Embed Size (px)

Citation preview

ULTRAPETROL ULTRAPETROL (Bahamas) Limited(Bahamas) Limited

Smart Rivers 2011

Presentation

New Orleans, LA

September 15, 2011

“Long-term prospects of the Hidrovia Region

in South America”

Our disclosure and analysis in this presentation concerning our operations, cash flows and financial position, including, in particular, the likelihood of our success in developing and expanding our business, include forward-looking statements. Statements that are predictive in nature, that depend upon or refer to future events or conditions, or that include words such as ‘‘expects,’’ ‘‘anticipates,’’ ‘‘intends,’’ ‘‘plans,’’ ‘‘believes,’’ ‘‘estimates,’’ ‘‘projects,’’ ‘‘forecasts,’’ ‘‘will,’’ ‘‘may,’’ ‘‘should,’’ and similar expressions are forward-looking statements. Although these statements are based upon assumptions we believe to be reasonable based upon available information, including projections of revenues, operating margins, earnings, cash flow, working capital, and capital expenditures, they are subject to risks and uncertainties. These forward-looking statements represent our estimates and assumptions only as of the date of this presentation and are not intended to give any assurance as to future results. As a result, you should not place undue reliance on any forward-looking statements. We assume no obligation to update any forward-looking statements to reflect actual results, changes in assumptions or changes in other factors, except as required by applicable securities laws.

Factors that might cause future results to differ include, but are not limited to, the following:– unexpected future operating or financial results– delays or increased costs in pending or recent acquisitions, deviations from our business strategy or unexpected increases in

capital spending or operating expenses, including drydocking and insurance costs– changes in general market conditions and trends, including charter rates, vessel values, and factors affecting vessel supply and

demand– our ability to obtain additional financing– changes in our financial condition and liquidity, including our ability to obtain financing in the future to fund capital

expenditures, acquisitions and other general corporate activities

Forward Looking Statements & EBITDA

2

expenditures, acquisitions and other general corporate activities– deviations from our expectations about the availability of vessels to purchase, the time that it may take to construct new vessels, or

vessels’ useful lives– delays or defaults by our contract counter-parties in performing their obligations to us– loss of one or more key members of our management team– changes in governmental rules and regulations or actions taken by regulatory authorities– adverse weather conditions that can affect production of the goods we transport and navigability of the river system– the highly competitive nature of the oceangoing transportation industry– the loss of one or more key customers– unexpected fluctuations in foreign exchange rates and devaluations– liabilities from future litigation– other factors discussed in the section titled ‘‘Risk factors” in our annual report on form 20-F for the year ended December 31, 2010– Adjusted EBITDA consists of net income (loss) prior to deductions for interest expense and other financial gains and losses related

to the financing of the Company, income taxes, depreciation of vessels and equipment and amortization of drydock expense, intangible assets, financial gain (loss) on extinguishment of debt and a premium paid for redemption of preferred shares. We have provided Adjusted EBITDA in this report because we use it to, and believe it provides useful information to investors toevaluate our ability to incur and service indebtedness. We do not intend for Adjusted EBITDA to represent cash flows from operations, as defined by GAAP (on the date of calculation) and it should not be considered as an alternative to measure our liquidity. This definition of Adjusted EBITDA may not be comparable to similarly titled measures disclosed by other companies. Generally, funds represented by Adjusted EBITDA are available for management’s discretionary use. Adjusted EBITDA has limitations as an analytical tool, and should not be considered in isolation, or as a substitute for analysis of our results as reported.

Hidrovia Waterway System – Navigation

�Navigation in this river started in the 16th century

3

�Commercial navigation in the Hidrovia picked up momentum as of the second half of the 19th

century

Jesuitical Map 1667

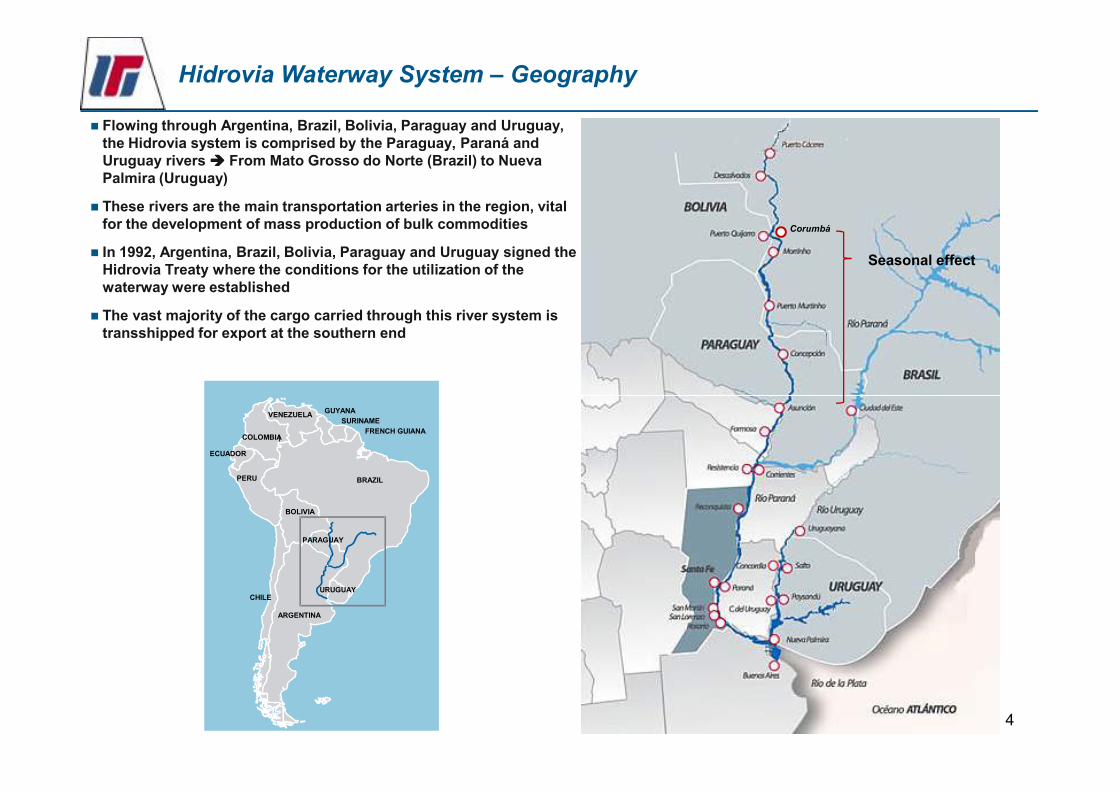

Hidrovia Waterway System – Geography

� Flowing through Argentina, Brazil, Bolivia, Paraguay and Uruguay, the Hidrovia system is comprised by the Paraguay, Paraná and Uruguay rivers ���� From Mato Grosso do Norte (Brazil) to Nueva Palmira (Uruguay)

� These rivers are the main transportation arteries in the region, vital for the development of mass production of bulk commodities

� In 1992, Argentina, Brazil, Bolivia, Paraguay and Uruguay signed the Hidrovia Treaty where the conditions for the utilization of the waterway were established

� The vast majority of the cargo carried through this river system is transshipped for export at the southern end

Corumbá

Seasonal effect

4

PARAGUAY

BRAZIL

SURINAME

GUYANAVENEZUELA

ARGENTINA

ECUADOR

FRENCH GUIANACOLOMBIA

PERU

BOLIVIA

CHILEURUGUAY

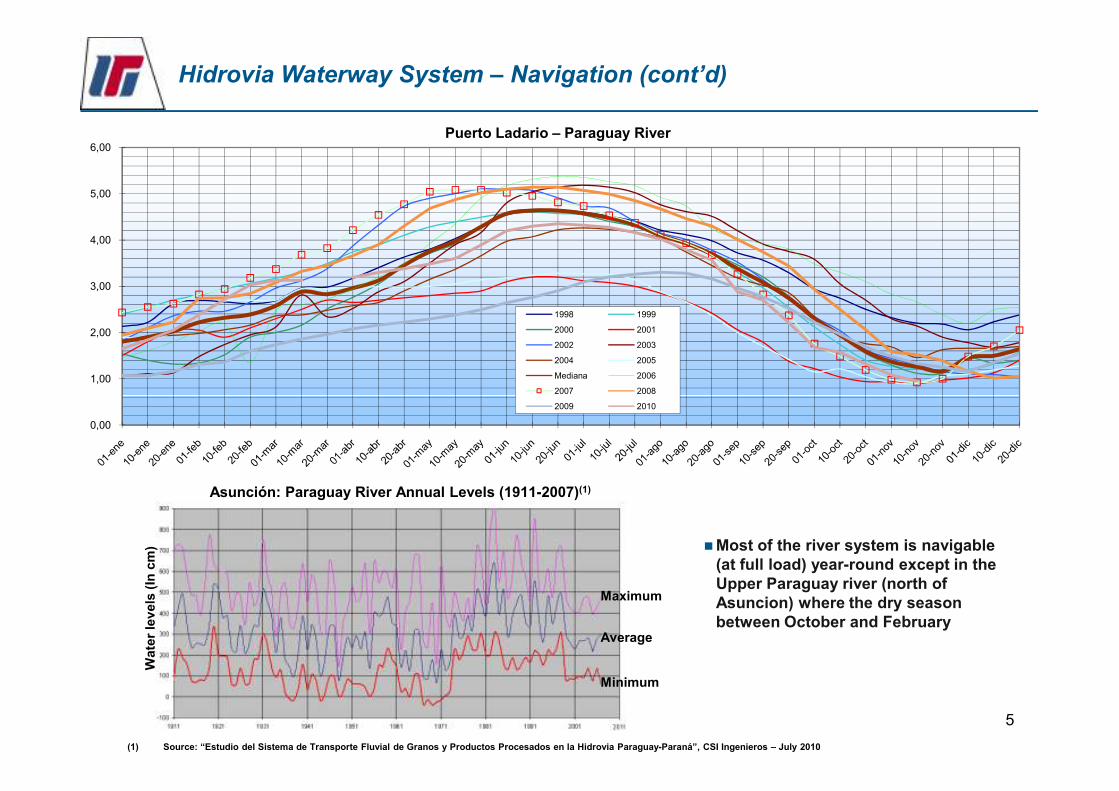

Hidrovia Waterway System – Navigation (cont’d)

1,00

2,00

3,00

4,00

5,00

6,00

1998 1999

2000 2001

2002 2003

2004 2005

Mediana 2006

2007 2008

Puerto Ladario – Paraguay River

5

�Most of the river system is navigable (at full load) year-round except in the Upper Paraguay river (north of Asuncion) where the dry season between October and February

Asunción: Paraguay River Annual Levels (1911-2007)(1)

(1) Source: “Estudio del Sistema de Transporte Fluvial de Granos y Productos Procesados en la Hidrovia Paraguay-Paraná”, CSI Ingenieros – July 2010

Wate

r le

vels

(In

cm

)

Maximum

Average

Minimum

0,00

2007 2008

2009 2010

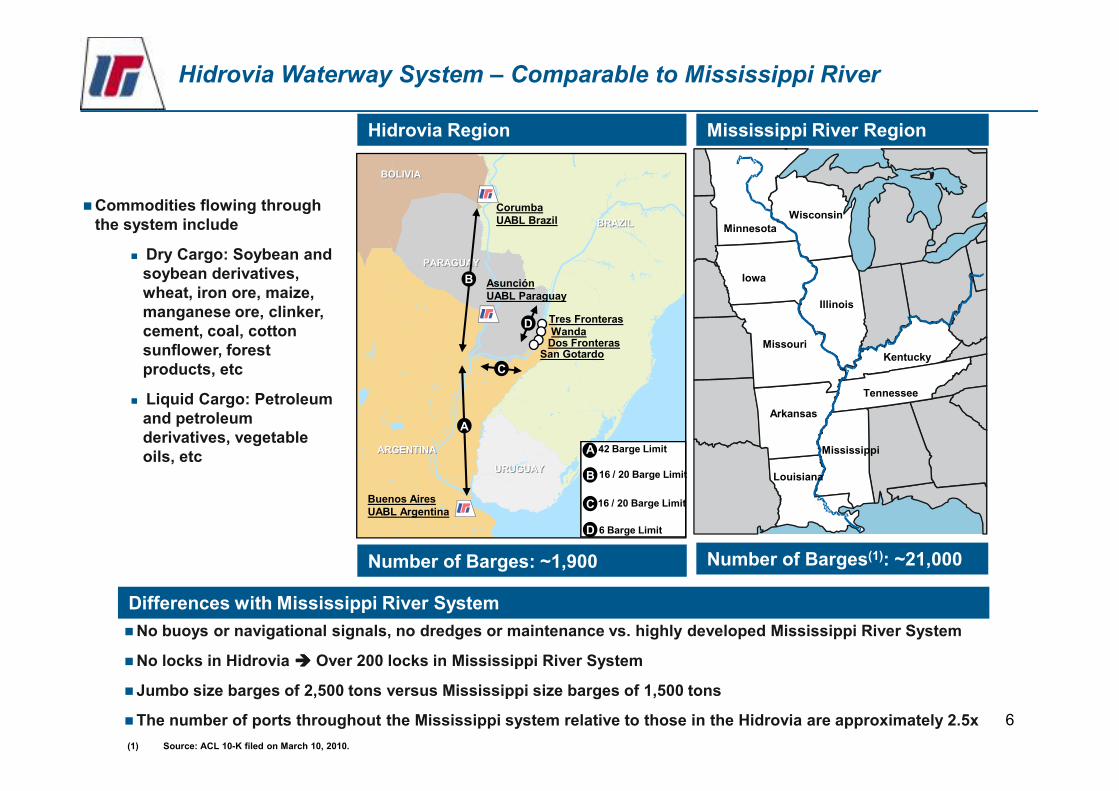

Hidrovia Waterway System – Comparable to Mississippi River

Hidrovia Region Mississippi River Region

Illinois

Kentucky

Tennessee

Missouri

Iowa

Minnesota

Wisconsin�Commodities flowing through

the system include

� Dry Cargo: Soybean and soybean derivatives, wheat, iron ore, maize, manganese ore, clinker, cement, coal, cotton sunflower, forest products, etc

Liquid Cargo: Petroleum

BRAZILBRAZIL

PARAGUAYPARAGUAY

BOLIVIABOLIVIA

CorumbaUABL Brazil

Tres FronterasWanda

Dos FronterasSan Gotardo

AsunciónUABL Paraguay

B

C

D

6

Number of Barges: ~1,900 Number of Barges(1): ~21,000

(1) Source: ACL 10-K filed on March 10, 2010.

Tennessee

Mississippi

Louisiana

Arkansas

�No buoys or navigational signals, no dredges or maintenance vs. highly developed Mississippi River System

�No locks in Hidrovia ���� Over 200 locks in Mississippi River System

�Jumbo size barges of 2,500 tons versus Mississippi size barges of 1,500 tons

�The number of ports throughout the Mississippi system relative to those in the Hidrovia are approximately 2.5x

� Liquid Cargo: Petroleum and petroleum derivatives, vegetable oils, etc

URUGUAYURUGUAY

ARGENTINAARGENTINA

Buenos AiresUABL Argentina

A

A

B

C

D

42 Barge Limit

16 / 20 Barge Limit

16 / 20 Barge Limit

6 Barge Limit

Differences with Mississippi River System

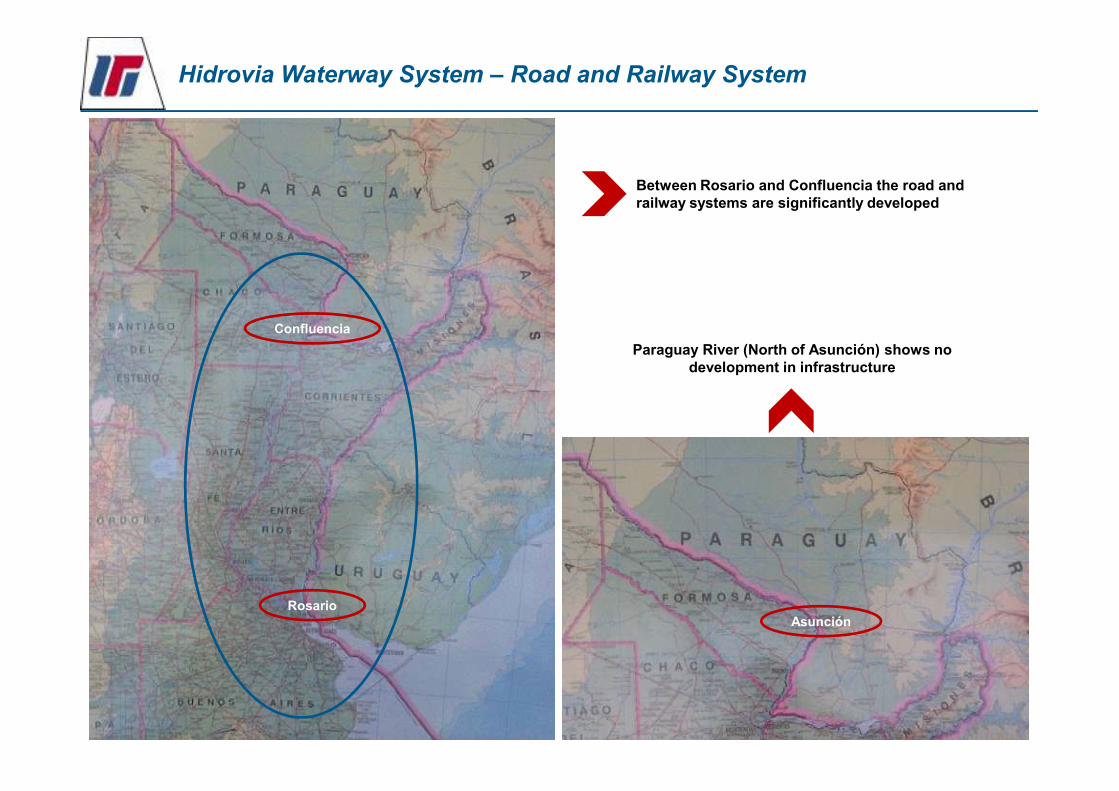

Hidrovia Waterway System – Road and Railway System

Between Rosario and Confluencia the road and railway systems are significantly developed

Confluencia

Paraguay River (North of Asunción) shows no development in infrastructure

7

RosarioAsunción

0,4 0,61,0 1,1 1,1 1,0 1,1 1,2 1,2 1,2 1,4 1,4 1,6

1,9 2,02,4 2,4 2,7 2,6 2,7 2,8

0,61,0

1,6 1,82,2 2,4

2,8 3,0 3,0 2,93,5 3,5

4,53,9 4,0

3,6

5,9

6,9

4,0

7,2

8,3

0

1

2

3

4

5

6

7

8

9

Millio

n H

ecta

res &

To

ns

Seeded Area Production

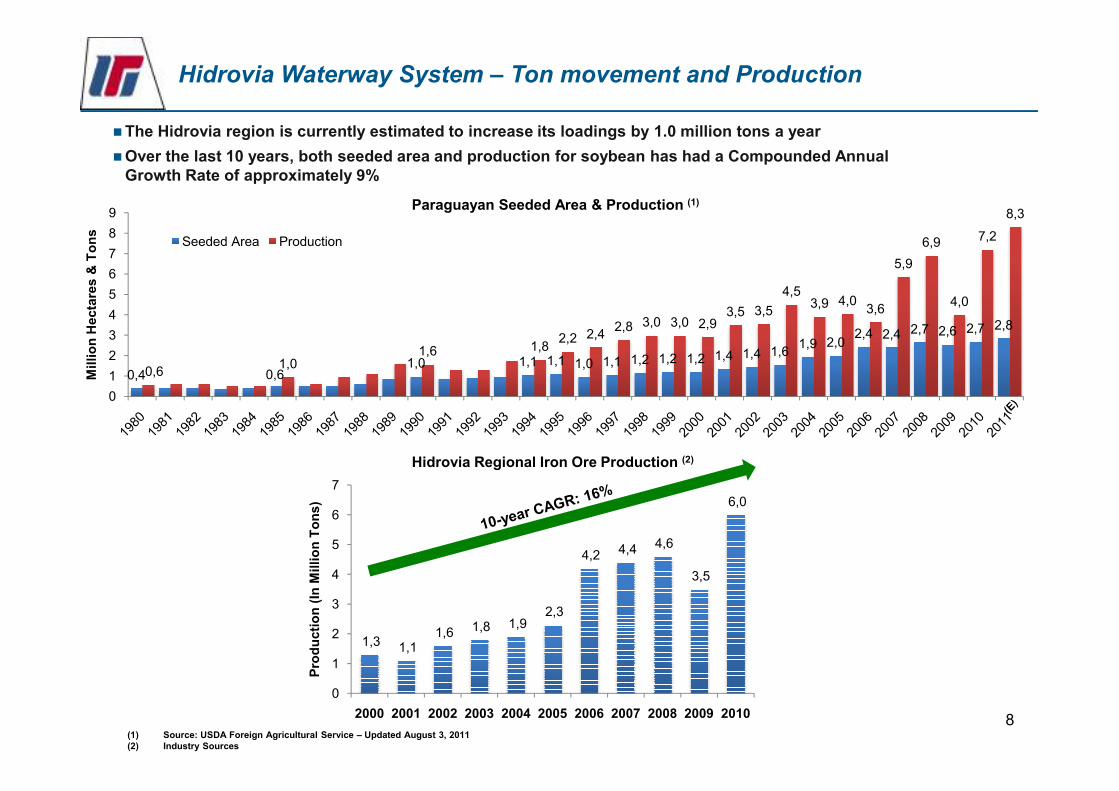

Hidrovia Waterway System – Ton movement and Production

�The Hidrovia region is currently estimated to increase its loadings by 1.0 million tons a year

Paraguayan Seeded Area & Production (1)

�Over the last 10 years, both seeded area and production for soybean has had a Compounded Annual Growth Rate of approximately 9%

8

0

1,3 1,1 1,6 1,8 1,9

2,3

4,2 4,4 4,6

3,5

6,0

0

1

2

3

4

5

6

7

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Pro

du

cti

on

(In

Millio

n T

on

s)

(1) Source: USDA Foreign Agricultural Service – Updated August 3, 2011(2) Industry Sources

Hidrovia Regional Iron Ore Production (2)

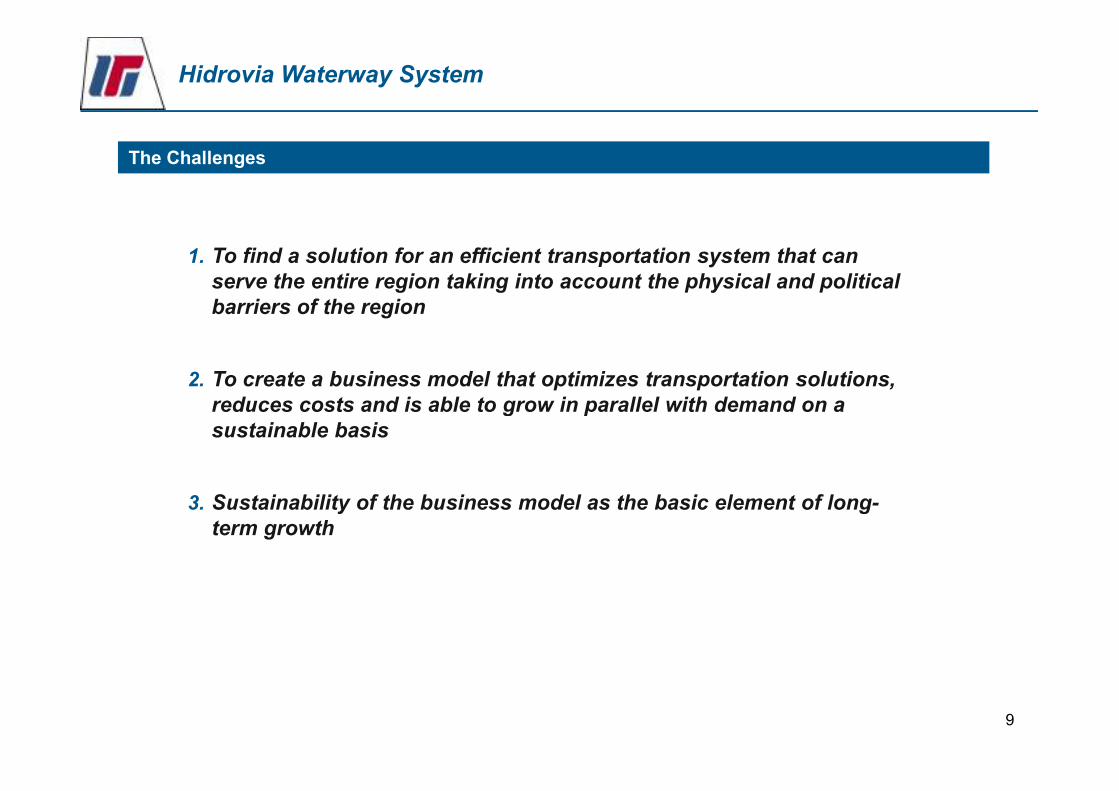

Hidrovia Waterway System

1. To find a solution for an efficient transportation system that can

serve the entire region taking into account the physical and political

barriers of the region

2. To create a business model that optimizes transportation solutions,

reduces costs and is able to grow in parallel with demand on a

The Challenges

9

reduces costs and is able to grow in parallel with demand on a

sustainable basis

3. Sustainability of the business model as the basic element of long-

term growth

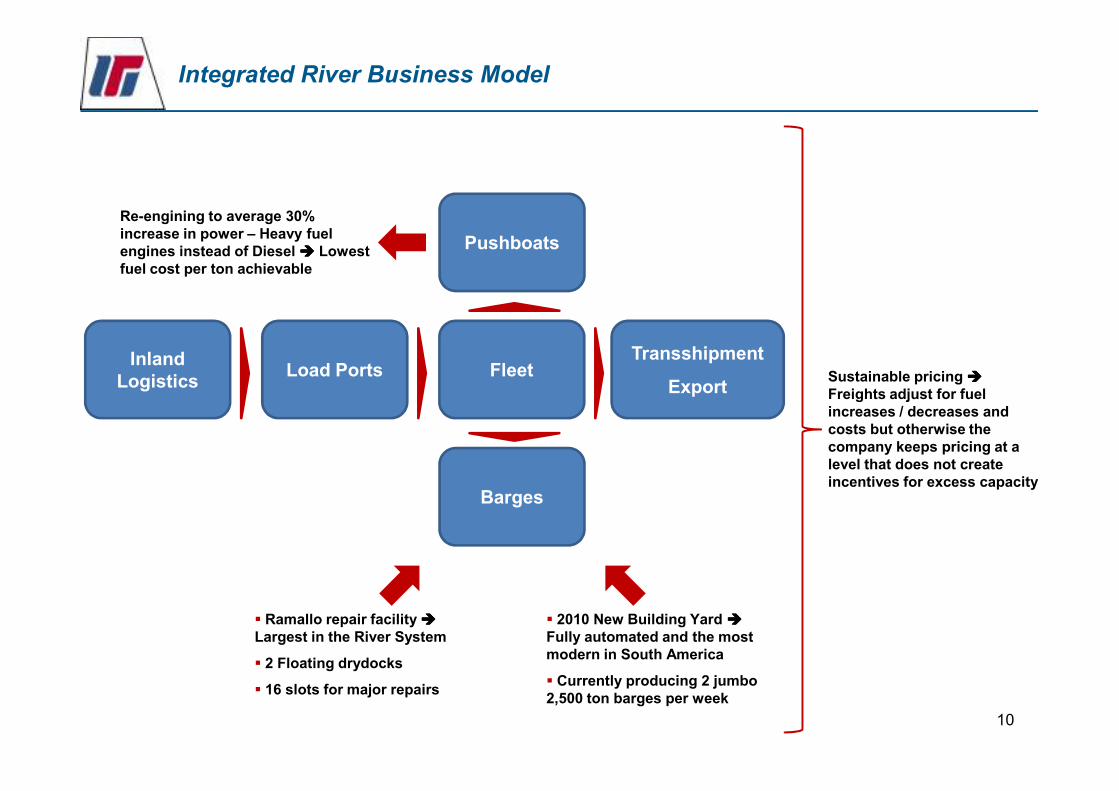

Integrated River Business Model

Fleet

Pushboats

Transshipment

ExportLoad Ports

Inland Logistics

Re-engining to average 30% increase in power – Heavy fuel engines instead of Diesel ���� Lowest fuel cost per ton achievable

Sustainable pricing ����Freights adjust for fuel

10

Export

Barges

� Ramallo repair facility ����Largest in the River System

� 2 Floating drydocks

� 16 slots for major repairs

� 2010 New Building Yard ����Fully automated and the most modern in South America

� Currently producing 2 jumbo 2,500 ton barges per week

Freights adjust for fuel increases / decreases and costs but otherwise the company keeps pricing at a level that does not create incentives for excess capacity

3 Fronteras Terminal

11

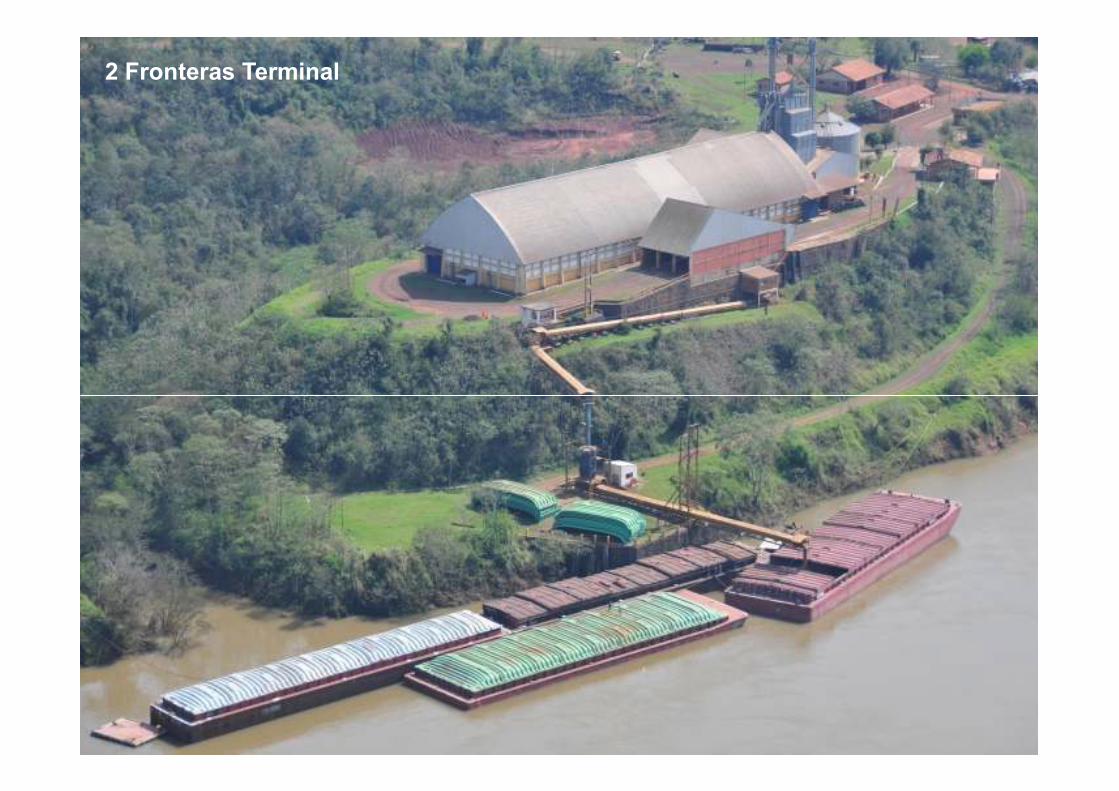

2 Fronteras Terminal

12

Zonda I, 8,300 HP heavy-fuel pushboat

13

42-barge tow

Ramallo repair facility

Punta Alvear barge-building facility

Robotic Welding Gantry

Alianza G2 Transshipment Station

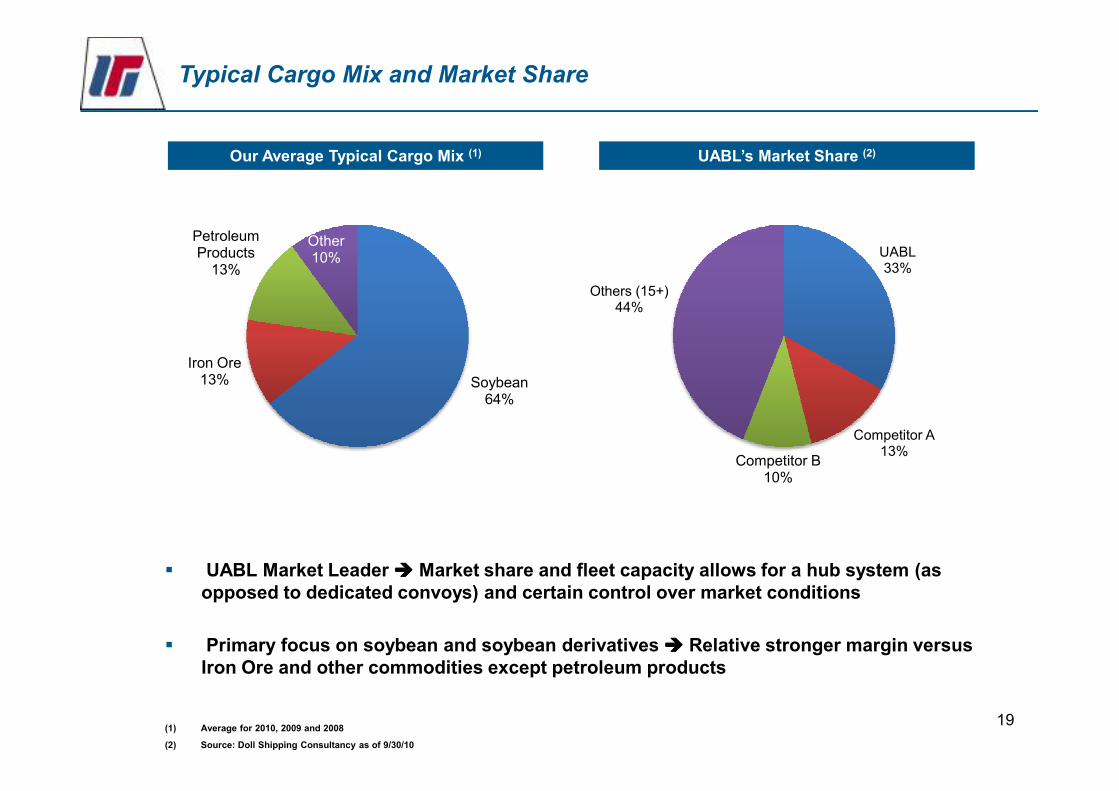

Our Average Typical Cargo Mix (1) UABL’s Market Share (2)

Soybean64%

Iron Ore13%

Petroleum Products13%

Other10% UABL

33%

Others (15+)44%

Typical Cargo Mix and Market Share

19(1) Average for 2010, 2009 and 2008

(2) Source: Doll Shipping Consultancy as of 9/30/10

� UABL Market Leader ���� Market share and fleet capacity allows for a hub system (as opposed to dedicated convoys) and certain control over market conditions

� Primary focus on soybean and soybean derivatives ���� Relative stronger margin versus Iron Ore and other commodities except petroleum products

64%

Competitor A13%

Competitor B10%

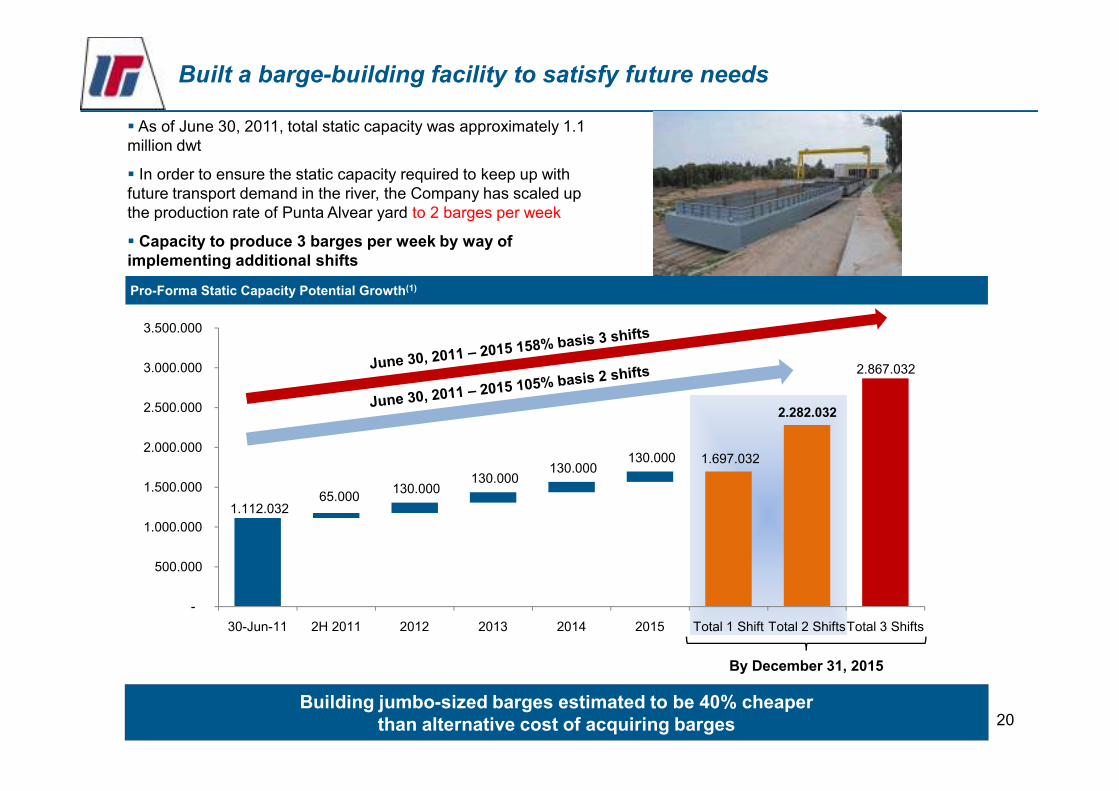

2.867.032 3.000.000

3.500.000

Pro-Forma Static Capacity Potential Growth(1)

Built a barge-building facility to satisfy future needs

� As of June 30, 2011, total static capacity was approximately 1.1 million dwt

� In order to ensure the static capacity required to keep up with future transport demand in the river, the Company has scaled up the production rate of Punta Alvear yard to 2 barges per week

� Capacity to produce 3 barges per week by way of implementing additional shifts

20

1.112.032 65.000

130.000 130.000

130.000 130.000 1.697.032

2.282.032

-

500.000

1.000.000

1.500.000

2.000.000

2.500.000

30-Jun-11 2H 2011 2012 2013 2014 2015 Total 1 Shift Total 2 ShiftsTotal 3 Shifts

Building jumbo-sized barges estimated to be 40% cheaperthan alternative cost of acquiring barges

By December 31, 2015

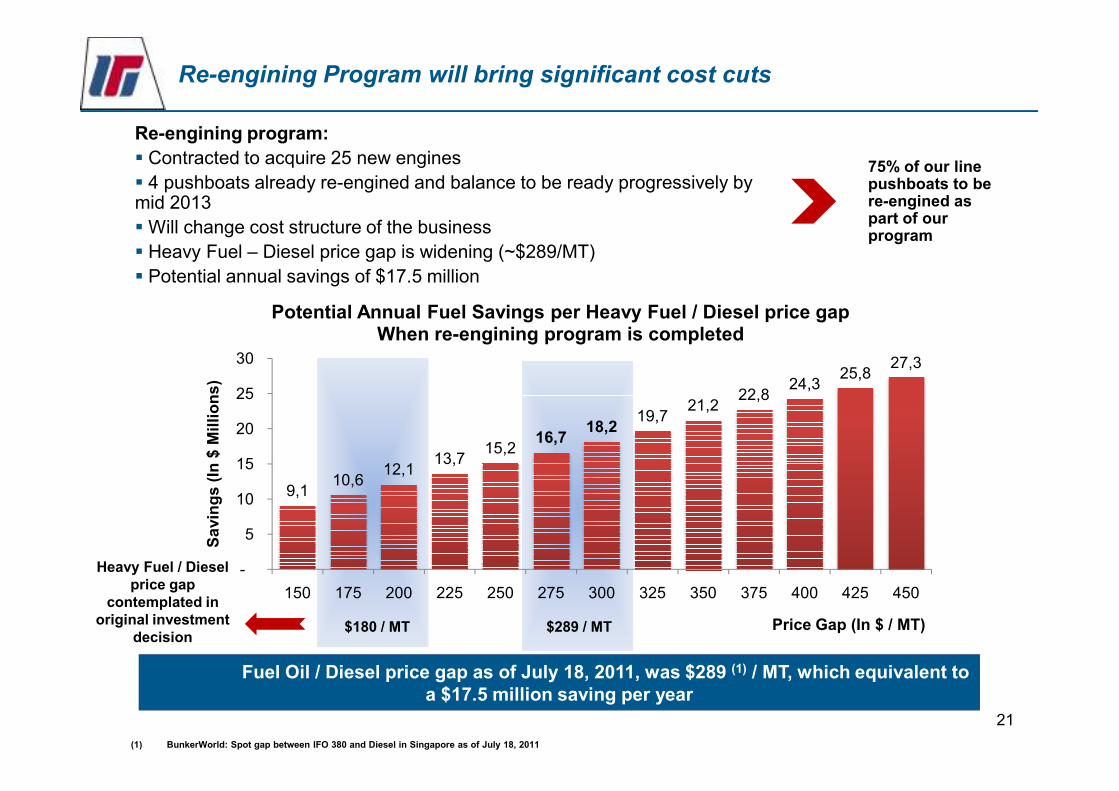

Re-engining Program will bring significant cost cuts

75% of our line pushboats to be re-engined as part of our program

22,824,3

25,827,3

25

30

Sa

vin

gs

(In

$ M

illi

on

s)

Potential Annual Fuel Savings per Heavy Fuel / Diesel price gap When re-engining program is completed

Re-engining program:

� Contracted to acquire 25 new engines

� 4 pushboats already re-engined and balance to be ready progressively by mid 2013

�Will change cost structure of the business

� Heavy Fuel – Diesel price gap is widening (~$289/MT)

� Potential annual savings of $17.5 million

21

Fuel Oil / Diesel price gap as of July 18, 2011, was $289 (1) / MT, which equivalent to a $17.5 million saving per year

$289 / MT$180 / MT

Heavy Fuel / Diesel price gap

contemplated in original investment

decision

(1) BunkerWorld: Spot gap between IFO 380 and Diesel in Singapore as of July 18, 2011

9,110,6

12,113,7

15,216,7

18,219,7

21,222,8

-

5

10

15

20

25

150 175 200 225 250 275 300 325 350 375 400 425 450

Sa

vin

gs

(In

$ M

illi

on

s)

Price Gap (In $ / MT)

180,6

160

180

200

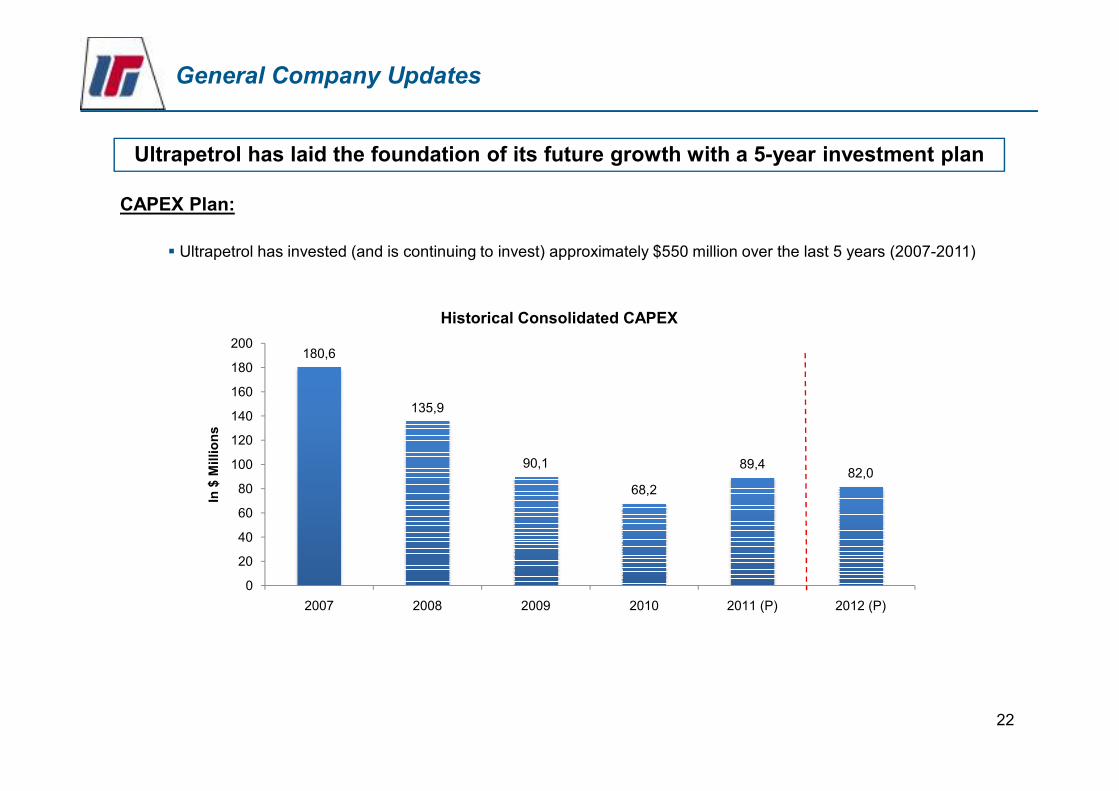

Historical Consolidated CAPEX

General Company Updates

CAPEX Plan:

� Ultrapetrol has invested (and is continuing to invest) approximately $550 million over the last 5 years (2007-2011)

Ultrapetrol has laid the foundation of its future growth with a 5-year investment plan

22

135,9

90,1

68,2

89,482,0

0

20

40

60

80

100

120

140

160

2007 2008 2009 2010 2011 (P) 2012 (P)

In $

Millio

ns

Long-term opportunities

5 years from now?

� Ultrapetrol / UABL will have tripled its carrying capacity through fleet expansion and increased power ���� lowest operational cost per ton

� Consuming heavy fuel ���� Lowest fuel cost per ton

23

� Consuming heavy fuel ���� Lowest fuel cost per ton

� We intend to build 6 ports for loading / discharging bulk cargoes (agriproducts + minerals) ���� Consolidate the lowest cost for logistics

� Maintain pricing at a level that does not create incentives for excess capacity ����Maintain market leadership on a sustainable basis

24