Embed Size (px)

Citation preview

Hanne-M

ari Hälinen

A-1:2015

Hanne-Mari Hälinen

UNDERSTANDING THE CONCEPT OF LOGISTICS COST IN MANUFACTURING

Turun kauppakorkeakoulu

Turku School of Economics

ISBN 978-952-249-382-8

Turun kauppakorkeakoulu

Turku School of Economics

Hanne-Mari Hälinen B5 Kansi s10.5 Inver260 February 6, 2015 9:18 AM

UNDERSTANDING THE CONCEPT O

F LOGISTICS COST IN MANUFACTURING

Hanne-Mari Hälinen

Sarja/Series A-1:2015

UNDERSTANDING THE CONCEPT OF LOGISTICS COST IN MANUFACTURING

Turun kauppakorkeakoulu

Turku School of Economics

Custos: Professor Lauri Ojala

Turku School of Economics

Supervisors: Professor Lauri Ojala

Turku School of Economics

Professor Juuso Töyli

Turku School of Economics

Pre-examiners: Professor Karen Spens

Hanken School of Economics

Professor Helena Forslund

Linnaeus University

Opponent: Professor Helena Forslund

Linnaeus University

Copyright Hanne-Mari Hälinen & Turku School of Economics

The originality of this thesis has been checked in accordance with the University of Turku

quality assurance system using the Turnitin OriginalityCheck service.

ISBN 978-952-249-382-8 (print) 978-952-249-383-5 (PDF)

ISSN 0357-4652 (print) 1459-4870 (PDF)

Publications of Turku School of Economics, Series A

Suomen yliopistopaino Oy – Juvenes Print, Turku 2015

ABSTRACT

This thesis aims at providing a better understanding of the concept of logisticscost in manufacturing. One of the reasons for choosing this topic was therealization that very little research has been published on this subject. This issomewhat surprising given the significance of logistics and supply chainmanagement (SCM) and its improvement for the profitability especially inmanufacturing.

The thesis has its roots in a broader research effort within the Operations &Supply Chain Management subject at the Turku School of Economics (TSE)on the relationships between logistics costs and performance. During the pastten years, the O&SCM team, of which the author has been a member, hasconducted five comprehensive logistics surveys in Finland, which haveproduced the largest national database on logistics – including logistics costs –in the World. This rich database has provided empirical evidence for threepublished PhD thesis at TSE (Rantasila 2013 and Solakivi 2014 at O&SM;and Heinonen 2013 at Dept. of Economics), and to well over 10 refereedjournal articles.

Due to the holistic nature of logistics and supply chain management (SCM),data of its cost are typically fragmented across organizations. Improvedinformation on the costs of logistics and SCM activities may assist themanagers to make better decisions. For example, a realistic view on inventoryholding cost may prevent over-optimistic offshoring decisions, not to mentionbetter information of the costs involved in sourcing, or the “black box” ofadministrative costs of logistics.

Literature related to logistics/SCM costing and cost controlling hastraditionally concentrated on the suitability and use of individual managementaccounting techniques such as activity-based costing, target costing, total costof ownership or balanced scorecard, or discusses performance measurement ingeneral, with strong emphasis on non-financial performance measurement. Inaddition, there are no commonly accepted international or national definitionson the concept of logistics cost(s). Thus, the meaning of the concepts used canvary significantly from one firm to another.

Management accounting literature, on the other hand, publishes research ofthe organization of costing in companies and the factors that affect the costand control systems in organizations, but the context of logistics and supplychain management is seldom represented. The level of analysis in the

empirical research is often at the company or business unit level, but that maybe too broad a level of aggregation to directly describe the cost controlling oflogistics and supply chain management. Similar mechanisms may apply toorganizing of costing in SCM as well, but the empirical evidence is virtuallynon-existent.

Based on the above, this thesis comprises two main research questions:RQ1: What are the specific features of the concept of logistics cost ina management accounting context in a manufacturing setting?; andRQ2: What factors contribute to how logistics cost management isorganized in firms?

The thesis comprises an introductory part, and a collection of one publishedjournal article and four conference papers that have been presented inacademic conferences in the fields of supply chain management and manage-ment accounting. Paper I addresses the effect of a specific contingent factor,namely geographic dispersion of the supply chain, to the intra-firm supplychain performance. The conceptual paper II addresses the RQ1. Conceptualpapers III and V deal with the both research questions. Paper IV that providessome empirical survey evidence on how logistics cost information is availablein Finnish companies is related to the RQ2.

The thesis provides a model that answers the second research question.Based on the model, multiple hypotheses can be presented for testing in futureresearch.

The published papers together with the introductory part provide a profoundand novel discussion that links the extant research literature in SCM/logisticswith that in the field of management accounting. This discussion is alsosupported by the empirical evidence provided in Papers I and IV.

The main theoretical contribution of the thesis lies in the treatment anddeeper understanding of the cost-related terminology and concepts inSCM/logistics vis-à-vis management accounting literature. The findings havealso a managerial relevance especially in the context of manufacturing firms.

TIIVISTELMÄ

Tämän tutkimuksen tarkoituksena on tuottaa uutta tietoa logistiikkakustan-nusten käsitteen parempaan ymmärtämiseen. Tarkastelun kohteena ovat erityi-sesti valmistavat yritykset. Aiheen valintaan ohjasi tutkimuksen alkuvaiheenhuomio siitä, että aihetta on tutkimuskirjallisuudessa käsitelty varsin vähän.Tämä havainto oli yllättävä, sillä logistiikan ja laajemmin toimitusketjujenjohtamisen merkitys yritysten kannattavuuteen on varsin iso.

Työ liittyy myös Turun kauppakorkeakoulun toimitusketjujen johtamisenoppiaineen laajempaan tutkimuskokonaisuuteen, jossa tarkastellaan logistiik-kakustannusten ja yritysten suorituskyvyn välisiä yhteyksiä. Kuluneen kym-menen vuoden aikana kirjoittaja on ollut osa aineen tutkijaryhmää, joka ontoteuttanut Suomessa viisi isoa logistiikkaselvitystä, joiden tietokanta muodos-taa tällä hetkellä laajimman kansallisen kyselyaineiston maailmassa. Aineistonpohjalta on TuKKK:ssa julkaistu mm. kolme väitöskirjaa (Rantasila 2013 jaSolakivi 2014 sekä Heinonen 2013 TuKKK:n taloustieteessä) sekä ylikymmen referoitua journal-artikkelia.

Logistiikkaan ja toimitusketjun hallintaan ja niiden kustannuksiin liittyvätieto on tyypillisesti hajautunut hyvin moniin paikkoihin yrityksissä, eikäkokonaiskuvan saaminen näistä ole usein kovin helppoa. Parempi informaatioja tietämys näistä auttaisi kuitenkin tekemään parempia liikkeenjohdollisiapäätöksiä mm. varaston hallinnan, sijoittumisen, hankintatoimen sekä näihintoimiin liittyvien yleishallinnon kulujen osalta.

Logistiikan ja toimitusketjujen johtamisen tutkimuskirjallisuus käsitteleekustannuksia ja kustannusten seurantaa useimmiten tiettyjen tuotantotaloudenja/tai liikkeenjohdon laskentatoimen menetelmien avulla. Näitä ovat esimer-kiksi toimintolaskento (activity-based costing), elinkaarilaskennan sovellukset(esim. total cost of ownership ja target costing) ja tasapainotettu mittaristo(balanced scorecard). Niissä mittaaminen painottuu usein ei-taloudelliseensuorituskykyyn. Logistiikkakustannusten käsitteelle ei myöskään ole olemassamitään yleisesti hyväksyttyä sisältöä. Tämän vuoksi käsitteen merkitys voivaihdella merkittävästi yrityksestä toiseen.

Liikkeenjohdon laskentatoimen tutkimuskirjallisuus painottuu puolestaanusein kustannuslaskennan järjestelyihin ja toteutukseen organisaatioissa sekäniihin vaikuttavien tekijöiden tarkasteluun. Kytkennät logistiikan ja toimitus-ketjujen johtamisen kontekstiin ja käsitteistöön ovat vähäiset. Ongelmiatarkastellaan tyypillisesti yrityksen tai liiketoimintayksikön tasolla, mikä on

usein hieman liian karkea taso logistiikkakustannuksia ajatellen. Vaikka liik-keenjohdon laskentatoimen ja logistiikan kustannustarkastelussa olisi paljon-kin yhteistä, niitä käsittelevää tutkimuskirjallisuutta ei juuri ole.

Tämä tutkimus pyrkii vastaamaan kahteen tutkimuskysymykseen:RQ1: Mitkä ovat logistiikkakustannusten käsitteen erityispiirteet liik-keenjohdon laskentatoimen kautta tarkasteltuna erityisesti valmis-tavassa yrityksessä?RQ2: Mitkä tekijät vaikuttavat logistiikkakustannusten hallinnanjärjestelyihin (valmistavissa) yrityksissä?

Tutkimus koostuu yhdestä julkaistusta vertaisarvioidusta artikkelista, nel-jästä vertaisarvioidusta kansainvälisestä konferenssijulkaisusta sekä johdanto-osasta. Paperi I tarkastelee toimitusketjujen maantieteellisen jakautumisenvaikutusta yritysten toimitusketjun suorituskykyyn. Paperi II on käsitteellinentarkastelu, joka vastaa osaltaan ensimmäiseen tutkimuskysymykseen (RQ1).Paperien III ja V käsitteellinen tarkastelu kohdistuu molempiin tutkimuskysy-myksiin. Paperin IV empiirinen tarkastelu suomalaisyritysten logistiikkakus-tannusten informaatiosta liittyy tutkimuskysymykseen 2. (RQ2); työssä kehi-tetty käsitteellinen malli liittyy myös tutkimuskysymykseen 2. Mallin pohjaltavoidaan testata useita aiheeseen liittyviä hypoteeseja.

Tämä tutkimus on perusteellinen ja uudenlainen kokonaiskatsaus liikkeen-johdon laskentatoimen ja logistiikan kustannustarkasteluista, joka pohjautuuosin sekä empiiriseen että käsitteelliseen aineistoon. Tämä tarkastelu on myöstyön keskeinen teoreettinen kontribuutio. Tulosten liikkeenjohdollinen rele-vanssi kohdistuu erityisesti valmistaviin yrityksiin.

TABLE OF CONTENTS

ABSTRACTTIIVISTELMÄ1 INTRODUCTION .................................................................................... 11

1.1 The relevance of logistics costing and cost information .................... 111.2 Research questions and structure of the thesis .................................. 121.3 Research process .............................................................................. 141.4 Defining the scope of logistics .......................................................... 211.5 Perception of logistics and supply chain management ...................... 23

2 THE MANAGERIAL AND ORGANIZATIONAL CONTEXT OFLOGISTICS COST ................................................................................... 292.1 Role of management accounting ....................................................... 292.2 The firm size .................................................................................... 312.3 Products and production process ....................................................... 322.4 ERP and other information systems .................................................. 38

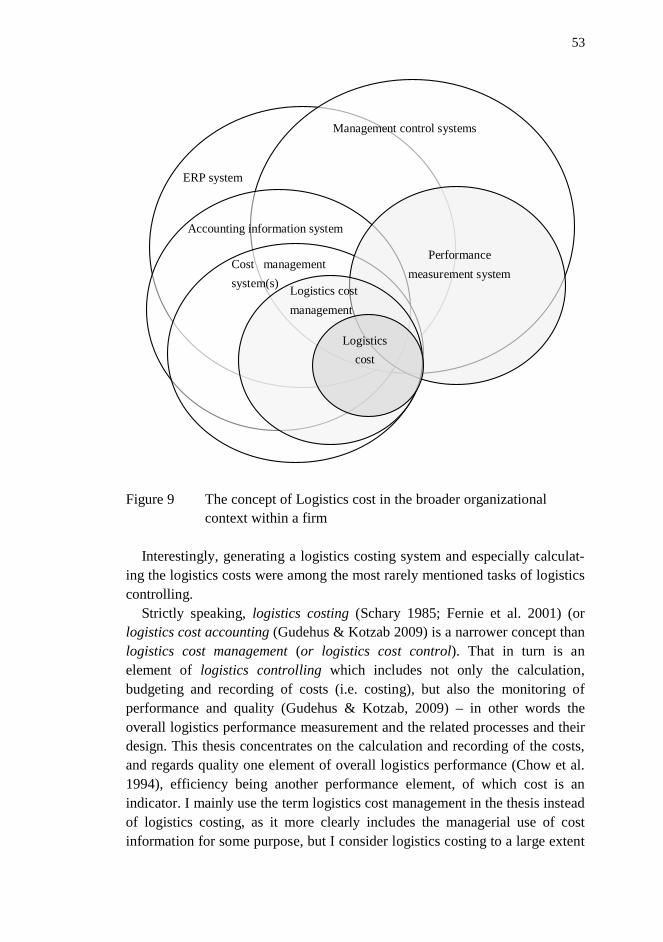

3 PERFORMANCE MEASUREMENT ...................................................... 414 LOGISTICS AND SUPPLY CHAIN RELATED COST TERMS ............ 51

4.1 Logistics controlling, logistics costing, and logistics cost controlor management ................................................................................. 51

4.2 Total cost of logistics and supply chain cost ..................................... 544.3 Typical components of logistics/SCM costs by activities and

cost types .......................................................................................... 574.3.1 Transportation cost ................................................................ 574.3.2 Inventory-related costs .......................................................... 584.3.3 Administrative cost................................................................ 604.3.4 Purchasing cost ...................................................................... 614.3.5 Logistics costs by cost types .................................................. 63

4.4 Costs of complexity .......................................................................... 645 DIVERGENT LOGISTICS COST INFORMATION NEEDS AND

USES WITHIN THE FIRM ...................................................................... 675.1 Accounting choices affecting logistics costing .................................. 67

5.1.1 Proportion of direct costs to indirect costs ............................. 675.1.2 Allocation of indirect/common costs ..................................... 685.1.3 Variable or absorption costing method in inventory

valuation................................................................................ 70

5.2 Cost information needs at different managerial levels and positions . 725.3 Need for multiple aggregation levels of cost data ............................. 745.4 On-going cost controlling versus special cost analyses ..................... 755.5 Characteristics of intra-company logistics/SCM control systems ...... 77

6 SUMMARY OF RESULTS IN APPENDED PAPERS ............................ 836.1 Paper I: Effects of geographic dispersion on intra-firm supply

chain performance ........................................................................... 836.2 Paper II: An approach for estimating total logistics costs at a

company level .................................................................................. 856.3 Paper III: A framework for evaluating the sophistication of internal

supply chain cost measurement in manufacturing companies ........... 856.4 Paper IV: The availability of logistics cost: A comparison between

Finnish manufacturing, trade and logistics service providers ............ 886.5 Paper V: Multiple perspectives on logistics costs: factors related to

information provision ....................................................................... 897 CONCLUSION ON FACTORS CONTRIBUTING TO INTRA-

COMPANY SUPPLY CHAIN COST ...................................................... 91REFERENCES ................................................................................................. 97

Paper I Lorentz, Harri – Töyli, Juuso – Solakivi, Tomi – Hälinen,Hanne-Mari – Ojala, Lauri (2012), Effects of geographicdispersion on intra-firm supply chain performance, SupplyChain Management: An International Journal, Vol. 17, No. 6,611–626 ..................................................................................... 107

Paper II Hälinen, Hanne-Mari (2010) An approach for estimating totallogistics costs at a company level, 10th ManufacturingAccounting Research (MAR) Conference Proceedings ............... 127

Paper III Hälinen, Hanne-Mari (2012) A framework for evaluating thesophistication of internal supply chain cost measurement inmanufacturing companies, 11th Manufacturing AccountingResearch (MAR) Conference Proceedings ................................. 141

Paper IV Hälinen, Hanne-Mari – Solakivi, Tomi – Ojala, Lauri (2013)The availability of logistics cost: A comparison betweenFinnish manufacturing, trade and logistics service providers,NOFOMA 2013 Conference Proceedings .................................. 169

Paper V Hälinen, Hanne-Mari (2013) Multiple perspectives onlogistics costs: factors related to information provision,Proceedings of the 7th Conference of PerformanceMeasurement and Management Control .................................... 193

LIST OF FIGURES

Figure 1 Focal areas of interest of the thesis indicated as shaded fields ...... 13Figure 2 The research process and the papers in chronological order .......... 15Figure 3 SCM and management accounting research in relation to

Burrell & Morgan (1979) paradigms for analyzing socialtheory ........................................................................................... 17

Figure 4 Change of management focus from efficient product flow todifferent customer group service requirements (Schary 1985) ...... 34

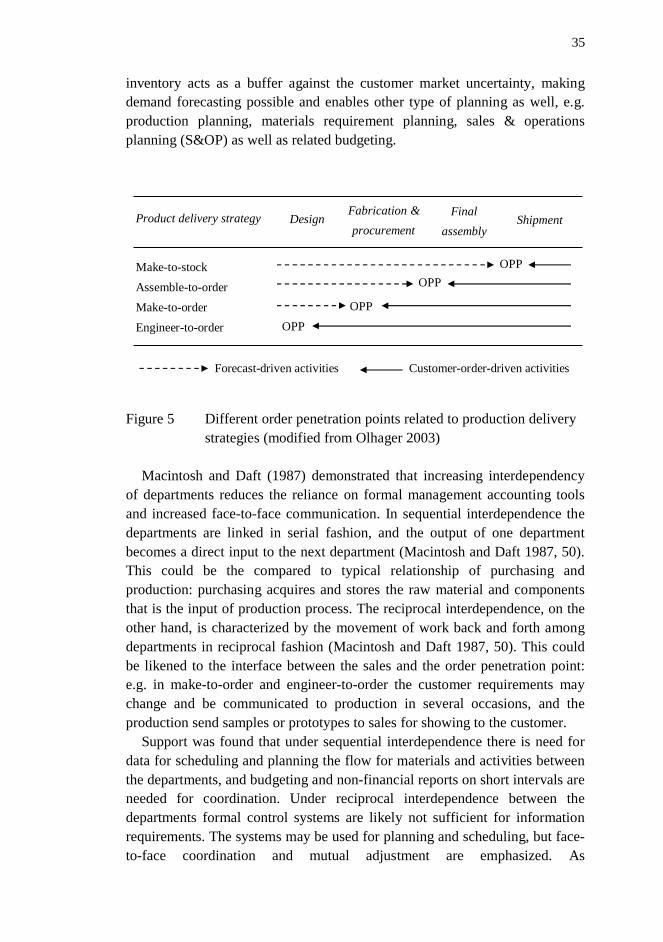

Figure 5 Different order penetration points related to productiondelivery strategies (modified from Olhager 2003) ........................ 35

Figure 6 Service classification and the traceability of cost (Brignall1997) ............................................................................................ 37

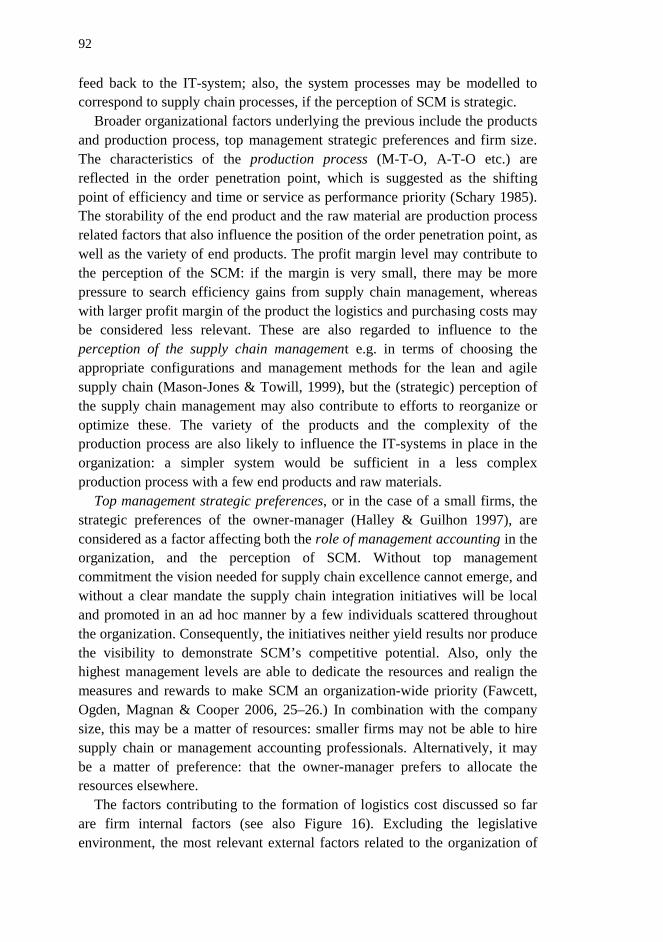

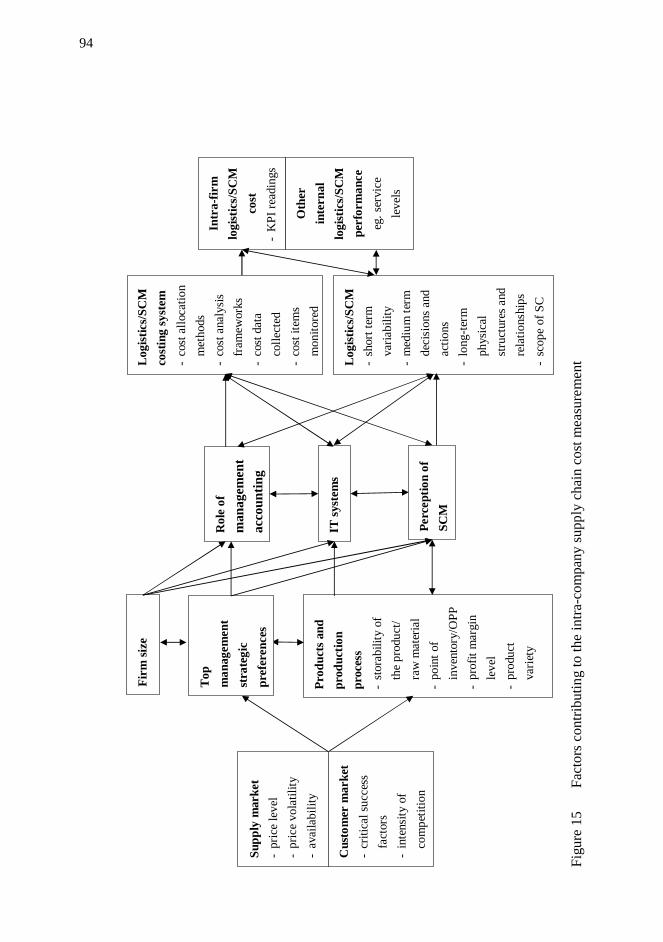

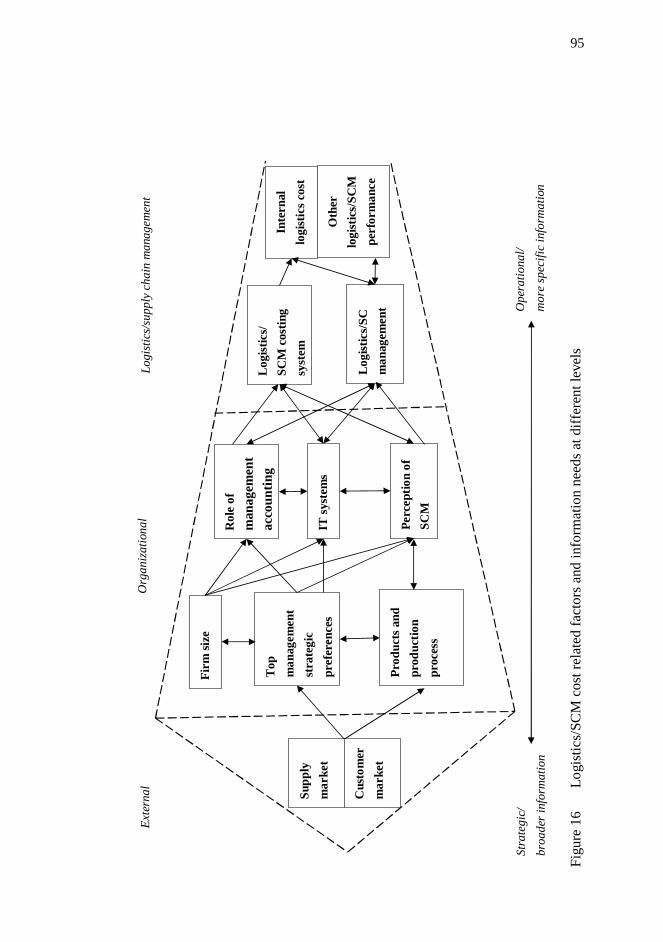

Figure 7 Logistics control as a cybernetic control system (Schary 1985) .... 45Figure 8 Logistics cost as a part of logistics performance ........................... 48Figure 9 The concept of Logistics cost in the broader organizational

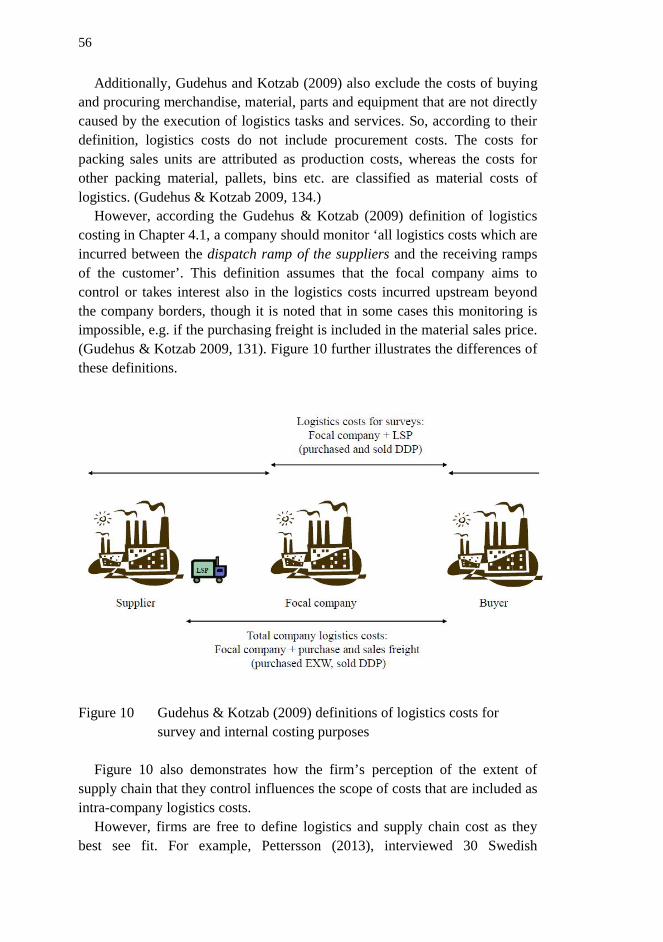

context within a firm .................................................................... 53Figure 10 Gudehus & Kotzab (2009) definitions of logistics costs for

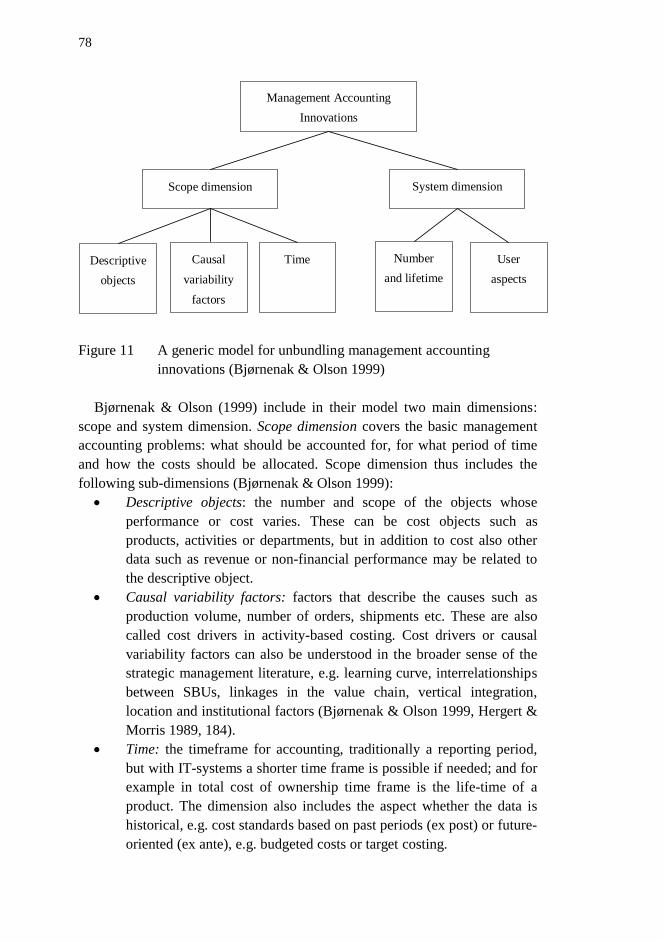

survey and internal costing purposes ............................................ 56Figure 11 A generic model for unbundling management accounting

innovations (Bjørnenak & Olson 1999) ........................................ 78Figure 12 A model for analyzing logistics/supply chain management

control systems (modified from Bjørnenak & Olson 1999) ........... 81Figure 13 The investigative model of the article (excerpt from Lorentz

et al. 2012) ................................................................................... 83Figure 14 Factors related to the construction of firm or business unit

internal logistics cost in manufacturing companies ....................... 86Figure 15 Factors contributing to the intra-company supply chain cost

measurement ................................................................................ 94Figure 16 Logistics/SCM cost related factors and information needs at

different levels ............................................................................. 95

LIST OF TABLES

Table 1 Research questions of the thesis and the papers addressing it ....... 14Table 2 Models of evolutionary development of supply chain

management and performance measurement ................................ 27

11

1 INTRODUCTION

1.1 The relevance of logistics costing and cost information

Due to the holistic nature of logistics and supply chain management (SCM)the data of its cost are typically fragmented to various places in theorganization. This may lead to underestimating the significance of supplychain management and its improvement for the profitability of theorganizations. In the mid-1980’s there were concerns that in seniormanagement distribution is considered solely as a necessary cost and service,and its profit enhancement potential is ignored. Distribution managers wereseen generally unaware of the value of financial information for improvingdistribution performance, and also financial and accounting resources incompanies were stated not to have kept pace with the developments indistribution. (Tyndall & Busher 1985.) Even in 2013 similar issues prevail:The Finnish Association of Purchasing and Logistics Professionals (LOGY)expressed concerns that SCM professionals are lacking in the ability todemonstrate how supply chain management affects the bottom line.Consequently perhaps, the top management tends to perceive supply chainmanagement as operational activities with little relevance to organizationalstrategy. (Kekäläinen 2013.)

Improved information on the costs of logistics and supply chainmanagement activities may assist the managers to make better decisions. Forexample, more realistic inventory holding cost than an industry average orother estimate may prevent over-optimistic offshoring decisions (Timme 2003,37), not to mention information of all the costs involved in sourcing (Platts &Song, 2010; Weber et al. 2010). Opening up the “black box” of theadministrative costs of logistics could contribute to the esteem of supply chainmanagement within the organization: although the labor and wage costs of thelogistics costs cover the largest part of administrative costs, a more detaileditemization of to which all activities those resources are spend might evokeinterest in the re-design of activities in order to streamline the processes byremoving redundancies and unnecessary tasks or replacing the tasks in thesupply chain.

Furthermore, deficient information of the logistics and supply chainmanagement costs hinders the negotiation and cooperation between supplychain partners. The members may have different understanding of the

12

definition or the content of some cost categories and may be unable todemonstrate the cost of performing certain activities or how the partner’sbehavior affects the whole supply chain’s costs. (Norek & Pohlen 2001;Dekker & van Goor 2000).

Supply chain management literature related to logistics costing and costcontrolling since 1980’s has concentrated predominantly on suitability and useof individual management accounting techniques such as activity-basedcosting, target costing, total cost of ownership or balanced scorecard in asupply chain management context, or discusses performance measurement ingeneral, with strong emphasis on non-financial performance measurement.Management accounting literature, on the other hand, publishes research of theorganization of costing in companies and the factors that affect the cost andcontrol systems in organizations, but the context of logistics and supply chainmanagement is seldom represented. The level of analysis in the empiricalresearch is often at the company or business unit level, but that may be toobroad a level of aggregation to directly describe the cost controlling oflogistics and supply chain management. One can logically deduce that similarmechanisms may apply to organizing of costing in supply chain managementas well, but the empirical evidence is virtually inexistent.

1.2 Research questions and structure of the thesis

Costing systems may exist in organizations for several purposes: for externalcosting, to motivate and to evaluate employees, and to provide information fordecision making. This thesis takes the viewpoint typically underlying thesupply chain management literature on the topic of logistics costing: that themain purpose of a costing system is to provide information for dailymanagement of the operations as well as strategic decision-making, althoughother uses are briefly presented. External reporting is addressed where itseffect is relevant from the supply chain management perspective.

The discussion on logistics cost management and the problems related to ittakes place from the perspective of a manufacturing firm unless otherwisestated in the text, as most of the literature reviewed takes that viewpoint.

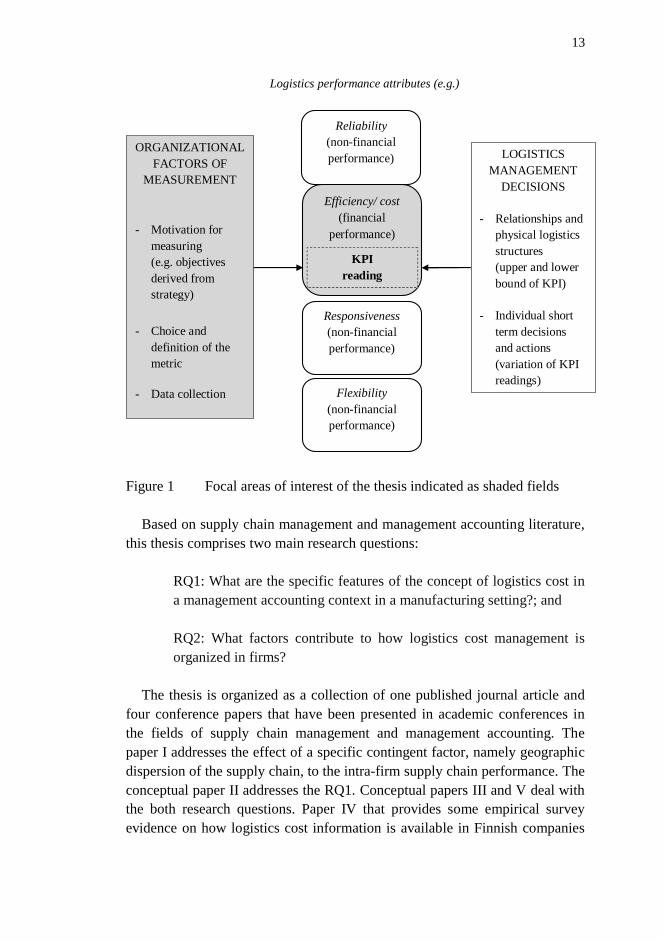

13

Figure 1 Focal areas of interest of the thesis indicated as shaded fields

Based on supply chain management and management accounting literature,this thesis comprises two main research questions:

RQ1: What are the specific features of the concept of logistics cost ina management accounting context in a manufacturing setting?; and

RQ2: What factors contribute to how logistics cost management isorganized in firms?

The thesis is organized as a collection of one published journal article andfour conference papers that have been presented in academic conferences inthe fields of supply chain management and management accounting. Thepaper I addresses the effect of a specific contingent factor, namely geographicdispersion of the supply chain, to the intra-firm supply chain performance. Theconceptual paper II addresses the RQ1. Conceptual papers III and V deal withthe both research questions. Paper IV that provides some empirical surveyevidence on how logistics cost information is available in Finnish companies

Reliability(non-financialperformance)

Responsiveness(non-financialperformance)

Efficiency/ cost(financial

performance)

KPIreading

ORGANIZATIONALFACTORS OF

MEASUREMENT

- Motivation formeasuring(e.g. objectivesderived fromstrategy)

- Choice anddefinition of themetric

- Data collection

LOGISTICSMANAGEMENT

DECISIONS

- Relationships andphysical logisticsstructures(upper and lowerbound of KPI)

- Individual shortterm decisionsand actions(variation of KPIreadings)

Flexibility(non-financialperformance)

Logistics performance attributes (e.g.)

14

is related to the RQ2. The connection between the RQ’s and the appendedarticles is shown in Table 1.

Table 1 Research questions of the thesis and the papers addressing it

Research question Paper nr

RQ1: What are the specific features of theconcept of logistics cost in a management

account context in a manufacturing setting?

Paper I

Paper II

RQ2: What factors contribute to howlogistics cost management is organized in

firms?

Paper III

Paper IV

Paper V

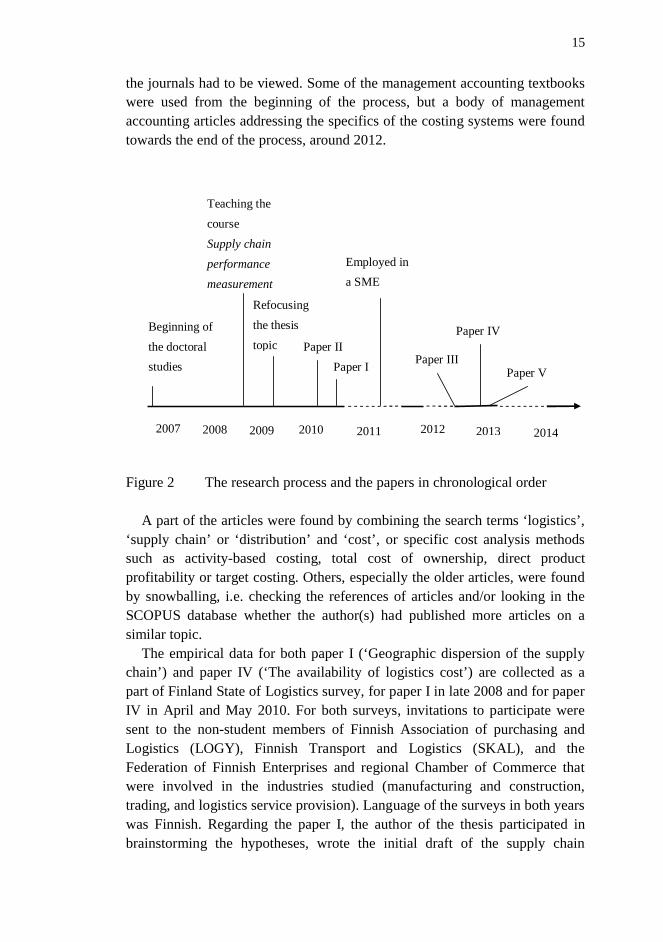

1.3 Research process

The papers in this thesis have been written between 2010 and 2013, and theyhave been presented in academic conferences in the fields of supply chainmanagement (NOFOMA 2013, paper IV) and management accounting(Manufacturing Accounting Research, MAR 2010 and 2012, papers II and III;and the 7th Conference on Performance Measurement and ManagementControl 2013, paper V).The NOFOMA conference paper has been doubleblind peer reviewed, and the both MAR papers have been presented in a Ph.D.track, with a discussant named of the conference participants for each paper.The conference admittance to the 7th Conference on PerformanceMeasurement and Management Control was based on submitted full papers,but the paper V was not otherwise reviewed. The published article was begunin 2010, and published in 2012. Figure 2 presents the course of the researchprocess and the papers in chronological order.

The literature used in this thesis is not systematically reviewed in the sensethat it would be collected from article databases using specific search terms ona selected set of journals and analyzed using pre-defined criteria. Instead,literature has been collected between about 2008 and August 2014, withmajority of the SCM oriented journal articles and literature on logistics costsfound before 2011, with the exception of some articles dating from the 1980sand 1970s. Most articles are found as full texts in EBSCO, Emerald andProQuest databases, but for some of the earlier, before 1990s, paper copies of

15

the journals had to be viewed. Some of the management accounting textbookswere used from the beginning of the process, but a body of managementaccounting articles addressing the specifics of the costing systems were foundtowards the end of the process, around 2012.

Figure 2 The research process and the papers in chronological order

A part of the articles were found by combining the search terms ‘logistics’,‘supply chain’ or ‘distribution’ and ‘cost’, or specific cost analysis methodssuch as activity-based costing, total cost of ownership, direct productprofitability or target costing. Others, especially the older articles, were foundby snowballing, i.e. checking the references of articles and/or looking in theSCOPUS database whether the author(s) had published more articles on asimilar topic.

The empirical data for both paper I (‘Geographic dispersion of the supplychain’) and paper IV (‘The availability of logistics cost’) are collected as apart of Finland State of Logistics survey, for paper I in late 2008 and for paperIV in April and May 2010. For both surveys, invitations to participate weresent to the non-student members of Finnish Association of purchasing andLogistics (LOGY), Finnish Transport and Logistics (SKAL), and theFederation of Finnish Enterprises and regional Chamber of Commerce thatwere involved in the industries studied (manufacturing and construction,trading, and logistics service provision). Language of the surveys in both yearswas Finnish. Regarding the paper I, the author of the thesis participated inbrainstorming the hypotheses, wrote the initial draft of the supply chain

2007 2008 2009 2010 2011 201420132012

Beginning ofthe doctoralstudies

Teaching thecourseSupply chainperformancemeasurement

Refocusingthe thesistopic

Paper IPaper II

Paper IIIPaper V

Paper IV

Employed ina SME

16

performance measurement section and commented on the paper at the reviewstage. (For more on data collection and the data analysis, see the paper I).

For paper IV (‘The availability of logistics cost’) 25 218 firms weretargeted by email, and 1813 responses were received (a response rate of7.1%). Of the respondents 31% (n=570) were from manufacturing companies(including construction) and 30% (n=545) from logistics companies. Theremaining 39% of responses was from trading companies and logisticsconsultants and teachers, which were not target group of the research. Afterexcluding missing responses and micro companies, 154 responses werequalified from manufacturing industry, 123 from trade and 150 from LSPs forthe paper. Micro companies were excluded as they were considered to be toosmall to find formal logistics cost information useful.

The data analysis in paper IV was conducted with statistical analysis bySPSS. The Kruskal-Wallis test of independence was used to test therelationships between the applicable contingent variables and the itemsregarding the detail and availability of logistics cost information, as all itemswere not normally distributed. Additionally, the ordinal regression was used totest the contingent variables that could meaningfully be placed in order fromsmaller to larger.

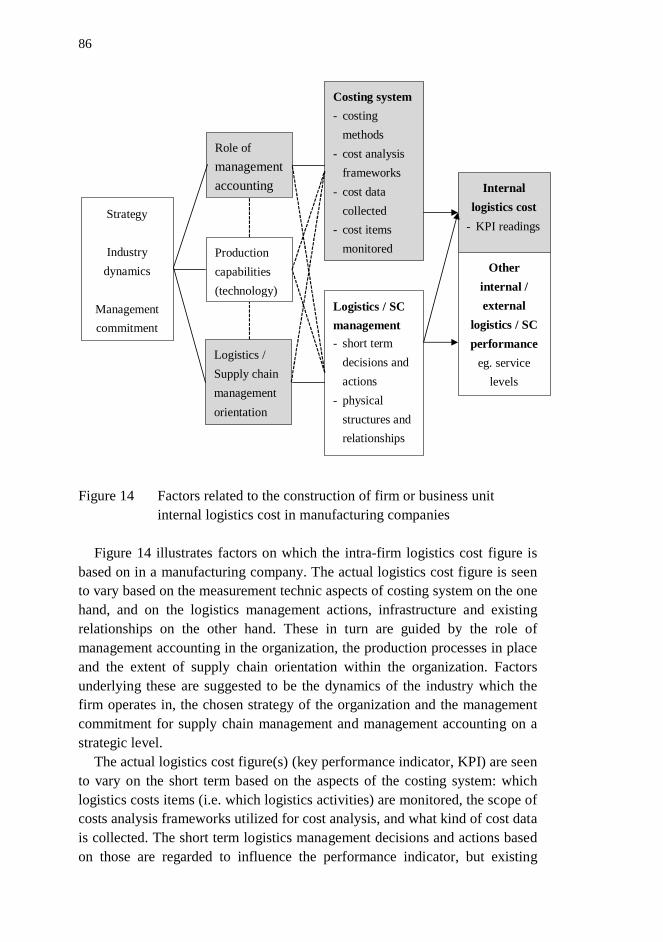

During the process of writing this introductory part of the thesis, Icomplemented the framework of Paper III of the factors related to constructionof company internal logistics cost (Figure 14) with additional factors, as theoriginal framework begun to appear overly simplified. The initial modelseemed to accentuate too much the internal capabilities of the firm, especiallythe management accounting and supply chain orientation. Some of the existingfactors in the initial model have been disaggregated in more detail whilewriting the introductory part of the thesis, too, as it was possible tocharacterize certain factors such as industry dynamics in more detail. Themodel also seemed to provide too simplified an explanation for the way oforganization of the logistics costing: Is professionalism in the fields ofmanagement accounting and supply chain management (or the lack of it)really a main contributing factor, particularly in the long run? If a firm islacking capabilities in a specific professional field, why would it not seek toacquire them?

Why did I consider it appropriate to borrow theories from managementaccounting research literature? Firstly, and most obviously, it is justifiable bythe topic area: logistics cost management and controlling are a facet or anapplication of overall cost management in companies, and most likely thesame basic principles, extensively studied in management accounting, applyalso there. Most supply chain management articles on logistics performancemeasurement and logistics costing do not address in depth the underlying

17

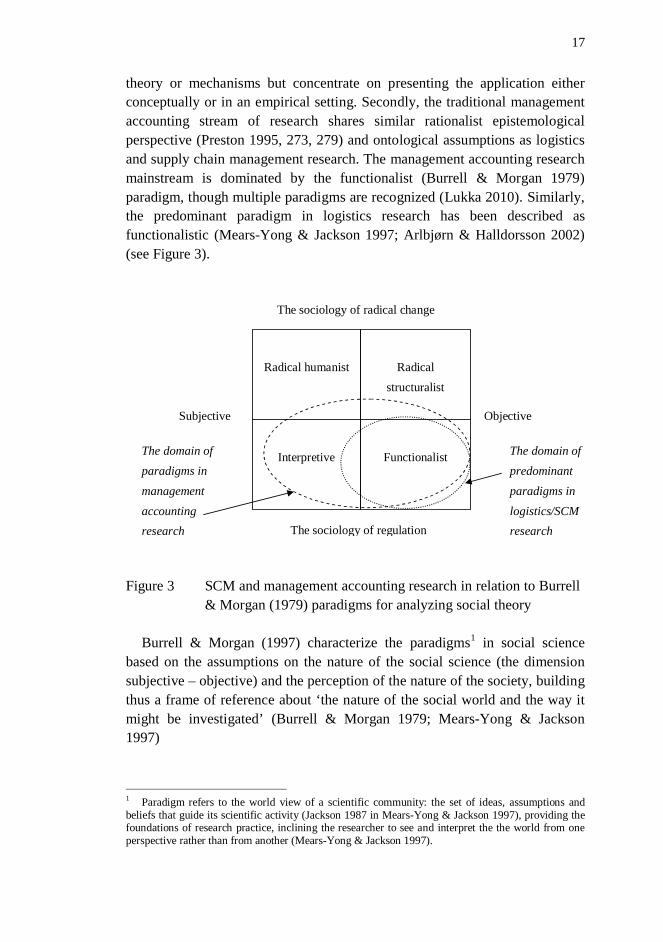

theory or mechanisms but concentrate on presenting the application eitherconceptually or in an empirical setting. Secondly, the traditional managementaccounting stream of research shares similar rationalist epistemologicalperspective (Preston 1995, 273, 279) and ontological assumptions as logisticsand supply chain management research. The management accounting researchmainstream is dominated by the functionalist (Burrell & Morgan 1979)paradigm, though multiple paradigms are recognized (Lukka 2010). Similarly,the predominant paradigm in logistics research has been described asfunctionalistic (Mears-Yong & Jackson 1997; Arlbjørn & Halldorsson 2002)(see Figure 3).

Figure 3 SCM and management accounting research in relation to Burrell& Morgan (1979) paradigms for analyzing social theory

Burrell & Morgan (1997) characterize the paradigms1 in social sciencebased on the assumptions on the nature of the social science (the dimensionsubjective – objective) and the perception of the nature of the society, buildingthus a frame of reference about ‘the nature of the social world and the way itmight be investigated’ (Burrell & Morgan 1979; Mears-Yong & Jackson1997)

1 Paradigm refers to the world view of a scientific community: the set of ideas, assumptions andbeliefs that guide its scientific activity (Jackson 1987 in Mears-Yong & Jackson 1997), providing thefoundations of research practice, inclining the researcher to see and interpret the the world from oneperspective rather than from another (Mears-Yong & Jackson 1997).

Radical humanist Radicalstructuralist

Interpretive Functionalist

The sociology of radical change

The sociology of regulation

Subjective Objective

The domain ofpredominantparadigms inlogistics/SCMresearch

The domain ofparadigms inmanagementaccountingresearch

18

The continuum subjective – objective describes the assumptions regardingthe view of the human nature, ontological and epistemological aspectsunderlying a paradigm, and the resulting type of methodology to be used inresearch. According to objectivist ontological assumptions, the world isconsidered a form an external, objective reality, independent of the researcher.Social sciences are correlated with the natural sciences, and the researcherswould take a positivist approach regarding knowledge as something that canbe objectively acquired; the aim is to understand what is true and false, and toidentify regularities, causalities and laws. Human behavior is consideredpredictable through the understanding of the society, as certain situations willcause certain reactions. The research methods are nomothetic2, follow thetraditional scientific line of approach, with systematic protocol and technique,maintaining ‘objectivity’ and avoiding intervening with the research subject.

In the polar opposite, the subjective approach, the research stressessubjective experience of the individuals in the creation of a social world.Subjectivists are anti-positivistic, regarding knowledge as dependent onunderstanding the perspective of the people creating the ‘reality’. Knowledgeis regarded as situation specific, with no possibility of laws or regularities.People are believed to have free will and therefore not to be ‘scientifically’predictable. Research methods tend to be qualitative, and acknowledge thebelief that only way to understand the social world is through first-handexperience and knowledge is situation specific. (Burrel & Morgan 1979;Mears-Yong & Jackson 1997, 609–610.)

The nature of society, on the other hand, characterizes the approach tosociety itself: what types of research topics are perceived relevant. Regulativetheories are to do with the explanation of status quo, and aim to explain whysociety is maintained as an entity and tends to hold together rather than breakinto oppositional factions. Characterizing the sociology of regulation are e.g.concepts social order, consensus and social integration and cohesion. (Burrell& Morgan 1979, 17; Mears-Yong & Jackson 1997). In the oppositeperspective, the theories of radical change question the status quo andenvisage emancipation for the humankind: the social ‘system’ is not seen assatisfying needs but as eroding the possibilities for human fulfillment.Characteristic concepts are structural conflict, modes of domination andcontradiction. The theories seek to surmount the norms imposed by currentsociety, and aim toward potentiality rather than actuality. (Burrell & Morgan1979, 18; Mears-Yong & Jackson 1997)

2 Nomothetic: ‘of or relating to the search for general laws or traits’ (MOT Collins EnglishDictionary, 2014)

19

Logistics research has been found to predominantly follow positivisticepistemology (e.g. Mears-Yong & Jackson 1997; Arlbjørn & Halldorsson2002), and to be based on realist ontology and determinist view of humannature (Mears-Yong & Jackson 1997, 611–612); and to show adherence toregulative sociology (Mears-Yong & Jackson 1997 ) - i.e. can be categorizedas functionalistic in the Burrel & Morgan framework. However, there areadvocates in logistics and supply chain researchers for e.g. 1) critical realism(Aastrup & Halldorsson 2002): ‘relaxing’ the realist assumptions of externaland objective reality, context-free knowledge, as well as the reliance onnatural sciences methodology by acknowledging the reality experienced byindividuals, and case research as a valid research method; and 2) actorsapproach, which sees researcher as an ‘insider’, an inseparable part of theresearch process, and emphasizes interpretations, contextualized knowledgeand understanding (Arbnor & Bjerke (1997); Gammelgaard 2004). Thereforethe range of logistics and supply chain management research can beconsidered to extend from the functionalist paradigm to the area of interpretiveresearch paradigm. Nevertheless, the paradigms of radical change appear aliento the logistics research. Mears-Yong & Jackson (1997) contrast logisticsresearch to the sociology of radical change, and argue that logistics researchconforms to the sociology of regulation in the sense that the logisticsprofessional is assumed to take the role of expert and guide the organization tothe objectives set or agreed upon by the powerful members of the supplychain. Also ‘non-logisticians’ of the organization are argued to be ‘coerced’into supposed social cohesion of the logistics managerial philosophy. Forexample, the functional attitudes and goals are seen to be hindering theintegration of supply chain (Mears-Yong & Jackson 1997, 613–614.)

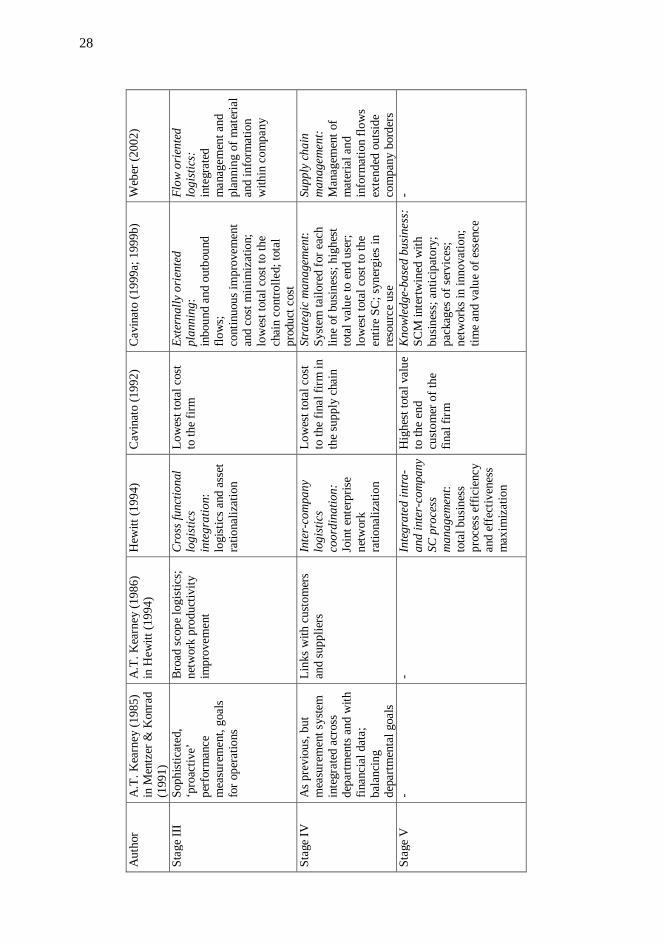

I identify three broader theoretical perspectives that underlie the discussionof the logistics and supply chain cost management presented in this thesis3. InChapter 1.5 were presented various development or evolutionary models of theconcept of logistics in the firms in connection with costing system relatedfactors. Especially Weber (2002) adopted this perspective in his extensivestudy of logistics costing. However, the evolutionary models were criticizedfor path dependency and not providing explanations why a company would beat a specific phase of development or what impacts the transition to the nextstage. Nevertheless, I support the idea that first an organization must reach anelementary level of cost system or logistics management upon which a moresophisticated system can be build.

Another theoretical background behind much of the discussion of costmanagement in SCM literature is the resource based-view (e.g. Barney 1991;

3 These are by no means inclusive of all the perspectives identifiable in management accounting

20

Collis & Montgomery 1995). The resource-based view states that firmperformance is driven by its resources or capabilities in a dynamic competitiveenvironment (Collis & Montgomery 1995) This perspective is partly inherentin the concept of supply chain itself, which originates from the value chainconcept (Porter 1980). The value chain is also the base of supply chain costingpromoted by Pohlen et al. (2009) but also the activity-based costing andactivity based management made popular by Kaplan & Cooper (1998) hasadapted the idea of sequentially focusing on value adding activities bringingcompetitive advantage. Also Hergert & Morris (1989) implicitly take aresource-based view in focusing on the value chain metaphor in the discussionof accounting data deficiencies for costing of processes and value addingactivities.

The principle in supply chain management and consequently also in supplychain cost management is to identify overlapping and redundant tasks andactivities that do not bring value to the end customer and to perform them in amost efficient location of the supply chain, simplify or automate them, or toeliminate completely, if possible (Pohlen et al. 2009). This would createunique processes of indeterminate durance that are hard to imitate by thecompetitors, i.e. the supply chain management and cost management‘resources’ of the organization would bring competitive advantage. However,an opposing view is that cost management systems would not be uniquesources of competitive advantage, as the management accounting innovationsand managerial trends are diffused by consultants, industry lobbyingorganizations, and professional education and professionals moving from oneorganization to another. Thus similar systems would appear in severalcompanies, and be ubiquitous within an industry.

The main underlying theory base of this thesis, however, is contingencyapproach which is common in management accounting research (Otley 1980;Preston 1986; Chenhall 2003). Contingency theorists argue that performanceis a function of the congruence between an organization and its environment,strategy and structure (Fredricks 2005) Management accounting literaturepresents contingency research of the connection of firm external factors on thebroader management control systems and emphasizes the fit of the controlsystem, the firm characteristics and the environment it operates in (acontingency perspective, in contrast to the resource-based approach explainingthe organizational performance with the organization’s capabilities). (Preston1986). In this thesis the contingency approach is apparent in the RQ2: ‘Whatfactors contribute to how logistics cost management is organized in firms?’, itshandling and the model summarizing the discussion (Chapter 7).

21

1.4 Defining the scope of logistics

One of the general problems of costing is the scope, i.e. deciding which costsrelate to specific cost object and should thus be included in the calculation(Kulmala et al. 2002; Kulmala 2003). In the context of supply chainmanagement this means defining which activities are at the responsibility oflogistics and which are the activities of purchasing, production or marketing,whether there are measurements at the supply chain level connecting these,and where to draw the boundaries of the supply chain to be measured.

The definition of logistics costs in a firm is based on how the logisticsactivities and outputs are defined. A factor complicating the definition oflogistics output is the shared use of resources such as personnel or buildingswith other company functions. (Weber 2002, 139.) Defining the logisticsoutputs is necessary for building cost standards for ongoing costing, and mightrequire some simplification in order not to make costing system unnecessarycomplicated. For large scale decisions which are made only occasionally,more specific analyses are needed in addition. (Weber 2002, 131.) Settingstandards for logistics activities has been considered more difficult than formanufacturing because – depending on the production process – moreactivities may exist than in production, and output measures vary more than inproduction (Lambert & Armitage 1979).

The extent of how far along the supply chain a firm aims to record andcontrol the costs is also significant for the definition of logistics and supplychain costs. In this thesis the demarcation is made following Gudehus &Kotzab (2009) (see Figure 10) that logistics costs are those resulting fromcompany internal processes and inbound and outbound transportation providedthat it is paid for by the company. If costs incurred outside the companyborders, e.g. expenses of logistics activities paid by customers in thedistribution channel or first and second tier suppliers are followed, those costsare here considered supply chain costs. Weber (2002, 139) also discusseswhether the logistics activities or outputs performed “for free” or at leastwithout a separate charge by other members of the supply chain should beincluded in logistics cost calculation, but concludes that it is not practical: theinformation is not needed on daily basis, only in specific cases, and as there isno knowledge of the other firm’s cost structure or the actual cost ofperforming the activities, the figures would be based on guesswork.

Management accounting literature addresses inter-organizational cost andaccounting controls (Caglio & Ditillo 2008) that extend the scope of analyzingthe costs outside the company’s internal supply chain processes. The cost datamay be mainly based on estimations, as in value chain analysis (Hergert &Morrias 1989; Shank & Govindarajan 1993) or based on shared information,

22

as in open-book accounting (Kulmala 2003; Agndal & Nilsson 2010) or costtransparency (Pohlen et al. 2009, 62), where a supply chain or network partnershares cost data of the internal processes. This sharing may be unilateral (e.g. alarge client pressures the suppliers to reveal cost information) or bi- ormultilateral sharing between partners or several members of a network(Kulmala 2003; Agndal & Nilsson 2010). Also target costing, a method wherethe allowable product cost is calculated starting from the desired market priceand profit margin and product design as well as production process areimproved to reach this cost target, may be rolled out also to the suppliers(Cooper & Slagmulder 2003; Pohlen et al. 2009, 61)

A supply chain or network partnership requires creating commonlyaccepted accounting practices between the partners (Kulmala et al. 2002). In astrategic partnership the process of negotiating and agreeing on costing orbenefit sharing issues is more important than within a company, as there is nohierarchical authority to regulate the relationship (Seal et al. 1999). Commonimprovement efforts and profit share agreements thus create demand forreliable cost information, and accordingly, weaknesses in the firms internalcost systems cause difficulties in developing open-book agreements (Kulmalaet al. 2002, 40; Seal et al. 1999). It is argued that in an established partnership,inter-company knowledge of costs forms the basis of continuous improvementprograms that reduce costs of the whole supply chain rather than just suppliermargins. And if the supplier asks for higher prices, the shared informationensures that price changes are based on actual changes in cost conditions.Correspondingly, a measurement system imposed on one of the partnersconflicts with the principle of common goal and weakens the long-termprospects of the relationship (Seal et al. 1999, 310, 320).

The paper III of this thesis presents a supply chain cost framework, whichgives an overview of the various activities and sub-processes that may beconsidered as the responsibility of logistics and supply chain management. Asdiscussed in more detail in Chapter 1.5, the company’s perception of logisticsor supply chain management is likely to influence what activities are includedas logistics, and consequently also to whether the cost of these activities ismonitored or explicitly recognized as logistics cost. A company with moresophisticated logistics management practices and more supply chain mindedperspective may be more likely to pursue the control and evaluation of theperformance of broader range of logistics activities than one with basicperception of logistics as materials management and movement.

Another problem related to the scope of logistics is related to a broaderperception of logistics as coordinating the internal operative processes.Although costs of activities previously considered as joint costs of severaldepartments or indirect cost of another area (for example order processing: an

23

indirect cost of sales) can now be recorded as direct costs of logisticsdepartment or responsibility area (Weber 2002, 140), there still remains thequestion of which coordination or planning activities precisely are theresponsibility of logistics. Which operative responsibility area manages forexample production planning, materials requirement planning or sales andoperations planning?

1.5 Perception of logistics and supply chain management

It has been suggested that the performance measurement and collection ofperformance information of logistics is related to how logistics or supply chainmanagement is perceived in companies (Weber 2002; Cavinato 1992); rangingfrom a basic function conducted in lower organizational levels to a businessstrategy fulfilling orientation inherent in every-day business and strategicdecision making at the senior management level. Also the firm’s definition ofthe scope of logistics activities can be considered stemming from what is thegeneral perception of logistics in a company (Weber 2002).

The idea that logistics and supply chain management develop in anevolutionary manner, in successive phases in firms has been persistent insupply chain literature, but has very rarely been empirically tested. In additionto the logistics of an individual company developing, the general perception oflogistics has been developing in time. In the earlier articles the conceptdiscussed was called distribution management (Heskett 1962), distributionlogistics or integrated logistics (Halley & Guilhon 1997); later, it has beencalled purchasing and supply management (Cavinato 1999a), as well aslogistics and supply chain management (Cavinato 1999b; Lockamy &McCormack 2004). The terms have different connotations especiallyregarding which functions (inbound or outbound) are in the focus and how faroutside the firm borders the responsibilities extend – the scope of the supplychain. The tendency has been that broader range of activities and processeshave been included in the supply chain management, and those logisticsmanagement practices that were earlier considered progressive or leading-edgehave become commonplace and ‘order-qualifiers’ instead of ‘order winners’.

Most of the articles on the development of logistics or the supply chain andthe measurement of its performance reviewed here are conceptual, and thosethat are based on surveys or interviews reveal little detail on the datacollection and analysis. Descriptions of the stages often are somewhat broadand by no means unified from one article to another. The models can also beconsidered to reflect the time of publication: over time the perceptions ofsupply chain management especially at the most advanced stage of the models

24

become more sophisticated and complex. The level of integration and thescope of operations required for the advanced stages tend to increase in thelater models compared to the earlier ones4. Some of the models (Mentzer &Konrad 1991; Cavinato 1999a; 1999b) specifically address the performancemeasurement and controlling issues of logistics at the different stages ofdevelopment, while others paint only a broad picture of the characteristics ofthe different stages (e.g. Hewitt 1994).

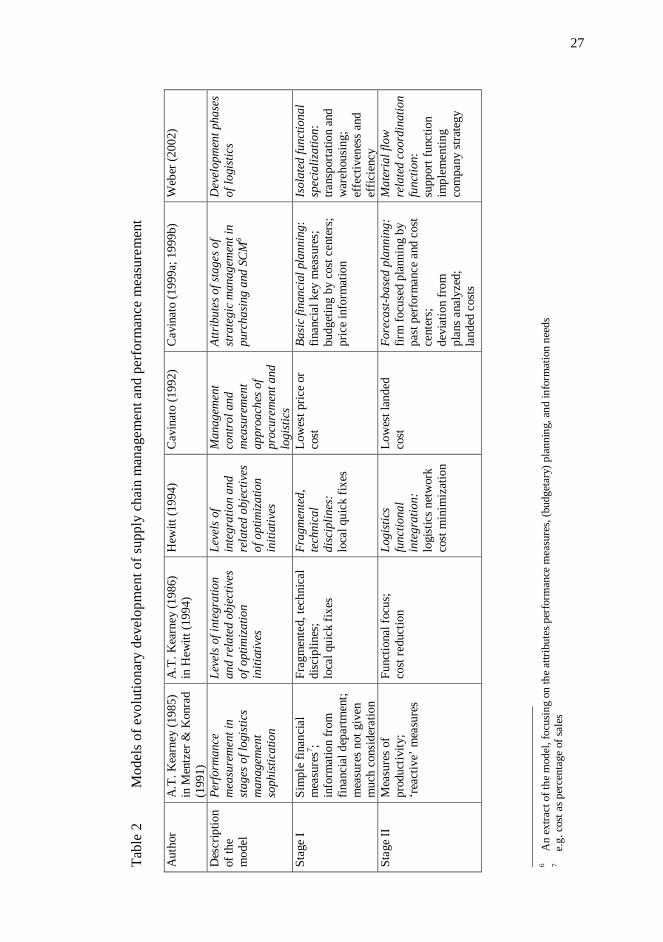

The models explicitly addressing supply chain cost measurement andcontrolling specific issues in different phases of development are summarizedin Table 2.

Cavinato (1999a; 1999b; 1992) presents several models, two with over adozen different attributes of the development phases of company orientation topurchasing and supply chain towards strategic management5. Here only theplanning and performance measurement related attributes are presented. Indifferent stages of development from a functional collection of activities to anarea of strategic management there are different expectations for supply chainor purchasing management, and consequently also different performanceinformation needs. At the first stage, basic financial planning focus is onfunctional operation of logistics, and formal planning concentrates inbudgeting by cost centers. Overriding objective is to meet the budgeted goalsand the concept of cost is the lowest price, rate or cost for a given item orservice. The notion of supply chain is internal and unidirectional; frommaterials management to outbound transportation. In the second stage,forecast-based planning, logistics department is perceived as the distributor,and the main goal is system efficiency, where the role of logistics is to keeporganizational costs in line. Forecasts are based in historical data, but may notbe updated as situations change. Cost focus is on the lowest landed cost to thefirm or to the next customer. (Cavinato 1999b, 167; 173.)

The third stage, externally oriented planning, seeks lowest total cost for thepart of the whole of the supply chain that the firm controls by continuousimprovement and cost minimization; the focus is on total product cost. Thereis a shift from orientation from being merely efficient to being competitive.Supply chain management provides all inbound and outbound flow functions,and is involved in procuring from third parties and creating inter-firmrelationships. In the fourth stage, strategic management, supply chainmanagement provides a tailored system for each line of business, and theperspective shifts from outsourced relationships to that of network

4 E.g. Heskett (1962) names the phases shipping, traffic, movement and physical distribution, thelatest including also demand-supply coordination; wheras in Cavinato (1999a; 1999b) this is includedalready in stage II at the latest.5 Based on Gluck et al. 1980 (in Cavinato 1999b)

25

orchestration. Synergies are sought across lines of businesses for logisticscosts and services. The focus is on adding customer value with the lowest totalcost to the entire supply chain. (Cavinato 1999b, 174–175.)

The final, fifth stage is knowledge-based management, and there supplychain strategy is coordinated with the firm as a whole as well as with eachproduct line. Supply chain management is inherent in all types of businessdecisions. Speed of operations as well as time of new products to market isessential, cost is only one element of performance, and supply chainmanagement is expected to anticipate the needs of the customers and todevelop packages of services for them. (Cavinato 1999b, 176.)

Weber (2002) discusses extensively and in great detail the organizing oflogistics cost measurement and controlling in connection with the level ofdevelopment of logistics or supply chain management in a company.However, vast majority of the discussion is based on the first developmentphase, logistics as an isolated functional specialization, and focuses on theefficiency of logistics. On the other hand, that is understandable, when oneassumes that the development stages build on top of each other. Similarly, thetransaction based general accounting systems and databases are the foundationof logistics costing system, enabling more complicated cost and profitabilityanalyses. For the other development stages broader guidelines are given. Thesecond development phase, material flow oriented coordination function,emphasizes strategic perspective and the efficiency of the logistics operations:for logistics controlling selecting strategy related key performance indicatorsand building a balanced scorecard for different areas of logistics arerecommended (Weber 2002, 294–307).

The main idea for the third development phase (flow oriented logistics) isthat logistics should be organized as processes, and measured accordingly.Finally, in logistics as supply chain management the scope of measurementshifts outside the company boarders to measuring and controlling supply chainrelationships. Also informal controls (e.g. cooperative practices and trust,shared values and understandings) gain in importance in this phase. (Weber2002, 307–313.)

There are certain common elements in the models that distinguish onedevelopmental stage from another. First is the integration of logistics function.The lowest stage is characterized by fragmentation into different logisticsactivities or isolation of the logistics function from the other activities of thecompany. This is also described with the metaphors flow (Weber 2002,Cavinato 1999a; 1999b) and process (Hewitt 1994). Second is the scope of theintegration: whether extending to all operative activities within the firm,extending outside the firm to the imminent suppliers and/or customers, or tothe whole supply chain. The element of performance in focus in each stage is

26

the third distinguishing element: whether efficiency or value added (to thecustomer), or a combination of both.

As deeply rooted in supply chain management literature as they may be,maturity or stage models in general have been criticized for oversimplifyingreality and neglecting the existence of multiple maturation paths, as well as formerely describing the sequence of levels toward a predefined state, instead ofclarifying factors that actually influence evolution and change (Röglinger et al.2012). In purchasing and supply management literature the evolutionary anddevelopmental metaphors have been criticized for taking certain assumptionsfor granted (Ramsay & Croom 2008), including:· that (purchasing and supply) activities are classified either as

‘strategic’ or ‘non-strategic’;· that strategic activities are associated with higher intra-organizational

status than non-strategic activities; and· that purchasing function is expected to undergo change following an

evolutionary or developmental path from ‘clerical’, ‘routine’ oroperational to a strategic focus.

Furthermore, the simplicity of the models undermines the complexities ofthe change from one stage to another, and does not acknowledge the fact thatevery company is different. Besides, different aspects of the same functionmay develop at a different pace. Doubts have also been raised about thesuitability of the models for other than very large corporations: smallcompanies may not afford to hire a specialized buyer, let alone a wholedepartment. (Rozemeijer 2008, 206; Ramsay & Croom 2008, 198–199.)

Also, the strategic importance of purchasing is noted to be contingent on atleast the overall strategic objectives of the organization, the type oforganization and the purchase. What is operative to one organization may be asource of competitive advantage to another. It is also possible that unless theindustry and market environment demands it, there may be no benefit for thefirm from a greater strategic role of purchasing (Ramsay & Croom 2008, 198).Therefore, development models should be regarded as conceptual, possiblehelpful for classifying companies in terms of their current position, but othercompany and industry specific factors should be examined when consideringpossible directions for strategic change (Rozemeijer 2008, 206). The similarapproach may be applied to the development models of logistics and supplychain management and their controlling: they may be helpful for broaddescription of the characteristics of the firm, but depending on the context alsoa less sophisticated system may be a satisfactory and functioning solution.

27

Tabl

e 2

Mod

els o

f evo

lutio

nary

dev

elop

men

t of s

uppl

y ch

ain

man

agem

ent a

nd p

erfo

rman

ce m

easu

rem

ent

Aut

hor

A.T

. Kea

rney

(198

5)in

Men

tzer

& K

onra

d(1

991)

A.T

. Kea

rney

(198

6)in

Hew

itt (1

994)

Hew

itt (1

994)

Cav

inat

o (1

992)

Cav

inat

o (1

999a

; 199

9b)

Web

er (2

002)

Des

crip

tion

of th

em

odel

Perf

orm

ance

mea

sure

men

t in

stag

es o

f log

istic

sm

anag

emen

tso

phis

ticat

ion

Leve

ls of

inte

grat

ion

and

rela

ted

obje

ctiv

esof

opt

imiz

atio

nin

itiat

ives

Leve

ls of

inte

grat

ion

and

rela

ted

obje

ctiv

esof

opt

imiz

atio

nin

itiat

ives

Man

agem

ent

cont

rol a

ndm

easu

rem

ent

appr

oach

es o

fpr

ocur

emen

t and

logi

stic

s

Attr

ibut

es o

f sta

ges o

fst

rate

gic

man

agem

ent i

npu

rcha

sing

and

SC

M6

Dev

elop

men

t pha

ses

of lo

gist

ics

Stag

e I

Sim

ple

finan

cial

mea

sure

s7 ;in

form

atio

n fr

omfin

anci

al d

epar

tmen

t;m

easu

res n

ot g

iven

muc

h co

nsid

erat

ion

Frag

men

ted,

tech

nica

ldi

scip

lines

;lo

cal q

uick

fixe

s

Frag

men

ted,

tech

nica

ldi

scip

lines

:lo

cal q

uick

fixe

s

Low

est p

rice

orco

stBa

sic

finan

cial

pla

nnin

g:fin

anci

al k

ey m

easu

res;

budg

etin

g by

cos

t cen

ters

;pr

ice

info

rmat

ion

Isol

ated

func

tiona

lsp

ecia

lizat

ion:

trans

porta

tion

and

war

ehou

sing

;ef

fect

iven

ess

and

effic

ienc

ySt

age

IIM

easu

res o

fpr

oduc

tivity

;‘r

eact

ive’

mea

sure

s

Func

tiona

l foc

us;

cost

redu

ctio

nLo

gist

ics

func

tiona

lin

tegr

atio

n:lo

gist

ics n

etw

ork

cost

min

imiz

atio

n

Low

est l

ande

dco

stFo

reca

st-b

ased

pla

nnin

g:fir

m fo

cuse

d pl

anni

ng b

ypa

st pe

rform

ance

and

cos

tce

nter

s;de

viat

ion

from

plan

s an

alyz

ed;

land

ed c

osts

Mat

eria

l flo

wre

late

d co

ordi

natio

nfu

nctio

n:su

ppor

t fun

ctio

nim

plem

entin

gco

mpa

ny st

rate

gy

6 A

n ex

tract

of t

he m

odel

, foc

usin

g on

the

attri

bute

s per

form

ance

mea

sure

s, (b

udge

tary

) pla

nnin

g, a

nd in

form

atio

n ne

eds

7 e.

g. c

ost a

s per

cent

age

of sa

les

27

Aut

hor

A.T

. Kea

rney

(198

5)i n

Men

tzer

& K

onra

d(1

991)

A.T

. Kea

rney

(198

6)in

Hew

itt (1

994)

He w

itt (1

994)

Cav

i nat

o (1

992)

Ca v

inat

o (1

999a

; 199

9b)

We b

er (2

002)

S tag

e III

Soph

istic

ated

,‘p

r oac

tive’

perf

orm

ance

mea

sure

men

t, go

als

for o

pera

tions

Broa

d sc

ope

logi

sti c

s;ne

twor

k pr

oduc

tivity

impr

ovem

ent

Cro

ss fu

nctio

nal

logi

stic

sin

tegr

atio

n:lo

g ist

ics a

nd a

sset

ratio

naliz

atio

n

Low

est t

otal

cos

tto

the

firm

Ext e

rnal

ly o

rien

ted

plan

ning

:i n

boun

d an

d ou

tbou

ndflo

ws;

cont

inuo

us im

prov

emen

tan

d co

st m

inim

izat

ion;

low

est t

otal

cos

t to

the

chai

n co

ntro

lled;

tota

lpr

oduc

t cos

t

F low

ori

ente

dlo

gist

ics:

inte

grat

edm

anag

emen

t and

plan

ning

of m

ater

ial

and

info

rmat

ion

with

in c

ompa

ny

Stag

e IV

As p

revi

ous,

but

me a

sure

men

t sys

tem

inte

grat

ed a

cros

sde

partm

ents

and

with

finan

cial

dat

a;ba

lanc

ing

depa

rtmen

tal g

oals

Link

s with

cus

tom

ers

and

supp

liers

Int e

r-co

mpa

nylo

gist

ics

coor

dina

tion:

J oin

t ent

erpr

isene

twor

kra

tiona

lizat

ion

Low

est t

otal

cos

tto

the

final

firm

inth

e su

pply

cha

in

Stra

tegi

c m

anag

emen

t:S y

stem

tailo

red

for e

ach

line

of b

usin

ess;

hig

hest

tota

l val

ue to

end

use

r;lo

wes

t tot

al c

ost t

o th

een

tire

SC; s

yner

gies

inre

sour

ce u

se

Supp

ly c

hain

man

agem

ent:

Man

agem

ent o

fm

ater

ial a

ndin

form

atio

n flo

ws

exte

nded

out

side

com

pany

bor

ders

Stag

e V

--

Inte

grat

ed in

tra-

and

inte

r-co

mpa

nySC

pro

cess

man

agem

ent:

tota

l bus

ines

spr

oces

s eff

icie

ncy

and

effe

ctiv

enes

sm

axim

izat

ion

Hig

hest

t ota

l val

ueto

the

end

cust

omer

of t

hefin

al fi

rm

Kno

w led

ge-b

ased

bus

ines

s:SC

M in

tertw

ined

with

busin

ess;

ant

icip

ator

y;pa

ckag

es o

f ser

vice

s;ne

twor

ks in

inno

vatio

n;tim

e an

d va

lue

of e

ssen

ce

-

28

29

2 THE MANAGERIAL AND ORGANIZATIONALCONTEXT OF LOGISTICS COST

2.1 Role of management accounting

The management accountants of the organization influence greatly if notalmost completely how logistics costing is organized in the firm. Thedevelopment of supply chain management places additional criteria to cost andperformance information than what has been traditional. Along with theuniversally increased importance of supply chain management also the role ofmanagement accountant in companies has changed. The managementaccountant nowadays is expected to have a more active, even pro-active rolein the provision of cost and performance information.

A general development similar to the development of supply chainmanagement has taken place in management accounting since mid-twentiethcentury. The emerging new management accounting techniques are argued tohave affected the whole process of management accounting (planning,controlling, decision-making and communication) and shifted the focus from‘simple’ role of cost determination and financial control to a ‘sophisticated’role of creating value through improved deployment of resources. The Inter-national Federation of Accountants (IFAC) has presented a four-stage con-ceptual framework of the general development. (Abdel-Kader & Luther 2006.)

The first stage, cost determination and financial control, is described tohave taken place mainly before 1950, when production technology wasrelatively simple, labor and material costs were easily identifiable, andcompetition on the basis of either price or quality was relatively low. Thefocus of management accounting was mainly on the determination of productcost, and the use of budgeting and cost accounting techniques were prevalent.However, cost information was not disseminated much, and its use formanagement decision-making was poorly exploited. The shift to the secondstage, information for management planning and control, is seen to have takenplace by mid-1960s. The focus shifted to the provision of information forplanning and control purposes, and management accounting was recognized amanagement activity, but in a staff role, providing staff support to linemanagement. Management accounting tended to be reactive, identifyingproblems and actions only from the deviations from the business plan.Management controls were oriented toward manufacturing and internal

30

administration rather than strategic and business environmental concerns.(Ashton et al. 1995, 1–2; Abdel-Kader & Luther 2006.)

The transition to the third stage, reduction of resource waste in businessprocesses, took place by the mid-1980s, motivated by the increased globalcompetition, shortened product life-cycles and rapid technological develop-ment both in production and information processing. This was met with intro-duction of new management and production techniques, at the same timecontrolling costs, often through reduction of waste in business processes. Thiswas in many instances supported by employee empowerment, and lead todistribution of decision-making and the need for management informationthroughout the organization. The fourth stage, creation of value through effec-tive resources use, is argued to have taken place by the mid-1990s. With thedevelopment of Internet, appearance of the e-commerce and ever increasingglobal competition the focus of management accounting shifted to the genera-tion of value through the effective use of resources. The critical differencecompared to earlier stages is the change in focus away from informationprovision and toward resource management, first in reducing waste and thencreating value. However, the attention in information provision is not lost, butinformation becomes a resource along with the other organizational resources.(Abdel-Kader & Luther 2006; Ashton et al. 1995, 3–4.)

This development model appears very similar to the general maturitymodels the logistics and SCM (as discussed in Chapter 1.5). Also similarcritique may be presented: the stages may not apply to all industries and allcompany-sizes, or to all countries. In some industries and competitive environ-ments more elementary role of management accounting may be sufficient, andthe firm has had no need to adopt the more sophisticated approach ofmanagement accounting. However, one may argue that in the most competi-tive environments at least, the aims of management accounting and supplychain management have converged. Nowadays, management accountants areincreasingly expected to act as business partners and part of the team, and areincreasingly involved in functional areas such as production and marketing.The audit and control mentality traditionally associated with managementaccounting is seen unhelpful for that. Flexibility is hoped for in the design ofreporting systems and in the budgets in response to changes in businessenvironment, and instead of standard information, more relevant informationtailored for the needs of managers is hoped for. (Pierce & O’Dea 2003.)

Pierce & O’Dea (2003) noted that managers reported the use of specificmanagement accounting techniques such as target costing, distribution channelprofitability analysis and benchmarking higher than the managementaccounting in the same organizations. This implies that it is not necessarilymanagement accounting function conducting the cost analyses but the

31

managers themselves – i.e. the data analysis and information provision rolehas shifted to some extent to the information users themselves. Crude analysesof customer profitability were used in some companies, avoiding thedifficulties of indirect cost allocation. This was raised as an example of ‘good-enough accounting’, where the managers appreciate the timeliness of specificdata more than technical accuracy (Pierce & O’Dea 2003, 282–283.)

As the strategic level of perception of both management accounting andsupply chain management increase, there is not so great difference for thepractice in the logistics context which term is used. Both aim for the creationof value through effective resources use, and this is likely to be pursued ininter-functional teams. At a lower level of supply chain orientation (logisticsmanagement) the difference between the roles of the two functions are morelikely to be higher. The perceptions of the information requirements andavailability as well as the purposes of the use of cost and performancemeasurement systems may be then less likely to converge.

2.2 The firm size

The company size has been recognized in management accounting literaturean important factor affecting the organization of management control. Largerorganizations have resources available to adopt more sophisticated andadvanced management accounting practices (MAP) than smaller ones. (Abdel-Kader & Luther 2008, 7). Increasing firm size also adds to the complexity ofoperations, increasing the need for formal controls and specialized functions(Chenhall 2003) The connection between the development level ofmanagement accounting practices and the organizational size has been foundstatistically significant e.g. by Al-Omiri & Drury (2007), Abdel-Kader &Luther (2008) and Askarany et al. (2010).

The firm size is also been used as a contingent variable in two of the papersin this thesis. Paper I uses firm size as a control variable in examining theeffect of geographical dispersion of supply chain to the intra-firm supply chainperformance, and paper IV finds the size of a firm to be related to theavailability of administrative logistics cost information in trading companiesand to the detail of logistics cost information available in trading andmanufacturing companies.

Halley & Guilhon (1997) set boundaries to the evolutionary metaphor ofgeneral development of logistics by including contextual factors, and present aframework for examining the logistics strategy of small companies. They statethat an external pressure from the market (e.g. in the form of customerdemands or increased competition) motivates the shift to a next phase.

32

Additionally, the distinctive competencies of the firm as well as the owner-manager’s preferences of strategy are seen influence the logistics strategypracticed in a small firm. Consequently, logistics strategy is described as· reactive: logistics activities are unintegrated, focus is on their

efficiency and cost reduction, and logistics is developed sporadically,often in response to another organization’s initiative;

· emergent: logistics performance is developed gradually, with thepurpose of jointly pursuing with other firms long-term competitivegoals; or

· pro-active: logistics is highly integrated within the organization, andthe objectives include effectiveness, value creation and broadening thecontrol of the firm (and the owner-manager) over the environment.(Halley & Guilhon 1997, 481–482.)

2.3 Products and production process

Product and production process related factors also contribute to the logisticscosting. The size and weight of the product affect the relative importance oflogistics costs in the total product cost. For a manufacturer of heavymachinery, for example, who uses great amounts of plate steel as well ascastings and forgings, which are costly to transport, receive and handle,logistics costs are a major expense (Jones 1991). Oversimplification of acosting system in this area would greatly distort logistics costs. Company thushas used a variation of an activity-based cost system, with specific cost poolsfor logistics. There are two cost pools for the cost of activities on shippingdocks, in the receiving areas and in the storage areas for the heavy materialgroups, and, similarly, two costs pools for the intra-plant handling of materialsas it moves through the production process. Based on these, variable andperiod costs rates are calculated, and allocated either by product weightpoundage (as planned to be used in the next period), or the poundagemultiplied by the number of material moves in the production process. Forlighter purchased finished material the costs of buying, receiving, storing andmoving are grouped together, and allocated based on material prices (Jones1991)

Product diversity has been identified as a factor contributing to the sophisti-cation of product costing system (Abernethy et al. 2001): higher level ofproduct diversity indicated low satisfaction in traditional (low sophisticationlevel) costing system, but high satisfaction in high sophistication level costingsystem. In firms with low product diversity, on the other hand, the managersexperienced high level of satisfaction with less sophisticated costing system.

33

The phase of the product life cycle also contributes to how high priority isplaced on efficiency and cost reduction. As the product moves from the phaseslaunch of the product and market growth to maturity and decline of themarket, the performance priority of logistics shifts from fast delivery to marketto availability of the product cost efficiently and finally to cost efficientdeliveries of small orders. (Fisher 1997)

Also the storability of end products and raw material, and the point ofinventory may influence the relevant importance of cost (efficiency) incontrast to other elements of performance in different parts of the intra-company supply chain. McKinnon and Bruns (1993) noticed that the nature ofproduction process and the raw material used for the product affected the mainconsideration in purchasing: the cost of running out of material versus the costof maintaining the material inventory. A relatively stable production process,where production is planned and plans rarely change also allows forpredictable material requirements. Prices and inventory levels were thenmonitored over longer time periods. Also long term contracts with supplierslengthened the time frame of monitoring the purchase price. (McKinnon andBruns 1993, 31–32)