Embed Size (px)

Citation preview

Trade, services and employmentPolicy panel: The Role of Services Trade and Policy for Employment

Geneva, 26 November 2015

UNCTAD

Mina MashayekhiHead

Trade Negotiations & Commercial Diplomacy Branch

Workshop on Employment Effects of Services Trade Reform

2

Lessons learned from the Trade, Employment and Sustainable Development meeting organised by UNCTAD, October 2015

• Role of services economy and trade

• Policy options

• Case-study Senegal

• Case-study South Africa

• UNCTAD toolkit

Outline

3

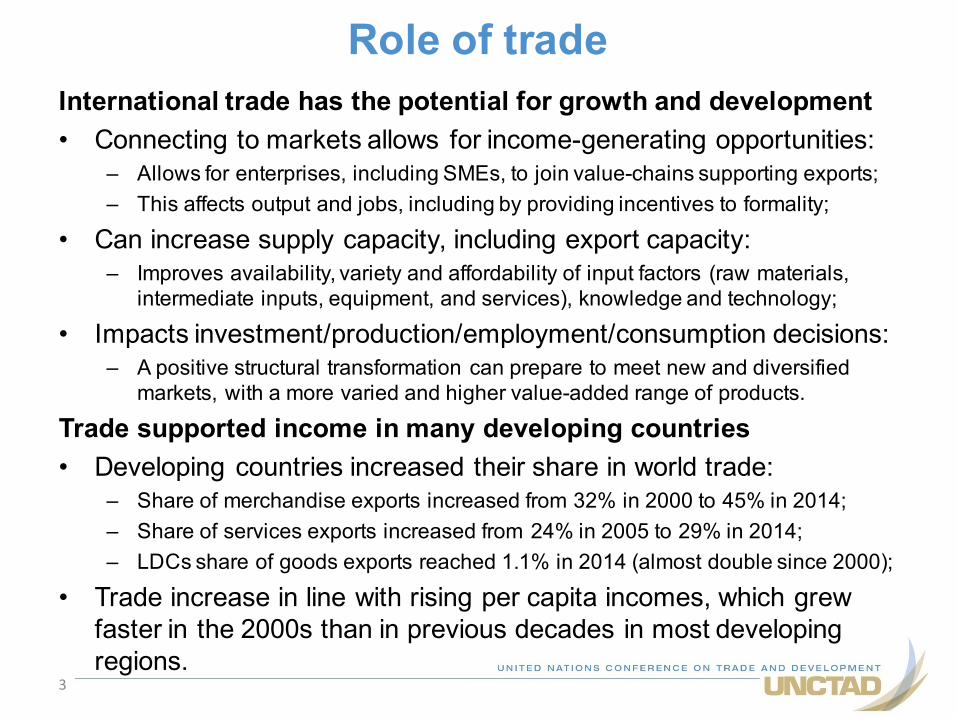

International trade has the potential for growth and development• Connecting to markets allows for income-generating opportunities:

– Allows for enterprises, including SMEs, to join value-chains supporting exports;;– This affects output and jobs, including by providing incentives to formality;;

• Can increase supply capacity, including export capacity:– Improves availability, variety and affordability of input factors (raw materials, intermediate inputs, equipment, and services), knowledge and technology;;

• Impacts investment/production/employment/consumption decisions:– A positive structural transformation can prepare to meet new and diversified markets, with a more varied and higher value-added range of products.

Trade supported income in many developing countries• Developing countries increased their share in world trade:

– Share of merchandise exports increased from 32% in 2000 to 45% in 2014;;– Share of services exports increased from 24% in 2005 to 29% in 2014;;– LDCs share of goods exports reached 1.1% in 2014 (almost double since 2000);;

• Trade increase in line with rising per capita incomes, which grew faster in the 2000s than in previous decades in most developing regions.

Role of trade

4

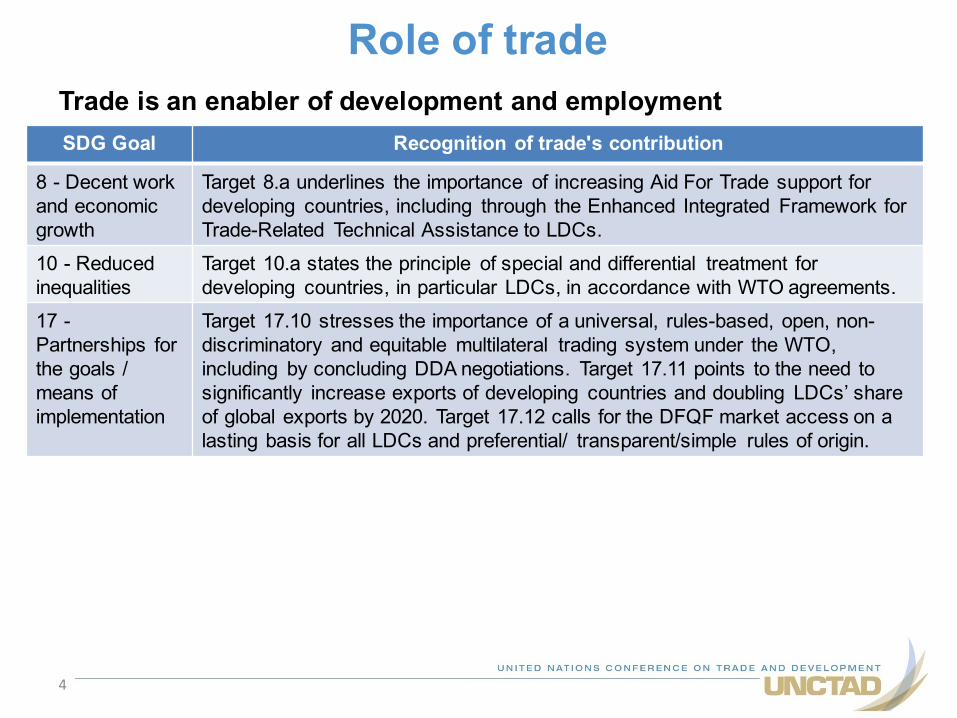

Trade is an enabler of development and employment

Role of trade

SDG Goal Recognition of trade's contribution

8 - Decent work and economic growth

Target 8.a underlines the importance of increasing Aid For Trade support for developing countries, including through the Enhanced Integrated Framework for Trade-Related Technical Assistance to LDCs.

10 - Reduced inequalities

Target 10.a states the principle of special and differential treatment for developing countries, in particular LDCs, in accordance with WTO agreements.

17 -Partnerships for the goals / means of implementation

Target 17.10 stresses the importance of a universal, rules-based, open, non-discriminatory and equitable multilateral trading system under the WTO, including by concluding DDA negotiations. Target 17.11 points to the need to significantly increase exports of developing countries and doubling LDCs’ share of global exports by 2020. Target 17.12 calls for the DFQF market access on a lasting basis for all LDCs and preferential/ transparent/simple rules of origin.

5

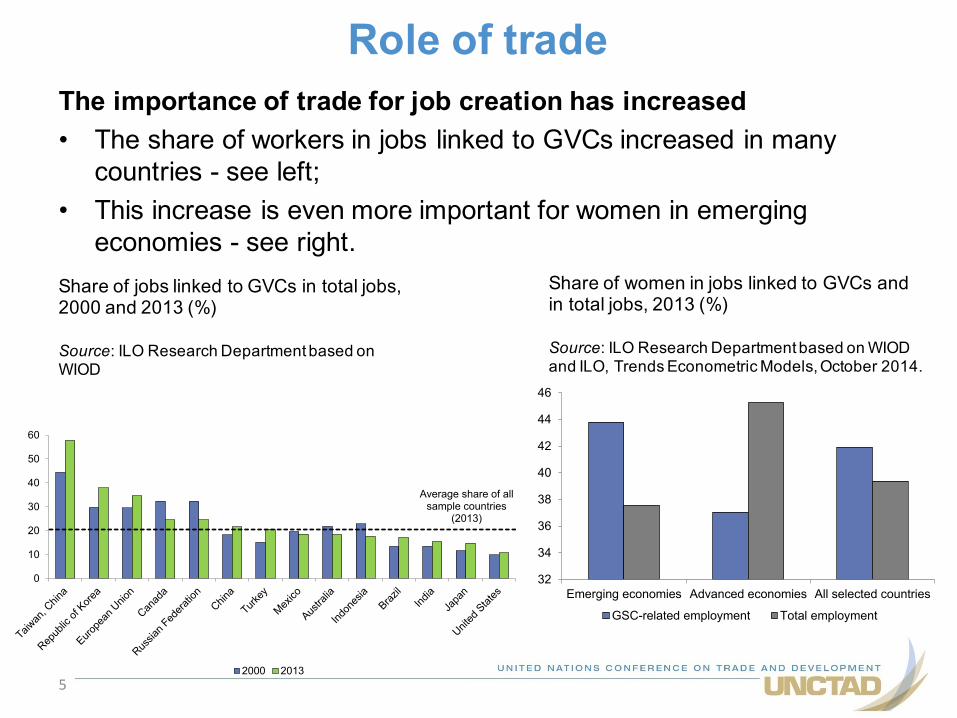

The importance of trade for job creation has increased• The share of workers in jobs linked to GVCs increased in many countries - see left;;

• This increase is even more important for women in emerging economies - see right.

Role of trade

Share of jobs linked to GVCs in total jobs, 2000 and 2013 (%)

Source: ILO Research Department based on WIOD

Average share of all sample countries

(2013)

0

10

20

30

40

50

60

2000 2013

32

34

36

38

40

42

44

46

Emerging economies Advanced economies All selected countries

GSC-related employment Total employment

Share of women in jobs linked to GVCs and in total jobs, 2013 (%)

Source: ILO Research Department based on WIOD and ILO, Trends Econometric Models, October 2014.

6

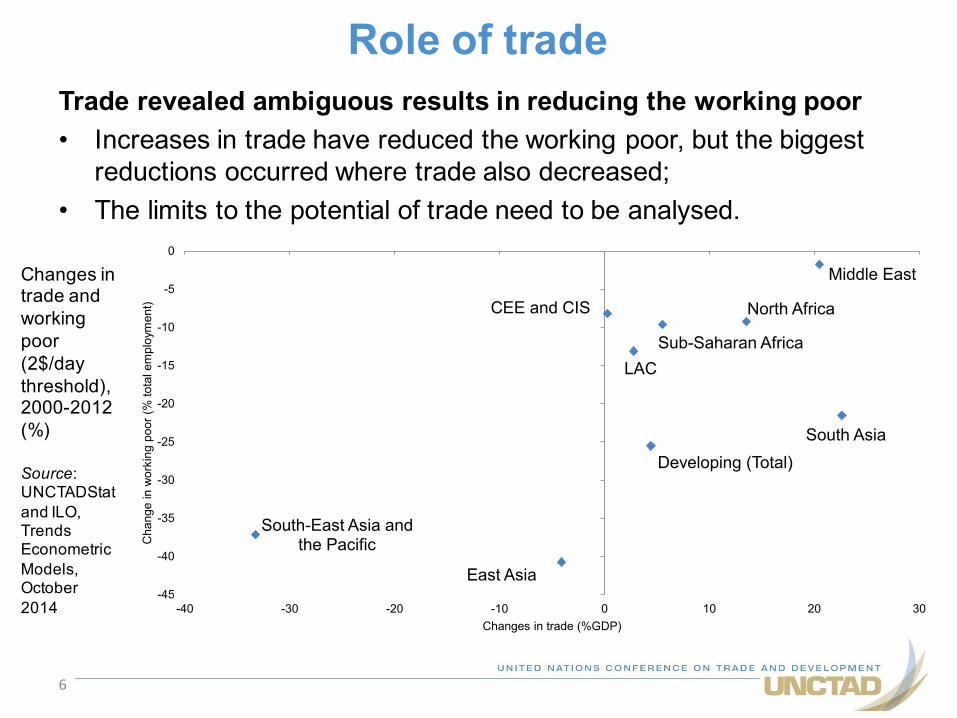

Trade revealed ambiguous results in reducing the working poor• Increases in trade have reduced the working poor, but the biggest reductions occurred where trade also decreased;;

• The limits to the potential of trade need to be analysed.

Role of trade

East Asia

South-East Asia and the Pacific

Developing (Total)South Asia

Sub-Saharan AfricaLAC

North AfricaCEE and CIS

Middle East

-45

-40

-35

-30

-25

-20

-15

-10

-5

0

-40 -30 -20 -10 0 10 20 30

Change in working poor (% total employment)

Changes in trade (%GDP)

Changes in trade and working poor (2$/day threshold), 2000-2012 (%)

Source: UNCTADStatand ILO, Trends Econometric Models, October 2014

7

Slow pace of trade expansion so far• Slow trade expansion (3.2% in 2014) reflects the slow pace of the global economy (3.2% in 2014):– Stagnation in major economies and economic slowdown in emerging economies contribute to weak global demand (China accounts for 1/3 of the slowdown in non-OECD import volume growth in 2014/2015);;

• And there is a decline in trade responsiveness to output growth:– Ratio of world trade growth to world output growth was 2:1 before the crisis and only 1:1 in 2012-2014. Among the possible reasons is the deceleration of GVCs trade, as major players increasingly source inputs domestically;;

– China is rebalancing its economy from infrastructure investment and manufacturing to services and consumption, reducing its role on GVCs and its import intensity, affecting trade flows and commodity prices.

Volatility affects trade and its development potential• Fluctuation in exchange rates affect export competitiveness:• Dropping prices worsen terms of trade in commodity-exporters;;• The combined effect of exchange rates and energy prices offset the increase in world trade vol. (decrease in unit values since Apr 2011).

Limits to the potential of trade

8

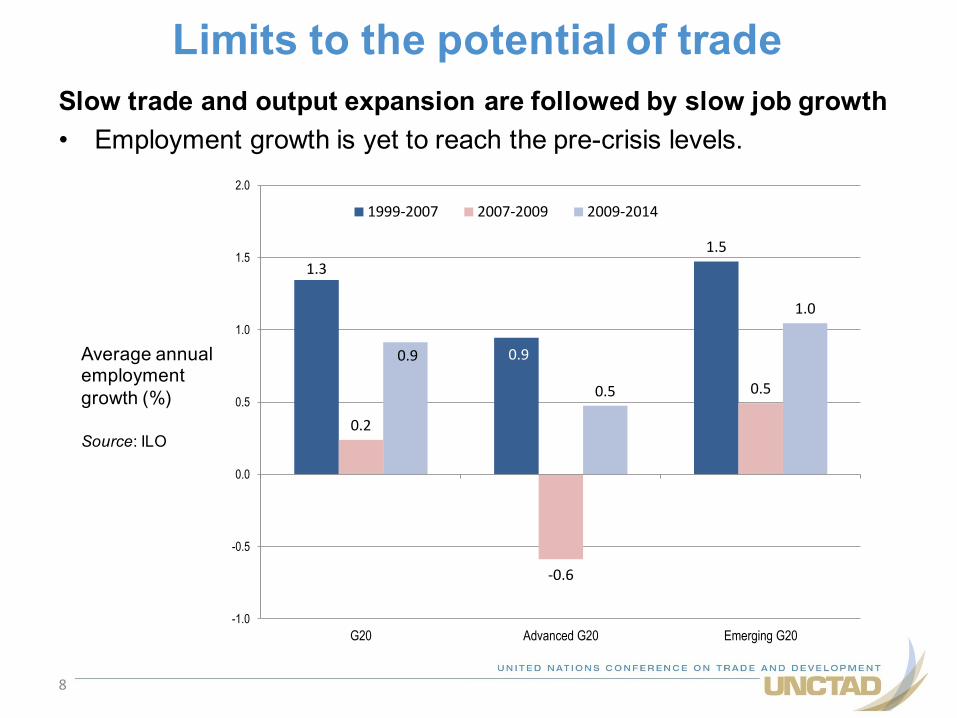

Slow trade and output expansion are followed by slow job growth• Employment growth is yet to reach the pre-crisis levels.

Limits to the potential of trade

1.3

0.9

1.5

0.2

-‐0.6

0.5

0.9

0.5

1.0

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

G20 Advanced G20 Emerging G20

1999-‐2007 2007-‐2009 2009-‐2014

Average annual employment growth (%)

Source: ILO

9

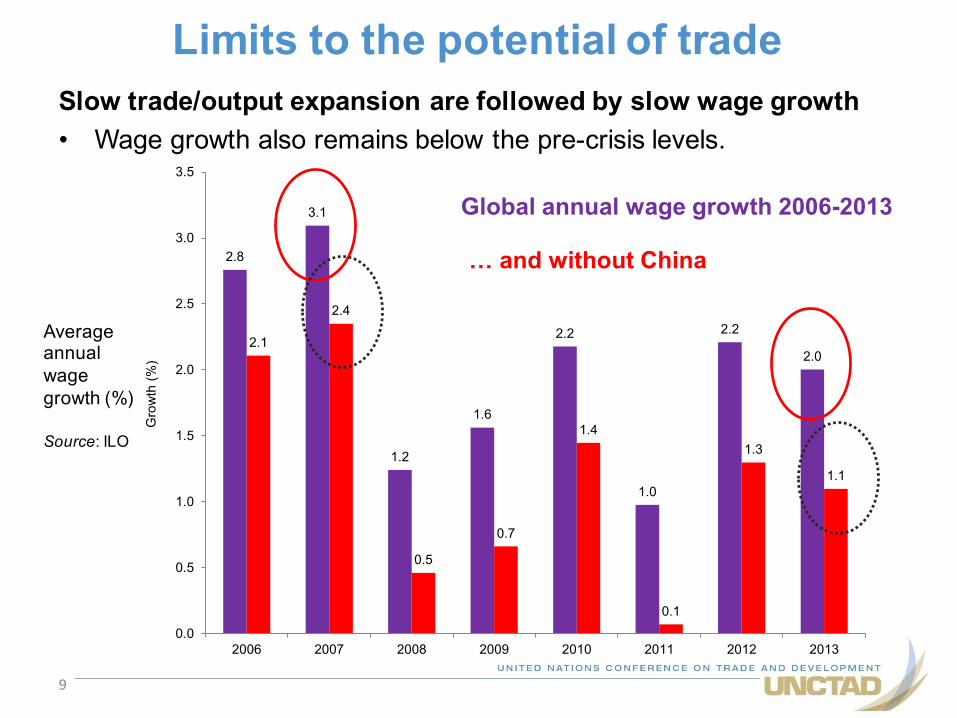

Slow trade/output expansion are followed by slow wage growth• Wage growth also remains below the pre-crisis levels.

Limits to the potential of trade

Average annual wage growth (%)

Source: ILO

2.8

3.1

1.2

1.6

2.2

1.0

2.2

2.02.1

2.4

0.5

0.7

1.4

0.1

1.3

1.1

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2006 2007 2008 2009 2010 2011 2012 2013

Growth (%

)

Global annual wage growth 2006-2013

… and without China

10

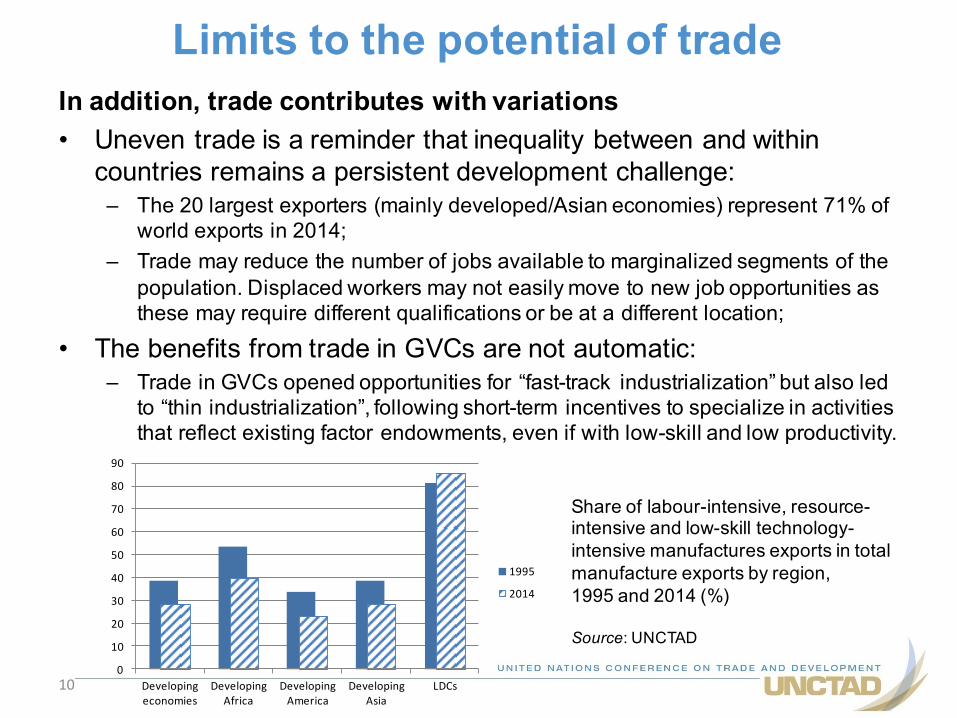

In addition, trade contributes with variations• Uneven trade is a reminder that inequality between and within countries remains a persistent development challenge:– The 20 largest exporters (mainly developed/Asian economies) represent 71% of world exports in 2014;;

– Trade may reduce the number of jobs available to marginalized segments of the population. Displaced workers may not easily move to new job opportunities as these may require different qualifications or be at a different location;;

• The benefits from trade in GVCs are not automatic:– Trade in GVCs opened opportunities for “fast-track industrialization” but also led to “thin industrialization”, following short-term incentives to specialize in activities that reflect existing factor endowments, even if with low-skill and low productivity.

Limits to the potential of trade

0

10

20

30

40

50

60

70

80

90

Developing economies

Developing Africa

Developing America

Developing Asia

LDCs

1995

2014

Share of labour-intensive, resource-intensive and low-skill technology-intensive manufactures exports in total manufacture exports by region, 1995 and 2014 (%)

Source: UNCTAD

11

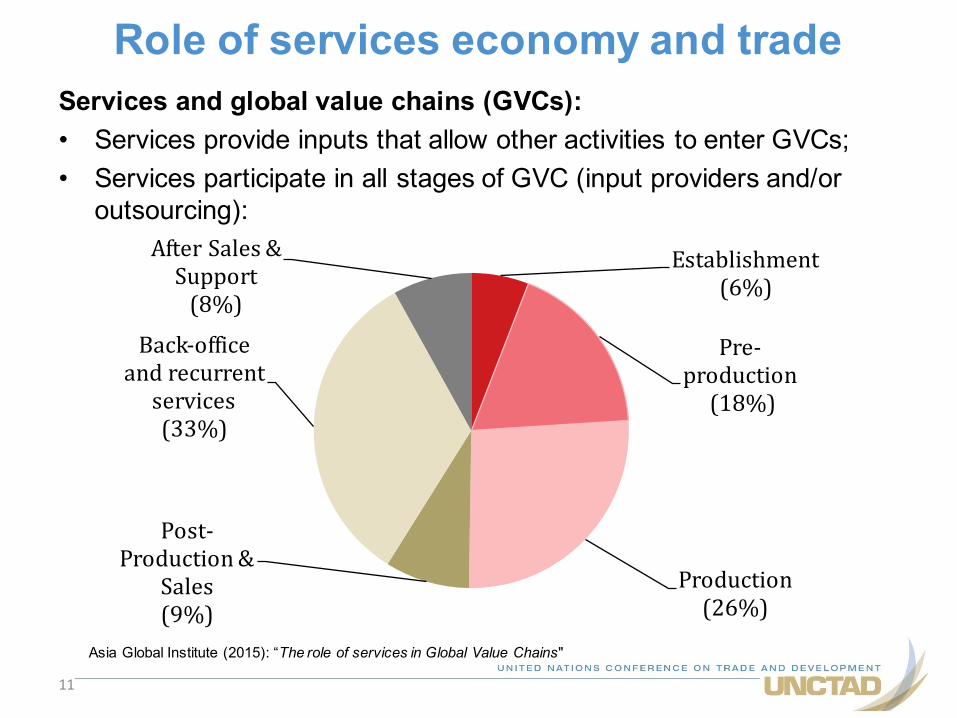

Services and global value chains (GVCs):• Services provide inputs that allow other activities to enter GVCs;;• Services participate in all stages of GVC (input providers and/or outsourcing):

Role of services economy and trade

Establishment (6%)

Pre-‐‑production(18%)

Production (26%)

Post-‐‑Production &

Sales(9%)

Back-‐‑officeand recurrent services(33%)

After Sales & Support(8%)

Asia Global Institute (2015): “The role of services in Global Value Chains"

12

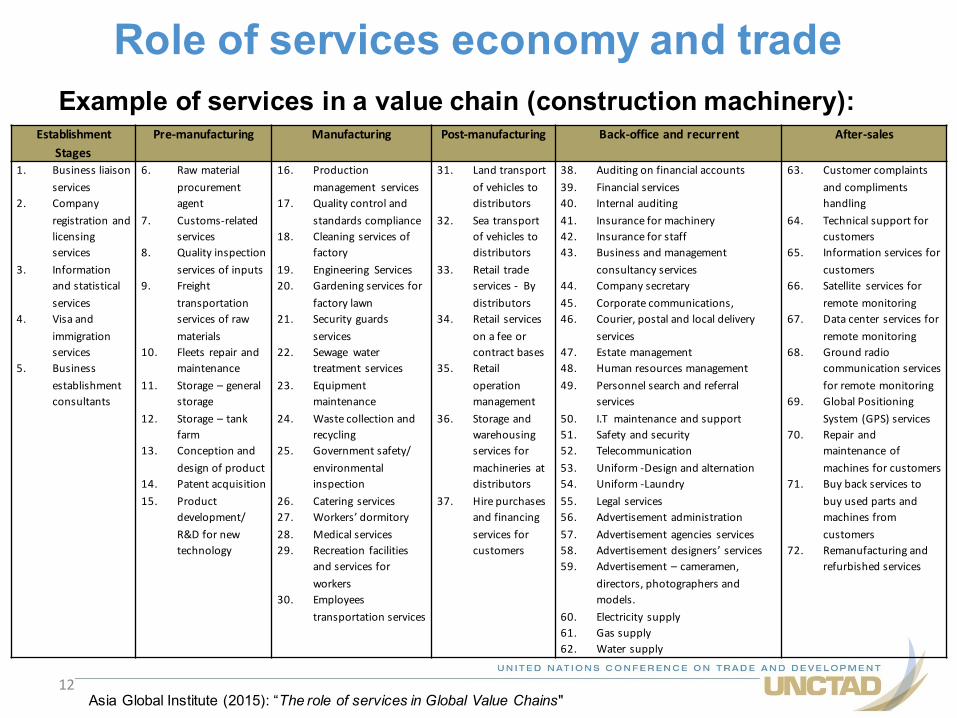

Example of services in a value chain (construction machinery):

Role of services economy and trade

Asia Global Institute (2015): “The role of services in Global Value Chains"

Establishment Stages

Pre-‐manufacturing Manufacturing Post-‐manufacturing Back-‐office and recurrent After-‐sales

1. Business liaison services

2. Company registration and licensing services

3. Information and statistical services

4. Visa and immigration services

5. Business establishment consultants

6. Raw material procurement agent

7. Customs-‐related services

8. Quality inspection services of inputs

9. Freight transportation services of raw materials

10. Fleets repair and maintenance

11. Storage – general storage

12. Storage – tank farm

13. Conception and design of product

14. Patent acquisition 15. Product

development/ R&D for new technology

16. Production management services

17. Quality control and standards compliance

18. Cleaning services of factory

19. Engineering Services20. Gardening services for

factory lawn21. Security guards

services22. Sewage water

treatment services23. Equipment

maintenance24. Waste collection and

recycling 25. Government safety/

environmental inspection

26. Catering services 27. Workers’ dormitory28. Medical services29. Recreation facilities

and services for workers

30. Employees transportation services

31. Land transport of vehicles to distributors

32. Sea transport of vehicles to distributors

33. Retail trade services -‐ By distributors

34. Retail services on a fee or contract bases

35. Retail operation management

36. Storage and warehousing services for machineries at distributors

37. Hire purchases and financing services for customers

38. Auditing on financial accounts39. Financial services 40. Internal auditing 41. Insurance for machinery 42. Insurance for staff43. Business and management

consultancy services44. Company secretary 45. Corporate communications,46. Courier, postal and local delivery

services47. Estate management48. Human resources management49. Personnel search and referral

services 50. I.T maintenance and support51. Safety and security 52. Telecommunication 53. Uniform -‐Design and alternation54. Uniform -‐Laundry55. Legal services56. Advertisement administration 57. Advertisement agencies services58. Advertisement designers’ services59. Advertisement – cameramen,

directors, photographers and models.

60. Electricity supply61. Gas supply62. Water supply

63. Customer complaints and compliments handling

64. Technical support for customers

65. Information services for customers

66. Satellite services for remote monitoring

67. Data center services for remote monitoring

68. Ground radio communication services for remote monitoring

69. Global Positioning System (GPS) services

70. Repair and maintenance of machines for customers

71. Buy back services to buy used parts and machines from customers

72. Remanufacturing and refurbished services

13

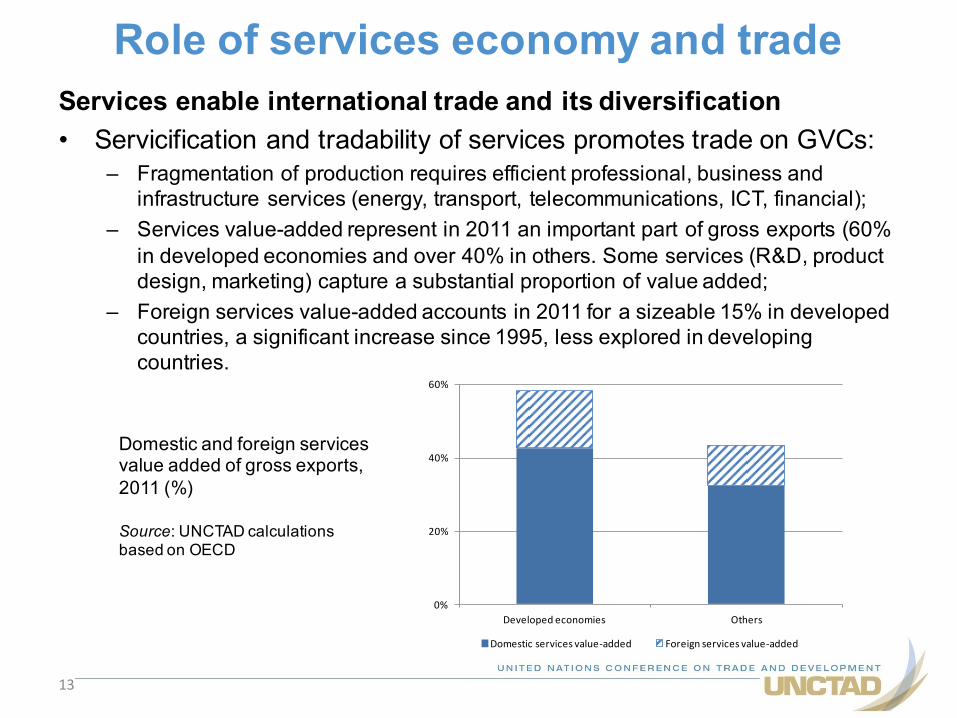

Services enable international trade and its diversification• Servicification and tradability of services promotes trade on GVCs:

– Fragmentation of production requires efficient professional, business and infrastructure services (energy, transport, telecommunications, ICT, financial);;

– Services value-added represent in 2011 an important part of gross exports (60% in developed economies and over 40% in others. Some services (R&D, product design, marketing) capture a substantial proportion of value added;;

– Foreign services value-added accounts in 2011 for a sizeable 15% in developed countries, a significant increase since 1995, less explored in developing countries.

Role of services economy and trade

Domestic and foreign services value added of gross exports, 2011 (%)

Source: UNCTAD calculations based on OECD

0%

20%

40%

60%

Developed economies Others

Domestic services value-‐added Foreign services value-‐added

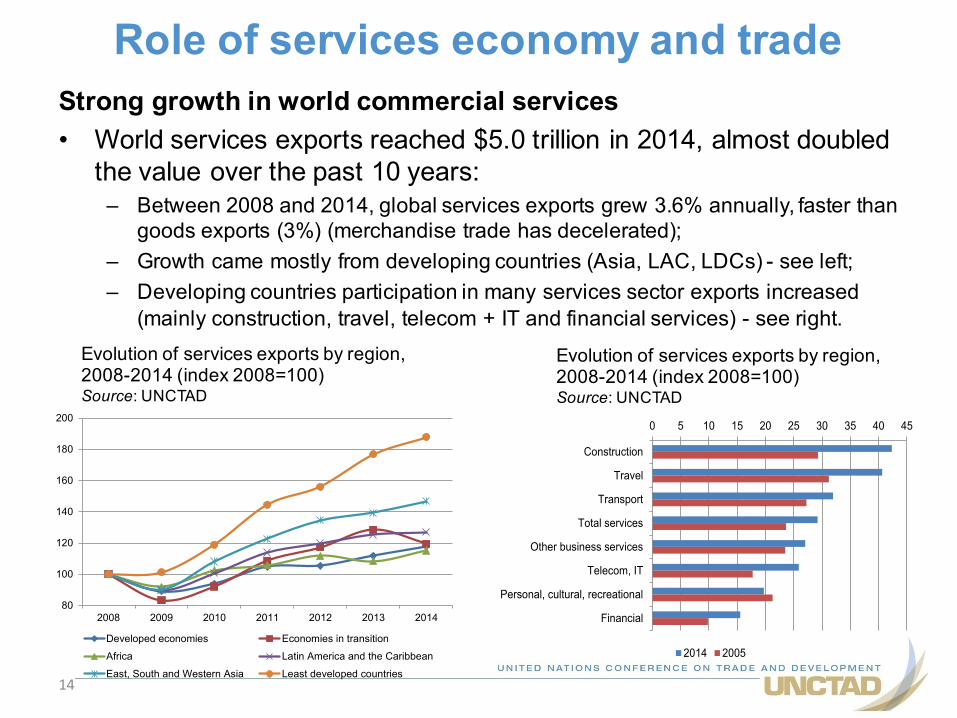

14

Strong growth in world commercial services• World services exports reached $5.0 trillion in 2014, almost doubled the value over the past 10 years:– Between 2008 and 2014, global services exports grew 3.6% annually, faster than goods exports (3%) (merchandise trade has decelerated);;

– Growth came mostly from developing countries (Asia, LAC, LDCs) - see left;;– Developing countries participation in many services sector exports increased (mainly construction, travel, telecom + IT and financial services) - see right.

Role of services economy and trade

Evolution of services exports by region, 2008-2014 (index 2008=100)Source: UNCTAD

80

100

120

140

160

180

200

2008 2009 2010 2011 2012 2013 2014

Developed economies Economies in transition

Africa Latin America and the Caribbean

East, South and Western Asia Least developed countries

0 5 10 15 20 25 30 35 40 45

Construction

Travel

Transport

Total services

Other business services

Telecom, IT

Personal, cultural, recreational

Financial

2014 2005

Evolution of services exports by region, 2008-2014 (index 2008=100)Source: UNCTAD

15

The importance of services is underestimated• Cross-border services trade data does not capture increasing trade by FDI and movement of natural persons:– In 2012, services were 63% of global FDI stock. Services sales by affiliates could have been $18 trillion in 2014, 4x greater than cross-border services exports;;

– Movement of natural persons is particularly important in professional and business services and in services related to agriculture, manufacture and mining;;

– Mode 4 is on a rising trend given the growth in global remittances – in 2014, global flows stood at $583 billion, $436 of which to developing countries.

• Remittances and financial inclusion are key for development:– Remittances represent 26% of total financial inflows, the 2nd more important source of external finance after official development assistance (ODA) in LDCs;;

– A 10% rise in remittances may contribute to a 3.5% reduction in the share of people living in poverty. They are private flows, thus public policy should provide options for people to apply these funds in development meaningful ways;;

– Financial services can contribute to their productive use and to reduce remittances’ transfer costs. Target 10.c of SDGs is to reduce these costs to less than 3% and eliminate corridors with costs higher than 5% by 2030;;

– A 5% reduction in remittances costs might yield $15 billions in savings.

Role of services economy and trade

16

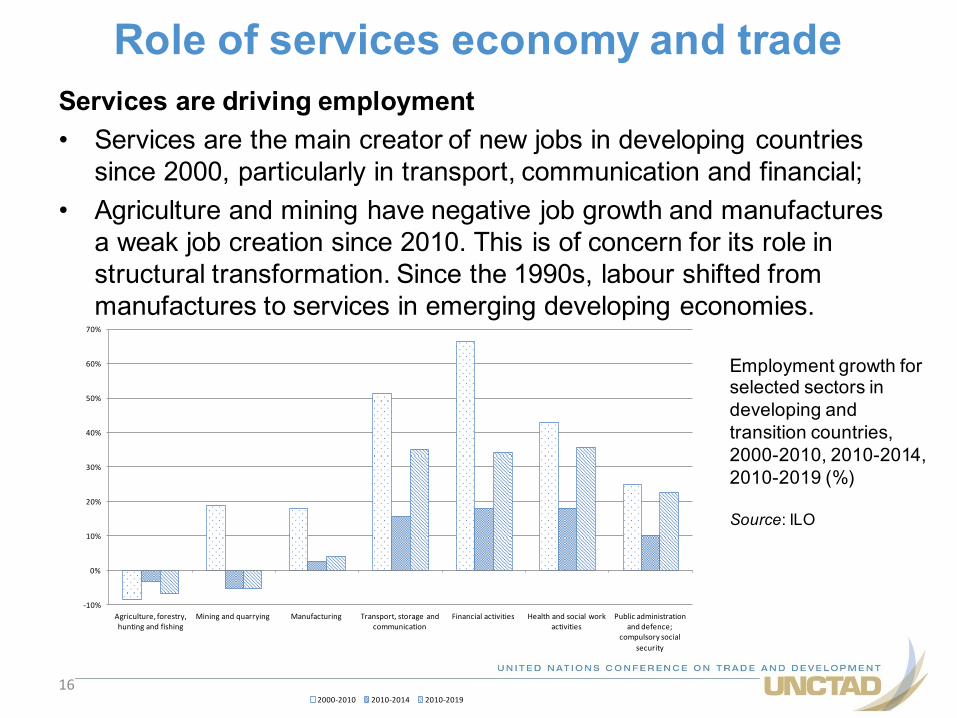

Services are driving employment• Services are the main creator of new jobs in developing countries since 2000, particularly in transport, communication and financial;;

• Agriculture and mining have negative job growth and manufactures a weak job creation since 2010. This is of concern for its role in structural transformation. Since the 1990s, labour shifted from manufactures to services in emerging developing economies.

Role of services economy and trade

Employment growth for selected sectors in developing and transition countries, 2000-2010, 2010-2014, 2010-2019 (%)

Source: ILO

-‐10%

0%

10%

20%

30%

40%

50%

60%

70%

Agriculture, forestry, hunting and fishing

Mining and quarrying Manufacturing Transport, storage and communication

Financial activities Health and social work activities

Public administration and defence;

compulsory social security

2000-‐2010 2010-‐2014 2010-‐2019

17

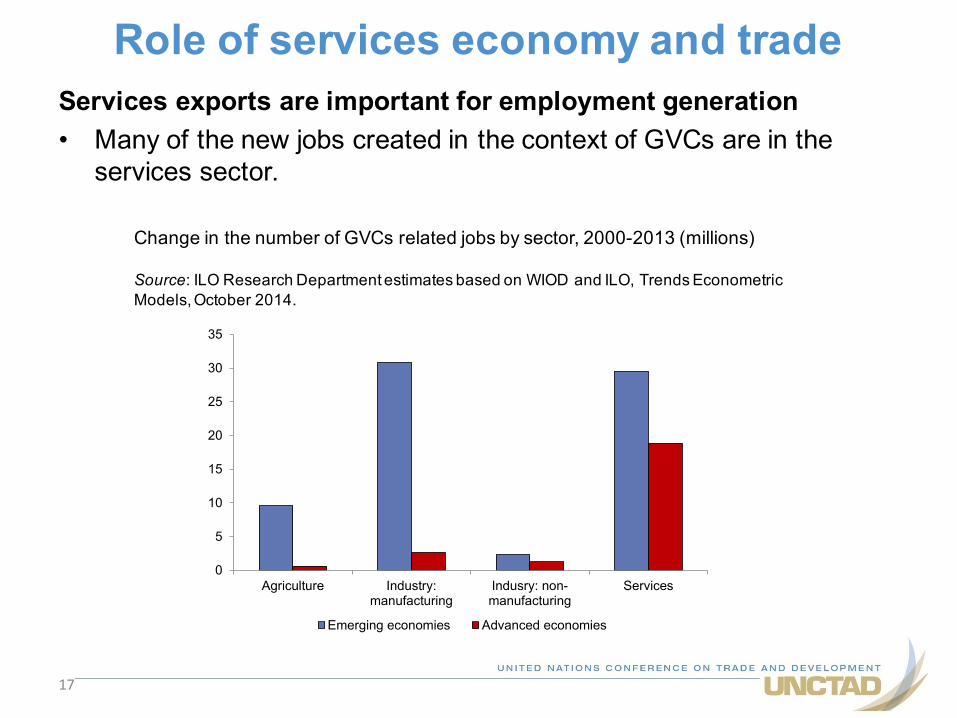

Services exports are important for employment generation• Many of the new jobs created in the context of GVCs are in the services sector.

Role of services economy and trade

Change in the number of GVCs related jobs by sector, 2000-2013 (millions)

Source: ILO Research Department estimates based on WIOD and ILO, Trends Econometric Models, October 2014.

0

5

10

15

20

25

30

35

Agriculture Industry:manufacturing

Indusry: non-manufacturing

Services

Emerging economies Advanced economies

18

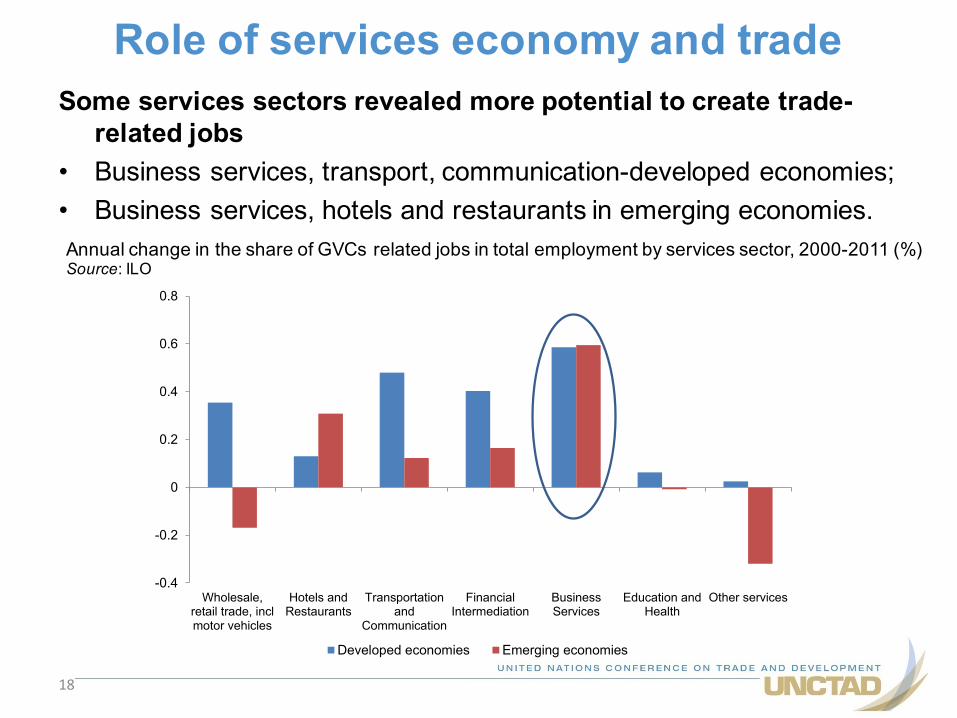

Some services sectors revealed more potential to create trade-related jobs

• Business services, transport, communication-developed economies;;• Business services, hotels and restaurants in emerging economies.

Role of services economy and trade

Annual change in the share of GVCs related jobs in total employment by services sector, 2000-2011 (%)Source: ILO

-0.4

-0.2

0

0.2

0.4

0.6

0.8

Wholesale,retail trade, inclmotor vehicles

Hotels andRestaurants

Transportationand

Communication

FinancialIntermediation

BusinessServices

Education andHealth

Other services

Developed economies Emerging economies

19

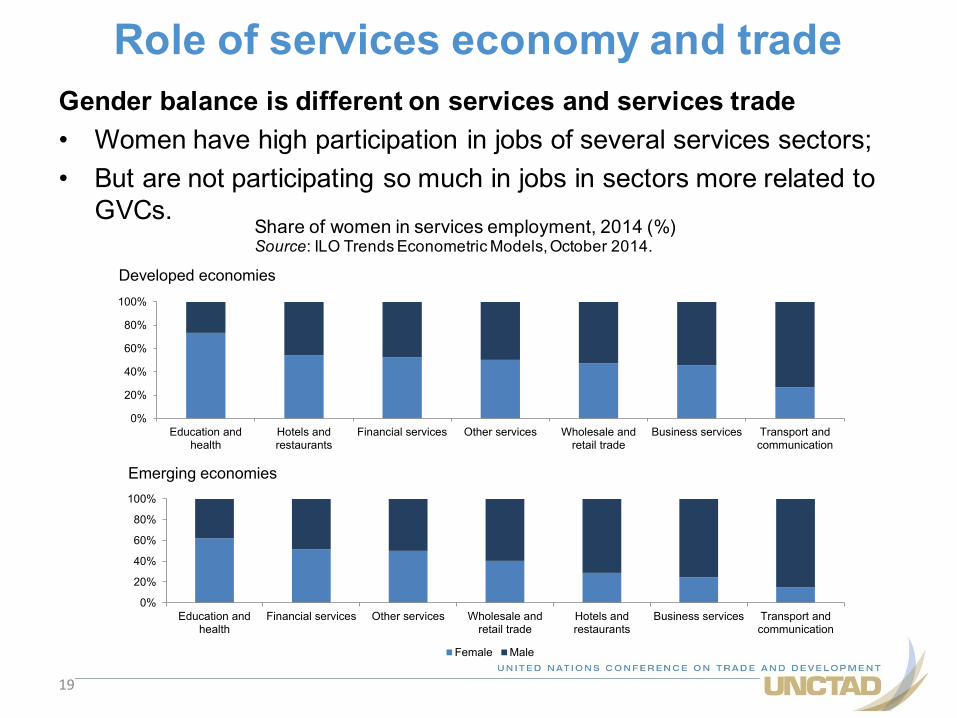

Gender balance is different on services and services trade• Women have high participation in jobs of several services sectors;;• But are not participating so much in jobs in sectors more related to GVCs.

Role of services economy and trade

Share of women in services employment, 2014 (%)Source: ILO Trends Econometric Models, October 2014.

Developed economies

Emerging economies

0%

20%

40%

60%

80%

100%

Education andhealth

Hotels andrestaurants

Financial services Other services Wholesale andretail trade

Business services Transport andcommunication

0%

20%

40%

60%

80%

100%

Education andhealth

Financial services Other services Wholesale andretail trade

Hotels andrestaurants

Business services Transport andcommunication

Female Male

20

Development benefits from trade require an enabling policy mix• A deliberate, coherent, integrated policy mix, supportive of a desired structural transformation, is needed to build broad-based productive capacities, diversification, technological upgrading and job creation:– Industrial development and technological policies are important to improve and create comparative advantages leading to a desired structural transformation;;

– Flanking policies are needed to enhance overall competitiveness, facilitate adjustments and support greater inclusiveness;;

– A sound regulatory and institutional framework is central to support all sectors of the economy, in particular services economy and trade;;

– International support, including through Aid for Trade, remains vital to support trade integration of developing countries;;

• Trade negotiations are relevant for trade and jobs in services– The existence of a trade agreement and lowering applied rates also creates GVCs’ jobs in services (with variations).

• UNCTAD assists countries in several of these dimensions:– Trade Policy Frameworks (TPFs) on trade and other flanking policies;;– Services policy reviews (SPRs) on strengthening services economy and trade;;– Contributes within the UN system to collaborative efforts to promote international support and Aid for Trade.

Policy options

21

Trade implies adjustments that need complementary policies• The reallocation of workers from declining to expanding activities is needed to contribute to employment;;

• Adequate employment protection legislation, under the oversight of the fundamental principles and rights at work, can be relevant to promote labour market adaptability while providing incentives for investment in workers and protecting them against arbitrariness;;

• The implementation of social safety nets, such as unemployment benefits, can be relevant. They should be linked to job-search incentives and re-employment services;;

• Active labour market policies such as labour reskilling contribute to market adaptive capacity and to the reintegration of trade-displaced workers with reduced costs on job losers;;

• Public-sector jobs, employment subsidies and support to entrepreneurship can also be relevant;;

• The effectiveness of these measures is amplified by sound labour market information and hampered by informality.

Policy options

22

Impact of trade in ICT services on employment• Senegal is an essentially agricultural country in terms of employment (more than half of the population) but services give the major contribution to GDP (more than 50% between 2000/2009);;

• Services were 1/3 of the labour force (2010) but this would probably be revised upward if accounting for the important informal sector;;

• Jobs (2000s) grew more in services (50%) than in agriculture (15%);;• The country made the choice to promote ICT services as a spearhead of its economic diversification strategy;;– Objective of addressing increased unemployment, in particular in youth (target of 240.000 direct and indirect jobs by 2015);;

– Building on significant investments made in ICT infrastructures;;– ICT activities were identified as complying with development criteria: growth potential, creation of value-added, job creation, and export potential;;

– Allows for innovation and value-addition in several sectors (banking, health, etc);;– Took preliminary measures to reform ICT markets, introducing competition and improving the legal and regulatory framework.

Case-study Senegal

23

Mixed results• Senegal is now recognised as a model for many Sub-Saharan countries in terms of ICT infrastructure and quality of ICT services and as a reliable destination for offshoring services;;

• The ICT sector is growing fast (14% annually between 2000-2010);;• Job results are improving but far from goals, due to several reasons:

– The ICT development strategy was built on a unique BPO sub-segment - call centre activities (in Senegal ICT include telecommunication, computer and related services, wholesale, maintenance, repair computer equipment, Internet supply, cell phones services, BPO, IT outsourcing, and media);;

– Furthermore, call centres activities are a segment where Senegal faces serious competition in Africa and where low labour costs competitiveness pressures;;

– Although the Government has pursued investors and offering FDI incentives (free trade zones and exemptions on taxes and import duties), the national action plans (and related SME support) are yet to be implemented by authorities;;

– Shortfalls in human resources are still a challenge. Many ICT actors admitted that the educational system was not adapted to job market needs and has failed to adapt training programmes to new jobs emerging in ICTs.

Case-study Senegal

24

A set of policies is necessary to enhance the job creation potential of the ICT services sector

• There is need for diversification within the ICT sector. Call centres can be a first stage with low value-added but policies need to shift investment to higher value-added ICT activities which could bring sustainable spill-overs on growth and employment;;

• Increasing competition in some telecom segments will improve ICT activities' competitiveness relying on those services;;

• Supporting SMEs through R&D incentives policy and by the simplification of procurement policy;;

• An export strategy should be developed with a multistakeholderapproach and considering regional markets;;

• Develop specific data on the sector would allow designing more evidence-based policies and tailored action plans;;

• Strengthening human skills, including through the reform of education programmes more oriented to ICT. This also alleviates brain drain.

Case-study Senegal

25

Impact of trade liberalization on services employment• South Africa has actively promoted the services economy and trade as part of the plan to create 5 million jobs by 2020:– Engaged in bilateral and multilateral agreements to stimulate trade in services;;– Provided a wide variety of incentives to promote the services sector;;

• The services sector has grew more than agriculture and manufacturing in both output and employment:– The services sector provides employment to a wide range of activities;;

• But results are mixed:– The services sector is not optimally employment-intensive;;– It has contributed to the skill-biased growth as much of the most significant growth in employment is on the highly-skilled worker category;;

– Policy priorities to job creation have not resulted in great job absorption by the services sector of surplus labour;;

– A policy mix to develop the service sector remains a vital challenge.

• Note on Lesotho: the services sector has the highest growth, but Lesotho remains a net importer of services. Services employment has made only a marginal contribution to total employment.

Case-study South Africa

26

At a sectoral level, the majority has created jobs during the past decade but not all at a rate that matches output growth

• Financial services:– Had the highest output growth in the last decade;;– With an employment elasticity of 1.05, employment increased analogously;;

• ICT services:– Shows significant output growth but with an heterogeneous job creation role;;– Hardware and software consultancy have high employment growth but telecom has negative job growth;;

– Jobs were concentrated in highly skilled workers;;

• Other business services:– Had low output growth (1.9%) but significant job growth (4.6%);;– The occupational composition is biased towards semi-skilled and elementary workers;;

– Employment elasticity has been higher than 1 for several years and is considered a key sector for job creation.

Case-study South Africa

27

UNCTAD's toolkit to enhance the development role of services• Services provide an opportunity for economic diversification, structural transformation, job creation and sustainable development:– Policy, regulatory and institutional frameworks are important to harness benefits of services, but remain a critical challenge, as services are complex and multifaceted in nature;;

(1) GSF and Multi-year Expert Meeting on Trade, Services and Development:– Platform for expert deliberation through an exchange of country experiences and lessons learned to identify best-fit practices on services, trade and development;;

– They have identified recommendations and areas for deeper research.

(2) SPRs serve as a toolkit for policymakers and regulators:– Identify constrains and offer practical recommendations on a best-fit policy mix;;– Ensure policy coherence and build institutional capacities;;– Aim to enhance productive and trade capacity in services, enhance economy-wide competitiveness and meet development objectives;;

(3) Country survey, case studies & dedicated research– E.g., Further to MYEM recommendations in 2009, UNCTAD conducted surveys of infrastructure regulators and competition authorities (part I on infrastructure regulation and institutions, and part II on trade of ISS), which useful insights.

UNCTAD toolkit

28

UNCTAD’s Services Policy Reviews enable the services’ potential and provide cross-cutting lessons

• Policy coherence and coordination to build complementarities between services and other sectors and services support to GVCs;;

• Multi-stakeholder approach to policymaking involving private sector, public-private partnerships and coalitions of services industries;;

• Data availability for evidence-based policymaking;;• Effective regulations, institutions and governance to enhance services’ competitiveness, access, quality and affordability;;

• Productive, technology and business environment that are enabling, including for SMEs and for the formalization of the economy;;

• Labour skill development;;• Capitalization of regional and international integration, productive and infrastructure capacity-building and regulatory cooperation.

UNCTAD toolkit

Thank You

UNCTAD

More information on trade policy frameworks:http://unctad.org/en/Pages/DITC/TNCD/Trade-Negotiations-and-Commercial-Diplomacy-.aspx

More information on services, trade and development:http://unctad.org/en/Pages/DITC/Trade-in-Services.aspx