Embed Size (px)

Citation preview

UK Tourism DynamicsSeizing opportunities in your region

3 Section one: Introduction4 Emerging economies

5 Enjoying the ‘staycation’

6 Total expenditure breakdown

7 UK regional performance

8 Section two: Focusing on the South West10 Domestic tourism spend on retail

11 Overseas tourism spend on retail

12 Domestic tourism spend on hospitality and leisure

13 Overseas tourism spend on hospitality and leisure

14 Exploring Bristol

16 Section three: Considerations for success17 Case study: Corinthia Hotel London

18 Section four: Key takeaways

Contents

2 of 19

This report has been produced by Conlumino for Barclays.

All content has been researched, developed and produced by Conlumino at the request of Barclays for the purpose of this report. All charts, data and statistics featured in this report are the product of this research.

All rights reserved. May 2014

[email protected]: 020 7936 6655

Section one: Introduction

Overseas tourism spend is anticipated to rise at a fasterrate (33.6%) than domestic (25.3%) across the UK’s retail,hospitality and leisure industries.

Expenditure on retail goods by overseas tourists is set to rise 36.3% to over £9.3bn by 2017, while overseastourist spend on hospitality and leisure is set to rise by33% to £14.7bn in the same period. Wealthy consumersfrom emerging economies such as Asia and the MiddleEast will largely drive this growth, as well as the increasingdisposable incomes of the middle classes from developingmarkets and Eastern Europe.

By 2017, domestic tourist expenditure on hospitality andleisure is set to grow to almost £69bn, and domestictourist spending on retail goods is set to reach £15.6bn.

Whilst online and mobile retail continues to pose a threat to high-street profits, consumers have shownincreasing willingness to spend on small indulgences,such as dining out and visiting leisure attractions.

There is further evidence of optimism around the retail,hospitality and leisure sectors, with increased investmentin developments predicted in the coming years, includingin typically less prosperous areas of the UK.

This report analyses how tourists are spending their moneyin the UK, across both retail and leisure destinations, withan in-depth focus on your region. The report also proposesstrategies that retailers and leisure operators may want toconsider when tailoring their services to ever-evolvingdomestic and overseas audiences.

We hope that you will find this report insightful, and that it will support you in considering how you can maximisethe opportunities afforded through UK tourism.

The UK’s impressive heritage and enthusiasm for contemporary culturemake it an attractive destination for the world’s tourists. By 2017, totalexpenditure by domestic and overseas tourists is expected to increase by 27% to just over £135.5bn.

Richard LoweHead of Retail & Wholesale

£135.5bnAnticipated total spend by domesticand overseas tourists across the UK by 2017

Mike SaulHead of Hospitality & Leisure

3 of 19

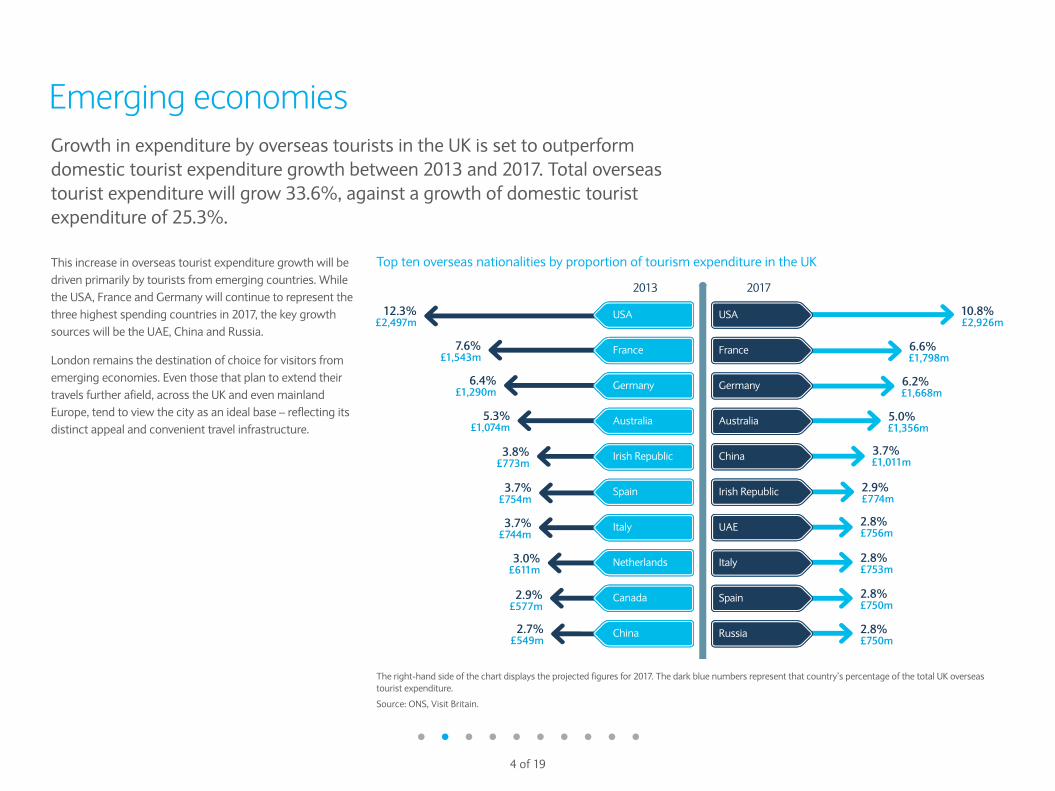

Emerging economies

This increase in overseas tourist expenditure growth will bedriven primarily by tourists from emerging countries. Whilethe USA, France and Germany will continue to represent thethree highest spending countries in 2017, the key growthsources will be the UAE, China and Russia.

London remains the destination of choice for visitors fromemerging economies. Even those that plan to extend theirtravels further afield, across the UK and even mainlandEurope, tend to view the city as an ideal base – reflecting itsdistinct appeal and convenient travel infrastructure.

The right-hand side of the chart displays the projected figures for 2017. The dark blue numbers represent that country’s percentage of the total UK overseastourist expenditure.

Source: ONS, Visit Britain.

Growth in expenditure by overseas tourists in the UK is set to outperformdomestic tourist expenditure growth between 2013 and 2017. Total overseastourist expenditure will grow 33.6%, against a growth of domestic touristexpenditure of 25.3%.

4 of 19

Top ten overseas nationalities by proportion of tourism expenditure in the UK

10.8%£2,926m

12.3%£2,497m

7.6%£1,543m

6.4%£1,290m

5.3%£1,074m

3.8%£773m

3.7%£754m

3.7%£744m

3.0%£611m

2.9%£577m

2.7%£549m

6.6%£1,798m

6.2%£1,668m

5.0%£1,356m

3.7%£1,011m

2.9%£774m

2.8%£756m

2.8%£753m

2.8%£750m

2.8%£750m

USA

France

Germany

Australia

China

Irish Republic

UAE

Italy

Spain

Russia

USA

2013 2017

France

Germany

Australia

Irish Republic

Spain

Italy

Netherlands

Canada

China

5 of 19

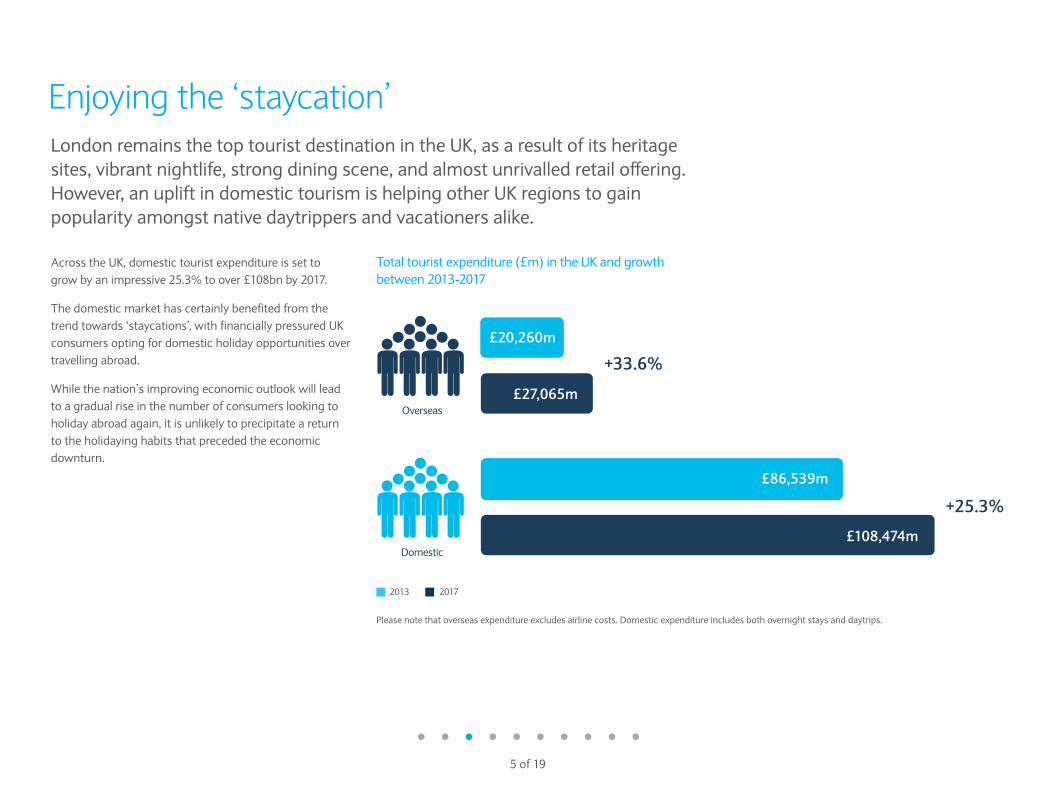

Across the UK, domestic tourist expenditure is set to grow by an impressive 25.3% to over £108bn by 2017.

The domestic market has certainly benefited from thetrend towards ‘staycations’, with financially pressured UKconsumers opting for domestic holiday opportunities overtravelling abroad.

While the nation’s improving economic outlook will leadto a gradual rise in the number of consumers looking toholiday abroad again, it is unlikely to precipitate a return to the holidaying habits that preceded the economicdownturn.

Total tourist expenditure (£m) in the UK and growthbetween 2013-2017

London remains the top tourist destination in the UK, as a result of its heritagesites, vibrant nightlife, strong dining scene, and almost unrivalled retail offering.However, an uplift in domestic tourism is helping other UK regions to gainpopularity amongst native daytrippers and vacationers alike.

Enjoying the ‘staycation’

Please note that overseas expenditure excludes airline costs. Domestic expenditure includes both overnight stays and daytrips.

Overseas

£20,260m

£27,065m

+33.6%

+25.3%

£86,539m

£108,474mDomestic

2013 2017

54.6%33.8% 54.4%34.5%

63.2%14.6% 14.4% 63.6%

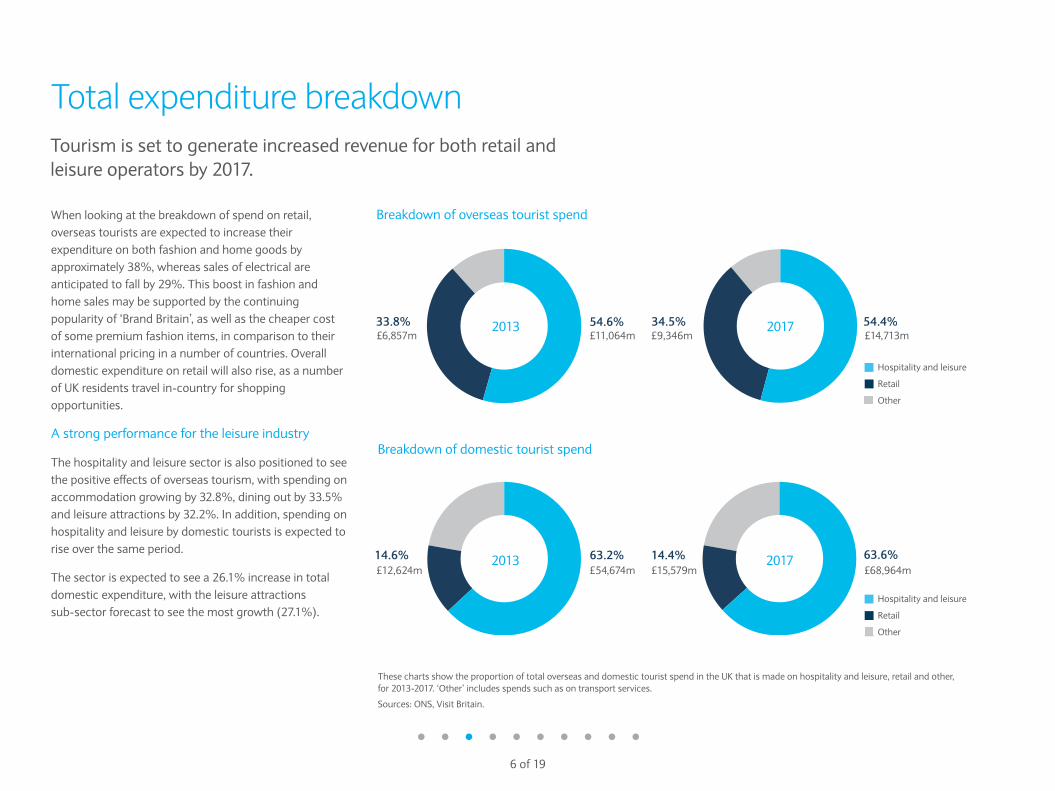

When looking at the breakdown of spend on retail,overseas tourists are expected to increase theirexpenditure on both fashion and home goods byapproximately 38%, whereas sales of electrical areanticipated to fall by 29%. This boost in fashion and home sales may be supported by the continuingpopularity of ‘Brand Britain’, as well as the cheaper cost of some premium fashion items, in comparison to theirinternational pricing in a number of countries. Overalldomestic expenditure on retail will also rise, as a numberof UK residents travel in-country for shoppingopportunities.

A strong performance for the leisure industry

The hospitality and leisure sector is also positioned to seethe positive effects of overseas tourism, with spending onaccommodation growing by 32.8%, dining out by 33.5%and leisure attractions by 32.2%. In addition, spending onhospitality and leisure by domestic tourists is expected torise over the same period.

The sector is expected to see a 26.1% increase in totaldomestic expenditure, with the leisure attractions sub-sector forecast to see the most growth (27.1%).

Breakdown of overseas tourist spend

Breakdown of domestic tourist spend

Tourism is set to generate increased revenue for both retail andleisure operators by 2017.

Total expenditure breakdown

6 of 19

These charts show the proportion of total overseas and domestic tourist spend in the UK that is made on hospitality and leisure, retail and other, for 2013-2017. ‘Other’ includes spends such as on transport services.

Sources: ONS, Visit Britain.

Hospitality and leisure

Retail

Other

Hospitality and leisure

Retail

Other

2013 2017

2013 2017

£11,064m£6,857m

£12,624m £68,964m£54,674m £15,579m

£9,346m £14,713m

7 of 19

UK regional performance

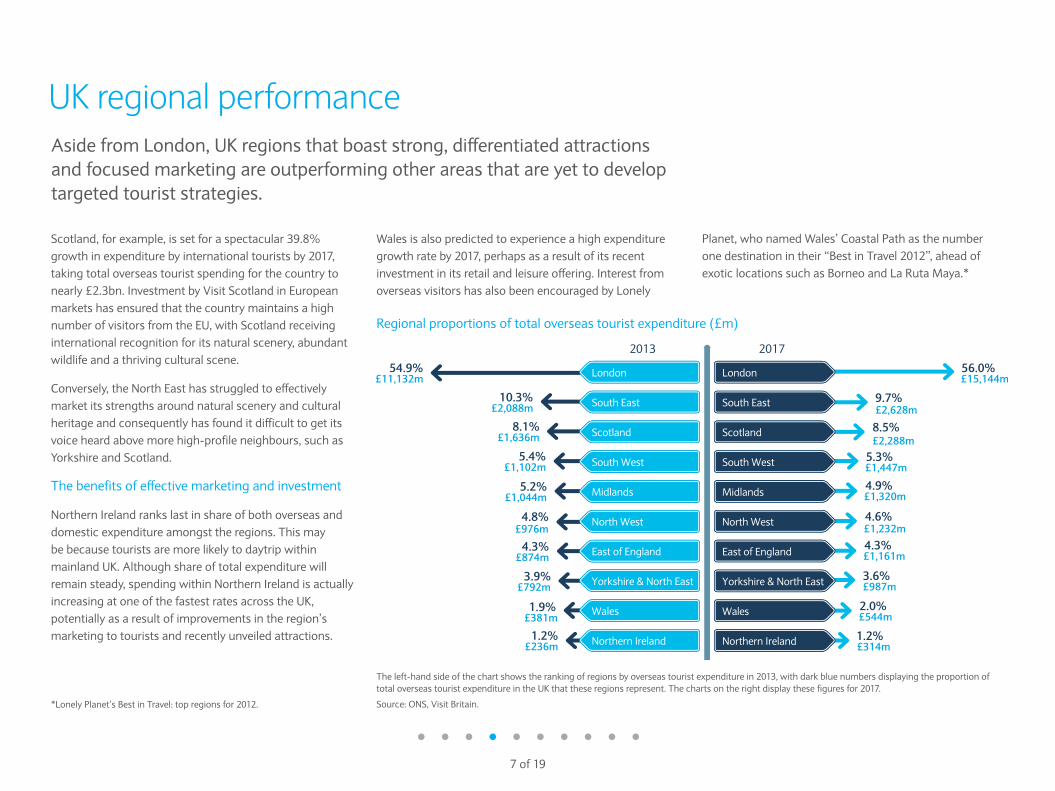

Scotland, for example, is set for a spectacular 39.8%growth in expenditure by international tourists by 2017,taking total overseas tourist spending for the country tonearly £2.3bn. Investment by Visit Scotland in Europeanmarkets has ensured that the country maintains a highnumber of visitors from the EU, with Scotland receivinginternational recognition for its natural scenery, abundantwildlife and a thriving cultural scene.

Conversely, the North East has struggled to effectivelymarket its strengths around natural scenery and culturalheritage and consequently has found it difficult to get itsvoice heard above more high-profile neighbours, such asYorkshire and Scotland.

The benefits of effective marketing and investment

Northern Ireland ranks last in share of both overseas anddomestic expenditure amongst the regions. This may be because tourists are more likely to daytrip withinmainland UK. Although share of total expenditure willremain steady, spending within Northern Ireland is actuallyincreasing at one of the fastest rates across the UK,potentially as a result of improvements in the region’smarketing to tourists and recently unveiled attractions.

Wales is also predicted to experience a high expendituregrowth rate by 2017, perhaps as a result of its recentinvestment in its retail and leisure offering. Interest fromoverseas visitors has also been encouraged by Lonely

Planet, who named Wales’ Coastal Path as the numberone destination in their “Best in Travel 2012”, ahead ofexotic locations such as Borneo and La Ruta Maya.*

Aside from London, UK regions that boast strong, differentiated attractionsand focused marketing are outperforming other areas that are yet to developtargeted tourist strategies.

The left-hand side of the chart shows the ranking of regions by overseas tourist expenditure in 2013, with dark blue numbers displaying the proportion oftotal overseas tourist expenditure in the UK that these regions represent. The charts on the right display these figures for 2017.

Source: ONS, Visit Britain.

56.0%£15,144m

54.9%£11,132m

10.3%£2,088m

8.1%£1,636m

5.4%£1,102m

5.2%£1,044m

4.8%£976m

4.3%£874m

3.9%£792m

1.9%£381m

1.2%£236m

9.7%£2,628m

8.5%£2,288m

5.3%£1,447m

4.9%£1,320m

4.6%£1,232m

4.3%£1,161m

3.6%£987m

2.0%£544m

1.2%£314m

London

South East

Scotland

South West

Midlands

North West

East of England

Yorkshire & North East

Wales

Northern Ireland

London

2013 2017

South East

Scotland

South West

Midlands

North West

East of England

Yorkshire & North East

Wales

Northern Ireland

*Lonely Planet’s Best in Travel: top regions for 2012.

Regional proportions of total overseas tourist expenditure (£m)

8 of 19

Overseas Domestic

£13,205m

£1,102m £1,447m

£10,485m

+25.9%+31.3%

2013 2014 2015 2016 2017

£1,102m

5.44% 5.43% 5.36% 5.34% 5.35%

£1,179m£1,250m

£1,337m£1,447m

+31.3%

2013 2014 2015 2016 2017

£10,485m

12.12% 12.08% 12.01% 12.14% 12.17%

£11,104m£11,709m

£12,523m£13,205m

+25.9%

Section two: Focusing on the South West

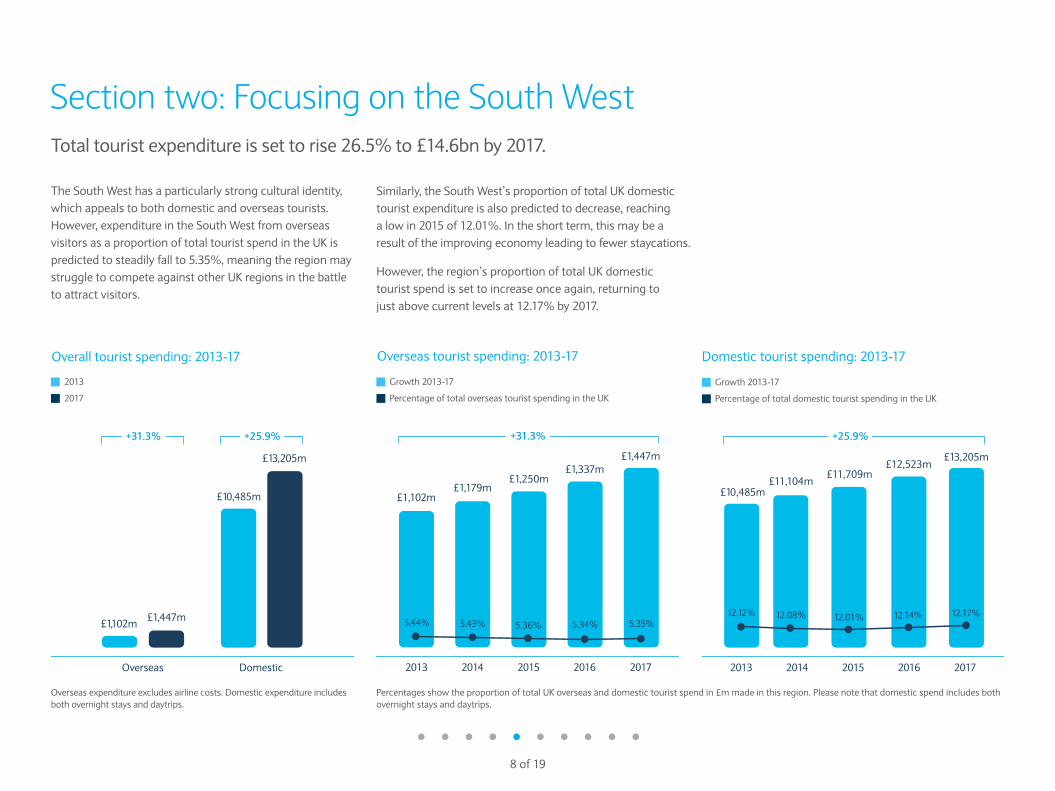

The South West has a particularly strong cultural identity,which appeals to both domestic and overseas tourists.However, expenditure in the South West from overseasvisitors as a proportion of total tourist spend in the UK ispredicted to steadily fall to 5.35%, meaning the region maystruggle to compete against other UK regions in the battleto attract visitors.

Similarly, the South West’s proportion of total UK domestictourist expenditure is also predicted to decrease, reaching a low in 2015 of 12.01%. In the short term, this may be aresult of the improving economy leading to fewer staycations.

However, the region’s proportion of total UK domestic tourist spend is set to increase once again, returning to just above current levels at 12.17% by 2017.

Overseas tourist spending: 2013-17 Domestic tourist spending: 2013-17

Total tourist expenditure is set to rise 26.5% to £14.6bn by 2017.

Growth 2013-17

Percentage of total overseas tourist spending in the UK

Overall tourist spending: 2013-17

2013

2017

Growth 2013-17

Percentage of total domestic tourist spending in the UK

Percentages show the proportion of total UK overseas and domestic tourist spend in £m made in this region. Please note that domestic spend includes bothovernight stays and daytrips.

Overseas expenditure excludes airline costs. Domestic expenditure includesboth overnight stays and daytrips.

9 of 19

13.4%£194m

15.2%£168m

11.3%£125m

8.6%£94m

6.2%£68m

4.9%£54m

4.0%£44m3.8%£41m3.5%£38m3.3%£36m2.9%£32m

9.0%£131m

7.6%£111m

5.9%£85m

4.7%£69m

3.6%£52m3.5%£51m

3.1%£44m

2.7%£40m2.7%£40m

Germany

France

USA

Australia

China

Switzerland

Spain

Italy

UAE

Netherlands

Germany

2013 2017

France

USA

Australia

Spain

Italy

Switzerland

China

Netherlands

Ireland

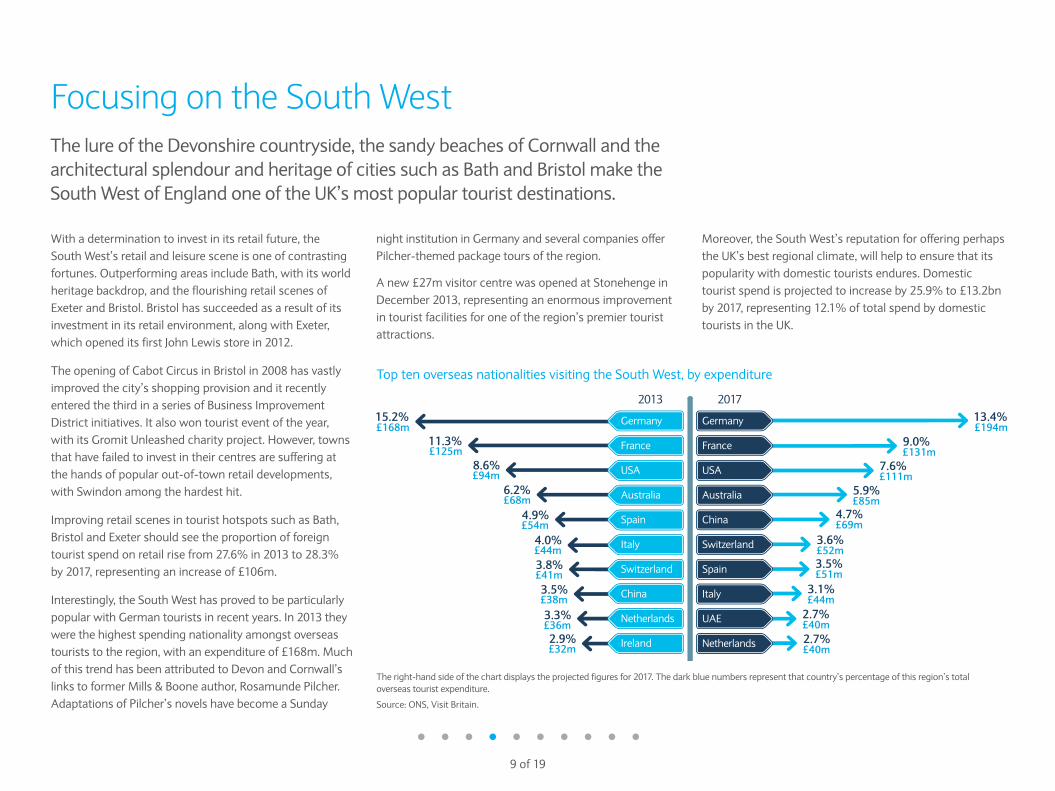

With a determination to invest in its retail future, the South West’s retail and leisure scene is one of contrastingfortunes. Outperforming areas include Bath, with its worldheritage backdrop, and the flourishing retail scenes ofExeter and Bristol. Bristol has succeeded as a result of itsinvestment in its retail environment, along with Exeter,which opened its first John Lewis store in 2012.

The opening of Cabot Circus in Bristol in 2008 has vastlyimproved the city’s shopping provision and it recentlyentered the third in a series of Business ImprovementDistrict initiatives. It also won tourist event of the year,with its Gromit Unleashed charity project. However, townsthat have failed to invest in their centres are suffering atthe hands of popular out-of-town retail developments,with Swindon among the hardest hit.

Improving retail scenes in tourist hotspots such as Bath,Bristol and Exeter should see the proportion of foreigntourist spend on retail rise from 27.6% in 2013 to 28.3% by 2017, representing an increase of £106m.

Interestingly, the South West has proved to be particularlypopular with German tourists in recent years. In 2013 theywere the highest spending nationality amongst overseastourists to the region, with an expenditure of £168m. Muchof this trend has been attributed to Devon and Cornwall’slinks to former Mills & Boone author, Rosamunde Pilcher.Adaptations of Pilcher’s novels have become a Sunday

night institution in Germany and several companies offerPilcher-themed package tours of the region.

A new £27m visitor centre was opened at Stonehenge inDecember 2013, representing an enormous improvementin tourist facilities for one of the region’s premier touristattractions.

Moreover, the South West’s reputation for offering perhapsthe UK’s best regional climate, will help to ensure that itspopularity with domestic tourists endures. Domestictourist spend is projected to increase by 25.9% to £13.2bnby 2017, representing 12.1% of total spend by domestictourists in the UK.

Focusing on the South WestThe lure of the Devonshire countryside, the sandy beaches of Cornwall and thearchitectural splendour and heritage of cities such as Bath and Bristol make the South West of England one of the UK’s most popular tourist destinations.

The right-hand side of the chart displays the projected figures for 2017. The dark blue numbers represent that country’s percentage of this region’s totaloverseas tourist expenditure.

Source: ONS, Visit Britain.

Top ten overseas nationalities visiting the South West, by expenditure

Fashionretail

Other

Homeretail

Electricalsretail

+29.2%211164

+32.7%489368

-25.3%119 159

+21.9%834 1,017

10 of 19

Domestic tourist spending: retail

2013 2017

14.5% 13.9%

The South West: Domestic tourism spend on retail

Bristol Shopping Quarter, offering over 500 stores acrossCabot Circus, Quakers Friars, The Galleries, Broadmeadand St James Arcade, is set to reap the benefits of the risein retail spending, as well as the many unique independentstores, cafés and restaurants situated in the city.

Bath’s large number of independent shops and stylishboutiques has established it as a fashion hub for the SouthWest. The city has successfully exploited the commercialbenefits of this high-end retail infrastructure, organising‘Bath in Fashion 2014’, a week-long festival, showcasingthe best the city has to offer with catwalk shows andhands-on workshops and exhibitions.

In order to continue to compete against other UK regions,the South West’s retailers will need to focus their attentionon understanding the mindset of the domestic customerswho regularly return to the region and ensure they targetthem effectively.

Total domestic tourist expenditure on retail goods is predicted to increase20.4% to over £1.8bn by 2017.

Total domestic tourist spending (£m) and growth on retail goods, by category

The above charts show the proportion of total domestic tourist spend in the region that is made on retail, for 2013 and 2017.

Retail and wholesale Other domestic tourist spending

£1,525m £1,835m

2013 2017

27.6% 28.3%

Fashionretail

Other

Homeretail

Electricalsretail

+38.4%5238

+35.1%161 217

-22.9%65

+36.3%136100

11 of 19

The South West: Overseas tourism spend on retail

Swindon Designer Outlet, close to Bath, Oxford andStonehenge, promotes the South West as a retail hot spot, offering over 90 stores, ranging from iconic fashionbrands like Polo Ralph Lauren, L K Bennett, Tommy Hilfiger and Hugo Boss. These kinds of retail outlet sitesare increasingly appealing to visitors from China and theMiddle East, providing access to designer labels atsignificantly reduced prices to those charged in theirhome markets.

As with domestic tourists, the purpose-built shoppingcentres of Cribbs Causeway and Cabot Circus in Bristol arefavoured destinations for tourists that seek a wide varietyof brands. They also provide the opportunity for visitors toaccess more niche, boutique shopping in places such asthe Artisan and Milsom quarters of Bath, where an eclecticmix continues to hold appeal.

Retailers in the region should work hard to maximise their chances of accessing this increased expenditure byoverseas tourists. Targeted social media focusing on thechannels utilised by the key nationalities visiting the region(USA, France, Germany and Australia) will help – furtherpromoting the link with Germany via Rosamunde Pilcherfor example. Similarly, retailers should look to build amarketing strategy around increased international trafficfrom upcoming regional airports as the rise of low costairlines flying to smaller destinations continues.

Total spending on retail goods by overseas visitors is predicted to increase34.7% to £410m by 2017.

2013 2017

Overseas tourist spending: retail

Total overseas tourist spending (£m) and growth on retail goods, by category

The above charts show the proportion of total overseas tourist spend in the region that is made on retail, for 2013 and 2017.

Retail and wholesale Other overseas tourist spending

£304m £410m

2013 2017

12 of 19

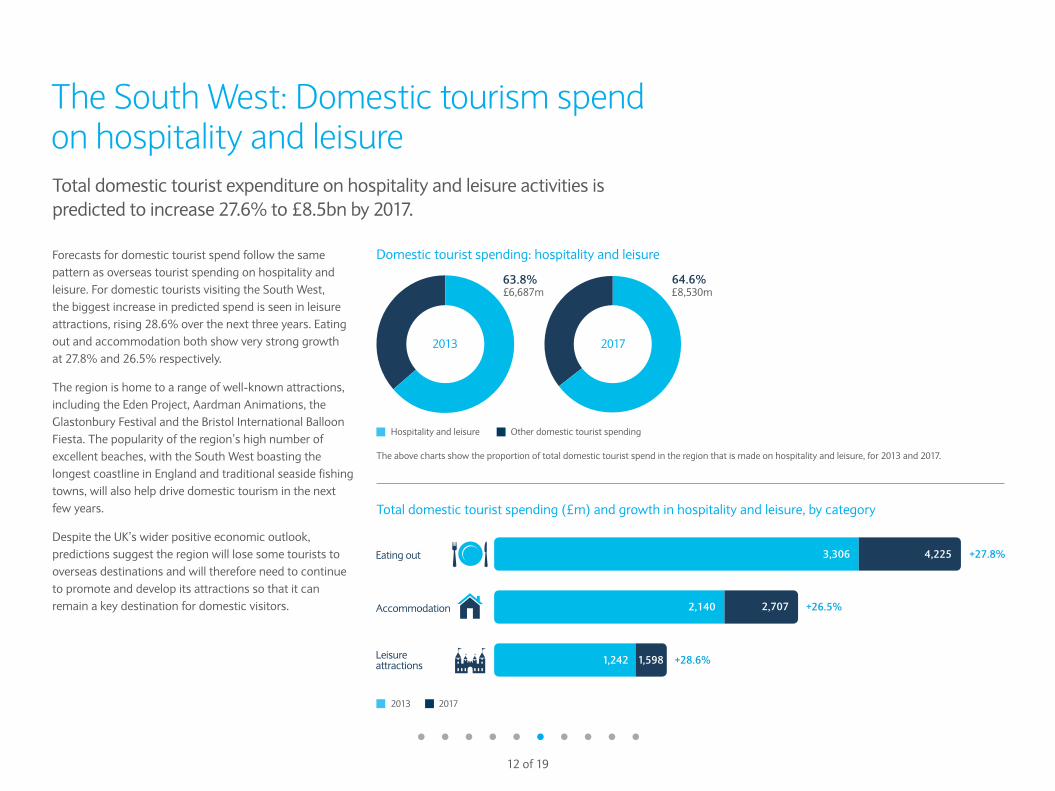

Accommodation +26.5%2,140 2,707

Leisure attractions +28.6%1,242 1,598

Eating out +27.8%3,306 4,225

Domestic tourist spending: hospitality and leisure

63.8% 64.6%

The South West: Domestic tourism spend on hospitality and leisure

Forecasts for domestic tourist spend follow the samepattern as overseas tourist spending on hospitality andleisure. For domestic tourists visiting the South West, the biggest increase in predicted spend is seen in leisureattractions, rising 28.6% over the next three years. Eatingout and accommodation both show very strong growth at 27.8% and 26.5% respectively.

The region is home to a range of well-known attractions,including the Eden Project, Aardman Animations, theGlastonbury Festival and the Bristol International BalloonFiesta. The popularity of the region’s high number ofexcellent beaches, with the South West boasting thelongest coastline in England and traditional seaside fishingtowns, will also help drive domestic tourism in the nextfew years.

Despite the UK’s wider positive economic outlook,predictions suggest the region will lose some tourists tooverseas destinations and will therefore need to continueto promote and develop its attractions so that it canremain a key destination for domestic visitors.

Total domestic tourist expenditure on hospitality and leisure activities ispredicted to increase 27.6% to £8.5bn by 2017.

2013 2017

Hospitality and leisure Other domestic tourist spending

The above charts show the proportion of total domestic tourist spend in the region that is made on hospitality and leisure, for 2013 and 2017.

Total domestic tourist spending (£m) and growth in hospitality and leisure, by category

£6,687m £8,530m

2013 2017

60.2% 59.9%

Accommodation +30.4%416 543

Leisure attractions +28.5%61 78

Eating out +31.8%187 246

The South West: Overseas tourism spend on hospitality and leisure

Traditionally, the South West of England has been wellknown for producing specialist food and drinks such asCheddar Cheese, Devon Cream teas, Cornish pasties and ciders – the continuing popularity of which maycontribute to the 31.8% rise in money spent on dining out by overseas tourists over the next three years.

Food festivals such as Bristol Wine & Food Fair, ExeterFestival of South West Food and Drink, and PlymouthFlavour Fest are attracting a growing number of visitorsand, as such, are contributing to the higher levels ofoverseas tourists within the region.

There are also an increasing number of Michelin-starredrestaurants opening in the South West, with well-knownchefs such as Anton Piotrowski, Rick Stein, Jamie Oliver,Nathan Outlaw and Paul Ainsworth migrating fromLondon to champion the region’s impressive seafood and fresh produce.

The South West’s hospitality businesses would be welladvised to consider promoting the positives associatedwith the region’s food scene as the interest in provenancecontinues to grow.

Total overseas tourist expenditure on hospitality and leisure activities is predictedto increase 30.6% to £867m by 2017.

Overseas tourist spending: hospitality and leisure

13 of 19

2013 2017

Hospitality and leisure Other overseas tourist spending

The above charts show the proportion of total overseas tourist spend in the region that is made on hospitality and leisure, for 2013 and 2017.

Total overseas tourist spending (£m) and growth in hospitality and leisure, by category

£663m £867m

2013 2017

14 of 19

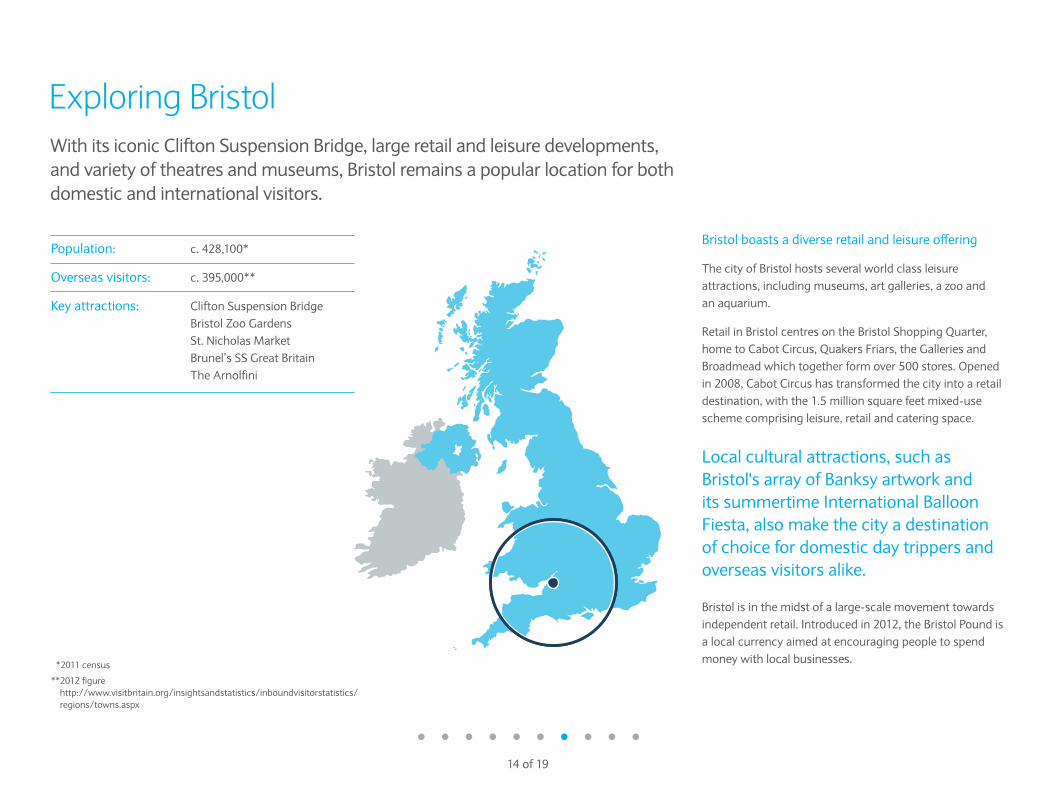

Exploring Bristol

Bristol boasts a diverse retail and leisure offering

The city of Bristol hosts several world class leisureattractions, including museums, art galleries, a zoo and an aquarium.

Retail in Bristol centres on the Bristol Shopping Quarter,home to Cabot Circus, Quakers Friars, the Galleries andBroadmead which together form over 500 stores. Openedin 2008, Cabot Circus has transformed the city into a retaildestination, with the 1.5 million square feet mixed-usescheme comprising leisure, retail and catering space.

Bristol is in the midst of a large-scale movement towardsindependent retail. Introduced in 2012, the Bristol Pound isa local currency aimed at encouraging people to spendmoney with local businesses.

Population: c. 428,100*

Overseas visitors: c. 395,000**

Key attractions: Clifton Suspension BridgeBristol Zoo GardensSt. Nicholas MarketBrunel’s SS Great BritainThe Arnolfini

With its iconic Clifton Suspension Bridge, large retail and leisure developments,and variety of theatres and museums, Bristol remains a popular location for bothdomestic and international visitors.

Local cultural attractions, such asBristol's array of Banksy artwork and its summertime International BalloonFiesta, also make the city a destinationof choice for domestic day trippers andoverseas visitors alike.

*2011 census

**2012 figure http://www.visitbritain.org/insightsandstatistics/inboundvisitorstatistics/regions/towns.aspx

15 of 19

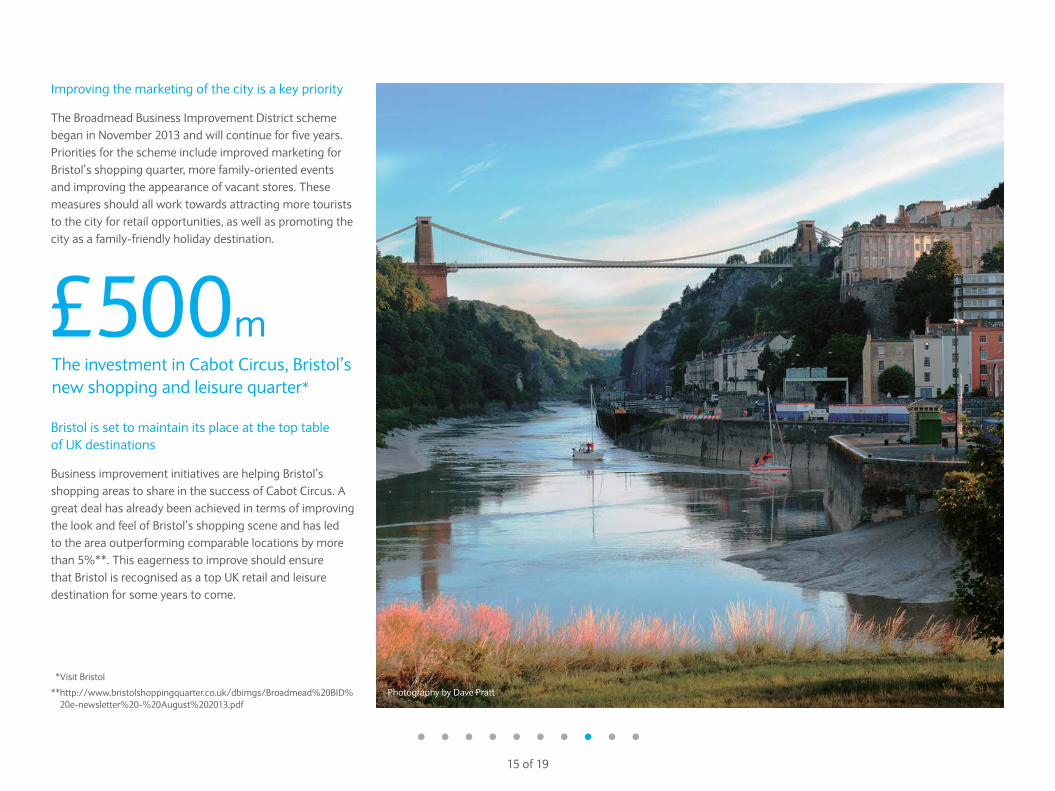

Improving the marketing of the city is a key priority

The Broadmead Business Improvement District schemebegan in November 2013 and will continue for five years.Priorities for the scheme include improved marketing forBristol’s shopping quarter, more family-oriented events and improving the appearance of vacant stores. Thesemeasures should all work towards attracting more touriststo the city for retail opportunities, as well as promoting thecity as a family-friendly holiday destination.

Bristol is set to maintain its place at the top table of UK destinations

Business improvement initiatives are helping Bristol’sshopping areas to share in the success of Cabot Circus. Agreat deal has already been achieved in terms of improvingthe look and feel of Bristol’s shopping scene and has led to the area outperforming comparable locations by morethan 5%**. This eagerness to improve should ensure that Bristol is recognised as a top UK retail and leisuredestination for some years to come.

*Visit Bristol

**http://www.bristolshoppingquarter.co.uk/dbimgs/Broadmead%20BID%20e-newsletter%20-%20August%202013.pdf

£500mThe investment in Cabot Circus, Bristol’s new shopping and leisure quarter*

Photography by Dave Pratt

16 of 19

Section three: Considerations for successThere are a number of strategies that retail, hospitality and leisure operatorscould consider in order to attract a higher volume of tourists.

Common strategiesKnow your audience• Talk to your audience in the channels they use, whether

it is social media, advertising, or television and radio• Tailor your social media and online services to different

international audiences, considering multiple languagesand cultural interests

• Proactively monitor foreign exchange rates, to ensurethat campaigns are launched at optimal times, whenparticular overseas visitors are more likely to come to the UK.

Strategic marketing• Consider location-based advertising, such as in

airports, train stations or nearby ports • Actively manage your media relations strategy• Work with local tourist offices• Engage with in-flight publications or hotel lobbies.

Working in partnership• Retailers and leisure operators may find collaboration

mutually beneficial. For example, hoteliers may look to advertise nearby shopping areas and restaurants, or even use local products throughout the building.

Retail & WholesaleEase of purchase• Appropriate payment options are a key

consideration. For example, Union Pay is particularly important to Chinese consumersand is something companies could offer if theywish to maximise potential spending.

‘Brand Britain’• British-made goods remain popular amongst

overseas consumers. Retailers may want toconsider how they are marketing their products to an audience eager for ‘Brand Britain’.

Hospitality & LeisureSelling tickets• Attractions requiring tickets should

consider how visitors are able to purchase in advance, which may be a simple way tosecure footfall.

Brochures and marketing communications • Brochures aimed at overseas tourists

should consider local tastes, preferences andrequirements – this could mean producing a number of subtly different campaigns for a variety of nationalities.

17 of 19

As a five-star hotel in London with just under 300bedrooms, Corinthia Hotel London might be mistaken for a company with a long-established brand image andhistory within the capital. Matthew Dixon, the hotel’sGeneral Manager, explains how the somewhat unknownleisure business has, within the last three years, developedeffective business strategies to build its brand and ensuresuccess in a crowded market.

Understanding your audience

“Understanding your client demographic is essential,”states Dixon. “We track which particular nationalities arevisiting our hotel on a regular basis, and identify how ourclients prefer to book with us.”

The hotel has identified the nationalities which make upthe bulk of its customer base, and targeting these variousaudiences requires different techniques to encouragereservations: in North America, for example, threededicated sales managers work in-country to profile thebrand with potential visitors. Matthew Dixon takes atailored approach to his interactions with the Middle East,ensuring he personally attends networking events to build word of mouth, whereas in China and Russia herecognises more traditional consumer patterns, withtravellers booking through UK-based agents.

Dynamic marketing

Marketing is key in successfully targeting Corinthia’sdifferent audiences. In the USA, the hotel advertises inspecific leisure publications, and deploys more innovativeapproaches, such as screening small-scale 3D movies inHollywood, which take viewers on a virtual tour of theirLondon building.

Search engines and travel review websites allow everydayconsumers to rate the establishment, and as such thehotel monitors online ratings with a dedicated social-media manager who attempts to respond to every onlinereview, engaging with visitors on a more personal level.

Dixon admits that the hotel’s nascent UK brand has allowedit to be more flexible and bespoke when attracting attentionfrom customers and the media. Building the brand from alow awareness has allowed Corinthia to be slightly bolderthan some of its more established competitors, helping it to stand out in the busy London market.

Making the most of your location

Situated near Trafalgar Square, Corinthia Hotel London does not share the Mayfair location of many of its five-starcompetitors; however, Dixon sees this as an opportunity.“We currently engage with the Business ImprovementDistrict, which allows us to collaborate with local retail,infrastructure and leisure projects – ensuring that we makethe most of our local community and keep attractingtourists from all areas, especially the local UK market.”

Indeed, this collaboration ensures that consumers areaware of the array of facilities on the North Bank, as wellas encouraging tourism and generally improving the localenvironment. By working with retailers and leisureoperators alike, Corinthia is able to reap the mutualbenefits of investing in its surroundings.

With an impressive location, luxurious facilities and anemerging brand, Corinthia is excited about what the nextdecade will bring, and looks forward to getting to know itsdeveloping client base even further.

Corinthia Hotel London has grown from strength to strength since itsopening in 2011, and owes its success to understanding its customer base,as well as celebrating its local surroundings.

Case study: Corinthia Hotel London

18 of 19

Section four: Key takeaways• By 2017, total expenditure by domestic and overseas tourists across the UK is expected to increase by

27%, to just over £135.5bn

• Domestic tourists continue to enjoy the ‘staycation’ across the UK, and competition for visitors isincreasing between the regions

• Mobile and online purchases continue to challenge high-street retailers; however, domestic touristsseem to be willing to spend in store on luxury items

• Premium retail remains a key draw for some overseas visitors seeking the UK’s lower prices

• Businesses should understand their audience to ensure that their service and marketing approach suit the needs of their most frequent visitors

• Effective marketing, including the use of social media channels, is essential for a region’s successwithin the UK’s wider tourism market, but should also be a key consideration for individual businesses

• When working together, both retailers and leisure operators can reap the benefits of tourist trade.

To find out more about how Barclays can support your business, please call 0800 015 4242* or visit barclays.com/corporatebanking

*To maintain a high quality of service, your call may be monitored or recorded for training and security purposes. Calls to 0800 numbers are free of charge, when calling from a UK landline. Charges may apply when using a mobile phone or when calling from abroad. Lines are open from 8am to 6pm Monday to Friday.

About the authors

19 of 19

Please note: these are mobile phone numbers and calls will be charged in accordance with your mobile tariff.

No part of this publication may be reproduced or stored in a retrieval system, in any form or by any means, electrical, mechanical, photocopying or otherwise, without the prior consent of the publishers. The views and forecasts presentedin this report represent independent findings and conclusions drawn from a study by Conlumino. Conlumino can accept no responsibility for any investment decision made on the basis of this information or for any omissions orinaccuracies that may be contained in this report. This report has been produced in good faith and independently of any operator or supplier to the industry. We trust that it will be of significant value to all readers.

The views expressed in this report are the views of third parties, and do not necessarily reflect the views of Barclays Bank PLC nor should they be taken as statements of policy or intent of Barclays Bank PLC. Barclays Bank PLC takes no responsibility for the veracity of information contained in third party narrative and no warranties or undertakings of any kind, whether expressed or implied, regarding the accuracy or completeness of the information given. Barclays Bank PLC takes no liability for the impact of any decisions made based on information contained and views expressed in any third party guides or articles.

Barclays is a trading name of Barclays Bank PLC and its subsidiaries. Barclays Bank PLC is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority(Financial Services Register No. 122702). Registered in England. Registered number is 1026167 with registered office at 1 Churchill Place, London E14 5HP.

May 2014.

For further information and to find out how our sectorspecialist teams can support your business, pleasecontact Richard Lowe, Head of Retail & Wholesale, or Mike Saul, Head of Hospitality & Leisure.

Richard LoweHead of Retail & WholesaleT: +44 (0) 7775 540 [email protected]

Mike SaulHead of Hospitality & LeisureT: +44 (0) 7775 540 [email protected]