Embed Size (px)

Citation preview

UNICREDITO ITALIANO Alessandro Profumo - CEO

UBSW ITALIAN FINANCIALS CONFERENCE

Rome, - February 7th, 2002

“CROSS-SELLING: REALITY OR MIRAGE?”

2

Today in Italy many banking and non-banking players, such as insurance companies and “utilities” (i.e. Poste Italiane, Italgas, AEM), leverage on cross-selling in order to sell financial services

This trend creates higher competition and market overshoot, supporting the belief that cross-selling is at the same time the most important factor and measure of success

TODAY CROSS-SELLING IS CONSIDERED THE KEY FACTOR FOR SUCCESS IN THE FINANCIAL SERVICES MARKET

THIS RAISES TWO QUESTIONS:

IS CROSS-SELLING REALLY SO IMPORTANT IN ORDER TO DETERMINE BUSINESS SUCCESS?

IS IT SO EASY TO MAKE A SUCCESSFUL CROSS-SELLING?

3

Is it easy to make a successful cross-selling ?

Requirements for a successful cross-selling

How to manage a successful cross-selling

Is cross-selling so important to succeed?

Conclusions

Agenda

4

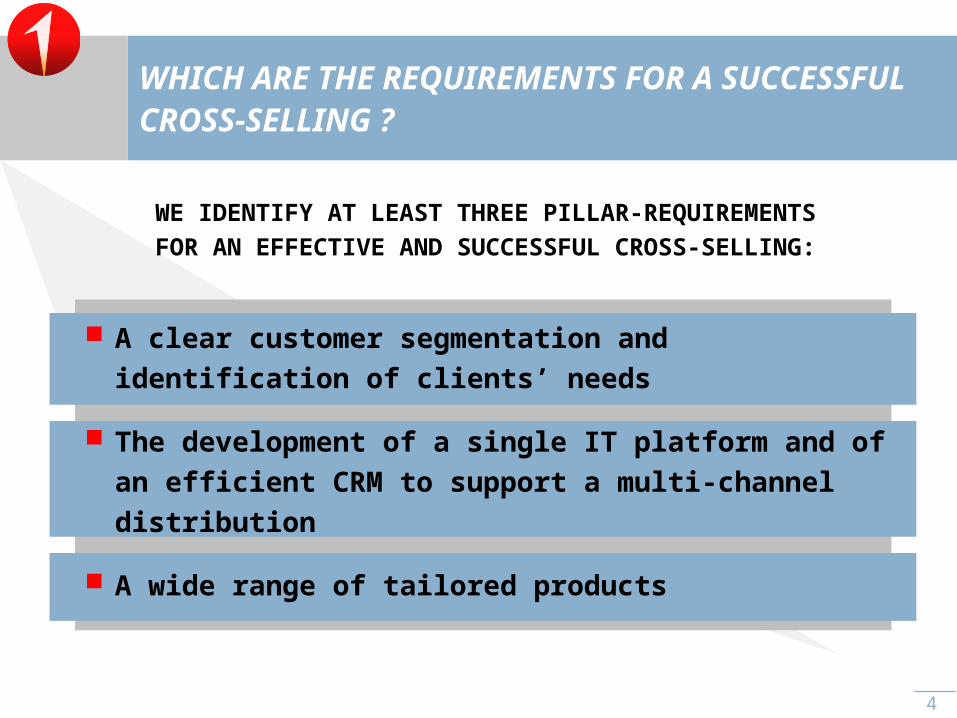

WHICH ARE THE REQUIREMENTS FOR A SUCCESSFUL CROSS-SELLING ?

WE IDENTIFY AT LEAST THREE PILLAR-REQUIREMENTS FOR AN EFFECTIVE AND

SUCCESSFUL CROSS-SELLING:

A clear customer segmentation and identification of clients’ needs

The development of a single IT platform and of an efficient CRM to support a multi-channel distribution

A wide range of tailored products

5

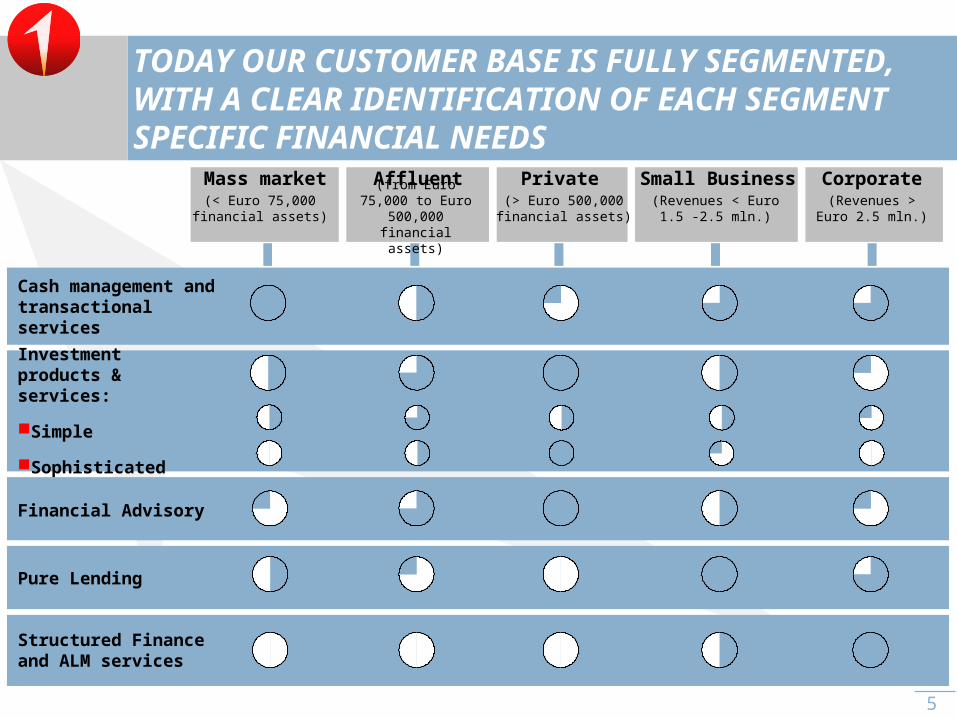

Mass market Affluent Private Small Business Corporate

Cash management and transactional services

Investment products & services:

Simple

Sophisticated

Financial Advisory

Pure Lending

Structured Finance and ALM services

TODAY OUR CUSTOMER BASE IS FULLY SEGMENTED, WITH A CLEAR IDENTIFICATION OF EACH SEGMENT SPECIFIC FINANCIAL NEEDS

(< Euro 75,000 financial assets)

(from Euro 75,000 to Euro 500,000 financial assets)

(> Euro 500,000 financial assets)

(Revenues < Euro 1.5 -2.5 mln.)

(Revenues > Euro 2.5 mln.)

6

Serviceplatforms BackOffice

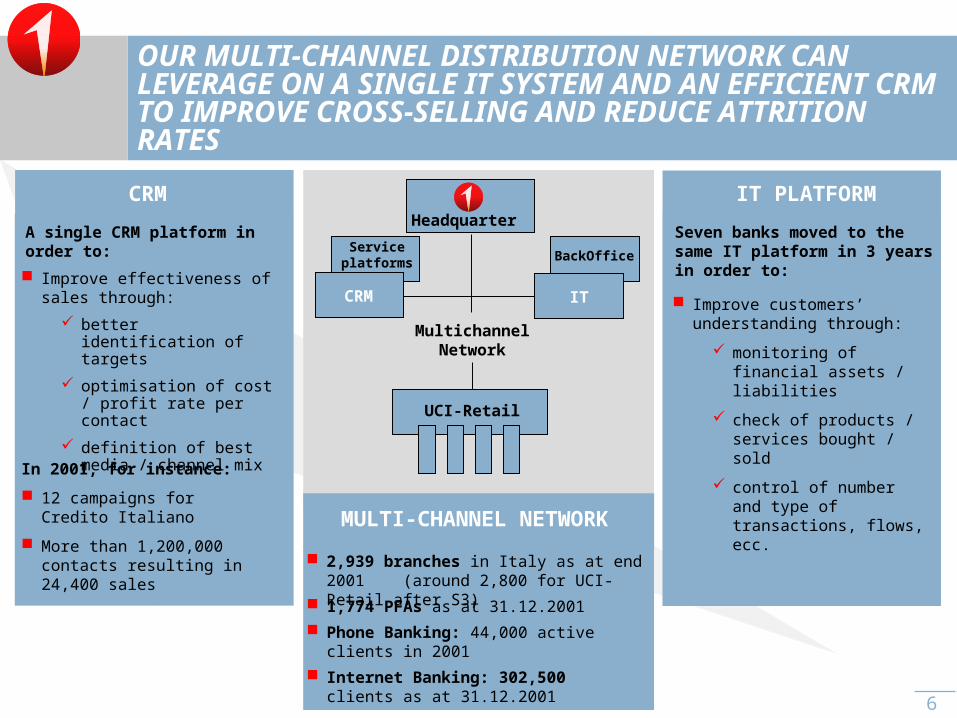

OUR MULTI-CHANNEL DISTRIBUTION NETWORK CAN LEVERAGE ON A SINGLE IT SYSTEM AND AN EFFICIENT CRM TO IMPROVE CROSS-SELLING AND REDUCE ATTRITION RATES

Headquarter

CRM IT

UCI-Retail

A single CRM platform in order to:

IT PLATFORM

Improve effectiveness of sales through:

better identification of targets

optimisation of cost / profit rate per contact

definition of best media / channel mix

CRM

MultichannelNetwork

Seven banks moved to the same IT platform in 3 years in order to:

Improve customers’ understanding through:

monitoring of financial assets / liabilities

check of products / services bought / sold

control of number and type of transactions, flows, ecc.

MULTI-CHANNEL NETWORK

2,939 branches in Italy as at end 2001 (around 2,800 for UCI-Retail after S3)

1,774 PFAs as at 31.12.2001

Phone Banking: 44,000 active clients in 2001

Internet Banking: 302,500 clients as at 31.12.2001

In 2001, for instance:

12 campaigns for Credito Italiano

More than 1,200,000 contacts resulting in 24,400 sales

7

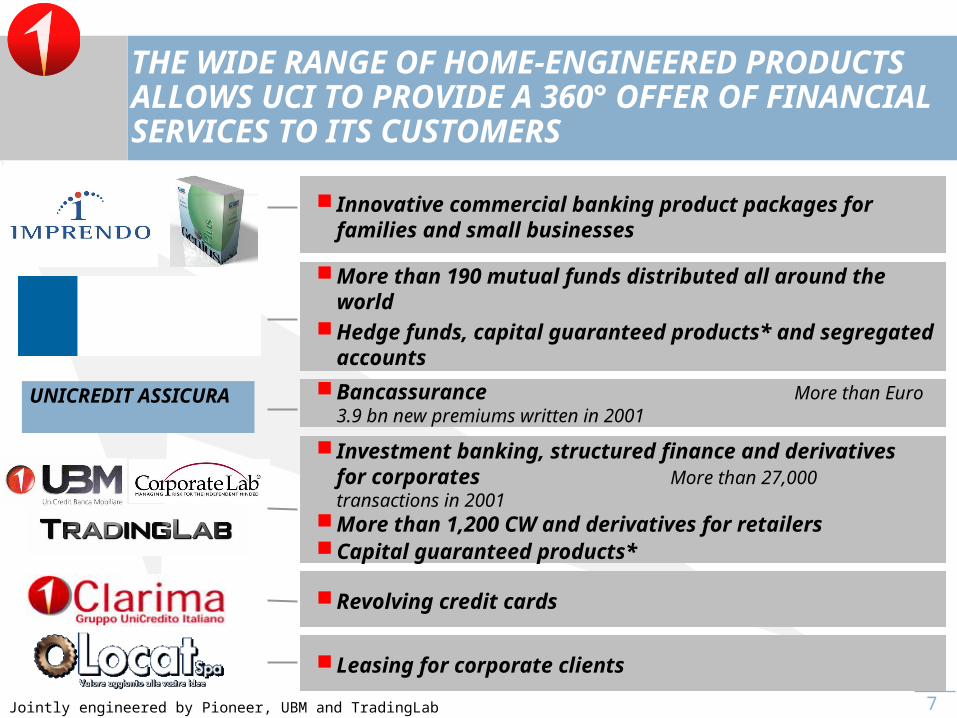

Innovative commercial banking product packages for families and small businesses

THE WIDE RANGE OF HOME-ENGINEERED PRODUCTS ALLOWS UCI TO PROVIDE A 360° OFFER OF FINANCIAL SERVICES TO ITS CUSTOMERS

UNICREDIT ASSICURA

More than 190 mutual funds distributed all around the world

Hedge funds, capital guaranteed products* and segregated accounts

Bancassurance More than Euro 3.9 bn new premiums written in 2001

Leasing for corporate clients

Revolving credit cards

Investment banking, structured finance and derivatives for corporates More than 27,000 transactions in 2001

More than 1,200 CW and derivatives for retailersCapital guaranteed products*

* Jointly engineered by Pioneer, UBM and TradingLab

8

Is it easy to make a successful cross-selling ?

Requirements for a successful cross-selling

How to manage a successful cross-selling

Is cross-selling so important to succeed?

Conclusions

Agenda

9

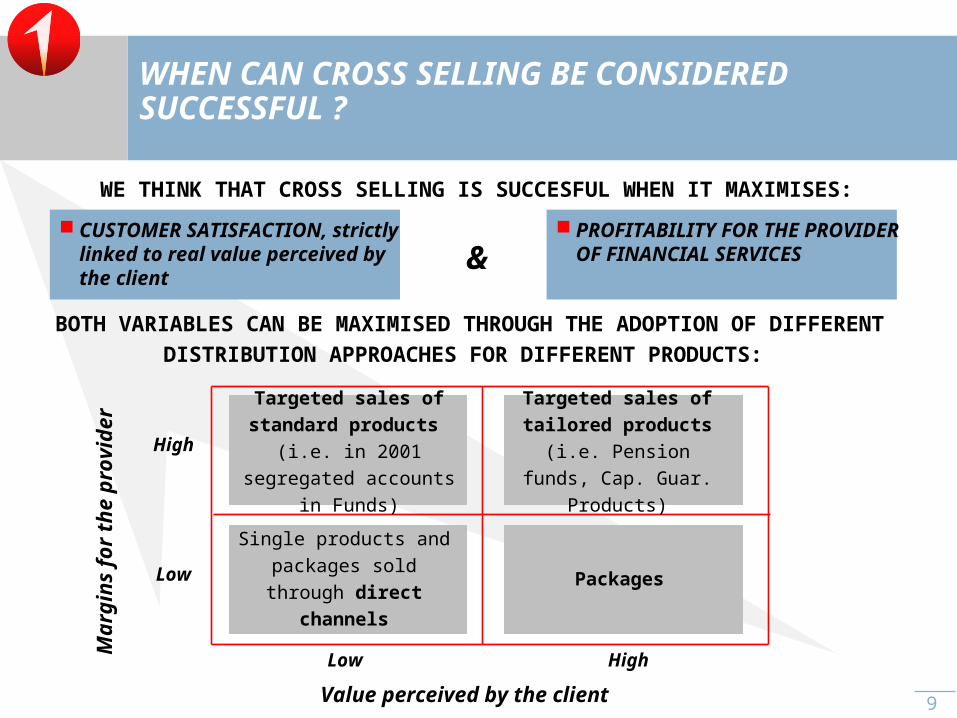

WHEN CAN CROSS SELLING BE CONSIDERED SUCCESSFUL ?

WE THINK THAT CROSS SELLING IS SUCCESFUL WHEN IT MAXIMISES:

CUSTOMER SATISFACTION, strictly linked to real value perceived by the client

& PROFITABILITY FOR THE

PROVIDER OF FINANCIAL SERVICES

BOTH VARIABLES CAN BE MAXIMISED THROUGH THE ADOPTION OF DIFFERENT DISTRIBUTION APPROACHES FOR DIFFERENT PRODUCTS:

Value perceived by the client

Marg

ins f

or

the p

rovid

er

HighLow

High

LowSingle products and

packages sold through direct channels

Packages

Targeted sales of tailored products (i.e. Pension funds,

Cap. Guar. Products)

Targeted sales of standard products

(i.e. in 2001 segregated accounts in Funds)

10

Valu

e f

or

the c

lien

t

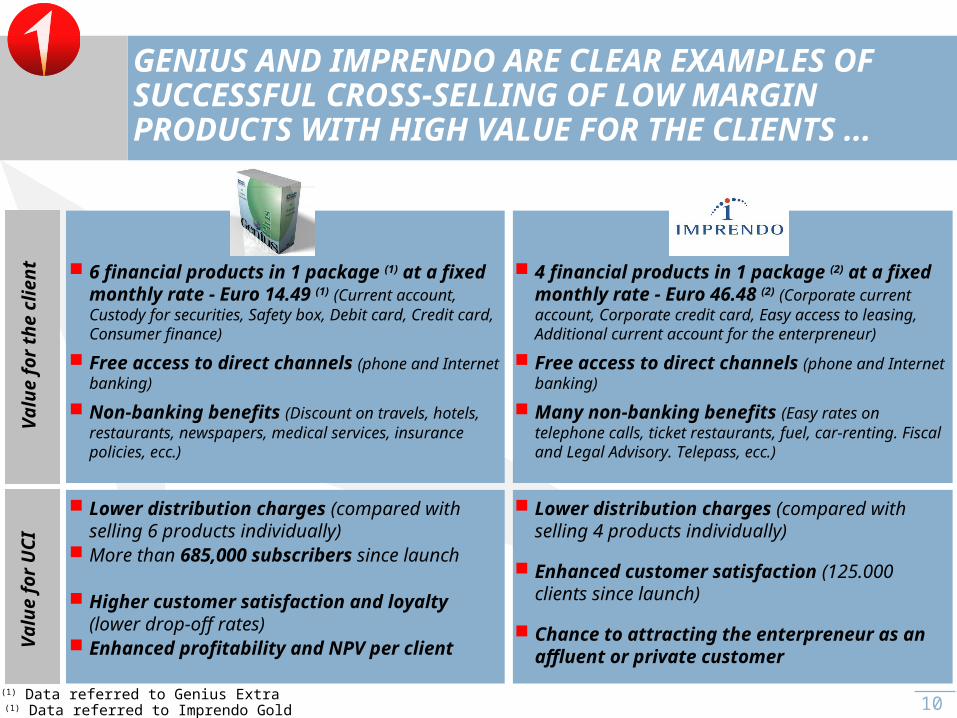

GENIUS AND IMPRENDO ARE CLEAR EXAMPLES OF SUCCESSFUL CROSS-SELLING OF LOW MARGIN PRODUCTS WITH HIGH VALUE FOR THE CLIENTS ...

Valu

e f

or

UC

I

6 financial products in 1 package (1) at a fixed monthly rate - Euro 14.49 (1) (Current account, Custody for securities, Safety box, Debit card, Credit card, Consumer finance)

Free access to direct channels (phone and Internet banking)

Non-banking benefits (Discount on travels, hotels, restaurants, newspapers, medical services, insurance policies, ecc.)

(1) Data referred to Genius Extra

4 financial products in 1 package (2) at a fixed monthly rate - Euro 46.48 (2) (Corporate current account, Corporate credit card, Easy access to leasing, Additional current account for the enterpreneur)

Free access to direct channels (phone and Internet banking)

Many non-banking benefits (Easy rates on telephone calls, ticket restaurants, fuel, car-renting. Fiscal and Legal Advisory. Telepass, ecc.)

(1) Data referred to Imprendo Gold

Lower distribution charges (compared with selling 6 products individually)

Higher customer satisfaction and loyalty (lower drop-off rates)

Enhanced profitability and NPV per client

Lower distribution charges (compared with selling 4 products individually)

Enhanced customer satisfaction (125.000 clients since launch)

Chance to attracting the enterpreneur as an affluent or private customer

More than 685,000 subscribers since launch

11

... AS SHOWN BY THE BRILLIANT RESULTS ACHIEVED

Clients without Genius

MAIN GENIUS PERFORMANCES (1):

Clients with% Ch.

Drop-off Ratio

Customer Satisfaction (2)

Cross-selling

Av. Yearly Margin per client

Gross NPV per client (in %) (3)

2.26

7.0%

58.6%

Euro 837

100.0%

4.48

2.7%

65.7%

Euro 1,056

165.6%

+98.2%

-4.3%

7.1%

+26.2%

+65.6%

(2) Measure of satisfaction towards the Bank (Credito Italiano) resulting from an EURISKO market research

(1) Source: MKS (UCI-Strategic Marketing), on 1999 and 2000 data

(3) Calculated as sum of revenues generated by each client on a 25 year timeframe, discounted at UCI’s cost of equity (8.95%) and taking into account drop-off ratios of each category. Data re-based in % terms.

12

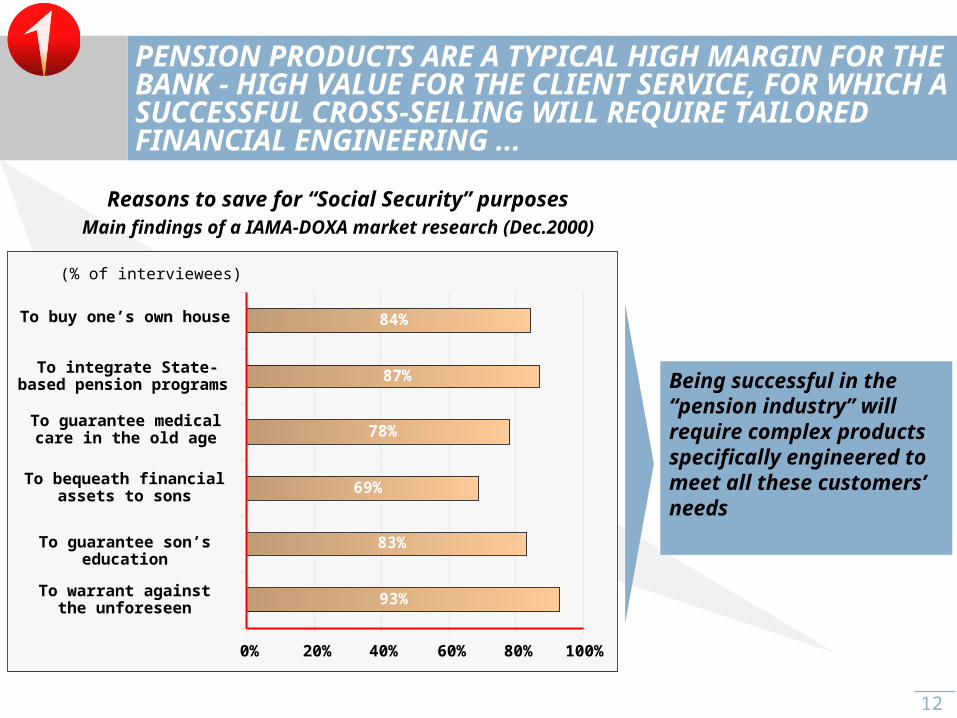

Being successful in the “pension industry” will require complex products specifically engineered to meet all these customers’ needs

PENSION PRODUCTS ARE A TYPICAL HIGH MARGIN FOR THE BANK - HIGH VALUE FOR THE CLIENT SERVICE, FOR WHICH A SUCCESSFUL CROSS-SELLING WILL REQUIRE TAILORED FINANCIAL ENGINEERING ...

93%

83%

69%

78%

87%

84%

0% 20% 40% 60% 80% 100%

To warrant against the unforeseen

To guarantee son’s education

To bequeath financial assets to sons

To guarantee medical care in the

old age

To integrate State-based pension programs

To buy one’s own house

Reasons to save for “Social Security” purposesMain findings of a IAMA-DOXA market research (Dec.2000)

(% of interviewees)

13

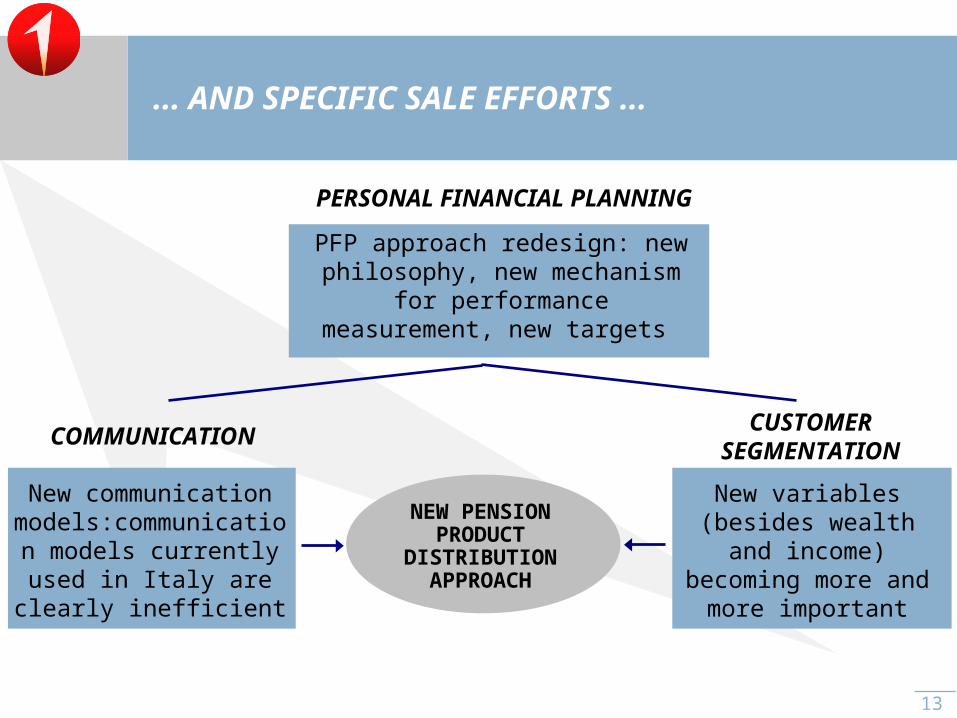

... AND SPECIFIC SALE EFFORTS ...

New communication models:communication models currently used

in Italy are clearly inefficient

PFP approach redesign: new philosophy, new mechanism for

performance measurement, new targets

NEW PENSION PRODUCT

DISTRIBUTION APPROACH

New variables (besides wealth and income) becoming

more and more important

PERSONAL FINANCIAL PLANNING

COMMUNICATIONCUSTOMER

SEGMENTATION

14

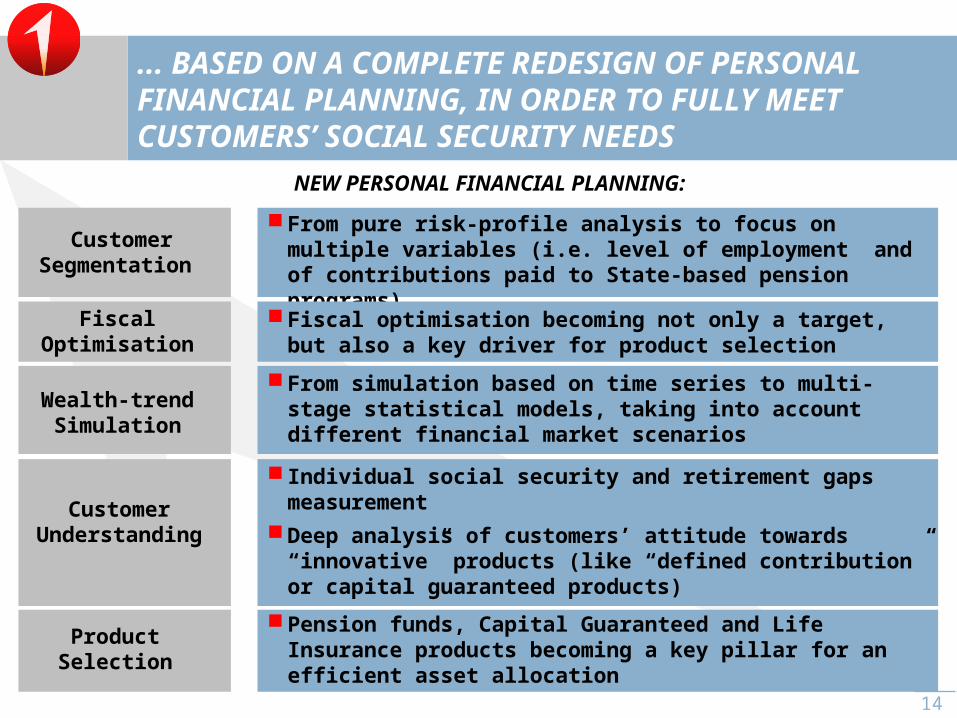

... BASED ON A COMPLETE REDESIGN OF PERSONAL FINANCIAL PLANNING, IN ORDER TO FULLY MEET CUSTOMERS’ SOCIAL SECURITY NEEDS

Fiscal Optimisation

Product Selection

From pure risk-profile analysis to focus on multiple variables (i.e. level of employment and of contributions paid to State-based pension programs)

Fiscal optimisation becoming not only a target, but also a key driver for product selection

From simulation based on time series to multi-stage statistical models, taking into account different financial market scenarios

Pension funds, Capital Guaranteed and Life Insurance products becoming a key pillar for an efficient asset allocation

Individual social security and retirement gaps measurement

Deep analysis of customers’ attitude towards “innovative” products (like “defined contribution” or capital guaranteed products)

Customer Segmentation

Wealth-trend Simulation

Customer Understanding

NEW PERSONAL FINANCIAL PLANNING:

15

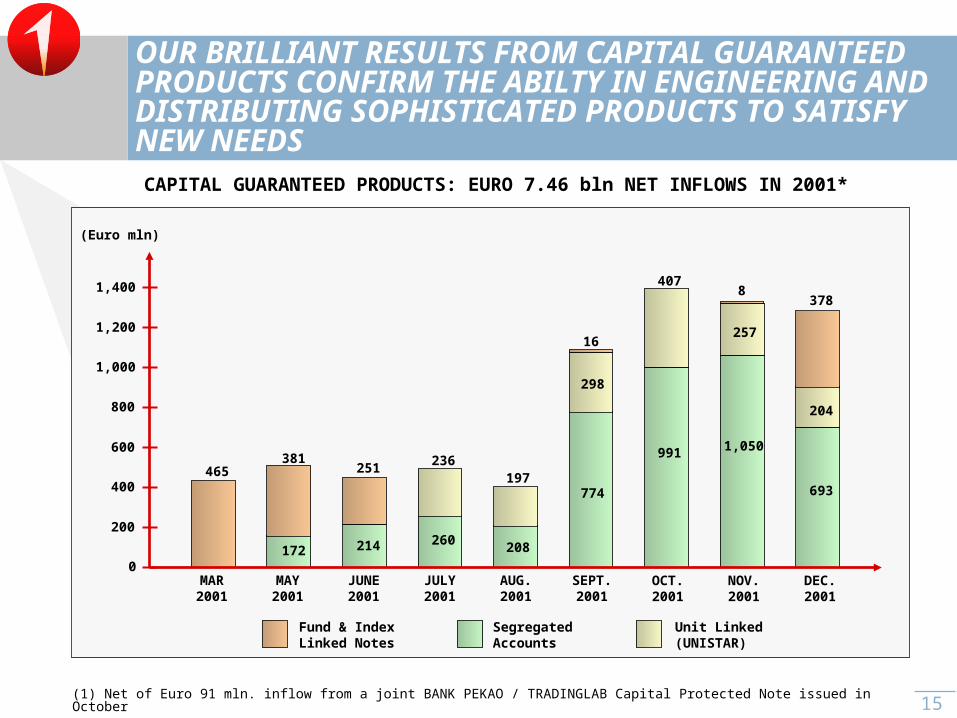

OUR BRILLIANT RESULTS FROM CAPITAL GUARANTEED PRODUCTS CONFIRM THE ABILTY IN ENGINEERING AND DISTRIBUTING SOPHISTICATED PRODUCTS TO SATISFY NEW NEEDSCAPITAL GUARANTEED PRODUCTS: EURO 7.46 bln NET INFLOWS IN

2001*

260200

400

600

800

1,000

(Euro mln)

0 208

774

298

197 236

214 172

MAY 2001

JUNE 2001

JULY 2001

AUG. 2001

SEPT. 2001

Segregated Accounts

Unit Linked (UNISTAR)

MAR 2001

465 381

251

16

Fund & Index Linked Notes

1,200

1,400

OCT. 2001

991

407

1,050

257

8

693

204

378

NOV. 2001

DEC. 2001

(1) Net of Euro 91 mln. inflow from a joint BANK PEKAO / TRADINGLAB Capital Protected Note issued in October

16

Is it easy to make a successful cross-selling ?

Requirements for a successful cross-selling

How to manage a successful cross-selling

Is cross-selling so important to succeed?

Conclusions

Agenda

17

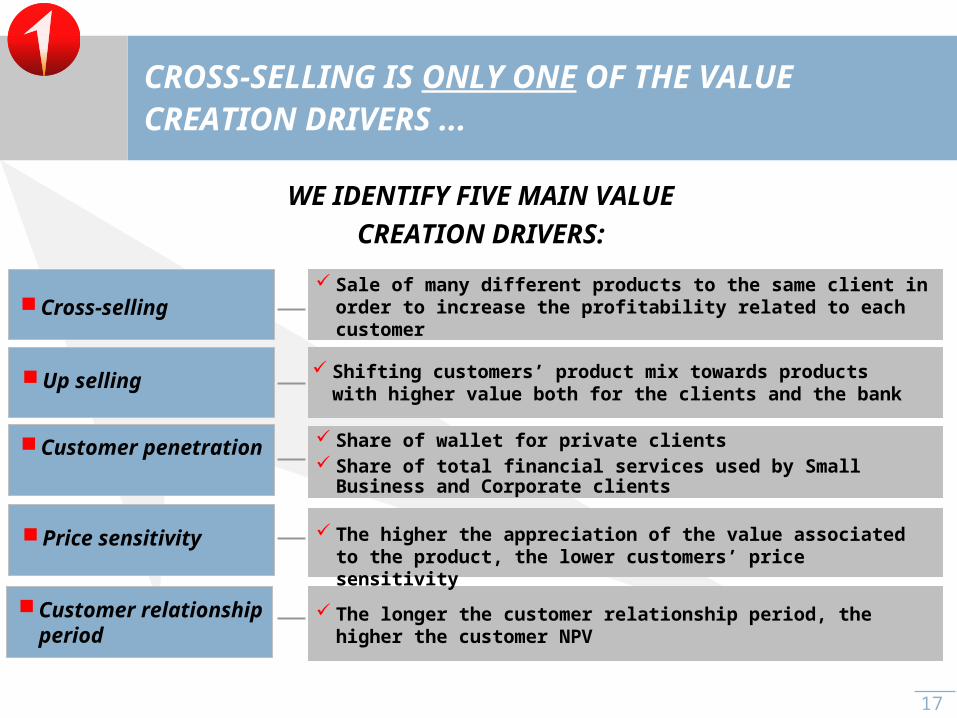

CROSS-SELLING IS ONLY ONE OF THE VALUE CREATION DRIVERS ...

Sale of many different products to the same client in order to increase the profitability related to each customer

Customer penetration

Customer relationship period

Price sensitivity

Up selling Shifting customers’ product mix towards products

with higher value both for the clients and the bank

Cross-selling

Share of wallet for private clients Share of total financial services used by Small Business

and Corporate clients

The higher the appreciation of the value associated to the product, the lower customers’ price sensitivity

The longer the customer relationship period, the higher the customer NPV

WE IDENTIFY FIVE MAIN VALUE CREATION DRIVERS:

18

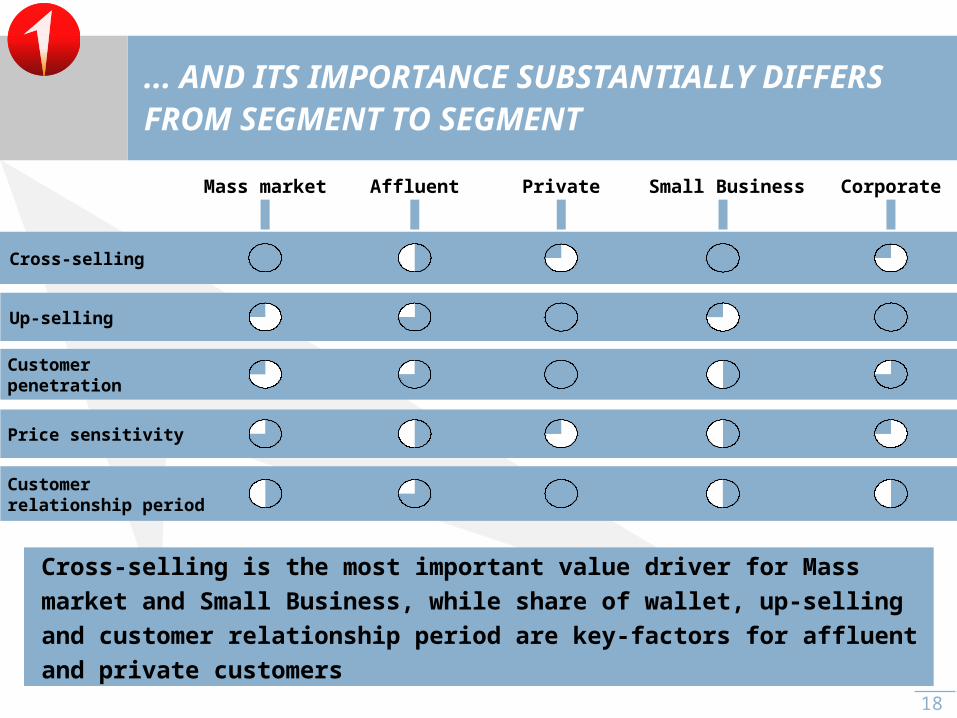

... AND ITS IMPORTANCE SUBSTANTIALLY DIFFERS FROM SEGMENT TO SEGMENT

Mass market Affluent Private Small Business Corporate

Cross-selling

Customer penetration

Price sensitivity

Customer relationship period

Up-selling

Cross-selling is the most important value driver for Mass market and Small Business, while share of wallet, up-selling and customer relationship period are key-factors for affluent and private customers

19

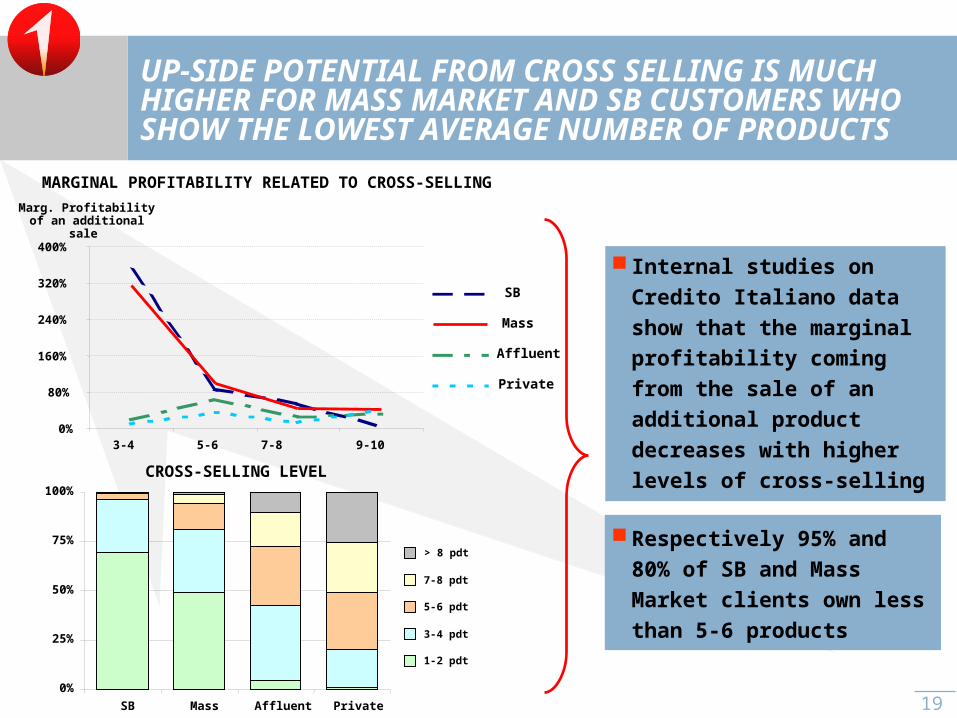

Respectively 95% and 80% of SB and Mass Market clients own less than 5-6 products

Internal studies on Credito Italiano data show that the marginal profitability coming from the sale of an additional product decreases with higher levels of cross-sellingCROSS-SELLING LEVEL

MARGINAL PROFITABILITY RELATED TO CROSS-SELLING

UP-SIDE POTENTIAL FROM CROSS SELLING IS MUCH HIGHER FOR MASS MARKET AND SB CUSTOMERS WHO SHOW THE LOWEST AVERAGE NUMBER OF PRODUCTS

0%

25%

50%

75%

100%

SB Mass Affluent Private

> 8 pdt

7-8 pdt

5-6 pdt

3-4 pdt

1-2 pdt

Marg. Profitability of an additional sale

0%

80%

160%

240%

320%

400%

3-4 5-6 7-8

9-10

SB

Mass

Affluent

Private

20

150,000 250,000 500,000 1,000,000

0

500

1,000

1,500

2,000

2,500

3,000

< 25,000 25-75,000 75- 150- 250- 500- > 1,000,000

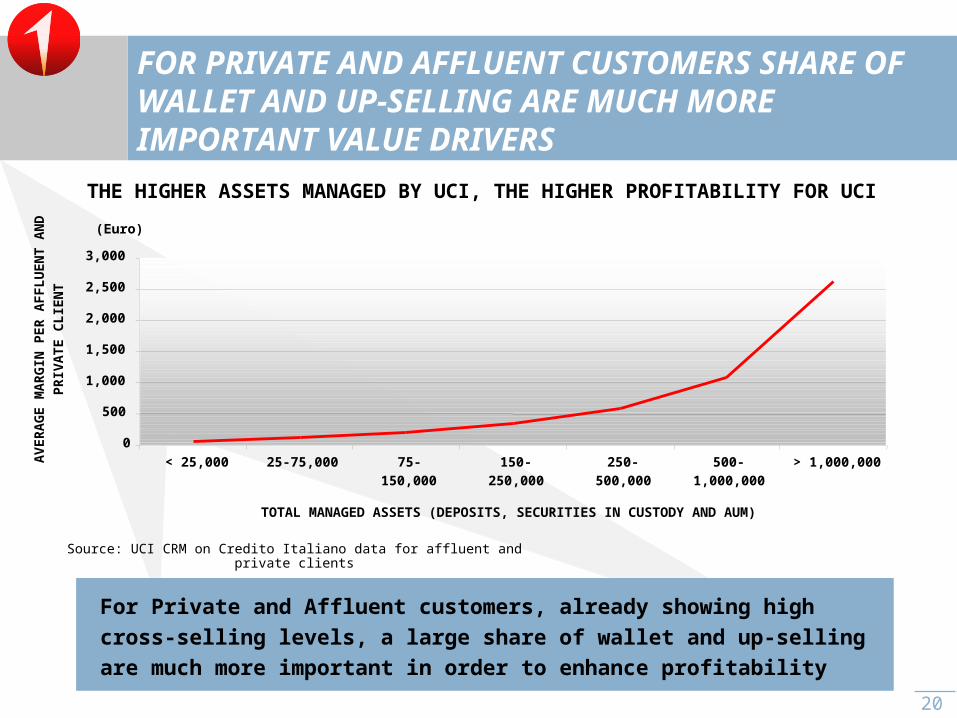

FOR PRIVATE AND AFFLUENT CUSTOMERS SHARE OF WALLET AND UP-SELLING ARE MUCH MORE IMPORTANT VALUE DRIVERS

For Private and Affluent customers, already showing high cross-selling levels, a large share of wallet and up-selling are much more important in order to enhance profitability

TOTAL MANAGED ASSETS (DEPOSITS, SECURITIES IN CUSTODY AND AUM)

AV

ER

AG

E M

AR

GIN

PER

AFFLU

EN

T

AN

D P

RIV

ATE C

LIE

NT

THE HIGHER ASSETS MANAGED BY UCI, THE HIGHER PROFITABILITY FOR UCI

Source: UCI CRM on Credito Italiano data for affluent and private clients

(Euro)

21

Is it easy to make a successful cross-selling ?

Requirements for a successful cross-selling

How to manage a successful cross-selling

Is cross-selling so important to succeed?

Conclusions

Agenda

22

Cross-selling is an important value driver, but it is not the only one and not always the most important

SUMMING UP: WHO WILL BE THE WINNERS OF THE GAME?

IN ORDER TO BE SUCCESSFUL IN THE CURRENT COMPETITIVE SCENARIO ALL PLAYERS SHOULD REMEMBER THAT:

Specialised players with critical mass will have a strategic advantage vs. competitors, thanks to their deep knowledge of the customer base and their increased focus

The success of cross-selling policies should not be measured by the number of products sold to the same client, but by their profitability and their capability to maximise both customers’ satisfaction and relationship period

With its strategic and operational tools UCI has made cross-selling a profitable reality and the creation of 3 segment banks will help to fully exploit the potential of this value driver