Embed Size (px)

Citation preview

US PRODUCTIVITY GROWTH:THE COMPANY AND SECTOR STORY

CONFIDENTIAL AND PROPRIETARY

Any use of this material without specific permission of McKinsey & Company is strictly prohibited

UNDERSTANDING THE PRODUCTIVITY SLOWDOWN

PETERSON INSTITUTE FOR INTERNATIONAL ECONOMICS

OCTOBER 16, 2015

McKinsey & Company | 111

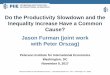

Company

managerial &

operational

factors

Industry

dynamics

Productivity

performance

• Exposure to global

best practice

• Domestic competitive

intensity

• Non-level playing

field/informality

• Product/format mix

• Technology

• Operations (Capacity

utilization, supplier

management,

organization of functions

and tasks)

External

factors

• Macroeconomic

environment

• Product and land

market barriers

• Capital and labor

market barriers

• Regulatory

environment and

enforcement

MGI approach identifies company and industry level

factors behind productivity performance

PERFORMANCE

PRESSURE

McKinsey & Company | 2

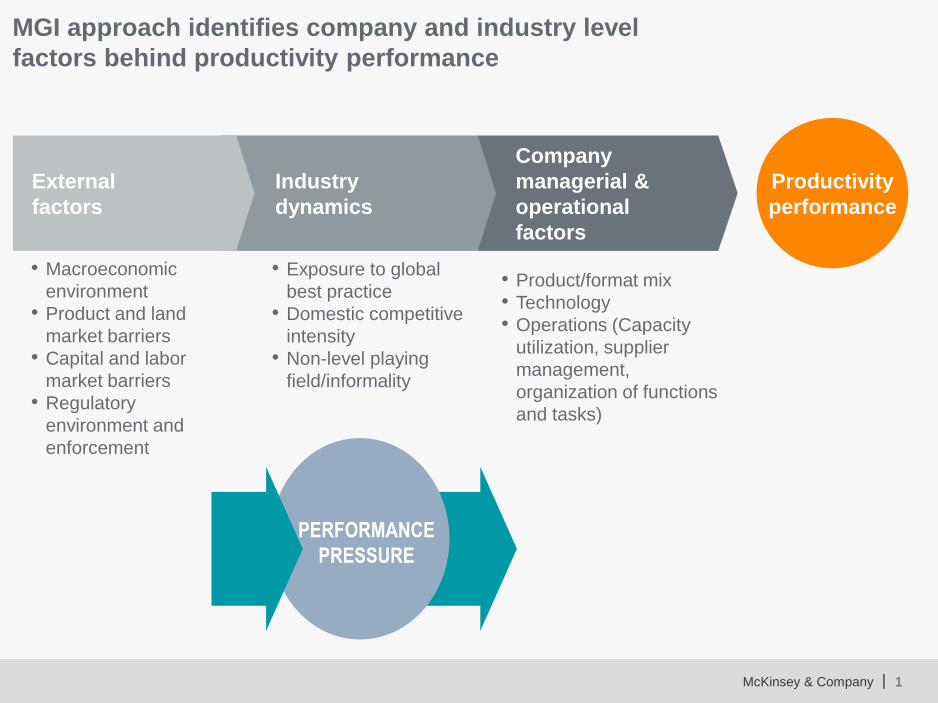

Wealth of accumulated knowledge over 25 years

11

11

1

1

2

22

22

3

3

3

34

66

6

7

8

810

1113

14

15

18

Retail banking

Retail

Automotive

Furniture

Oil

Beer

Machine equipment

Agriculture

Apparel

Road freight

Hotels

Cement

Wheat milling

Semiconductors

Steel

Software

Meat processing

Dairy processing

Telecom

Electric utilities

Housing construction

Health care

Electronics

Confectionery

Airlines

Soap and detergent

Public transportation

Wholesale

SOURCE: McKinsey Global Institute

Number of MGI has studied a sector Number of sectors studied by country

2

3

4

4

5

6

7

7

7

8

8

9

9

9

10

10

11

12

12

28

Sweden

France

United Kingdom

Mexico

Thailand

China

Vietnam

The Netherlands

Poland

Indonesia

Myanmar

Australia

Korea

Japan

Brazil

Turkey

Russia

India

Germany

United States

Developed countries

McKinsey & Company | 3

US productivity growth: the company and sector story

Productivity growth

is an evolving

sector story

There are large

opportunities across

all industries to

raise productivity

growth

What can catalyze

future productivity

growth spurts?

McKinsey & Company |

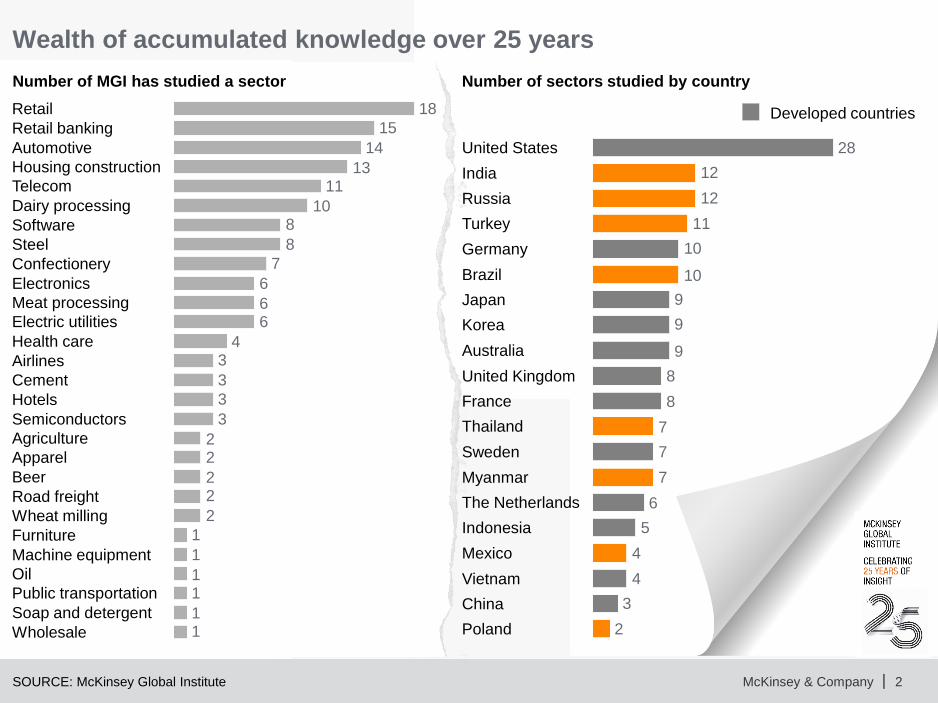

In the 1990s, productivity growth was driven by a virtuous

cycle of jobs growth and increasing value added

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

-5 -4 -3 -2 -1 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23

Professional services

Manufacturing

Agriculture

and mining

Wholesale

Utilities

Management

Government

Construction

Accommodation/

food services

Retail

Value-added growth

Employment growth

Real estate

Information

Administration

Finance/insurance

Other services

Transport

Health care

Education

Arts/recreation

Negative

Positive

Compound annual growth rate, 1990–2000, %

1 Productivity contribution calculated using Moody’s Economy.com data.

.

Size represents

productivity

contribution

SOURCE: US Bureau of Economic Analysis; Moody’s Economy.com; McKinsey Global Institute Sunrise Productivity

Model

McKinsey & Company |

In the 1990s, productivity growth was driven by a virtuous

cycle of jobs growth and increasing value added

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

-5 -4 -3 -2 -1 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23

Utilities

Transport

Education

Employment growth

Management

Professional servicesReal estate

Value-added growth

Government

Manufacturing

Construction

Finance/

insurance

Arts/recreation

Other services

RetailWholesale

Information

Health care

Agriculture

and mining

Administration

Accommodation/

food services

Negative

Positive

Compound annual growth rate, 1990–2000, %

1 Productivity contribution calculated using Moody’s Economy.com data.

Size represents

productivity

contribution

SOURCE: US Bureau of Economic Analysis; Moody’s Economy.com; McKinsey Global Institute Sunrise Productivity

Model

McKinsey & Company | 6

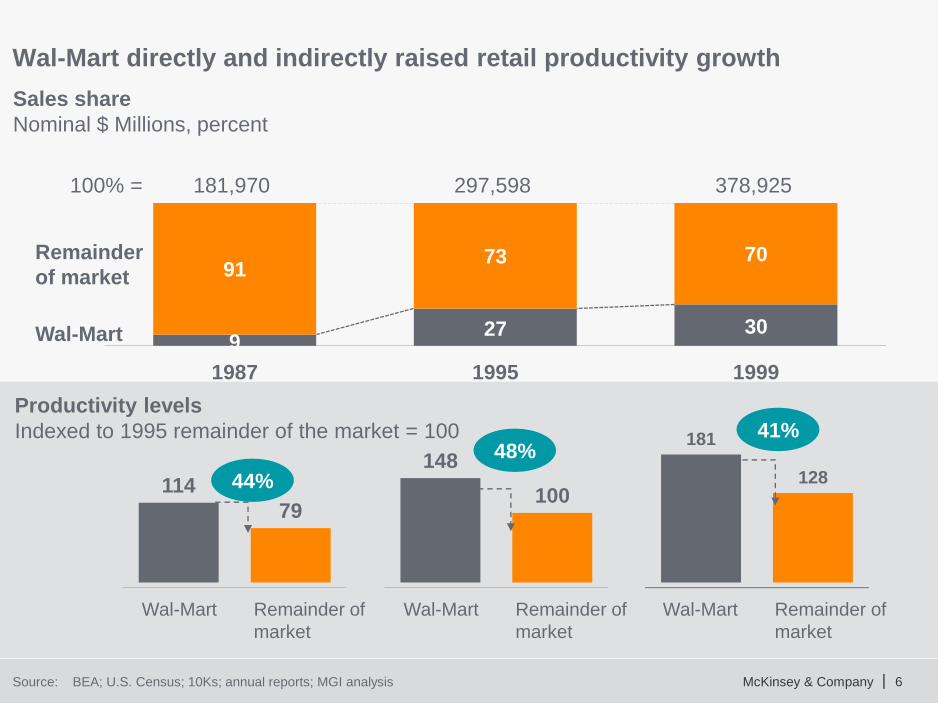

Wal-Mart directly and indirectly raised retail productivity growth

Source: BEA; U.S. Census; 10Ks; annual reports; MGI analysis

927 30

9173 70

1987 1995 1999

Wal-Mart

Remainder

of market

100% = 181,970 297,598 378,925

114

79

148

100

181

128

Wal-Mart Remainder of

market

Wal-Mart Remainder of

market

Wal-Mart Remainder of

market

Sales share

Nominal $ Millions, percent

Productivity levels

Indexed to 1995 remainder of the market = 100

44%

48%41%

McKinsey & Company |

Between 2000-2008, large productivity improvements came from

efficiency gains that often were accompanied by job losses

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

-5 -4 -3 -2 -1 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23

Value-added growth

Health care

Construction

Accommodation/

food services

Government

Real estate

Manufacturing

Finance/insurance

Other services

Information

Education

Arts/recreation

Agriculture

and mining

Management

Computers/

electronics

Professional services

AdministrationUtilities

Retail

Employment growth

Wholesale

Transport

Positive

NegativeCompound annual growth rate, 2000–08, % Size represents

productivity

contribution

SOURCE: US Bureau of Economic Analysis; Moody’s Economy.com; McKinsey Global Institute Sunrise

Productivity Model

1 Productivity contribution calculated using Moody’s Economy.com data.

McKinsey & Company | 8

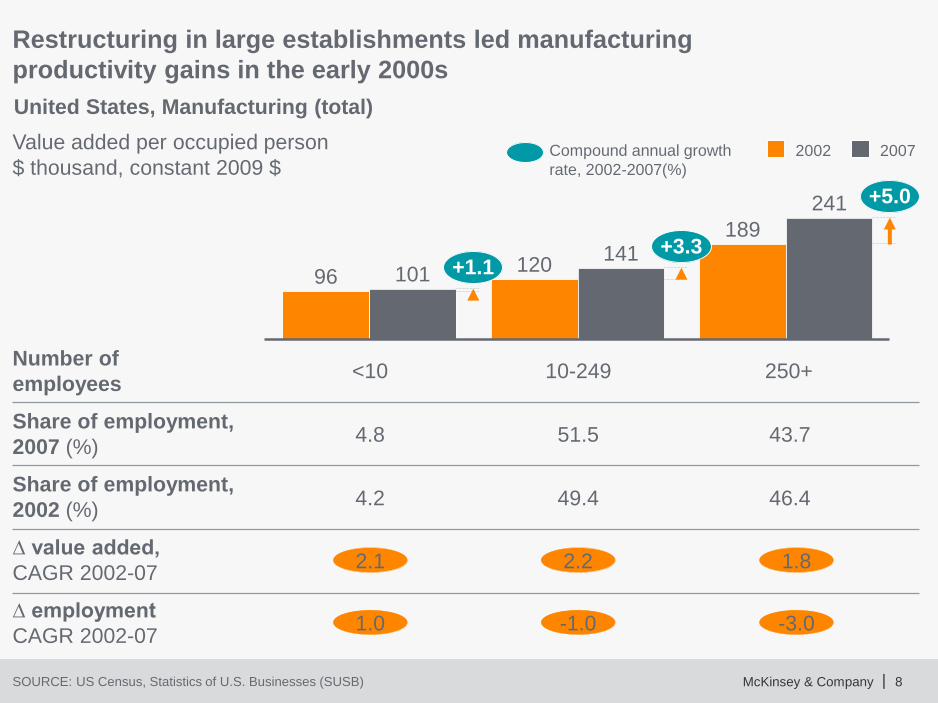

United States, Manufacturing (total)

Restructuring in large establishments led manufacturing

productivity gains in the early 2000s

+5.0

+3.3120+1.1

241

14110196

189

2002 2007

SOURCE: US Census, Statistics of U.S. Businesses (SUSB)

Value added per occupied person

$ thousand, constant 2009 $Compound annual growth

rate, 2002-2007(%)

Number of

employees<10 10-249 250+

Share of employment,

2007 (%)4.8 51.5 43.7

Share of employment,

2002 (%)4.2 49.4 46.4

∆ value added,

CAGR 2002-072.1 2.2 1.8

∆ employment

CAGR 2002-071.0 -1.0 -3.0

McKinsey & Company |

Most sectors contributed positively to productivity after the recession,

while employment contracted in most industries

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

-5 -4 -3 -2 -1 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23

Administration

Accommodation/

food services

Manufacturing

Professional services

Real estate

Transport

Retail

Information

Health care

Government

Finance/insurance

Education

Construction

Mining

Computers/electronics

Agriculture and forestry

Other services

Value-added growth

Employment growth

Wholesale

Negative

PositiveSize represents

productivity

contribution

Compound annual growth rate, 2008-2013, %

SOURCE: US Bureau of Economic Analysis; Moody’s Economy.com; McKinsey Global Institute

Sunrise Productivity Model

1 Productivity contribution calculated using Moody’s Economy.com data.

McKinsey & Company | 10

US productivity growth: the company and sector story

Productivity growth

is an evolving

sector story

There are large

opportunities across

all industries to

raise productivity

growth

What can catalyze

future productivity

growth spurts?

McKinsey & Company | 11

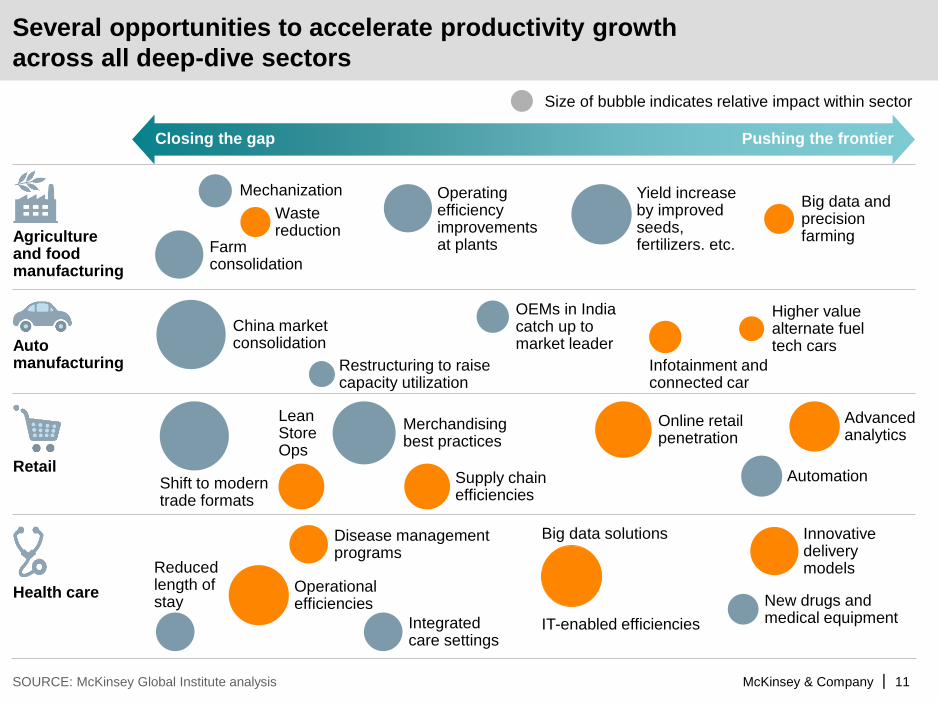

Several opportunities to accelerate productivity growth

across all deep-dive sectors

SOURCE: McKinsey Global Institute analysis

Pushing the frontierClosing the gap

Size of bubble indicates relative impact within sector

Mechanization Yield increase by improved seeds, fertilizers. etc.

Waste reduction

Farm consolidation

Big data and precision farming

Operating efficiency improvements at plants

Agriculture and food manufacturing

China market consolidation

Restructuring to raise capacity utilization

OEMs in India catch up to market leader

Infotainment and connected car

Higher value alternate fuel tech carsAuto

manufacturing

Shift to moderntrade formats

Lean Store Ops

Merchandisingbest practices

Supply chain efficiencies

Advanced analytics

Automation

Online retail penetration

Retail

Innovative delivery models

Operational efficiencies

Reduced length of stay

Disease management programs

IT-enabled efficiencies

Big data solutions

Integrated care settings

New drugs and medical equipment

Health care

McKinsey & Company | 12

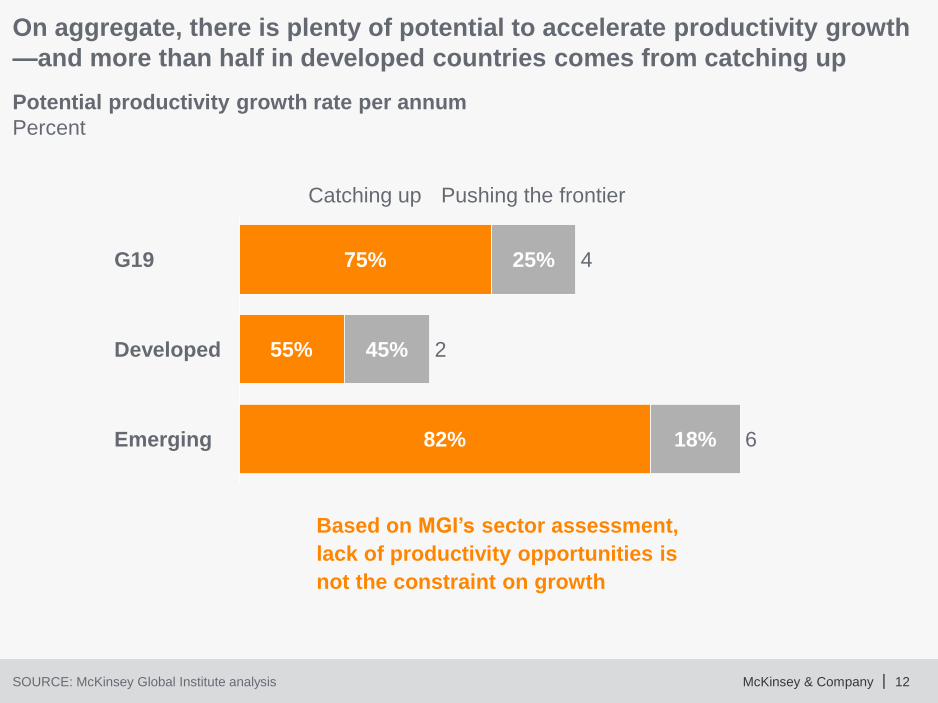

Pushing the frontier

6

Catching up

Emerging

475% 25%G19

82%

Developed

18%

45% 255%

On aggregate, there is plenty of potential to accelerate productivity growth

—and more than half in developed countries comes from catching up

SOURCE: McKinsey Global Institute analysis

Based on MGI’s sector assessment,

lack of productivity opportunities is

not the constraint on growth

Potential productivity growth rate per annum

Percent

McKinsey & Company | 13

US productivity growth: the company and sector story

Productivity growth

is an evolving

sector story

There are large

opportunities across

all industries to

raise productivity

growth

What can catalyze

future productivity

growth spurts?

McKinsey & Company | 14

Potential catalysts for productivity growth spurts

▪ Regulatory changes

▪ Technology-enabled

productivity growth

▪ Increased competition

▪ Other?

McKinsey & Company |

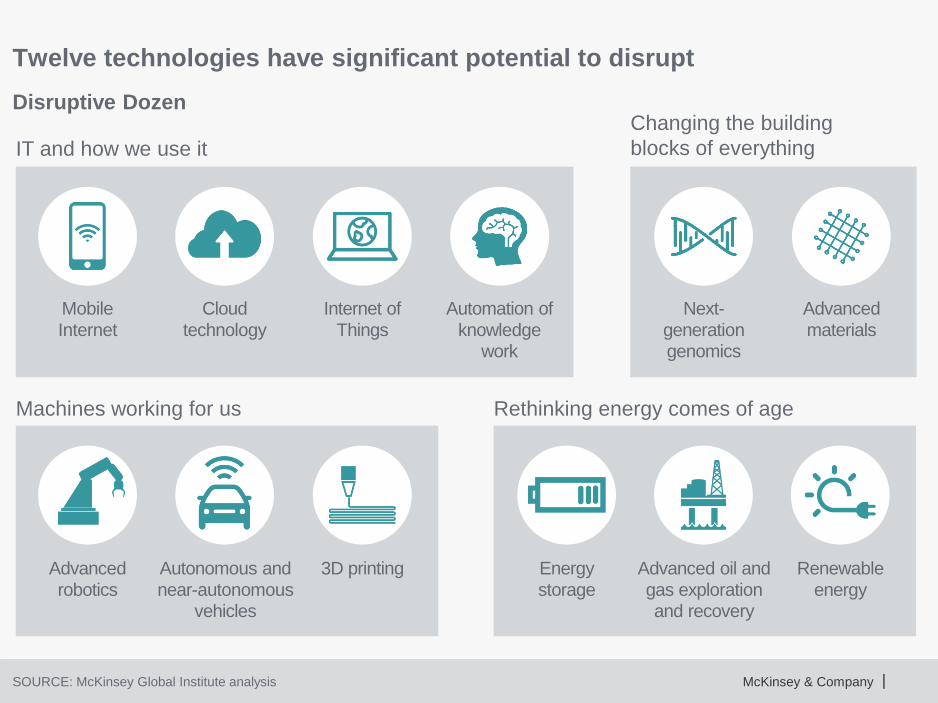

Twelve technologies have significant potential to disrupt

SOURCE: McKinsey Global Institute analysis

Disruptive Dozen

IT and how we use it

Mobile

Internet

Cloud

technology

Internet of

Things

Automation of

knowledge work

Changing the building

blocks of everything

Next-

generation genomics

Advanced

materials

Machines working for us

Autonomous and

near-autonomous vehicles

Advanced

robotics

3D printing

Rethinking energy comes of age

Advanced oil and

gas exploration and recovery

Energy

storage

Renewable

energy

@JaanaRemes

@McKinsey_MGI

DOWNLOAD MGI RESEARCH AT

WWW.MCKINSEY.COM./MGI