Embed Size (px)

Citation preview

UK reflections

on the golden rule

Presentation to Austrian Fiscal Advisory Council seminar

Andy King

Chief of Staff

Office for Budget Responsibility

29 September 2015

Background

The Office for Budget Responsibility

• Created in 2010 to provide independent and

authoritative analysis of the public finances

• Produces the budget and autumn statement forecasts of

the economy and public finances

• Assesses Government progress against fiscal targets

• Reports on the sustainability of the public finances and

the health of the public sector balance sheet

• Scrutinises the Government’s costing of policy measures

• Objective to make fiscal forecasts and costings unbiased

and clear, but we have no role in making or commenting

on Government policy

Core outputs of the OBR

Core outputs of the OBR

Core outputs of the OBR

Core outputs of the OBR

UK fiscal framework

1997 to 2008:

Golden rule &

Sustainable investment rule

Institutional context: macroeconomic policy reforms

• Bank of England given operational independence

for monetary policy, to hit Govt inflation target

• Financial regulation would be brought together

under a single statutory authority

• Fiscal policy would be guided by two new fiscal

rules:

– Golden rule – borrow only to invest over the economic

cycle

– Sustainable investment rule – keep debt at a prudent level

over the economic cycle*

* The name of the rule and the 40% of GDP specification came later

Golden rule: Rationale and objectives

The ‘Silver Book’ argued:

• It would approximate to the principle of achieving

fairness between generations

• It would address past fiscal failings by removing

the bias against capital spending

• It would allow the automatic stabilisers to work, by

targeting balance over the economic cycle

• Coupled with debt rule, it would ensure the public

finances were on a long-term sustainable path

Sustainable investment rule: Rationale and objectives

The ‘Silver Book’ argued:

• It should focus on a net measure of public debt,

for the whole public sector, as a per cent of GDP

• While public debt plays important roles, high levels

of public debt reduce the buffer against shocks and

may impose other costs (e.g. via interest rates)

• While current levels of public debt were not high by

historical or international standards, a modest

reduction to 40 per cent of GDP was consistent

with balanced and responsible fiscal management

Real-time critiques

of the golden rule

in the UK

Real-time critiques: Dating the economic cycle

Real-time critiques: Dating the economic cycle

Real-time critiques: Dating the economic cycle

Real-time critiques: Dating the economic cycle

IFS Green Budget 2006:

“Re-dating the cycle at

such a convenient time

risks undermining the

credibility of the fiscal

framework. The golden

rule should be made more

forward-looking and less

reliant on a precisely

dated economic cycle. If

still required, the task of

estimating the output gap

could be handed to an

independent body.”

Real-time critiques: Backward-looking approach

Real-time critiques: Backward-looking approach

Budget 2007 forecast for the golden rule from 1997-98

-6

-5

-4

-3

-2

-1

0

1

2

3

1997-98 1999-00 2001-02 2003-04 2005-06 2007-08 2009-10 2011-12

Average surplus on current budget since 1997-98

Cyclically-adjusted surplus on current budget

Source: HM Treasury

Budget 2007 forecast

Real-time critiques: Backward-looking approach

IFS Green Budget 2006:

“…defining a particular period as ‘a cycle’ and seeking to

balance the current budget over this period is not the only

way to allow the automatic stabilisers to function. This

approach is backward-looking in the sense that the amount

you can borrow today and in the near term depends on the

impact on borrowing of shocks and policy mistakes earlier in

the cycle. A more forward-looking approach would set policy

today consistent with meeting the rule in the future, whether

or not it was consistent with meeting it in the past.”

Real-time critiques: Backward-looking approach

Budget 2007 forecast for the golden rule from 1997-98

-6

-5

-4

-3

-2

-1

0

1

2

3

1997-98 1999-00 2001-02 2003-04 2005-06 2007-08 2009-10 2011-12

Average surplus on current budget since 1997-98

Cyclically-adjusted surplus on current budget

Source: HM Treasury

Budget 2007 forecast

Real-time critiques: Backward-looking approach

Latest data for the golden rule from 1997-98

-6

-5

-4

-3

-2

-1

0

1

2

3

1997-98 1999-00 2001-02 2003-04 2005-06 2007-08 2009-10 2011-12

Average surplus on current budget since 1997-98

Cyclically-adjusted surplus on current budget

Source: ONS, OBR

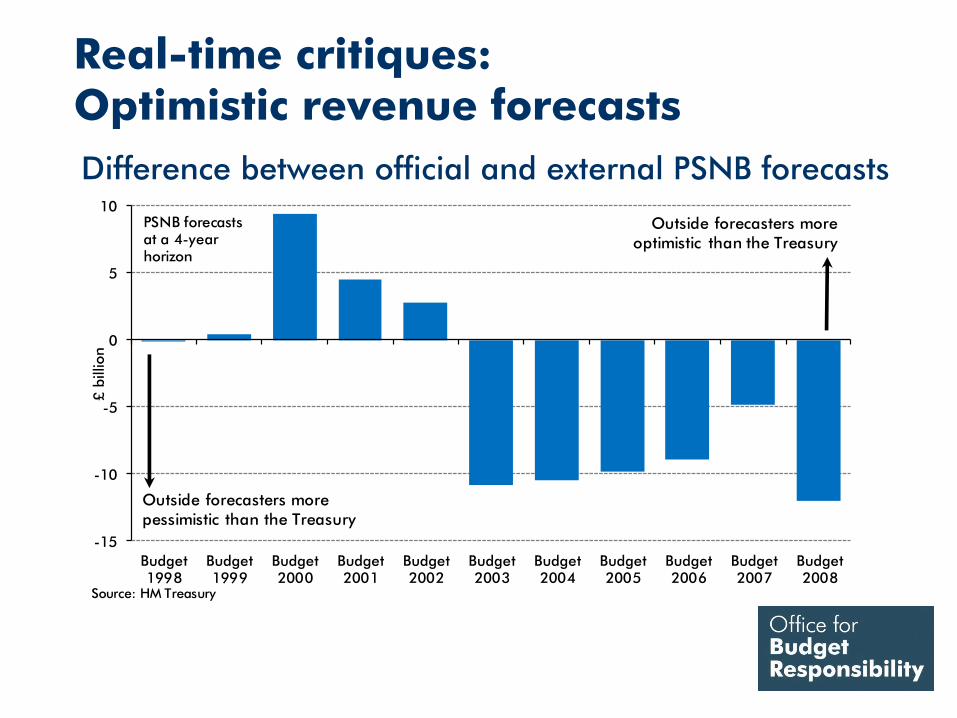

Real-time critiques: Optimistic revenue forecasts

Real-time critiques: Optimistic revenue forecasts

Difference between official and external PSNB forecasts

-15

-10

-5

0

5

10

Budget1998

Budget1999

Budget2000

Budget2001

Budget2002

Budget2003

Budget2004

Budget2005

Budget2006

Budget2007

Budget2008

£ b

illio

n

Source: HM Treasury

Outside forecasters more pessimistic than the Treasury

Outside forecasters more optimistic than the Treasury

PSNB forecasts at a 4-year horizon

Looking back at pre- and post-crisis

fiscal performance

UK running structural deficit when the crisis struck

Contemporaneous and recent OECD estimates

-12 -10 -8 -6 -4 -2 0 2 4 6

New ZealandFinlandIceland

DenmarkNorwaySweden

LuxembourgAustraliaCanada

SwitzerlandSpain

GermanyNetherlands

BelgiumAustriaJapan

Czech RepublicItaly

IrelandPortugal

FranceUnited States

United KingdomHungaryGreece

Per cent of GDP

June 2014 forecast

-12 -10 -8 -6 -4 -2 0 2 4 6

New ZealandDenmark

FinlandIcelandSwedenIreland

SwitzerlandAustralia

SpainCanada

LuxembourgBelgium

NetherlandsNorwayAustria

GermanyPortugal

FranceItaly

GreeceUnited Kingdom

JapanUnited States

Czech RepublicHungary

Per cent of GDP

June 2007 forecast

Source: OECD

UK public sector debt rising before the crisis struck

Change in general govt net liabilities: 2004 to 2007

-40 -30 -20 -10 0 10 20

NorwayFinlandIcelandSweden

DenmarkIsrael

BelgiumSpain

New ZealandCanadaFrance

NetherlandsSlovenia

IrelandKorea

PolandItaly

SwitzerlandGermanyAustralia

Czech RepublicUnited States

JapanGreece

PortugalUnited Kingdom

LuxembourgAustriaEstonia

Slovak RepublicHungary

Per cent of GDPSource: OECD

Revenue forecasts and spending plans

-2

-1

0

1

2

3

4

5

6

SR20002000-01 vs 2003-04

SR20022002-03 vs 2005-06

SR20042004-05 vs 2007-08

CSR20072007-08 vs 2010-11

Per

cent

of G

DP

TME planned TME outturn

Receipts forecast Receipts outturn

Source: HM Treasury

Successive pre-crisis Spending Reviews

Revenue forecasts and spending plans

Successive pre-crisis Spending Reviews

-2

-1

0

1

2

3

4

5

6

SR20002000-01 vs 2003-04

SR20022002-03 vs 2005-06

SR20042004-05 vs 2007-08

CSR20072007-08 vs 2010-11

Per

cent

of G

DP

TME planned TME outturn

Receipts forecast Receipts outturn

Source: HM Treasury

Crisis-related structural hit to the public finances

90

100

110

120

130

140

150

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Act

ual

outp

ut

20

07

Q4 =

10

0

March 2008 actual

March 2008 potential

July 2015 actual

July 2015 potential

Source: HM Treasury, ONS, OBR

Range of implied external forecasts

for potential output in 2016

Pre-crisis and latest estimates of potential output

Temporary fiscal rules

2008 to 2010

Temporary fiscal rules

November 2008: Temporary operating rule:

“to set policies to improve the cyclically adjusted current

budget each year, once the economy emerges from the

downturn, so it reaches balance and debt is falling as a

proportion of GDP once the global shocks have worked their

way through the economy in full”

Temporary fiscal rules

November 2008: Temporary operating rule:

“to set policies to improve the cyclically adjusted current

budget each year, once the economy emerges from the

downturn, so it reaches balance and debt is falling as a

proportion of GDP once the global shocks have worked their

way through the economy in full”

February 2010: Fiscal Responsibility Act:

Legislative duties:

– Borrowing to be more than halved to 5.5% of GDP or less in 2013-14

– Borrowing to be reduced as a share of GDP in each and every year from

2009-10 to 2015-16; and

– Public sector net debt to be falling as a share of GDP in 2015-16

UK fiscal framework

2010 to 2015:

Fiscal mandate &

Supplementary target

The 2010 fiscal framework

Fiscal mandate:

• to achieve cyclically-adjusted current balance by the

end of the rolling, five-year forecast period

Supplementary debt target:

• for public sector net debt as a percentage of GDP to

be falling at a fixed date of 2015-16

Office for Budget Responsibility:

• an independent fiscal institution

Fiscal mandate: Rationale and objectives

June 2010 Budget argued:

• The fiscal mandate is based on:

– the current balance, to protect the most

productive public investment expenditure

– a cyclically adjusted aggregate, to allow some

fiscal flexibility at a time of economic uncertainty

• Unlike the golden rule, the fiscal mandate is:

– forward-looking, not backward-looking

– based on an independent OBR assessment of the structural

fiscal position

Supplementary target: Rationale and objectives

June 2010 Budget argued:

• “At this time of rapidly rising debt, the fiscal

mandate will be supplemented by a target for public

sector net debt… ensuring that the public finances

are restored to a sustainable path.”

• “once the exceptional rise in debt has been

addressed, a new target for debt as a percentage of

GDP will be set, taking account of the OBR’s

assessment of the long-term sustainability of the

public finances.”

Office for Budget Responsibility: Rationale and objectives

June 2010 Budget argued:

• In order to promote international and domestic

confidence in the sustainability of the public

finances, the Government had:

“created the new Office for Budget Responsibility

(OBR), which introduces independence, greater

transparency and credibility to the economic and

fiscal forecasts on which fiscal policy is based.”

UK fiscal framework

from 2015:

Proposed new fiscal targets

Proposed fiscal rules

Draft Charter for Budget Responsibility sets out:

• In normal times: a target for a surplus on public sector

net borrowing in each subsequent year

• For the period outside normal times from 2015-16: a

surplus on public sector net borrowing by 2019-20

• Until 2019-20, the mandate is supplemented by a

target for public sector net debt as a percentage of

GDP to be falling in each year

Proposed fiscal rules

Draft Charter for Budget Responsibility sets out:

• These targets apply unless and until the Office for

Budget Responsibility assess, as part of their economic

and fiscal forecast, that there is a significant negative

shock to the UK. A significant negative shock is

defined as real GDP growth of less than 1% on a

rolling 4 quarter-on-4 quarter basis.

Public investment

in the UK

Current budget deficit and net investment

Budget 2007 outturns and forecast

0.0

0.6

1.2

1.8

2.4

3.0

3.6

-4

-2

0

2

4

6

8

1979-80 1983-84 1987-88 1991-92 1995-96 1999-00 2003-04 2007-08 2011-12

Current budget deficit (LHS) Net investment (RHS)

Source: ONS, HM Treasury

Budget 2007

forecast

Current budget deficit and net investment

Latest current budget and Budget 2007 investment

0.0

0.6

1.2

1.8

2.4

3.0

3.6

-4

-2

0

2

4

6

8

1979-80 1983-84 1987-88 1991-92 1995-96 1999-00 2003-04 2007-08 2011-12

Current budget deficit (LHS) Net investment (RHS)

Source: ONS, HM Treasury

Current budget deficit and net investment

Latest outturns

0.0

0.6

1.2

1.8

2.4

3.0

3.6

-4

-2

0

2

4

6

8

1979-80 1983-84 1987-88 1991-92 1995-96 1999-00 2003-04 2007-08 2011-12

Current budget deficit (LHS) Net investment (RHS)

Source: ONS, HM Treasury

International comparison

0

1

2

3

4

5

6

Germ

an

y

Belg

ium

Irela

nd

Ita

ly

Mexi

co

Tu

rke

y

Icela

nd

UK

Gre

ece

Sp

ain

Au

stri

a

Sw

itze

rlan

d

Po

rtu

ga

l

Jap

an

Slo

vak R

ep

Au

stra

lia

New

…

Den

ma

rk US

Neth

erl

and

s

Fin

land

Luxe

mb

ou

rg

Fra

nce

Cze

ch R

ep

Can

ad

a

Hu

nga

ry

No

rwa

y

Slo

ven

ia

Sw

ede

n

Ko

rea

Po

lan

d

Est

onia

Source: OECD

General government GFCFPer cent of GDP (2010-2014 average)

Government investment in the OECD

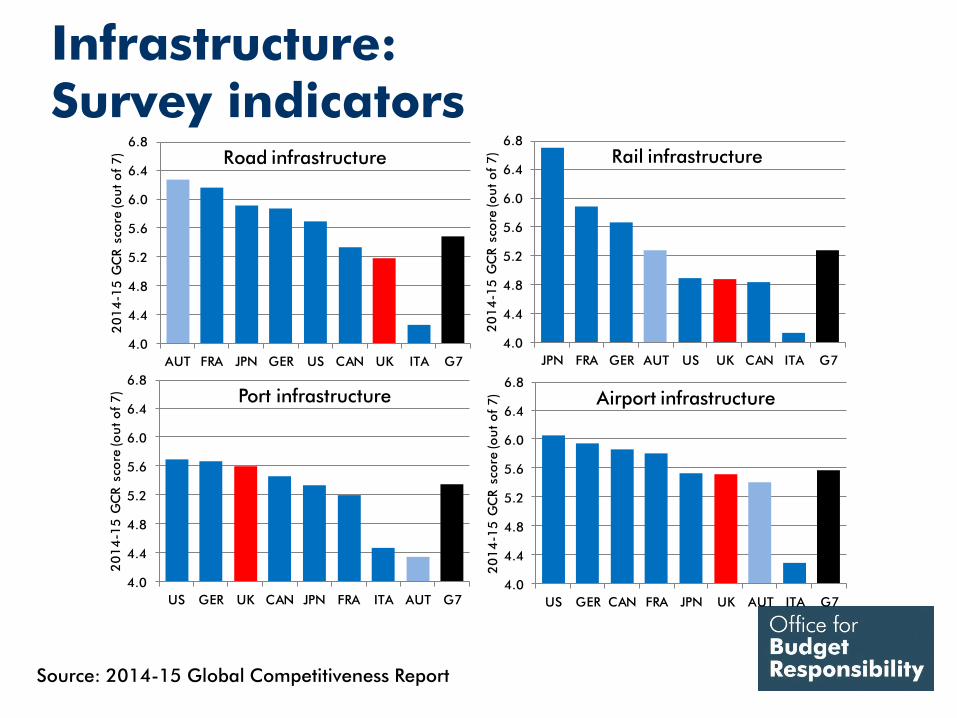

Infrastructure: Survey indicators

Source: 2014-15 Global Competitiveness Report

4.0

4.4

4.8

5.2

5.6

6.0

6.4

6.8

AUT FRA JPN GER US CAN UK ITA G7

20

14

-15

GC

R s

core

(o

ut

of

7) Road infrastructure

4.0

4.4

4.8

5.2

5.6

6.0

6.4

6.8

JPN FRA GER AUT US UK CAN ITA G7

20

14

-15

GC

R s

core

(o

ut

of

7) Rail infrastructure

4.0

4.4

4.8

5.2

5.6

6.0

6.4

6.8

US GER UK CAN JPN FRA ITA AUT G7

20

14

-15

GC

R s

core

(o

ut

of

7) Port infrastructure

4.0

4.4

4.8

5.2

5.6

6.0

6.4

6.8

US GER CAN FRA JPN UK AUT ITA G7

20

14

-15

GC

R s

core

(o

ut

of

7) Airport infrastructure

Conclusions

![& V Institutional Profile - Golden Helixgenomics and personalized medicine [101]. The GHI is named after the house of Francis Crick (‘The Golden Helix’, Cambridge, UK) to emphasize](https://img.pdfslide.us/doc/110x75/5f5a4de68488a9687541e31d/-v-institutional-profile-golden-genomics-and-personalized-medicine-101.jpg)