Embed Size (px)

Citation preview

Part IIIReducing the Cost of UMTS

Fraser CurleyBonnNovember 2001

Arthur D. Little Int., Inc.Martin-Luther-Platz 26D-40212 DüsseldorfTel. +49-211-8609-0Fax +49-211-8609-599

1clientxx\kunde\present\pres0000.ppt/w

Table of contents

1

2 Typical approach and methodology

Infrastructure sharing

2clientxx\kunde\present\pres0000.ppt/w

General market development - Overview1

The rapid development of the new economy boom and bust cycle has hit themobile industry in the UMTS roll-out

The "New Economy Hype Curve"

Mar

ket c

ap

Time2000 2001

Q1 Q2 Q3 Q4 Q1 Q2 Q3

Dot.coms

ISPs

Telcos

Telecom equipment suppliers

Management Consultants

Financiers?

Tro

ub

led in

du

stries

illustrative

3clientxx\kunde\present\pres0000.ppt/w

Infrastructure sharing - Refocusing roll-out strategies1

Making the situation more difficult, this happens in a time of sharplyincreasing competition on the European mobile markets

• A late market entry isdifficult to accomplish inmobile telephony -providers usually takea long time (if ever) toreach their "fair"market share

• The already very highmobile penetrationleaves few room forgrowth in new marketsegments

• Lack of (spectrum)capacity in this specificmarket could force afaster market entry ofnew players in UMTS

• The development of in-house applicationsolutions with exclusivepartners will beincreasingly difficultfor mobile operators

Number of UMTS license holders by country Issues

Number of UMTS licenses

Source: UMTS forum, 2001

0 1 2 3 4 5 6

Co

un

try

AustriaUK

SwitzerlandPortugalNorway

NetherlandsItaly FranceFinland

DenmarkSpainBelgium

Germany

4clientxx\kunde\present\pres0000.ppt/w

Infrastructure sharing - Refocusing roll-out strategies1

The rapid roll-out schedule for UMTS has put additional pressure onoperators as well as on vendors

3 31

74

2 3 31

14

85 5

3 2

96

2 10

10

20

30

40

50

60

70

1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001E

2002E

Num

ber

of m

ajor

net

wor

k la

unch

es

Network launches in 16 European countries

• Equipment and handsets• Cell sites and planning application• IT and support systems (implementation

time frame)• Roll-out teams and radio planners• Integrity testing teams• Application development and

implementation teams

> 60networks

Source: Mobile Communications, Arthur D. Little research 2001

Constraining Factors

5clientxx\kunde\present\pres0000.ppt/w

4Reducing network and infrastructure cost

4Optimize spectrum utilization (partnering)

4Optimize equipment utilization (synergies through partnering)

4Expedite the roll-out of services

4Avoiding repetition of WAP and GPRS roll-out mistakes

4Bringing services to the (increasingly skeptical) market

Main targets

Infrastructure sharing - Refocusing roll-out strategies1

In view of this changing market environment, operators are redesigning theirroll-out strategies

6clientxx\kunde\present\pres0000.ppt/w

Late availability of handsets

Limited coverage

High pricing

Shortage in infrastructure supply*

Scarcity of antenna sites

No killer applications

No difference to GPRS

No need for fast data services

Saturation of the mobile market

Electrosmog concerns

3,8

3,5

3,4

3,3

3,2

3,1

3,0

2,5

2,3

2,1

0 1 2 3 4 5

Source: Arthur D. Little survey, 11/2000

Purely network roll-out related

weak strong

Network roll-out related problems are regarded as among the mostthreatening showstoppers for UMTS introduction

Infrastructure sharing - Refocusing roll-out strategies1

Importance of UMTS barriers

*) within the intended roll-out timeframe

7clientxx\kunde\present\pres0000.ppt/w

TMNVodafoneOptimus

ONI WAY

DoCoMoJ-Phone

Manx Telecom

Monaco Telecom

TelefónicaAirtel

RetevisiónXfera

CellnetVodafoneOrange

One2OneHutchison 3G

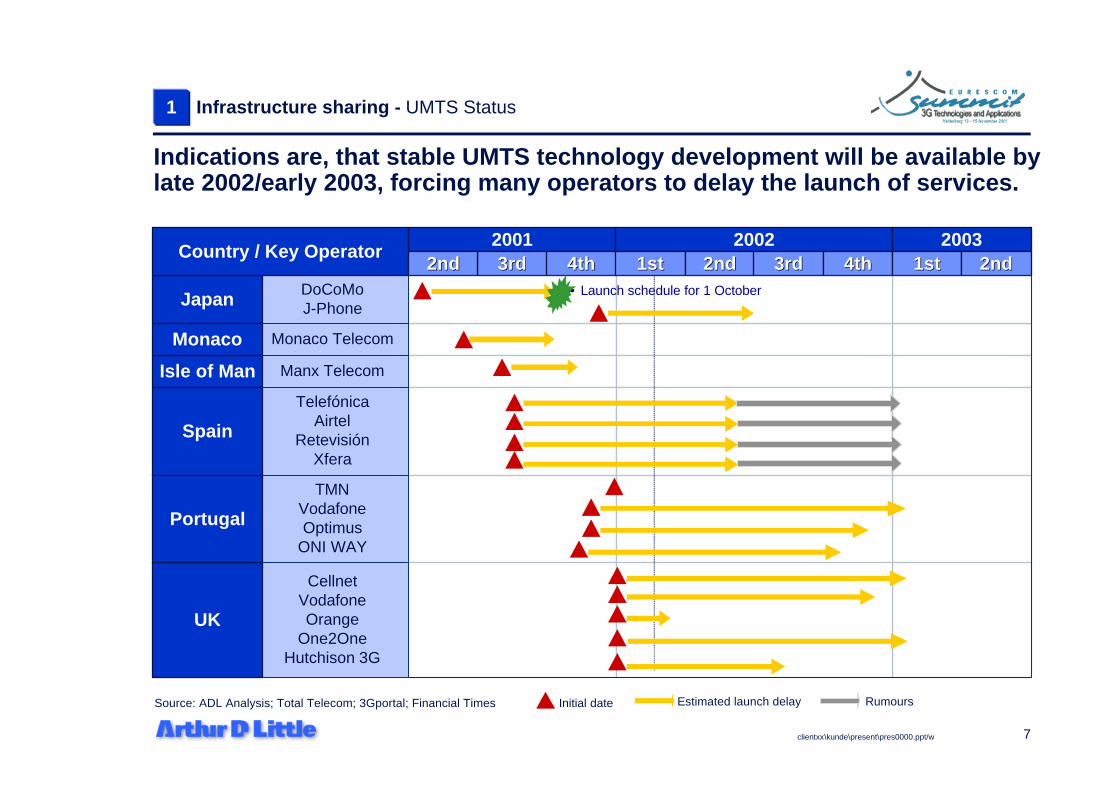

Indications are, that stable UMTS technology development will be available bylate 2002/early 2003, forcing many operators to delay the launch of services.

Portugal

Japan

Country / Key Operator

Isle of Man

Monaco

Spain

UK

Source: ADL Analysis; Total Telecom; 3Gportal; Financial Times Initial date Estimated launch delay Rumours

1 Infrastructure sharing - UMTS Status

2001 2002 20033rd3rd 4th4th 1st1st 2nd2nd 3rd3rd 4th4th 1st1st 2nd2nd2nd2nd

• Launch schedule for 1 October

8clientxx\kunde\present\pres0000.ppt/w

Source: ADL Analysis; Total Telecom; 3Gportal; Financial Times Initial date Estimated launch delay

Germany

T-MobilD2

E-Plus HutchisonViag Interkom

MobilcomGroup 3G

BelgiumKPN -Orange

MobistarProximus

to be awarded

Switzerland

SwisscomOrange

Team 3GdSpeed

Sunrise (Diax)

SwedenEuropolitanTele2 - Telia

HI3GOrange

FinlandSonera

RadiolinjaTelia Finland

Suonen

3rd3rdCountry / Key Operator

4th4th 1st1st 2nd2nd 3rd3rd 4th4th 1st1st 2nd2nd2001 2002 2003

1

Indications are, that stable UMTS technology development will be available bylate 2002/early 2003, forcing many operators to delay the launch of services.

Infrastructure sharing - UMTS Status

9clientxx\kunde\present\pres0000.ppt/w

In addition, some issues still remain regarding full operator interoperability.

• Mobility - Problems with the handover from one base station to another and from onecontroller to another

• Stability of trial 3G services

• Interoperability - European markets will require an “interoperability period" to allowmore testing to ensure that handsets and infrastructure, both old and new, are able tointeroperate with each other.

• Software problems and delays in agreeing standards, which means that production isdelayed.

• Obtaining sites and equipment availability (high number of simultaneous installations)

NetworkInfrastructure

UMTS Technology Issues

• Integration of Applications with Service Platforms and Interoperability Tests

• Software problems and browser integration problems

• Battery miniaturisation and power control

• Dual mode availability

Handsets

App.

Source: ADL Analysis; Vendor reports and Interviews; Total Telecom; 3Gportal; Financial Times

1 Infrastructure sharing - UMTS Status

10clientxx\kunde\present\pres0000.ppt/w

Mass market UMTS handsets are expected to be available in the second half of2003, the development being driven by strong competition amongst vendors.

Source: ADL Database; Merril Lynch; Vendors reports Demo Mass Production Temporary WithdrawalLegend:

Country / Key Operator2000

1st1st 2nd2nd 3rd3rd 4th4th

20011st1st 2nd2nd 3rd3rd 4th4th

20021st1st 2nd2nd 3rd3rd 4th4th

20031st1st 2nd2nd 3rd3rd

19993nd3nd 4nd4nd

MassProd.R520

Mass Production

DemoTimeport 260

DemoR520

EstimatedLauchT68

TemporaryWithdrawalR520

Mass Production

Demo Timeport 260

1st Test of 3G handsetMassProductionVoice Phones

MassProductionData Phones

UMTS

WAP

GPRS

Demo710

Mass Production 7110/Nokia 6210 was 2 months delayed

Other Vendors

Other Vendors

Other Vendors

NEC

DemoR320 Mass Production R320/ Other models were 6 months delayed

Mass ProductionNokia Imaging

MassProd.8310

FOMA

Sagem 959 & 979

Trial Visual Upgrade Starts Delivery inEurope

TrialPhone

UpgradedTrial VisualPhone

TrialVisualPhone

GPRSMassiveLaunch

1 Infrastructure sharing - UMTS Status

11clientxx\kunde\present\pres0000.ppt/w

Infrastructure sharing - Recent developments1

Facing the rapidly changing environment, operators start to look for newways to reduce the risk of the 3G roll-out while meeting their objectives

Network sharing agreement in GermanyThe Telefonica and Sonera JV, Group 3G, has confirmed that it has signed a memorandum ofunderstanding for a network sharing co-operation with KPN's E-Plus.

3G Newsroom, September 11, 2001

BT and DT to share 3G network costsBT and Deutsche Telekom have struck a landmark agreement to co-operate in the rollout of 3Gnetworks in the U.K. and Germany, the companies said on Tuesday.The agreement between mobile arms BT Wireless and T-Mobile could save them each up to 30%of the capital cost of building the networks.Reuters, June 12 2001

BT's 3G network sharing plan could come trueUK government said today that it would support 3G network sharing if it brings benefit toconsumers and the environment.3G News, May 04, 2001

Green party encouraging network sharingEnvironmentalists are lobbying the European Union to allowing 3G operators to shareinfrastructure.3G News, May 13, 2001

12clientxx\kunde\present\pres0000.ppt/w

Source: DKB 2000

Coverage phase - covering major cities - first year of roll-outExpansion phase - reaching national coverage - 2002-2005Capacity - further increasing capacity - from 2005

The main reason for sharing the burden is to lower the level of investmentper user

Infrastructure sharing - Main reason cost pressure1

Investments per roll-out phase

13clientxx\kunde\present\pres0000.ppt/w

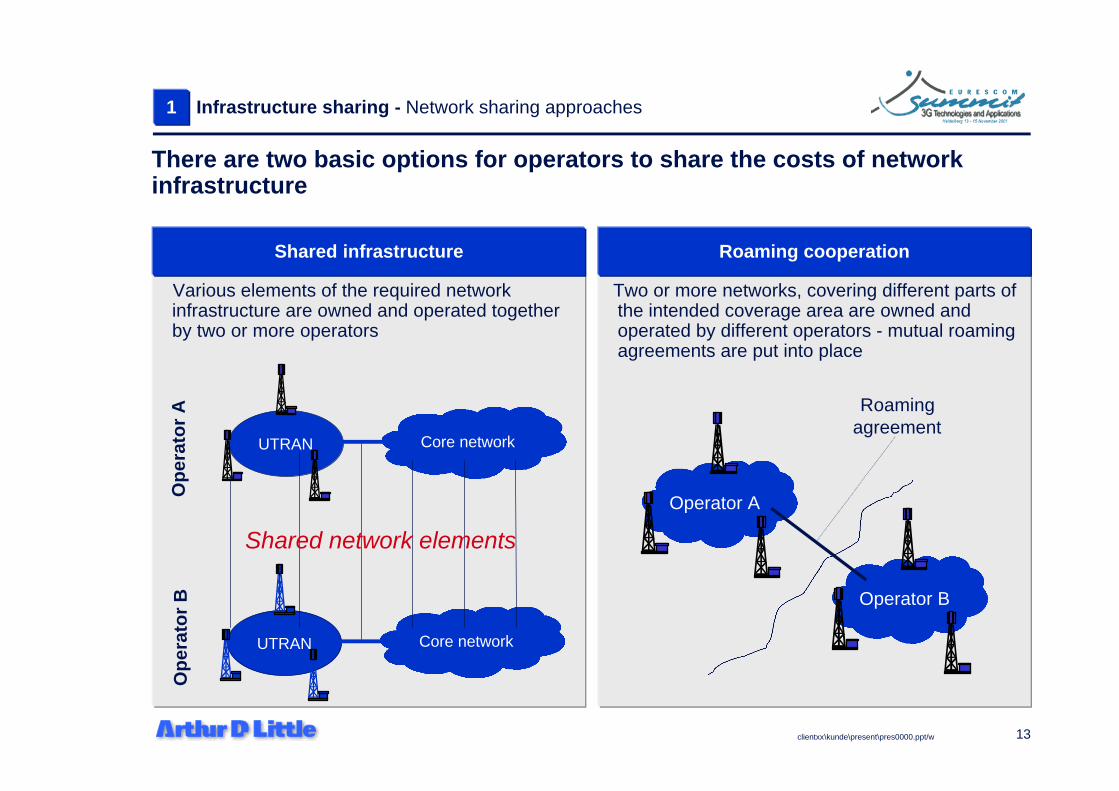

Two or more networks, covering different parts ofthe intended coverage area are owned andoperated by different operators - mutual roamingagreements are put into place

Roaming cooperation

Operator A

Operator B

Roamingagreement

Various elements of the required networkinfrastructure are owned and operated togetherby two or more operators

Shared infrastructure

Core networkUTRAN

Core networkUTRAN

Op

erat

or

AO

per

ato

r B

Shared network elements

Infrastructure sharing - Network sharing approaches1

There are two basic options for operators to share the costs of networkinfrastructure

14clientxx\kunde\present\pres0000.ppt/w

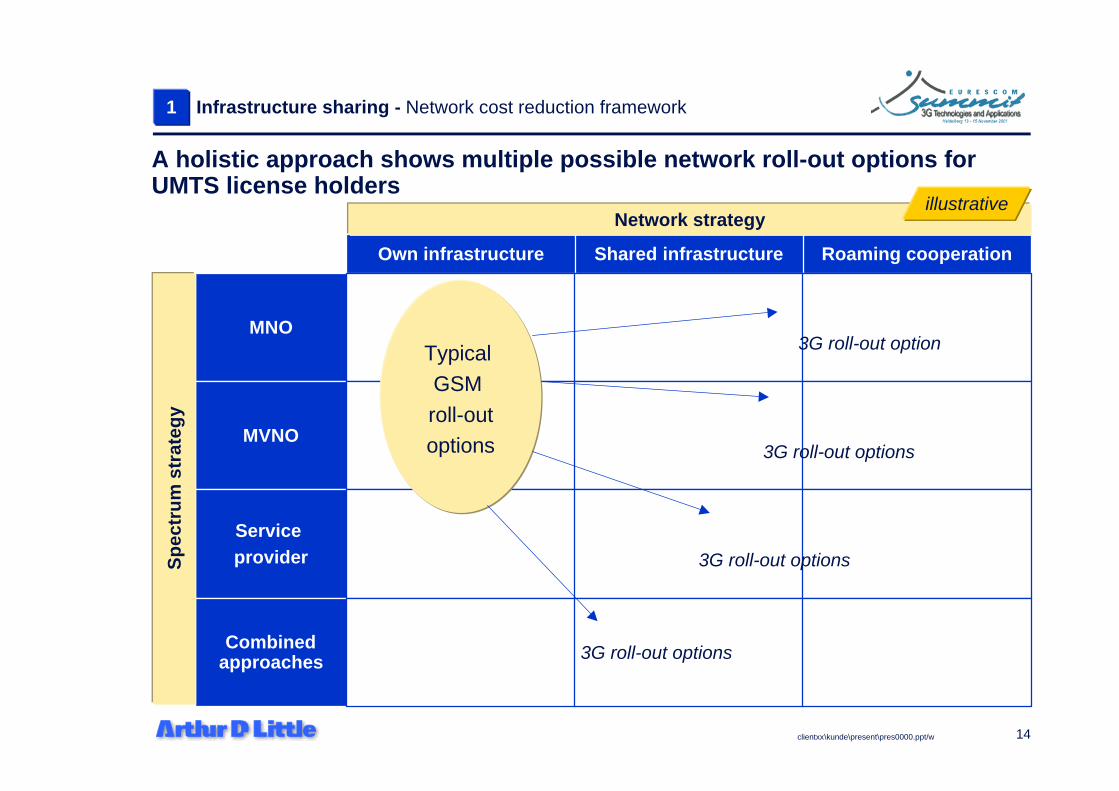

Roaming cooperationShared infrastructureOwn infrastructure

MNO

MVNO

Service provider

Combinedapproaches

MNO

MVNO

Service provider

Combined approaches

MNO

MVNO

Service provider

Combined approaches

MNO

MVNO

Service provider

Combined approaches

Typical

GSM

roll-out

options

3G roll-out option

3G roll-out options

3G roll-out options

3G roll-out options

Network strategy

Sp

ectr

um

str

ateg

y

Infrastructure sharing - Network cost reduction framework1

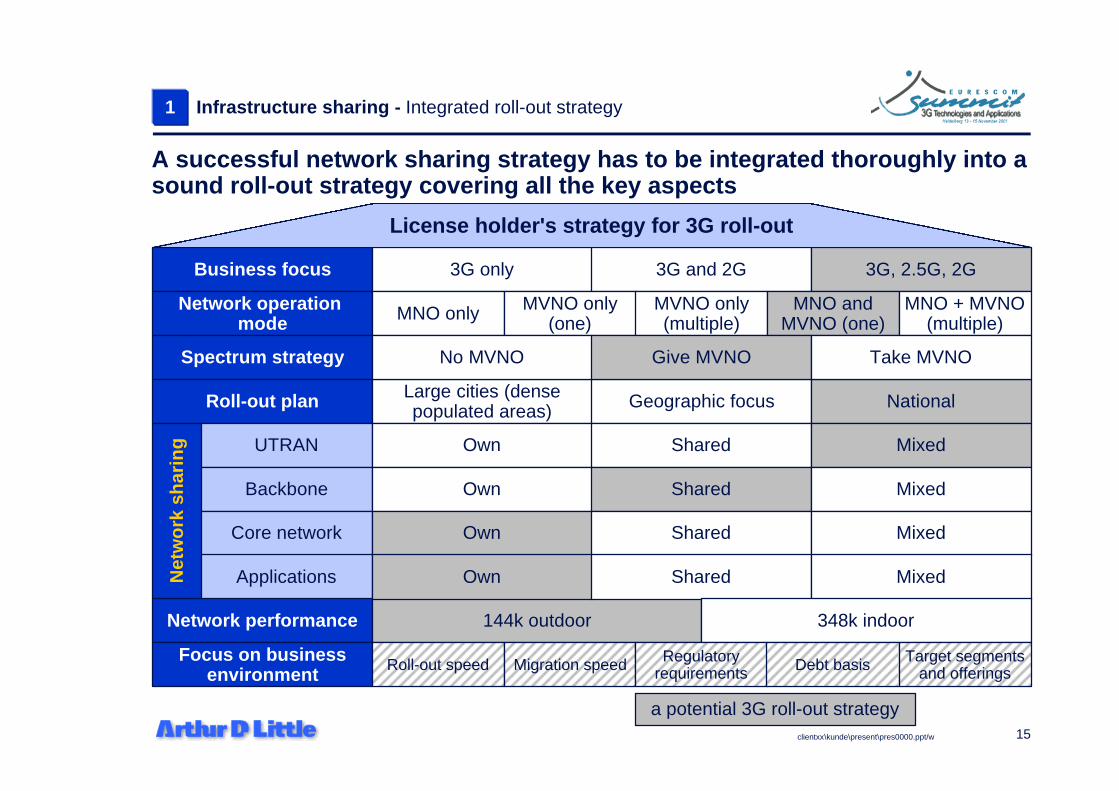

A holistic approach shows multiple possible network roll-out options forUMTS license holders

illustrative

15clientxx\kunde\present\pres0000.ppt/w

Business focus 3G only 3G and 2G 3G, 2.5G, 2G

Network operation mode MNO only

Spectrum strategy

Roll-out plan Large cities (densepopulated areas) Geographic focus National

UTRAN Own Shared Mixed

Backbone

Core network

Applications

Network performance 144k outdoor

Net

wo

rk s

har

ing

MVNO only(one)

MVNO only(multiple)

MNO andMVNO (one)

MNO + MVNO(multiple)

No MVNO Give MVNO Take MVNO

Own Shared Mixed

Own Shared Mixed

Own Shared Mixed

348k indoor

License holder's strategy for 3G roll-out

a potential 3G roll-out strategy

Focus on businessenvironment Roll-out speed Migration speed Regulatory

requirements Debt basis Target segmentsand offerings

1

A successful network sharing strategy has to be integrated thoroughly into asound roll-out strategy covering all the key aspects

Infrastructure sharing - Integrated roll-out strategy

16clientxx\kunde\present\pres0000.ppt/w

1

Network sharing decisions and rollout strategy are interdependent with thebusiness strategy and environment of a UMTS license holder

Business strategy and environment

Migration speed (2G-3G) Slow Average Fast

Rollout speed Slow Average Fast

Rollout cost Minimize

Regulatory environment Coveragerequirements

Networkperformancerequirements

MVNO legal

Target segment

Offering Multimedia products Business products Standard products

Secondary

Network sharinglegal

Wholesale Corporate SME SoHo HEC LEC

Infrastructure sharing - Integrated roll-out strategy - Further elements

17clientxx\kunde\present\pres0000.ppt/w

NetworkManagement

Center

UMTS radioaccess network

Node B /site

Link / LL

RNC

Core network

iuU-MSC

(incl. GSM, GPRS)

• OMC• Customer Care• Billing• Provisioning• Call Center• Applications

Shared UTRAN

Shared network

Shared operation

Shared applications and support functions

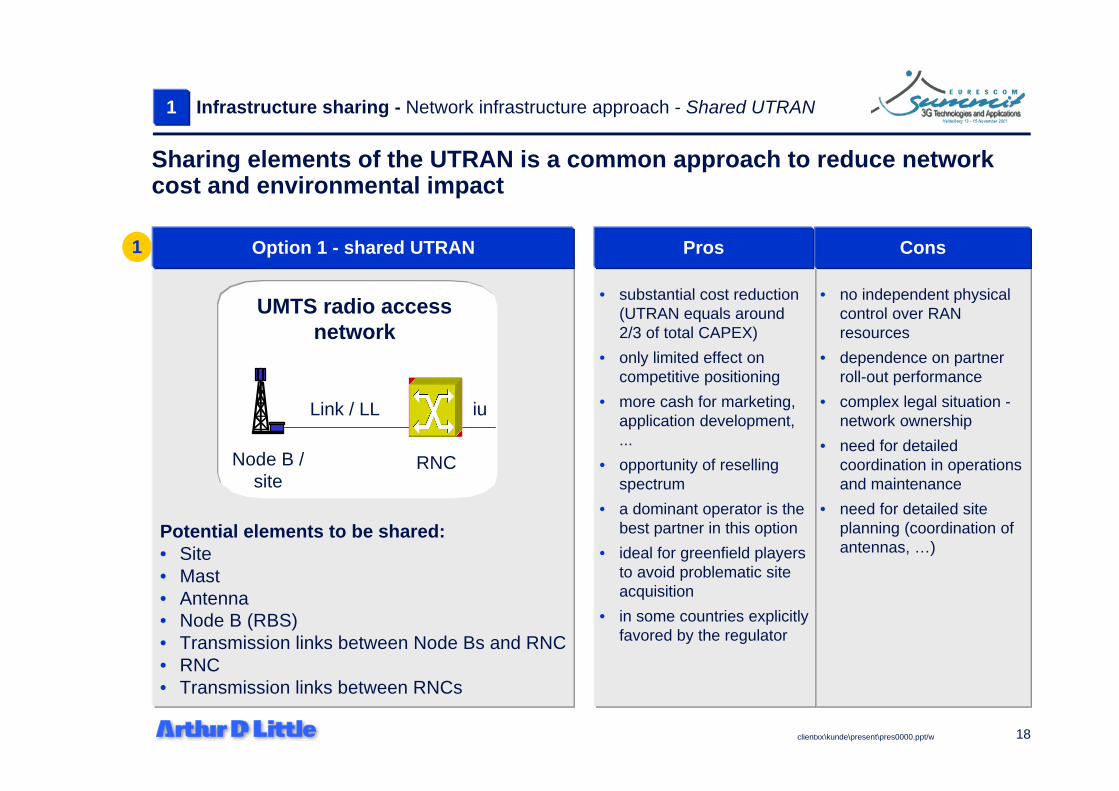

Infrastructure sharing - Network infrastructure approach1

The "shared infrastructure" approach allows for multiple levels of co-operation with different risks and benefits

1

2

3

4

Networkmanagement

Applicationsand support

18clientxx\kunde\present\pres0000.ppt/w

• no independent physicalcontrol over RANresources

• dependence on partnerroll-out performance

• complex legal situation -network ownership

• need for detailedcoordination in operationsand maintenance

• need for detailed siteplanning (coordination ofantennas, …)

• substantial cost reduction(UTRAN equals around2/3 of total CAPEX)

• only limited effect oncompetitive positioning

• more cash for marketing,application development,...

• opportunity of resellingspectrum

• a dominant operator is thebest partner in this option

• ideal for greenfield playersto avoid problematic siteacquisition

• in some countries explicitlyfavored by the regulator

Option 1 - shared UTRAN

Potential elements to be shared:• Site• Mast• Antenna• Node B (RBS)• Transmission links between Node Bs and RNC• RNC• Transmission links between RNCs

ConsPros

Infrastructure sharing - Network infrastructure approach - Shared UTRAN1

Sharing elements of the UTRAN is a common approach to reduce networkcost and environmental impact

1

UMTS radio accessnetwork

Node B /site

Link / LL

RNC

iu

19clientxx\kunde\present\pres0000.ppt/w

UMTS radio accessnetwork

Node B /site

RNC

iu

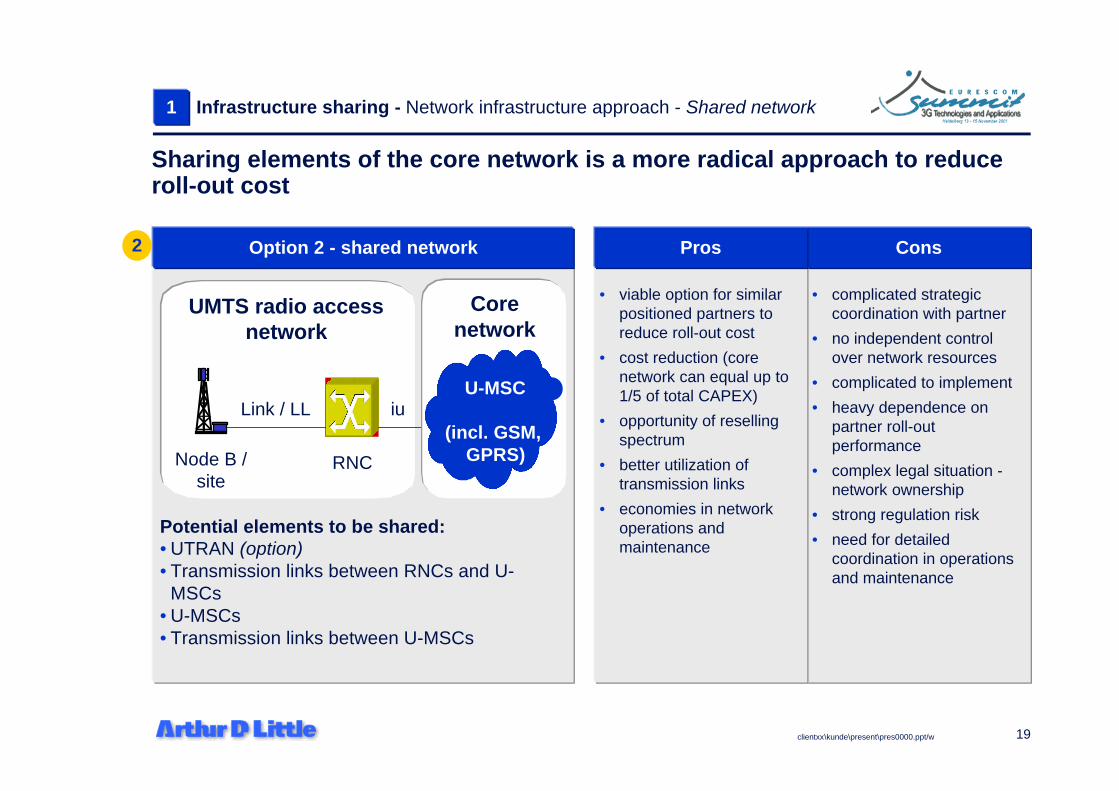

Option 2 - shared network

Potential elements to be shared:• UTRAN (option)• Transmission links between RNCs and U-

MSCs• U-MSCs• Transmission links between U-MSCs

• complicated strategiccoordination with partner

• no independent controlover network resources

• complicated to implement

• heavy dependence onpartner roll-outperformance

• complex legal situation -network ownership

• strong regulation risk

• need for detailedcoordination in operationsand maintenance

Cons

• viable option for similarpositioned partners toreduce roll-out cost

• cost reduction (corenetwork can equal up to1/5 of total CAPEX)

• opportunity of resellingspectrum

• better utilization oftransmission links

• economies in networkoperations andmaintenance

Pros

Corenetwork

U-MSC

(incl. GSM, GPRS)

Infrastructure sharing - Network infrastructure approach - Shared network1

Sharing elements of the core network is a more radical approach to reduceroll-out cost

2

Link / LL

20clientxx\kunde\present\pres0000.ppt/w

Option 3 - shared operation

Potential elements to be shared:• UTRAN (option)• Core network• NMC

• spectrum control is notcredible

• heavy dependence onpartner in all operationalaspects

• complex legal situation -spectrum "ownership"

• only little overall costreduction compared toshared UTRAN/CoreNetwork option

Cons

• opportunity for greenfieldlicense holders tocapitalize license withoutrisking additionalinvestment - or focussingexclusively on serviceprovision

• similar to one network withbroader frequencyspectrum

• viable approach incountries with limitedspectrum size (fordominant operators)

Pros

UMTS radioaccess network

Node B /site

Link / LL

RNC

Core network

iuU-MSC

(incl. GSM, GPRS)

Networkmanagement

Infrastructure sharing - Network infrastructure approach - Shared operation1

Reducing 3G operation to a "spectrum lease" or "merge" business could bea viable option for a greenfield operators that owns a cost effective license

3

21clientxx\kunde\present\pres0000.ppt/w

Option 4 - shared applications and support functions

Potential elements to be shared:• Other network elements (optional)• Specific applications or support systems (in

combination with other options) OMC CRM Billing Call center (CTI) Provisioning

• market positioning

• complicatedimplementation and/ormigration

• limited cost impact inmany cases

• detailed interfacedefinition required

• critical service levels

Cons

• viable approach to co-operate on standardapplications

• viable approach foroperators with licenses inmultiple countries - investin applications only once

• combination with UTRANor network sharing optionpossible

• potential co-operation /sharing with non-operatorexternal partner

• reduced overall scale ofoperations

Pros

UMTS radioaccess network

Node B /site

Link / LL

RNC

Core network

iu U-MSC

(incl. GSM, GPRS)

NetworkManagement

Center

Infrastructure sharing - Network infrastructure approach - Applications & support1

Sharing applications and support functions can be an approach to furtherreduce the scale of operations

4

Applicationsand support

• OMC• Customer

Care• Billing• Provisioning• Call Center• Applications

Networkmanagement

22clientxx\kunde\present\pres0000.ppt/w

Roaming cooperation

Operator A

Operator B

Areas with high population /traffic density

• regional separation isextremely difficult

• redundant structures willbe required in some areas(and can lead to extracosts)

• regional structures can notbe adjusted to economicand socio-demographicdevelopments

• inefficient spectrumutilization

Cons

• reasonable reduction ofnetwork cost

• little coordination effort

• no complexity increasedue to equipment sharing

• more flexible partnershipenvironment than sharingapproaches

Pros

2G roaming

• Gives a clear advantage (and strong negotiation position)to incumbent operators

• Many regulative frameworks force some form of 2Groaming, but usually do not define conditions

• Adds another element to network/spectrum strategyframework

Infrastructure sharing - Roaming approach1

A roaming cooperation does not increase complexity but requires a higherdegree of partnership coordination

23clientxx\kunde\present\pres0000.ppt/w

Sharedapplication &

support

Relevant costreductions insome areas

Roamingcooperation

Fully functionalnetwork atsmaller scale

Shared network Shared operationShared UTRAN

Reasonablesavings

Very limitedadditionalsavings

Most substantialcost reduction(up to 40%)

Cost reduction

least favorable most favorable

Not affected byregulation

Limited bycoveragerequirements

Will need to benegotiated

Currently notpossible in mostcountries*

Activelypromoted insome regulations

Regulation*

Clear interfaces Smaller scaleLowerredundancies

SynergiesMost critical tomanage

Operationalcomplexity

*) tends to become less important in the future as regulators become more flexible

Infrastructure sharing - Approach evaluation1

From the current point of view both sharing of UTRAN as well as selectiveapplications and support functions seem most promising

Key

cri

teri

a

illustrative

24clientxx\kunde\present\pres0000.ppt/w

2004

Performance

-200,0

0,0

200,0

2001 2002 2003 2005 2006 2007 2008 2009 2010

MEuro

EBITDA

-200,0

0,0

200,0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

MEuro

EBITDA

Savings achieved

Cumulated total CAPEX

Cumulated total networkOPEX

NPV of FCF incl. TV

Peak funding

37-40% reduction

35-40% reduction

two years earlier

>200% increase

55-60% reduction

Own Network Shared Network

MVNO only(no ownbrand)

Own network Shared network Roaming cooperation

MNO only(own brand)

MNO and

MVNO

Scenario 2

Scenario 3

Scenario 1Base scenario

Scenario 4Scenario 5

Network strategy

Sp

ectr

um

str

ateg

y

Combined approach

Performance

In real-world scenarios, CAPEX as well as OPEX have been reduced by ~37%by sharing parts of the UTRAN, transmission links and applications

Infrastructure sharing - Greefield rollout strategy1

illustrative

25clientxx\kunde\present\pres0000.ppt/w

1

Despite substantial savings that can be achieved by infrastructure sharingagreements in the short run, negative implications can affect the long termbusiness case

Top cost reduction results fromnetwork sharing business cases

Source: Arthur D. Little network sharing business case

CAPEX OPEX Peak funding

100%(=full independentroll-out accordingto regulatoryrequirements)

50%

-40% -40%

-60%

Negative long runeffect due to- co-ordination cost- legal risks- operational risks- ...

Infrastructure sharing - Long run cost view

26clientxx\kunde\present\pres0000.ppt/w

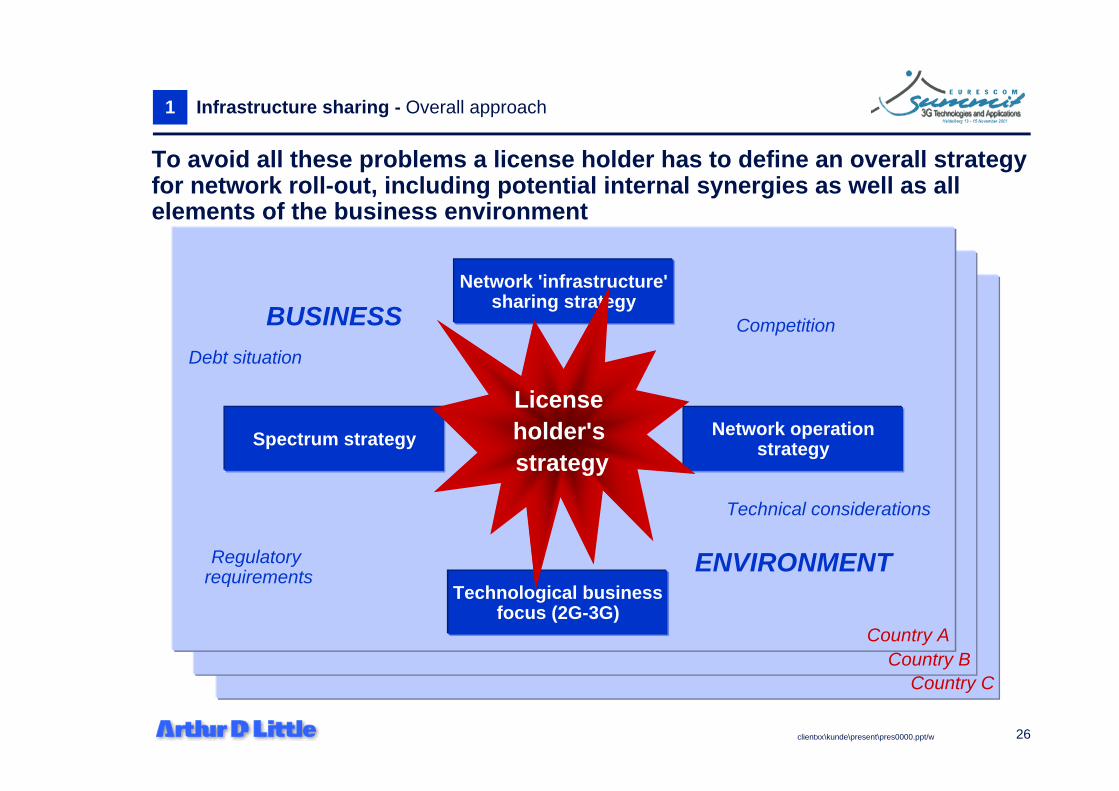

BUSINESS

ENVIRONMENT

Country C

BUSINESS

ENVIRONMENT

Country B

1

To avoid all these problems a license holder has to define an overall strategyfor network roll-out, including potential internal synergies as well as allelements of the business environment

Infrastructure sharing - Overall approach

BUSINESS

ENVIRONMENT

Country A

Network 'infrastructure'sharing strategy

Technological businessfocus (2G-3G)

Spectrum strategy Network operationstrategy

Regulatory requirements

Competition

Debt situation

Technical considerations

License holder's strategy

27clientxx\kunde\present\pres0000.ppt/w

Table of contents

1 Infrastructure sharing

Typical approach and methodology2

28clientxx\kunde\present\pres0000.ppt/w

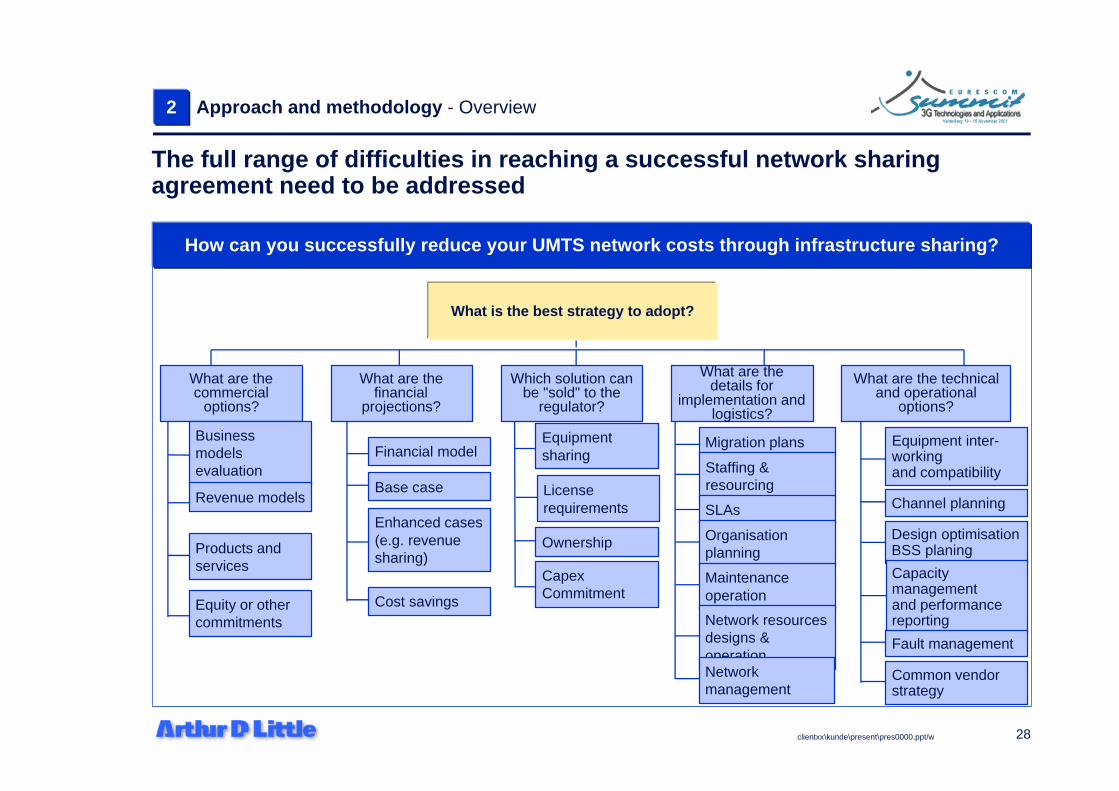

How can you successfully reduce your UMTS network costs through infrastructure sharing?

What are thecommercial

options?

What are thefinancial

projections?

What are thedetails for

implementation andlogistics?

Equipment inter-workingand compatibility

Channel planning

Design optimisationBSS planing

Capacitymanagementand performancereporting

Fault management

Common vendorstrategy

What are the technicaland operational

options?

Businessmodelsevaluation

Products andservices

Equity or othercommitments

Financial model

Base case

Enhanced cases(e.g. revenuesharing)

Cost savings

Migration plans

Staffing &resourcing

SLAs

Organisationplanning

Maintenanceoperation

Network resourcesdesigns &operation

Revenue models

Which solution canbe "sold" to the

regulator?

Equipmentsharing

Ownership

CapexCommitment

Licenserequirements

What is the best strategy to adopt?

Networkmanagement

The full range of difficulties in reaching a successful network sharingagreement need to be addressed

Approach and methodology - Overview2

29clientxx\kunde\present\pres0000.ppt/w

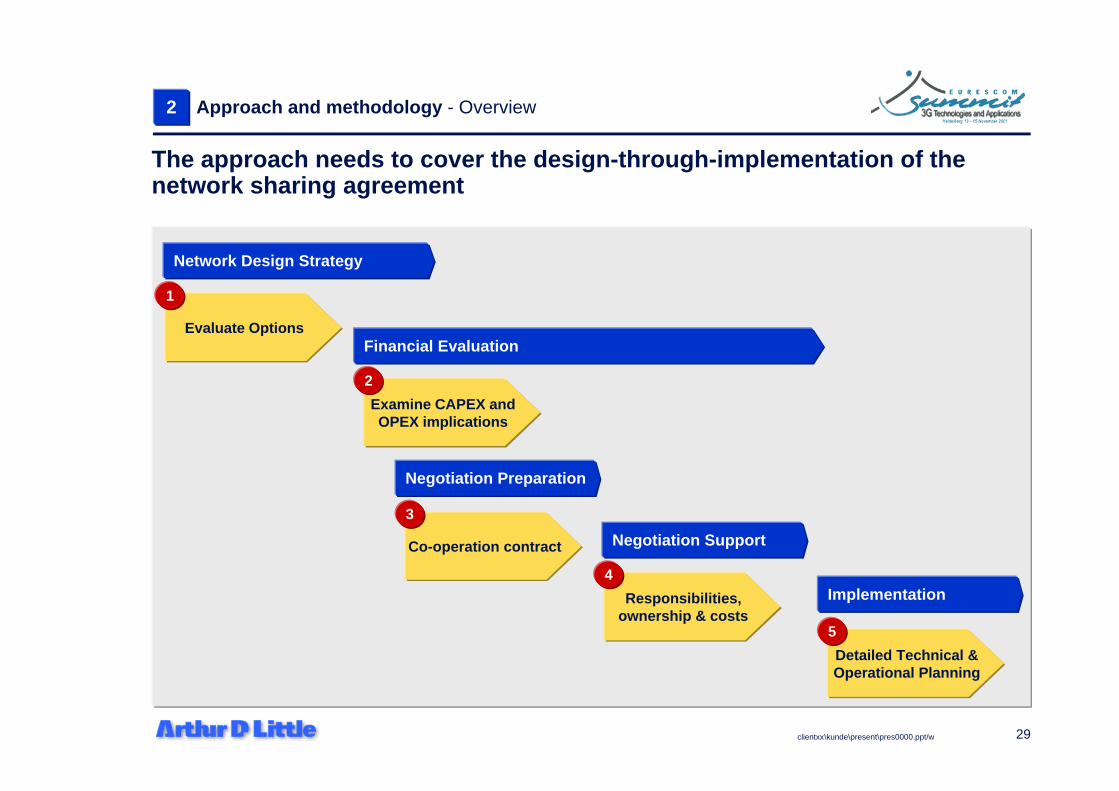

Network Design Strategy

Negotiation Preparation

Examine CAPEX andOPEX implications

2

Responsibilities,ownership & costs

4

Detailed Technical &Operational Planning

5

Co-operation contract

3

Evaluate Options

1

Negotiation Support

Financial Evaluation

Implementation

The approach needs to cover the design-through-implementation of thenetwork sharing agreement

Approach and methodology - Overview2

30clientxx\kunde\present\pres0000.ppt/w

StepsIdentify NetworkDesign Options

1Evaluate NetworkDesign Options

2Select preferredoptions

3

Tasks

• Explore competitors willingnessto cooperate

• Determine current competitorsituation

– GSM status

– UMTS vendor selection

• Determine interworking andinterconnections possibilities

• Determine internationalresources (within the company)available for sharing

Network Design Strategy

Results

• Is a harmonisation of vendorstrategies possible?

• GSM/UMTS roaming possibilities

• Viability of network infrastructuresharing options I-IV

• Ownership options and costestimates

• Check fit with Group technicalplans for other Europeanholdings

• Select preferred option to pursuein negotiations (Operators) andlobbying activities (Reg.Authority)

• Identify fallback positions

• Identify no-go limit

Understanding of the regulatory,competitive and technical UMTSenvironment

Clear negotiation position withfallback position identified

Clear lobbying position towardsReg Auth.

Technical and commercialevaluation of the main optionsavailable

Approach and methodology - Network design strategy2

The approach needs to cover the design-through-implementation of thenetwork sharing agreement

31clientxx\kunde\present\pres0000.ppt/w

Steps Evaluate CAPEX

1

Evaluate OPEX

2

Ongoing support

3

Tasks

• Determine capex requirementsfor the selected options

– UTRAN– Core network– Transmission– Application platforms

(if applicable)– etc

• Based upon Group's UMTSrollout/coverage plans (forEurope)

Results

• Ongoing business planningsupport during the negotiationphase

View of CAPEX requirements, withsensitivity analysis for negotiation

Clear identification of currentnegotiation position with financialimplications

Financial Evaluation

• Determine opex requirementsfor the selected options

– Geo split– Common infrastructure– UTRAN only– etc

• Modelling of national roamingcosts based upon current marketforecasts

View of OPEX requirements, withsensitivity analysis for negotiation

Approach and methodology - Financial evaluation2

The approach needs to cover the design-through-implementation of thenetwork sharing agreement

32clientxx\kunde\present\pres0000.ppt/w

StepsCo-operationIssues

1

Tasks• Identify the key elements of the

co-operation contract

– Level of co-operation

– Vendor relationships

– Service Level Agreements

• Draft responsibility matrix– Design– Implementation– Operations

• Draft line for negotiation withother Group units in Europe

Results Draft contract elements and terms

Negotiation Preparation

Draft Contract

2

• Draft contract terms review

• Local legal support required

Draft contract elements and terms

Approach and methodology - Negotiation preparation2

The approach needs to cover the design-through-implementation of thenetwork sharing agreement

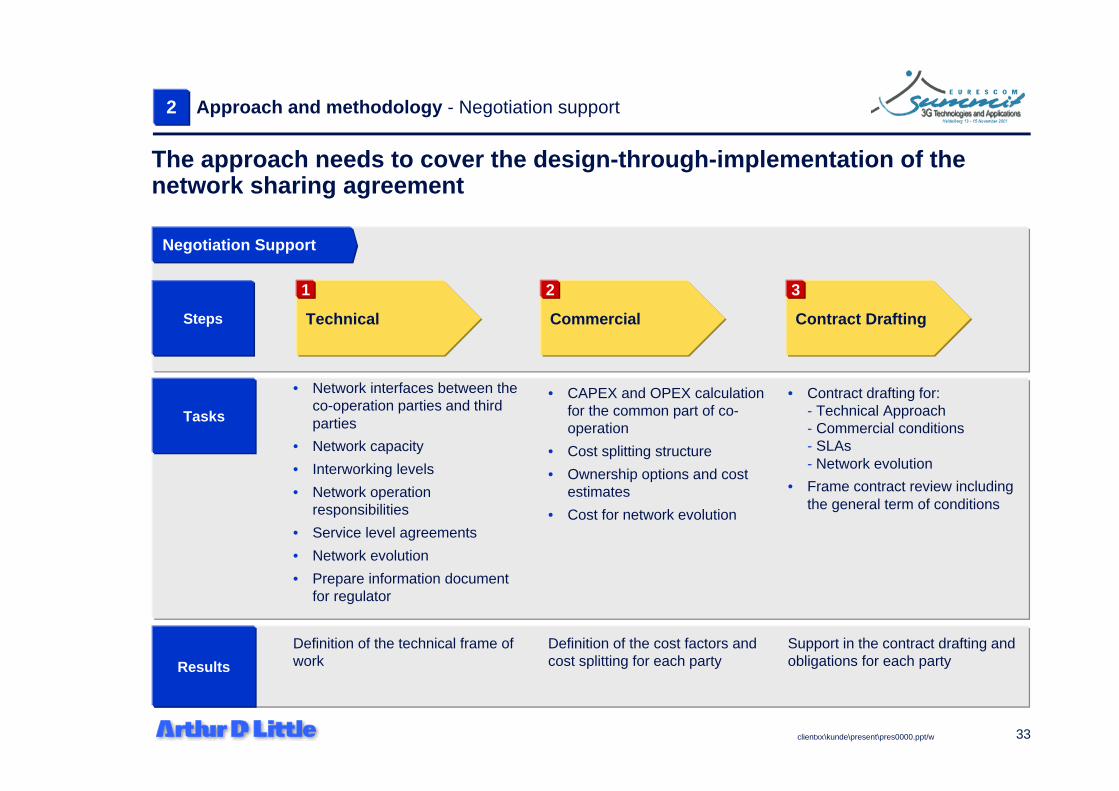

33clientxx\kunde\present\pres0000.ppt/w

Steps Technical

1

Commercial

2

Contract Drafting

3

Tasks

• Network interfaces between theco-operation parties and thirdparties

• Network capacity

• Interworking levels

• Network operationresponsibilities

• Service level agreements

• Network evolution

• Prepare information documentfor regulator

Results

• CAPEX and OPEX calculationfor the common part of co-operation

• Cost splitting structure

• Ownership options and costestimates

• Cost for network evolution

• Contract drafting for:- Technical Approach- Commercial conditions- SLAs- Network evolution

• Frame contract review includingthe general term of conditions

Definition of the technical frame ofwork

Support in the contract drafting andobligations for each party

Definition of the cost factors andcost splitting for each party

Negotiation Support

Approach and methodology - Negotiation support2

The approach needs to cover the design-through-implementation of thenetwork sharing agreement

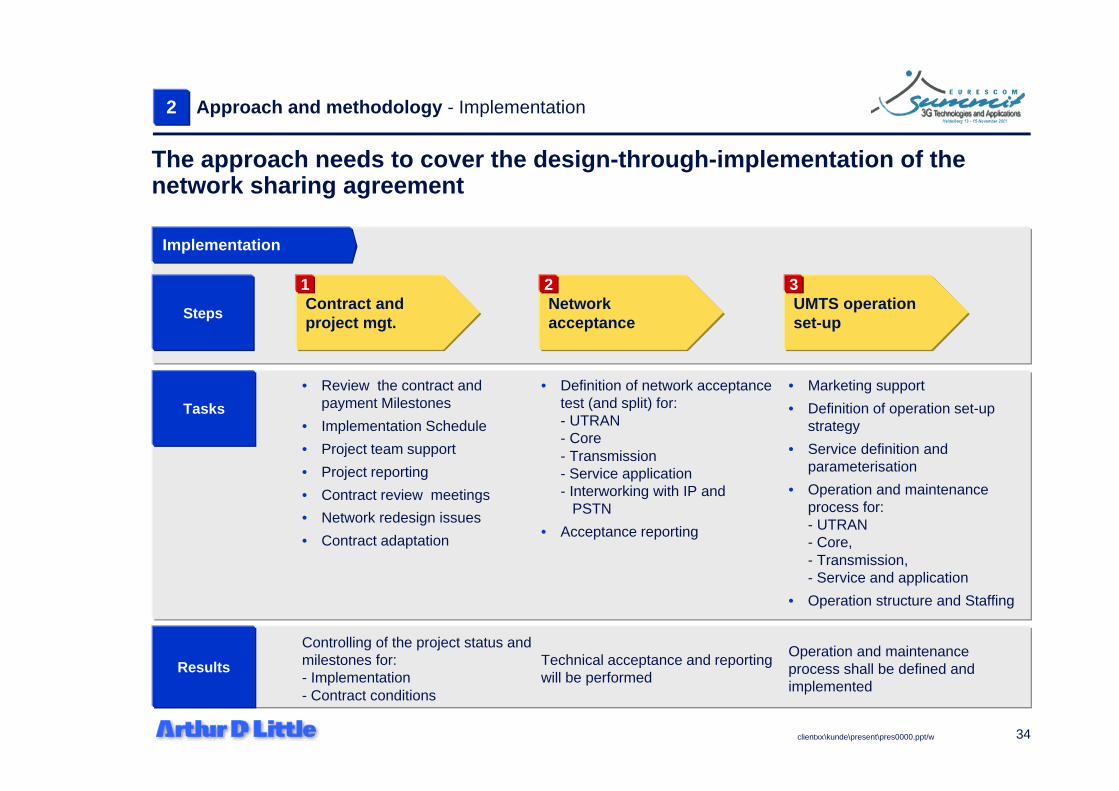

34clientxx\kunde\present\pres0000.ppt/w

StepsContract andproject mgt.

1Networkacceptance

2UMTS operationset-up

3

Tasks

• Review the contract andpayment Milestones

• Implementation Schedule

• Project team support

• Project reporting

• Contract review meetings

• Network redesign issues

• Contract adaptation

Results

• Definition of network acceptancetest (and split) for:- UTRAN- Core- Transmission- Service application- Interworking with IP and PSTN

• Acceptance reporting

• Marketing support

• Definition of operation set-upstrategy

• Service definition andparameterisation

• Operation and maintenanceprocess for:- UTRAN- Core,- Transmission,- Service and application

• Operation structure and Staffing

Controlling of the project status andmilestones for:- Implementation- Contract conditions

Operation and maintenanceprocess shall be defined andimplemented

Technical acceptance and reportingwill be performed

Implementation

Approach and methodology - Implementation2

The approach needs to cover the design-through-implementation of thenetwork sharing agreement