Embed Size (px)

Citation preview

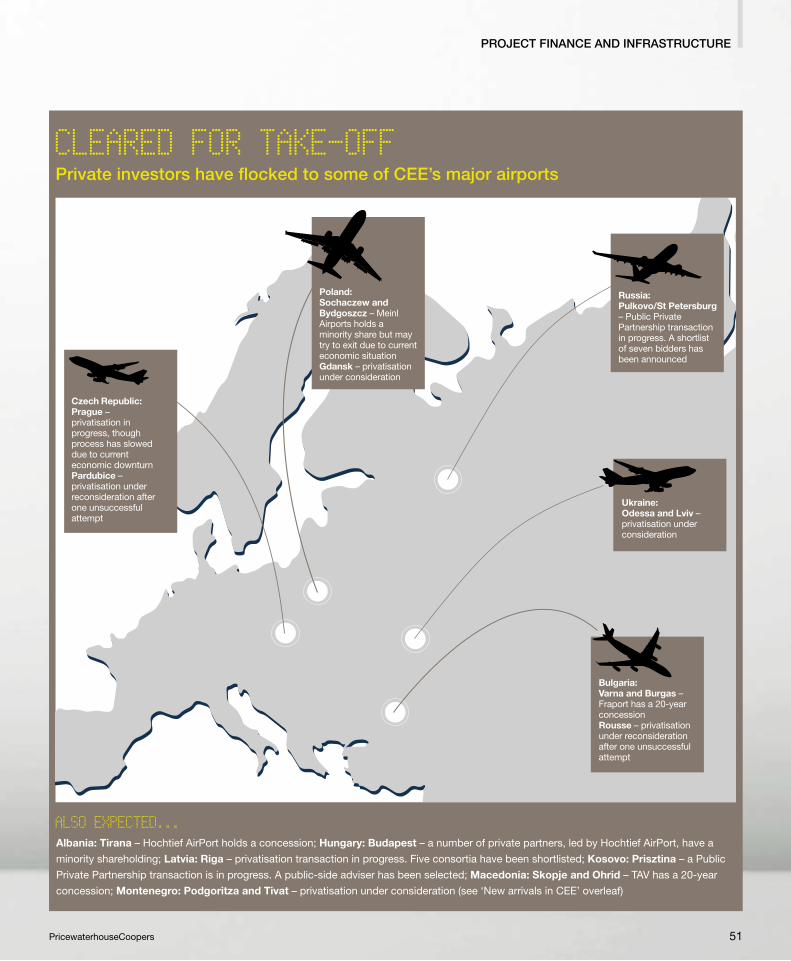

Now boardingWhy governments are rushing to revitalise the region’s airports

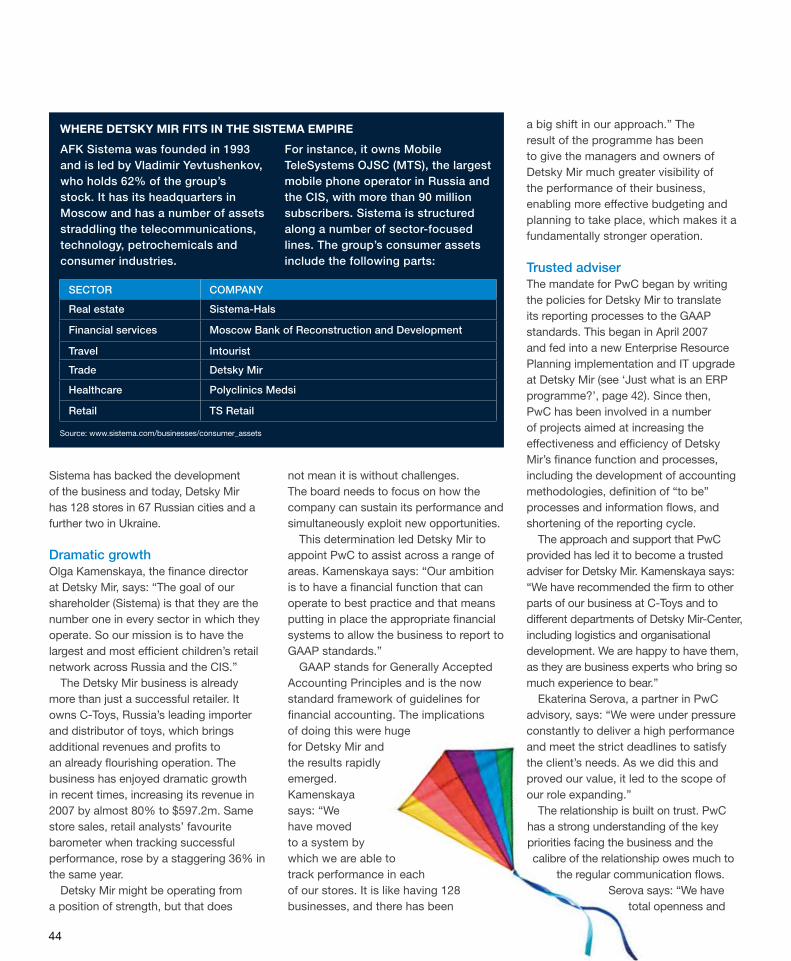

Child’s playAll systems go at Russia’s largest toy retailer

Food loversRetailers Tesco and Metro seek a bigger slice of the market

Made in DonetskUkraine’s SCM reveals its international expansion plans

Transform Issue 3/Spring 2009

© 2009 PricewaterhouseCoopers. All rights reserved. “PricewaterhouseCoopers” refers to the network of member firms of PricewaterhouseCoopers International Limited, each of which is a separate and independent legal entity.

ContactsCEE AdvISoRy REgIonAL LEAdER

Mark okes-voysey

[email protected] +7 495 232 5713

ALbAnIA

Laura Qorlaze

[email protected] +355 4 242 254

boSnIA

Aida Soko

[email protected] +387 33 295 234

bULgARIA

bojidar neitchev

[email protected] +359 2 93 55 288

CRoATIA

Tanya Rukavina

[email protected] +385 1 6328 834

CzECh REPUbLIC

Jiri Moser

[email protected] +420 251 152 048

ESTonIA

Teet Tender

[email protected] +372 614 1800

gEoRgIA/ARMEnIA/AzERbAIJAn

Clifford Isaak

[email protected] +995 32 50 80 61

hUngARy

david Wake

[email protected] +36 1 461 9514

KAzAKhSTAn/UzbEKISTAn

vadim Khrapoun

[email protected] +7 495 232 5709

LATvIA

Arvids Kostomarovs

[email protected] +371 6709 4453

LIThUAnIA

vidas venckus

[email protected] +370 5 239 2308

MACEdonIA

Philippe bozier

[email protected] +389 23 111 012

PoLAnd

olga grygier

[email protected] +48 22 523 4214

RoMAnIA/MoLdovA

dinu bumbacea

[email protected] +40 21 202 882

RUSSIA

bob gruman

[email protected] +7 495 232 5725

SERbIA/MonTEnEgRo

Tanja gligorevic

[email protected] +381 11 33 02 100

SLovAKIA

Matt Pottle

[email protected] +4212 59350 402

SLovEnIA

Francois Mattelaer

[email protected] +386 1 58 36 000

UKRAInE

boris Krasnyansky

[email protected] +38 044 490 6777

PEoPLE

John Wynn

[email protected] +44 7802 948 447

TEChnoLogy

Philip gudgeon

[email protected] +7 495 232 5434

oPERATIonS And RESTRUCTURIng

Rafal Krasnodebski

[email protected] +48 22 523 4498

govERnAnCE, RISK And CoMPLIAnCE

Michelle Moore

[email protected] +7 495 967 6150

FInAnCE And ACCoUnTIng

Marc goessi

[email protected] +41 79 342 03 89

FInAnCIAL dUE dILIgEnCE

Mike Wilder

[email protected] +48 22 523 4413

CoMMERCIAL/STRATEgIC dUE dILIgEnCE

daniel Cappelletti

[email protected] +420 251 151 333

MERgERS & ACQUISITIonS

Chris butters

[email protected] +420 251 151 203

CoRPoRATE FInAnCE & InFRASTRUCTURE

nick Allen

[email protected] +420 251 151 330

CAPITAL MARKETS

Jim Klein

[email protected] +7 495 223 5177

vALUATIon

Tibor Almassy

[email protected] +36 1 461 9644

dISPUTE/FoREnSIC AnALySIS

John Wilkinson

[email protected] +7 495 967 6187

Tough conditionsRiding the economic storm

This publication has been prepared as general information on matters of interest only, and does not constitute professional advice. you should not act upon the information contained in this publication without obtaining specific professional advice. no representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, neither PricewaterhouseCoopers nor bladonmore accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

Pricew

aterhouseCoop

ers

T

RA

NS

FOR

M

Issue 3/S

pring 2009

© 2008 PricewaterhouseCoopers. All rights reserved. “PricewaterhouseCoopers” refers to the network of member firms of PricewaterhouseCoopers International Limited, each of which is a separate and independent legal entity.

*connectedthinking

Uncertainty isthe humanemotion thatsurfaces rightbefore geniusemerges.*

Change can uncover golden opportunities.Let us help you turn your complex businessissues into opportunity. What would you liketo change? Visit pwc.com/change

PricewaterhouseCoopers Central and Eastern Europe

Chief Executive OfficerMike Kubena +420 251 151 803

Managing Partner Advisory Mark Okes-Voysey +7 495 232 5713

Managing Partner AssuranceNick Brasington +7 495 967 63 99

Managing Partner Tax & Legal ServicesSteven Snaith +420 251 151 804

Awillingness to make and implement tough decisions is a distinguishing feature of all great business leaders. In recent years, the toughest decisions focused on how many new products to launch or which

overseas markets to enter. That was yesterday. Today, the decisions are tougher and are focused on where costs can be

sensibly cut; where new customers can be found to replace the old; and how to motivate your talent.

It is still a time of huge opportunity. Fortunes will undoubtedly be made by those who make the right decisions. The opportunities to acquire on valuations that have not been lower in more than a decade will provide a magnetic pull to some. Others will use this time to focus on their absolute distinguishing features and reposition themselves in the markets they operate in. New businesses will emerge.

PricewaterhouseCoopers works with clients throughout the region to transform their future, by making the important decisions now. This edition of Transform, for instance, highlights the importance of strategic cost reduction programmes which will be a major theme throughout 2009.

It is by no means all doom and gloom. Many firms are still seeking support to develop their growth strategies as they look to take advantage of these changing times. For instance, Detsky Mir, Russia’s largest children’s retailer, continues to grow and is profiled in this edition. Whatever challenge your business faces, PwC can assist. We look forward to standing shoulder to shoulder with you as we work through these difficult times.

We would be delighted to receive any feedback you have. You can email us at [email protected]

Mike Kubena

PricewaterhouseCoopersCEO Central and Eastern Europe:

Mike Kubena

Managing Partner Advisory in CEE:

Mark Okes-Voysey

Managing Partner Assurance in CEE:

Nick Brasington

Managing Partner Tax & Legal Services in CEE:

Steven Snaith

Industry Leaders in CEE:

Financial Services:

Paul Cunningham

Technology, InfoComm & Entertainment:

Dinu Bumbacea

Consumer & Industrial Products:

Mike Hackworth

Energy, Utilities & Mining:

David Gray

Published by Bladonmore Media Ltd

Editor-in-chief: Richard Rivlin

Editor: Eila Rana

Managing editor: Sean Kearns

Sub-editor: Lynne Densham

Art director: Owen Thomas

Designer: Ivelina Ivanova

Production manager: Andrew Miller

Publisher: Siân Griffiths

Managing director: Jonty Summers

T: +44 (0)20 7631 1155

Editorial letter

3PricewaterhouseCoopers

co

ve

r im

ag

e: p

ho

toli

br

ar

y

236 UpfrontAchieving tax transparency; examining future trends in deal-making; Failsafe Strategies: Profit and Grow from Risks that Others Avoid by Dr Sayan Chatterjee; conversations with Miroslav Singer and Inna Fokina; and identifying effective customer relationship management

financial crisis special report

23 Weathering the stormAfter years of roaring growth, how are CEE countries navigating the current economic crisis?

28 Holding groundBanks in CEE may not be completely insulated from the ravages of the financial whirlwind, but their position remains strong

32 safe cargoAs bank financing evaporates, exporters to untested overseas markets are turning to a different source for credit insurance – governments

34 talent spottersIn lean times the temptation is often to slash training budgets, but it is a mistake to do so at the cost of talent management

contents

28

4

tHe Big pictUre

10 checking out ceeRetail is one of the most mature and competitive sectors in the region. So how can the UK’s Tesco and Germany’s Metro increase their share of the market?

16 good to growAlready established as a leading Ukrainian conglomerate with interests in more than 90 business divisions, SCM plans to use its policies of transparency and good governance as a springboard to global success

16

42

34

5PricewaterhouseCoopers

tHe poWer of private capital

38 floating towards successHaving proved itself as a CEE heavyweight, Warsaw Stock Exchange is now a serious contender in Europe

optimising operations

42 child’s playDetsky Mir, Russia’s largest children’s retailer, has ensured its continued success by improving business processes

christian Doherty has 10 years’ experience as a financial journalist on a range of titles. He specialises in corporate governance, risk and accountancy issues. Most recently he edited Real FD.

Widget finn is a business journalist who writes regularly for The Times and the Daily Telegraph in the UK and a wide range of management publications. Her special interests include board level issues, business education and small businesses.

adam leyland is editor of The Grocer. He has edited a number of leading weekly business magazines in a 20-year career, including Real Business, Press Gazette, PrintWeek and the US edition of PRWeek.

tony mcauley is a senior editor within The Economist Intelligence Unit’s Industry and Management Group. He has written on capital markets, banking, finance and energy for 20 years for, among others, Reuters and Dow Jones.

vicky meek is an award-winning business and finance journalist of more than 15 years’ standing. Specialising in private equity and M&A, she regularly contributes to a range of titles including Real Deals, Emerging Private Equity and Corporate Financier.

scott payton is a regular contributor to numerous publications including Spectator Business, The Spectator, Financial Management and Accountancy. He is also editor of Linklaters Quarterly and former editor of Business Voice.

Kimberly romaine has been researching and writing about private equity for seven years, and has a particular interest in Central and Eastern Europe. She is currently editor-in-chief of unquote”.

elliot Wilson is an associate editor of Spectator Business and Hong Kong’s Asiamoney magazines. He also writes for The Spectator and Euromoney.

46 factory settingsIt may not be an ideal time to open a new production facility, but it is worth getting the ball rolling on feasibility studies

project finance anD infrastrUctUre50 Upgrade to first classGovernments in CEE are pushing to improve the region’s airport infrastructure with a number of plans on the drawing board

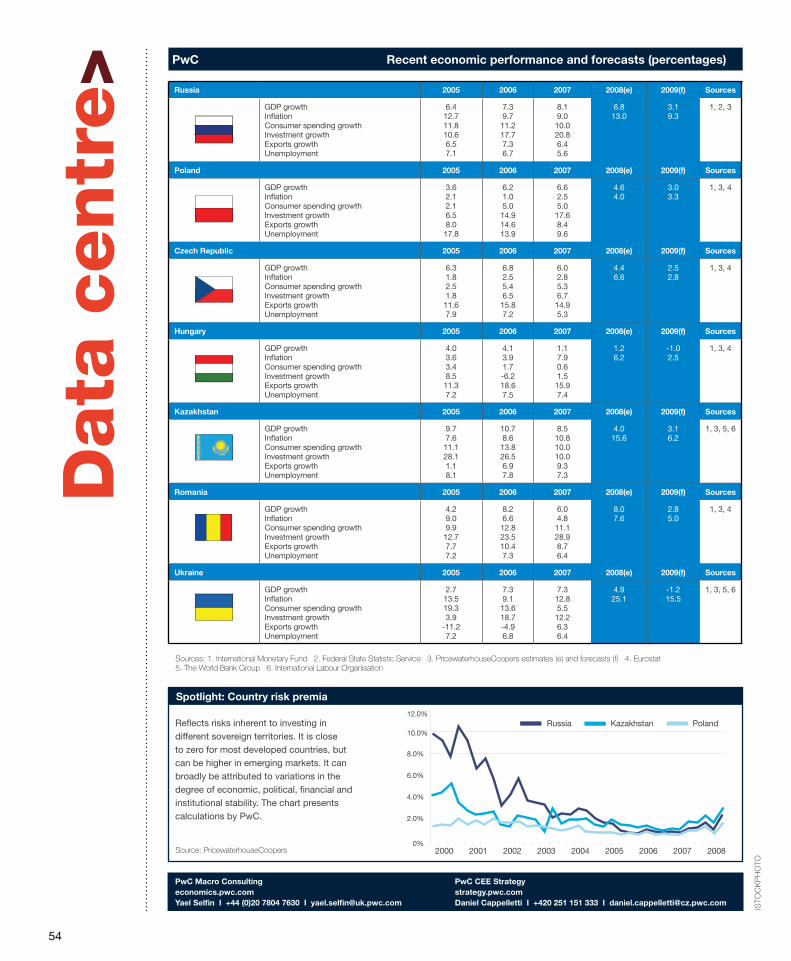

54 Data centreFacts and figures from across the region

co

nt

riB

Ut

or

s

6

upfr

ont>

Most companies do not know what their total tax bill is, let

alone how it breaks down. That puts them on the back foot

when it comes to knowing the full extent of taxes borne that

hit their P&L account and the taxes collected, which affect

their administrative costs. Not having such information limits

what can be communicated externally to demonstrate the

true total tax contribution being made to public finances.

One company that has managed to produce a detailed

breakdown of its tax bill is Kazakhmys – the London-

headquartered natural resources company, whose principal

operations are in Kazakhstan. It paid $1.1bn in taxes in

2007 – $1,058.9m of that went towards corporate income

taxes, excess profits tax, royalties and employer taxes; the

company paid the remaining $48.6m indirectly by collecting

it on behalf of government authorities.

Standardised methodologyKazakhmys has achieved such high levels of transparency

in its tax affairs by adopting the principles set out in

PwC’s Total Tax Contribution (TTC) framework. TTC uses

a standardised methodology for gathering data across

different companies, industry sectors and countries.

Not only can the framework gather data on taxes borne

and collected, it can also collect data on other payments

made to or received from government, the costs of tax

compliance and on the company’s economic footprint.

Data, collected via a standard questionnaire, can be

analysed in various ways.

Compare and contrastNot only can TTC create overviews of how an entire

industry is contributing to a country’s tax revenues, it also

allows companies to benchmark themselves against others

in their sector. That can lead to high-level discussions with

the management of companies around understanding what

the company pays and collecting the taxes efficiently.

PwC first developed TTC four years ago. Today, it

collects and analyses tax data for companies and business

groups across 15 countries and that number is set to grow.

This international dimension is also captured by a project

undertaken with the World Bank, called Paying Taxes –

The Global Picture. This study compares the tax regimes

around 181 economies using TTC to calculate one of three

indicators, the Total Tax Rate. The latest edition of the study

has been published this quarter.

For Kazakhmys, the benefits of TTC have been

numerous. The detailed reporting of its total tax contribution

in its annual report positions it as a company that is using

good practice when it comes to transparency, corporate

reporting and governance.

From the networktax transparency

ph

oto

lib

ra

ry,

isto

ck

ph

oto

0706050403

Amount ($bn)20

18

16

14

12

10

8

6

4

2

0

7PricewaterhouseCoopers

From the networkDeal-making in 09

Pricing is expected to be the biggest challenge for deal-makers in

Central and Eastern Europe (CEE) over the coming year, according

to a new report from PwC. Future Trends in CEE M&A: Which Way

Forward? reveals that buyers – particularly private equity firms – are

becoming much more selective with a focus on quality and price as

the business environment cools off, but sellers are still looking for

high prices.

Step change“A year ago an acquisition might have been done at 12-15 times

EBITDA but as we go forward, the buyers are less excited about

growth potential and more driven by hard economics,” says Chris

Butters, PwC’s CEE M&A leader.

“We will probably come back to

something more consistent with

the historical average, which is

between 5-8 times EBITDA.”

Just as private investors become

more picky, their investment

opportunities are likely to grow.

The credit crunch is squeezing

traditional funding sources, making

CEE entrepreneurs more willing

to entertain equity partners as

a way of securing growth capital or refinancing loans. And despite

an anticipated fall-off in 2008, private equity funds in CEE enjoyed

increased liquidity (see chart).

The rise of the middle class in CEE is expected to be the underlying

driver of deal activity. “They have an expectation to live like their

Western European neighbours,” says Butters.

For a copy of Future Trends, please contact Jitka Hauserova at

[email protected] or on +420 251 151 229.

Between the Covers managing risk

Private equity fundraising in Cee

Source: Emerging Markets Private Equity Association

The rise of the middle class in CEE is expected to be the underlying driver of deal activity

Lev holubec, a partner with PwC in Ukraine, shares his thoughts on his favourite business book – Failsafe Strategies: Profit and Grow from Risks that Others Avoid, by Dr sayan Chatterjee (wharton school Publishing, $25.59).

why is this your favourite business book?

The whole concept of risk is something that people fear. This author took a different perspective on risk. What he

tried to do is show that companies that know how to take and manage risk are the companies that differentiate themselves and maintain a sustainable level of growth and profit over time.

what made you pick it up?

I teach a class at the University of Virginia’s Darden School of Business on making a success out of M&A.

Dr Chatterjee is a fellow there. I got to know him a little and he asked me to review the book before it was published.

Can you summarise the book’s main message?

The reason for the existence of business is to take risks. Profit is the

result of a firm’s ability to take risks and avoid the adverse impact of those risks.

what would you say is its key strength?

The strength is that it provides a different, positive perspective on

risk. That positive perspective will be extremely applicable to today’s world in particular. With what is happening with the credit markets, companies that sit on their laurels and take no risks at this point in time frankly may find themselves in worse positions than they were before the crisis.

what did you learn from the book?

Many of our clients ask us to show them best practice. But how can you get beyond best practice and find those

opportunities that will leapfrog you beyond the others so that you can create best practice as well? This book helped put that all into perspective.

8

upfr

ont>

where are they now?miroslav singer, vice-governor, Czech national Bank

As vice-governor of the Czech National Bank (CNB),

Miroslav Singer oversees one of the most stable financial

systems in Central and Eastern Europe (CEE) – a system

that is weathering the current global financial storm more

successfully than many of its peers.

Before joining the CNB in 2005, Singer spent what he

describes as “three very fine years” at PwC. As director

of business services in PwC’s Czech Republic practice,

he specialised in corporate recovery, restructuring and

distressed assets transactions, and spearheaded a

range of high-profile and complex projects, including a

comprehensive financial feasibility study for holding the

Olympic Games in Prague.

Another stringOn top of all this, Singer has an ongoing career as a

lecturer on mathematical analysis and economics at the

University of Economics in Prague. He previously lectured

at the Centre for Economic Research and Graduate

Education at Charles University, also in Prague.

“I am an economist by education,” Singer explains.

After receiving a PhD from the University of Pittsburgh

in 1995, he became chief

economist at Expandia

Finance, a stocks and bonds

trading company based

in the Czech Republic. “In

this role, I took part in a

major restructuring of the

overall Expandia Group,

and became managing

director in 1998,” he says.

“As a consequence of this,

I started talking to PwC about joining their restructuring

team – and did just this in 2001.”

Singer’s successful, high-profile work at PwC, alongside

his influential lectures and contributions to economic

journals such as the Review of Economics and Statistics

and Economics of Transition, led to an invitation to join the

board of the CNB in February 2005.

Despite the demanding nature of his role steering the

Czech economy through the financial crisis, Singer remains

a regular attendee at PwC alumni meetings. “And I often

see my friends at PwC on a social basis, too,” he adds. ala

my,

re

ute

rs

, is

toc

kp

ho

to

9PricewaterhouseCoopers

Inna Fokina, a senior manager with

PwC’s forensics practice, rejoined the

moscow office in December 2008 after

a three-year secondment in London.

Fokina joined PwC russia in 1996,

working as an auditor for six years

before moving to transaction services.

after getting a taste for forensics, she

transferred to London to learn from

PwC’s forensics experts. Transform

found out how her time in London will

help PwC russia step up a gear.

how did you first get into

forensics work?

While I was working in the Moscow

office, a partner who transferred

from the Polish office established a

forensics practice. I began working on a

few forensics projects before switching to

the forensics practice entirely. I realised

I really liked it, but I needed to get some

technical expertise and I wanted to learn

from a centre of excellence. London was

considered to be just that for forensics.

what experience have you picked

up during your time in London?

When I started to do forensics in

Russia, I thought it was only about

investigations work. When I moved to

London I realised that there are more

than 13 to 14 different lines within

forensics – international arbitration;

commercial disputes; transaction

shareholder disputes; money laundering,

etc. Forensics is a really well-developed

practice in the UK office and during my

time there, I focused on transaction

shareholder disputes – because it fits

well with my experience in transaction

services – international arbitration and

commercial disputes.

90 seConDs wIth... Inna Fokina

how will your new skills add to

what PwC already offers clients

from its moscow office?

We do investigations work in

Russia but as far as transaction

shareholder disputes, international

arbitration and litigation support work are

concerned, this is not currently widely

performed in the Moscow office. That is

the case generally across Russia. These

types of projects used to be performed

by the foreign branches of the consulting

firms, but that is changing now so it

is perfect timing for me to return to

Moscow. Russian clients are not used to

getting the services we can now provide,

so we will need to explain the unique

benefits they can bring.

so has it been worth investing such

a long time in the secondment?

These three years have been

valuable not only in terms of career

development, but also in terms of personal

development. Getting the chance to

broaden my horizons, learn the way the

world works and raise my levels of self-

awareness has been absolutely amazing.

trenD watChCustomer care

A global economic crisis is not all bad news.

As companies cut back on spending, they

can expect their business advisers to step

up their game on customer service – not

only will suppliers in the business advisory

field be fighting to hold on to their existing

contracts, they will also be facing increased

competition for less new business.

Those supplying the Central and Eastern

European (CEE) market face an even greater

challenge, reckons Mikhail Magrilov, a

Russia-based PwC partner who advises

telecoms companies. He says that for

the majority of CEE companies trying to

achieve economies of scale, the market for

helping them do that was already fiercely

competitive anyway.

Magrilov says customer relationship

management (CRM) – the business jargon

for good customer service – can be a real

differentiator during hard times. So much

so that during a downturn, some companies

will not commit themselves to the time and

cost of a tender process, going straight to

the supplier that they know and trust.

Key pointersSo what are the signs of effective CRM?

Magrilov says a good business adviser will

know their client and have excellent one-

to-one relationships with the key decision

makers within the organisation. They will

not only react quickly to problems and

difficulties but more importantly, they will be

proactive. Great advisers stay on top of their

clients’ financials and anticipate problems

before they even arise. They also share

contacts, encouraging clients to network

with and learn from each other.

Such personalised CRM does not work

in all industries though. Magrilov says

it is most effective where there are a limited

number of players. In industries that

are more saturated, CRM tends to be

more systematic.

“Getting the chance to learn the way the world works has been absolutely amazing”INNA FOKINA, SENIOR MANAGER, PwC

10

11

The big picTure

checking out ceeencouraged by the consumer boom of the 1990s, global retailers opened stores across the region, but has one expansion strategy proved more effective than another?

Words: Adam Leyland

Scaling back growth plans during an economic downturn may be a disheartening prospect but on

the plus side, it is also an opportunity to regroup and review the effectiveness of expansion strategies in readiness for the upturn. That is what many of Central and Eastern Europe’s (CEE) inward investors are doing right now.

Retail, one of the most mature and competitive of CEE’s sectors, has attracted many multinationals since the region’s markets opened up at the beginning of the 1990s. Two of the early movers were Germany’s Metro and Tesco, the leading supermarket in the UK. At first glance, Metro’s strategy of regionwide expansion promises greater profitability but experts say, on closer inspection, Tesco’s approach of targeted expansion has its own merits.

Since expanding into Eastern Europe in 1994, Metro has built a €15bn-sales business in the region, with operations in 13 countries – and it continues to push outwards and eastwards. In 2009, a number of new cash and carry outlets that are due to open have been earmarked for Eastern Europe.

bright outlook Metro’s prospects in CEE are good, says Christopher Hogbin, a senior retail analyst at Sanford C Bernstein, a research firm. “The strategy for Metro is to keep growing its cash and carry business and Media Markt [its consumer electronics outlet]. Although it has high shares of the wholesale market in Europe, it’s generally underpenetrated in Eastern Europe,” he says.

Tesco made its move into CEE at a similar juncture to Metro. Its first thrust beyond the former Iron Curtain was to Hungary, with the acquisition in 1994 of Global. Since then, the British retailer has g

ett

y im

ag

es

Trolley dash: while German retailer Metro made its move into the CEE market as a cash and carry wholesaler, UK supermarket giant Tesco has adopted a different strategy, entering as a pure-play retailer

12

forEiGn rETailErs in rUssia For multinational retailers with expansion sights set on Central and Eastern Europe (CEE), Russia is undoubtedly the biggest prize. The country is now a bigger retail market than Poland, Spain and Italy and, based on recent growth forecasts, it will soon be bigger than Germany and the UK.

Globally, of the world’s seven fastest growing economies, Russia will have the highest income per head by 2050, according to PwC. And the International Monetary Fund says that the Russian economy is still expected to grow by 3.5% in 2009, despite the global economic downturn.

High demand, regional expansion opportunities and improved consumer credit infrastructure will all attract new foreign investors, and provide growth opportunities to already established market players.

Yet Russia remains a daunting prospect for Western companies. “It’s a very tricky market to be in,” says Bob Robbins, CEO for CEE at Tesco – a UK-based global retailer that has chosen, thus far, to steer clear of Russia. Wal-Mart, Carrefour, Lidl and Aldi also have no presence there. In fact, there are currently only a handful of foreign-based retailers in Russia of any note: Germany’s Metro and Rewe, Ikea, French supermarket group Auchan and Turkey’s Ramstore.

For many global retailers, Russia may be a step too far. The challenges are numerous: the struggle for operational effectiveness, the difficulty in finding affordable retail space, warehousing, logistic and supply chain management including the availability of specialists.

The lack of international players also reflects the fierceness of the competition there, says Chris Skirrow, the PwC partner responsible for consumer industrial products in Russia.

“When the Russian retail scene started to open up, the foreign-based companies had the technology and the experience, while the Russians knew how to do business,” he says. “Now the international players are familiar with how to do business and the Russians have the technology, so there’s true competition. In this market, it’s really now who’s the better retailer.”

If Tesco has a good track record elsewhere – in China and India, for example – why would it not want to consider Russia? But it already has, says Robbins: “We have looked at Russia, but it’s not where we want to be at the moment. We went to the markets we saw as the fastest emerging and westernising. That’s not necessarily the case with Russia. There’s lots of opportunity, but it’s very expensive, and there’s instability. And it looks like it’s about to go through a difficult time.”

Skirrow understands the decision. “There are not many local scale players in China,” he says. That suits Tesco, which is better at competing with international rivals rather than domestic retailers.

Christopher Hogbin, a senior retail analyst at Sanford C Bernstein, adds: “The issue with Russia is that it’s been very fast growing, and it’s quite well contested, with every kind of format from discounter to hypermarket already established, and that’s made it expensive. In the US, on the other hand, although it is competitive, Tesco has identified a gap and developed a unique format (Fresh & Easy) so if it moves fast enough Tesco can establish a lot of clear water from its rivals there.”

Another thing to consider – Russia’s population is declining by approximately 70,000 people per year. That said, the larger cities are insulated from this to some extent by inward migration from smaller centres and generally better life expectancies.

Skirrow reckons the Russian market has a strong future, despite any challenges it poses: “It’s hard to see why companies would want to ignore a country with 6% growth at a time when most international retailers are finding it hard to show any real growth at all.”

The current economic downturn is likely to kick-start consolidation in the country’s retail sector as target prices start to come down, Skirrow adds. Already there are signs of movement – Wal-Mart and Carrefour have reportedly locked horns over the acquisition of Lenta, a domestic hypermarket chain, as Carrefour steps up plans to invest up to $100m to develop a hypermarket business in Russia.

On the scene

Weighing it up

13PricewaterhouseCoopers

The big picTure

expanded into four other CEE markets – Poland, Czech Republic, Slovakia and Turkey – and built a business which has contributed to sales of just under €7bn across Europe in the year to February 2008. The CEE operations are a major contributor to that Europewide figure – to put this into perspective, sales in CEE in 2007 were more than Tesco’s 1989 group sales figure of £4.7bn.

To understand the performance of the two retailers, says Hogbin, you need to appreciate their different strategies. Metro chose to enter the market as a purely cash and carry wholesaler. “Cash and carry works particularly well in developing economies. You’re not trying to change consumer habits, or the structure of the market economy, you’re just bringing a new wholesale supply chain for existing customers. Often, in Eastern Europe, that means bringing new, Western products to consumers.”

Subsequently, Metro has been able to piggyback on the infrastructure it has established, to launch hypermarket retailing operations. The modus operandi, notes Chris Skirrow, PwC’s partner responsible for consumer industrial products in Russia, “is to start in big cities, getting to grips with the supply chain, build a hub and then push out from there to smaller cities.”

In contrast, Tesco entered CEE as a pure-play retailer, buying small businesses. The strategy has been the same in each country, says Bob Robbins, the group’s CEE CEO. “Global was a toe in the water: it helped us to see what was going on.” In each of the subsequent markets it entered, the supermarket giant made similar acquisitions: in 1995, it bought the Savia chain in Poland and the Carrefour hypermarket business in the Czech Republic; in 1996, KMart’s operations in

TEsCo 2007/2008 salEs in CEE

Source: Annual Report

Notes: Tesco sales are ex-VAT and have been rebased from sterling at an exchange rate of £1: €1.2

Total: x5,972m

x784m

x524m

x1,192m

x1,688mx1,784m

n Polandn Hungary

n Czech Republic

n Turkeyn Slovakia

fruitful yield: Metro’s approach for entry into russia is to start in big cities, establish a supply chain then expand outwards to smaller cities

© 2008 PricewaterhouseCoopers. All rights reserved. “PricewaterhouseCoopers” refers to the network of member firms of PricewaterhouseCoopers International Limited, each of which is a separate and independent legal entity.

*connectedthinking

Growthcan beachievedin anyclimate.*No matter what the markets are doing,or how buoyant the economy may ormay not be, it’s never all doom andgloom. There are always ways forbusinesses to grow.

All you need is the right advice fromthe right people at the right time.

PricewaterhouseCoopers Central and Eastern EuropeIndustry Leaders

Financial ServicesPaul Cunningham +420 251 152 012

Technology, InfoComm & EntertainmentDinu Bumbacea +40 21 202 8620

Consumer & Industrial ProductsMike Hackworth +420 251 151 801

Energy, Utilities & MiningDavid Gray +7 495 9676311

15PricewaterhouseCoopers

The big picTure

the Czech Republic and Slovakia; and in 2002, Hit supermarkets in Poland.

“If you enter as a pure-play retailer,” says Hogbin, “that can be a longer adoption process, because you’re trying to change the structure of the marketplace and change consumer behaviour with it. They are very different entry strategies. Metro has been able to enter earlier and more profitably into each market.”

But Tesco is certainly gaining momentum. With more than 750 stores and 13 distribution centres, it has built a sophisticated supply chain across CEE and is now number one or number two in each market in which it operates. And it is profitable too, Robbins adds. One of the keys to its strategy has been its multi-format approach. “We started with hypermarkets,” explains Robbins, “but to reach a higher percentage of the population, which is predominantly rural, you need to have more than one format.”

The multi-format approach marks Tesco out from its international rivals. “On the one hand, the variety of formats makes it more complex, but it’s worked very hard to simplify the running of the business,” says Hogbin. “It has Tesco in a box: the systems, organisation, it’s

set out and copied that from country to country. They’re very good at best practice sharing across the countries.”

The key difference, however, is not format. It is scale. Hogbin explains: “Tesco has entered relatively few countries. One every year. It’s now in 12 to 13 countries around the globe. But when it’s entered, it’s sought to build share as quickly as it can. In Hungary, Tesco has a mid-teen share; in Poland, the Czech Republic and Slovakia, its share is in the high single digits, so it’s much more likely to be aggressive in these markets.”

increasing scaleScale can also be the catalyst for new opportunities. Although each country in Tesco CEE has its own supply chain, the company has developed two pan-European distribution centres, which allows the company to directly source Asia-manufactured products at highly competitive prices. Other possible future opportunities include rolling out retailing services such as personal finance and internet retailing.

To speed the adoption of scale, Tesco has supported its growth through strategic acquisition. Until a couple of years ago, for example, Tesco was a minnow in Poland, with a 4% market share. But in July 2006, it bought the 279-store Leader Price chain from French supermarket chain Casino for €105m to become the clear market leader in grocery retail. Tesco shared the spoils from Casino’s Polish divestment with Metro, which picked up 19 Géant hypermarkets and seven land bank projects for €224m. The deal perfectly illustrates the different approaches to growth that Tesco and Metro have taken.

Cash is key to both groups sustaining that growth. Even in a cash-generative business like food retailing, it is imperative, and right now it is difficult.

“In food retailing there should be good

cash flows. The flipside is retailers work on negative working capital, a position that has been complicated by using cash and short-term facilities to fund expansion and the acquisition of long-term assets.

“If any company has expansion plans, and can’t arrange debt, it’s a more complex equation,” says Skirrow. “Everyone is seriously looking at reducing their expansion plans right now. It’s going to be intriguing to see who will be able to continue to expand. Because when things get better, the retailer that’s been able to do that will have clear blue water.” n

METRO 2007/2008 SALES IN CEE

Source: Annual Report

n Polandn Romania

n Russia

n Turkey

Total: x2,296m

x367m

x290m

x258m

x1,381m

“We started with hypermarkets, but to reach a higher percentage of the population, which is predominantly rural, you need to have more than one format”BOB ROBBInS, CEE CEO, TESCO

ph

oto

lib

ra

ry

Donetsk, an industrial city of 1.1 million founded in 1869 by a Welsh businessman, John Hughes, is often compared to America’s Pittsburgh or Britain’s Newcastle, cities built on coal and steel. The Donets Basin holds the country’s largest seam of iron ore and coking coal, and during the Cold War the city was renamed ‘Stalino’, as much in deference to Joseph Stalin as the former Soviet premier’s adopted surname, which translates in Russian to ‘Man of Steel’.

Steel cityAkhmetov is not just Ukraine’s leading businessman. He is also an ardent supporter of the country’s extension of influence into the wider world. The industrialist, named by Korrespondent magazine as being the richest man in the CIS region, with a fortune of $31.1bn, has been the president of Shakhtar Donetsk football club since 1996, providing unmeasured financial support to a provincial team that has become a mainstay of Europe’s premier footballing

16

Good to grow

System Capital Management (SCM) is to Ukraine what General Electric is to the United States, CITIC

Group is to China, or the Tata Group is to India. Few corporates in a region encompassing the former Soviet bloc, including Central and Eastern Europe (CEE), can reasonably claim to cover such a vast range of sectors and industries, or to do so with world-class levels of corporate governance and transparency.

Founded in 2000 in Donetsk, an eastern Ukrainian city close to the Russian border, SCM’s interests straddle more than 90 business divisions, led by metals and mining, energy, finance, telecommunications, real estate and media interests. By far the group’s largest presence is in metals and mining, where its Metinvest subsidiary controls steel-rolling facilities as far afield as Italy, Bulgaria, Switzerland and the UK.

The man behind SCM’s prodigious success, Rinat Leonidovich Akhmetov – a 42-year-old Ukrainian who made his first fortune in the 1990s, after the Soviet Union was dismantled, and his second after merging his sprawling business interests into a single, centrally controlled corporate outfit – is not shy about promoting domestic industrial and cultural interests. A graduate of Donetsk National University, Akhmetov has done much to advance the international exposure of both his home country and his hometown.

Ukraine’s largest company, System Capital Management, has already implemented world-class standards internally – now it is ready to become a global business

Words: Elliot Wilson

All new sovereign states need role models, and in SCM Ukraine is lucky to have unearthed a brace of top-notch corporate and cultural leaders

Lofty ambitions: SCM subsidiary DTEK aims to become the largest power company in Ukraine

the biG piCtUre

17

18

tournament, the Champions League. Akhmetov has earned praise at home for supporting the fortunes of a Ukrainian football team rather than a soccer outfit in, say, the English Premier League. He also owns two five-star hotels, one in Donetsk, the other in Kiev, as well as two Ukrainian media outlets: the TV station TRK Ukraina and the newspaper Segodnya.

Akhmetov’s charitable interests have grown in lockstep with his wealth. He founded the Foundation for Effective Governance, a forum that supports economic reform and development in Ukraine, and the Rinat Akhmetov Foundation for Development of Ukraine, which aims to tackle and eliminate underlying social problems in a country of 46 million people struggling to impose the interests of an ancient land with a new identity on a world dominated by more powerful national interests.

All new sovereign states need role models, and in SCM Ukraine is lucky to have unearthed a brace of top-notch corporate and cultural leaders. “I would describe Mr Akhmetov as the country’s leading businessman, an entrepreneur who saw the potential inherent in building a leading business in the private sector when the Soviet

Union fell,” says Jock Mendoza-Wilson, SCM’s director of international and investor relations. “SCM was set up in order to manage his assets; he then put in place a team capable of managing those assets transparently. It shows his entrepreneurial flair, and his ability to build and manage a wide variety of industrial assets over the long term.”

SCM is the country’s largest firm by far, generating an estimated 8% of annual gross domestic product. Net sales leapt 42% year-on-year in 2007 to $9.6bn, following hard on the heels of a near-20% rise in sales the previous year. Earnings before interest, tax, depreciation and amortisation jumped by more than 70% in 2007 over 2006 figures, to $2.7bn, with net profit almost doubling over the period, to $1.4bn. The value of SCM’s total assets under management rose to nearly $20bn in 2007, from less than $12bn the previous year, while the group added 5,000 new staff to its roster, pushing employee numbers to 165,000 at the end of 2007.

ever readyThe years preceding the credit crunch have been good to almost everyone, but particularly to leading diversified energy and metals and mining firms, and SCM is no exception. But the best of the best have spent those years improving internal procedures – improving the plumbing and plugging leaks – in expectation of a rainy day. Notes Mendoza-Wilson: “It’s always better to repair the roof while the sun is shining. While steel prices have been high over the past three to four years, we used the time wisely, investing in energy efficiency and production efficiency, and ensuring we have best-practice corporate governance in place.

“Investors and banks trust us, and that helps them understand our structure. And now that capital is scarce, that structure is helping to weather the downturn. Having that clean corporate

structure is not a silver bullet,” he adds. “But we’ve made certain that our actions over recent years have made us more attractive to the capital markets.”

It’s clear that the current global economic environment provides SCM with a stern test of its ability to operate

Staying at home: SCM’s concerns include the five-star Dombass Palace (main picture) in Donetsk; Vostokenergo (right), which owns three thermal power plants; and steel-rolling facilities (below) in Ukraine and Western Europe

“Having that clean corporate structure is not a silver bullet. But we have made certain that our actions have made us more attractive to the capital markets”JoCK MENDozA-WILSoN, SCM

19PricewaterhouseCoopers

the biG piCtUre

under pressure. Ukraine recently received a hefty capital injection from the International Monetary Fund, and Kiev’s problems will not stop there. The issue for SCM, a company that operates across multiple business sectors, is to ensure that it is capable of adapting with alacrity to the current, forbidding business environment.

Looking ahead“The situation at the moment is challenging,” admits Mendoza-Wilson. “When there is a downturn in steel prices it hurts our business, and the slowdown in many industries affects the capital we have at our disposal. It has made it harder to fully fund our aims and our production processes.” But he adds that SCM is prepared for the added pressure it places on the company. “over the next 15 months the aim is to operate as efficiently as possible, and remove from the cost line any extra fat. At every stage of the production process we are looking to cut inefficiency.”

Two unanswered questions about SCM remain: its listing plans, and the scope

of its determination to become a major global player across multiple sectors, whether organically or via a slew of mergers and acquisitions.

In terms of seeking to list one or all of its subsidiaries, Mendoza-Wilson admits the opportunity should be a compelling one when the market returns to normal, and says that the systematic process of improving corporate governance and transparency allows the management structure of SCM’s disparate divisions to operate as though they were already listed vehicles.

He notes: “The goal for each of our sub-holding firms, such as Metinvest and DTEK, is to put in place a corporate structure, governance, management team, financial reporting and operational standards and performance which ensure they are capable of being market-ready. We don’t have any concrete plans to list any division right now. But the benefit of being market-ready is significant.”

Acquisitions are a different kettle of fish. SCM has plenty of cash on hand, and in recent years it has been strongly

on the acquisition trail. In late 2007, Metinvest paid around €500m to buy steel-rolling mills in Europe. The mills – Trametal, based in northeast Italy, and Newcastle-based Spartan UK – boosted Metinvest’s plate-rolling capacity to more than one million tonnes of steel per annum. Those two new assets posted combined sales of more than €370m in 2006. At the time, Metinvest’s general director, Igor Syry, said the two acquisitions suited Metinvest’s long-term strategy of producing “more value-added products” and “improving the company’s industrial balance”.

The current fiscal environment is an equally challenging time for major acquisitions, yet SCM remains on the lookout for high-quality, low-priced prospects, particularly in the metals and mining sector. “We’re trying to compete globally in the steel market,” says Mendoza-Wilson. “our acquisition of Trametal and Spartan helped us to be closer to customers in those markets (Italy and the UK, as well as the European Union). our expansion needs in that sector are being met.

The current fiscal environment is a challenging time for major acquisitions, yet SCM remains on the lookout for high-quality, low-priced prospects, particularly in the metals and mining sector

© 2008 PricewaterhouseCoopers. All rights reserved. “PricewaterhouseCoopers” refers to the network of member firms of PricewaterhouseCoopers International Limited, each of which is a separate and independent legal entity.

*connectedthinking

In a downturn,do you planor react?*

In a downturn, businesses and their financial stakeholders need to take decisive steps to understand the situation and what it means for their future success. A clear-headed approach to planning allows you to maximise the opportunities available and come through difficult times invigorated and fit for the future.

We believe we have the skills and experience to help you define your strategy and take early action to protect your revenues.

Visit pwc.com/managingthroughthedownturn

Advisory Managing Partner – CEE Mark Okes-Voysey +7 495 232 5713

Consulting Leader – CEE Bob Gruman +7 495 232 5725

Finance and accounting functions Marc Goessi +41 793 420 389

Governance, risk and compliance Michelle Moore +7 495 967 6150

Operations and restructuringRafal Krasnodebski +48 22 523 4498

TechnologyPhilip Gudgeon +7 495 232 5434

PeopleJohn Wynn +44 7802 948 447

21PricewaterhouseCoopers

the big picture

In eight years, Rinat Akhmetov has grown SCM into Ukraine’s largest private corporation, estimated to generate about 8% of annual gross domestic product

Akhmetov has done much to advance the international exposure of both his home country and his hometown

“We’ve also been looking at opportunities in North America, which would allow us to increase our supplies of high-energy coal used in the steel-making process, particularly in terms of acquisitions in terms of coking coal. We want those deals to be a good strategic addition to our overall metals and mining strategy,” he adds.

SCM’s leading executives are looking down the line to a time when the group is a leading global holding company with one or several business divisions listed and heavily traded on one or more international stock exchanges. From the group’s 39-year-old chief executive officer, Oleg Popov, a graduate of Donetsk State University, to the 33-year-old chief financial officer, Roman Vodolazkyy, a former executive at PwC, the group’s upper echelons exude youthfulness. Mendoza-Wilson, a Scot who ran his own public relations firms in London and Dubai, adds a dash of international piquancy to a company that covets greater international exposure and accomplishments.

external assistanceThose aims are being aided and abetted by advisers including PwC. And SCM’s drive for transparency and best practice is further evidenced by its commitment to international audits, performed by PwC since 2004, and the introduction of audit committees, which include experienced independent members who have vast international expertise.

The drive for transparency has also, as Mendoza-Wilson noted, boosted SCM’s global reputation, enabling it to raise capital when other domestic and regional private corporations have stumbled. Last year, Metinvest completed the issuance of a $1.5bn syndicated loan underwritten by four global lenders: ABN AMRO, BNP Paribas, Deutsche Bank and ING. That marked the largest credit facility ever raised by a privately run Ukrainian firm.

To a large extent, SCM has benefited

as ArcelorMittal and Tata Steel,” he adds. “In the metals world, it’s a global marketplace so you have to be able to compete with the best. We are constantly upgrading our technology, improving energy efficiency, and investing in new, more environmentally sustainable business procedures.”

The message that comes out from SCM’s leading executives is that it is good to be clean and it is good to be transparent, especially when one is trying to create a leading emerging market corporate capable of competing alongside global leaders in the worlds of energy, metals and mining, telecommunications, media, and beyond. Of course, it is also good to be big and, as Ukraine’s largest private corporation, that battle is being won as well. This is a company that started in Donetsk, and expanded to Europe, but is already becoming one of Ukraine’s leading corporate flagships to the world. n

from ensuring that each of its corporate divisions is separately run by professional managers. Akhmetov might sign off on every important deal, and views everything from a central position at the heart of the firm, but the likes of DTEK and Metinvest are run to industry maxims by managers with long histories in their respective industries.

SCM sees itself less as a conglomerate in the historical sense of the term – sprawling groups that hold assets in every possible industry, whether they generate profit or not – than as a strategic, professional investor which invests in the long term in the industry sectors in which it is involved.

“Our aim is to employ world-class standards in each of the sectors,” says Mendoza-Wilson, “and to bring global best practice to each of our company divisions. We are competing on a par with the world’s best corporations, with global steel companies such

22

In this special report, Transform analyses the impact of the global financial crisis on companies in Central and Eastern Europe (CEE) and examines how they can survive and even become stronger (p23). CEE’s banks are a case in point. While the crisis may have caused their balance sheets to shrink, growth opportunities remain (p28). As bank lending dries up, businesses are looking elsewhere for financial security. Among export businesses, for example, credit export guarantee schemes have risen in popularity (p32). As in every downturn, job losses have been inevitable but experts are urging companies not to stop developing their brightest talent (p34).

Special RepoRt: financial cRiSiS

PricewaterhouseCoopers 23

Miroslav Singer, vice-governor of the Czech National Bank (CNB) and a former director at PwC,

has reason to be cheerful. As the global financial crisis continues to rock the foundations of economies elsewhere in the world, the Czech Republic’s financial system remains in good shape. “It’s a case of so far, so good,” he says. “Less than 1% of total assets in the Czech financial sector are toxic, and even these are not concentrated in a way that could harm one particular institution.”

But not all Central and Eastern European (CEE) states are weathering the international financial storm so well. “The CEE region is not homogenous,” Singer explains. “Countries have developed very different financial structures, which means

Weathering the storm

that the crisis is having very different effects from one state to another.”

The impact on the financial sector A key factor determining the impact of the global financial turmoil on specific CEE countries has been the proportion of foreign currency loans as a percentage of total recent borrowing in each state.

Hungary and the Czech Republic are the two extremes in this area. During 2008, almost 90% of loans to Hungarian households were made in Swiss francs or euros rather than in the local currency, the forint. Indeed, by October, nearly one third of Hungary’s total debt was denominated in a foreign currency. Taking out a foreign-denominated loan made sense while interest rates were low. But as the forint

weakened, Hungarian borrowers faced soaring repayment costs.

The result was widespread market panic over the ability of the Hungarian financial system to sustain itself. In October 2008, the International Monetary Fund (IMF), the European Union (EU) and the World Bank stepped in with a $25.1bn rescue package. Early signs indicate that the bailout seems to be working. In the days following the announcement of the rescue, the forint recovered some of its value against other major currencies.

In the Czech Republic, the impact of the global crisis could not be more different. As the country’s national bank announced at the end of September: “The Czech financial system continues to be relatively isolated from global turbulence.”

through the clouds: the financial crisis has not yet broken over many cee economies

Words: Scott Payton

ph

oto

lib

ra

ry

%8

7

6

5

4

3

2

1

0

24

This, says Singer, is due in large part to a far lower dependence on foreign-denominated loans. “Foreign exchange flows to households in the Czech Republic are virtually zero, compared to 90% in Hungary,” he says. Why? “Czech banks have preferred to invest in the healthily growing domestic economy rather than

looking abroad. And they have not been hit on the liability side because they financed themselves from the deposits of Czech citizens when interest rates were around or below eurozone levels,” Singer says. “So there was little incentive for the banks to engage in anything risky.”

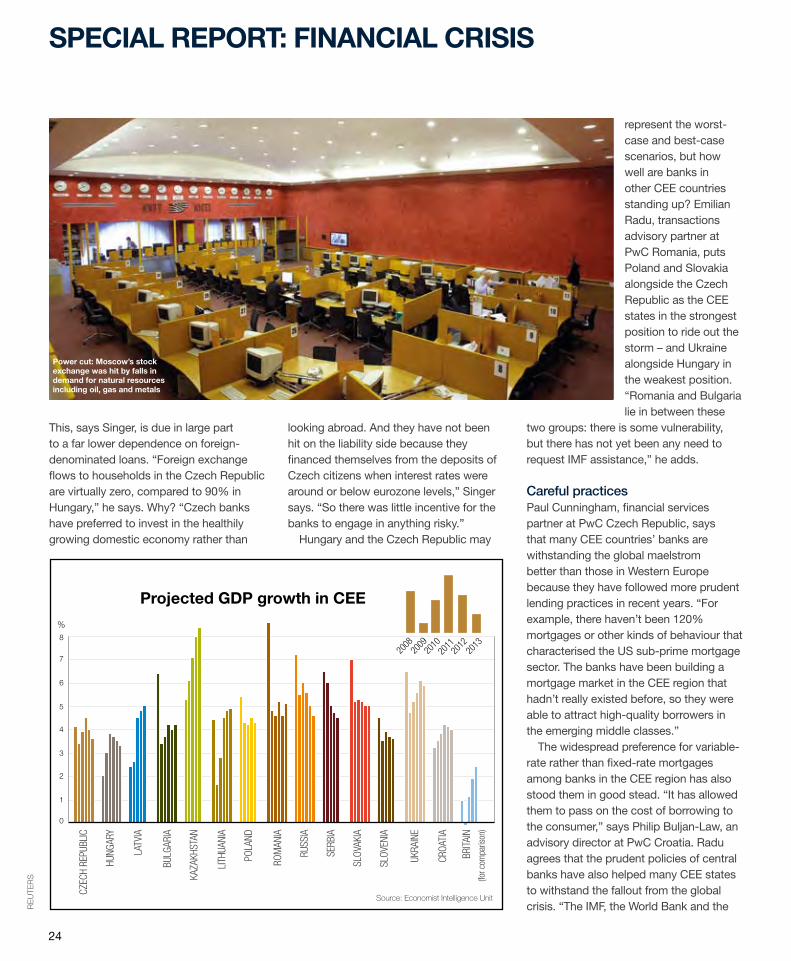

Hungary and the Czech Republic may

represent the worst-case and best-case scenarios, but how well are banks in other CEE countries standing up? Emilian Radu, transactions advisory partner at PwC Romania, puts Poland and Slovakia alongside the Czech Republic as the CEE states in the strongest position to ride out the storm – and Ukraine alongside Hungary in the weakest position. “Romania and Bulgaria lie in between these

two groups: there is some vulnerability, but there has not yet been any need to request IMF assistance,” he adds.

Careful practicesPaul Cunningham, financial services partner at PwC Czech Republic, says that many CEE countries’ banks are withstanding the global maelstrom better than those in Western Europe because they have followed more prudent lending practices in recent years. “For example, there haven’t been 120% mortgages or other kinds of behaviour that characterised the US sub-prime mortgage sector. The banks have been building a mortgage market in the CEE region that hadn’t really existed before, so they were able to attract high-quality borrowers in the emerging middle classes.”

The widespread preference for variable-rate rather than fixed-rate mortgages among banks in the CEE region has also stood them in good stead. “It has allowed them to pass on the cost of borrowing to the consumer,” says Philip Buljan-Law, an advisory director at PwC Croatia. Radu agrees that the prudent policies of central banks have also helped many CEE states to withstand the fallout from the global crisis. “The IMF, the World Bank and the

Source: Economist Intelligence Unit

Special RepoRt: financial cRiSiSCz

eCh

Repu

bliC

hung

aRy

latv

ia

bulg

aRia

Kaza

Khst

an

lith

uani

a

pola

nd

Rom

ania

Russ

ia

seRb

ia

slov

aKia

slov

enia

uKRa

ine

CRoa

tia

bRita

in (f

or c

ompa

rison

)

projected GDp growth in cee

re

ute

rs

power cut: Moscow’s stock exchange was hit by falls in demand for natural resources including oil, gas and metals

PricewaterhouseCoopers 25

EU imposed strong financial regulations in the run-up to the first wave of EU accessions, so countries took the rules of the game seriously,” he says.

Tight regulations have certainly helped to protect banks operating in Croatia, adds Buljan-Law. “A couple of years ago, the Croatian National Bank limited the growth of banks’ loans portfolios to 12%,” he explains. “For banks, mortgages and the like then became unattractive as there is more profit to be made from unsecured personal lending. As banks were slow to react (to improve credit processes, etc) and migrate from mortgages and security-backed lending to unsecured personal lending, they were spared the full force of the credit crash.”

Drop in demand In the commodity-driven and, until recently, booming economies of Russia and Kazakhstan, the financial crisis has been compounded by recent falls in demand for oil, gas, metals and other natural resources. “In the Commonwealth of Independent States, a lot of the phenomenal growth enjoyed by major companies was built on high commodity prices, availability of ample credit and dynamic construction and real estate sectors,” explains Alper Akdeniz, PwC managing partner, Central Asia and Caucasus. “As with Russia, Kazakhstan has been, and will continue to be, affected by a decline in oil and gas prices.”

Both the Russian and Kazakh governments have taken dramatic steps to shore up their banking systems and commodity-focused companies. The Kremlin, for example, has earmarked $50bn to help Russian resource companies and financial institutions meet their foreign debt obligations – which exceeded $500bn by November 2008.

In turn, the Kazakh government has allocated

a total of $15bn for supporting banks and other businesses through the global crisis. Like their Russian counterparts, Kazakh banks were left heavily exposed to foreign debt obligations when the global financial crisis began to bite. Akdeniz believes that while the government’s immediate reaction is timely, the degree of success will depend on how conditions develop. “The situation is evolving on a daily basis, so the response will have to be fluid, depending on how events unfold, and the government’s agile response is paramount,” says Akdeniz.

He says that the global crisis highlights a crucial long-term issue for the Kazakh economy: that it must branch out in order to secure future growth. “Countries like Kazakhstan cannot rely on their commodity-based economy to drive sustainable economic development going forward, so diversification is essential,” he says. “This will not be easy. It will require a lot of homework to determine how to diversify, and how to measure the successes of the diversification process.”

The Kazakh government is all too aware of the need to diversify, Akdeniz says. This is the reason authorities are working to achieve a much broader economy by 2030. Agriculture is one area of diversification with significant potential for Kazakhstan, he adds. “Given the size of the country, and its fertile land, there is an opportunity to help meet rising global demand for food.”

Beyond financial services Three other sectors that are key in many CEE economies are also being directly affected by global market turmoil: car manufacturing, construction and real estate. Although he is positive about the Czech banking system’s ability to withstand the global financial crisis, Singer admits that other sectors in his country are more vulnerable. “We will be harmed through the real economy: that’s the bottom line.”

For the Czech Republic, Slovakia and many other CEE states, the global fall in demand for new cars is having an adverse effect on the prospects for export revenues and, potentially, job security. “Central Europe has become a major auto maker. So the consequences of the crisis are very obvious,” Singer says. “You are already seeing car manufacturers cutting back production in the CEE region,” adds Cunningham. In November 2008, Volkswagen announced that output at its Czech Skoda plants would be reduced by 18,000 vehicles during the last two months of the year. This came on top of an earlier cut of 13,000 vehicles. Auto makers in other parts of the CEE region have also announced production cuts.

The repercussions of the crisis are being felt just as acutely by the real

estate and construction sectors. “We’re seeing a real reluctance to lend, transactions drying up and entities finding it very

Brakes on: Skoda cut production by 18,000 cars at the end of 2008, prompted by a fall in demand in Western european car markets

“Czech banks have preferred to invest in the healthily growing domestic economy rather than looking abroad”MIROSLAV SINGER, VICE-GOVERNOR, CzECH NATIONAL BANK

26

difficult to raise finance, even for existing projects,” says Cunningham. “The property bubble – particularly that seen in the Baltic states – has been pretty sharply pierced.”

While the effects of the financial crisis vary dramatically from country to country, banks are generally unified in their response: they are cutting costs,

Sept 17, 2008 the Russian government closes trading on the country’s two major bourses, RtS and MiceX, following the sharpest share falls in a decade.

Sept 29, 2008 Russian prime minister Vladimir putin announces that $50bn worth of loans will be made available through Russian state-owned Vneshekonombank (VeB) to help the country’s financial institutions and companies meet their foreign debt obligations.

cee flashpoints

turbulent times: Hungary’s stock market has been badly hit by the global financial crisis

while pressing on with their business transformation and expansion plans. “They still expect to grow this market, but they are looking to do so more efficiently than in the past,” says Cunningham.

Best practiceWhat banks are not doing, adds Buljan-Law, is making extensive redundancies. “Instead, they are looking at standardising processes, optimising efficiency, tightening controls and focusing hard on profitability. They realise that they can’t stop reducing the time to market for new products; improving their services; and enhancing customer support – because if they freeze any of this activity, then a competitor will step in and take away market share,” Buljan-Law says. This acceleration of the business transformation process

is leading banks to differentiate their business models more clearly, he adds. “Some banks are focusing on the service side, losing market share but winning more profitable segments of the market; while others are focused on becoming a supermarket – saying: ‘We want as many customers as we can because we’re lean and mean.’” Banks’ advisory requirements have also sharpened, he adds. “In this market, clients are looking for real value-add. More than ever, they want truly specialist help from advisers who deeply understand the local market, language and culture – as well as having the ability to offer a world-class service.”

Cunningham, meanwhile, points to another reason why CEE financial institutions and organisations in other sectors are particularly keen to tap into the best possible advisory services: many senior executives have never experienced a downturn in their professional lives. “It’s been 10 years since Russia had a problem, and longer than that in other parts of the region. Things have been very comfortable for many institutions. Now it’s only the clever that are going to make the decent money and the rest are going to struggle.”

Mark Okes-Voysey, CEE advisory regional leader, says that CEE companies outside the financial sector are also responding to the global uncertainty by focusing their minds on improving efficiencies wherever they can: “Companies tend to learn a great deal during crisis periods. It’s important that businesses take out non-core activities and ensure they have the right people to r

eu

ter

s

“Diversification is essential… Given the size of Kazakhstan, and its fertile land, there is an opportunity to help meet rising global demand for food”ALPER AKDENIz, PARTNER, PwC

Special RepoRt: financial cRiSiS

PricewaterhouseCoopers 27

drive the business forward. There will be a lot of restructuring.”

How should the region’s governments and central banks help their economies through the challenging months ahead? Radu urges them to strike the delicate balance between tightening controls and maintaining the flow of credit. “What’s really important for the Romanian government and central bank, for example, is not to fall into the trap of completely discouraging credit. By not injecting cash into economies, we will run the risk of recession. We need a balanced approach that still funds growth, yet also provides credit on more prudent terms – but not on excessively stringent terms.”

“Balance” is also the watchword for Singer at the CNB. “Our conflicting goals

oct 27, 2008 the international Monetary fund offers a $16.4bn loan “to restore financial and macroeconomic stability” to the Ukrainian economy, following a 25% fall in the value of the local currency and tumbling global demand for steel – a key export for Ukraine.

oct – nov 2008 the Kazakh government earmarks $15bn for supporting the country’s financial institutions and companies. this includes an injection of $3.4bn into four major banks – alliance Bank, Bta Bank, Halyk Bank and Kazkommertsbank – plus $5bn worth of short-term loans and a $1bn fund to absorb toxic debt.

nov 5, 2008 the iMf, World Bank and eU agree a $25.1bn rescue package for the Hungarian financial system, designed to restore investor confidence and reduce stress on debt holders – many of whom faced soaring repayment costs on foreign-denominated loans. in november 2008, Hungary has a national debt worth 97% of GDp.

the long term. However, the short-term challenges are considerable and require decisive policy measures.

Cunningham agrees with Radu, adding that the outlook for investors in the CEE region remains relatively rosy, although, as the downturn proves, nothing is predictable and uncertainty remains in all markets. Okes-Voysey says: “Sure there are risks out there, but pricing is becoming a lot more attractive and sellers’ markets are becoming buyers’ markets.” He anticipates that the new global economic landscape will attract new types of investors to the CEE region: “I think we will see a raft of different potential investors coming in – such as sovereign wealth funds – from countries which are less affected by the crisis, yet haven’t shown substantial interest in the region to date.”

Singer also believes that the environment for inward investors remains favourable in the CEE region. “There are still natural growth opportunities in many sectors, including finance. And since the developed world appears to be harmed more severely than Central and Eastern Europe, it may pay off for investors to look for localised growth opportunities.”

Akdeniz believes that Central Asia is also in a strong long-term position. “We will bounce back, particularly in Kazakhstan, due to our very close proximity to significant emerging markets such as China and India and robust fundamentals,” he says. “There is going to be a global slowdown, but growth will remain prevalent in this part of the world.”

As Okes-Voysey concludes: “The region at large is still going to be an exciting place; fortune will definitely favour the brave.” n

are achieving price stability and avoiding deflation on the one hand, and preserving our credibility on the international financial markets on the other.”

The long viewDespite the ongoing consequences of the global financial crisis across CEE, Radu cites one reason to be positive. “A recent Economist Intelligence Unit report projected that growth in the CEE region during 2009 will average 4%. This might be around 2% lower than those seen in recent years – but growth in the UK and the eurozone will average -0.4%.” (See ‘Projected GDP growth in CEE’ p.24.) In other words, compared with Western Europe, CEE countries will continue to enjoy substantial economic growth in

“Pricing is becoming more attractive and sellers’ markets are becoming buyers’ markets”MARK OKES-VOYSEY, CEE ADVISORY REGIONAL LEADER, PwC

cold comfort: debts owed to distributors have led to empty freezers in stores

28

Bankers in CEE have to get used to a slowdown in growth and consolidation strategies, though they are still in a position of strength

Words: Tony McAuley

Holding ground

Special RepoRt: financial cRiSiS

For European banking, the markets east of the Danube have been the continent’s most compelling growth story for so long

that it is particularly depressing when the hope that they might be able to escape the financial crisis is dashed. There was no way, of course, to completely avoid the epochal financial unravelling, even for the relatively under-developed and fast-growth banking markets of Central and Eastern Europe (CEE). However, there are still plenty of growth opportunities, especially for the well-positioned banking groups – the early international movers that have established dominant market positions, such as Erste, Raiffeisen International (RI) and UniCredit.

It is becoming clear, though, that the nature of competition is likely to change, and therefore the way that banks must respond. The “land grab” of the past few years will most likely give way to a period when banks concentrate on organic growth. Already, there is evidence of the effect of the financial crisis on the sector’s mergers and acquisitions activity. Whereas banking groups had been falling over themselves to buy

THE Big piCTurE

29

isto

ck

ph

oto

“Banks have to optimise their distribution networks, significantly improve their customer service, anything that can help them to grow organically”MARC gössI, pARTnER, pwC

up assets over the previous five years, the brakes came on for deal flow in 2008. In the year through to november 10, the total value of announced acquisitions was less than half that for 2007 (full year) and none of the deals topped €1bn (see chart overleaf).

The earlier pace of deal-making is not likely to return anytime soon. “It’s not only the market risk that analysts are now focused on, but also the perception that banking is not as profitable as it was in the past,” says Roman Hager, who is general secretary to RI CEO Herbert stepic. “To buy a bank in such an environment, with assets that you cannot 100% evaluate or determine how risk is developing, and with financing resources scarce… it’s not happening.”

some deals have continued to go through (see table overleaf). For example, the purchase by gE Money of poland’s BpH banking group in 2008 is a deal that typifies the strategy of many of those that continue to pursue expansion plans in

CEE. With BpH, gE expanded its polish offering from consumer finance to universal banking. gE’s strategy is to merge its polish banking interests in the first half of 2009 and to expand the branch network over the next three years.

But CEE banking M&A is, nonetheless, expected to hit a dry spell. As Federico ghizzoni, head of UniCredit poland’s markets division and CEE banking, says: “It’s not because opportunities will not come but clearly the so-called consolidators are looking at their own balance sheets. There are very few banks willing to invest, not only in Eastern Europe but overall. Maybe in the second half of 2009 there will be some more consolidation, though probably indirectly,” as international groups may pull out of the region and put their banks up for sale, he says.

Although it is slowing down, CEE banking has shown remarkable resilience. According to a report from Raiffeisen Zentralbank österreich (RZB), CEE banking assets grew

0

5,000

10,000

15,000

20,000

25,000

0

50

100

150

200

2007

Value ($m) Number of transactions

Announcement date 2008 (to Nov 10) 2007 2008 (to Nov 10)Announcement date

0

5,000

10,000

15,000

20,000

25,000

0

50

100

150

200

2007

Value ($m) Number of transactions

Announcement date 2008 (to Nov 10) 2007 2008 (to Nov 10)Announcement date

30

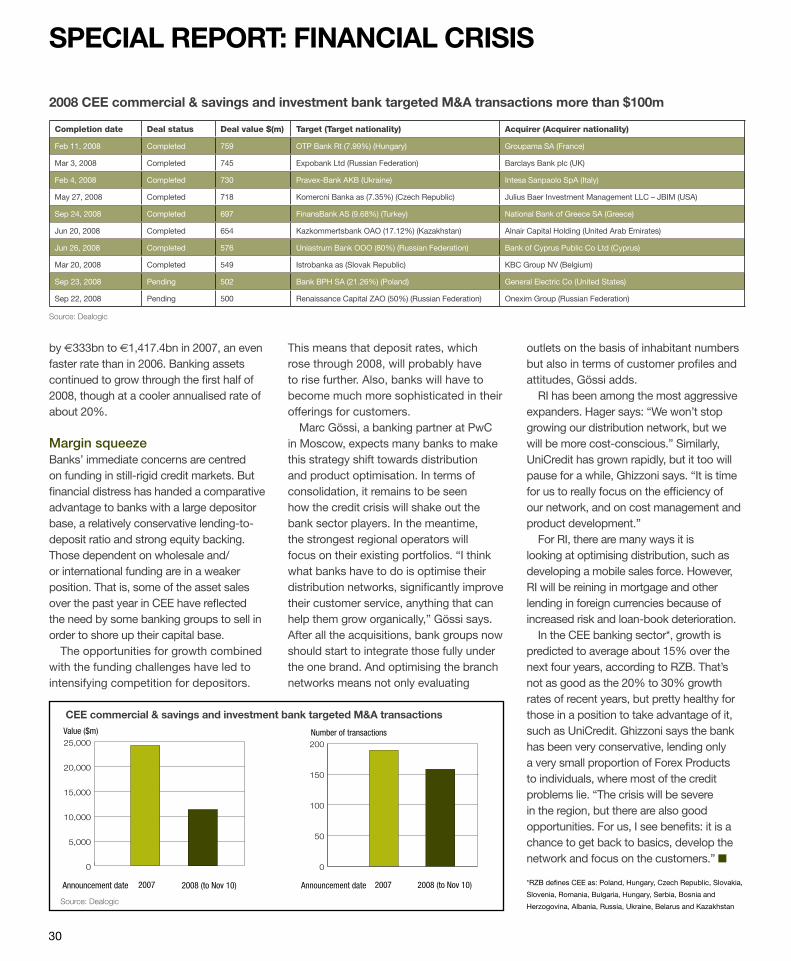

2008 cee commercial & savings and investment bank targeted M&a transactions more than $100m

Completion date Deal status Deal value $(m) Target (Target nationality) Acquirer (Acquirer nationality)

Feb 11, 2008 Completed 759 OTp Bank Rt (7.99%) (Hungary) groupama sA (France)

Mar 3, 2008 Completed 745 Expobank Ltd (Russian Federation) Barclays Bank plc (UK)

Feb 4, 2008 Completed 730 pravex-Bank AKB (Ukraine) Intesa sanpaolo spA (Italy)

May 27, 2008 Completed 718 Komercni Banka as (7.35%) (Czech Republic) Julius Baer Investment Management LLC – JBIM (UsA)

sep 24, 2008 Completed 697 FinansBank As (9.68%) (Turkey) national Bank of greece sA (greece)

Jun 20, 2008 Completed 654 Kazkommertsbank OAO (17.12%) (Kazakhstan) Alnair Capital Holding (United Arab Emirates)

Jun 26, 2008 Completed 576 Uniastrum Bank OOO (80%) (Russian Federation) Bank of Cyprus public Co Ltd (Cyprus)

Mar 20, 2008 Completed 549 Istrobanka as (slovak Republic) KBC group nV (Belgium)

sep 23, 2008 pending 502 Bank BpH sA (21.26%) (poland) general Electric Co (United states)

sep 22, 2008 pending 500 Renaissance Capital ZAO (50%) (Russian Federation) Onexim group (Russian Federation)

source: Dealogic

by €333bn to €1,417.4bn in 2007, an even faster rate than in 2006. Banking assets continued to grow through the first half of 2008, though at a cooler annualised rate of about 20%.

Margin squeezeBanks’ immediate concerns are centred on funding in still-rigid credit markets. But financial distress has handed a comparative advantage to banks with a large depositor base, a relatively conservative lending-to-deposit ratio and strong equity backing. Those dependent on wholesale and/or international funding are in a weaker position. That is, some of the asset sales over the past year in CEE have reflected the need by some banking groups to sell in order to shore up their capital base.

The opportunities for growth combined with the funding challenges have led to intensifying competition for depositors.

This means that deposit rates, which rose through 2008, will probably have to rise further. Also, banks will have to become much more sophisticated in their offerings for customers.