Embed Size (px)

Citation preview

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Understanding Telecom Usage in Bahrain Business Module Findings

July 2007

U & A Research Findings –Business Module

Page 2August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Agenda

Background &

Methodology

Background &

MethodologyTelecom Usage

Telecom Usage

TRA Under-standing

TRA Under-standing ConclusionsConclusions

U & A Research Findings –Business Module

Page 3August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Agenda

Background &

Methodology

Background &

Methodology

Telecom Scenario within the

Organization

Telecom Scenario within the

Organization

TRA Under-standing

TRA Under-standing ConclusionsConclusions

Study Background

Research Objectives

Research Design

Sample Profile

U & A Research Findings –Business Module

Page 4August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Background • Bahrain Telecommunications Regulatory Authority (TRA) was formed in October 2002. The

TRA is an independent body which has a direct responsibility to ensure effective liberalization of the telecommunications market.

• Bahrain TRA is in the process of carrying out an extensive strategic review of the telecommunications sector in the Kingdom of Bahrain for which it needs to collect and analyze information about the sector.

• TRA commissioned Nielsen to conduct a market research study with the objective of understanding the detailed usage behavior across various user segments in Bahrain.

• The telecom users are divided into two broad segments i.e. Residential and Corporate thus two separate modules were conducted to collect the required information.

• This presentation details the findings of the research conducted amongst the Corporate / Businesses to achieve TRA’s information needs.

U & A Research Findings –Business Module

Page 5August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Research Objectives

• The key objectives of this phase of the study is to understand the following within the corporate:

Detailed Usage of all Telecom Services -Fixed Line, Mobile and Data Services

Satisfaction with various services and Switching Behavior

Awareness of TRA and its activities

U & A Research Findings –Business Module

Page 6August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Research Design

Target Respondent• Responsible for telecom needs in the

organization ( Decision makers or Influencers).

• Following sectors were included in research:– Construction and building

– Financial, insurance, real estate and business services

– Health care

– Hotels and Restaurants

– Manufacturing Industries

– Transport and Communication

– Wholesale and Retail trade

– Business Services (Ad agencies, Consultants) / Professional services, etc

Research Methodology

• 159 Quantitative face to face interviewsacross various industries were conducted amongst the target respondents using a structured questionnaire.

• Interviews were conducted in English / Arabic as convenient to the respondent.

• Interview length was approximately of 40-45 minutes.

• Field work Timing : May 2007

U & A Research Findings –Business Module

Page 7August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Sample ProfileIndustry Type Sample

SizeSample

Proportions

Wholesale and Retail trade 25 16%

Business Services (Ad agencies / Consultants) etc 14 9%

Construction and building 23 14%

Financial, Insurance, Real estate & Business services 33

5

32

21

6

159

21%

Health care 3%

Hotels + Restaurants 20%

Manufacturing industries 13%

Transport, IT and Communication 4%

Total 100

20-99 employees

40%

100+ employees

18%Less than

20 employees

42%

Employee Size

Base: All respondents = 159

U & A Research Findings –Business Module

Page 8August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Agenda

Background &

Methodology

Background &

MethodologyTelecom Usage

Telecom Usage

TRA Under-standing

TRA Under-standing ConclusionsConclusions

Fixed Line Status

Mobile Status

International Calls

Internet / Data Services

Imperatives

Telecom expenses

U & A Research Findings –Business Module

Page 9August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Agenda

Background &

Methodology

Background &

MethodologyTelecom Usage

Telecom Usage

TRA Under-standing

TRA Under-standing ConclusionsConclusions

Fixed Line Status

Mobile Status

International Calls

Internet / Data Services

Imperatives

Telecom expenses

U & A Research Findings –Business Module

Page 10August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Importance of Telecom Services

• Telecom is the key to run the business.

– As expected, majority of the businesses find telecom an integral part of their work and claim that business is incomplete without it.

– This is more so for large companies where 54% of the company representatives claim that telecom is Indispensable for them.

59

35

6

Indispensable (Can notconduct businessw ithout telecom service)

Very important

Others

Base: All respondents = 159

Less than 20 employees

20-99 employees

100+ employees

Base 66%

65%

32

62

28*%

54

Very Important 68 32

29Indispensable

*small base, findings are indicative

U & A Research Findings –Business Module

Page 11August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Important Factors

• ‘Tariffs/Charges’ is the most important element followed by the ‘Quality of services’ across industries.

– With the increasing employee size, criteria changes, Quality of Services and Brand Reputation play larger role

– Financial services sector attach greater significance to the pricing aspect, where 66% of the company representatives mentioned Tariffs are the No. 1 parameter

– ‘Health & Social’ sector consider brand reputation as more important than the others.

43

35

1183

Customer/account care

Range of business servicesavailableBrand/reputation

Quality of services

Tarif fs/charges

Rank 1 scores

Base: All respondents = 159

Rank 1 Less than 20 employees

20-99 employees

100+ employees

Base 66%

65%

43

Quality of Services

29 35 46

Brand Reputation 9 6 25

28*%

2553Tariffs / Charges

*small base, findings are indicative

U & A Research Findings –Business Module

Page 12August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Existing Number Importance

• Existing number is very crucial for businesses.

– More than 70% say it is extremely important and consider it essential for smooth running of the business.

Retaining the old number

Important22%

Not Important5%

No response2%

Very Important (It is essential for

business)71%

Base: All respondents = 159

U & A Research Findings –Business Module

Page 13August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Agenda

Background &

Methodology

Background &

Methodology

Telecom Scenario

with Organization

Telecom Scenario

with Organization

TRA Under-standing

TRA Under-standing ConclusionsConclusions

Fixed Line Status

Mobile Status

International Calls

Internet / Data Services

Imperatives

Telecom expenses

U & A Research Findings –Business Module

Page 14August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Type of Fixed line Connection

• Analog Fixed Voice and Fax lines are most commonly used across business.

– As expected the average number of lines increase with the increase in employee size.

– Financial sector has the maximum

Average Number of Lines

Total Less than 20 employees

20-99 employees

100+ employees

Base 159%

66%

4

2

Fixed Voice lines

28*%

65%

4

Fax lines 1 2

11

4

2

number of fixed lines.

• Batelco is universally recognized as a fixed line provider.

• Other brands have low awareness as fixed line service providers

Other Service Providers - Awareness

26

14 144

Mena Kalaam 2Connect Nuetel

Base: All respondents = 159

*small base, findings are indicative

U & A Research Findings –Business Module

Page 15August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Value Added Services

• Caller Line Identification is most commonly used value added service by business fixed line users.

• Conference Call is used by nearly 1/3rd of the businesses

• More value added services used by large companies.

Fixed line VAS used

61

33

27

24

18

5

Call Line Identif ication

Conference Calls

Bahrain Direct

Home Direct

Voicemail

V ideo Conference Calls

Base: All respondents – 159

U & A Research Findings –Business Module

Page 16August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Number of National Calls made daily

63 70

15136 46 6

10 7

Fixed to f ixed Fixed to Mobile

200+ calls

151-200 calls

101-150 calls

51-100 calls

upto 50 calls

• Most of businesses make up to 50 National calls per day to both fixed line and mobile.

• As expected larger companies make more number of calls compare to smaller firms.

Base: All respondents – 159

Average No. of Calls

Less than 20 employees

20-99 employees

100+ employees

Base 66%

65%

90

Fixed to Mobile 35 65 140

28*%

13530Fixed to Fixed

*small base, findings are indicative

U & A Research Findings –Business Module

Page 17August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Duration of National Calls from Fixed Line

• Majority of the calls made last for 3-10 minutes. However a significant portion (45%) of calls are up to 3 minutes of duration.

• Some differences have been recorded between industries.

– Finance companies make longer calls, where 72% of calls made are more than 3 minutes.

– Large companies (employee size more than 100) also tend to make longer calls, where 64% of calls made are more than 3 minutes.

19

35

46

9

Fixed line

More than 10 minutes

More than 3 minutes up to 10minutes

2 to 3 minutes

1 to 2 minutes

Less than 1 minute

Average scores across respondents

Base: All respondents – 159

45%

U & A Research Findings –Business Module

Page 18August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Fixed Line Billing Pulse Awareness

• Most corporate customers think that the billing pulse for fixed line is ‘Per minute’ calls to Fixed line and Mobile.

• The individual customers also perceive the same as seen in residential research module.

817

82 67

1

7 1512

Fixed to Fixed Fixed to Mobile

Others/ Don't know

Per 3 Minutes

Per 90 Seconds

Per Minute

Per Second

Base: All respondents – 159

U & A Research Findings –Business Module

Page 19August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Private Network (LAN) to make National Calls

Base: All respondents – 159

• Overall low response recorded for Private Network (LAN) usage.

– Seems to be popular only amongst the large organizations.

Use24%

Do not use76%

Less than 20 employees 20-99 employees 100+ employees

Base – All respondents 66%

65%

22

28*%

649Using a Private Network (LAN) to make national calls between offices

*small base, findings are indicative

U & A Research Findings –Business Module

Page 20August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Satisfaction Levels

• Most Corporate customers are satisfied with Fixed Line services at an overall level.

• Some have expressed uncertainties about ‘Customer Care Parameters’. Maximum dissatisfaction is observed for Tariffs.

Satisfaction Levels - Fixed Line Parameters

3 4 4 7 531

9 11 1320 23

2355 4351

42 44

27

33 42 32 31 28 19

Overall servicelevel

Range o fservices pro vided

Quality o f service Respo nse whendealing withpro blems

Custo mer care Charges fo rNatio nal Calls

Very Satisf ied

Fairly Satisf ied

Neither satisf iednor dissatisf ied

Not satisf ied

Base: All respondents – 159

U & A Research Findings –Business Module

Page 21August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Switching Inclination - Fixed line provider

• Majority of the corporate customers are not likely to switch fixed line service provider in case of choice availability

• The resistance is higher amongst the large companies (more than 100 employees) where 60% state that they are not likely to change.

Likeliness to switch

47

35

18Likely

Neither likely nor unlikely

Not likely

Base: All those who are not willing to switch – 75

Reasons for not switching the provider…• Don’t want to change the number 36%• Satisfied with Batelco – 27%• Current provider offer good services – 25%• Have good features – 7%

Base: All respondents – 159

Reasons for switching the provider…• Cheaper prices – 50 %• Better services – 43%

Base: All those who are willing to switch – 28*

*small base, findings are indicative

U & A Research Findings –Business Module

Page 22August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

To sum up

Fixed line Status

Fixed line Status

• All corporate customers use fixed and fax line services. High volume of national calls for both : Fixed to Fixed and Fixed to Mobile.

• While Batelco subscription is universal, there is a low awareness for other players.

• Value Added Services subscription limited to a few services like CLIP and conference calls

• Majority of the calls made last for 3-10 minutes. However a significant portion (45%) of calls are less than 3 minutes of duration.

• Very few businesses use Private Network (LAN) to make national calls.

• Overall Satisfaction levels are high, however some express uncertainties about customer care. Tariffs is a concern for many.

• On probing for inclination to switch, most company representatives feel it in unlikely because they do not want to change their numbers and are satisfied with the services provided by their current operator.

U & A Research Findings –Business Module

Page 23August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Agenda

Background &

Methodology

Background &

Methodology

Telecom Scenario

with Organization

Telecom Scenario

with Organization

TRA Under-standing

TRA Under-standing ConclusionsConclusions

Fixed Line Status

Mobile Status

International Calls

Internet / Data Services

Imperatives

Telecom expenses

U & A Research Findings –Business Module

Page 24August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

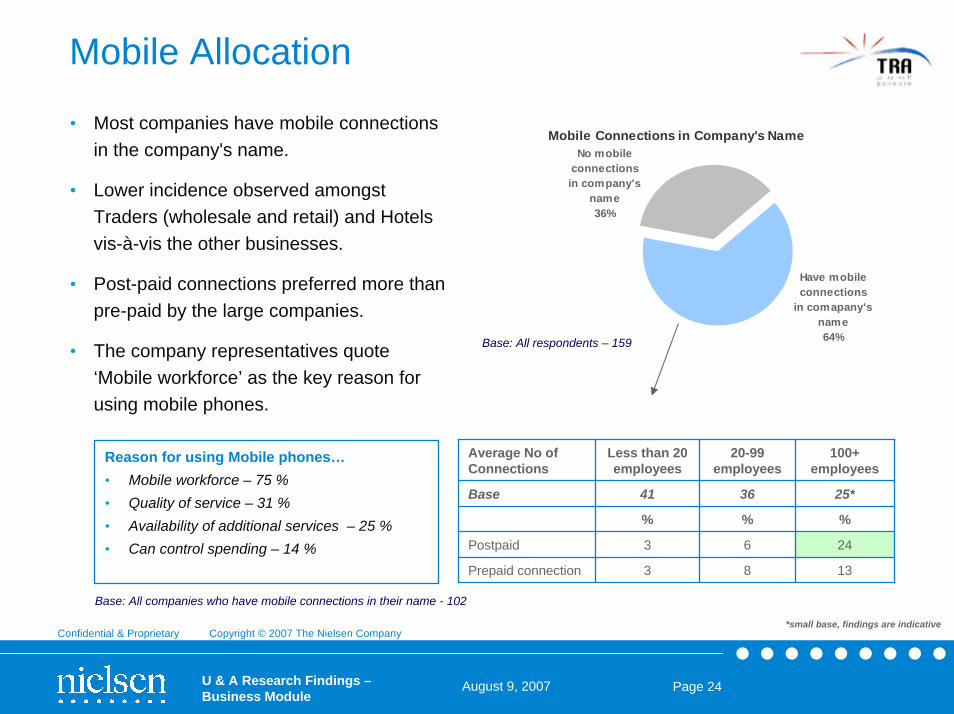

Mobile Allocation

• Most companies have mobile connections in the company's name.

• Lower incidence observed amongst Traders (wholesale and retail) and Hotels vis-à-vis the other businesses.

• Post-paid connections preferred more than pre-paid by the large companies.

• The company representatives quote ‘Mobile workforce’ as the key reason for using mobile phones.

Base: All respondents – 159

Mobile Connections in Company's Name

Have mobile connections

in comapany's name64%

No mobile connections in company's

name36%

Base: All companies who have mobile connections in their name - 102

Average No of Connections

Less than 20 employees

20-99 employees

100+ employees

Base 41 36

%

6

8

%

25*

%

24

13Prepaid connection 3

3Postpaid

Reason for using Mobile phones…• Mobile workforce – 75 %• Quality of service – 31 % • Availability of additional services – 25 % • Can control spending – 14 %

*small base, findings are indicative

U & A Research Findings –Business Module

Page 25August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

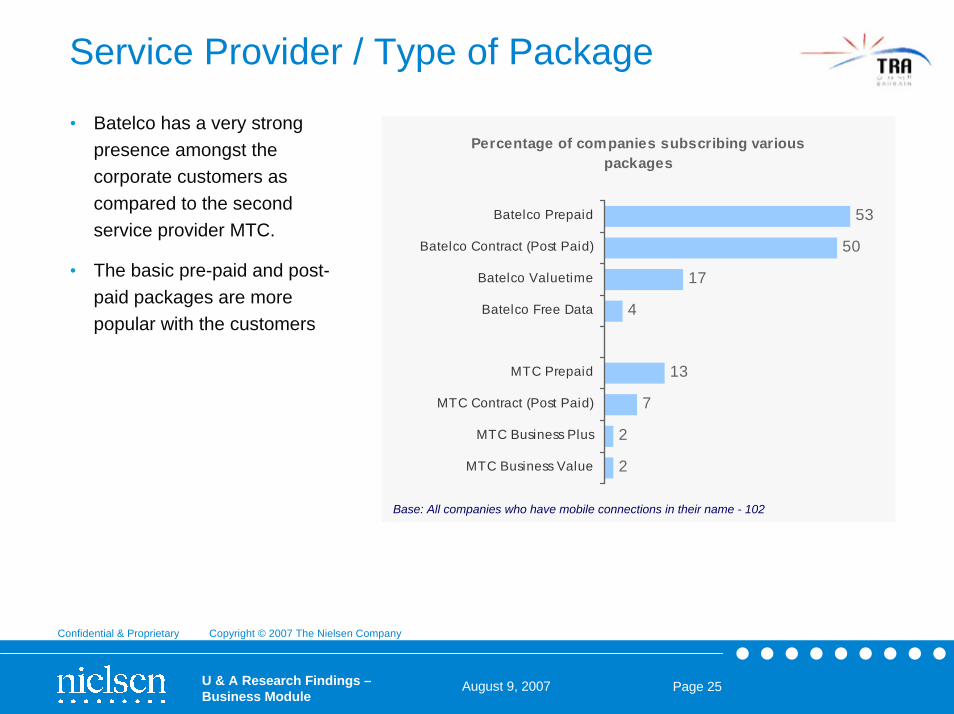

Service Provider / Type of Package

• Batelco has a very strong presence amongst the corporate customers as compared to the second service provider MTC.

• The basic pre-paid and post-paid packages are more popular with the customers

Percentage of companies subscribing various packages

53

50

17

4

13

7

2

2

Batelco Prepaid

Batelco Contract (Post Paid)

Batelco Valuetime

Batelco Free Data

MTC Prepaid

MTC Contract (Post Paid)

MTC Business Plus

MTC Business Value

Base: All companies who have mobile connections in their name - 102

U & A Research Findings –Business Module

Page 26August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Value Added Services Mobile VAS used

50

41

21

15

4

3

SMS+

InternationalRoaming

Bulk SMS

Voicemail

MENAFNSMS

SMS BillPayment

Base: All companies who have mobile connections in their name - 102

• Only a moderate use of value added services by the corporate users.

• SMS+, International Roaming are the most availed service.

U & A Research Findings –Business Module

Page 27August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

No. of National Calls made daily

• Most business need to make up to 50 calls per day to various channels.

• Large companies (100 plus employees) tend to make almost double the number of calls than counterparts 78 79 78

12 11 1310 10 9

Mobile to mobile -on net

Mobile to mobile -off net

Mobile to f ixedline

More than 100 calls

51-100 calls

upto 50 calls

Base: All companies who have mobile connections in their name - 102

U & A Research Findings –Business Module

Page 28August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Duration of National Calls from Mobile

• Duration of calls from mobile is very similar to the calls originating from fixed line, where maximum calls are between 3 to 10 minutes.

• As per the company representatives, nearly 49% of their calls from mobile are of durations up to 3 minutes.

114

34

43

8

Mobile

More than 10 minutes

More than 3 minutes up to 10minutes2 to 3 minutes

1 to 2 minutes

Less than 1 minute

Base: All companies who have mobile connections in their name - 102

Average scores across respondents

49%

U & A Research Findings –Business Module

Page 29August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Satisfaction Levels

• Like fixed line, high satisfaction recorded for Mobile service amongst businesses. No major issues with regards to customer care unlike Fixed Line services.

• Tariffs is the only concern area.

Satisfaction Levels - Mobile Service Parameters

1 2 2 2 8 3 5 16 269 15 20 21

20 22 2123

1957 3948 48 44 47 47

40 34

33 4430 29 28 28 27 21 21

Overallservice level

Range ofservices

Serviceavailability

Quality ofservice

No droppedcalls

Customercare

Dealing w ithproblems

SMS Charges National CallTarif fs

Very Satisf ied

Fairly Satisf ied

Neither satisf iednor dissatisf ied

Not satisf ied

Base: All companies who have mobile connections in their name - 102

U & A Research Findings –Business Module

Page 30August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Switching Inclination – Mobile Service

• As seen for fixed line, corporate customers are not keen to switch. This is more so for large companies.

• Unwillingness to change existing number seems to be a prime reason.

Likeliness to switch

53

31

16Likely

Neither likely nor unlikely

Not likely

Base: All companies who have mobile connections in their name - 102

Reasons for not switching the provider…• Don’t want to change the numbers – 41%• Satisfied currently with existing provider – 24%• Offer good services – 19% • Good Features – 7%

Base: All those who are not willing to switch – 54

U & A Research Findings –Business Module

Page 31August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

To sum up

Mobile Status

Mobile Status

• Most companies subscribe to mobile connections primarily becauseof mobile workforce.

• Post-paid connections preferred over pre-paid. Batelco has a very strong presence amongst corporate customers.

• Value added services used only moderately.

• Higher number of calls per day. Most calls are of 3-10 minutes duration.

• High satisfaction observed for Mobile service amongst Corporate users.

• Users are quite loyal and are not likely to switch service providers.

U & A Research Findings –Business Module

Page 32August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Agenda

Background &

Methodology

Background &

Methodology

Telecom Scenario

with Organization

Telecom Scenario

with Organization

TRA Under-standing

TRA Under-standing ConclusionsConclusions

Fixed Line Status

Mobile Status

International Calls

Internet / Data Services

Imperatives

Telecom expenses

U & A Research Findings –Business Module

Page 33August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Channels used to make International Calls

• Majority of the international calls are made through Fixed line using the Direct IDD by the customers

• Small proportion use Mobile IDD to make calls abroad.

• Others options like pre-selected carrier, calling cards, VOIP are only marginally used by the corporate customers currently.

74

15443

Mobile - using prepaidcalling cards Fixed line - using prepaidcalling cardsFixed line - Pre-selectedcarrierMobile - Direct IDD

Fixed line - Direct IDD Calls

Average scores across respondents

Base: All those who make international calls – 138 respondents

Popular International Calling Cards - Used by the business customers

• MENA Talk• K Talk

U & A Research Findings –Business Module

Page 34August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Destinations called

• More than 70% of the companies call UAE and Saudi Arabia .

• Duration of international calls is

Top 8 countries called...

8473

52 49 4841 36

28

UAE

Saudi Arabia

India

Kuwait

Qatar

Oman

United Kingdom

USA

somewhat shorter than the local calls

1

40

38

12

9

More than 10 minutes

More than 3 minutesup to 10 minutes2 to 3 minutes

1 to 2 minutes

Less than 1 minute

Base: All those who make international calls – 138 respondents

U & A Research Findings –Business Module

Page 35August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Satisfaction – International Tariffs • Low satisfaction with international

tariffs - both fixed line and mobile.

• The disappointment is more prominent amongst the mid-size (20 to 99 employees) companies where the dissatisfaction score is more than 40%

Likeliness to switch

38 35

2011

2735

15 19

Fixed Line Mobile

Very Satisfied

Fairly Satisfied

Neither satisf ied nordissatisfiedNot Satisf ied

Base: All 159 102

U & A Research Findings –Business Module

Page 36August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

To sum up

International Calls

International Calls

• The main channels used for international calls are Fixed Line and Mobile IDD calling.

• Amongst those companies which use calling cards, MENA Talk and K Talk are the most popular.

• KSA and UAE are the top called destinations, where most calls are in the range of 1-2 minutes.

• High dissatisfaction for international call tariffs, especially amongst mid-size companies.

U & A Research Findings –Business Module

Page 37August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Agenda

Background &

Methodology

Background &

Methodology

Telecom Scenario

with Organization

Telecom Scenario

with Organization

TRA Under-standing

TRA Under-standing ConclusionsConclusions

Fixed Line Status

Mobile Status

International Calls

Internet / Data Services

Imperatives

Telecom expenses

U & A Research Findings –Business Module

Page 38August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Data Service Usage

• Data services other than Broadband Internet have very low incidence of usage.

• The companies which do not use any data service are mainly traders and restaurants etc.

• Accessibility of advanced data / net services is limited to large sized firms.

Internet services used in organizations67

9 8 5

33

InternetBroadbandservices

BusinessData

services

E-Applications

ICT Solutions Do not useany dataservice

Base: All respondents – 159

Less than 20 employees

20-99 employees

100+ employees

Base 66%

65%

80

5

E-Applications 2 3 36

ICT Solutions - 2 25

28*%

93

Business Data 5 32

42Internet Broadband

*small base, findings are indicative

U & A Research Findings –Business Module

Page 39August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Broadband Packages% of companies susbcribing broadband

packages

11

7

10

9

37

10

8

15

INET Business Dialup

INET Direct Dial-up

Business 256k (2.5GB)

Business 256k (5GB)

Business 512k(10GB)

Business 512 (Unlimited)

Business 1028 (Unlimited)

Don’t know bandw idth

Base: All respondents – 106

• Broadband 512k (10 GB) is the package subscribed by most companies

Almost 100% have subscribed to services offered by Batelco

Base - 106

U & A Research Findings –Business Module

Page 40August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Satisfaction Levels • While most internet subscriber claim that they are satisfied, the satisfaction scores are lower

than Fixed Line and Mobile. Concerns on tariffs and speed of connection.

• Suggest improvements i.e. ‘Reduce price’ (46%), ‘Increase speed’ (25%) and ‘Improve service quality (16%).

Satisfaction with fixed line

5 4 5 4 5 4 610 6 11 20 12 9

4615 18

1915 19 19

838 40 35 37 37 42

2532 32 30 24 27 26

15

Overallservice level

Range o fservices

Quality o fservice

Effectivespeed o f

co nnectio n

Respo nseduring

pro blems

Custo mercare

Charges

Very Satisf ied

Fairly Satisf ied

Neither satisf iednor dissatisf iedNot satisf ied

No Response

Base: All having broadband internet connection – 106

U & A Research Findings –Business Module

Page 41August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

To sum up

Data Services

Data Services

• Broadband Internet is the most common Internet service used by the businesses in Bahrain.

• Other advanced data services are availed only by large organizations.

• Fair satisfaction with the Internet service available, relatively lower than Fixed line and Mobile. Suggestions provided by the customers are related to reducing charges and providing faster speed.

U & A Research Findings –Business Module

Page 42August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Agenda

Background &

Methodology

Background &

Methodology

Telecom Scenario

with Organization

Telecom Scenario

with Organization

TRA Under-standing

TRA Under-standing ConclusionsConclusions

Fixed Line Status

Mobile Status

International Calls

Internet / Data Services

Imperatives

Telecom expenses

U & A Research Findings –Business Module

Page 43August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

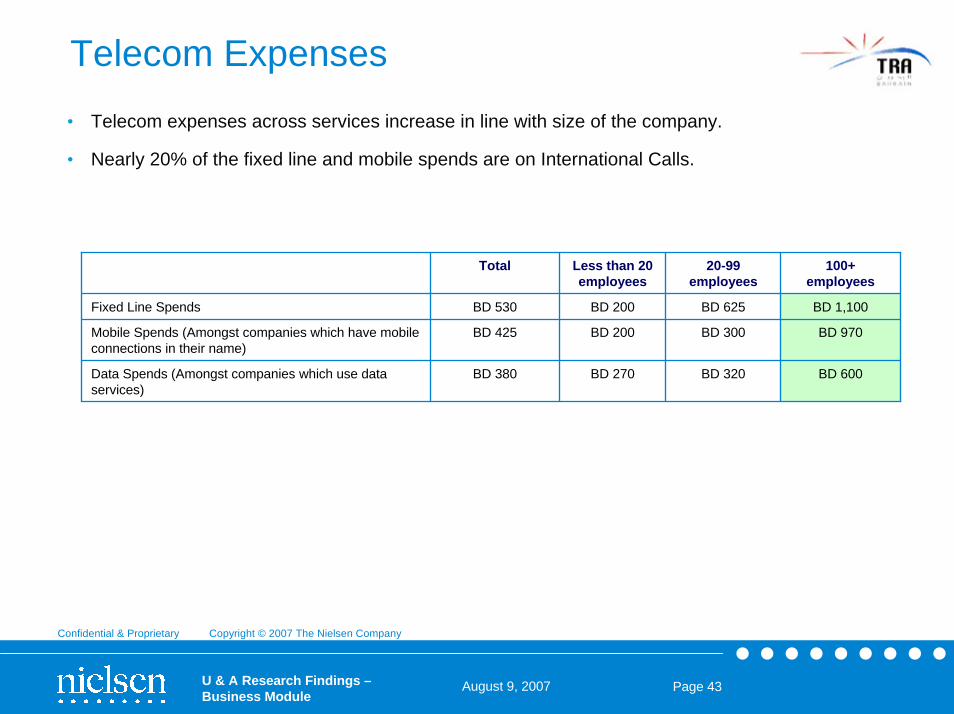

Telecom Expenses• Telecom expenses across services increase in line with size of the company.

• Nearly 20% of the fixed line and mobile spends are on International Calls.

Total Less than 20 employees

20-99 employees

100+ employees

Fixed Line Spends BD 530

BD 425

BD 380

BD 1,100

Mobile Spends (Amongst companies which have mobile connections in their name)

BD 625BD 200

BD 200 BD 300

BD 270 BD 320

BD 970

Data Spends (Amongst companies which use data services)

BD 600

U & A Research Findings –Business Module

Page 44August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Agenda

Background &

Methodology

Background &

MethodologyTelecom Usage

Telecom Usage

TRA Under-standing

TRA Under-standing ConclusionsConclusions

Awareness

Knowledge of TRA services

U & A Research Findings –Business Module

Page 45August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

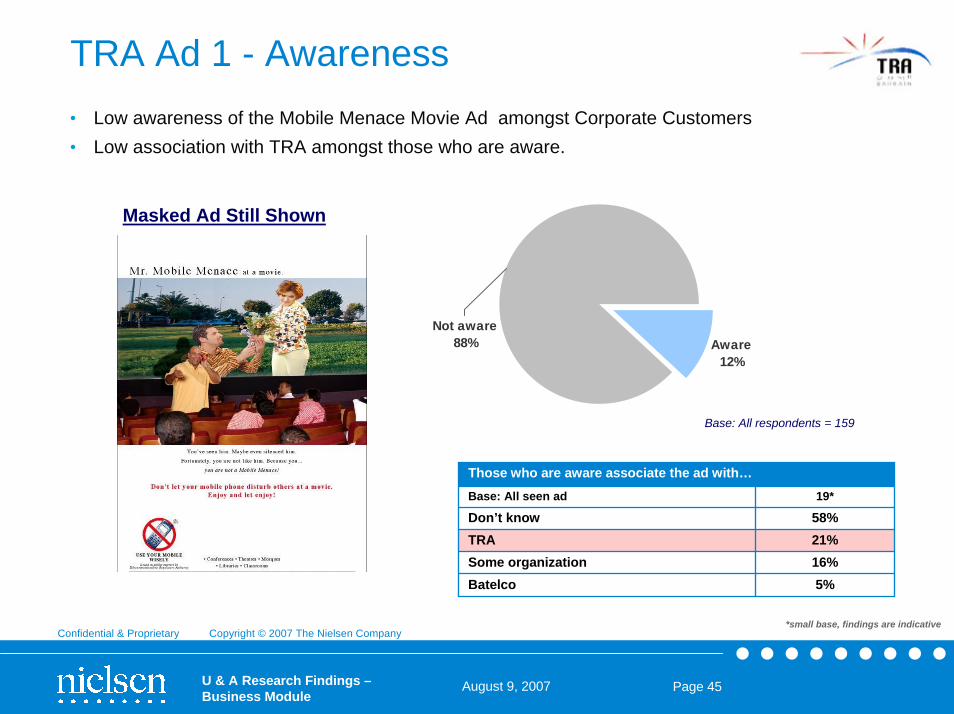

TRA Ad 1 - Awareness

Aware12%

Not aware88%

Masked Ad Still Shown

Those who are aware associate the ad with…Base: All seen ad 19*

TRA 21%Some organization 16%

Don’t know 58%

Batelco 5%

Base: All respondents = 159

• Low awareness of the Mobile Menace Movie Ad amongst Corporate Customers • Low association with TRA amongst those who are aware.

*small base, findings are indicative

U & A Research Findings –Business Module

Page 46August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

TRA Ad 2 - Awareness

Aware38%

Not aware62%

Masked Ad Still Shown

Those who are aware associate the ad with…Base: All seen ad 68

TRA 7%

Movie 3%

Don’t know 80%

Batelco 5%

Bahrain TV 2%

Base: All respondents = 159

• Better awareness for Mobile Menace Conference Ad however association is comparatively lower.

U & A Research Findings –Business Module

Page 47August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Aware30%

Not aware70%

Logo shown to the respondent

Base: All respondents = 159

• Low awareness scores for TRA.– However, as expected, awareness is better amongst corporate than individual customers.

TRA Logo Awareness

U & A Research Findings –Business Module

Page 48August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

TRA Booklet Awareness • Negligible awareness for TRA’s ‘Keep Asking’ Booklet within organizations.

Base: All respondents = 159

Aware of 'Keep Asking Booklet...

Yes4%

96%No

U & A Research Findings –Business Module

Page 49August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

TRA – Source of Awareness

56

21

8

8

4

4

2

2

2

New spaper

Billboard

Cinema

Friends & Relatives

Internet

Leaf lets

Radio

Magazines

TV

% scores

• Newspaper is the main source of awareness for TRA.

• Score for other sources are negligible.

Base: All aware of TRA – 48 respondents

U & A Research Findings –Business Module

Page 50August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

TRA – Website

• Very low awareness of the TRA website, amongst those who know the organization. Heard of TRA website?

19

81

Heard of

No

Yes

Base: All aware of TRA – 48 respondents

U & A Research Findings –Business Module

Page 51August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Agenda

Background &

Methodology

Background &

MethodologyTelecom Usage

Telecom Usage

TRA Under-standing

TRA Under-standing ConclusionsConclusions

Awareness

Knowledge of TRA services

U & A Research Findings –Business Module

Page 52August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Role of TRA • Fair understanding of TRA’s role and duties amongst those who known the organization.

Customer say on the role of TRA

Don’t know much about it 8

Just heard the name 8

%

To control service / telecom / communication 35

Regulate rules of a telecom companies 31

It control charges 6

They take care of our complaints 2

Base: All aware of TRA – 48 respondents

U & A Research Findings –Business Module

Page 53August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

TRA Activities

Do you know that TRA asks comments from public on issues related to regulatiions?

19%

81%

Yes No

• Low awareness for requests for consultations.

Base: All heard of TRA as an organization – 48 respondents

U & A Research Findings –Business Module

Page 54August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

TRA – Awareness

54

13

3

The Rights as a TelecomService Consumer

Can register complaintswith TRA

TRA Consumer AdvisoryGroups

Base: All aware of TRA - 48

• Sound awareness of Telecom Consumer Rights amongst the telecom users.

– Interestingly the word of mouth working for TRA as it seems to be the best source of awareness so far.

• The awareness of other activities / issues is fairly low even amongst those who are aware of TRA as an organization.

•Friends & relatives – 46%•TV – 19%

•Newspapers – 15%

Base: All aware of Consumer Rights – 26* respondents

*small base, findings are indicative

U & A Research Findings –Business Module

Page 55August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

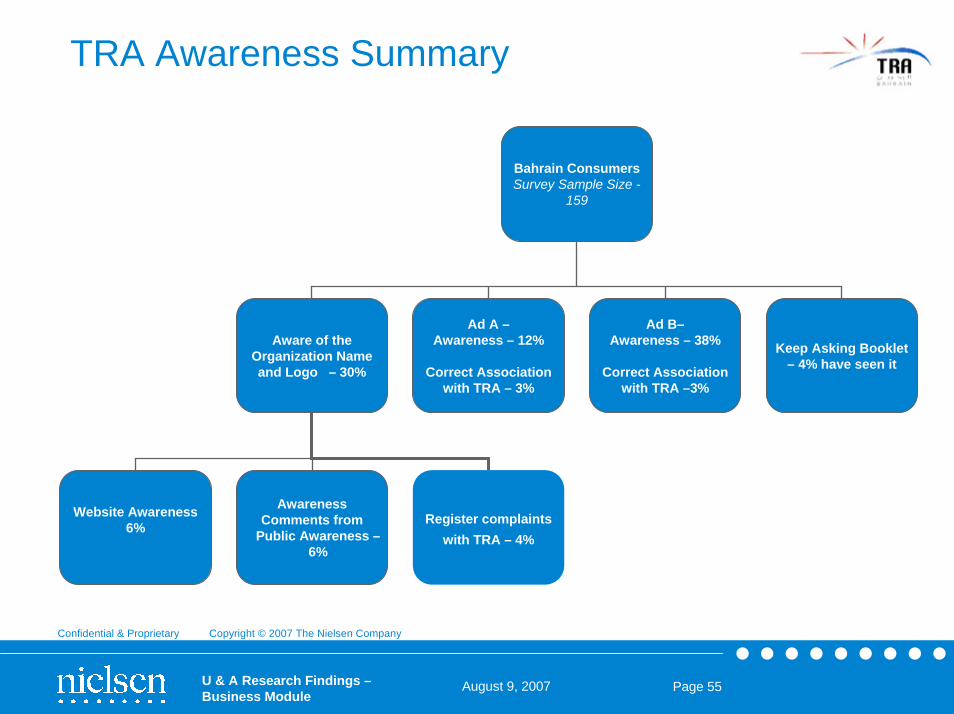

TRA Awareness Summary

Bahrain Consumers Survey Sample Size -

159

Aware of the Organization Name and Logo – 30%

Ad A –Awareness – 12%

Correct Association with TRA – 3%

Ad B–Awareness – 38%

Correct Association with TRA –3%

Website Awareness 6%

Keep Asking Booklet – 4% have seen it

AwarenessComments from

Public Awareness –6%

Register complaints with TRA – 4%

U & A Research Findings –Business Module

Page 56August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Agenda

Background &

Methodology

Background &

MethodologyTelecom Usage

Telecom Usage

TRA Under-standing

TRA Under-standing ConclusionsConclusions

U & A Research Findings –Business Module

Page 57August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Conclusions

Fixed Line (National Calls)High Usage of Fixed Line for voice. Only a moderate use of value added services other than call line ID. While overall high satisfaction, main concerns are

related to Tariffs and uncertainties on customer care. Low intention to switch. Low correct awareness of

billing pulse.

Mobile (National Calls)High usage, mainly of postpaid connections.

Batelco dominates amongst corporate customers. Only a moderate use of Value added services.

Satisfaction High, Concerns on Tariff, Intention to switch is low.

International Calls

Main usage restricted only to regular channels like Fixed Line or Mobile IDD Calls.

KSA and UAE are the top countries called.Low satisfaction with international tariff rates.

Data Services

Usage of data services mainly restricted to Internet. Advanced services used only by larger

organizations. Business 512K (10GB) package subscribed by most customers.

Satisfaction levels lower than other telecom services.

TRA Awareness and InteractionCurrently Corporate Customers have a low awareness and interaction with TRA.

U & A Research Findings –Business Module

Page 58August 9, 2007

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Thank you

Confidential & Proprietary Copyright © 2007 The Nielsen Company