsed time for funds transfer” is based on the paymentsystem/method a non-federal entity uses

More emphasis on cost-reimbursement contracts under the FederalAcquisition Regulation (FAR)

Credit any Interest earned back to the federal government

CASH MANAGEMENT (CONT’D.)

43

Suggested Audit Procedures – Compliance

Review trial balances related to Federal funds for unearned revenue. Ifunearned revenue balances are identified, consider if such balances areconsistent with the requirement to minimize the time between drawing anddisbursing Federal funds.

Select a sample of advance payments and verify that the non-Federal entityminimized the time elapsing between the transfer of funds from the U.S.Treasury or pass-through entity and disbursement by the non-Federal entity.

When non-Federal entities are funded under the reimbursement method, selecta sample of transfers of funds from the U.S. Treasury or pass-through entityand trace to supporting documentation and ascertain if the entity paid for thecosts for which reimbursement was requested prior to the date of thereimbursement request (2 CFR section 200.305(b)(3)).

CASH MANAGEMENT (CONT’D.)

44

Suggested Audit Procedures – Compliance (cont’d)

When a program receives program income (including repayments to arevolving fund), rebates, refunds, contract settlements, audit recoveries, orinterest earned on such funds; perform tests to ascertain if these funds weredisbursed before requesting additional Federal cash draws (2 CFR section200.305(b)(5)).

Review records to determine if interest in excess of $500 per year was earnedon Federal cash draws. If so, review evidence to ascertain if it was remittedannually to the Department of Health and Human Services, PaymentManagement System (2 CFR section 200.305(9)).

Cost-reimbursement contracts under the Federal Acquisition Regulation

Perform tests to ascertain if the non-Federal entity requesting reimbursement(a) disbursed funds prior to the date of the request, or (b) meets the conditionsallowing for the request for costs incurred, but not necessarily paid for, i.e.,ordinarily within 30 days of the request (48 CFR section 52.216-7(b)).

ALLOWABLE COSTS AND COST PRINCIPLES

45

Need to Understand Subpart E - Cost Principles• Describes the cost accounting requirements associated with federal

awards • Includes requirements for indirect costs• Includes requirements for compensation – personal services

OMB Compliance Supplement includes a table of selected items of cost allowability for differing types of organizations• Do not rely on exclusively; instead refer to Uniform Guidance

Key area of focus for auditees:• Compensation – Personal Services• Indirect Costs• Preapproval Items (see §200.407 for list)

COMPENSATION – PERSONAL SERVICES

46

Time and distribution records must be maintained for all employees whose salary is:

• Paid in whole or in part with federal funds• Used to meet a match/cost share requirement

Not based on budget estimates alone – needs to be ACTUAL

Full disclosure• All time worked for the organization and what percentage is federal

COMPENSATION – PERSONAL SERVICES –DOCUMENTATION 2 CFR 200.430

47

Charges to federal awards for salaries and wages must be based on records that accurately reflect the work performed

Numerous record requirements including: • Must be supported by a system of internal controls which

provides reasonable assurance that amounts are accurate,allowable and properly allocated

• Must be incorporated into official records

• Must reasonably reflect total activity for which the employee iscompensated by the non-federal entity, not exceeding 100% ofcompensated activities

COMPENSATION – PERSONAL SERVICES –DOCUMENTATION §200.430

48

Numerous record requirements including:

• Nonexempt employees must also prepare records indicatingthe total number of hours worked each day

• Salaries and wages of employees used in meeting cost sharingor matching requirements on federal awards must be supportedin the same manner

COST PRINCIPLES – INDIRECT COSTS

49

Federal agencies and PTEs will have to accept a non-federal entity’s negotiated indirect cost rate

Unless a statute or regulation allows for an exception

Non-federal entities will have a one-time option to extend rate for up to four years

For non-federal entities who have never received a negotiated rate, de minimis rate of 10% of modified total direct costs may be used indefinitely

ALLOWABLE COSTS

50

Suggested Compliance Audit Procedures – Direct Costs

Test direct costs charged to Federal awards with the following criteria:

a. Costs were approved by the Federal awarding agency, if required. (See 2CFR section 200.407 for items of cost that require prior written approval andExhibit 1, Selected Items of Cost, in this part of the Supplement.)

b. Costs were necessary and reasonable for the performance of the Federalaward and allocable under the principles of 2 CFR 200, subpart E.

c. Costs conformed to any limitations or exclusions set forth in 2 CFR 200,subpart E, or in the Federal award as to types or amount of cost items.

d. Costs were consistent with policies and procedures that apply uniformly toboth federally financed and other activities of the NPO.

ALLOWABLE COSTS

51

Suggested Compliance Audit Procedures – Direct Costs

e. Costs were accorded consistent treatment. Cost were not assigned to aFederal award as a direct cost if any other cost incurred for the samepurpose in like circumstances was allocated to a Federal award as anindirect cost.

f. Costs were not included as a cost of any other federally financed program in eitherthe current or a prior period.

g. Costs were not used to meet the cost‐sharing or matching requirements of anotherfederal program, except where authorized by Federal statute.

h. Costs were adequately documented.

ALLOWABLE COSTS

52

Suggested Compliance Audit Procedures – Indirect Costs

Test indirect costs with the following criteria:

1) Conform to the allowability of cost provisions in 2 CFR part 200.

2) Are supported by appropriate documentation, such as purchase orders, receivingreports, contractor invoices, canceled checks, and time and attendance records, andcorrectly charged as to account, amount, and period.

3) Are calculated in conformity with generally accepted accounting principles or CAS, asrequired.

4) Are not used to meet cost-sharing or matching requirements of other federallysupported activities.

5) Be given consistent accounting treatment within and between accounting periods.Consistency in accounting requires that costs incurred for the same purpose, in likecircumstances, be treated as either direct costs only or indirect costs only with respectto final cost objectives.

ALLOWABLE COSTS

53

Suggested Compliance Audit Procedures – Indirect Costs

For NPO’s that charge indirect costs to Federal awards based on federally negotiatedrates, obtain the current indirect cost rate agreement, including the proposal used inthe negotiation of the agreement, and determine the type of rates (i.e., pre‐determined, fixed rate, provisional rate, or final rate as described in 2 CFR part 200,Appendix IV, section C) and terms in effect for the year being audited.

1) If a fixed rate agreement with carry-forward provisions has been negotiated with thecognizant agency for indirect cost, determine that the difference between theestimated indirect costs and the actual indirect costs of the period was correctlycalculated and carried forward to the rate computation in the current year.

2) If a provisional rate was used to bill for indirect costs, determine whether a final ratehas been negotiated and appropriate billing adjustments have been made based onthe final negotiated rate.

54

QUESTIONS & ANSWERS

WE ARE COMMITTED TO YOUR SUCCESSOur priority is to help you make smart decisions at every turn.