Embed Size (px)

Citation preview

Page 1 of 25

BEFORE THE ADJUDICATING OFFICER SECURITIES AND EXCHANGE BOARD OF INDIA

[ADJUDICATION ORDER NO. MIRSD/ISRL/DRK/ASG/EAD3- 313 / 11 - 2012]

UNDER SECTION 15 I OF SECURITIES AND EXCHANGE BOARD OF INDIA ACT, 1992 READ WITH RULE 5(1) OF SECURITIES AND EXCHANGE BOARD OF INDIA (PROCEDURE FOR HOLDING INQUIRY AND IMPOSING PENALTIES BY ADJUDICATING OFFICER) RULES, 1995

Against Link Intime India Pvt. Ltd.

(Formerly known as Intime Spectrum Registry Ltd.) Registrar to an Issue and Share Transfer Agent,

SEBI Registration No. INR000003761

FACTS OF THE CASE IN BRIEF 1. Securities and Exchange Board of India (hereinafter referred to as ‘SEBI’)

conducted an inspection of Link Intime India Pvt. Ltd. (formerly known as

Intime Spectrum Registry Ltd., hereinafter referred to as ‘the noticee’)

during the period January 18, 2007 to February 03, 2007. The inspection

covered a period from January 2004 to the date of inspection.

APPOINTMENT OF ADJUDICATING OFFICER

2. I was appointed as the Adjudicating Officer vide the proceedings of the

Whole Time Member appointing Adjudicating Officer dated December 10,

2008, under section 15 I of Securities and Exchange Board of India Act,

1992 (hereinafter referred to as the ‘SEBI Act’) read with Section 19H of the

Depositories Act, 1996 (hereinafter referred to as the ‘Depositories Act’) read with Rule 3 of Securities and Exchange Board of India (Procedure for

Holding Inquiry and Imposing Penalties by Adjudicating Officer) Rules, 1995

(hereinafter referred to as ‘Adjudication Rules’) and Rule 3 of Depositories

(Procedure for Holding Inquiry and Imposing Penalties by Adjudicating

Officer) Rules, 2005 (hereinafter referred to as ‘Depositories Rules’) to

inquire into and adjudge under Section 15 C and Section 15HB of the SEBI

Act and Section 19G of Depositories Act, the violations of provisions of the

Page 2 of 25

SEBI (Registrars to an Issue and Share Transfer Agents) Regulations, 1993

(hereinafter referred to as ‘RTI & STA Regulations’) and the SEBI

(Depositories and Participants) Regulations, 1996 (hereinafter referred to as

‘D& P Regulations’) and SEBI circular dated November 05, 1993 alleged

to have been committed by the noticee.

SHOW CAUSE NOTICE, HEARING AND REPLY 3. A Show Cause Notice No. A&E/DRK/ASG/ 163495/2011 dated May 15,

2009 (hereinafter referred to as ‘SCN’) was served on the noticee by

Registered Post Acknowledgment Due in terms of the provisions of Rule 4

of the Adjudication Rules seeking reply of the noticee as to why an inquiry

should not be held against the noticee in respect of the violations alleged to

have been committed by the noticee.

4. The SCN stated that the Inspection Report (hereinafter referred to as ‘IR’)

had made the following observations:

Regarding functioning as Registrar to an Issue (hereinafter referred to as

‘RTI’): 4.1 It was alleged that the noticee did not independently verify the details of

entries keyed in with the physical application for shares from investors

before upload of corporate action resulting in several investor complaints

due to improper allocation and wrong data entry.

4.2 Credit had been given to beneficiary account where the name, status was

not matching; thus, these are wrong allotments / credit of shares to wrong

beneficiary accounts. Thus, it was alleged that the noticee had not

exercised due skill, diligence, care, caution required of an RTI while

processing the applications received in a public issue.

4.3 There were many allotments / credit of shares given to persons who had not

even applied in the public issue. This shows that the validation process

employed by the noticee was highly unreliable. On the wrong credits or

allotments made to persons who have not even applied in the public issue,

when the noticee was queried specifically on this, it had declared minimum

number of instances. Whereas, information obtained from the Depositories

i.e., NSDL/CDSL suggested large number of instances.

Page 3 of 25

4.4 Further, the cases furnished by the Inspection Report had not been

identified by the noticee through its procedures, but because of investor

complaints. Thus, the above also evidences the wrong validation process

and absence of a proper system to unearth wrong credits, at the noticee’s

end.

4.5 In many applications, PAN details provided by the applicants were not

matching with the details as provided while opening of the beneficiary

account, but the noticee had considered these for allotment.

4.6 Multiple allotments had been made to applicants with the same PAN.

Regarding Bank Schedules:

4.7 There appeared to be dummy numbers provided in the column for

instrument number just to populate the same. These could have been easily

unearthed.

4.8 Certain serious issues like absence of names, instrument number, bank

names etc, should have raised an alarm. However, the noticee had

accepted the applications without voicing its concerns.

Regarding functioning as Share Transfer Agent (hereinafter referred to as

‘STA’):

4.9 The noticee had failed to dematerialize and rematerialize securities in the

prescribed time.

4.10 The noticee had made erroneous confirmations of demat request as well as

delayed issue of duplicate shares.

4.11 The noticee had failed to process the transfer of shares within the

prescribed time

4.12 In 13754 instances, the noticee had delayed the processing of demat

requests beyond 15 days of receipt and had rejected/dispatched the same

after 15 days.

4.13 The noticee had failed to reconcile its records on a daily basis as stipulated

under Regulation 55 of the DP Regulations.

Regarding redressal of investor grievances:

4.14 In 4981 instances, the noticee had failed to attend to investor grievances

within one month from the date of receipt.

Page 4 of 25

4.15 The noticee did not have a dedicated e-mail id for complaints related to

share transfer agent activities as on the date of inspection. Also, there was

no auto response system, hence the investor did not come to know whether

his grievance has been received by the noticee or not.

5. It was alleged that the above actions on the noticee’s part violated the

following provisions:

a. Sections 14(3), 19C and 19D of the Depositories Act, 1996;

b. Regulations 54 (5) and 55 of D&P Regulations;

c. Clauses 2, 3, 5 , 21 and 27 of the Code of Conduct prescribed under

Regulation 13 of the RTI & STA regulations;

d. SEBI circular- RRTI Circ. No. 1(93-94) dated November 05, 1993

6. A reply dated June 19, 2009 (hereinafter referred to as ‘reply’) was received

from the noticee which inter alia stated that: Regarding functioning as Registrar to an Issue

6.1 While handling a very large number of applications for processing, the

standard practice is to tally / reconcile the controls of key fields, have the

important fields validated and carry out a detailed check of exceptions. At

the time of data entry and processing of IPO applications as well, a similar

methodology is used and the verification process is under :

i. All application numbers in the noticee’s data are matched with the

application numbers in the Bid files given by the Exchanges. All

exceptions (like appearing in bid file and not appearing in the noticee’s

file or vice cersa) are verified with the physical applications.

ii. The amounts are tallied with the Bank schedules, Bank-branchwise

totals are reconciled and a final certificate is obtained from the Bank for

the total collections. In case of discrepancies between the Bank

schedule and the noticee’s Application file, physical applications are

checked and after interaction with the Bank the same are sorted out. If

the noticee still finds a difference in respect of ‘amount’, bank figure is

taken as final (after reconfirming with the Bank) since the same reflects

the actual amount received.

Page 5 of 25

iii. All DP Id / Client Ids are validated at the data entry level for identifying

the same as ‘valid Id’ and then these data are fed into the Depository

and the names obtained are verified with the names entered in the

noticee’s data file. Considering the large volumes and the possibility of

‘some’ errors (however ‘low’ the percentage may be), the noticee wished

to avoid situations where the Investor Id (wrongly given or captured)

matches with a ‘valid’ Id of another person and hence the Refund is sent

to the wrong person. By using the name captured by the noticee and if

client Id is wrong, the refund will get rejected due to the name and bank

details obtained from the Depository not matching. All ‘exceptional’

cases like large applications, rejections due to all types of reasons (like

minor, bid price below final price, Amount short paid, multiple

applications etc.) get verified with the physical applications.

Thus the noticee reiterated that it was carrying out an elaborate

verification process of all entries keyed in with the applications to avoid /

minimize investor complaints. However due to sheer volumes and tight

timelines, a few errors (a miniscule percentage when compared to the

volume of applications received and the timelines available to complete

the process) do creep in.

6.2 The noticee matches the names captured by it and the Depository data

obtained from the Depository based on the DP Id / Client Id of the investor.

First it programmatically checked for a total match of names without any

discrepancy in spelling/ spaces etc. Secondly it matched names based on

the first 10 characters, which are accepted. Lastly for all the balance

mismatch cases, the noticee physically verified each and every case on the

computer monitor (a visual check) to see whether the two names match and

most of the times, errors are rectified at this stage. Only after this process,

the noticee credited the shares to the Demat Account. However as stated

earlier, due to sheer volume of applications and the stringent timelines a few

cases (a miniscule in percentage terms) may slip verification during this

process, due to inadvertent human error. Such errors cannot be construed

as not exercising due skill, diligence, due care and caution to the best of the

noticee’s ability and circumstances, in the given situation.

Page 6 of 25

6.3 As explained in the earlier paragraphs, such credits to persons who had not

applied in the public issue arose because, the investor Id captured was

matching with another valid Id of a different person (either due to wrong

filling up in the application form by the investor, illegible handwriting or due

to wrong data entry). These are some of the exception cases, which missed

being found out at the time of visual comparison of names, explained in

earlier paragraph. In any case, these cannot be construed as allotment to

persons who have not applied in the issue.

6.4 Regarding difference in number of errors given by the noticee and those

given by NSDL / CDSL, the noticee had provided information of only such

cases, where rectification were carried out by it for reversal of wrong credits,

which was due to either wrong information provided by the investors in the

application or error at the noticee’s end due to data capture (again very

negligible compared to the volumes handled). It did not provide the data

wherein inadvertently shares were transferred twice into the same accounts

(582 nos.) by way of off-market transfer from the escrow account.

6.5 When there are hundreds of thousands of allottees, and when an investor

gets wrongly allotted or wrongly refunded, it is not possible to proactively

find out such cases unless either of the parties (one who has been deprived

or one who has wrongly received) complain. The noticee submitted that it

was not following a wrong validation process but due to volumes and time

constraints, sometimes some errors creep in purely due to the pressure on

human mind.

6.6 As a part of the then prevailing data capture process, PAN details of

Investors were captured from application forms. As long as PAN detail is

provided in the application forms, same was taken as correct and not

matched with PAN details as per depository data. Also, since PAN copy was

not attached with all application form, correctness of PAN details could not

be ascertained and hence such cases were not rejected by the noticee. In

case PAN was not available in application form, same was retrieved from

demat account (if available). Earlier PAN was not mandatory for application

up to ` 50000 but subsequently in November 2007 it was made mandatory

irrespective of amount. However, now, PAN is compulsory for all active

Page 7 of 25

demat accounts and accordingly where valid DP ID/Client ID is available in

application form, PAN details are drawn from depository data provided by

Depositories and hence this problem stands resolved as on date. In fact,

earlier, demat account could be operated as active account even without

PAN. Amendments were made in depository system by which without PAN

KYC, demat account was suspended for debit action. Rules were further

modified in October 2010 by which, without PAN KYC, both debit and credit

corporate action are not allowed.

6.7 Regarding multiple allotment to Applications with same PAN, the process

followed for elimination of multiple applications and providing PAN details in

the Application have been undergoing continuous refinement and only in

July 2007 (much after the period of Inspection), it was made mandatory to

provide for PAN details in the Application irrespective of the amount

involved. Hence to evaluate the allotment process in IPOs of prior date

based on subsequent developments is not proper. The noticee stated that

out of the instances highlighted in SEBI inspection report of 258 cases

reported, 234 cases had only one application above ` 50000.

Regarding Bank Schedules

6.8 Bank schedules were used only for the purpose of verification of amount

received against the application based on matching of Application No. and

Name of the investor. The cheque numbers were not verified nor scrutinized

by the noticee in the course of the processing since such verification is not

required to be carried out at the RTI’s end. It also should be noted that

within the given time frame and considering the huge volume of applications

handled and processed, it was very difficult to scan through all these details

and form any opinion. The capturing of wrong instrument number by the

banks, is an issue outside the noticee’s purview, and the noticee did not

possess any knowledge at the time of processing of any wrongdoing by the

banks.

Page 8 of 25

Regarding functioning as STA 6.9 Regarding the delay in processing of demat requests beyond 15 days the

noticee submitted that during the period of Inspection (i.e. January 2004 to

December 2006) it had handled in all 4,94,295 demat requests. As already

mentioned, there were many clients who were availing of only electronic

connectivity from the noticee and hence processing of demat requests in

such cases, was dependent on the companies and hence the same were

delayed which was not under its control. The surges in volumes of demat

requests received, depended on the volatility in the market prices of these

scrips which was quite high during the period of inspection. This period of

inspection also included the quarter July-September 2005, when due to the

devastating floods in Mumbai of 26th July, 2005 there were numerous cases

of delays in transit and loss of documents in transit, leading to such delays.

Most of the cases, where delays were beyond 30 days, it was mainly due to

the additional documentation required for variation in signatures. This was

more common in old companies, where shares have been held for a long

time. 13754 cases of demat requests, observed in the Inspection Report are

mainly due to one or more of the above reasons and it can be seen that this

amounts to hardly 2.75% of the total demat requests received during the

subject period. Out of the 6600 cases reported by the inspection team as

pending, 4039 requests were pertaining to companies, where the noticee

was providing only electronic connectivity. Further 1350 requests pertain to

companies, for whom services had been terminated but the companies had

not made alternate arrangement for RTA services. Thus it can be seen that

what were really pending was forming a very miniscule percentage of the

total volumes handled.

7. Subsequently, the noticee made an application for consent dated June 22,

2009. However, the High Powered Advisory Committee on Consent was of

the view that the proposal does not have to be considered under consent

terms and hence recommended that the case be rejected. The noticee was

intimated of the rejection of the consent application vide the SEBI letter

dated December 21, 2010.

Page 9 of 25

8. As requested by the noticee in its reply, a hearing notice dated January 20,

2011, granting a personal hearing to the noticee on February 09, 2011 was

served on the noticee. In response to the same, Mr. Jai Kishan Lakhwani,

Advocate, Mr. Paras K. Parekh, Advocate from J. Sagar Associates,

Advocates & Solicitors, Mr.S. Ramanujam, Managing Director and Mr. H.N.

Modi, Chief Operating Officer of the noticee appeared as Authorised

Representatives and requested for an inspection of documents and

materials relied upon by SEBI in order to make detailed submissions in reply

to the Show Cause Notice.

9. Subsequent to the inspection of documents, the noticee submitted a

detailed reply vide letter dated August 10, 2011 which, apart from reiterating

the submissions made in the previous reply, inter alia stated the following:

9.1 The entire inspection was carried out in January-February of 2007 and was

obviously based on regulatory guidelines and industry practices being

followed at that point of time. Obviously, the noticee also was following the

guidelines and industry wide practices prevalent and being followed at that

point of time. The various changes which have happened in the subsequent

period, themselves are sufficient indications to show that the entire process

was “evolving” based on the experiences and consequences faced by all

the players in the capital market. The noticee listed below some of the

amendments / changes which were brought about by SEBI in the

subsequent period (after the period of inspection) which will highlight these

point:

• Initially PAN was not mandatory for application up to ` 50000.

Subsequently it was made mandatory irrespective of application amount.

Also, earlier PAN was captured from application form and if not

available, same was retrieved from demat account (if available).

• Also, earlier, demat account could be operated as an active account

even without PAN. Later Amendments were made in Depository system

by which without PAN KYC, demat account was suspended for Debit

action. Rules were further modified as late in October 2010 through

which without PAN KYC, both Debit and Credit corporate action are not

allowed.

Page 10 of 25

• Till April 2010, Allotment process involved 3-way reconciliation involving

Bid file, application data file and Bank schedule file. In May 2010, SEBI

introduced a paradigm change in the process, which resulted in 2-way

reconciliation of Bid file and Bank schedule. Due to this, verification of

some of the fields on application form like, Age of the bidder,

Status(Minor/Major), signature of applicant on application form, Rubber

stamp of Corporate etc were made redundant for allotment processing

by Registrar. With this, even Name verification as per application and as

per depository data was removed, since Name was not available in Bid

file. Accordingly, as long as DP ID/Client ID/PAN as per bid file matches

with DP ID/Client ID/PAN in Depository system, credit corporate action is

effected without verification of applicant’s name.

• Earlier, for weeding out Multiple applications, different criterias were

applied. Through subsequent SEBI notification, PAN was made sole

criteria for determining Multiple applications.

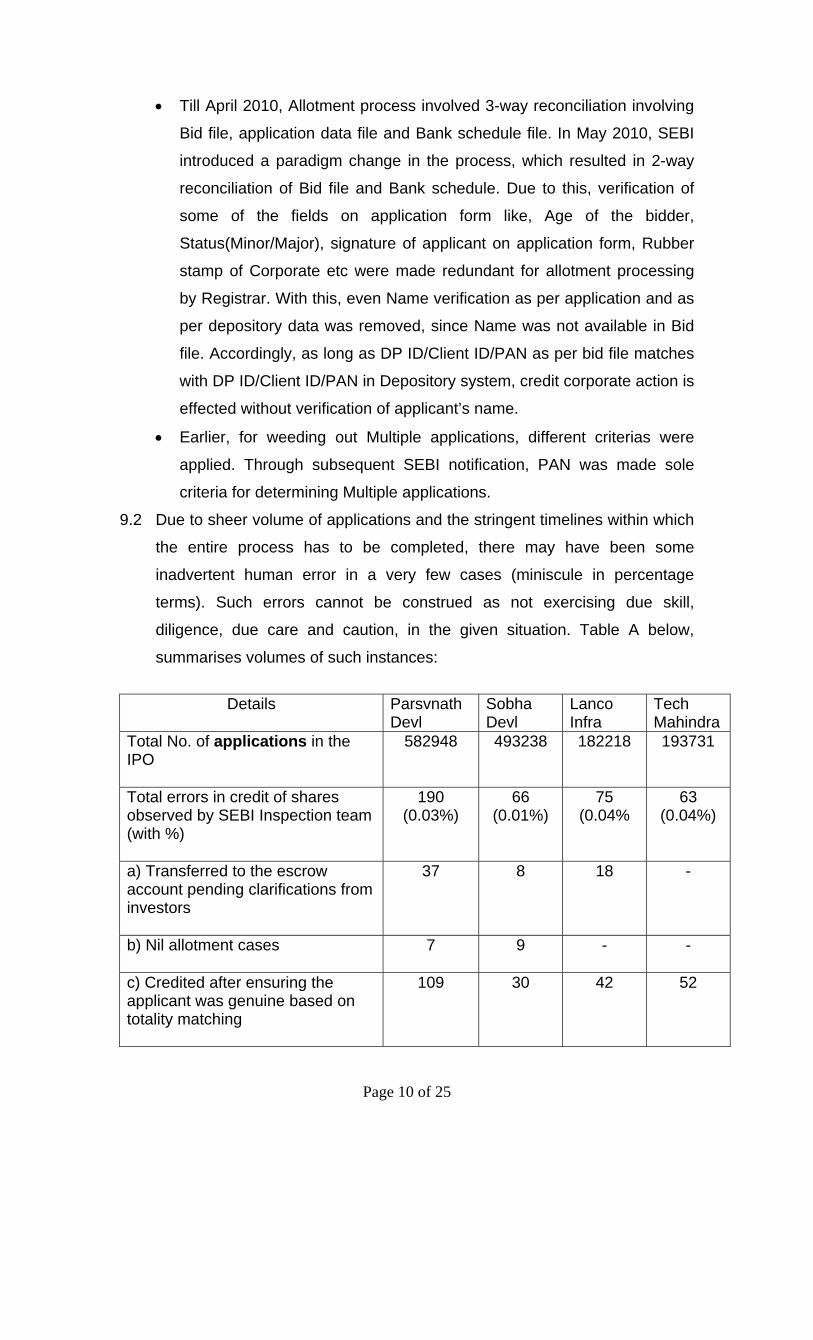

9.2 Due to sheer volume of applications and the stringent timelines within which

the entire process has to be completed, there may have been some

inadvertent human error in a very few cases (miniscule in percentage

terms). Such errors cannot be construed as not exercising due skill,

diligence, due care and caution, in the given situation. Table A below,

summarises volumes of such instances:

Details Parsvnath

Devl Sobha Devl

Lanco Infra

Tech Mahindra

Total No. of applications in the IPO

582948 493238 182218 193731

Total errors in credit of shares observed by SEBI Inspection team (with %)

190 (0.03%)

66 (0.01%)

75 (0.04%

63 (0.04%)

a) Transferred to the escrow account pending clarifications from investors

37 8 18 -

b) Nil allotment cases

7 9 - -

c) Credited after ensuring the applicant was genuine based on totality matching

109 30 42 52

Page 11 of 25

d) Wrong credits due to errors of data capture & later rectified (with %)

37 (0.006%)

19 (0.004%)

15 (0.008%)

11 (0.002%)

9.3 Proactively the noticee identified many of the problem cases for non receipt

of refund amount and shares and took prompt corrective actions. Some

such steps are as follows :

• In cases where the applicant has furnished incorrect Demat account

details in his application form because of which the beneficiary name

available with the Depository didn’t match with the IPO application form,

refunds for such investor was not sent through ECS but processed as

physical refund orders and sent to the address as captured from the

physical application forms. This ensured that investor’s refund is not held

up in ECS process due to mismatch of name/Bank account details.

• Shares allotted against application referred in pre-para above were

uploaded for credit through Corporate Action only after re-verification of

demat account and name with the Physical Application forms to

eliminate possibility of data capture error.

• Investor was approached over telephone and /or email, wherever such

information is available, to obtain correct demat account details for

crediting / uploading the shares to the correct account.

• In case telephone no. / email id is not available, then concerned

Depository participant was approached to verify beneficiary contact

details / demat account details with same available in the application

form.

• Periodic reminders were also sent to investors seeking details of correct

demat account.

• In case, refund order was returned as “undelivered”, and the address as

per application form was different from same as per depository records,

Refund order was redespatched to the address as per application form.

• In case, shares are credited to wrong beneficiary account, vigorous

follow up was done to recover the same and arrange credit to the correct

beneficiary account. In some cases, pending recovery, required shares

were purchased from the market and credited to correct beneficiary

account.

Page 12 of 25

• In case refund amount was credited to wrong beneficiary account under

ECS, efforts were made through sponsor bank to arrange for roll-back of

wrong credit to ensure that right beneficiary receives refund amount as

soon as possible. If required, the noticee interacted with the receiving

banker directly to arrange for roll-back of wrong credit. Simultaneously, it

also followed up with the wrong beneficiary through its branch offices for

refund of money.

9.4 During the period of Inspection, 458 cases have been observed to have

been delayed beyond the statutory period out of a total of 9479 requests for

issue of duplicate certificates. This is less than 5% of the total number of

cases. In the process of issue of duplicate certificates there are a number of

steps involved like ascertaining the genuineness of the investor as well as

the Share certificate claimed to have been lost, obtaining all the

documentation like indemnity, affidavit etc., release of advertisement in the

Gazette / press, approval of the Company’s Board/ Committee of Directors

(this is required in many cases) etc. All these activities take time and many

a time the delay is caused due to the delay in response from the investors

or delay in receipt of approval from the Company/ies.

9.5 Normally transfers were effected within the 30 days time limit as prescribed.

During the period under review a total of 2,17,861 transfers had been

received and processed, out of which 23,857 requests were duly processed

and dispatched beyond stipulated 30 days (i.e. about 11%). Further, over

75% of such delays were due to sending of notice to transferor to confirm

the transfer, due to variation in signature, with a view to eliminate chances

of improper / fraudulent transfer. Considering the 21 days’ time given in

such notices, it becomes impossible to dispatch the transferred certificates

within 30 days. Further, quite a few client companies insist on authorizing

the endorsements on share certificates for transfer, which contributes to

further delays. Efforts are being made to convince such companies to

delegate the authority to RTA.

9.6 Normally the sequence of activities for demat request processing, updating

of the back office is carried out first and immediately thereafter, the

electronic file is forwarded to the Depository section for release of the same.

Page 13 of 25

Most of the days, this process is concluded before end of the day. However

on certain days due to various reasons like, power, unavailability of the

Depositories’ system, unforeseen server problem, high traffic of BOD

resulting in overflow to the next day etc., and this step may not get

completed on the same day resulting in difference in capital as per the RTA

system and depositories. In the 214 cases observed by the Inspection team,

actual differences were seen only in 61 cases and in 50 of the 61 cases the

difference was due to the late release of the demat / remat request to the

Depository system. It is confirmed that reconcilitiation activity is religiously

carried out on a daily basis and action is taken immediately for any

discrepancies observed therein.

9.7 During the period under inspection, there were in all letters received from

investors, out of which 4981 letters have been observed to be redressed

beyond the prescribed period of one month. While the normal practice is to

reply all letters within the one month period, there are certain reasons due to

which the delay becomes inevitable. The Inspection team had verified a

sample of 150 such cases and the breakup of reasons for delay in these

150 cases is as under:

• In case of 101 complaints, the companies were taken over by the

noticee within the previous 3-4 month period and more time was

required to retrieve the old records of such companies which were

received from other Registrars. Detailed list of such cases has been

provided in the Reply to the Inspection Report.

• Further 38 cases were pertaining to non-receipt of dividend. To resolve

these complaints, duplicate dividend warrants had to be obtained from

the Dividend banker, which had caused a delay, on the part of the

Company / Bankers.

• Thus it can be seen that over 90% of such delays were due to reasons

beyond the noticee’s control.

9.8 The Inspection team visited during 2nd half of January, 2007. SEBI, vide its

circular no. : MIRSD/DPS III /Cir-01/07 dated 22-01-2007, directed all RTAs

to have a dedicated e-mail id. Prior to that the noticee had

[email protected] was a dedicated e-mail id for the purpose of

Page 14 of 25

investors and this was highlighted in all communications to the investors of

client companies. Immediately on receipt of the abovementioned circular, 2

separate dedicated email ids were created as:

[email protected], [email protected].

This was also informed to SEBI vide the letter dated February 02, 2007.

Thus it can be seen that the Circular was immediately complied with and

there was no question of non-compliance.

9.9 The noticee has independently verified the details of entries keyed in from

the Applications through various electronic processes and ‘exceptions’

checking. The processes and timelines for Dematerialisation,

Rematerialisation, issue of duplicates, transfer of certificates, handling of

investor correspondence etc. are all well-tested and refined / fine-turned

over the years. The noticee has been putting in best efforts to ensure

timelines are fully met in all cases, inspite of which certain delays do creep

in due to factors beyond its control.

9.10 Based on the various observations and suggestion of the SEBI inspection

team, the noticee had made quite a few improvements / refinements in its

processes (this is a continuous process) which is in the direction of better

service to the investors.

9.11 The noticee further submitted that it was also the Back Office Service

Provider for SEBI, Mumbai.

10. In view of the same, the noticee requested SEBI to condone the minor

errors / discrepancies which have occurred in its processing and dispose of

the subject Show Cause Notice. The noticee has been following all the

statutory and regulatory guidelines prevalent at that point of time and had

been constantly improvising in the processes on its own as well as based on

regulatory changes.

11. Vide hearing notice dated August 29, 2011 an opportunity of hearing was

granted to the noticee on September 09, 2011. The noticee requested for an

adjournment of the same since the communication reached the noticee at a

Page 15 of 25

short notice. A final hearing notice dated September 26, 2011 was served

on the noticee granting it an opportunity of hearing on October 12, 2011.

12. In response to the personal hearing notice, the noticee vide its letter dated

October 07, 2011 authorised Shri Jai Kishan Lakhwani, Advocate,Shri

Paras K. Parekh, Advocate from J. Sagar Associates, Advocates &

Solicitors, Shri Kishor P. Thakkar, Director of the noticee, Shri Sanjeev M.

Nandu, Director-Operations and Compliance Officer of the noticee and Shri

Haren N. Modi, Chief Operating Officer of the noticee to appear as the

Authorised Representatives (‘AR’s) and accordingly the aforesaid persons

appeared. The ARs reiterated the submissions of the noticee made in its

reply dated June 19, 2009 and August 10, 2011. The ARs submitted that at

the time of inspection, PAN Number was not a mandatory parameter for

application and the bid data received by the RTI from the stock exchange

was in many cases insufficient and the noticee had exercised all possible

due diligence in matching the bid data, data from the application forms and

the data received from the banks. While data entry/ capture some human

error occurred which is very minuscule in percentage and the same may be

condoned. The ARs submitted that during the inspection approximately 19

lakh applications had been considered and the percentage of error on the

noticee’s part was miniscule i.e. 1.25%. Regarding dummy instrument

numbers, the ARs submitted that since this data was provided by the banks

thus the noticee had no control over it. Regarding the issue of allotment of

shares to the wrong beneficiary account or refund to wrong accounts, the

ARs submitted that in such cases a continuous/ vigorous follow up was

undertaken and in some cases where the recovery of the shares took time

the noticee had purchased the shares from the market and credited to the

correct beneficiary account. The cost of the same had been borne by the

noticee in those cases and while following this procedure the noticee had

also incurred losses in some cases. The same procedure was also followed

by the noticee in case of refunds. The ARs undertook to provide documents

in support of this submission. Regarding the functioning as STA the ARs

submitted that delay in demat/ remat of shares had occurred since in some

cases only electronic connectivity was being provided by the noticee and

the dematting/ rematting had to be done at the company’s end, which was

Page 16 of 25

delayed and this was beyond the noticee’s control. Moreover, certain delays

had also taken place due to the Mumbai floods in 2005. The ARs submitted

that in the present case only minor irregularities had taken place in the

functioning of the noticee as RTI/STA and may be condoned. The ARs

undertook to submit documentary evidence in support of their various

submissions/ claims. The noticee was granted time till October 24, 2011 to

submit documents and to make additional submissions, if any.

13. Subsequent to the personal hearing, vide letter dated November 02, 2011

the noticee made additional submissions which inter alia stated that:

13.1. There was erroneous upload of credit of one lot of 572 shares (inadvertently

referred as 582 nos. in the Reply) in respect of 57 cases of IPO of Shobha

Developers Ltd. The error was immediately rectified through a debit

corporate action. Further, rectification through corporate action for 35662

shares pertaining to two different schemes of UTI Infrastructure Fund was

carried out. The noticee submitted letter dated November 28, 2006 sent to

NSDL seeking rectification as proof of the same.

13.2. In cases where investors grievances were caused due to human error of

omission/commission at the noticee’s end, it had arranged to compensate

the investor at its cost, though these were genuine human errors. Details of

some of such instances were provided by the noticee. The noticee had

purchased 444 shares of Techmahindra at a cost of ` 411,550.61, 596

shares of Parsvanath Deveopers at ` 257,739.97, 10 shares of Shobha

developers and 86 shares of Lanco Infrantech Ltd. at ` 38,635.

13.3. The noticee also submitted copies of periodic reminders sent to investors

seeking correct demat accounts details in order to credit the allotted shares

to the correct demat account.

13.4. The noticee provided client-wise details of 13,754 instances of delayed

demat/remat request processing and submitted that out of these instances,

in 6,600 instances, the noticee was either only depository connectivity

provider or it had already terminated client services and hence these delays

were beyond its control and therefore not attributed to it. Single erroneous

Page 17 of 25

demat request confirmation of 2,949 shares with lock-in date pertained to

DCB Bank which was subsequently rectified. The noticee also provided the

company-wise details of 23,857 cases of delayed transfers

CONSIDERATION OF EVIDENCE AND FINDINGS

14. I have taken into consideration the facts and circumstances of the case and

the material made available on record.

15. The observations in the IR against the noticee have been detailed in

paragraph 4 and it is alleged that the noticee had violated the provisions as

stated in paragraph 5.

Functioning as RTI:

16. The observations against the noticee regarding its functioning as RTI

included failure to verify details in physical application, wrong allotment of

shares, multiple allotments, etc., which have been stated in detail in

paragraph 4.1 to 4.6. Moreover, the IR has observed that the information

given to the Inspection team by the noticee regarding the number of such

instances was not matching with the information obtained from the

Depositories i.e., NSDL/CDSL. Further, the cases furnished by the

Inspection Report had not been identified by the noticee through its

procedures, but because of investor complaints.

17. The noticee’s reply has been elaborated in paragraph 6.1 to 6.7. The

noticee has submitted that it was carrying out an elaborate verification

process of all entries and the details have been provided in para 6.1 which

includes due to sheer volumes and tight timelines, few errors had occurred

due to inadvertent human error. The noticee has submitted that credits to

persons who had not applied in the public issue arose because, the investor

ID captured was matching with another valid ID of a different person (either

due to wrong filling up in the application form by the investor, illegible

handwriting or due to wrong data entry), these are some of the exception

cases, which missed being found out at the time of visual comparison of

names.

Page 18 of 25

18. Regarding difference in number of errors given by the noticee and those

given by NSDL / CDSL, the noticee stated that it had provided information of

only such cases, where rectification was carried out by it for reversal of

wrong credits, which was due to either wrong information provided by the

investors in the application or error at its end due to data capture. It did not

provide the data wherein inadvertently shares were transferred twice into

the same accounts (572 nos.) by way of off-market transfer from the escrow

account. The noticee has submitted that as a part of the then prevailing data

capture process, PAN details of Investors were captured from application

forms, since PAN copy was not attached with all application forms,

correctness of PAN details could not be ascertained. Earlier PAN was not

mandatory for application up to ` 50,000 but subsequently in November

2007 it was made mandatory irrespective of amount. The noticee has stated

that out of the instances highlighted in SEBI inspection report of 258 cases

reported, 234 cases had only one application above ` 50000. In its letter

dated November 02, 2011 the noticee has submitted a client wise detail

regarding wrong allotment, allotment due to client error, due to the noticee’s

error, copies of follow-up letters sent to the clients, etc. However, it has

been noted that the noticee has not submitted any proof of dispatch/

delivery of such correspondences.

19. The noticee has accepted that certain discrepancies had taken place in the

credit of shares to wrong entity who had not applied in the IPO/ allotment to

entity whose details were not matching / transfer of refund to wrong entities,

etc.. The noticee has stated that in such cases it had followed up the matter

and ensured that the correct entity receives the amount/ shares, sometimes

the noticee even bought the shares from the market and credited it to the

correct beneficiary account as detailed in para 13.2 .

20. From the material submitted by the noticee, I have noted that in the IPO of

Gateway Distriparks Ltd. the total percentage of grievances regarding wrong

allotment/ wrong data entry, etc. as compared to the total number of

applications wherein the redressal had taken place within 90 days was

1.15% out of which 52.69% was due to error at the noticee’s end. Similarly,

in the IPOs of Tech Mahindra Ltd., Parsvnath Developers Ltd., Sobha

Page 19 of 25

Developers Ltd., Lanco Infratech Ltd., Amar Remedies Ltd. and FCS

Software Ltd. the percentage of similar grievances/ discrepancies compared

to the total number of applications where the redressal had taken place

within 90 days were 0.85%, 1.96%, 0.96%, 1.56%, 0.57% and 0.46%

respectively and where redressal had taken place after 90 days were

.0046%, .0966%, .0016%, .1114%, .0019% and 0% respectively.

Bank Schedules

21. Regarding dummy numbers provided in the column for instrument numbers

in the bank schedule, the noticee has stated that bank schedules were used

only for the purpose of verification of amount received against the

application based on matching of Application No. and Name of the investor.

The cheque numbers were not verified nor scrutinized by the noticee in the

course of the processing since such verification is outside the purview of

RTI as stated in para 6.8.

Functioning as STA:

22. Regarding its functioning as STA, it has been alleged that the noticee had

failed to dematerialize and rematerialize securities in the prescribed time,

made erroneous confirmations of demat request as well as delayed issue of

duplicate shares, failed to process the transfer of shares within the

prescribed time, delayed in processing of demat requests beyond 15 days

of receipt and failed to reconcile its records on a daily basis as stipulated

under Regulation 55 of the D&P Regulations.

23. The noticee’s reply regarding the delay in processing demat/ remat requests

has been stated in para 6.9. The noticee has stated that out of the 13,754

instances of delayed demat/remat request in 6,600 instances, it was either

only depository connectivity provider or it had already terminated client

services and hence these delays were beyond its control. Out of the total

4,94,295 requests handled by the noticee during the period of inspection the

number of instances where there was a delay in processing were 7154

instances (1.44%).

Page 20 of 25

24. Regarding issue of duplicate share certificates and transfers the noticee’s

reply has been stated in paras 8.4 and 8.5., the noticee has mainly taken

the plea that delays had occurred in a very few cases and most of the

delays had taken place because of the verification procedure to be followed

before effecting these transfers/ issue of duplicate share certificates. The

noticee has argued that the percentage of application where delays had

occurred, compared to the total number of applications handled by the

noticee was around 11%. I have noted that there were 23,857 cases of

delayed transfers and the noticee has made a general defense that in most

cases the delays were due to reasons beyond its control. I have noted that

in five scrips where the number of such instances were more than 1000 are

as given below:

• GTC Industries Ltd.: 1420 instances

• Gujarat Sidhee Cement Ltd.: 1418 instances

• IndusInd Bank Ltd.: 3476 instances

• International Hometex Ltd.: 1582 instances

• SM Dyechem Ltd.: 2644 instances.

However, the noticee has not provided break-up as to the reasons for delay.

Further, I have noted that the noticee has not provided supporting

documents such as proof of dispatch/ delivery of seller notice etc.

25. It has been alleged that the noticee had failed to reconcile its records on a

daily basis as stipulated under Regulation 55 of the D&P Regulations. The

noticee, in its defense has stated that normally the reconciliation of the

noticee’s record was done daily and this process was concluded before end

of the day. However on certain days due to various reasons like, power,

unavailability of the Depositories’ system, unforeseen server problem, high

traffic of BOD resulting in overflow to the next day etc., and this step may

not get completed on the same day resulting in difference in capital as per

the RTA system and depositories. As per the material made available by the

noticee there were 61 such instances wherein the noticee had not

reconciled its records on a daily basis.

Page 21 of 25

Redressal of investor grievances:

26. a. Regarding the delay in redressal of investor grievances, the noticee

has stated that for over 90% of such delays were due to reasons

beyond its control. During the period under inspection, there were in all

grievances received from investors, out of which 4,981 greivances had

been observed to be redressed beyond the prescribed period of one

month. The noticee has submitted that while the normal practice is to

reply to all letters within the one month period, there were certain

reasons due to which the delay becomes inevitable. The Inspection

team had verified a sample of 150 such cases and the breakup of

reasons for delay in these 150 cases were as under:

• In case of 101 complaints, the companies were taken over by the

noticee within the previous 3-4 month period and more time was

required to retrieve the old records of such companies which were

received from other Registrars.

• Further 38 cases were pertaining to non-receipt of dividend. To

resolve these complaints, duplicate dividend warrants had to be

obtained from the Dividend banker, which had caused a delay, on

the part of the Company / Bankers.

b. Regarding the allegation that the noticee did not have a dedicated e-

mail ID for redressal of investor grievances, the noticee’s reply has

been stated in para 9.8 and I accept the same.

27. I have taken into consideration the facts and circumstances of the case and

the material made available on record. The allegations against the noticee

in the SCN were that it had violated the provisions mentioned in para 5.

I have observed that in functioning as RTI, the noticee itself has accepted

that certain discrepancies had taken place in the credit of shares to wrong

entity who had not applied in the IPO/ allotment to entity whose details were

not matching / transfer of refund to wrong entities, etc..

28. In its functioning as STA the percentage of delays in processing of demat/

remat request were approximately 1.44%. Regarding delays in transfers/

Page 22 of 25

issuance of duplicate share certificates the notice has accepted that delays

had occurred mainly due to issuance of seller notices. Regarding delays in

redressal of investor grievances the noticee has mainly stated that delays

had occurred in only a miniscule number of cases.

29. In view of the above discussions/ admissions by the noticee, it may be

concluded that the noticee has not complied with the following provisions:

i. Section 14 (3) of the Depositories Act, 1996

ii. Regulation 54(5) and 55 of D& P Regulations;

iii. Clauses 2, 3, 5 , 21 and 27 of the Code of Conduct prescribed under

Regulation 13 of the RTI & STA regulations;

iv. SEBI circular- RRTI Circ. No. 1(93-94) dated November 05, 1993.

The texts of the provisions are as follows: Depositories Act, 1996 “14.(3) Every issuer shall, within thirty days of the receipt of intimation from the

depository and on fulfilment of such conditions and on payment of such fees as may be specified by the regulations, issue the certificate of securities to the beneficial owner or the transferee, as the case may be.”

SEBI (Depositories and Participants) Regulations, 1996 “54.(5) Within 15 days of receipt of the certificate of security from the participant

the issuer shall confirm to the depository that securities comprised in the said certificate have been listed on the stock exchange or exchanges where the earlier issued securities are listed and shall also after due verification immediately mutilate and cancel the certificate of security and substitute in its record the name of the depository as the registered owner and shall send a certificate to this effect to the depository and to every stock exchange where the security is listed : Provided that in case of unlisted companies the condition of listing on all the stock exchanges where earlier issued shares are listed, shall not be applicable.”

Reconciliation. “55. The issuer or its agent shall reconcile the records of dematerialized

securities with all the securities issued by the issuer, on a daily basis: ….”

SEBI (Registrars to an Issue and Share Transfer Agents) Regulations, 1993

Code of Conduct 2. A Registrar to an Issue and Share Transfer Agent shall fulfill its obligations in

a prompt, ethical and professional manner. 3. A Registrar to an Issue and Share Transfer Agent shall at all times exercise

due diligence, ensure proper care and exercise independent professional judgment.

Page 23 of 25

5. A Registrar to an Issue and Share Transfer Agent shall always endeavor to ensure that - a. inquiries from investors are adequately dealt with; b. grievances of investors are redressed without any delay; c. transfer of securities held in physical form and confirmation of

dematerialisation / rematerialisation requests and distribution of corporate benefits and allotment of securities is done within the time specified under any law .

….. 21. A Registrar to an Issue and Share Transfer Agent shall endeavor to resolve

all the complaints against it or in respect of the activities carried out by it as quickly as possible.”

Moreover, the noticee has also not complied with SEBI circular- RRTI Circ.

No. 1(93-94) dated November 05, 1993.which imposes a liability on the RTI

to take proper care and evolve a suitable system whereby multiple

applications can be weeded out and eliminated and the instances of multiple

applications should be brought to the notice of the Companies (Issuers) as

also the lead managers for necessary action.

30. Further, I have noted that Clause 27 of the Code of Conduct under

Regulation 13 of the RTI & STA Regulations will not apply in this case since

it deals with STA developing its internal Code of Conduct. 31. Thus, it can be concluded that the noticee has failed to comply with the

provisions mentioned in para 29 above. The failure on the noticee’s part

attract penalty under the provisions given below SEBI Act, 1996:

“15C. Penalty for failure to redress investors' grievances.- If any listed

company or any person who is registered as an intermediary, after having been called upon by the Board in writing, to redress the grievances of investors, fails to redress such grievances within the time specified by the Board, such company or intermediary shall be liable to a penalty of one lakh rupees for each day during which such failure continues or one crore rupees, whichever is less.”

“15HB: Penalty for contravention where no separate penalty has been

provided.- Whoever fails to comply with any provision of this Act, the rules or the regulations made or directions issued by the Board thereunder for which no separate penalty has been provided, shall be liable to a penalty which may extend to one crore rupees.”

“19C. Penalty for failure to redress investors' grievances.

If any depository or participant or any issuer or its agent or any person, who is registered as an intermediary under the provisions of section 12 of the Securities and Exchange Board of India Act, 1992, after having been called upon by the Board in writing, to redress the grievances of the

Page 24 of 25

investors, fails to redress such grievances within the time specified by the Board, such depository or participant or issuer or its agents or intermediary shall be liable to a penalty of one lakh rupees for each day during which such failure continues or one crore rupees, whichever is less.”

“19D. Penalty for delay in dematerialisation or issue of certificate of

securities. If any issuer or its agent or any person, who is registered as an intermediary under the provisions of section 12 of the Securities and Exchange Board of India Act, 1992 (15 of 1992), fails to dematerialise or issue the certificate of securities on opting out of a depository by the investors, within the time specified under this Act or regulations or bye-laws made thereunder or abets in delaying the process of dematerialisation or issue the certificate of securities on opting out of a depository of securities, such issuer or its agent or intermediary shall be liable to a penalty of one lakh rupees for each day during which such failure continues or one crore rupees, whichever is less.”

“19G. “Penalty for contravention where no separate penalty has been provided. Whoever fails to comply with any provision of this Act, the rules or the regulations or bye-laws made or directions issued by the Board thereunder for -which no separate penalty has been provided, shall be liable to a penalty which may extend to one crore rupees.”

32. In this regard, the provisions of Section 15J of the SEBI Act and Rule 5 of

the Rules require that while adjudging the quantum of penalty, the

adjudicating officer shall have due regard to the following factors namely;

a. the amount of disproportionate gain or unfair advantage wherever

quantifiable, made as a result of the default

b. the amount of loss caused to an investor or group of investors as a

result of the default

c. the repetitive nature of the default

33. Considering all of the above, I hereby impose a penalty of ` 1,50,000/-

(Rupees One Lakh Fifty Thousand Only) on the noticee under Section 15 C

and 15HB of the SEBI Act, 1992 and ` 1,50,000/- (Rupees One Lakh Fifty

Thousand Only) under Section 19C, 19 D and 19G of the Depositories Act,

1996, which is appropriate in the facts and circumstances of the case.

Page 25 of 25

ORDER 34. In exercise of the powers conferred under Section 15 I of the Securities and

Exchange Board of India Act, 1992, and Rule 5 of Securities and Exchange

Board of India (Procedure for Holding Inquiry and Imposing Penalties by

Adjudicating Officer) Rules, 1995, I hereby impose a consolidated penalty of

` 3,00,000/- (Rupees Three Lakh Only) on the noticee in terms of the

provisions of 15 C and 15HB of the SEBI Act, 1992 and Section 19G of the

Depositories Act, 1996, for the violation of the provisions of SEBI Act, 1992,

Depositories Act, 1996, SEBI (Registrars to an Issue and Share Transfer

Agents) Regulations, 1993 and SEBI (Depositories and Participants)

Regulations, 1996. In the facts and circumstances of the case, I am of the

view that the said penalty is commensurate with the violations committed by

the noticee.

35. The penalty shall be paid by way of Demand Draft drawn in favour of “SEBI

– Penalties Remittable to Government of India” payable at Mumbai within 45

days of receipt of this order. The said demand draft shall be forwarded to

Deputy general Manager, MIRSD, SEBI.

36. In terms of the provisions of Rule 6 of the Securities and Exchange Board of

India (Procedure for Holding Inquiry and Imposing Penalties by Adjudicating

Officer) Rules 1995, copies of this order are being sent to Link Intime India

Pvt. Ltd., (formerly known as Intime Spectrum Registry Ltd.), Registrar to an

Issue and Share Transfer Agent, (SEBI Registration No. INR000003761)

and also to the Securities and Exchange Board of India, Mumbai.

Place: Mumbai D. RAVI KUMAR CHIEF GENERAL MANAGER &

Date: February 22, 2012 ADJUDICATING OFFICER

![SECURITIES AND EXCHANGE BOARD OF INDIA [ADJUDICATION … · securities and exchange board of india [adjudication order no. ak/ao- 7-11 /2017] _____ under section 15-i of securities](https://img.pdfslide.us/doc/110x75/5ea030364416c9485e57e911/securities-and-exchange-board-of-india-adjudication-securities-and-exchange-board.jpg)

![Securities and Exchange Board of India Act, 1992 · 1 Securities and Exchange Board of India Act, 1992 [As amended by the Securities Laws(Amendment) Act, 2014] SECTIONS CHAPTER I](https://img.pdfslide.us/doc/110x75/5b61bfa47f8b9a40488cb707/securities-and-exchange-board-of-india-act-1992-1-securities-and-exchange-board.jpg)