Embed Size (px)

Citation preview

Understanding your clients’ tax requirements

Perry Truster, FCA,TEP

Truster Zweig LLP

Chartered Accountants

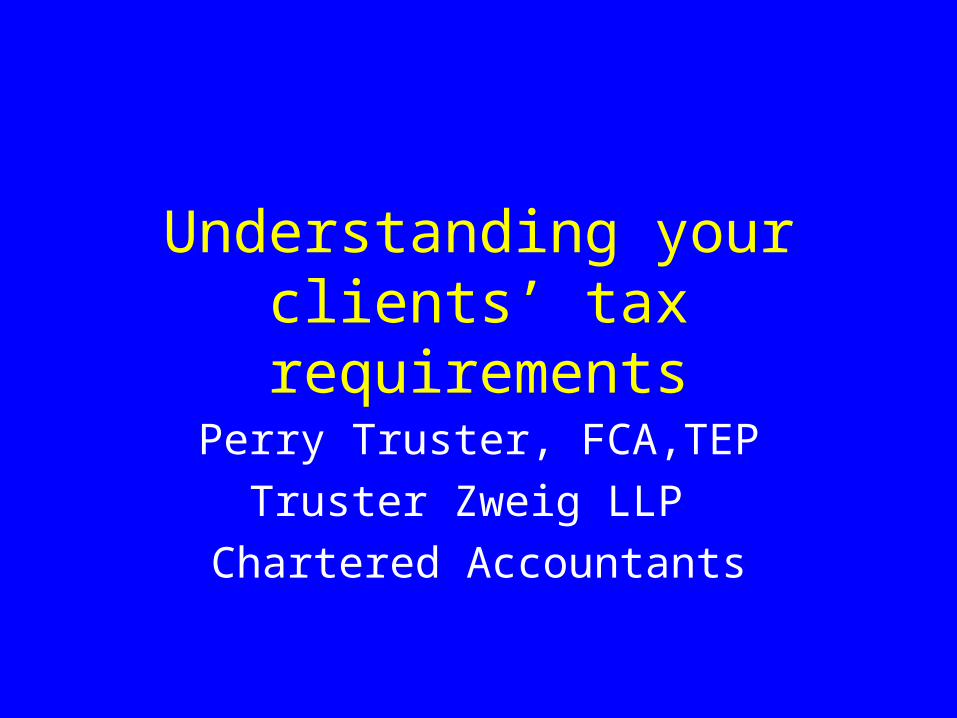

The impact of tax rates

• Selected Ont.2003 personal tax rates

Tax Ordinary Capital

bracket income Dividends gains

$ 0 22.05% 4.48% 11.03%

32,435 31.15 15.86 15.58

64,368 36.98 21.86 18.49

104,648 46.41 31.34 23.21

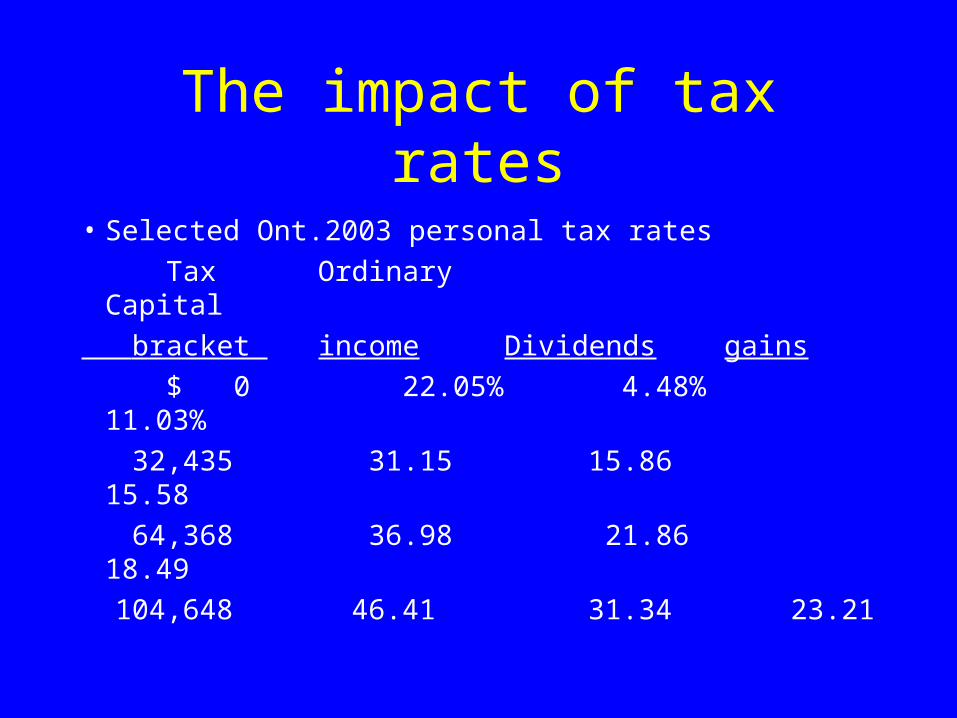

The impact of tax rates

• Obviously the after-tax return on dividends and capital gains is greater than on ordinary income. Therefore lesser amounts of these can be realized while earning the same after-tax returns.

Interest Dividends Gains

Amount 1,000 780 698

Max tax 464 244 162

Net 536 536 536

Public income trusts

• Investments in publicly traded income trusts should yield greater after-tax returns than investments in publicly traded corporations.

• The corporation will incur tax on its income. The shareholder receiving a dividend will incur tax as well. The total of the corporate and personal taxes can exceed 56% to a top bracket Ontarian.

Public income trusts

• This rate substantially exceeds the maximum personal tax rate in Ontario of 46.41% in 2003.

• The trust would be liable for tax at he highest personal rate. However, if the trust distributes all of its income, annually, it will have no income subject to tax. Rather, the unitholders are taxed on the income.

Public income trusts

• If the unitholder is a deferred plan such as a RRSP, the result is more dramatic in that there is no tax at all until funds are withdrawn from the RRSP.

• The trust can distribute cash flow sheltered from tax by, say, capital cost allowance. Such distributions are considered to be returns of capital and reduce the adjusted cost base of the units.

Public income trusts

• Only if the ACB goes negative by virtue of such reduction will the return of capital be taxed immediately.

• Otherwise, the ACB reduction will result in a larger capital gain or reduced capital loss on the eventual disposition of the unit.n

Interest deductibility

• When interest is deductible for tax purposes is widely misunderstood.

• For example, the Income Tax Act has, since 1972, contained a provision (subsection 9(3)) that negates the deduction of interest which is incurred to realize capital gains.

Interest deductibility

• In theory, therefore, interest incurred on funds borrowed to acquire traditionally non-dividend paying stocks could be disallowed.

• However, this has not been the government’s administrative policy.

• Recently, the government has lost a number of high profile tax cases in which the courts have been very liberal in allowing interest deductions and have refused to apply the “REOP” test where there is no personal element present .

Interest deductibility

• The government’s response has been to introduce draft legislation which, if passed in its present form, will commencing in 2005, introduce a REOP test into the law.

• In broad terms, draft section 3.1 will disallow losses unless, in the year, the taxpayer can reasonably be expected to realize a cumulative profit over the holding period, including future years.

Interest deductibility

• The draft legislation also provides that, for this purpose, profits are to be determined without considering capital gains or losses.

• In the context of investments in the market, this could mean that interest will be disallowed where it is incurred to fund the purchase of stocks which do not pay dividends or other investments which do not distribute income.

• The government would use hindsight.

Interest deductibility

• Investors may have to report gains on the disposition of investments as ordinary income in order to preserve their interest deductions if the legislation is passed in its present form.

Corporate owned life insurance

• For purposes of determining the FMV of corporate shares that are deemed to have been disposed of by an individual on his/her death, the FMV of an insurance policy on the life of the individual (or on an individual not at arm’s length with the shareholder) is deemed to be its CSV immediately before the individual’s death.

Corporate owned life insurance

• For purposes of the small business capital gains exemption

- the FMV of corporate owned life insurance is deemed to be equal to its CSV at any time before the death of a shareholder whose life is insured, and

- after death, the FMV of the life insurance proceeds to a corporation is

Corporate owned life insurance

deemed not to exceed the CSV immediately before death if the proceeds are used, within 24 months after death (or upon written request, a longer period, if reasonable) to redeem, acquire or cancel the deceased’s shares.

Corporate owned life insurance

• The portion of life insurance proceeds that increases a corporation’s capital dividend account is the amount in excess of the policy’s ACB.

• Therefore, consideration should be given to having the corporation acquire a policy that returns premiums.

Corporate owned life insurance

• When a deceased’s estate acquires shares upon his/her death, in the absence of the spousal/common-law partner rollover, the estate’s tax value of the shares is deemed to be equal to their FMV immediately before the deceased’s demise.

• If the estate tenders the shares for redemption, the estate is deemed to have realized a dividend equal

Corporate owned life insurance

to the excess of its proceeds over the paid-up capital (generally nominal) of the shares.

• At the same time, the estate is deemed to have incurred a capital loss equal to the paid-up capital of the shares less their high tax value.

• Such capital loss can be utilized on the deceased’s terminal return to offset any

Corporate owned life insurance

capital gains reflected thereon, generally the gain resulting from the deemed disposition of the shares immediately before death.

• However, if the deemed dividend is elected to be a capital dividend, rules introduced on April 26, 1995 are problematic in this regard.

Corporate owned life insurance

• Unless the pre April 26, 1995 rules are grandfathered, the capital loss incurred by the estate on the redemption, will be reduced by 50% of the capital dividend received by the estate if the loss is utilized on the deceased’s terminal return.

Corporate owned life insurance

• This problem can be eliminated if the deceased bequeaths the shares to a spouse or common–law partner.

• The automatic rollover would be availed of on the transfer to the spouse or common-law partner.

• The shareholder should not, prior to death, enter into an agreement requiring that the

Corporate owned life insurance

spouse or common-law partner to sell to the surviving shareholder(s) as this would negate the rollover on death.

• Instead, prior to death, the shareholders would enter into put/call arrangements

-the surviving spouse or common-law partner would have the right to tender the inherited shares for redemption and to

Corporate owned life insurance

receive capital dividend treatment, to the extent possible, on the resultant deemed dividend.

-the surviving shareholder(s) would be given a call option to force the surviving spouse or common-law partner to sell, if the shares were not tendered.

Corporate owned life insurance

• In most cases, the surviving spouse or common-law partner, having inherited the low ACB of the deceased, will not incur a capital loss that would otherwise be reduced by 50%.

Miscellaneous tax planning ideas

• Consider transferring investments to a corporation and drawing a salary from the corporation to create “earned income” for RRSP purposes.

• Consider transferring investments to a corporation to reduce or eliminate the OAS clawback (which commenced at a taxable income level of $57,879 in 2003).

Miscellaneous tax planning ideas

• CPP benefits transferred to a spouse or common-law partner are not subject to the attribution rules.

• Capital gains earned by a minor are not subject to the attribution or kiddie tax rules.

• Income on income is not attributed.

• Business income is not attributed.

Miscellaneous tax planning ideas

• An individual who is older than 69 can contribute to the RRSP of a spouse or common-law partner who is 69 or younger.

• It may be possible to establish a trust which is resident in a lower taxed jurisdiction within Canada, such as Alberta, to earn income which would otherwise be taxable in a more highly taxed jurisdiction.

Miscellaneous tax planning ideas

• Consider having a will create multiple testamentary trusts rather than making direct bequests.